September 2, 2014 September 2, 2014 ALBANIA ACQUISITION ARRANGEMENT AGREEMENT TO ACQUIRE STREAM OIL & GAS LTD. ALBANIA ACQUISITION ARRANGEMENT AGREEMENT TO ACQUIRE STREAM OIL & GAS LTD. Exhibit 99.2 |

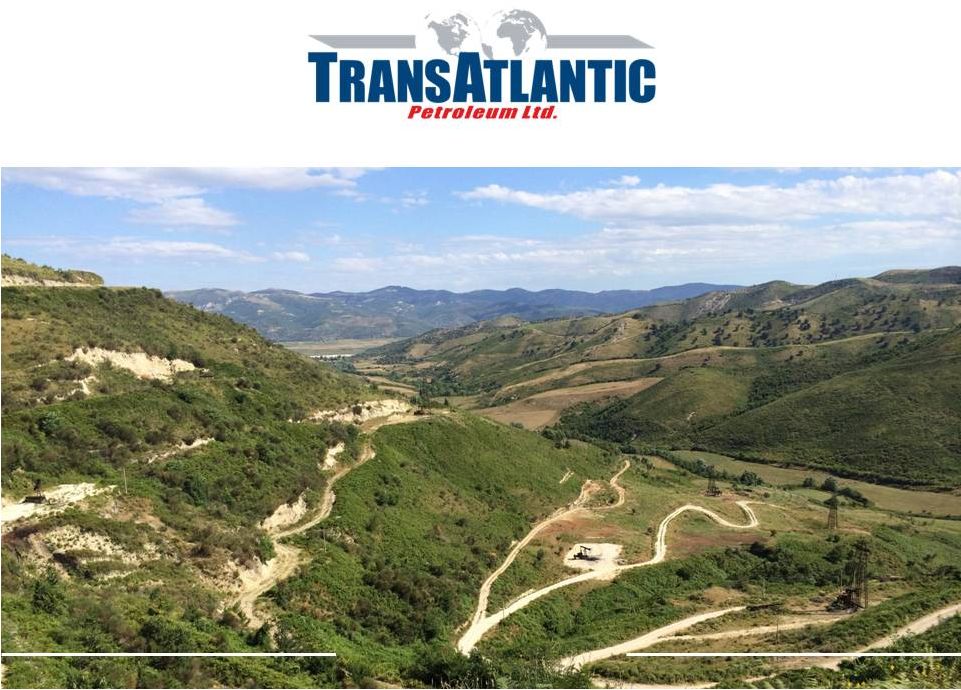

FORWARD LOOKING STATEMENTS 2 Cover Photo: Gorisht field in Albania. Outlooks, projections, estimates, targets and business plans in this presentation or any related subsequent discussions are forward-looking statements. Actual future results, including TransAtlantic Petroleum Ltd.’s or Stream Oil & Gas Ltd.’s production growth and mix; financial results; the amount and mix of capital expenditures; resource additions and recoveries; finding and development costs; project and drilling plans, timing, costs, and capacities; revenue enhancements and cost efficiencies; industry margins; margin enhancements and integration benefits; and the impact of technology could differ materially due to a number of factors. These include market prices for natural gas, natural gas liquids and oil products; estimates of reserves and economic assumptions; the ability to produce and transport natural gas, natural gas liquids and oil; the results of exploration and development drilling and related activities; economic conditions in the countries and provinces in which we carry on business, especially economic slowdowns; actions by governmental authorities, receipt of required approvals, increases in taxes, legislative and regulatory initiatives relating to fracture stimulation activities, changes in environmental and other regulations, and renegotiations of contracts; political uncertainty, including actions by insurgent groups or other conflict; the negotiation and closing of material contracts; shortages of drilling rigs, equipment or oilfield services; and other factors discussed here and under the heading “Risk Factors" in TransAtlantic’s Annual Report on Form 10-K for the year ended December 31, 2013 which is available at www.transatlanticpetroleum.com and www.sec.gov. See also TransAtlantic’s audited financial statements and the accompanying management discussion and analysis. See Stream’s financial statements and company profile at www.sedar.com. Forward-looking statements are based on management’s knowledge and reasonable expectations on the date hereof, and we assume no duty to update these statements as of any future date. The information set forth in this presentation does not constitute an offer, solicitation or recommendation to sell or an offer to buy any securities of the Company. The information published herein is provided for informational purposes only. The Company makes no representation that the information and opinions expressed herein are accurate, complete or current. The information contained herein is current as of the date hereof, but may become outdated or subsequently may change. Nothing contained herein constitutes financial, legal, tax, or other advice. The SEC has generally permitted oil and gas companies, in their filings with the SEC, to disclose only proved reserves that a company has demonstrated by actual production or conclusive formation tests to be economically and legally producible under existing economic and operating conditions. We may use the terms “estimated ultimate recovery,” “EUR,” “probable,” “possible,” and “non-proven” reserves, “prospective resources” or “upside” or other descriptions of volumes of resources or reserves potentially recoverable through additional drilling or recovery techniques that the SEC’s guidelines may prohibit us from including in filings with the SEC. These estimates are by their nature more speculative than estimates of proved reserves and accordingly are subject to substantially greater risk of actually being realized by the Company. There is no certainty that any portion of estimated prospective resources will be discovered. If discovered, there is no certainty that it will be commercially viable to produce any portion of the estimated prospective resources. Note on Possible Reserves: possible reserves are those additional reserves that are less certain to be recovered than probably reserves. There is a 10% probability that the quantities actually recovered will equal or exceed the sum of proved plus probable plus possible reserves. Note on BOE: BOE (barrel of oil equivalent) is derived by converting natural gas to oil in the ratio of six thousand cubic feet (MCF) of natural gas to one barrel (bbl) of oil. BOE may be misleading, particularly if used in isolation. A BOE conversion ratio of 6 Mcf:1 bbl is based on an energy equivalency conversion method primarily applicable at the burner tip and does not represent a value equivalency at the wellhead. |

ALBANIA ACQUISITION OBJECTIVE 3 Albania To Be a Third Source of Production and Income Growth; Provides Reservoir and Geographical Diversification • Large oil in place; known location • Exploitation, not exploration • 2015 – analyze, resize, streamline operation, reactivate wells, expand waterflood • 2016+ – focused horizontal development • Gas highly prospective, but markets need development Photo: Gorisht field in Albania. |

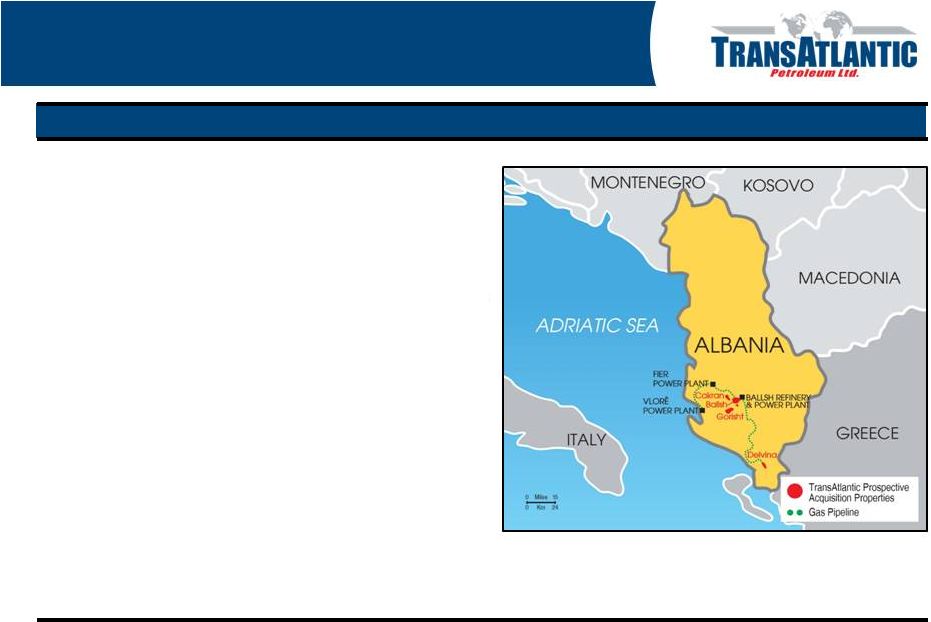

4 ALBANIA ACQUISITION SUMMARY 1 Reserves as of November 30, 2013, independent reserves evaluation by Deloitte LLP, in accordance with the provisions of NI51-101 and the Canadian Oil & Gas Evaluation Handbook. Ten year forward prices range from US$78.96 to US$89.53 per BO and US$9.70 to US$11.82 per MCF. TransAtlantic expects to finalize purchased reserves at year-end 2014. 2 Production is for the three months ended May 31, 2014. TransAtlantic to acquire 100% of Stream Oil & Gas Ltd. (“Stream”) (TSX Venture: SKO) Albanian Assets • Three oil fields, one gas field, one exploration license • 25 year prod. licenses with unlimited 5-yr extensions • Approximately 75,000 net acres • Stream’s reported net proved reserves: 20.9 MMBOE 1 Note: TransAtlantic expects proved reserves to decrease at year-end 2014 due to unaccomplished 2014 work program. • Production: 1,522 BOPD gross, 973 BOPD net 2 • Prices: oil: 68-75% of Brent, gas: ~$9/MCF • Fiscal terms: 12% royalty until 100% cost recovery; 13-16% royalty and 50% net profit tax after 100% recovery; VAT exempt Summary of Terms • US$41.2 million (C$0.67/US$0.62 per share) plus balance sheet assumption • To be paid 85% upon transaction closing, 15% upon final required approvals within nine months |

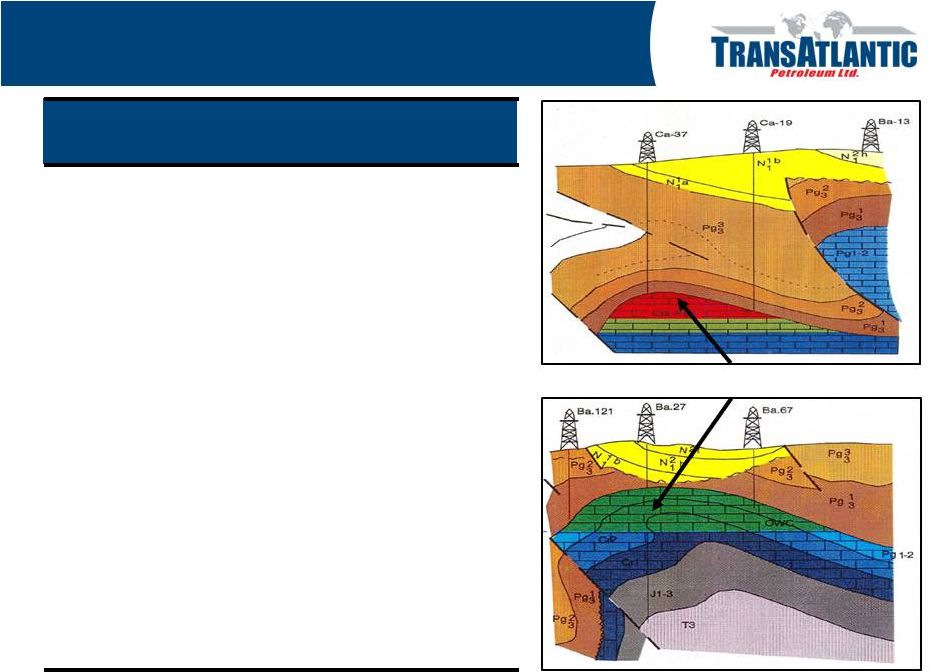

THREE OIL FIELDS IN ALBANIA Source: Albanian National Agency of Natural Resources. Oil trapped in carbonate reservoirs Cakran Field Ballsh Field 5 1 Fields contain other previously producing wells, some of which are no longer active. The actual penetration of the reservoir, mechanical success and current wellbore condition of these wells is uncertain. Structural Traps of Fractured Carbonates Cretaceous-Paleocene Age Gorisht Field (~800 BOPD gross, ~400 BOPD net) • Discovered 1965, 25,000 BOPD at peak (15 o API) • 150 producing wells 1 ; 3,000 net acres; two pilot waterfloods have mitigated decline • Well depths: 1,300 – 4,100 feet (400 – 1,250 meters) Cakran Field (~625 BOPD gross, ~500 BOPD net) • Discovered 1977, 6,000 BOPD at peak (25 o API) • 30 producing wells 1 ; 6,000 net acres • Well depths: 8,600 – 12,200 feet (2,650 – 3,700 meters) Ballsh Field (~100 BOPD gross, ~75 BOPD net) • Discovered 1966, 7,500 BOPD at peak (11 o API) • 15 producing wells 1 ; 6,000 net acres; expect to take over another 60+ wells in 2014 (~175 BOPD gross) • Well depths: 1650 – 4,600 feet (500 –1400 meters) |

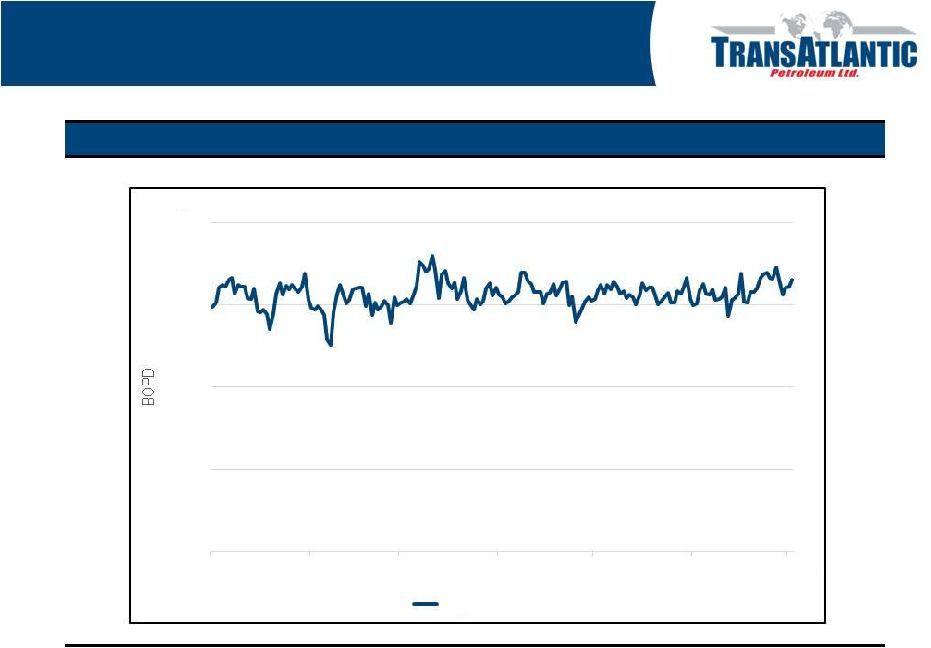

2014 Average Gross Production of Stream’s Three Oil Fields in Albania OIL FIELDS IN ALBANIA ARE ON FLAT DECLINE Source: Stream Oil & Gas Ltd. 6 0 500 1,000 1,500 2,000 1/1/2014 2/1/2014 3/1/2014 4/1/2014 5/1/2014 6/1/2014 7/1/2014 Daily Oil Production |

7 ONE GAS FIELD IN ALBANIA Photo: Drilling a well in the Delvina field in southern Albania, 2014. Structural Trap of Fractured Carbonates Cretaceous-Paleocene Age Delvina Field • • Two existing vertical wells, third well spudded March 2014; well depth: 9,200 – 11,500 feet (2,800 – 3,500 meters) • Wells currently non-producing Adjacent Exploration License • Holds the rights to 60,000 net acres adjacent to Delvina field • Three adjacent undrilled structures Discovered 1987, gas condensate (63 o API) |

8 DEVELOPMENT OPPORTUNITIES Plan for Growth • Upgrade oilfield technology to optimize field recovery and increase production levels • Drill infill and horizontal oil wells; reactivate wells; expand waterflood infrastructure in the Gorisht field • Optimize wells with recompletions and workover activity: upgrade pumps on existing wells, introduce artificial lift systems, re-enter and clean out legacy wells, introduce modern stimulation technology, utilize casinghead gas for onsite power generation • Drill natural gas development wells in the Delvina field and expand the monetization of condensates • Modify infrastructure and increase port storage facilities to decrease transport costs, debottleneck surface production facilities Photo: Gorisht field in Albania, primary development area. |

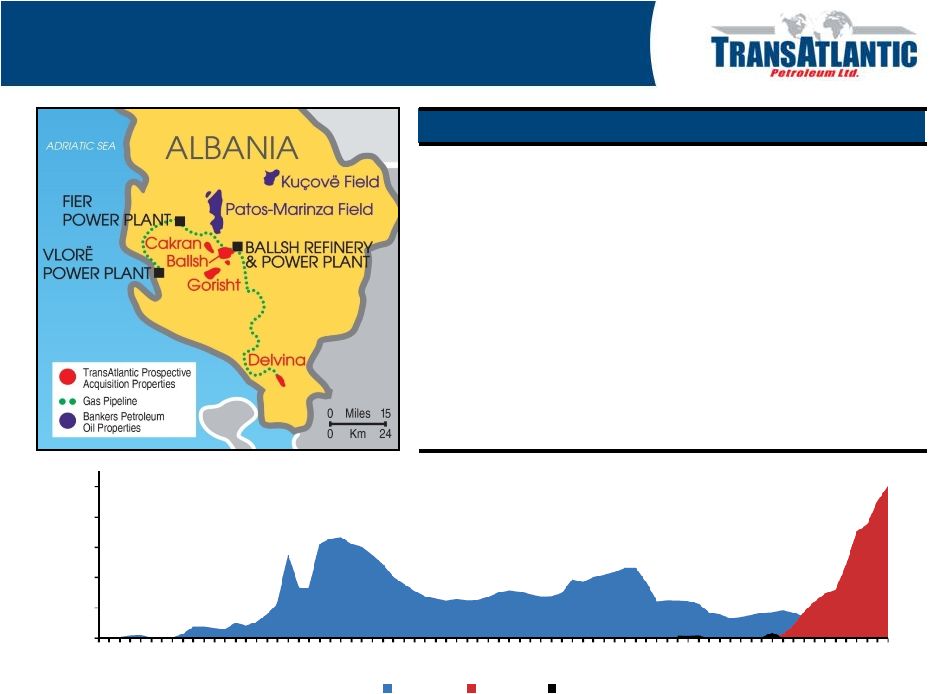

PRECEDENT: BANKERS PETROLEUM Average Historical Production in Patos-Marinza Field Albpetrol Bankers AAP 20,000 16,000 12,000 8,000 4,000 9 Source: Bankers Petroleum, August 2014 corporate presentation. 1939 1944 1949 1954 1959 1964 1969 1974 1979 1984 1989 1994 1999 2004 2009 2014 Bankers Petroleum – Albanian Oil Assets • in 2004 and developed it from 400 BOD to more than 20,000 BOD over a ten year period • Field development included reactivations, optimizations, horizontal drilling, secondary recovery, modernization of surface facilities, field electrification, expansion of export capabilities, preparing to initiate tertiary recovery (steam) • Same oil source, carbonate reservoir breached into shallower sandstones Bankers signed a concession for the Patos-Marinza oil field |

10 Taylor C. Beach Director of Investor Relations (214) 265-4746 Taylor.Beach@tapcor.com Matthew W. McCann General Counsel & Corporate Secretary (214) 220-4323 www.TransAtlanticPetroleum.com CONTACTS |