ZIONS BANCORPORATION

Press Release – Page 1

April 24, 2017

|

| |

Zions Bancorporation One South Main Salt Lake City, UT 84133 April 24, 2017 www.zionsbancorporation.com |

|

First Quarter 2017 Financial Results: FOR IMMEDIATE RELEASE

Investor and Media Contact: James Abbott (801) 844-7637

|

|

| Zions Bancorporation Reports: 1Q17 Net Earnings¹ of $129 million, diluted EPS of $0.61 |

compared with 4Q16 Net Earnings¹ of $125 million, diluted EPS of $0.60,

and 1Q16 Net Earnings¹ of $79 million, diluted EPS of $0.38 |

|

FIRST QUARTER RESULTS

|

| | | | | | |

| $0.61 | | $129 million | | 3.38% | | 12.2% |

| Earnings per diluted common share | | Net Earnings 1 | | Net interest margin (“NIM”) | | Common Equity Tier 1 |

|

| | |

| FIRST QUARTER HIGHLIGHTS |

| | | |

| Net Interest Income and Net Interest Margin | | Net interest income was $489 million, up 2% from 4Q16 and up 8% from 1Q16 |

| NIM was 3.38% compared with 3.37% in 4Q16 and 3.35% in 1Q16 |

| | | |

Operating Performance2 | | Pre-provision net revenue ("PPNR") was $215 million, up 1% from 4Q16 and up 20% from 1Q16 |

| Adjusted PPNR² was $213 million, down 2% from 4Q16 and up 17% from 1Q16 |

| Noninterest expense was $414 million, compared with $404 million in 4Q16 |

| Adjusted noninterest expense² was $411 million, compared with $395 million in 4Q16 |

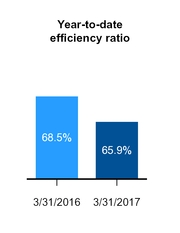

| Efficiency ratio² was 65.9%, compared with 64.5% for 4Q16 |

| | | |

| Loans and Credit Quality | | Net loans and leases were $42.7 billion, compared with $42.6 billion for 4Q16 |

| Provision for credit losses was $18 million, compared with less than $1 million in 4Q16 |

| Net charge-offs were $46 million, compared with $27 million in 4Q16 |

| | | |

| Oil and Gas-Related Exposure | | Net charge-offs for oil and gas loans were $14 million, compared with $16 million in 4Q16 |

| Oil and gas allowance for credit losses continued to exceed 8% of the portfolio |

| 38% of oil and gas-related loans were criticized for both 1Q17 and 4Q16 |

| | | |

| Capital Return | | Tangible return on average tangible common equity² was 8.8%, compared with 8.4% in 4Q16 and 5.6% in 1Q16 |

| Common stock repurchases of $45 million during the quarter |

| | | |

| Income Taxes | | The tax rate of 24.5% in 1Q17 was lower due to a one-time adjustment and the adoption of new stock-based compensation accounting guidance |

|

|

| CEO COMMENTARY |

| |

Harris H. Simmons, Chairman and CEO, commented, “While we are pleased with the strong 61% improvement in earnings per share over the same period a year ago, results relative to the fourth quarter of 2016 were muted due to lackluster loan growth, a condition which has recently been prevalent throughout the industry. Although we experienced a single loan loss that comprised nearly two-thirds of total net charge-offs during the quarter, credit quality was generally strong and improving, with classified loan totals improving by 7% relative to fourth quarter results.” Mr. Simmons concluded, “While operating costs were seasonally higher, we remain committed to a continued focus on expense control and improvement in our profitability through the remainder of 2017 and beyond.”

|

|

|

¹ Net Earnings is net earnings applicable to common shareholders.

² For information on non-GAAP financial measures and why the Company presents these numbers, see pages 16-18. Included in these non-GAAP financial measures are the key metrics to which Zions announced it would hold itself accountable in its June 1, 2015 efficiency initiative, and to which executive compensation is tied. |

ZIONS BANCORPORATION

Press Release – Page 2

April 24, 2017

RESULTS OF OPERATIONS

|

| | | | | | | | | | | | | | | | | | | | | | | | | |

| Net Interest Income |

| | | | | | | | 1Q17 - 4Q16 | | 1Q17 - 1Q16 |

| (In millions) | 1Q17 | | 4Q16 | | 1Q16 | | $ | | % | | $ | | % |

| Interest and fees on loans | $ | 433 |

| | $ | 438 |

| | $ | 421 |

| | $ | (5 | ) | | (1 | )% | | $ | 12 |

| | 3 | % |

| Interest on money market investments | 4 |

| | 4 |

| | 7 |

| | — |

| | — |

| | (3 | ) | | (43 | ) |

| Interest on securities | 78 |

| | 59 |

| | 47 |

| | 19 |

| | 32 |

| | 31 |

| | 66 |

|

| Total interest income | 515 |

| | 501 |

| | 475 |

| | 14 |

| | 3 |

| | 40 |

| | 8 |

|

| Interest on deposits | 13 |

| | 13 |

| | 12 |

| | — |

| | — |

| | 1 |

| | 8 |

|

| Interest on short and long-term borrowings | 13 |

| | 8 |

| | 10 |

| | 5 |

| | 63 |

| | 3 |

| | 30 |

|

| Interest expense | 26 |

| | 21 |

| | 22 |

| | 5 |

| | 24 |

| | 4 |

| | 18 |

|

| Net interest income | $ | 489 |

| | $ | 480 |

| | $ | 453 |

| | $ | 9 |

| | 2 |

| | $ | 36 |

| | 8 |

|

Net interest income increased to $489 million in the first quarter of 2017 from $480 million in the fourth quarter of 2016. The increase in net interest income was due to a $19 million increase in interest from investment securities. Average securities increased in the first quarter of 2017 by $2.5 billion as the Company continued to reposition the balance sheet and moderately reduce its interest rate sensitivity. The Company expects to maintain its securities portfolio at approximately the current level in the near term. Average loans were relatively stable during the first quarter of 2017, and the yield on the loan portfolio increased 3 basis points to 4.14% during the quarter. However, an increase in nonaccrual loans, a decrease in prepayments, and a decline in the revenue from loans purchased from the FDIC in 2009 muted some of the natural asset sensitivity of the Company. These factors, and two fewer days in the quarter, resulted in a $5 million decrease in interest and fees on loans in the first quarter of 2017.

The net interest margin increased slightly to 3.38% in the first quarter of 2017, compared with 3.37% in the fourth quarter of 2016. The increase in net interest margin was driven by increased yields on the loans and securities portfolios, up 3 and 20 basis points from the prior quarter, respectively, but was tempered somewhat due to the continued shift to a greater concentration of securities as a percentage of earning assets and lower marginal net yields on balance sheet growth.

|

| | | | | | | | | | | | | | | | | | | | | | | | | |

| Noninterest Income |

| | | | | | | | 1Q17 - 4Q16 | | 1Q17 - 1Q16 |

| (In millions) | 1Q17 | | 4Q16 | | 1Q16 | | $ | | % | | $ | | % |

| Service charges and fees on deposit accounts | $ | 42 |

| | $ | 43 |

| | $ | 41 |

| | $ | (1 | ) | | (2 | )% | | $ | 1 |

| | 2 | % |

| Other service charges, commissions and fees | 49 |

| | 52 |

| | 49 |

| | (3 | ) | | (6 | ) | | — |

| | — |

|

| Wealth management income | 10 |

| | 11 |

| | 8 |

| | (1 | ) | | (9 | ) | | 2 |

| | 25 |

|

| Loan sales and servicing income | 7 |

| | 6 |

| | 8 |

| | 1 |

| | 17 |

| | (1 | ) | | (13 | ) |

| Capital markets and foreign exchange | 7 |

| | 6 |

| | 6 |

| | 1 |

| | 17 |

| | 1 |

| | 17 |

|

| Customer-related fees | 115 |

| | 118 |

| | 112 |

| | (3 | ) | | (3 | ) | | 3 |

| | 3 |

|

| Dividends and other investment income | 12 |

| | 4 |

| | 5 |

| | 8 |

| | 200 |

| | 7 |

| | 140 |

|

| Securities gains (losses), net | 5 |

| | (3 | ) | | — |

| | 8 |

| | 267 |

| | 5 |

| | NM |

| Other | — |

| | 9 |

| | — |

| | (9 | ) | | (100 | ) | | — |

| | — |

|

| Total noninterest income | $ | 132 |

| | $ | 128 |

| | $ | 117 |

| | $ | 4 |

| | 3 |

| | $ | 15 |

| | 13 |

|

ZIONS BANCORPORATION

Press Release – Page 3

April 24, 2017

Total noninterest income for the first quarter of 2017 was $132 million, compared with $128 million for the fourth quarter of 2016. The increase in total noninterest income during the quarter was driven by an $8 million increase in net securities gains and an $8 million increase in dividends and other investment income, primarily due to increased market values of the Company’s Small Business Investment Company (“SBIC”) investments. These gains were partially offset by a $9 million decline in other noninterest income, driven by a $7 million decline in fair value and nonhedge derivative income resulting from fair value adjustments.

Customer-related fees decreased by $3 million in the first quarter of 2017 compared with the prior quarter, which was primarily due to a decline in lending activity, partially offset by an increase in credit card and interchange fees. Customer-related fees increased by $3 million compared with the first quarter of 2016, primarily due to increased wealth management income.

|

| | | | | | | | | | | | | | | | | | | | | | | | | |

| Noninterest Expense |

| | | | | | | | 1Q17 - 4Q16 | | 1Q17 - 1Q16 |

| (In millions) | 1Q17 | | 4Q16 | | 1Q16 | | $ | | % | | $ | | % |

| Salaries and employee benefits | $ | 262 |

| | $ | 241 |

| | $ | 258 |

| | $ | 21 |

| | 9 | % | | $ | 4 |

| | 2 | % |

| Occupancy, net | 33 |

| | 32 |

| | 30 |

| | 1 |

| | 3 |

| | 3 |

| | 10 |

|

| Furniture, equipment and software, net | 32 |

| | 33 |

| | 32 |

| | (1 | ) | | (3 | ) | | — |

| | — |

|

| Other real estate expense, net | — |

| | — |

| | (1 | ) | | — |

| | — |

| | 1 |

| | 100 |

|

| Credit-related expense | 8 |

| | 7 |

| | 6 |

| | 1 |

| | 14 |

| | 2 |

| | 33 |

|

| Provision for unfunded lending commitments | (5 | ) | | 3 |

| | (6 | ) | | (8 | ) | | (267 | ) | | 1 |

| | 17 |

|

| Professional and legal services | 14 |

| | 17 |

| | 12 |

| | (3 | ) | | (18 | ) | | 2 |

| | 17 |

|

| Advertising | 5 |

| | 5 |

| | 6 |

| | — |

| | — |

| | (1 | ) | | (17 | ) |

| FDIC premiums | 12 |

| | 11 |

| | 7 |

| | 1 |

| | 9 |

| | 5 |

| | 71 |

|

| Amortization of core deposit and other intangibles | 2 |

| | 2 |

| | 2 |

| | — |

| | — |

| | — |

| | — |

|

| Other | 51 |

| | 53 |

| | 50 |

| | (2 | ) | | (4 | ) | | 1 |

| | 2 |

|

| Total noninterest expense | $ | 414 |

| | $ | 404 |

| | $ | 396 |

| | $ | 10 |

| | 2 |

| | $ | 18 |

| | 5 |

|

Adjusted noninterest expense 1 | $ | 411 |

| | $ | 395 |

| | $ | 396 |

| | $ | 16 |

| | 4 | % | | $ | 15 |

| | 4 | % |

| |

1 | For information on non-GAAP financial measures see pages 16-18. |

Noninterest expense for the first quarter of 2017 was $414 million, compared with $404 million for the fourth quarter of 2016, and $396 million for the first quarter of 2016. The increase in total noninterest expense from the fourth quarter of 2016 was driven by a $21 million increase in salaries and employee benefits, partially offset by an $8 million decline in the provision for unfunded lending commitments. The change in salaries and employee benefits during the first quarter was due to a $4 million increase in severance and the following seasonal increases:

| |

| • | $7 million in stock-based compensation related to equity grants to retirement-eligible employees |

| |

| • | $6 million in payroll taxes |

| |

| • | $4 million related to the Company’s contribution to the employee 401(k) plan |

These increases in salaries and employee benefits were partially offset by a $3 million reduction in salary expense, primarily related to loan originations. This was the result of an update in the estimation process associated with the consolidation of loan operations.

ZIONS BANCORPORATION

Press Release – Page 4

April 24, 2017

The Company is committed to its expense and efficiency ratio goals for 2017, which are to hold adjusted noninterest expense growth to 2-3% in 2017, and to achieve an efficiency ratio in the low 60s. For information on non-GAAP measures see pages 16-18.

The tax rate of 24.5% as of March 31, 2017 was lower than the 33.8% tax rate at December 31, 2016. The reduction in tax rate was primarily driven by a one-time $14 million benefit to tax expense related to state tax adjustments, and a $4 million benefit from the implementation of new accounting guidance related to stock-based compensation. Excluding these items, the Company expects the tax rate for the rest of 2017 to be approximately 34% to 35%.

BALANCE SHEET ANALYSIS

|

| | | | | | | | | | | | | | | | | | | | | | | | | |

| Asset Quality |

| | | | | | | | 1Q17 - 4Q16 | | 1Q17 - 1Q16 |

| (In millions) | 1Q17 | | 4Q16 | | 1Q16 | | bps | | | | bps | | |

| Ratio of nonperforming assets to loans and leases and other real estate owned | 1.37 | % | | 1.34 | % | | 1.33 | % | | 3 |

| | | | 4 |

| | |

| Annualized ratio of net loan and lease charge-offs to average loans | 0.43 |

| | 0.25 |

| | 0.35 |

| | 18 |

| | | | 8 |

| | |

| Ratio of total allowance for credit losses to loans and leases outstanding | 1.41 |

| | 1.48 |

| | 1.64 |

| | (7 | ) | | | | (23 | ) | | |

| | | | | | | | $ | | % | | $ | | % |

| Classified loans | $ | 1,464 |

| | $ | 1,577 |

| | $ | 1,532 |

| | $ | (113 | ) | | (7 | )% | | $ | (68 | ) | | (4 | )% |

| Provision for credit losses | 18 |

| | — |

| | 36 |

| | 18 |

| | NM | | (18 | ) | | (50 | ) |

Asset quality for the total portfolio remained strong and was generally stable when compared with the prior quarter. Classified loans for the total portfolio decreased to $1.5 billion at March 31, 2017, from $1.6 billion at December 31, 2016. Nonperforming assets were $588 million at March 31, 2017, compared with $573 million at December 31, 2016. The ratio of nonperforming assets to loans and leases and other real estate owned remained relatively stable at 1.37% at March 31, 2017, compared with 1.34% at December 31, 2016. Total net charge-offs were $46 million in the first quarter of 2017, or an annualized 0.43% of average loans, compared with $27 million, or an annualized 0.25% of average loans, in the fourth quarter of 2016. Nearly two-thirds of the total net charge-offs in the first quarter of 2017 were related to an isolated event with one non oil and gas-related borrower, who is subject to a government investigation and seizure of assets. Additionally, $14 million of net charge-offs were related to the oil and gas-related portfolio.

The Company provided $18 million for credit losses during the first quarter of 2017, compared with less than $1 million during the fourth quarter of 2016. The increase in the provision for credit losses was primarily due to the isolated charge-off discussed previously, partially offset by a decrease in the provision related to the oil and gas portfolio. The allowance for credit losses decreased to $604 million at March 31, 2017 from $632 million at December 31, 2016, which was 1.41% and 1.48% of loans and leases, respectively. The allowance for credit losses

ZIONS BANCORPORATION

Press Release – Page 5

April 24, 2017

decreased as a result of credit quality improvement in the total portfolio. The reserve for unfunded lending commitments decreased by $5 million as a result of credit quality improvement in the oil and gas-related portfolio.

|

| | | | | | | | | | | | | | | | | | | | | | | | | |

| Loans and Leases |

| | | | | | | | 1Q17 - 4Q16 | | 1Q17 - 1Q16 |

| (In millions) | 1Q17 | | 4Q16 | | 1Q16 | | $ | | % | | $ | | % |

| Loans held for sale | $ | 128 |

| | $ | 172 |

| | $ | 109 |

| | $ | (44 | ) | | (26 | )% | | $ | 19 |

| | 17 |

|

| Loans and leases: | | | | | | | | | | | | | |

| Commercial | 21,556 |

| | 21,615 |

| | 21,745 |

| | (59 | ) | | — |

| | (189 | ) | | (1 | ) |

| Commercial real estate | 11,206 |

| | 11,341 |

| | 10,794 |

| | (135 | ) | | (1 | ) | | 412 |

| | 4 |

|

| Consumer | 9,980 |

| | 9,693 |

| | 8,879 |

| | 287 |

| | 3 |

| | 1,101 |

| | 12 |

|

| Loans and leases, net of unearned income and fees | 42,742 |

| | 42,649 |

| | 41,418 |

| | 93 |

| | — |

| | 1,324 |

| | 3 |

|

| Less allowance for loan losses | 544 |

| | 567 |

| | 612 |

| | (23 | ) | | (4 | ) | | (68 | ) | | (11 | ) |

| Loans held for investment, net of allowance | $ | 42,198 |

| | $ | 42,082 |

| | $ | 40,806 |

| | $ | 116 |

| | — |

| | $ | 1,392 |

| | 3 |

|

Loans and leases, net of unearned income and fees, were $42.7 billion at March 31, 2017, compared with $42.6 billion at December 31, 2016. During the first quarter of 2017, consumer loans increased $287 million, predominately in 1-4 family residential loans, which includes the purchase of $166 million of loans. This increase was slightly offset by a $97 million decline in the oil and gas-related portfolio, primarily due to active management of the portfolio, including payoffs, paydowns and charge-offs. Excluding the reduction in oil and gas-related loans, net loans and leases increased $190 million during the first quarter of 2017. Unfunded lending commitments were $19.4 billion at March 31, 2017, compared with $19.3 billion at December 31, 2016.

|

| | | | | | | | | | | | | | | | | | | | | | | | | |

Oil and Gas-Related Exposure1 |

| | | | | | | | 1Q17 - 4Q16 | | 1Q17 - 1Q16 |

| (In millions) | 1Q17 | | 4Q16 | | 1Q16 | | $ | | % | | $ | | % |

| Loans and leases | | | | | | |

|

| |

|

| |

|

| |

|

| Upstream – exploration and production | $ | 685 |

| | $ | 733 |

| | $ | 859 |

| | $ | (48 | ) | | (7 | )% | | $ | (174 | ) | | (20 | )% |

| Midstream – marketing and transportation | 603 |

| | 598 |

| | 649 |

| | 5 |

| | 1 |

| | (46 | ) | | (7 | ) |

| Downstream – refining | 108 |

| | 137 |

| | 129 |

| | (29 | ) | | (21 | ) | | (21 | ) | | (16 | ) |

| Other non-services | 38 |

| | 38 |

| | 43 |

| | — |

| | — |

| | (5 | ) | | (12 | ) |

| Oilfield services | 466 |

| | 500 |

| | 734 |

| | (34 | ) | | (7 | ) | | (268 | ) | | (37 | ) |

| Oil and gas service manufacturing | 161 |

| | 152 |

| | 229 |

| | 9 |

| | 6 |

| | (68 | ) | | (30 | ) |

Total loan and lease balances 2 | 2,061 |

| | 2,158 |

| | 2,643 |

| | (97 | ) | | (4 | ) | | (582 | ) | | (22 | ) |

| Unfunded lending commitments | 1,886 |

| | 1,722 |

| | 2,021 |

| | 164 |

| | 10 |

| | (135 | ) | | (7 | ) |

| Total oil and gas credit exposure | $ | 3,947 |

| | $ | 3,880 |

| | $ | 4,664 |

| | $ | 67 |

| | 2 |

| | $ | (717 | ) | | (15 | ) |

| | | | | | | | | | | | | | |

| Private equity investments | $ | 6 |

| | $ | 7 |

| | $ | 12 |

| | $ | (1 | ) | | (14 | ) | | $ | (6 | ) | | (50 | ) |

| | | | | | | | | | | | | | |

Credit quality measures 2 | | | | | | | | | | | | | |

| Criticized loan ratio | 38.0 | % | | 37.8 | % | | 37.5 | % | | | | | | | | |

| Classified loan ratio | 30.4 | % | | 31.6 | % | | 26.9 | % | | | | | | | | |

| Nonaccrual loan ratio | 14.8 | % | | 13.6 | % | | 10.8 | % | | | | | | | | |

| Ratio of nonaccrual loans that are current | 73.1 | % | | 86.1 | % | | 90.6 | % | | | | | | | | |

Net charge-off ratio, annualized 3 | 2.7 | % | | 3.0 | % | | 5.4 | % | | | | | | | | |

| |

1 | Because many borrowers operate in multiple businesses, judgment has been applied in characterizing a borrower as oil and gas-related, including a particular segment of oil and gas-related activity, e.g., upstream or downstream; typically, 50% of revenues coming from the oil and gas sector is used as a guide. |

ZIONS BANCORPORATION

Press Release – Page 6

April 24, 2017

2 Total loan and lease balances and the credit quality measures do not include $21 million of oil and gas loans held for sale at March 31, 2017.

| |

3 | Calculated as the ratio of annualized net charge-offs for each respective period to loan balances at each period end. |

Oil and gas-related loans represent 5% of the total loan portfolio. Unfunded lending commitments increased by $164 million during the first quarter of 2017, primarily in the midstream portfolio. Criticized oil and gas-related loans decreased $32 million, or 4%, during the first quarter of 2017, mainly due to payoffs and paydowns. Oil and gas-related loan net charge-offs were $14 million in the first quarter of 2017, compared with $16 million in the fourth quarter of 2016, and were predominantly in the upstream portfolio. The allowance for credit losses related to oil and gas-related loans continued to exceed 8% at the end of the first quarter of 2017.

|

| | | | | | | | | | | | | | | | | | | | | | | | | |

| Deposits |

| | | | | | | | 1Q17 - 4Q16 | | 1Q17 - 1Q16 |

| (In millions) | 1Q17 | | 4Q16 | | 1Q16 | | $ | | % | | $ | | % |

| Noninterest-bearing demand | $ | 24,410 |

| | $ | 24,115 |

| | $ | 21,872 |

| | $ | 295 |

| | 1 | % | | $ | 2,538 |

| | 12 | % |

| Interest-bearing: | | | | | | | | | | | | | |

| Savings and money market | 26,071 |

| | 26,364 |

| | 25,724 |

| | (293 | ) | | (1 | ) | | 347 |

| | 1 |

|

| Time | 2,994 |

| | 2,757 |

| | 2,072 |

| | 237 |

| | 9 |

| | 922 |

| | 44 |

|

| Foreign | — |

| | — |

| | 220 |

| | — |

| | — |

| | (220 | ) | | (100 | ) |

| Total deposits | $ | 53,475 |

| | $ | 53,236 |

| | $ | 49,888 |

| | $ | 239 |

| | — |

| | $ | 3,587 |

| | 7 |

|

Total deposits increased to $53.5 billion at March 31, 2017, compared with $53.2 billion at December 31, 2016, as a result of a temporary increase in client activity at quarter-end. Average total deposits were $52.2 billion for both the first quarter of 2017 and the fourth quarter of 2016. Average noninterest bearing deposits decreased slightly to $23.5 billion for the first quarter of 2017, compared with $23.6 billion for the fourth quarter of 2016, and were 45% of average total deposits.

|

| | | | | | | | | | | | | | | | | | | | | | | | | |

| Long-term Debt and Shareholders’ Equity |

| | | | | | | | 1Q17 - 4Q16 | | 1Q17 - 1Q16 |

| (In millions) | 1Q17 | | 4Q16 | | 1Q16 | | $ | | % | | $ | | % |

| Shareholders’ equity: | | | | | | | | | | | | | |

| Preferred Stock | $ | 710 |

| | $ | 710 |

| | $ | 828 |

| | $ | — |

| | — | % | | $ | (118 | ) | | (14 | )% |

| Common Stock | 4,696 |

| | 4,725 |

| | 4,778 |

| | (29 | ) | | (1 | ) | | (82 | ) | | (2 | ) |

| Retained earnings | 2,435 |

| | 2,321 |

| | 2,031 |

| | 114 |

| | 5 |

| | 404 |

| | 20 |

|

| Accumulated other comprehensive income (loss) | (111 | ) | | (122 | ) | | (12 | ) | | 11 |

| | 9 |

| | (99 | ) | | (825 | ) |

| Total shareholders' equity | $ | 7,730 |

| | $ | 7,634 |

| | $ | 7,625 |

| | $ | 96 |

| | 1 |

| | $ | 105 |

| | 1 |

|

During the first quarter of 2017, the Company continued its stock buyback program and repurchased $45 million of common stock during the quarter at an average price of $42.43 per share, and has repurchased $135 million of common stock since July 1, 2016 at an average price of $34.18 per share, leaving $45 million of buyback capacity remaining in the 2016 capital plan (which spans the timeframe of July 2016 to June 2017). Despite the share repurchases, the increase in the average market price per share of common stock for the first quarter, compared with

ZIONS BANCORPORATION

Press Release – Page 7

April 24, 2017

the fourth quarter, increased the weighted average diluted shares by 5.0 million due to warrants that have been outstanding since 2008 (“TARP” warrants - NASDAQ: ZIONZ) and 2010 (NASDAQ: ZIONW).

Preferred dividends are expected to be $12.4 million for the second quarter of 2017. Our preferred stock may be reduced if we redeem $144 million of preferred equity in the second quarter of 2017, as outlined by our 2016 capital plan. Additionally, the Company reduced its long-term debt by $152 million during the first quarter of 2017 due to the maturity of 4.50% senior notes.

Tangible book value per common share increased to $29.61 at March 31, 2017, compared with $29.06 at December 31, 2016. The estimated Basel III common equity tier 1 (“CET1”) capital ratio was 12.2% at March 31, 2017 compared with 12.1% at December 31, 2016; Basel III capital ratios are based on the applicable phase-in periods, however, the fully phased-in ratio is not substantially different. For information on non-GAAP measures see pages 16-18.

ZIONS BANCORPORATION

Press Release – Page 8

April 24, 2017

Supplemental Presentation and Conference Call

Zions has posted a supplemental presentation to its website, which will be used to discuss these first quarter results at 5:30 p.m. ET this afternoon (April 24, 2017). Media representatives, analysts, investors, and the public are invited to join this discussion by calling 253-237-1247 (domestic and international) and entering the passcode 91430582, or via on-demand webcast. A link to the webcast will be available on the Zions Bancorporation website at zionsbancorporation.com. The webcast of the conference call will also be archived and available for 30 days. About Zions Bancorporation

Zions Bancorporation is one of the nation's premier financial services companies with total assets exceeding $65 billion. Zions operates under local management teams and distinct brands in 11 western states: Arizona, California, Colorado, Idaho, Nevada, New Mexico, Oregon, Texas, Utah, Washington and Wyoming. The company is a national leader in Small Business Administration lending and public finance advisory services, and is a consistent top recipient of Greenwich Excellence awards in banking. In addition, Zions is included in the S&P 500 and NASDAQ Financial 100 indices. Investor information and links to local banking brands can be accessed at zionsbancorporation.com. Forward-Looking Information

Statements in this press release that are based on other than historical data or that express the Company’s expectations regarding future events or determinations are forward-looking within the meaning of the Private Securities Litigation Reform Act of 1995. Statements based on historical data are not intended and should not be understood to indicate the Company’s expectations regarding future events. Forward-looking statements provide current expectations or forecasts or intentions regarding future events or determinations. These forward-looking statements are not guarantees of future performance or determinations, nor should they be relied upon as representing management’s views as of any subsequent date. Forward-looking statements involve significant risks and uncertainties, and actual results may differ materially from those presented, either expressed or implied, in this press release. Factors that could cause actual results to differ materially from those expressed in the forward-looking statements include the actual amount and duration of declines in the price of oil and gas, our ability to meet our efficiency and noninterest expense goals, as well as other factors discussed in the Company’s most recent Annual Report on Form 10-K and Quarterly Report on Form 10-Q, filed with the Securities and Exchange Commission (“SEC”) and available at the SEC’s Internet site (http://www.sec.gov).

Except as required by law, the Company specifically disclaims any obligation to update any factors or to publicly announce the result of revisions to any of the forward-looking statements included herein to reflect future events or developments.

ZIONS BANCORPORATION

Press Release – Page 9

April 24, 2017

FINANCIAL HIGHLIGHTS

(Unaudited)

|

| | | | | | | | | | | | | | | | | | | |

| | Three Months Ended |

| (In millions, except share, per share, and ratio data) | March 31,

2017 | | December 31,

2016 | | September 30,

2016 | | June 30,

2016 | | March 31,

2016 |

BALANCE SHEET 1 | | | | | | | | | |

| Loans held for investment, net of allowance | $ | 42,198 |

| | $ | 42,082 |

| | $ | 41,943 |

| | $ | 41,894 |

| | $ | 40,806 |

|

| Total assets | 65,463 |

| | 63,239 |

| | 61,039 |

| | 59,643 |

| | 59,180 |

|

| Deposits | 53,475 |

| | 53,236 |

| | 50,849 |

| | 50,271 |

| | 49,888 |

|

| Total shareholders’ equity | 7,730 |

| | 7,634 |

| | 7,679 |

| | 7,626 |

| | 7,625 |

|

| STATEMENT OF INCOME | | | | | | | | | |

| Net earnings applicable to common shareholders | $ | 129 |

| | $ | 125 |

| | $ | 117 |

| | $ | 91 |

| | $ | 79 |

|

| Net interest income | 489 |

| | 480 |

| | 469 |

| | 465 |

| | 453 |

|

| Taxable-equivalent net interest income | 497 |

| | 488 |

| | 476 |

| | 471 |

| | 458 |

|

| Total noninterest income | 132 |

| | 128 |

| | 145 |

| | 126 |

| | 117 |

|

| Total noninterest expense | 414 |

| | 404 |

| | 403 |

| | 382 |

| | 396 |

|

Adjusted pre-provision net revenue 2 | 213 |

| | 217 |

| | 209 |

| | 211 |

| | 182 |

|

| Provision for loan losses | 23 |

| | (3 | ) | | 19 |

| | 35 |

| | 42 |

|

| Provision for unfunded lending commitments | (5 | ) | | 3 |

| | (3 | ) | | (4 | ) | | (6 | ) |

| Provision for credit losses | 18 |

| | — |

| | 16 |

| | 31 |

| | 36 |

|

| PER COMMON SHARE | | | | | | | | | |

| Net earnings per diluted common share | $ | 0.61 |

| | $ | 0.60 |

| | $ | 0.57 |

| | $ | 0.44 |

| | $ | 0.38 |

|

| Dividends | 0.08 |

| | 0.08 |

| | 0.08 |

| | 0.06 |

| | 0.06 |

|

Book value per common share 1 | 34.65 |

| | 34.09 |

| | 34.19 |

| | 33.72 |

| | 33.23 |

|

Tangible book value per common share 1, 2 | 29.61 |

| | 29.06 |

| | 29.16 |

| | 28.72 |

| | 28.20 |

|

| SELECTED RATIOS AND OTHER DATA | | | | | | | | | |

| Return on average assets | 0.88 | % | | 0.88 | % | | 0.84 | % | | 0.77 | % | | 0.62 | % |

| Return on average common equity | 7.48 | % | | 7.11 | % | | 6.66 | % | | 5.32 | % | | 4.68 | % |

Tangible return on average tangible common equity 2 | 8.8 | % | | 8.4 | % | | 7.9 | % | | 6.3 | % | | 5.6 | % |

| Net interest margin | 3.38 | % | | 3.37 | % | | 3.36 | % | | 3.39 | % | | 3.35 | % |

Efficiency ratio 2 | 65.9 | % | | 64.5 | % | | 65.9 | % | | 64.6 | % | | 68.5 | % |

| Effective tax rate | 24.5 | % | | 33.8 | % | | 33.9 | % | | 34.5 | % | | 31.1 | % |

| Ratio of nonperforming assets to loans and leases and other real estate owned | 1.37 | % | | 1.34 | % | | 1.37 | % | | 1.30 | % | | 1.33 | % |

| Annualized ratio of net loan and lease charge-offs to average loans | 0.43 | % | | 0.25 | % | | 0.28 | % | | 0.37 | % | | 0.35 | % |

Ratio of total allowance for credit losses to loans and leases outstanding 1 | 1.41 | % | | 1.48 | % | | 1.55 | % | | 1.58 | % | | 1.64 | % |

| Full-time equivalent employees | 10,076 |

| | 10,057 |

| | 9,968 |

| | 10,064 |

| | 10,092 |

|

CAPITAL RATIOS 1 | | | | | | | | | |

| Tangible common equity ratio | 9.31 | % | | 9.49 | % | | 9.91 | % | | 10.05 | % | | 9.92 | % |

Basel III: 3 | | | | | | | | | |

| Common equity tier 1 capital | 12.2 | % | | 12.1 | % | | 12.0 | % | | 12.0 | % | | 12.1 | % |

| Tier 1 leverage | 10.8 | % | | 11.1 | % | | 11.3 | % | | 11.3 | % | | 11.4 | % |

| Tier 1 risk-based capital | 13.6 | % | | 13.5 | % | | 13.5 | % | | 13.4 | % | | 13.9 | % |

| Total risk-based capital | 15.3 | % | | 15.2 | % | | 15.3 | % | | 15.5 | % | | 16.0 | % |

| Risk-weighted assets | 50,016 |

| | 49,937 |

| | 49,318 |

| | 49,017 |

| | 47,696 |

|

| Weighted average common and common-equivalent shares outstanding (in thousands) | 210,405 |

| | 205,446 |

| | 204,714 |

| | 204,536 |

| | 204,096 |

|

Common shares outstanding (in thousands) 1 | 202,595 |

| | 203,085 |

| | 203,850 |

| | 205,104 |

| | 204,544 |

|

| |

2 | For information on non-GAAP financial measures see pages 16-18. |

| |

3 | Basel III capital ratios became effective January 1, 2015 and are based on the applicable phase-in periods. Current period ratios and amounts represent estimates. |

ZIONS BANCORPORATION

Press Release – Page 10

April 24, 2017

CONSOLIDATED BALANCE SHEETS

|

| | | | | | | | | | | | | | | | | | | |

| (In millions, shares in thousands) | March 31,

2017 | | December 31,

2016 | | September 30,

2016 | | June 30,

2016 | | March 31,

2016 |

| | (Unaudited) | |

| | (Unaudited) | | (Unaudited) | | (Unaudited) |

| ASSETS | | | | | | | | | |

| Cash and due from banks | $ | 566 |

| | $ | 737 |

| | $ | 553 |

| | $ | 560 |

| | $ | 518 |

|

| Money market investments: | | | | | | | | | |

| Interest-bearing deposits | 1,761 |

| | 1,411 |

| | 1,489 |

| | 2,155 |

| | 3,039 |

|

| Federal funds sold and security resell agreements | 363 |

| | 568 |

| | 1,676 |

| | 620 |

| | 1,587 |

|

| Investment securities: | | | | | | | | | |

| Held-to-maturity, at amortized cost (approximate fair value $803, $850, $718, $721, and $636) | 815 |

| | 868 |

| | 715 |

| | 713 |

| | 631 |

|

| Available-for-sale, at fair value | 15,606 |

| | 13,372 |

| | 10,358 |

| | 9,477 |

| | 8,702 |

|

| Trading account, at fair value | 40 |

| | 115 |

| | 108 |

| | 119 |

| | 66 |

|

| | 16,461 |

| | 14,355 |

| | 11,181 |

| | 10,309 |

| | 9,399 |

|

| Loans held for sale | 128 |

| | 172 |

| | 160 |

| | 147 |

| | 109 |

|

| Loans and leases, net of unearned income and fees | 42,742 |

| | 42,649 |

| | 42,540 |

| | 42,502 |

| | 41,418 |

|

| Less allowance for loan losses | 544 |

| | 567 |

| | 597 |

| | 608 |

| | 612 |

|

| Loans held for investment, net of allowance | 42,198 |

| | 42,082 |

| | 41,943 |

| | 41,894 |

| | 40,806 |

|

| Other noninterest-bearing investments | 973 |

| | 884 |

| | 894 |

| | 851 |

| | 856 |

|

| Premises, equipment and software, net | 1,047 |

| | 1,020 |

| | 987 |

| | 956 |

| | 925 |

|

| Goodwill | 1,014 |

| | 1,014 |

| | 1,014 |

| | 1,014 |

| | 1,014 |

|

| Core deposit and other intangibles | 7 |

| | 8 |

| | 10 |

| | 12 |

| | 14 |

|

| Other real estate owned | 3 |

| | 4 |

| | 8 |

| | 8 |

| | 11 |

|

| Other assets | 942 |

| | 984 |

| | 1,124 |

| | 1,117 |

| | 902 |

|

| | $ | 65,463 |

| | $ | 63,239 |

| | $ | 61,039 |

| | $ | 59,643 |

| | $ | 59,180 |

|

| LIABILITIES AND SHAREHOLDERS’ EQUITY | | | | | | | | | |

| Deposits: | | | | | | | | | |

| Noninterest-bearing demand | $ | 24,410 |

| | $ | 24,115 |

| | $ | 22,711 |

| | $ | 22,277 |

| | $ | 21,872 |

|

| Interest-bearing: | | | | | | | | | |

| Savings and money market | 26,071 |

| | 26,364 |

| | 25,503 |

| | 25,540 |

| | 25,724 |

|

| Time | 2,994 |

| | 2,757 |

| | 2,516 |

| | 2,336 |

| | 2,072 |

|

| Foreign | — |

| | — |

| | 119 |

| | 118 |

| | 220 |

|

| | 53,475 |

| | 53,236 |

| | 50,849 |

| | 50,271 |

| | 49,888 |

|

| Federal funds and other short-term borrowings | 3,137 |

| | 827 |

| | 1,116 |

| | 271 |

| | 233 |

|

| Long-term debt | 383 |

| | 535 |

| | 570 |

| | 699 |

| | 802 |

|

| Reserve for unfunded lending commitments | 60 |

| | 65 |

| | 62 |

| | 65 |

| | 69 |

|

| Other liabilities | 678 |

| | 942 |

| | 763 |

| | 711 |

| | 563 |

|

| Total liabilities | 57,733 |

| | 55,605 |

| | 53,360 |

| | 52,017 |

| | 51,555 |

|

| Shareholders’ equity: | | | | | | | | | |

| Preferred stock, without par value, authorized 4,400 shares | 710 |

| | 710 |

| | 710 |

| | 710 |

| | 828 |

|

| Common stock, without par value; authorized 350,000 shares; issued and outstanding 202,595, 203,085, 203,850, 205,104 and 204,544 shares | 4,696 |

| | 4,725 |

| | 4,748 |

| | 4,783 |

| | 4,778 |

|

| Retained earnings | 2,435 |

| | 2,321 |

| | 2,212 |

| | 2,110 |

| | 2,031 |

|

| Accumulated other comprehensive income (loss) | (111 | ) | | (122 | ) | | 9 |

| | 23 |

| | (12 | ) |

| Total shareholders’ equity | 7,730 |

| | 7,634 |

| | 7,679 |

| | 7,626 |

| | 7,625 |

|

| | $ | 65,463 |

| | $ | 63,239 |

| | $ | 61,039 |

| | $ | 59,643 |

| | $ | 59,180 |

|

ZIONS BANCORPORATION

Press Release – Page 11

April 24, 2017

CONSOLIDATED STATEMENTS OF INCOME

(Unaudited)

|

| | | | | | | | | | | | | | | | | | | |

| | Three Months Ended |

| (In millions, except share and per share amounts) | March 31,

2017 | | December 31,

2016 | | September 30,

2016 | | June 30,

2016 | | March 31,

2016 |

| Interest income: | | | | | | | | | |

| Interest and fees on loans | $ | 433 |

| | $ | 438 |

| | $ | 437 |

| | $ | 434 |

| | $ | 421 |

|

| Interest on money market investments | 4 |

| | 4 |

| | 5 |

| | 5 |

| | 7 |

|

| Interest on securities | 78 |

| | 59 |

| | 49 |

| | 48 |

| | 47 |

|

| Total interest income | 515 |

| | 501 |

| | 491 |

| | 487 |

| | 475 |

|

| Interest expense: | | | | | | | | | |

| Interest on deposits | 13 |

| | 13 |

| | 13 |

| | 12 |

| | 12 |

|

| Interest on short- and long-term borrowings | 13 |

| | 8 |

| | 9 |

| | 10 |

| | 10 |

|

| Total interest expense | 26 |

| | 21 |

| | 22 |

| | 22 |

| | 22 |

|

| Net interest income | 489 |

| | 480 |

| | 469 |

| | 465 |

| | 453 |

|

| Provision for loan losses | 23 |

| | (3 | ) | | 19 |

| | 35 |

| | 42 |

|

| Net interest income after provision for loan losses | 466 |

| | 483 |

| | 450 |

| | 430 |

| | 411 |

|

| Noninterest income: | | | | | | | | | |

| Service charges and fees on deposit accounts | 42 |

| | 43 |

| | 45 |

| | 42 |

| | 41 |

|

| Other service charges, commissions and fees | 49 |

| | 52 |

| | 54 |

| | 52 |

| | 49 |

|

| Wealth management income | 10 |

| | 11 |

| | 10 |

| | 9 |

| | 8 |

|

| Loan sales and servicing income | 7 |

| | 6 |

| | 11 |

| | 10 |

| | 8 |

|

| Capital markets and foreign exchange | 7 |

| | 6 |

| | 6 |

| | 5 |

| | 6 |

|

| Customer-related fees | 115 |

| | 118 |

|

| 126 |

| | 118 |

| | 112 |

|

| Dividends and other investment income | 12 |

| | 4 |

| | 9 |

| | 6 |

| | 5 |

|

| Securities gains (losses), net | 5 |

| | (3 | ) | | 8 |

| | 3 |

| | — |

|

| Other | — |

| | 9 |

| | 2 |

| | (1 | ) | | — |

|

| Total noninterest income | 132 |

| | 128 |

| | 145 |

| | 126 |

| | 117 |

|

| Noninterest expense: | | | | | | | | | |

| Salaries and employee benefits | 262 |

| | 241 |

| | 242 |

| | 241 |

| | 258 |

|

| Occupancy, net | 33 |

| | 32 |

| | 33 |

| | 30 |

| | 30 |

|

| Furniture, equipment and software, net | 32 |

| | 33 |

| | 29 |

| | 31 |

| | 32 |

|

| Other real estate expense, net | — |

| | — |

| | — |

| | (1 | ) | | (1 | ) |

| Credit-related expense | 8 |

| | 7 |

| | 7 |

| | 6 |

| | 6 |

|

| Provision for unfunded lending commitments | (5 | ) | | 3 |

| | (3 | ) | | (4 | ) | | (6 | ) |

| Professional and legal services | 14 |

| | 17 |

| | 14 |

| | 12 |

| | 12 |

|

| Advertising | 5 |

| | 5 |

| | 6 |

| | 5 |

| | 6 |

|

| FDIC premiums | 12 |

| | 11 |

| | 12 |

| | 10 |

| | 7 |

|

| Amortization of core deposit and other intangibles | 2 |

| | 2 |

| | 2 |

| | 2 |

| | 2 |

|

| Other | 51 |

| | 53 |

| | 61 |

| | 50 |

| | 50 |

|

| Total noninterest expense | 414 |

| | 404 |

| | 403 |

| | 382 |

| | 396 |

|

| Income before income taxes | 184 |

| | 207 |

| | 192 |

| | 174 |

| | 132 |

|

| Income taxes | 45 |

| | 70 |

| | 65 |

| | 60 |

| | 41 |

|

| Net income | 139 |

| | 137 |

| | 127 |

| | 114 |

| | 91 |

|

| Preferred stock dividends | (10 | ) | | (12 | ) | | (10 | ) | | (13 | ) | | (12 | ) |

| Preferred stock redemption | — |

| | — |

| | — |

| | (10 | ) | | — |

|

| Net earnings applicable to common shareholders | $ | 129 |

| | $ | 125 |

| | $ | 117 |

| | $ | 91 |

| | $ | 79 |

|

| | | | | | | | | | |

| Weighted average common shares outstanding during the period: | | | | | | | | |

| Basic shares (in thousands) | 202,347 |

| | 202,886 |

| | 204,312 |

| | 204,236 |

| | 203,967 |

|

| Diluted shares (in thousands) | 210,405 |

| | 205,446 |

| | 204,714 |

| | 204,536 |

| | 204,096 |

|

| Net earnings per common share: | | | | | | | | | |

| Basic | $ | 0.63 |

| | $ | 0.61 |

| | $ | 0.57 |

| | $ | 0.44 |

| | $ | 0.38 |

|

| Diluted | 0.61 |

| | 0.60 |

| | 0.57 |

| | 0.44 |

| | 0.38 |

|

ZIONS BANCORPORATION

Press Release – Page 12

April 24, 2017

Loan Balances Held for Investment by Portfolio Type

(Unaudited)

|

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| (In millions) | March 31,

2017 | | December 31,

2016 | | September 30,

2016 | | June 30,

2016 | | March 31,

2016 |

| Commercial: | | | | | | | | | | | | | | | | | | | |

| Commercial and industrial | | $ | 13,368 |

| | | | $ | 13,452 |

| | | | $ | 13,543 |

| | | | $ | 13,757 |

| | | | $ | 13,590 |

| |

| Leasing | | 404 |

| | | | 423 |

| | | | 439 |

| | | | 426 |

| | | | 437 |

| |

| Owner occupied | | 6,973 |

| | | | 6,962 |

| | | | 6,889 |

| | | | 6,989 |

| | | | 7,022 |

| |

| Municipal | | 811 |

| | | | 778 |

| | | | 753 |

| | | | 756 |

| | | | 696 |

| |

| Total commercial | | 21,556 |

| | | | 21,615 |

| | | | 21,624 |

| | | | 21,928 |

| | | | 21,745 |

| |

| Commercial real estate: | | | | | | | | | | | | | | | | | | | |

| Construction and land development | | 2,123 |

| | | | 2,019 |

| | | | 2,147 |

| | | | 2,088 |

| | | | 1,968 |

| |

| Term | | 9,083 |

| | | | 9,322 |

| | | | 9,303 |

| | | | 9,230 |

| | | | 8,826 |

| |

| Total commercial real estate | | 11,206 |

| | | | 11,341 |

| | | | 11,450 |

| | | | 11,318 |

| | | | 10,794 |

| |

| Consumer: | | | | | | | | | | | | | | | | | | | |

| Home equity credit line | | 2,638 |

| | | | 2,645 |

| | | | 2,581 |

| | | | 2,507 |

| | | | 2,433 |

| |

| 1-4 family residential | | 6,185 |

| | | | 5,891 |

| | | | 5,785 |

| | | | 5,680 |

| | | | 5,418 |

| |

| Construction and other consumer real estate | | 517 |

| | | | 486 |

| | | | 453 |

| | | | 419 |

| | | | 401 |

| |

| Bankcard and other revolving plans | | 459 |

| | | | 481 |

| | | | 458 |

| | | | 460 |

| | | | 439 |

| |

| Other | | 181 |

| | | | 190 |

| | | | 189 |

| | | | 189 |

| | | | 188 |

| |

| Total consumer | | 9,980 |

| | | | 9,693 |

| | | | 9,466 |

| | | | 9,255 |

| | | | 8,879 |

| |

| Loans and leases, net of unearned income and fees | | $ | 42,742 |

| | | | $ | 42,649 |

| | | | $ | 42,540 |

| | | | $ | 42,501 |

| | | | $ | 41,418 |

| |

Nonperforming Assets

(Unaudited)

|

| | | | | | | | | | | | | | | | | | | |

| (In millions) | March 31,

2017 | | December 31,

2016 | | September 30,

2016 | | June 30,

2016 | | March 31,

2016 |

| | | | | | | | | | |

Nonaccrual loans1 | $ | 585 |

| | $ | 569 |

| | $ | 579 |

| | $ | 547 |

| | $ | 542 |

|

| Other real estate owned | 3 |

| | 4 |

| | 8 |

| | 8 |

| | 10 |

|

| Total nonperforming assets | $ | 588 |

| | $ | 573 |

| | $ | 587 |

| | $ | 555 |

| | $ | 552 |

|

Ratio of nonperforming assets to loans1 and leases and other real estate owned | 1.37 | % | | 1.34 | % | | 1.37 | % | | 1.30 | % | | 1.33 | % |

| Accruing loans past due 90 days or more | $ | 30 |

| | $ | 36 |

| | $ | 29 |

| | $ | 29 |

| | $ | 37 |

|

Ratio of accruing loans past due 90 days or more to loans1 and leases | 0.07 | % | | 0.08 | % | | 0.07 | % | | 0.07 | % | | 0.09 | % |

| Nonaccrual loans and accruing loans past due 90 days or more | $ | 616 |

| | $ | 605 |

| | $ | 608 |

| | $ | 576 |

| | $ | 579 |

|

Ratio of nonaccrual loans and accruing loans past due 90 days or more to loans1 and leases | 1.44 | % | | 1.41 | % | | 1.42 | % | | 1.35 | % | | 1.39 | % |

| Accruing loans past due 30-89 days | $ | 137 |

| | $ | 126 |

| | $ | 164 |

| | $ | 133 |

| | $ | 100 |

|

| Restructured loans included in nonaccrual loans | 131 |

| | 100 |

| | 125 |

| | 143 |

| | 133 |

|

| Restructured loans on accrual | 167 |

| | 151 |

| | 170 |

| | 172 |

| | 195 |

|

| Classified loans | 1,464 |

| | 1,577 |

| | 1,615 |

| | 1,610 |

| | 1,532 |

|

1 Includes loans held for sale.

ZIONS BANCORPORATION

Press Release – Page 13

April 24, 2017

Allowance for Credit Losses

(Unaudited)

|

| | | | | | | | | | | | | | | | | | | |

| | Three Months Ended |

| (In millions) | March 31,

2017 | | December 31,

2016 | | September 30,

2016 | | June 30,

2016 | | March 31,

2016 |

| Allowance for Loan Losses | | | | | | | | | |

| Balance at beginning of period | $ | 567 |

| | $ | 597 |

| | $ | 608 |

| | $ | 612 |

| | $ | 606 |

|

| Add: | | | | | | | | | |

| Provision for losses | 23 |

| | (3 | ) | | 19 |

| | 35 |

| | 42 |

|

| Deduct: | | | | | | | | | |

| Gross loan and lease charge-offs | (57 | ) | | (38 | ) | | (54 | ) | | (58 | ) | | (48 | ) |

| Recoveries | 11 |

| | 11 |

| | 24 |

| | 19 |

| | 12 |

|

| Net loan and lease charge-offs | (46 | ) | | (27 | ) | | (30 | ) | | (39 | ) | | (36 | ) |

| Balance at end of period | $ | 544 |

| | $ | 567 |

| | $ | 597 |

| | $ | 608 |

| | $ | 612 |

|

Ratio of allowance for loan losses to loans1 and leases, at period end | 1.27 | % | | 1.33 | % | | 1.40 | % | | 1.43 | % | | 1.48 | % |

Ratio of allowance for loan losses to nonaccrual loans1 at period end | 98.55 | % | | 107.18 | % | | 108.74 | % | | 113.86 | % | | 112.92 | % |

| Annualized ratio of net loan and lease charge-offs to average loans | 0.43 | % | | 0.25 | % | | 0.28 | % | | 0.37 | % | | 0.35 | % |

| Reserve for Unfunded Lending Commitments | | | | | | | | | |

| Balance at beginning of period | $ | 65 |

| | $ | 62 |

| | $ | 65 |

| | $ | 69 |

| | $ | 75 |

|

| Provision charged (credited) to earnings | (5 | ) | | 3 |

| | (3 | ) | | (4 | ) | | (6 | ) |

| Balance at end of period | $ | 60 |

| | $ | 65 |

| | $ | 62 |

| | $ | 65 |

| | $ | 69 |

|

| Total Allowance for Credit Losses | | | | | | | | | |

| Allowance for loan losses | $ | 544 |

| | $ | 567 |

| | $ | 597 |

| | $ | 608 |

| | $ | 612 |

|

| Reserve for unfunded lending commitments | 60 |

| | 65 |

| | 62 |

| | 65 |

| | 69 |

|

| Total allowance for credit losses | $ | 604 |

| | $ | 632 |

| | $ | 659 |

| | $ | 673 |

| | $ | 681 |

|

Ratio of total allowance for credit losses to loans1 and leases outstanding, at period end | 1.41 | % | | 1.48 | % | | 1.55 | % | | 1.58 | % | | 1.64 | % |

1 Does not include loans held for sale.

ZIONS BANCORPORATION

Press Release – Page 14

April 24, 2017

Nonaccrual Loans by Portfolio Type

(Unaudited)

|

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| (In millions) | March 31,

2017 | | December 31,

2016 | | September 30,

2016 | | June 30,

2016 | | March 31,

2016 |

| | | | | | | | | | | | | | | | | | | | |

| Loans held for sale | | $ | 34 |

| | | | $ | 40 |

| | | | $ | 29 |

| | | | $ | 13 |

| | | | $ | — |

| |

| | | | | | | | | | | | | | | | | | | | |

| Commercial: | | | | | | | | | | | | | | | | | | | |

| Commercial and industrial | | $ | 358 |

| | | | $ | 354 |

| | | | $ | 387 |

| | | | $ | 341 |

| | | | $ | 356 |

| |

| Leasing | | 13 |

| | | | 14 |

| | | | 14 |

| | | | 14 |

| | | | 14 |

| |

| Owner occupied | | 89 |

| | | | 74 |

| | | | 66 |

| | | | 69 |

| | | | 74 |

| |

| Municipal | | 1 |

| | | | 1 |

| | | | 1 |

| | | | 1 |

| | | | 1 |

| |

| Total commercial | | 461 |

| | | | 443 |

| | | | 468 |

| | | | 425 |

| | | | 445 |

| |

| Commercial real estate: | | | | | | | | | | | | | | | | | | | |

| Construction and land development | | 7 |

| | | | 7 |

| | | | 4 |

| | | | 5 |

| | | | 6 |

| |

| Term | | 38 |

| | | | 29 |

| | | | 28 |

| | | | 51 |

| | | | 33 |

| |

| Total commercial real estate | | 45 |

| | | | 36 |

| | | | 32 |

| | | | 56 |

| | | | 39 |

| |

| Consumer: | | | | | | | | | | | | | | | | | | | |

| Home equity credit line | | 9 |

| | | | 11 |

| | | | 11 |

| | | | 12 |

| | | | 11 |

| |

| 1-4 family residential | | 35 |

| | | | 36 |

| | | | 36 |

| | | | 39 |

| | | | 44 |

| |

| Construction and other consumer real estate | | 1 |

| | | | 2 |

| | | | 1 |

| | | | 1 |

| | | | 1 |

| |

| Bankcard and other revolving plans | | — |

| | | | 1 |

| | | | 2 |

| | | | 1 |

| | | | 2 |

| |

| Total consumer | | 45 |

| | | | 50 |

| | | | 50 |

| | | | 53 |

| | | | 58 |

| |

| Total nonaccrual loans | | $ | 585 |

| | | | $ | 569 |

| | | | $ | 579 |

| | | | $ | 547 |

| | | | $ | 542 |

| |

Net Charge-Offs by Portfolio Type

(Unaudited)

|

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Three Months Ended |

| (In millions) | March 31,

2017 | | December 31,

2016 | | September 30,

2016 | | June 30,

2016 | | March 31,

2016 |

| Commercial: | | | | | | | | | | | | | | | | | | | |

| Commercial and industrial | | $ | 45 |

| | | | $ | 25 |

| | | | $ | 33 |

| | | | $ | 32 |

| | | | $ | 37 |

| |

| Leasing | | — |

| | | | — |

| | | | — |

| | | | — |

| | | | — |

| |

| Owner occupied | | 1 |

| | | | (1 | ) | | | | — |

| | | | — |

| | | | (1 | ) | |

| Municipal | | — |

| | | | — |

| | | | — |

| | | | — |

| | | | — |

| |

| Total commercial | | 46 |

| | | | 24 |

| | | | 33 |

| | | | 32 |

| | | | 36 |

| |

| Commercial real estate: | | | | | | | | | | | | | | | | | | | |

| Construction and land development | | (2 | ) | | | | — |

| | | | (1 | ) | | | | (1 | ) | | | | (2 | ) | |

| Term | | 1 |

| | | | 1 |

| | | | (5 | ) | | | | 7 |

| | | | — |

| |

| Total commercial real estate | | (1 | ) | | | | 1 |

| | | | (6 | ) | | | | 6 |

| | | | (2 | ) | |

| Consumer: | | | | | | | | | | | | | | | | | | | |

| Home equity credit line | | (1 | ) | | | | — |

| | | | 1 |

| | | | — |

| | | | 1 |

| |

| 1-4 family residential | | (1 | ) | | | | — |

| | | | — |

| | | | (1 | ) | | | | 1 |

| |

| Construction and other consumer real estate | | — |

| | | | — |

| | | | — |

| | | | — |

| | | | — |

| |

| Bankcard and other revolving plans | | 3 |

| | | | 2 |

| | | | 2 |

| | | | 1 |

| | | | — |

| |

| Total consumer loans | | 1 |

| | | | 2 |

| | | | 3 |

| | | | — |

| | | | 2 |

| |

| Total net charge-offs (recoveries) | | $ | 46 |

| | | | $ | 27 |

| | | | $ | 30 |

| | | | $ | 38 |

| | | | $ | 36 |

| |

ZIONS BANCORPORATION

Press Release – Page 15

April 24, 2017

CONSOLIDATED AVERAGE BALANCE SHEETS, YIELDS AND RATES

(Unaudited) |

| | | | | | | | | | | | | | | | | | | | |

| | Three Months Ended |

| | March 31, 2017 | | December 31, 2016 | | March 31, 2016 |

| (In millions) | Average balance | | Average yield/rate 1 | | Average balance | | Average

yield/rate 1 | | Average balance | | Average

yield/rate 1 |

| ASSETS | | | | | | | | | | | |

| Money market investments | $ | 1,983 |

| | 0.93 | % | | $ | 2,367 |

| | 0.70 | % | | $ | 5,122 |

| | 0.55 | % |

| Securities: | | | | | | | | | | | |

| Held-to-maturity | 847 |

| | 3.90 | % | | 762 |

| | 4.09 | % | | 562 |

| | 4.86 | % |

| Available-for-sale | 14,024 |

| | 2.14 | % | | 11,501 |

| | 1.89 | % | | 8,109 |

| | 2.11 | % |

| Trading account | 61 |

| | 3.75 | % | | 120 |

| | 4.04 | % | | 53 |

| | 3.56 | % |

| Total securities | 14,932 |

| | 2.24 | % | | 12,383 |

| | 2.04 | % | | 8,724 |

| | 2.30 | % |

| Loans held for sale | 132 |

| | 3.22 | % | | 162 |

| | 2.73 | % | | 140 |

| | 3.95 | % |

Loans held for investment 2: | | | | | | | | | | | |

| Commercial | 21,606 |

| | 4.22 | % | | 21,618 |

| | 4.21 | % | | 21,624 |

| | 4.20 | % |

| Commercial real estate | 11,241 |

| | 4.27 | % | | 11,463 |

| | 4.24 | % | | 10,556 |

| | 4.23 | % |

| Consumer | 9,719 |

| | 3.82 | % | | 9,558 |

| | 3.73 | % | | 8,823 |

| | 3.90 | % |

| Total loans held for investment | 42,566 |

| | 4.14 | % | | 42,639 |

| | 4.11 | % | | 41,003 |

| | 4.14 | % |

| Total interest-earning assets | 59,613 |

| | 3.56 | % | | 57,551 |

| | 3.52 | % | | 54,989 |

| | 3.51 | % |

| Cash and due from banks | 974 |

| | | | 894 |

| | | | 728 |

| | |

| Allowance for loan losses | (566 | ) | | | | (589 | ) | | | | (600 | ) | | |

| Goodwill | 1,014 |

| | | | 1,014 |

| | | | 1,014 |

| | |

| Core deposit and other intangibles | 8 |

| | | | 10 |

| | | | 15 |

| | |

| Other assets | 2,952 |

| | | | 2,866 |

| | | | 2,680 |

| | |

| Total assets | $ | 63,995 |

| | | | $ | 61,746 |

| | | | $ | 58,826 |

| | |

| LIABILITIES AND SHAREHOLDERS’ EQUITY | | | | | | | | | | |

| Interest-bearing deposits: | | | | | | | | | | | |

| Savings and money market | $ | 25,896 |

| | 0.14 | % | | $ | 25,873 |

| | 0.14 | % | | $ | 25,350 |

| | 0.15 | % |

| Time | 2,856 |

| | 0.59 | % | | 2,638 |

| | 0.54 | % | | 2,088 |

| | 0.44 | % |

| Foreign | — |

| |

| | 21 |

| | 0.31 | % | | 235 |

| | 0.26 | % |

| Total interest-bearing deposits | 28,752 |

| | 0.19 | % | | 28,532 |

| | 0.18 | % | | 27,673 |

| | 0.17 | % |

| Borrowed funds: | | | | | | | | | | | |

| Federal funds and other short-term borrowings | 2,924 |

| | 0.71 | % | | 665 |

| | 0.36 | % | | 268 |

| | 0.18 | % |

| Long-term debt | 521 |

| | 5.92 | % | | 537 |

| | 5.71 | % | | 809 |

| | 5.02 | % |

| Total borrowed funds | 3,445 |

| | 1.50 | % | | 1,202 |

| | 2.75 | % | | 1,077 |

| | 3.82 | % |

| Total interest-bearing liabilities | 32,197 |

| | 0.33 | % | | 29,734 |

| | 0.28 | % | | 28,750 |

| | 0.31 | % |

| Noninterest-bearing deposits | 23,460 |

| | | | 23,648 |

| | | | 21,882 |

| | |

| Other liabilities | 632 |

| | | | 656 |

| | | | 579 |

| | |

| Total liabilities | 56,289 |

| | | | 54,038 |

| | | | 51,211 |

| | |

| Shareholders’ equity: | | | | | | | | | | | |

| Preferred equity | 710 |

| | | | 710 |

| | | | 828 |

| | |

| Common equity | 6,996 |

| | | | 6,998 |

| | | | 6,787 |

| | |

| Total shareholders’ equity | 7,706 |

| | | | 7,708 |

| | | | 7,615 |

| | |

| Total liabilities and shareholders’ equity | $ | 63,995 |

| | | | $ | 61,746 |

| | | | $ | 58,826 |

| | |

| | | | | | | | | | | | |

| Spread on average interest-bearing funds | | | 3.23 | % | | | | 3.24 | % | | | | 3.20 | % |

| Net yield on interest-earning assets | | | 3.38 | % | | | | 3.37 | % | | | | 3.35 | % |

1 Rates are calculated using amounts in thousands and taxable-equivalent rates used where applicable.

2 Net of unearned income and fees, net of related costs. Loans include nonaccrual and restructured loans.

ZIONS BANCORPORATION

Press Release – Page 16

April 24, 2017

GAAP to Non-GAAP Reconciliations

(Unaudited)

This press release presents both GAAP and non-GAAP financial measures to provide investors with additional information. The adjustments to reconcile from the applicable GAAP financial measures to the non-GAAP financial measures are presented in the following tables. The Company considers these adjustments to be relevant to ongoing operating results. The Company believes that excluding the amounts associated with these adjustments to present the non-GAAP financial measures provides a meaningful base for period-to-period and company-to-company comparisons. These non-GAAP financial measures are used by management to assess the performance and financial position of the Company and for presentations of Company performance to investors. The Company further believes that presenting these non-GAAP financial measures will permit investors and analysts to assess the performance of the Company on the same basis as that applied by management.

Non-GAAP financial measures have inherent limitations, are not required to be uniformly applied, and are not audited. Although non-GAAP financial measures are frequently used by stakeholders to evaluate a company, they have limitations as an analytical tool and should not be considered in isolation or as a substitute for analysis of results reported under GAAP.

The following are the non-GAAP financial measures presented in this Earnings Release and a discussion of why management uses these non-GAAP measures:

| |

| • | Tangible Book Value per Common Share - this table also includes “Tangible common equity.” Tangible book value per common share is a non-GAAP financial measure that management believes provides additional useful information about the level of tangible assets in relation to outstanding shares of common stock. Management believes the use of ratios that utilize tangible equity provides additional useful information because they present measures of those assets that can generate income. |

| |

| • | Tangible Return on Average Tangible Common Equity - this table also includes “Net earnings applicable to common shareholders, excluding the effects of the adjustments, net of tax” and “Average tangible common equity.” Tangible return on average tangible common equity is a non-GAAP financial measure that management believes provides useful information about the Company’s use of equity. Management believes the use of ratios that utilize tangible equity provides additional useful information because they present measures of those assets that can generate income. |

| |

| • | Efficiency Ratio - this table also includes “Adjusted noninterest expense,” “Taxable-equivalent net interest income,” “Adjusted tax-equivalent revenue,” and “Adjusted pre-provision net revenue (“PPNR”).” The methodology of determining the efficiency ratio may differ among companies. Management makes adjustments to exclude certain items as identified in the subsequent schedule which management believes allows for more consistent comparability among periods. Management believes the efficiency ratio provides useful information regarding the cost of generating revenue. Adjusted noninterest expense provides a measure as to how well the Company is managing its expenses, and adjusted PPNR enables management and others to assess the Company’s ability to generate capital to cover credit losses through a credit cycle. Taxable-equivalent net interest income allows management to assess the comparability of revenue arising from both taxable and tax-exempt sources. The efficiency ratio and adjusted noninterest expense are the key metrics to which the Company announced it would hold itself accountable in its June 1, 2015 efficiency initiative, and to which executive compensation is tied. |

ZIONS BANCORPORATION

Press Release – Page 17

April 24, 2017

GAAP to Non-GAAP Reconciliations

(Unaudited)

|

| | | | | | | | | | | | | | | | | | | | |

| (In millions, except shares and per share amounts) | | March 31,

2017 | | December 31,

2016 | | September 30,

2016 | | June 30,

2016 | | March 31,

2016 |

| Tangible Book Value per Common Share | | | | | | | | |

| | | | | | | | | | | |

| Total shareholders’ equity (GAAP) | | $ | 7,730 |

| | $ | 7,634 |

| | $ | 7,679 |

| | $ | 7,626 |

| | $ | 7,625 |

|

| Preferred stock | | (710 | ) | | (710 | ) | | (710 | ) | | (710 | ) | | (828 | ) |

| Goodwill | | (1,014 | ) | | (1,014 | ) | | (1,014 | ) | | (1,014 | ) | | (1,014 | ) |

| Core deposit and other intangibles | | (7 | ) | | (8 | ) | | (10 | ) | | (12 | ) | | (14 | ) |

| Tangible common equity (non-GAAP) | (a) | $ | 5,999 |

| | $ | 5,902 |

| | $ | 5,945 |

| | $ | 5,890 |

| | $ | 5,769 |

|

| Common shares outstanding (in thousands) | (b) | 202,595 |

| | 203,085 |

| | 203,850 |

| | 205,104 |

| | 204,544 |

|

| Tangible book value per common share (non-GAAP) | (a/b) | $ | 29.61 |

| | $ | 29.06 |

| | $ | 29.16 |

| | $ | 28.72 |

| | $ | 28.20 |

|

| | | | | | | | | | | |

| | | Three Months Ended |

| (Dollar amounts in millions) | | March 31,

2017 | | December 31,

2016 | | September 30,

2016 | | June 30,

2016 | | March 31,

2016 |

| Tangible Return on Average Tangible Common Equity | | | | | | | | |

| | | | | | | | | | | |

| Net earnings applicable to common shareholders (GAAP) | | $ | 129 |

| | $ | 125 |

| | $ | 117 |

| | $ | 91 |

| | $ | 79 |

|

| Adjustments, net of tax: | | | | | | | | | | |

| Amortization of core deposit and other intangibles | | 1 |

| | 1 |

| | 1 |

| | 1 |

| | 1 |

|

| Net earnings applicable to common shareholders, excluding the effects of the adjustments, net of tax (non-GAAP) | (a) | $ | 130 |

| | $ | 126 |

| | $ | 118 |

| | $ | 92 |

| | $ | 80 |

|

| Average common equity (GAAP) | | $ | 6,996 |

| | $ | 6,998 |

| | $ | 6,986 |

| | $ | 6,883 |

| | $ | 6,787 |

|

| Average goodwill | | (1,014 | ) | | (1,014 | ) | | (1,014 | ) | | (1,014 | ) | | (1,014 | ) |

| Average core deposit and other intangibles | | (8 | ) | | (10 | ) | | (11 | ) | | (14 | ) | | (15 | ) |

| Average tangible common equity (non-GAAP) | (b) | $ | 5,974 |

| | $ | 5,974 |

| | $ | 5,961 |

| | $ | 5,855 |

| | $ | 5,758 |

|

| Number of days in quarter | (c) | 90 |

| | 92 |

| | 92 |

| | 91 |

| | 91 |

|

| Number of days in year | (d) | 365 |

| | 366 |

| | 366 |

| | 366 |

| | 366 |

|

| Tangible return on average tangible common equity (non-GAAP) | (a/b/c)*d | 8.8 | % | | 8.4 | % | | 7.9 | % | | 6.3 | % | | 5.6 | % |

ZIONS BANCORPORATION

Press Release – Page 18

April 24, 2017

GAAP to Non-GAAP Reconciliations

(Unaudited)

|

| | | | | | | | | | | | | | | | | | | | |

| | | Three Months Ended |

| (In millions) | | March 31,

2017 | | December 31,

2016 | | September 30,

2016 | | June 30,

2016 | | March 31,

2016 |

| Efficiency Ratio | | | | | | | | | | |

| | | | | | | | | | | |

| Noninterest expense (GAAP) | (a) | $ | 414 |

| | $ | 404 |

| | $ | 403 |

| | $ | 382 |

| | $ | 396 |

|

| Adjustments: | | | | | | | | | | |

| Severance costs | | 5 |

| | 1 |

| | — |

| | — |

| | 4 |

|

| Other real estate expense | | — |

| | — |

| | — |

| | (1 | ) | | (1 | ) |

| Provision for unfunded lending commitments | | (5 | ) | | 3 |

| | (3 | ) | | (4 | ) | | (6 | ) |

| Debt extinguishment cost | | — |

| | — |

| | — |

| | — |

| | — |

|

| Amortization of core deposit and other intangibles | | 2 |

| | 2 |

| | 2 |

| | 2 |

| | 2 |

|

Restructuring costs 1 | | 1 |

| | 3 |

| | — |

| | — |

| | 1 |

|

| Total adjustments | (b) | 3 |

| | 9 |

| | (1 | ) | | (3 | ) | | — |

|

| Adjusted noninterest expense (non-GAAP) | (a-b)=(c) | $ | 411 |

| | $ | 395 |

| | $ | 404 |

| | $ | 385 |

| | $ | 396 |

|

| Net interest income (GAAP) | (d) | $ | 489 |

| | $ | 480 |

| | $ | 469 |

| | $ | 465 |

| | $ | 453 |

|

| Fully taxable-equivalent adjustments | (e) | 8 |

| | 8 |

| | 7 |

| | 6 |

| | 5 |

|

| Taxable-equivalent net interest income (non-GAAP) | (d+e)=(f) | 497 |

| | 488 |

| | 476 |

| | 471 |

| | 458 |

|

| Noninterest income (GAAP) | (g) | 132 |

| | 128 |

| | 145 |

| | 126 |

| | 117 |

|

| Combined income | (f+g)=(h) | 629 |

| | 616 |

| | 621 |

| | 597 |

| | 575 |

|

| Adjustments: | | | | | | | | | | |

| Fair value and nonhedge derivative income (loss) | | — |

| | 7 |

| | — |

| | (2 | ) | | (3 | ) |

| Securities gains (losses), net | | 5 |

| | (3 | ) | | 8 |

| | 3 |

| | — |

|

| Total adjustments | (i) | 5 |

| | 4 |

| | 8 |

| | 1 |

| | (3 | ) |

| Adjusted taxable-equivalent revenue (non-GAAP) | (h-i)=(j) | $ | 624 |

| | $ | 612 |

| | $ | 613 |

| | $ | 596 |

| | $ | 578 |

|

| Pre-provision net revenue (PPNR) | (h)-(a) | $ | 215 |

| | $ | 212 |

| | $ | 218 |

| | $ | 215 |

| | $ | 179 |

|

| Adjusted PPNR | (j-c) | 213 |

| | 217 |

| | 209 |

| | 211 |

| | 182 |

|

| Efficiency ratio | (c/j) | 65.9 | % | | 64.5 | % | | 65.9 | % | | 64.6 | % | | 68.5 | % |

1 The restructuring costs in the fourth quarter of 2016 are primarily related to the termination of the Zions Direct auction platform and changes to create a simplified lending approach for our business banking customers.