UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 20-F

| o | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| | For the fiscal year ended December 31, 2011 |

| o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| o | SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission file number 0-30224

(Exact name of Registrant as specified in its charter)

Guernsey, Channel Islands

(Jurisdiction of incorporation or organization)

Marine House, Clanwilliam Place

(Address of principal executive offices)

Huw Spiers

Marine House, Clanwilliam Place

Dublin 2, Ireland

Tel: +353 1 234 0400 Fax: +353 1 661 9637

(Name, telephone, e-mail and/or facsimile number and address of contact person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

| Title of each class: | Name of each exchange

on which registered: |

| Ordinary Shares | NASDAQ Global Select Market |

| | |

Securities registered or to be registered pursuant to Section 12(g) of the Act: None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of December 31, 2011.

13,819,051 Ordinary Shares (including 848,511 Exchangeable Shares)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes o No x

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes o No x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act.

Large accelerated filer o Accelerated filer o �� Non-Accelerated Filer x

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

o U.S. GAAP

x International Financial Reporting Standards as issued by the International Accounting Standards Board

o Other

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

Item 17 o

Item 18 o

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes o No x

TABLE OF CONTENTS

| PRESENTATION OF FINANCIAL AND OTHER INFORMATION | 1 |

| | |

| CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING INFORMATION | 2 |

| | |

| PART I | 3 |

| | ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS | 3 |

| | | |

| | ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE | 3 |

| | | |

| | ITEM 3. KEY INFORMATION | 3 |

| | | |

| | | SELECTED FINANCIAL DATA | 3 |

| | | | |

| | | RISK FACTORS | 4 |

| | | | |

| | ITEM 4. INFORMATION ON THE COMPANY | 12 |

| | | |

| | | A. | HISTORY AND DEVELOPMENT OF THE COMPANY | 12 |

| | | B. | BUSINESS OVERVIEW | 13 |

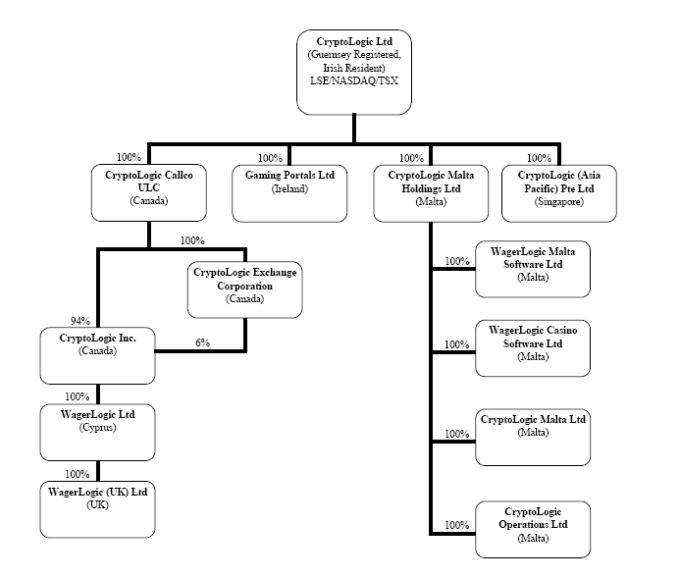

| | | C. | ORGANIZATIONAL STRUCTURE | 18 |

| | | D. | PROPERTY, PLANTS AND EQUIPMENT | 19 |

| | ITEM 4A. UNRESOLVED STAFF COMMENTS | 19 |

| | | |

| | ITEM 5. OPERATING AND FINANCIAL REVIEW AND PROSPECTS | 20 |

| | | |

| | | A. | OPERATING RESULTS | 21 |

| | | B. | LIQUIDITY AND CAPITAL RESOURCES | 25 |

| | | C. | RESEARCH AND DEVELOPMENT | 33 |

| | | D. | TREND INFORMATION | 33 |

| | | E. | OFF-BALANCE SHEET ARRANGEMENTS | 34 |

| | | F. | CONTRACTUAL OBLIGATIONS | 34 |

| | | G. | SAFE HARBOR | 34 |

| | ITEM 6. DIRECTORS, SENIOR MANAGEMENT AND EMPLOYEES | 34 |

| | | |

| | | A. | DIRECTORS AND SENIOR MANAGEMENT | 34 |

| | | B. | COMPENSATION | 36 |

| | | C. | BOARD PRACTICES | 39 |

| | | D. | EMPLOYEES | 40 |

| | | E. | SHARE OWNERSHIP | 41 |

| | ITEM 7. MAJOR SHAREHOLDERS AND RELATED PARTY TRANSACTIONS | 43 |

| | | |

| | | A. | MAJOR SHAREHOLDERS | 43 |

| | | B. | RELATED PARTY TRANSACTIONS | 43 |

| | ITEM 8. FINANCIAL INFORMATION | 44 |

| | | |

| | | A. | CONSOLIDATED STATEMENTS AND OTHER FINANCIAL INFORMATION | 44 |

| | | B. | SIGNIFICANT CHANGES | 44 |

| | ITEM 9. THE OFFER AND LISTING | 45 |

| | | |

| | ITEM 10. ADDITIONAL INFORMATION | 46 |

| | | |

| | | B. | MEMORANDUM AND ARTICLES OF ASSOCIATION | 46 |

| | | C. | MATERIAL CONTRACTS | 48 |

| | | D. | EXCHANGE CONTROLS | 48 |

| | | E. | TAXATION | 48 |

| | | F. | DIVIDENDS AND PAYING AGENTS | 55 |

| | | G. | STATEMENT BY EXPERTS | 55 |

| | | H. | DOCUMENTS ON DISPLAY | 55 |

| | | I. | SUBSIDIARY INFORMATION | 55 |

| | ITEM 11. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK | 55 |

| | | |

| | ITEM 12. DESCRIPTION OF SECURITIES OTHER THAN EQUITY SECURITIES | 57 |

| | |

| PART II | 58 |

| | ITEM 13. DEFAULTS, DIVIDEND ARREARAGES AND DELINQUENCIES | 58 |

| | | |

| | ITEM 14. MATERIAL MODIFICATIONS TO THE RIGHTS OF SECURITY HOLDERS AND USE OF PROCEEDS | 58 |

| | | |

| | ITEM 15. CONTROLS AND PROCEDURES | 58 |

| | | |

| | ITEM 16A. AUDIT COMMITTEE FINANCIAL EXPERT | 58 |

| | | |

| | ITEM 16B. CODE OF ETHICS | 59 |

| | | |

| | ITEM 16C. PRINCIPAL ACCOUNTANT FEES AND SERVICES | 59 |

| | | |

| | ITEM 16D. EXEMPTIONS FROM THE LISTING STANDARDS FOR AUDIT COMMITTEES | 59 |

| | | |

| | ITEM 16E. PURCHASES OF EQUITY SECURITIES BY THE ISSUER AND AFFILIATED PURCHASERS | 59 |

| | | |

| | ITEM 16F. CHANGE IN REGISTRANT’S CERTIFYING ACCOUNTANT | 59 |

| | | |

| | ITEM 16G. CORPORATE GOVERNANCE | 59 |

| | ITEM 17. FINANCIAL STATEMENTS | 61 |

| | | |

| | ITEM 18. FINANCIAL STATEMENTS | 61 |

| | | |

| | ITEM 19. EXHIBITS | 61 |

| | | |

| SIGNATURE | 63 |

PRESENTATION OF FINANCIAL AND OTHER INFORMATION

In this annual report, except as otherwise indicated or as the context otherwise requires, the “Company”, “we”, “us” and “our” refers to CryptoLogic Limited (“CryptoLogic”) and its operating subsidiaries.

Pursuant to a business reorganization implemented by way of an Ontario Superior Court of Justice court approved plan of arrangement (the “Arrangement”) and approved by the shareholders on May 24, 2007, CryptoLogic acquired control over all of the issued and outstanding common shares of CryptoLogic Inc., an Ontario company, which through the Arrangement became an indirect subsidiary of CryptoLogic. As part of the Arrangement, the Company issued either an equivalent amount of CryptoLogic ordinary shares (“Ordinary Shares”) or, in the case of taxable Canadian residents, exchangeable shares (“Exchangeable Shares”) of CryptoLogic Exchange Corporation (“CEC”), an indirect subsidiary of CryptoLogic. The Exchangeable Shares are, as nearly as practicable, the economic equivalent of the Ordinary Shares. The holders of Exchangeable Shares and Ordinary Shares participate equally in voting and dividends. No additional Exchangeable Shares have been or will be issued.

For accounting purposes, the Arrangement has been accounted for using the continuity of interest method, which recognizes CryptoLogic as the successor entity to CryptoLogic Inc. Accordingly, financial information presented in the annual report reflects the financial position, results of operations and cash flows as if CryptoLogic has always carried on the business formerly carried on by CryptoLogic Inc., with all assets and liabilities recorded at the carrying values of CryptoLogic Inc. The interest held by Exchangeable Shareholders has been presented as a non-controlling interest in the consolidated financial statements, as required under International Financial Reporting Standards (“IFRS”).

Our consolidated financial statements have been prepared in accordance with IFRS, which are different from generally accepted accounting principles in the United States (“US GAAP”) and may not be comparable to financial statements of United States companies. We have availed of the exemption under SEC rules to prepare consolidated financial statements without a reconciliation to US GAAP as at and for the three year period ended December 31, 2011 as the Company is a foreign private issuer and the consolidated financial statements have been prepared in accordance with IFRS as issued by the International Accounting Standards Board.

In this annual report, all currency refers to US Dollars (US$) and all information is as of March 16, 2012 unless indicated otherwise.

Percentages and some amounts in this annual report have been rounded for ease of presentation. Any discrepancies between totals and the sums of the amounts listed are due to rounding.

Information contained in this annual report concerning the industry in which we operate has been obtained from publicly available information from third party sources (including Global Betting and Gaming Consultants, March 2009, or “GBGC”). Although we believe such information is reliable, we have not had such information verified by any independent source.

This annual report contains trade names, trademarks, registered marks, and service marks including DC Comics™, Superman™, Wonder Woman™, Marvel™, Jenga™, Batman™, Spider-Man™, The Hulk™, Paramount™, Braveheart™, and Forrest Gump™ belonging to us and other companies. All trademarks, trade names, registered marks, and service marks appearing in this annual report are the property of their respective holders.

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING INFORMATION

This annual report contains forward-looking statements within the meaning of Section 27A of the US Securities Act of 1933, as amended, and Section 21E of the US Securities Exchange Act of 1934, as amended, adopted pursuant to the Private Securities Litigation Reform Act of 1995. Statements that are not purely historical may be forward-looking, including statements regarding our expectations, objectives, anticipations, estimations, intentions, plans, hopes, beliefs, or strategies regarding the future. Such forward-looking statements include, but are not limited to:

| ● | the financial or business impact of new or amendments to legislation or regulation in individual countries or by multi-jurisdictional governmental organizations; |

| ● | the impact of the loss of key licensees; |

| ● | the success of Instant Click as a platform enabling deployment of titles from our suite of games; |

| ● | the ability to control our recurring cost base; |

| ● | the ability to expand the network of licensees and channel partners; |

| ● | the ability to expand our offerings to platforms to include mobile, and government licensed in-hotel room systems; |

| ● | the ability to leverage existing partnerships for potential future growth based upon both the brand recognition and loyalty associated with these partners and their unique and distinctive intellectual property; |

| ● | expected revenue growth from Branded Games and Hosted Casino licensing in 2012; |

| ● | potential new revenue sources in 2012 from gambling sites and new product launches; |

| ● | the impact of potential legal proceedings upon our business; and |

| ● | statements that include the words “may”, “will”, “plans”, “estimates”, “anticipates”, “believes”, “expects”, “intends” and other similar words. |

We cannot guarantee that any forward-looking statement will be realized, although we believe we have been prudent in our plans and assumptions. Achievement of future results is subject to risks, uncertainties, and potentially inaccurate assumptions. These risks and uncertainties include, among others, those discussed in “Item 3. Key Information – Risk Factors” of this annual report, (including without limitation, risks associated with i) existing and potential future changes to government regulation, ii) the current global financial condition, iii) legal proceedings, iv) foreign exchange fluctuations, and v) competition) as well as our consolidated financial statements, related Notes, and the other financial information appearing elsewhere in this annual report and our other documents we file with or furnish to the Securities and Exchange Commission. Should known or unknown risks or uncertainties materialize, or should underlying assumptions prove inaccurate, actual results could differ materially from past results and those anticipated, estimated or projected. You should bear this in mind as you consider forward-looking statements. We undertake no obligation to publicly update forward-looking statements, whether as a result of new information, future events, or otherwise.

PART I

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not Applicable.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not Applicable.

ITEM 3. KEY INFORMATION

SELECTED FINANCIAL DATA

The following financial information of our Company, expressed in US dollars unless otherwise indicated, is only a summary and should be read in conjunction with, and is qualified in its entirety by reference to, our audited annual consolidated financial statements and the related notes, which are included in this annual report. The selected historical financial data set forth below as of and for each of the years ended indicated has been derived from our consolidated financial statements.

| | | IFRS | | | IFRS | | | Canadian GAAP | | | Canadian GAAP | | | Canadian GAAP | |

| For the Years Ended December 31, | | 2011 | | | 2010 | | | 2009 | | | 2008 | | | 2007 | |

| (In thousands, except per share disclosure) | | | | | | | | | | | | | | | |

| Revenue | | $ | 27,253 | | | $ | 25,988 | | | $ | 39,794 | | | $ | 61,526 | | | $ | 73,659 | |

| Total comprehensive income/(loss) | | $ | 6,455 | | | $ | (21,621 | ) | | $ | (38,473 | ) | | $ | (35,414 | ) | | $ | 6,499 | |

| Basic earnings /(loss) per share | | $ | 0.47 | | | $ | (1.56 | ) | | $ | (2.78 | ) | | $ | (2.55 | ) | | $ | 0.47 | |

| Diluted earnings /(loss) per share | | $ | 0.47 | | | $ | (1.56 | ) | | $ | (2.78 | ) | | $ | (2.55 | ) | | $ | 0.47 | |

| Basic weighted average number of shares | | | 13,820 | | | | 13,820 | | | | 13,820 | | | | 13,888 | | | | 13,891 | |

| Diluted weighted average number of shares | | | 13,830 | | | | 13,820 | | | | 13,820 | | | | 13,888 | | | | 13,907 | |

| Total assets | | $ | 35,802 | | | $ | 37,545 | | | $ | 63,370 | | | $ | 105,806 | | | $ | 170,633 | |

| Total equity | | $ | 24,538 | | | $ | 18,041 | | | $ | 39,744 | | | $ | 78,822 | | | $ | 118,997 | |

| Share capital | | $ | 34,246 | | | $ | 34,129 | | | $ | 33,916 | | | $ | 33,552 | | | $ | 33,407 | |

| Dividends per share | | $ | – | | | $ | – | | | $ | 0.07 | | | $ | 0.39 | | | $ | 0.48 | |

| For the Years Ended December 31, | | 2009 | | | 2008 | | | 2007 | |

| (In thousands, except per share disclosure) | | | | | | | | | |

| Net earnings/(loss) | | $ | (39,632 | ) | | $ | (35,724 | ) | | $ | 6,611 | |

| Basic earnings/(loss)/ per share | | $ | (2.87 | ) | | $ | (2.57 | ) | | $ | 0.48 | |

| Diluted earnings/(loss)/ per share | | $ | (2.87 | ) | | $ | (2.57 | ) | | $ | 0.48 | |

RISK FACTORS

An investment in the Company involves significant risks. Accordingly, prospective investors should consider carefully the specific risk factors set out below in addition to the other information contained in this document before investing in the Company. Additional risks and uncertainties not presently known to CryptoLogic, or that the Board currently considers immaterial, may also affect the business, financial condition, results or future operations of the Company and the trading price of the Ordinary Shares. If any of the following risks materialize, the business, financial conditions, results or future operation could be materially and adversely affected. In such circumstances, the trading price of the Ordinary Shares could decline and investors could lose part or all of their investment. Before making any investment decision, prospective investors are advised to consult an independent adviser who specializes in advising upon investments.

Current and future legislation and court decisions may have a material impact on our operations and financial results

The Company and our licensees are subject to applicable laws in the jurisdictions in which they operate. The Company holds government licenses issued by Malta and Denmark to operate Internet gambling sites. Our Hosted Casino licensees and our Branded Games licensees hold similar licenses issued by various jurisdictions. Some countries have introduced regulations attempting to restrict or prohibit Internet gambling, while others have taken the position that Internet gambling should be regulated and have adopted or are in the process of considering legislation to enable that regulation.

While the United Kingdom (“UK”) and other European countries such as Malta and Gibraltar have adopted a regime which permits their licensees to accept wagers from any jurisdiction, other countries, including Italy, France, Spain and Denmark have, or are in the process of, implementing regimes which only permit the targeting of the domestic market provided a local license is obtained and local taxes accounted for. Other European territories continue to defend a licensing regime that protects monopoly providers and have combined this with an attempt to outlaw all other supplies. Either of these restrictive approaches may yet be deemed to be in potential conflict (in any specific jurisdiction) with European Union (“EU”) treaty law (governing the free movement of trade and services throughout the EU) and case law rendered by the European Court of Justice (the “ECJ”), but recent ECJ decisions have given EU Member States wide latitude in regulating the online gambling markets. Over the past several years, the European Commission (the “EC”) has attempted to prompt the introduction of directives that would harmonize online gambling within the EU, which is in line with the EC’s stated goal of encouraging a free and open cross-border market. In early 2011, the EC’s Internal Market Commissioner, Michel Barnier, began an EU-wide consultation and review process on online gambling regulation. Harmonization in the area of online gambling, however, has met with substantial opposition in the past, and there can be no certainty that the consultation and review will recommend such harmonization or that any recommendation of harmonization will be adopted. There is, therefore, no indication that any such harmonization will be achieved in the near term. Contemporaneous with its efforts to harmonize European online gambling laws, the EC has initiated infringement proceedings against various member states in relation to perceived breaches of Article 56 of the Treaty on the Functionality of the EU (which article enshrines the principle of freedom of movement of services), but in most cases these have not reached conclusion.

As companies and consumers involved in Internet gambling are located around the globe, including our licensees and their players, there is uncertainty regarding which government has authority to regulate or legislate the industry. The Unlawful Internet Gambling Enforcement Act (“UIGEA”), which is designed to prohibit payments relating to Internet gambling was enacted on October 13, 2006 in the United States, and similar legislation may be adopted in other jurisdictions.

Future legislative and court decisions may have a material impact on our operations and financial results. There is a risk that governmental authorities may view us or our licensees as having violated their local laws, despite CryptoLogic’s contractual requirement that each of its licensees is appropriately licensed to operate its Internet gambling business. Therefore, there is a risk that civil and criminal proceedings, including class actions brought by or on behalf of prosecutors or public entities, incumbent monopoly providers, or private individuals, could be initiated against us, our licensees, Internet service providers, credit card processors, advertisers and others involved in the Internet gambling industry. Such potential proceedings could involve substantial litigation expense, penalties, fines, seizure of assets, injunctions or other restrictions being imposed upon us or our licensees or other business partners, while diverting the attention of key executives. Such proceedings could have a material adverse effect on our business, revenues, operating results and financial condition as well as impact upon our reputation.

There can be no assurance that legally enforceable prohibiting legislation will not be proposed and passed in jurisdictions relevant or potentially relevant to our business to legislate or regulate various aspects of the Internet or the Internet gambling industry (or that existing laws in those jurisdictions will not be interpreted negatively). Compliance with any such legislation may have a material adverse effect on our business, financial condition and results of operations, either as a result of our determining that a jurisdiction should be blocked, or because a local license may be costly for us or our licensees to obtain and/or such licenses may contain other commercially undesirable conditions.

There have recently been a number of legal developments associated with the manner in which the business of gambling, and in particular, Internet gambling, is treated in the UK and Continental Europe. Some of these developments can be considered as positive and some as negative. In this regard a brief summary of the regulatory situation in the UK, Europe, and the United States follows:

United Kingdom

In September 2007, the UK Gambling Act came into force, which regulated online gambling for the first time in that jurisdiction. Most of the underlying codes in relation to entities established in the UK, or marketing into the UK have been enacted. However, there is no assurance that the UK regulatory regime as interpreted by the Gambling Commission, the Gambling Act’s independent regulator, will provide a commercially-viable market and may create restrictions that would have a material adverse effect on CryptoLogic’s customers, business, revenues, operating results and/or financial condition. Indeed, the Department of Culture Media and Sport (the “DCMS”) (the government body with responsibility for overseeing gambling), has announced that it may reconsider one of the main tenets of the Gambling Act, namely that if an online gambling operator were regulated either in Europe or in a jurisdiction approved by the DCMS (the so called “white listed” jurisdictions) such an operator could fully target the UK gambling market. The DCMS is in the process of conducting a review of online gambling and is expected to publish the results of this review in the next few months, and the minister responsible in the DCMS for gambling stated that the Government was aiming to file remote gambling legislation in the next parliamentary session. It seems likely that the DCMS will recommend that it will require entities not licensed in the UK to acquire some form of additional accreditation to access the UK market and/or pay taxes in the UK.

Continental Europe

France

The French law authorizing the licensing of online gambling operators came into effect in April 2010, and the first licenses were issued in June 2010. Licenses are currently available only in relation to poker games and sportsbook. The French authorities have adopted an aggressive enforcement stance against those operators that attempt to operate in France without a French license. Moreover, the licenses are subject to undesirable commercial terms, such as limits on maximum payouts and high levels of tax. Moreover, all poker play can only be amongst French customers, which severely impedes liquidity.

Germany

Online gambling was expressly prohibited in Germany by the State Gambling Treaty of 2008, under which an operator is liable to civil or administrative sanctions. Article 284 of the German Criminal Code, which applies criminal sanctions to operators who provide online gambling services into Germany without a form of authorization, has been the subject of legal debate over the purported breadth of its application.

Conflicting domestic court decisions on the legality of domestic law relating to online gambling (in light of the uncertainty of the application of Article 284 of the Criminal Code to online gambling businesses licensed outside of Germany, in particular by other EU member states, and the legality of the State Gambling Treaty under EU law) has led to uncoordinated enforcement action.

In September 2010, the ECJ handed down two judgments that call into question the enforceability of the State Gambling Treaty under EU law. Moreover, the State Gambling Treaty expired on 31 December 2011, requiring Germany to address again the issue of online gambling. Although fifteen of Germany’s sixteen regional governments agreed a new State Gambling Treaty that attempts to prohibit internet poker and casinos and imposes a tax regime considered unattractive by many operators, the regional government of Schleswig-Holstein has introduced its own licensing regime which attempts to offer an unlimited number of licenses in betting, casino and poker, with a more attractive tax regime. The divergence between Schleswig-Holstein and the other fifteen regions has created uncertainty as to the status of the regulation of online gambling in Germany. In addition, the new State Gambling Treaty may also be subject to challenge in the ECJ. There can be no certainty, therefore, as to what form regulation of online gambling in Germany will take, and whether Germany will continue to ban online gambling or provide licensing of online gambling, nor can there be any certainty as to the terms of licensing (or commercial viability of any license) in the event that licensing is implemented throughout Germany.

Italy

Italy introduced a licensing regime in 2010, which allows licenses for online casino games as well as sports betting and poker. The administrative, technical, tax and financial burdens, however, associated with these licenses are high. Moreover, there can be no guarantee that the Company's licensees will be successful in obtaining an Italian license, nor that the Company's games will be approved under the Italian licensing regime. The Company and its licensees remain at risk that

Italy may take aggressive action against parties whose operations are not licensed pursuant to the regulatory regimes established by Italy.

Spain

In May 2011, Spain approved a new online gambling licensing regime which licenses online casinos and poker, but not online slot machine-type games, and imposes taxes and fees on the operators. The Company and its licensees remain at risk that Spain may take aggressive action against parties whose operations are not licensed in Spain.

The Netherlands

The Dutch government has consistently taken steps to support and protect its state-sponsored casino operator’s (Holland Casino) monopoly, including taking legal action against Internet gambling operators. In addition, an announcement in 2009 by the Dutch Minister of Justice to the effect that payment support by Dutch banks of online gambling was unlawful (and precluded by existing law) caused a number of operators to be blocked from the territory. This cautious approach has been further exacerbated by the judgment of the ECJ in June 2010, following the negative opinion of Advocate General Bot, upholding the Dutch regulations as not inconsistent with EU law, in the case referred to the ECJ by Betfair and Ladbrokes. In the event that the Dutch courts implement the ECJ decision and the government seeks to take further steps to protect the online business of Holland Casino by discouraging other operators from operating in the Dutch marketplace, either through changes in legislation or enforcement measures, the Company and its licensees could be adversely impacted. In March 2011, the Dutch government announced proposals to grant licenses for Internet gambling in the Netherlands and, in December 2011, the Dutch parliament passed a bill establishing a new Dutch Gaming Authority to be operational from April 2012. Nevertheless, these proposals to license Internet gambling are at a preliminary stage and subject to the Dutch parliament’s approval. Therefore, there can be no guarantee that the Dutch government will implement a licensing regime or that the terms of such licenses, including the tax and technical requirements thereof, would create commercially viable conditions for online operators.

Scandinavia

Governments in most Scandinavian countries have attempted to discourage their citizens from gambling with online operators by taxing their citizens’ winnings. Generally speaking, winnings realized through a state sponsored operator are not taxable, but winnings from other sources can be subject to inconsistent application of taxation law in relation to domestic and non-domestic products in the EU Until such time as the tax authorities in the various countries make an official pronouncement on the manner in which these tax laws will be applied, it is unclear as to what impact these tax policies will have on the business of the Company or its licensees. In Norway, the government has specifically banned payment support of online gambling which came into force in 2010. The ban means only payment support of state-owned gambling services will remain legal. Sweden prohibits advertising by foreign gambling operators. In Denmark, the Danish parliament has approved a licensing regime for online gambling, which came into effect on January 1, 2012. The Company applied for and received a Danish license, effective January 1, 2012. However, there can be no guarantee that the Company's licensees will also be successful in obtaining a Danish license, nor that the Danish licensing regime or the terms of such licenses, including the tax and technical requirements thereof, will remain commercially viable for online operators.

United States

Since the enactment of UIGEA in October 2006, the Company has prohibited its licensees from taking any wagers from US residents. UIGEA sought to clarify the illegality of processing or transferring any funds connected with unlawful Internet gambling, although some US enforcement agencies claimed that previous existing legislation similarly outlawed these activities. Given that the Company had previously derived licensing revenue and provided payment processing solutions (through its e-cash services) on behalf of some licensees who took wagers from the US, there is no guarantee that the US Department of Justice will not seek to prosecute the Company, its officers or directors for alleged historical transgressions or similarly prosecute its licensees or their directors or shareholders. Such proceedings could result in criminal penalties, substantial fines, damages and sequestration of assets. They also could damage the reputation of the Company, divert the attention of the Company’s key executives and have a material adverse effect on the business, revenues, operating results and/or financial condition of the Company. Although there have been a number of recent proposals in various states for intra-state only online gambling licensing regimes, there can be no guarantee that any such proposals will ultimately be successful and there remain doubts as to the compatibility of such a regime with federal law. Moreover, such limited markets or the terms and conditions of such proposed licensing regimes, may not be commercially viable for online operators.

The loss of a major payment option could limit our ability to accept deposits.

With the enactment of UIGEA, financial institutions in the US ceased to accept online gambling transactions. There can be no assurance that other financial institutions or credit card issuers outside the US will not enact additional restrictions. The

loss of a major payment option would have a material adverse effect on our business, revenues, operating results and financial condition.

There can be no assurance that the systems and protective measures we have in place will or can guarantee protection against fraudulent activities and unauthorized access from minors.

There can be no assurance that the systems and protective measures we have in place will or can guarantee protection against fraudulent activities and unauthorized access from minors, which could have a material adverse effect on our reputation, business, revenue, operating results and financial conditions. We attempt to mitigate these concerns with systematic controls and a dedicated anti-fraud team.

In addition to regulations pertaining specifically to online gambling, we may become subject to any number of laws and regulations that may be adopted with respect to the Internet and electronic commerce.

In addition to regulations pertaining specifically to online gambling, we may become subject to any number of laws and regulations that may be adopted with respect to the Internet and electronic commerce. New laws and regulations that address issues such as user privacy, pricing, online content regulation, taxation, advertising, intellectual property, information security, and the characteristics and quality of online products and services may be enacted. As well, current laws, which predate or are incompatible with the Internet and electronic commerce, may be applied and enforced in a manner that restricts the electronic commerce market. The application of such pre-existing laws regulating communications or commerce in the context of the Internet and electronic commerce is uncertain. Moreover, it may take years to determine the extent to which existing laws relating to issues such as intellectual property ownership and infringement, libel and personal privacy are applicable to the Internet.

The adoption of new laws or regulations relating to the Internet, or particular applications or interpretations of existing laws, could decrease the growth in the use of the Internet, decrease the demand for our products and services, increase our cost of doing business or could otherwise have a material adverse effect on our business, revenues, operating results and financial condition.

Current global financial conditions have been characterized by increased volatility and several financial institutions have either gone into bankruptcy or have had to be rescued by governmental authorities. Access to public financing has been negatively impacted by both the rapid decline in the value of sub-prime mortgages and the liquidity crisis affecting the asset-backed commercial paper market.

Current global financial conditions have been characterized by increased volatility and several financial institutions have either gone into bankruptcy or have had to be assisted by governmental authorities. Access to public financing has been negatively impacted by both the rapid decline in value of sub-prime mortgages and the liquidity crisis affecting the asset-backed commercial paper market. As a result, several major economies have been in prolonged recessions, including but not limited to, the United Kingdom, as well as Ireland, where the Company is headquartered. If these economies do not recover in a timely manner, future revenues may be adversely impacted. Secondly, the disruption to the global finance markets may impact the ability of the Company to obtain equity or debt financing in the future on terms favorable to the Company, if at all. If such increased levels of volatility and market turmoil continue, the Company’s operations could be adversely impacted and the trading price of the Ordinary Shares may be adversely affected.

There can be no assurance that the Internet infrastructure or the Company’s own network systems will continue to be able to support the demands placed on it by the continued growth of the Internet, the overall online gambling industry or of our customers.

The growth of Internet usage has caused frequent interruptions and delays in processing and transmitting data over the Internet. There can be no assurance that the Internet infrastructure or the Company’s own network systems will continue to be able to support the demands placed on it by the continued growth of the Internet, the overall online gambling industry or of our customers.

The Internet’s viability could be affected if the necessary infrastructure is not sufficient, or if other technologies and technological devices eclipse the Internet as a viable channel.

End-users of our software depend on Internet Service Providers (“ISPs”), online service providers and our system infrastructure for access to the Internet gambling sites operated by the Company and our licensees. Many of these services have experienced service outages in the past and could experience service outages, delays and other difficulties due to system failures, stability or interruption. The Company and/or our licensees may lose customers as a result of delays or interruption in service, including delays or interruptions relating to high volumes of traffic or technological problems. As a result, we

may not be able to meet service levels that we have contracted for, putting us in breach of contractual commitments, which in turn could materially adversely affect our business, revenues, operating results and financial condition.

The demand and acceptance for new products and services are subject to a level of uncertainty and growing competition.

The Internet gambling industry continues to evolve rapidly. The demand and acceptance for new products and services are subject to a level of uncertainty and growing competition, and if our services do not continue to receive market acceptance, our business, revenues, operating results and financial condition could be materially adversely affected.

Our Internet gambling software and electronic commerce services are reliant on technologies and network systems to handle transactions and user information securely over the Internet, which may be vulnerable to system intrusions, unauthorized access or manipulation.

Our Internet gambling software and electronic commerce services are reliant on technologies and network systems to handle transactions and user information securely over the Internet, which may be vulnerable to system intrusions, unauthorized access or manipulation. As increasingly sophisticated and new ways to commit fraud are devised, our security and network systems may be tested and subject to attack. We have experienced such system attacks in the past and implemented measures to protect against these intrusions. However, there is no assurance that all such intrusions or attacks will or can be prevented in the future, and any system intrusion/attack may cause a delay, interruption or financial loss, which could have a material adverse effect on our business, revenue, operating results and financial condition.

If ISPs experience service interruptions, communications over the Internet may be interrupted and impair our ability to carry on business.

Our electronic commerce product relies on ISPs to allow our and our licensees’ customers and servers to communicate with each other. If ISPs experience service interruptions, communications over the Internet may be interrupted and impair our ability to carry on business. In addition, our ability to process e-commerce transactions depends on bank processing and credit card systems. Any system failure as a result of reliance on third parties, including network, software or hardware failure, which causes a delay or interruption in our e-commerce services could have a material adverse effect on our business, revenues, operating results and financial condition.

The Company and the licensees of our software and services compete with existing and established recreational services and products, in addition to other forms of entertainment.

The Company and the licensees of our software and services compete with existing and established recreational services and products, in addition to other forms of entertainment. Our success will depend, in part, upon our ability to keep pace with technological developments, respond to evolving customer requirements and achieve continued market acceptance.

We compete with a number of public and private companies, which provide electronic commerce and/or Internet gambling software. In addition to known current competitors, traditional land-based casino operators and other entities, many of which have significant financial resources, an entrenched position in markets and name-brand recognition, may provide Internet gambling services in the future, and thus become our competitors. As well, such companies may be able to require that their own software, rather than the software of others, including our gambling software or our e-cash systems and support, be used in connection with their payment mechanisms.

The barriers to entry into most Internet markets are relatively low, making them accessible to a large number of entities and individuals.

Increased competition from current and future competitors has and may in the future result in price reductions and reduced margins, or may result in the loss of our market share, any of which could materially adversely affect our business, revenues, operating results and financial condition.

In fiscal 2011, our top 7 licensees accounted for approximately 80% (2010: 81%) of our total revenue before amortization. In addition, all our key licensees operate from a limited number of licensing jurisdictions.

In fiscal 2011, our top 7 licensees accounted for approximately 80% (2010: 81%) of our total revenue before amortization. In addition, all our key licensees operate from a limited number of licensing jurisdictions. The loss of one or more of these key licensees, or the loss of their license to operate in the limited number of licensing jurisdictions, could have a material adverse effect on our business, revenues, operating results and financial condition.

Contracts are subject to renewal, renegotiation and may be contingent on certain performance requirements. There can be no assurance that license agreements will be renewed or that there will not be a material change in the terms of the contracts, which could adversely affect our business, revenues, operating results and financial condition.

Licensing contracts generally have multi-year terms and have renewal provisions, which provide us with a long-term ongoing revenue stream. Contracts are subject to renewal, renegotiation and may be contingent on certain performance requirements. There can be no assurance that license agreements will be renewed or that there will not be a material change in the terms of the contracts, which could adversely affect our business, revenues, operating results and financial condition.

Similar issues exist in respect of brand licensing agreements. Our Branded Games business is dependent on our ability to continue to incorporate into our Branded Games the intellectual property licensed to us by brand licensors, such as Marvel Comics, DC Comics, a division of Warner Bros., and Paramount Digital Entertainment. There can be no assurance that key brand license agreements will be renewed or that there will not be a material change in the terms of the contracts, which could adversely affect our business, revenues, operating results and financial condition.

Disputes may also develop with respect to contracts with other parties, including licensees, brand licensors or games development companies, which, if resolved unfavorably to the Company, could adversely affect our business, revenues, operating results and financial conditions.

We are subject to exposure in regard to chargebacks, which may also result in possible penalties and elimination of payment options.

We are subject to exposure in regard to chargebacks, which may also result in possible penalties and elimination of payment options. Chargebacks refer to any deposit transaction credited to a user’s account that is later reversed or repudiated. While the Company has various control measures which seek to minimize exposure to chargebacks, it is not possible entirely to eliminate or prevent chargebacks, and a materially increased incidence of chargebacks could have a material adverse effect on our business, revenues, operating results and financial conditions.

There are certain difficulties and risks inherent in doing business internationally, including the burden of complying with multiple and conflicting regulatory requirements, foreign exchange controls, potential restrictions or tariffs on gambling activities that may be imposed.

There are certain difficulties and risks inherent in doing business internationally, including the burden of complying with multiple and conflicting regulatory requirements, foreign exchange controls, potential restrictions or tariffs on gambling activities that may be imposed, potentially adverse tax consequences and tax risks, and changes in the political and economic stability, regulatory and taxation structures, and the interpretation thereof, of jurisdictions in which we and our licensees operate, and in which our and our licensees’ customers are located, all of which could have a material adverse effect on our business, revenues, operating results and financial condition.

There can be no assurance that we will be able to sustain or increase revenue derived from international operations or that we will be able to penetrate linguistic, cultural or other barriers to new foreign markets.

Fluctuations in the exchange rate of world currencies could have a negative effect on our reported results.

Our financial results are reported in US dollars, which is subject to fluctuations as against the value of the currencies in which we operate, including British pounds, euro, and Canadian dollars. Fluctuations in the exchange rate of world currencies could have a negative effect on our reported results. There can be no assurance that we will not experience currency losses in the future, which could have a material adverse effect on our business, revenues, operating results and financial condition.

Our effective tax rate in the future could be adversely affected by changes in the mix of earnings in countries with differing statutory tax rates, changes in the valuation of deferred tax assets and liabilities and changes in tax laws.

We are subject to income taxes in Ireland, Canada, Cyprus, Malta and other jurisdictions. Our tax calculations involve estimates in several areas including, but not limited to, transfer pricing. Tax authorities may disagree with our estimates and assess additional taxes, which could have a material adverse effect on our results and financial condition. In addition, our effective tax rate in the future could be adversely affected by changes in the mix of earnings in countries with differing statutory tax rates, changes in the valuation of deferred tax assets and liabilities and changes in tax laws. In particular, the carrying value of future tax assets is dependent on our ability to generate future taxable income in the jurisdiction where we have recognized the deferred tax assets.

We may be involved in litigation arising in the ordinary course of business. The outcome of such matters cannot be predicted with certainty, and could have a material adverse effect on our business, revenues, operating results and financial condition.

We are involved in litigation arising in the ordinary course of business. The outcome of such matters cannot be predicted with certainty, and could have a material adverse effect on our business, revenues, operating results and financial condition.

Moreover, from time to time, third parties have asserted and may continue to assert patent, trademark, copyright and other intellectual property rights to technologies or business methods that we consider important. There can be no assurance that the assertion of such claims will not result in litigation or that we would prevail in any such litigation or be able to obtain a license for the use of any infringed intellectual property from a third party or, if such a license is required, that it would be available on terms acceptable to us.

In December 2010, a significant supplier of games delivered to the Company a notice of arbitration relating to the agreement between the two companies. In February 2011, the Company delivered to the supplier a notice of termination of the agreement, to take effect from March 2011. Notwithstanding this termination, in April 2011, a non-binding memorandum of understanding setting out a commercially acceptable solution was signed between the parties with the aim of concluding a binding agreement. In June 2011, such binding agreement was concluded and signed.

In February 2011, a brand licensor delivered to the Company a notice purporting to terminate the brand license agreement between the two companies, claiming that the Company had breached such agreement. In May 2011, the brand licensor reaffirmed its position that the brand license agreement is terminated. The Company believes there is no breach that warrants termination of the agreement. In June 2011, the Company filed suit against the brand licensor seeking judgment that any breach was cured and the agreement remains in force. In October 2011, the brand licensor answered the complaint, denying any cure and filed a countersuit seeking monetary damages for the alleged breach of the agreement and a declaration that the agreement has been terminated. This litigation is ongoing.

Our competitive position is dependent in part upon our ability to protect our proprietary technology.

We rely on a combination of laws and contractual provisions to establish and protect our rights in our software and proprietary technology. We believe that our competitive position is dependent in part upon our ability to protect our proprietary technology. We regard our source code as proprietary information, trade secrets and unpublished copyrighted works. Despite our precautions and measures implemented to protect against such attempts, unauthorized parties may have or could in the future copy or otherwise reverse engineer portions of our products or otherwise obtain and use information that we regard as proprietary.

Our Company has patents and trademarks in certain jurisdictions and is in the process of applying for further trademark registrations and patents, which may provide such protection in relevant jurisdictions. However, there can be no assurance that this will be sufficient to protect our proprietary technology fully. In addition, certain provisions of our license agreements, including provisions protecting against unauthorized use, transfer and disclosure, may be found to be unenforceable in certain jurisdictions.

We also have a proprietary interest in our name. The names “CryptoLogic” and “WagerLogic” have become known in the Internet gambling industry. Accordingly, our competitive position could be affected if our name were misappropriated and our reputation in any way compromised.

There can be no assurance that the steps we have taken to protect our proprietary rights will be adequate to deter misappropriation of our technology or independent development by others of technologies that are substantially equivalent or superior to our technology. Any misappropriation of our name, technology or development of competitive technologies could have a material adverse effect on our business, revenues, operating results and financial condition.

We may infringe upon the intellectual property rights of third parties.

Due to the complex, sophisticated and global nature of the business, there can be no assurance that there has been no breach of third parties’ intellectual property rights by the Company, and any adverse judgment in this regard could have a material adverse effect on our business, revenues, operating results and financial condition.

Our future success is dependent on certain key management and technical personnel.

Our future success is dependent on certain key management and technical personnel. The loss of these individuals or the inability to attract and retain highly qualified employees and advisors could have a material adverse effect on our business, revenues, operating results and financial condition.

Our future success is dependent on the ability to retain and hire personnel.

Our future success is dependent on the ability to retain and hire personnel. In March 2011, the Company announced the appointment of Deloitte Corporate Finance to act as its independent financial adviser to assist it with a strategic review encompassing a range of options available to the Company from continuing as an independent entity through to the sale of part or all of its business, as well as to provide advice with respect to any potential transaction. In February 2012, a recommended cash offer from Amaya Gaming Group Inc. for the entire issued and to be issued share capital of CryptoLogic was announced at a price of $2.535 per Ordinary Share.

The strategic review process and the announcement of an offer for the Company, may create uncertainty amongst personnel. The ability of the Company to retain such personnel or to hire replacement personnel should certain personnel depart may be adversely affected by such uncertainty, which could have a material adverse effect on our business, revenues, operating results and financial condition.

The challenges of our business and the increasing complexity of our product offerings, coupled with the rapid evolution of our markets, are expected to continue to place a significant strain on our management and operational resources and to increase demands on our internal systems, procedures and controls.

The challenges of our business and the increasing complexity of our product offerings, coupled with the rapid evolution of our markets, are expected to continue to place a significant strain on our management and operational resources and to increase demands on our internal systems, procedures and controls. Our future operating results will depend on management’s ability to develop and manage growth, enhance our products and services to respond to market demand, deal with competition and evolving customer requirements, manage our system infrastructure and requirements to meet the growing demands of our business, hire and retain significant numbers of qualified employees, accurately forecast revenues and control expenses. A decline in our revenues without a corresponding and timely slowdown in our expenses, or our inability to manage or build future growth efficiently, could have a material adverse effect on our business, revenues, operating results and financial condition.

The market price of our Ordinary Shares has experienced significant fluctuation and may continue to fluctuate significantly.

The market price of our Ordinary Shares has experienced significant fluctuation and may continue to fluctuate significantly. The market price of our Ordinary Shares may be adversely affected by various factors, such as proposed Internet gambling legislation or enforcement of existing laws, the loss of a customer, the announcement of new products or enhancements, innovation and technological changes, quarterly variations in revenue and results of operations, changes in earnings estimates by financial analysts, speculation in the press or analyst community and general market conditions or market conditions specific to particular industries, including the Internet and gambling.

In addition, the stock market has from time to time experienced extreme price and volume fluctuations. These company-specific or broad market fluctuations may adversely affect the market price for our Ordinary Shares. Anti-online gambling legislation could also impact our ability to remain listed.

Although our Ordinary Shares are listed and traded on the Toronto Stock Exchange, the NASDAQ Global Select Market and the London Stock Exchange’s Main Market, this should not imply that there will always be a liquid market in our Ordinary Shares. In addition, pursuant to the Arrangement, Exchangeable Shares were issued, and are listed and traded on the Toronto Stock Exchange. Because of separate listings, the trading prices of the Ordinary Shares and Exchangeable Shares may not reflect equivalent values. Company-specific or broader market fluctuations may adversely affect the market price of the Exchangeable Shares, and there can be no assurance that there will continue to be an active market for these securities.

In February 2012, a recommended cash offer from Amaya Gaming Group Inc. for the entire issued and to be issued share capital of CryptoLogic was announced at a price of $2.535 per Ordinary Share. The offer is conditional upon, inter alia, valid acceptances being received by March 28, 2012 in respect of more than 50% in value of CryptoLogic’s issued share capital and more than 50% of the voting rights attached to CryptoLogic’s issued share capital. In the absence of the offer completing, the market price of the Ordinary Shares and Exchangeable Shares may be adversely affected.

The Company is subject to listing requirements in respect of its listings on the NASDAQ Global Select Market, the Toronto Stock Exchange and the London Stock Exchange Main Market and, in the absence of compliance with all such listing requirements, may face delisting action with consequent reduction in markets available for its Ordinary Shares to trade.

The Company is subject to listing requirements in respect of its listings on the NASDAQ Global Select Market, the Toronto Stock Exchange and the London Stock Exchange Main Market and, in the absence of compliance with all such listing requirements, may face delisting action with consequent reduction in markets available for its Ordinary Shares to trade.

Under NASDAQ’s continued listing requirements, a security is considered deficient if it fails to achieve at least a $1.00 closing bid price for a period of 30 consecutive business days. Global Market issuers are provided one automatic 180-day period to regain compliance. An issuer can regain compliance by achieving a $1.00 closing bid price for a minimum of ten consecutive business days. The Company’s closing bid price on NASDAQ was below $1.00 between March 1, 2011 and March 18, 2011.

Under NASDAQ’s continued listing requirements, an issuer is required to have an audit committee consisting of at least three independent directors. Upon Mr. Gavagan’s appointment as Interim Chief Executive Officer, he was no longer considered independent and, accordingly, the Company did not have three independent directors. The Company reported to NASDAQ that the audit committee comprised only two members. The Company, under NASDAQ continued listing requirements, rectified this situation at the Annual General Meeting held in June 2011 with the appointment of a third independent director.

The Company incurred significant operating losses and negative cash flows from operations for the three years to December 31, 2010, which resulted in a decrease in cash and cash equivalents in each year. A reoccurrence of such operating losses, negative cash flows from operations and decreases in cash and cash equivalents may cast doubt upon the Company's ability to continue as a going concern.

The consolidated financial statements were prepared on a going concern basis. The going concern basis assumes that the Company will continue in operation for the foreseeable future and will be able to realize its assets and discharge its liabilities and commitments in the normal course of business.

The Company incurred significant operating losses and negative cash flows from operations for the three years to December 31, 2010, which resulted in a decrease in cash and cash equivalents in each year. A reoccurrence of such operating losses, negative cash flows from operations and decreases in cash and cash equivalents may cast doubt upon the Company's ability to continue as a going concern.

During 2010, management determined that a material reduction in expenses was necessary in order to preserve cash and give the Company sufficient time to focus on increasing revenues. Accordingly, the Company made a significant restructuring effort resulting in a reduction in operating and general and administrative expense, an operating profit and positive cash flows from operations for the year ended December 31, 2011. However, the Company may incur further operating losses and negative cash flows in future periods and, if its cash resources and financing options are insufficient, its ability to operate would be adversely impacted.

ITEM 4. INFORMATION ON THE COMPANY

A. HISTORY AND DEVELOPMENT OF THE COMPANY

The Company originally was formed by articles of amalgamation under the Business Corporations Act (Ontario) effective March 7, 1996 pursuant to an amalgamation agreement dated January 19, 1996 between Inter.tain.net Inc., a private corporation, and Biroco Kirkland Mines Limited. Immediately prior to the amalgamation, Biroco Kirkland Mines Limited did not carry on active operations. On June 28, 1996, we changed our name from “Inter.tain.net Inc.” to “CryptoLogic Inc.” Currently, the Company operates under the name “CryptoLogic Limited”.

On June 1, 2007, in order to advance its global strategy, the Company moved its headquarters from Canada to the Republic of Ireland by forming a new parent company, CryptoLogic, a company incorporated under the laws of Guernsey with its place of business in Dublin, Ireland. This business reorganization was implemented by way of the Arrangement. CryptoLogic acquired control over all of the issued and outstanding common shares of CryptoLogic Inc., which through the Arrangement, became an indirect subsidiary of CryptoLogic.

In February 2011, the Company appointed Deloitte Corporate Finance to act as its independent financial adviser to assist it with a strategic review encompassing a range of options available to the Company from continuing as an independent entity through to the sale of part or all of its business, as well as to provide advice with respect to any potential transaction. During 2011, in connection with the strategic review, a number of parties contacted or were contacted by Deloitte Corporate Finance. In February 2012, a recommended cash offer from Amaya Gaming Group Inc. for the entire issued and to be issued share capital of CryptoLogic was announced at a price of $2.535 per Ordinary Share, a premium of approximately 110% to the closing price of $1.21 per Ordinary Share on NASDAQ on March 24, 2011, the day prior to the announcement of the strategic review.

In January 2012, the Company announced that it had acquired, for nominal consideration, the Maltese online gambling licenses for InterCasino from OIGE, the Company’s largest and longest-standing Hosted Casino licensee, resulting in the Company becoming an online casino owner. Our registered office is at 11 New Street, St. Peter Port, Guernsey, GY1 2PF. Our head office is located at Marine House, Clanwilliam Place, Dublin 2, Ireland, and our telephone number is +353 1 234 0400.

Our head office provides executive and administrative functions to our corporate group. Our subsidiaries, including WagerLogic companies and Gaming Portals, through their offices in Ireland, Malta and the UK, provide software, licensing, e-cash systems and support, customer support and marketing support services for our Internet gambling software to third-party gambling operators. Our Toronto, Canada office provides software development, upgrades and technical support for WagerLogic.

B. BUSINESS OVERVIEW

CryptoLogic is a publicly traded online gambling software developer and supplier servicing the Internet gambling market. CryptoLogic, through its wholly-owned subsidiaries, provides software licensing, e-cash management and customer support services for our Internet gambling software to an international client base (“licensees” or “customers”) around the world, who operate under government authority where their Internet businesses are licensed.

Founded in 1995, the Company launched the world’s first online casino games that year. With a resilient and scalable platform, a commitment to developing the best games in the marketplace and complemented with excellent customer support, the Company thereafter secured an excellent reputation for its product offering.

The enactment in the United States of the Unlawful Internet Gambling Enforcement Act in late 2006, which effectively banned online gambling in the United States by making it illegal to process the related financial transactions, had a very significant negative impact on the Company’s revenue. The Company sought to grow its business internationally and, from 2009, launched a new business model, centered on the Company evolving from purely a developer and licensor of Internet gambling software on its own network, to one which still develops and licenses an excellent casino product, but also delivers high-quality, Branded and non-Branded Games to the industry at large.

The Company faced substantial ongoing challenges in 2010 as it continued its strategy aimed at returning to profitability and long-term growth against the backdrop of a global economic downturn, continuing disappointing returns from major Hosted Casino licensees and licensee delays in the roll-out of Branded Games.

By Q1 2010, the Company had incurred eight continuous quarters of significant operating losses and negative cash flows. Against this backdrop of a continuing decline in revenues and working capital, management determined that a material reduction in expenses was necessary in order to preserve cash and give the Company sufficient time to focus on increasing revenues. Accordingly, the Company made a significant restructuring effort, commencing midway through Q3 2010, and resulting in a reduction of almost 50% in operating and general and administrative expense to $6.2 million in Q4 2010 from $12.1 million in Q2 2010, the last full quarter before this restructuring.

The focus on cost control continued into 2011 with operating and general and administrative expense averaging $5.8 million per quarter during the year. The breathing space afforded by the restructuring allowed the Company to arrest the decline in revenues, resulting in the Company reporting, as further analyzed below:

| ● | its first annual increase in revenues since 2006; |

| ● | a turnaround in results from a reported loss of $21.6 million in 2010 to a reported profit of $6.5 million in 2011; and |

| ● | an increase in cash and cash equivalents during the year from $10.6 million to $16.6 million. |

In February 2011, the Company appointed Deloitte Corporate Finance to act as its independent financial adviser to assist it with a strategic review encompassing a range of options available to the Company from continuing as an independent entity through to the sale of part or all of its business, as well as to provide advice with respect to any potential transaction. During 2011, in connection with the strategic review, a number of parties contacted or were contacted by Deloitte Corporate Finance. In February, 2012, a recommended cash offer from Amaya Gaming Group Inc. for the entire issued and to be issued share capital of CryptoLogic was announced at a price of $2.535 per Ordinary Share, a premium of approximately 110% to the closing price of $1.21 per Ordinary Share on NASDAQ on March 24, 2011, the day prior to the announcement of the strategic review.

In January 2012, the Company announced that it had acquired, for nominal consideration, the Maltese online gambling licenses for InterCasino from OIGE, the Company’s largest and longest-standing Hosted Casino licensee, resulting in the Company becoming an online casino owner.

We currently market our technology and services through a select sales and marketing strategy whereby we identify key potential customers that meet our licensee profile, and then contact such prospects directly. We also attend industry trade shows around the world to generate new prospects, and respond to referrals from existing customers and other industry participants. CryptoLogic has generally sought licensees with an established brand, an audience with a propensity to gamble, and sufficient resources and commitment to successfully market the business.

In Hosted Casino and Branded Games, the key to success is differentiation through the combination of our new and innovative games and effective marketing to players by our licensees. Additionally, in Hosted Casino, a robust e-wallet with multiple payment options is key.

REVENUE SOURCES

Revenue increased 4.9% to $27.3 million for the year ended December 31, 2011 when compared with the same period in the prior year (2010: $26.0 million).

Fees and licensing revenue from both our Hosted Casino and Branded Games businesses are calculated as a percentage of a licensee’s level of activity in its online casino site. This is affected by the number of active players on the licensee’s site and their related gambling activity. In addition, these results are influenced by a number of factors such as the entertainment value of the games developed by CryptoLogic, the frequency and success of new game offerings and the effectiveness of the licensee’s marketing programs. Hosted Casino and Branded Games revenue are also impacted by the relative value of the US dollar to both the euro and the British pound as our licensees provide online casinos in these currencies for which we earn a percentage that is translated into US dollars, our functional currency.

Hosted Casino

Hosted Casino revenue increased 6.5% to $23.4 million for the year ended December 31, 2011 when compared with the same period in the prior year (2010: $22.0 million). Hosted Casino revenue represented 85.9% of total revenue in the year ended December 31, 2011 (2010: 84.6%).

The increase in revenue in the year ended December 31, 2011 is primarily due to an increase in contribution from a major licensee of $0.5 million and an increase in jackpot revenue of $1.4 million, including a revision of our estimate to discharge future jackpot payouts of $0.9 million, and a reduction of $0.3 million in liabilities previously provided against Hosted Casino revenue through the resolution of a dispute with a significant supplier of games. The relative value of the US dollar positively impacted Hosted Casino revenue by $0.7 million when compared with the same period in the prior year.

Branded Games

Branded Games revenue increased 24.8% to $6.9 million for the year ended December 31, 2011 when compared with the same period in the prior year (2010: $5.5 million). Branded Games revenue represented 25.2% of total revenue in the year ended December 31, 2011 (2010: 21.1%). During the year ended December 31, 2011, the Company’s revenue producing games increased from 170 to 212 games. The increase in Branded Games revenue is primarily due to the increased number of revenue producing games through an increased number of licensees and games per licensee and a reduction of $0.5 million in liabilities previously provided against Branded Games revenue through the resolution of a dispute with a significant supplier of games, partially offset by a lower contribution from a major licensee. The relative value of the US dollar positively impacted Branded Games revenue by $0.2 million when compared with the same period in the prior year.

Poker

The Company offers a virtual poker room for its licensees using software and technology provided on GTECH Corporation’s International Poker Network. Fees from online poker are based on a percentage of the licensee’s rake per hand in regular or ring games (the rake is typically 5% of the pot, up to a maximum amount per hand), or fixed entry fees for entry into poker tournaments.

Poker revenue decreased 46.8% to $0.9 million in the year ended December 31, 2011 when compared with the same period in the prior year (2010: $1.6 million). Poker revenue represented 3.2% of total revenue in the year ended December 31, 2011 (2010: 6.3%). The decrease in Poker revenue is primarily due to a reduction in contribution from a major licensee. The relative value of the US dollar did not have a material impact on Poker revenue when compared with the same period in the prior year.

Other revenue includes fees for software customization, and advertising and marketing services generated from our portal business.

Other revenue decreased 69.5% to $0.3 million for the year ended December 31, 2011 when compared with the same period in the prior year (2010: $1.1 million). Other revenue represented 1.2% of total revenue in the year ended December 31, 2011 (2010: 4.4%). The decrease in Other revenue is due to a one-time termination fee from a licensee in Q1 2010. The relative value of the US dollar did not have a material impact on Other revenue when compared with the same period in the prior year.

Amortization of Royalties

The Company licenses various royalty rights from several owners of intellectual property rights. These rights are used to produce games for use in Hosted Casino and Branded Games. Generally, the arrangements require material prepayments of minimum guaranteed amounts which have been recorded as prepayments. These prepaid amounts are amortized over the life of the arrangement as gross revenue is generated or on a straight-line basis if the underlying games are expected to have an effective royalty rate greater than the agreed amount. The amortization of these amounts is recorded as a reduction in revenue.

Amortization of royalties increased 11.4% to $3.4 million for the year ended December 31, 2011 when compared with the same period in the prior year (2010: $3.1 million). Amortization of royalties represented (12.6%) of total revenue in the year ended December 31, 2011 (2010: (11.9%)). The increase in royalty amortization was as a result of the Company’s regular review of estimates of future revenue under its license arrangements which identified in Q2 2010 that it was appropriate to begin amortizing certain of these royalties on a straight-line basis, such that substantially all of these royalty payments are amortized on a straight-line basis.

Player Restrictions

No revenue is derived from US based players.

Revenue Trends

The global economic downturn is impacting the Company’s business.

While the global online gambling market continues to promise growth potential, competition is intensifying for players and market position.

It is expected that increased regulation of online gambling in key markets will also impact the Company’s business in the future.

Recurring Revenue

CryptoLogic’s licensing fees reflect a revenue model based on building long-standing relationships with customers. In 2011, 99.8% (2010: 96.2%) of CryptoLogic’s fee revenue before amortization was generated from software licensing and services contracts that generate recurring revenue.

Geographical analysis of revenue before amortization is made according to the jurisdiction of the gambling license of the licensee. This does not reflect the region of the end users of the Company’s licensees.

| For the Years Ended December 31, | | 2011 | | | 2010 | |

| Malta | | | 78 | % | | | 80 | % |

| Gibraltar | | | 16 | % | | | 15 | % |

| Alderney | | | 5 | % | | | 3 | % |

| Curaçao | | | 1 | % | | | 1 | % |

| Rest of the World | | | – | % | | | 1 | % |

| Total | | | 100 | % | | | 100 | % |

Our Internet-based gambling and electronic commerce software products are used by licensees to create virtual casinos. The downloadable software package transfers the “front-end” information (e.g., playing cards, roulette wheel, dice numbers) between users and remote servers. The software package utilizes each user’s computer to generate the graphics of the virtual gambling site, while the gambling servers perform the “dealer” function, generating the random numbers of playing cards,

roulette numbers and dice numbers, as applicable. Many of our most popular casino games are also available on either the Flash platforms, which provide an entertaining gambling experience without having to wait for software to download.

Among other things, our software contains proprietary encryption features, which allows secure transmission of data, and permits our licensees to offer multi-player games, a panoramic virtual casino floor populated by real players, progressive jackpots, Internet browsing features and inter-player chatting.

As part of our commitment and obligation to safe and responsible gambling, our gambling solution provides personal options and security features including deposit and bet limits, temporary and permanent account locks, personal identification verification, and online tracking of a player’s gambling activity and financial transactions. We are also able to restrict registration and game play from residents of prohibited jurisdictions.