UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| [X] | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2010

or

| [ ] | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number: 1-15259

ARGO GROUP INTERNATIONAL HOLDINGS, LTD.

(Exact name of Registrant as specified in its charter)

| | |

| Bermuda | | 98-0214719 |

(State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification Number) |

| |

110 Pitts Bay Road Pembroke HM08 Bermuda | | P.O. Box HM 1282 Hamilton HM FX Bermuda |

| (Address of principal executive offices) | | (Mailing address) |

(441) 296-5858

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| | |

| Title of Security | | Name of Each Exchange on Which Registered |

| Common Stock, par value of $1.00 per share | | NASDAQ Global Select Market |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes [X] No [ ]

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes [ ] No [X]

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes [X] No [ ]

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes [X] No [ ]

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [X]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| | | | | | |

| Large accelerated filer [X] | | Accelerated filer [ ] | | Non-accelerated filer [ ] | | Smaller reporting company [ ] |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes [ ] No [X]

As of June 30, 2010, the aggregate market value of the common stock held by non-affiliates was approximately $901.2 million.

As of February 16, 2011, the Registrant had 31,230,481 shares of common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Part III: Excerpts from Argo Group International Holdings, Ltd.’s Proxy Statement for the Annual Meeting of Shareholders to be held on May 3, 2011

ARGO GROUP INTERNATIONAL HOLDINGS, LTD.

Annual Report on Form 10-K

For the Year Ended December 31, 2010

TABLE OF CONTENTS

Forward Looking Statements

Certain statements in this document are “forward-looking statements” as that term is defined in the Private Securities Litigation Reform Act of 1995 and are made pursuant to the safe harbor provisions of that act. Some of the forward-looking statements can be identified by the use of forward-looking words such as “believes”, “expects”, “potential”, “continued”, “may”, “will”, “should”, “seeks”, “approximately”, “predicts”, “intends”, “plans”, “estimates”, “anticipates” or the negative version of those words or other comparable words. The forward-looking statements are based on the current expectations of Argo Group International Holdings, Ltd. (“Argo Group,” “we” or the “Company”) and our beliefs concerning future developments and their potential effects on Argo Group. There can be no assurance that actual developments will be those anticipated by Argo Group. Actual results may differ materially as a result of significant risks and uncertainties including but not limited to:

| | • | | changes in the pricing environment including those due to the cyclical nature of the insurance and reinsurance industry; |

| | • | | the adequacy of our projected loss reserves including; |

| | o | development of claims that varies from that which was expected when loss reserves were established; |

| | o | adverse legal rulings which may impact the liability under insurance and reinsurance contracts beyond that which was anticipated when the reserves were established; |

| | o | development of new theories related to coverage which may increase liabilities under insurance and reinsurance contracts beyond that which were anticipated when the loss reserves were established; |

| | o | reinsurance coverage being other than what was anticipated when the loss reserves were established; |

| | • | | changes to regulatory and tax conditions and legislation; |

| | • | | natural and/or man-made disasters, including terrorist acts; |

| | • | | the inability to secure reinsurance; |

| | • | | the inability to collect reinsurance recoverables; |

| | • | | a downgrade in our financial strength ratings; |

| | • | | changes in interest rates; |

| | • | | changes in the financial markets that impact investment income and the fair market values of our investments; |

| | • | | changes in asset valuations; |

| | • | | inability to successfully execute our mergers and acquisitions growth strategy; and |

| | • | | other risks detailed in this Form 10-K and that may be detailed in other filings with the Securities and Exchange Commission. |

These risks and uncertainties are discussed in greater detail in Item 1A “Risk Factors.” We undertake no obligation to publicly update any forward-looking statements.

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

PART I

Item 1. Business

Business Overview

Argo Group International Holdings, Ltd. (“Argo Group,” “we” or the “Company”) is an international underwriter of specialty insurance and reinsurance products in the property and casualty market. Argo Group is the result of a merger in 2007 between Argonaut Group, Inc. and PXRE Group Ltd. (“PXRE”) (the “Merger”). We target niches where we can develop a leadership position and which we believe will generate superior underwriting profits. Our growth has been achieved both organically through an operating strategy focused on disciplined underwriting and as a result of strategic acquisitions.

3

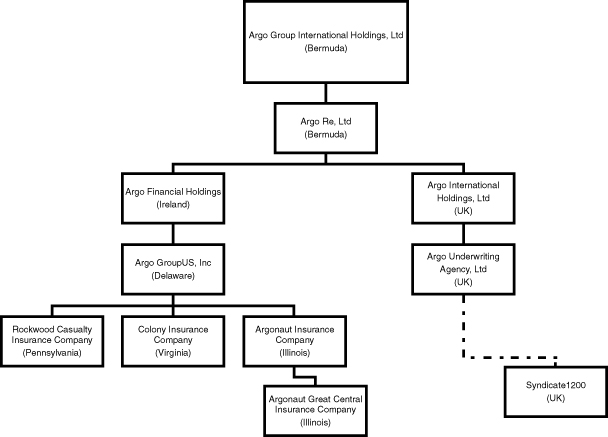

Following is a summary organization chart for Argo Group:

Business Segments and Products

For the year ended December 31, 2010, Argo Group’s operations included four ongoing business segments: Excess and Surplus Lines, Commercial Specialty, Reinsurance and International Specialty. Additionally, we have a Run-off Lines segment for products we no longer underwrite. For discussion of the operating results of each business segment, please refer to Item 7 “Management’s Discussion and Analysis of Financial Condition and Results of Operations” on pages 42-72 and Note 14, “Segment Information” in the Notes to the Consolidated Financial Statements.

Excess and Surplus Lines (“E&S”). Excess and surplus lines carriers focus on risks that the standard (admitted) market is unwilling or unable to underwrite. The lack of insurers willing to offer such coverage is often due to the unique risk characteristics of the insureds, the perils involved, the nature of the business, or the insured’s loss experience. Excess and surplus lines carriers are able to underwrite these risks with more flexible policy terms at unregulated premium rates on a non-admitted basis.

In 2010, our E&S business segment consisted of three operating platforms: Colony Group (“Colony”), Argonaut Specialty and Argo Pro. In the fourth quarter of 2010, we announced the restructuring of this segment and the consolidation of Colony and Argonaut Specialty under a unified platform branded “Colony Specialty.” For purposes of this annual report, we continue to refer separately to Colony and Argonaut Specialty consistent with the manner in which we managed and reported on these operations during 2010. While focused primarily on underwriting on a non-admitted basis, each of these operations may also underwrite certain classes of business on an admitted basis for insureds with risk profiles that meet our underwriting standards.

Colony focuses on a broad class of risks that the standard market chooses not to underwrite, operating through four divisions: Casualty, Property, Transportation and Binding Authority. Colony provides coverage to a broad group of commercial enterprises including restaurants, contractors, day care centers, apartment complexes, condominium associations, manufacturers and distributors. A portion of its business, primarily Transportation (commercial automobile) coverage, is written on an admitted basis.

4

Argo Pro is comprised of four divisions: Allied Medical, Errors & Omissions, Environmental and Insight. The Allied Medical division targets medical facilities within the social services, miscellaneous healthcare, and long term care segments. The Errors & Omissions division targets insurance agents, lawyers, miscellaneous professions, employment practices and real estate related accounts. The Environmental division offers package policies for environmental consultants and contractors, storage tanks, dry cleaners pollution liability as well as other environmental related liability exposures. Our Insight division offers coverage for architects and engineers, accountants and insurance agents. All Argo Pro divisions focus on small to medium size risks on both an admitted and non admitted basis.

Argonaut Specialty underwrites risks, primarily on an excess and surplus lines basis, which are slightly larger in size and complexity than those traditionally targeted by Colony. It underwrites primary casualty and excess/umbrella coverages for hard to place risks and/or distressed businesses that fall outside of the standard insurance market’s risk appetite. Primary casualty risks comprised 61% of Argonaut Specialty’s premium volume in 2010. The excess/umbrella casualty division accounted for 39% of Argonaut Specialty’s premium volume during 2010.

Commercial Specialty. This segment provides property casualty and surety coverages designed to meet the specialized insurance needs of businesses within certain well defined markets. It targets business classes and industries with distinct risk profiles that can benefit from specially designed insurance programs, tailored loss control and expert claims handling. This segment serves its targeted niche markets with a narrowly focused underwriting profile and an understanding of the businesses it serves. In 2010, our Commercial Specialty segment consisted of the following operations: Argo Select, Rockwood, Commercial Programs Alteris and Argo Surety. During the fourth quarter of 2010, we also announced the acquisition of ARIS Title Insurance Corporation, a statutory insurance company licensed by the New York State Department of Insurance to provide art title insurance that serves the needs of the art marketplace and related fiduciary banking, legal, museum and non-profit communities.

The core operations of Argo Select consist of Grocery, Restaurants, and Specialty Retail (including dry cleaners, commercial launderers, convenience stores, and retail furniture stores). In addition, Argo Select partnered with First Insurance Company of Hawaii (“FICOH”) providing stand-alone hurricane coverage for personal lines policies in that state, a program that was discontinued in 2010. Approximately 48% of Argo Select’s 2010 gross written premium was from the Grocery segment, followed by 24% in Specialty Retail, 16% from Restaurants, 9% from FICOH, and 2% from our discontinued Religious Organizations lines. Argo Select provides property, liability, workers compensation, auto, and umbrella coverage throughout the United States. In the last quarter of 2010, we announced that Argo Select would be marketed going forward under the “Argo Insurance” brand, a unified brand which also includes non-U.S. retail products that we offer independently of our Argo International operation.

Rockwood is recognized as a leading specialty underwriter of workers compensation for the mining industry. It also underwrites business coverage for small commercial businesses including office, retail operations, light manufacturing, services, and restaurants. Rockwood’s strategy includes a strong commitment to its insureds, a highly experienced staff, and a dedication to selective underwriting of individual risks. Approximately 52% of its premiums are written in Pennsylvania where it is the largest workers compensation insurer of independent coal mines. Rockwood underwrites policies on both a large deductible basis and on a guaranteed cost basis for smaller commercial accounts. In addition, Rockwood provides supporting general liability, pollution liability, umbrella liability, property, commercial automobile and surety coverages, for certain of its mining accounts. These supporting lines of business represented approximately 16% of Rockwood’s gross written premiums in 2010.

Argo Surety offers surety products to a diverse range of U.S. businesses operating in numerous industries. The focus of Argo Surety is to deliver high-quality surety credit solutions to businesses that must satisfy various eligibility conditions in order to conduct commerce, such as licensure requirements promulgated by government statute or regulation, counterparty conditions found in private or public construction projects or satisfactory performance of contracted services. Surety products are commonly grouped into two broad categories referred to as Contract Bonds and Commercial Bonds. Contract bonds are typically third-party performance, payment or maintenance guarantees associated with construction projects, whereas commercial bonds are generally required of businesses that guarantee their compliance with regulations and statutes, or the payment and performance assurance for various forms of contractual obligations, or the completion of services.

5

Argo Surety targets multiple industries including but not limited to construction (general, trade and service contractors), manufacturing, transportation, energy (coal, oil & gas and waste), industrial equipment, technology, retail, public utilities, and healthcare.

Commercial Programs (formerly Programs & Product Development) partners with retail insurance program administrators to develop specialized commercial programs in niche markets. They work with Program Administrators who have expertise in a particular field, a proven record of managing profitable programs, and an established distribution network. The typical Program Administrator selected for Alteris Commercial Programs is equipped to handle responsibilities such as marketing, underwriting, rating and policy issuance subject to our oversight. Target markets for this division include retail and service industries, such as landscaping operations, forestry/logging operations, wineries, and industries related to pet care. Specialty programs are also provided for building management/maintenance companies, community and condominium associations, and landlords (lease guarantee program).

Alteris focuses on specialty programs and alternative risks solutions for selected niche markets, operating through the following divisions: Trident, Alteris Public Risk Solutions and and Alteris Alternative Risk Solutions (formerly Corporate Accounts).

| | • | | Trident functions as both an underwriter and a managing general agency and is a nationally recognized program manager providing insurance products for small to intermediate sized accounts in targeted sectors. Trident manages primary insurance programs serving public entities, public schools, special districts, private education (K-12), home heating dealers, propane dealers, student transportation, septic contractors, waste haulers and lawyers. Trident offers fully insured solutions for individual accounts in the sectors it serves. Its product lines include general liability, automobile liability, automobile physical damage, property, inland marine, crime, public official’s liability, educator’s legal liability, employment practices, law enforcement liability, environmental liability, lawyers professional liability, student accident, police and firefighters accident, workers compensation, inmate medical and tax interruption coverages. |

| | • | | Alteris Public Risk Solutions serves large individual governmental entities and self-insured governmental pools. Using both traditional and creative approaches, APRS aligns interests with its clients by targeting sophisticated accounts that participate in their own risk bearing. It’s product lines include general liability, automobile liability, automobile physical damage, property, inland marine, crime, public official’s liability, educator’s legal liability, law enforcement professional liability, employment practices liability and excess liability. |

| | • | | Alteris Alternative Risk Solutions provides unbundled alternative risk structures supporting both carriers and program managers through a broad spectrum of products and services. These include program placement, underwriting, administration, acquisition of capital and credit capacity, strategic alliances, policy systems solutions, claims services, risk and safety consultation and reinsurance for property, casualty, workers compensation and other commercial lines of insurance coverage. |

Reinsurance. The Reinsurance segment underwrites international and U.S. reinsurance business through the segment’s primary business platform, Argo Re, Ltd., a Bermuda Class 4 insurance company (“Argo Re”). Argo Re also maintains offices through its subsidiary, Argo Solutions, S.A., in Belgium. The Reinsurance segment also operates a Casualty and Professional Lines division that provides primary excess coverage for general and products liability, Directors and Officers liability, Errors and Omissions liability, and Employment Practices Liability for global clients.

The Casualty and Professional Lines division accounted for approximately 29% of the Reinsurance business segment’s premium volume in 2010. In the last quarter of 2010 we announced that going forward, products offered by this division will be marketed under the unified Argo Insurance brand as Argo Insurance Worldwide Professional Lines and Argo Insurance Worldwide Casualty Lines.

Argo Re focuses on underwriting property catastrophe excess of loss reinsurance for a relatively small number of cedents whose accounts are known by the division’s underwriters. Argo Re will also underwrite property per risk and pro rata reinsurance on a select basis. Reinsurance underwritten by Argo Re covers underlying exposures which are located throughout the world including the United States. Property catastrophe reinsurance generally covers claims arising from large catastrophic events such as hurricanes, windstorms, hailstorms, earthquakes, volcanic eruptions, fires, industrial explosions, freezes, riots, floods and other man-made or natural disasters. In underwriting the property catastrophe portfolio, exposures are diversified geographically and by peril in order to manage the risks assumed and maximize return.

6

International Specialty. The International Specialty segment is focused on underwriting worldwide property and non-U.S. liability insurance on behalf of one underwriting syndicate, under the Lloyd’s of London (“Lloyd’s”) global franchise. The segment’s business platform, Argo International, is based in London and comprised of three principal components:

| | • | | Argo Managing Agency, which manages the syndicate for the providers of capital; |

| | • | | Syndicate 1200, which underwrites the insurance risk on a year of account basis; and |

| | • | | Argo Underwriting Agency, which participates with other capital providers on the syndicate. |

Argo International obtains its underwriting capital from a variety of sources and seeks to maintain a balance between capital managed on behalf of third parties and capital managed on behalf of Argo Group. The sources of the underwriting capital for the International Specialty segment include our interest provided through Argo International and Argo Re, third party capital participants referred to as trade capital providers and third party capital attributable to individual members referred to as Names and Other Capital. Trade capital providers participate either on a quota share basis or participate directly through the syndicate, assuming 100% of their contractual participation in the syndicate results with such results settled on a year of account basis. The flexibility in the sources of capital allows Argo International to manage its underwriting exposure over the insurance cycle with a view to maximizing profitability.

The table below represents our participation in the syndicate we manage by year of account:

| | | | | | | | |

| Year of account | | 2011 | | 2010 | | 2009 | |

| Participations on syndicate | | 1200 | | 1200 | | 1200 | |

Argo Group interest | | 69% | | 62% | | | 61% | |

Third party - Trade capital providers | | 20% | | 23% | | | 23% | |

Third party - Names and Other Capital | | 11% | | 15% | | | 16% | |

Argo International earns its income from return on the underwriting capital that is provided from its own resources, investment income on its capital resources and from commission earned from the management of third party capital. This commission is largely linked to profits generated on behalf of such capital.

Argo International’s worldwide property division concentrates mainly on underwriting short-tail risks with an emphasis on commercial property which are also exposed to catastrophes and other man-made or natural disasters. In underwriting the property portfolio, exposures are diversified geographically and by peril in order to manage the risks assumed and maximize return. The division maintains a flexible approach to underwriting and attempts to identify and respond to opportunities in territories and classes of business as they arise.

Argo International’s liability division underwrites non-U.S. professional indemnity, international general liability and directors & officers insurance. In addition, approximately 3% of the syndicate premium income is written on a range of U.S. general liability risks.

Underwriters leverage opportunities across geographies and risk layers within each of their divisions. Business is evaluated against risk and return requirements. Operating through Lloyd’s global franchise, Argo International is able to select the markets it operates in by their position in the insurance cycle and thus seek the most profitable business. Lloyd’s business is often written on a syndicate basis across the market. Argo International is the lead underwriter on approximately 40% of the business it underwrites.

Marketing and Distribution

We provide products and services to well defined niche markets. We leverage our capital strength and the Argo Group brands by cross-marketing the products offered by each of our segments among our other platforms and divisions the various operating companies. We offer our distribution partners tailored, innovative solutions for managing risk using the full range of products and services we have available.

Excess and Surplus Lines. Colony distributes its products through a network of appointed wholesale excess and surplus lines agents and brokers specializing in excess and surplus lines and certain targeted admitted lines. Approximately 71% of Colony’s premium volume during 2010 was produced through Colony wholesale agents that are appointed to underwrite, quote and issue policies subject to stated underwriting parameters authorized by Colony. The remaining 29% of Colony’s premium volume in 2010 was produced by Colony wholesale agents and brokers who submit business to Colony underwriters for quoting and issuance by Colony personnel. Argo Pro uses wholesale brokers in Allied Medical, Errors & Omissions and Environmental as well as retail agents for Insight’s products. Argonaut Specialty uses a select network of appointed excess and surplus lines brokers to distribute its products.

7

Commercial Specialty. Commercial Specialty’s distribution is multi-faceted, utilizing retail agents, direct to the insured, program managers and wholesale agents. Rockwood distributes its product lines through a network of independent retail and wholesale agents. Argo Select products and services are distributed through selected independent agents, brokers, wholesalers and program managers with demonstrated expertise in one or more of its targeted niche markets and through its in-house managing general agent and on a direct basis in a limited number of states. Alteris provides its insurance products and related services through licensed retail agents and selected state program managers for its Trident public entity operations, and through selected brokers, wholesalers and program managers within the specialty markets served by its other divisions. Argo Surety distributes its products through selected surety specialty agents and brokers across the United States.

Reinsurance. Argo Re has obtained substantially all of its insurance and reinsurance business through brokers and intermediaries who represent clients in negotiations for the purchase of reinsurance. None of the intermediaries through which Argo Re obtains this business are authorized to bind insurance business in our name without our approval. Argo Re pays commissions to these intermediaries or brokers that vary in size based on the amount of premiums and type of business assumed by Argo Re. The Casualty and Professional Lines division distributes its products through selected brokers who have established their credentials and experience with our underwriters through prior dealings.

International Specialty. Argo International obtains underwriting business from two main sources: the Lloyd’s open market, and underwriting agencies with delegated authority. In the Lloyd’s open market, brokers approach Argo International directly with individual insurance risk opportunities for consideration by our underwriters. Brokers also approach Argo International through selected underwriting agencies that have been granted limited authority delegated by Argo International to make underwriting decisions on individual risks In general, risks written on the open market business are larger than risks written on our behalf by authorized agencies in terms of both exposure and premium.

Competition

We compete in a variety of markets against a variety of competitors. While Argo Group’s principal direct insurance competitors cannot be easily summarized our principal lines of business are written by numerous other insurance companies as well. Competition for any one account may come from very large international firms or smaller regional companies in the domiciles in which we operate.

To remain competitive, our strategy includes, among other measures, (1) focusing on rate adequacy and underwriting discipline, (2) leveraging our distribution network, (3) controlling expenses, (4) maintaining financial strength and issuer credit ratings, (5) providing quality services to agents and policyholders and (6) acquiring suitable property and casualty books of business.

Excess and Surplus Lines. Competition within the excess and surplus lines marketplace comes from a wide range of carriers. In addition to mature companies that operate nationwide, there is competition from carriers formed in recent years. The Excess and Surplus Lines segment may also compete with national and regional carriers from the standard market willing to underwrite selected accounts on an admitted basis.

Commercial Specialty. Due to the diverse nature of the products offered by the Commercial Specialty segment, competition comes from various sources. The majority of the competition comes from regional companies or regional subsidiaries of national carriers in the domiciles in which they operate. National carriers tend to compete for larger accounts along all product lines. Competition for our public entity products is primarily from small to medium size commercial insurers as well as from state and regional risk pools.

Reinsurance.Argo Re competes with numerous reinsurance and insurance companies. These competitors, many of whom have higher credit ratings and substantially greater financial, marketing and management resources than Argo Re, include independent insurance and reinsurance companies, subsidiaries or affiliates of established worldwide insurance companies, departments of certain commercial insurance companies and underwriting syndicates.

8

International Specialty.The principal lines of business in this segment are written by numerous other insurance companies and syndicates at Lloyd’s. Competition for any one account may come from other Lloyd’s syndicates, international firms or smaller regional companies. To remain competitive, Argo International’s strategy includes, among other measures, leveraging the Lloyd’s brand.

Ratings

Financial Strength Ratings are an important factor in establishing the competitive position of insurance and reinsurance companies. A.M. Best Company (“A.M. Best”) and Standard & Poor’s (“S&P”) have each developed a rating system to provide an opinion of an insurer’s or reinsurer’s financial strength and ability to meet ongoing obligations to its policyholders. Each rating reflects the rating agency’s opinion of the capitalization, management and sponsorship of the entity to which it relates, and is neither an evaluation directed to investors in our common shares nor a recommendation to buy, sell or hold our common shares.

A.M. Best ratings current range from “A++” (Superior) to “F” (In Liquidation) and include 16 separate ratings categories. S&P maintains a letter scale rating system ranging from “AAA” (Extremely Strong) to “R” (under regulatory supervision) and includes 21 separate ratings categories. With the exception of ARIS Title Insurance Corporation which has yet to be rated, all of our insurance and reinsurance companies have a Financial Strength Rating of “A” (Excellent) with a stable outlook from A.M. Best, and our U.S. insurance subsidiaries have a Financial Strength Rating of “A-” (Strong) with a stable outlook from S&P.

In addition, Argo Group US, Inc. has an Issuer Credit Rating of “BBB-” (Good) with a stable outlook from S&P.

Argo International operates as a Lloyd’s syndicate, and therefore, benefits from the ratings assigned to Lloyd’s rather than receiving an independent rating. As all Lloyd’s policies are ultimately backed by the Lloyd’s Central Fund, a single market rating is applied. Lloyd’s, as a market, is rated “A” (Excellent) by A.M. Best and “A+” (Strong) by S&P.

Regulation

General

The business of insurance and reinsurance is regulated in most countries, although the degree and type of regulation varies significantly from one jurisdiction to another. The principal jurisdictions in which our insurance and reinsurance segments operate are Bermuda, the United States and the United Kingdom. We are also regulated by other countries where we do business.

Bermuda

As a holding company, we are not currently subject to Bermuda insurance regulations. However, the Insurance Act of 1978 and related regulations, as amended (together, the “Insurance Act”), govern the insurance business activities of Argo Re, our operating subsidiary in Bermuda, and provide that no person may carry on the insurance business in or from within Bermuda unless registered as an insurer by the Bermuda Monetary Authority (the “BMA”). Under the Insurance Act, no distinction is made between insurance and reinsurance business.

Classification of Insurers

The Insurance Act distinguishes between special purpose insurers, insurers carrying on long-term business and insurers carrying on general business. There are six classifications of insurers carrying on general business, with Class 4 insurers subject to the strictest regulation. Argo Re, which is incorporated to carry on general insurance and reinsurance business, is registered as a Class 4 insurer in Bermuda and is regulated as such under the Insurance Act.

Principal Representative

An insurer is required to maintain a principal office in Bermuda and to appoint and maintain a principal representative in Bermuda.

9

Solvency and Group Regulation

Regulators in Bermuda and other jurisdictions in which we operate are considering various proposals for financial and regulatory reform. In particular, Bermuda continues to enhance its risk-based regulatory regime, which is intended to meet or exceed international standards. The directives covering this regime are often referred to as Solvency II. Many of the areas covered under this initiative will be phased over a number of years. The BMA’s aim is to create a regime which has three core components: (1) Capital Adequacy, (2) Governance and Risk Management, and (3) Disclosure. Most of these elements are interconnected and potentially influenced by developments in other international regimes. As a risk-based capital regime necessitates a strong system of governance and risk management, which reflects the integration of risk and capital management, the BMA has issued its “Insurance Code of Conduct” in February 2010, allowing the market to be fully compliant by 1st July 2011.

Additionally, Bermuda is striving to become recognized by the EU as having an “equivalent solvency regime” in an effort to benefit Bermuda-based companies by utilizing recognition agreements which would acknowledge equivalent solvency requirements and protect these insurers and reinsurers from having to fulfill the solvency requirements under various and differing regimes.

Furthermore, Solvency II-like directives will result in the appointment of a designated “group supervisor” to oversee the group’s overall risk and solvency situation. BMA has asserted that it believed itself to be the proper Group Supervisor for Argo Group.

Argo Re

Effective December 31, 2007, Argo Group amalgamated its two Bermuda reinsurers, Peleus Re and PXRE Reinsurance Ltd. (“PXRE Bermuda”), with Peleus Re as the continuing company. Peleus Re, prior to the amalgamation, was a Class 3 general business insurer, and PXRE Bermuda was a Class 4 general business insurer. As a result of the amalgamation, Peleus Re was granted a Class 4 license under the Insurance Act. Effective April 7, 2008, the name of Peleus Re was changed to Argo Re, Ltd.

The Insurance Act imposes on Bermuda insurance companies, including Argo Re, solvency and liquidity standards and auditing and reporting requirements, and grants to the BMA powers to supervise, investigate and intervene in the affairs of insurance companies. Specifically, the Insurance Act provides that the value of the general business assets of a Class 4 insurer must exceed the amount of its general business liabilities by an amount greater than the prescribed minimum solvency margin. Argo Re, as a Class 4 insurer, is required to maintain a minimum solvency margin equal to the greatest of: (a) $100.0 million, (b) 50% of net premiums written (with a deduction for ceded reinsurance from gross premiums written not exceeding 25% of gross premiums written) or (c) 15% of loss reserves. If Argo Re’s total statutory capital and surplus falls to $75.0 million or less, it will have to comply with additional reporting requirements as mandated by the BMA.

The Insurance Act sets out a standard mathematical model designed to give the BMA more advanced methods for determining an insurer’s capital adequacy: the Bermuda Solvency Capital Requirement model (the “BSCR”). Insurers may also apply in-house models that deal with their own particular risks and where such models satisfy the standards established by the BMA, such insurers may apply to the BMA to use such models in lieu of the BSCR. The amount calculated in accordance with the BSCR or a company’s approved in-house model is referred to as its enhanced capital requirement (“ECR”).

In addition to the BMA’s powers under the Insurance Act to issue directions, where the BMA concludes that the risk profile of an insurer deviates significantly from (a) the assumptions underlying the enhanced capital requirement applicable to it or (b) from the insurer’s own assessment of its risk management policies and practices in calculating its own enhanced capital requirement, the BMA may, subject to compliance with the relevant provisions of the Act, make such adjustments to an insurer’s enhanced capital requirement and available statutory capital and surplus as it considers appropriate.

Underlying the BSCR is the belief that all insurers should operate with a view to maintaining their capital at a prudent level in excess of the minimum solvency margin prescribed under the Insurance Act. Currently all Class 4 insurers, including Argo Re, are expected to maintain their capital at a target level that is set at 120% of the ECR. At December 31, 2010, Argo Re exceeded the target level.

10

The Insurance Act provides a minimum liquidity ratio for general business. An insurer engaged in general business is required to maintain the value of its relevant assets at not less than 75% of the amount of its relevant liabilities. Relevant assets include cash and time deposits, quoted investments, unquoted bonds and debentures, first liens on real estate, investment income due and accrued, accounts and premiums receivable and reinsurance balances receivable. There are certain categories of assets that, unless specifically permitted by the BMA, do not automatically qualify as relevant assets; these include unquoted equity securities, investments in and advances to affiliates, real estate and collateral loans. The relevant liabilities are total general business insurance reserves and total other liabilities less deferred income tax and sundry liabilities (by interpretation, those not specifically defined).

As of December 31, 2010, Argo Re’s solvency and liquidity margins and statutory capital and surplus were in excess of the minimum levels required by the Insurance Act.

As a registered Class 4 insurer, Argo Re is required to submit an opinion of its approved loss reserve specialist with its statutory financial return in respect of its loss and loss expense reserves. The appointment of a loss reserve specialist, who will normally be a qualified casualty actuary, must be approved by the BMA. Argo Re has appointed a loss reserve specialist who has been approved by the BMA to serve in such capacity.

Any person who, directly or indirectly, becomes a holder of at least 10 percent, 20 percent, 33 percent or 50 percent of our common shares must notify the BMA in writing within 45 days of becoming such a holder or 30 days from the date they have knowledge of having such a holding, whichever is later. The BMA may, by written notice, object to such a person if it appears to it that the person is not fit and proper to be such a holder. The BMA may require the holder to reduce its holding of our common shares and direct, among other things, that voting rights attaching to the common shares shall not be exercisable.

Dividends

The payment of dividends by Argo Re is limited under the Insurance Act. Argo Re is prohibited from declaring or paying any dividends during any financial year it is in breach of its minimum solvency margin or minimum liquidity ratio or if the declaration or payment of such dividends would cause it to fail to meet such margin or ratio. If it fails to meet its minimum solvency margin or minimum liquidity ratio on the last day of any financial year, the insurer will be prohibited, without the approval of the BMA from declaring or paying any dividends during the next financial year. As of December 31, 2010, Argo Re’s solvency and liquidity margins and statutory capital and surplus were in excess of the minimum levels required by the Insurance Act. As of December 31, 2010, the unaudited statutory capital and surplus of Argo Re was estimated to be $1,251.0 million and the amount required to be maintained was estimated to be $268.7 million. As of December 31, 2010, Argo Re’s total investments in subsidiaries in its statutory balance sheet were approximately $761.6 million.

In March 2010, Argo Re paid a cash dividend of $17.5 million to Argo Group. Argo Re did not pay dividends to Argo Group in 2009 and 2008.

United States

State Insurance Regulation

Argo Group’s U.S. insurance subsidiaries are subject to the supervision and regulation of the states in which they are domiciled. We currently have twelve insurance companies domiciled in five states (the “U.S. Subsidiaries”). Argo Group, as the indirect parent of the U.S. Subsidiaries, is subject to the insurance holding company laws of Illinois, New York, Ohio, Pennsylvania and Virginia. These laws generally require each of the U.S. Subsidiaries to register with its respective domestic state insurance department and to furnish annually financial and other information about the operations of the companies within the holding company group. Generally, all material transactions among companies in the holding company group to which any of the U.S. Subsidiaries is a party, including sales, loans, reinsurance agreements and service agreements, must be fair and, if material or of a specified category, require prior notice and approval or non-disapproval by the insurance department where the subsidiary is domiciled. Transfers of assets among such affiliated companies, certain dividend payments from insurance subsidiaries and certain material transactions between companies within the group may be subject to prior notice to, or prior approval by, state regulatory authorities. Such supervision and regulation is designed to protect our policyholders rather than our shareholders. Matters relating to authorized lines of business, underwriting standards, financial condition standards, licensing of insurers, investment standards, premium levels, policy provisions, the filing of annual and other financial reports prepared on the basis of Statutory Accounting Principles, the filing and form of actuarial reports, dividends, and a variety of other financial and non-financial matters are also areas that are regulated and supervised by the state in which our insurance subsidiaries are domiciled.

11

Guarantee Associations

Our U.S. insurance subsidiaries are participants in the statutorily created insolvency guarantee associations in all states where they are admitted licensed carriers. These associations were formed for the purpose of paying claims of insolvent companies. We are assessed our pro rata share of such claims based upon our premium writings, subject to a maximum annual assessment per line of insurance. Such costs can generally be recovered through surcharges on future premiums. Non-admitted business is neither supported by or subject to guaranty assessments.

Dividends

Effective December 31, 2007, Argonaut Group, Inc. and PXRE Corporation, two of our intermediate holding companies merged. PXRE Corporation was the surviving entity and was renamed Argonaut Group, Inc. Effective April 7, 2008, Argonaut Group, Inc. was renamed Argo Group US, Inc. (“Argo Group US”). As a result of the merger, all of our U.S. Subsidiaries became subsidiaries of Argo Group US.

As an insurance and reinsurance holding company, Argo Group is largely dependent on dividends and other permitted payments from our insurance subsidiaries to pay cash dividends to our shareholders, for debt service and for our operating capital. The ability of our insurance subsidiaries to pay dividends to Argo Group is subject to certain restrictions imposed by the jurisdictions of domicile that regulate our immediate insurance subsidiaries and each jurisdiction has calculations for the amount of dividends that an insurance company can pay without the approval of its insurance regulator. Argo Group US is able to receive dividends from its direct subsidiaries: Argonaut Insurance Company, Colony and Rockwood. For the year ended December 31, 2010, Colony paid a dividend to Argo Group US in the amount of $50.0 million in the form of $25.2 million in cash and $24.8 million in securities. The dividend was paid and notice was provided to the Virginia Bureau of Insurance. For the year ended December 31, 2010, Rockwood paid an extraordinary dividend to Argo Group US in the amount of $30.0 million. The dividend was paid after receiving approval from the Pennsylvania Department of Insurance. For the year ended December 31, 2010, Argonaut Insurance Company paid a dividend to Argo Group US in the amount of $25.0 million. During 2011, Argonaut Insurance Company may be permitted to pay dividends of up to $13.0 million in cash without approval from the Illinois Department of Insurance, based on the state of domicile’s ordinary dividend calculation. Colony may be permitted, during 2011, to pay dividends of up to $53.5 million in cash without approval from the Virginia Bureau of Insurance, based on the state of domicile’s ordinary dividend calculation. Rockwood may be permitted, during 2011, to pay dividends of up to $13.7 million in cash without approval from the Pennsylvania Department of Insurance, based on the state of domicile’s ordinary dividend calculation. Business and regulatory considerations may impact the amount of dividends actually paid, and prior approval of dividend payments may be required.

State laws require prior notice or regulatory agency approval of direct or indirect changes in control of an insurer, reinsurer, or its holding company, and of certain significant inter-corporate transfers of assets within the holding company structure. An investor who acquires or attempts to acquire shares representing or convertible into more than 10% of the voting power of the securities of Argo Group would become subject to at least some of such regulations, would require approval by the five regulators of Argo Group’s U.S. Subsidiaries prior to acquiring such shares and would be required to file certain notices and reports with the five regulators prior to such acquisition.

The Terrorism Risk Insurance Program Reauthorization Act

The Terrorism Risk Insurance Program Reauthorization Act of 2007 was signed into law by the U.S. President on December 26, 2007. This law renews the prior federal terrorism risk insurance program through December 31, 2014. The program includes protections for acts of domestic terrorism. The insurer deductible is fixed at 20% of an insurer’s direct earned premium, and the federal share of compensation is fixed at 85% of insured losses that exceed insurer deductibles, subject to a $100 billion cap. The U.S. Treasury Department is required to promulgate regulations to determine the pro-rata share of insured losses if they exceed the $100 billion cap. In addition, clear and conspicuous notice to policyholders of the $100 billion cap is required. Under the program reauthorization, the trigger at which federal compensation becomes available remains fixed at $100 million per year through 2014.

12

United Kingdom

FSA Regulations.

Argo International’s operations are regulated by the U.K. Financial Services Authority (“FSA”) and franchised by Lloyd’s of London. The FSA has substantial powers of intervention in relation to the Lloyd’s managing agents (such as Argo International) which it regulates, including the power to remove their authorization to manage Lloyd’s syndicates. In addition, each year the FSA requires Lloyd’s to satisfy an annual solvency test that measures whether Lloyd’s has sufficient assets in the aggregate to meet all outstanding liabilities of its members, both current and run-off. If Lloyd’s fails this test, the FSA may require Lloyd’s to cease trading and/or its members to cease or reduce underwriting.

Lloyd’s Regulations and Requirements.

Argo International’s operations are franchised by Lloyd’s. The Council of Lloyd’s has wide discretionary powers to regulate members’ underwriting at Lloyd’s. The Lloyd’s Franchise Board is responsible for setting risk management and profitability targets for the Lloyd’s market and operates a business planning and monitoring process for all syndicates, including reviewing and approving the syndicates’ annual business plan. The Lloyd’s Franchise Board requires annual approval of Argo International’s business plan, including maximum underwriting capacity, and may require changes to any business plan presented to it or that additional capital to be provided to support underwriting. Lloyd’s also imposes various charges and assessments on its members. Dividends from a Lloyd’s managing agent and a Lloyd’s corporate member can be declared and paid provided it has sufficient profits available.

Argo International predominately participates in the Lloyd’s market through Argo (No 604) Ltd, a Lloyd’s corporate member. By entering into a membership agreement with Lloyd’s, Argo (No 604) Ltd undertakes to comply with all Lloyd’s by-laws and regulations as well as the provisions of the Lloyd’s Acts and Financial Services and Markets Act 2000 that are applicable to it. The underwriting capacity of a member of Lloyd’s must be supported by providing a deposit (referred to as “Funds at Lloyd’s) in the form of cash, securities or letters of credit in an amount determined under the Individual Capital Adequacy regime of the FSA. The amount of such deposit is calculated for each member through the completion of an annual capital adequacy exercise. These requirements allow Lloyd’s to evaluate that each member has sufficient assets to meet its underwriting liabilities plus a required solvency margin.

If a member of Lloyd’s is unable to pay its debts to policyholders, such debts may be payable by the Lloyd’s Central Fund, which in many respects acts as an equivalent to a state guaranty fund in the United States. If Lloyd’s determines that the Central Fund needs to be increased, it has the power to assess premium levies on current Lloyd’s members. The Council of Lloyd’s has discretion to call or assess up to 3% of a member’s underwriting capacity in any one year as a Central Fund contribution.

Solvency II

The European Commission, which acts as the initiator of action and executive body of the EU, has introduced a new directive on insurance regulation and solvency requirements known as Solvency II. This directive was approved by the European Parliament in April 2009 and adopted by the European Council in November 2009. Currently, the European Commission is implementing the Directive and utilizing a three stage process of consultation with Member State regulators and insurance firms. The full implementation of Solvency II is set for December 31, 2012. Solvency II, which is a significant enhancement of the existing Solvency I framework, is the improved regulatory regime which will impose economic risk-based solvency requirements across all EU Member States and consists of three pillars: (1) Pillar I – quantitative capital requirements, based on a valuation of the entire balance sheet; (2) Pillar II – qualitative regulatory review, which includes governance, internal controls, enterprise risk management and supervisory review process; and (3) Pillar III – market discipline, which is accomplished through reporting of the insurer’s financial condition to regulators.

Argo International, Argo Group’s European-based operation at Lloyd’s of London, will be required to comply with Solvency II and is undertaking actions to be compliant by the imposed implementation date.

Dividends

Dividend payments from Argo International to its immediate parent are not restricted by regulatory authority. Dividend payments will be at the discretion of Argo International’s Board of Directors and will be subject to the earnings, operations, financial condition, capital and general business requirements of Argo International.

13

Reinsurance

As is common practice within the insurance industry, Argo Group’s insurance and reinsurance subsidiaries transfer a portion of the risks insured under their policies by entering into a reinsurance treaty with another insurance company. Purchasing reinsurance protects primary carriers against the frequency and/or severity of losses incurred on the policies they issue, such as in the case of unusually serious occurrences in which a number of claims on one policy aggregate to produce an extraordinary loss on one policy or where a catastrophe generates a large number of serious claims on multiple policies at the same time. Reinsurance does not discharge the issuing primary carrier from its obligation to pay a policyholder for losses insured under its policy. Rather, the reinsured portion of each loss covered under a reinsurance treaty is ceded to the assuming reinsurer for reimbursement to the primary carrier. Because this creates a receivable owed by the reinsurer to the primary carrier, there is credit exposure with respect to losses ceded to the extent that any reinsurer is unable or unwilling to meet the obligations assumed under its reinsurance treaty. The ability to collect on reinsurance is subject to the solvency of the reinsurers, interpretation of contract language and other factors. We are selective in regard to our reinsurers, seeking out those with strong financial strength ratings from A.M. Best or S&P. However, the financial condition of a reinsurer may change over time based on market conditions. We perform credit reviews on our reinsurers, focusing on, among other things, financial condition, stability, trends and commitment to the reinsurance business. In certain instances we also require deposit of assets in trust, letters of credit or other acceptable collateral to support balances due from certain reinsurers whose financial strength ratings fall below a certain level or who transact business on a non-admitted basis in the case of the US subsidiaries in the state where our insurance subsidiary is domiciled.

At December 31, 2010, Argo Group’s reinsurance recoverable balance totaled $1,203.9 million, net of an allowance for doubtful accounts of $15.7 million. The following table reflects the credit ratings for the reinsurers comprising the $1,203.9 million reinsurance recoverable balance at December 31, 2010:

| | | | | | | | |

($’s in millions) Ratings per A.M. Best | | Reinsurance

Recoverables | | | % of Total | |

| | |

Reinsurers rated A+ or better | | $ | 365.5 | | | | 30.4% | |

Reinsurers rated A | | | 660.3 | | | | 54.8% | |

Reinsurers rated A- | | | 69.8 | | | | 5.8% | |

Reinsurers rated below A- or not rated | | | 108.3 | | | | 9.0% | |

| | | | | | | | |

| | $ | 1,203.9 | | | | 100.0% | |

| | | | | | | | |

The top ten reinsurers, all rated A or higher, accounted for $802.7 million, or approximately 67% of the reinsurance recoverable balance as of December 31, 2010. Management has concluded that all net balances are considered recoverable as of December 31, 2010.

Additional information relating to our reinsurance activities is included under Item 7 “Management’s Discussion and Analysis of Financial Condition and Results of Operations” on pages 42-72 and Note 4, “Reinsurance” in the Notes to the Consolidated Financial Statements.

Reserves for Losses and Loss Adjustment Expenses

Argo Group records reserves for specific claims incurred and reported, as well as reserves for claims incurred but not reported. The estimates of losses for reported claims are established judgmentally on an individual case basis. Such estimates are based on our particular experience with the type of risk involved and our knowledge of the circumstances surrounding each individual claim. Reserves for reported claims consider our estimate of the ultimate cost to settle the claims, including investigation and defense of the claim, and may be adjusted for differences between costs originally estimated and costs re-estimated or incurred.

Reserves for incurred but not reported claims are based on the estimated ultimate cost of settling claims, including the effects of inflation and other social and economic factors, using past experience adjusted for current trends and any other factors that would modify past experience. Argo Group uses a variety of statistical and actuarial techniques to analyze current claims costs, frequency and severity data, and prevailing economic, social and legal factors. Reserves established in prior years are adjusted as loss experience develops and new information becomes available. Adjustments to previously estimated reserves are reflected in results in the year in which they are made.

14

The estimate of reinsurance recoverables related to reported and unreported losses and loss adjustment expenses represent the portion of the gross liabilities that are anticipated to be recovered from reinsurers. Amounts recoverable from reinsurers are recognized as assets at the same time as, and in a manner consistent with, the gross losses associated with the reinsurance treaty.

Argo Group is subject to claims arising out of catastrophes that may have a significant effect on its business, results of operations, and/or financial condition. Catastrophes can be caused by various events, including hurricanes, windstorms, earthquakes, hailstorms, explosions, power outages, severe winter weather, fires and by man-made events, such as terrorist attacks. The incidence and severity of catastrophes are inherently unpredictable. The extent of losses from a catastrophe is a function of both the total amount of insured exposure in the area affected by the event and the severity of the event.

Terrorism peril is deemed by Argo Group to include the damage resulting from various terrorist attacks through either conventional weapons or weapons of mass destruction such as nuclear or radioactive explosive devices as well as chemical and biological contaminants. We continue to review our underwriting data in assessing aggregate exposure to this peril. We underwrite against the risk of terrorism with a philosophy of avoidance wherever possible to the extent permitted by applicable law. For both property and casualty exposures, this is accomplished through the use of portfolio tracking tools that identify high risk areas, as well as areas of potential concentration. We estimate the probable maximum loss from each risk as well as for the portfolio in total and factor this analysis into the underwriting and reinsurance buying process. The probable maximum loss is model generated, and subject to assumptions that may not be reflective of ultimate losses incurred for a terrorist act.

Additionally, Argo Group has identified certain high risk locations and hazardous operations where there is a potential for an explosion or a rapid spread of fire due to a terrorist act. Through modeling, we continue to refine our estimates of the probable maximum loss from such an event and factor this analysis into the underwriting evaluation process and also seek to mitigate this exposure through various policy terms and conditions (where allowed by statute) and through the use of reinsurance, to the extent possible. Our current reinsurance arrangements either exclude terrorism coverage or significantly limit the level of coverage that is provided.

Terrorism exclusions are not permitted in the United States for workers compensation policies under United States federal law or under the laws of any state or jurisdiction in which we operate. When underwriting existing and new workers compensation business, we consider the added potential risk of loss due to terrorist activity, including foreign and domestic, and this may lead us to decline to underwrite or to renew certain business. However, even in lines where terrorism exclusions are permitted, because our clients may object to terrorism exclusion in connection with business that we may still desire to underwrite without an exclusion, some or many of our insurance policies may not include a terrorism exclusion. Given the retention limits imposed under the U.S. federal act and that some or many of our policies may not include exclusion for terrorism, future foreign or domestic terrorist attacks may result in losses that have a material adverse effect on our business, results of operations and/or financial condition.

Argo Group has discontinued underwriting certain lines of business; however, we are still obligated to pay losses incurred on these lines. Certain lines currently in run-off are characterized by long elapsed periods between the occurrence of a claim and any ultimate payment to resolve the claim. Included in Run-off Lines are claims related to asbestos and environmental liabilities arising out of liability policies primarily written in the 1960s, 1970s and into the mid-1980s, with a limited number of claims occurring on policies written into the early 1990s. Also included in Run-off Lines is other business previously written and classified by PXRE as property catastrophe and Lloyd’s of London. Business formerly written in our Risk Management segment is also classified in the Run-off Lines segment. Additional discussion on Run-off Lines can be found under Item 7 “Management’s Discussion and Analysis of Financial Condition and Results of Operations” on pages 42 - 72

The tables below present a development of loss and loss adjustment expense reserve liabilities and payments for the years 2000 through 2010. The information presented in Table I is net of the effects of reinsurance. The information presented in Table II includes only amounts related to direct and assumed insurance. The amounts in the tables for the year ended December 31, 2000 do not include Colony’s and Rockwood’s unpaid losses and loss adjustment expenses since these entities were acquired in 2001. Amounts for the former PXRE companies are not included for the years prior to 2007, the year of acquisition. Additionally, amounts for Argo International are not included for the years prior to 2008, the year of acquisition.

15

Table I

Analysis of Losses and Loss Adjustment Expense (“LAE”) Development

(Net of Reinsurance)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| (in millions) | | 2000 | | | 2001 | | | 2002 | | | 2003 | | | 2004 | | | 2005 | | | 2006 | | | 2007 | | | 2008 | | | 2009 | | | 2010 | |

| | | | | | | | | | | |

Reserves for Losses and LAE (1) | | | $ 757.6 | | | | $ 929.6 | | | | $ 838.2 | | | | $ 965.5 | | | | $ 1,060.8 | | | | $ 1,394.8 | | | | $ 1,530.5 | | | | $ 1,863.3 | | | | $ 2,115.6 | | | | $ 2,213.2 | | | | $ 2,253.0 | |

Cumulative Amount Paid as of (2) | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

1 year later | | | 154.0 | | | | 200.1 | | | | 188.7 | | | | 230.5 | | | | 183.1 | | | | 235.6 | | | | 286.6 | | | | 410.9 | | | | 567.8 | | | | 577.9 | | | | | |

2 years later | | | 255.1 | | | | 327.5 | | | | 348.8 | | | | 354.1 | | | | 341.9 | | | | 435.2 | | | | 517.8 | | | | 721.5 | | | | 965.5 | | | | | | | | | |

3 years later | | | 326.7 | | | | 449.8 | | | | 431.9 | | | | 471.6 | | | | 492.9 | | | | 600.3 | | | | 712.7 | | | | 930.0 | | | | | | | | | | | | | |

4 years later | | | 394.2 | | | | 509.5 | | | | 514.0 | | | | 588.5 | | | | 614.0 | | | | 734.0 | | | | 840.9 | | | | | | | | | | | | | | | | | |

5 years later | | | 428.4 | | | | 573.1 | | | | 609.3 | | | | 683.0 | | | | 717.1 | | | | 822.2 | | | | | | | | | | | | | | | | | | | | | |

6 years later | | | 471.9 | | | | 656.3 | | | | 688.0 | | | | 765.5 | | | | 785.3 | | | | | | | | | | | | | | | | | | | | | | | | | |

7 years later | | | 538.9 | | | | 726.8 | | | | 763.4 | | | | 825.4 | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

8 years later | | | 597.7 | | | | 796.5 | | | | 817.4 | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

9 years later | | | 658.6 | | | | 847.7 | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

10 years later | | | 702.3 | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | |

Reserves Re-estimated as of (3) | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

1 year later | | | 773.2 | | | | 991.5 | | | | 879.0 | | | | 964.6 | | | | 1,216.0 | | | | 1,349.9 | | | | 1,499.4 | | | | 1,798.6 | | | | 2,109.3 | | | | 2,170.1 | | | | | |

2 years later | | | 820.3 | | | | 1,034.0 | | | | 889.9 | | | | 1,158.2 | | | | 1,196.3 | | | | 1,331.4 | | | | 1,472.5 | | | | 1,757.9 | | | | 2,018.4 | | | | | | | | | |

3 years later | | | 851.1 | | | | 1,053.5 | | | | 1,090.7 | | | | 1,161.3 | | | | 1,200.2 | | | | 1,306.5 | | | | 1,446.1 | | | | 1,696.9 | | | | | | | | | | | | | |

4 years later | | | 875.7 | | | | 1,084.9 | | | | 1,099.7 | | | | 1,187.3 | | | | 1,196.0 | | | | 1,316.3 | | | | 1,413.5 | | | | | | | | | | | | | | | | | |

5 years later | | | 905.9 | | | | 1,100.9 | | | | 1,138.0 | | | | 1,189.0 | | | | 1,219.5 | | | | 1,296.8 | | | | | | | | | | | | | | | | | | | | | |

6 years later | | | 921.8 | | | | 1,141.9 | | | | 1,142.6 | | | | 1,208.3 | | | | 1,208.1 | | | | | | | | | | | | | | | | | | | | | | | | | |

7 years later | | | 961.8 | | | | 1,147.7 | | | | 1,166.1 | | | | 1,208.4 | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

8 years later | | | 964.7 | | | | 1,174.3 | | | | 1,172.9 | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

9 years later | | | 987.2 | | | | 1,184.0 | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

10 years later | | | 991.7 | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Cumulative (Deficiency) Redundancy (4) (5) | | | (234.1) | | | | (254.4) | | | | (334.7) | | | | (242.9) | | | | (147.3) | | | | 98.0 | | | | 117.0 | | | | 166.4 | | | | 97.2 | | | | 43.1 | | | | | |

Prior Yr. Cumulative (Deficiency) Redundancy (5) | | | (229.6) | | | | (244.7) | | | | (327.9) | | | | (242.8) | | | | (158.7) | | | | 78.5 | | | | 84.4 | | | | 105.4 | | | | 6.3 | | | | - | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Change in Cumulative (Deficiency) Redundancy | | | $ (4.5) | | | | $ (9.7) | | | | $ (6.8) | | | | $ (0.1) | | | | $ 11.4 | | | | $ 19.5 | | | | $ 32.6 | | | | $ 61.0 | | | | $ 90.9 | | | | $ 43.1 | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| (1) | Original estimated reserves for losses and LAE, net of reinsurance, as of the balance sheet date for each of the years indicated. |

| (2) | Cumulative amounts paid, net of reinsurance payments as of the end of successive years related to those reserves. |

| (3) | Re-estimated reserves are calculated by adding cumulative amounts paid subsequent to year-end to the re-estimated unpaid losses and LAE for each year. |

| (4) | Cumulative (deficiency) redundancy, compares the adjusted reserves (3) to the reserves as originally established (1) and shows that the reserves as originally recorded were either inadequate or excessive to cover the estimated cost of claims as of the respective year end. |

| (5) | The Cumulative (Deficiency) Redundancy for each of the current year and prior year lines includes $176.2 million of (Deficiency) related to the commutation of the Adverse Development Contract (“ADC”) for each of the 2002 through 2004 years. There is no net effect to the change in Cumulative (Deficiency) Redundancy. |

16

Table II

Analysis of Losses and Loss Adjustment Expense (“LAE”) Development

(Gross Reserves)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| (in millions) | | 2000 | | | 2001 | | | 2002 | | | 2003 | | | 2004 | | | 2005 | | | 2006 | | | 2007 | | | 2008 | | | 2009 | | | 2010 | |

| | | | | | | | | | | |

Reserves for Losses and LAE (1) | | $ | 930.7 | | | $ | 1,147.8 | | | $ | 1,281.6 | | | $ | 1,480.8 | | | $ | 1,607.5 | | | $ | 1,875.4 | | | $ | 2,029.2 | | | $ | 2,425.5 | | | $ | 2,996.6 | | | $ | 3,203.3 | | | $ | 3,152.2 | |

Cumulative Amount Paid as of (2) | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

1 year later | | | 190.0 | | | | 246.0 | | | | 236.7 | | | | 316.2 | | | | 275.2 | | | | 335.6 | | | | 358.9 | | | | 499.5 | | | | 789.5 | | | | 834.9 | | | | | |

2 years later | | | 316.1 | | | | 411.5 | | | | 464.6 | | | | 501.0 | | | | 470.4 | | | | 578.5 | | | | 650.4 | | | | 894.6 | | | | 1,383.8 | | | | | | | | | |

3 years later | | | 404.8 | | | | 594.1 | | | | 596.1 | | | | 638.8 | | | | 645.5 | | | | 784.1 | | | | 903.7 | | | | 1,198.9 | | | | | | | | | | | | | |

4 years later | | | 515.2 | | | | 688.8 | | | | 691.3 | | | | 771.7 | | | | 791.9 | | | | 957.1 | | | | 1,086.7 | | | | | | | | | | | | | | | | | |

5 years later | | | 577.7 | | | | 762.8 | | | | 798.5 | | | | 882.2 | | | | 924.0 | | | | 1,085.4 | | | | | | | | | | | | | | | | | | | | | |

6 years later | | | 628.1 | | | | 854.7 | | | | 890.0 | | | | 990.4 | | | | 1,026.2 | | | | | | | | | | | | | | | | | | | | | | | | | |

7 years later | | | 700.0 | | | | 934.6 | | | | 988.8 | | | | 1,081.0 | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

8 years later | | | 764.4 | | | | 1,025.9 | | | | 1,072.5 | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

9 years later | | | 844.8 | | | | 1,105.9 | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

10 years later | | | 913.4 | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Reserves Re-estimated as of (3) | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

1 year later | | | 966.2 | | | | 1,265.3 | | | | 1,370.1 | | | | 1,489.5 | | | | 1,604.1 | | | | 1,792.0 | | | | 1,960.1 | | | | 2,369.6 | | | | 3,044.0 | | | | 3,135.0 | | | | | |

2 years later | | | 1,061.3 | | | | 1,346.3 | | | | 1,394.1 | | | | 1,519.2 | | | | 1,547.1 | | | | 1,741.6 | | | | 1,939.8 | | | | 2,333.4 | | | | 2,899.6 | | | | | | | | | |

3 years later | | | 1,094.0 | | | | 1,381.4 | | | | 1,425.7 | | | | 1,486.5 | | | | 1,540.8 | | | | 1,727.4 | | | | 1,932.3 | | | | 2,254.1 | | | | | | | | | | | | | |

4 years later | | | 1,146.5 | | | | 1,405.4 | | | | 1,410.5 | | | | 1,513.7 | | | | 1,542.9 | | | | 1,764.7 | | | | 1,869.9 | | | | | | | | | | | | | | | | | |

5 years later | | | 1,167.7 | | | | 1,406.0 | | | | 1,455.6 | | | | 1,515.5 | | | | 1,608.2 | | | | 1,725.1 | | | | | | | | | | | | | | | | | | | | | |

6 years later | | | 1,171.0 | | | | 1,457.6 | | | | 1,459.4 | | | | 1,587.1 | | | | 1,588.5 | | | | | | | | | | | | | | | | | | | | | | | | | |

7 years later | | | 1,218.3 | | | | 1,461.4 | | | | 1,533.1 | | | | 1,581.7 | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

8 years later | | | 1,217.9 | | | | 1,533.9 | | | | 1,536.7 | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

9 years later | | | 1,279.1 | | | | 1,542.0 | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

10 years later | | | 1,281.8 | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Cumulative (Deficiency) Redundancy (4) | | | (351.1) | | | | (394.2) | | | | (255.1) | | | | (100.9) | | | | 19.0 | | | | 150.3 | | | | 159.3 | | | | 171.4 | | | | 97.0 | | | | 68.3 | | | | | |

Prior Yr. Cumulative (Deficiency) Redundancy | | | (348.4) | | | | (386.1) | | | | (251.5) | | | | (106.3) | | | | (0.7) | | | | 110.7 | | | | 96.9 | | | | 92.1 | | | | (47.4) | | | | - | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Change in Cumulative (Deficiency) Redundancy | | $ | (2.7) | | | $ | (8.1) | | | $ | (3.6) | | | $ | 5.4 | | | $ | 19.7 | | | $ | 39.6 | | | $ | 62.4 | | | $ | 79.3 | | | $ | 144.4 | | | $ | 68.3 | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| (1) | Original estimated reserves for losses and LAE, prior to the effects of reinsurance, as of the balance sheet date for each of the years indicated. |

| (2) | Cumulative amounts paid, prior to the effects of reinsurance as of the end of successive years related to those reserves. |

| (3) | Re-estimated reserves are calculated by adding cumulative amounts paid subsequent to year-end to the re-estimated unpaid losses and LAE for each year. |

| (4) | Represents changes of the original estimate of the year indicated (1) and the reserves re-estimated (3) as of the current year-end. |

Excluded from the preceding tables are loss reserves of $135.7 million, which were classified as “Liabilities held for sale” as of December 31, 2007.

On September 15, 2005, Argo Group commuted the ADC which originally became effective in 2002. Reserves previously ceded under the contract of $176.2 million are added back to the Reserves Re-estimated section of the Analysis of Losses and Loss Adjustment Expense Development Net of Reinsurance table for the 2002 through 2004 years and is included in the 2005 Reserves for Losses and LAE line. As a result, the Cumulative (Deficiency) Redundancy line and the Prior Year Cumulative (Deficiency) Redundancy line include a $176.2 million deficiency related to the commutation for each of the 2002 through 2004 years. Retention of loss reserves previously ceded under the ADC did not result in additional loss expense.

Caution should be exercised in evaluating the information shown in the above tables. It should be noted that each amount includes the effects of all changes in amounts for prior periods. In addition, the tables present calendar year data, not accident or policy year development data, that some readers may be more accustomed to analyzing. The social, economic and legal conditions and other trends which have had an impact on the changes in the estimated liability in the past are not necessarily indicative of the future. Accordingly, readers are cautioned against extrapolating any conclusions about future results from the information presented in these tables.

17

Additional information relating to our loss reserve development is included under Item 7 “Management’s Discussion and Analysis of Financial Condition and Results of Operations” on Pages 42 – 72 and Note 6, “Reserves for Losses and Loss Adjustment Expenses” in the Notes to Consolidated Financial Statements.

Investments

Investment Strategy and Guidelines

We follow a conservative investment strategy designed to emphasize the preservation of our invested assets and provide adequate liquidity for the prompt payment of our obligations, including claims payments. To ensure adequate liquidity for payment of claims, we take into account the maturity and duration of our investment portfolio and our general liability profile. To meet our liquidity needs, our fixed income portfolio consists primarily of investment grade, fixed-maturity securities. As of December 31, 2010, these securities, along with cash, represented 78.5% of our total investments and cash.

In an effort to meet business needs and mitigate risks, our investment guidelines provide restrictions on our portfolio’s composition, including limits on the type of issuer, sector limits, credit quality limits, portfolio duration, limits on the amount of investments in approved countries and permissible security types. We may direct our investment managers to invest some of the investment portfolio in currencies other than the U.S. dollar based on the business we have written, the currency in which our loss reserves are denominated, or regulatory requirements.

The performance of our investment portfolio is subject to a variety of risks, including risks related to general economic conditions, market volatility, interest rate fluctuations, liquidity risk and credit and default risk. Investment guideline restrictions have been established in an effort to minimize the effect of these risks but may not always be effective due to factors beyond our control. A significant rise in interest rates could result in losses, realized or unrealized, in the value of our investment portfolio. Additionally, with respect to some of our investments, we are subject to prepayment and possibly reinvestment risk. Certain investments in our Capital Appreciation Portfolio, which includes high yield fixed income securities, equities, and other alternative investments are subject to restrictions on sale, transfer and redemption, which may limit our ability to withdraw funds or realize gains on such investments for some period of time after our initial investment. The values of, and returns on, such investments may also be more volatile.

Investment Committee and Investment Managers

The Investment Committee of our Board of Directors has approved an investment policy statement that contains investment guidelines and supervises our investment activity. The Investment Committee regularly monitors our overall investment results, compliance with investment objectives and guidelines, and ultimately reports our overall investment results to the Board of Directors.

We currently utilize ten professional investment managers to manage our portfolio. Certain short-term investments and other strategic investments are managed internally.