ZENITH NATIONAL INSURANCE CORP. 2005

ANNUAL REPORT

2005

FINANCIAL HIGHLIGHTS

Year Ended December 31,

| | 2005

| | 2004

| | 2003

|

|

|---|

|

|---|

RESULTS OF OPERATIONS: |

|

|

(Dollars in thousands, except per share data) |

|

| Total revenues | | $ | 1,280,124 | | $ | 1,044,880 | | $ | 849,335 | |

| Net investment income after tax | | | 53,358 | | | 42,265 | | | 37,966 | |

| Realized gains on investments after tax | | | 14,446 | | | 24,726 | | | 12,631 | |

Income from continuing operations after tax |

|

$ |

156,447 |

|

$ |

117,714 |

|

$ |

65,846 |

|

| Gain on sale of discontinued real estate segment after tax (1) | | | 1,253 | | | 1,286 | | | 1,154 | |

| | |

| |

| |

| |

| Net income | | $ | 157,700 | | $ | 119,000 | | $ | 67,000 | |

| | |

| |

| |

| |

PER SHARE DATA: (2)(3) |

|

|

|

|

|

|

|

|

|

|

| Income from continuing operations after tax | | $ | 4.29 | | $ | 3.35 | | $ | 2.04 | |

| Gain on sale of discontinued real estate segment after tax (1) | | | 0.03 | | | 0.03 | | | 0.03 | |

| | |

| |

| |

| |

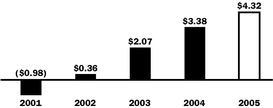

| Net income | | $ | 4.32 | | $ | 3.38 | | $ | 2.07 | |

| | |

| |

| |

| |

| Cash dividends declared per common share | | $ | 0.94 | | $ | 0.75 | | $ | 0.67 | |

KEY STATISTICS: |

|

|

|

|

|

|

|

|

|

|

| Underwriting income (loss) before tax (4): | | | | | | | | | | |

| Workers' compensation | | $ | 213,244 | | $ | 104,098 | | $ | 29,260 | |

| Reinsurance | | | (56,183 | ) | | (11,956 | ) | | 9,562 | |

| Combined ratios (5): | | | | | | | | | | |

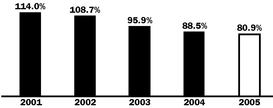

| Workers' compensation | | | 80.9 | % | | 88.5 | % | | 95.9% | |

| Reinsurance | | | 187.1 | % | | 128.2 | % | | 84.3% | |

| Stockholders' equity | | $ | 712,795 | | $ | 502,147 | | $ | 383,246 | |

| Stockholders' equity per share (3) | | | 19.14 | | | 17.28 | | | 13.51 | |

| Closing common stock price (3) | | | 46.12 | | | 33.23 | | | 21.70 | |

(1) In 2002, we sold our home-building business and related real estate assets. Gains of $1.9 million, $2.0 million and $1.8 million before tax ($1.3 million, $1.3 million and $1.2 million after tax) were recorded from additional sales proceeds received in 2005, 2004 and 2003, respectively, under the earn-out provision of the sale. The last such payment under the earn-out provision was received in 2005.

(2) Diluted per share amounts reflect the impact of additional shares issuable in connection with Zenith's 5.75% Convertible Senior Notes.

(3) All per share amounts and stock prices throughout this annual report reflect the 3-for-2 stock split distributed on October 11, 2005.

(4) Underwriting income (loss) before tax from the workers' compensation and reinsurance segments is determined by deducting net loss and loss adjustment expenses incurred and underwriting and other operating expenses incurred from net premiums earned.

(5) The combined ratio, expressed as a percentage, is a key measurement of profitability traditionally used in the property-casualty insurance industry. The combined ratio is the sum of the loss and loss adjustment expense ratio and the underwriting and other operating expense ratio. The loss and loss adjustment expense ratio is the percentage of net incurred loss and loss adjustment expenses to net premiums earned. The underwriting and other operating expense ratio is the percentage of underwriting and other operating expenses to net premiums earned. The key operating goal for our insurance segments is to achieve a combined ratio of 100% or lower and to achieve a workers' compensation combined ratio that is at least three percentage points lower than the combined ratio of the national workers' compensation industry.

1

TABLE OF CONTENTS

• |

Letter to Stockholders |

|

3 |

• |

Management's Discussion and Analysis of Consolidated

Financial Condition and Results of Operations |

|

24 |

• |

5-Year Summary of Selected Financial Information |

|

50 |

• |

Consolidated Balance Sheets |

|

52 |

• |

Consolidated Statements of Operations |

|

53 |

• |

Consolidated Statements of Cash Flows |

|

54 |

• |

Consolidated Statements of Stockholders' Equity and Consolidated Statements of Comprehensive Income |

|

56 |

• |

Notes to Consolidated Financial Statements |

|

57 |

• |

Report of Independent Registered Public Accounting Firm |

|

87 |

• |

Certifications and Management's Report on Internal Controls over Financial Reporting |

|

89 |

• |

Corporate Directory |

|

|

|

Zenith National Insurance Corp. |

|

94 |

|

Zenith Insurance Company |

|

95 |

|

Zenith Marketing, Underwriting and Claims Offices |

|

96 |

TheZenith and Zenith are registered U.S. trademarks.

2

TO OUR STOCKHOLDERS

Zenith improved its financial strength and generated record revenues and earnings during 2005, despite the negative impact on our results caused by hurricane losses. Net income was $4.32 per share, including $1.25 of hurricane losses.

We report in two insurance business segments: workers' compensation and reinsurance. Workers' compensation trends continue favorable with substantial underwriting profits and cash flow for investment. Reinsurance operations lost money due to the hurricanes and as a result, we have exited this business.

Zenith's investment portfolio increased from $1.9 billion to $2.2 billion, including cash, treasury bills and United States government securities maturing in two years or less in the amount of approximately $1.2 billion at year-end. This liquidity together with our cash flow provides additional investment income opportunities.

Our financial strength was significantly improved due to our earnings, the conversion of $123.8 million of convertible debt into common stock and our loss reserving data.

We approach the New Year with optimism because we believe our specialist workers' compensation experience and service strategy will continue to support favorable results for our insureds, claimants and shareholders alike. Zenith's staff is committed to managing risk in a professional manner, and as a new initiative, we plan to implement a major focus on upgrading and providing, where possible, the highest quality healthcare services for seriously injured claimants.

With regard to corporate governance, we believe our controls are excellent and our disclosures provide full transparency.

This report will discuss current trends as well as our future challenges and opportunities.

3

NET INCOME IN 2005 WAS $157.7 MILLION, OR $4.32 PER SHARE, COMPARED TO $119.0 MILLION, OR $3.38 PER SHARE IN 2004.

FINANCIAL SUMMARY

Net income + 33%

Investment income + 28%

Workers' Compensation Combined Ratio 80.9%

Stockholders' Equity + 42%

- 1.

- Workers' Compensation Segment:

- •

- Income was $213.2 million compared to $104.1 million in 2004.

- •

- Combined ratio improved to 80.9% from 88.5% in 2004.

- •

- Industry combined ratio for 2005 estimated at 106.2% by A.M. Best Company.

- •

- Premiums written increased 6% to $1,139.3 million.

- •

- Premiums in-force increased 1% to about $1,049.8 million.

- •

- Rates are adequate and are trending downward as are claim costs.

- 2.

- Reinsurance Segment:

- •

- Combined ratio 187.1%.

- •

- Underwriting loss $56.2 million.

- •

- Discontinued business.

- 3.

- Additional Financial Strength:

- •

- Cash flow from operating activities was $344.9 million in 2005 compared to $345.9 million the prior year.

- •

- Debt to debt and equity ratio of 8%.

- •

- Market capitalization of Zenith at year-end was $1.7 billion compared to $1.2 billion at December 31, 2004.

4

STOCKHOLDERS' EQUITY PER SHARE

- 4.

- Net income:

- •

- Net income was $157.7 million compared $119.0 million in 2004.

- •

- Net income per diluted share was $4.32 compared to $3.38 the prior year.

- •

- Reinsurance losses due to hurricanes reduced net income by $46.5 million, or $1.25 per share, compared to $18.4 million, or $0.50 per share, the prior year. We have exited this business.

- •

- Return on average equity was 26.3% compared to 27.2% the prior year.

- 5.

- Investments:

- •

- Investment income before tax was $79.2 million in 2005 compared with $61.9 million the prior year.

- •

- Average yield increased due to short portfolio and increases in short-term rates.

- •

- Investment portfolio increased to $2.2 billion in 2005 compared to $1.9 billion in 2004.

- •

- Capital gains before tax in 2005 were $22.2 million compared to $38.6 million the prior year.

- •

- Unrealized portfolio gains were $1.5 million before tax compared to $65.0 million the prior year. The change is due to increased interest rates and realized gains.

ANALYSIS

The following table summarizes pre-tax workers' compensation and reinsurance results during the past three years.

|

|---|

Segment Income (Loss)

| | 2005

| | 2004

| | 2003

|

|---|

|

|---|

| | | | (Dollars in thousands) |

| Workers' Compensation | | $ | 213,244 | | $ | 104,098 | | $ | 29,260 |

| Reinsurance | | | (56,183 | ) | | (11,956 | ) | | 9,562 |

| Catastrophe losses included in Reinsurance segment* | | | (69,200 | ) | | (21,100 | ) | | 0 |

|

| *Additional catastrophe losses in 2005 and 2004 from Advent Capital were $2.3 million and $7.3 million before tax, respectively. |

5

STOCKHOLDERS' EQUITY INCREASED TO $712.8 MILLION COMPARED TO $502.1 MILLION AT DECEMBER 31, 2004.

2005 results improved significantly:

- •

- 2005 combined ratio for the workers' compensation segment was 80.9% compared to 88.5% in 2004.

- •

- Accident year combined ratios for the workers' compensation operations were 83.2%, 77.6% and 85.6% for 2005, 2004 and 2003, respectively.

- •

- Combined ratio for the reinsurance segment was 187.1% in 2005 compared to 128.2% in 2004.

- •

- Gross written insurance premiums were $1.2 billion in 2005 compared to $1.1 billion the prior year, an increase of 8%.

- •

- Investment income after tax was $53.4 million, or $1.44 per share, in 2005 compared to $42.3 million, or $1.15 per share, in 2004.

- •

- Stockholders' equity at December 31, 2005 was $712.8 million compared to $502.1 million at December 31, 2004.

- •

- Net cash flow from operating activities was $344.9 million in 2005 compared to $345.9 million in 2004. Workers' compensation increased year over year by $44.0 million.

- •

- At December 31, 2005, Zenith had long-term debt of $60.2 million compared to $184.0 million the prior year. During the year, $123.8 million of convertible debt was converted into 7.4 million shares of common stock resulting in 37.2 million outstanding shares of common stock at year-end. Earnings per share calculations were not affected by the conversions.

- •

- Zenith's subsidiaries are rated A- (Excellent) by A.M.Best Company. Moody's Investors Service and Standard & Poor's have assigned insurance financial strength ratings of Baa1 (Adequate) and BBB+ (Good), respectively.

- •

- Dividends paid to shareholders were $33.4 million in 2005 compared to $21.5 million in 2004.

- •

- Reserve adequacy strengthened.

6

NET INCOME (LOSS) PER COMMON SHARE

RESERVES

Information in the following table provides estimates of Zenith's net incurred losses and loss adjustment expenses for our workers' compensation and reinsurance segments by accident year, evaluated in the year they were incurred and as they were subsequently evaluated in succeeding years. These data are of critical importance in judging the historical accuracy of our reserve estimates, as well as providing a guide to setting fair prices and rates. The accuracy of reserve estimates is one of our major business risks which we endeavor to manage professionally. Loss reserve estimates are refined continually in an ongoing process as experience develops, new information is obtained and evaluated, and claims are reported and paid. The inflation or deflation trend of paid claim costs compared to the assumptions included in the loss reserve estimates is the most important factor in understanding reserve adequacy. Data from 2003, 2004 and 2005 indicate deflation for the current and recent accident years compared to substantial inflation in prior years. The primary causes of these developments are the California legislative reforms enacted in 2003 and 2004, Florida reforms enacted in 2003, and the long-term trend of declining claim frequency. Due to the relatively small sample of paid claims to estimated total claim costs for 2003, 2004 and 2005, inflation estimates in loss reserves are higher than short-term paid deflation rates, and as more data become available, estimates will be adjusted, as indicated. To the extent that the data continue at low or declining levels, it will help future earnings and our financial strength. For additional information on reserving and inflation trends, the reader should turn to pages 32 to 38 of this report.

Estimating catastrophe losses in the reinsurance business is highly dependent upon the nature and timing of the event and our ability to obtain timely and accurate information with which to estimate our liability to pay losses. There remains uncertainty as to the nature and amount of monetary losses associated with the hurricanes in 2005, although many of our treaties are already reflecting maximum losses from Katrina.

7

RESERVE ADEQUACY IS APPARENT FROM RECENT TRENDS.

|

|---|

Accident Year Reserve Development from Operations

|

|---|

|

|---|

| | Net incurred losses and loss adjustment expenses reported at end of year

|

|---|

|

|---|

Years in which losses were incurred

| | 1999

| | 2000

| | 2001

| | 2002

| | 2003

| | 2004

| | 2005

|

|---|

|

|---|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(Dollars in thousands) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Prior to 1999 | | $ | 3,912,943 | | $ | 3,912,865 | | $ | 3,899,912 | | $ | 3,910,900 | | $ | 3,911,393 | | $ | 3,937,898 | | $ | 3,977,884 |

| 1999 | | | 262,932 | | | 293,890 | | | 306,462 | | | 298,644 | | | 310,080 | | | 306,654 | | | 316,569 |

| Cumulative | | | 4,175,875 | | | 4,206,755 | | | 4,206,374 | | | 4,209,544 | | | 4,221,473 | | | 4,244,552 | | | 4,294,453 |

| 2000 | | | | | | 289,946 | | | 294,674 | | | 304,251 | | | 311,853 | | | 321,447 | | | 326,205 |

| Cumulative | | | | | | 4,496,701 | | | 4,501,048 | | | 4,513,795 | | | 4,533,326 | | | 4,565,999 | | | 4,620,658 |

| 2001 | | | | | | | | | 409,586 | | | 426,007 | | | 437,452 | | | 447,619 | | | 454,475 |

| Cumulative | | | | | | | | | 4,910,634 | | | 4,939,802 | | | 4,970,778 | | | 5,013,618 | | | 5,075,133 |

| 2002 | | | | | | | | | | | | 391,960 | | | 375,199 | | | 397,817 | | | 413,764 |

| Cumulative | | | | | | | | | | | | 5,331,762 | | | 5,345,977 | | | 5,411,435 | | | 5,488,897 |

| 2003 | | | | | | | | | | | | | | | 523,707 | | | 471,615 | | | 443,744 |

| Cumulative | | | | | | | | | | | | | | | 5,869,684 | | | 5,883,050 | | | 5,932,641 |

| 2004 | | | | | | | | | | | | | | | | | | 615,397 | | | 538,906 |

| Cumulative | | | | | | | | | | | | | | | | | | 6,498,447 | | | 6,471,547 |

| 2005 | | | | | | | | | | | | | | | | | | | | | 730,770 |

| Cumulative | | | | | | | | | | | | | | | | | | | | | 7,202,317 |

| Loss and loss adjustment expense ratios: | | | | | | | | | | | | | | | | | | |

| 1999 | | | 83.4% | | | 93.2% | | | 97.2% | | | 94.7% | | | 98.3% | | | 97.3% | | | 100.4% |

| 2000 | | | | | | 85.6% | | | 87.0% | | | 89.8% | | | 92.1% | | | 94.9% | | | 96.3% |

| 2001 | | | | | | | | | 85.9% | | | 89.3% | | | 91.7% | | | 93.9% | | | 95.3% |

| 2002 | | | | | | | | | | | | 70.4% | | | 67.4% | | | 71.4% | | | 74.3% |

| 2003 | | | | | | | | | | | | | | | 67.7% | | | 60.9% | | | 57.3% |

| 2004 | | | | | | | | | | | | | | | | | | 65.2% | | | 57.1% |

| 2005 | | | | | | | | | | | | | | | | | | | | | 62.0% |

|

This analysis displays the accident year net incurred losses and loss adjustment expenses on a GAAP basis for accident years prior to 1999 and for each of the accident years 1999-2005 for our workers' compensation and reinsurance businesses, together. The total of net loss and loss adjustment expenses for all claims occurring within each annual period is shown first at the end of that year and then annually thereafter. The total cost includes both payments made and the estimate of future payments as of each year-end. Past development may not be an accurate indicator of future development since trends and conditions change. The data prior to 1999 exclude the results of CalFarm Insurance Company, which was sold effective March 31, 1999.

The total change in our incurred loss estimates for all accident years during 2000 through 2005 was a net increase of about $65.1 million, comprised of $19.8 million for our reinsurance loss reserves and $45.3 million for our workers' compensation loss reserves. We recorded small amounts of adverse development of our workers' compensation loss reserves in each of 2001 through 2004 offset by net favorable development of $26.3 million in 2005 which resulted from a reallocation of our workers' compensation loss reserves by accident year to better reflect the paid claim cost deflation and inflation trends. Net adverse development of incurred losses in our reinsurance business was attributable to increased loss reserve estimates for catastrophe losses in 2000 and 2001, offset by favorable development of $6.9 million in 2004 due to a reduction of our 2001 World Trade Center loss.

8

INVESTMENT INCOME AFTER TAX PER SHARE

INVESTMENTS

Investment activities are a major part of our revenues and earnings; we believe our portfolio is diversified to achieve a reasonable balance of risk and a stable source of earnings. Zenith primarily invests in debt securities, as compared to equity securities, due to regulations, and our largest holdings are cash and short-term U.S. Government securities. In comparison to other insurers, we believe our portfolio consists of a smaller percentage of equity securities to total assets and a larger percentage of cash or short-term securities, with no derivative securities or credit enhancement exposure.

- •

- Zenith's investment portfolio increased $267.0 million, or 14%, in 2005 to $2.2 billion.

- •

- Consolidated investment income after tax and after interest expense was $47.7 million, or $1.35 per share, in 2005 compared to $33.8 million, or $1.06 per share, in 2004. Average yields on this portfolio in 2005 were 3.9% before tax and 2.6% after tax compared to 3.8% and 2.5%, respectively, in 2004.

- •

- During 2005, Zenith recorded capital gains before tax of $22.2 million compared to $38.6 million the prior year.

- •

- Net unrealized gains in our portfolio were $1.5 million before tax in 2005 compared to unrealized gains of $65.0 million before tax in 2004. The decline is due to realized gains and increases in interest rates.

- •

- Zenith's investment portfolio is recorded in the financial statements primarily at market value. Average life of the portfolio was 3.8 years at December 31, 2005 compared to 4.6 years at December 31, 2004. The portfolio quality is high, with 95% of fixed maturity securities rated investment grade at December 31, 2005 and 2004.

9

INVESTMENT INCOME AFTER TAX INCREASED 26% OVER THE PRIOR YEAR.

The major developments affecting the U.S. bond markets were continued low core inflation and fluctuating interest rates with the Federal Reserve Board increasing short rates. Long rates ended the year at a 4.54% yield for 30-year U.S. Government bonds. Since we are capable of holding bonds to maturity, and the average maturities are relatively short, fluctuations in bond values do not significantly impact our operations.

Short-term investments and liquidity remained high as we searched for investment opportunities. We have invested only a small amount of our capital in common stocks, since we believe the volatility in the market could impact our ability to expand our insurance business.

|

|---|

Securities Portfolio

| At December 31, 2005

| | At December 31, 2004

|

|---|

|

|---|

| Amortized Cost*

| Market Value

| | Amortized Cost*

| Market Value

|

|---|

|

|---|

| | (Dollars in Thousands) |

Short-term investments

U.S. Govt. and other securities

maturing within 2 years | $1,153,516 | $1,151,982 | | $ 901,820 | $ 901,296 |

| Other fixed maturity securities: | | | | | |

| Taxable, investment grade | 706,382 | 706,746 | | 621,014 | 638,927 |

| Taxable, non-investment grade | 78,457 | 76,582 | | 46,886 | 48,711 |

| Municipal bonds | 125,926 | 124,001 | | 127,378 | 127,242 |

| Redeemable preferred stocks | 25,436 | 26,685 | | 24,741 | 27,553 |

| Mortgage loans* | | | | 12,645 | 12,645 |

| Other preferred stocks* | 3,317 | 3,328 | | 4,732 | 4,857 |

| Common stocks* | 64,731 | 69,976 | | 58,230 | 101,205 |

| Other* | 7,402 | 7,402 | | 40,146 | 40,146 |

|

| Total | $2,165,167 | $2,166,702 | | $1,837,592 | $1,902,582 |

|

*Equity securities and other investments at cost. Mortgage loans at unpaid principal balance. |

10

WORKERS' COMPENSATION PREMIUM EARNED (IN MILLIONS)

From time to time, on a selective basis, we find excellent real estate investment opportunities. As previously reported, during 2003 we pursued development of a 3.2 acre site near our Sarasota, Florida office building with a partner. The project includes a Whole Foods Market, a parking structure, 23,000 square feet of commercial property and 95 condominium residences. Our interest in the commercial portion of the project was sold in the fourth quarter of 2005 resulting in a capital gain of $2.8 million. During the first quarter of 2006, we anticipate a distribution representing our share of the profit on the sale of the condominiums. At present, we are not involved in any real estate development investments.

WORKERS' COMPENSATION

Zenith is a workers' compensation specialist with 55 years of experience with primary operations in California and Florida. We also operate in 43 other states. We estimate that Zenith ranks among the top five underwriters in California and Florida, the two states in which we conduct 87% of our business. Our business philosophy does not include any planned goals as to size, market share or ranking, but is focused entirely on providing quality services to our insureds and claimants, and delivering a fair return to our shareholders.

Gross premiums written in 2005 were $1,139.3 million, an increase of 6% from the prior year with California premiums representing 68% of the total. Profits before tax in this segment were a record $213.2 million in 2005 compared to $104.1 million in 2004. During the past five years, our profit from this segment was $244.4 million, or 7% of earned premium.

Zenith's combined ratio (ratio of losses and expenses to total premiums) improved to 80.9% in 2005 from 88.5% the prior year. Industry combined ratios for workers' compensation are estimated at 106.2% and 106.6%, respectively, for 2005 and 2004. Our strategy and culture have produced

11

UNDERWRITING PROFITABILITY WAS ENHANCED BY DECLINING LOSS COSTS.

results substantially superior to industry averages over a long period of time. This performance provides the financial wherewithal to refine and strengthen our customer service strategy, to enhance our capital for growth, and improve our ability to assume risk.

Premium growth for the past two years is a result of the interaction of an increase in the number of policies and a change in net rates, experience modifications and payrolls. Net rates declined during this period as a result of favorable short-term cost trends that are consistent with the goals of the recently enacted California and Florida legislated reforms. Additionally, many policyholders received further price reductions because of lower experience modifications due to favorable claim experience. At year-end 2005, there were 44,400 policies in-force, an increase of 2.3% from the prior year. We have a very diversified group of policies; by size, geography and classes of business, including charities and not-for-profit employers. Zenith offers guaranteed cost (the vast majority of our policies), deductible, dividend and retro plans. Restaurants, dairies and dentists represent the largest policyholder classifications.

We estimate that rates have decreased 9% in 2005 and further expect them to decrease in 2006 due to reductions in cost trends primarily related to recent reform legislation. California rate decreases were larger and amounted to about 12% in 2005. California 2006 rates are anticipated to be lower than in the past two years by 29% due to the favorable short-term inflation trends, however at amounts reasonably sufficient to cover the estimated loss cost trends and to provide favorable underwriting profits. Additional rate changes may be advisable depending on developments, however it is quite possible that we are coming close to the end of the California rate decrease cycle. This will most definitely be true if reforms are modified in a major way, a circumstance we do not anticipate, although the unions and lawyers can be expected to make efforts to modify the reform legislation. In this regard, we expect an increase in the state minimum wage and it would not be a

12

WORKERS' COMPENSATION COMBINED RATIO

surprise if cash benefits were modestly increased. Accident year loss ratios, future rate decisions as well as any reserve releases will be determined as new data become available, most particularly, the updated inflation or deflation information.

Our workers' compensation segment profits are a result of a combination of a number of factors. First, the long-term trend of declining claim frequency relative to our premiums. Second, our pricing, underwriting and reserving strategy. Third, declining California costs in the medical area due to legislation reducing chiropractic and physical therapy visits and providing utilization guidelines and peer review to reduce excessive or unnecessary medical treatments. Fourth, the actuarial indications that our loss reserves are conservatively stated. This is crucial with respect to the recent accident years where only limited data are available, estimates are calculated with more significant assumptions determining the results, and the variance between current estimates and ultimate results could be substantial. Zenith's accident year loss ratios remain substantially below industry averages and have been for many years, except for 2004 in California, as indicated in the following table:

|

|---|

| | California

| | Outside of California

|

|---|

Accident Year

Loss Ratios

|

|---|

| | Zenith

| | Industry

| | Zenith

| | Industry

|

|---|

|

|---|

| 1999 | | 94% | | 139% | | 57% | | 85% |

| 2000 | | 87% | | 124% | | 57% | | 89% |

| 2001 | | 78% | | 107% | | 58% | | 79% |

| 2002 | | 66% | | 85% | | 51% | | 70% |

| 2003 | | 45% | | 54% | | 43% | | 64% |

| 2004 | | 38% | | 36% | | 40% | | 64% |

| 2005 | | 38% | | — | | 44% | | — |

We believe that the 2004 results in California may be temporary and caused primarily by the more conservative assumptions in our loss reserve estimates compared to the industry. As time passes and actual data replace estimates, we expect the traditional relationships to reappear.

13

OUR 2005 PERFORMANCE PROVIDES THE FINANCIAL STRENGTH TO CONTINUE REFINING OUR CUSTOMER SERVICE STRATEGY, SUPPORTING CAPITAL FOR GROWTH AND ENHANCING OUR ABILITY TO ASSUME RISK.

The favorable long-term comparisons set forth on the previous page are due to a number of factors: workers' compensation specialization, application of our own actuarial rates in California, well-established agency relationships, reasonable (not perfect) reserving accuracy, disciplined underwriting, and our commitment to quality customer services. Most importantly, the excellent performance of our experienced people working together over a long period of time makes a significant difference. Profitable industry results in California and a growing economy continue to provide an attractive operating environment. Legislative reforms have resulted in dramatic initial short-term benefits to our customers to a greater extent than could have been reasonably anticipated when they were enacted. Industry results projecting a 2004 accident year combined ratio of 59% are unbelievable and unprecedented. We doubt these estimates are reasonable or that current year results will be comparable, and we do not use these data to set adequate future rates or reserves. From 1995-2002, in comparison, combined ratios ranged between 116% and 184%. As a result of the current estimated results, competition in the California marketplace is more aggressive and from time to time a few competitors buy business at prices that make little sense.

Zenith adheres to disciplined and consistent underwriting and customer service principles and a commitment to pricing strategies based on realistic assumptions anticipated to generate an underwriting profit. Significantly, our agents and brokers offer us numerous opportunities for business, however, we are successful in writing only a small proportion of the prospective new accounts. We do, however, write a substantial percentage of renewal accounts. Based on current market conditions, we expect California to continue to be our most important and profitable market although price decreases and competitive pressures will most likely curtail premium growth. As previously discussed, underwriting profit margins will be primarily dependent upon data relating to inflation or deflation trends and the frequency of expensive claims in relation to payroll and premium.

At year-end 2005, California was an estimated $21.2 billion workers' compensation market. Our California in-force premium at year-end 2005 was $722.9 million compared to $731.3 million at the end of 2004. Zenith's total national in-force premium at year-end was $1,049.8 million, an increase

14

WE ADHERE TO DISCIPLINED UNDERWRITING AND SERVICE PRINCIPLES.

of 1% from the prior year. (In-force premiums differ from the accounting statement terminology of written and earned premium and are estimates of the premium to be received on all policies prior to their expirations.) Our insureds' payrolls have grown 7% in 2005 compared to the prior year.

Claim frequency trends in 2005 remained favorable as they have for a number of years. Severity trends in recent years have continued at reduced levels; and our ultimate loss estimates reflect caution regarding the long-term outcome of the reform legislation. Severity impact is caused primarily by health care and pharmacy cost trends, the duration and amount of temporary disability, and in benefit levels and permanent disability ratings. California reforms have required that we become more effective in dealing with healthcare issues than in the past. Healthcare inflation, in general, continues to increase in the 8-9% range per year. In contrast, California workers' compensation healthcare costs have declined from 2002-2004. It is unclear whether this short-term trend will continue or materially modify the long-term pattern of increases. Historically, long-term trends tend to be interrupted for relatively short periods, but the current situation may prove different due to medical networks, utilization guidelines and peer review. It should be obvious, but it is worth saying, that the longer that the healthcare costs for our business remain at reduced levels, the more beneficial it will be for our customers and shareholders.

We believe that quality healthcare and improved medical management from claim inception to outcome is essential to helping our injured workers return to work and productivity while recovering from job-related injuries. Highly experienced healthcare experts are in consultation with us in designing and implementing improved medical management practices and systems. Employers tend to believe that over-treatment is the norm; while labor argues that under-treatment of injured workers is prevalent. We believe that these different views can only be balanced with quality medical treatment, based upon best practices and outcome data. As a result, we are working to change our business practices to upgrade the quality of medical care around medical best practices supported by data and outcome measures.

15

QUALITY HEALTH CARE AND IMPROVED MEDICAL MANAGEMENT FROM CLAIM INCEPTION TO OUTCOME ARE ESSENTIAL SERVICES FOR HELPING INJURED WORKERS.

As a result of large insurance company insolvencies several years ago, it is expected that the California Insurance Guarantee Association will continue funding hundreds of millions of dollars in losses. Under current law, each of our policyholders (and all policyholders in the State) will continue to be assessed up to 2% of their premiums annually to cover these losses for the foreseeable future.

Our catastrophe management strategies are designed to mitigate our exposure to earthquakes and terrorism. Through a combination of reinsurance and careful tracking of our exposures with technology, we are focused on controlling our risks. During the fourth quarter of 2005, a modified version of the Terrorism Risk Insurance Act (TRIA) was extended for two years. Deductibles applicable to workers' compensation are 17.5% of direct premiums earned provided the total industry loss is more than $50 million in 2006.

Workers' compensation and California politics are inseparable. Changes are always being lobbied and discussed. The success of the recent reforms has reduced employer costs and acted as a stimulant to the economy greater than could have been accomplished by a large tax decrease. Since growth of tax revenue is essential to the State of California, we are optimistic that the reforms will continue despite occasional rhetoric to the contrary.

One of the most controversial aspects of the reforms is a change in the permanent disability rating system. The goal of the rating schedule was to give consideration to diminished future earning capacity in place of diminished ability to compete in the labor market. AMA guides were to be used as in many other states as compared to subjective considerations unique to California. The legislature delegated to the Administrative Director the implementation of the changes. Critics and so-called experts without real data are already pressing for changes. We believe changes should not be made until proper data has been obtained and evaluated, but this issue is being politicized and we do not know what may happen at this time.

16

TEAMWORK, IN CONCERT WITH TECHNOLOGY PROVIDES THE BASIS FOR ABOVE-AVERAGE RESULTS.

ZENITH'S MISSION

Reducing employer loss ratios, experience modifications and ultimately the long-term cost of their insurance while providing for the quality care and treatment for injured workers is our hallmark and our mission. We have specialized for many years in providing the necessary services and information to assist employers, their agents or brokers and employees in the realization and delivery of this mission. Accident and illness prevention improve productivity and morale. We are proud of Zenith's value-added specialist services, implemented in partnership with our policyholders, agents and brokers. Reducing job-related accidents, and in turn, the net cost of insurance and mitigating risk to many of our customers while providing for the quality care and treatment of injured workers, is our fundamental goal.

- •

- Expert Safety and Health professionals armed with state-of-the-art programs assist with accident and illness prevention, incident investigation and remediation, and safe work practices education and motivation for managers, supervisors and employees. Our concentration is on identifying exposures and assisting policyholders in reducing risk.

- •

- Claims and Medical/Disability Management procedures facilitate prompt injury reporting, the use of recommended physicians and medical facilities (where permitted state-by-state), nurse case management of serious claims, analysis and negotiation of hospital and medical bills, and ongoing communications and reviews to monitor and manage recoveries, costs and reserving. Claims costs are minimized by primarily utilizing the services of our internal claim staff, including claim, health and legal professionals, supported, where appropriate, by utilization guidelines and independent peer review of medical procedures. Our health care specialists are in consultation with experts to improve quality medical services and outcomes.

17

ZENITH'S RETURN ON AVERAGE EQUITY WAS 26.3% IN 2005 COMPARED TO 27.2% THE PRIOR YEAR.

- •

- Fraud experts, in concert with healthcare professionals and specialized workers' compensation legal personnel, protect employers from fraud and abuse, cooperate with law enforcement agencies, negotiate settlements where prudent and represent policyholders and our Company throughout the dispute resolution process as required.

- •

- Fair reserving is essential so that employers are treated properly with respect to the computation of their experience modifications, where applicable.

- •

- Intensified Return-to-Work programs place recovering employees in transitional duties with physician approval, improving morale and productivity, while containing costs and contributing significantly to long-term premium reduction.

- •

- Premium auditors provide proper payroll classifications to assure accuracy and avoid unanticipated retroactive billing.

- •

- E-Commerce on the Internet provides valuable current information to our agents and insureds, with some agents obtaining quotes and writing business through our technology.

Quality services require a substantial infrastructure investment in experienced employees and information technology. In this regard, change continues at a rapid pace at Zenith and, therefore, we have a long-term commitment to investing in the ongoing training and development of our people and the improvement of our systems and services. Zenith's objective is a stable, self-motivated workforce focused on continuing education and self-improvement. Teamwork in concert with technology among the various departmental disciplines provides the basis for above average results. As our business has grown and its complexity increased, we have hired and trained additional employees to support our quality services. At year-end 2005, there were 1,800 employees serving our customers compared to 1,600 at the end of 2004. We are confident in the abilities of our staff and management to build upon and continue to improve our services and their effectiveness in a fast changing environment. Our people are our most important asset. Training, teamwork and technology, along with specialization, are providing major improvements in our focus and capabilities resulting in benefits to our customers and shareholders.

18

OUR DECISION TO EXIT THE REINSURANCE MARKET REDUCES THE RISK AND VOLATILITY OF OUR EARNINGS.

REINSURANCE

Zenith has been engaged in the reinsurance business for 20 years and, despite large hurricane losses in the last two years, has made a profit over the period, including investment income. Our combined ratio for the 20 years was about 109%. Even so, we have decided to discontinue the business for several reasons:

- 1.

- Zenith is a small player in a business dominated by giants.

- 2.

- The frequency and severity of storms may be increasing.

- 3.

- Long-term profitability may not be possible due to the pricing inadequacy relative to risk and the reckless, "bet-the-bank" behavior of certain participants.

- 4.

- Our earnings volatility should be reduced and, therefore, capital utilized will be available for our main business.

At December 31, 2005, our reinsurance loss reserves were $179.5 million and we will continue to earn investment income until they are fully paid.

During 2005, written premiums were $67.2 million compared to $40.7 million in 2004. Earned premiums were $64.5 million compared to $42.4 million the prior year. (The increase in premiums is due to additional premiums resulting from the hurricane losses.) Segment losses were $56.2 million and $12.0 million, respectively, in 2005 and 2004.

Even though we will not write new or renewal business, we will have certain contracts that will not expire in accordance with their terms until September 2006.

Since we will have eliminated California earthquake reinsurance exposure by exiting this business, we will restructure the reinsurance we purchase for our workers' compensation business, assume some risk and save some premiums.

19

ZENITH'S INTERNAL FINANCIAL CONTROLS ARE EFFECTIVE AND CONSISTENT WITH SARBANES-OXLEY COMPLIANCE.

CORPORATE GOVERNANCE

Zenith's management and Audit Committee have spent considerable time and resources during 2005 to comply with Sarbanes-Oxley and Section 404 requirements. Section 404 relates to management's responsibilities to establish and maintain adequate internal controls over financial reporting and the effectiveness of these controls at year-end. We believe that we have maintained effective controls, however, Sarbanes-Oxley legislation requires that we continue to document these controls in a more formal and professional manner. Internal auditors, including consultants, review our results and our management committees provide supervision and oversight on a regular basis. External auditors have attached to this report the requisite opinion that the Company maintained, in all material respects, effective internal control over financial reporting as of December 31, 2005.

Zenith's Audit, Compensation, and Nominating and Corporate Governance Committees have conducted numerous meetings and oversight reviews to make certain our company is in the forefront of compliance with the highest standards of corporate governance. Our Directors should be complimented for their service and commitment to continuing corporate governance education to assure we are among the leaders in this important area.

INFORMATION TECHNOLOGY

The utilization of technology to enable new work processes and to provide "real time" information to our claims, claims legal and medical specialists is our highest priority. As we continue on the path of standardizing workflows around "best practices," we have built our systems utilizing an architecture that supports rapid changes in our business environment, including the ability to interface with multiple external partners.

We completed our integration to one national claims and policy system in 2005.

20

SHAREHOLDER DIVIDENDS WERE INCREASED IN THE PAST TWO YEARS.

As we continue to grow our electronic commerce operation beyond California and Florida, we are in the process of upgrading our E-commerce technology to the next generation that is designed to improve our efficiencies and lower operating costs.

During 2005, we added new and valuable content to our website: www.thezenith.com. We are gratified that there were over 500,000 visits to our site and we anticipate that number to increase in the coming year as more customers look to us for knowledge and support.

ACCOUNTING DISCLOSURE

Our financial statements include full disclosure of the accounting policies, estimates and assumptions used in their preparation. As we have discussed earlier in this report, estimating our workers' compensation loss costs and loss reserves is one of our major business risks. Our loss costs, or cost of goods sold, are not quantifiable with a high degree of certainty for several years until a large percentage of the claims for a given year are closed. This is particularly true in light of the California and Florida reforms where it is difficult to know whether the initial trends will continue over the long-term.

Zenith's actuaries perform comprehensive analyses of our loss reserves on a quarterly basis. Assumptions are required to project estimates of loss costs and loss reserves, with the key assumption being the rate of inflation in the most recent accident years of our workers' compensation loss reserves. In the table on page 35, we show the available data concerning paid loss inflation rates for the past several accident years and the inflation rates that we have assumed in our loss reserve estimate. We also provide a discussion of the long-term uncertainty surrounding the inflation trends of our workers' compensation loss costs.

21

OUR MANAGEMENT TEAM IS FOCUSED ON DELIVERING VALUE TO OUR CUSTOMERS AND ABOVE-AVERAGE RETURNS TO OUR SHAREHOLDERS, MANY OF WHOM ARE EMPLOYEES OF OUR COMPANY.

CONCLUSION

Our improved operating performance and financial strength provide optimism to believe that we can continue to produce excellent results for our agents, insureds and shareholders. Deflationary loss cost trends during the past three accident years are providing robust workers' compensation profitability.

Zenith is motivated to take advantage of opportunities and to meet the challenges ahead. Our business model as a specialist focused on an effective, customer-sensitive service strategy will continue to deliver above-average performance. Rate decreases in California are responsive to our cautious view of favorable short-term cost trends, and we anticipate our current rates are adequate to continue generating favorable returns. Also, our concentration on quality healthcare and medical outcomes is a long-term initiative that will enhance our specialist capabilities and benefit each of our constituencies.

Zenith's financial strength is better than is recognized by the rating agencies in light of the small amount of debt outstanding in relation to our equity. We believe we are being penalized as a specialist for lack of diversification. Under the circumstances, we would rather have a business model as a specialist that outperforms the industry over the long-run regardless of ratings. As a result, we should always be strongly capitalized.

Shareholder dividends were increased during 2005 and again on February 7, 2006. Our Board of Directors will continue to evaluate future dividends in relation to our performance.

The contributions of our distinguished Board of Directors serve as an inspiration to us all. We appreciate the confidence and support of our agents, brokers, policyholders, reinsurers, investors,

22

DEFLATIONARY LOSS COST TRENDS PROVIDE OPTIMISM FOR RESERVE ADEQUACY AND PROFITABILITY.

lenders and shareholders. In conclusion, we are financially and operationally strong and are well positioned to manage risk professionally and enhance shareholder value. Our management team consists of professionals with ambition, intelligence and motivation focused on delivering value to our customers and above average returns to our shareholders, many of whom are employees of our Company.

Stanley R. Zax

Chairman of the Board and President

Woodland Hills, California, February 2006

23

MANAGEMENT'S DISCUSSION AND ANALYSIS OF CONSOLIDATED FINANCIAL CONDITION AND RESULTS OF OPERATIONS

ZENITH NATIONAL INSURANCE CORP. AND SUBSIDIARIES

Zenith National Insurance Corp. ("Zenith National") is a holding company engaged, through its wholly-owned subsidiaries (primarily Zenith Insurance Company ("Zenith Insurance")), in the workers' compensation insurance business, nationally, and in the assumed reinsurance business. Unless otherwise indicated, all references to "Zenith," "we," "us," "our," the "Company" or similar terms refer to Zenith National together with its subsidiaries.

The Private Securities Litigation Reform Act of 1995 provides a safe harbor for forward-looking statements if accompanied by meaningful cautionary statements identifying important factors that could cause actual results to differ materially from those discussed. Forward-looking statements include those related to the plans and objectives of management for future operations, future economic performance, or projections of revenues, income, earnings per share, capital expenditures, dividends, capital structure, or other financial items. Statements containing words such asexpect, anticipate, believe, estimate, or similar words that are used in this Management's Discussion and Analysis of Consolidated Financial Condition and Results of Operations ("MD&A"), in other parts of this report or in other written or oral information conveyed by or on behalf of Zenith, are intended to identify forward-looking statements. The Company undertakes no obligation to update such forward-looking statements, which are subject to a number of risks and uncertainties that could cause actual results to differ materially from those projected. These risks and uncertainties include, but are not limited to, the following: (1) competition; (2) adverse state and federal legislation and regulation; (3) changes in interest rates causing fluctuations of investment income and fair values of investments; (4) changes in the frequency and severity of claims and catastrophes; (5) adequacy of loss reserves; (6) changing environment for controlling medical, legal and rehabilitation costs, as well as fraud and abuse; (7) losses associated with any terrorist attacks that impact our workers' compensation business in excess of our reinsurance protection; (8) losses caused by nuclear, biological, chemical or radiological events whether or not there is any applicable reinsurance protection; and (9) other risks detailed herein and from time to time in Zenith's other reports and filings with the Securities and Exchange Commission ("SEC").

OVERVIEW

Zenith is in the business of managing insurance and investment risk with the major risk factors set forth in the preceding paragraph. Our main business activity is the workers' compensation insurance business. We measure our performance by our ability to increase stockholders' equity over the long-term. Following is a summary of our recent business performance and how we expect the trends to continue for the foreseeable future:

1) Revenues. Our revenues are comprised of the net premiums earned from our workers' compensation and reinsurance segments and the net investment income and realized gains from our investments segment. Total revenues increased in each of the three years ended December 31, 2005 principally because our workers' compensation premium revenues increased in each of the three years ended December 31, 2005. In the twelve months ended December 31, 2005, there is a favorable impact on our workers' compensation net premiums

24

earned because we no longer ceded 10% of our workers' compensation earned premiums under a quota share reinsurance agreement which reduced net premiums earned in the corresponding periods of 2004 and 2003.

Our operating goals do not include objectives for revenues or market share. As a result of premium rate decreases in California, our largest state of operations, we expect that the growth in our workers' compensation net premiums earned will not continue into 2006. Our workers' compensation premiums are discussed further below under "Results of Operations—Workers' Compensation Segment" on pages 27 through 30.

2) Income (loss) from the workers' compensation and reinsurance segments. The results of our workers' compensation and reinsurance segments may fluctuate from time to time.

Workers' compensation. Income in 2005 increased compared to 2004, and in 2004 compared to 2003 as follows:

|

|---|

| | Year Ended December 31,

|

|---|

(Dollars in thousands)

| | 2005

| | 2004

| | 2003

|

|---|

|

|---|

| Income before tax from workers' compensation segment | | $ | 213,244 | | $ | 104,098 | | $ | 29,260 |

|

Reinsurance. The losses in 2005 and 2004 were due to catastrophe losses which reduced the results for the twelve months ended December 31, 2005 by $69.2 million, or $45.0 million after tax ($1.21 per share), and reduced the results for the twelve months ended December 31, 2004 by $21.1 million, or $13.7 million after tax ($0.37 per share).

In September 2005, we announced that we will exit the assumed reinsurance business.

3) Loss reserves. At December 31, 2005, we re-allocated our workers' compensation loss reserves by accident year compared to the allocation at December 31, 2004 to better reflect the facts and trends based on our current knowledge. In this regard, we recognized $26.3 million of net favorable development on prior year loss reserves during the year ended December 31, 2005.

4) Investments segment. We increased our investment portfolio by $267.0 million in the year ended December 31, 2005, principally as a result of favorable net cash flow from operations. We expect favorable net cash flow from operations to continue in 2006. Investment income increased in each of the three years ended December 31, 2005 because of increases in the investment portfolio in each of these years and higher short-term interest rates in 2005. At December 31, 2005, $1.2 billion of the investment portfolio was in fixed maturities of two years or less compared to $0.9 billion at December 31, 2004.

We recorded substantial realized gains from investments in each of the last three years, but we cannot predict future realized gains from investments.

5) Outstanding debt. In 2005, we reduced our outstanding debt because $123.8 million principal amount of our 5.75% Convertible Senior Notes due 2023 ("Convertible Notes") was converted into Zenith National's common stock, par value $1.00 per share ("Zenith National's common stock"). As a result of these conversions, the ratio of outstanding debt (the remaining balance of the Convertible Notes plus the balance of our redeemable securities) was 8% of the sum of all outstanding debt and stockholders' equity at December 31, 2005, compared to 27% at December 31, 2004. We do

25

not expect to incur any additional debt in the foreseeable future.

6) Stockholders' equity. During the last three years, our consolidated stockholders' equity increased from $383.2 million ($13.51 per share) at December 31, 2003 to $502.1 million ($17.28 per share) at December 31, 2004 and to $712.8 million ($19.14 per share) at December 31, 2005. These per share amounts reflect the 3-for-2 stock split distributed on October 11, 2005. Stockholders' equity will depend upon the future level of net income and any fluctuations in the values of our investments.

More information about the key elements of our performance follows below.

RESULTS OF OPERATIONS

Summary Results by Segment. Our business is classified into the following segments: investments; workers' compensation; reinsurance; and parent. Our real estate segment was discontinued in 2002. Income from operations of the investments segment includes investment income and realized gains and losses on investments and we do not allocate investment income to the results of our workers' compensation and reinsurance segments. Income (loss) from the workers' compensation and reinsurance segments is determined solely by deducting net losses and loss adjustment expenses incurred and underwriting and other operating expenses incurred from net premiums earned. The loss from operations of the parent segment includes interest expense and the general operating expenses of Zenith National. The comparative components of net income for the three years ended December 31, 2005 are set forth in the following table:

| |

|---|

| | Year Ended December 31,

| |

|---|

(Dollars in thousands)

| | 2005

| | 2004

| | 2003

| |

|---|

| |

|---|

| Net investment income | | $ | 79,200 | | $ | 61,876 | | $ | 56,103 | |

| Realized gains on investments | | | 22,224 | | | 38,579 | | | 19,433 | |

| |

| Income before tax from investments segment | | | 101,424 | | | 100,455 | | | 75,536 | |

| Income (loss) before tax from: | | | | | | | | | | |

| | Workers' compensation segment | | | 213,244 | | | 104,098 | | | 29,260 | |

| | Reinsurance segment | | | (56,183 | ) | | (11,956 | ) | | 9,562 | |

| | Parent segment | | | (20,938 | ) | | (19,051 | ) | | (17,694 | ) |

| |

| Income from continuing operations before tax and equity in earnings of investee | | | 237,547 | | | 173,546 | | | 96,664 | |

| Income tax expense | | | 81,894 | | | 57,213 | | | 33,664 | |

| |

| Income from continuing operations after tax and before equity in earnings of investee | | | 155,653 | | | 116,333 | | | 63,000 | |

| Equity in earnings of investee after tax | | | 794 | | | 1,381 | | | 2,846 | |

| |

| Income from continuing operations after tax | | | 156,447 | | | 117,714 | | | 65,846 | |

| Gain on sale of discontinued real estate segment after tax | | | 1,253 | | | 1,286 | | | 1,154 | |

| |

| Net income | | $ | 157,700 | | $ | 119,000 | | $ | 67,000 | |

| |

Net income improved in 2005 compared to 2004, and in 2004 compared to 2003, principally as a result of improved results in the workers' compensation segment, offset by catastrophe losses in the reinsurance segment in 2005 and 2004.

The combined ratio, expressed as a percentage, is a key measurement of profitability traditionally used in the property-casualty insurance industry. The combined ratio is the sum of the loss and loss adjustment expense ratio and the underwriting and other operating

26

expense ratio. The loss and loss adjustment expense ratio is the percentage of net incurred loss and loss adjustment expenses to net premiums earned. The underwriting and other operating expense ratio is the percentage of underwriting and other operating expenses to net premiums earned. The key operating goal for our insurance segments is to achieve a combined ratio of 100% or lower and to achieve a workers' compensation combined ratio that is at least three percentage points lower than the combined ratio of the national workers' compensation industry.

The combined ratios of the workers' compensation and reinsurance segments for the three years ended December 31, 2005 are set forth in the following table:

|

|---|

| | Year Ended December 31,

|

|---|

| | 2005

| | 2004

| | 2003

|

|---|

|

|---|

| Workers' compensation: | | | | | | |

| | Loss and loss adjustment expenses | | 53.0% | | 64.6% | | 69.9% |

| | Underwriting and other operating expenses | | 27.9% | | 23.9% | | 26.0% |

|

| Combined ratio | | 80.9% | | 88.5% | | 95.9% |

|

| Reinsurance: | | | | | | |

| | Loss and loss adjustment expenses | | 175.4% | | 107.6% | | 65.5% |

| | Underwriting and other operating expenses | | 11.7% | | 20.6% | | 18.8% |

|

| Combined ratio | | 187.1% | | 128.2% | | 84.3% |

|

Workers' Compensation Segment. In the workers' compensation segment, we provide insurance coverage for the statutorily prescribed benefits that employers are required to provide to their employees who may be injured in the course of employment. We establish our prices (in those states in which we are not required by regulation to use mandated rates) with the goal of achieving a combined ratio under 100%. We continually analyze data and use our best judgment about loss cost trends, particularly claim inflation, to set adequate premium rates and loss reserves.

The combined ratio of our workers' compensation segment improved in 2005 compared to 2004 and in 2004 compared to 2003, principally because of a lower estimated loss and loss adjustment expense ratio in 2005 compared to 2004 and in 2004 compared to 2003. This favorable trend in our estimated workers' compensation loss costs is attributable to a continuing favorable trend in the frequency of claims relative to premiums and lower rates of claim cost inflation in recent accident years. Our assumptions underlying our loss cost estimates are discussed further under "Loss Reserves" on pages 32 to 38. The lower loss and loss adjustment expenses ratio estimate in 2005 caused us to re-evaluate and increase our estimate for accrued policyholder dividends resulting in an increase in the underwriting and other operating expense ratio in 2005 of about two percentage points.

Our workers' compensation net premiums earned increased in 2005 compared to 2004 and in 2004 compared to 2003 as shown in the following table:

|

|---|

| | Year Ended December 31,

|

|---|

(Dollars in thousands)

| | 2005

| | 2004

| | 2003

|

|---|

|

|---|

| Net premiums earned: | | | | | | | | | |

| | Workers' compensation: | | | | | | | | | |

| | | California | | $ | 762,095 | | $ | 621,284 | | $ | 458,312 |

| | | Outside California | | | 352,099 | | | 280,763 | | | 254,484 |

|

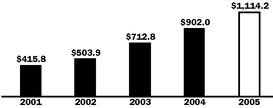

| | Total workers' compensation | | $ | 1,114,194 | | $ | 902,047 | | $ | 712,796 |

|

27

Workers' compensation premiums in-force and number of policies in-force in California and outside of California were as follows (premiums in-force is a measure of the amount of premiums billed or to be billed on all un-expired policies at the date shown):

|

|---|

| | California

| | Outside of California

|

|---|

(Dollars in millions)

| | Premiums

in-force

| | Policies

in-force

| | Premiums

in-force

| | Policies

in-force

|

|---|

|

|---|

| December 31, | | | | | | | | | | |

| 2005 | | $ | 722.9 | | 27,500 | | $ | 326.9 | | 16,900 |

| 2004 | | | 731.3 | | 27,200 | | | 311.0 | | 16,200 |

| 2003 | | | 587.9 | | 25,900 | | | 277.8 | | 15,600 |

|

The increase in workers' compensation net premiums earned is a function of the increase in policies, the payrolls of our policyholders, changes in premium rates and changes in our policyholders' experience modification factors. We believe that the insureds' payroll is our best indicator of exposure. We estimate that the underlying payroll associated with our policies in-force increased during the same periods as follows:

| |

|---|

| | Annual Increase in

Insureds' Payroll

| |

|---|

Policies in-force at December 31,

| | California Only

| | Total Company

| |

|---|

| |

|---|

| 2005 | | 7 | % | 7 | % |

| 2004 | | 25 | | 20 | |

| 2003 | | 13 | | 9 | |

| |

In California, the state in which the largest amount of our workers' compensation premium is earned, we set our own rates based upon actuarial analysis of current and anticipated cost trends. In Florida, the state in which the second largest amount of our workers' compensation premiums is earned, rates for workers' compensation insurance are set by the Florida Department of Insurance. Percentage changes in average premium rates in these two states during 2005 and 2004 were as follows (premium rate decreases are shown in parentheses):

| |

|---|

Effective date of change

| | California

| | Florida

| |

|---|

| |

|---|

| January 1, 2006 | | (13.1 | )% | (13.4 | )% |

| July 1, 2005 | | (12.0 | ) | 0.0 | |

| January 1, 2005 | | (1.6 | ) | (4.0 | ) |

| July 1, 2004 | | (10.0 | ) | 0.0 | |

| January 1, 2004 | | 0.0 | | 0.0 | |

| |

Average premium rates do not necessarily indicate charged rates since underwriters are given authority to increase or decrease rates based upon individual risk characteristics. According to published California industry data, Zenith's major competitors also reduced rates January 1, 2006 in a range from 6% to 20% and July 1, 2005 in a range from 12% to 25%.

Net premiums earned in 2004 and 2003 are net of $98.7 million and $78.5 million, respectively, of ceded premiums earned in connection with a 10% quota share ceded reinsurance agreement which was terminated effective December 31, 2004. The underwriting and other operating expense ratio for the workers' compensation segment is higher in 2005 compared to 2004 and 2003 by approximately two percentage points due to the absence in 2005 of ceding commissions received in 2004 and 2003 on the terminated 10% quota share ceded reinsurance agreement.

Workers' Compensation Reform Legislation. During 2005, Zenith wrote workers' compensation insurance in 45 states, but the largest concentrations, 68% and 19% of the workers' compensation net premiums earned during 2005, were in California and Florida, respectively. The concentration of

28

Zenith's workers' compensation business in these states makes the results of our operations dependent on trends that are characteristic of these states as compared to national trends. For example, state legislation, competition and workers' compensation inflation or deflation trends.

In California, workers' compensation reform legislation was enacted in October 2003 and April 2004 with the principal objectives of lowering the trend of increasing costs and improving fairness in the system. The principal changes in the legislation of October 2003 are as follows: 1) a reduction in the reimbursable amount for certain physician fees, outpatient surgeries, pharmaceutical products and certain durable medical equipment; 2) a limitation on the number of chiropractor or physical therapy office visits; 3) the introduction of medical utilization guidelines; 4) a requirement for second opinions on certain spinal surgeries; 5) a repeal of the presumption of correctness afforded to the treating physician, except where the employee has pre-designated a treating physician; and 6) a presumption of correctness is to be afforded to the evidence-based medical utilization guidelines developed by the American College of Occupational and Environmental Medicine.

The principal changes in the legislation of 2004 are as follows: 1) employers and insurers are authorized, beginning in 2005, to establish networks of medical providers within which injured workers are required to be treated (an independent medical review would be allowed if the claimant disputes the treatment recommended in the network only after obtaining the opinions of three network physicians); 2) within one working day of filing a claim form, a claimant must be afforded necessary treatment for up to $10,000 in medical fees (however, employers and insurers still have up to 90 days to investigate the compensability of a claim); 3) a methodology for apportioning disabilities between covered, work-related and prior causes was created such that employers are only liable for the portion of permanent disability that accrues from a covered, work-related injury; 4) Temporary Disability ("TD") benefits are not to exceed 104 weeks within 2 years of the first TD payment, but cases with certain specified injuries will be allowed up to 240 weeks of TD benefits within 5 years of the date of injury; 5) Permanent Disability ("PD") ratings are based on a new, objective disability rating schedule effective January 1, 2005 (and for some injuries prior to January 1, 2005) as well as upon the injured workers' diminished future earning capacity, rather than their ability to compete in the open labor market (PD benefits were revised to make available higher benefits to more severely injured workers and lower benefits to less severely injured workers); 6) incentives were created to encourage employers to offer return-to-work programs; and 7) new medical-legal processes for resolving disputed medical issues were created.

In Florida, legislation was enacted effective October 1, 2003, which provides changes to the workers' compensation system. Such changes are designed to expedite the dispute resolution process, provide greater compliance and enforcement authority to combat fraud, revise certain indemnity benefits and increase medical reimbursement fees for physicians and surgical procedures.

The short-term data for loss costs in recent accident years in California indicate a favorable impact from the reforms. As a result, we have

29

reduced our California premium rates in a manner that deals prudently with the uncertainty about the long-term outcome of loss cost trends for recent accident years. Future California premium rate decisions will be based on the data about loss cost trends or upon any modifications to the workers' compensation system. The uncertainties surrounding the estimation of workers' compensation loss costs are described under "Loss Reserves" on pages 32 to 38.

Some constituencies in the California workers' compensation system have expressed dissatisfaction with the reforms and these groups may seek changes either to the California workers' compensation reforms or the system itself. Such changes could include changes initiated through the California ballot initiative process. We cannot currently predict if any such changes will occur.

Reinsurance Segment. In assumed reinsurance, we provide coverage that protects other insurance and reinsurance companies from the accumulation of large losses from major loss events, known in the insurance industry as "catastrophes." Results of the reinsurance segment will be favorable in the absence of catastrophes and may be unfavorable in periods when they occur and, consequently, the results of this segment will fluctuate. The $56.2 million loss before tax in the reinsurance segment for the year ended December 31, 2005 was due to estimated catastrophe losses of $69.2 million ($45.0 million after tax, or $1.21 per share) net of additional premiums earned from reinstatement premiums. Catastrophe losses in 2005 were attributable to Hurricanes Katrina, Rita and Wilma.

The $12.0 million loss before tax in the reinsurance segment for the year ended December 31, 2004 was due to estimated catastrophe losses of $21.1 million before tax ($13.7 million after tax, or $0.37 per share). Catastrophe losses in 2004 were attributable to $26.8 million from the Florida hurricanes of 2004 offset by a $5.7 million reduction of previously estimated loss reserves, net of reinstatement premiums, for the 2001 World Trade Center loss. There were no major catastrophe losses that impacted the reinsurance treaties we wrote in the year ended December 31, 2003 and the result of the reinsurance segment was a profit of $9.6 million.

Estimating catastrophe losses in the reinsurance business is highly dependent upon the nature and timing of the event and Zenith's ability to obtain timely and accurate information with which to estimate its liability to pay losses. Estimates of the impact of catastrophes on the reinsurance segment are based on the information that is currently available and such estimates could change based on new information that becomes available or based upon reinterpretation of existing information. We describe in more detail the uncertainty surrounding catastrophe loss reserve estimates in the "Loss Reserves" section following.

In September 2005, we announced that we will exit the reinsurance business. Zenith will not renew existing assumed reinsurance contracts and has ceased writing any new contracts. We will service our obligations under our existing assumed reinsurance contracts and will receive earned premiums and be subject to continuing exposure to losses until our in-force assumed reinsurance contracts expire. The majority of our excess of loss assumed reinsurance contracts expired on December 31,

30

2005, and the remainder will be fully expired by the third quarter of 2006. Also, under our quota share assumed reinsurance contracts we will continue to assume premiums through the third quarter of 2006. However, premiums earned from assumed reinsurance contracts in 2006 will be substantially less than in 2005, and the exposure to any losses will be substantially less than the maximum exposure in previous years.

The results of the Reinsurance segment will continue to be included in the results of continuing operations.

Investments Segment. Investment income and realized gains and losses are discussed in the "Investments" section following.

Parent Segment. The parent segment loss reflects the holding company activities of Zenith National. The parent segment loss before tax for the three years ended December 31, 2005 was as follows:

| |

|---|

| | Year Ended December 31,

| |

|---|

(Dollars in thousands)

| | 2005

| | 2004

| | 2003

| |

|---|

| |

|---|

| Interest expense | | $ | (8,757 | ) | $ | (13,051 | ) | $ | (12,350 | ) |

| Parent expenses | | | (12,181 | ) | | (6,000 | ) | | (5,344 | ) |

| |

| Parent segment loss | | $ | (20,938 | ) | $ | (19,051 | ) | $ | (17,694 | ) |

| |

Parent expenses in 2005 include $4.7 million related to certain conversions of the Convertible Notes in 2005 (see Note 9 to the Consolidated Financial Statements). Interest expense on the Convertible Notes is added back to net income in the computation of diluted earnings per share (see Note 14 to the Consolidated Financial Statements).

Investment in Advent Capital. Through the second quarter of 2005, we accounted for our investment in Advent Capital (Holdings) PLC ("Advent Capital") under the equity method of accounting.

Zenith's share of Advent Capital's net income included in our Consolidated Statements of Operations was as follows:

|

|---|

| | Year Ended December 31,

|

|---|

(Dollars in thousands)

| | 2005

| | 2004

| | 2003

|

|---|

|

|---|

| Zenith's share of Advent Capital's net income, after tax | | $ | 794 | | $ | 1,381 | | $ | 2,846 |

|

Our share of Advent Capital's net income was reduced by $1.5 million, $4.7 million and $0.9 million in 2005, 2004 and 2003, respectively, for our share of Advent Capital's catastrophe losses.

Advent is no longer accounted for under the equity method since our ownership has been reduced to 10% and we no longer have representation on the board of directors.

At December 31, 2005 and 2004, Zenith owned 22.1 million shares of Advent Capital common stock. On June 3, 2005, Advent Capital sold 114.3 million shares of its common stock in a public offering at the United States dollar equivalent of $0.64 per share. On the same date, Advent Capital common stock was listed for trading on the Alternative Investments Market of the London Stock Exchange ("AIM") under the symbol ADV LN.

To reflect the new, publicly traded price of Advent Capital, Zenith reduced the carrying value of this investment to its fair value resulting in a charge of $9.5 million before tax ($6.2 million after tax) in the second quarter of 2005 as a reduction of realized gains on investments. The charge resulted from the difference between the fair value of our investment in Advent Capital, based upon the offering price for Advent Capital's common stock, and the carrying value of the investment under the equity method as of the date of the public offering.

31

At December 31, 2005, our investment in Advent Capital is included in equity securities classified as "available for sale." The fair value of the investment is the publicly traded price for Advent Capital's common stock obtained from the AIM and reflected in United States dollars. Changes in the fair value of the investment since the date of the public offering are recorded as a component of other comprehensive income. We do not presently intend to sell any of our shares of Advent Capital common stock.

Discontinued Real Estate Segment. In 2002, Zenith sold its home-building business and related real estate assets to MTH-Homes Nevada, Inc. ("MTH Nevada"), a subsidiary of Meritage Corporation.

In addition to the consideration received in 2002, we were entitled to receive 10% of MTH Nevada's pre-tax net income, subject to certain adjustments, for each of the twelve-month periods ending September 30, 2003, September 30, 2004 and September 30, 2005. We recorded additional gains on this sale of $1.9 million ($1.3 million after tax), $2.0 million before tax ($1.3 million after tax) and $1.8 million before tax ($1.2 million after tax) in 2005, 2004 and 2003, respectively. These gains represent our share of MTH Nevada's profits for the twelve months ended September 30, 2005, 2004 and 2003, respectively, under the earn-out provision of the sale agreement. The last such payment under the earn-out provision was received in 2005.

LOSS RESERVES

Accounting for the workers' compensation and reinsurance segments requires us to estimate the liability for the expected ultimate cost of unpaid losses and loss adjustment expenses as of the balance sheet date ("loss reserves"). Our loss reserves were as follows:

|

|---|

| | December 31,

|

|---|