16

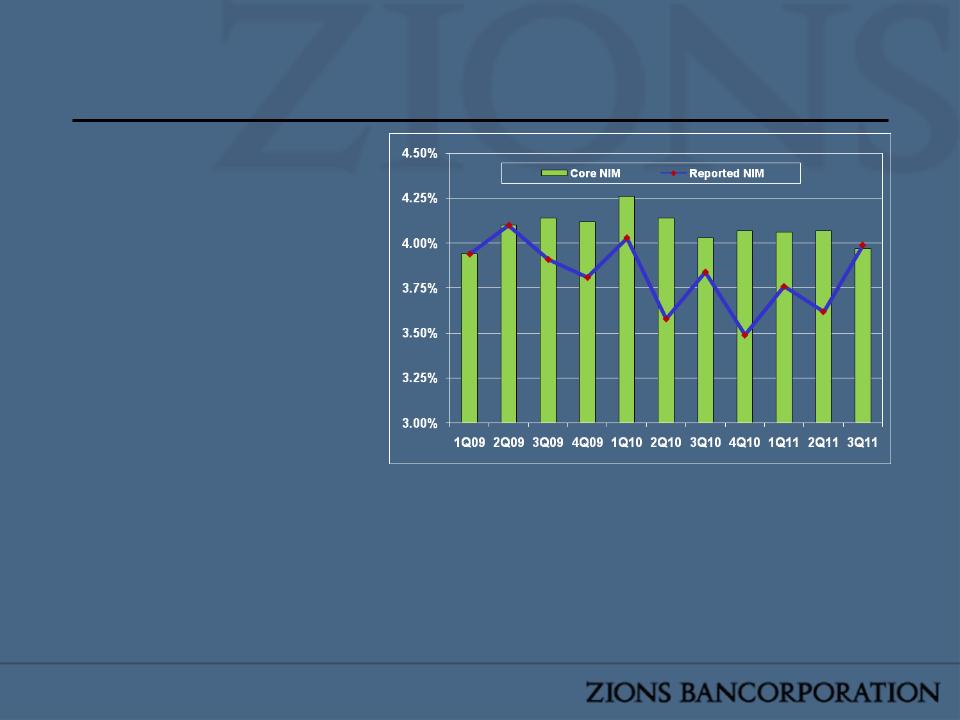

Core NIM Trends

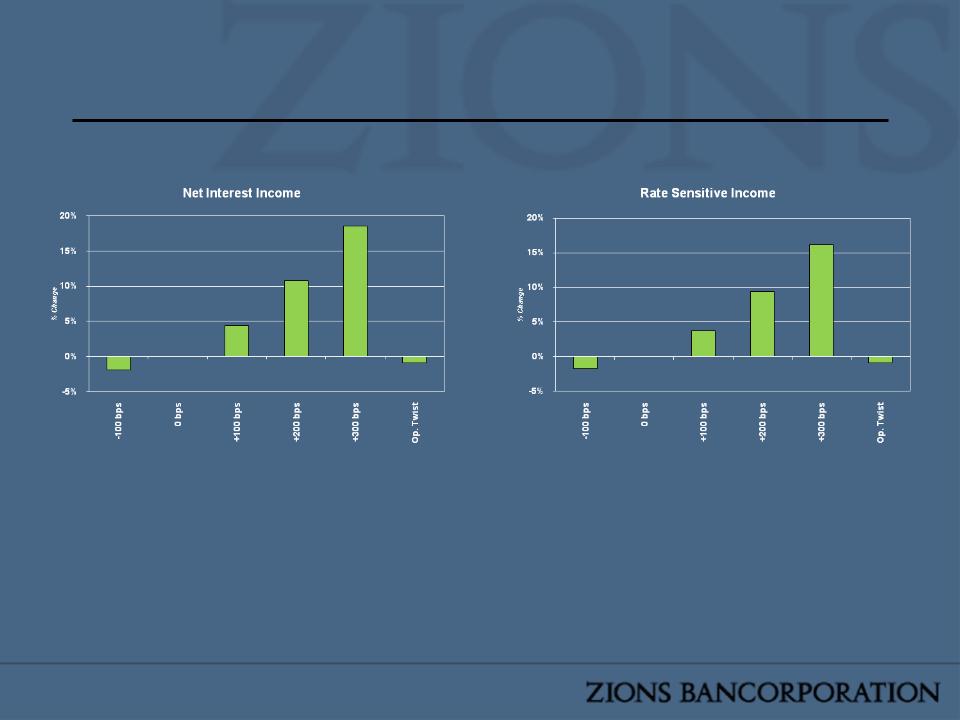

§ Zions expects net interest sensitive

income to increase between an

estimated 6.2% and 9.4% if interest

rates were to rise 200 bps* in the first

year

§ Core NIM (excludes discount accretion)

has been generally stable

– 2010 core NIM compression attributable to

a greater drag from cash balances

– 1Q09 experienced a temporary dip partially

due to an intentional build-up of excess

liquidity during the significant turmoil during

late 2008/early 2009

– Large senior note issuance in September

2009 had about 8 bps adverse impact on

the core NIM in 4Q09

(1) Cash drag refers to the adverse impact on the net interest margin due to the total balance of cash held in interest-bearing accounts. Assumptions used to compute the cash drag include

investing the cash at a rate of 4.5%, similar to the rate achieved on recent loan production. Liquidity targets and loan demand are factors that may prevent fully deploying such cash; the cash

drag is shown for illustrative purposes only.

*Assumes a parallel shift in the yield curve; key assumptions include a slow and a fast deposit repricing response (i.e. if deposit rates are slow to increase Zions expects a 9.4% increase in

interest sensitive income, and if deposits were to reprice quickly Zions expects a 6.2% increase in interest sensitive income); sensitivity analysis based on September 2011 data. Also

assumes $6.4 billion of DDA and interest-on-checking deposits are replaced with market rate funds.

Due to the extinguishment/ reissuance of subordinated debt in June 2009, Zions experiences non-cash discount accretion, which increases interest expense, reducing GAAP NIM

| 2009 | 2010 | 2011 |

| 1Q | 2Q | 3Q | 4Q | 1Q | 2Q | 3Q | 4Q | 1Q | 2Q | 3Q |

Cash Drag (1) | 24

bps | 17

bps | 16

bps | 24

bps | 20

bps | 35

bps | 46

bps | 45

bps | 41

bps | 43

bps | 50

bps |