February 13, 2014

Zions 2014 Biennial Investor Conference

Forward-Looking Statements

This presentation contains statements that relate to the projected or modeled performance or condition

of Zions Bancorporation and elements of or affecting such performance or condition, including

statements with respect to forecasts, opportunities, models, illustrations, scenarios, beliefs, plans,

objectives, goals, guidance, expectations, anticipations or estimates, and similar matters. These

statements constitute forward-looking information within the meaning of the Private Securities Litigation

Reform Act. Actual facts, determinations, results or achievements may differ materially from the

statements provided in this presentation since such statements involve significant known and unknown

risks and uncertainties. Factors that might cause such differences include, but are not limited to:

competitive pressures among financial institutions; economic, market and business conditions, either

nationally, internationally, or locally in areas in which Zions Bancorporation conducts its operations,

being less favorable than expected; changes in the interest rate environment reducing expected interest

margins; changes in debt, equity and securities markets; adverse legislation or regulatory changes; and

other factors described in Zions Bancorporation’s most recent annual and quarterly reports. In addition,

the statements contained in this presentation are based on facts and circumstances as understood by

management of the company on the date of this presentation, which may change in the future. Except

as required by law, Zions Bancorporation disclaims any obligation to update any statements or to

publicly announce the result of any revisions to any of the forward-looking statements included herein

to reflect future events, developments, determinations or understandings.

of Zions Bancorporation and elements of or affecting such performance or condition, including

statements with respect to forecasts, opportunities, models, illustrations, scenarios, beliefs, plans,

objectives, goals, guidance, expectations, anticipations or estimates, and similar matters. These

statements constitute forward-looking information within the meaning of the Private Securities Litigation

Reform Act. Actual facts, determinations, results or achievements may differ materially from the

statements provided in this presentation since such statements involve significant known and unknown

risks and uncertainties. Factors that might cause such differences include, but are not limited to:

competitive pressures among financial institutions; economic, market and business conditions, either

nationally, internationally, or locally in areas in which Zions Bancorporation conducts its operations,

being less favorable than expected; changes in the interest rate environment reducing expected interest

margins; changes in debt, equity and securities markets; adverse legislation or regulatory changes; and

other factors described in Zions Bancorporation’s most recent annual and quarterly reports. In addition,

the statements contained in this presentation are based on facts and circumstances as understood by

management of the company on the date of this presentation, which may change in the future. Except

as required by law, Zions Bancorporation disclaims any obligation to update any statements or to

publicly announce the result of any revisions to any of the forward-looking statements included herein

to reflect future events, developments, determinations or understandings.

2

Agenda

• Overview

• Return On Equity: Scenario Analysis

• Under the Hood: Net Interest Margin

• Fee Income Initiative

• Risk Oversight and Credit Management

• CDO Portfolio and Volcker Rule Update

• CCAR

• FutureCore

• Updated Guidance

• Appendix

3

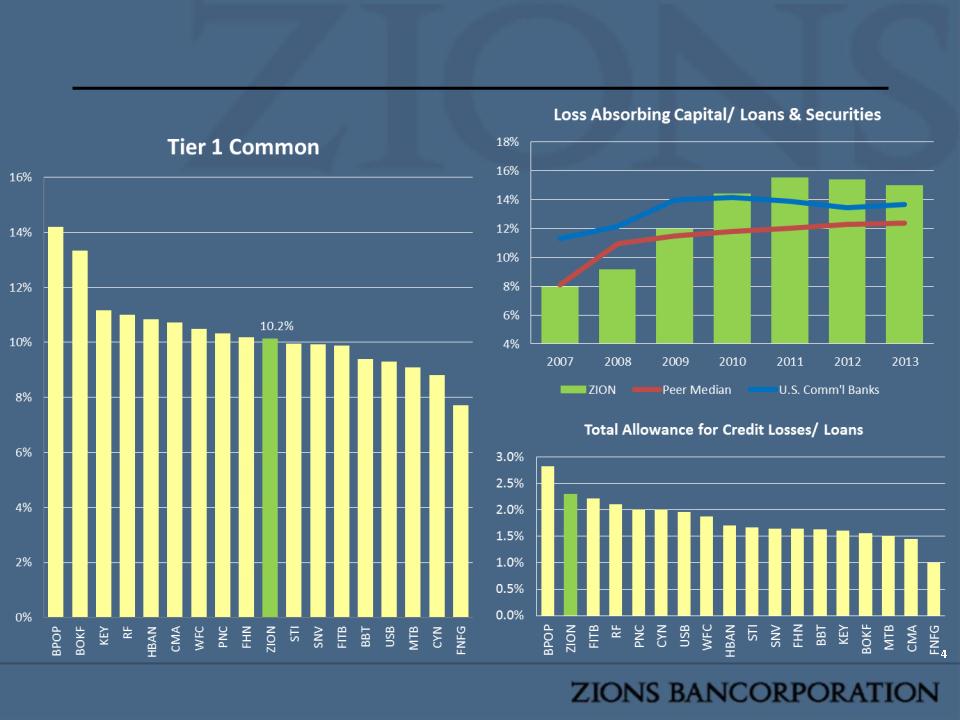

Capital Levels are In Line to Strong Relative to Peers

Source: Company documents for Zions as of 4Q13, SNL Financial as of 3Q13 for peers.

Loss absorbing capital defined to include tangible common equity, Basel III-qualifying non-common Tier 1 equity,

and the allowance for credit losses

and the allowance for credit losses

Credit Quality is Improving and is In Line-to-Better Than Peers

Nonperforming Lending Related Assets and Classified Loans

Nonperforming Lending Related Assets and Classified Loans

Nonperforming ratio consists of nonaccrual loans, real estate owned, and loans 90+ days past due and still accruing.

The ratio excludes accrual troubled debt restructured (TDR) loans and loans supported by FDIC loss-sharing

agreements. Source: Company Documents & SNL Financial.

The ratio excludes accrual troubled debt restructured (TDR) loans and loans supported by FDIC loss-sharing

agreements. Source: Company Documents & SNL Financial.

(In billions)

Annualized Losses Relative to Classified Loans

(In Millions)

Credit Quality is Improving and is In Line-to-Better Than Peers

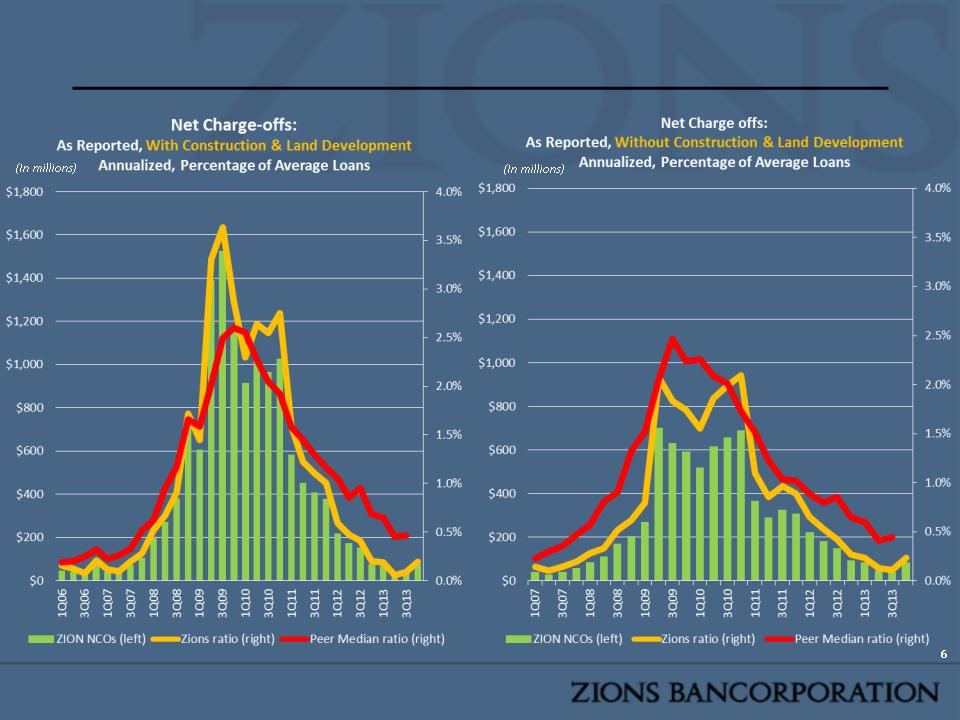

Net Charge-offs: Quarterly Trend, With and Without Construction & Land Development Loans

Net Charge-offs: Quarterly Trend, With and Without Construction & Land Development Loans

Source: Company documents for Zions as of 4Q13, SNL Financial as of 3Q13 for peers. Net charge-off ratios annualized.

Net Charge-offs: Through the Cycle, With and Without Construction Loans

NCO rate compares favorably with peers through the cycle

NCO rate compares favorably with peers through the cycle

Source: Company Documents & SNL Financial. Net charge-off ratios annualized.

7

Summary View of Profitability

Improvement in 2013 driven by capital actions, partially offset by a decline in net interest income

Improvement in 2013 driven by capital actions, partially offset by a decline in net interest income

1. ROAA and reserve release adjusted ROAA based on net income available to common.

Source: SNL Financial and Company documents.

* Net Income normalized for one-time debt extinguishment expense in 2Q13, preferred stock redemption in 3Q13, OTTI

and debt extinguishment cost in 4Q13

and debt extinguishment cost in 4Q13

Source: SNL Financial as of 4Q13.

Risk adjusted NIM calculated as net interest income less net charge-offs divided by average earning assets.

9

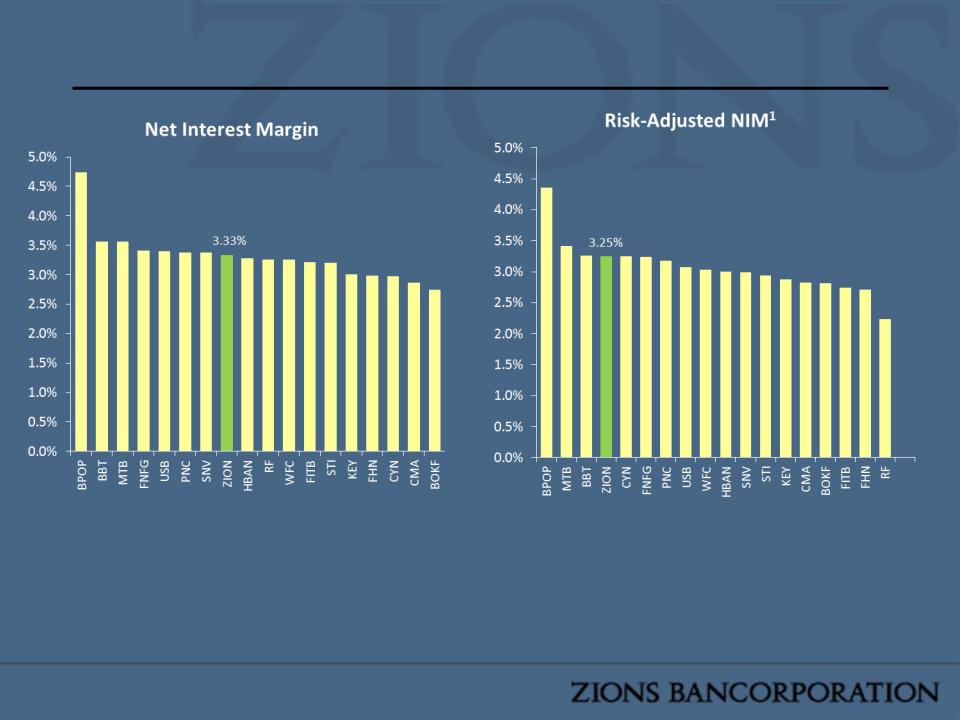

Net Interest Margin

Net interest income, less net charge-offs, is considerably stronger than most peers

Net interest income, less net charge-offs, is considerably stronger than most peers

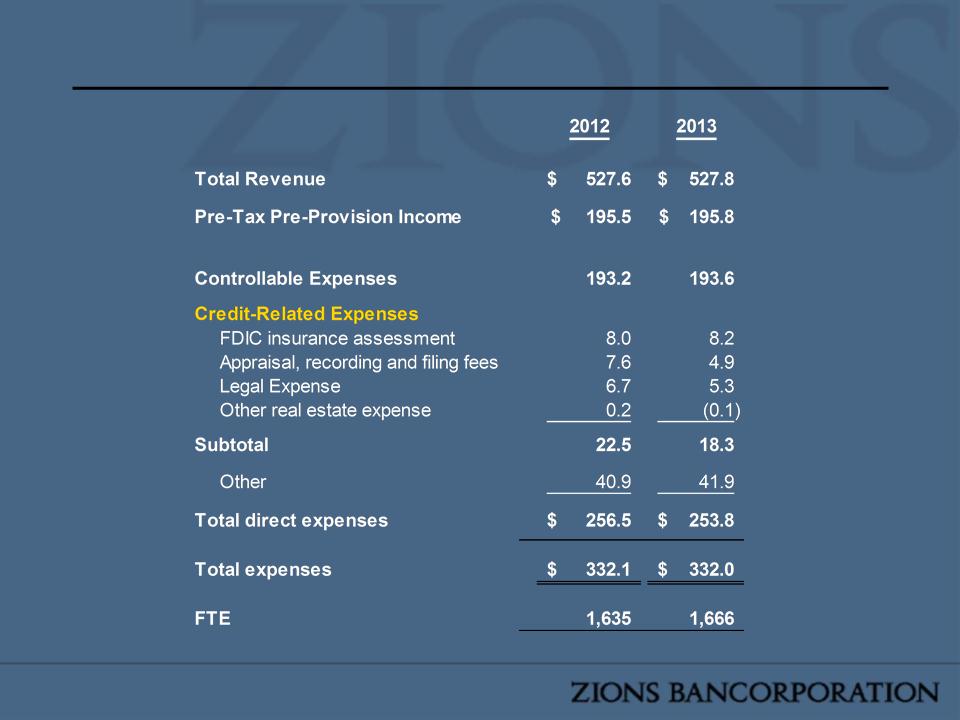

Non-Interest Expense: Medium Term Outlook

Adjusts 4Q13 NIE for items such as debt extinguishment, FDIC Indemnification Asset Amortization and CCAR costs

Adjusts 4Q13 NIE for items such as debt extinguishment, FDIC Indemnification Asset Amortization and CCAR costs

10

Source: Company Documents

*There will be a proportionate revenue reduction related to the decline in the indemnification

asset expense; Such revenue amounted to an annualized $135 million in 4Q13.

asset expense; Such revenue amounted to an annualized $135 million in 4Q13.

Professional & Legal ($40mm), Debt Extinguishment ($320mm), Regulatory Related ($24mm), Credit Related ($12mm), Allowance for Unfunded Commitments

($12mm), Indemnification Asset Expense ($80mm) *

($12mm), Indemnification Asset Expense ($80mm) *

Additions to Non-Interest Expense:

Systems Upgrade (“FutureCore” - core processing system upgrade, chart of accounts overhaul, and front-end loan entry system upgrade): $28mm additional

estimated, on average (This does not include the approximately $18 mm annualized of systems upgrade expense recognized in 4Q13); salary & other growth-

related increases: $100mm (dynamic balance sheet)

estimated, on average (This does not include the approximately $18 mm annualized of systems upgrade expense recognized in 4Q13); salary & other growth-

related increases: $100mm (dynamic balance sheet)

(In millions)

Fee Income Initiative

• Zions has proportionately low fee income relative to peers

• Long term fixes through organic growth, not major M&A

• Areas Targeted for Growth:

• Treasury Management

• Business Credit Cards

• Wealth Management

• Mortgage

• Growth focused within Zions’ footprint with relationship

customers

customers

11

Capital Actions

12

2013 Capital Actions |

§ Redeemed all $285 million 8.0% Series B trust preferred § Redeemed (via tender offer) $257 million 7.75% Senior Notes § Issued $800 million of preferred stock (6.2% weighted average dividend rate) and redeemed all $800 million 9.5% Series C preferred stock § Issued $250 million of subordinated debt (6.1% weighted average coupon) § Redeemed (via tender offer) $250 million of high cost subordinated debt |

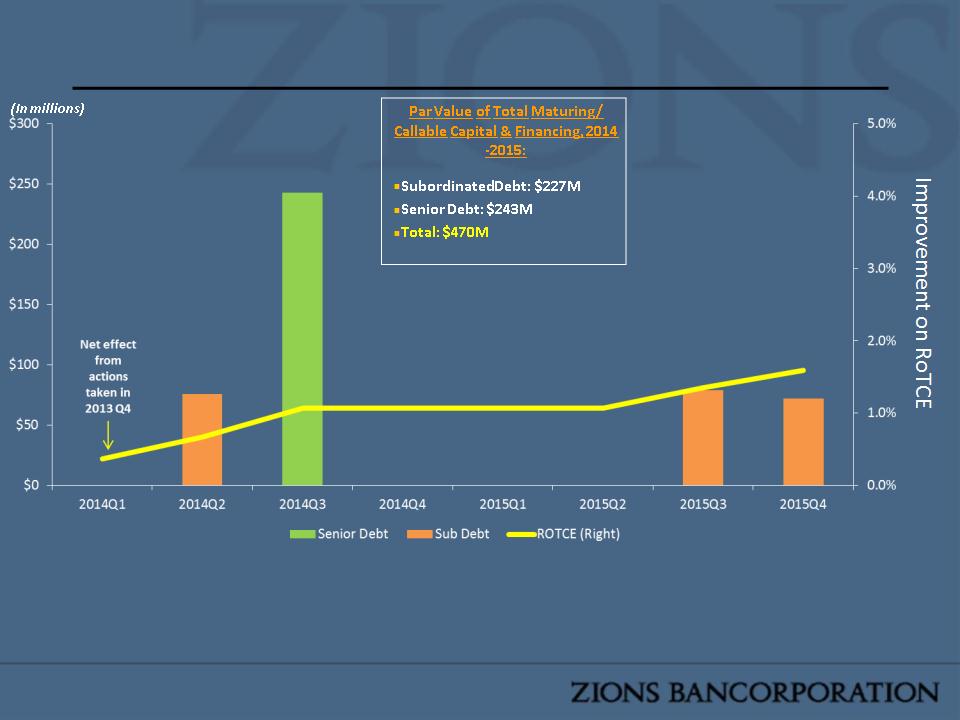

Remaining Significant High Cost Debt Reduction Opportunities

Effective GAAP Interest Cost In High Cost Debt Maturity Profile; Return on Tangible Common Equity (RoTCE) Expansion

Assumes No Replacement of Debt Because of Strong Cash Balances at Parent Company

Effective GAAP Interest Cost In High Cost Debt Maturity Profile; Return on Tangible Common Equity (RoTCE) Expansion

Assumes No Replacement of Debt Because of Strong Cash Balances at Parent Company

13

Assumes no replacement cost

Effective pre-tax cost listed above each bar

In the chart above, no adjustments have been made to other sources of revenue

or expense, which may increase or decrease, depending upon various factors,

such as loan growth or attrition, net interest margin expansion or compression,

and non-interest expense increases or reductions.

or expense, which may increase or decrease, depending upon various factors,

such as loan growth or attrition, net interest margin expansion or compression,

and non-interest expense increases or reductions.

26.7%

11.3%

23.4%

21.8%

Agenda

• Overview

• Return On Equity: Scenario Analysis

• Under the Hood: Net Interest Margin

• Fee Income Initiative

• Risk Oversight and Credit Management

• CDO Portfolio and Volcker Rule Update

• CCAR

• FutureCore

• Updated Guidance

• Appendix

14

Drivers of Expansion to RoTCE- Bear Case: Medium Term Outlook

15

Source: Company Documents

*NIE increase to reflect normal salary adjustments

Bear Case for Contraction

of RoTCE:

of RoTCE:

•RoTCE Normalization Assumptions

Found on Slide 86

Found on Slide 86

•Provision Expense adjusted to 0.4% of

total loans per year

total loans per year

•Added $20 Million of Growth Related

Non-Interest Expense*

Non-Interest Expense*

•Loan Portfolio turns over at a

weighted average yield of 3.9% (vs.

portfolio yield of 4.4% in 4Q13)

weighted average yield of 3.9% (vs.

portfolio yield of 4.4% in 4Q13)

•Financial Restructuring assumptions

found on Slide 13

found on Slide 13

•Rates Unchanged

•Deployment of $1 billion of Cash into

Loans at 4%

Loans at 4%

•Enter into $500 million of Receive

Fixed/Pay Floating Swaps at 3% Yield

to Zions (~5 year duration)

Fixed/Pay Floating Swaps at 3% Yield

to Zions (~5 year duration)

•Fee Income remains unchanged

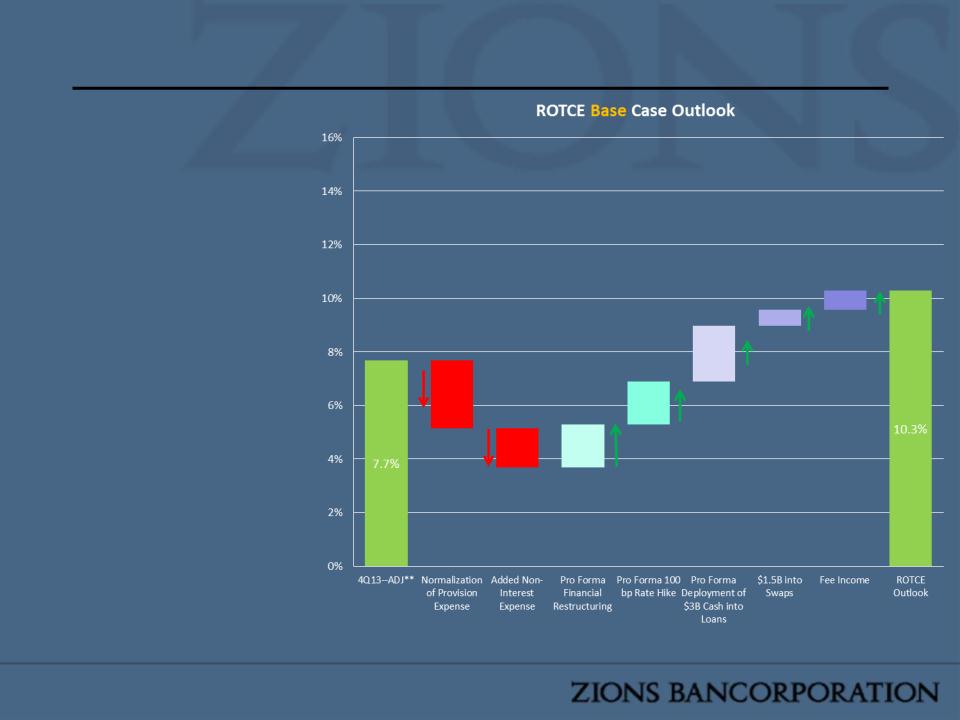

Drivers of Expansion to RoTCE- Base Case: Medium Term Outlook

16

Base Case for Expansion

of RoTCE:

of RoTCE:

•RoTCE Normalization Assumptions

Found on Slide 86

Found on Slide 86

•Provision Expense adjusted to 0.4%

of total loans per year

of total loans per year

•Added $100 Million of Growth

Related Non-Interest Expense*

Related Non-Interest Expense*

•Financial Restructuring assumptions

found on Slide 13

found on Slide 13

•100 bp Rate Hike

•Deployment of $3 billion of Cash

into Loans at 5% (Assumes 100 bp

rate hike has already occurred)

into Loans at 5% (Assumes 100 bp

rate hike has already occurred)

•Enter into $1.5 billion of Receive

Fixed/Pay Floating Swaps at 3% Yield

to Zions (~5 year duration)

Fixed/Pay Floating Swaps at 3% Yield

to Zions (~5 year duration)

•Additional $50 million of Fee Income

Source: Company Documents

*NIE increase to reflect growth related salary adjustments

Rate Hike assumes “fast “ deposit response - meaning, deposit pricing adjusts quickly to an upward shift in

interest rates.

interest rates.

The above assumptions are illustrative only, and do

not reflect targets, goals or budgeted amounts.

not reflect targets, goals or budgeted amounts.

Drivers of Expansion to ROTCE- Bull Case: Medium Term Outlook

17

Source: Company Documents

*NIE increase to reflect growth related salary adjustments

Rate Hike assumes “fast “ deposit response - meaning, deposit pricing adjusts quickly to an upward shift

in interest rates.

in interest rates.

Bull Case for Expansion

of RoTCE:

of RoTCE:

•RoTCE Normalization Assumptions

Found on Slide 86

Found on Slide 86

•Provision Expense adjusted to 0.4%

of total loans per year

of total loans per year

•Added $130 Million of Growth

Related Non-Interest Expense*

Related Non-Interest Expense*

•Financial Restructuring assumptions

found on Slide 13

found on Slide 13

•200 bp Rate Hike

•Deployment of $4 billion of Cash into

Loans at 6% (Assumes 200 bp rate

hike has already occurred)

Loans at 6% (Assumes 200 bp rate

hike has already occurred)

•Enter into $1.5 billion of Receive

Fixed/Pay Floating Swaps at 4% Yield

to Zions (~5 year duration)

Fixed/Pay Floating Swaps at 4% Yield

to Zions (~5 year duration)

•Additional $100 million of Fee

Income

Income

The above assumptions are illustrative only, and do

not reflect targets, goals or budgeted amounts.

not reflect targets, goals or budgeted amounts.

Agenda

• Overview

• Return On Equity: Scenario Analysis

• Under the Hood: Net Interest Margin

• New Production Pricing Vs. Portfolio Yield

• Interest Rate Risk Positioning

• Fee Income Initiative

• Risk Oversight and Credit Management

• CDO Portfolio and Volcker Rule Update

• CCAR

• FutureCore

• Updated Guidance

• Appendix

18

Business Confidence Levels: Large Business vs. Small Business

Small Business Optimism Still Soft

Small Business Optimism Still Soft

19

Average Levels (1988-2006):

•ISM: 55

•NFIB: 101

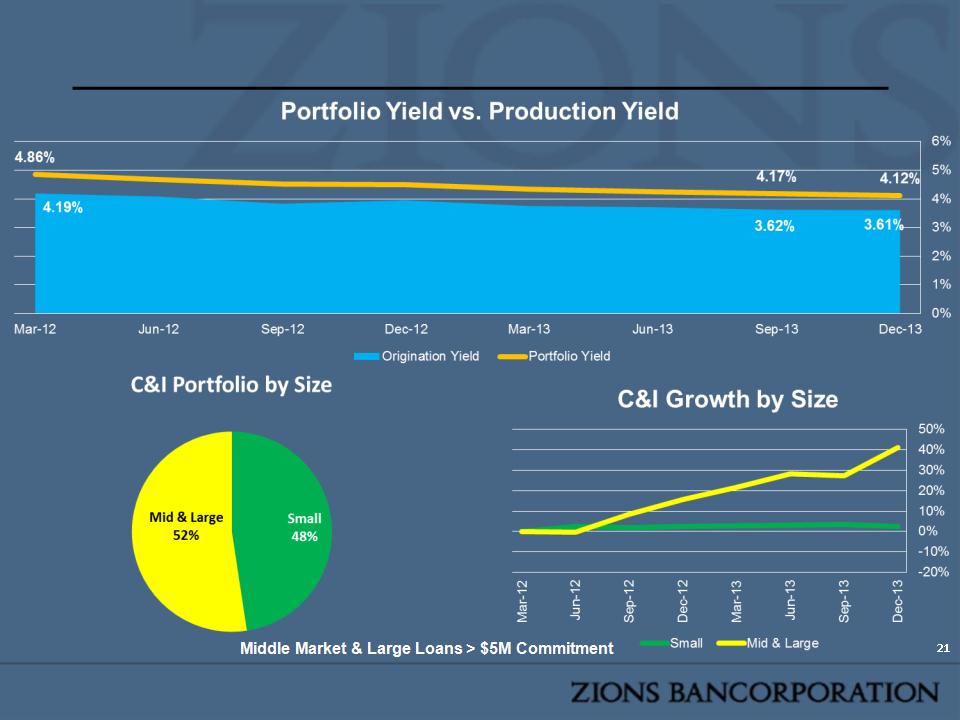

Total Loan Portfolio - C&I, CRE, and Consumer

Pricing on new production stabilizing

Pricing on new production stabilizing

Small Loans < $5M Commitment

Source: Company Documents; Loans Held For Investment, excluding FDIC-Supported

Loans. Production defined as new loans and marginal draws on existing lines of credit

Loans. Production defined as new loans and marginal draws on existing lines of credit

C&I Portfolio (53% of yearly production)

Pricing on production stabilizing, gap has narrowed from nearly 70 bps to approximately 50 bps

Pricing on production stabilizing, gap has narrowed from nearly 70 bps to approximately 50 bps

Source: Company Documents; Production defined as new loans and marginal draws on

existing lines of credit

existing lines of credit

Small Loans < $5M Commitment

Owner Occupied Portfolio (7% of yearly production)

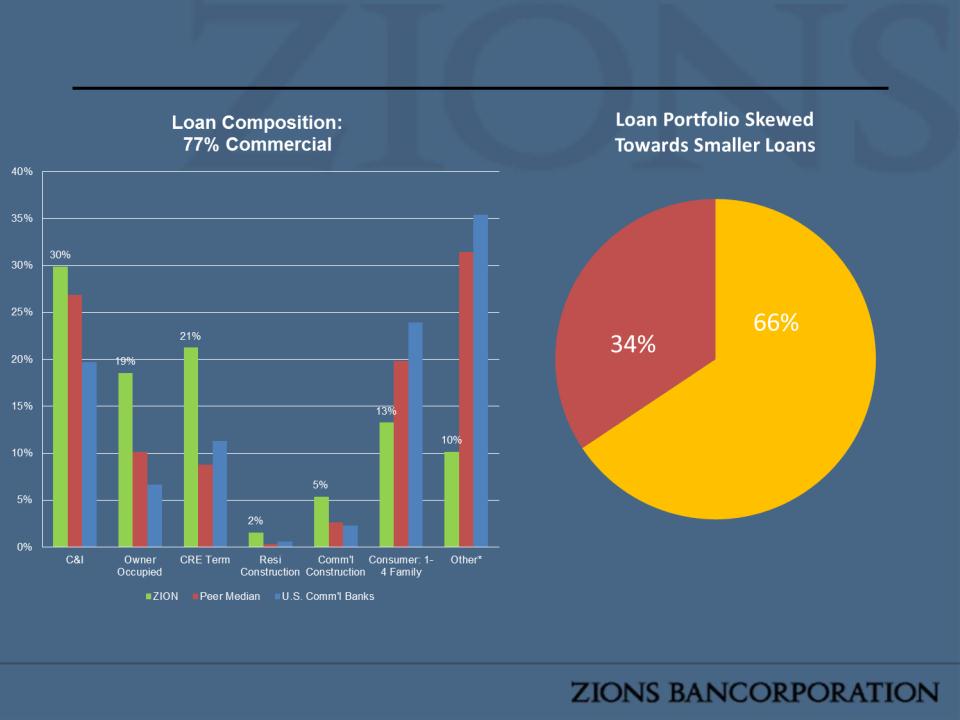

Owner occupied loans equaled $7.4 billion or 19% of the total portfolio

Owner occupied loans equaled $7.4 billion or 19% of the total portfolio

Source: Company Documents; Production defined as new loans and marginal draws on

existing lines of credit

existing lines of credit

Small Loans < $5M Commitment

Middle Market & Large Loans > $5M Commitment

Term CRE Portfolio (11% of yearly production)

Pricing on Term CRE remains dilutive to portfolio yield

Pricing on Term CRE remains dilutive to portfolio yield

Source: Company Documents; Production defined as new loans and marginal draws on

existing lines of credit

existing lines of credit

Small Loans < $5M Commitment

Other Loans (29% of yearly production)

Pricing on Other Loans improving - higher residential mortgage rates a contributing factor

Pricing on Other Loans improving - higher residential mortgage rates a contributing factor

Small Loans < $5M Commitment

Source: Company Documents; Production defined as new loans and marginal draws on

existing lines of credit. Other Loans includes: Construction, HECL, 1-4 Family, Bankcard

existing lines of credit. Other Loans includes: Construction, HECL, 1-4 Family, Bankcard

Smaller loan yields are only slightly lower than the overall portfolio yield

A shift to smaller business loans would have a favorable impact on the NIM trend

A shift to smaller business loans would have a favorable impact on the NIM trend

25

Source: Company documents as of 4Q13.

Production defined as new loans and marginal draws on existing lines of credit

Small Loans < $5M Commitment

Middle Market & Large Loans > $5M Commitment

Small Loan

Production (Coupon)

Production (Coupon)

Mid & Large Loan

Production (Coupon)

Production (Coupon)

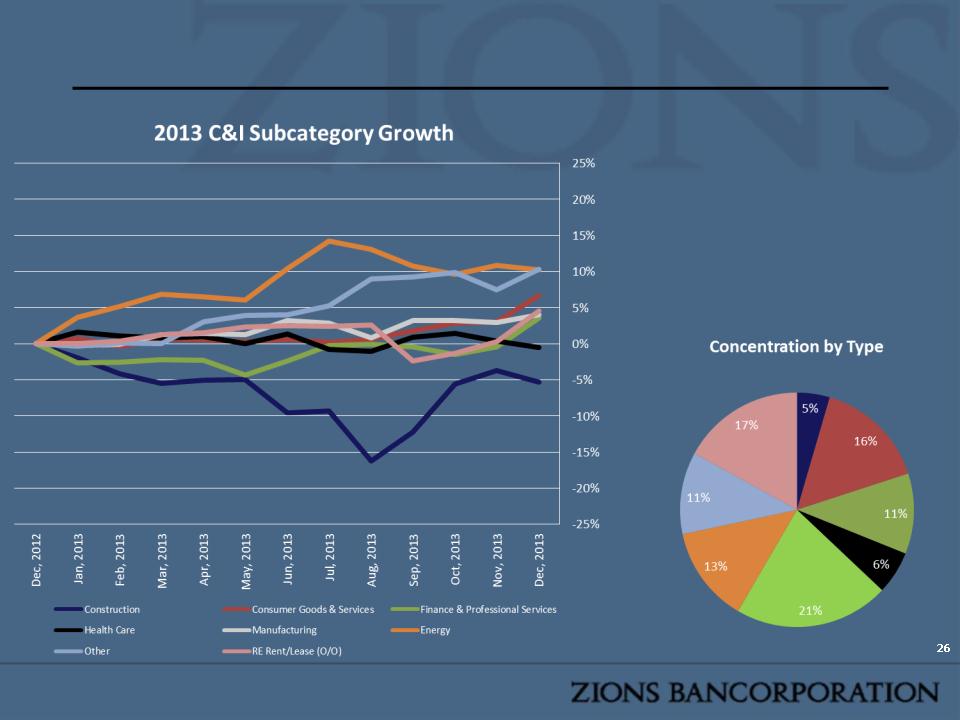

Commercial/Industrial (incl. Owner Occupied) Loan Growth by Industry

Energy loans have been a significant driver of C&I growth

Energy loans have been a significant driver of C&I growth

Other includes:

•19% Agriculture, Forestry, Fishing,

Hunting

Hunting

•13% Utilities

•13% Administrative and Support and

Waste Management and Remediation

Services

Waste Management and Remediation

Services

•11% Information

•10% Education

•9% Public Administration

•25% Other Services Excluding Public

Admin (Autos, Religious, Hair Salons, Civic

and Social Organizations some of the

largest contributors)

Admin (Autos, Religious, Hair Salons, Civic

and Social Organizations some of the

largest contributors)

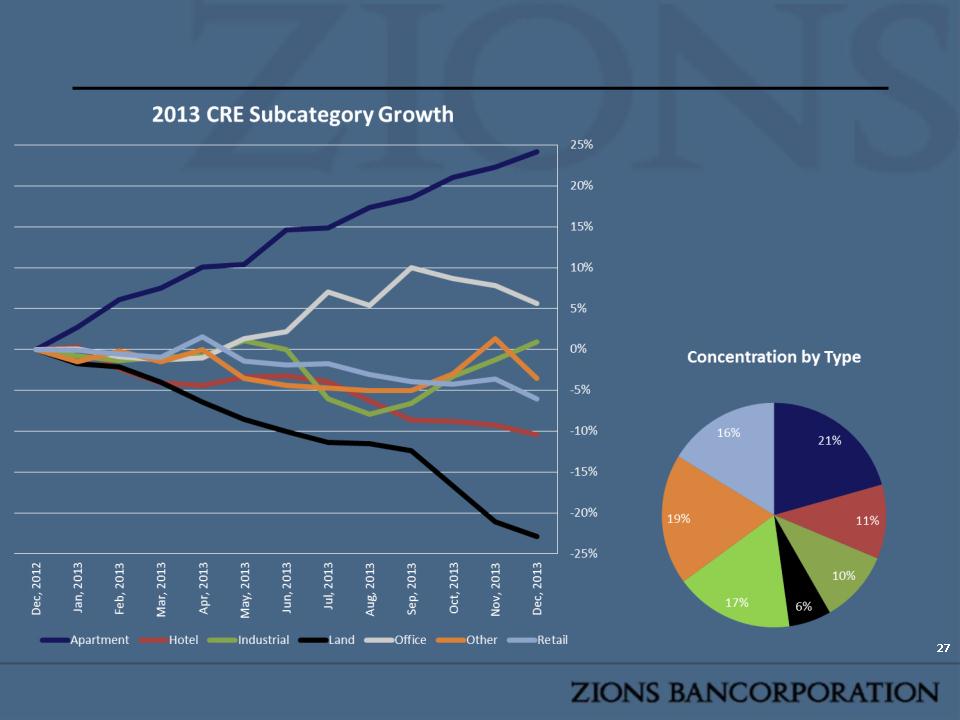

CRE (Term & Construction) Loan Growth By Type

Apartment loan concentration has increased, while land loan concentration continues to decline

Apartment loan concentration has increased, while land loan concentration continues to decline

Other includes:

•17% Recreation/Restaurant

•13% Hospital/Medical Centers

•70% General Other

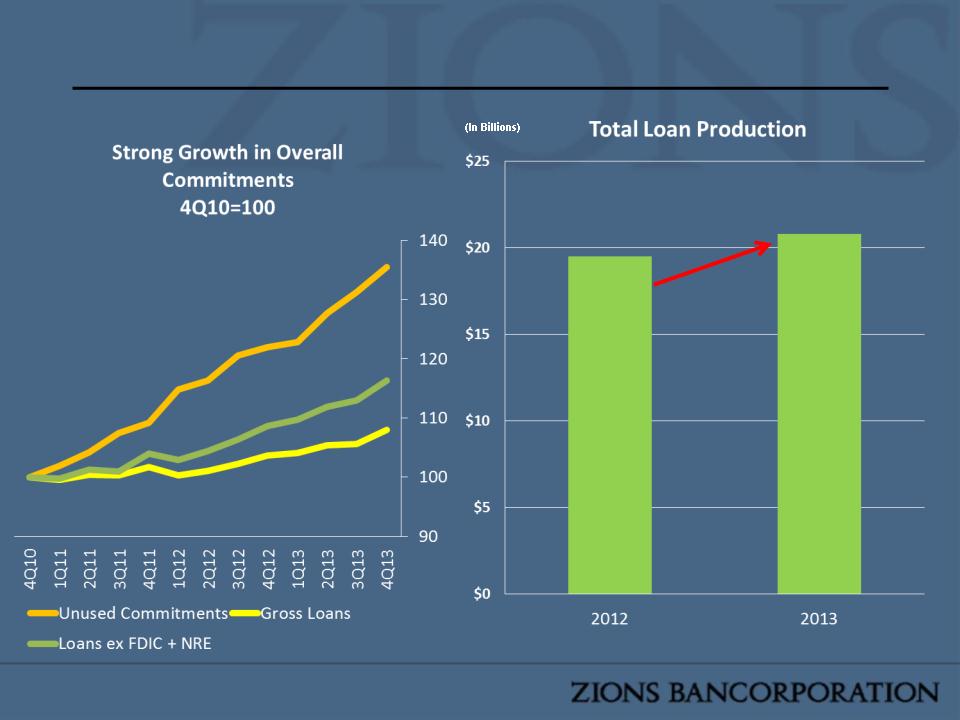

Loan Growth and Production Remains Positive

Favorable Trends in Commitments and Production

Favorable Trends in Commitments and Production

28

Source: Company documents as of 4Q13. “FDIC” refers to FDIC-supported loans; “NRE” refers to National Real

Estate. Both of these portfolios are currently in run-off mode

Estate. Both of these portfolios are currently in run-off mode

7% Growth

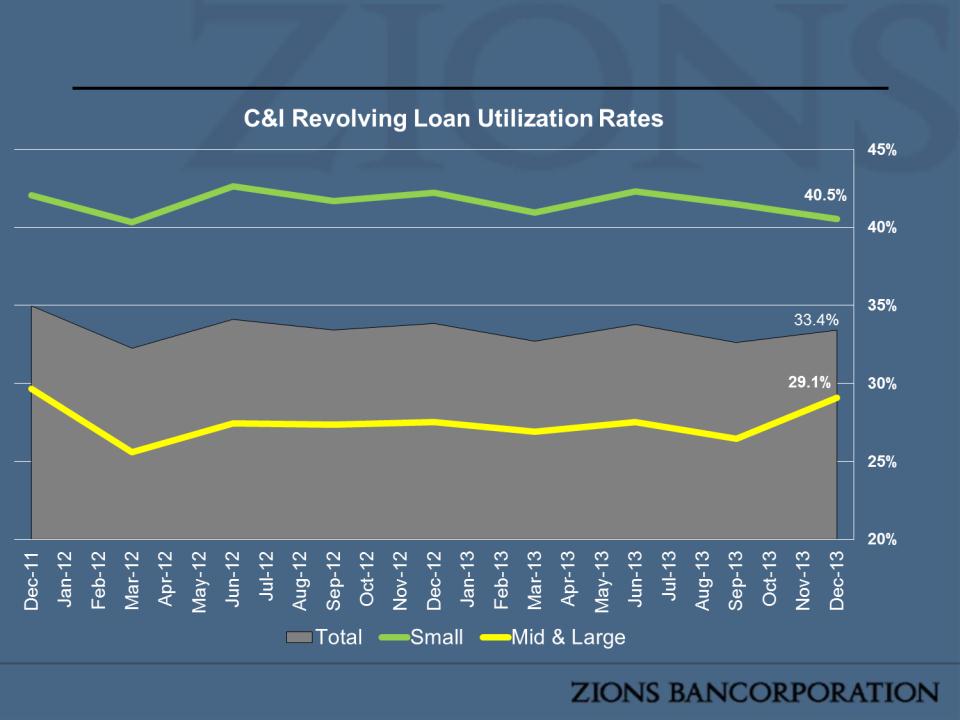

C&I Utilization Rate

Smaller Loan Utilization Rates Materially Higher than Larger Loan Utilization Rates

Smaller Loan Utilization Rates Materially Higher than Larger Loan Utilization Rates

29

Small < $5M Commitment

Middle Market & Large > $5M Commitment

Agenda

• Overview

• Return On Equity: Scenario Analysis

• Under the Hood: Net Interest Margin

• New Production Pricing Vs. Portfolio Yield

• Interest Rate Risk Positioning

• Fee Income Initiative

• Risk Oversight and Credit Management

• CDO Portfolio and Volcker Rule Update

• CCAR

• FutureCore

• Updated Guidance

• Appendix

30

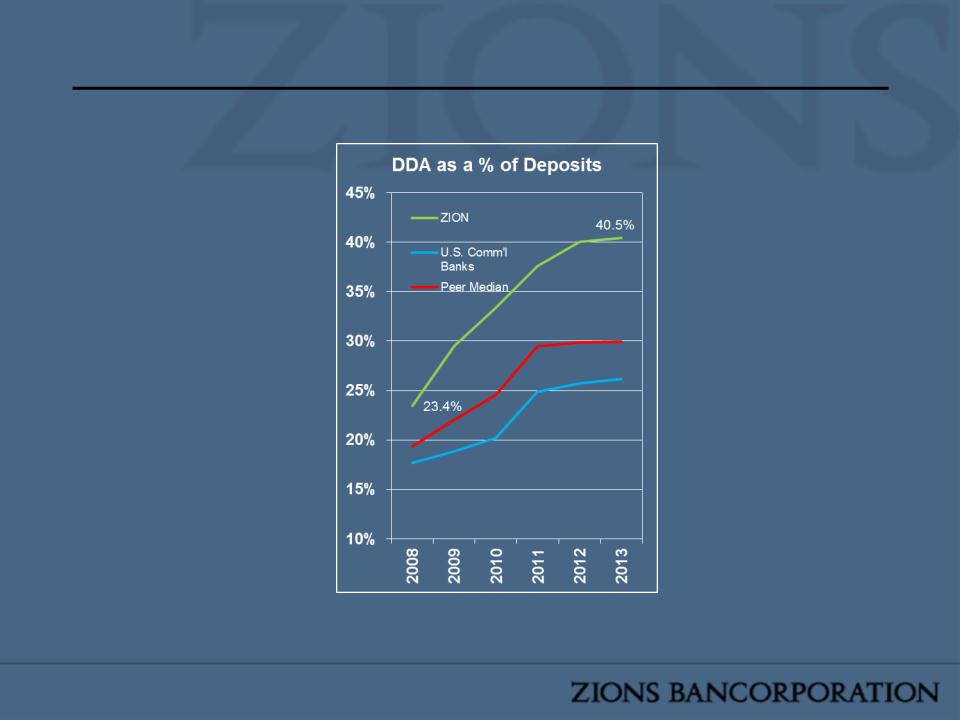

Zions Deposit Franchise is Among Best of Peers

Source: SNL Financial as of 4Q13

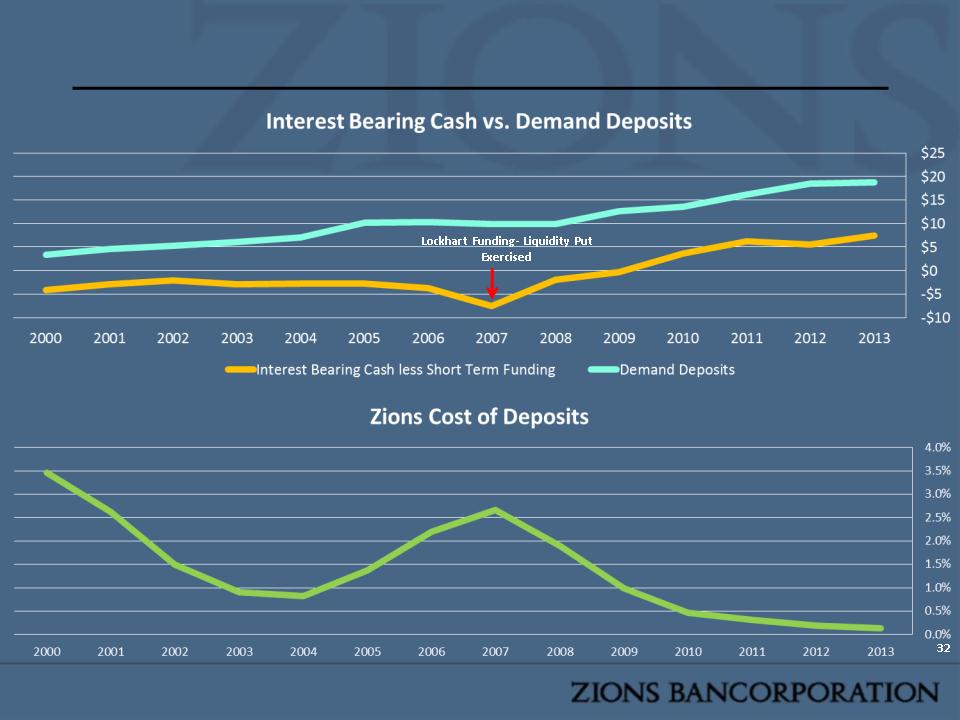

Zions’ History of Interest Bearing Cash vs. DDAs

Growth in DDA has been Primarily Held in Cash; Deposit Costs at Historic Lows

Growth in DDA has been Primarily Held in Cash; Deposit Costs at Historic Lows

Source: Company Documents SNL Financial as of 4Q13

(In Billions)

Avoiding the Next Big Risk to Equity: Securities & Cash Portfolio

ZION has one of the Smallest Securities (and MBS) Portfolio vs. its Peers

ZION has one of the Smallest Securities (and MBS) Portfolio vs. its Peers

Source: Company Documents for Zions as of 4Q13, SNL Financial for peers as of 3Q13

MBS securities include resi mortgage pass-through investments that are not guaranteed by the U.S. Government

§ Estimated option-adjusted duration of Zions’:

§ Loan portfolio < 2 years

§ Cash portfolio ~ 0.1 years

§ Securities portfolio < 2 years

33

Avoiding the Next Big Risk to Equity:

Long-Term Capital Risk not Traded for Short-Term Profitability

Long-Term Capital Risk not Traded for Short-Term Profitability

34

Source: Zions' estimates based upon Bloomberg MBS models; key assumptions include the WAC of the underlying mortgages is

approximately 4%, 30-year pass-through paper, Bloomberg's DAPAX model for duration extension (increasingly slower prepayment

speeds with each incremental increase in interest rates), and the trailing six months for empirical prepayment history; analysis as of

February 11, 2014.

approximately 4%, 30-year pass-through paper, Bloomberg's DAPAX model for duration extension (increasingly slower prepayment

speeds with each incremental increase in interest rates), and the trailing six months for empirical prepayment history; analysis as of

February 11, 2014.

3rd Party Analysis Ranks Zions Near Top of Asset Sensitive Banks

35

Source: Raymond James Research, June 2013

Rate: Balance Sheet Remains Significantly Asset Sensitive

36

Zions estimates net interest income

would increase between an

estimated 14.2% and 17.1% if

interest rates were to rise 200 bps*

in the first year.

would increase between an

estimated 14.2% and 17.1% if

interest rates were to rise 200 bps*

in the first year.

* 12-month simulated impact using a static balance sheet and a parallel shift in the yield curve, and is based on regression analysis comparing deposit repricing changes against

similar duration benchmark indices (e.g. Libor, U.S. Treasuries); also includes management input across all major geographies in which Zions does business, intended to adjust for

local market conditions. “Slow Response” refers to an assumption that market rates on deposits will adjust at a moderate rate (i.e. supply of deposits exceeds demand for loans). Data

as of 4Q13

similar duration benchmark indices (e.g. Libor, U.S. Treasuries); also includes management input across all major geographies in which Zions does business, intended to adjust for

local market conditions. “Slow Response” refers to an assumption that market rates on deposits will adjust at a moderate rate (i.e. supply of deposits exceeds demand for loans). Data

as of 4Q13

Effective

duration

Effective

duration

Effective

duration

Effective

duration

FAST

SLOW

Agenda

• Overview

• Return On Equity: Scenario Analysis

• Under the Hood: Net Interest Margin

• Fee Income Initiative

• Risk Oversight and Credit Management

• CDO Portfolio and Volcker Rule Update

• CCAR

• FutureCore

• Updated Guidance

• Appendix

37

Zions vs. Peer Group

38

Source: Company documents for Zions as of 4Q13, SNL Financial as of 3Q13 for peers.

Zions vs. Community Bank Peers in Footprint

($5-15B in assets)

($5-15B in assets)

Source: Company documents for Zions as of 4Q13, SNL Financial as of 3Q13 for peers.

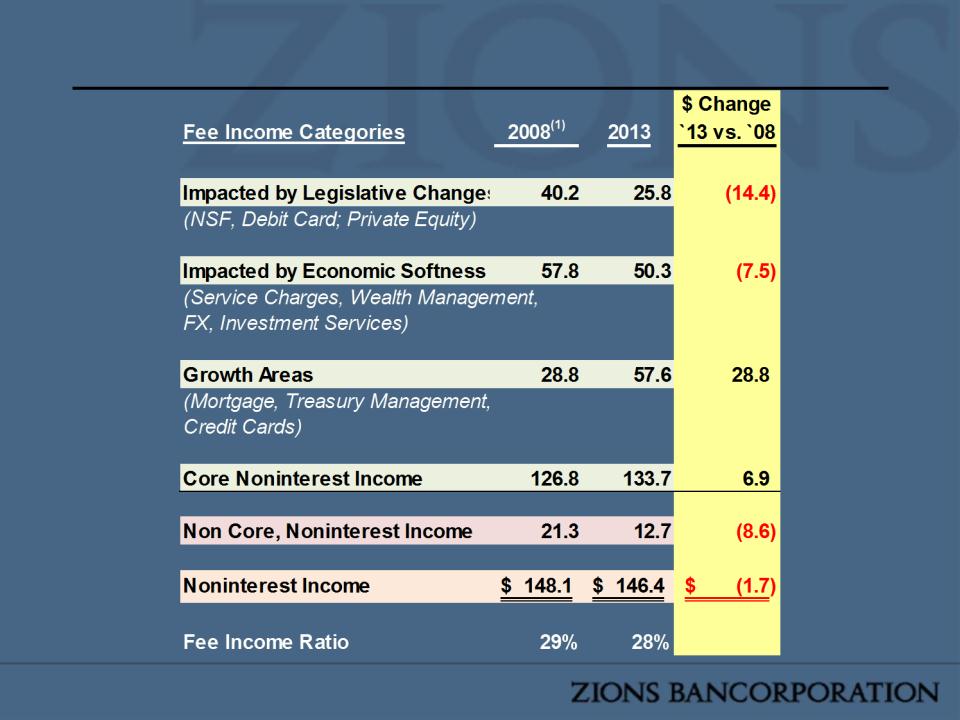

Historical “Impediments” and “Growth Areas”

40

2013 Fee Income

$527MM

*

Impediments:

•NSF

•Debit Cards

•DDA Service Charges

•Sweep Income

Growth Areas:

•Card

•Treasury Management (Core)

•Mortgage

*$333MM as reported adjusted for fixed income securities, net impairment on OTTI,

Treasury Management fees compensated by balances.

Treasury Management fees compensated by balances.

Case Study: Fee Growth Muted by Legislative and

Economic Pressure

Economic Pressure

41

(in millions)

Case Study…Amegy Bank

(1) 2008 Adjusted for $38mm swap

gain.

gain.

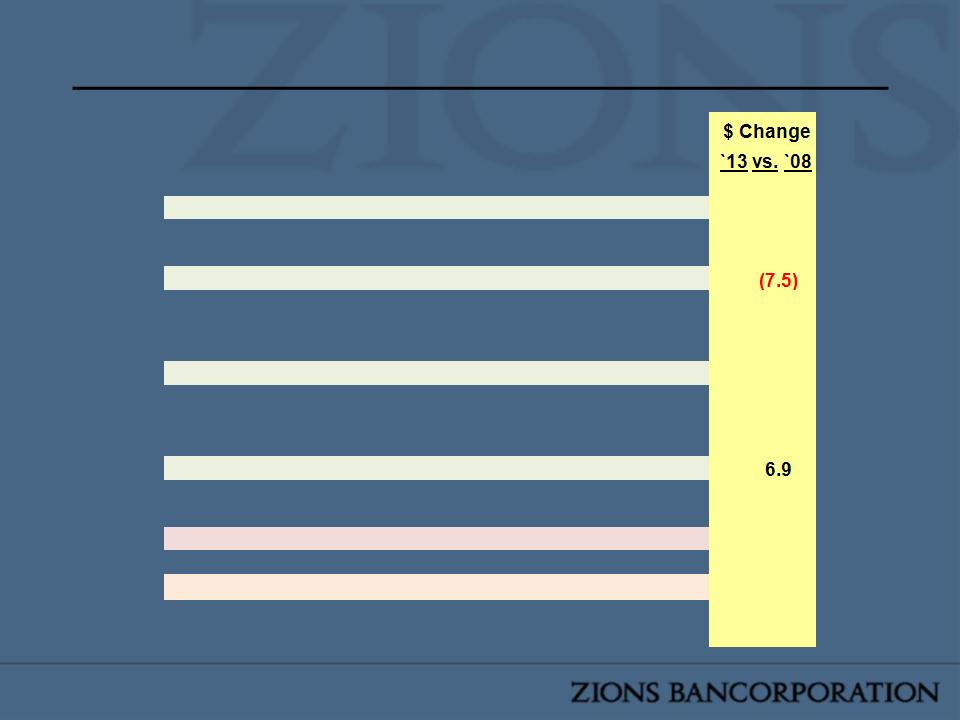

$ Change | ||||||

Fee Income Categories | 2008(1) | 2013 | `13 vs. `08 | |||

Impacted by Legislative Changes | 40.2 | 25.8 | (14.4) | |||

(NSF, Debit Card, Private Equity) | ||||||

Impacted by Economic Softness | 57.8 | 50.3 | (7.5) | |||

(Service Charges, Wealth Management, | ||||||

FX, Investment Services) | ||||||

Growth Areas | 28.8 | 57.6 | 28.8 | |||

(Mortgage, Treasury Management, | ||||||

Credit Cards) | ||||||

Core Noninterest Income | 126.8 | 133.7 | 6.9 | |||

Non Core, Noninterest Income | 21.3 | 12.7 | (8.6) | |||

Noninterest Income | $ 148.1 | $ 146.4 | $ (1.7) | |||

Fee Income Ratio | 29% | 28% | ||||

Zions Fee Income Mix

42

Treasury Management | 32% | |

Card* | 14% | |

Loan Fees | 8% | |

Mortgage | 7% | |

Capital Markets | 7% | |

Wealth Management | 5% | |

Foreign Exchange | 2% | |

Subtotal | 75% | |

25% | ||

100% |

% of Total

Growth Products

Other

*Commercial Card included in Treasury Management

Treasury Management

Key to Zions’ Community Banking Strategy

Key to Zions’ Community Banking Strategy

43

Ø Represents 32% of Non-

Interest Income

Interest Income

Ø 63% of DDA balances

are tied to Corporate

Treasury Management

(CTM) accounts

are tied to Corporate

Treasury Management

(CTM) accounts

Ø Recognized by

Greenwich Associates

for Overall Satisfaction

and Customer Service

Greenwich Associates

for Overall Satisfaction

and Customer Service

Ø Significant investment

in treasury systems

since 2007

in treasury systems

since 2007

Source: SNL Financial as of 4Q13

Banking Entity (by Geography) | Account Analysis DDA as % of total DDA |

Washington/Oregon | 88% |

Texas | 84% |

Nevada | 76% |

Bancorp | 63% |

Colorado | 63% |

Arizona | 55% |

California | 48% |

Utah/Idaho | 45% |

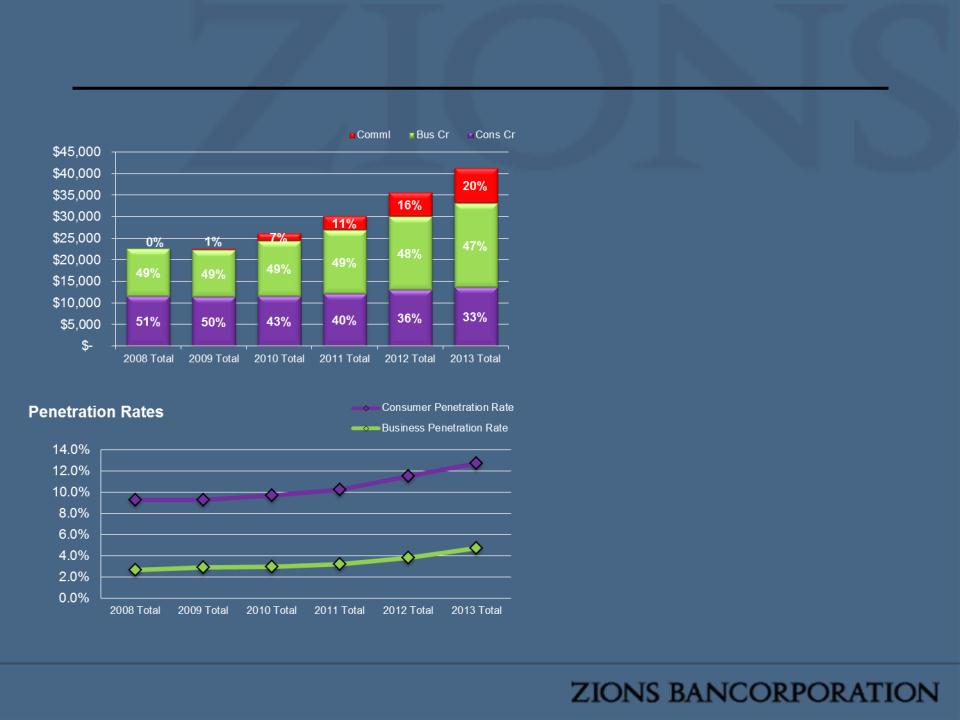

Card…Low Penetration…Competitive Offering

44

Card Products Fee Income (000's)

• Corporate platform delivered

locally

locally

• Penetration:

Consumer - 12.7%...25% optimal

Business - 4.8%...15% optimal

Commercial - nominal…growing

rapidly

rapidly

• 2013 total spend growth - 18%

• #13 U.S. business card issuer in

terms of sales volume (spend)

terms of sales volume (spend)

• Product offering/infrastructure

significantly enhanced

significantly enhanced

• Commercial card fastest growing

treasury management product

nationally

treasury management product

nationally

Mortgage…Community Banks Uniquely Positioned

45

• 2013 Results:

Production - $3.3 billion

Fee income - $37.7 million

Production - $3.3 billion

Fee income - $37.7 million

• Model leverages community bank franchise

to achieve higher level of “purchase”

business

to achieve higher level of “purchase”

business

• Investing in corporate operations,

compliance, product development with

local sales and service

compliance, product development with

local sales and service

• Volatile industry volumes and dramatically

higher CFPB compliance mandates are

eroding mortgage industry capacity

higher CFPB compliance mandates are

eroding mortgage industry capacity

• Ability to leverage community bank

franchise relationships with builders,

realtors, and high net worth clients

franchise relationships with builders,

realtors, and high net worth clients

• Mortgage colleagues’ referrals to other

bank products accelerating

bank products accelerating

Fee Income…What to Expect

46

• Greater focus and tracking

• Enhanced utilization of corporate infrastructure, product

development with local pricing

development with local pricing

• Above average growth rates, assisted by generally low

current penetration rates

current penetration rates

• Simple products that can be leveraged over entire employee

base

base

• Community bank relationship advantage

Agenda

• Overview

• Return On Equity: Scenario Analysis

• Under the Hood: Net Interest Margin

• Fee Income Initiative

• Risk Oversight and Credit Management

• CDO Portfolio and Volcker Rule Update

• CCAR

• FutureCore

• Updated Guidance

• Appendix

47

Risk Management Changes in the last 3-5 Years

• Implemented a Board Risk Oversight Committee

• Standardized Risk Committees at all affiliate banks

based upon Risk Appetite Framework

based upon Risk Appetite Framework

• Increased risk management staffing with expertise in

specific areas including:

specific areas including:

• Investments

• Operations

• Model management

• Credit

• Enhanced risk and control reporting

48

The Future of Enterprise Risk Management (ERM)

Establish an ERM Program commensurate with the size and complexity of Zions

Ø Formalize the Operational Risk function

Ø Integrated the Compliance function into ERM

Ø Enhance existing risk areas (e.g., Credit, Market, Liquidity, Interest rate, Model)

Ø Formalize the Wealth Management risk program

Enhance ERM’s interaction and Status

Ø Grant Risk Management “veto” capacity for all risks (e.g., liquidity, interest rate, credit)

Ø Involve Risk Management in all committees

Ø Chief Risk Officer and Chief Credit Officer reside on the Executive Management Committee

Ø Hired a Director for Operational Risk

Enhance key Policy and Oversight

Ø Revise the Risk Appetite Framework to include quantitative and qualitative metrics

Ø Improve ERM Governance and Reporting

Ø Update the Board Risk Oversight & Enterprise Risk Management Committee Charters

Drive the Risk Culture

Ø Communicate Risk Appetite and principles

• We take risks we can understand, manage, and measure

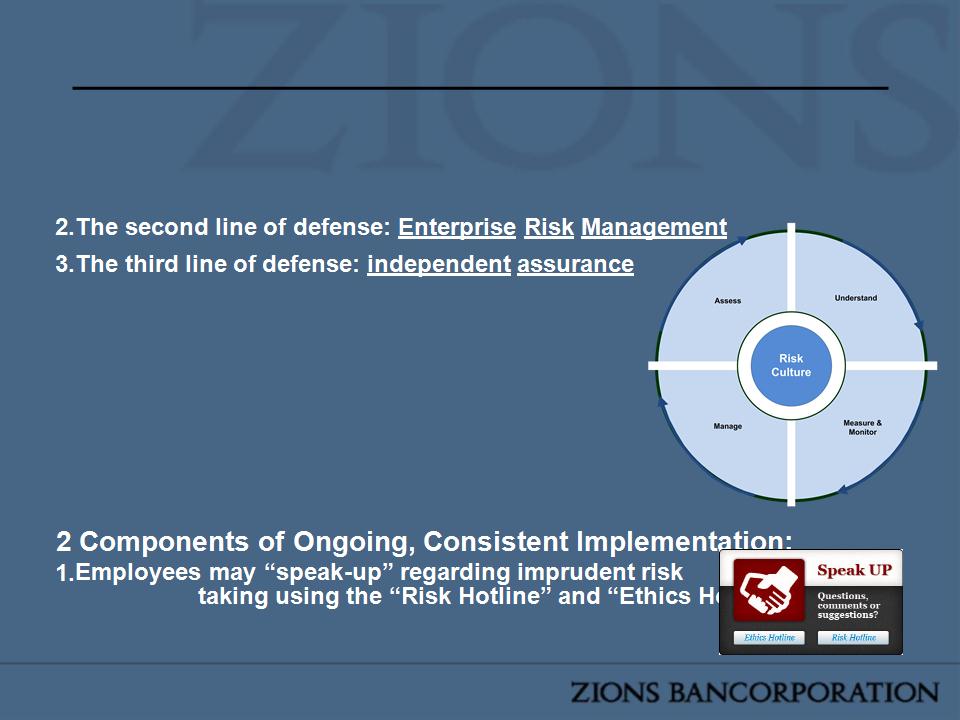

• Implemented a Risk Hotline for employees to “speak up”

49

50

Enhanced Future Risk Reporting Structure

Risk Appetite Framework

Core Principles

Core Principles

3 Lines of Defense:

1.The first line of defense: business lines

5 Key Basic Concepts:

1.We take risks we assess

2.We take risks we understand

3.We take risks that we can measure

4.We take risks that we can monitor, and,

5.We take risks that we can manage.

2.Employees complete annual i-achieve training.

51

Select Credit Risk Management Changes Since 2008

production

nCorporate Chief Credit Officer governs all credit approvals and policy

n Delegates (or retracts) authority to Affiliate Bank Chief Credit Officers.

nCCOs have veto (decline) over any transaction, program, or concentration

nEnhanced senior loan committees with Corporate involvement

nCentralized support and underwriting processes for Small Business

nEstablished CRE risk hurdles (threshold criteria for each market and asset class)

nImplemented CRE triggers - concentrations and “hot spots” early warning

52

Account Management

n Centralized oversight of CRE appraisal, environmental and engineering

n Enhanced loan risk grading tool and refined grade definitions

n Centralized underwriting and implemented standard loan monitoring for small commercial credits with automated triggers for

review

review

Corporate Credit Oversight

n Established high quality, formal Corporate Credit organization

n Credit Administrators for each portfolio segment

n Concentration Risk Manager

n Launched key initiatives to improve credit performance and achieve common credit culture

n Launched multiple enterprise-wide credit training programs

n Rewrote company general credit policy

n Enhanced market analyses through underwriting triggers and hurdles

Future Improvements of Credit Risk Management

• Enhance Concentration Management

Ø Introduce Industry Risk Ratings

Ø Portfolio/Segment Stress Testing

Ø Introduce a “white paper” process

• Eliminate remaining exceptions to the uniform underwriting

standards

standards

• Enhance Data Management and oversight

• Implement Hold limits that incorporate PD Risk Ratings and

Industry Ratings at Corporate and Affiliate levels

Industry Ratings at Corporate and Affiliate levels

• Enhance Risk Rating Models

• Improve Reporting Lines for Affiliate Chief Credit Officers

53

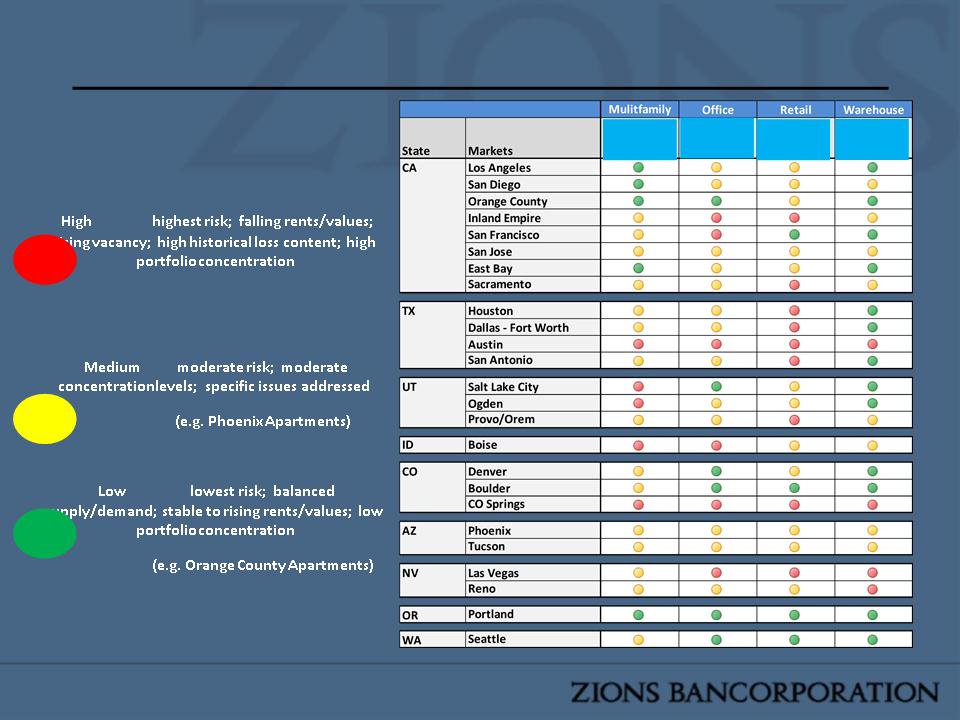

CRE Risk Hurdles - Disciplined Approach to Asset Classes and Markets

54

(e.g. Las Vegas Office)

Definitions

Enabling Growth, While Carefully Managing Risk

• Developing key metrics that serve the purpose of

• Growing the business in a managed way

• Adhering to the strategic plan

• Exceptions to the policy are being monitored,

managed and escalated in an effective manner

managed and escalated in an effective manner

• Ensuring “business lines” have critical input into

risk decisions and jointly develop any risk

mitigation plans

risk decisions and jointly develop any risk

mitigation plans

55

Credit Quality - Total Portfolio

4Q13 | 3Q13 | 4Q12 | |

Total Loan Balance ($B) | 39.2 | 38.4 | 37.9 |

Total Delinquencies | 0.8% | 0.8% | 1.5% |

Total Non-Performing Loans | 1.0% | 1.2% | 1.7% |

Total Classifieds | 3.2% | 3.7% | 4.7% |

% of Classifieds Performing | 84.4% | 83.9% | 78.6% |

Total Net Charge-Offs | 0.2% | 0.1% | 0.2% |

Total Loan Balance

Total Loan Balance Key Statistics

56

Source: SNL and company documents

Loan growth is strong and charge offs remain low compared to Comm’l Banks

Rolling NCO rate gradually declined from 0.41% in 2012 Q4 to 0.13% in 2013 Q4

Credit quality metrics indicate improving trends

Rolling NCO rate gradually declined from 0.41% in 2012 Q4 to 0.13% in 2013 Q4

Credit quality metrics indicate improving trends

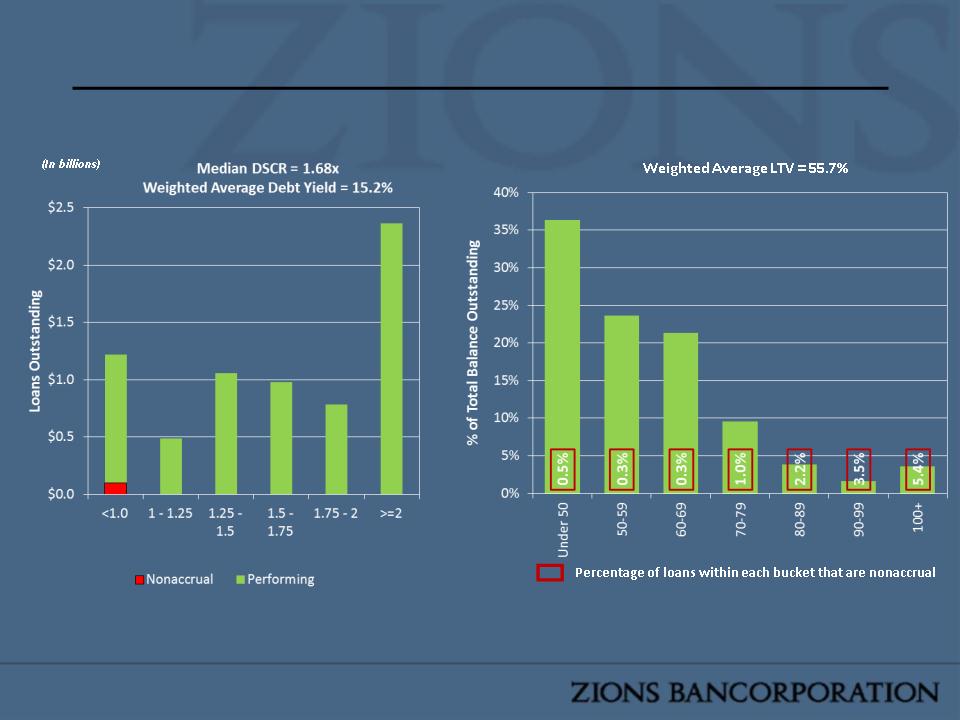

Term CRE Portfolio Improving

Term CRE Key Statistics

4Q13 | 3Q13 | 4Q12 | |

Loan Balance ($B) | 8.0 | 8.2 | 8.1 |

Delinquencies | 1.1% | 0.8% | 1.8% |

Non-Performing Loans | 1.4% | 1.4% | 2.9% |

Classifieds | 3.3% | 3.7% | 4.9% |

% of Classifieds Performing | 90.8% | 89.0% | 80.9% |

Net Charge-Offs | 0.1% | 0.2% | 0.3% |

Collateral

57

Gradient Fill - 2013 % mix ↓from 2008

Solid Fill - 2013 % mix ↑ from 2008

Source: SNL and company documents

Current Term CRE Balance - $8.0B (21.0% of Total Loans)

Term CRE balances steady with improving NCO rate

Credit quality metrics for Term CRE show improving trends

Credit quality metrics for Term CRE show improving trends

• Left - Sample data: As of 4Q13; non-FDIC supported term loans > $500k balance

• Right - As of 4Q13; LTVs were adjusted using PPR’s market level/property type value trend indices

58

Term CRE Metrics are Solid

Net Charge-offs: Through the Cycle, Term CRE and Multi-Family

NCO rate compares favorably with peers through the cycle

NCO rate compares favorably with peers through the cycle

Source: Company Documents & SNL Financial. Net charge-off ratios annualized.

59

60

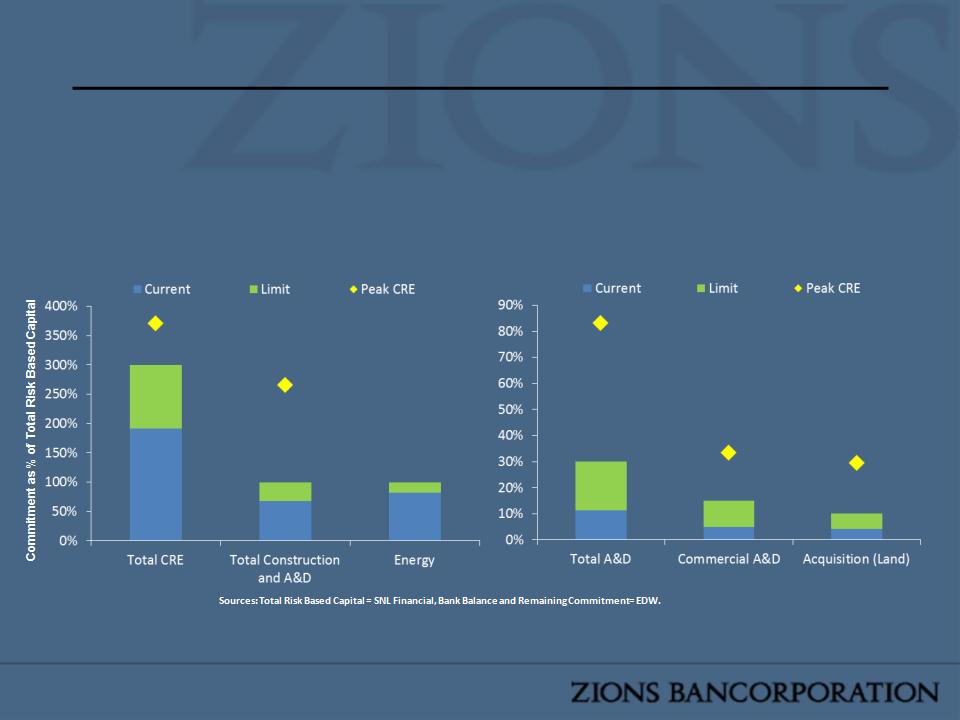

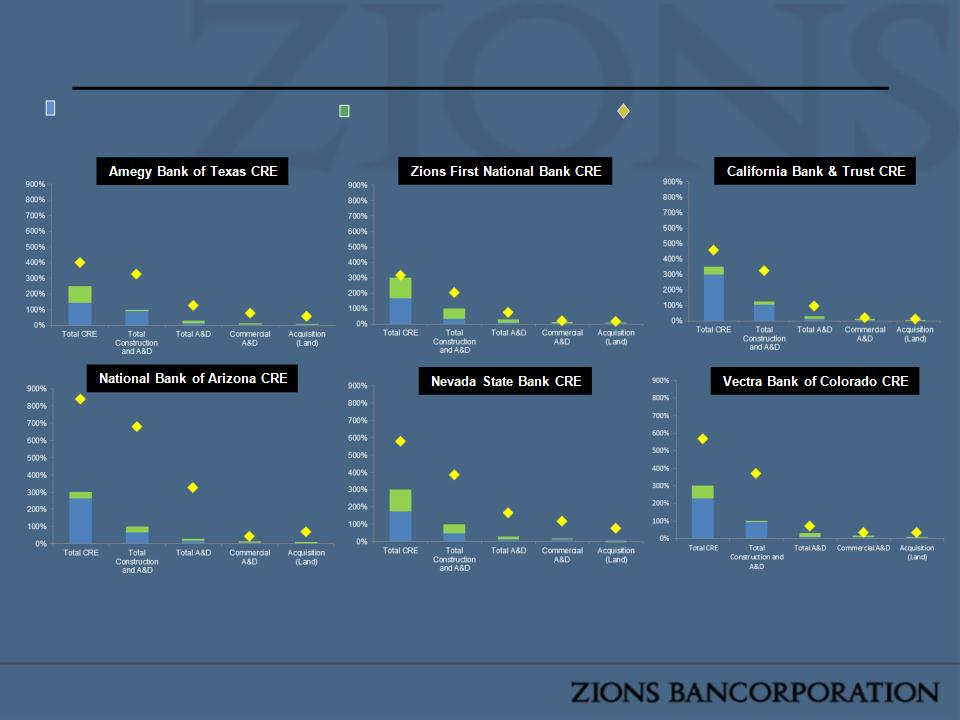

n Concentration policy limits & organization established; integrated into business process

n Board approved risk appetite & limits; risk boundaries aligned with capital

n Corporate Concentration Risk Committee (CCRC) manages appetite and limits

n Limit asset levels set conservatively lower than actual peak downturn

n Current portfolios well below peak concentration levels

n Risk management assessment considers new loan production by market and asset class

n CRE high risk loan alerts provided to relationship managers

Notes: As of Date = 12/31/13; Risk-based cap. As of 9/30/13. Values are Committed Exposure as a percentage of Total Risk Based Capital (CE / TRBC);

Committed Exposure = Bank Balance + Remaining Commitment * Credit Conversion Factor (100% for Construction, 0% for Bankcard, 100% for

C&I and CRE, and 50% for all other assets.;

Exposures Below Limits and Historical Highs

61

Affiliates Within Limits and Historical Highs

Current portfolio as a % of risk based capital

Portfolio limit as a % of regulatory capital

Portfolio peak as a % of regulatory capital

Sources: Total Risk Based Capital = SNL Financial, Bank Balance and Remaining Commitment = EDW.

Notes: As of Date = 12/31/13 (Risk Based Numbers as of 9/30); Values are Committed Exposure as a percentage of Total Risk Based Capital (CE / TRBC);

Committed Exposure = Bank Balance + Remaining Commitment * Credit Conversion Factor (100% for Construction, 0% for Bankcard, 100% for C&I and CRE, and 50% for all

other assets.

other assets.

Commercial Real Estate (CRE) excludes Owner Occupied; Commerce Bank of Washington and Commerce Bank of Oregon excluded as not being material

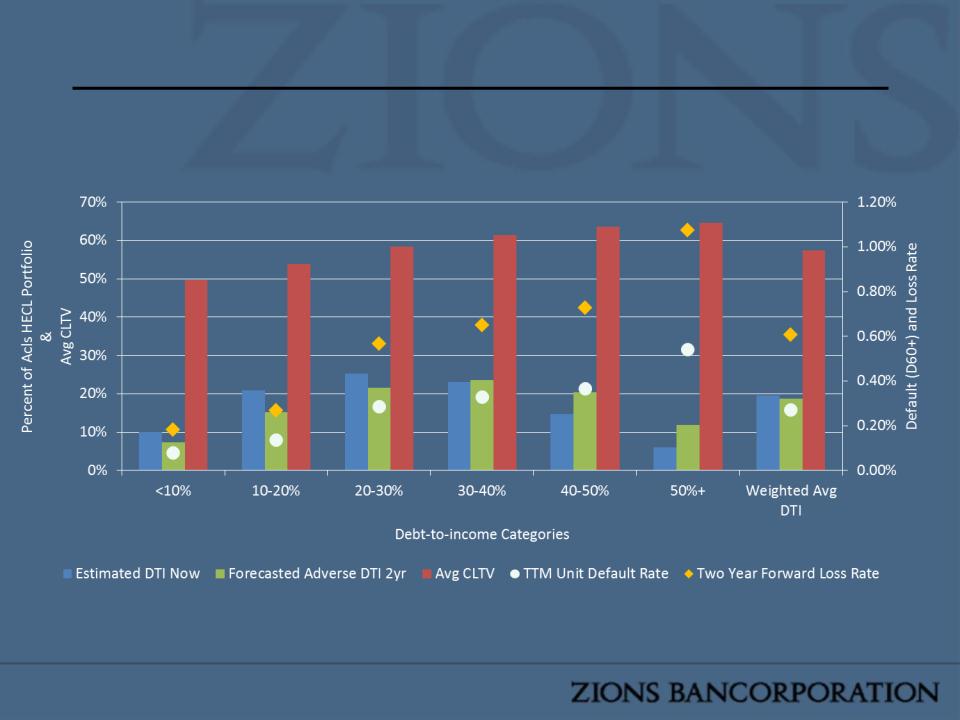

Nominal near-term risk: Under roll-rate methodology, $2B HECL portfolio would generate $5.6 million and $5.3

million in 2014 and 2015 net losses, respectively. Using payment shock method, there is only a nominal

increase to $6.1 million of expected loss for each 2014 and 2015.

million in 2014 and 2015 net losses, respectively. Using payment shock method, there is only a nominal

increase to $6.1 million of expected loss for each 2014 and 2015.

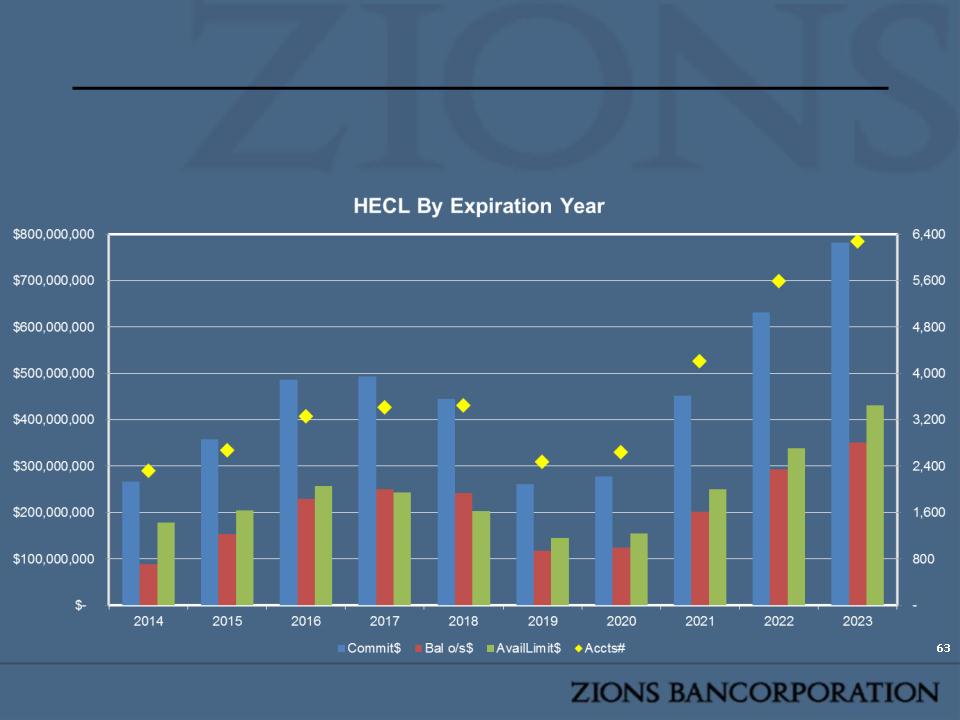

Home Equity Credit Line (HECL) Payment Shock Risk: 2014-2015

62

Combined payment shock of HECLs rolling into an amortizing payment and experiencing an interest rate increase (HECLs are adjustable rate)

estimated by shifting DTIs given higher payment, holding income and other debts flat from origination. The rate environment

contemplated is the Fed’s Adverse Economic Scenario from CCAR (which has the highest interest rate assumptions).

estimated by shifting DTIs given higher payment, holding income and other debts flat from origination. The rate environment

contemplated is the Fed’s Adverse Economic Scenario from CCAR (which has the highest interest rate assumptions).

No Particular Balloon to Pop: There’s a fairly even distribution of loans coming to end of their draw

period over next several years. Highest exposure to payment shock is clearly 2016 and 2017,

but should not have dramatic impact on portfolio as a whole.

period over next several years. Highest exposure to payment shock is clearly 2016 and 2017,

but should not have dramatic impact on portfolio as a whole.

HECL End of Draw Schedule

Loan Growth Outlook, by Type

64

Ø C&I and Owner Occupied Loans

§ Healthy growth expected in Commercial & Industrial lending

§ Small business loan growth is emphasized across the company

§ Middle-market business banking will also play a major role in 2014 C&I growth

Ø CRE Loans

§ Generally limited growth in CA, AZ, CO

§ Stronger growth expected in UT and TX

Ø Mortgage Related Consumer Loans

§ Expect continued healthy to robust growth

Ø Memorandum: National Real Estate (a division of Zions

Bank)

Bank)

§ National Real Estate loans continue to decline; estimated 2014 decline: $500 million

(split between Term CRE and Owner Occupied buckets).

(split between Term CRE and Owner Occupied buckets).

Agenda

• Overview

• Return On Equity: Scenario Analysis

• Under the Hood: Net Interest Margin

• Fee Income Initiative

• Risk Oversight and Credit Management

• CDO Portfolio and Volcker Rule Update

• CCAR

• FutureCore

• Updated Guidance

• Appendix

65

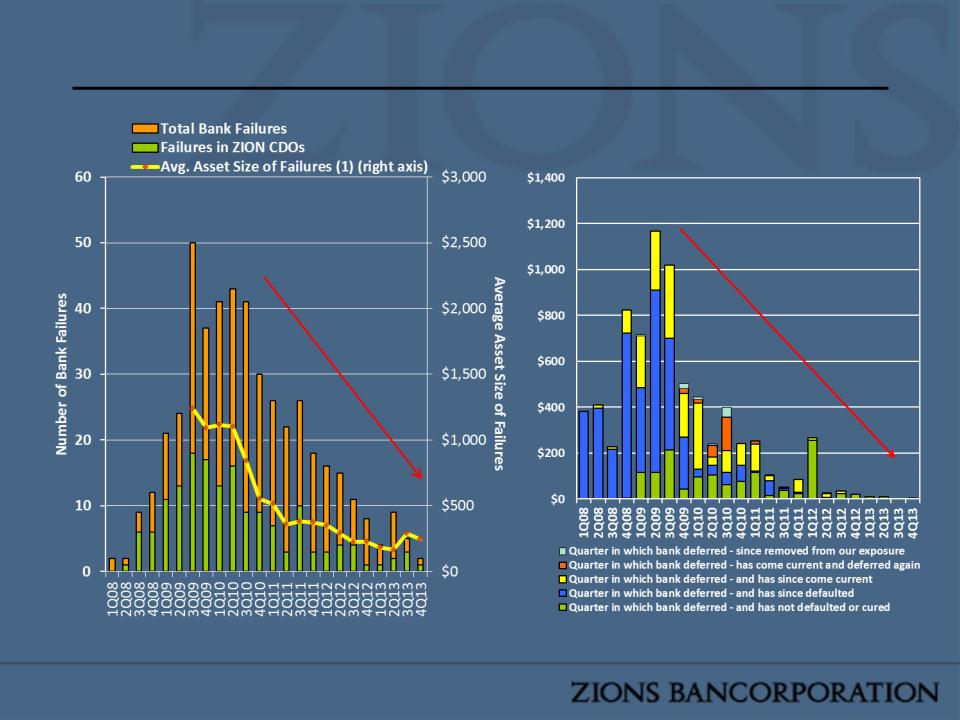

Bank CDOs: Fundamental Trends are Improving

Failures and Deferrals Have Declined Sharply

Failures and Deferrals Have Declined Sharply

66

As of 12-31-2013

(1) Last 12 months. Prior to 3Q09, averages were predominately large banks, significantly skewing the

data.

data.

New Bank Deferrals in Zions’ CDOs

are Trending Downward

(Aggregate Underlying Collateral)

are Trending Downward

(Aggregate Underlying Collateral)

(In millions)

(In millions)

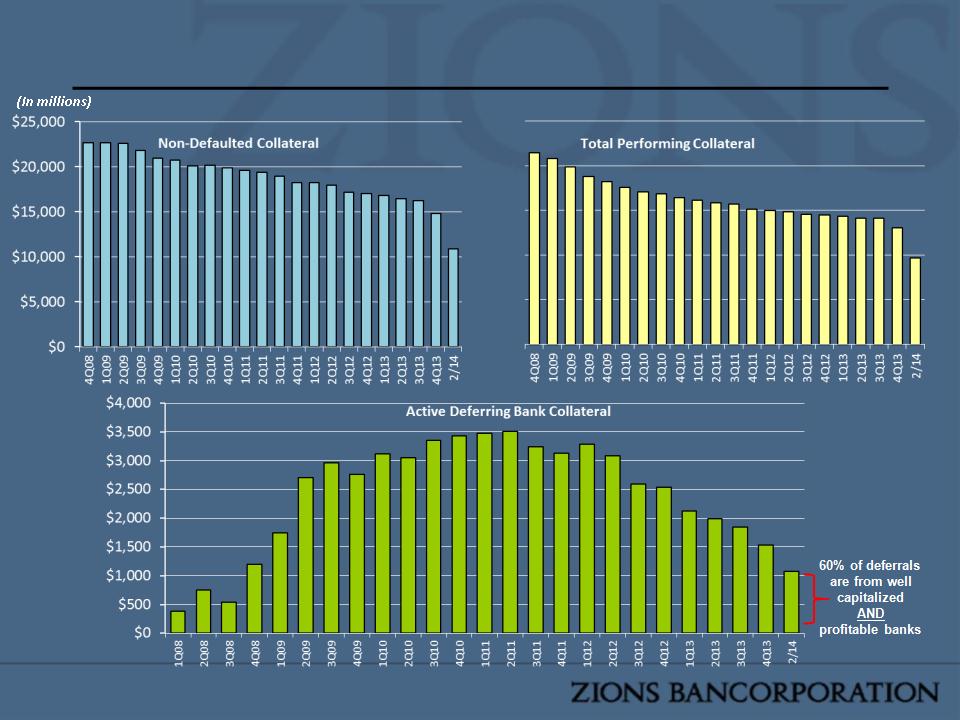

Bank CDOs: Fundamental Trends are Improving

Deferring Bank Re-performance has Increased

Deferring Bank Re-performance has Increased

67

As of 12-31-2013

67

(In millions)

Net of $250 million of re-deferrals from 9 banks

• Peak dollar value of deferring collateral: $3.5 billion (2Q11)

• Current deferring collateral: $1.46 billion

Underlying Collateral for Zions’ CDOs (after 1st Q Sales)

Collateral = the sum of the all trust preferred securities (TRUPS) for all owners of Zions CDO tranches

Collateral = the sum of the all trust preferred securities (TRUPS) for all owners of Zions CDO tranches

68

*Non Defaulted Collateral

CDO Portfolio Composition & Values as of 4Q13

69

December 31, 2013 | |||||

(Amounts in Millions) | # of Tranches | Par Amount | Amortized Cost | Carrying Value | Net Unrealized Losses Recognized in AOCI |

Performing CDOs | |||||

Predominantly Bank CDOs | 23 | $687 | $617 | $499 | -$118 |

Insurance CDOs | 22 | 433 | 413 | 346 | -67 |

Other CDOs | 3 | 43 | 26 | 26 | -- |

Total Performing CDOs | 48 | 1163 | 1056 | 871 | -185 |

Nonperforming CDOs | |||||

CDOs Credit Impaired Prior to Last 12 Months | 32 | 614 | 369 | 285 | -84 |

CDOs Credit Impaired During Last 12 Months | 23 | 448 | 187 | 147 | -40 |

Total Nonperforming CDOs | 55 | 1062 | 556 | 432 | -121 |

Total CDOs | 103 | $2,225 | $1,612 | $1,303 | -$309 |

CDOs Identified for Sale

70

December 31, 2013 | ||||

(Amounts in Millions) | # of Tranches | Par Amount | Amortized Cost | Carrying Value |

Performing CDOs | ||||

Predominantly Bank CDOs | 0 | $0 | $0 | $0 |

Insurance CDOs | 3 | 71 | 55 | 55 |

Other CDOs | 3 | 43 | 26 | 26 |

Total Performing CDOs | 6 | 114 | 81 | 81 |

Nonperforming CDOs | ||||

CDOs Credit Impaired Prior to Last 12 Months | 15 | 291 | 124 | 124 |

CDOs Credit Impaired During Last 12 Months | 12 | 226 | 78 | 78 |

Total Nonperforming CDOs | 27 | 517 | 202 | 202 |

Total CDOs | 33 | $631 | $283 | $283 |

CDO Sale Results

February 14, 2014 | ||||||

(Amounts in Millions) | # of Tranches | Par Amount | Amortized Cost | Loss Taken in 4Q13 | Sale Proceed | Realized Gain/Loss |

Performing CDOs | ||||||

Predominantly Bank CDOs | 0 | $0 | $0 | $0 | $0 | $0 |

Insurance CDOs | 3 | 71 | 55 | -16 | 55 | 0 |

Other CDOs | 3 | 43 | 26 | -8 | 28 | 3 |

Total Performing CDOs | 6 | 114 | 81 | -24 | 83 | 3 |

Nonperforming CDOs | ||||||

CDOs Credit Impaired Prior to Last 12 Months | 15 | 291 | 123 | -53 | 154 | 30 |

CDOs Credit Impaired During Last 12 Months | 12 | 226 | 78 | -60 | 111 | 33 |

Total Nonperforming CDOs | 27 | 517 | 201 | -113 | 265 | 63 |

Total CDOs | 33 | $631 | $282 | -$137 | $348 | $65 |

71

CDO Portfolio Composition & Values

Pro Forma for Sold CDOs*

Pro Forma for Sold CDOs*

72

*Does not reflect improvement observed in values on securities not sold

February 14, 2014 | |||||

(Amounts in Millions) | # of Tranches | Par Amount | Amortized Cost | Carrying Value* | Net Unrealized Losses Recognized in AOCI* |

Performing CDOs | |||||

Predominantly Bank CDOs | 23 | $687 | $617 | $499 | -$118 |

Insurance CDOs | 19 | 362 | 358 | 292 | -66 |

Other CDOs | 0 | 0 | 0 | 0 | 0 |

Total Performing CDOs | 42 | 1049 | 975 | 791 | -184 |

Nonperforming CDOs | |||||

CDOs Credit Impaired Prior to Last 12 Months | 17 | 323 | 245 | 161 | -84 |

CDOs Credit Impaired During Last 12 Months | 11 | 222 | 109 | 69 | -40 |

Total Nonperforming CDOs | 28 | 545 | 354 | 230 | -124 |

Total CDOs | 70 | $1,594 | $1,329 | $1,021 | -$308 |

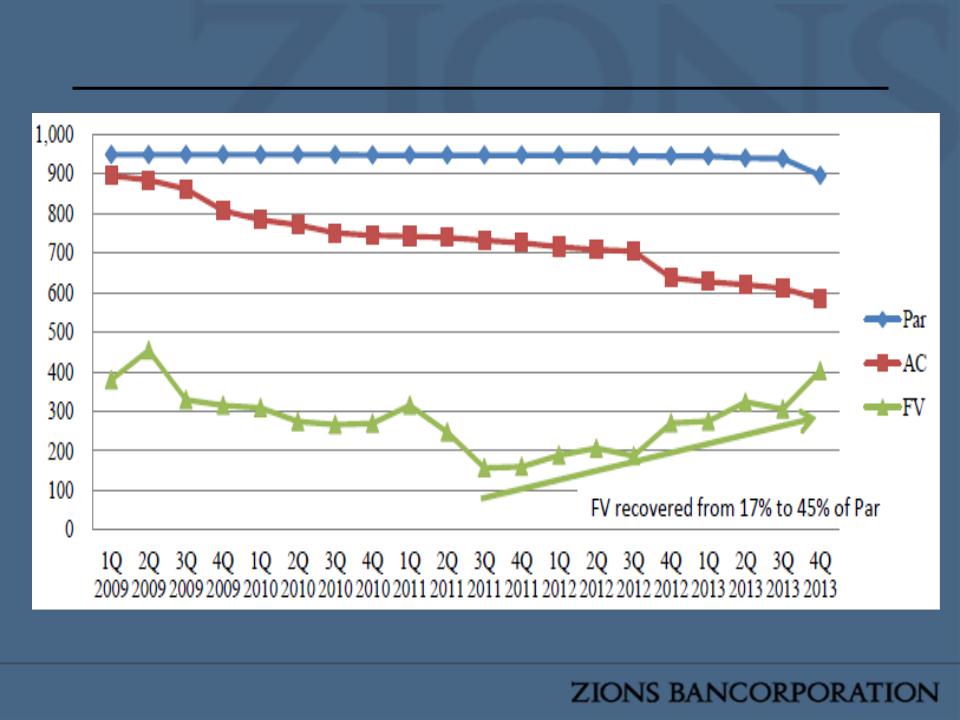

Mezzanine CDO Value History: Recovery of value has been

significant, particularly on mezzanine (Original A Rated) securities

significant, particularly on mezzanine (Original A Rated) securities

73

Agenda

• Overview

• Return On Equity: Scenario Analysis

• Under the Hood: Net Interest Margin

• Fee Income Initiative

• Risk Oversight and Credit Management

• CDO Portfolio and Volcker Rule Update

• CCAR

• FutureCore

• Updated Guidance

• Appendix

74

CCAR, Volcker Rule, and CDO Sales

• Original CCAR submission projected over $600

million of capital stress from CDO portfolio under

severe stress scenarios due to Volcker Rule.

million of capital stress from CDO portfolio under

severe stress scenarios due to Volcker Rule.

• CDO sales and Volcker Rule revisions materially

reduce the adverse impact.

reduce the adverse impact.

• Zions expects to resubmit a revised CCAR stress

test and capital plan by late March / early April.

test and capital plan by late March / early April.

• Capital distributions are still likely to be

conservative in 2014.

conservative in 2014.

75

Major improvements in all CCAR principles

1. Foundation Risk Management

• Created CRO position, updated all major risk policies and risk appetite

framework

framework

2. Effective Loss Estimation

• Created loan level loss models for C&I and Resi

• Approximately 90% of loan portfolio modeled at loan level

3. Capital Resource Estimation

• Significant enhancement to revenue projection methods

• Model loan origination, prepayment, charge-off, amortization

• Loan growth and pricing estimated at major product level

4. Capital Adequacy Impact

• Integrated loss and revenue projection in ALM system

• Developed Bottom-up approach to forecast RWA

• Created CAP improvement group

76

Major improvements in all CCAR principles (Cont’d)

5. Comprehensive Capital Policy and Planning

• Rewritten Capital Policy

• Substantial improvements and documentation of procedures

6. Robust Internal Controls

• Improved Model Risk Management practice

• Increased control points in CAP procedures

• Expanded documentation

7. Effective Governance

• Increased level and standardization of Board reporting

• Established governance procedures for management overlays

• Enhanced guidelines for reviewing potential capital transactions

77

Agenda

• Overview

• Return On Equity: Scenario Analysis

• Under the Hood: Net Interest Margin

• Fee Income Initiative

• Risk Oversight and Credit Management

• CDO Portfolio and Volcker Rule Update

• CCAR

• FutureCore

• Updated Guidance

• Appendix

78

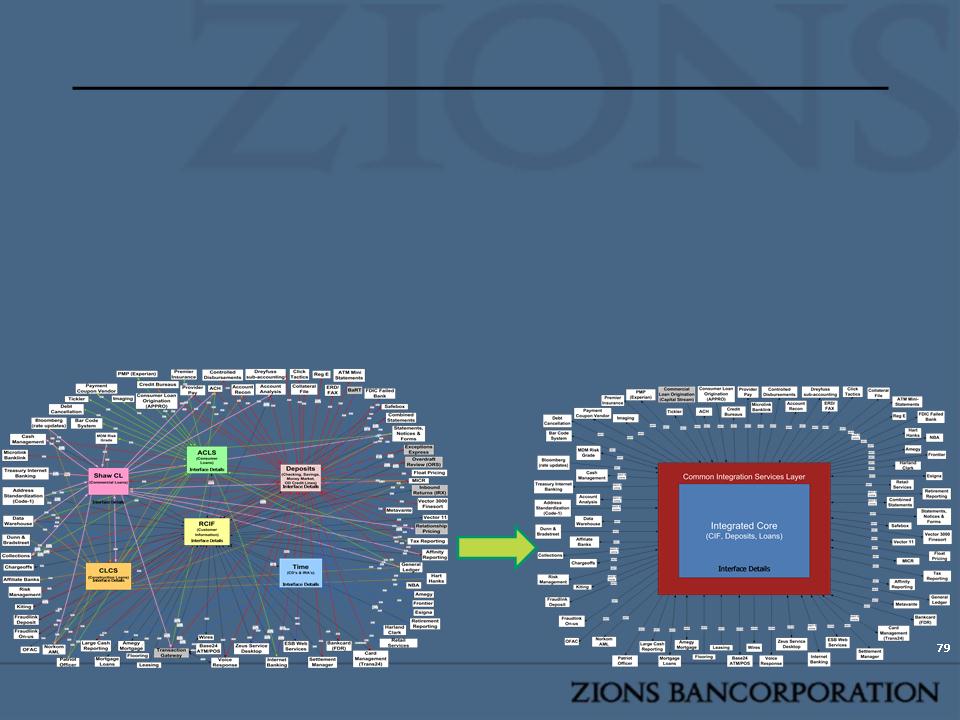

Systems Upgrade Overview

• FutureCore is a program initiated by Zions Bancorporation to replace

its core operating systems into a single application

its core operating systems into a single application

• Zions is working with TCS (Tata Consultancy Services) to implement

their BαNCS operating software

their BαNCS operating software

• Zions managed, but 3rd party oversight reports directly to the board

Current State

Future State

Systems Upgrade Benefits

Key benefits of FutureCore | How will this help? |

Real-time processing | -Transactions, balances and other information updated immediately -Less manual and more efficient processing |

Standardization of processes and data | -Reduced customization reduces cost -Significant improvement to customer profitability analysis -Better equipped for FR Y-14 stress test data |

Loans & deposits on one system | -360* view of our relationship with customer -Quicker to access customer information across multiple systems -Fewer systems to maintain & train |

Parameter-based | -Ability to quickly develop & introduce banking products |

Configurable | -Quicker and less costly system upgrades |

Agenda

• Overview

• Return On Equity: Scenario Analysis

• Under the Hood: Net Interest Margin

• Fee Income Initiative

• Risk Oversight and Credit Management

• CDO Portfolio and Volcker Rule Update

• CCAR

• FutureCore

• Updated Guidance

• Appendix

81

Key Takeaways: Medium to Long Term Outlook

82

Ø Return on Equity

§ Return on Tangible Common Equity can improve through loan growth, modest

amounts of asset duration extension, executing on the fee income initiative, and/or an

increase in interest rates

amounts of asset duration extension, executing on the fee income initiative, and/or an

increase in interest rates

Ø Significant Reduction in Risk Profile vs. Pre-Crisis

§ Sale of CDOs with highest risk weighting and greatest impact on stress test capital

§ Significant reduction of land acquisition and development and construction loans

Ø Significant Improvement in Risk Processes vs. Pre-Crisis

§ Upgraded data integrity and management information systems, streamlined processing

§ Comprehensive Risk Appetite Framework, including concentration limits

§ Stress testing capabilities greatly expanded, which is assisting in identifying and

mitigating elevated risk areas

mitigating elevated risk areas

§ Enabling loan growth, while carefully managing risk

Key Takeaways: Medium to Long Term Outlook (Cont’d)

83

Ø Net Interest Income: Playing for the Long Term

§ Will continue to avoid assuming risk we don’t know how to manage - namely, duration

extension risk from MBS, with a related shortage of funding for loan growth at precisely

the time when MBS prepayments are slowing

extension risk from MBS, with a related shortage of funding for loan growth at precisely

the time when MBS prepayments are slowing

§ May add receive fixed/pay float swaps to extend duration somewhat as rates rise -

“Zions may taper in, as the Fed tapers out”

“Zions may taper in, as the Fed tapers out”

§ Loan pricing on new production appears to be stabilizing, but at dilutive yields to book

yields

yields

Ø Fee Income Initiative

§ Significant opportunities to improve penetration rates for existing products, driven by

stronger focus and better cross-selling tools and effort

stronger focus and better cross-selling tools and effort

§ Infrastructure already in place in most cases

Ø Non-Interest Expense: Long Term Effort to Improve Efficiency

§ So-called “environmental costs” & FDIC indemnification asset expense reductions to

layer in over 12-24 months.

layer in over 12-24 months.

§ FutureCore and other systems upgrades will ultimately reduce costs and enable a more

streamlined organization, but not in the near term horizon.

streamlined organization, but not in the near term horizon.

§ Ongoing expense management (e.g. branch office rationalization)

Topic | Outlook | Comment |

Loan Balances | Slightly to Moderately Increasing | • Prepayments remain volatile, making net loan growth difficult to forecast |

Net Interest Income | Moderately Declining | • FDIC Covered Loan income likely to experience further decline • Excluding interest income from covered loans, NII likely generally stable to slightly increasing, assuming moderate loan growth and debt reduction |

Provisions | Moderately Negative | • Includes Provisions for Loan Losses & Reserve for Unfunded Loan Commitment |

Fee Income | Increasing | • Excluding securities impairment charge, fee income initiatives likely to result in moderate increase |

Noninterest Expense | Decreasing | • 4Q13 NIE included $80 million from debt extinguishment and elevated expenses from professional services related to regulatory obligations (CCAR, living will) • Higher expenses stemming from loan/deposit/accounting systems upgrade, offset by reduced credit-related NIE and subsiding FDIC Indemnification Asset amortization |

Net Income Available to Common | Increasing | • 4Q13 included the significant effects from two items that are unlikely to reoccur, which resulted in a loss for the quarter. Excluding such items, GAAP Net Income Available to Common is likely to be stable to slightly higher. |

One-Year Outlook Summary

Relative to 4Q13 Results

Relative to 4Q13 Results

84

Agenda

• Overview

• Return On Equity: Scenario Analysis

• Under the Hood: Net Interest Margin

• Fee Income Initiative

• Risk Oversight and Credit Management

• CDO Portfolio and Volcker Rule Update

• CCAR

• FutureCore

• Updated Guidance

• Appendix

85

Calculation for Normalized Net Income in 4Q13

86

Right hand column reflects a tax rate of 38.75%

Systems Upgrade (“FutureCore” - core processing system upgrade, chart of accounts overhaul, and front-end

loan entry system upgrade): $28mm additional estimated, on average (This does not include the

approximately $18 mm annualized of systems upgrade expense recognized in 4Q13)

loan entry system upgrade): $28mm additional estimated, on average (This does not include the

approximately $18 mm annualized of systems upgrade expense recognized in 4Q13)

Item | Pre-Tax | After-Tax | ||

Net Income as Reported | -$59.4 | |||

OTTI | $141.7 | $86.8 | ||

Debt Extinguishment | $79.9 | $48.9 | ||

Professional & Legal | $10.0 | $6.1 | ||

Regulatory Related | $6.0 | $3.7 | ||

Credit Related | $3.0 | $1.8 | ||

Allowance for Unfunded | $3.0 | $1.8 | ||

Indemnification Asset Exp. | $19.9 | $12.2 | ||

FDIC Income | -$28.5 | -$17.5 | ||

Additional Expenses for Systems Upgrade* | -$7.0 | -$4.3 | ||

Adjusted Net Income | $80.3 |

A Collection of Great Banks

More than 70% of Assets in Utah / Texas / Coastal California

More than 70% of Assets in Utah / Texas / Coastal California

87

Subsidiary information as of 3Q13

§ Superior lending capacity relative

to community banks

to community banks

§ Superior local customer access to

bank decision makers relative to

big nationals

bank decision makers relative to

big nationals

§ Centralization of some processing

and other non-customer facing

elements of the business to

achieve efficiencies

and other non-customer facing

elements of the business to

achieve efficiencies

§ Strategic local “ownership” of

market opportunities and

challenges

market opportunities and

challenges

Awards: Nationally Recognized for Excellence

• Twelve (12) Greenwich Excellence Awards in Small Business and

Middle Market Banking (2013)

Middle Market Banking (2013)

• Including:

§ Excellence: Overall Satisfaction

§ Excellence: Likelihood to Recommend

§ Excellence: Treasury Management

§ Excellence: Financial Stability

Only 11 U.S. banks were awarded more than 10 Excellence awards in 2013; Zions has

been consistently awarded more than 10 awards per year for many years in a

row.

been consistently awarded more than 10 awards per year for many years in a

row.

• Nationally Ranked in the Top 10 in Small Business Loan production 1

• Top team of women bankers - American Banker2

88

1. Volume and number of loans, SBA fiscal year ended September 30, 2013

2. One of four winning teams, 2013, Zions Bank

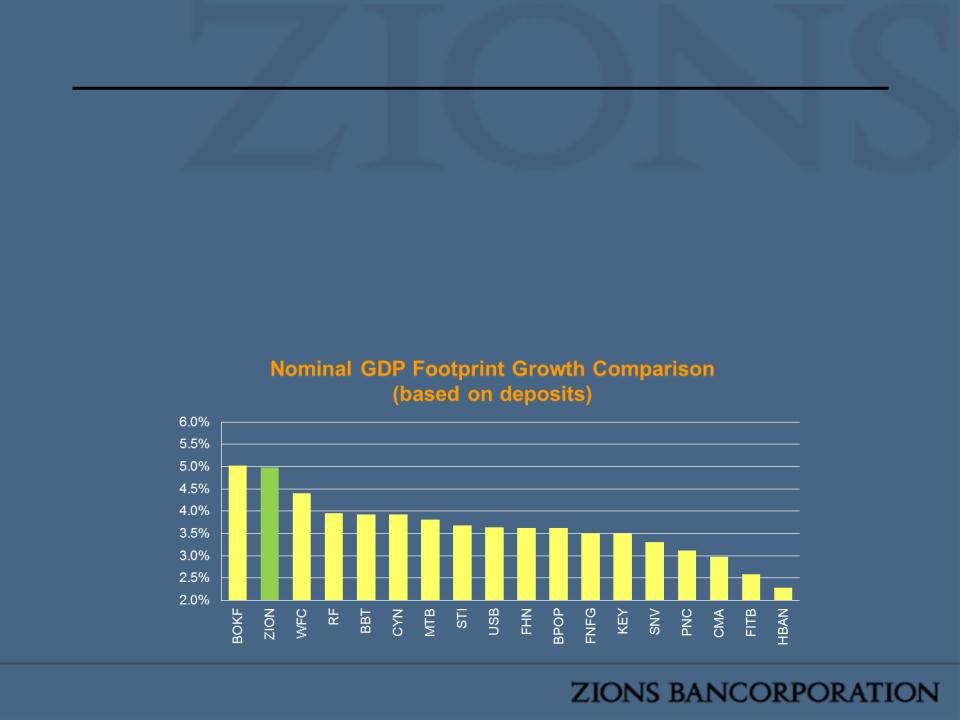

§ Job Creation:

Jobs grew in Zions' footprint by 13.5% during the last 10 years, a full 8 percentage points

better than U.S. nonfarm payroll growth

better than U.S. nonfarm payroll growth

§ GDP Growth:

GDP growth in our footprint exceeded nominal U.S. GDP by an average of 1.3 percentage

points per year (compounded) over the last ten years

points per year (compounded) over the last ten years

Stronger Economic Growth than Overall U.S.

89

Source: SNL, Bureau of Economic Analysis and Zions’ calculations as of 4Q13

Balance Sheet Mix

Strengths include a strong mix of loans and DDA funding

Strengths include a strong mix of loans and DDA funding

90

Source: Company documents as of 3Q13

Source: Company Documents for Zions as of 4Q13, SNL Financial for peers as of 3Q13

*Includes farm, home equity, consumer, and other loans

91

Strong Focus on Business Banking & Smaller-Sized Customers - Loan Mix

• Small Loans < $5M Commitment

• Large Loans > $5M Commitment

Small

Loans

Loans

Large

Loans

Loans

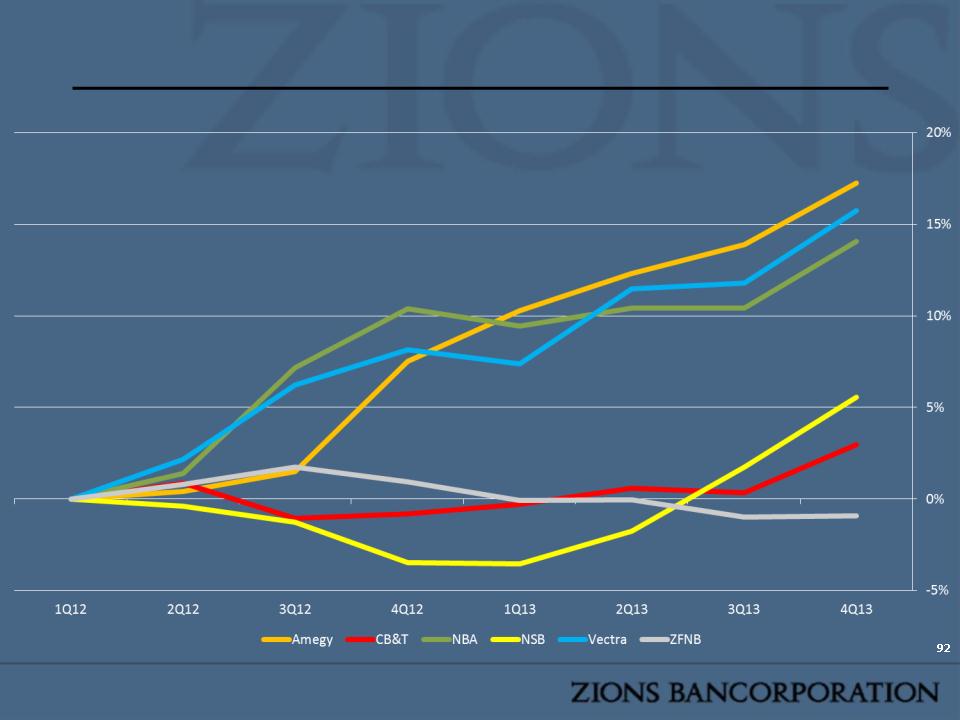

Loan Growth by Bank

Portfolio overview:

§Credit quality metrics have improved materially in:

– All loan types

– All geographies

§Problem loan inflows continue to slow; most resolutions

are favorable; charge-offs are declining; loss severities are

declining

are favorable; charge-offs are declining; loss severities are

declining

§Loan loss reserve is strong and problem loan coverage

improving

improving

Credit Quality Key Takeaways

93

Credit Quality - Total Portfolio

4Q13 | 3Q13 | 4Q12 | |

Total Loan Balance ($B) | 39.2 | 38.4 | 37.9 |

Total Delinquencies | 0.8% | 0.8% | 1.5% |

Total Non-Performing Loans | 1.0% | 1.2% | 1.7% |

Total Classifieds | 3.2% | 3.7% | 4.7% |

% of Classifieds Performing | 84.4% | 83.9% | 78.6% |

Total Net Charge-Offs | 0.2% | 0.1% | 0.2% |

Total Loan Balance

Total Loan Balance Key Statistics

94

Source: SNL and company documents

Loan growth is strong and charge offs remain low compared to Comm’l Banks

Rolling NCO rate gradually declined from 0.41% in 2012 Q4 to 0.13% in 2013 Q4

Credit quality metrics indicate improving trends

Rolling NCO rate gradually declined from 0.41% in 2012 Q4 to 0.13% in 2013 Q4

Credit quality metrics indicate improving trends

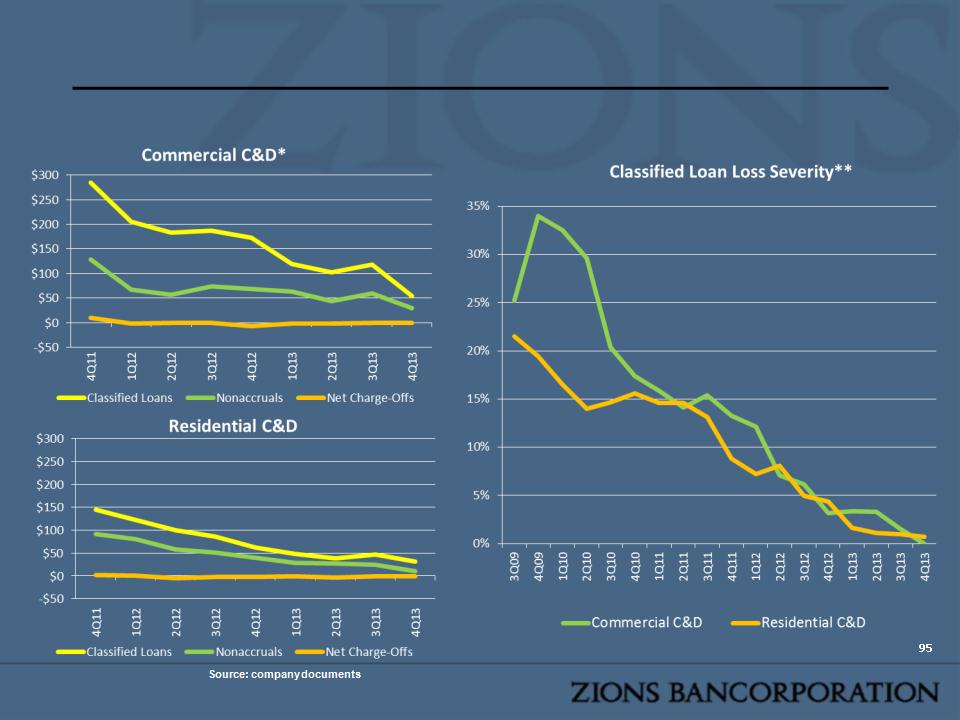

C&D Problem Loans Also Improving

*Commercial includes multi-family

**Based on gross charge-offs

Current Commercial C&D Balance - $1.5B (3.9% of Total Loans); Residential C&D - $713MM (1.8% of Total

Loans)

Loans)

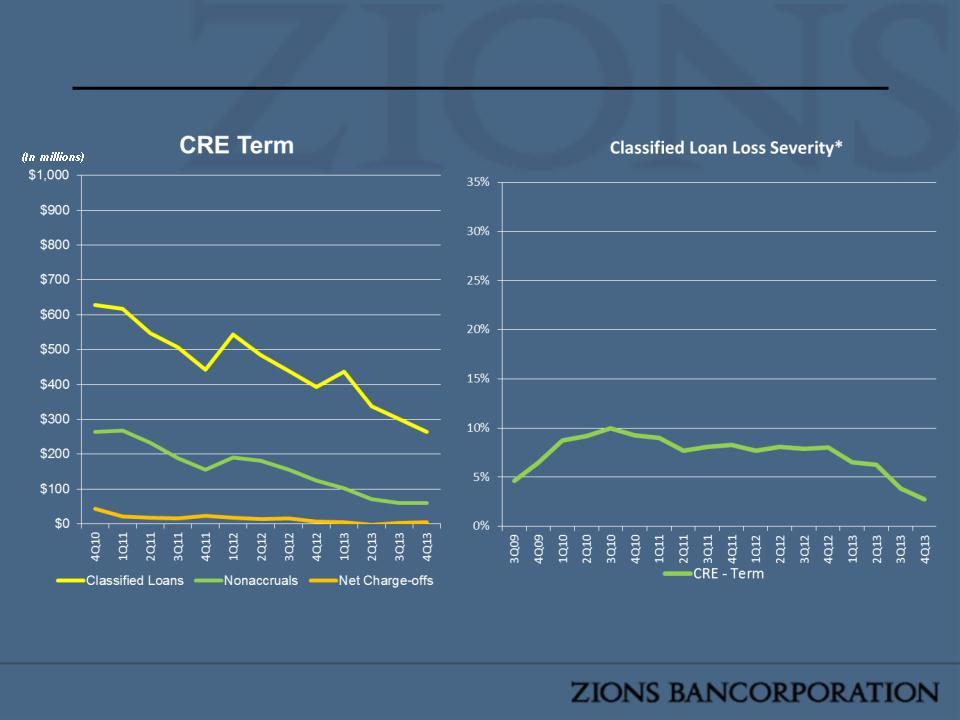

Term CRE Portfolio Improving

Term CRE Key Statistics

4Q13 | 3Q13 | 4Q12 | |

Loan Balance ($B) | 8.0 | 8.2 | 8.1 |

Delinquencies | 1.1% | 0.8% | 1.8% |

Non-Performing Loans | 1.4% | 1.4% | 2.9% |

Classifieds | 3.3% | 3.7% | 4.9% |

% of Classifieds Performing | 90.8% | 89.0% | 80.9% |

Net Charge-Offs | 0.1% | 0.2% | 0.3% |

Collateral

96

Gradient Fill - 2013 % mix ↓from 2008

Solid Fill - 2013 % mix ↑ from 2008

Source: SNL and company documents

Current Term CRE Balance - $8.0B (21.0% of Total Loans)

Term CRE balances steady with improving NCO rate

Credit quality metrics for Term CRE show improving trends

Credit quality metrics for Term CRE show improving trends

Source: company documents and earnings releases

*Based on gross charge-offs

Term CRE Losses and Loss Severity Improving

97

• Left - Sample data: As of 4Q13; non-FDIC supported term loans > $500k balance

• Right - As of 4Q13; LTVs were adjusted using PPR’s market level/property type value trend indices

98

Term CRE Metrics are Solid

Term CRE collateral shows strong cash flow

99

(In billions)

• Sample data: As of 4Q13; term loans > $500k balance

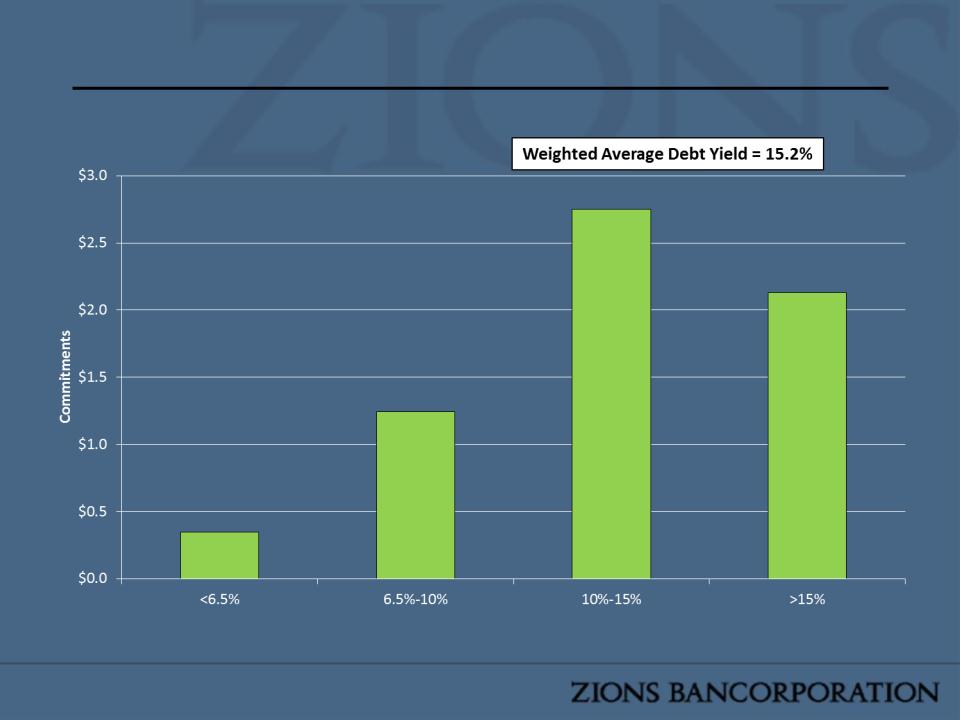

Loans with high debt yield ratios have lower refinance risk.

Real Estate Loan Portfolio Mix

Higher Risk Loans Declining, Growth in Apartment Loans

Higher Risk Loans Declining, Growth in Apartment Loans

100

Portfolio Mix Shifting Away From Risky Assets

Loan Balance Changes From 2008

RE Property Type | 4Q13 |

Residential | 30.3% |

Warehouse | 9.2% |

Other | 12.4% |

Office | 19.1% |

Retail | 10.4% |

Apartment | 6.4% |

Hospitality | 7.6% |

Land and Lots | 3.6% |

Unsecured | 1.2% |

Total | 100.0% |

4Q08 | 4Q13 | % Change | |

Apartment | 1.4 | 2.1 | 50.0% |

Office* | 5.1 | 2.8 | -45.1% |

Warehouse* | 2.5 | 4.2 | 68.0% |

Other Real Estate | 3.5 | 3.2 | -8.6% |

Hospitality | 2.2 | 1.7 | -22.7% |

Retail | 3.0 | 2.2 | -26.7% |

Residential | 9.0 | 7.9 | -12.2% |

Unsecured | 0.5 | 0.2 | -60.0% |

Land and Lots | 2.5 | 0.7 | -72.0% |

Grand Total | 29.7 | 25.0 | -15.8% |

Source: Company documents

*An internal collateral code classification was changed from office to warehouse in 2012; warehouse and office

collectively dropped 7.9% from 4Q08-4Q13

Current RE Balance - $25.0B (63.8% of Total Loans)

Portfolio Diversified by Geography and Property Type

Term CRE Predominately in Footprint

Term CRE Predominately in Footprint

10

1

1

Location

Property Type

Data as of 4Q13. Source: company documents

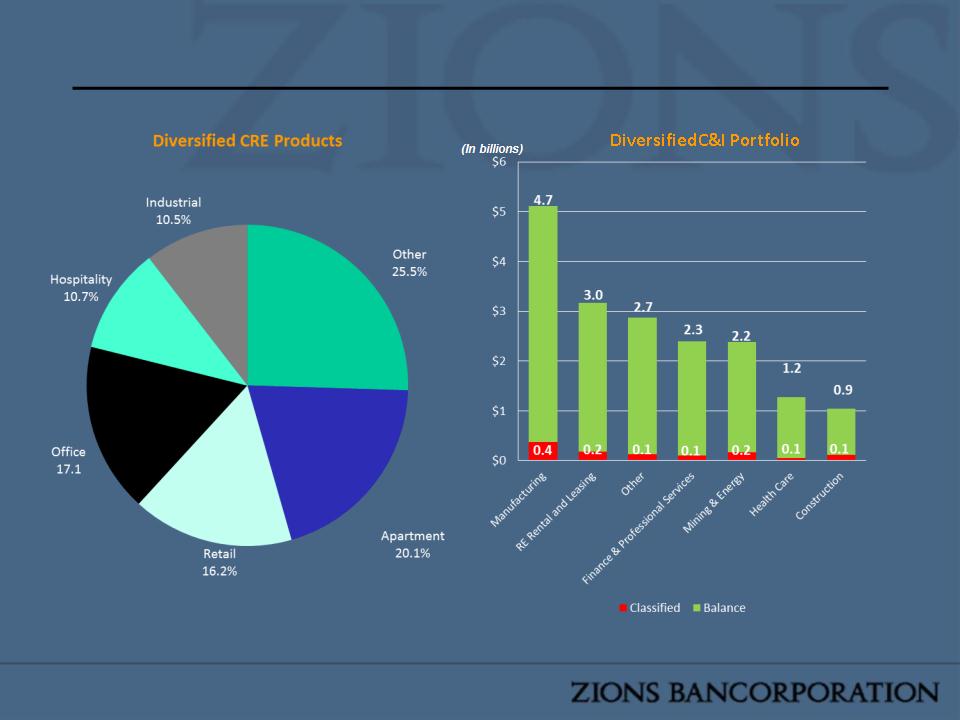

Sources of Interest Income from Diversified

Property Types and Industries

Property Types and Industries

102

Data as of 4Q13. Source: company documents

Credit Quality Improving in Commercial and Industrial

C&I Key Statistics

4Q13 | 3Q13 | 4Q12 | |

Loan Balance ($B) | 20.7 | 20.1 | 19.5 |

Delinquencies | 0.9% | 0.9% | 1.4% |

Non-Performing Loans | 1.2% | 1.3% | 1.6% |

Classifieds | 4.1% | 4.5% | 4.6% |

% of Classifieds Performing | 86.1% | 87.4% | 80.9% |

Net Charge-Offs | 0.1% | 0.1% | 0.2% |

C&I Loan Balance

10

3

3

Current C&I Balance - $20.7B (53.3% of Total Loans)

Source: SNL and company documents

C&I balances increasing with improving NCO rate

Credit quality metrics for C&I show uniformly improving trends

Credit quality metrics for C&I show uniformly improving trends

Source: Company Documents.

* Based on gross charge-offs

Owner Occupied Losses & Loss Severity Improving

10

4

4

Current C&I OO Balance - $7.7B (19.8% of Total Loans)

Increase attributable to

National Real Estate

grading methodology

change

National Real Estate

grading methodology

change

Credit Quality Improving in Consumer

Consumer Key Statistics

4Q13 | 3Q13 | 4Q12 | |

Balance ($B) | 7.7 | 7.5 | 7.3 |

% of Total Loan Portfolio | 19.6% | 19.7% | 19.3% |

Delinquencies | 0.7% | 0.8% | 1.2% |

Net Charge-Offs | 0.02% | 0.1% | 0.6% |

Consumer Loan Balance

10

5

5

Current Consumer Balance - $7.7B (19.8% of Total Loans)

Source: SNL and company documents

Consumer balances increasing with improving NCO rate

Credit quality metrics for Consumer show improving trends

Credit quality metrics for Consumer show improving trends

106

Source: company documents

*Sample covers 99% of portfolio

Data as of 4Q13

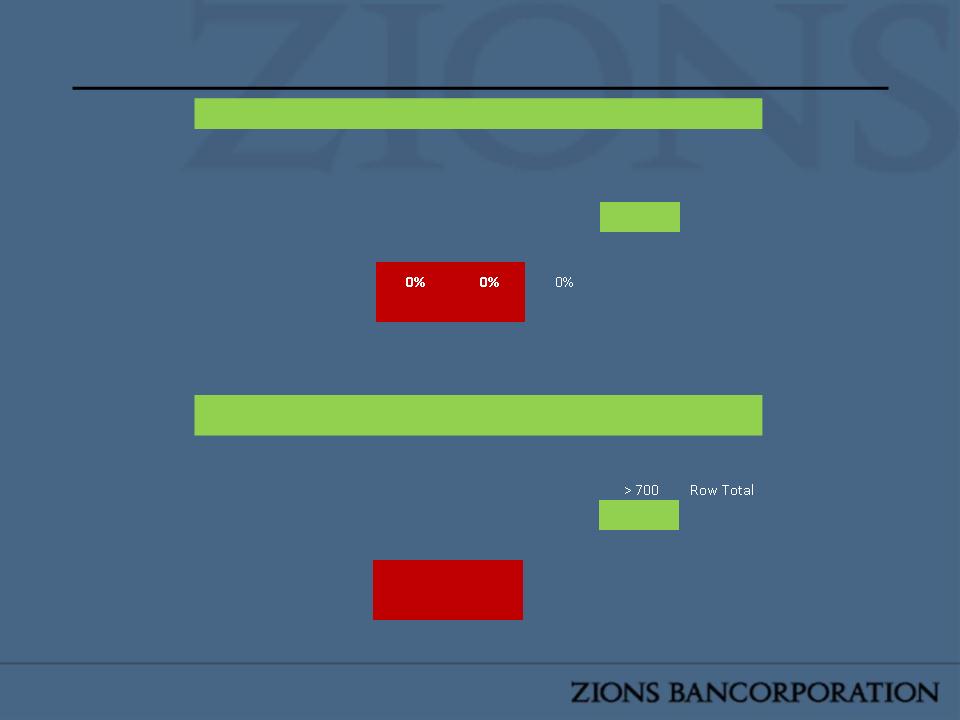

Majority of HECLs in Under 80% LTV Category

Current LTV- FICO Distribution on Mortgage Loans:

Very Limited Layering of Risk (e.g. high LTV, low FICO)

Very Limited Layering of Risk (e.g. high LTV, low FICO)

107

FICO Segments | ||||||

<= 600 | 600-650 | 650-700 | > 700 | Row Total | ||

LTV Segments | < 80 | 2% | 2% | 7% | 67% | 79% |

80-90 | 1% | 0% | 1% | 7% | 10% | |

90-100 | 0% | 0% | 1% | 4% | 5% | |

> 100 | 0% | 0% | 1% | 5% | 6% | |

Column Total | 3% | 4% | 10% | 83% | 100% | |

FICO Segments | ||||||

<= 600 | 600-650 | 650-700 | > 700 | Row Total | ||

LTV Segments | < 80 | 2% | 2% | 6% | 81% | 90% |

80-90 | 0% | 0% | 0% | 4% | 5% | |

90-100 | 0% | 0% | 0% | 2% | 2% | |

> 100 | 0% | 0% | 0% | 2% | 2% | |

Column Total | 2% | 2% | 7% | 89% | 100% | |

1st Lien Mortgages

Junior Lien Mortgages

Source: company documents

Data as of 4Q13

Affiliate Information

108

Amegy Bank of Texas

February 2014

• 15th largest economy in the world

• Population ranks 2nd in the U.S.

• Leads the nation in job creation

• 5.6% unemployment rate

• 2012 housing starts exceeded 60,000

• Ranked 1st by export revenues in the

U.S.

U.S.

110

Houston…Operating in a Diversified Economy

• 3,700+ energy-related

entities

entities

• Home to 40 of the nation’s

145 publicly traded oil and

gas E&P firms, and 10 of the

top 25

145 publicly traded oil and

gas E&P firms, and 10 of the

top 25

• The nine refineries in the

Houston region produces

13.3% of total U.S. crude oil

capacity

Houston region produces

13.3% of total U.S. crude oil

capacity

• By 2021, the Eagle Ford Shale

should generate $90+ billion

in total economic output and

support 116,000 jobs

should generate $90+ billion

in total economic output and

support 116,000 jobs

• 106,000 employees

• Construction projects worth

$7B to be completed by 2014

$7B to be completed by 2014

• Creates $10 billion in

regional spending

regional spending

• 1,300+ acres; larger than

Chicago’s Inner Loop

Chicago’s Inner Loop

• 45.8MM sq. ft. of patient

care, education & research

space

care, education & research

space

• 54 institutions

• First in U.S. in foreign

tonnage; second in U.S. for

total tonnage; world’s tenth

largest

tonnage; second in U.S. for

total tonnage; world’s tenth

largest

• 7,700+ ships visit annually

• $15 billion petrochemical

complex; 2nd largest in the

world

complex; 2nd largest in the

world

• 3,500+ companies trade 180+

types of products in 183

countries

types of products in 183

countries

• Ship channel-related

businesses contribute 1MM+

jobs across Texas

businesses contribute 1MM+

jobs across Texas

Home of the world’s largest

health care complex

health care complex

Energy capital of the world

Port of Houston

111

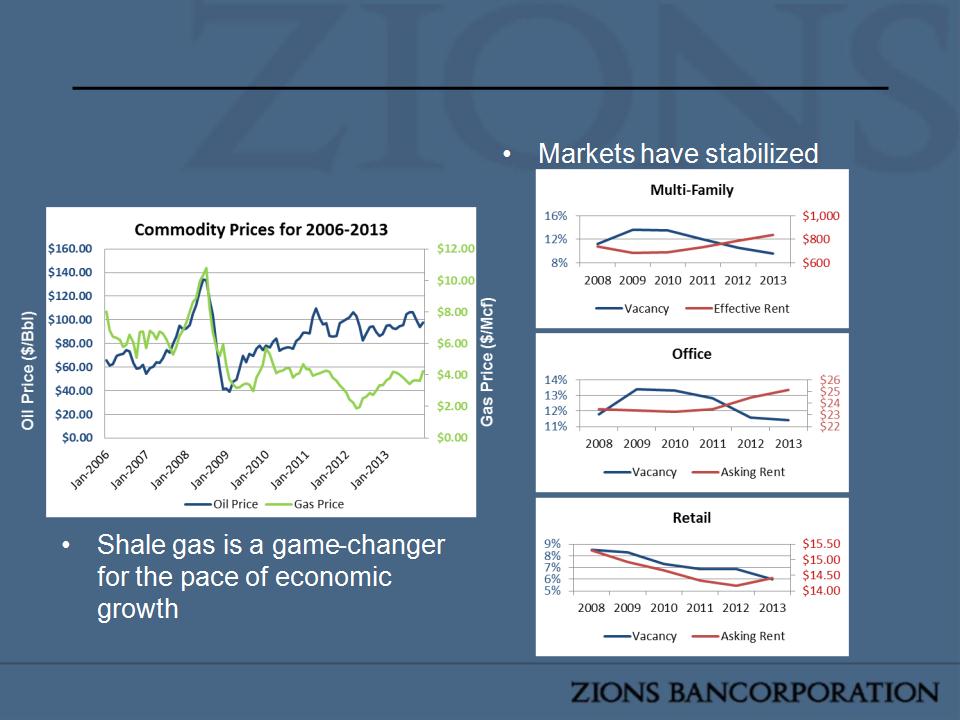

Two Key Market Segments

Energy

• Economy has rebounded since

`08-`09 price volatility

`08-`09 price volatility

Commercial Real Estate

112

Source: Property and Portfolio Research (PPR)

Recent Significant Accomplishments

•#1 middle market bank* (lead

relationship share)

relationship share)

•#2 treasury management bank*

•#3 small business bank* (lead

relationship share)

relationship share)

•#2 SBA lender in Houston

•4.8% deposit market share (JPM,

BAC, WFC: 58% deposit market

share)

BAC, WFC: 58% deposit market

share)

•#7 in U.S. for EX-IM working

capital loans with Fast Track

Lending Authority

capital loans with Fast Track

Lending Authority

*Data based on 2011 full-year Greenwich Associates research

113

Core Earnings Remain Strong

114

($’s in millions)

Loan Portfolio…Becoming More Granular

115

Loans by Line of Business

Dec MTD Average

Expense Control…Remains a Key

116

Fee Income…Growth Opportunity Muted by Legislative and Economic

Conditions

Conditions

117

(1) 2008 Adjusted for $38mm swap

gain.

gain.

Net Charge-offs…Fared Better than Most

118

(1) Peer Group includes 64 publicly traded companies with assets > $10 Billion. Average is

weighted by Total Net Loans.

weighted by Total Net Loans.

(2) Analyst Peer Group consists of 19 publicly traded banks stock analysts deem Zions’

Peers. Average is weighted by Total Net Loans.

Peers. Average is weighted by Total Net Loans.

119

Amegy Bank of Texas…Well-positioned for the Future

120

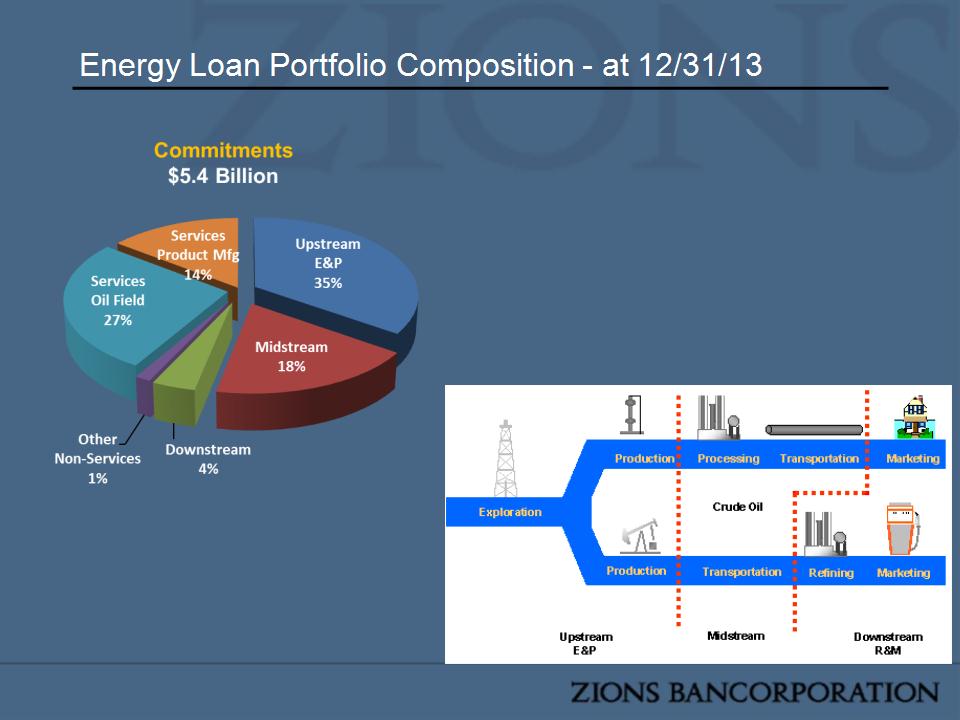

Energy Loan Portfolio

Energy Cycle

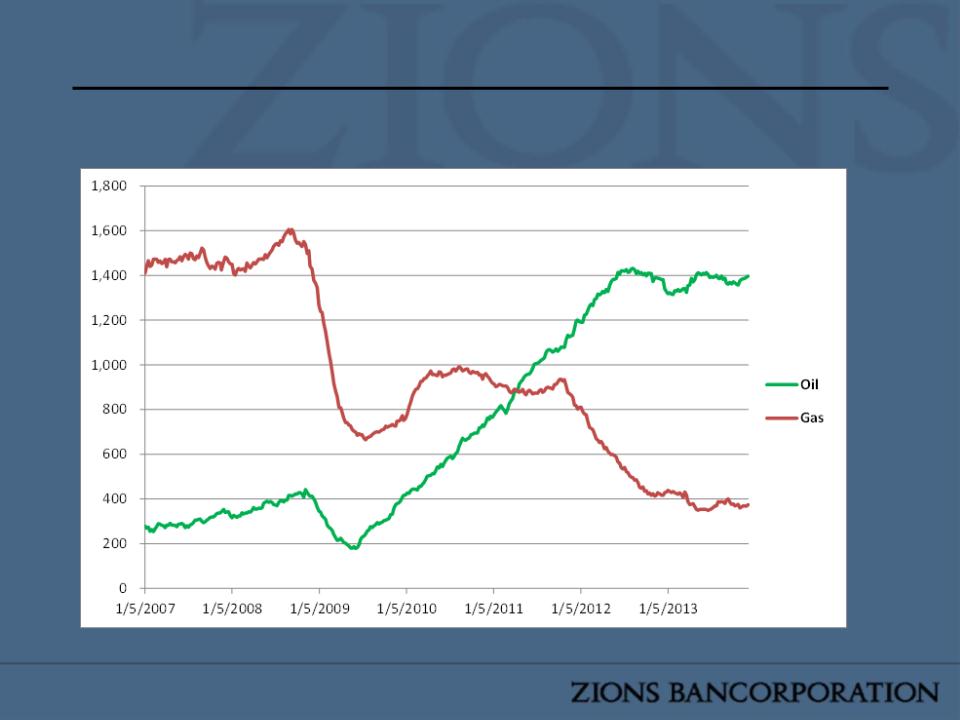

Oil and Gas…A Historical Snapshot

122

US Rig Count - Oil/Gas

123

124

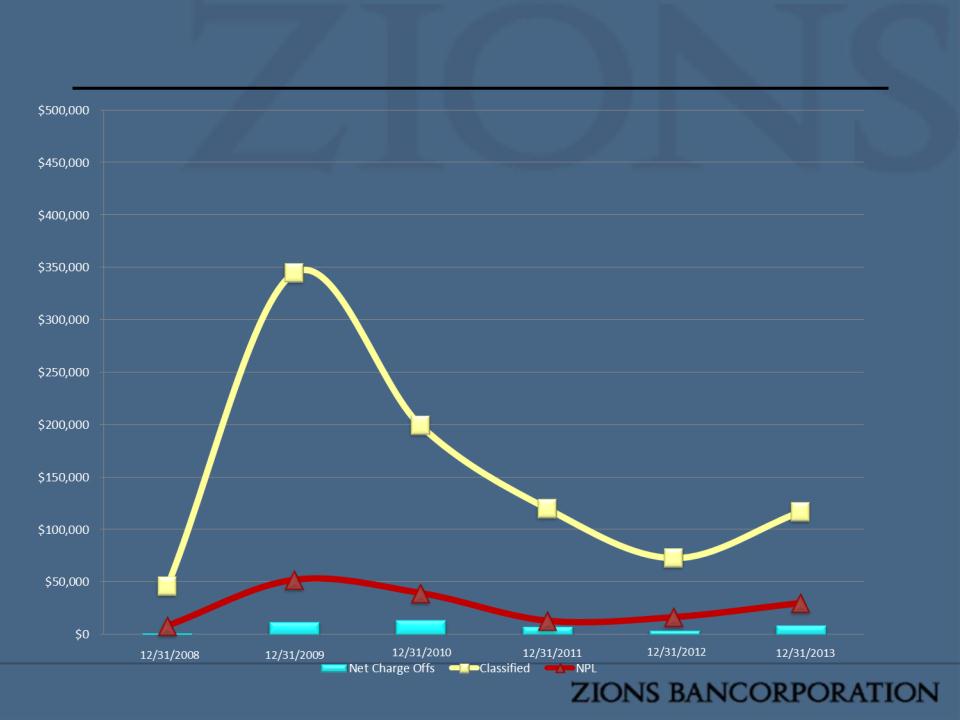

Credit Quality…Significant Improvement

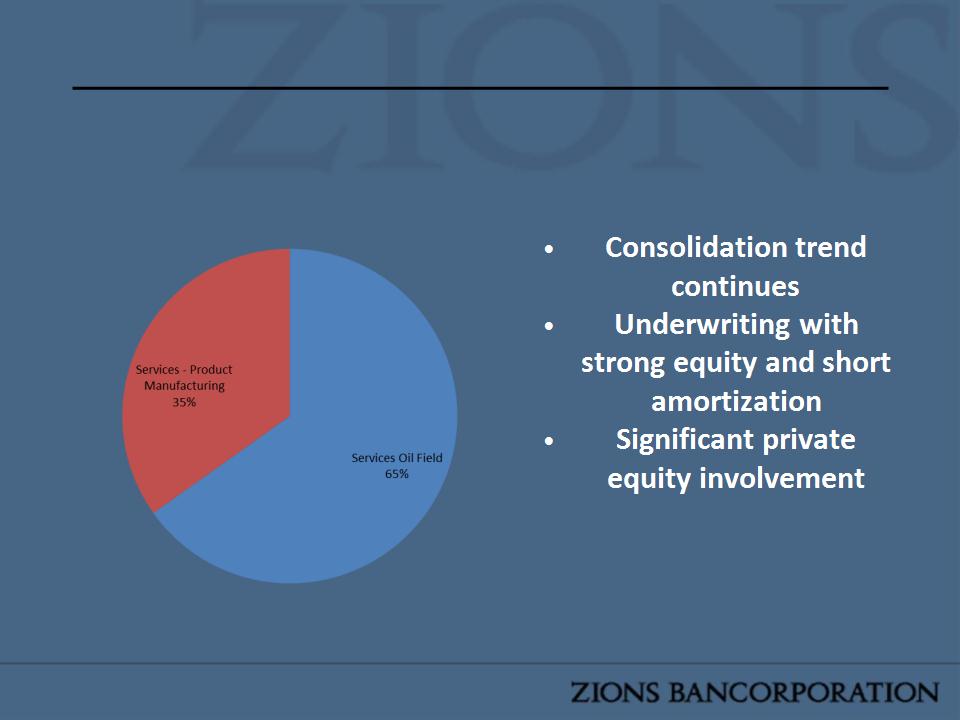

Energy Service Exposure By Market Segment

$2.2 Billion in Commitments

125

Reserve-Based Underwriting

126

($ in millions)

Typical Oil & Gas Reserve based loan

$100 - value using NYMEX oil and gas prices

$ 85 - Amegy risk-adjusted reserves (i.e. collateral value)

$ 68 - apply Amegy prices (80% of NYMEX)

$ 51 - loan value 75% adv. rate (25% of reserves hedged)

$ 41 - loan value 60% adv. rate (no hedging)

Note

• Average utilization on reserve-based facilities ~54%.

• PDNP reserves limited to 25%.

• 75% producing reserves.

127

Gas Shale Plays: A New Dimension

Outlook

128

Industry Condition

• Consolidation has resulted in larger companies with stronger

balance sheets and access to multiple capital sources

balance sheets and access to multiple capital sources

Price Outlook

• Continued Price Volatility

• Increased Global Oil & Gas Demand

• Increased production costs and tight supply will provide upward

price pressure

price pressure

Amegy’s Energy Team

• Experienced Team

• Conservative Underwriting Standards

• Active use of Hedging

• Diversified Energy Portfolio

Page *

California Bank & Trust

Investor Day

David Blackford

February 13, 2014

Investor Day

David Blackford

February 13, 2014

Page *

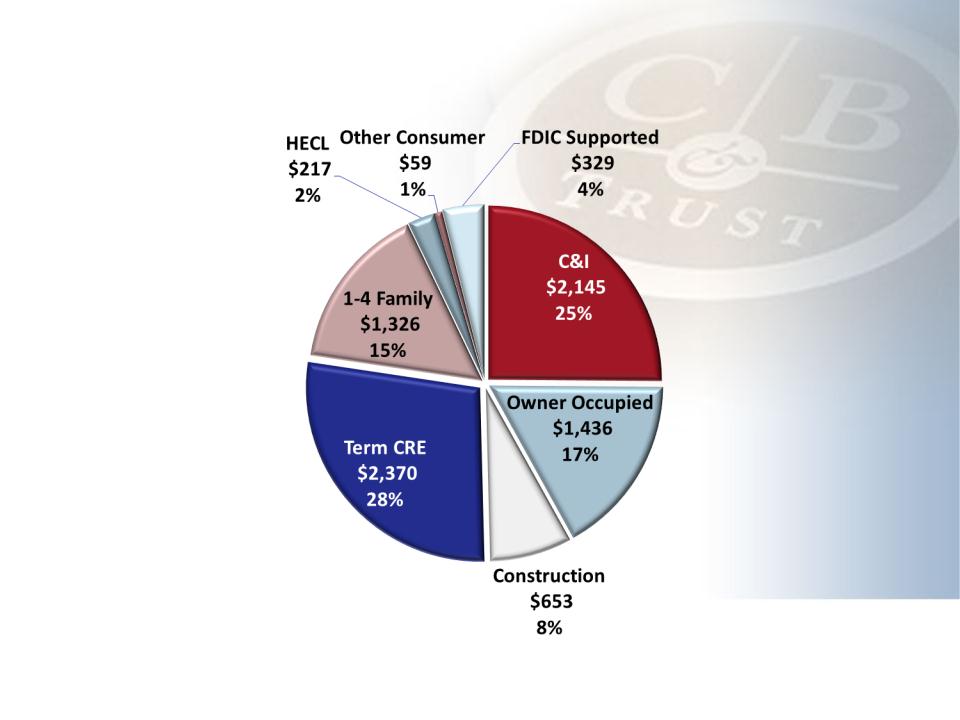

Loan Portfolio - December 2013

Page *

2013 Loan Growth

$ Growth (in MM) | % Growth | |

C&I | $374 | +21% |

Owner Occupied | $19 | +1% |

CRE - Construction | $164 | +34% |

CRE - Term | -$13 | -1% |

1-4 Family | -$29 | -2% |

HECL | -$20 | -9% |

Other Consumer | -$22 | -3% |

Total - Core | $493 | +6% |

FDIC Supported | -$178 | -35% |

Total - Net | $315 | +4% |

Growth in monthly average balances from December 2012 to December 2013

Page *

Net Interest Margin

Page *

FDIC Supported Loan Recap

($ in millions) | 2009-13 | 2014F |

Bargain Purchase Gain | 172 | 0 |

Recoveries | 14 | 0 |

Excess Accretion | 265 | 33 |

IA Amortization Expense | 212 | 21 |

Provision, Net | 22 | 0 |

Pretax Benefit | 217 | 12 |

Ending FDIC Loans | 321 | 219 |

Classified Cmmt | 20 | 57 |

Ending IA Balance | 26 | ~0-4 |

® Acquired $2.4 billion in unpaid principal balances in 2009

® Loss share coverage for non-single family loans ends in 2014

® Recovery period is 3 years (includes expense reimbursement for loans with charge-

offs during loss share period)

offs during loss share period)

® Accounting for Indemnification Asset on track for orderly resolution

Excess accretion is defined as discount accretion above fair value yields determined at time of acquisition

Classified commitments increase in 2014 due to expiration of loss share coverage

Page *

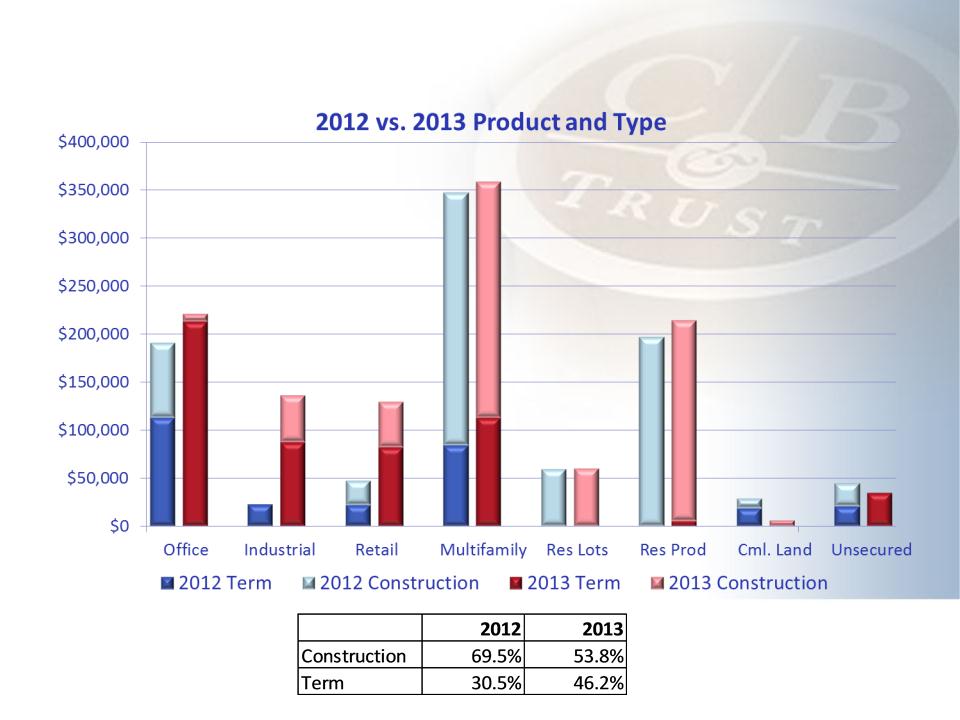

Real Estate Division Originations Year-Over-Year

Page *

2013 Real Estate Division

Originations by Location

71% of originations in SF Bay, Los Angeles and Orange County

Page *

LTV | Cml Land | Industrial | Multi- family | Office | Res Lots | Res Prod | Retail | % LTV Segment |

< =50% | 0.0% | 22.3% | 18.3% | 34.4% | 55.8% | 27.2% | 19.3% | 25.7% |

50.1% - 60% | 100.0% | 55.9% | 55.3% | 18.1% | 44.2% | 25.1% | 24.7% | 38.1% |

60.1% - 70% | 0.0% | 15.9% | 24.9% | 24.0% | 0.0% | 33.4% | 56.0% | 27.7% |

>70.1% | 0.0% | 5.9% | 1.4% | * 23.5% | 0.0% | ** 14.3% | 0.0% | 8.6% |

% Total New Orig. | 0.5% | 10.5% | 32.4% | 20.0% | 5.2% | 19.6% | 11.7% | 100.0% |

LTV 2013 Real Estate Division Originations

* Office > 70% consists of three term loans, one of which repaid.

** Res Prod > 70% includes completed building repositioned as for-sale condos with

substantive guarantor.

Page *

Credit Quality

® Credit quality improved steadily throughout 2013

® The majority of remaining non-performing loans consist of small

business and SBA 504 loans, which have smaller average balances and

longer resolution periods

business and SBA 504 loans, which have smaller average balances and

longer resolution periods

2012 | 2013 | |

NCO/Average Loans | 0.30% | -0.003% |

NPAs/Loans + OREO | 1.66% | 1.27% |

Classified Loans/Loans | 3.26% | 2.24% |

ACL/Loans | 1.99% | 1.57% |

Page *

Recap of CBT Strategic Objectives for 2014

® Expand core non-interest income

® Grow loans while maintaining desired product mix, geographic

diversification, and risk profile

diversification, and risk profile

® Increase core operating deposit accounts, with cross sell of fee

income services

income services

® Manage expenses carefully with continued focus on branch

repositioning

repositioning

® Continue strong risk management practices