1Q 2013 Investor Presentation June 2013 Exhibit 99.1 |

Forward-Looking Statements This presentation contains “forward-looking statements” which are made pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. The forward-looking statements are based on the Company's current expectations and beliefs concerning future developments and their potential effects on the Company. There can be no assurance that actual developments will be those anticipated by the Company. Actual results may differ materially from those projected as a result of significant risks and uncertainties, including non-receipt of the expected payments, changes in interest rates, effect of the performance of financial markets on investment income and fair values of investments, development of claims and the effect on loss reserves, accuracy in projecting loss reserves, the impact of competition and pricing environments, changes in the demand for the Company's products, the effect of general economic conditions, adverse state and federal legislation, regulations and regulatory investigations into industry practices, developments relating to existing agreements, heightened competition, changes in pricing environments, and changes in asset valuations. The Company undertakes no obligation to publicly update any forward-looking statements as a result of events or developments subsequent to the presentation. 2. |

3. Argo Group at a Glance Exchange / Ticker: NASDAQ / “AGII” Share Price: $40.26 Market Capitalization: $1.1 billion Annual Dividend / Yield: $0.60 per share / 1.5% Gross Written Premium: $1.8 billion Capital: $1.9 billion Analyst Coverage: Macquarie (Outperform) - Amit Kumar Raymond James (Outperform) - Greg Peters William Blair (Outperform) - Adam Klauber Dowling & Partners (Neutral) - Kyle LaBarre Compass Point (Neutral) - Ken Billingsley Atlanta Barcelona Bermuda Boston Brussels Chicago Dallas Denver Dubai Houston London Los Angeles Malta New York Paris Portland Richmond Rio de Janeiro Rockwood San Antonio San Francisco Sao Paulo Scottsdale Seattle Zurich Note: Market information as of June 07, 2013 and annual performance figures as of TTM March 31, 2013. |

4. Strong & Focused Specialty Franchise Global underwriter of specialty P&C insurance and reinsurance through four segments Broad footprint strategically located in major insurance centers U.S., Bermuda, London and Brazil Focused on specialty insurance & casualty lines Leader in U.S. Excess & Surplus Lines Top quartile Lloyd’s Syndicate by stamp Deep relationships with retailers, wholesalers and Lloyd’s brokers A.M. Best rating of “A” (excellent financial strength) Proven track record of active capital management 1Q 2013 TTM GWP |

Strategy Aligned Toward Shareholder Value Sustain competitive advantage through superior customer service, product innovation and underwriting knowledge Opportunistically grow organically and/or through strategic acquisitions throughout the underwriting cycle Manage capital and risk appropriately / maintain strong ratings Proven ability to attract talent 5. |

6. Evolution of Growth and Diversification 6. *Excludes GWP recorded in runoff and corporate & other. |

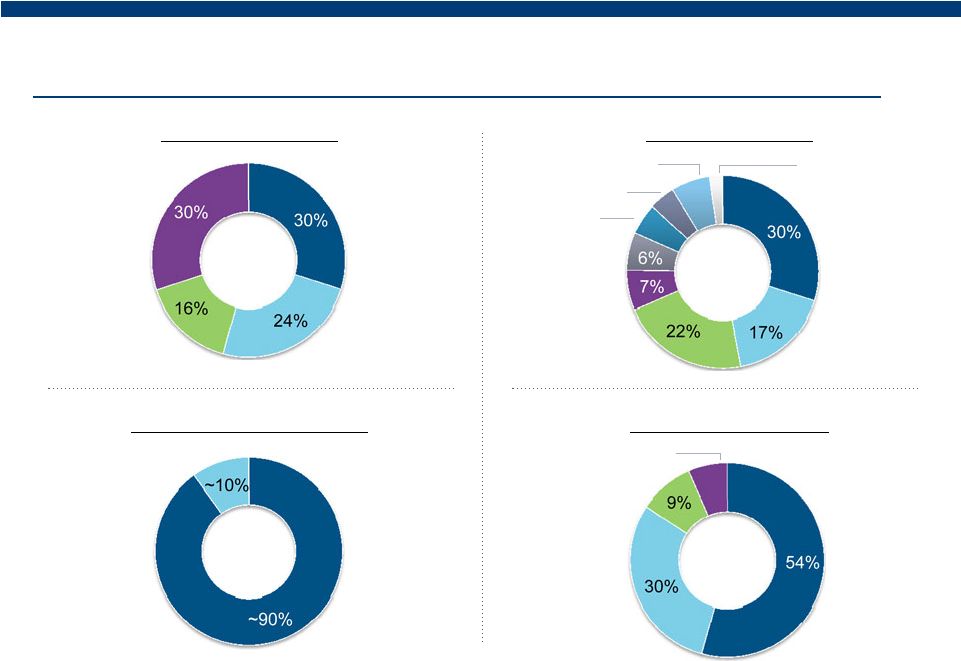

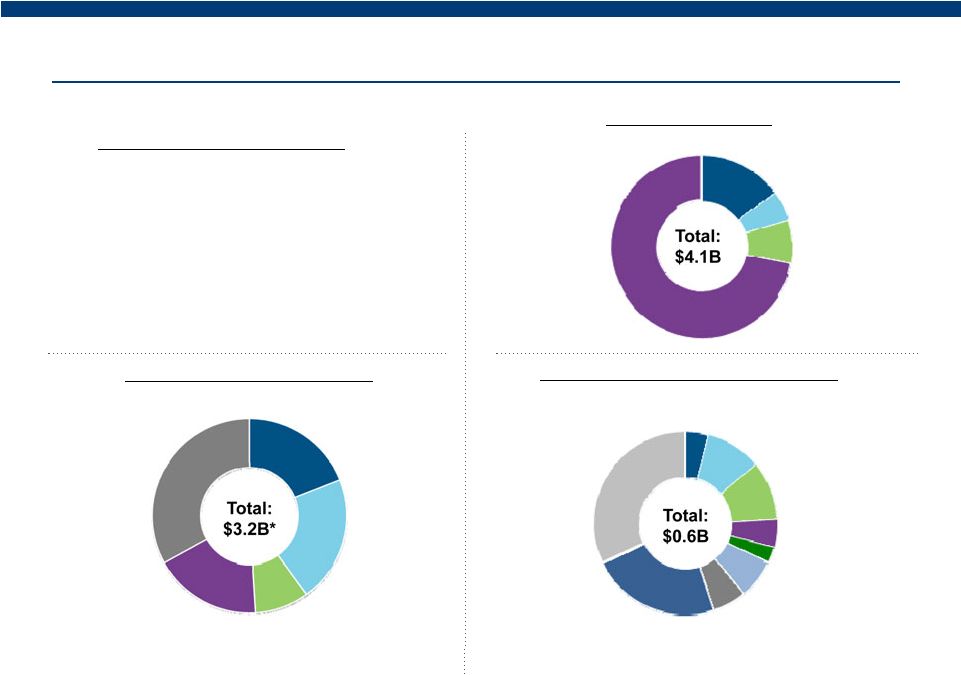

7. Argo Group Business Mix ($1.8B in GWP) 7. GWP by Segment Excess & Surplus Lines Commercial Specialty Syndicate 1200 International Specialty GWP by Product GWP by Business Type Primary Insurance Reinsurance GWP by Geography United States London Bermuda *Data is based on TTM as of March 31, 2013. Excludes GWP recorded in runoff and corporate & other. Excess & Surplus Lines Other Commercial Specialty Property Public Entity 7% Marine & Aerospace Surety 2% Alteris 5% Mining 4% Emerging Mkts 7% Emerging Markets 7% |

8. Multi-Channel Distribution Strategy |

Maximizing Shareholder Value – BVPS Growth * Book value per common share – outstanding. Adjusted for June 2013 stock dividend. Also includes the impact of the Series A Mandatory Convertible Preferred Stock as if on a converted basis. Preferred stock had fully converted into common shares as of Dec. 31, 2007. 1 Price / book calculated at 52-week high and most recent book value per share. Stock price and book value adjusted for PXRE merger for 2006 and prior years. Note the book value amounts for 2011 and 2010 reflect the effect of the Company’s adoption of new guidance related to accounting for costs associated with acquiring or renewing insurance contracts. 2009 and prior periods have not been restated. 9. |

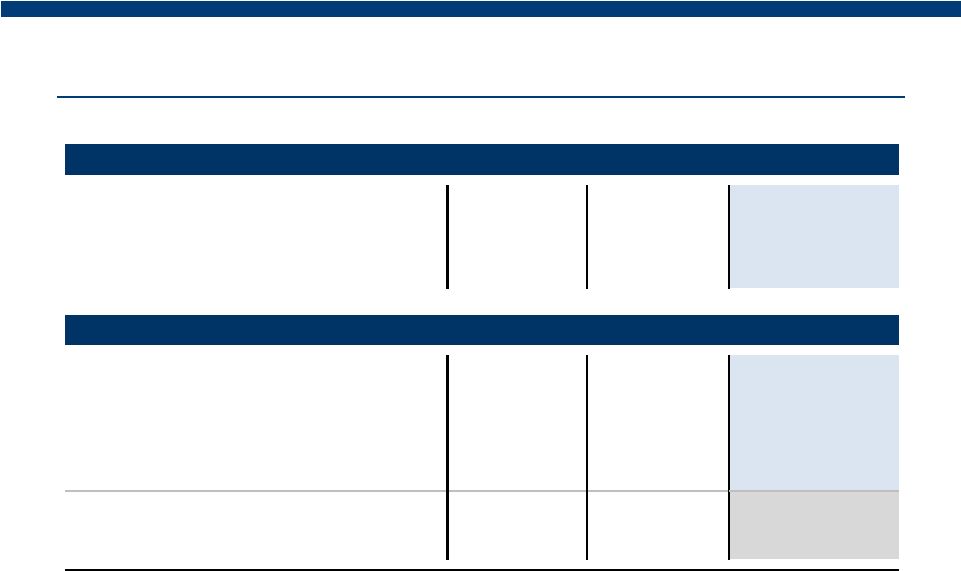

10. Substantial Growth and Financial Strength Scale 2000 2006 TTM 1Q'13 '00-1Q'13 Factor Gross Written Premiums $186.1 $1,155.6 $1,787.6 9.6x Net Written Premiums 163.9 847.0 1,282.3 7.8x Net Earned Premiums 124.6 813.0 1,213.4 9.7x Financial Strength 2000 2006 TTM 1Q'13 '00-1Q'13 Factor Total Assets $1,565.8 $3,721.5 $6,602.5 4.2x Total Investments 1,085.6 2,514.1 4,133.2 3.8x Shareholder's Equity 501.1 847.7 1,546.6 3.1x Total Capital 501.1 992.0 1,948.1 3.9x Debt / Total Capital 0.0% 14.5% 20.6% A.M. Best Rating A A A |

11. Consolidated GWP up 10.6% in 1Q 2013 vs. 1Q 2012 1Q YoY Premium Growth in 3 out of 4 Segments Reflects impact of strategic initiatives taken, rate increases and improved retention 11. |

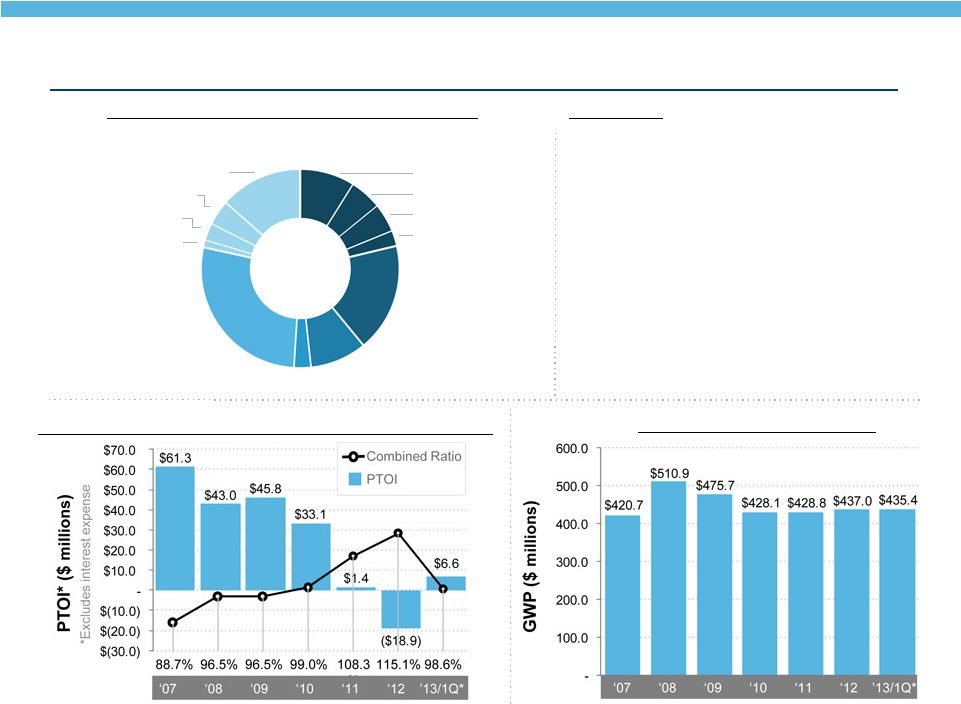

12. About Us • Leader in U.S. Excess & Surplus Lines • Strong relationships with national, local and regional wholesale brokers • Seasoned U/W expertise is a competitive advantage • Target all sizes of non-standard (hard-to-place) risks, with focus on small/medium accounts • Underwrites on both admitted & non-admitted basis and across all business enterprises via two brands: • Colony Specialty • Argo Pro GWP by Business Unit (TTM 3/31/13) Casualty 32% Transportation 16% Environmental 4% Allied Medical 5% Management Liability 3% Property 10% Contract 23% Errors & Omissions 7% Excess & Surplus Lines Segment (30% of TTM GWP) 12. Gross Written Premium Pre-Tax Operating Income & Combined Ratio *Data is based on TTM as of March 31, 2013. *Data is based on YTD as of March 31, 2013. |

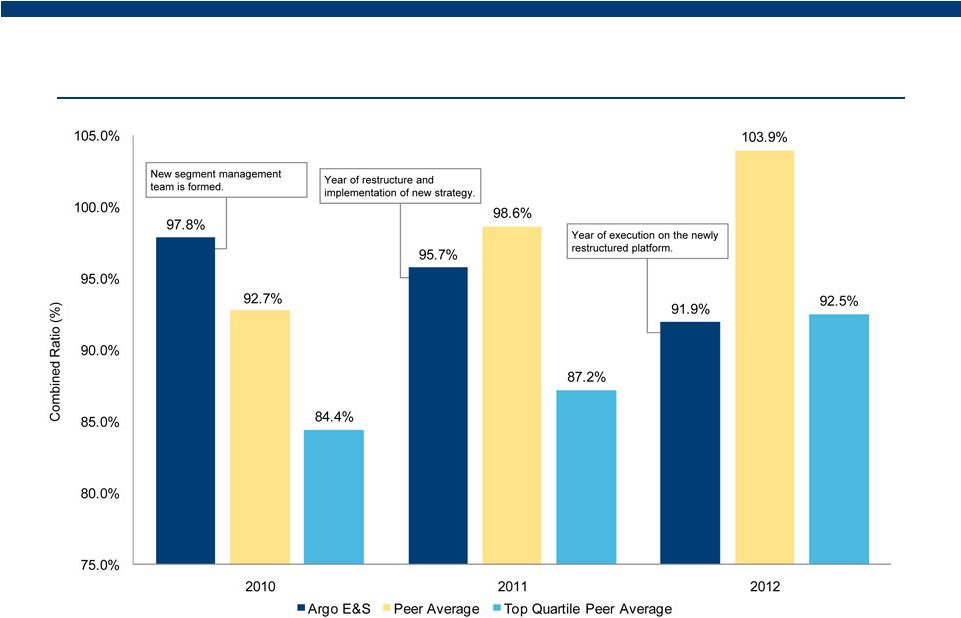

13. Outperformed E&S Peers in 2012 Peers include: WR Berkley Specialty Segment, Alterra US Segment, American Safety E&S Segment, Aspen Insurance Segment, Axis Insurance Segment, Endurance Insurance Segment, HCC US P&C Segment, Markel E&S Segment, Navigators Insurance Segment, RLI P&C Segments, Arch Insurance Segment, United National Insurance Segment. Top quartile peers include the above mentioned segments from WR Berkley, RLI, and HCC. |

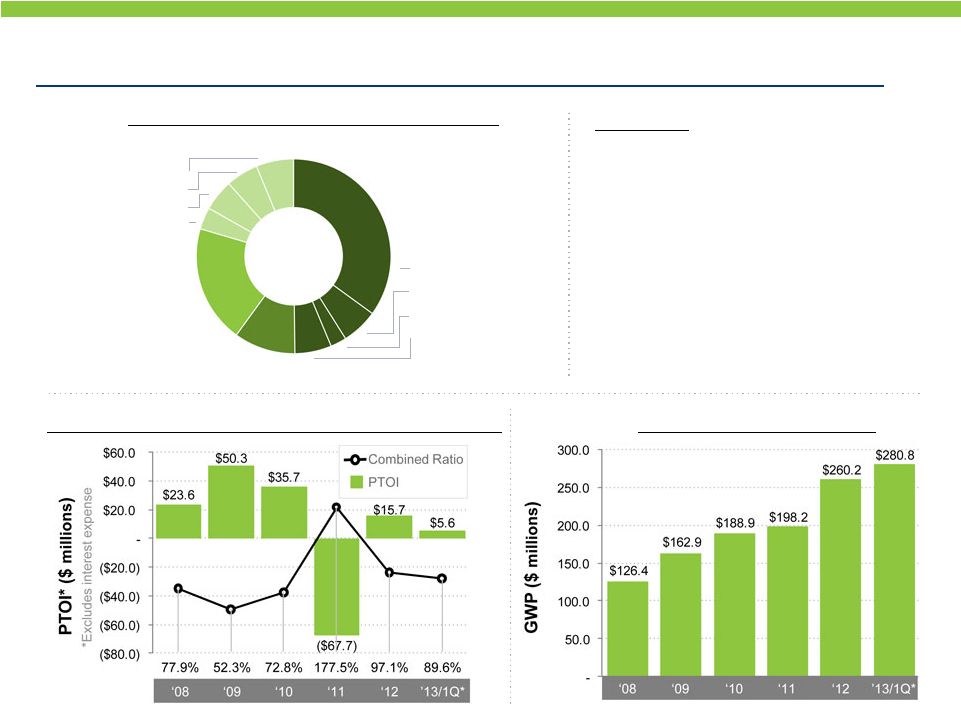

14. Commercial Specialty (24% of GWP) About Us • Business primarily placed through retail distribution partners • Argo Insurance – Designs customized commercial insurance programs for grocers, dry cleaners, restaurants and other specialty retail clients • Trident – 2 largest provider of insurance to small and midsize U.S. public entities • Rockwood – 2 largest provider of commercial insurance to coal mining industry • Alteris – fee based business where Argo or others accept the risk Gross Written Premium Pre-Tax Operating Income & Combined Ratio *Data is based on TTM as of March 31, 2013. *Data is based on YTD as of March 31, 2013. GWP by Business Unit (TTM 3/31/13) U.S. Retail (Argo Insurance) 21% Restaurants 5% Grocery 9% Dry Cleaners 5% Other Industries 2% Public Entity (Trident) 28% Surety 9% Mining (Rockwood) 18% Other 3% Alteris Managed Premium 22% Other 1% Transportation 3% State Workers’ Comp Funds 14% Self Insured Public Entity 4% nd nd |

15. General Liability 14% Prof. Indemnity 13% Directors & Officers 2% Int’l Casualty Treaty 2% Other 2% Syndicate 1200 (30% of GWP) About Us • Well-established multi-class platform at Lloyd’s of London • Ranks among the largest Syndicates at Lloyd’s by Stamp Capacity • Lloyd’s market ratings: • ‘A’ (Excellent) by A.M. Best • ‘A+’ (Strong) by S&P GWP by Business Unit (TTM 3/31/13) Property 46% Liability 33% Specialty 16% Aerospace 5% Property Fac 18% N. Am. & Int’l Binders 10% Personal Accident 10% Int’l Property Treaty 2% Other 6% 15. Gross Written Premium Pre-Tax Operating Income & Combined Ratio ‘12 ‘10 ‘09 ‘08 ‘11 ’13/1Q* *Data is based on TTM as of March 31, 2013. *Data is based on YTD as of March 31, 2013. Cargo 2% Offshore Energy 7% Onshore Energy 4% Yachts & Hulls 2% |

16. International Specialty (16% of GWP) About Us • Bermuda team underwrites • Property cat, short tail per risk and proportional treaty reinsurance worldwide • Excess casualty and professional liability for Fortune 1000 accounts • Building diversity through international expansion: • Established primary operations in Brazil • Established operations in Euro zone • Established regional office in Dubai • Distributes through brokers 16. Gross Written Premium Pre-Tax Operating Income & Combined Ratio GWP by Business Unit (TTM 3/31/13) Excess Casualty 20% Professional Liability 10% Brazil 20% Marine Cargo 6% Property & Engineering 5% Motor 5% Financial Lines 4% *Data is based on TTM as of March 31, 2013. *Data is based on YTD as of March 31, 2013. Reinsurance 50% Other Assumed Re 6% Property Risk XS 3% Property Pro Rata 6% Property CAT 35% |

17. 1Q Operating Results 17. 1Q 2013 1Q 2012 Gross Written Premiums $438.2 $396.3 Net Written Premiums 279.0 241.2 Earned Premiums 304.2 277.3 Losses and LAE 170.5 165.8 Other Reinsurance-Related Expenses 5.1 6.9 Underwriting, Acquisition and Insurance Expenses 126.7 113.7 Underwriting Income / (Loss) $1.9 ($9.1) Net Investment Income 27.9 31.4 Fee Income, net 0.0 1.3 Interest Expense 4.9 5.7 Operating Income / (Loss) $24.9 $17.9 Foreign Currency Exchange Gain / (Loss) 3.1 (2.9) Net Realized Investment Gains 9.5 13.1 Pre-Tax Income / (Loss) $37.5 $28.1 Income Tax Provision 4.8 8.5 Net Income / (Loss) $32.7 $19.6 Operating Income (Loss) per Common Share (Diluted) 1 $0.78 $0.54 Net Income (Loss) per Common Share (Diluted) $1.28 $0.74 Loss Ratio² 57.0% 61.3% Expense Ratio³ 42.4% 42.1% Combined Ratio 99.4% 103.4% All data in millions except for per share data and ratio calculations. (1) At an assumed tax rate of 20%. (2) Defined as Losses & LAE / (Earned Premiums less Other Reinsurance-Related Expenses). (3) Defined as Underwriting, Acquisition and Insurance Expenses / (Earned Premiums less Other Reinsurance-Related Expenses). |

18. 17% 18. As of March 31, 2013 • Duration of 3.3 years • Average rating of ‘AA-’ • Book yield of 3.4% • Very liquid • Conservatively managed Portfolio Characteristics Equity Investments by Sector 10% Healthcare Energy 23% 4% Industrials 14% Funds 5% Financials 11% Info Tech 3% Materials 6% Consumer Discretionary Consumer Staples 24% Asset Allocation 8% Other Fixed 72% Maturities. 6% Short Term 14% Equities Fixed Maturities by Type 7% Short Term Corporate 35%. 19% Gov. 18% Structured State/Muni 21%. *$2.97b in fixed maturities, $0.23b in short term Conservative Investment Strategy |

19. Active Capital Management Through share repurchases and dividends, we have returned >$250 million of capital and repurchased 22% of shares outstanding from 2009 through Q1 2013 Note: Not adjusted for June 2013 stock dividend 2009 2010 2011 2012 Q1 13 2009-Q1 13 Total Shares O/S 30,982,839 31,206,796 31,285,469 31,384,271 31,463,460 Less: Treasury Shares 145,999 3,363,560 4,971,305 6,459,613 6,785,438 Net Shares 30,836,840 27,843,236 26,314,164 24,924,658 24,678,022 Shares Repurchased 145,999 3,217,561 1,607,745 1,488,308 325,825 6,785,438 As % of Beg. Net Shares 0% 10% 6% 6% 1% 22% Avg. Repurchase Price/sh $35.23 $33.08 $30.72 $29.92 $37.71 Total Repurchased ($mm) $5.1 $106.4 $49.4 $44.5 $12.3 $217.8 Dividends/sh $0.48 $0.48 $0.48 $0.15 Dividend Payments ($mm) $14.3 $13.1 $12.3 $3.7 $43.4 Repurchases + Dividends ($mm) $5.1 $120.7 $62.5 $56.8 $16.0 $261.1 |

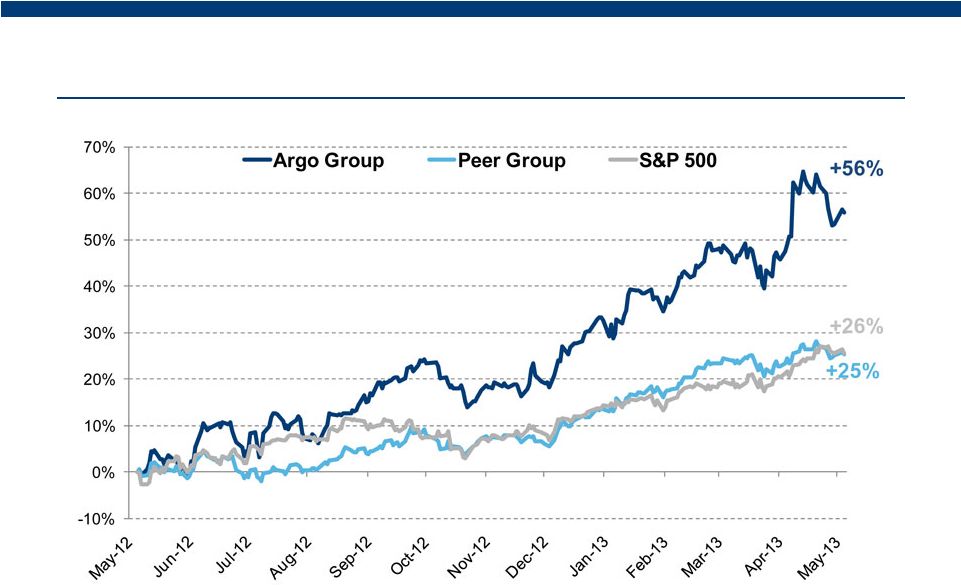

20. Stock Price Performance – Last 12 Months Source: Thomson Peer Group consists of: Allied World, American Financial, AmTrust, Arch Capital, Aspen, AXIS Capital, Endurance, Global Indemnity, HCC, Markel, Navigators, OneBeacon, RLI Corp, Selective Group, Tower Group, W.R. Berkley |

21. Price/Book Jan-00 May-13 Argo 0.70x 0.69x Peer Avg. 1.17x 1.15x Difference 0.47x 0.46x - 0.2x 0.4x 0.6x 0.8x 1.0x 1.2x 1.4x 1.6x 1.8x 2.0x Jan-00 Jan-01 Jan-02 Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Argo Peer Group Compelling Valuation vs. Peer Group Source: Thomson, SNL, internal analysis. Note: Price to book is average price/book across all peer companies. Peers include: Allied World , American Financial, AmTrust, Arch, Aspen, AXIS, Endurance, Global Indemnity, HCC, Markel, Navigators, OneBeacon, RLI, Selective, Tower, W.R. Berkeley. 0.69x 1.15x 0.46x Difference |

22. Well Positioned for Value Creation in 2013 and Beyond • Compelling investment case • Stock trading at a discount to book value and below peers • Upside potential as past and ongoing efforts continue We believe that Argo Group has potential to generate substantial value for new and existing investors. • Significant changes to premium composition completed • Results of re-underwriting and efficiency efforts are emerging in financials • Modest pricing increases expected to favorably impact growth and loss ratios • Continue to employ and attract some of the best talent in the industry • Brazil has traction and is beginning to scale • Building more revenue from non-risk bearing MGA strategy • Incremental yield improvements can have a favorable impact on ROE • Moderate financial leverage • Strong balance sheet with adequate reserves and excellent asset quality |