Investor Presentation Jay S. Bullock, CFO September 7, 2011 Exhibit 99.1 |

2. Forward-Looking Statements This presentation contains “forward-looking statements” which are made pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. The forward-looking statements are based on the Company's current expectations and beliefs concerning future developments and their potential effects on the Company. There can be no assurance that actual developments will be those anticipated by the Company. Actual results may differ materially from those projected as a result of significant risks and uncertainties, including non-receipt of the expected payments, changes in interest rates, effect of the performance of financial markets on investment income and fair values of investments, development of claims and the effect on loss reserves, accuracy in projecting loss reserves, the impact of competition and pricing environments, changes in the demand for the Company's products, the effect of general economic conditions, adverse state and federal legislation, regulations and regulatory investigations into industry practices, developments relating to existing agreements, heightened competition, changes in pricing environments, and changes in asset valuations. The Company undertakes no obligation to publicly update any forward-looking statements as a result of events or developments subsequent to the presentation. |

Argo Group – About Us International Specialty Underwriter of P&C Insurance and Reinsurance Risks • Business platform is comprised of four distinct businesses; Each fully accountable • Core U.S. businesses are profitable • International platform supports corporate objectives of growth, profitability and diversification. First and Foremost an Underwriting Company • Underwriting results ex. CATS in the 1H of 2011 were good in spite of competition • Five-year (2006-10) average combined ratio was 98.7% vs. 99.4% (industry) Solid Financial Strength (Balance Sheet) • Rated ‘A’ (Excellent) by A.M. Best (Class Size XII) 1 • Conservatively capitalized/modest use of financial leverage 1 Argo P/C Insurance & reinsurance operations 3. |

Our Strategy • Become a recognized worldwide leader of custom insurance and reinsurance solutions for our clients • Create a competitive advantage through superior customer service, product innovation and underwriting knowledge • Achieve profitable growth organically and/or through opportunistic acquisitions throughout the cycle • Manage capital and risk appropriately / maintain strong ratings • Hire top tier talent to support our strategy 4. Maximize shareholder value through growth in book value per share |

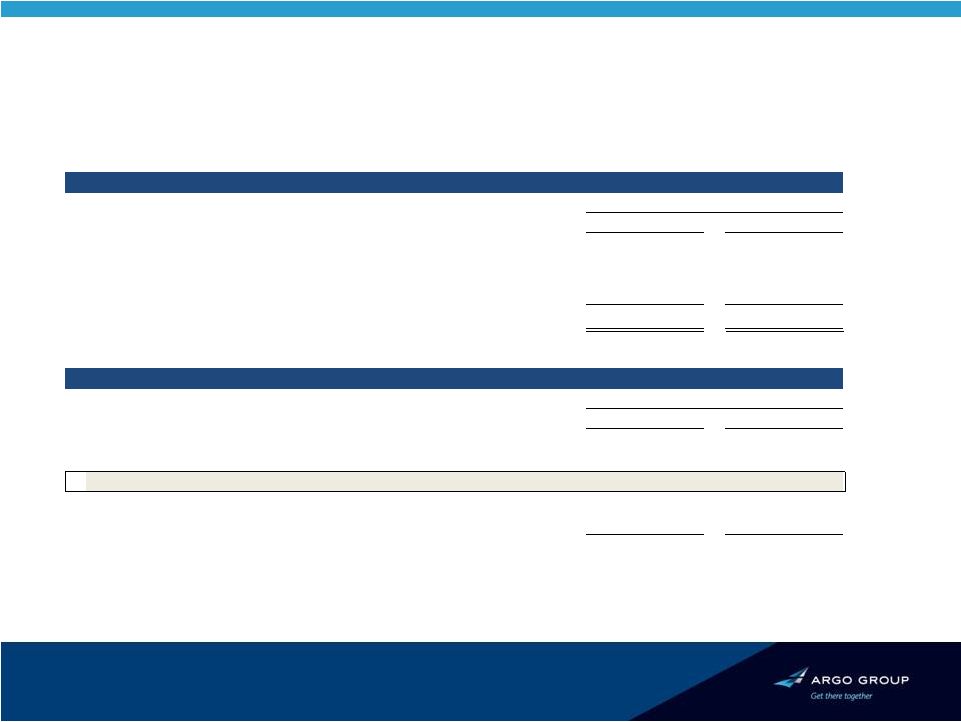

BVPS Growth Since 2002 *2011-Q2 impacted primarily by tornado activity in Missouri and Alabama totaling $31.9M (net of reinstatement premiums). **Book value per common share - outstanding, includes the impact of the Series A Mandatory Convertible Preferred Stock on an as if converted basis. Preferred stock had fully converted into common shares as of Dec. 31, 2007. Our Track Record: Maximizing Shareholder Value 5. 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011-Q2 $23,40 $27.22 $30.36 $33.52 $39.08 $45.15 $44.18 $52.36 $58.41 $56.65* |

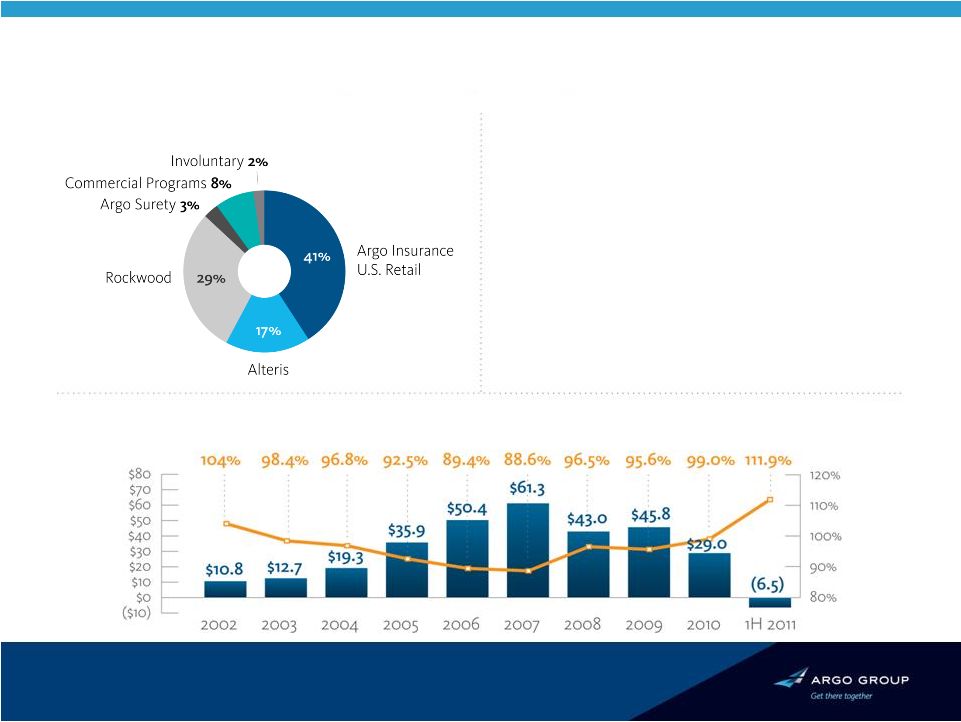

Commercial Specialty Segment Pre-Tax Operating Income (Data in Millions) and Combined Ratio 6. About Us • Designs customized commercial insurance programs for grocers, fabricare, restaurants and other specialty retail clients • 2 largest provider of commercial insurance to small and midsize U.S. public entities • 2 largest provider of commercial insurance to the coal mine industry • Distributes products direct, through wholesalers and independent agents NWP by Business Unit nd nd |

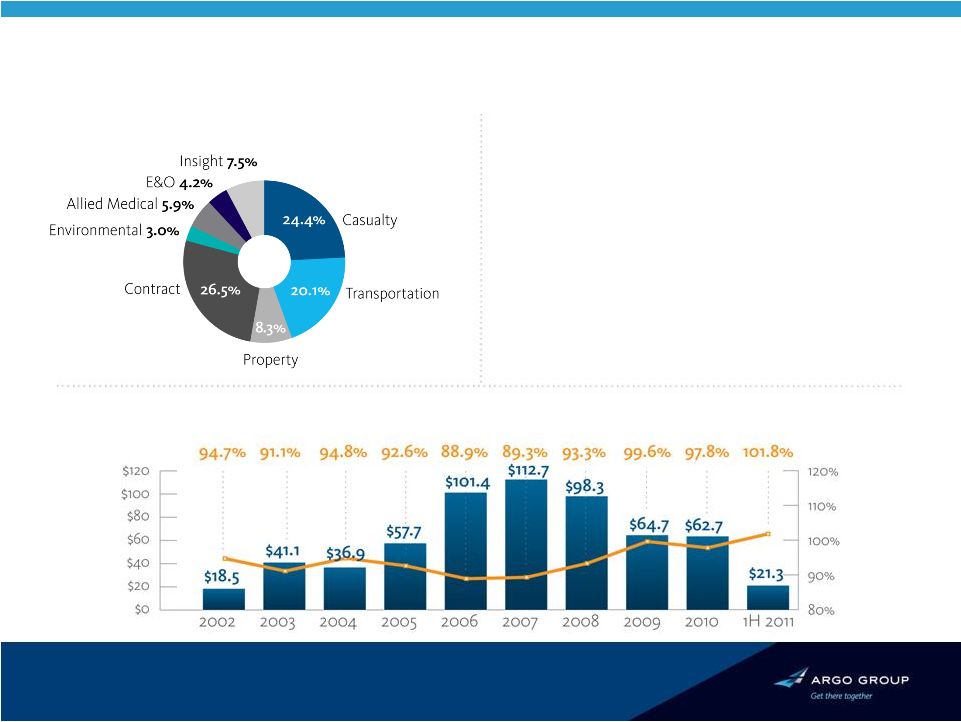

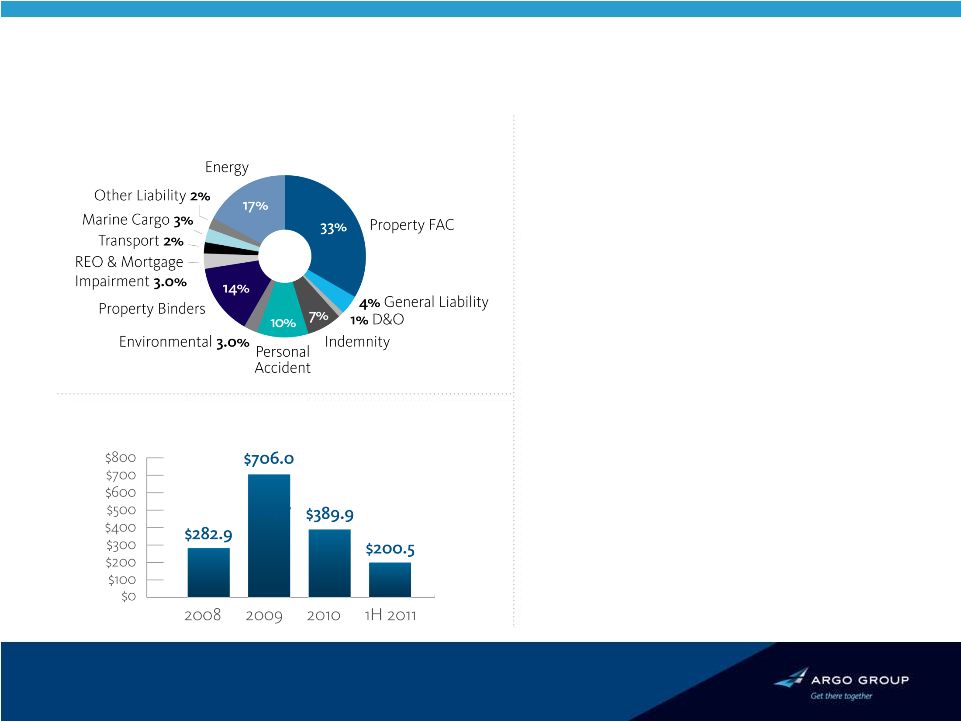

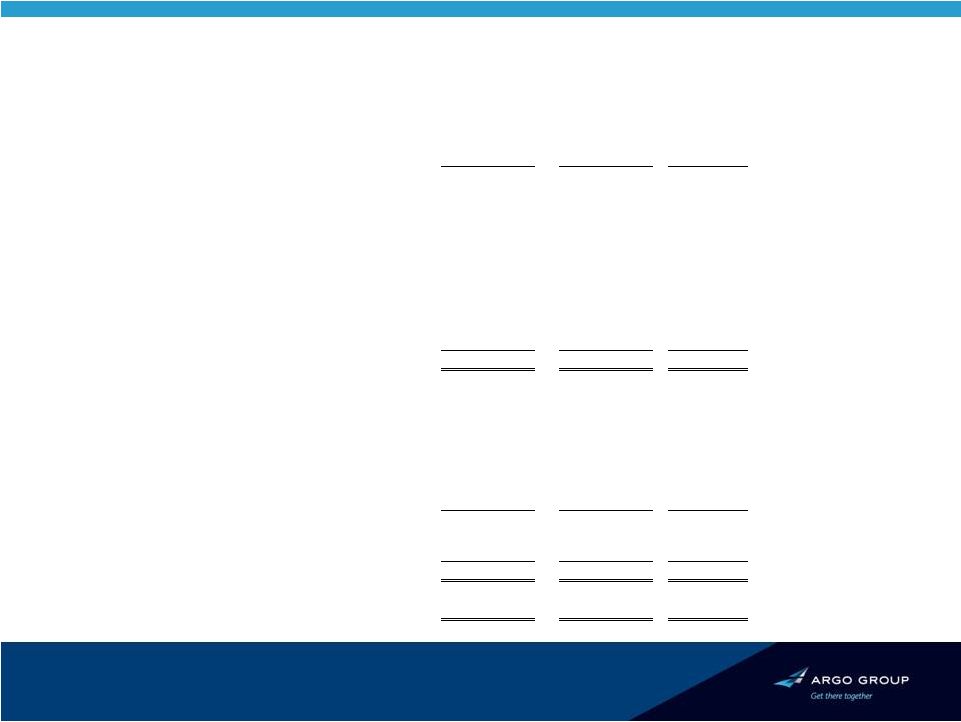

Q2 NWP By Business Unit About Us Excess & Surplus Lines Segment 7. Pre-Tax Operating Income (Data in Millions) and Combined Ratio • Ranked among the top 10 E&S carriers in the U.S. based on 2010 DWP • Strong relationships with national, local and regional wholesale brokers • Target market is non-standard (hard-to-place) risks • U/W expertise is a competitive advantage |

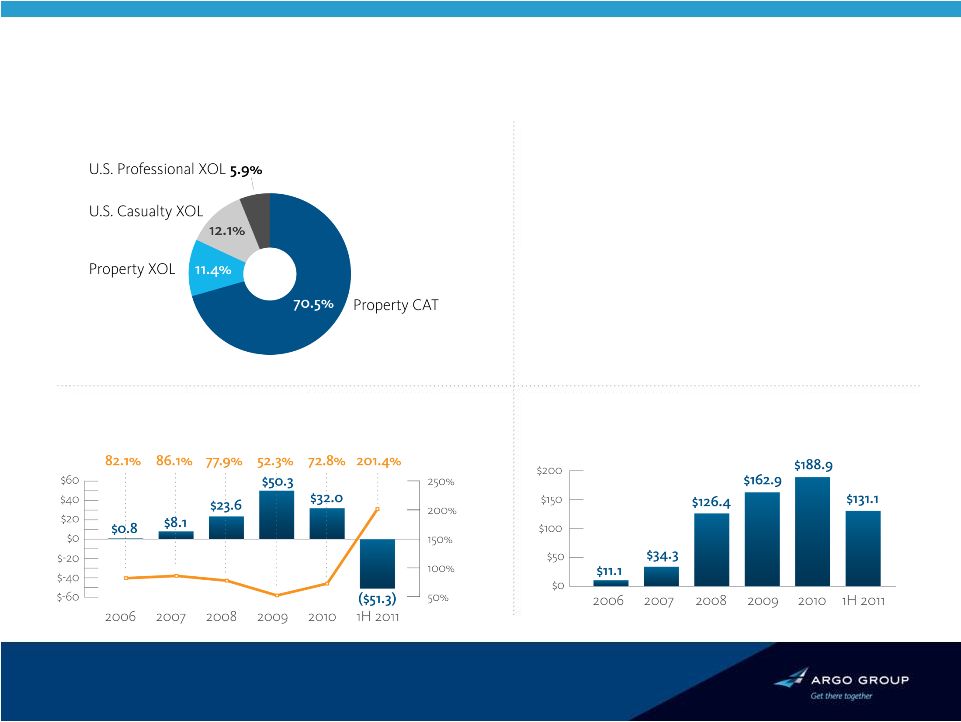

Syndicate 1200 About Us 8. Gross Written Premiums (Millions) Q2 NWP by Line of Business Primary Classes of Business • Property (D&F) • Professional Lines • Aviation • Energy & Marine Mix of Business: • Worldwide property (67% of GPW) • Non-U.S. liability (33% of GPW) Lloyd’s Rated: • ‘A’ (Excellent) by A.M. Best • ‘A+’ (Strong) by S&P |

International Specialty About Us Gross Written Premium 9. Q2 NWP by Line of Business Operating Income (Data in Millions) and Combined Ratio • Underwrites excess casualty & professional lines insurance, property CAT, property per risk and proportional property treaty reinsurance worldwide • Established regional office in Dubai • Establishing operations in Brazil • History of strong U/W profits • Distributes through brokers |

Argo Group Q2 2011 Financial Highlights CONSOLIDATED GAAP VIEW Net written premium decreased 14.5% in the quarter. • Marketplace still undisciplined • Will continue to exit or walk away from unattractively priced risks The combined ratio before CATS and PY reserve development 97.2% vs. 100.9% in Q2 2010. • Underlying results remain strong despite the competitive market • Pre-tax losses from Q2 CATS were $31.9 million (net of estimated reinstatement premiums), compared to pre-tax losses in Q2 2010 of $15.1 million (net of estimated reinstatement premiums) • Previous actions to de-risk the portfolio not yet reflected in results 10. Book value per share (BVPS) was $56.65 at June 30, 2011, an increase from 54.76 at June 30, 2010. $ |

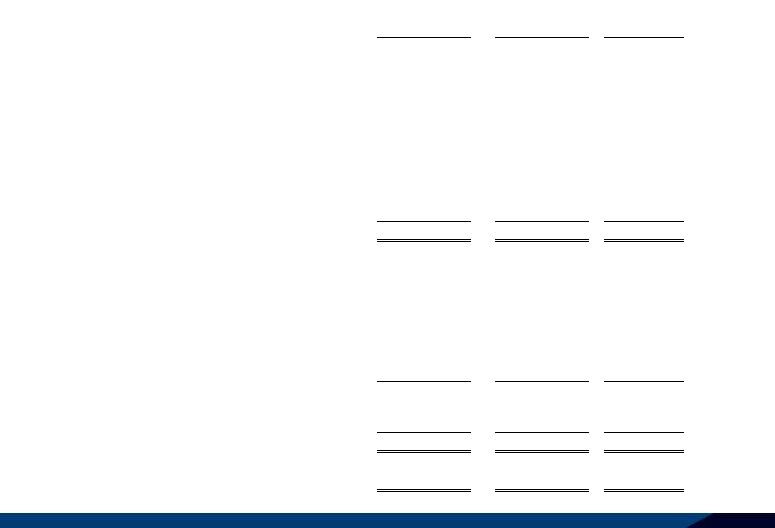

Q2’2011 Financial Highlights CONSOLIDATED GAAP VIEW 11. ($ in millions) Operating Income For the Quarter Ended 6/30/2011 6/30/2010 Pre-tax operating income (before CATs & PY development) 1 35.2 24.4 CATs, net of estimated reinstatement premium (31.9) (15.1) Prior year reserve (increase) / decrease 1.1 9.3 Pre-tax operating income 4.4 18.6 Combined Ratio For the Quarter Ended 6/30/2011 6/30/2010 Loss Ratio (before CATs & PY development) 59.1% 64.6% Expense Ratio 38.1% 36.3% Combined Ratio (before CATs & PY development) 97.2% 100.9% CATs, net of estimated reinstatement premium 11.7% 4.8% Prior year reserve increase / (decrease) -0.3% -3.0% Total Combined Ratio 108.6% 102.7% 1 Also excludes realized capital gains / (losses) and foreign exchange gains / (losses). Note: All CATS and all associated calculations in the table are adjusted for reinstatement premium. |

H1’2011 Financial Highlights CONSOLIDATED GAAP VIEW 12. ($ in millions) Operating Income For the Six Months Ended 6/30/2011 6/30/2010 Pre-tax operating income (before CATs & PY development) 1 $62.6 $54.4 CATs, net of estimated reinstatement premium (144.9) (43.9) Prior year reserve (increase) / decrease (3.6) 20.3 Pre-tax operating income ($85.9) $30.8 Combined Ratio For the Six Months Ended 6/30/2011 6/30/2010 Loss Ratio (before CATs & PY development) 59.4% 62.3% Expense Ratio 39.3% 37.9% Combined Ratio (before CATs & PY development) 98.7% 100.2% CATs, net of estimated reinstatement premium 27.1% 6.9% Prior year reserve increase / (decrease) 0.8% -3.3% Total Combined Ratio 126.6% 103.8% 1 Also excludes realized capital gains / (losses) and foreign exchange gains / (losses). Note: All CATS and all associated calculations in the table are adjusted for reinstatement premium. |

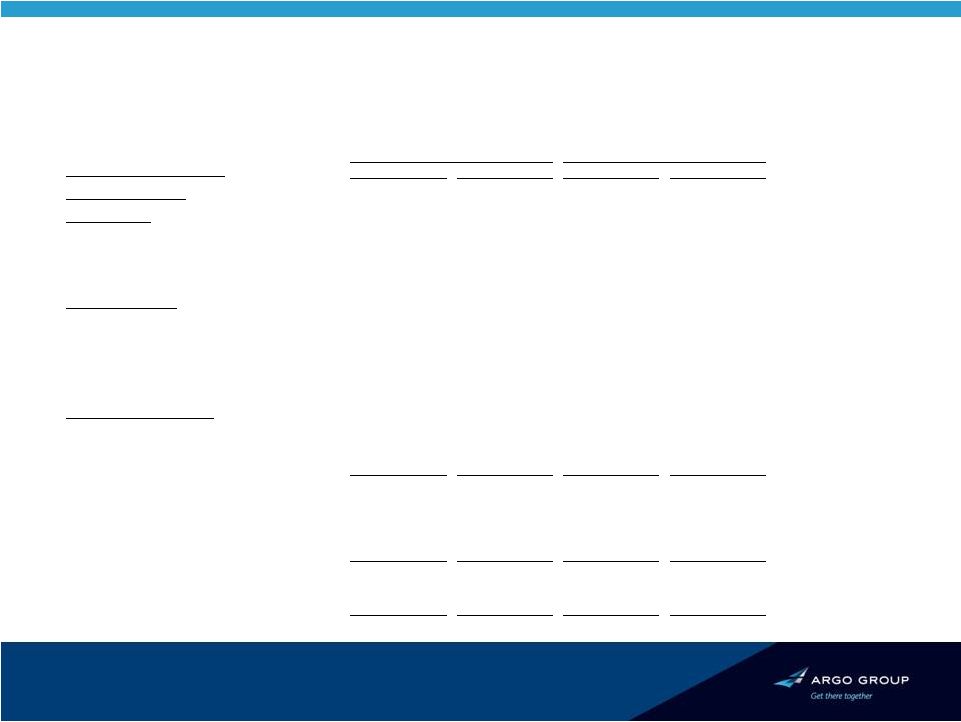

Balance Sheet CONSOLIDATED GAAP VIEW 13. ($ in millions) June 30, December 31, % 2011 2010 Variance (unaudited) Total investments 4,298.9 $ 4,215.4 $ 2.0% Cash and cash equivalents 49.0 83.5 (41.3%) Accrued investment income 32.7 33.5 (2.4%) Receivables 1,433.6 1,505.7 (4.8%) Goodwill and intangible assets 247.1 249.1 (0.8%) Deferred acquisition costs 135.4 139.7 (3.1%) Ceded unearned premiums 195.9 164.0 19.5% Other assets 121.1 97.6 24.1% 6,513.7 $ 6,488.5 $ 0.4% Reserves for losses and loss adjustment expenses 3,356.1 $ 3,152.2 $ 6.5% Unearned premiums 664.7 654.1 1.6% Ceded reinsurance payable 397.3 524.3 (24.2%) Debt 68.2 65.0 4.9% Junior subordinated debentures 311.5 311.5 0.0% Other liabilities 167.3 155.3 7.7% 4,965.1 4,862.4 2.1% Total shareholders' equity 1,548.6 1,626.1 (4.8%) 6,513.7 $ 6,488.5 $ 0.4% Book value per common share 56.65 $ 58.41 $ (3.0%) Assets Total assets Liabilities and Shareholders' Equity Total liabilities Total liabilities and shareholders' equity |

Investment Portfolio CONSOLIDATED GAAP VIEW 14. ($ millions) Jun. 30, 2011 Mar. 31, 2011 Total cash and investments Fair Value % of Total Fair Value % of Total USD DENOMINATED: Fixed maturities U.S. Governments $440.7 10.1% $413.2 9.6% Non-U.S. Governments 35.9 0.8% 3.9 0.1% Obligations of states and political subdivisions 617.4 14.2% 614.7 14.3% Corporate securities 1,031.8 23.7% 1,007.6 23.5% Structured securities CMO/MBS-agency 562.4 12.9% 614.0 14.3% CMO/MBS-non agency 34.7 0.8% 37.0 0.9% CMBS 184.1 4.2% 195.6 4.6% ABS-residential 15.5 0.4% 16.5 0.4% ABS-non residential 81.7 1.9% 99.1 2.3% FOREIGN DENOMINATED: Governments 208.0 4.8% 200.1 4.7% Credit 100.7 2.3% 90.3 2.1% Total Fixed maturities $3,312.9 76.2% $3,292.0 76.7% Equity securities $375.9 8.6% $336.5 7.8% Other investments 226.1 5.2% 164.3 3.8% Short-term investments 384.0 8.8% 391.3 9.1% Total investments $4,298.9 98.9% $4,184.1 97.5% Cash and cash equivalents 49.0 1.1% 105.4 2.5% Total cash and investments $4,347.9 100.0% $4,289.5 100.0% |

Argo Group - Recap of Major Highlights Argo is an established carrier in the international specialty insurance and reinsurance markets. • Core U.S. operations continue to perform well • International platform supports diversification & future growth strategy • Underwriting focus & talent are key competitive advantages • Businesses well-positioned to take advantage of a hardening market Management committed to maximizing shareholder value • Achieved book value per share CAGR of 11% since 2002 • Quality of capital and balance sheet is excellent • Will continue to repatriate capital as appropriate 15. |

|