UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM 10-K

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

FOR THE FISCAL YEAR ENDED DECEMBER 31, 2006 |

OR |

o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

COMMISSION FILE NUMBER: 000-27707 |

NEXCEN BRANDS, INC. |

| (EXACT NAME OF REGISTRANT AS SPECIFIED IN ITS CHARTER) |

DELAWARE | | 20-2783217 |

(State or other jurisdiction of incorporation or organization) | | (IRS Employer Identification Number) |

1330 Avenue of the Americas, New York, N.Y. | | 10019-5400 |

| (Address of principal executive offices) | | (Zip Code) |

(Registrant’s telephone number, including area code): (212) 277-1100 |

| |

| SECURITIES REGISTERED PURSUANT TO SECTION 12(b) OF THE ACT: |

| Title of Each Class | Name of Each Exchange on Which Registered |

Common Stock, par value $.01 | The NASDAQ Stock Market LLC |

| SECURITIES REGISTERED PURSUANT TO SECTION 12(g) OF THE ACT: NONE |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes o No ý

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes o No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of regulation S-K is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of the Form 10-K or any amendment of this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer o | Accelerated filer x | Non-accelerated filer o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No ý

The aggregate market value of the voting stock held by nonaffiliates of the registrant was $210,085,794 ($5.50 per share) as of June 30, 2006.

As of March 1, 2007 50,402,562 shares of the registrant’s common stock, $.01 par value per share, were outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

The registrant will disclose the information required under Part III, Items 10, 11, 12, 13, and 14 by (a) incorporating the information by reference from the registrant’s definitive proxy statement or (b) filing an amendment to this Form 10-K which contains the required information no later than 120 days after the end of the registrant’s fiscal year.

NEXCEN BRANDS, INC.

ANNUAL REPORT ON FORM 10-K

FOR THE YEAR ENDED DECEMBER 31, 2006

INDEX

| PART I | 3 |

| | | |

| Item 1 | Business | 3 |

| Item 1A | Risk Factors | 9 |

| Item 1B | Unresolved Staff Comments | 15 |

| Item 2 | Properties | 15 |

| Item 3 | Legal Proceedings | 16 |

| Item 4 | Submission of Matters to a Vote of Security Holders | 17 |

| | | |

| PART II | 19 |

| | | |

| Item 5 | Market for the Company’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | 19 |

| Item 6 | Selected Financial Data | 20 |

| Item 7 | Management’s Discussion and Analysis of Financial Condition and Results of Operations | 21 |

| Item 7A | Quantitative and Qualitative Disclosures About Market Risk | 30 |

| Item 8 | Financial Statements and Supplementary Data | 31 |

| Item 9 | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | 58 |

| Item 9A | Controls and Procedures | 58 |

| Item 9B | Other Information | 59 |

| | |

| PART III | 59 |

| | | |

| Item 10 | Directors and Executive Officers of the Registrant | 59 |

| Item 11 | Executive Compensation | 59 |

| Item 12 | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters. | 59 |

| Item 13 | Certain Relationships and Related Transactions | 59 |

| Item 14 | Principal Accounting Fees and Services | 60 |

| | | |

| PART IV | 61 |

| | | |

| Item 15 | Exhibits, Financial Statement Schedules | 61 |

FORWARD-LOOKING STATEMENTS

In this Annual Report on Form 10-K, we make statements that are considered forward-looking statements within the meaning of the Securities Act of 1934, as amended. The words “anticipate,” “believe,” “estimate,” “intend,” “may,” “will,” “expect”, and similar expressions often indicate that a statement is a “forward-looking statement.” Statements about non-historic results also are considered to be forward-looking statements. None of these forward-looking statements are guarantees of future performance or events, and they are subject to numerous risks, uncertainties and other factors. Given the risks, uncertainties and other factors, you should not place undue reliance on any forward-looking statements. Our actual results, performance or achievements could differ materially from those expressed in, or implied by, these forward-looking statements. Factors that could cause or contribute to such differences include those discussed in Item 1A of this Report under the heading “Risk Factors,” as well as elsewhere in this Report. Forward-looking statements reflect our reasonable beliefs and expectations as of the time we make them, and we have no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise.

General Overview

NexCen Brands engages in the acquisition and management of established consumer brands in intellectual property-centric industries. NexCen’s goal is to be the world leader in brand management for the 21st century. Our business is focused on acquiring, managing and developing intellectual property, which we refer to as IP, and IP-centric businesses. IP-centric companies own, license or otherwise possess rights to trademarks, trade names, copyrights, patents, trade secrets and other intangible assets. IP that we have acquired and expect to acquire in the future includes trademarks, trade names, copyrights, franchise rights, patents, trade secrets, know-how and other similar, valuable property, primarily used in the retail and consumer branded products and franchise businesses. In building our IP business, we expect to focus on three vertical segments: retail franchising, consumer branded products and quick service restaurant franchising (which we refer to as “QSR” franchising).

We commenced our IP business in June 2006, when we acquired UCC Capital Corporation, which we refer to as UCC. Upon the closing of that acquisition, Robert W. D’Loren, who was the president and chief executive officer of UCC, became our president and chief executive officer and a member of our Board of Directors.

In November 2006, we entered the retail franchising business by acquiring Athlete’s Foot Brands, LLC, along with an affiliated company and certain related assets. As a result of this acquisition, we are now the owner of The Athlete’s Foot brand and related marks. The Athlete’s Foot is one of the largest athletic footwear and apparel franchisors with over 600 retail locations in over 40 countries.

In February 2007, we entered the consumer branded products business by acquiring Bill Blass Holding Co., Inc. and two affiliated businesses. The Bill Blass label represents timeless style, modern American and is an American legacy brand in the fashion industry.

Also in February 2007, we acquired MaggieMoo’s International, LLC (“MaggieMoo’s”) and the assets of Marble Slab Creamery, Inc. (“Marble Slab”), two well known and established brands within the hand-mixed, premium ice cream category. With these acquisitions NexCen entered the QSR franchising business.

More detailed information about The Athlete’s Foot, Bill Blass, MaggieMoo’s, and Marble Slab acquisitions is included below under the caption “Company Brands.”

We are evaluating various other potential acquisitions and are actively in discussions to acquire additional IP-centric businesses. On March 13, 2007 we signed a definitive agreement to acquire the Waverly brand from F. Schumacher & Co. for $36.75 million in cash and a warrant to purchase 50,000 common shares (to be priced at issuance). Waverly is a home décor lifestyle brand for harmonious and tasteful decorating. We expect to close this transaction by the end of April 2007, and intend to finance 50% of the purchase price with borrowings under the new credit facility entered into on March 12, 2007, as discussed under Item 7. Management Discussion and Analysis of Financial Condition and Results of Operations under the caption “Liquidity and Capital Resources”.

At December 31, 2006, we had only one operating segment - our intellectual property business. As we continue to acquire IP businesses, we expect to have three segments in the future: retail franchising, consumer brand products, and quick service restaurants. The businesses that we owned and operated in 2005 and 2004 have been sold. As a result, their results have been reclassified to discontinued operations in our historical financial statements, and our continuing operations in 2005 and earlier years reflect only corporate expenses and other non-operating items.

We own the proprietary rights to a number of trademarks used in this Report which are important to our business, including The Athlete’s Foot, Bill Blass, MaggieMoo’s and Marble Slab. We have omitted the “®” and “TM” trademark designations for such trademarks in this Report. Nevertheless, all rights to such trademarks named in this Report are reserved.

Our Business

Operations and Strategy

Our operating strategy is to generate revenue from licensing and other commercial arrangements with third parties who want to use the IP that we acquire. These third parties pay us licensing and other contractual fees and royalties for the right to use our IP on either an exclusive or non-exclusive basis. Our contractual arrangements may apply to a specific demographic product market, a specific geographic market or to multiple demographics and/or markets.

We expect that licensing and other contractual fees paid to us will include a mixture of upfront payments, required periodic minimum payments (regardless of sales volumes), and volume-dependent periodic royalties (based upon the number or dollar amount of branded products and services sold). Accordingly, we expect that our revenues will reflect both recurring and non-recurring payment streams.

We operate our IP business in what we call a “value net” business model. This model does not require us to incur substantial operating or capital costs in running our business, as we do not (and do not plan to) manufacture, warehouse or distribute the branded products associated with the IP we acquire (or build stores in the case of franchise operations). We intend to rely on third-party licensees and other business partners to incur such capital costs and perform such services. However, we will generally be involved in the marketing, promotion and quality control of products and services that make use of our IP (such as trademarks and trade names that we own), and we also may provide certain merchandising, purchasing and training support services with respect to franchise operations. We believe that this business model mitigates -- or transfers to third parties -- the risks related to working capital (i.e. inventory and receivables) and capital expenditures. We believe that this model allows us to maintain maximum operational and financial flexibility and positions us to succeed in today’s competitive global economy. As a result of our business model, we rely heavily on third parties, including licensees and franchisees, to make sales, generate revenues and help grow our business. Such reliance involves various risks and uncertainties, which are discussed below in Item 1A. Risk Factors under the caption “Risks of Business We Acquire.”

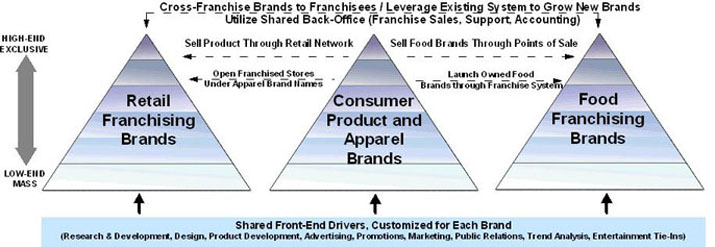

We intend to leverage our brand management, marketing, and licensing expertise, costs and professionals across our three operating verticals. We expect that these operating verticals will enable us to generate royalties at the wholesale and retail level on sales of goods for brands that we acquire, through distribution channels that we own, without the loss of sales in third-party channels. For example, we might decide to contract with third parties to produce a “private label” brand of socks that use our owned brand, The Athlete’s Foot, for sale in our chain of The Athlete’s Foot franchisee stores. The manufacturer of the socks who sells the product to the franchisees would pay us a royalty on those sales and in turn the franchisees who sell the socks to their retail customers also would pay us a royalty on their sales.

The following graphic summarizes our three operating segments (retail franchising, consumer branded products and QSR franchising) and the opportunities to cross-leverage the operating verticals with each other. Franchise concepts we purchase can be sold to our existing network of master franchisees who currently manage our franchise brands worldwide. Brands that we acquire can be sold through third party retail channels and channels that we own and control, allowing us to earn wholesale and retail royalties. Our objective is to create a flexible operating structure, control our distribution channels, and sell our owned brands through these channels as well as third party channels.

Diversification and Growth

As we build a portfolio of IP-centric businesses, we expect to operate a business model that is diversified in several ways:

| | · | across industries, ranging from apparel, footwear and sporting goods to QSR and retail franchising; |

| | · | across channels of distribution, ranging from luxury to mass-market; |

| | · | across consumer demand categories, ranging from luxury to mass-market; |

| | · | across licensees and franchisees, ranging from large licensees to individual franchisees; and |

| | · | across geographies (both within the United States and internationally); and |

| | · | across multiple demographic groups. |

We believe that this multi-category diversification will help reduce potential volatility in our financial results (given the varied sources of royalty payments from franchisees and licensees of different types and in different markets, demographics, and geographies) and may mitigate impairment risk.

We believe that our business model offers a three-tiered growth opportunity:

| | · | our businesses can grow both domestically and internationally through organic, and synergistic growth; |

| | · | our businesses can grow organically by expanding and extending owned brands into new product categories and retail channels, increasing brand awareness and executing new licenses or selling new franchises; |

| | · | we can grow through acquisition by acquiring new brands or additional franchise systems; and |

| | · | our business can grow synergystically by leveraging our three operating verticals. |

We can grow acquired brands by enabling them to sell branded products through franchise systems that we own. Conversely, we can expand our franchise systems by allowing them to sell additional branded products that we own or acquire. In either case, our objective will be to allow both our product brands and our systems to increase their sales. In each case, we would collect additional retail and wholesale royalties.

Development of Our IP Business and Acquisition Strategy

We entered the IP business when we acquired UCC in June 2006. Historically, UCC provided strategic advice and structured finance solutions to IP-centric companies. At the time that we acquired UCC, UCC’s former president and chief executive officer, Robert D’Loren, became our president and chief executive officer, as well as a member of our board of directors. In September 2006, we hired David B. Meister to become our new chief financial officer, and in December 2006 we hired Charles Zona to become our Executive Vice President, Brand Management and Licensing. Other members of the UCC management team assumed management roles in our developing IP business, and at the end of 2006 we moved our corporate headquarters to New York City, where our IP business is based.

Since June 2006, we have acquired four IP-centric companies. We have also been (and expect to continue to be) in active discussions with other potential acquisition candidates. Our objective is to acquire 3 to 5 businesses or significant groups of IP assets per year, with transaction sizes generally in excess of $50 million total enterprise value.

We maintain a highly disciplined pricing approach to acquisitions. Our objective is to acquire consumer branded products companies at transaction multiples that range from 4.5 to 5.5 times royalties. For QSR franchise concepts, our target range is from 3.0 to 4.5 times revenues. We believe this approach will enable us to make accretive acquisitions given our capital structure (using a combination of cash on hand, shares of our common stock and borrowings under debt facilities). For a discussion of limitations and risks associated with the use of our stock for acquisitions and to raise additional capital, see Item 1A. Risk Factors under the caption “Risks of Our Acquisition Strategy.”

Company Brands

Acquisition of The Athlete’s Foot. On November 7, 2006, our NexCen Acquisition Corp. subsidiary acquired Athlete’s Foot Brands, LLC, along with an affiliated advertising and marketing fund, and certain nominal fixed assets owned by an affiliated company. The Athlete’s Foot is an athletic footwear and apparel franchisor with 600 retail locations in over 40 countries. The business also provides advertising and marketing support for the benefit of the franchisees, using a portion of the royalties it receives from franchisees. This business operates in our retail franchising vertical.

The purchase price for this acquisition, excluding contingent consideration, was $53.1 million, consisting of approximately $42.1 million in cash and $9.2 million in our common stock (approximately 1.4 million shares which were valued at $6.55 per share), which was the average closing price of our common stock for the five consecutive days that ended on November 6, 2006, which is the day immediately preceeding the date in which we closed the agreement to purchase The Athhlete’s Foot), and $1.8 million in other deal related costs. At the closing on November 7, 2006, we also issued to one of the sellers a three-year warrant to purchase an additional 500,000 shares of our common stock at a per share price of $6.49 (which was the closing price of our common stock on November 7, 2006). On March 14, 2007, we borrowed $26.5 million under a new $150 million senior credit facility secured by the assets of The Athlete’s Foot. This debt facility is discussed below in Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations under the caption “Liquidity and Capital Resources.”

Under the purchase agreement for The Athlete’s Foot, we may be required to pay up to an additional $8.5 million of cash and stock (in the same proportion as the initial acquisition), if the revenue and EBITDA of the acquired business (as defined in the purchase agreement) for the year ended December 31, 2006 equal or exceed performance targets specified in the purchase agreement. The purchase agreement requires a stand-alone audit of the 2006 financial results of Athletes Foot Brands, LLC to be completed by March 31, 2007. The earn-out will be calculated based on the 2006 audited financial results. We estimate that the contingent consideration will be $4.0 million, and we have recorded a liability as of December 31, 2006 to reflect this expected payment.

Acquisition of Bill Blass. On February 15, 2007, our Blass Acquisition Corp. subsidiary acquired Bill Blass Holding Co., Inc. and two affiliated businesses. The Bill Blass label represents timeless style, modern American and is an American legacy brand. This business operates in our consumer brands vertical.

At the closing, one of the Bill Blass companies executed a licensing agreement for men’s and women’s denim with Designer License Holding Company, LLC. The new license replaced a denim license and an active wear license that were terminated and had been held by two companies that are affiliated with one of the prior owners of Bill Blass.

The initial purchase price for this acquisition was $54.6 million, consisting of $39.1 million in cash and $15.5 million in our common stock (approximately 2.2 million shares which were valued at $7.09 per share, which was the average closing price of our common stock for the ten consecutive days that ended on December 19, 2006, which is when we signed the agreement to purchase Bill Blass). Under the purchase agreement, the sellers will be entitled to receive up to an additional $16.2 million of consideration, payable in early 2008. The additional consideration under the earn-out will be equal to the amount by which the royalties generated from the Bill Blass trademarks in fiscal 2007, multiplied by 5.5, exceed $51.8 million, subject to certain adjustments. The total purchase price will not exceed $70.8 million. We expect to borrow approximately $27 million under our new credit facility, which will be secured by the assets of Bill Blass.

Acquisition of MaggieMoo’s. On February 28, 2007, we acquired MaggieMoo’s International, LLC (“MaggieMoo’s”). The initial purchase price for this acquisition was $16.1 million, consisting of approximately $10.8 million of cash and debt repayment, and 515,352 shares of our common stock (reflecting valued at $5.3 million, based on the average closing price of our common stock for the fifteen consecutive days that ended on February 27, 2007, of $10.21). Under the purchase agreement, the sellers will be entitled to receive up to an additional $2.0 million of consideration in the form of an earn-out, payable on March 31, 2008. The earn-out will be based on the amount royalty payments earned during fiscal 2007 exceed royalty payments earned by MaggieMoo’s during fiscal 2006, pursuant to a formula set forth in the purchase agreement. MaggieMoo’s is the franchisor of 184 stores located in 36 states domestically. Each location features a menu of freshly made super-premium ice creams, mix-ins, smoothies, and custom ice cream cakes. This business operates in our QSR vertical.

Acquisition of Marble Slab. On February 28, 2007, we acquired the assets of Marble Slab Creamery, Inc. (“Marble Slab”). The purchase price of the acquisition was $21 million, consisting of $16 million of cash, and the issuance of $5.0 million of notes payable which mature on February 28, 2008. The notes accrue interest at an annual rate of 6% per annum until maturity, and 8% thereafter, and are payable in cash or common stock priced at the time of issuance, at the Company’s option. We have deposited $5.0 million into an escrow account to collateralize the payment of these notes. Marble Slab is the franchisor of 336 stores located in 35 states, Puerto Rico, Canada and the United Arab Emirates. Since 1983, each Marble Slab Creamery has featured homemade super-premium ice cream that is hand-rolled in freshly baked waffle cones. This business operates in our QSR vertical. We intend to borrow $19 million under the new senior credit facility entered into on March 12, 2007 secured by the assets of MaggieMoo’s and Marble Slab.

We expect to borrow $19 million under our new senior credit facility, which will be secured by the assets of MaggieMoo’s and Marble Slab. Assuming we borrow all of the expected amounts for the Bill Blass, MaggieMoo’s and Marble Slab acquisitions, our total borrowings under our new $150 million credit facility (including the $26.5 million we borrowed for The Athlete’s Foot acquisition) would be approximately $72.5 million. For a discussion of risks associated with borrowings, see Item 1A. Risk Factors under the caption “Risks of Our Our Current Business - Any failure to meet our debt obligations would adversely affect our business and financial condition.”

Competition

Our brands are all subject to extensive competition by numerous domestic and foreign brands. Each of our brands has numerous competitors within each of our specific distribution channels. Our degree of success is dependent on the image of our brands to consumers and our licensees' ability to design, manufacture and sell products bearing our brands.

In seeking to make acquisitions of IP and IP-centric businesses, we compete with other companies and financial buyers (such as private equity funds). While we believe the number of competitors is currently limited, we expect that more competitors will develop over time. Competitors may be larger than us, have access to greater financial and other resources or be willing to pay higher prices in acquisitions or assume greater acquisition-related risks. See Item 1A. Risk Factors under the caption “Risks of Our Acquisition Strategy - Competition may negatively affect our ability to complete suitable acquisitions.”

The Athletes Foot. Our franchisees operate in the retail athletic footwear and apparel business which is highly competitive with relatively low barriers to entry. The principal competitive factors in these markets are price, quality, selection of merchandise, reputation, store location, advertising and customer service.

The businesses we acquired in 2007, and businesses we acquire in the future, are also subject to competitive risks and pressures, including price, quality, selection of merchandise, reputation, store location, advertising and customer service.

Historical Operations

Historical Overview

Until late 2004, we owned, acquired and operated a number of mobile and wireless communications businesses. These businesses never became profitable, and during 2004 we sold these businesses and started a mortgage-backed securities, or MBS, business. During 2004 and 2005, we assembled a leveraged portfolio of MBS investments. However, market conditions for the MBS business changed significantly during 2005 and into 2006, and the profitability of our leveraged MBS portfolio declined. In light of these changing market conditions, in late 2005 and into 2006, we began to explore additional and alternative business strategies that we thought could help us become profitable more quickly and create shareholder value. These efforts resulted in our decision to acquire UCC in June 2006. On October 31, 2006, at the 2006 Annual Meeting of Stockholders (the “Annual Meeting”), our stockholders approved the sale of our MBS portfolio for the purpose of discontinuing our MBS business and allocating all cash proceeds from such sale to the growth and development of our IP business. We sold our MBS investments in November 2006, and since that time, we have focused entirely on our IP business.

Holding Company Reorganization and Name Change

Aether Systems Inc. (“Aether Systems”), the historical entity through which we previously conducted the Mobile Government, EMS and Transportation businesses, was formed in January 1996. On July 12, 2005, the stockholders of Aether Systems approved a holding company reorganization of Aether Systems in which each share of Aether Systems common stock was exchanged for one share of common stock of Aether Holdings, Inc. (“Aether Holdings”), and Aether Systems became a wholly owned subsidiary of Aether Holdings. The reorganization was undertaken to implement restrictions on certain changes in the ownership of our common stock in an effort to protect the long-term value of our substantial net operating loss and capital loss carry forwards (as described in further detail below). In recognition of the changing business strategy of the Company, on October 31, 2006, our stockholders approved a change of our Company name from Aether Holdings to NexCen Brands. Effective November 1, 2006, we changed our “ticker” symbol, under which our common stock is traded on the Nasdaq Global Market, from “AETH” to “NEXC.”

Tax Loss Carry Forwards

As a result of the substantial losses incurred by our mobile and wireless communications businesses through 2004, as of December 31, 2006, we had federal net operating loss carry forwards of approximately $777 million that expire on various dates between 2011 and 2026. These tax loss carryforwards are generally available to offset federal income taxes. We expect to remain subject to certain state, local, and foreign tax obligations, as well as to a portion of the federal alternative minimum tax, as discussed below in Item 1A. Risk Factors under the caption “Risks of Our Tax Loss Carry Forwards.” In addition, we had capital loss carry forwards of approximately $251 million that expire between 2007 and 2011. If we had an ownership change as defined in Section 382 of the Internal Revenue Code of 1986, as amended (“IRC”), our net operating loss carryforwards and capital loss carry forwards generated prior to the ownership change would be subject to annual limitations, which could reduce, eliminate, or defer the utilization of these losses.

Generally, an ownership change occurs if one or more stockholders, each of whom owns 5% or more in value of a corporation’s stock, increase or decrease their aggregate percentage ownership by 50% or more as compared to the lowest percentage of stock owned by such stockholders at any time during the preceding three-year period. For example, if a single stockholder owning 10% of our stock acquired an additional 50% of our stock in a three-year period, a change of ownership would occur. Similarly, if ten persons, none of whom owned our stock, each acquired slightly over 5% of our stock within a three-year period (so that such persons own, in the aggregate more than 50%) an ownership change would occur. Ownership of stock is determined by certain constructive ownership rules which can attribute ownership of stock owned by entities (such as estates, trusts, corporations, and partnerships) to the ultimate indirect owner.

For purposes of this rule, all holders who each own less than 5% of a corporation’s stock are generally treated together as one (or, in certain cases, more than one) 5% stockholder. Transactions in the public markets among stockholders owning less than 5% of the equity securities generally are not included in the calculation. Special rules can result in the treatment of options (including warrants) or other similar interests as having been exercised if such treatment would result in an ownership change.

As a result of the holding company reorganization that we completed in 2005, as described above under the caption “Holding Company Reorganization and Name Change,” shares of our common stock are subject to transfer restrictions contained in our certificate of incorporation. In general, the transfer restrictions prohibit any person from acquiring 5% or more of our stock without our consent. Persons who owned 5% or more of our stock prior to May 4, 2005 are permitted to sell the shares owned as of May 4, 2005 without regard to the transfer restrictions. Shares acquired by such persons after May 4, 2005 are subject to the transfer restrictions. While we expect that these transfer restrictions will help guard against a change of ownership occurring under Section 382 and the related rules, because we are using stock as consideration to make acquisitions, because we may decide (or need) to sell additional shares of our common stock in the future to raise capital for our business and because persons who held 5% or more of our stock prior to these restrictions taking effect can sell (and in some cases have sold) shares of our stock, we cannot guarantee that these restrictions will prevent a change of ownership from occurring. Our board of directors also has the right to waive the application of these restrictions to any transfer.

One of our principal business objectives is to operate profitably so that we can realize value, in the form of tax savings, from our accumulated tax loss carry forwards. The Company monitors the change in shareholdings on a monthly basis and has an outside accounting firm (other than our independent auditor) perform a quarterly analysis to determine the cumulative percent change through the end of the particular quarter. Based upon a review of past changes in our ownership, as of December 31, 2006, we do not believe that we have experienced an ownership change (as defined under Section 382) that would result in any limitation on our future ability to use these net operating loss and capital loss carry forwards. However, we can not be certain that the IRS or some other taxing authority may not disagree with our position and contend that we have already experienced such an ownership change, which would severely limit our ability to use our net operating loss carry forwards and capital loss carry forwards to offset future taxable income.

For a discussion on the risks associated with our tax loss carry forwards, please refer to Item 1A. Risk Factors under the caption “Risks of Our Tax Loss Carry Forwards.”

Employees

As of December 31, 2006, we employed a total of 36 persons. None of our employees is covered by a collective bargaining agreement. We believe that our relations with our employees are good. As we acquire additional businesses, our employee base will increase.

General Corporate Matters

Our executive offices are located at 1330 Avenue of the Americas, 34th Floor, New York, NY 10019. Our telephone number is (212) 277-1100 and our fax number is (212) 277-1160.

Availability of Information

We maintain a website at www.nexcenbrands.com, which provides a wide variety of information on each of its brands. You may read and copy any materials we file with the Securities and Exchange Commission at the SEC’s Public Reference Room at 100 F Street, N.E., Washington, DC 20549. For further information concerning the SEC’s Public Reference Room, you may call the SEC at 1-800-SEC-0330. Some of this information may also be accessed on the SEC’s website at www.sec.gov. We also make available free of charge, on or through our website, our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports filed or furnished to the SEC pursuant to Section 13(a) or Section 15(d) of the Securities Exchange Act of 1934, as amended (the “Exchange Act”) as soon as reasonably practicable after we electronically file such material with, or furnish it to, the SEC. We are providing the address of our internet website solely for the information of investors. We do not intend the internet address to be an active link, and the contents of the website are not a part of this Report. We also maintain, in some cases through our licensees, sites for each of the Company's brands and operations, www.theathletesfoot.com, www.ucccapital.com and www.billblass.com.

ITEM 1A. RISK FACTORS

Investing on our common stock involves a high degree of risk. Before making an investment decision, you should carefully consider these risks as well as information we include or incorporate by reference in this prospectus. If any of the following risks actually occur, our business, financial condition or results of operations could be materially and adversely affected, and you may lose some or all of your investment.

Risks of Our Current Business

We have incurred significant losses throughout our history and may not be profitable in the future.

Since our inception, we have incurred net losses of approximately $2.5 billion. We only recently began to implement our new IP-centric business strategy. There is no assurance that we will be able to operate this new IP business profitably or to report net income in the future and realize the value of our substantial tax loss carryforwards.

Our IP-centric business is new, and we may not be successful in operating or expanding it.

We do not have an established history of acquiring IP, or IP-centric businesses, and managing IP assets and businesses. We began to implement our IP-centric business in June 2006, when we acquired UCC. Upon the closing of that acquisition, Mr. D’Loren, who was the president and chief executive officer of UCC, became our president and chief executive officer. During their tenure with UCC, Mr. D’Loren and the other members of our senior management team were involved primarily in providing banking, finance, consulting and other advisory services to IP-centric businesses. They did not own or manage an IP-centric business directly. As a result, we may encounter unanticipated difficulties or challenges as we work to implement our new business strategy. If we are unable to address and overcome such difficulties or challenges, we may not be successful with our new business strategy.

We are dependent upon our president and chief executive officer, Robert W. D’Loren. If we lose Mr. D’Loren’s services, we may not be able to successfully implement our IP business strategy.

The successful implementation of our IP business strategy will depend primarily upon the efforts of Mr. D’Loren, our president and chief executive officer. Mr. D’Loren is the person primarily responsible for conceiving of and implementing our IP business strategy. Although we have entered into an employment agreement with Mr. D’Loren that runs through June 2009, there is no guarantee that he will remain employed by us throughout the period. If he ceases to work with us, or if his services are reduced, we will need to identify and hire other qualified executives, and we may not be successful in finding or hiring adequate replacements. This could impede our ability to fully implement our IP business strategy, which would harm our business and prospects.

The market price of our common stock has been, and may continue to be, volatile, which could reduce the market price of our common stock and, among other things, make it more expensive for us to complete acquisitions using our stock as consideration.

Since we announced the acquisition of UCC and the hiring of Mr. D’Loren, the trading price of our common stock has experienced significant price and volume fluctuations. This market volatility could reduce the market price of our common stock, regardless of our operating performance. In addition, the trading price of our common stock could change significantly over short periods of time in response to actual or anticipated variations in our quarterly operating results, announcements by us or by third parties on whom we rely or against whom we compete, factors affecting the markets in which we do business or changes in national or regional economic conditions. If our stock price declines, we may be required to issue additional shares to complete acquisitions, which would make them more dilutive to our stockholders. The market price of our common stock also could be reduced by general market price declines or market volatility in the future or future declines or volatility in the prices of stocks for companies against whom we compete or companies in the industries in which our licensees compete.

We are unlikely to become profitable unless we can identify and acquire IP and IP-centric businesses on favorable terms.

Our ability to achieve our business objective of becoming profitable will depend on our ability to identify and acquire suitable acquisitions on favorable terms, so that we can increase our revenues and generate net income. If we are unable to complete acquisitions on favorable terms, our new IP business will be very limited and may not generate sufficient revenues to cover our expenses. There is no assurance that we will be able to complete any future acquisitions or that such transactions, if completed, will contribute positively to our operations and financial results and condition.

We are involved in litigation with respect to a business that we sold in 2005.

In 2005, we sold our mobile transportation business to Geologic Solutions, Inc. Since that time, Geologic has notified us of, and we have responded to, various indemnification claims for alleged breaches of representations and warranties under the asset purchase agreement pursuant to which we sold the transportation business to Geologic. We were unable to resolve these claims with Geologic, and in March 2006, Geologic filed a lawsuit against us in state court in New York. Geologic’s claims primarily involve allegations that we did not fully disclose certain aspects of our transportation business’ relationships with one of its major customers and two of its major suppliers that allegedly resulted in the devaluation of inventory and other adverse effects to the business. Geologic contends that it has suffered damages in excess of $30 million as a result of these alleged breaches. The Company believes it has meritorious defenses to Geologic’s claims and is vigorously defending against them. However, we cannot predict the outcome of this litigation, and an adverse resolution of such claims could require us to make a significant cash payment to Geologic. In such event, we would record a charge against earnings, further increasing the loss on the sale of the transportation business, and decreasing the amount of cash we have available for acquisitions and operations.

Any failure to meet our debt obligations would adversely affect our business and financial condition.

On March 12, 2007, we entered into a new $150 million master loan agreement with BTMU Capital Corporation. As of March 14, 2007, we have approximately $26.5 million of long-term debt outstanding, and expect to draw an additional $46 million shortly to refinance the acquisitions of Bill Blass, MaggieMoo’s and Marble Slab. Interest rates for our master loan agreement vary based upon utilization and whether the borrowings are at the base rate or the London Interbank Offering Rate ("LIBOR").

Our master loan agreement contains affirmative and negative covenants customary for senior secured credit facilities, including, among other things, restrictions on indebtedness, liens, fundamental changes, loans, acquisitions, capital expenditures, restricted payments, transactions with affiliates, common stock repurchases, dividends and other payment restrictions affecting subsidiaries and sale leaseback transactions. Our failure to comply with the financial and other restrictive covenants relating to our indebtedness could result in a default under the indebtedness, which could materially adversely affect our business, financial condition and results of operations. These restrictions may also limit our ability to operate our businesses and may prohibit or limit our ability to enhance our operations or take advantage of potential business opportunities as they arise.

As a result of our indebtedness, we will need to use a portion of our cash flow to pay principal and interest, which will reduce the cash available to finance our operations and other business activities and could limit our flexibility in planning for or reacting to changes in our business. The master loan agreement may also limit our ability to obtain future financings which could negatively impact our business, financial condition, results of operations and growth. The amount of our debt may also cause us to be more vulnerable to economic downturns and adverse developments in our business.

Risks of Our Acquisition Strategy

Competition may negatively affect our ability to complete suitable acquisitions.

We believe that there are a limited number of other companies competing for acquisitions of the type that we are seeking. However, we will face competition for acquisitions, and competition may increase as the business strategy we are pursuing continues to receive publicity. Existing and future competitors may be larger than us and have access to greater financial and other resources. As a result, acquisitions may become more expensive, and we may face greater difficulty in identifying suitable acquisition candidates on terms that we believe will make sense. If we are unable to expand our business by completing acquisitions on favorable terms, our financial results may be negatively affected.

Acquisitions involve numerous risks that we may not be able to address or overcome, and could result in acquisitions that negatively affect our business and financial results.

Even if we are successful in completing IP-centric acquisitions, we may not be able to achieve or maintain profitability levels that will justify our investments in those acquisitions. Among other things, we may not be able to realize anticipated benefits from our acquisitions, including various synergies and economies of scope and scale. Each acquisition involves numerous risks, any of which could have a detrimental effect on our results of operations and/or the value of our equity. These risks include, among others:

| | · | overpaying for acquired assets or businesses; |

| | · | being unable to license, market or otherwise exploit IP that we acquire on anticipated terms or at all; |

| | · | negative effects on reported results of operations from acquisition-related expenses and amortization or impairment of acquired intangibles; |

| | · | diversion of management's attention from management of day-to-day operational issues; |

| | · | failing to maintain focus on, or ceasing to execute, core strategies and business plans as our IP portfolio grows and becomes more diversified; |

| | · | failing to acquire or hire additional successful managers, or being unable to retain critical acquired managers; |

| | · | potential adverse effects of a new acquisition on an existing business or business relationship; and |

| | · | underlying risks of the businesses that we acquire, which may differ from one acquisition to the next, including those related to entering new lines of business or markets in which we have little or no prior experience. |

Our ability to grow through the acquisition of additional IP assets and business will depend on the availability of capital to complete acquisitions.

We financed the acquisitions of The Athlete’s Foot, Bill Blass, MaggieMoo’s and Marble Slab with a combination of cash and equity, and we intend to finance our future IP acquisitions through a combination of available cash, bank or other institutional financing, and issuances of equity and possibly debt securities. As of March 14, 2007, we had approximately $39 million of cash on hand after borrowing $26.5 million under the new senior credit facility we entered into on March 12, 2007. There is no assurance that we will be able to secure borrowings in the future to fund acquisitions, either on terms that we consider reasonable or at all. In addition, under Section 382 of the Internal Revenue Code of 1986, as amended, we face limitations on the number of shares of equity that we can issue without triggering limitations on our future ability to use our substantial accumulated tax loss carry forwards. Under certain circumstances, these limitations (if triggered) could significantly or, under certain circumstances, totally reduce the future value of our tax loss carry forwards (assuming we are able to generate taxable income that would benefit from the use of the tax loss carry forwards).

As a result of these factors, we may lack access to sufficient capital to complete acquisitions that we identify and want to complete. In such a case, our inability to complete acquisitions could have a material adverse effect on our business, our financial results and the trading price of our stock.

We operate a global business that exposes us to additional risks that may negatively affect our results of operations and financial condition.

Our Athlete’s Foot franchisees operate in over 40 countries. In addition, the brands and other IP assets that we acquire and manage are currently used, and in the future are expected to be used, for products and services that will be advertised and sold in many different countries. As a result. we are subject to risks associated with doing business globally. We intend to continue to pursue growth opportunities for our IP business outside the United States, which could expose us to greater risks. The risks associated with our IP business outside the United States include:

| | · | Political and economic instability or civil unrest; |

| | · | Armed conflict, natural disasters or terrorism; |

| | · | Health concerns or similar issues, such as a pandemic or epidemic; |

| | · | Multiple foreign regulatory requirements that are subject to change and that differ between jurisdictions; |

| | · | Changes in trade protection laws, policies and measures, and other regulatory requirements effecting trade and investment; |

| | · | Differences from one country to the next in legal protections applicable to IP assets, including trademarks and similar assets, enforcement of such protections and remedies available for infringements; |

| | · | Fluctuations in foreign currency exchange rates and interest rates; and |

| | · | Adverse consequences from changes in tax laws. |

The effects of these risks, individually or in the aggregate, could have a material adverse impact on our IP business.

Risks of Businesses We Acquire

Our business will depend on market acceptance of the IP that we intend to acquire such as trademarks, brands and franchise rights. We expect these markets to be highly competitive.

Continued market acceptance of the IP that we intend to acquire, such as trademarks, brands and franchise rights is critical to our future success and subject to great uncertainty. The consumer branded products industries on which we expect to focus our acquisition activities are extremely competitive, both in the United States and overseas. Accordingly, we expect that we and our future licensees and other business partners (including franchisees) will face intense and substantial competition with respect to marketing and expanding products and services under acquired IP. As a result, we may not be able to attract licensees, franchisees and other business partners on favorable terms or at all. In addition, licensees and other third parties with whom we deal may not be successful in selling products and services that make use of our acquired IP. They (and we) also may not be able to expand the distribution of such products and services into new markets.

In general, competitive factors include quality, price, style, name recognition and service. In addition, the presence in the marketplace of short-lived “fads” and the limited availability of shelf space can affect competition for many consumer products. Changes in consumer tastes, national, regional and local economic conditions, discretionary spending priorities, demographic trends, traffic patterns and the type, number and location of competing products and outlets also can affect market results. Competing trademarks and brands may have the backing of companies with greater financial, distribution, marketing, capital and other resources than do us or our licensees and other business partners. This may increase the obstacles that we and they face in competing successfully. Among other things, we may have to spend more on advertising and marketing or may need to reduce the amounts that we charge licensees and other business partners. This could have a negative impact on our business and financial results.

Because we expect to rely on unaffiliated third parties to market, distribute, sell and in some cases design products and services using IP such as trademarks and brands that we license, the success of our business may depend upon various factors that are beyond our control.

We expect to have limited personnel and operations. Substantially all of our earnings are expected to come from royalties generated from licensees, franchisees and similar contractual relationships involving IP that we acquire. Licensees, franchisees and other business partners are independent operators, and we will not exercise day-to-day control over any of them. As a result, our business will face a number of risks, including the following:

| | · | We expect that products using our IP will be manufactured by third party licensees, either directly or through third-party manufacturers on a subcontract basis. All manufacturers have limited production capacity, and the ones with whom we work (directly or indirectly) may not, in all instances, be able to satisfy manufacturing requirements for our (and our licensees’) products. |

| | · | We expect to provide limited training and support to franchisees. Consequently, franchisees may not successfully operate their businesses in a manner consistent with our standards and requirements, or may not hire and train qualified managers and other store personnel. |

| | · | While we will try to ensure that our licensees and other business partners maintain a high quality of products and services that use our IP, they may take actions that adversely affect the value of our IP or our business reputation. |

Our failure to protect proprietary rights that we acquire could decrease the value of those assets.

We expect to acquire a combination of trademarks, copyrights, franchise rights, service marks, trade secrets and similar intellectual property rights. The success of our IP business strategy will depend in part on our ability to license this intellectual property for use by third parties in selling various products and services and developing brand and product awareness in new geographic and product markets. Although we expect that much of our intellectual property will be protected by registration or other legal rules in the United States, in some cases registration may not be in place or available, particularly outside of the United States. In some cases, third parties may be using similar trademarks or other intellectual property in certain countries, and we may not be able to use certain of our intellectual property in those countries.

We intend to monitor on an ongoing basis unauthorized filings of registrations for our trademarks and other intellectual property and to rely primarily upon a combination of trademark, copyright, know-how, trade secrets and contractual restrictions to protect our intellectual property rights. We believe that such measures afford only limited protection and, accordingly, there can be no assurance that actions taken in the past, or that we take in the future, to establish and protect our proprietary rights will be adequate to prevent infringement by others, or prevent a loss of revenue or other damages. In addition, the laws of some countries do not protect intellectual property rights to the same extent as the laws of the United States.

We may be required to spend significant time and money on protecting or defending our intellectual property rights.

We may from time to time be required to institute litigation to enforce legal protections that we believe apply to intellectual property that we acquire, including to protect our trade secrets. Such litigation could result in substantial costs and diversion of resources and could negatively affect our sales, profitability and prospects, regardless of whether we are able to successfully enforce our rights. In addition, to the extent that any of the intellectual property we acquire is deemed to violate the proprietary rights of others, we could be prevented from using it, which could cause a termination of licensing and other commercial arrangements. This would adversely affect our revenues and cash flow. We also could be required to defend litigation brought against us, which can be costly and time-consuming. It could also result in a judgment or monetary damages being levied against us.

The acquisition of IP assets and IP-centric businesses will result in us recording a material amount of goodwill and other intangible assets on our balance sheet. If we are required to write down a portion of this goodwill and other intangible assets, our financial results would be adversely affected.

As a result of our acquisition strategy, certain identifiable intangible assets with indefinite lives which meet specified accounting criteria will consist of identifiable intangible assets and goodwill. We will not amortize goodwill. We may not be able to realize the full fair value of intangible assets with indefinite lives and goodwill from our acquisitions. We will evaluate on at least an annual basis whether all or a portion of identifiable intangible assets and goodwill and intangible assets may be impaired. Any write-down of intangible assets or goodwill resulting from future periodic evaluations would decrease our net income, and those decreases could be material.

Material weaknesses in disclosure controls and procedures and internal control over financial reporting of the businesses we acquire could adversely impact our ability to provide timely and accurate financial information.

The integration of acquisitions includes ensuring that our disclosure controls and procedures and our internal control over financial reporting effectively apply to and address the operations of newly acquired businesses. While we will make every effort to thoroughly understand any acquired entity’s business processes, our planning for proper integration into our company can give no assurance that we will not encounter operational and financial reporting difficulties impacting our controls and procedures. As a result, we may be required to change our disclosure controls and procedures or our internal control over financial reporting to accommodate newly acquired operations, and we may also be required to remediate historic weaknesses or deficiencies at acquired businesses. Our review and evaluation of disclosure controls and procedures and internal controls of the companies we acquire may take time and require additional expense, and if they are not effective on a timely basis could adversely affect our business and the market’s perception of our company.

Risks of Our Tax Loss Carry Forwards

We may not be able to realize value from our tax loss carry forwards.

As of December 31, 2006, we had federal net operating loss carry forwards of approximately $777 million that expire between 2011 and 2026. In addition, we had capital loss carry forwards of approximately $251 million that expire between 2006 and 2011. If we had an “ownership change” as defined in section 382 of the Internal Revenue Code, our net operating loss carry forwards and capital loss carry forwards generated prior to the ownership change would be subject to annual limitations, which could reduce, eliminate, or defer the utilization of these losses. Based upon a review of past changes in our ownership, as of December 31, 2006, we do not believe that we have experienced an ownership change (as defined under section 382) that would result in any limitation on our future ability to use these net operating loss and capital loss carry forwards. However, we can not assure you that the IRS or some other taxing authority may not disagree with our position and contend that we have already experienced such an ownership change, which would severely limit our ability to use our net operating loss carry forwards and capital loss carry forwards to offset future taxable income.

Generally, an ownership change occurs if one or more stockholders, each of whom owns 5% or more in value of a corporation’s stock, increase or decrease their aggregate percentage ownership by 50% or more as compared to the lowest percentage of stock owned by such stockholders at any time during the preceding three-year period. For example, if a single stockholder owning 10% of our stock acquired an additional 50% of our stock in a three-year period, a change of ownership would occur. Similarly, if ten persons, none of whom owned our stock, each acquired slightly over 5% of our stock within a three-year period (so that such persons own, in the aggregate more than 50%) an ownership change would occur. Ownership of stock is determined by certain constructive ownership rules which can attribute ownership of stock owned by entities (such as estates, trusts, corporations, and partnerships) to the ultimate indirect owner.

For purposes of this rule, all holders who each own less than 5% of a corporation’s stock are generally treated together as one (or, in certain cases, more than one) 5% stockholder. Transactions in the public markets among stockholders owning less than 5% of the equity securities generally are not included in the calculation. Special rules can result in the treatment of options (including warrants) or other similar interests as having been exercised if such treatment would result in an ownership change.

On July 12, 2005, our stockholders approved a holding company reorganization in which each share of what was then Aether Systems common stock was exchanged for one share of common stock of a new holding company (then called Aether Holdings, and now called NexCen Brands). As a result of this transaction, shares of our common stock are subject to transfer restrictions contained in our certificate of incorporation. In general, the transfer restrictions prohibit any person from acquiring more than 5% of our stock without our consent. Persons who owned 5% or more of our stock prior to May 4, 2005 are permitted to sell the shares owned as of May 4, 2005 without regard to the transfer restrictions. Shares acquired by such persons after May 4, 2005 are subject to the transfer restrictions. While we expect that these transfer restrictions will help guard against an ownership change occurring under section 382 and the related rules, because we are using stock as consideration to make acquisitions, and because we may decide (or need) to sell additional shares of our common stock in the future to raise capital for our business and because persons who held more than 5% of our stock prior to these restrictions taking effect can sell (and in some cases have sold) shares of our stock, we cannot guarantee that these restrictions will prevent a change of ownership from occurring.

We may not be able to use our tax loss carry forwards because we may not generate taxable income.

The use of our net operating loss carry forwards is subject to uncertainty because it is dependent upon the amount of taxable income we generate. Similarly, the extent of our actual use of our capital loss carry forwards is also subject to uncertainty because their use depends on the amount of capital gains we generate. There can be no assurance that we will have sufficient taxable income (or capital gains) in future years to use the net operating loss carry forwards or capital loss carry forwards before they expire. This is especially true for our capital loss carry forwards, because they expire over a shorter period of time than our net operating loss carry forwards.

The IRS could challenge the amount of our tax loss carry forwards.

The amount of our net operating loss carry forwards and capital loss carry forwards has not been audited or otherwise validated by the IRS. The IRS could challenge the amount of our net operating loss carry forwards and capital loss carry forwards, which could result in an increase in our liability for income taxes. In addition, calculating whether an ownership change has occurred is subject to uncertainty, both because of the complexity and ambiguity of section 382 and because of limitations on a publicly traded company’s knowledge as to the ownership of, and transactions in, its securities. Therefore, we cannot assure you that the calculation of the amount of our net loss carry forwards may not be changed as a result of a challenge by a governmental authority or our learning of new information about the ownership of, and transactions in, our securities.

We expect to be subject to state, local and foreign taxes, as well as the alternative minimum tax. Our net loss carry forwards would not offset the alternative minimum tax in its entirety.

We will continue to be subject to state, local and foreign taxes. As a result of our capital loss carry forwards and net operating loss carry forwards, we anticipate our federal income tax liability over the next several years will be reduced substantially. However, we expect to be subject to the alternative minimum tax provisions of the Internal Revenue Code which limits the use of net operating loss carry forwards. These provisions would result, in effect, in 10% of our alternative minimum taxable income being subject to the 20% alternative minimum tax assessed on corporations. This amounts to a 2% effective tax rate on our alternative minimum taxable income.

The IRS may seek to impose the accumulated earnings tax on some or all of the taxable income we retain.

We expect to retain all or a substantial portion of future earnings over the next several years to finance the development and growth of our IP business. As a result, we may not declare or pay any significant dividends on shares of our common stock for an extended period. If the IRS believed we were accumulating earnings beyond our reasonable business needs, the IRS could seek to impose an accumulated earnings tax, or AET, of 15% on our accumulated taxable income. We do not believe that we will be subject to the AET due to various reasons, including the existence of our large deficit in accumulated earnings and profits. However, the IRS may disagree with us on this point, and the IRS may attempt to impose the AET on all or a portion of our taxable income. In such event, we would expect to challenge any attempt by the IRS to impose the AET on our business, but the outcome of such a challenge is uncertain.

If we distributed our accumulated taxable income for each year to our stockholders as dividends, we would not be subject to the AET for the amounts so distributed, but would be subject to the AET only for the amount of earnings retained. If we paid dividends to stockholders out of current earnings, these dividends would, generally speaking, be eligible to be treated as “qualified dividends” for federal income tax purposes, taxed at the current maximum federal rate of 15%, assuming that the recipient stockholder met the various requirements under the Internal Revenue Code for such treatment. The maximum rate for qualified dividends is currently projected to increase to the maximum federal income tax rate applicable to ordinary income (currently 35%) for tax years beginning after December 31, 2008 in accordance with the Jobs and Growth Tax Relief Reconciliation Act of 2003.

Limits on ownership of our common stock could have an adverse consequence to you and could limit your opportunity to receive a premium on our stock.

As noted above, it is important that we avoid an ownership change under section 382 of the Internal Revenue Code, in order to retain the ability to use our net operating loss carry forwards and capital loss carry forwards to offset future income. Under transfer restrictions that have been applicable to our common stock since 2005, no one is permitted to acquire 5% or more of our stock without the consent of our Board of Directors. In addition, even if our Board of Directors consented to a significant stock acquisition, a potential buyer might be deterred from acquiring our common stock while we still have significant tax losses being carried forward, because such an acquisition might trigger an ownership change and severely impair our ability to use our tax losses against future income. Thus, this potential tax situation could have the effect of delaying, deferring or preventing a change in control and, therefore, could affect adversely our shareholders’ ability to realize a premium over the then prevailing market price for our common stock in connection with a change in control.

The transfer restrictions that apply to shares of our common stock, although designed as a protective measure to avoid an ownership change, may have the effect of impeding or discouraging a merger, tender offer or proxy contest, even if such a transaction may be favorable to the interests of some or all of our shareholders. This effect might prevent our stockholders from realizing an opportunity to sell all or a portion of their common stock at a premium to the prevailing market price.

None.

ITEM 2. PROPERTIES

As of December 31, 2006, we leased a total of approximately 16,450 square feet of office space. Our principal offices total 10,250 square feet and are located in New York, NY. The Athlete’s Foot office is located in Norcross, GA and totals 6,200 square feet of leased office space. In addition, we maintain a lease for space in Marlborough, Massachusetts that we used for the Mobile Government business that we sold in 2005. We have sublet this office space to BIO-Key International, Inc., the company that purchased the Mobile Government business (“BIO-Key”). We believe that our retained facilities are adequate for the purposes for which they are presently used and that replacement facilities are available at comparable cost, should the need arise.

As we acquire additional businesses, we expect to own or lease additional office space. Such additions may come through assuming leases of businesses we acquire, purchasing property owned by acquired businesses as part of the acquisitions, or entering into new leases either to consolidate operations in multiple locations or to accommodate the needs of our business as it expands. We do not own or lease property used by our franchisees.

ITEM 3. LEGAL PROCEEDINGS

IPO Litigation. NexCen is among the hundreds of defendants named in a series of class action lawsuits seeking damages due to alleged violations of securities law. The case is being heard in the United States District Court for the Southern District of New York. The court has consolidated the actions by all of the named defendants that actually issued the securities in question. There are approximately 310 consolidated cases before Judge Scheindlin, including this action, under the caption In Re Initial Public Offerings Litigation, Master File 21 MC 92 (SAS).

As to NexCen, these actions were filed on behalf of persons and entities that acquired the Company’s stock after its initial public offering in October 20, 1999. Among other things, the complaints claim that prospectuses, dated October 20, 1999 and September 27, 2000 and issued by NexCen in connection with the public offerings of common stock, allegedly contained untrue statements of material fact or omissions of material fact in violation of securities laws because the prospectuses allegedly failed to disclose that the offerings’ underwriters had solicited and received additional and excessive fees, commissions and benefits beyond those listed in the arrangements with certain of their customers which were designed to maintain, distort and/or inflate the market price of the Company’s common stock in the aftermarket. The actions seek unspecified monetary damages and rescission. NexCen believes the claims are without merit and is vigorously contesting these actions.

After initial procedural motions and the start of discovery in 2002 and 2003, the plaintiffs voluntarily dismissed without prejudice the officer and director defendants of each of the 310 named issuers, including NexCen. Then in June 2003, the Plaintiff’s Executive Committee announced a proposed settlement with the issuer-defendants, including NexCen, and the officer and director defendants of the issuers (the “Issuer Settlement”). A settlement agreement was signed in 2004 and presented to the District Court for approval. The proposed Issuer Settlement does not include the underwriter-defendants, and they have continued to defend the actions and have objected to the proposed settlement. (One of the defendant-underwriters signed a memorandum of understanding in April 2006 agreeing to a $425 million settlement of claims against it.) Under terms of the proposed Issuer Settlement, NexCen has a reserve of $465,000 for its estimated exposure. If the proposed settlement is approved by the court, it is extremely unlikely that NexCen would incur any material financial or other liability.

The District Court granted preliminary approval of the proposed Issuer Settlement in 2005 and held a fairness hearing on the matter in April 2006. In December 2006, before final action by the District Court on the proposed Issuer Settlement, the U.S. Court of Appeals for the Second Circuit issued a ruling vacating class certification for certain plaintiffs in the actions against the underwriter-defendants. A petition was filed in early 2007 seeking rehearing of this decision, but the Second Circuit had not acted on the petition as of March 1, 2007. The impact of this decision on the claims against the issuer-defendants (including NexCen) and on the proposed Issuer Settlement is unclear. Since December 2006, the District Court has stayed all proceedings in these cases pending further action by the Second Circuit.

Transportation Business Sale. On March 13, 2006, a complaint captioned Geologic Solutions, Inc. v. Aether Holdings, Inc. was filed against the Company in the Supreme Court for the State of New York, New York County. The complaint generally alleges that plaintiff Geologic was damaged as a result of certain alleged breaches of contract and fraudulent inducement arising out of NexCen’s alleged misrepresentations and failure to disclose certain information in connection with the asset purchase agreement dated as of July 20, 2004 for the purchase and sale of our Transportation business. The allegations in Geologic’s complaint are substantially similar to claims Geologic made in a previous request to the Company for indemnification. The complaint seeks monetary damages in an amount not less than $30 million and other relief. During the second quarter of 2006, the plaintiff agreed to substitute Aether Systems, Inc. for Aether Holdings, Inc. as defendant in the case because Aether Systems, Inc. was the party to the asset purchase agreement upon which Geologic’s claims are based. We believe we have a meritorious defense to Geologic’s claims and are vigorously defending against this action; however, we cannot predict the outcome of this litigation, and an adverse resolution of such claims could require us to make a significant cash payment to Geologic. We have incurred costs in connection with the defense of this lawsuit, which have been recorded against discontinued operations, further increasing the loss on the sale of the Transportation segment, and decreasing the amount of cash we have available for acquisitions and operations.

Legacy UCC Litigation. UCC and Mr. D’Loren in his capacity as president of UCC are parties along with unrelated parties to litigation resulting from a default on a loan to The Songwriter Collective, LLC (“TSC”), which UCC had referred to a third party. A shareholder of TSC filed a lawsuit in the U.S. District Court for the Middle District of Tennessee alleging, that certain misrepresentations by TSC and its agents (including UCC and D’Loren) induced the shareholder to contribute certain rights to musical compositions to TSC. The lawsuit, which is captioned Tim Johnson v. Fortress Credit Opportunities I, L.P., et al., seeks declaratory judgment, reformation and rescission, and monetary damages relating to the loan and alleged loss of value on contributed assets. UCC and Mr. D’Loren have filed cross-claims against TSC and certain TSC officers claiming indemnity. TSC has filed various cross and third-party claims against UCC, Mr. D’Loren and another TSC shareholder, Annie Roboff. Roboff has filed a separate action in the Chancery Court in Davidson County, Tennessee, which is captioned Roboff v. Mason, et al., as well as claims in the federal court lawsuit, against UCC, Mr. D’Loren, TSC and the other parties. The claims include fraud and negligent misrepresentation allegations against Mr. D’Loren, and UCC. Ms. Roboff previously made these same claims in a lawsuit that she filed in state court in New York. That lawsuit was dismissed on procedural grounds, and Ms. Roboff has appealed the dismissal. UCC believes these claims are without merit and is vigorously defending the actions. UCC’s insurance carrier is defending the litigation. The litigation is in discovery and the outcome cannot be estimated at this time; however, settlement discussions are being held. The loss, if any, could exceed existing insurance coverage and any excess could adversely affect our financial condition and results.

Other. In addition to the matters discussed above, we become involved from time to time in other litigation in the ordinary course of our business. As of the date of this Report, there are no other proceedings that management considers material to the Company.

On October 31, 2006, the Company held its Annual Meeting, at which six proposals were presented to the Company’s stockholders for consideration. The six matters presented for consideration were: (1) a proposal to approve the sale of the Company’s existing MBS portfolio for the purpose of discontinuing the Company’s MBS business and allocating all cash proceeds from such sale to the growth and development of the IP business; (2) a proposal to amend the Certificate of Incorporation to change the Company’s name to “NexCen Brands, Inc.”; (3) the election of eight directors to hold office until the 2007 Annual Meeting of Stockholders or until their successors are elected and qualified; (4) a proposal to ratify the appointment of KPMG LLP as the Company’s independent registered public accounting firm for the fiscal year ending December 31, 2006; (5) a proposal to approve the adoption of the Company’s 2006 Long-Term Equity Incentive Plan (the “2006 Plan”); and (6) a proposal to approve the adoption of the 2006 Management Bonus Plan (the “Bonus Plan”).