BONTAN CORPORATION INC.

THREE MONTHS ENDED DECEMBER 31, 2010

MANAGEMENT’S DISCUSSION AND ANALYSIS

Prepared as at February 22, 2011

Index

| Overview | 3 |

| Summary of results | 3 |

| Number of common shares, options and warrants | 4 |

Business environment | 4 |

| Risk factors | 4 |

| Forward looking statements | 4 |

| Business plan | 5 |

Results of operations | 5 |

Liquidity and Capital Resources | 9 |

| Working capital | 9 |

| Operating cash flow | 10 |

| Investing cash flows | 10 |

| Financing cash flows | 13 |

| Key contractual obligations | 13 |

| Off balance sheet arrangements | 13 |

Transactions with related parties | 14 |

Financial and derivative instruments | 14 |

New accounting policies | 16 |

Critical accounting estimates | 18 |

Disclosure controls and procedures | 18 |

Internal control over financial reporting | 18 |

Public securities filing | 19 |

Bontan Corporation Inc. – M D & A Quarter ended December 31, 2010 – prepared on February 22, 2011Page 2

Management Discussion and Analysis

The following discussion and analysis by management of the financial condition and financial results for Bontan Corporation Inc. for the three months ended December 31, 2010 should be read in conjunction with the unaudited Consolidated Financial Statements for the three and nine months ended December 31, 2010, unaudited Consolidated Financial Statements and Management Discussion & Analysis for the three and six months ended September 30, 2010 and unaudited Consolidated Financial Statements and Management Discussion & Analysis for three months ended June 30, 2010 and the audited Consolidated Financial Statements and Annual Report in Form F-20 for the year ended March 31, 2010. The financial statements and the financial information herein have been prepared in accordance with generally acce pt accounting principles in Canada, as applicable to interim financial statements.

This management discussion and analysis is prepared by management as at December 31, 2010. The Company’s auditors have not reviewed it.

In this report:

| a. | The words “us”, “our”, “the Company” and “Bontan” have the same meaning unless otherwise stated and refer to Bontan Corporation Inc. and its subsidiary. |

| b. | Our indirect working interest in two drilling licenses offshore Israel is sometimes referred to as “Israel project” |

| c. | Our subsidiary, Israel Petroleum Company, Ltd Cayman is referred to as “IPC Cayman” |

.

Overview

Summary of Results

The following table summarizes financial information for the quarter ended December 31, 2010 and the preceding seven quarters: (All amounts in ‘000 CDN$ except Net income (loss) per share, which are actual amounts)

| Quarter ended | Dec. 31 | Sept. 30 | Jun.30 | Mar.31 | Dec. 31 | Sept.30 | Jun.30 | Mar.31 | ||

| 2010 | 2010 | 2010 | 2010 | 2009 | 2009 | 2009 | 2009 | |||

| Total Revenue | - | - | - | - | - | - | - | - | ||

| Net (loss) income | (1,065) | (1,329) | (486) | (2,275) | (630) | (763) | (206) | (266) | ||

| Working capital | 1,167 | 960 | 1,085 | 372 | (10,907) | 1,564 | 1,542 | 1,432 | ||

| Shareholder’s equity | 8,364 | 8,323 | 8,448 | 6,900 | 6,809 | 1,572 | 1,552 | 1,441 | ||

| Net loss per share - basic and diluted | $(0.01) | $(0.02) | $(0.01) | $(0.05) | $(0.01) | $(0.02) | $(0.01) | $(0.01) | ||

Bontan Corporation Inc. – M D & A Quarter ended December 31, 2010 – prepared on February 22, 2011Page 3

Number of common shares, options and warrants

These are as follows:

| As at Dec. 31, 2010 AND February 22, 2011 | |

| Shares issued and outstanding | 78,664,076 |

| Warrants issued and outstanding (a) | 73,071,420 |

| Options granted but not yet exercised (b) | 5,775,000 |

| (a) | Warrants are convertible into equal number of common shares of the Company within two to five years of their issuance, at average exercise price of $0.30. These warrants have weighted average remaining contractual life of 3.85 years. |

| (b) | Options are exercisable into equal number of common shares at an average exercise price of US$0.18 and have a weighted average remaining contractual life of approximately 3.86 years. |

Business Environment

Risk factors

Please refer to the Annual Report in the form F-20 for the fiscal 2010 for detailed information as the economic and industry factors that are substantially unchanged.

Forward looking statements

Certain statements contained in this report are forward-looking statements. All statements, other than statements of historical facts, included herein or incorporated by reference herein, including without limitation, statements regarding our business strategy, plans and objectives of management for future operations and those statements preceded by, followed by or that otherwise include the words “believe”, “expects”, “anticipates”, “intends”, “estimates” or similar expressions or variations on such expressions are forward-looking statements. We can give no assurances that such forward-looking statements will prove to be correct.

Each forward-looking statement reflects our current view of future events and is subject to risks, uncertainties and other factors that could cause actual results to differ materially from any results expressed or implied by our forward-looking statements.

Risks and uncertainties include, but are not limited to:

| · | Our lack of substantial operating history; |

| · | The success of the exploration prospects, in which we have interests; |

| · | Uninsured risks; |

| · | The impact of competition; |

| · | The enforceability of legal rights; |

| · | The volatility of oil and gas prices; |

| · | Weather and unforeseen operating hazards; |

Important factors that could cause the actual results to differ materially from our expectations are disclosed in more detail under the “Risk Factors” in our Annual report for fiscal 2010. Our forward-looking statements are expressly qualified in their entirety by this cautionary statement.

Currently we do not hold interests in any exploration projects and have no reserves as defined in Canadian National Instrument 51-101 Standards of Disclosure for Oil and Gas Activities ("NI 51-101"). All information contained herein regarding resources is references to undiscovered resources under NI 51-101, whether stated or not.

Bontan Corporation Inc. – M D & A Quarter ended December 31, 2010 – prepared on February 22, 2011Page 4

Business plan

We invest in the exploration and development of oil and gas wells. We focus on partnering with established developers and operators. We have never had any oil and gas operations and do not currently own any oil and gas properties with proven reserves.

In fiscal 2010, we acquired indirect working interest, which is currently 5.23%, in two licenses for drilling oil and gas in offshore location in Israel. Currently there are several disputes with the management of our subsidiary, IPC Cayman surrounding our rights to this property. As explained later, these disputes are being contested in Israeli courts.

We are therefore currently focused on resolving the disputes. There are also efforts in progress in out of court settlement with the management of IPC Cayman. These actions may result in us selling our interest on terms acceptable to us. If this happens, then we will invest the cash acquired through sale into other business opportunities. On the other hand , if we are successful in preserving our working interest, we will focus on participating in the future development of these two licenses.

Results of operations

| Three months ended Dec. 31, | 2010 | 2009 |

| In 000’ CDN$ | ||

| Income | - | - |

| Expenses | (1,186) | (683) |

| (1,186) | (683) | |

| Non-controlling interests | 121 | 52 |

| Net loss for period | (1,065) | (631) |

| Deficit at end of period | (40,142) | (34,935) |

Overview

The key events during the quarter ended December 31, 2010 were as follows:

| 1. | 5% of our indirect working interest in the Israeli project was sold to the operator Geoglobal Resources (India) Inc. for US$171,900 as per an agreement. |

| 2. | In October 2010, IPC Cayman signed an agreement with an Israeli Shell public company, Shaldieli Ltd. (“Shaldieli”) to sell our indirect working interest in the Israeli property for 90% equity in Shaldieli without our prior knowledge or approval as required. The transaction has not yet been approved by the shareholders of Shaldieli and Israeli Securities and Exchange Commission. Further, we have also taken legal action against the transaction. |

| 3. | We are also in disputes with the management of our subsidiary, IPC Cayman. They filed a counter claim against us and we filed responses and made counter claims for damages. These legal actions in the Israeli courts have not yet been heard. |

During the three months ended December 31, 2009, the main activities were as follows:

| a. | Completing acquisition of Offshore Israel Project as explained earlier in this report. |

Bontan Corporation Inc. – M D & A Quarter ended December 31, 2010 – prepared on February 22, 2011Page 5

| b. | Completing private placement to raise US$ 500,000 that was announced previously in December 2009. This was completed in October 2009. |

| c. | Reviewing various short term investments in our investment portfolio and disposing off significant portion of those investments which indicated declining values. |

| d. | Began a new private placement to raise up to US$ 5.5 million to be followed by another fund raising campaign to raise up to further US$ 13 million to fund the seismic data acquisition on the offshore Israel project.. |

Income

We had no revenue during the three months ended December 31, 2010 and 2009.

Expenses

The overall analysis of the expenses is as follows:

Three months ended Dec. 31, | 2010 | 2009 |

| Operating expenses | 152,137 | 377,371 |

| Consulting fees & payroll | 367,804 | 214,634 |

| Exchange gain | (4,889) | (231,634) |

| Loss on disposal of short term investments | 94,378 | 313,489 |

| Professional fees | 576,671 | 8,653 |

| 1,186,101 | 682,513 |

Operating Expenses

Three months ended Dec. 31, | 2010 | 2009 |

| Travel, meals and promotion | 89,484 | 22,657 |

| Shareholders information | 40,106 | 45,231 |

| Other | 22,547 | 309,483 |

| 152,137 | 377,371 |

Travel, meals and promotions

During the three months ended December 31, 2010, the Company’s management, lawyers and consultants had to undertake extensive travel to Israel, USA and Cayman Island to discuss the matters concerning the Israeli project and also to retain lawyers to discuss and organize various legal actions against Shaldieli and the management of IPC Cayman in connection with various disputes relating to the Israeli project as explained elsewhere in this report. IPC Cayman charged approximately $ 42,000 for travel, meals and promotion during the period, which included travels to Israel and stay there for several weeks by the manager and other consultants of IPC Cayman.

Expenses for the three months ended December 31, 2009 were substantially incurred by the key consultant, Mr. Terence Robinson and other consultants in visiting Vancouver, UK and USA in connection with the Israel Offshore Project and fund raising efforts and local club and entertainment costs in business meetings.

Bontan Corporation Inc. – M D & A Quarter ended December 31, 2010 – prepared on February 22, 2011Page 6

Shareholder information

Shareholder information costs comprise investor and media relations fee, costs of holding Annual general meeting of the shareholders and various regulatory filing fees.

Major cost consists of media relation and investor relation services provided by Current Capital Corp. under contracts dated July 1, 2004, which are being renewed automatically unless canceled in writing by a 30-day notice for a total monthly fee of US$10,000. Current Capital Corp. is a shareholder Corporation where the Chief Executive and Financial Officer of the Company provide accounting services.

Fees were consistent for the 2010 and 2009 periods.

Management believes that such services are essential to ensure our existing shareholder base and prospective investors/brokers and other interested parties are constantly kept in contact and their comments and concerns are brought to the attention of the management on a timely basis.

Other operating costs

These costs include rent, telephone, Internet, transfer agents fees and other general and administration costs.

During the quarter ended December 31, 2009, other costs included interest and advisory fee of $ 276,496. The company and its subsidiary, IPC borrowed a total of approximately $ 1.8 million as short term loans. Two of these loans carried interest at 10% per annum and one carried interest at 5% per annum. Interest cost on these loans was approximately $ 15, 800.The Company’s subsidiary; IPC also had an obligation to pay Western Geophysical, a survey company a sum of approximately US$ 12 million for 2D and 3D seismic data relating to the Offshore Israel Project. The net outstanding balance payable carried interest at the rate of 1.5% per month. Total interest cost for the quarter was approximately $ 44,000. Further, the Company and its subsidiary, IPC paid advisory fee of approximately $220,000 to Bandel Interests LLC, a non-related corporation, computed on funds raised. This amount was expensed.

| Consulting fees and payroll |

| Three months ended December 31 | 2010 | 2009 |

| Fees settled in common shares | $ 20,717 | $ 80,258 |

| Fees settled in cash | 337,731 | 121,572 |

| Payroll | 9,356 | 12,804 |

| $ 367,804 | $ 214,634 |

Stock based compensation is made up of the Company’s common shares and options being issued to various consultants and directors of the Company for services provided. The Company used this method of payment mainly to conserve its cash flow for business investments purposes. This method also allows the Company to avail the services of consultants with specialized skills and knowledge in the business activities of the Company without having to deplete its limited cash flow.

Bontan Corporation Inc. – M D & A Quarter ended December 31, 2010 – prepared on February 22, 2011Page 7

The following were the key details forming part of consulting fee and payroll costs during the three months ended December 31, 2010:

| a. | No new consultants were hired or paid for in shares or options during the period. However, value of shares previously allotted and deferred was expensed to the extent it related to the services provided during the period. |

| b. | Fees settled in cash consisted of a fee of $60,000 paid to Mr. Cooper as manager of IPC Cayman , $ 45,000 to Mr. Kam Shah, the chief executive and financial officer $ 30,000 to Mr. Terence Robinson, a key consultant, $ 2,500 to the two independent directors for their services as members of the audit committee, for the quarter. The balances of the fees were paid to consultants hired by the Company and by IPC Cayman. |

The following were the key details forming part of consulting fee and payroll costs during the quarter ended December 31, 2009

| a. | Three independent consultants were retained during the quarter for services related to the Israel Offshore Project. Total of 228,333 shares were issued to them as fee out of the 2009 Consultant Stock Compensation Plan. These shares were valued at a market price on the date of their issuance. |

| b. | Fees settled in cash consisted of fee of $30,000 each paid to Mr. Kam Shah, the chief executive and financial officer and Mr. Terence Robinson, a key consultant for the quarter. Two independent directors were paid $2,500 for their services as members of the audit committee. Approximately $ 60,000 was paid to consultants hired by the Company as well as its subsidiary, IPC during the quarter. |

Payroll related to the administrative assistant hired as an employee by the Company. Change in the assistant during the fiscal 2011 caused salary cost to decline during this period compared to the previous period.

Exchange (gain) loss

Exchange differences related to translation losses arising from converting foreign currency balances, mainly in US dollars into Canadian dollars, which is the reporting unit of currency, on consolidation.

As at December 31, 2010, the Company had excess of liabilities in US dollar of approximately $1.6 million over its monetary assets in US dollar. US dollar declined in value against Canadian dollar from 1.0331CDN$ in September 2010 to 0.9946 CDN$ at December 31, 2010, which resulted in a small exchange gain on December 31, 2010 translation.

During the quarter ended December 31, 2009, we acquired significant asset – Offshore Israel Project – as explained earlier. The purchase price was in US dollar. We also took over liability to pay for the seismic data as part of the Project which was approximately US$ 12 million and also borrowed short term funds in US$ of approximately $ 1.6 million. Thus, at the period end, almost all our current liabilities were in US dollar. US dollar weakened marginally against Canadian dollar during the quarter form US$ 1 = CDN$ 1.06 at the beginning of the quarter to US$1= CDN$ 1.05 at the end of the quarter. Bulk of the translation gains arose from this exchange differences when we converted all liabilities in US dollar into Canadian dollar at the yearend rate. Majority of the Company’s assets and capital t ransactions were done at historical costs and were not converted at the period end rate and so there were no significant offsetting gains.

Bontan Corporation Inc. – M D & A Quarter ended December 31, 2010 – prepared on February 22, 2011Page 8

Loss on disposal of short term investments

During the three months ended December 31, 2010, the Company sold some of the shares in one of its holdings at a loss to meet its cash flow requirement.

During the quarter ended December 31, 2009, management continued its previous quarter review of its short-term investment portfolio and identified one holding, Probe Resources Limited, whose market value remained depreciated for quite some time and showed no signs of any recovery in the near future. We therefore decided to dispose of this investment, which had carrying value of $389,620 for $76,120 and focus on those whose values are likely to improve.

Professional fees

Professional fees for the three months ended December 31, 2010 consisted of audit and accounting fees of approximately $162,000 and legal fees of approximately $ 415,000.

Audit and accounting includes accrual for the audit fee apportioned for the quarter and charges from the auditors regarding registration statement and its various amendments filed of $24,000 and accounting fee of approximately $138,000 charged by IPC Cayman.

Legal fees included fees incurred by the Company for its legal actions against Shaldieli and IPC Cayman management as discussed elsewhere in this report of approximately $252,000 and fees regarding its registration filings and other routine legal work of approximately $ 60,000 and legal fees of approximately $ 103,000 incurred by IPC Cayman.

The Company expects its legal costs to increase as it accelerates its legal actions in other jurisdictions.

During the quarter ended December 31, 2009, audit fee was accrued at approximately $8,000 on the basis of the estimated annual fee of $35,000. Legal costs incurred in connection with the offshore Israel Project were capitalized.

Liquidity and Capital Resources

Working Capital

As at December 31, 2010, the Company had a net working capital of was approximately $1.0 million, compared to a working capital of approximately $400,000 as at March 31, 2010.

Almost the entire working capital at December 31, 2010 and March 31, 2010 was in the form of cash and short term investments.

Value of our short term investment portfolio increased during the quarter by approximately $ 1 million.

Cash on hand as at December 31, 2010 was approximately $275,000 compared to $2.4 million as at March 31, 2010. Cash was used to pay off term loans, incur additional costs on the Israel project and on the operating and legal expenses which increased significantly due to IPC Cayman.

The Company will require working capital of approximately $ 12 million to meet its exploration obligations with respect to its interest in the Israeli property within the next twelve months on the two wells, based on our current estimates of the exploration and drilling costs of these wells. These costs are covered by the deal with Ofer brothers to whom IPC Cayman sold 50% of our interest for $ 28 million dollar which they agreed to spend on the exploration costs.

Bontan Corporation Inc. – M D & A Quarter ended December 31, 2010 – prepared on February 22, 2011Page 9

Operating cash flows

During the three months ended December 31, 2010, operating activities required net cash out flow of approximately $ 392,000, which was met from the available cash and proceeds from the disposal of short term investments.

During the quarter ended September 30, 2009, operating activities generated a net cash inflow of approximately $11.3 million, mainly due to withholding payments to the surveyor.

The company expects its operating cash requirements to increase as explained elsewhere in the report, the Company has launched several legal actions which will require significant cash as the legal matters progress and may get expanded in different jurisdictions. We hope to meet the expected increase in operating cash requirement through profitable disposal of some of our short term investments which have begun to grow in value.

Investing cash flows

During the three months ended December 31, 2010, the company received proceeds of approximately $ 165,000 from its sale of 5% interest in the Israeli project and $114,000 from disposal of its short term investment, thus generating a net cash inflow of approximately $279,000.

During the quarter ended December 31, 2009, the management continued its reviewed its entire short term portfolio and disposed of one major investment which continued to decline in value and showed no sign for any improvement in the near future. The disposal generated a net cash flow of approximately $61,000, which after netting off small acquisitions of $46,000 resulted in net cash flow of $15,000. During this period, the Company acquired certain software and computer for approximately $ 2,000 and invested approximately $ 15 million in the Offshore Israel Project, thus overall outflow of approximately $ 15 million. Of this, approximately $11.3 representing surveyor’s costs were withheld and balance was met from equity and loans financing.

Two key investing activities are discussed below in detail:

Oil and gas properties and related expenditure

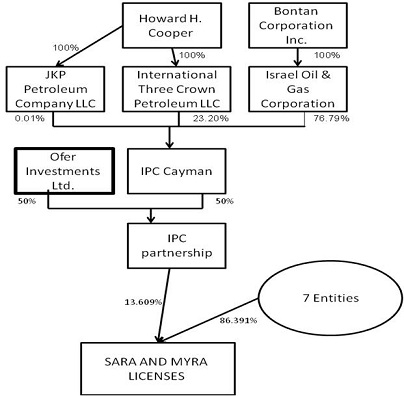

The Company currently holds indirect 5.23% working interest in the Israeli property. This is held by way of the Company’s equity interest of 76.79% in IPC Cayman which holds 50% equity interest in IPC limited partnership in Israel (“IPC Israel”). IPC Israel is the registered holder of 13.609% interest in two licenses to drill oil and gas offshore Israel.

The relevant tree structure of the holdings in the various companies, prior to the Shaldieli Transaction, is as follows:

Bontan Corporation Inc. – M D & A Quarter ended December 31, 2010 – prepared on February 22, 2011Page 10

BontanBontan’s working interest is 76.79% of 50% of 13.609% = 5.23% |

The key events that happened during the three months ended December 31, 2010 were:

| (i) | On October 13, 2010, IPC Cayman and its wholly owned IPC Partnership signed a Partnership Subscription and Contribution Agreement with Ofer Investments Ltd., an Israeli company, (“Ofer”). Under this agreement, Ofer agreed to contribute up to US$ 28 million towards the IPC Partnership’s share of the cost of drilling of the initial two exploratory wells under the Sara and Myra licenses and related exploration costs in exchange for a 50% limited partnership interest in IPC Partnership and certain voting and management rights related to IPC Partnership. |

As a result of the above transactions, the Company’s indirect interest in the two licenses now stands at 5.23%.

| (ii) | On October 6, 2010, the partners of the Israel Project signed a new joint operating agreement with Geoglobal Resources (India) Inc., as operator. The new agreement provides for early termination and replacement of the operator subject to certain compensation. |

| (iii) | On October 25, 2010, IPC Cayman announced that it signed an agreement to acquire a publicly listed Israeli company, Shaldieli Ltd in a reverse takeover by placing its ownership interests in the Israel project in to Shaldieli , Ltd in exchange for 90% ownership of Shaldieli, Ltd. The Company as a majority shareholder of IPC Cayman has not yet agreed to this deal. The matter is currently under dispute and litigation between the Company and IPC Cayman management. Besides, Shaldieli deal is subject to approval by the shareholders of Shaldieli and Israeli Securities and Exchange Commission. These approvals have not yet been available. |

| PENDING DISPUTES |

| (i) | On October 26, 2010, ITC purported to enter into an agreement on behalf of IPC Cayman with Shaldieli Ltd., an Israeli shell public company (Shaldieli) pursuant to which IPC Cayman would acquire 90% of Shaldieli’s common equity (subject to further dilution for options etc.) in exchange for IPC Cayman’s contribution of its 50% interest in IPC Israel to Shaldieli. IPC Israel is the registered owner of a 13.609% working interest (the “Working Interest”) in the “Myra” and “Sara” licenses to conduct marine oil and gas exploration in the Levantine Basin, . We believe that the transaction is subject to the Company’s approval as the majority stockholder of IPC Cayman and to Israeli regulatory approvals. The Company has not given this approval. However, Shaldieli has announced a shareholders meeting to approve the said transaction [and IT C has taken contradictory positions with respect to whether the Company's approval is required for the transaction to proceed.] |

Bontan Corporation Inc. – M D & A Quarter ended December 31, 2010 – prepared on February 22, 2011Page 11

The Company’s attorneys filed a petition in Israel for a temporary injunction enjoining the proposed shareholders meeting by Shaldieli. The temporary injunction was originally granted on January 5, 2011 but after a hearing, the Israeli District court lifted its temporary injunction on January 15, 2011. On January 18, 2011, the Company filed an appeal with the Supreme Court in Israel which upheld the district court decision on January 20, 2011. Both the courts made clear in their rulings that they were not ruling on the merits of the Company’s claim. The Company also filed a claim for a permanent injunction and has asked that its claim would be amended so as to include a claim for damages as well with the district court in Israel, which has not yet been heard.

Shaldieli has postponed its shareholders meeting a number of times, and it has further been postponed without any future date being set.

| (ii) | On January 23, 2011, IPC Cayman and ITC counterclaimed against the Company for monetary damages and for an order cancelling Bontan’s shares in IPC Cayman (or requiring them to be transferred to IPC Cayman or to ITC). On February 21, 2011, the Company submitted its responses to the counter claim denying all allegations. The Company also asked that its claim against IPC Cayman, ITC and Mr Cooper be amended to include claims for monetary damages against them. |

The Company continues to consider a range of alternatives, including an out of court settlement involving the sale of its shares in IPC Cayman. However, no assurance can be given that any settlement or sale will be achieved. In the absence of a settlement or sale, the Company will continue to pursue its legal remedies, including legal actions in other jurisdictions to protect its rights with respect to the oil and gas properties in Israel.

Short Term Investments

The Company had short term investments at a carrying cost of approximately $ 3.1 million as at December 31, 2010 – all of which were held in five Canadian public companies. These investments were stated at their fair value of approximately $ 2.7 million as at December 31, 2010 and the difference representing unrealised loss of approximately $400,000 was transferred to accumulated other comprehensive loss and included under shareholders equity.

The Company had short term investments at a carrying cost of approximately $4.3 million as at December 31, 2009 – of which $4.1 million or 95% was held in Canadian currency and the balance 5% was held in US currency. Approximately 93% of the investments were in 12 public companies while 7% was invested in two private companies. These investments were stated at their fair value of approximately $2 million as at December 31, 2009 and the difference representing unrealised loss of approximately $2.3 million was transferred to accumulated other comprehensive loss and included under shareholders equity.

The following are our key investments:

Bontan Corporation Inc. – M D & A Quarter ended December 31, 2010 – prepared on February 22, 2011Page 12

| March 31, | December 31, 2010 | March 31, 2010 | ||||

| in 000' | ||||||

| # of shares | cost | fair value | # of shares | cost | fair value | |

| Marketable Securities | ||||||

| Brownstone Ventures Inc. | 1,142 | 1652 | 1130 | 1,292 | 1869 | 775 |

| Bowood Venture Inc. | 1,744 | 658 | 1046 | 1,744 | 658 | 244 |

| Skana Capital Corp | 750 | 699 | 495 | 773 | 706 | 155 |

| 2 (March 31, 2010:10 ) other public companies - mainly resource sector | 92 | 43 | 775 | 185 | ||

| $3,101 | $2,714 | $4,008 | $1,359 | |||

| Non-marketable securities | ||||||

| Cookee Corp | - | 1,000 | 200 | - | ||

| One other private company | - | 63 | - | |||

| $- | $- | $263 | $- | |||

| $3,101 | $2,714 | $4,271 | $1,359 | |||

We believe that the three main investments are likely to grow in value in future.

Financing cash flows

Major financing activity during the three months ended December 31, 2010 consisted of exercise of 350,000 warrants by two shareholders for a total cash price of $35, 600.

During the three months ended December 31, 2009, the Company received eight subscriptions for a total of 7.5 million units for net proceeds of $359,252.

On November 20, 2009, The Board of Directors of the Company approved a private placement to raise equity funds up to US$ 5,500,000. The private placement consists of Units up to maximum of 27.5 million, to be issued at US0.20 per Unit. Each Unit would comprise one common share of the Company and one full warrant convertible into one common share of the Company at an exercise price of US$0.35 each within five years of the issuance of warrant.

The board also approved a finder’s fee at 10% of the proceeds from the issuance of units and from the warrants attached thereto plus 10% in warrants of the warrants issued at the same terms payable to Current Capital Corp., a related party, subject to reduction by the finder’s fee payable to ITC at 5% of the net proceeds of Units subscribed by investors introduced through ITC.

During the three months ended December 31, 2009, the Company received ten subscriptions for a total of 8,725,000 million units for net proceeds of approximately $ 1.6 million.

The Company also borrowed approximately $ 1.8 million through three loans. Details of these loans are explained in note 9 of the three and nine months ended financial statements as at December 31, 2009.

Key Contractual obligations

The only contractual obligation as at December 31, 2010 related to the commitment to cover our share of the exploration costs on the two exploration wells to be drilled on the Israeli property on or before July 2011. These costs are expected to be covered by $ 28 million payable by Ofer brothers who acquired 50% of the working interest from our subsidiary, IPC Cayman.

Off balance sheet arrangements

At December 31, 2010 and 2009, the Company did not have any off balance sheet arrangements, including any relationships with unconsolidated entities or financial partnership to enhance perceived liquidity.

Bontan Corporation Inc. – M D & A Quarter ended December 31, 2010 – prepared on February 22, 2011Page 13

Transactions with related parties

Transactions with related parties are incurred in the normal course of business and are measured at the exchange amount. Related party transactions and balances have been listed in Note 13 and elsewhere of the consolidated unaudited financial statements for the three and nine months ended December 31, 2010.

Given below is background information on some of the key related parties and transactions with them:

| 1. | Current Capital Corp. (CCC). CCC is a related party in following ways – |

| a. | Director/President of CCC, Mr John Robinson is a consultant with Bontan |

| b. | CCC provides media and investor relation services to Bontan under a consulting contract. |

| c. | Chief Executive and Financial Officer of Bontan is providing services to CCC as CFO. |

| d. | CCC and John Robinson hold significant shares, options and warrants in Bontan. |

CCC also charged a finder’s fee at the rate of 10% of the gross money raised for the Company through issuance of shares and warrants under private placements. In addition,

| 2. | Mr Kam Shah is a director of the Company and also provides services as chief executive and financial officer under a five-year contract. The compensation is decided by the board on an annual basis and is usually given in the form of shares and options. |

| 3. | Mr. Terence Robinson was Chairman of the Board and Chief Executive Officer of the Company since October 1, 1991. He resigned from the Board on May 17, 2004 but continues with the Company as a key consultant. He advises the board in the matters of shareholders relations, fund raising campaigns, introduction and evaluation of investment opportunities and overall operating strategies for the Company. |

| 4. | Mr. Howard Cooper and Three Crown Petroleum LLC, (TCP) a Company controlled by Mr. Cooper. Mr. Cooper/TCP is the sole director and manager of our subsidiary, IPC Cayman and is also the minority shareholder, holding 23.21% equity in IPC Cayman. Mr. Cooper receives a fee of US$ 20,000 per month for acting as manager of IPC Cayman and representing the Company on the Israeli Project. |

Financial and derivative Instruments

The Company is exposed in varying degrees to a number of risks arising from financial instruments. Management’s close involvement in the operations allows for the identification of risks and variances from expectations. The Company does not participate in the use of financial instruments to mitigate these risks and has no designated hedging transactions. The Board approves and monitors the risk management processes. The Board’s main objectives for managing risks are to ensure liquidity, the fulfilment of obligations and limited exposure to credit and market risks while ensuring greater returns on the surplus funds on hand. There were no changes to the objectives or the process from the prior year. Cash, short term investments, accounts payable and accruals are classified as level one financial instrume nt.

The types of risk exposure and the way in which such exposures are managed are as follows:

| (a) | Concentration risk: |

Bontan Corporation Inc. – M D & A Quarter ended December 31, 2010 – prepared on February 22, 2011Page 14

Concentration risks exist in cash and cash equivalents because significant balances are maintained with one financial institution and a brokerage firm. The risk is mitigated because the financial institutions are international banks and the brokerage firm is well known Canadian brokerage firm with good market reputation and all its assets are backed up by a major Canadian bank. The Company’s key asset, the indirect working interest in two off shore drilling licenses is located in Israel.

| (b) | Market price risk: |

Market risk primarily arises from the Company’s short term investments in marketable securities which accounted for approximately 26% of total assets of the Company as at December 31, 2010 (13% as at March 31, 2010). Further, the Company’s holding in two Canadian marketable security accounted for approximately 79% (March 31, 2010: 75%) of the total short term investment in marketable securities or 20% (March 31, 2010: 9.7%) of total assets as at December 31, 2010. The Management tries to mitigate this risk by monitoring daily all its investments with experienced consultants and ensuring that investments are made in companies which are financially stable with viable businesses.

| (c) | Liquidity risk: |

The Company monitors its liquidity position regularly to assess whether it has the funds necessary to fulfill planned exploration commitments on its petroleum and natural gas properties or that viable options are available to fund such commitments from new equity issuances or alternative sources such as farm-out agreements. However, as an exploration company at an early stage of development and without significant internally generated cash flow, there are inherent liquidity risks, including the possibility that additional financing may not be available to the Company, or that actual exploration expenditures may exceed those planned. The current uncertainty in global markets could have an impact on the Company’s future ability to access capital on terms that are acceptable to the Company. The Company has so f ar been able to raise the required financing to meet its obligations on time.

As explained above, the Company’s financial obligation up to the first two exploratory wells on the licenses in which the Company holds indirect working interest is covered through a deal with Ofer brothers group.

The Company believes that its current cash and short term investments will be sufficient to enable it to continue its various legal actions until they can be satisfactorily resolved and to meet its operational needs.

The Company maintains limited cash for its operational needs while most of its surplus cash is invested in short term marketable securities which are available on short notice to fund the Company’s operating costs and other financial demands.

| (d) | Currency risk |

The operating results and financial position of the Company are reported in Canadian dollars. Approximately 9% of total monetary assets at December 31, 2010 (28% as at March 31, 2010), and approximately 93% of its liabilities as at that date (89% as at March 31, 2010) were held in US dollars. The results of the Company’s operations are therefore subject to currency transaction and translation risk.

The fluctuation of the US dollar in relation to the Canadian dollar will consequently impact the loss of the Company and may also affect the value of the Company’s assets and the amount of shareholders’ equity.

Bontan Corporation Inc. – M D & A Quarter ended December 31, 2010 – prepared on February 22, 2011Page 15

Comparative foreign exchange rates are as follows:

December 31, 2010 | March 31, 2010 | December 31, 2009 | |

| One US Dollar to CDN Dollar | 0.9946 | 1.0156 | 1.0470 |

The Company has not entered into any agreements or purchased any foreign currency hedging arrangements to hedge possible currency risks at this time.

New accounting policies

Recent accounting pronouncements

International Financial Reporting Standards (“IFRS”)

In January 2006, the CICA’s Accounting Standards Board ("AcSB") formally adopted the strategy of replacing Canadian GAAP with IFRS for Canadian enterprises with public accountability. The current conversion timetable calls for financial reporting under IFRS for accounting periods commencing on or after January 1, 2011. On February 13, 2008 the AcSB confirmed that the use of IFRS will be required in 2011 for publicly accountable profit-oriented enterprises. For these entities, IFRS will be required for interim and annual financial statements relating to fiscal years beginning on or after January 1, 2011. The Company has assessed the impact of IFRS on its consolidated financial statements and concluded that switching to IFRS would not require any major changes in its existing accounting policies.

The Company’s transition date of April 1, 2011 will require the restatement for comparative purposes of amounts reported by the Company for the year ending March 31, 2011.

The key elements of our changeover plan include:

| 1. | Scoping and diagnostic |

High level analysis to:

| · | Assess differences between IFRS and GAAP |

| · | Identify elective and mandatory exceptions available under IFRS 1 |

| · | Scope out potential impacts on systems and process |

| · | Identify impacts on business relationship including contractual arrangements |

IFRS 1 – First Time Adoption of IFRS and Opening Balance Sheet Quantifications

IFRS 1 requires an entity to comply with each IFRS effective at the reporting date for its first IFRS financial statements. In particular, the IFRS requires an entity to do the following in the opening IFRS balance sheet that it prepares as a starting point for its accounting under IFRSs:

| a) | Recognize all assets and liabilities whose recognition is required by IFRSs; |

| b) | Not recognize items as assets or liabilities if IFRSs do not permit such recognition; |

| c) | Reclassify items that it recognized under previous GAAP as one type of asset, liability or component of equity, but are a different type of asset, liability or component of equity under IFRSs; and |

| d) | Apply IFRSs in measuring all recognized assets and liabilities. |

IFRS 1 offers entities adopting IFRS for the first time with a number of exemptions (optional and in some areas mandatory). The Company is currently evaluating exemptions available to determine the most appropriate to its circumstances. The most appropriate IFRS 1 exemptions applicable to the Company that have been identified to date are:

Bontan Corporation Inc. – M D & A Quarter ended December 31, 2010 – prepared on February 22, 2011Page 16

Property, Plant and Equipment

The IFRS 1 election related to property, plant and equipment allows the Company to report property, plant and equipment in its balance sheet on the transition date at a deemed cost instead of actual cost. The exemption can be applied on an asset-by-asset basis.

Given the insignificant size of the Company’s property, plant and equipment, we will continue to report at the actual cost.

IAS 36 - Impairment of Assets

The objective of this Standard is to prescribe the procedures that an entity applies to ensure that its assets are carried at no more than their recoverable amount.

The Company is currently assessing the impact of this standard on its reporting requirements as regards its Israeli property. While the current factors indicate that the value of this property is unlikely to be less than its fair market value, the final out come will not be known until the current legal actions and negotiations are concluded.

IFRS 2 - Share Based Payments

This standard provides guidance for the recognition and measurement of share-based payments. Management must determine the fair value of a share-based payment at the grant date and the period over which this fair value should be recognized.

The Company’s current policy is consistent with this standard.

IFRS 6 – Exploration for and Evaluation of Mineral Resources

The objective of this standard is to specify the financial reporting for the exploration for and evaluation of mineral resources. Under IFRS 6, the Company may continue to use its current accounting policies for reporting on and evaluating its mineral resources. This includes continuing to use recognition and measurement practices that are part of those accounting policies.

The Company is currently reviewing its impairment testing requirements under IFRS 6 and the requirement to report the allocation of exploration assets to cash-generating units or groups of cash-generating units for the purpose of assessing such assets for impairment.

IAS 37 - Provisions, Contingent Liabilities and Contingent Assets

This requires that appropriate recognition criteria and measurement bases are applied to provisions, contingent liabilities and contingent assets and that sufficient information is disclosed in the notes to enable users to understand their nature, timing and amount.

The Company is currently assessing the impact of this standard on its reporting requirements but is not expecting any significant changes.

IAS 12 - Income Taxes

The objective of this standard is to prescribe the accounting treatment for income taxes. For the purposes of this standard, income taxes include all domestic and foreign taxes which are based on taxable profits. Income taxes also include taxes, such as withholding taxes, which are payable by a subsidiary, associate or joint venture on distributions to the reporting entity.

Bontan Corporation Inc. – M D & A Quarter ended December 31, 2010 – prepared on February 22, 2011Page 17

As the Company is still in the exploration phase, this standard will not have any immediate impact on the Company’s reporting requirements

| 2. | Impact analysis, evaluation and design |

| · | Determine projected impact of adopting IFRS on financial statements and develop accounting processes |

| · | Develop and finalize changes to systems and internal controls |

| · | Address business activities including contractual arrangements, compensation arrangements, budgeting/forecasting |

| · | Prepare reporting templates and training plan |

| - | Our current preliminary assessment does not indicate any major changes. However, we will continue to evaluate as our project goes into exploration stage |

| 3. | Implementation and Review |

| · | Collect and compile IFRS information for reporting |

| · | Execute changes to information systems and business activities |

| · | Communicate |

Critical accounting estimates

The Company’s unaudited consolidated financial statements have been prepared in accordance with generally accepted accounting principles in Canada. The significant accounting policies used by the Company are same as those disclosed in note 4 to the consolidated financial statements for the year ended March 31, 2010. Certain accounting policies require that the management make appropriate decisions with respect to estimates and assumptions that affect the assets, liabilities, revenue and expenses reported by the Company. The Company’s management continually reviews its estimates based on new information, which may result in changes to current estimated amounts.

Disclosure Controls and Procedures

The Company maintains a set of disclosure controls and procedures designed to ensure that information required to be disclosed in filings made pursuant to Multilateral Instrument 52-109 and as defined in Rules 13a-15(e) and 15d-15(e) of the Securities Exchange Act of 1934, is recorded, processed, summarized and reported within the time periods specified in the applicable regulatory bodies’ rules and forms.

Our management, including our Chief Executive Officer, who also acts as Chief Financial Officer, together with the members of our audit committee, has evaluated the effectiveness of our disclosure controls and procedures as of the end of the period covered by this report. Based upon that evaluation, our Chief Executive Officer has concluded that our disclosure controls and procedures were effective in relation to the level and complexity of activities in our Company as of the end of the period covered by this report.

Internal Controls over Financial Reporting

Our Chief Executive Officer who also serves as Chief Financial Officer (“CEO”) is primarily responsible in establishing and maintaining controls and procedures concerning disclosure of material information and their timely reporting in consultation and under direct supervision of the audit committee which comprises two independent directors. CEO is assisted by one employee. We therefore do not have effective internal controls and procedures due to lack of segregation of duties. However, given the size and nature of our current operations and involvement of independent directors in the process significantly reduce the risk factors associated with the lack of segregation of duties.

Bontan Corporation Inc. – M D & A Quarter ended December 31, 2010 – prepared on February 22, 2011Page 18

The CEO has instituted a system of disclosure controls for the Company to ensure proper and complete disclosure of material information. The limited number of consultants and direct involvement of the CEO facilitates access to real time information about developments in the business for drafting disclosure documents. All documents are circulated to the board of directors and audit committee according to the disclosure time-lines.

As at March 31, 2010, the management carried out a comprehensive review and update of the internal controls existing over the financial reporting. Mitigating controls and procedures were identified wherever possible. New procedures were implemented in a couple of cases, including the information from our subsidiary, IPC Cayman where it was evident that controls were not robust enough to ensure appropriate disclosure in a timely manner. Some controls were implemented as a secondary detection mechanism if the initial controls failed to prevent errors from occurring.

There were no significant changes in the Company's internal controls or in other factors that could significantly affect these controls subsequent to the date the CEO completed his evaluation, nor were there any significant deficiencies or material weaknesses in the Company's internal controls requiring corrective actions other than the lack of segregation of duties.

Public securities filings

Additional information, including the Company’s annual information form in the Form 20-F annual report is filed with the Canadian Securities Administrators at www.sedar.com and with the United States Securities and Exchange Commission and can be viewed at www.edgar.com.

Bontan Corporation Inc. – M D & A Quarter ended December 31, 2010 – prepared on February 22, 2011Page 19