Keefe, Bruyette & Woods

2008 Large Cap Bank Conference

12 August ■ Colorado Springs, CO

Forward-Looking Statements

This presentation contains statements that relate to the projected performance of

Zions Bancorporation and elements of or affecting such performance, including

statements with respect to the beliefs, plans, objectives, goals, guidelines,

expectations, anticipations and estimates of management. These statements

constitute forward-looking information within the meaning of the Private Securities

Litigation Reform Act. Actual facts, determinations, results or achievements may

differ materially from the statements provided in this presentation since such

statements involve significant known and unknown risks and uncertainties. Factors

that might cause such differences include, but are not limited to: competitive

pressures among financial institutions; economic, market and business conditions,

either nationally or locally in areas in which Zions Bancorporation conducts its

operations, being less favorable than expected; changes in the interest rate

environment reducing expected interest margins; changes in debt, equity and

securities markets; adverse legislation or regulatory changes and other factors

described in Zions Bancorporation’s Annual Report on Form 10-K for the year

ended December 31, 2007. In addition, the statements contained in this

presentation are based on facts and circumstances as understood by management

of the company on the date of this presentation, which may change in the future.

Zions Bancorporation disclaims any obligation to update any statements or to

publicly announce the result of any revisions to any of the forward-looking

statements included herein to reflect future events, developments, determinations or

understandings.

Zions Bancorporation and elements of or affecting such performance, including

statements with respect to the beliefs, plans, objectives, goals, guidelines,

expectations, anticipations and estimates of management. These statements

constitute forward-looking information within the meaning of the Private Securities

Litigation Reform Act. Actual facts, determinations, results or achievements may

differ materially from the statements provided in this presentation since such

statements involve significant known and unknown risks and uncertainties. Factors

that might cause such differences include, but are not limited to: competitive

pressures among financial institutions; economic, market and business conditions,

either nationally or locally in areas in which Zions Bancorporation conducts its

operations, being less favorable than expected; changes in the interest rate

environment reducing expected interest margins; changes in debt, equity and

securities markets; adverse legislation or regulatory changes and other factors

described in Zions Bancorporation’s Annual Report on Form 10-K for the year

ended December 31, 2007. In addition, the statements contained in this

presentation are based on facts and circumstances as understood by management

of the company on the date of this presentation, which may change in the future.

Zions Bancorporation disclaims any obligation to update any statements or to

publicly announce the result of any revisions to any of the forward-looking

statements included herein to reflect future events, developments, determinations or

understandings.

Today’s Agenda

Current Issues |

Credit |

Lockhart Funding |

Investment Portfolio |

Net Interest Margin |

Capital & Dividends |

Outlook Summary |

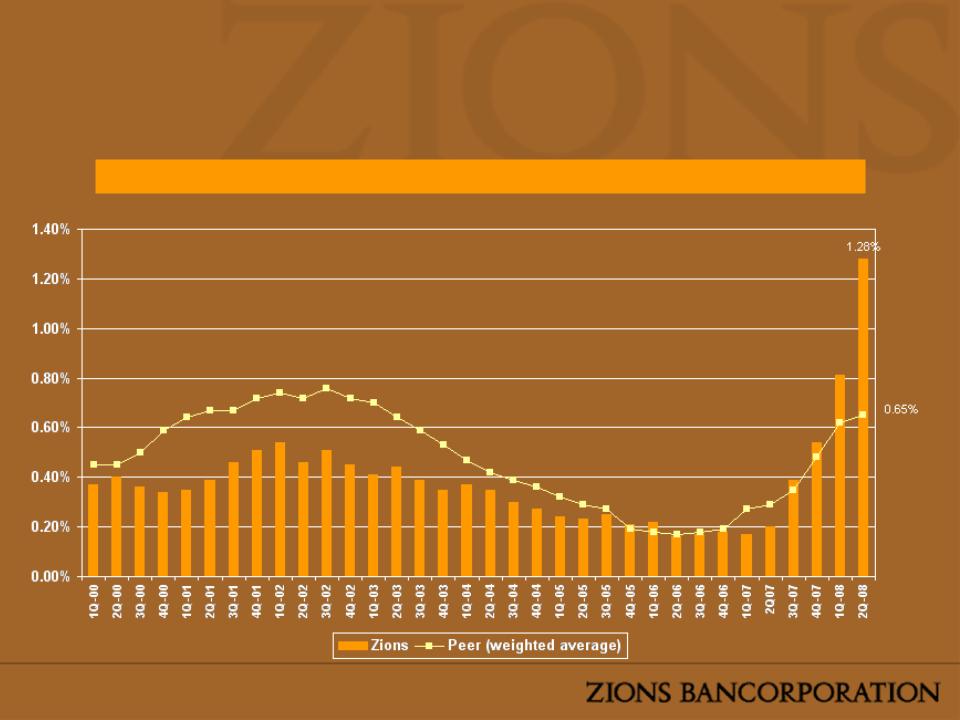

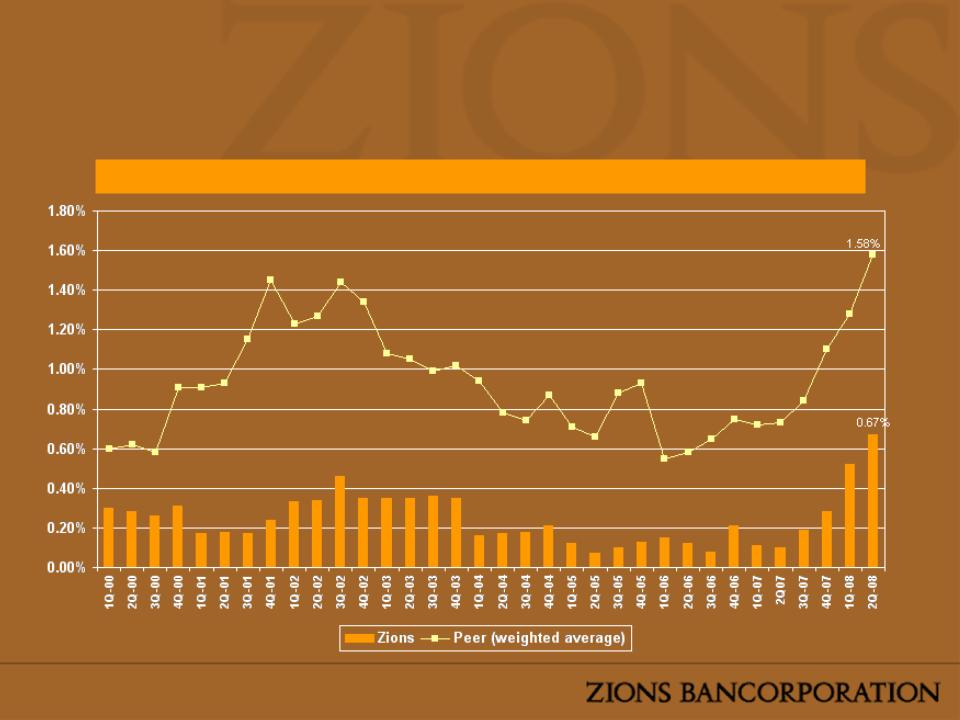

Note: Peer group defined as bank holding companies with assets >= $10 billion. At the date of this data was

not yet available for 2 of the 50 companies in the peer group.

not yet available for 2 of the 50 companies in the peer group.

Peer data source: SNL

NPAs as % of Total Assets

Strong Asset Quality

Relative to Peers

Relative to Peers

NCOs as % of Average Total Loans (Annualized)

Note: Peer group defined as bank holding companies with assets >= $10 billion.

Peer data source: SNL

Strong Asset Quality

Relative to Peers

Relative to Peers

Peers

1.5

Reserves / Net Charge Offs (Annualized)

Note: Peer group defined as bank holding companies with assets >= $10 billion.

Peer data source: SNL

Zions 2.0

Strong Asset Quality

Relative to Peers

Relative to Peers

2nd Quarter Reserves / Net Charge Offs (Annualized)

Source: SNL As Reported NIM for selected banks ($5-$20 Billion Market Cap or

Large Presence in the West)

Large Presence in the West)

Strong Asset Quality

Relative to Peers

Relative to Peers

C&I

47%

Consumer

18%

CRE

34%

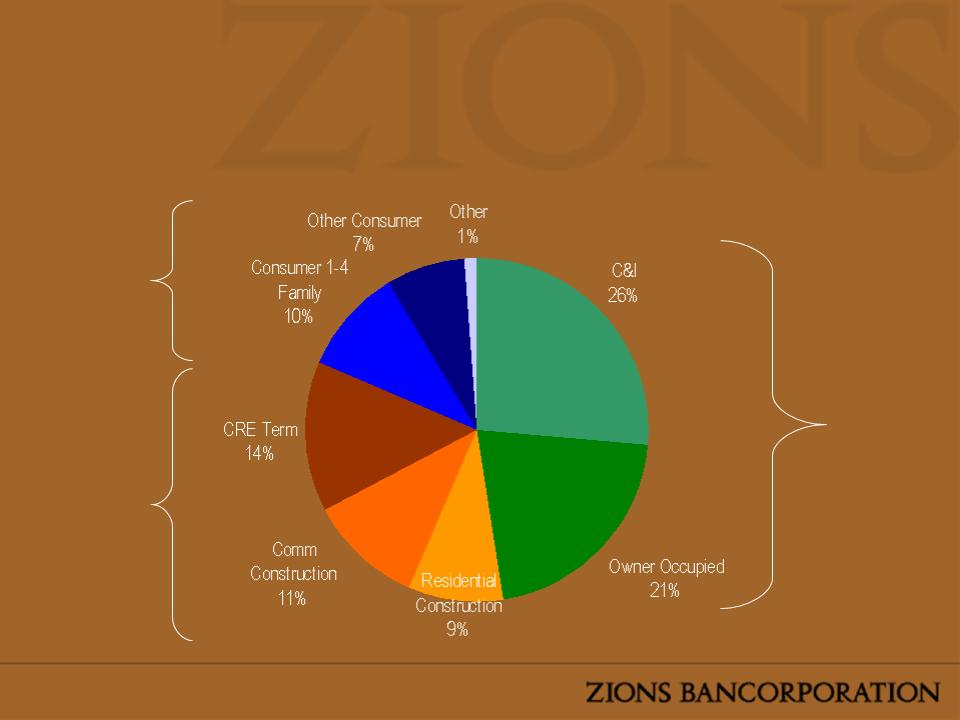

Loan Portfolio Diversification

Loans by Purpose - 6/30/2008

Loans by Purpose - 6/30/2008

Total Outstanding: $1.9 billion (6/30/08)

Residential Mortgage Loans

Total Outstanding: $0.2 billion (6/30/08)

Bankcard

Total Outstanding: $1.8 billion (6/30/08)

Average HECL FICO: 756

HECL Only

Commercial & Industrial Loans

Commercial Real Estate Loans

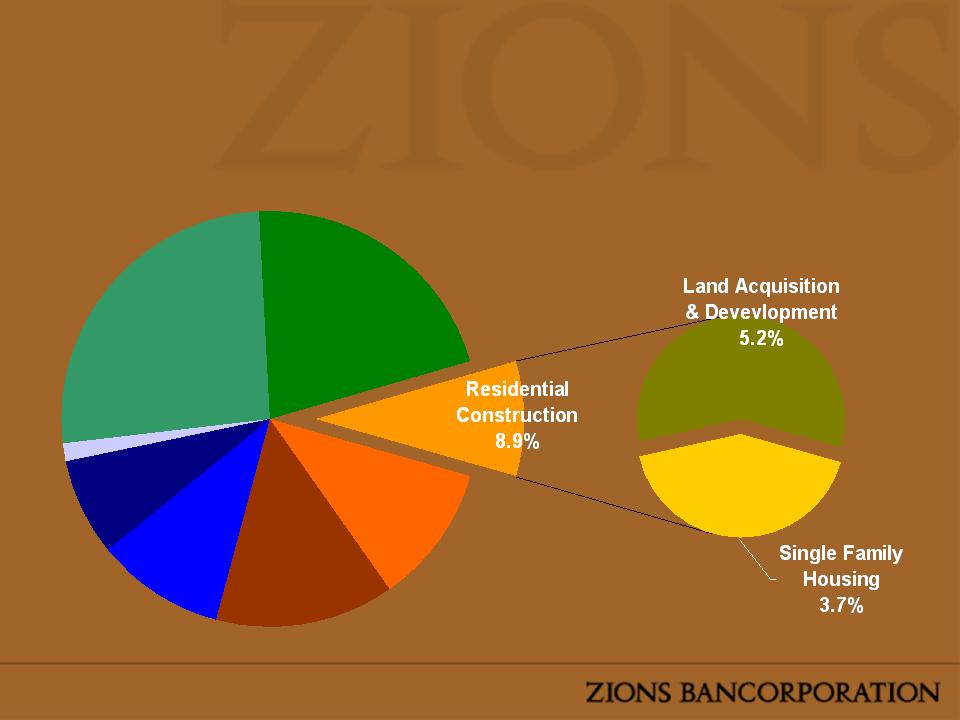

Residential Construction Components

Loans by Purpose - 6/30/2008

Loans by Purpose - 6/30/2008

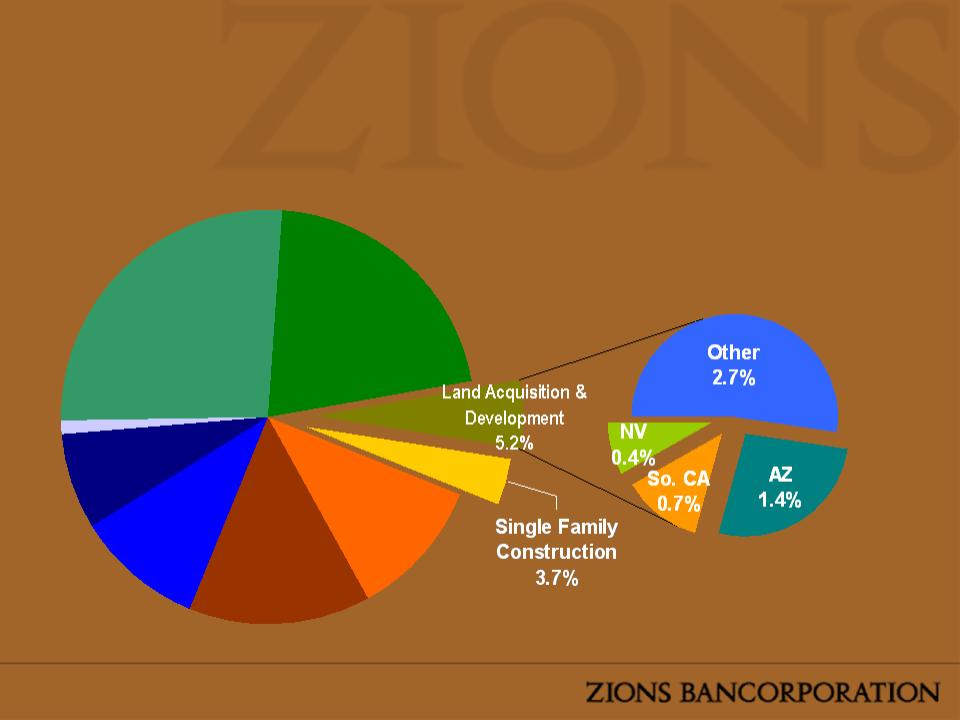

Land Acquisition & Dev. Components

Loans by Purpose by Geography - 6/30/2008

Loans by Purpose by Geography - 6/30/2008

Average LTV: 55.7% (as of 6/30/2008)

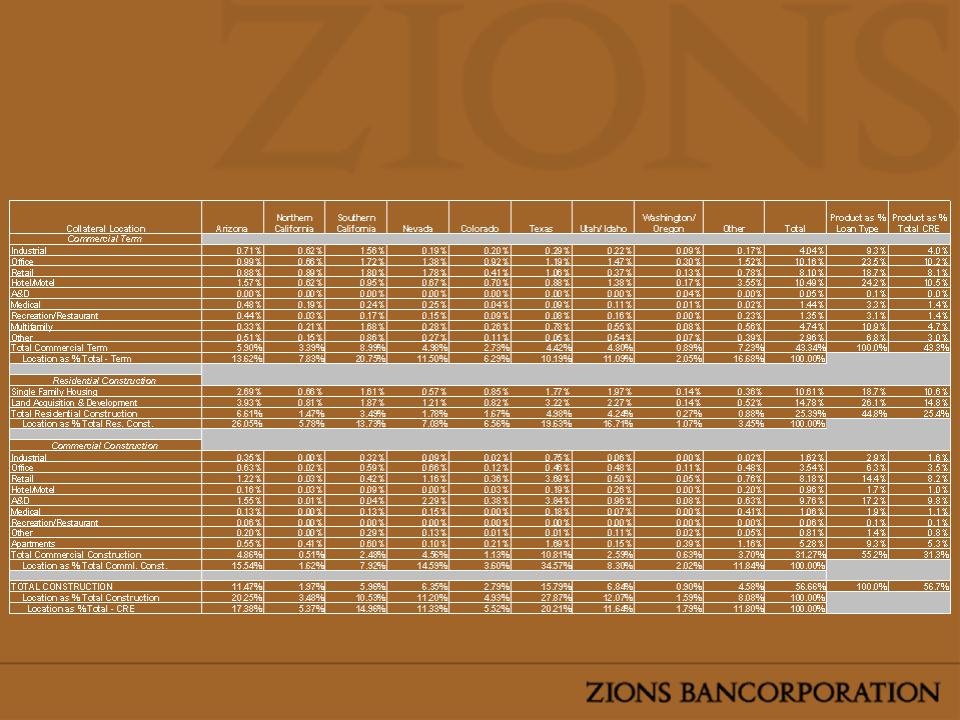

Diversified CRE Portfolio

Loans by Product Type and Location - 06/30/08

Loans by Product Type and Location - 06/30/08

Average LTV: 55.7% (as of 6/30/2008)

*LTVs for CRE loans with a commitment amount of $1MM or greater. Appraisals as of loan

origination, or renewal (in a declining market), or upon adverse classification.

origination, or renewal (in a declining market), or upon adverse classification.

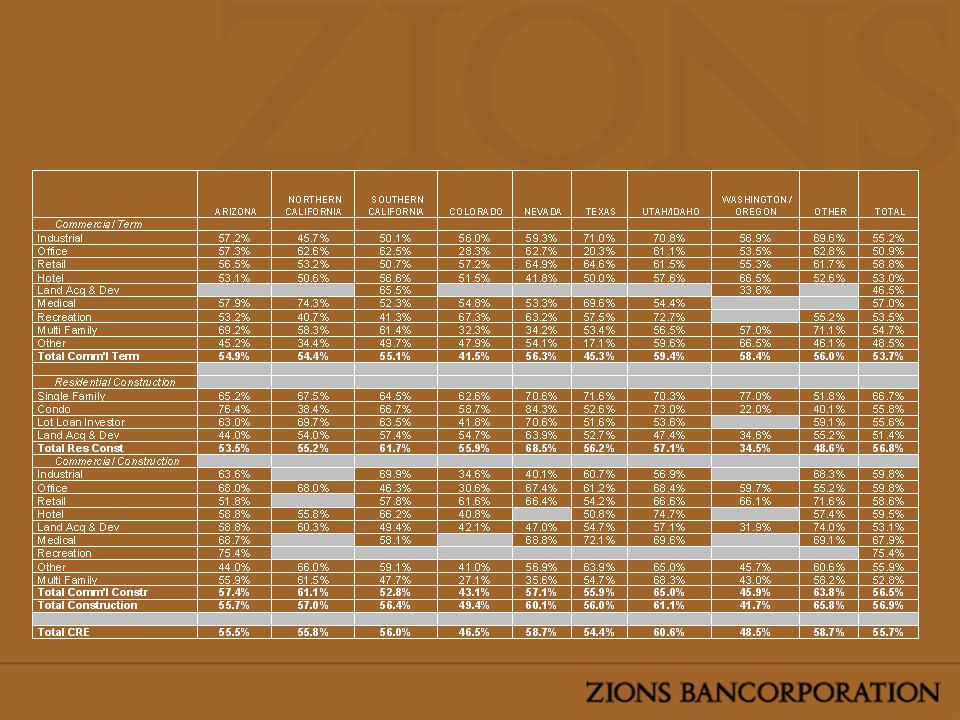

Actual CRE LTV Ratios*

Loans by Product Type and Location - 06/30/08

Loans by Product Type and Location - 06/30/08

*60 of the 216 updated appraisals come from affiliates not shown on the table above (UT, CO, and TX).

**Jan-08 LTV’s based on initial appraisal or reappraisal prior to Jan. 2008

Jun-08 LTV’s based on most recent reappraisal post Jan. 2008

Loan-to-Value Comparison

For Residential A&D & Lot Loans reappraised between Jan 08 to Jun 08

For Residential A&D & Lot Loans reappraised between Jan 08 to Jun 08

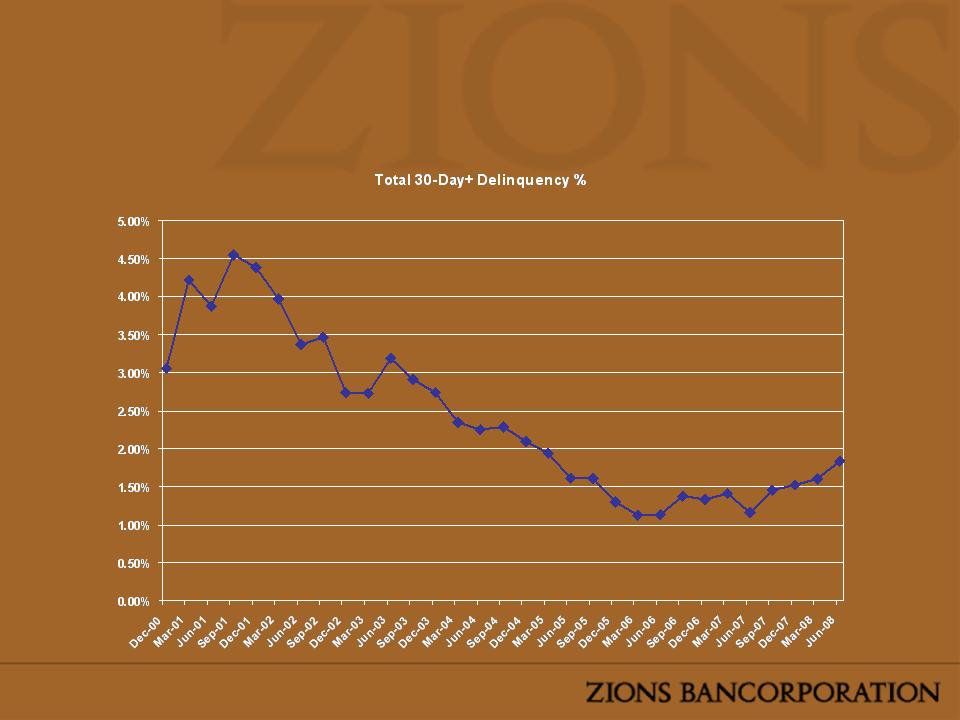

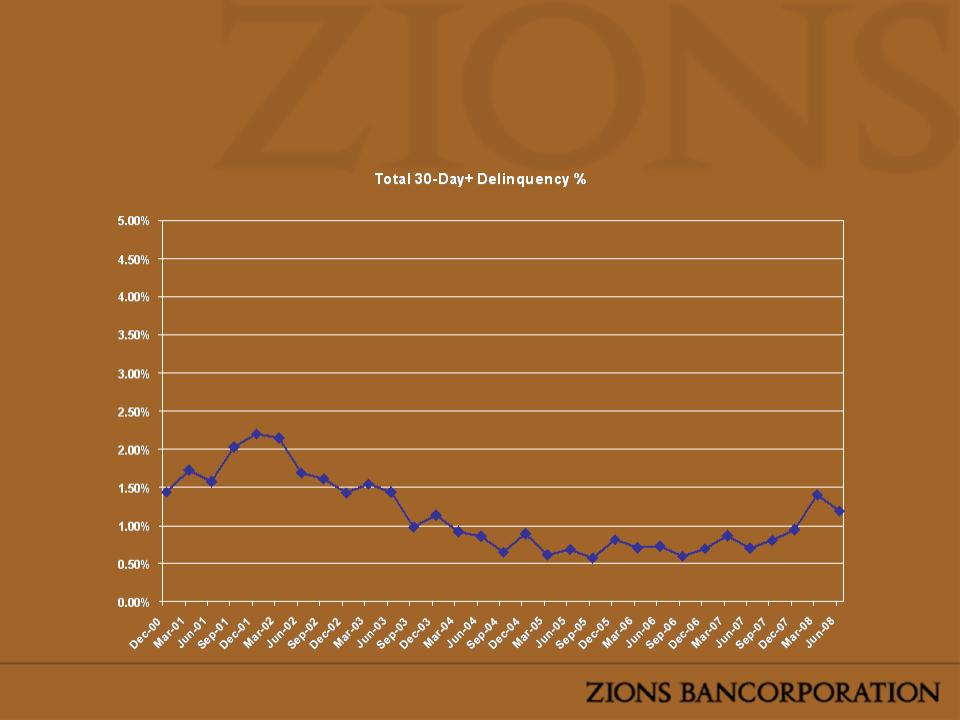

Strong underwriting and credit management

reduced losses almost by half

reduced losses almost by half

Note: Includes Top 20 substandard loans each quarter and all doubtful loans greater than $1 million.

Impact of Re-Margining

• Of the 50 largest credits classified

substandard or doubtful at any time during

the past 9 months there’s been

substandard or doubtful at any time during

the past 9 months there’s been

– $117 million in charge-offs

– $104 million in new equity through re-margining

Residential Land and

Development Loans

6/30/2008

Development Loans

6/30/2008

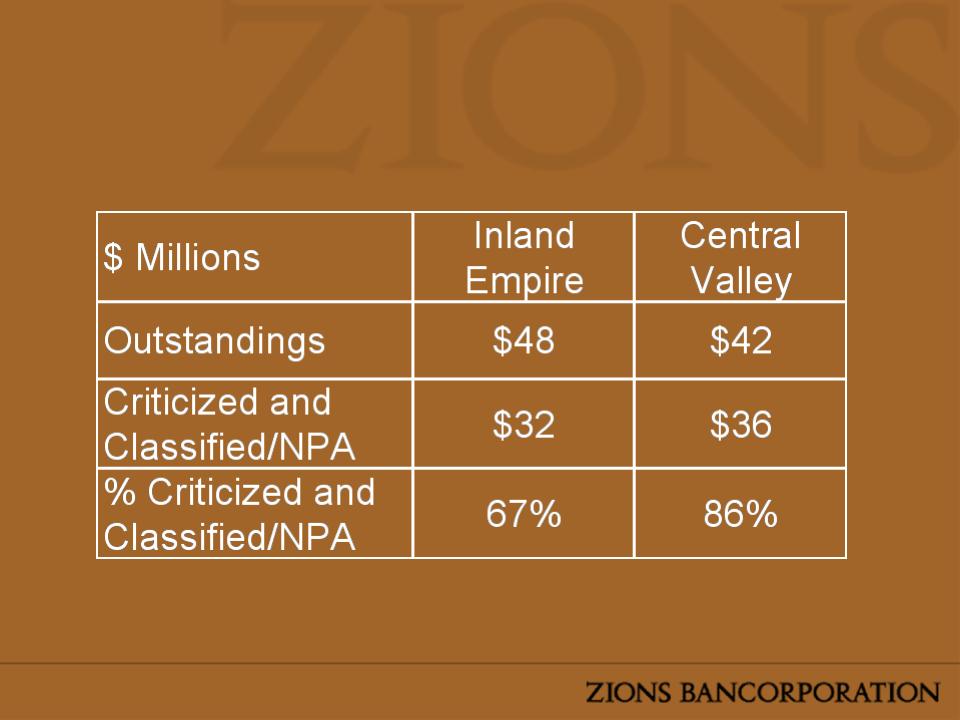

Select California Loan Views:

6/30/2008

6/30/2008

Credit Quality

Outlook

Outlook

• Weakness in residential construction activity and

land values in the Southwest expected to persist into

2009

land values in the Southwest expected to persist into

2009

• No current evidence of material spread of credit

problems to other geographies or loan categories

problems to other geographies or loan categories

• Some further increase in NPAs likely

• Provisions and Net Losses likely to remain at similar

levels to 2nd Quarter 2008

levels to 2nd Quarter 2008

• Charge-offs in California likely to decline

Loan Growth

Outlook

Outlook

• Loan demand and pricing are strong

across the footprint

across the footprint

• Managing balance sheet growth in the

context of current capital generation

and funding capabilities

context of current capital generation

and funding capabilities

Today’s Agenda

Current Issues |

Credit |

Lockhart Funding |

Investment Portfolio |

Net Interest Margin |

Capital & Dividends |

Outlook Summary |

As of 6-30-08

GAAP capital impact if remaining Net Lockhart exposure is brought on the balance sheet

(including impact of fair value marks): -12 bps

(including impact of fair value marks): -12 bps

10/31/07 | Corporate Purch. & Paydowns | 06/30/08 | |

AAA MBIA insured (small business loans originated by Zions) | $1.2B | $-1.2B | $0.0B |

AAA rated bank trust pref’d pools | $1.1B | $-0.6B | $0.5B |

US gov’t & agencies | $0.3B | $-0.1B | $0.2B |

Other insured | $0.2B | $-0.1B | $0.1B |

Other structured | $0.3B | $-0.16B | $0.04B |

Total | $3.1B | $-2.2B | $.86B |

Lockhart Funding

Today’s Agenda

Current Issues |

Credit |

Lockhart Funding |

Investment Portfolio |

Net Interest Margin |

Capital & Dividends |

Outlook Summary |

6-30-08

(in Billions)

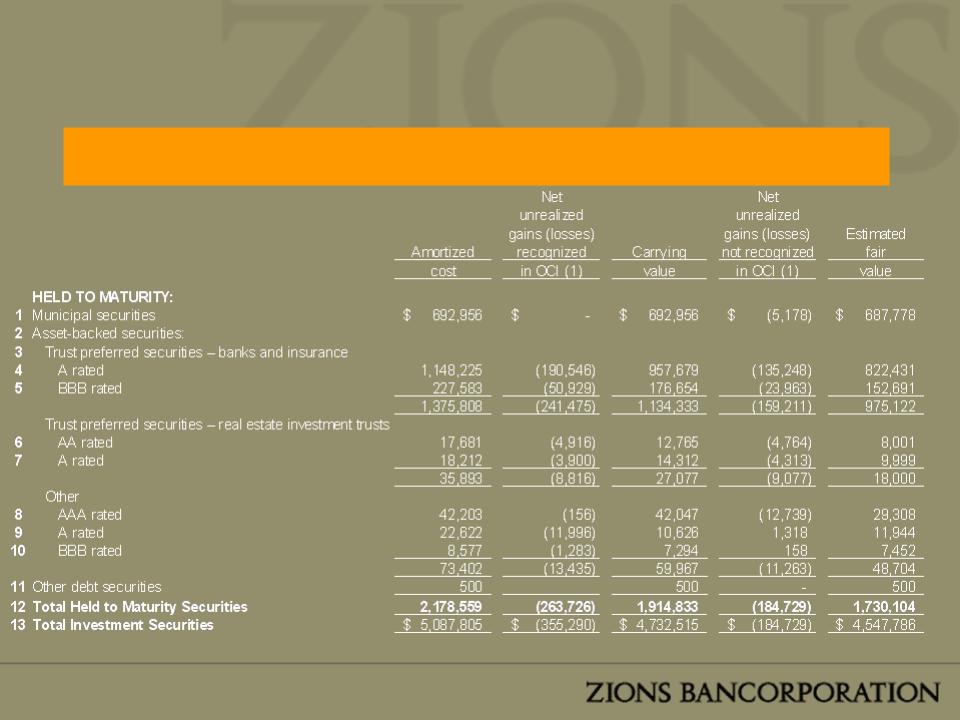

*All fair value marks have been recognized through OCI

Held to Maturity Securities

*All fair value marks have been recognized through OCI

6-30-08

(in Billions)

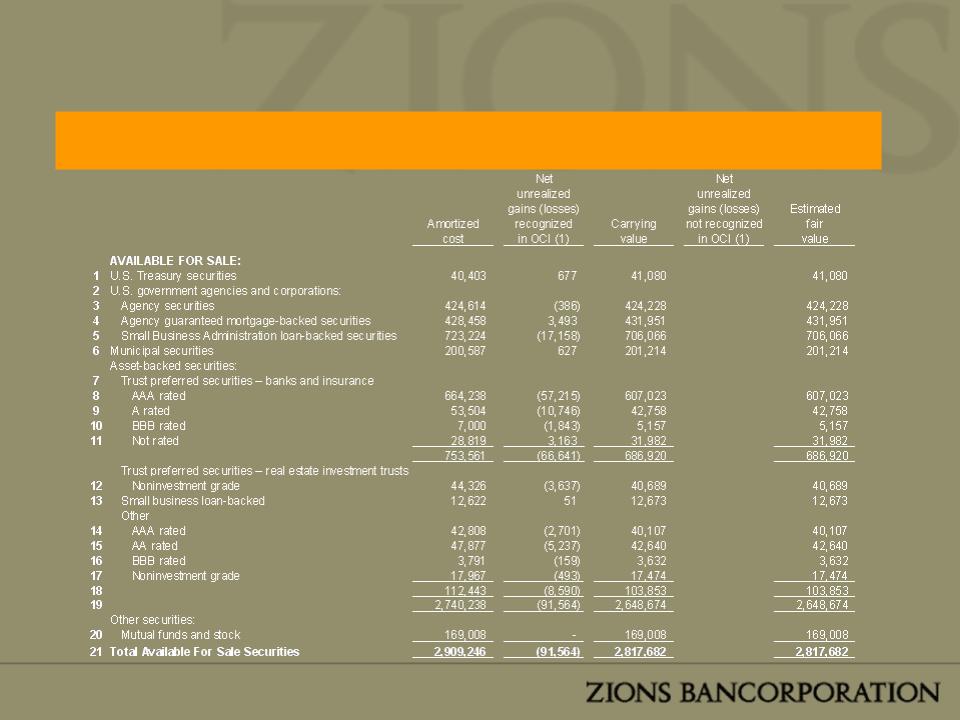

Available for Sale Securities

Securities Transferred to Held To

Maturity

Maturity

• $1.500 billion of predominantly A-rated (or higher) Bank &

Insurance Trust Preferred CDO securities transferred from

AFS to HTM on April 30, 2008

Insurance Trust Preferred CDO securities transferred from

AFS to HTM on April 30, 2008

– $1.227 billion fair value

– $273 million unrealized pre-tax losses from marks in OCI accrete

back into tangible equity over remaining life of securities

back into tangible equity over remaining life of securities

• No other future impacts on OCI, earnings, and capital

unless a security were to become Other Than Temporarily

Impaired (OTTI)

unless a security were to become Other Than Temporarily

Impaired (OTTI)

Today’s Agenda

Current Issues |

Credit |

Lockhart Funding |

Investment Portfolio |

Net Interest Margin |

Capital & Dividends |

Outlook Summary |

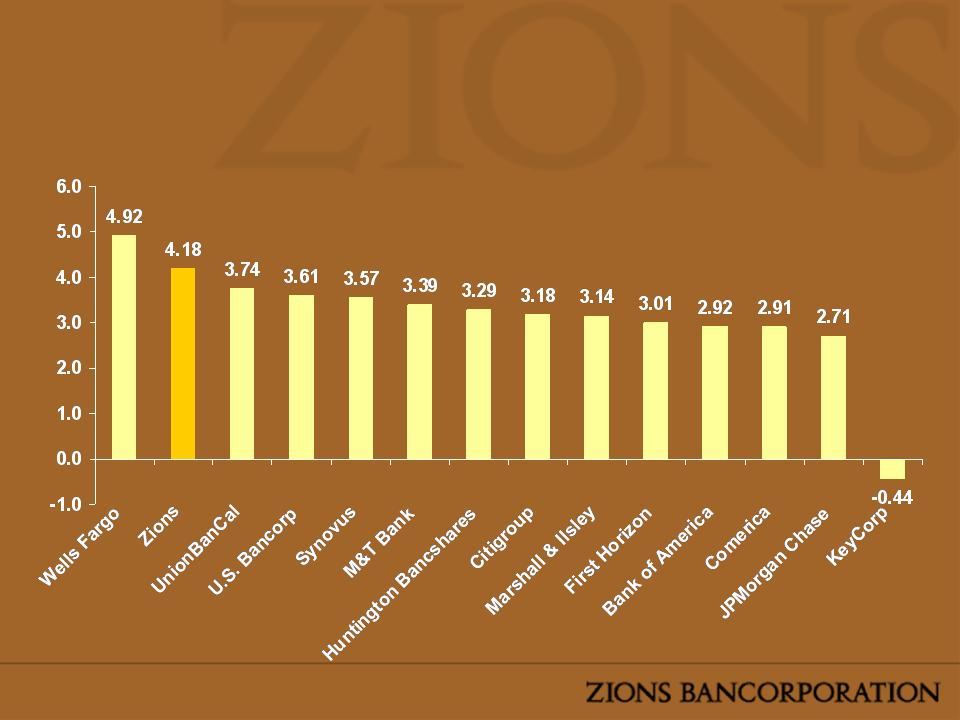

A High Net Interest Margin

2Q 2008 NIM for Selected Banks

2Q 2008 NIM for Selected Banks

Source: SNL As Reported NIM for selected banks ($5-$20 Billion Market Cap or

Large Presence in the West)

Large Presence in the West)

Zions NIM vs. 30-Day LIBOR

A Stable Net Interest Margin

in a Volatile Environment

in a Volatile Environment

Source: SNL As Reported NIM (Top 50 Banks by Assets)

LIBOR is Quarter Average

NIM Outlook

• Positives

– Loan pricing

• Pressures

– Continued strong competition for deposits

– Weak core deposit growth

– Adverse shifting of funding mix

– Increasing NPA’s

• Summary: Still some downward pressure

Today’s Agenda

Current Issues |

Credit |

Lockhart Funding |

Investment Portfolio |

Net Interest Margin |

Capital & Dividends |

Outlook Summary |

Zions Bancorporation Actual / Pro

Forma Capital Ratios

Forma Capital Ratios

Dividend Summary

Today’s Agenda

Current Issues |

Credit |

Lockhart Funding |

Investment Portfolio |

Net Interest Margin |

Capital & Dividends |

Outlook Summary |

• Managing balance sheet growth in the context of current capital

generation and funding capabilities

generation and funding capabilities

• Low cost deposit growth: Continues to be weak

• Security impairment charges may continue at 1H 2008 levels

• Credit costs: Similar to 2Q through year end, perhaps slight

increase

increase

• Net Interest Margin: Modest downward pressure

• Capital and Dividend:

– Continue to look for opportunities to raise $200-300 million of core capital

• Mitigate growth constraints and strengthen capital ratios

• We’re sensitive to dilution

– No plans to cut dividend

Outlook Summary

Keefe, Bruyette & Woods

12 August 2008