Exhibit 99.1

CANADIAN OPEN HOUSE EVENTS

TORONTO · CALGARY · VANCOUVER

November 3 – 4, 2014

FORWARD LOOKING STATEMENTS

Outlooks, projections, estimates, targets and business plans in this presentation or any related subsequent discussions are forward-looking statements. Actual future results, including TransAtlantic Petroleum Ltd.’s own production growth and mix; financial results; the amount and mix of capital expenditures; resource additions and recoveries; finding and development costs; project and drilling plans, timing, costs, and capacities; revenue enhancements and cost efficiencies; industry margins; margin enhancements and integration benefits; and the impact of technology could differ materially due to a number of factors. These include market prices for natural gas, natural gas liquids and oil products; estimates of reserves and economic assumptions; the ability to produce and transport natural gas, natural gas liquids and oil; the results of exploration and development drilling and related activities; economic conditions in the countries and provinces in which we carry on business, especially economic slowdowns; actions by governmental authorities, receipt of required approvals, increases in taxes, legislative and regulatory initiatives relating to fracture stimulation activities, changes in environmental and other regulations, and renegotiations of contracts; political uncertainty, including actions by insurgent groups or other conflict; the negotiation and closing of material contracts; shortages of drilling rigs, equipment or oilfield services; and other factors discussed here and under the heading “Risk Factors” in our Annual Report on Form 10-K for the year ended December 31, 2013, which is available on our website at www.transatlanticpetroleum.com and on www.sec.gov. See also TransAtlantic’s audited financial statements and the accompanying management discussion and analysis. Forward-looking statements are based on management’s knowledge and reasonable expectations on the date hereof, and we assume no duty to update these statements as of any future date.

The information set forth in this presentation does not constitute an offer, solicitation or recommendation to sell or an offer to buy any securities of the Company. The information published herein is provided for informational purposes only. The Company makes no representation that the information and opinions expressed herein are accurate, complete or current. The information contained herein is current as of the date hereof, but may become outdated or subsequently may change. Nothing contained herein constitutes financial, legal, tax, or other advice.

The SEC has generally permitted oil and gas companies, in their filings with the SEC, to disclose only proved reserves that a company has demonstrated by actual production or conclusive formation tests to be economically and legally producible under existing economic and operating conditions. We may use the terms “estimated ultimate recovery,” “EUR,” “probable,” “possible,” and “non-proven” reserves, “prospective resources” or “upside” or other descriptions of volumes of resources or reserves potentially recoverable through additional drilling or recovery techniques that the SEC’s guidelines may prohibit us from including in filings with the SEC. These estimates are by their nature more speculative than estimates of proved reserves and accordingly are subject to substantially greater risk of actually being realized by the Company. There is no certainty that any portion of estimated prospective resources will be discovered. If discovered, there is no certainty that it will be commercially viable to produce any portion of the estimated prospective resources.

Note on Possible Reserves: possible reserves are those additional reserves that are less certain to be recovered than probable reserves. There is a 10% probability that the quantities actually recovered will equal or exceed the sum of proved plus probable plus possible reserves.

Note on BOE: BOE (barrel of oil equivalent) is derived by converting natural gas to oil in the ratio of six thousand cubic feet (MCF) of natural gas to one barrel (bbl) of oil. BOE may be misleading, particularly if used in isolation. A BOE conversion ratio of 6 Mcf:1 bbl is based on an energy equivalency conversion method primarily applicable at the burner tip and does not represent a value equivalency at the wellhead.

Cover Photo: Şelmo-34 well site in southeastern Turkey.

2

THE COMBINED COMPANY

Malone Mitchell 3rd – Chairman & CEO

3

WHY STREAM SHOULD MERGE WITH

TRANSATLANTIC

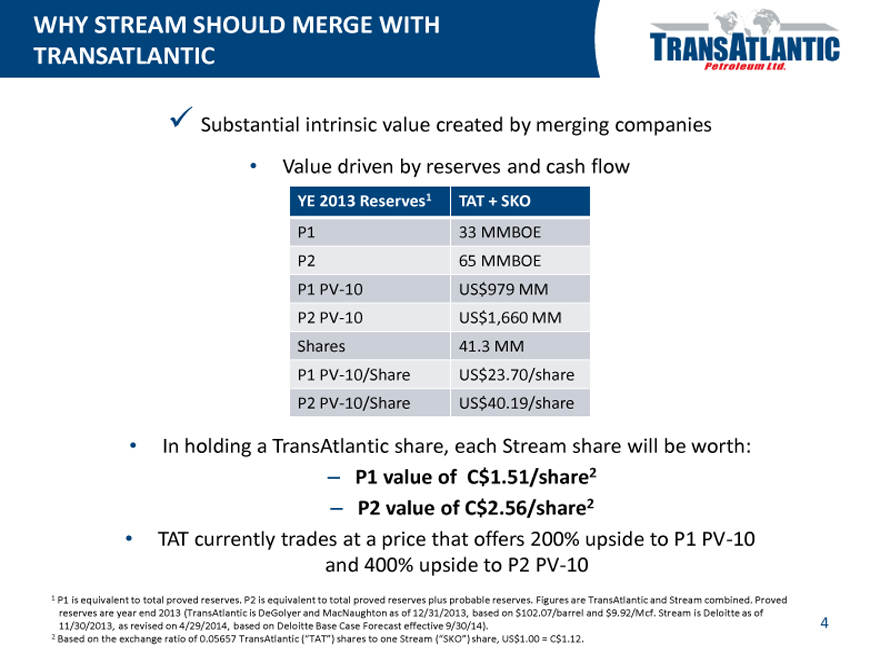

Substantial intrinsic value created by merging companies

Value driven by reserves and cash flow

YE 2013 Reserves1 TAT + SKO

P1 33 MMBOE

P2 65 MMBOE

P1 PV-10 US$979 MM

P2 PV-10 US$1,660 MM

Shares 41.3 MM

P1 PV-10/Share US$23.70/share

P2 PV-10/Share US$40.19/share

In holding a TransAtlantic share, each Stream share will be worth:

– P1 value of C$1.51/share2

– P2 value of C$2.56/share2

TAT currently trades at a price that offers 200% upside to P1 PV-10 and 400% upside to P2 PV-10

1 P1 is equivalent to total proved reserves. P2 is equivalent to total proved reserves plus probable reserves. Figures are TransAtlantic and Stream combined. Proved reserves are year end 2013 (TransAtlantic is DeGolyer and MacNaughton as of 12/31/2013, based on $102.07/barrel and $9.92/Mcf. Stream is Deloitte as of 11/30/2013, as revised on 4/29/2014, based on Deloitte Base Case Forecast effective 9/30/14).

2 Based on the exchange ratio of 0.05657 TransAtlantic (“TAT”) shares to one Stream (“SKO”) share, US$1.00 = C$1.12.

4

WHY STREAM SHOULD MERGE WITH

TRANSATLANTIC

Merger will result in an experienced, diversified oil and gas company

Advantages of scale together, expect to grow beyond 10,000 BOEPD much sooner

Working with an experienced operator who sees potential in Albania properties, with a plan and the demonstrated ability to increase their asset value

Management is successfully developing similar assets in the region

Combined company will have improved access to high quality, low cost services

Owning shares of combined company gives Stream investors access to upside potential in Turkey, Albania and Bulgaria

Photo: Bahar field in southeastern Turkey.

5

FOCUSED ON ESTABLISHED, UNDEREXPLORED

PETROLEUM SYSTEMS

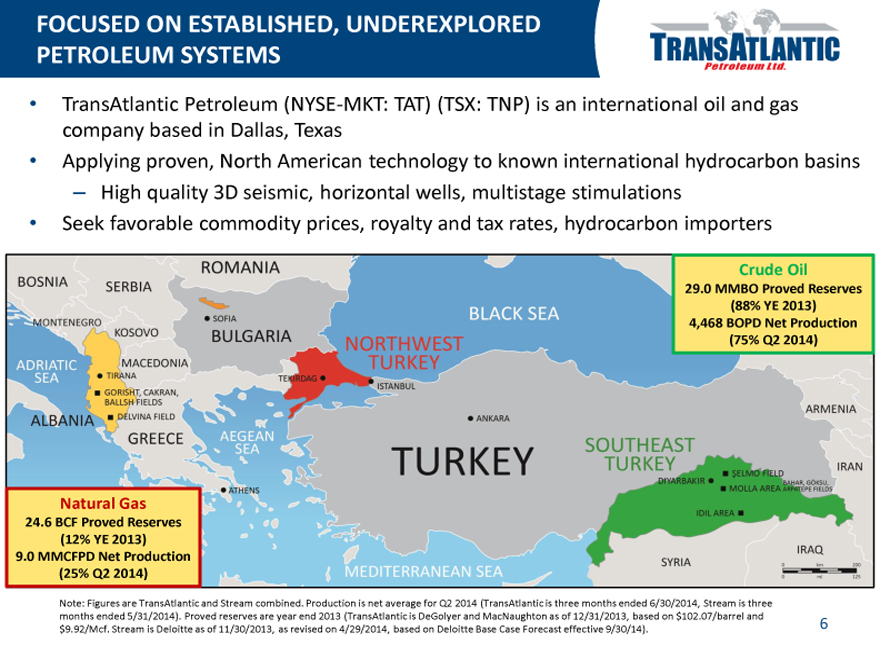

TransAtlantic Petroleum (NYSE-MKT: TAT) (TSX: TNP) is an international oil and gas company based in Dallas, Texas Applying proven, North American technology to known international hydrocarbon basins

– High quality 3D seismic, horizontal wells, multistage stimulations

Seek favorable commodity prices, royalty and tax rates, hydrocarbon importers

Crude Oil

29.0 MMBO Proved Reserves

(88% YE 2013) 4,468 BOPD Net Production (75% Q2 2014)

Natural Gas

24.6 BCF Proved Reserves (12% YE 2013) 9.0 MMCFPD Net Production (25% Q2 2014)

Note: Figures are TransAtlantic and Stream combined. Production is net average for Q2 2014 (TransAtlantic is three months ended 6/30/2014, Stream is three months ended 5/31/2014). Proved reserves are year end 2013 (TransAtlantic is DeGolyer and MacNaughton as of 12/31/2013, based on $102.07/barrel and $9.92/Mcf. Stream is Deloitte as of 11/30/2013, as revised on 4/29/2014, based on Deloitte Base Case Forecast effective 9/30/14).

6

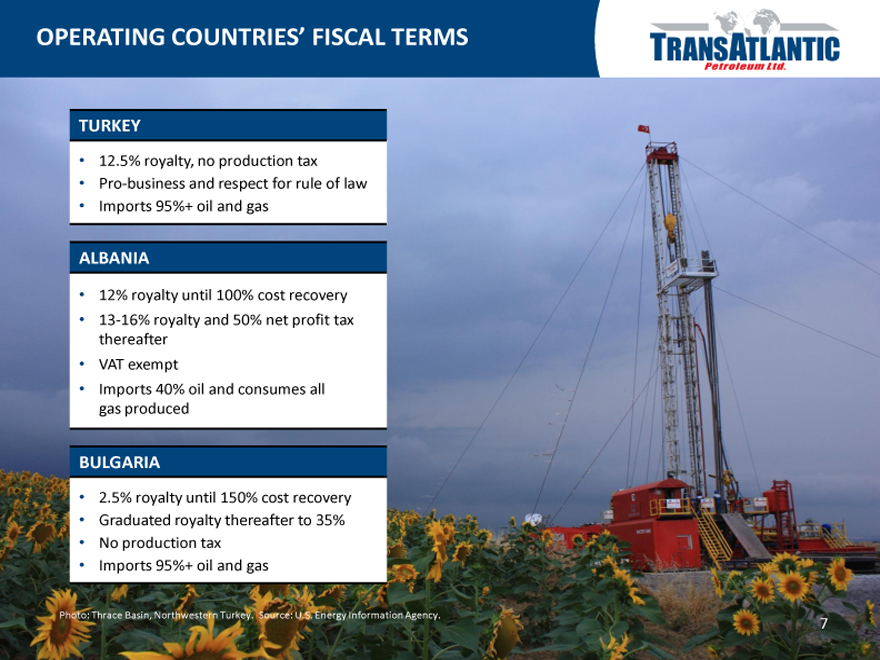

OPERATING COUNTRIES’ FISCAL TERMS

TURKEY

12.5% royalty, no production tax

Pro-business and respect for rule of law

Imports 95%+ oil and gas

ALBANIA

12% royalty until 100% cost recovery

13-16% royalty and 50% net profit tax thereafter

VAT exempt

Imports 40% oil and consumes all gas produced

BULGARIA

2.5% royalty until 150% cost recovery

Graduated royalty thereafter to 35%

No production tax

Imports 95%+ oil and gas

Photo: Thrace Basin, Northwestern Turkey. Source: U.S. Energy Information Agency.

7

ADVANTAGES OF COMBINED COMPANY

Geographical diversification – presence in three countries

Geological variation – production in several basins

Balanced oil and natural gas portfolio

Broader base of production will result in less impact per well

Upgraded listing on stock exchange

Additional trading liquidity appeals to investors

Photo: Şelmo-54H well in southeastern Turkey.

8

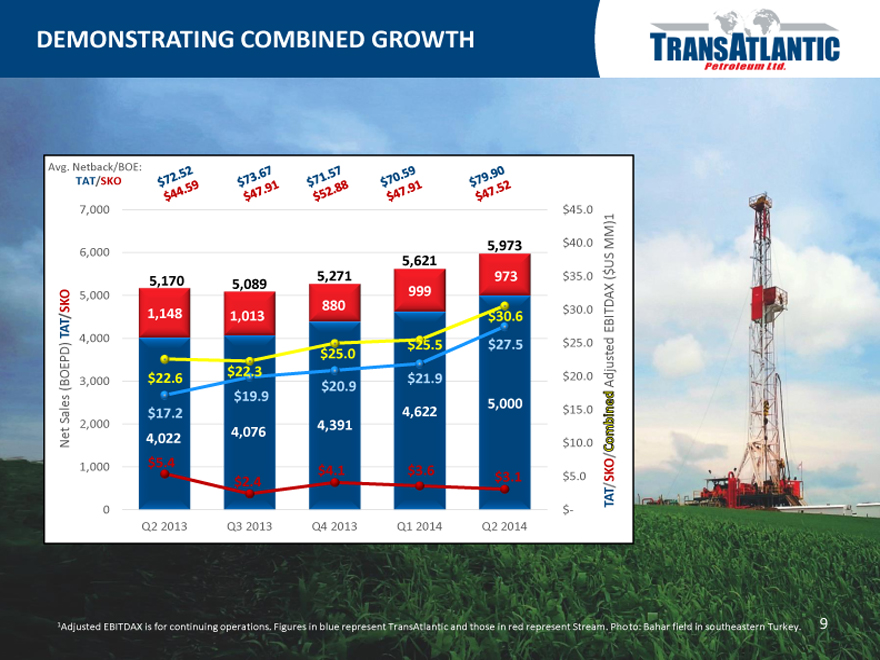

DEMONSTRATING COMBINED GROWTH

Avg. Netback/BOE:

Net Sales (BOEPD) TAT/SKO

TAT/SKO

7,000

6,000

5,000

4,000

3,000

2,000

1,000

0

$72.52

$44.59

$73.67

$47.91

$71.57

$52.88

$70.59

$47.91

$79.90

$47.52

5,973 5,621 5,170 5,271 973 5,089 999 880 1,148 1,013 $30.6 $25.5 $27.5 $25.0 $22.3 $22.6 $21.9 $20.9 $19.9 5,000 $17.2 4,622 4,391 4,076 4,022

$5.4

$4.1 $3.6

$2.4 $3.1

Q2 2013 Q3 2013 Q4 2013 Q1 2014 Q2 2014

$45.0

$40.0

$35.0

$30.0

$25.0

$20.0

$15.0

$10.0

$5.0

$—

TAT/SKO/ Combined Adjusted EBITDAX ($US MM)1

1Adjusted EBITDAX is for continuing operations. Figures in blue represent TransAtlantic and those in red represent Stream. Photo: Bahar field in southeastern Turkey.

9

MANAGEMENT TEAM

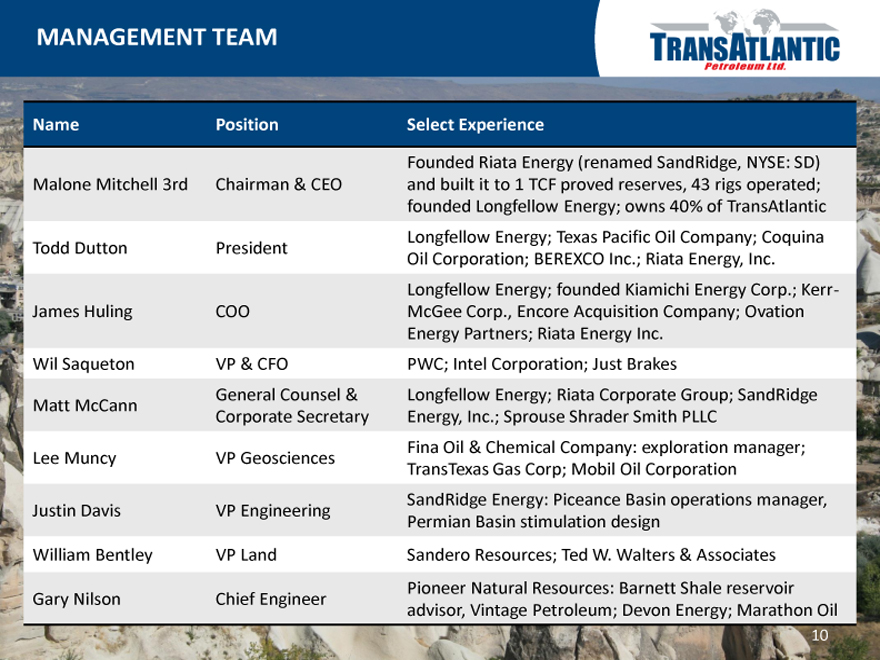

Name

Malone Mitchell 3rd

Todd Dutton

James Huling Wil Saqueton Matt McCann Lee Muncy Justin Davis William Bentley Gary Nilson

Position

Chairman & CEO

President

COO

VP & CFO General Counsel & Corporate Secretary

VP Geosciences VP Engineering VP Land Chief Engineer

Select Experience

Founded Riata Energy (renamed SandRidge, NYSE: SD) and built it to 1 TCF proved reserves, 43 rigs operated; founded Longfellow Energy; owns 40% of TransAtlantic Longfellow Energy; Texas Pacific Oil Company; Coquina Oil Corporation; BEREXCO Inc.; Riata Energy, Inc. Longfellow Energy; founded Kiamichi Energy Corp.; Kerr-McGee Corp., Encore Acquisition Company; Ovation Energy Partners; Riata Energy Inc.

PWC; Intel Corporation; Just Brakes

Longfellow Energy; Riata Corporate Group; SandRidge Energy, Inc.; Sprouse Shrader Smith PLLC

Fina Oil & Chemical Company: exploration manager; TransTexas Gas Corp; Mobil Oil Corporation SandRidge Energy: Piceance Basin operations manager, Permian Basin stimulation design

Sandero Resources; Ted W. Walters & Associates

Pioneer Natural Resources: Barnett Shale reservoir advisor, Vintage Petroleum; Devon Energy; Marathon Oil

10

OIL ASSETS

Lee Muncy – VP Geosciences

Top Value Generators YE 2014

1. Şelmo Field, Turkey

2. Molla Area, Turkey

3. Gorisht-Cakran-Ballsh, Albania

4. Idil Prospect, Turkey

Expected Top Value Generators 2016

1. Gorisht-Cakran-Ballsh, Albania

2. Molla Area, Turkey

3. Şelmo Field, Turkey

? Idil Prospect, Turkey

11

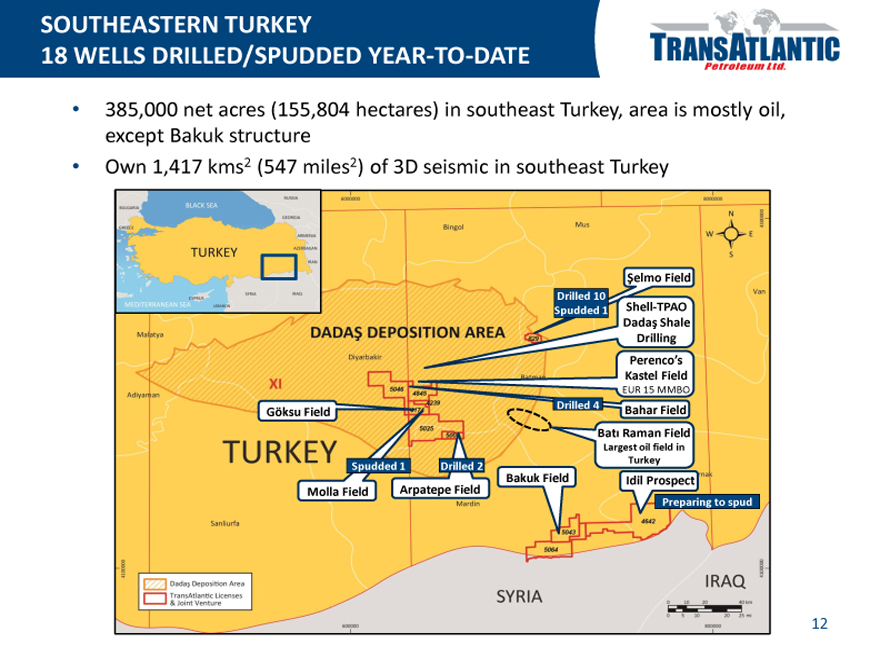

SOUTHEASTERN TURKEY

18 WELLS DRILLED/SPUDDED YEAR-TO-DATE

385,000 net acres (155,804 hectares) in southeast Turkey, area is mostly oil, except Bakuk structure Own 1,417 kms2 (547 miles2) of 3D seismic in southeast Turkey

Şelmo Field

Drilled 10

Spudded 1

Shell-TPAO

Dadaş Shale

Drilling

Perenco’s

Kastel Field

EUR 15 MMBO

Drilled 4

Bahar Field Göksu Field

Bat; Raman Field

Largest oil field in Turkey

Spudded 1 Drilled 2

Bakuk

Field Idil Prospect Molla Field Arpatepe Field

Preparing to spud

DADAŞ DEPOSITION AREA

TURKEY

SYRIA

IRAQ

12

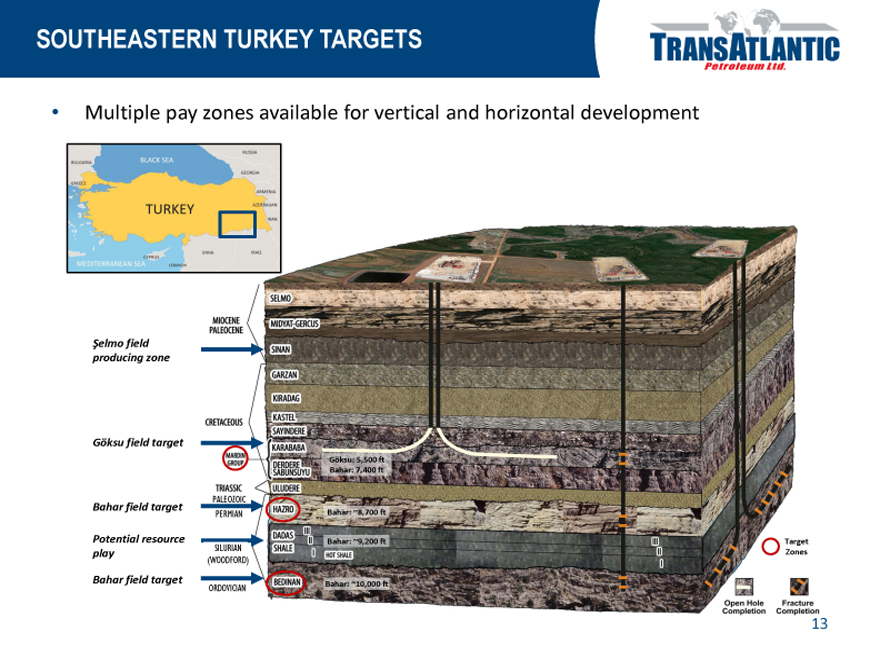

SOUTHEASTERN TURKEY TARGETS

Multiple pay zones available for vertical and horizontal development

Şelmo field producing zone

Göksu field target

Bahar field target

Potential resource play

Bahar field target

MIOCENE

PALEOCENE

CRETACEOUS

MARDIN

GROUP

TRIASSIC

PALEOZOIC

PERMIAN

SILURIAN

(WOODFORD)

ORDOVICIAN

SELMO

MIDYAT-GERCUS

SINAN

GARZAN

KIRADAG

KASTEL

SAYINDERE

KARABABA

DERDERE

SABUNSUYU

ULUDERE

HAZRO

DADAS

SHALE

BEDINAN

HOT SHALE

Göksu: 5,500 ft

Bahar: 7,400 ft

PERMIAN

Bahar: ~8,700 ft

Bahar: ~9,200 ft

Bahar: ~10,000 ft

Target Zones

Open Hole Completion

Fracture Completion

13

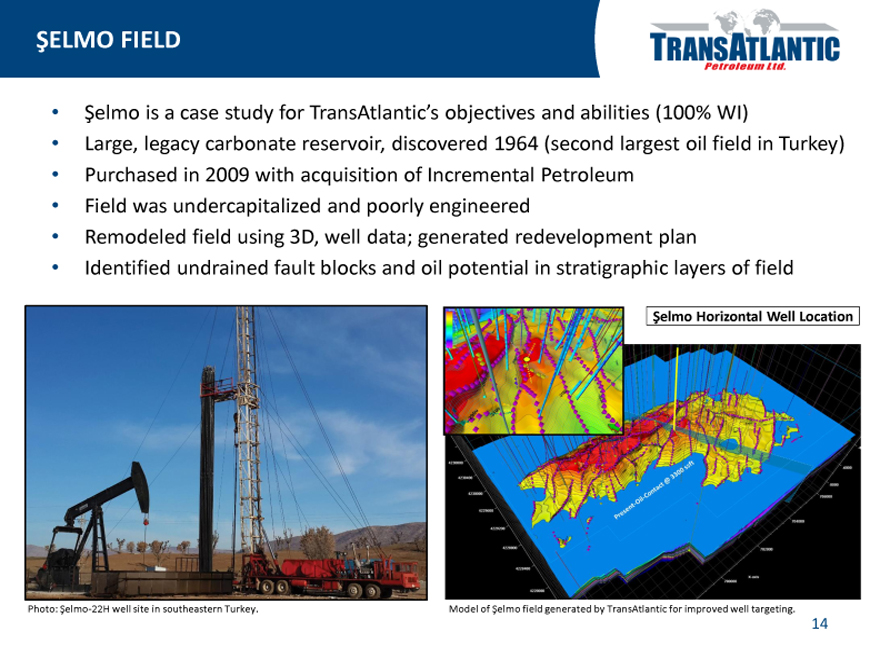

ŞELMO FIELD

Şelmo is a case study for TransAtlantic’s objectives and abilities (100% WI)

Large, legacy carbonate reservoir, discovered 1964 (second largest oil field in Turkey) Purchased in 2009 with acquisition of Incremental Petroleum Field was undercapitalized and poorly engineered Remodeled field using 3D, well data; generated redevelopment plan Identified undrained fault blocks and oil potential in stratigraphic layers of field

Şelmo Horizontal Well Location

Photo: Şelmo-22H well site in southeastern Turkey.

Model of Şelmo field generated by TransAtlantic for improved well targeting.

14

ŞELMO FIELD – 3D SEISMIC CROSS SECTION

Geophysical team has recently determined how seismic attributes point to oil locations, giving us the ability to drill in more precise locations

Areas of high oil saturation lead to booking additional locations

Intend to test same technique on deeper zones – Lower Sinan Limestone (LSL) and Lower Sinan Dolomite (LSD)

Example – proposed trajectory for Selmo-39H2:

Proposed 1,500-foot lateral

High oil saturation

Low oil saturation

15

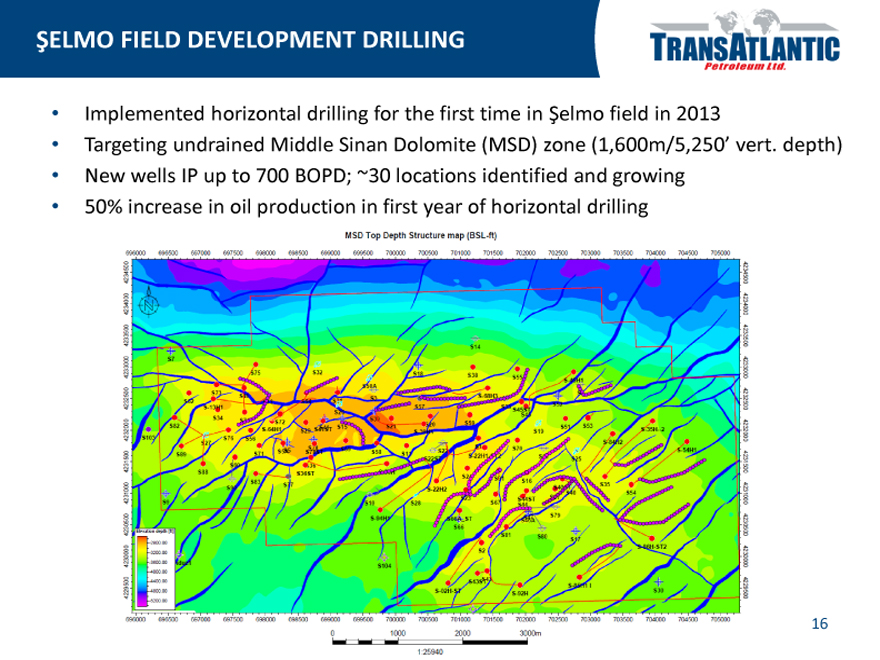

ŞELMO FIELD DEVELOPMENT DRILLING

Implemented horizontal drilling for the first time in Şelmo field in 2013

Targeting undrained Middle Sinan Dolomite (MSD) zone (1,600m/5,250’ vert. depth) New wells IP up to 700 BOPD; ~30 locations identified and growing 50% increase in oil production in first year of horizontal drilling

MSD Top Depth Structure map (BSL-ft)

16

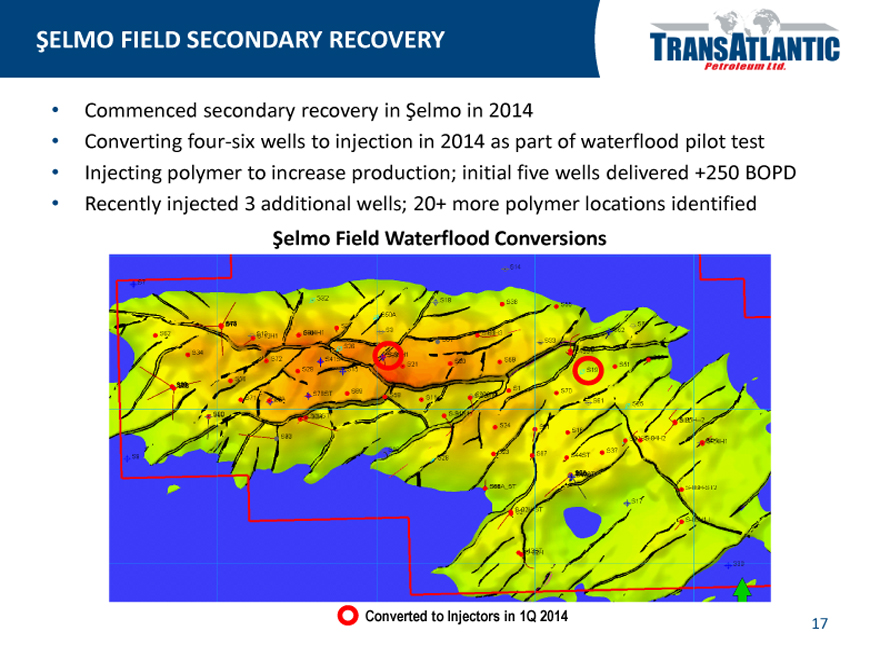

ŞELMO FIELD SECONDARY RECOVERY

Commenced secondary recovery in Şelmo in 2014

Converting four-six wells to injection in 2014 as part of waterflood pilot test Injecting polymer to increase production; initial five wells delivered +250 BOPD Recently injected 3 additional wells; 20+ more polymer locations identified

Şelmo Field Waterflood Conversions

Converted to Injectors in 1Q 2014

17

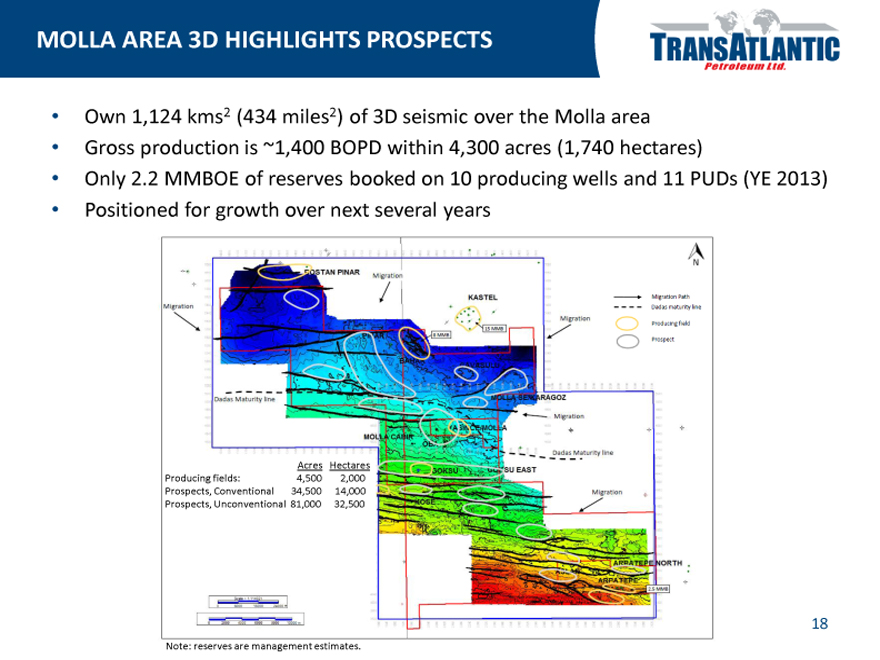

MOLLA AREA 3D HIGHLIGHTS PROSPECTS

Own 1,124 kms2 (434 miles2) of 3D seismic over the Molla area Gross production is ~1,400 BOPD within 4,300 acres (1,740 hectares)

Only 2.2 MMBOE of reserves booked on 10 producing wells and 11 PUDs (YE 2013) Positioned for growth over next several years

Acres Hectares

Producing fields: 4,500 2,000

Prospects, Conventional 34,500 14,000

Prospects, Unconventional 81,000 32,500

Note: reserves are management estimates.

18

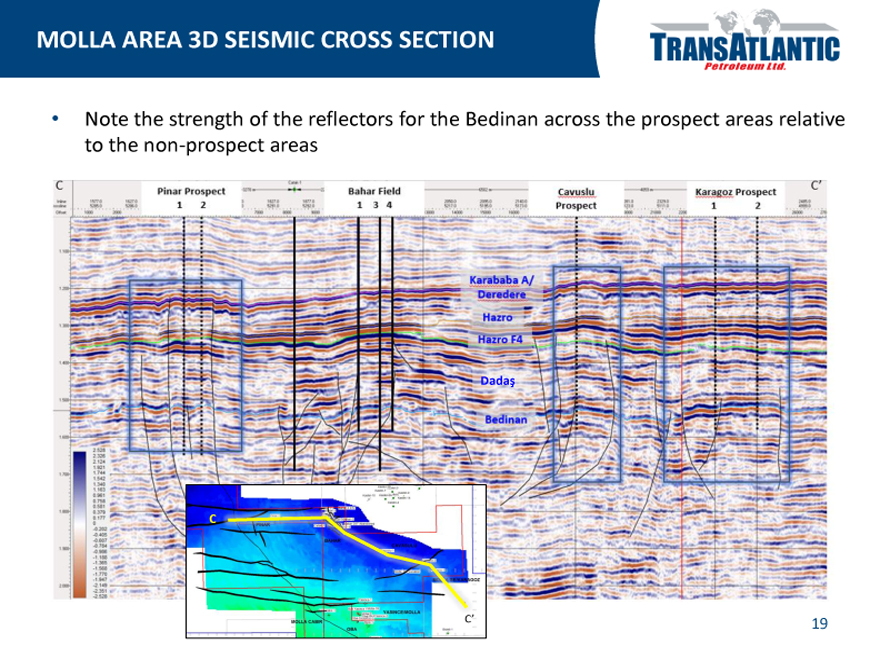

MOLLA AREA 3D SEISMIC CROSS SECTION

Note the strength of the reflectors for the Bedinan across the prospect areas relative to the non-prospect areas

19

ALBANIAN OIL FIELDS

Gorisht Field

Discovered 1965, 25,000 BOPD peak

13 – 16 degree API, 3,000 net acres (1,214 hectares)

Currently producing from ~150 wells: ~800 BOPD gross, ~400 BOPD net1

Depth: 1,000 – 2,500 meters (3,300 – 8,200 feet)

Producing formations: Cretaceous, Eocene carbonates

Cakran Field

Discovered 1978, 6,000 BOPD peak

14 – 37 degree API, condensates 53 degree API

6,000 net acres (2,428 hectares)

Currently producing from ~30 wells: ~625 BOPD gross, ~500 BOPD net1

Depth: 3,000 – 4,500 meters (9,800 – 15,000 feet)

Ballsh Field

Discovered 1967, 7,500 BOPD peak

12 – 24 degree API, 6,000 net acres (2,428 hectares)

Currently producing from ~15 wells: ~100 BOPD gross, ~75 BOPD net1

Depth: 1,000 – 3,000 meters (3,300 – 9,800 feet)

Producing formations: Cretaceous, Eocene carbonates

Photo: Gorisht field in Albania.

1 Production is for the three months ended May 31, 2014. Source: Stream Oil & Gas.

Note: On September 3, 2014, TransAtlantic announced it entered into an agreement to merge with Stream Oil & Gas Ltd. The Boards of Directors of both companies have approved the transaction, but the merger is conditioned upon, among other things, the affirmative vote of at least 66 2/3% of the Stream common shares that are voted at the November 12, 2014 shareholder meeting that will be held to consider the merger. The transaction is subject to the receipt of corporate, government, regulatory and court approvals, among other customary closing conditions. The merger is expected to close in November 2014.

20

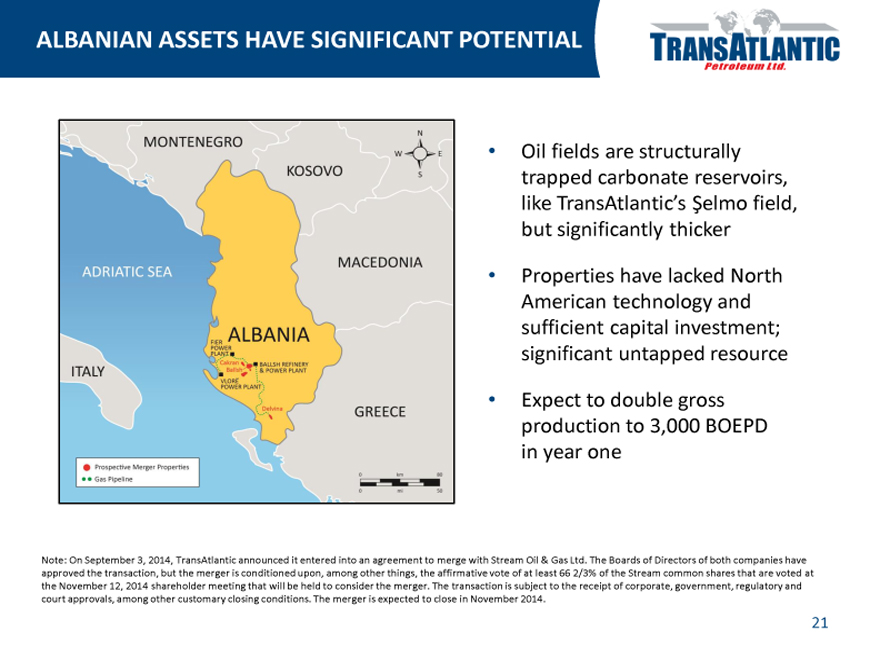

ALBANIAN ASSETS HAVE SIGNIFICANT POTENTIAL

Oil fields are structurally trapped carbonate reservoirs, like TransAtlantic’s Şelmo field, but significantly thicker

Properties have lacked North American technology and sufficient capital investment; significant untapped resource

Expect to double gross production to 3,000 BOEPD in year one

Note: On September 3, 2014, TransAtlantic announced it entered into an agreement to merge with Stream Oil & Gas Ltd. The Boards of Directors of both companies have approved the transaction, but the merger is conditioned upon, among other things, the affirmative vote of at least 66 2/3% of the Stream common shares that are voted at the November 12, 2014 shareholder meeting that will be held to consider the merger. The transaction is subject to the receipt of corporate, government, regulatory and court approvals, among other customary closing conditions. The merger is expected to close in November 2014.

21

SUMMARY OF ALBANIA GROWTH PLAN

Upgrade oilfield technology to optimize field recovery and increase production levels

Drill infill and horizontal oil wells; reactivate wells; initiate waterfloods

Optimize wells with recompletions and workover activity; upgrade pumps on existing wells, introduce artificial lift systems, re-enter and clean out legacy wells, introduce modern stimulation technology, utilize casinghead gas for onsite power generation

Modify infrastructure; increase port storage facilities to decrease transport costs, debottleneck surface production facilities

Photo: Gorisht field in Albania, primary development area.

Note: On September 3, 2014, TransAtlantic announced it entered into an agreement to merge with Stream Oil & Gas Ltd. The Boards of Directors of both companies have approved the transaction, but the merger is conditioned upon, among other things, the affirmative vote of at least 66 2/3% of the Stream common shares that are voted at the November 12, 2014 shareholder meeting that will be held to consider the merger. The transaction is subject to the receipt of corporate, government, regulatory and court approvals, among other customary closing conditions. The merger is expected to close in November 2014.

22

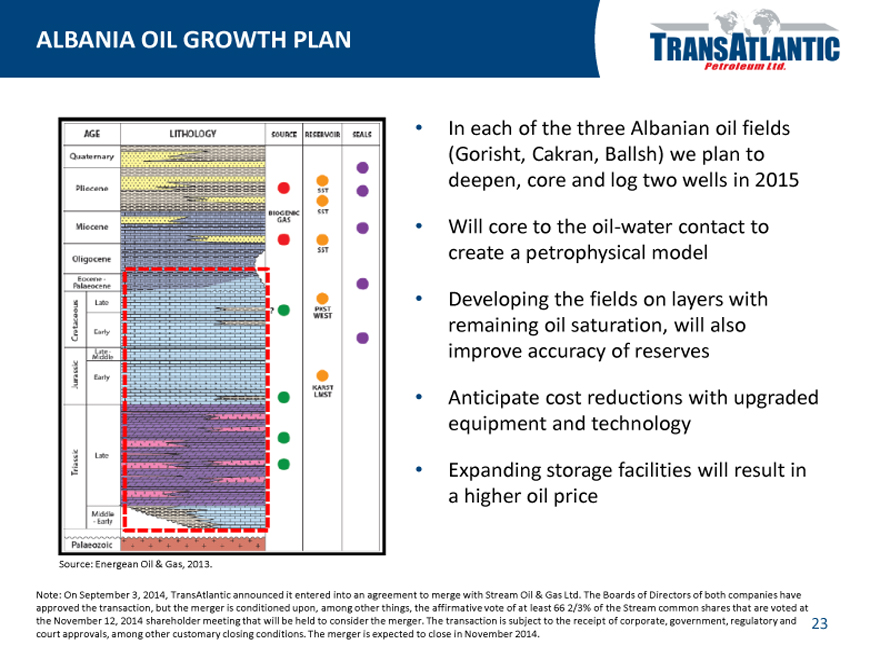

ALBANIA OIL GROWTH PLAN

In each of the three Albanian oil fields (Gorisht, Cakran, Ballsh) we plan to deepen, core and log two wells in 2015

Will core to the oil-water contact to create a petrophysical model

Developing the fields on layers with remaining oil saturation, will also improve accuracy of reserves

Anticipate cost reductions with upgraded equipment and technology

Expanding storage facilities will result in a higher oil price

Source: Energean Oil & Gas, 2013.

Note: On September 3, 2014, TransAtlantic announced it entered into an agreement to merge with Stream Oil & Gas Ltd. The Boards of Directors of both companies have approved the transaction, but the merger is conditioned upon, among other things, the affirmative vote of at least 66 2/3% of the Stream common shares that are voted at the November 12, 2014 shareholder meeting that will be held to consider the merger. The transaction is subject to the receipt of corporate, government, regulatory and court approvals, among other customary closing conditions. The merger is expected to close in November 2014.

23

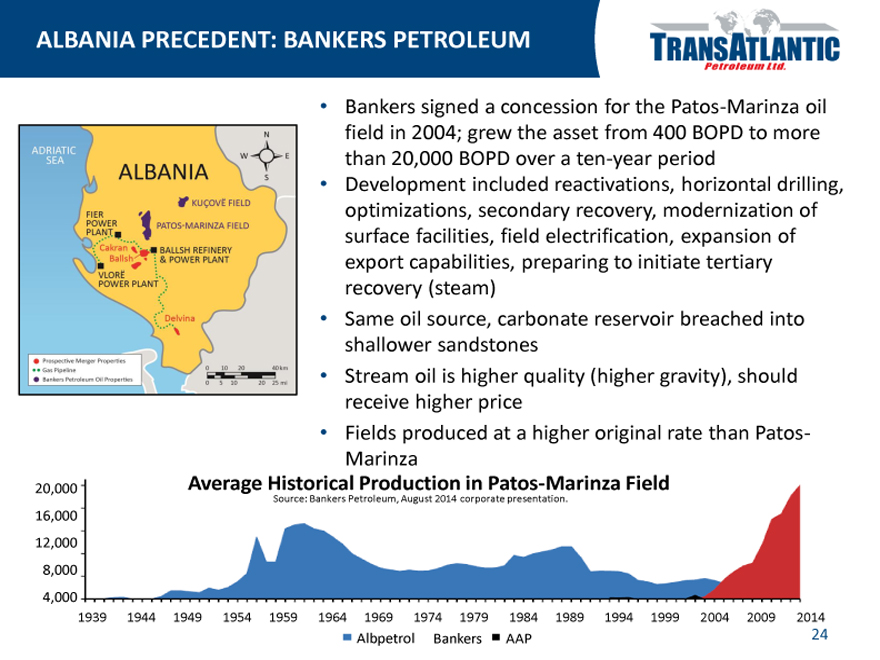

ALBANIA PRECEDENT: BANKERS PETROLEUM

Bankers signed a concession for the Patos-Marinza oil field in 2004; grew the asset from 400 BOPD to more than 20,000 BOPD over a ten-year period

Development included reactivations, horizontal drilling, optimizations, secondary recovery, modernization of surface facilities, field electrification, expansion of export capabilities, preparing to initiate tertiary recovery (steam)

Same oil source, carbonate reservoir breached into shallower sandstones

Stream oil is higher quality (higher gravity), should receive higher price

Fields produced at a higher original rate than Patos-Marinza

Average Historical Production in Patos-Marinza Field

Source: Bankers Petroleum, August 2014 corporate presentation.

20,000 16,000 12,000 8,000 4,000

1939 1944 1949 1954 1959 1964 1969 1974 1979 1984 1989 1994 1999 2004 2009 2014

Albpetrol Bankers AAP

ALBANIA

ADRIATIC SEA

24

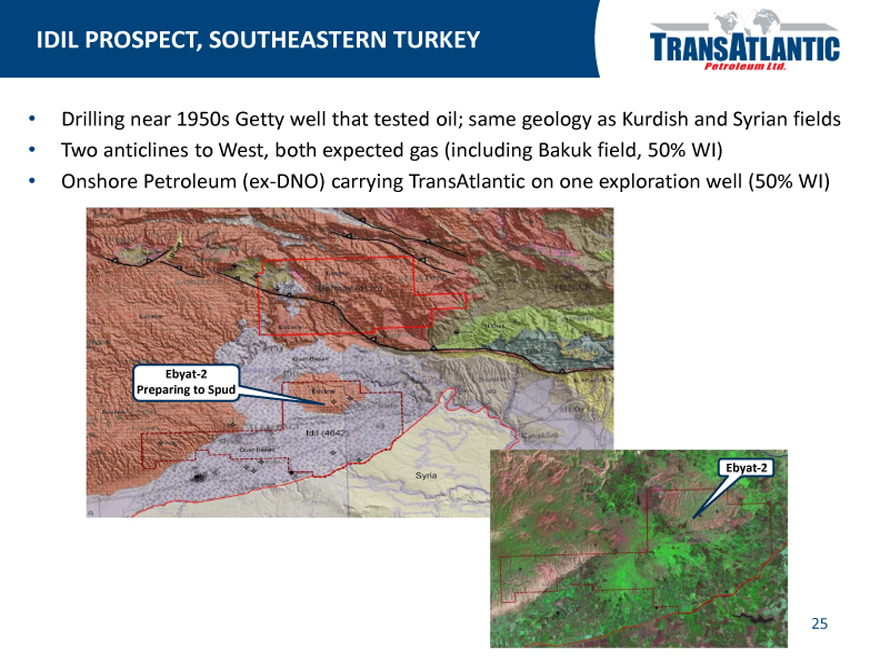

IDIL PROSPECT, SOUTHEASTERN TURKEY

Drilling near 1950s Getty well that tested oil; same geology as Kurdish and Syrian fields Two anticlines to West, both expected gas (including Bakuk field, 50% WI) Onshore Petroleum (ex-DNO) carrying TransAtlantic on one exploration well (50% WI)

Ebyat-2

Preparing to Spud

Ebyat-2

25

NATURAL GAS ASSETS

James Huling – Chief Operating Officer

Top Value Generators YE 2014

1. Thrace Basin, Turkey

2. Bakuk Field, Turkey

3. Delvina Field, Albania

4. Koynare Concession, Bulgaria

Expected Top Value Generators 2016

1. Delvina Field, Albania

2. Thrace Basin, Turkey

3. Koynare Concession, Bulgaria

4. Bakuk Field, Turkey

26

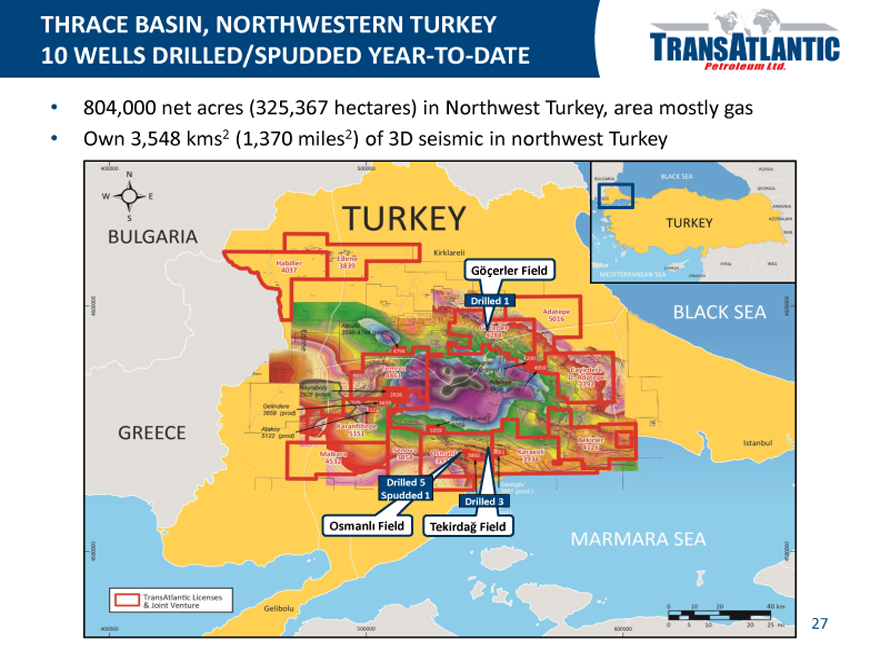

THRACE BASIN, NORTHWESTERN TURKEY

10 WELLS DRILLED/SPUDDED YEAR-TO-DATE

804,000 net acres (325,367 hectares) in Northwest Turkey, area mostly gas Own 3,548 kms2 (1,370 miles2) of 3D seismic in northwest Turkey

Göçerler Field

Drilled 1

Drilled 5 Spudded 1

Drilled 3

Osmanli Field Tekirdağ Field

TURKEY

BLACK SEA

MARMARA SEA

BULGARIA

GREECE

27

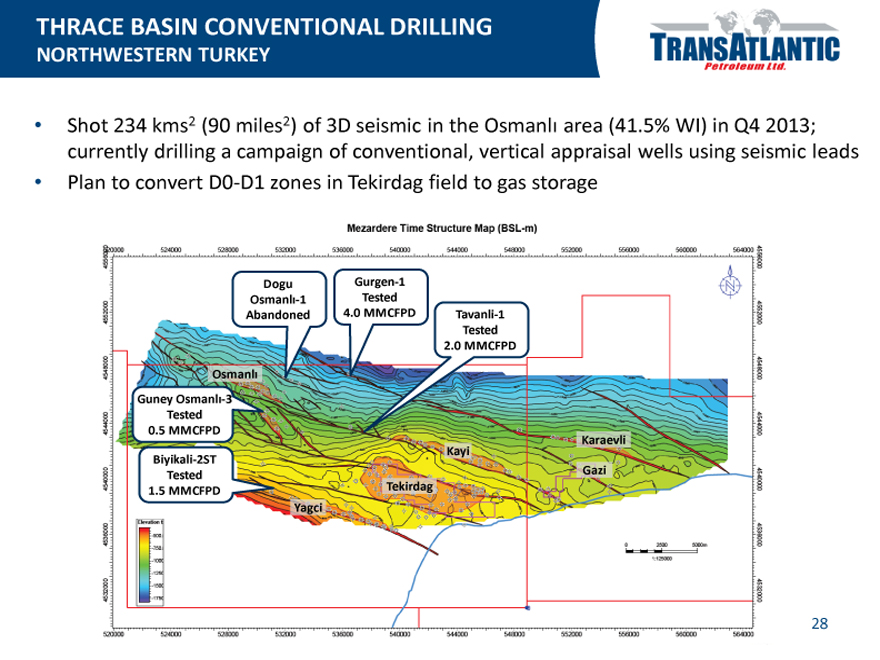

THRACE BASIN CONVENTIONAL DRILLING

NORTHWESTERN TURKEY

Shot 234 kms2 (90 miles2) of 3D seismic in the Osmanli area (41.5% WI) in Q4 2013; currently drilling a campaign of conventional, vertical appraisal wells using seismic leads Plan to convert D0-D1 zones in Tekirdag field to gas storage

Dogu Gurgen-1

Osmanli-1 Tested

Abandoned 4.0 MMCFPD Tavanli-1

Tested

2.0 MMCFPD

Osmanli

Guney Osmanli-3

Tested

0.5 MMCFPD Karaevli Kayi Biyikali-2ST

Tested Gazi

1.5 MMCFPD Tekirdag Yagci

Mezardere Time Structure Map (BSL-m)

28

THRACE BASIN HORIZONTAL DRILLING

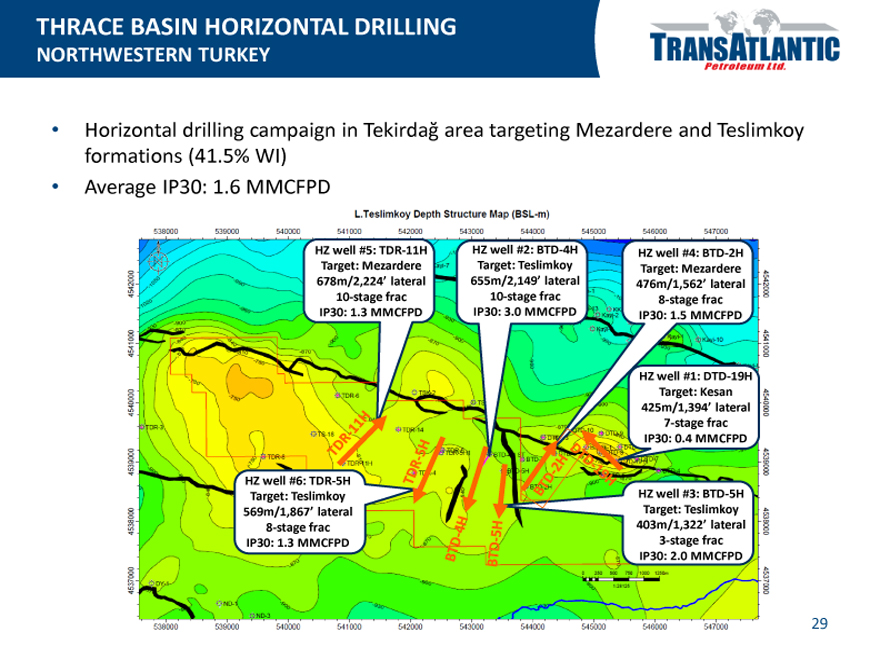

NORTHWESTERN TURKEY

Horizontal drilling campaign in Tekirdağ area targeting Mezardere and Teslimkoy formations (41.5% WI) Average IP30: 1.6 MMCFPD

HZ well #5: TDR-11H

Target: Mezardere

678m/2,224’ lateral

10-stage frac IP30: 1.3 MMCFPD

HZ well #2: BTD-4H

Target: Teslimkoy

655m/2,149’ lateral

10-stage frac

IP30: 3.0 MMCFPD

HZ well #4: BTD-2H Target: Mezardere

476m/1,562’ lateral

8-stage frac IP30: 1.5 MMCFPD

HZ well #1: DTD-19H Target: Kesan

425m/1,394’ lateral

7-stage frac

IP30: 0.4 MMCFPD

HZ well #3: BTD-5H

Target: Teslimkoy

403m/1,322’ lateral

3-stage frac

IP30: 2.0 MMCFPD

HZ well #6: TDR-5H Target: Teslimkoy

569m/1,867’ lateral

8-stage frac IP30: 1.3 MMCFPD

L. Teslimkoy Depth Structure Map (BSL-m)

29

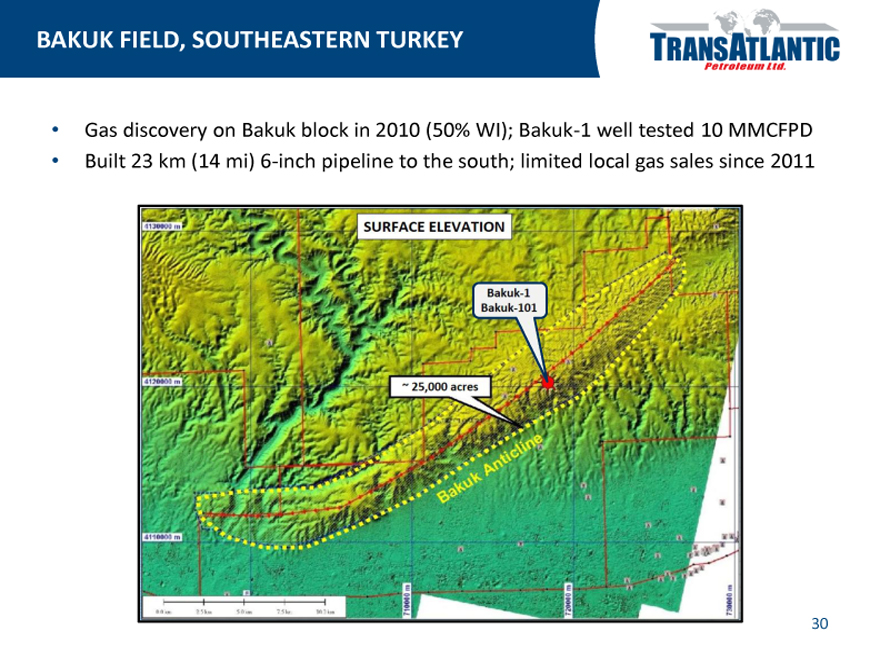

BAKUK FIELD, SOUTHEASTERN TURKEY

Gas discovery on Bakuk block in 2010 (50% WI); Bakuk-1 well tested 10 MMCFPD Built 23 km (14 mi) 6-inch pipeline to the south; limited local gas sales since 2011

SURFACE ELEVATION

Bakuk-1

Bakuk-101

~25,000 acres

30

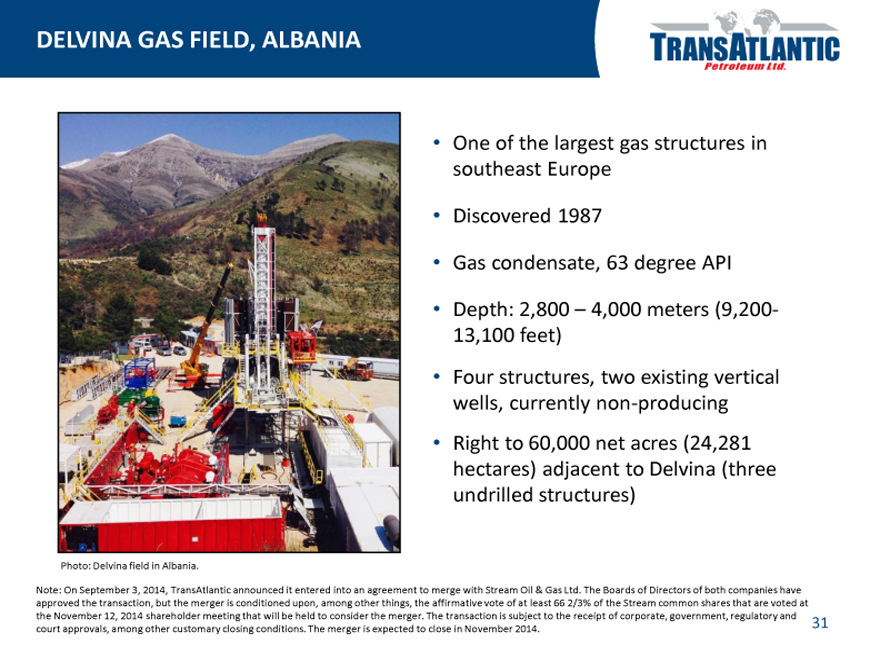

DELVINA GAS FIELD, ALBANIA

One of the largest gas structures in southeast Europe

Discovered 1987

Gas condensate, 63 degree API

Depth: 2,800 – 4,000 meters (9,200-13,100 feet)

Four structures, two existing vertical wells, currently non-producing

Right to 60,000 net acres (24,281 hectares) adjacent to Delvina (three undrilled structures)

Photo: Delvina field in Albania.

Note: On September 3, 2014, TransAtlantic announced it entered into an agreement to merge with Stream Oil & Gas Ltd. The Boards of Directors of both companies have approved the transaction, but the merger is conditioned upon, among other things, the affirmative vote of at least 66 2/3% of the Stream common shares that are voted at the November 12, 2014 shareholder meeting that will be held to consider the merger. The transaction is subject to the receipt of corporate, government, regulatory and court approvals, among other customary closing conditions. The merger is expected to close in November 2014.

31

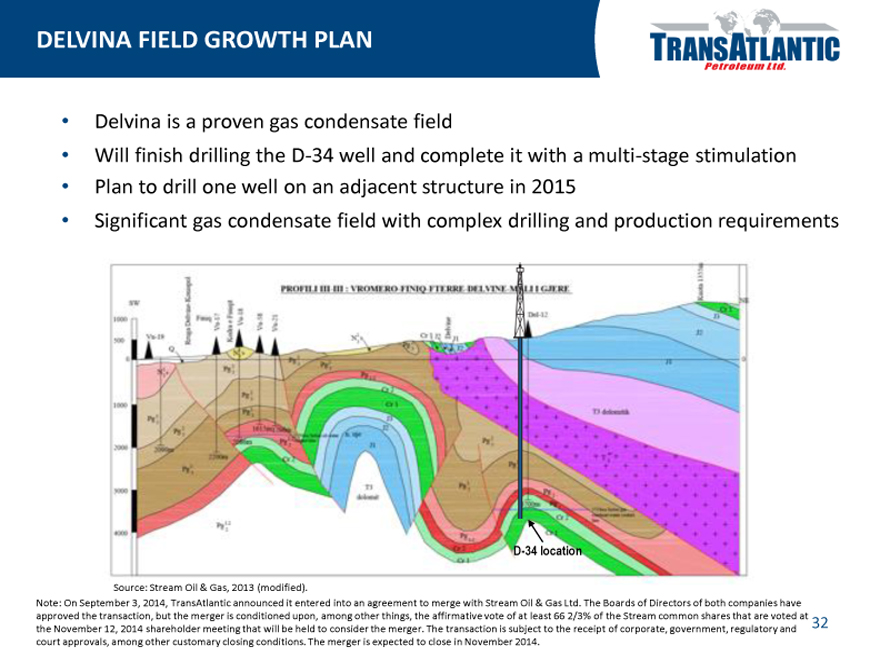

DELVINA FIELD GROWTH PLAN

Delvina is a proven gas condensate field

Will finish drilling the D-34 well and complete it with a multi-stage stimulation Plan to drill one well on an adjacent structure in 2015 Significant gas condensate field with complex drilling and production requirements

D-34 location

Source: Stream Oil & Gas, 2013 (modified).

Note: On September 3, 2014, TransAtlantic announced it entered into an agreement to merge with Stream Oil & Gas Ltd. The Boards of Directors of both companies have approved the transaction, but the merger is conditioned upon, among other things, the affirmative vote of at least 66 2/3% of the Stream common shares that are voted at the November 12, 2014 shareholder meeting that will be held to consider the merger. The transaction is subject to the receipt of corporate, government, regulatory and court approvals, among other customary closing conditions. The merger is expected to close in November 2014.

32

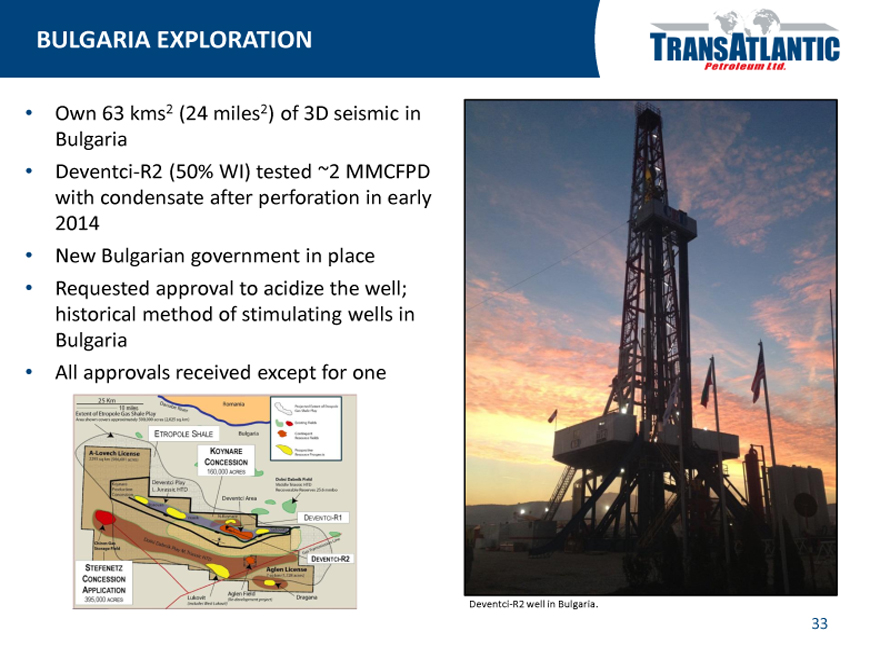

BULGARIA EXPLORATION

Own 63 kms2 (24 miles2) of 3D seismic in Bulgaria Deventci-R2 (50% WI) tested ~2 MMCFPD with condensate after perforation in early 2014 New Bulgarian government in place Requested approval to acidize the well; historical method of stimulating wells in Bulgaria All approvals received except for one

Deventci-R2 well in Bulgaria.

33

MARKET PERFORMANCE TRANSACTION VALUE

Dr. Sotiris Kapotas –

President & CEO, Stream Oil & Gas

34

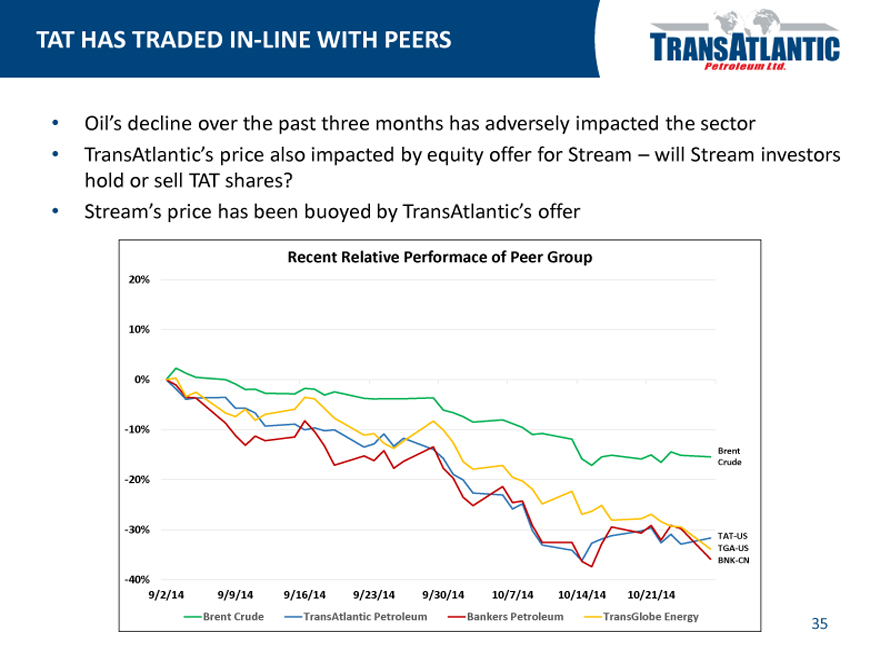

TAT HAS TRADED IN-LINE WITH PEERS

Oil’s decline over the past three months has adversely impacted the sector

TransAtlantic’s price also impacted by equity offer for Stream – will Stream investors hold or sell TAT shares

Stream’s price has been buoyed by TransAtlantic’s offer

Recent Relative Performace of Peer Group

20% 10% 0%

-10%

Brent Crude

-20%

-30%

TAT-US TGA-US BNK-CN

-40%

9/2/14 9/9/14 9/16/14 9/23/14 9/30/14 10/7/14 10/14/14 10/21/14

Brent Crude TransAtlantic Petroleum Bankers Petroleum TransGlobe Energy

35

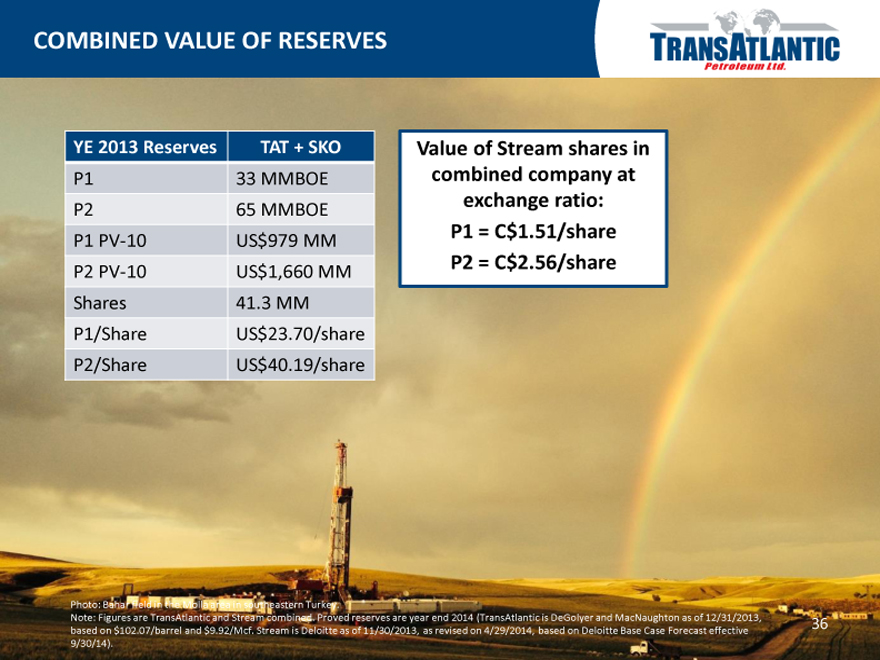

COMBINED VALUE OF RESERVES

YE 2013 Reserves TAT + SKO

P1 33 MMBOE

P2 65 MMBOE

P1 PV-10 US$979 MM

P2 PV-10 US$1,660 MM

Shares 41.3 MM

P1/Share US$23.70/share

P2/Share US$40.19/share

Value of Stream shares in combined company at exchange ratio: P1 = C$1.51/share P2 = C$2.56/share

Photo: Bahar field in the Molla area in southeastern Turkey.

Note: Figures are TransAtlantic and Stream combined. Proved reserves are year end 2014 (TransAtlantic is DeGolyer and MacNaughton as of 12/31/2013, based on $102.07/barrel and $9.92/Mcf. Stream is Deloitte as of 11/30/2013, as revised on 4/29/2014, based on Deloitte Base Case Forecast effective 9/30/14).

36

WHY STREAM SHOULD MERGE WITH

TRANSATLANTIC

Merger will result in an experienced, diversified oil and gas company

Advantages of scale together, expect to grow beyond 10,000 BOEPD much sooner

Working with an experienced operator who sees potential in Albania properties, with a plan and the demonstrated ability to increase their asset value

Management is successfully developing similar assets in the region

Combined company will have improved access to high quality, low cost services

Owning shares of combined company gives Stream investors access to upside potential in Turkey, Albania and Bulgaria

Photo: Bahar field in southeastern Turkey.

37

CONTACTS

Taylor Beach

Director of Investor Relations (214) 265-4746 Taylor.Beach@tapcor.com

Matt

McCann

Gen.

Counsel

& Corp. Secretary

(214)

220-4323

www.TransAtlanticPetroleum.com

38

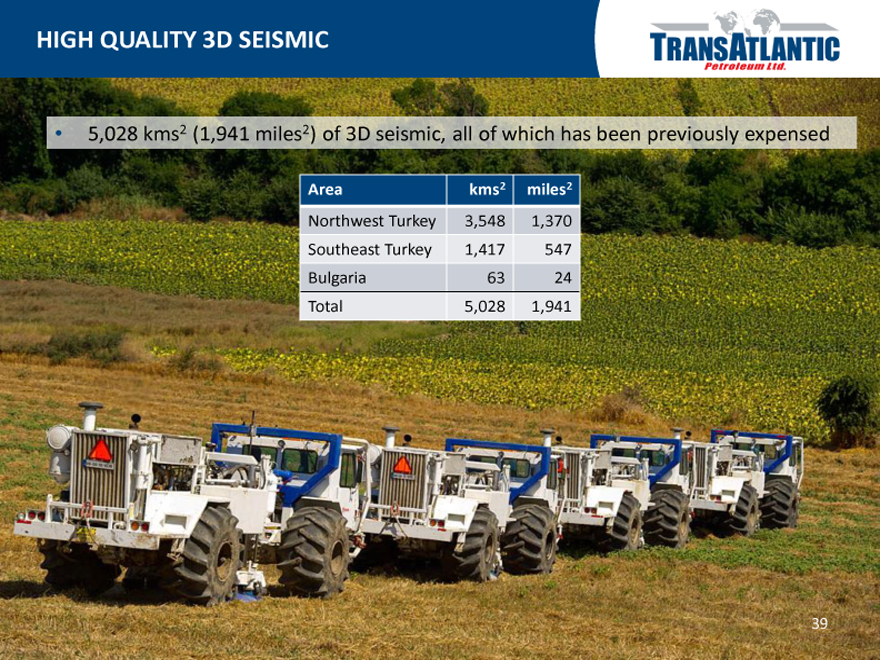

HIGH QUALITY 3D SEISMIC

5,028 kms2 (1,941 miles2) of 3D seismic, all of which has been previously expensed

Area kms2 miles2

Northwest Turkey 3,548 1,370

Southeast Turkey 1,417 547

Bulgaria 63 24

Total 5,028 1,941

39

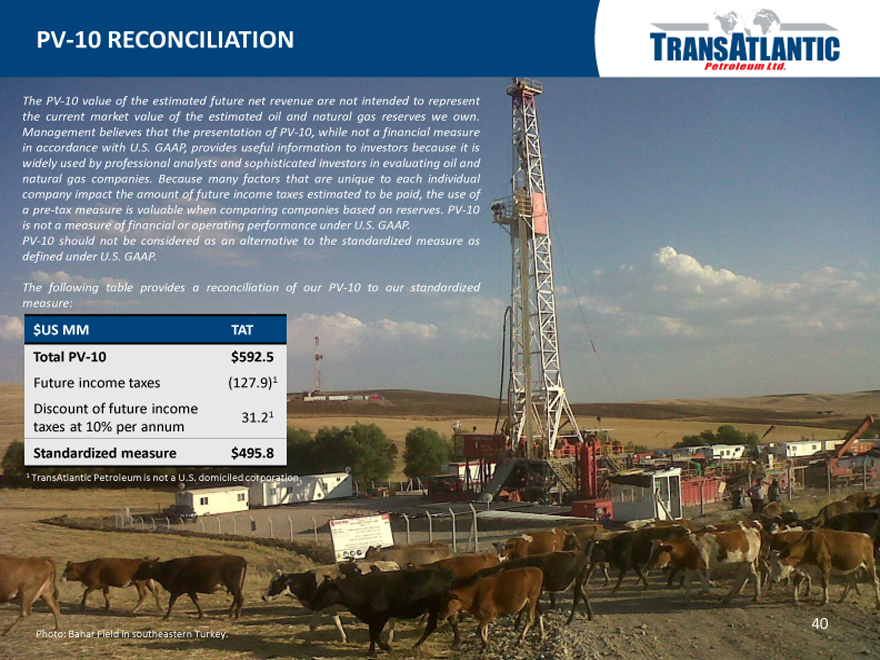

PV-10 RECONCILIATION

The PV-10 value of the estimated future net revenue are not intended to represent the current market value of the estimated oil and natural gas reserves we own.

Management believes that the presentation of PV-10, while not a financial measure in accordance with U.S. GAAP, provides useful information to investors because it is widely used by professional analysts and sophisticated investors in evaluating oil and natural gas companies. Because many factors that are unique to each individual company impact the amount of future income taxes estimated to be paid, the use of a pre-tax measure is valuable when comparing companies based on reserves. PV-10 is not a measure of financial or operating performance under U.S. GAAP.

PV-10 should not be considered as an alternative to the standardized measure as defined under U.S. GAAP.

The following table provides a reconciliation of our PV-10 to our standardized measure:

$US MM TAT

Total PV-10 $592.5

Future income taxes (127.9)1

Discount of future income 31.21

taxes at 10% per annum

Standardized measure $495.8

1 TransAtlantic Petroleum is not a U.S. domiciled corporation.

Photo: Bahar Field in southeastern Turkey.

40