Table of Contents

UNITED STATES SECURITIES AND

EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

Annual report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 for the fiscal year ended December 31, 2006

Commission File Number 001-15811

MARKEL CORPORATION

(Exact name of registrant as specified in its charter)

A Virginia Corporation

IRS Employer Identification No. 54-1959284

4521 Highwoods Parkway, Glen Allen, Virginia 23060-6148

(Address of principal executive offices) (Zip code)

Registrant’s telephone number, including area code: (804) 747-0136

Securities registered pursuant to Section 12(b) of the Act:

Common Stock, no par value, New York Stock Exchange, Inc.

7.50% Senior Debentures due 2046, New York Stock Exchange, Inc.

(title of class and name of the exchange on which registered)

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yesx No¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes¨ Nox

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yesx No¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K.x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (check one):

Large accelerated filerx Accelerated filer¨ Non-accelerated filer¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes¨ Nox

The aggregate market value of the shares of the registrant’s Common Stock held by non-affiliates as of June 30, 2006 was approximately $3,015,580,251.

The number of shares of the registrant’s Common Stock outstanding at February 22, 2007: 9,963,465.

Documents Incorporated By Reference

The portions of the registrant’s Proxy Statement for the Annual Meeting of Shareholders scheduled to be held on May 14, 2007, referred to in Part III.

Table of Contents

Index and Cross References-Form 10-K

Annual Report

Item No. | Page | |||||||

| Part I | ||||||||

| 1. | Business | 12-31, 115-117 | ||||||

| 1A. | Risk Factors | 30 | ||||||

| 1B. | Unresolved Staff Comments | NONE | ||||||

| 2. | Properties (note 5) | 47-48 | ||||||

| 3. | Legal Proceedings (note 15) | 63 | ||||||

| 4. | Submission of Matters to a Vote of Security Holders | NONE | ||||||

| 4A. | Executive Officers of the Registrant | 118 | ||||||

| Part II | ||||||||

| 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | 78, 116 | ||||||

| 6. | Selected Financial Data | 32-33 | ||||||

| 7. | Management’s Discussion & Analysis of Financial Condition and Results of Operations | 79-115 | ||||||

| 7A. | Quantitative and Qualitative Disclosures About Market Risk | 109-112 | ||||||

| 8. | Financial Statements and Supplementary Data | |||||||

| The response to this item is submitted in Item 15 and on page 78. | ||||||||

| 9. | Changes in and Disagreements With Accountants on Accounting and Financial Disclosure | NONE | ||||||

| 9A. | Controls and Procedures | 75-77, 113 | ||||||

| 9B. | Other Information | NONE | ||||||

| Part III | ||||||||

| 10. | Directors, Executive Officers and Corporate Governance* | 118 | ||||||

| Code of Conduct | 117 | |||||||

| 11. | Executive Compensation* | |||||||

| 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters* | |||||||

| 13. | Certain Relationships and Related Transactions, and Director Independence* | |||||||

| 14. | Principal Accounting Fees and Services* | |||||||

* Portions of Item Number 10 and Items Number 11, 12, 13 and 14 will be incorporated by reference from the Registrant’s 2007 Proxy Statement pursuant to instructions G(1) and G(3) of the General Instructions to Form 10-K. | ||||||||

| Part IV | ||||||||

| 15. | Exhibits, Financial Statement Schedules | |||||||

| a. | Documents filed as part of this Form 10-K | |||||||

| (1) | Financial Statements | |||||||

| Consolidated Balance Sheets at December 31, 2006 and 2005 | 34 | |||||||

| Consolidated Statements of Income and Comprehensive Income for the Years Ended December 31, 2006, 2005 and 2004 | 35 | |||||||

| Consolidated Statements of Changes in Shareholders’ Equity for the Years Ended December 31, 2006, 2005 and 2004 | 36 | |||||||

| Consolidated Statements of Cash Flows for the Years Ended December 31, 2006, 2005 and 2004 | 37 | |||||||

| Notes to Consolidated Financial Statements for the Years Ended December 31, 2006, 2005 and 2004 | 38-73 | |||||||

| Reports of Independent Registered Public Accounting Firm | 74-76 | |||||||

| (2) | Schedules have been omitted since they either are not required or are not applicable, or the information called for is shown in the Consolidated Financial Statements and Notes thereto. | |||||||

| (3) | See Index to Exhibits for a list of Exhibits filed as part of this report | |||||||

| b. | See Index to Exhibits and Item 15a(3) | |||||||

| c. | See Index to Financial Statements and Item 15a(2) | |||||||

Table of Contents

Markel Corporation & Subsidiaries

We market and underwrite specialty insurance products and programs to a variety of niche markets and believe that our specialty product focus and niche market strategy enable us to develop expertise and specialized market knowledge. We seek to differentiate ourselves from competitors by our expertise, service, continuity and other value-based considerations. We compete in three segments of the specialty insurance marketplace: the Excess and Surplus Lines, the Specialty Admitted and the London markets. Our financial goals are to earn consistent underwriting profits and superior investment returns to build shareholder value.

Specialty Insurance

The specialty insurance market differs significantly from the standard market. In the standard market, insurance rates and forms are highly regulated, products and coverages are largely uniform with relatively predictable exposures and companies tend to compete for customers on the basis of price. In contrast, the specialty market provides coverage for hard-to-place risks that do not fit the underwriting criteria of standard carriers. For example, United States insurance regulations generally require an Excess and Surplus Lines (E&S) account to be declined by three admitted carriers before an E&S company may write the business. Hard-to-place risks written in the Specialty Admitted market cover insureds engaged in similar, but highly specialized activities who require a total insurance program not otherwise available from standard insurers or insurance products that are overlooked by large admitted carriers. Hard-to-place risks in the London market are generally distinguishable from standard risks due to the complexity or significant size of the risk.

Competition in the specialty insurance market tends to focus less on price and more on availability, service and other value-based considerations. While specialty market exposures may have higher perceived insurance risks than their standard market counterparts, we manage these risks to achieve higher financial returns. To reach our financial and operational goals, we must have extensive knowledge and expertise in our chosen markets. Most of our accounts are considered on an individual basis where customized forms and tailored solutions are employed.

By focusing on the distinctive risk characteristics of our insureds, we have been able to identify a variety of niche markets where we can add value with our specialty product offerings. Examples of niche markets that we have targeted include wind and earthquake exposed commercial properties, liability coverage for highly specialized professionals, horse mortality and other horse-related risks, yachts and other watercraft, high-value motorcycles and marine and energy related activities. Our market strategy in each of these areas of specialization is tailored to the unique nature of the loss exposure, coverage and services required by insureds. In each of our niche markets, we assign teams of experienced underwriters and claims specialists who provide a full range of insurance services.

Markets

Our nine underwriting units are focused on three specialty market segments. We have five underwriting units that compete in the E&S market, three that compete in the Specialty Admitted market and one that competes in the London market.

The E&S market focuses on hard-to-place risks and loss exposures that admitted insurers specifically refuse to write. E&S eligibility allows our insurance subsidiaries to underwrite unique loss exposures with more flexible policy forms and unregulated premium rates. This typically results in coverages that are more restrictive and more expensive than coverages in the standard admitted market. In

12

Table of Contents

2005, the E&S market represented approximately $33 billion, or 7%, of the $489 billion United States property and casualty (P&C) industry.(1)

We are the sixth largest domestic E&S writer in the United States as measured by direct premium writings.(1)Our five underwriting units that write in the E&S market are: Essex Excess and Surplus Lines, Shand Professional/Products Liability, Markel Brokered Excess and Surplus Lines (formerly referred to as the Investors Brokered Excess and Surplus Lines unit), Markel Southwest Underwriters and Markel Re. In 2006, we wrote $1.5 billion of business in our Excess and Surplus Lines segment.

We also write business in the Specialty Admitted market. Most of these risks, although unique and hard-to-place in the standard market, must remain with an admitted insurance company for marketing and regulatory reasons. We estimate that the Specialty Admitted market is comparable in size to the E&S market. The Specialty Admitted market is subject to more state regulation than the E&S market, particularly with regard to rate and form filing requirements, restrictions on the ability to exit lines of business, premium tax payments and membership in various state associations, such as state guaranty funds and assigned risk plans.

Our three underwriting units that write in the Specialty Admitted market are: Markel Specialty Program Insurance, Markel American Specialty Personal and Commercial Lines and Markel Global Marine and Energy. Markel Global Marine and Energy began writing business in late 2006. In 2006, we wrote $340 million of business in our Specialty Admitted segment.

The London market, which produced approximately $49 billion of gross written premium in 2005, is the largest insurance market in Europe and third largest in the world.(2)The London market is known for its ability to provide innovative, tailored coverage and capacity for unique and hard-to-place risks. It is primarily a broker market, which means that insurance brokers bring most of the business to the market. The London market is also largely a subscription market, which means that loss exposures brought into the market are typically insured by more than one insurance company or Lloyd’s syndicate, often due to the high limits of insurance coverage required. We write business on both a direct and subscription basis in the London market. When we write business in the subscription market, we prefer to participate as lead underwriter in order to control underwriting terms, policy conditions and claims handling.

Gross premium written through Lloyd’s syndicates represented approximately one-half of the London market’s international insurance business(2), making Lloyd’s the world’s second largest commercial surplus lines insurer and sixth largest reinsurer.(3)Corporate capital providers often provide a majority of a syndicate’s capacity and also often own or control the syndicate’s managing agent. This structure permits the capital provider to exert greater influence on, and demand greater accountability for, underwriting results. In 2006, corporate capital providers accounted for approximately 83% of total underwriting capacity in Lloyd’s.(3)

We participate in the London market through Markel International, which includes Markel Capital Limited (Markel Capital) and Markel International Insurance Company Limited (MIICL). Markel Capital is the corporate capital provider for our syndicate at Lloyd’s, Markel Syndicate 3000, which is managed by Markel Syndicate Management Limited. In 2006, we wrote $729 million of business in our London Insurance Market segment.

(1)Surplus Lines Market 2006, A.M. Best Special Report (September 2006).

(2)International Financial Markets in the UK, International Financial Services of London (November 2006).

(3) Lloyd’s Close Up Review 2006, Lloyd’s.

13

Table of Contents

Markel Corporation & Subsidiaries

BUSINESS OVERVIEW (continued)

In 2006, 22% of consolidated premium writings related to foreign risks (i.e., coverage for risks located outside of the United States), of which 36% were from the United Kingdom. In 2005, 21% of our premium writings related to foreign risks, of which 42% were from the United Kingdom. In 2004, 24% of our premium writings related to foreign risks, of which 40% were from the United Kingdom. In each of these years, the United Kingdom was the only individual foreign country from which premium writings were material. Premium writings are attributed to individual countries based upon location of risk.

Competition

We compete with numerous domestic and international insurance companies and reinsurers, Lloyd’s syndicates, risk retention groups, insurance buying groups, risk securitization programs and alternative self-insurance mechanisms. Competition may take the form of lower prices, broader coverages, greater product flexibility, higher quality services or higher ratings by independent rating agencies. In all of our markets, we compete by developing specialty products to satisfy well-defined market needs and by maintaining relationships with agents, brokers and insureds who rely on our expertise. This expertise is our principal means of competing. We offer over 90 major product lines. Each of these products has its own distinct competitive environment. With each of our products, we seek to compete with innovative ideas, appropriate pricing, expense control and quality service to policyholders, agents and brokers.

Few barriers exist to prevent insurers from entering our segments of the P&C industry. Market conditions and capital capacity influence the degree of competition at any point in time. Periods of intense competition, which typically include broader coverage terms, lower prices and excess underwriting capacity, are referred to as a “soft market.” A favorable insurance market is commonly referred to as a “hard market” and is characterized by stricter coverage terms, higher prices and lower underwriting capacity. During soft markets, unfavorable conditions exist due, in part, to what many perceive to be excessive amounts of capital in the industry. In an attempt to utilize their capital, many insurance companies seek to write additional premiums without appropriate regard for ultimate profitability and standard insurance companies are more willing to write specialty coverages. The opposite is typically true during hard markets.

After a decade of soft market conditions, we believe the industry began to experience favorable conditions in late 2000. The impact of the hardening market was accelerated by the significant insured losses from the terrorist attacks of September 11, 2001 and continued into 2002. Insurance market conditions then began to soften again in 2003 and 2004 and although we continued to receive rate increases compared to prior years for most product lines, the rate of increase slowed and, in certain lines, rates declined. This increase in competition continued into 2005 and new and renewal business declined as a result of our continuing commitment to adequate pricing. With the exception of large rate increases on catastrophe-exposed business, rates in 2006 were generally flat or down slightly compared to 2005. We expect that competition in the P&C insurance industry will remain strong in 2007. We remain focused on writing business that we believe will allow us to achieve our goal of underwriting profitability.

Underwriting Philosophy

By focusing on market niches where we have underwriting expertise, we seek to earn consistent underwriting profits. Underwriting profits are a key component of our strategy. We believe that the ability to achieve consistent underwriting profits demonstrates knowledge and expertise, commitment to superior customer service and the ability to manage insurance risk. We use underwriting profit or loss as a basis for evaluating our underwriting performance.

14

Table of Contents

The combined ratio is a measure of underwriting performance and represents the relationship of incurred losses, loss adjustment expenses and underwriting, acquisition and insurance expenses to earned premiums. A combined ratio less than 100% indicates an underwriting profit, while a combined ratio greater than 100% reflects an underwriting loss. In 2006, our combined ratio was 87%. See Management’s Discussion & Analysis of Financial Condition and Results of Operations for further discussion of our underwriting results.

The following graph compares our combined ratio to the P&C industry’s combined ratio for the past five years.

Underwriting Segments

We define our underwriting segments based on the areas of the specialty insurance market in which we compete. We have five underwriting units that compete in the Excess and Surplus Lines market, three that compete in the Specialty Admitted market and one that competes in the London market. See note 18 of the notes to consolidated financial statements for additional segment reporting disclosures.

Lines of business that have been discontinued in conjunction with an acquisition and non-strategic insurance subsidiaries are included in Other for purposes of segment reporting. The lines were discontinued because we believed some aspect of the product, such as risk profile or competitive environment, would not allow us to earn consistent underwriting profits.

15

Table of Contents

Markel Corporation & Subsidiaries

BUSINESS OVERVIEW (continued)

Excess and Surplus Lines Segment

Our Excess and Surplus Lines segment reported gross premium volume of $1.5 billion, earned premiums of $1.2 billion and an underwriting profit of $279.3 million in 2006.

In the E&S market, we write business through the following five underwriting units:

| • | Essex Excess and Surplus Lines (Glen Allen, VA) |

| • | Shand Professional/Products Liability (Deerfield, IL) |

| • | Markel Brokered Excess and Surplus Lines (Red Bank, NJ) |

| • | Markel Southwest Underwriters (Scottsdale, AZ) |

| • | Markel Re (Glen Allen, VA) |

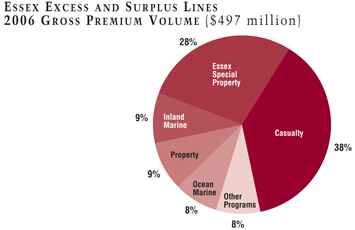

Essex Excess and Surplus Lines. The Essex Excess and Surplus Lines unit (Essex E&S unit) focuses primarily on the following products written predominately on a non-admitted basis: casualty, property, inland marine, ocean marine, physical damage, and railroad. The casualty division writes a variety of liability coverages focusing on light-to-medium casualty exposures such as artisan contractors, habitational risks, restaurants and bars, child and adult care facilities, vacant properties, office buildings and light manufacturing operations. The property division writes property insurance on classes of business ranging from small, single-location accounts to large, multi-state, multi-location accounts. Property coverages consist principally of fire, allied lines, including windstorm, hail and water damage, and more specialized property coverages. In addition, the Essex E&S unit offers coverages for catastrophe-exposed property risks on both an excess and primary basis, including earthquake and wind, through its Essex Special Property division. These risks are typically larger and are of a low frequency and high severity nature.

The Essex E&S unit’s inland marine facility provides coverages for risks that include motor truck cargo, warehouseman’s legal liability, builder’s risk and contractor’s equipment. The ocean marine facility writes risks that include marinas, hull coverage, cargo and builder’s risk for yacht manufacturers. The special transportation division focuses on physical damage coverage for all types of commercial vehicles such as trucks, buses and high-value automobiles. The railroad division writes all-risk property coverages on rolling stock and real property and liability coverages for shortline, regional, tourist and scenic railroads as well as modern commuter rail and light rail.

16

Table of Contents

The Essex E&S unit’s business is written through two distribution channels. Business written by the property and casualty divisions is primarily generated by approximately 200 professional surplus lines general agents who have limited quoting and binding authority. The Essex Special Property, inland marine, ocean marine, transportation and railroad divisions produce business on a brokerage basis through approximately 210 wholesale brokers. The Essex E&S unit seeks to be a substantial underwriter for its producers in order to enhance the likelihood of receiving the most desirable underwriting opportunities. The Essex E&S unit writes the majority of its business in Essex Insurance Company, which is admitted in Delaware and is eligible to write E&S insurance in 49 states and the District of Columbia.

Shand Professional/Products Liability. The Shand Professional/Products Liability unit focuses primarily on tailored coverages that offer unique solutions on a claims-made basis for highly specialized professions. These coverages include medical malpractice for physicians and allied healthcare risks and professional liability for lawyers, architects and engineers, agents and brokers and management consultants. Specified professions errors and omissions coverage is targeted to start-up companies, small businesses and emerging technologies. Special risks include claims-made products liability coverage focused on new business products and technology. In addition, the Shand Professional/Products Liability unit offers not-for-profit directors’ and officers’ liability and employment practices liability (EPL) coverage. The unit also provides EPL clients a full menu of loss prevention programs offering consultation services which can be accessed through telephone inquiry, the Internet and live seminars across the United States.

Business is written nationwide and is developed through approximately 325 wholesale brokers. The Shand Professional/Products Liability unit has access to both admitted and surplus lines markets in all 50 states and writes the majority of its business in Evanston Insurance Company (EIC).

17

Table of Contents

Markel Corporation & Subsidiaries

BUSINESS OVERVIEW (continued)

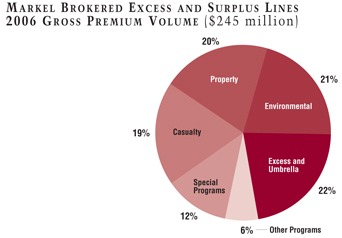

Markel Brokered Excess and Surplus Lines.The Markel Brokered Excess and Surplus Lines unit is comprised of the following seven divisions: primary casualty, property, excess and umbrella, environmental, special programs, taxi liability and surety. Primary casualty targets hard-to-place, mid-size and large general liability and products liability accounts. The property division emphasizes non-standard property placements and commercial multi-peril policies. They approach monoline property business on a participating, primary or excess of loss basis. The excess and umbrella division offers its products on both a lead and excess position. Coverage is provided primarily for commercial businesses. The environmental division offers a complete array of environmental coverages including environmental consultants’ professional liability, contractors’ pollution liability and site specific environmental impairment liability. The special programs division considers unique or hard-to-place programs that have a proven track record where we can provide value-added services. The taxi liability division provides auto liability coverage for small-to-medium-sized local cab fleets on either an admitted or non-admitted basis. The surety division concentrates on writing surety reinsurance as a broker market focusing on treaty placements for both national and regional surety underwriting companies. The Markel Brokered Excess and Surplus Lines unit provides product solutions to its insureds through approximately 325 wholesale brokers and writes the majority of its business in EIC.

Markel Southwest Underwriters.Markel Southwest Underwriters (MSU) writes commercial casualty and property coverages focusing on businesses in the western, southwestern and southeastern United States. Casualty business consists of light-to-medium liability exposures including artisan contractors, habitational risks, office buildings, light manufacturing operations and vacant properties. MSU also writes property insurance on classes of business ranging from small, single location risks to large, multi-state, multi-location risks. Property business consists principally of fire, allied lines, including windstorm, hail and water damage, and other specialized property coverages.

Most of MSU’s business is generated by approximately 80 contracted professional surplus lines general agents who have limited quoting and binding authority. MSU seeks to be a substantial underwriter for its producers in order to enhance the likelihood of receiving the most desirable underwriting opportunities. The majority of its business is written in EIC.

18

Table of Contents

Markel Re.Markel Re writes direct excess and umbrella risks as well as casualty facultative reinsurance placements. The excess and umbrella division offers its products on both a lead and excess position and coverage is provided primarily for commercial businesses. The facultative placements possess favorable underwriting characteristics, including control of individual risk selection and pricing. Additionally, Markel Re offers a specialty underwriting facility for alternative risk transfer, which has been branded Specialized Markel Alternative Risk Transfer (SMART). SMART offers innovative solutions and quality products to buyers who commit significant financial resources to risk assumption through an alternative risk entity such as a captive insurance company, risk retention group or self-insured retention. The SMART division is led by a team of experienced professionals who target production sources which include retail and wholesale brokers, reinsurance intermediaries and program managers. Markel Re’s excess and umbrella business is generated through approximately 275 professional surplus lines general agents and the casualty facultative reinsurance business is written both directly and through reinsurance brokers for approximately 50 admitted and surplus lines carriers. The majority of Markel Re’s assumed business is written in Markel Insurance Company (MIC), while the direct business is written in Essex Insurance Company, MIC and EIC.

19

Table of Contents

Markel Corporation & Subsidiaries

BUSINESS OVERVIEW (continued)

Specialty Admitted Segment

Our Specialty Admitted segment reported gross premium volume of $340.5 million, earned premiums of $317.4 million and an underwriting profit of $28.1 million in 2006.

In the Specialty Admitted market, we write business through the following three underwriting units:

| • | Markel Specialty Program Insurance (Glen Allen, VA) |

| • | Markel American Specialty Personal and Commercial Lines (Pewaukee, WI) |

| • | Markel Global Marine and Energy (Houston, TX) |

Markel Specialty Program Insurance.The Markel Specialty Program Insurance unit focuses on providing total insurance programs for businesses engaged in similar but highly specialized activities. These activities typically do not fit the risk profiles of standard insurers and make complete coverage difficult to obtain from a single insurer.

The Markel Specialty Program Insurance unit is organized into four product areas that concentrate on particular markets and customer groups. The property and casualty division writes commercial coverages for youth and recreation oriented organizations, such as children’s summer camps, conference centers, YMCAs, YWCAs, Boys and Girls Clubs, child care centers, nurseries, private and Montessori schools and gymnastics, martial arts and dance schools. This division also writes commercial coverages for social service organizations, garages, gas stations, used car dealers, moving and storage businesses, museums, art organizations, bed & breakfast and country inns, pool and spa maintenance operations and lumber products. The agriculture division specializes in insurance coverages for horse-related risks, such as horse mortality coverage and property and liability coverages for farms, boarding, breeding and training facilities as well as outfitters and guides, hunting and fishing lodges and dude ranches. The accident and health division writes liability and accident insurance for amateur sports organizations, accident and medical insurance for colleges, universities, public schools and private schools and limited benefit accident and medical insurance for selected private insurers. The Markel Risk Solutions facility works with select retail producers on a national basis to provide admitted market solutions to accounts having difficulty finding coverage in the standard marketplace. Accounts of various classes and sizes are written with emphasis placed on individual risk underwriting and pricing.

20

Table of Contents

The majority of Markel Specialty Program Insurance business is produced by approximately 4,000 retail insurance agents. Management grants very limited underwriting authority to a few carefully selected agents and controls agency business through regular audits and pre-approvals. Certain products and programs are also marketed directly to consumers or through wholesale producers. Markel Specialty Program Insurance business is underwritten primarily in MIC. MIC is licensed to write P&C insurance in all 50 states, including its state of domicile, Illinois, and the District of Columbia.

Markel American Specialty Personal and Commercial Lines.The Markel American Specialty Personal and Commercial Lines unit offers its insurance products in niche markets that are overlooked by large admitted carriers and focuses its underwriting on watercraft and commercial marine, small boat and yacht, motorcycle and all-terrain vehicle (ATV), property, motor home, special event and supplemental natural disaster coverages. The watercraft program markets personal lines insurance coverage for watercraft, older boats and high performance boats. The focus of the commercial marine program is small fishing ventures, charters and small boat rentals. The yacht program is designed for experienced owners of moderately priced yachts and the small boat program targets newer watercraft up to 26 feet. The motorcycle and ATV programs target mature riders on touring and cruising bikes and ATV riders over age 16. The property program provides coverage for mobile homes and dwellings that do not qualify for standard homeowners coverage, as well as contents coverage for renters. The motor home program includes coverage for both personally used motor homes and motor home rental operations. The special event program offers cancellation and/or liability coverage for weddings, anniversary celebrations and other personal events. The supplemental natural disaster program offers additional living expense protection for loss due to specific named perils, including flood.

Markel American Specialty Personal and Commercial Lines products are characterized by high numbers of transactions, low average premiums and creative solutions for under-served and emerging markets. The unit distributes its watercraft, small boat and yacht, property, motor home and special event products through wholesale or specialty retail producers. The motorcycle program is marketed directly to the consumer using direct mail, Internet and telephone promotions, as well as relationships with various motorcycle manufacturers, dealers and associations. The Markel American Specialty Personal and Commercial Lines unit writes the majority of its business in Markel American Insurance Company (MAIC). MAIC is licensed to write P&C business in all 50 states, including its state of domicile, Virginia, and the District of Columbia.

21

Table of Contents

Markel Corporation & Subsidiaries

BUSINESS OVERVIEW (continued)

Markel Global Marine and Energy.The Markel Global Marine and Energy unit provides insurance specifically designed to meet the needs of businesses in the marine and energy industries. The unit began writing business in late 2006 offering two product lines, excess marine and energy liability and onshore energy property. Gross premium volume for the Markel Global Marine and Energy unit was $1.8 million for 2006.

The excess liability program offers excess casualty and bumbershoot coverages for marine and energy related businesses. The onshore energy property program covers small to mid-sized onshore energy facilities such as oil refineries, chemical manufacturers and electrical power plants.

Business is produced by both wholesale and retail agents. In addition to offering its products domestically, certain products are available worldwide on a subscription basis. The program is underwritten primarily in MIC.

London Insurance Market Segment

Our London Insurance Market segment reported gross premium volume of $729.2 million, earned premiums of $624.6 million and a combined ratio of 100% in 2006.

22

Table of Contents

This segment is comprised of Markel International, which is headquartered in London, England. In addition to eight branch offices in the United Kingdom, Markel International also has offices in Spain and Canada. At Markel International, we write specialty property, casualty, professional liability and marine insurance on a direct and reinsurance basis. We take a service-oriented approach to underwriting these complex and unique risks. Business is written worldwide with approximately 22% of writings coming from the United States.

Markel International. Markel International is comprised of the following five underwriting divisions which, to better serve the needs of our customers, have the ability to write business through either MIICL or Markel Syndicate 3000:

| • | Marine and Energy |

| • | Non-Marine Property |

| • | Professional and Financial Risks |

| • | Retail |

| • | Specialty |

In the Marine and Energy division, we underwrite a portfolio of coverages for cargo, energy, hull, liability, war and specie risks. The cargo account is an international transit-based book covering many types of cargo. The energy account includes all aspects of oil and gas activities. The hull account covers physical damage to ocean-going tonnage and yachts. The liability account provides coverage for a broad range of energy liabilities, as well as traditional marine exposures including charterers, terminal operators and ship repairers. The war account covers the hulls of ships and aircraft, and other related interests, against war and associated perils. The specie account includes coverage for fine art on exhibit and in private collections, securities, bullion, precious metals, cash in transit and jewelry.

The Non-Marine Property division writes property and liability business for a wide range of insureds. We provide coverage ranging from fire to catastrophe perils such as earthquake and windstorm. Business is written in either the open market or delegated authority accounts. The open market account writes direct and facultative risks, typically for Fortune 1000 companies. Open market business is written mainly on a worldwide basis by our underwriters to London brokers, with each risk being considered on its own merits. The delegated authority account focuses mainly on small commercial insureds and is written through a network of coverholders. The delegated authority account is primarily written in the United States. Coverholders underwriting this business are closely monitored, subject to audit and must adhere to strict underwriting guidelines.

The Professional and Financial Risks division underwrites professional indemnity and directors’ and officers’ liability coverage. The professional indemnity account offers unique solutions in four main professional classes including miscellaneous professionals and consultants, construction professionals, financial service professionals and professional practices. The miscellaneous professionals and consultants class includes coverages for a wide range of professionals including management consultants, publishers, broadcasters, pension trustees and public officials. The construction class includes coverages for surveyors, engineers, architects and estate agents. The financial services class includes coverages for insurance brokers, insurance agents, financial consultants, stockbrokers, fund managers and venture capitalists. The professional practices class includes coverages for accountants and solicitors. The directors’ and officers’ liability account offers coverage to public, private and non-profit companies of all sizes on either an individual or blanket basis. The Professional and Financial Risks division writes business on a worldwide basis, limiting exposure in the United States.

23

Table of Contents

Markel Corporation & Subsidiaries

BUSINESS OVERVIEW (continued)

The Retail division offers a full range of professional liability products including professional indemnity, directors’ and officers’ liability and employment practices liability through seven branch offices in England and one branch office in Scotland. Coverage is provided for small-to-medium sized commercial property risks on both a stand-alone and package basis. The branch offices provide insureds and brokers with direct access to decision-making underwriters who possess specialized knowledge of their local markets.

The Specialty division provides property treaty reinsurance on an excess of loss and proportional basis for per risk and catastrophe exposures. A significant portion of the division’s excess of loss catastrophe and per risk treaty business comes from the United States with the remainder coming from international property treaties. The Specialty division also offers direct coverage for a number of specialist classes including financial institutions, contingency and extreme sports.

Reinsurance

We purchase reinsurance in order to reduce our retention on individual risks and enable us to write policies with sufficient limits to meet policyholder needs. As part of our underwriting philosophy, we seek to offer products with limits that do not require significant amounts of reinsurance. We purchase catastrophe reinsurance coverage for our catastrophe-exposed policies, and we seek to manage our exposures under this coverage so that no exposure to any one reinsurer is material to our ongoing business. Over the past several years, as the capital capacity of our insurance subsidiaries has grown, we have reduced the amount of reinsurance that we purchase. As a result, our retention of gross premium volume has increased consistent with our strategy to retain more of our profitable business. We do not purchase or sell finite reinsurance products or use other structures that would have the effect of discounting loss reserves.

The ceding of insurance does not legally discharge us from our primary liability for the full amount of the policies, and we will be required to pay the loss and bear collection risk if the reinsurer fails to meet its obligations under the reinsurance agreement. We attempt to minimize credit exposure to reinsurers through adherence to internal reinsurance guidelines. To become our reinsurance partner, prospective companies generally must: (i) maintain an A.M. Best Company (Best) or Standard & Poor’s (S&P) rating of “A” (excellent); (ii) maintain minimum capital and surplus of $500 million and (iii) provide collateral for recoverables in excess of an individually established amount. In addition, certain foreign reinsurers for our United States insurance operations must provide collateral equal to 100% of recoverables, with the exception of reinsurers who have been granted authorized status by an insurance company’s state of domicile. Lloyd’s syndicates generally must have a minimum of a “B” rating from Moody’s Investors Service (Moody’s) to be our reinsurers.

When appropriate, we pursue reinsurance commutations that involve the termination of ceded reinsurance contracts. Our commutation strategy related to ceded reinsurance contracts is to reduce credit exposure and eliminate administrative expenses associated with the run-off of reinsurance placed with certain reinsurers.

The following table displays balances recoverable from our ten largest reinsurers by group at December 31, 2006. The contractual obligations under reinsurance agreements are typically with individual subsidiaries of the group or syndicates at Lloyd’s and are not typically guaranteed by other

24

Table of Contents

group members or syndicates at Lloyd’s. These ten reinsurance groups represent approximately 71% of our $1.4 billion reinsurance recoverable balance.

Reinsurers | A.M. Best Rating | Reinsurance Recoverable | |||

| (dollars in thousands) | |||||

Munich Re Group | A+ | $ | 185,350 | ||

Lloyd’s of London | A | 137,906 | |||

Swiss Re Group | A+ | 130,569 | |||

XL Capital Group | A+ | 113,979 | |||

Fairfax Financial Group | A | 113,700 | |||

HDI Group | A | 78,364 | |||

White Mountains Insurance Group | A- | 64,978 | |||

Everest Re Group | A+ | 52,284 | |||

Ace Group | A+ | 48,856 | |||

Alea Group | NR(1) | 46,499 | |||

Reinsurance recoverable on paid and unpaid losses for ten largest reinsurers | 972,485 | ||||

Total reinsurance recoverable on paid and unpaid losses | $1,362,456 | ||||

(1) | NR-Not Rated. During 2005, Alea Group Holdings (Bermuda) Ltd. (Alea Group) placed its insurance operations into run off and A.M. Best withdrew its ratings. At December 31, 2006, we held collateral for 95% of our recoverable balances due from the Alea Group. |

Reinsurance recoverable balances for the ten largest reinsurers are shown before consideration of balances owed to reinsurers and any potential rights of offset, any collateral held by us and allowances for bad debts.

Reinsurance treaties are generally purchased on an annual basis and are subject to yearly renegotiations. Reinsurance needs are assessed and coverages are purchased at the operating unit level with corporate oversight. In most circumstances, the reinsurer remains responsible for all business produced prior to termination. Treaties typically contain provisions concerning ceding commissions, required reports to reinsurers, responsibility for taxes, arbitration in the event of a dispute and provisions that allow us to demand that a reinsurer post letters of credit or assets as security if a reinsurer becomes an unauthorized reinsurer under applicable regulations or if their rating falls below an acceptable level.

See note 14 of the notes to consolidated financial statements and Management’s Discussion & Analysis of Financial Condition and Results of Operations for additional information about our reinsurance programs and exposures.

25

Table of Contents

Markel Corporation & Subsidiaries

BUSINESS OVERVIEW (continued)

Investments

Our business strategy recognizes the importance of both consistent underwriting profits and superior investment returns to build shareholder value. We rely on sound underwriting practices to produce investable funds while minimizing underwriting risk. Approximately three-quarters of our investable assets come from premiums paid by policyholders. Policyholder funds are invested predominately in high-quality corporate, government and municipal bonds with relatively short durations. The balance, comprised of shareholder funds, is available to be invested in equity securities, which over the long run, have produced higher returns relative to fixed maturity investments. We seek to invest in profitable companies, with honest and talented management, that exhibit reinvestment opportunities and capital discipline, at reasonable prices. We intend to hold these investments over the long term. The investment portfolio is managed by company officers.

Total investment return includes items that impact net income, such as net investment income and realized investment gains or losses, as well as changes in unrealized holding gains or losses, which do not impact net income. Our investment portfolio produced net investment income of $271.0 million and net realized investment gains of $63.6 million in 2006. During the year ended December 31, 2006, net unrealized holding gains on the investment portfolio increased by $246.1 million. We do not lower the quality of our investment portfolio in order to enhance or maintain yields. Our focus on long-term total investment return results in variability in the level of realized and unrealized investment gains or losses from one period to the next.

We believe the ultimate success of our investment strategy is best analyzed from the review of total investment return over several years. The following table presents taxable equivalent total investment return before and after the effects of foreign currency movements.

ANNUAL TAXABLE EQUIVALENT TOTAL INVESTMENT RETURNS

| Years Ended December 31, | Weighted Average Five-Year Annual Return | Weighted Average Ten-Year Annual Return | ||||||||||||||||||||||||

| 2002 | 2003 | 2004 | 2005 | 2006 | ||||||||||||||||||||||

Equities | (8.8 | %) | 31.0 | % | 15.2 | % | (0.3 | %) | 25.9 | % | 13.9 | % | 14.3 | % | ||||||||||||

Fixed maturities | 9.8 | % | 4.5 | % | 4.8 | % | 3.9 | % | 5.2 | % | 5.4 | % | 6.0 | % | ||||||||||||

Investments in affiliates | — | — | — | — | 13.2 | % | — | — | ||||||||||||||||||

Total portfolio, before foreign currency effect | 7.0 | % | 8.3 | % | 6.6 | % | 2.9 | % | 9.6 | % | 6.8 | % | 7.3 | % | ||||||||||||

Total portfolio | 8.3 | % | 10.5 | % | 7.9 | % | 1.5 | % | 11.2 | % | 7.8 | % | 7.9 | % | ||||||||||||

Ending portfolio balance (in millions) | $ | 4,314 | $ | 5,350 | $ | 6,317 | $ | 6,588 | $ | 7,535 | ||||||||||||||||

Taxable equivalent total investment return provides a measure of investment performance that considers the yield of both taxable and tax-exempt investments on an equivalent basis.

Our disciplined, value-oriented investment approach has generated solid investment results over the long term, as evidenced in the above table.

26

Table of Contents

We monitor our portfolio to ensure that credit risk does not exceed prudent levels. S&P and Moody’s provide corporate and municipal debt ratings based on their assessment of the credit quality of an obligor with respect to a specific obligation. S&P’s ratings range from “AAA” (capacity to pay interest and repay principal is extremely strong) to “D” (debt is in payment default). Securities with ratings of “BBB” or higher are referred to as investment grade securities. Debt rated “BB” and below is regarded by S&P as having predominately speculative characteristics with respect to capacity to pay interest and repay principal. Moody’s ratings range from “Aaa” to “C” with ratings of “Baa” or higher considered investment grade.

Our fixed maturity portfolio has an average rating of “AA,” with 89% rated “A” or better by at least one nationally recognized rating organization. Our policy is to invest in securities that are rated investment grade and to minimize investments in fixed maturities that are unrated or rated below investment grade.

See “Market Risk Disclosures” in Management’s Discussion & Analysis of Financial Condition and Results of Operations for additional information about investments.

The following chart presents our fixed maturity portfolio, at estimated fair value, by rating category at December 31, 2006.

Shareholder Value

Our financial goals are to earn consistent underwriting profits and superior investment returns to build shareholder value. More specifically, we measure financial success by our ability to compound growth in book value per share at a high rate of return over a long period of time. We recognize that it is difficult to grow book value consistently each year, so we measure ourselves over a five-year period. We believe that growth in book value per share is the most comprehensive measure of our success because it includes all underwriting and investing results. For the year ended December 31, 2006, book value per share increased 32% primarily due to net income of $392.5 million and an increase of $160.0 million in net unrealized holding gains, net of taxes. For the year ended December 31, 2005, book value per share increased 3% primarily due to net income of $147.9 million partially offset by a decrease of $74.6 million in net unrealized holding gains, net of taxes. Over the past five years, we have grown book value per share at a compound annual rate of 16% to $229.78 per share.

27

Table of Contents

Markel Corporation & Subsidiaries

BUSINESS OVERVIEW (continued)

The following graph presents book value per share for the past five years.

Regulatory Environment

Our insurance subsidiaries are subject to regulation and supervision by the insurance regulatory authorities of the various jurisdictions in which they conduct business. Regulation is intended for the benefit of policyholders rather than shareholders or holders of debt securities.

United States Insurance Regulation.In the United States, state regulatory authorities have broad regulatory, supervisory and administrative powers relating to solvency standards, the licensing of insurers and their agents, the approval of forms and policies used, the nature of, and limitations on, insurers’ investments, the form and content of annual statements and other reports on the financial condition of such insurers and the establishment of loss reserves. Additionally, the business written in the Specialty Admitted segment typically is subject to regulatory rate and form review.

As an insurance holding company, we are also subject to certain state laws. Under these laws, insurance departments may, at any time, examine us, require disclosure of material transactions, require approval of certain extraordinary transactions, such as extraordinary dividends from our insurance subsidiaries to us, or require approval of changes in control of an insurer or an insurance holding company. Generally, control for these purposes is defined as ownership or voting power of 10% or more of a company’s shares.

The laws of the domicile states of our insurance subsidiaries govern the amount of dividends that may be paid to our holding company, Markel Corporation. Generally, statutes in the domicile states of our insurance subsidiaries require prior approval for payment of extraordinary as opposed to ordinary dividends. At December 31, 2006, our United States insurance subsidiaries could pay up to $335.3 million during the following 12 months under the ordinary dividend regulations.

28

Table of Contents

United Kingdom and Lloyd’s Insurance Regulation. With the enactment of the Financial Services and Markets Act, the United Kingdom government authorized the Financial Services Authority (FSA) to supervise all securities, banking and insurance businesses, including Lloyd’s. The FSA oversees compliance with established periodic auditing and reporting requirements, risk assessment reviews, minimum solvency margins and individual capital assessment requirements, dividend restrictions, restrictions governing the appointment of key officers, restrictions governing controlling ownership interests and various other requirements. Both MIICL and Markel Syndicate Management Limited are authorized and regulated by the FSA. We are required to provide 14 days advance notice to the FSA for any dividends from MIICL. In addition, our foreign insurance subsidiaries must comply with the United Kingdom Companies Act of 1985, which provides that dividends may only be paid out of distributable profits.

Other Regulation. During 2006, we made an investment in First Market Bank, a thrift institution based in Richmond, VA. In connection with this investment, we became a thrift holding company under the Home Owners Loan Act. As a thrift holding company, we are subject to regulatory oversight by the Office of Thrift Supervision and to regulations regarding acquisition of control similar to those applicable to insurance holding companies.

Ratings

Financial stability and strength are important purchase considerations of policyholders and insurance agents and brokers. Because an insurance premium paid today purchases coverage for losses that might not be paid for many years, the financial viability of the insurer is of critical concern. Various independent rating agencies provide information and assign ratings to assist buyers in their search for financially sound insurers. Rating agencies periodically re-evaluate assigned ratings based upon changes in the insurer’s operating results, financial condition or other significant factors influencing the insurer’s business. Changes in assigned ratings could have an adverse impact on an insurer’s ability to write new business.

Best assigns financial strength ratings (FSRs) to P&C insurance companies based on quantitative criteria such as profitability, leverage and liquidity, as well as qualitative assessments such as the spread of risk, the adequacy and soundness of reinsurance, the quality and estimated market value of assets, the adequacy of loss reserves and surplus and the competence, experience and integrity of management. Best’s FSRs range from “A++” (superior) to “F” (in liquidation).

Best has assigned our United States insurance subsidiaries a group FSR of “A” (excellent). Markel Syndicate 3000 has been assigned an FSR of “A” (excellent) and MIICL has been assigned an FSR of “A-” (excellent).

In addition to Best, our United States insurance subsidiaries are rated “A” (high) by Fitch Ratings (Fitch), an independent rating agency. MIICL has been assigned an FSR of “A-” (high) by Fitch.

The various rating agencies typically charge companies fees for the rating and other services they provide. During 2006, we paid rating agencies, including Best and Fitch, approximately $0.5 million for their services.

29

Table of Contents

Markel Corporation & Subsidiaries

BUSINESS OVERVIEW (continued)

A wide range of factors could materially affect our future prospects and performance. The matters addressed under “Safe Harbor and Cautionary Statements,” “Critical Accounting Estimates” and “Market Risk Disclosures” in Management’s Discussion and Analysis of Financial Condition and Results of Operations and other information included or incorporated in this report describe most of the significant risks that could affect our operations and financial results. We are also subject to the risks described below.

We may experience losses from catastrophes. Because we are a property and casualty insurance company, we frequently experience losses from man-made or natural catastrophes. Catastrophes may have a material adverse effect on operations. Catastrophes include windstorms, hurricanes, earthquakes, tornadoes, hail, severe winter weather and fires and may include terrorist events. We cannot predict how severe a particular catastrophe will be before it occurs. The extent of losses from catastrophes is a function of the total amount of losses incurred, the number of insureds affected, the frequency and severity of the events and the effectiveness of our catastrophe reinsurance coverage. Most catastrophes occur over a small geographic area; however, some catastrophes may produce significant damage in large, heavily populated areas.

Our results may be affected because actual insured losses differ from our loss reserves. Significant periods of time often elapse between the occurrence of an insured loss, the reporting of the loss to us and our payment of that loss. To recognize liabilities for unpaid losses, we establish reserves as balance sheet liabilities representing estimates of amounts needed to pay reported and unreported losses and the related loss adjustment expenses. The process of estimating loss reserves is a difficult and complex exercise involving many variables and subjective judgments. As part of the reserving process, we review historical data and consider the impact of such factors as:

| • | trends in claim frequency and severity, |

| • | changes in operations, |

| • | emerging economic and social trends, |

| • | uncertainties relating to asbestos and environmental exposures, |

| • | inflation, and |

| • | changes in the regulatory and litigation environments. |

This process assumes that past experience, adjusted for the effects of current developments and anticipated trends, is an appropriate basis for predicting future events. There is no precise method, however, for evaluating the impact of any specific factor on the adequacy of reserves, and actual results will differ from original estimates. As part of the reserving process, we regularly review our loss reserves and make adjustments as necessary. Future increases in reserves could result in additional charges.

We are subject to regulation by insurance regulatory authorities that may affect our ability to implement our business objectives. Our insurance subsidiaries are subject to supervision and regulation by the insurance regulatory authorities in the various jurisdictions in which they conduct business. Regulation is intended for the benefit of policyholders rather than shareholders or holders of debt securities. Insurance regulatory authorities have broad regulatory, supervisory and administrative powers relating to solvency standards, licensing, policy rates and forms and the form and content of financial reports.

30

Table of Contents

Our ability to make payments on debt or other obligations depends on the receipt of funds from our subsidiaries. We are a holding company, and substantially all of our operations are conducted through our subsidiaries. As a result, our cash flow and the ability to service our debt are dependent upon the earnings of our subsidiaries and on the distribution of earnings, loans or other payments by our subsidiaries to us. In addition, payment of dividends by our insurance subsidiaries may require prior regulatory notice or approval.

Competition in the property and casualty insurance industry could adversely affect our ability to grow or maintain premium volume. Among our competitive strengths have been our specialty product focus and our niche market strategy. These strengths also make us vulnerable in periods of intense competition to actions by other insurance companies who seek to write additional premiums without appropriate regard for ultimate profitability. During soft markets, it may be very difficult for us to grow or maintain premium volume levels without sacrificing underwriting profits.

Associates

At December 31, 2006, we had 1,897 employees, six of whom were executive officers.

As a service organization, continued profitability and growth are dependent upon our talented and enthusiastic associates who share our common value system as outlined in the “Markel Style.” We have structured incentive compensation plans and stock purchase plans to encourage associates to achieve corporate objectives and think and act like owners. Associates are offered many opportunities to become shareholders. Associates eligible to participate in our 401(k) plan receive one-third of our contribution in Markel stock and may purchase stock with their own contributions. Stock also may be acquired through a payroll deduction plan, and associates (other than executive officers and directors as precluded by the Sarbanes-Oxley Act) are given the opportunity to purchase stock through loans financed by us with a partially subsidized interest rate. Under our incentive compensation plans, associates may earn a meaningful bonus based on individual and company performance. For some of our executive officers and other members of senior management, part of that bonus consists of restricted stock unit awards. Additionally, executive officers and other members of senior management are required to hold Markel stock in amounts that represent a substantial multiple of their annual compensation. At December 31, 2006, we estimate associates’ ownership, including executive officers and directors, to be approximately 9% of our outstanding shares. We believe that employee stock ownership and rewarding value-added performance align associates’ interests with the interests of non-employee shareholders.

31

Table of Contents

Markel Corporation & Subsidiaries

SELECTED FINANCIAL DATA(dollars in millions, except per share data)(1, 2)

| 2006 | 2005 | 2004 | ||||||||||

RESULTS OF OPERATIONS | ||||||||||||

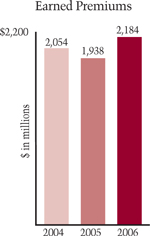

Earned premiums | $ | 2,184 | $ | 1,938 | $ | 2,054 | ||||||

Net investment income | 271 | 242 | 204 | |||||||||

Total operating revenues | 2,519 | 2,200 | 2,262 | |||||||||

Net income (loss) | 393 | 148 | 165 | |||||||||

Comprehensive income (loss) | 526 | 64 | 273 | |||||||||

Diluted net income (loss) per share | $ | 39.40 | $ | 14.80 | $ | 16.41 | ||||||

FINANCIAL POSITION | ||||||||||||

Total investments and cash and cash equivalents | $ | 7,535 | $ | 6,588 | $ | 6,317 | ||||||

Total assets | 10,088 | 9,814 | 9,398 | |||||||||

Unpaid losses and loss adjustment expenses | 5,584 | 5,864 | 5,482 | |||||||||

Convertible notes payable | — | 99 | 95 | |||||||||

Senior long-term debt | 752 | 609 | 610 | |||||||||

8.71% Junior Subordinated Debentures | 106 | 141 | 150 | |||||||||

Shareholders’ equity | 2,296 | 1,705 | 1,657 | |||||||||

Common shares outstanding (at year end, in thousands) | 9,994 | 9,799 | 9,847 | |||||||||

| OPERATING PERFORMANCE MEASURES(1, 2, 3) | ||||||||||||

OPERATING DATA | ||||||||||||

Book value per common share outstanding | $ | 229.78 | $ | 174.04 | $ | 168.22 | ||||||

Growth (decline) in book value | 32 | % | 3 | % | 20 | % | ||||||

5-Year CAGR in book value(4) | 16 | % | 11 | % | 20 | % | ||||||

Closing stock price | $ | 480.10 | $ | 317.05 | $ | 364.00 | ||||||

RATIO ANALYSIS | ||||||||||||

U.S. GAAP combined ratio(5) | 87 | % | 101 | % | 96 | % | ||||||

Investment yield(6) | 4 | % | 4 | % | 4 | % | ||||||

Taxable equivalent total investment return(7) | 11 | % | 2 | % | 8 | % | ||||||

Investment leverage(8) | 3.3 | 3.9 | 3.8 | |||||||||

Debt to total capital | 27 | % | 33 | % | 34 | % | ||||||

(1) | Reflects our acquisitions of Gryphon Holding Inc. (January 15, 1999) and Terra Nova (Bermuda) Holdings Ltd. (March 24, 2000) using the purchase method of accounting. Terra Nova (Bermuda) Holdings Ltd. was acquired in part by the issuance of 1.8 million common shares. We also issued 2.5 million common shares with net proceeds of $408 million in 2001. |

(2) | In accordance with the provisions of Statement of Financial Accounting Standards No. 142, we discontinued the amortization of goodwill as of January 1, 2002. |

(3) | Operating Performance Measures provide a basis for management to evaluate our performance. The method we use to compute these measures may differ from the methods used by other companies. See further discussion of management’s evaluation of these measures in Management’s Discussion and Analysis of Financial Condition and Results of Operations. |

32

Table of Contents

| 2003 | 2002 | 2001 | 2000 | 1999 | 1998 | 1997 | 10-Year CAGR (4) | ||||||||||||||||||||||

| $ | 1,864 | $ | 1,549 | $ | 1,207 | $ | 939 | $ | 437 | $ | 333 | $ | 333 | 22 | % | ||||||||||||||

| 183 | 170 | 171 | 154 | 88 | 71 | 69 | 18 | % | |||||||||||||||||||||

| 2,092 | 1,770 | 1,397 | 1,094 | 524 | 426 | 419 | 21 | % | |||||||||||||||||||||

| 123 | 75 | (126 | ) | (28 | ) | 41 | 57 | 50 | — | ||||||||||||||||||||

| 222 | 73 | (77 | ) | 81 | (40 | ) | 68 | 92 | — | ||||||||||||||||||||

| $ | 12.31 | $ | 7.53 | $ | (14.73 | ) | $ | (3.99 | ) | $ | 7.20 | $ | 10.17 | $ | 8.92 | — | |||||||||||||

| $ | 5,350 | $ | 4,314 | $ | 3,591 | $ | 3,136 | $ | 1,625 | $ | 1,483 | $ | 1,410 | 21 | % | ||||||||||||||

| 8,532 | 7,409 | 6,441 | 5,473 | 2,455 | 1,921 | 1,870 | 20 | % | |||||||||||||||||||||

| 4,930 | 4,367 | 3,700 | 3,037 | 1,344 | 934 | 971 | 20 | % | |||||||||||||||||||||

| 91 | 86 | 116 | — | — | — | — | — | ||||||||||||||||||||||

| 522 | 404 | 265 | 573 | 168 | 93 | 93 | — | ||||||||||||||||||||||

| 150 | 150 | 150 | 150 | 150 | 150 | 150 | — | ||||||||||||||||||||||

| 1,382 | 1,159 | 1,085 | 752 | 383 | 425 | 357 | 24 | % | |||||||||||||||||||||

| 9,847 | 9,832 | 9,820 | 7,331 | 5,590 | 5,522 | 5,474 | — | ||||||||||||||||||||||

| $ 140.38 | $ 117.89 | $ 110.50 | $ 102.63 | $ 68.59 | $ 77.02 | $ 65.18 | 17 | % | |||||||||||||||||||||

| 19 | % | 7 | % | 8 | % | 50 | % | (11 | %) | 18 | % | 33 | % | — | |||||||||||||||

| 13 | % | 13 | % | 18 | % | 21 | % | 22 | % | 23 | % | 26 | % | — | |||||||||||||||

| $ 253.51 | $ 205.50 | $ 179.65 | $ 181.00 | $155.00 | $181.00 | $156.13 | — | ||||||||||||||||||||||

| 99 | % | 103 | % | 124 | % | 114 | % | 101 | % | 98 | % | 99 | % | — | |||||||||||||||

| 4 | % | 4 | % | 5 | % | 6 | % | 5 | % | 5 | % | 5 | % | — | |||||||||||||||

| 11 | % | 8 | % | 8 | % | 12 | % | (1 | %) | 9 | % | 13 | % | — | |||||||||||||||

| 3.9 | 3.7 | 3.3 | 4.2 | 4.2 | 3.5 | 4.0 | — | ||||||||||||||||||||||

| 36 | % | 36 | % | 33 | % | 49 | % | 45 | % | 36 | % | 41 | % | — | |||||||||||||||

(4) | CAGR—compound annual growth rate. |

(5) | The U.S. GAAP combined ratio measures the relationship of incurred losses, loss adjustment expenses and underwriting, acquisition and insurance expenses to earned premiums. |

(6) | Investment yield reflects net investment income as a percentage of average invested assets. |

(7) | Taxable equivalent total investment return includes net investment income, realized investment gains or losses, the change in market value of the investment portfolio and the effect of foreign exchange movements during the period as a percentage of average invested assets. Tax-exempt interest and dividend payments are grossed up using the U.S. corporate tax rate to reflect an equivalent taxable yield. |

(8) | Investment leverage represents total invested assets divided by shareholders’ equity. |

33

Table of Contents

Markel Corporation & Subsidiaries

CONSOLIDATED BALANCE SHEETS

| December 31, | ||||||||

| 2006 | 2005 | |||||||

| (dollars in thousands) | ||||||||

ASSETS | ||||||||

Investments, available-for-sale, at estimated fair value: | ||||||||

Fixed maturities (amortized cost of $4,996,386 in 2006 and $4,586,164 in 2005) | $ | 5,000,969 | $ | 4,613,296 | ||||

Equity securities (cost of $1,059,345 in 2006 and $940,290 in 2005) | 1,766,273 | 1,378,556 | ||||||

Short-term investments (estimated fair value approximates cost) | 139,499 | 248,541 | ||||||

Investments in affiliates | 73,439 | 14,072 | ||||||

TOTAL INVESTMENTS | 6,980,180 | 6,254,465 | ||||||

Cash and cash equivalents | 555,115 | 333,757 | ||||||

Receivables | 322,982 | 334,513 | ||||||

Reinsurance recoverable on unpaid losses | 1,257,453 | 1,824,300 | ||||||

Reinsurance recoverable on paid losses | 105,003 | 91,311 | ||||||

Deferred policy acquisition costs | 218,392 | 212,329 | ||||||

Prepaid reinsurance premiums | 117,889 | 130,513 | ||||||

Goodwill | 339,717 | 339,717 | ||||||

Other assets | 191,400 | 293,193 | ||||||

TOTAL ASSETS | $ | 10,088,131 | $ | 9,814,098 | ||||

LIABILITIES AND SHAREHOLDERS’ EQUITY | ||||||||

Unpaid losses and loss adjustment expenses | $ | 5,583,879 | $ | 5,863,677 | ||||

Unearned premiums | 1,007,801 | 993,737 | ||||||

Payables to insurance companies | 58,880 | 115,613 | ||||||

Convertible notes payable (estimated fair value of $108,000 in 2005) | — | 98,891 | ||||||

Senior long-term debt (estimated fair value of $801,000 in 2006 and $647,000 in 2005) | 751,978 | 608,945 | ||||||

Junior Subordinated Deferrable Interest Debentures (estimated fair value of $111,000 in 2006 and $150,000 in 2005) | 106,379 | 141,045 | ||||||

Other liabilities | 282,821 | 286,757 | ||||||

TOTAL LIABILITIES | 7,791,738 | 8,108,665 | ||||||

Shareholders’ equity: | ||||||||

Common stock | 854,561 | 743,503 | ||||||

Retained earnings | 1,015,679 | 669,057 | ||||||

Accumulated other comprehensive income: | ||||||||

Net unrealized holding gains on fixed maturities and equity securities, net of taxes of $249,029 in 2006 and $162,889 in 2005 | 462,482 | 302,509 | ||||||

Cumulative translation adjustments, net of tax benefit of $6,094 in 2006 and $5,189 in 2005 | (11,316 | ) | (9,636 | ) | ||||

Net actuarial pension loss, net of tax benefit of $13,469 in 2006 | (25,013 | ) | — | |||||

TOTAL SHAREHOLDERS’ EQUITY | 2,296,393 | 1,705,433 | ||||||

Commitments and contingencies | ||||||||

TOTAL LIABILITIES AND SHAREHOLDERS’ EQUITY | $ | 10,088,131 | $ | 9,814,098 | ||||

See accompanying notes to consolidated financial statements.

34

Table of Contents

CONSOLIDATED STATEMENTS OF INCOME AND COMPREHENSIVE INCOME

| Years Ended December 31, | ||||||||||||

| 2006 | 2005 | 2004 | ||||||||||

| (dollars in thousands, except per share data) | ||||||||||||

OPERATING REVENUES | ||||||||||||

Earned premiums | $ | 2,184,381 | $ | 1,938,461 | $ | 2,053,887 | ||||||

Net investment income | 271,016 | 241,979 | 204,032 | |||||||||

Net realized investment gains | 63,608 | 19,708 | 4,139 | |||||||||

TOTAL OPERATING REVENUES | 2,519,005 | 2,200,148 | 2,262,058 | |||||||||

OPERATING EXPENSES | ||||||||||||

Losses and loss adjustment expenses | 1,132,579 | 1,299,983 | 1,308,343 | |||||||||

Underwriting, acquisition and insurance expenses | 767,853 | 650,323 | 673,450 | |||||||||

TOTAL OPERATING EXPENSES | 1,900,432 | 1,950,306 | 1,981,793 | |||||||||

OPERATING INCOME | 618,573 | 249,842 | 280,265 | |||||||||

Interest expense | 65,172 | 63,842 | 56,220 | |||||||||

INCOME BEFORE INCOME TAXES | 553,401 | 186,000 | 224,045 | |||||||||

Income tax expense | 160,899 | 38,085 | 58,633 | |||||||||

NET INCOME | $ | 392,502 | $ | 147,915 | $ | 165,412 | ||||||

OTHER COMPREHENSIVE INCOME (LOSS) | ||||||||||||

Net unrealized gains (losses) on securities, net of taxes: | ||||||||||||

Net holding gains (losses) arising during the period | $ | 201,318 | $ | (61,755 | ) | $ | 108,945 | |||||

Less reclassification adjustments for net gains included in net income | (41,345 | ) | (12,810 | ) | (2,690 | ) | ||||||

Net unrealized gains (losses) | 159,973 | (74,565 | ) | 106,255 | ||||||||

Currency translation adjustments, net of taxes | (1,680 | ) | (9,709 | ) | 1,010 | |||||||

Net actuarial pension loss, net of taxes | (25,013 | ) | — | — | ||||||||

TOTAL OTHER COMPREHENSIVE INCOME (LOSS) | 133,280 | (84,274 | ) | 107,265 | ||||||||

COMPREHENSIVE INCOME | $ | 525,782 | $ | 63,641 | $ | 272,677 | ||||||

NET INCOME PER SHARE | ||||||||||||

Basic | $ | 40.43 | $ | 15.05 | $ | 16.79 | ||||||

Diluted | $ | 39.40 | $ | 14.80 | $ | 16.41 | ||||||

See accompanying notes to consolidated financial statements.

35

Table of Contents

Markel Corporation & Subsidiaries

CONSOLIDATED STATEMENTS OF CHANGES IN SHAREHOLDERS‘ EQUITY

| Common Shares | Common Stock | Retained Earnings | Accumulated Other Comprehensive Income | Total | ||||||||||||||

| (in thousands) | ||||||||||||||||||

Shareholders’ Equity at January 1, 2004 | 9,847 | $ | 737,356 | $ | 375,041 | $ | 269,882 | $ | 1,382,279 | |||||||||

Net income | — | — | 165,412 | — | 165,412 | |||||||||||||

Net unrealized gains on securities, net of taxes | — | — | — | 106,255 | 106,255 | |||||||||||||

Currency translation adjustments, net of taxes | — | — | — | 1,010 | 1,010 | |||||||||||||

Comprehensive income | 272,677 | |||||||||||||||||

Issuance of common stock | 12 | — | — | — | — | |||||||||||||

Repurchase of common stock | (12 | ) | — | (3,385 | ) | — | (3,385 | ) | ||||||||||

Restricted stock units expensed | — | 1,232 | — | — | 1,232 | |||||||||||||

Tax benefit on closed stock option plans | — | 3,700 | — | — | 3,700 | |||||||||||||

Shareholders’ Equity at December 31, 2004 | 9,847 | 742,288 | 537,068 | 377,147 | 1,656,503 | |||||||||||||

Net income | — | — | 147,915 | — | 147,915 | |||||||||||||

Net unrealized losses on securities, net of taxes | — | — | — | (74,565 | ) | (74,565 | ) | |||||||||||

Currency translation adjustments, net of taxes | — | — | — | (9,709 | ) | (9,709 | ) | |||||||||||

Comprehensive income | 63,641 | |||||||||||||||||

Issuance of common stock | 1 | — | — | — | — | |||||||||||||

Repurchase of common stock | (49 | ) | — | (15,926 | ) | — | (15,926 | ) | ||||||||||

Restricted stock units expensed | — | 1,215 | — | — | 1,215 | |||||||||||||

Shareholders’ Equity at December 31, 2005 | 9,799 | 743,503 | 669,057 | 292,873 | 1,705,433 | |||||||||||||

Net income | — | — | 392,502 | — | 392,502 | |||||||||||||

Net unrealized gains on securities, net of taxes | — | — | — | 159,973 | 159,973 | |||||||||||||

Currency translation adjustments, net of taxes | — | — | — | (1,680 | ) | (1,680 | ) | |||||||||||

Net actuarial pension loss, net of taxes | — | — | — | (25,013 | ) | (25,013 | ) | |||||||||||

Comprehensive income | 525,782 | |||||||||||||||||

Repurchase of common stock | (140 | ) | — | (45,880 | ) | — | (45,880 | ) | ||||||||||

Conversion of convertible notes payable | 335 | 108,842 | — | — | 108,842 | |||||||||||||

Restricted stock units expensed | — | 1,342 | — | — | 1,342 | |||||||||||||

Tax benefit on closed stock option plans | — | 874 | — | — | 874 | |||||||||||||

SHAREHOLDERS’ EQUITY AT DECEMBER 31, 2006 | 9,994 | $ | 854,561 | $ | 1,015,679 | $ | 426,153 | $ | 2,296,393 | |||||||||

See accompanying notes to consolidated financial statements.

36

Table of Contents

CONSOLIDATED STATEMENTS OF CASH FLOWS

| Years Ended December 31, | ||||||||||||

| 2006 | 2005 | 2004 | ||||||||||

| (dollars in thousands) | ||||||||||||

OPERATING ACTIVITIES | ||||||||||||

Net income | $ | 392,502 | $ | 147,915 | $ | 165,412 | ||||||

Adjustments to reconcile net income to net cash provided by operating activities: | ||||||||||||

Deferred income tax expense (benefit) | 30,561 | (44,513 | ) | (29,800 | ) | |||||||

Depreciation and amortization | 27,610 | 29,581 | 31,336 | |||||||||

Net realized investment gains | (63,608 | ) | (19,708 | ) | (4,139 | ) | ||||||

Decrease in receivables | 11,531 | 50,274 | 34,834 | |||||||||

Increase in deferred policy acquisition costs | (6,063 | ) | (10,363 | ) | (4,295 | ) | ||||||

Increase in unpaid losses and loss adjustment expenses, net | 273,357 | 266,920 | 567,239 | |||||||||

Increase in unearned premiums, net | 26,688 | 20,541 | 7,556 | |||||||||

Increase (decrease) in payables to insurance companies | (56,733 | ) | 33,887 | (60,523 | ) | |||||||

Other | (124,252 | ) | 76,717 | (16,927 | ) | |||||||

NET CASH PROVIDED BY OPERATING ACTIVITIES | 511,593 | 551,251 | 690,693 | |||||||||

INVESTING ACTIVITIES | ||||||||||||

Proceeds from sales of fixed maturities and equity securities | 1,559,977 | 1,839,065 | 2,528,166 | |||||||||

Proceeds from maturities, calls and prepayments of fixed maturities | 173,997 | 164,150 | 248,760 | |||||||||

Cost of fixed maturities and equity securities purchased | (2,125,618 | ) | (2,444,059 | ) | (3,497,841 | ) | ||||||

Net change in short-term investments | 109,042 | (126,827 | ) | (39,702 | ) | |||||||

Cost of investments in affiliates | (58,703 | ) | (14,072 | ) | — | |||||||

Net proceeds from sale of subsidiary | — | 43,237 | — | |||||||||

Additions to property and equipment | (9,192 | ) | (29,498 | ) | (6,963 | ) | ||||||

Other | 1,715 | 727 | (116 | ) | ||||||||

NET CASH USED BY INVESTING ACTIVITIES | (348,782 | ) | (567,277 | ) | (767,696 | ) | ||||||

FINANCING ACTIVITIES | ||||||||||||

Additions to senior long-term debt | 145,402 | — | 196,816 | |||||||||

Repayments and retirement of senior long-term debt | (4,549 | ) | (3,603 | ) | (110,000 | ) | ||||||

Retirement of Junior Subordinated Deferrable Interest Debentures | (36,421 | ) | (9,627 | ) | — | |||||||

Repurchases of common stock | (45,880 | ) | (15,926 | ) | (3,385 | ) | ||||||

Other | (5 | ) | — | — | ||||||||

NET CASH PROVIDED (USED) BY FINANCING ACTIVITIES | 58,547 | (29,156 | ) | 83,431 | ||||||||