January 24, 2022

VIA EDGAR

Division of Corporation Finance

Office of Finance

U.S. Securities and Exchange Commission

100 F Street, N.E.

Washington, D.C. 20549

| Re: | Argo Group International Holdings, Ltd. |

Form 10-K for Fiscal Year Ended December 31, 2020

Filed March 15, 2021

File No. 001-15259

Dear Division of Corporation Finance:

Please find below the responses of Argo Group International Holdings, Ltd. (the “Company”) to comments of the staff (the “Staff”) of the U.S. Securities and Exchange Commission (the “Commission”) contained in your comment letter dated December 17, 2021. For your convenience in reviewing our response, we have repeated each comment and presented our response thereto.

Comment

Form 10-K filed March 15, 2021

Note 2. Revisions of Previously Issued Financial Statements, page F-17.

| 1. | We note your disclosure that you identified certain immaterial errors in your historical financial statements primarily related to the accounting for (1) foreign currency exchange gains and losses associated with a specific reinsurance contract and (2) errors in the Company’s tax provision primarily related to the Company’s allocation of certain corporate-level expenses to your subsidiary companies, as well as other previously identified immaterial errors. We further note your disclosure that you concluded that although these errors were not material to the previously issued financial statements, however, correcting the cumulative effect of the errors in 2020 would materially misstate the 2020 consolidated financial statements, and therefore you have revised your historical financial statements to correct for these immaterial errors. In light of the nature of the errors and their quantitative significance to the adjusted financial statements presented, including, for instance income tax provision, net income (loss) and earnings per share for certain of the revised periods, please provide us with your analysis considering the guidance in Staff Accounting Bulletin No. 99. In your response please discuss how you evaluated the total mix of information, taking into account both quantitative and qualitative factors considered, when determining materiality of the error to investors and other users. |

Office of Finance

January 24, 2022

Page 2

Response

During the preparation of the Company’s 2020 Consolidated Financial Statements (“2020 Financial Statements”), the Company identified errors in the following areas: intercompany transactions, such as foreign currency exchange gains and losses associated with a specific reinsurance contract, the allocation of certain corporate-level expenses to its subsidiaries, the accounting for federal and state income taxes including the tax implications of certain intercompany transactions, the completeness and accuracy of information used in recording deferred tax balances, and the timeliness of analyses of income tax accounting. As disclosed in Note 2 to the Company’s Consolidated Financial Statements included in the Annual Report on 2020 Form 10-K (“2020 Form 10-K”), the Company analyzed the materiality of the errors, both individually and in the aggregate, that were identified when preparing its 2020 Form 10-K in accordance with the guidance provided in Staff Accounting Bulletin No. 99 Topic 1M (“SAB No. 99”) and Staff Accounting Bulletin No. 108 Topic 1N (“SAB No. 108”). Based on this analysis, the Company concluded that correcting the cumulative effect of these errors in the Company’s 2020 Financial Statements would materially misstate the 2020 financial statements, but the errors were not material to the Company’s previously issued financial statements for the periods ending December 31, 2018 and 2019, respectively (referred to herein as the “2018 Financial Statements” and “2019 Financial Statements,” respectively) or the related quarterly financial statements included in Forms 10-Q filed during those periods.

Specifically, the Company concluded that the impact of the errors on Pre-Tax Income, Tax Provision (Benefit), and Net Income (Loss) were not material to the 2018 or 2019 Financial Statements. This conclusion was based on an assessment of the total mix of information, taking into account both quantitative and qualitative factors, as provided for in SAB No. 99 and as further described below.

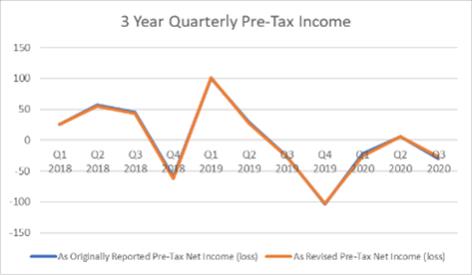

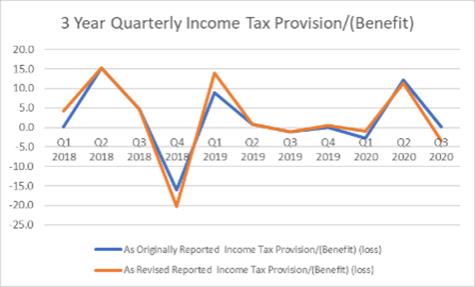

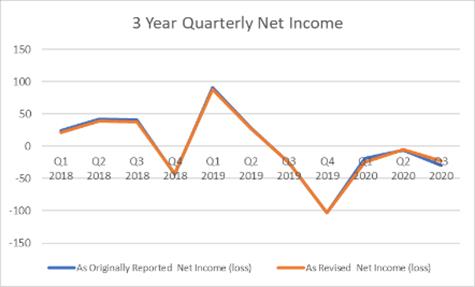

In support of this conclusion, the graphs below illustrate the impact of the errors on Pre-Tax Income, Income Tax (Benefit) Provision and Net Income for each of the quarters impacted for the prior three years. The graphs show that the impact on these income statement line items is not significant and, more importantly, that the impact of the errors has not materially altered any trends associated with these financial metrics.

Office of Finance

January 24, 2022

Page 3

The Company respectfully believes that informed readers of the Company’s financial statements understand that changes to Net Income (Loss) would have a corresponding impact on earnings per share (“EPS”) and would therefore not assess the impact of a change in EPS independently of changes in Net Income (Loss). This is particularly true when operating at or near break-even as EPS is a function of Net Income (Loss) over the outstanding number of shares. Small changes in Net Income (Loss) can have a correspondingly large impact on EPS, in percentage terms. In addition, the Company’s dividends have not historically followed its EPS and therefore EPS is not considered an indicator of future dividends especially given the volatility of EPS during the prior three years. The dividend per common share in 2018 was $1.08 for the full year and $1.24 for each of the full years 2019 and 2020. The Company also reviewed the impact of the errors on variable compensation for its named executive officers (“NEO’s”) and determined that there was no impact for 2020 and 2019. For 2018, correcting for the errors would have resulted in approximately a $35,000 decrease in the aggregate variable compensation for the NEOs which was not considered significant.

Office of Finance

January 24, 2022

Page 4

The Company’s Approach to Evaluating Materiality

In accordance with SAB No. 99, the Company considers both quantitative and qualitative factors to determine whether an error in the Company’s previously issued financial statements is material. The misstatement of an item in a financial statement is material if, in the light of surrounding circumstances, the magnitude of the item is such that it is probable that the judgment of a reasonable person relying upon the report, specifically users of the Company’s financial statements, would have been changed or influenced by the inclusion or correction of the item. SAB No. 99 states the following with respect to quantitative materiality threshold:

“The use of a percentage as a numerical threshold, such as 5%, may provide the basis for a preliminary assumption that – without considering all relevant circumstances – a deviation of less than the specified percentage with respect to a particular item on the registrant’s financial statements is unlikely to be material. The staff has no objection to such a “rule of thumb” as an initial step in assessing materiality. But quantifying, in percentage terms, the magnitude of a misstatement is only the beginning of an analysis of materiality; it cannot appropriately be used as a substitute for a full analysis of all relevant considerations.”

In response to this guidance, the Company first established a materiality threshold to initially guide it in its evaluation. The Company then performed a full analysis of all relevant considerations in reaching its conclusion that correcting the cumulative effect of these errors in the Company’s 2020 Financial Statements would materially misstate the 2020 financial statements, but the errors were not material to the Company’s previously issued 2018 Financial Statements and 2019 Financial Statements, or the related quarterly financial statements included in Forms 10-Q filed during those periods.

Quantitative Assessment of Materiality

The Company considers the materiality of any errors to the financial information presented in its public earnings releases and periodic filings, including the “Management’s Discussion and Analysis of Financial Condition and Results of Operations” included in its periodic filings on Forms 10-K and 10-Q (which includes both GAAP and non-GAAP measures) based on what management believes users of our financial statements, in particular investors and analysts, would consider important if materially misstated.

The financial results for insurance companies traditionally include a number of non-GAAP measures, adjusting for the financial impact from catastrophe events and prior year reserve development. Because catastrophe events and prior year reserve development generate an inherent level of volatility in an insurance company’s financial results, analysts and investors review financial results that include and exclude the impact of both of these items when evaluating an insurance company. As a global insurance provider, management (like its analysts and investors) considers the impact of such items when evaluating the Company’s financial results and performance. Therefore, management believes it is important to consider the impact of these errors on the financial results that both include and exclude catastrophe events and prior year development.

The Company considered Pre-Tax Net Income (adjusted for the financial impacts from catastrophe events and prior year reserve development) for the 5-year period, 2016-2020, as a basis for determining the quantitative materiality threshold. The table below provides the Pre-Tax Net Income, adjusted for Catastrophe Losses and Prior Year Reserve Development to arrive at Adjusted Pre-Tax Net Income, for each of the past five fiscal years. Then, applying a 5% threshold (as further explained below) to the three-year rolling average Adjusted Pre-Tax Income for 2018, 2019 and 2020, management established a quantitative materiality threshold for income statement items as follows:

Year | Pre-Tax Net Income (loss) | Catastrophe Losses* | Prior Year Reserve Development (Favorable)/ Unfavorable | Adjusted Pre-Tax Net Income | 3-Year Average Adjusted Pre- Tax Net Income ($) (in millions) | Quantitative Materiality Threshold ($) (in millions) | ||||||||||||||||||

2016 | 181.9 | 61.7 | (33.3 | ) | 210.3 | N/A | N/A | |||||||||||||||||

2017 | 39.9 | 145.1 | (8.2 | ) | 176.8 | N/A | N/A | |||||||||||||||||

2018 | 61.0 | 61.9 | (18.0 | ) | 104.9 | 164.0 | 8.2 | |||||||||||||||||

2019 | 0 | 34.3 | 138.1 | 172.5 | 151.4 | 7.6 | ||||||||||||||||||

2020 | (46.4 | ) | 186.8 | 7.7 | 148.1 | 141.8 | 7.1 | |||||||||||||||||

| * | Includes the impact of reinstatement premiums. |

Office of Finance

January 24, 2022

Page 5

The Company chose 5% of the rolling 3-year average of Adjusted Pre-Tax Net Income to test materiality on a quantitative basis on income statement items for the following reasons:

| • | the Company had been profitable historically but was currently making a loss or breaking-even; |

| • | the occurrence of natural catastrophe events can have a significant impact on any single year financial results; and |

| • | the emergence of historical favorable or unfavorable loss trends can have a significant impact on any single year financial results. |

In addition to Adjusted Pre-Tax Net Income, informed readers of the Company’s financial statements focus on Total Shareholders’ Equity as part of their analysis because capital is a key metric of perceived financial strength within the insurance industry. The Company also uses additional metrics to evaluate financial performance and help investors and analysts understand the Company’s financial results. As such, the assessment of materiality of the identified errors also focused on the following financial metrics:

| • | Gross written premiums |

| • | Underwriting income (loss) |

| • | Ex-catastrophe, accident year combined ratio |

| • | Operating income (loss) |

| • | Net Income (loss) before taxes |

| • | Net Income (loss) |

| • | Diluted EPS (loss) |

While readers of our financial statements may consider other financial metrics, the above items represent those metrics most often relied upon by such readers.

Qualitative Assessment of Materiality

Establishing a quantitative threshold for materiality by itself does not determine whether an item is considered material. A qualitative assessment is also conducted in conjunction with the quantitative assessment to determine whether an item is material. As laid out in SAB No. 99 the following factors are used to assist in the qualitative assessment of materiality:

| • | whether the misstatement arises from an item capable of precise measurement or whether it arises from an estimate and, if so, the degree of imprecision inherent in the estimate |

| • | whether the misstatement masks a change in earnings or other trends |

| • | whether the misstatement hides a failure to meet analysts’ consensus expectations for the enterprise |

| • | whether the misstatement changes a loss into income or vice versa |

| • | whether the misstatement concerns a segment or other portion of the registrant’s business that has been identified as playing a significant role in the registrant’s operations or profitability |

| • | whether the misstatement affects the registrant’s compliance with regulatory requirements |

| • | whether the misstatement affects the registrant’s compliance with loan covenants or other contractual requirements |

| • | whether the misstatement has the effect of increasing management’s compensation – for example, by satisfying requirements for the award of bonuses or other forms of incentive compensation |

| • | whether the misstatement involves concealment of an unlawful transaction. |

Office of Finance

January 24, 2022

Page 6

Determining Whether the Errors Identified were Material to the 2020 Financial Statements

The Company first determined if the impact of the errors identified during the preparation of the 2020 Financial Statements exceeded the Company’s preliminary quantitative materiality threshold. The cumulative quantitative impact of the errors identified on Net Income for the 2020 Financial Statement was $12.3 million, which is above the $7.1 million materiality threshold for income statement items described above. The Company also considered if there was a substantial likelihood that a reasonable person would consider the errors important to the individual amounts reported and concluded that the errors would be important to a reasonable person. Further, the Company did not identify any qualitative factors that would overcome the quantitative significance of the cumulative errors. Therefore, the Company concluded that the cumulative effect of the errors could not be corrected in 2020 without materially misstating the 2020 Financial Statements.

Determining Whether the Errors Identified were Material to the Quarterly 2020 Financial Statements

Management assessed the impact on the quarterly line items of the income statement and on the financial metrics below that were included in the Company’s 2020 Form 10-Qs.

Metric | Impact | |||||||||||||||||||||||

| Q1 | % Change | Q2 | % Change | Q3 | % Change | |||||||||||||||||||

Gross written premiums | $ | Nil | 0.0 | % | $ | Nil | 0.0 | % | $ | Nil | 0.0 | % | ||||||||||||

Underwriting income/(loss) | $ | (0.1 | ) m | (0.7 | )% | $ | 0.1 | m | 8.3 | % | $ | (0.2 | ) m | (0.4 | )% | |||||||||

Ex-catastrophe, accident year combined ratio | 0.0 | % | 0.0 | 0.0 | % | 0.0 | 0.0 | % | 0.0 | |||||||||||||||

Operating Income | $ | (0.1 | ) m | (0.8 | )% | $ | (0.2 | ) m | (4.3 | )% | $ | (0.3 | ) m | (2.5 | )% | |||||||||

(Loss) Income before income taxes | $ | (4.1 | ) m | (19.0 | )% | $ | 0.2 | m | 3.5 | % | $ | 2.9 | m | 9.9 | % | |||||||||

Net Income (Loss) | $ | (5.9 | ) m | (31.4 | )% | $ | 1.0 | m | 15.6 | % | $ | 6.5 | m | 22.0 | % | |||||||||

Diluted EPS (Loss) | $ | (0.17 | ) | (30.9 | )% | $ | 0.02 | 11.1 | % | $ | 0.19 | 20.9 | % | |||||||||||

The quantitative impact to the Company’s quarterly balance sheets included in 2020 Form 10-Qs were as follows:

Metric | % Impact | |||||||||||

| Q1 | Q2 | Q3 | ||||||||||

Total Assets | (0.2 | )% | (0.2 | )% | (0.1 | )% | ||||||

Total Liabilities | (0.0 | )% | 0.0 | % | 0.0 | % | ||||||

Total Shareholders’ Equity | (1.4 | )% | (1.3 | )% | (0.8 | )% | ||||||

The Company considered both the quantitative and qualitative factors in assessing whether any of the errors identified above materially impacted the quarters reported during 2020 and determined that none of the quarters had been materially impacted. In each of the quarters, the quantitative materiality threshold of $7.1 million was not breached for any of the financial metrics identified above. While management acknowledges that the $7.1 million materiality threshold is based on an annual assessment, the errors impacted line items that tend to be volatile, and changes to Pre-Tax Net Income, Tax Provision/(Benefit) and Net Income/(Loss) in the first three quarters of 2020 did not impact trends as demonstrated in the quarterly graphs above.

While the percentage changes to Pre-Tax Net Income and Net Income (Loss) for the first and third quarters were significant, the dollar value changes were immaterial.

The Company also analyzed the impact of the errors on individual line items in the income statement and concluded that none of the impacted line items would likely impact a user’s view of such line items or the Company’s results of operations.

The most notable impact on the quarterly financial results was on Foreign Currency Exchange Gains (Losses) and Income Tax (Benefit) Provision, as provided in the table below:

Line Item | Impact | |||||||||||||||||||||||

| Q1 | % Change | Q2 | % Change | Q3 | % Change | |||||||||||||||||||

Foreign Currency Exchange Gains (Losses) | 3.9 | 130 | % | (2.1 | ) | (32.8 | )% | (3.2 | ) | (27.6 | )% | |||||||||||||

Income Tax (Benefit) Provision | 1.8 | 64.3 | % | (0.8 | ) | (6.6 | )% | (3.6 | ) | (1,800 | )% | |||||||||||||

Office of Finance

January 24, 2022

Page 7

The Company concluded that while the percentage changes on these balances were significant, the changes were not material from a dollar perspective. Moreover, Foreign Currency Exchange Gains (Losses) is not a significant line item to the income statement and is generally prone to significant fluctuations. Additionally, given the nature of the Company’s business with multiple international jurisdictions, the global effective tax rate can fluctuate significantly from period to period and is not a primary focus of the users of the financial statements.

While management also acknowledges that the impact on Diluted EPS of $0.17 in the first quarter and $0.19 in third quarter of 2020 are quantitatively large, management notes that the driver behind this impact was relatively small changes in Net Income. Moreover, the change in Diluted EPS in percentage terms is exaggerated by the fact that Net Income was close to break-even during the 2020 quarters. In this instance, even a small change in Net Income in dollar terms would have a large impact in percentage terms. As stated previously, in the Company’s opinion, informed readers of financial statements will understand that small changes in Net Income can have a correspondingly large impact, in percentage terms, on Diluted EPS and would therefore not view this change on Diluted EPS independently without considering the impact across the financial statements when taken as a whole.

Having assessed the qualitative factors consistent with those considered below for the 2019 and 2018 Financial Statements, the Company determined that the errors were not material to the financial statements issued through the first three quarters of 2020. However, the Company recognized that not correcting the additional errors identified in the fourth quarter of 2020 would result in the 2020 Financial Statements being materially misstated and therefore corrected such errors in its 2020 Form 10-K.

Determining Whether the Errors Identified were Material to the 2018 and 2019 Financial Statements

Having determined that the errors identified during the preparation of the 2020 Financial Statements impacted both the 2018 and 2019 Financial Statements, the Company undertook a quantitative and qualitative evaluation of such periods in accordance with SAB No. 99 and SAB No. 108 to determine whether the prior period financial statements were materially misstated.

The Company analyzed the impact on the Company’s capital position by comparing Total Shareholders’ Equity for each of the periods impacted by the errors and concluded the errors were immaterial with respect to Total Shareholders’ Equity for the 2018 and 2019 Financial Statements.

The impact of the errors on 2018 and 2019 Total Shareholders’ Equity was as follows:

Year | As reported ($) millions | Adjustment ($) millions | As Adjusted ($) millions | % Change | ||||||||||||

2018 | 1,746.7 | (11.7 | ) | 1,735.0 | (0.7 | )% | ||||||||||

2019 | 1,781.1 | (17.4 | ) | 1,763.7 | (1.0 | )% | ||||||||||

Analyzing the impact on the 2019 Financial Statements

The table below includes information from Note 2 to the 2020 Financial Statements as included in the 2020 Form 10-K and reflects the adjustments made to each line item in the income statement for the errors identified in 2019 Consolidated Statement of Income (Loss):

| Year Ended December 31, 2019 | ||||||||||||||||

| As previously reported | Adjustments | As adjusted | % Change | |||||||||||||

| (in millions, except per share amounts) | ||||||||||||||||

Earned premiums | $ | 1,729.5 | $ | 0.2 | $ | 1,729.7 | 0.0 | % | ||||||||

Net realized investment gains | 80.0 | 0.1 | 80.1 | 0.1 | % | |||||||||||

Total revenue | 1,969.7 | 0.3 | 1,970.0 | 0.0 | % | |||||||||||

Underwriting, acquisition and insurance expenses | 665.8 | 0.2 | 666.0 | 0.0 | % | |||||||||||

Interest expense | 33.6 | 0.5 | 34.1 | 1.5 | % | |||||||||||

Foreign currency exchange gains | (9.6 | ) | (0.2 | ) | (9.8 | ) | (2.1 | )% | ||||||||

Total expenses | 1,969.5 | 0.5 | 1,970.0 | 0.0 | % | |||||||||||

(Loss) income before income taxes | 0.2 | (0.2 | ) | — | (100.0 | )% | ||||||||||

Income tax provision | 8.6 | 5.5 | 14.1 | 64.0 | % | |||||||||||

Net loss | (8.4 | ) | (5.7 | ) | (14.1 | ) | (67.9 | )% | ||||||||

Net loss per common share: | ||||||||||||||||

Basic | $ | (0.25 | ) | $ | (0.16 | ) | $ | (0.41 | ) | (64.0 | )% | |||||

Diluted | $ | (0.25 | ) | $ | (0.16 | ) | $ | (0.41 | ) | (64.0 | )% | |||||

Office of Finance

January 24, 2022

Page 8

The table below reflects the adjustments made to account for the errors on the 2019 Consolidated Balance Sheet:

| December 31, 2019 | ||||||||||||||||

| (in millions) | As previously reported | Adjustments | As adjusted | % Change | ||||||||||||

Fixed maturities available-for-sale, at fair value | $ | 3,633.5 | $ | (3.6 | ) | $ | 3,629.9 | (0.1 | )% | |||||||

Equity securities available-for-sale, at fair value | 124.4 | 11.6 | 136.0 | 9.3 | % | |||||||||||

Other investments | 496.5 | (9.9 | ) | 486.6 | (2.0 | )% | ||||||||||

Total investments | 5,099.4 | (1.9 | ) | 5,097.5 | (0.0 | )% | ||||||||||

Premiums receivable | 688.2 | (11.7 | ) | 676.5 | (1.7 | )% | ||||||||||

Reinsurance recoverables | 3,104.6 | 2.6 | 3,107.2 | 0.1 | % | |||||||||||

Deferred tax asset, net | 6.1 | 4.5 | 10.6 | 73.8 | % | |||||||||||

Other assets | 387.1 | 0.8 | 387.9 | 0.2 | % | |||||||||||

Total assets | 10,514.5 | (5.7 | ) | 10,508.8 | (0.1 | )% | ||||||||||

Accrued underwriting expenses and other liabilities | 226.0 | (4.1 | ) | 221.9 | (1.8 | )% | ||||||||||

Ceded reinsurance payable, net | 1,203.1 | (1.9 | ) | 1,201.2 | (0.2 | )% | ||||||||||

Funds held | 50.6 | 4.6 | 55.2 | 9.1 | % | |||||||||||

Current income taxes payable, net | 0.8 | 13.1 | 13.9 | 1,637.5 | % | |||||||||||

Total liabilities | 8,733.4 | 11.7 | 8,745.1 | 0.1 | % | |||||||||||

Retained earnings | 811.1 | (17.4 | ) | 793.7 | (2.1 | )% | ||||||||||

Total shareholders’ equity | 1,781.1 | (17.4 | ) | 1,763.7 | (1.0 | )% | ||||||||||

Total liabilities and shareholders’ equity | 10,514.5 | (5.7 | ) | 10,508.8 | (0.1 | )% | ||||||||||

Assessment of Materiality

In assessing the materiality of the errors identified in the 2019 Financial Statements, the Company performed a quantitative and qualitative assessment of the errors having already determined the errors were immaterial to the Company’s capital position. The errors resulted in an adjustment of $5.7 million to the 2019 Net Loss, which falls below the materiality threshold for 2019 of $7.6 million for income statement items. Moreover, 2019 was near breakeven before and after adjusting for these errors. They did not change an overall loss into a gain nor did they materially impact any of the Company’s operating segment results as the most significant change, being the Income Tax Provision, is not allocated to the Company’s operating segments.

Furthermore, the dollar value impact of those errors on the Balance Sheet were not material to the overall Total Asset, Total Liabilities and Total Shareholders’ Equity balances in the 2019 Balance Sheet as highlighted below:

Metric | $ Impact (in millions) | % Change | ||||||

Total Assets | (5.7 | ) | (0.1 | )% | ||||

Total Liabilities | 11.7 | 0.1 | % | |||||

Total Shareholders’ Equity | (17.4 | ) | (1.0 | )% | ||||

The following is an assessment of the impact on the Company’s additional financial metrics:

Metric | Impact | % Change | ||||||

Gross written premiums | $ | 1.0 m | 0.0 | % | ||||

Underwriting income | $ | Nil | 0.0 | % | ||||

Ex-catastrophe, accident year combined ratio | 0.0 | % | N/M | |||||

Operating Income | $ | (0.5 | ) m | (1.6 | )% | |||

(Loss) income before income taxes | $ | (0.2 | ) m | (100.0 | )% | |||

Net Income (Loss) | $ | (5.7 | ) m | (67.9 | )% | |||

Diluted EPS (Loss) | $ | (0.16 | ) | (64.0 | )% | |||

Office of Finance

January 24, 2022

Page 9

Based on the foregoing tables for 2019, management also noted changes in dollar amounts or percentages that warranted additional consideration as set forth below:

| • | Income Tax Provision: The errors most significantly impacted the Income Tax Provision and related gross up of tax balances in the 2019 Balance Sheet, such as Deferred Tax Assets, net, and Current Income Taxes Payable, net. Given the nature of the Company’s business with multiple international jurisdictions, the global effective tax rate can fluctuate significantly from period to period and therefore is not a primary focus of the users of the financial statements. The Deferred Tax Asset, net, and Current Income Taxes Payable, net are not deemed to be significant line items in the Balance Sheet. These errors also did not materially impact the Total Asset, Total Liability and Total Shareholders’ Equity balances. |

| • | Net Loss and Diluted EPS: While the impact to the Income Tax Provision, as described above, resulted in significant dollar and percentage changes in Net Loss and Diluted EPS, it did not materially affect the Company’s financial metrics: Gross Written Premiums, Underwriting Income, Ex-catastrophe accident year combined ratio and Operating Income. The percentage impact appears large due to the near break-even (Loss) income before income taxes and Net Loss for the year (adjusted Net Loss is less than 1% of revenues). Furthermore, the Company believes that informed readers of financial statements will not view the Net Loss and Diluted EPS changes independently without considering the impact across the financial statements when taken as a whole. |

| • | Equity Securities Available-for-Sale, at Fair Value: The Company notes significant dollar and percentage impact on Equity Securities Available-for-Sale, at Fair Value. Given that this balance sheet line item fluctuates with the market, users of financial statements expect movements in this line item and changes to this line item would not generally impact their evaluation of the financial statements. |

| • | Other Investments: While the Company notes a significant dollar value change on this balance sheet line item, the percentage change was not significant. Given that this balance sheet line item fluctuates with the market, users of financial statements expect movements in this line item and changes to this line item would not generally impact their evaluation of the financial statements. |

| • | Premiums Receivable: The Company notes that while the dollar value change is significant on Premium Receivable the percentage change is small given the large dollar value of the Premium Receivable balance. In the Company’s opinion this change would not influence or be important to a reader of the financial statements. |

Considering the foregoing quantitative impact of the errors to the 2019 Consolidated Statement of Loss, the Company determined that none of the impacted line items, individually or in aggregate, would likely impact a user’s view of such line items or the Company’s results of operations.

In addition to the quantitative review, the Company considered several qualitative factors as noted below that contributed to management’s overall conclusion that the errors were not material to the 2019 Financial Statements.

We summarize the qualitative factors considered:

| • | The errors were not the result of the use of estimates. The errors in the Company’s tax provision were caused by errors in the allocation of certain corporate expenses to subsidiaries. |

| • | The errors did not mask a change in earnings or other trends. The errors did not change the losses in fiscal year ended December 31, 2019 into a gain. Instead, the Company was essentially break-even before and after the adjustments. |

| • | The errors did not hide a failure to meet analysts’ consensus expectations for the Company, which are based on adjusted operating loss. The adjusted operating loss as reported in the Company’s 2019 fourth quarter Earnings Press Release was $30.8 million compared with $31.3 million post the correction of the errors. |

| • | The errors do not materially concern a segment or other portion of the Company’s business that has been identified as playing a significant role in the Company’s operations or profitability. The provision (benefit) for income is not allocated to the Company’s reported segments. |

| • | The errors did not affect the Company’s regulatory compliance and were timely reported to the Company’s group regulatory supervisor. |

| • | The errors had no adverse impact on the Company’s compliance with its loan covenants. |

Office of Finance

January 24, 2022

Page 10

| • | None of our named executive officers received annual incentive awards for 2019, except for Mr. Hernandez and Mr. Rehnberg. Mr. Hernandez did not participate in the annual incentive program but was eligible to receive a special bonus conditioned on the successful completion of certain targets, none of which were impacted by the errors. Mr. Rehnberg received an annual incentive award based on the Company-wide pre-tax operating income performance (weighted 30%) and business unit underwriting income performance (weighted 70%). Because both metrics were not significantly impacted by the errors, Mr. Rehnberg’s annual incentive award for 2019 was unaffected. |

| • | Management is not aware of evidence indicating that these errors involved any concealment activities or any unlawful transaction. |

| • | Investors were informed of the errors and the related impact in a timely manner through the Company’s 2020 Form 10-K. The 2020 Form 10-K filed by the Company contained the Company’s most current financial and other information, including the necessary disclosure of errors. As described further below, investors did not negatively react to these disclosures. |

Analyzing the impact on the 2018 Financial Statements

The table below includes information from Note 2 to the 2020 Financial Statements as included in the 2020 Form 10-K and reflects the adjustments made to each line item in the income statement for the errors identified in 2018 Consolidated Statement of Income (Loss):

| Year Ended December 31, 2018 | ||||||||||||||||

| (in millions, except per share amounts) | As reported | Adjustments | As adjusted | % Change | ||||||||||||

Earned premiums | $ | 1,731.7 | $ | (0.2 | ) | $ | 1,731.5 | (0.0 | )% | |||||||

Net investment income | 133.1 | (0.8 | ) | 132.3 | (0.6 | )% | ||||||||||

Total revenue | 1,801.8 | (1.0 | ) | 1,800.8 | (0.1 | )% | ||||||||||

Underwriting, acquisition and insurance expenses | 654.7 | 1.4 | 656.1 | 0.2 | % | |||||||||||

Interest expense | 31.6 | 0.3 | 31.9 | 0.9 | % | |||||||||||

Foreign currency exchange losses (gains) | (0.1 | ) | 4.0 | 3.9 | 4000.0 | % | ||||||||||

Total expenses | 1,734.1 | 5.7 | 1,739.8 | 0.3 | % | |||||||||||

(Loss) income before income taxes | 67.7 | (6.7 | ) | 61.0 | (9.9 | )% | ||||||||||

Income tax (benefit) provision | 4.1 | (0.1 | ) | 4.0 | (2.4 | )% | ||||||||||

Net (loss) income | 63.6 | (6.6 | ) | 57.0 | (10.4 | )% | ||||||||||

Net income (loss) per common share: | ||||||||||||||||

Basic | $ | 1.87 | $ | (0.19 | ) | $ | 1.68 | (10.2 | )% | |||||||

|

|

|

|

|

|

|

| |||||||||

Diluted | $ | 1.83 | $ | (0.18 | ) | $ | 1.65 | (9.8 | )% | |||||||

|

|

|

|

|

|

|

| |||||||||

The table below reflects the adjustments made to account for the errors to the 2018 Consolidated Balance Sheet:

| Impact on opening balances as of January 1, 2019 | ||||||||||||||||

| As previously reported | Adjustments | As adjusted | % Change | |||||||||||||

Equity securities available-for-sale, at fair value | $ | 354.5 | $ | 11.6 | $ | 366.1 | 3.3 | % | ||||||||

Other investments | 489.8 | (9.9 | ) | 479.9 | (2.0 | )% | ||||||||||

Cash | 139.2 | 0.5 | 139.7 | 0.4 | % | |||||||||||

Premiums receivable | 649.9 | (4.7 | ) | 645.2 | (0.7 | )% | ||||||||||

Reinsurance recoverables | 2,688.3 | 0.9 | 2,689.2 | 0.0 | % | |||||||||||

Current income taxes receivable, net | 8.2 | (8.2 | ) | — | (100.0 | )% | ||||||||||

Deferred tax asset, net | — | 1.3 | 1.3 | N/M | ||||||||||||

Accrued underwriting expenses and other liabilities | 261.9 | 1.1 | 263.0 | 0.4 | % | |||||||||||

Ceded reinsurance payable, net | 970.5 | (1.3 | ) | 969.2 | (0.1 | )% | ||||||||||

Funds held | 37.2 | 7.2 | 44.4 | 19.4 | % | |||||||||||

Current income taxes payable, net | — | 2.4 | 2.4 | N/M | ||||||||||||

Deferred tax liabilities, net | 6.2 | (6.2 | ) | — | (100.0 | )% | ||||||||||

Retained earnings | 862.6 | (11.7 | ) | 850.9 | (1.4 | )% | ||||||||||

Office of Finance

January 24, 2022

Page 11

Assessment of Materiality

In assessing the materiality of the errors identified in the 2018 Financial Statements the Company performed a quantitative and qualitative assessment of the errors having already determined the errors were immaterial to the Company’s capital position.

The errors resulted in an adjustment of $6.6 million to 2018 Net Income, which falls below the materiality threshold for 2018 of $8.2 million for income statement items. Moreover, these errors did not change an overall loss into a gain nor did they materially impact any of the Company’s operating segment results as the most significant change, being the Income Tax Provision, is not allocated to the Company’s operating segments.

In evaluating the impact further, management noted that the dollar value impact of those errors impacting the Balance Sheet was not material to the overall Total Asset, Total Liabilities and Total Shareholders’ Equity balances in the 2018 Balance Sheet as highlighted below:

Metric | $ Impact (in millions) | % Change | ||||||

Total Assets | (8.5 | ) | (0.1 | )% | ||||

Total Liabilities | 3.2 | 0.0 | % | |||||

Total Shareholders’ Equity | (11.7 | ) | (0.7 | )% | ||||

The following is an assessment of the impact on the Company’s additional financial metrics:

Metric | Impact | % Change | ||||||

Gross written premiums | $ | (1.0 | ) m | (0.0 | )% | |||

Underwriting income | $ | (1.6 | ) m | (4.4 | )% | |||

Ex-catastrophe, accident year combined ratio | 0.1 | % | N/M | |||||

Operating Income | $ | (2.7 | ) m | (2.4 | )% | |||

(Loss) income before income taxes | $ | (6.7 | ) m | (9.9 | )% | |||

Net Income (Loss) | $ | (6.6 | ) m | (10.4 | )% | |||

Diluted EPS (Loss) | $ | (0.18 | ) | (9.8 | )% | |||

Based on the foregoing tables for 2018, management also noted changes in dollar amounts or percentages that warranted additional consideration as set forth below:

| • | Foreign Currency Exchange Losses (Gains): While the Company noted significant dollar and percentage impact on Foreign Currency Exchange Losses (Gains), this line item is not a significant element of the financial statements. This line item is also generally susceptible to fluctuations and therefore is not a primary focus of the users of the financial statements. |

| • | Net Income and Diluted EPS: While the impact to the Foreign Currency Exchange Losses (Gains), as described above, resulted in significant percentage changes in Net Income and Diluted EPS, it did not materially affect the Company’s financial metrics: Gross Written Premiums, Underwriting Income, Ex-catastrophe accident year combined ratio and Operating Income. While the Company had a Net Income of $63.6 million and the impact to Diluted EPS may be viewed as quantitatively significant (Diluted EPS $1.83, Adjusted Diluted EPS $1.65), the Company’s operating results were significantly deteriorated as compared to prior years and was operating just above break-even (adjusted net income was only 3.2% of revenues). Additionally, there was significant volatility in the Company’s historical Diluted EPS (e.g., Diluted EPS was $1.83, $1.42, and $4.13 in fiscal years 2018, 2017, and 2016, respectively) and the adjustments did not materially change trends in Diluted EPS was also not an indicator of potential dividends. As noted above, the Company believes that informed readers of financial statements will not view Diluted EPS changes independently without considering the impact across the financial statements when taken as a whole. |

| • | Other 2018 Balance Sheet Line Items. Current Income Taxes Receivable, net and Funds Held are line items that are not deemed significant in the Balance Sheet and the dollar value changes in Equity Securities-Available- For Sale, at fair value, and Other Investments are not significant to those line items. The dollar value impact of those errors was not material to the overall Total Asset, Total Liability and Total Shareholders’ Equity balances in the 2018 Balance Sheet. |

Office of Finance

January 24, 2022

Page 12

Considering the foregoing quantitative impact of the errors to the Consolidated Statement of Income, the Company determined that none of line items, individually or in aggregate, would likely impact a user’s view of the line item or the Company’s results of operations.

In addition to the quantitative review, the Company considered several qualitative factors as noted below that contributed to management’s overall conclusion that the errors were not material to the 2018 Financial Statements. We summarize the qualitative factors considered:

| • | The errors were not the result of the use of estimates. The foreign currency gain (loss) errors were caused by an inadvertent error due to certain book entries related to a whole account quota share reinsurance contract not containing the foreign exchange impact on the whole account quota share. |

| • | The errors did not mask a change in earnings or other trends. The errors did not change the net income or positive Diluted EPS numbers for fiscal year ended December 31, 2018 into a loss. |

| • | The errors did not hide a failure to meet analysts’ consensus expectations for the Company, which are based on adjusted operating loss. The adjusted operating loss as reported in the Company’s 2018 fourth quarter Earning Press Release was $111.7 million compared with $109.0 million post the correction of the errors. |

| • | The errors do not materially concern a segment or other portion of the Company’s business that has been identified as playing a significant role in the Company’s operations or profitability. Foreign Currency Gains (Losses) are not allocated to the reporting segments. |

| • | The errors did not affect the Company’s regulatory compliance and were timely reported to the Company’s group regulatory supervisor. |

| • | The errors had no adverse impact on the Company’s compliance with its loan covenants. |

| • | For 2018, our named executive officers received annual incentive awards generally based on the Company’s pre-tax operating income. In addition, the annual incentive awards for Messrs. Rehnberg and Hernandez were measured based on both Company-wide pre-tax operating income performance (weighted 30%) and business unit pre-tax operating income performance (weighted 70%). None of these metrics used to evaluate annual incentive awards were impacted materially by the errors. Correcting for the errors would have resulted in approximately a $35,000 decrease in the aggregate variable compensation. |

| • | Management is not aware of evidence indicating that these errors involved any concealment activities or any unlawful transaction. |

Disclosures

As noted in the Staff’s comment, the Company’s 2020 Form 10-K fully disclosed the nature and quantitative impact of the errors on its 2018, 2019 and 2020 financial statements. Furthermore, prior to filing its 2020 Form 10-K, the Company disclosed in a Form 8-K filed with the Commission on March 12, 2021 (i) these errors and (ii) that management concluded a related material weakness in internal control over financial reporting existed. The Company also noted these errors and the material weakness during its March 12, 2021 investor update call attended by more than 70 analysts and investors. Even so, no investors or analysts asked about the errors or material weakness during the call’s “Q&A” session. Similarly, management does not believe there was significant impact on the price of the Company’s shares on the date the Form 8-K was filed or the following trading day—March 15, 2021, after the intervening weekend as a result of the disclosure of the errors. The Company has not received any indication from investors that the errors were viewed as material or significant. In fact, from March 2021 through December 2021, the Company attended 76 meetings, including attendance at conferences, with various investors and analysts and received only a handful of questions which sought clarity as to the scope and quantum of the errors. Further, the Company was not subject to any analyst downgrades as a result of these errors.

The Company believes the appropriate disclosures of the errors were included in Note 2 of the 2020 Financial Statements included in the 2020 Form 10-K for the relevant financial periods.

Office of Finance

January 24, 2022

Page 13

Controls and Procedures

As disclosed in the 2020 Form 10-K, management determined that both the Company’s disclosure controls and procedures and internal control over financial reporting were ineffective as of December 31, 2020. These conclusions were based on the timeliness and completeness of internal communication of certain relevant financial information within the Company, as well as in controls that used such information, which resulted in the errors.

Other Considerations

The Company discussed the accounting, financial reporting, and disclosure considerations associated with this adjustment with its independent auditors and the Audit Committee of the Board of Directors, each of which supported management’s conclusions.

* * * * *

Conclusion

Based on the foregoing, the Company continues to believe that the errors it identified were not material to the Company’s previously issued financial statements and the approach it took to disclose and account for the errors is in compliance with the applicable accounting standards and Staff guidance. If you have any questions or would like any additional information regarding the foregoing, please do not hesitate to contact me at +44 20 7712 7698.

| Very truly yours, |

| /s/ Scott Kirk |

| Scott Kirk |

| Chief Financial Officer |

| cc: | Brian V. Breheny |

Partner

Skadden, Arps, Slate, Meagher & Flom LLP and Affiliates