Registration Nos. 333-146207, 333-146207-01, and 333-146207-02 |

As filed with the Securities and Exchange Commission on May 23, 2008. |

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 |

PRE-EFFECTIVE AMENDMENT No. 1 TO FORM S-3

ON

FORM S-1

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933 |

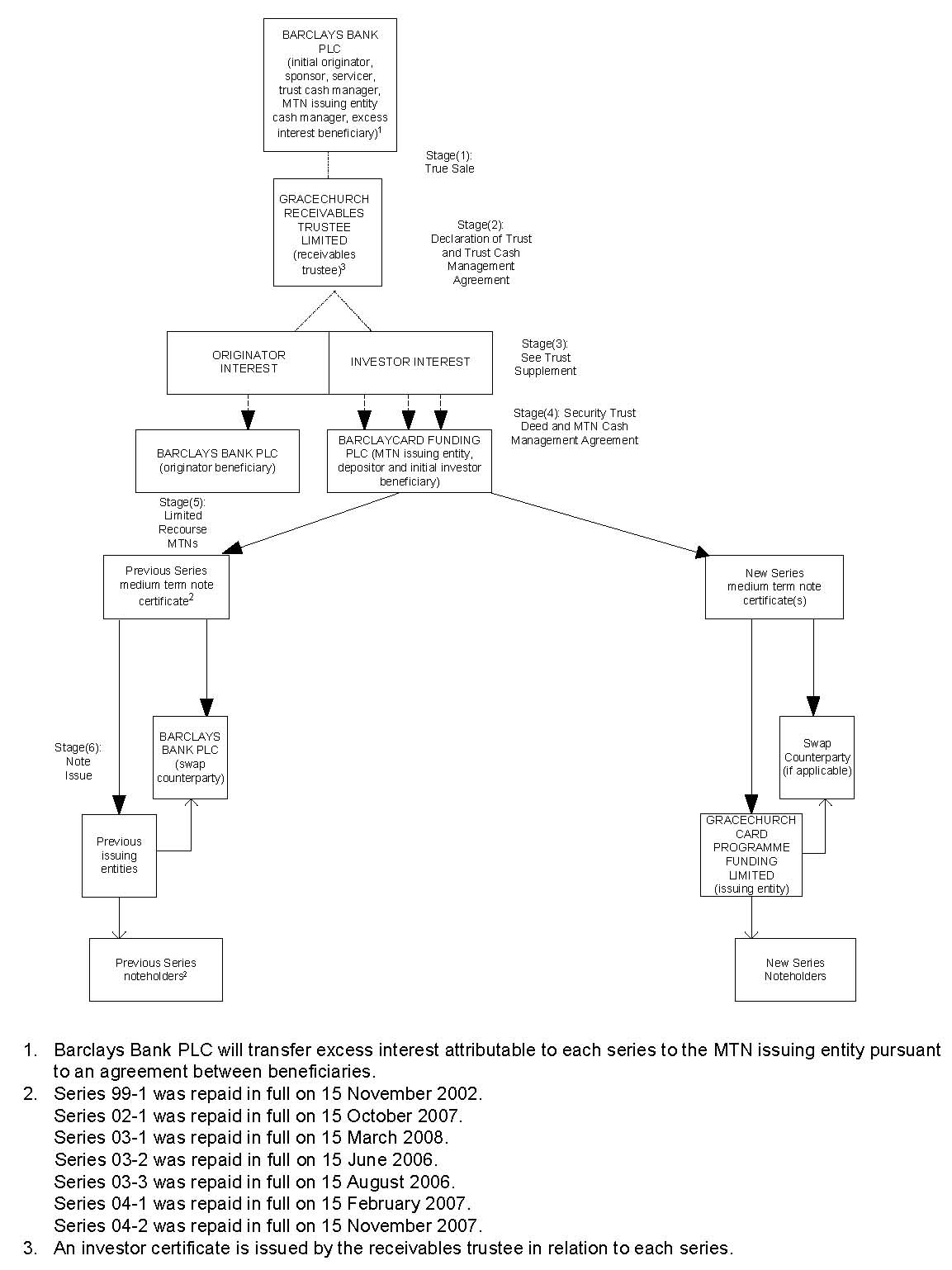

GRACECHURCH CARD PROGRAMME FUNDING LIMITED (Issuing entity in respect of the Notes) | GRACECHURCH RECEIVABLES TRUSTEE LIMITED (Receivables Trustee) | BARCLAYCARD FUNDING PLC (Depositor and MTN Issuing Entity) | |||

(Exact name of each Registrant as specified in its charter) | |||||

JERSEY, CHANNEL ISLANDS | JERSEY, CHANNEL ISLANDS | ENGLAND AND WALES | |||

(State or other jurisdictions of incorporation or organization) | |||||

6189 | |||||

(Primary Standard Industrial Classified Code Numbers) | |||||

NONE | |||||

(I.R.S. Employer Identification Numbers) | |||||

26 New Street St. Helier, Jersey JE2 3RA Channel Islands +44 1534 814814 | 26 New Street St. Helier, Jersey JE2 3RA Channel Islands +44 1534 814814 | 1 Churchill Place London E14 5HP United Kingdom +44 (0) 207 6995000 | |||

(Address, including zip code, and telephone number, including area code, of Registrants’ principal executive offices) | |||||

Giuseppe Pagano 200 Park Avenue New York, New York 10166 United States of America +1 (212) 412 4000 | |||||

(Name, address, including zip code, and telephone number, including area code, of agent for service) | |||||

| WITH COPIES TO: | |||||

Lewis Rinaudo Cohen, Esq. CLIFFORD CHANCE US LLP 31 West 52nd Street New York, NY 10019 United States of America +1 (212) 878 3144 | Michael Brady, Esq. WEIL, GOTSHAL & MANGES One South Place London EC2M 2WG United Kingdom + 44 (0) 20 7903 1000 | Robert Trefny, Esq. CLIFFORD CHANCE LLP 10 Upper Bank Street London E14 5JJ United Kingdom + 44 (0) 20 7006 1000 | |||

Approximate date of commencement of proposed sale to the public: As soon as practicable after this Registration Statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933 check the following box: o

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering: o

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer o | Accelerated filer o | |

| Non-accelerated filer ý (Do not check if a smaller reporting company) | Smaller reporting company o |

| CALCULATION OF REGISTRATION FEE |

| Title of each class of securities to be registered(1) | Amount to be registered(2) | Proposed maximum offering price per unit | Proposed maximum aggregate offering price(3) | Amount of registration fee | ||||

| Notes | $1,000,000 | 100% | $1,000,000 | $39.30 | ||||

| Medium Term Note Certificates | $1,000,000 | — | — | — | ||||

| Investor Certificates | $1,000,000 | — | — | — | ||||

| Total | — | — | $1,000,000 | $39.30 | ||||

Notes to the ‘‘Calculation of Registration Fee” Table |

| (1) | Gracechurch Receivables Trustee Limited is the registrant for the principal amount of the investor certificate; Barclaycard Funding PLC is the registrant for the medium term note certificates and Gracechurch Card Programme Funding Limited is the registrant for the notes to be issued from time to time. The investor certificate will be annotated from time to time to reflect the amendments to the principal amounts thereof. The medium term note certificates will be issued to Gracechurch Card Programme Funding Limited from time to time and will be the primary sources of payments on the notes. The medium term note certificates and the investor certificate are not being offered directly to investors. |

| (2) | With respect to any securities issued with original issue discount, the amount to be registered is calculated on the basis of the initial public offering price of such securities. With respect to securities denominated in a currency other than U.S. dollars, the amount to be registered is the U.S. dollar equivalent thereof based on the prevailing exchange rate at the time such securities are first offered. |

| (3) | Estimated solely for the purpose of calculating the registration fee pursuant to Rule 457(o) under the Securities Act. No additional consideration will be paid for the medium term note certificates or the investor certificate. |

The Registrants hereby amend this registration statement on such date or dates as may be necessary to delay its effective date until the Registrants shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

INTRODUCTORY NOTE

This Registration Statement includes:

| • | A base prospectus, filed with the United Kingdom Financial Services Authority in its capacity as the United Kingdom Listing Authority (the “UKLA”) by Gracechurch Card Programme Funding Limited (the “issuing entity”) in connection with the listing on the Official List of the UKLA of the issuing entity’s $[ ],000,000,000 medium term note programme (the “programme”); and |

| • | A prospectus supplement/final terms prepared by the issuing entity for the offering pursuant to this Registration Statement of the issuing entity’s series 2008-1 notes to be issued under the programme. |

The information in this preliminary prospectus supplement/final terms is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus supplement/final terms is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED [•], 2008

PRELIMINARY PROSPECTUS SUPPLEMENT/FINAL TERMS

(to the base prospectus dated [•], 2008)

GRACECHURCH CARD PROGRAMME FUNDING LIMITED

issuing entity

(incorporated in Jersey, Channel Islands with limited liability under registered number 98638)

Issue of $•,000,000 principal amount of series 2008-1, class A notes

$•,000,000 principal amount of series 2008-1, class B notes

$•,000,000 principal amount of series 2008-1, class C notes

$•,000,000 principal amount of series 2008-1, class D notes

under the $[•] Gracechurch Card Programme Funding Limited medium term note programme

(ultimately backed by trust property in the receivables trust)

Barclays Bank PLC

sponsor, originator, trust cash manager and servicer

Barclaycard Funding PLC

depositor and MTN issuing entity

| The issuing entity will issue | Class A notes | Class B notes | Class C notes | Class D notes | ||||

| Principal Amount | •,000,000 | •,000,000 | •,000,000 | •,000,000 | ||||

| Interest rate | • | • | • | • | ||||

| Interest Payment Dates | The 15th day of each month, beginning on •, 2008 | The 15th day of each month, beginning on •, 2008 | The 15th day of each month, beginning on •, 2008 | The 15th day of each month, beginning on •, 2008 | ||||

| Scheduled Redemption Date | •, 20•• | •, 20•• | •, 20•• | •, 20•• | ||||

| Final Redemption Date | •, 20•• | •, 20•• | •, 20•• | •, 20•• | ||||

| Price to public | • ,000,000 (or •%) | • ,000,000 (or •%) | • ,000,000 (or •%) | • ,000,000 (or •%) | ||||

| Underwriting discount or fee | • ,000,000 (or •%) | • ,000,000 (or •%) | • ,000,000 (or •%) | • ,000,000 (or •%) | ||||

| Proceeds to Sponsor | • ,000,000 (or •%) | • ,000,000 (or •%) | • ,000,000 (or •%) | • ,000,000 (or •%) |

Payments on the class B notes are subordinated to payments on the class A notes of the same series. Payments on the class C notes are subordinated to payments on the class A and class B notes of the same series. Payments on the class D notes are subordinated to payments on the class A, class B and class C notes of the same series.

Each of the class A notes, class B notes, class C notes and class D notes will have the benefit of a currency swap between the issuing entity and Barclays Bank PLC as swap counterparty.

Please review and carefully consider the Risk Factors beginning on page 21 of the base prospectus and any additional Risk Factors on page S-4 of this prospectus supplement/final terms before you purchase any notes.

Neither the United States Securities and Exchange Commission nor any state securities commission has approved or disapproved of these notes or determined if this prospectus supplement/final terms is truthful or complete. Any representation to the contrary is a criminal offence.

The ultimate source of payment on the notes will be collections on consumer credit and charge card accounts originated or acquired in the United Kingdom by Barclays Bank PLC acting through its Barclaycard division.

The notes offered in this base prospectus will be obligations of the issuing entity only. They will not be obligations of, nor will they be guaranteed by, any other party, including Barclays Bank PLC in any of its capacities, Barclays Capital, Barclays Capital Inc., Barclaycard Funding PLC, Gracechurch Receivables Trustee Limited or any of their affiliates or advisers, successors or assigns. The issuing entity will only have a limited pool of assets to satisfy its obligations on the notes.

You should read this prospectus supplement/final terms and the base prospectus carefully before you invest. A note is not a deposit and neither the notes nor the underlying receivables are insured or guaranteed by Barclays Bank PLC or by any United Kingdom or United States governmental agency.

Underwriter and Arranger

Barclays Capital

U.S. Distributor

Barclays Capital Inc.

S-ii

IMPORTANT NOTICES

In the event that any withholding or deduction for any taxes, duties, assessments or government charges of whatever nature is imposed, levied, collected, withheld or assessed on payments of principal or interest in respect of the notes or the coupons by Jersey, the United Kingdom, or any other jurisdiction or any political subdivision or any authority in or of such jurisdiction having power to tax, the issuing entity or the Paying Agents shall make such payments after such withholding or deduction and neither the issuing entity nor the Paying Agents nor any other person will be required to make any additional payments to holders of notes in respect of such withholding or deduction.

This document constitutes a prospectus supplement/final terms for the purposes of Article 5.4 of the prospectus directive and is supplemental to and must be read in conjunction with the base prospectus. Full information on the issuing entity and the offer of the notes is only available on the basis of the combination of this prospectus supplement/final terms and the base prospectus. The base prospectus is available for viewing at 5 The North Colonnade, Canary Wharf, London E14 4BB, United Kingdom and copies may be obtained from 5 The North Colonnade, Canary Wharf, London E14 4BB, United Kingdom.

The issuing entity has confirmed to the underwriters named under “Plan of Distribution” below that this prospectus supplement/final terms, when read in conjunction with the base prospectus, contains all information which is (in the context of the programme, the issue, offering and sale of the notes) material; that such information is true and accurate in all material respects and is not misleading in any material respect; that any opinions, predictions or intentions expressed in this prospectus supplement/final terms are honestly held or made and are not misleading in any material respect; that this prospectus supplement/final terms does not omit to state any material fact necessary to make such information, opinions, predictions or intentions (in the context of the programme, the issue and offering and sale of the notes) not misleading in any material respect; and that all proper enquiries have been made to verify the foregoing.

No person has been authorised to give any information or to make any representation not contained in or not consistent with this prospectus supplement/final terms or any other document entered into in relation to the programme or any information supplied by the issuing entity or such other information as is in the public domain and, if given or made, such information or representation should not be relied upon as having been authorised by the issuing entity or any underwriter.

Neither the delivery of this prospectus supplement/final terms nor the offering, sale or delivery of any note shall, in any circumstances, create any implication that the information contained in this prospectus supplement/final terms is true subsequent to the date hereof or the date upon which any future prospectus supplement/final terms (in relation to any future issue of other notes) is produced or that there has been no adverse change, or any event reasonably likely to involve any adverse change, in the condition (financial or otherwise) of the issuing entity since the date thereof or, if later, the date upon which any future prospectus supplement/final terms (in relation to any future issue of other notes) is produced or that any other information supplied in connection with the programme is correct at any time subsequent to the date on which it is supplied or, if different, the date indicated in the document containing the same.

The distribution of this prospectus supplement/final terms and the offering, sale and delivery of the notes in certain jurisdictions may be restricted by law. Persons in possession of the prospectus supplement/final terms are required by the issuing entity and the underwriters to inform themselves about and to observe any such restrictions. For a description of certain restrictions on offers, sales and deliveries of notes and on the distribution of this prospectus supplement/final terms and other offering material relating to the notes, see “Plan of Distribution” in the base prospectus.

Until a date that is 90 days after the date of this prospectus supplement/final terms, all dealers effecting transactions in this series of notes, whether or not participating in this distribution, may be required to deliver the appropriate prospectus supplement/final terms and the base prospectus. This is in addition to the obligation of underwriters to deliver a prospectus supplement/final terms and base prospectus when acting as the underwriter of the notes and with respect of their unsold allotment or subscription.

The maximum aggregate principal amount of notes outstanding at any one time under the programme will not exceed $[•] (and for this purpose, any notes denominated in another currency shall be translated into U.S. dollars at the date of the agreement to issue such notes (calculated in accordance with the provisions of the programme dealer agreement and the relevant series subscription agreement)). The maximum aggregate principal amount of notes which may be outstanding at any one time under the programme may be increased

S-iii

from time to time, subject to compliance with the relevant provisions of the programme dealer agreement and the relevant series subscription agreement.

Certain figures included in this prospectus supplement/final terms have been subject to rounding adjustments; accordingly, figures shown for the same category presented in different tables may vary slightly and figures shown as totals in certain tables may not be an arithmetic aggregation of the figures which precede them.

The information about the series 2008-1 notes appears in two separate documents: a base prospectus and this prospectus supplement/final terms. The base prospectus provides general information about each series of notes issued under the Gracechurch Card Programme Funding Limited medium term note programme, some of which may not apply to the series 2008-1 notes described in this prospectus supplement/final terms. With respect to the series 2008-1 notes, this prospectus supplement/final terms is the “relevant prospectus supplement/final terms” or the “applicable prospectus supplement/final terms” referred to in the base prospectus.

This prospectus supplement/final terms may be used to offer and sell the series 2008-1 notes only if accompanied by the base prospectus.

This prospectus supplement/final terms supplements, with respect to the series 2008-1 notes, the disclosure in the base prospectus.

You should rely only on the information in this prospectus supplement/final terms and the base prospectus, including information incorporated by reference. We have not authorised anyone to provide you with different information.

AN INVESTMENT IN THE NOTES IS ONLY SUITABLE FOR FINANCIALLY SOPHISTICATED INVESTORS WHO ARE CAPABLE OF EVALUATING THE MERITS AND RISKS OF SUCH INVESTMENT AND WHO HAVE SUFFICIENT RESOURCES TO BE ABLE TO BEAR ANY LOSSES WHICH MAY RESULT FROM SUCH INVESTMENT. IF YOU ARE IN ANY DOUBT ABOUT THE CONTENTS OF THIS BASE PROSPECTUS YOU SHOULD CONSULT YOUR STOCKBROKER, BANK MANAGER, SOLICITOR, ACCOUNTANT OR OTHER FINANCIAL ADVISER.

S-iv

S-v

This prospectus supplement/final terms supplements the disclosure in the base prospectus. The series 2008-1 notes will be governed, to the extent not described in this prospectus supplement/final terms, by the applicable provisions of the base prospectus. Unless otherwise indicated, words and expressions defined in the base prospectus shall have the same meanings below.

| Class of notes | Initial Principal Balance | % of Total | |||

| A | $• | • | |||

| B | $• | • | |||

| C | $• | • | |||

| D | $• | • | |||

| 100% |

| SERIES OF NOTES ISSUED |

| Series Number: | Series 2008-1 | ||||||||

| Class of Notes: | A | B | C | D | |||||

| Anticipated Ratings: | • | • | • | • | |||||

| Rating Agencies: | Moody’s/Standard & Poor’s | Moody’s/Standard & Poor’s | Moody’s/Standard & Poor’s | Moody’s/Standard & Poor’s | |||||

| Issue Date: | • 2008 | • 2008 | • 2008 | • 2008 | |||||

| Issue Price: | • per cent. | • per cent. | • per cent. | • per cent. | |||||

| Net Proceeds: | • | • | • | • | |||||

| Specified Currency: | Class A notes are to be denominated in US dollars. | Class B notes are to be denominated in US dollars. | Class C notes are to be denominated in US dollars. | Class D notes are to be denominated in US dollars. | |||||

| Minimum Denomination: | $100,000 | $100,000 | $100,000 | $100,000 | |||||

| Specified Denomination(s): | [$100,000 and amounts in excess thereof which are integral multiples of $10,000] | [$100,000 and amounts in excess thereof which are integral multiples of $10,000] | [$100,000 and amounts in excess thereof which are integral multiples of $10,000] | [$100,000 and amounts in excess thereof which are integral multiples of $10,000] | |||||

| Subject to Repricing Arrangements: | • | • | • | • | |||||

If yes: | |||||||||

Repricing Transfer Dates: | [Any Interest Payment Date] | [Any Interest Payment Date] | [Any Interest Payment Date] | [Any Interest Payment Date] | |||||

| Fixed or Floating Designation: | • | • | • | • | |||||

| Series Scheduled Redemption Date: | • | • | • | • | |||||

| Final Redemption Date: | • | • | • | • | |||||

| Initial Rate (if applicable): | • | • | • | • | |||||

S-1

| Margin (Until Repricing Transfer Date): | • | • | • | • | |||||

| LIBOR/EURIBOR | • | • | • | • | |||||

| Day Count Fractions: | • | • | • | • | |||||

| Interest Commencement Date: | • | • | • | • | |||||

| Floating Rate Commencement Date (if applicable): | • | • | • | • | |||||

| Interest Payment Dates: | 15th day of each month beginning • subject to adjustment for non-business days in accordance with the Business Day Convention specified below. | 15th day of each month beginning • subject to adjustment for non-business days in accordance with the Business Day Convention specified below. | 15th day of each month beginning • subject to adjustment for non-business days in accordance with the Business Day Convention specified below. | 15th day of each month beginning • subject to adjustment for non-business days in accordance with the Business Day Convention specified below. | |||||

| First Interest Payment Date: | • | • | • | • | |||||

| Interest Rate Calculations: | • | • | • | • | |||||

| Listing: | London | London | London | London | |||||

| Additional Business Centre: | London, New York, Jersey | London, New York, Jersey | London, New York, Jersey | London, New York, Jersey | |||||

| Additional Financial Centre: | London, New York, Jersey | London, New York, Jersey | London, New York, Jersey | London, New York, Jersey | |||||

| Additional Interest Margin: | • | • | • | • | |||||

| Indemnification Amount: | • | ||||||||

| Additional Details of Related Swap Agreement (if any): | • | • | • | • | |||||

| Internal Credit Support-Subordination: | Classes B, C and D | Classes C and D | Class D | N/A | |||||

| Payment Priorities and Allocation of Funds: | Within series 2008-1, amounts received by the issuing entity from the MTN issuing entity will be applied, pre-enforcement of the note trust deed and the relevant series note trust deed supplement, in a manner whereby notes of each class and sub-class will rank pari passu and pro rata among themselves without preference or priority among themselves. However, the class B notes (and every sub-class thereof (if any)) are subordinated in right of payment of interest and principal to the class A notes (and every sub-class thereof (if any)) while the |

S-2

| class C notes (and every subclass thereof (if any)) are subordinated in right of payment of interest and principal to the class A notes (and every sub-class thereof (if any)) and the class B notes (and every sub-class thereof (if any)) while the class D notes (and every subclass thereof (if any)) are subordinated in right of payment of interest and principal to the class A notes (and every sub-class thereof (if any)), the class B notes (and every sub-class thereof (if any)) and the class C notes (and every sub-class thereof (if any)). Payments due to swap counterparties (if any) will rank pari passu with payments of interest on the notes with payments to a swap counterparty for a swap with respect to the class B notes (and every sub-class thereof) being subordinate in right to the payments to a swap counterparty for a swap with respect to the class A notes (and every sub-class thereof) and with payments to a swap counterparty for a swap with respect to the class C notes (and every sub-class thereof) being subordinate in right to the payments to a swap counterparty for a swap with respect to the class A notes (and every sub-class thereof) and the class B notes (and every sub-class thereof) and with payments to a swap counterparty for a swap with respect to the class D notes (and every sub-class thereof) being subordinate in right to the payments to a swap counterparty for a swap with respect to the class A notes (and every sub-class thereof), the class B notes (and every sub-class thereof) and the class C notes (and every sub-class thereof). Following enforcement of the note trust deed and the relevant series note trust deed supplement, interest and principal in respect of each class of notes will be paid pari passu and pro rata so that the most senior class will have all accrued interest and all principal paid before any subordinated class. |

| Please see the section entitled “Securitisation Cashflows” on page 92 of the base prospectus. |

| Clearing and Settlement: | • |

| Business Day Convention: | • |

| Estimated total expenses related to admission to trading: | • |

| ERISA: | • |

| Notes treated as debt or equity for U.S. federal income tax purposes: | • |

| Required Retained Principal Percentage: | • |

| Controlled Accumulation Period: | • |

| Closing Date: | • |

| Cash Management Fee: | • |

S-3

ADDITIONAL RISK FACTORS APPLYING ONLY TO SERIES 2008-1

| Early termination of a swap agreement may expose Noteholders to the risk of currency exchange rate movement. | If a swap agreement terminates and the relevant notes do not become immediately due and payable, then the Noteholders in respect of such notes will be subject to exchange rate risk as the issuing entity will exchange GBP amounts for USD at a spot rate of exchange and there is no guarantee that such spot rate of exchange will equal the rate of exchange applicable under the swap agreement. |

| Each swap agreement may be terminated prior to payment in full of the notes | Any swap agreement may be terminated upon the occurrence of certain events. In the event that a swap agreement is terminated without replacement, an Event of Default will occur under the terms and conditions of the notes. There can be no assurance that a swap agreement will not be terminated prior to the payment in full of the notes of the relevant class. |

| Change in law may result in the imposition of withholding taxes on payments to be made under the swap agreements | Each of the issuing entity and the swap counterparty will represent in each swap agreement that, under current applicable law, they are entitled to make all payments required to be made by them under such swap agreement free and clear and without deduction for or on account of, any taxes, assessments or any other charges. In the event that the swap counterparty is required to make any such deduction due to any action taken by a taxing authority, any action brought in a court of competent jurisdiction, or a change in tax law, the swap counterparty will not be required to indemnify the issuing entity for such deduction. As a result, payments to the issuing entity may be reduced. In such circumstances, the issuing entity may as a result of a deduction for or on account of any taxes, assessments or any other charges be entitled to terminate the relevant swap agreement. |

S-4

The series 2008-1 notes will be collateralised by the series 2008-1 Medium Term Note (the “Related Medium Term Note”) which shall have the following terms as set out in the series 2008-1 medium term note supplement.

| Designation for the purposes of the security trust deed and MTN cash management agreement: | Series 2008-1 |

| Issuance Date: | •, 2008 |

| Initial Principal Amount: | • |

| Medium Term Note Certificate First Interest Payment Date: | •, 2008 |

| Medium Term Note Certificate Interest Payment Date: | [•th] day of each month beginning • subject to adjustment for non-business days. |

| Medium Term Note Certificate Interest Period: | • |

| Required Re-investment Amount: | • |

| Series Scheduled Redemption Date: | • |

| Series Termination Date: | • |

| Additional Early Redemption Events: | None/• |

| Listing: | None |

| Initial Investor Interest: | • |

| Class A Initial Investor Interest: | • |

| Class B Initial Investor Interest: | • |

| Class C Initial Investor Interest: | • |

| Class D Initial Investor Interest: | • |

| Medium Term Note Certificate Interest Rate: | • |

S-5

SERIES INVESTOR INTEREST SUPPORTING MEDIUM TERM NOTE

The series 2008-1 medium term note will be collateralised by the series 2008-1 investor interest (the “Series Investor Interest”) which shall have the following terms as set out in the series 2008-1 supplement to the declaration of trust and trust cash management agreement.

| Designation for the purposes of the Receivables Trust Deed Supplement: | Series 2008-1 | ||

| Issuance Date: | • | ||

| Initial Principal Amount: | • | ||

| First Payment Date: | • | ||

| Class A Finance Rate: | • | ||

| Class B Finance Rate: | • | ||

| Class C Finance Rate: | • | ||

| Class D Finance Rate: | • | ||

| Series Scheduled Redemption Date: | • | ||

| Controlled Deposit Amount: | • | ||

| Series Termination Date: | • | ||

| Additional Early Redemption Events: | None/ • | ||

| Series Initial Investor Interest: | £• | ||

| Release Date: | • |

The Controlled Accumulation Period Commencement Date in respect of series 2008-1 investor interest will be the first Business Day of • provided, however, that if on the first business day of the Controlled Accumulation Period, its length is determined to be less than 12 months, the Revolving Period may be extended and the start of the Controlled Accumulation Period will be postponed. The Controlled Accumulation Period will, in any event, begin no later than •.

The “Series Cash Reserve Account Percentage” will be determined on each Determination Date by the level of the quarterly excess spread percentage as follows:

| Quarterly Excess Spread Percentage | Series Cash Reserve Account Percentage | ||

| on a given day is: | on same date will be: | ||

| above • per cent. | • per cent. | ||

| above • per cent. but equal to or below • per cent. | • per cent. | ||

| above • per cent. but equal to or below • per cent | • per cent. | ||

| above • per cent. but equal to or below • per cent. | • per cent. | ||

| above • per cent. but equal to or below • per cent. | • per cent. | ||

| above • per cent. but equal to or below • per cent. | • per cent. | ||

| equal to or below • per cent. | • per cent. |

After the Series Cash Reserve Account Percentage has been increased above 0 per cent. as specified in the table above, the Series Cash Reserve Account Percentage will remain at that percentage until: (1) either it is further increased to a higher required percentage as specified in the table above, or (2) the date on which the quarterly excess spread percentage has increased to a level above that for the then current Series Cash Reserve Account Percentage. The Series Cash Reserve Account Percentage will be decreased to the appropriate percentage as stated above.

S-6

| Lead underwriter(s): | Barclays Bank PLC |

| Underwriters: | Barclays Capital |

| U.S. Distributor: | Barclays Capital Inc. |

| Issuing Entity: | Gracechurch Card Programme Funding Limited. |

| Note Trustee: | The Bank of New York, acting through its London branch. The Note Trustee’s address, at the date of this prospectus supplement/final terms, is One Canada Square, London E14 5AL, United Kingdom. |

| Principal Paying Agent and Agent Bank for the Notes: | The Bank of New York, acting through its London branch. The Principal Paying Agent will make payments of interest and principal when due on the notes. The Agent Bank will calculate the interest rates applicable to each class of notes. The Bank of New York’s address in London is One Canada Square, London E14 5AL, United Kingdom. |

| Registrar and U.S. Paying Agent: | The Bank of New York, acting through its New York branch. The Bank of New York’s address in New York is One Wall Street, New York, New York 10286, United States. |

| Receivables Trustee: | Gracechurch Receivables Trustee Limited |

| MTN Issuing Entity, Investor Beneficiary and Depositor: | Barclaycard Funding PLC |

| Sponsor, Originator and Originator Beneficiary: | Barclays Bank PLC |

| Servicer: | Barclays Bank PLC |

| Security Trustee: | The Bank of New York, acting through its London Branch |

| Swap Counterparty for Series 2008-1: | Barclays Capital |

| [Series 2008-1 Market Repricing Bank for the Class [•] Notes:] | [Barclays Capital ] |

S-7

| General |

The notes will be denominated in US dollars and the issuing entity will be obliged to make US dollar payments of interest and repayments of principal in respect of the notes. However, certain amounts received by the issuing entity will be denominated in sterling. In order to protect the issuing entity against currency exchange rate exposure, the issuing entity and the swap counterparty have entered into a currency swap transaction in relation to each class of notes.

Subject to the provisions set out under “Early Termination” below under the terms of each currency swap transaction relating to each class of notes, the issuing entity will pay to the swap counterparty:

| (a) | on or after the issue date, an amount to be paid in respect of the proceeds received by the issuing entity on the issue of the relevant class of notes; |

| (b) | on each interest payment date, an amount in sterling determined by reference to applying a floating rate of interest to the relevant currency amount (as determined pursuant to the relevant swap confirmation); and |

| (c) | on each date upon which any notes are redeemed pursuant to Condition 7 (Redemption and Purchase) of the terms and conditions of the notes, an amount in sterling determined in accordance with the provisions of the relevant swap confirmation. |

| In return, the swap counterparty will be obliged to pay to the issuing entity: |

| (a) | on or after the issue date, an amount in sterling calculated by reference to the US dollar proceeds of the issue of the relevant class of notes converted into sterling at the relevant exchange rate as provided in the relevant swap agreement; |

| (b) | on each interest payment date, an amount in US dollars determined by reference to applying a fixed or floating rate of interest (as the case may be) to the relevant currency amount; and |

| (c) | on each date upon which any notes are redeemed pursuant to Condition 7 (Redemption and Purchase) of the terms and conditions of the notes, an amount in US dollars determined in accordance with the provisions of the relevant swap confirmation. |

To ensure the issuing entity’s compliance with its ongoing periodic reporting requirements under the Exchange Act, the issuing entity and the swap counterparty expect to enter into an agreement governing the information concerning the swap counterparty to be included in such periodic reports (the “Disclosure Agreement”).

Based on a reasonable good faith estimate of probable exposure, the significance percentage of each swap agreement is [•] per cent.

| Early Termination |

Each currency swap transaction may be terminated prior to its scheduled termination date in certain circumstances, including, but not limited to, the following:

| (a) | subject to the provisions of the swap agreement in respect of such transaction, at the option of the issuing entity, after the expiration of any applicable grace period if there is a failure by the swap counterparty to pay any amounts due under such swap agreement and, at the option of the swap counterparty after the expiration of any applicable grace period, if there is a failure to pay amounts due under the swap agreement by the issuing entity; |

| (b) | at the option of the issuing entity, in respect of a rating downgrade with respect to the swap counterparty below the levels specified in the swap agreement relating to such currency swap transaction where the swap counterparty fails to take appropriate action within the requisite time period; |

| (c) | at the option of the swap counterparty, pursuant to the occurrence of an Event of Default under Condition 10 of the terms and conditions of the notes and the delivery by the note trustee of an Enforcement Notice; |

| (d) | upon the occurrence of certain other events with respect to either party to such currency swap transaction, including but not limited to certain insolvency related events, merger without an assumption of the obligations in respect of the swap agreement, or changes in law resulting in illegality; |

S-8

| (e) | in the event that there is a withholding tax imposed, (1) at the option of the swap counterparty in accordance with the provisions of the swap agreement, in relation to the issuing entity’s payments under such swap agreement and (2) at the option of the issuing entity in accordance with the provisions of the swap agreement, in relation to such swap counterparty’s payments under the swap agreement; |

| (f) | at the option of the swap counterparty or the issuing entity (provided that the relevant class of Noteholders in respect of the relevant notes shall first have directed the note trustee by way of extraordinary resolution to terminate the transaction(s) relating to such notes), in the event that there is a withholding tax imposed (1) in relation to the issuing entity’s payments under the notes or (2) in relation to any payments to the issuing entity under a medium term note certificate which corresponds to such notes; |

| (g) | at the option of the swap counterparty if any amendment and/or supplement is made to the note trust deed, the issuing entity master framework agreement or the terms and conditions of the notes without the swap counterparty’s prior written consent, where such amendment and/or supplement would be reasonably expected to result in the swap counterparty being required to pay more or receive less, were it to replace itself as swap counterparty, than it would otherwise have been required to prior to such amendment and/or supplement; and |

| (h) | at the option of the swap counterparty, in respect of only the relevant transactions or relevant portions of such transactions that correspond to any notes that may have been redeemed by the issuing entity (as determined by the swap counterparty in consultation with the issuing entity) in circumstances where some or all of a relevant series of notes have been redeemed pursuant to Condition 7(b) (Mandatory Early Redemption or Mandatory Sale of Class B Notes, Class C Notes and Class D Notes to the issuing entity) of the terms and conditions of the notes following the imposition of any requirement on the MTN Issuing Entity to withhold or deduct any amounts for or on account of tax on the payment of any principal or interest in respect of a medium term note certificate of a relevant series. |

Upon any such early termination of a currency swap transaction, either the issuing entity or the swap counterparty may be liable to make a termination payment to the other. The amount of any such termination payment will be based on the value of the swap computed in accordance with the terms of the swap agreement relating to such currency swap transaction, in the first instance on the basis of market quotations of the cost of entering into a swap transaction with the same terms and conditions that would have the effect of preserving the respective full payment obligations of the parties, in accordance with the procedures set forth in such swap agreement. Any such termination payment may, if interest rates and/or the relevant currency exchange rate had changed significantly, be substantial.

Upon termination of a currency swap transaction and the swap agreement relating to such currency swap transaction if no replacement swap transaction has been obtained the security under the Note Trust Deed (and the Note Trust Deed Supplement) in respect of Series 2008-1 will become enforceable. If such security is enforced, the proceeds thereof will be applied in payment of amounts set out under the order of priority of payments set forth in the terms and conditions of the notes of such series. In the event that a swap agreement with respect to a specific class is terminated other than as a result of a Swap Counterparty Swap Event of Default (as defined below), then any termination payment to be paid to the swap counterparty by the issuing entity in accordance with the early termination provisions of such swap agreement shall rank pari passu with only those payments to be made to the holders of the relevant class of notes to which such swap agreement relates.

Events constituting a Swap Counterparty Swap Event of Default (as defined on page [•] of the base prospectus) may result in the early termination of the relevant swap agreement. In the event that a swap agreement is terminated as a result of a Swap Counterparty Swap Event of Default, then any termination payment to be paid to the swap counterparty by the issuing entity in accordance with the early termination provisions of such swap agreement shall be subordinated to any payments to be made under the relevant notes.

The swap counterparty’s payment obligations pursuant to the relevant swap agreement are subject to the condition that no event of default has occurred and is continuing with respect to the issuing entity pursuant to the relevant swap agreement.

S-9

| Taxation |

Neither the issuing entity nor the swap counterparty is obliged under each swap agreement to gross up if withholding taxes are imposed on payments made under such swap agreement.

In the event that any withholding tax is imposed on payments to be made to the issuing entity under any currency swap transaction then the issuing entity may terminate such currency swap transaction and either the issuing entity or the swap counterparty may be required to pay a swap termination payment to the other party. In the event that any withholding tax is imposed on payments to be made by the issuing entity under any currency swap transaction, [the swap counterparty may terminate such currency swap transaction and either the issuing entity or the swap counterparty may be required to pay a swap termination payment to the other party] [to be confirmed - consider amending Additional Risk Factor for Withholding Tax above] or the swap counterparty shall be entitled to deduct amounts in the same proportion (as calculated in accordance with the provisions of the confirmation relating to such transaction) from the corresponding payment due from it. In [such event] [the latter scenario], payments on the relevant class will be subject to deferral in proportion to the amount so deducted. In the event that any withholding tax is imposed on payments due by the swap counterparty under a swap agreement, the issuing entity shall not be entitled to deduct corresponding amounts from the corresponding payments due from it and payments on the relevant series will be subject to deferral in proportion to the amount so withheld by the swap counterparty.

Pursuant to the provisions of the swap agreements, if on the next date that either party was required to make a payment under a swap agreement, such party would be required by any applicable law or relevant taxing authority or court of competent jurisdiction to withhold any amount from such payment in respect of tax, such party will inform the other party and will use all reasonable efforts (which will not require such party to incur a loss, excluding immaterial, incidental expenses) to, within 20 days after informing the other party, restructure the affected transaction or transfer all its rights and obligations under the relevant swap agreement to another of its offices or affiliates so as to avoid any such requirement to withhold any amount in respect of tax, provided that such party will only effect a transfer or restructuring in accordance with the transfer provisions in the swap agreements. If such party is not able to make such a transfer or restructuring it will give notice to that effect within such 20 day period, whereupon the other party may effect such a transfer or restructuring within 30 days after having being informed of the requirement to withhold, provided that it will only effect a transfer or restructuring in accordance with the transfer provisions in the swap agreements. Any such transfer by either party will be subject to and conditional upon the prior written consent of the other party, which consent will not be withheld if such other party’s policies in effect at such time would permit it to enter into transactions with the transferee on the terms proposed. Any such restructuring by either party will be subject to and conditional upon the confirmation by Standard and Poor's and the prior written consent of the other party, which consent will not be unreasonably withheld. If neither party is able to arrange the transfer or restructuring, as set out above, the party which is not required to withhold any amount in respect of tax from such payment may terminate the relevant currency swap transaction.

| Rating Downgrade or Withdrawal |

If the swap counterparty is downgraded below the ratings specified in the relevant swap agreement (in accordance with the requirements of Standard & Poor’s and Moody’s), or if the rating of the swap counterparty is withdrawn, then the swap counterparty will, in accordance with the provisions of and subject to the timeframes specified in the relevant swap agreement, be required to take certain remedial measures which may include: (a) providing collateral in accordance with a mark to market collateral agreement between the swap counterparty and the issuing entity (the Credit Support Annex, as defined below), (b) obtaining a guarantee from a guarantor that satisfies the requirements specified in the relevant swap agreement, (c) transferring the relevant swap agreement to an entity that satisfies the requirements specified in the relevant swap agreement, or (d) in respect of a downgrade or rating withdrawal by Standard & Poor’s only, taking such other actions as it may agree with Standard & Poor’s.

In accordance with the requirements of Standard & Poor’s and Moody’s, if the swap counterparty remains a party to the swap agreement and the swap counterparty is subject to further downgrades, then the swap counterparty will be subject to additional, more restrictive requirements. If the swap counterparty is downgraded by Standard & Poor’s or Moody’s and the swap counterparty fails to comply with the applicable ratings downgrade provisions as set out in the relevant swap agreement, the issuing entity may terminate such swap agreement in accordance with the terms of the relevant swap agreement. Where the swap counterparty provides collateral in accordance with the terms of the relevant swap agreement, such collateral will be credited to the issuing entity distribution account and amounts in respect of such collateral may be returned by the issuing entity to the swap counterparty from time to time in accordance with the terms of the swap agreement and the Credit Support Annex.

S-10

The swap counterparty may, subject to certain conditions specified in the swap agreement, including certain requirements of Standard & Poor’s and Moody’s, transfer its rights and obligations in respect of the swap agreement to another entity. See “Transfers” below.

| Credit Support Annex |

The swap counterparty will enter into a 1995 ISDA Credit Support Annex (Bilateral Form Transfer) with the issuing entity (the “Credit Support Annex”) on or prior to the closing date in support of the swap counterparty’s obligations under the swap agreement.

Pursuant to the terms of the Credit Support Annex, if at any time the swap counterparty is required to provide collateral in respect of any of its obligations under the swap agreement, the Credit Support Annex will provide that, from time to time and subject to the conditions specified in the Credit Support Annex and the swap agreement, the swap counterparty will make transfers of cash or securities by way of collateral to the issuing entity in support of its obligations under the swap agreement and the issuing entity will be obliged to return such collateral in accordance with the terms of the Credit Support Annex.

| Interest Deferral |

In certain circumstances payments due to be made by either party under the swap agreement may be deferred and to the extent such payments are deferred interest shall accrue in respect thereof.

| Transfers |

Except as stated under “Taxation” above, or as otherwise permitted under each swap agreement and as provided below, neither the issuing entity nor the swap counterparty is permitted to assign, novate or transfer as a whole or in part any of its rights, obligations or interests under such swap agreement.

Any transfer by the issuing entity of its interests under a swap agreement to any other entity shall be subject to the consent of the note trustee, Standard & Poor’s and Moody’s.

The issuing entity may transfer any interest under a swap agreement to any other entity with the swap counterparty’s prior written consent, except that such consent is not required in the case of a transfer, charge or assignment to the note trustee as contemplated in the note trust deed or any note trust deed supplement thereto in relation to a relevant series.

The swap counterparty may transfer all its rights and obligations with respect to a swap agreement to any other entity (a “Transferee”) subject to the satisfaction of certain conditions, including, but not limited to the following:

| (a) | it has given five Business Days prior written notice to the note trustee; |

| (b) | the Transferee is an eligible replacement, as defined in the Moody’s rating methodology, and the Transferee’s short-term, unsecured and unsubordinated debt obligations are then rated not less than “A-1” by Standard & Poor’s (or its equivalent by any substitute rating agency) or such Transferee’s obligations under the swap agreement are guaranteed by an entity whose short-term, unsecured and unsubordinated debt obligations are then rated not less than “A-1” by Standard & Poor’s (or its equivalent by any substitute rating agency) provided that Standard & Poor’s has had sight of such guarantee; |

| (c) | a termination event or an event of default does not occur under the swap agreement as a result of such transfer; |

| (d) | the Transferee contracts with the issuing entity on terms that (1) have the same economic effect as the terms of the swap agreement in respect of any obligation (whether absolute or contingent) to make payment or delivery after the effective date of such transfer and (2) insofar as they do not relate to payment or delivery obligations, are, in all material respects, no less beneficial for the issuing entity than the terms of the swap agreement immediately before such transfer; and |

| (e) | (if the Transferee is domiciled in a different country from both the swap counterparty and the issuing entity) Standard & Poor’s has provided prior written notification that the then current ratings of the notes will not be adversely affected. |

S-11

The swap counterparty, Barclays Bank PLC (“Barclays”), is described in the section entitled “Barclays Bank PLC” in the base prospectus.

The obligations of Barclays under the swap agreements entered into with the issuing entity in respect of the notes are not insured by the FDIC or any other agency or insurer.

S-12

OTHER SERIES OF NOTES AND MEDIUM TERM NOTE CERTIFICATES ISSUED

| Notes – Gracechurch Card Programme Funding Limited and predecessors |

The table below sets forth the principal characteristics of the other series previously issued by other issuing entities that are outstanding at the date of this prospectus supplement/final terms, in connection with the receivables trust and the receivables assigned by the originator. For more information with respect to any series, any prospective investor should contact Barclays Capital, 5 The North Colonnade, Canary Wharf, London E14 4BB, United Kingdom, Attention Securitisation Group. Barclaycard will provide, without charge, to any prospective purchaser of the notes, a copy of the disclosure document for any such other publicly-issued series.

| Series 05-1 | |||||

| Class | Tranche Size | Interest Rate | |||

| Class A | $1,350,000,000 | One month U.S.D LIBOR + 0.01 | % | ||

| Class B | $75,000,000 | One month U.S.D LIBOR + 0.14 | % | ||

| Class C | $75,000,000 | One month U.S.D LIBOR + 0.33 | % | ||

| relevant Issuance Date: | 21 June 2005 | ||||

| Scheduled Redemption Date: | 15 June 2008 | ||||

| Legal Final Redemption Date: | 15 June 2010 | ||||

| Series 05-2 | ||||

| Class | Tranche Size | Interest Rate | ||

| Class A | $1,350,000,000 | One month U.S.D LIBOR + 0.01 | % | |

| Class B | $75,000,000 | One month U.S.D LIBOR + 0.15 | % | |

| Class C | $75,000,000 | One month U.S.D LIBOR + 0.31 | % | |

| relevant Issuance Date: | 20 September 2005 | |||

| Scheduled Redemption Date: | 15 September 2008 | |||

| Legal Final Redemption Date: | 15 September 2010 | |||

S-13

| Series 05-3 | ||||

| Class | Tranche Size | Interest Rate | ||

| Class A1 | €650,000,000 | One month EURIBOR + 0.08 | % | |

| Class A2 | £700,000,000 | 3 Month Sterling LIBOR + 0.08 | % | |

| Class B1 | €72,500,000 | 3 Month EURIBOR + 0.25 | % | |

| Class B2 | £15,000,000 | 3 Month Sterling LIBOR + 0.25 | % | |

| Class C1 | €68,000,000 | 3 Month EURIBOR + 0.45 | % | |

| Class C2 | £18,000,000 | 3 Month Sterling LIBOR + 0.45 | % | |

| relevant Issuance Date: | 20 October 2005 | |||

| Scheduled Redemption Date: | 15 October 2010 | |||

| Legal Final Redemption Date: | 15 October 2012 | |||

| Series 05-4 | ||||

| Class | Tranche Size | Interest Rate | ||

| Class A | $900,000,000 | One month U.S.D LIBOR + 0.01 | % | |

| Class B | $50,000,000 | One month U.S.D LIBOR + 0.15 | % | |

| Class C | $50,000,000 | One month U.S.D LIBOR + 0.28 | % | |

| relevant Issuance Date: | 28 November 2005 | |||

| Scheduled Redemption Date: | 17 November 2008 | |||

| Legal Final Redemption Date: | 15 November 2010 | |||

| Series 06-1 | ||||

| Class | Principal Balance | Interest Rate | ||

| Class A1 | €60,000,000 | One month EURIBOR + 2.45 | % | |

| Class A2 | £71,500,000 | 1 Month Sterling LIBOR +2.45 | % | |

| relevant Issuance Date: | 28 September 2006 | |||

| Scheduled Redemption Date: | 15 October 2010 | |||

| Legal Final Redemption Date: | 15 October 2012 | |||

S-14

| Medium Term Note Certificates – Barclaycard Funding PLC |

Series | Issuance Date | Tranche Size | Note Interest Rate currently in effect | Scheduled Redemption Date | Final Redemption Date | |||||

| 05-1 | 21 June 2005 | £824,764,942 | three month sterling LIBOR – plus 0.0530% | 15 June 2008 | 15 June 2010 | |||||

| 05-2 | 20 September 2005 | £815,239,545 | For monthly interest periods up to and including July 2008, the interest rate applicable will be three month sterling LIBOR plus 0.0551%; for the interest period commencing in July 2008, the interest rate applicable will be two month sterling LIBOR plus 0.0551%; | 15 September 2008 | 15 September 2010 | |||||

| 05-3 | 20 October 2005 | £1,273,702,000 | three month sterling LIBOR plus 0.1228% | 15 October 2010 | 15 October 2012 | |||||

| 05-4 | 28 November 2005 | £583,600,817 | three month sterling LIBOR plus 0.0556% | 17 November 2008 | 15 November 2010 | |||||

| 06-1 | 28 September 2006 | £111,890,441 | one-month sterling LIBOR plus 2.585% | 15 October 2010 | 15 October 2012 |

S-15

The following tables show information relating to the historic performance of Eligible Accounts originated using Barclays’ underwriting criteria. The receivables from these accounts will ultimately back the notes and comprise the receivables trust (the “Securitised Portfolio”). All Eligible Receivables arising on designated product lines, as described under “The Receivables – Assignment of Receivables to the Receivables Trustee” in the base prospectus, are included in the Securitised Portfolio.

Static Pool Information

[Static pool information regarding the performance of the receivables in the receivables trust since [•] Quarter 200[•] is being provided through a website at http://[*]. Such information, to the extent that it relates to periods before January 1, 2006 shall not be deemed to be part of this prospectus or part of the registration statement of which this prospectus is a part.]

Receivable Yield Considerations

The following table sets forth the gross revenues from finance charges and fees billed to accounts in the Securitised Portfolio, for each of the years ended 2007, 2006, 2005, 2004 and 2003 and for the [3] months ended [31 March 2008]. Each table has been provided by Barclaycard and has not been audited. These revenues vary for each account based on the type and volume of activity for each account. The historical yield figures in these tables are calculated on an accrual basis. Collections of receivables included in the receivables trust will be on a cash basis and may not reflect the historical yield experience in the table. For further detail, please see the base prospectus.

Securitised Portfolio Yield

(non percentage amounts are expressed in sterling)

3 Months Ended 31 March 2008 | Year Ended | |||||||||||

31 December 2007 | 31 December 2006 | 31 December 2005 | 31 December 2004 | 31 December 2003 | ||||||||

| Average Receivables Outstanding(1) (2) | • | 7,644,449,748 | 8,240,046,846 | 9,127,756,808 | 8,789,036,883 | 8,274,226,639 | ||||||

| Finance Charges(3) | • | 1,067,421,976 | 1,106,903,362 | 1,063,839,826 | 961,325,011 | 962,287,676 | ||||||

| Fees(3) | • | 120,811,317 | 192,459,829 | 243,943,641 | 233,872,119 | 220,385,404 | ||||||

| Total Recoveries | • | 84,142,232 | 113,176,992 | 121,728,191 | 119,717,964 | 85,647,951 | ||||||

| Foreign Exchange | • | 29,750,175 | 34,284,252 | 39,083,509 | 41,952,089 | 45,784,484 | ||||||

| Interchange | • | 128,421,099 | 131,904,797 | 155,416,714 | 176,211,134 | 191,405,583 | ||||||

| Yield from Finance Charges(4) | • | 13.96% | 13.43% | 11.65% | 10.94% | 11.63% | ||||||

| Yield from Fees | • | 1.58% | 2.34% | 2.67% | 2.66% | 2.66% | ||||||

| Yield from Recoveries | • | 1.10% | 1.37% | 1.33% | 1.36% | 1.04% | ||||||

| Yield from Foreign Exchange | • | 0.39% | 0.42% | 0.43% | 0.48% | 0.55% | ||||||

| Yield from Interchange(4) | • | 1.68% | 1.60% | 1.70% | 2.00% | 2.31% | ||||||

| Total Yield from Charges, Fees and Interchange(4) | • | 18.71% | 19.16% | 17.79% | 17.44% | 18.20% | ||||||

| Notes: |

| (1) | The receivables outstanding on the accounts consist of amounts due from obligors as posted to the accounts as of the date above. |

| (2) | Average receivables outstanding is the average of the month end balances for the period indicated. |

| (3) | Finance Charges and Fees are comprised of monthly periodic charges and other credit card fees net of adjustments made pursuant to Barclays normal servicing procedures, including removal of incorrect or disputed monthly periodic finance charges. |

| (4) | Yield percentages for the [3] months ended [31 March 2008] are presented on an annualised basis. |

[Discussion of information presented in table to follow]

S-16

DELINQUENCY AND LOSS EXPERIENCE

The following tables set forth the delinquency and loss experience of the Securitised Portfolio for each of the periods shown. The Securitised Portfolio includes platinum, gold and classic VISA and MasterCard credit cards and the Premier VISA charge card. The Securitised Portfolio currently does not include the portfolio of credit card accounts acquired by Barclaycard with Barclays PLC’s purchase of Woolwich in October 2000 or the portfolio of credit card accounts purchased from Providian’s U.K. operations in April 2002 or the portfolio of store card accounts purchased from Clydesdale Financial Services in May 2003. Because the economic environment may change, we cannot assure you that the delinquency and loss experience of the Securitised Portfolio will be the same as the historical experience set forth below.

The delinquency statistics are obtained from billing cycle information as opposed to month end positions.

S-17

Delinquency and Loss Experience

Securitised Portfolio

(non percentage amounts are expressed in sterling)

| Year Ended | |||||||||||||||||||||||||||||||||

3 Months Ended 31 March 2008 | 31 December 2007 | 31 December 2006 | 31 December 2005 | 31 December 2004 | 31 December 2003 | ||||||||||||||||||||||||||||

Receivables | Percentage of Total Receivables | Receivables | Percentage of Total Receivables | Receivables | Percentage of Total Receivables | Receivables | Percentage of Total Receivables | Receivables | Percentage of Total Receivables | Receivables | Percentage of Total Receivables | ||||||||||||||||||||||

| Receivables Outstanding | • | • | 7,835,499,807 | 100% | 7,867,599,274 | 100% | 8,649,205,272 | 100% | 9,319,428,059 | 100% | 8,526,736,246 | 100% | |||||||||||||||||||||

| Receivables Delinquent: | |||||||||||||||||||||||||||||||||

| Up to 29 days | • | • | 644,755,721 | 8.23% | 759,464,725 | 9.65% | 874,426,101 | 10.11% | 985,816,513 | 10.58% | 1,196,377,796 | 14.03% | |||||||||||||||||||||

| 30-59 days | • | • | 128,202,385 | 1.64% | 171,990,942 | 2.19% | 192,094,847 | 2.22% | 187,126,137 | 2.01% | 197,718,817 | 2.32% | |||||||||||||||||||||

| 60-89 days | • | • | 71,284,632 | 0.91% | 103,234,499 | 1.31% | 109,091,082 | 1.26% | 89,217,231 | 0.96% | 87,201,085 | 1.02% | |||||||||||||||||||||

| 90-119 days | • | • | 44,562,875 | 0.57% | 77,695,561 | 0.99% | 79,135,091 | 0.91% | 60,498,851 | 0.65% | 57,575,248 | 0.68% | |||||||||||||||||||||

| 120-149 days | • | • | 32,995,680 | 0.42% | 62,901,373 | 0.80% | 64,730,738 | 0.75% | 47,973,708 | 0.51% | 45,450,061 | 0.53% | |||||||||||||||||||||

| 150-179 days | • | • | 30,170,615 | 0.39% | 57,918,154 | 0.74% | 55,024,538 | 0.64% | 39,333,457 | 0.42% | 33,771,806 | 0.40% | |||||||||||||||||||||

| 180 days or more | • | • | 23,867,638 | 0.30% | 45,359,061 | 0.58% | 8,116,022 | 0.09% | 6,248,656 | 0.07% | 2,880,022 | 0.03% | |||||||||||||||||||||

| Total 30 days or more Delinquent | • | • | 331,083,825 | 4.23% | 519,099,591 | 6.60% | 508,192,317 | 5.88% | 430,398,038 | 4.62% | 424,597,040 | 4.98% | |||||||||||||||||||||

| Note: |

| The Receivables Outstanding on the accounts consist of all amounts due from account holders as posted to the accounts as of the respective dates set forth above. |

S-18

Net Charge-off Experience

Securitised Portfolio

(non percentage amounts are expressed in sterling)

Year Ended | ||||||||||||||||||||||||

3 Months Ended 31 March 2008 | 31 December 2007 | 31 December 2006 | 31 December 2005 | 31 December 2004 | 31 December 2003 | |||||||||||||||||||

Receivables | Percentage of Total Receivables | Receivables | Percentage of Total Receivables | Receivables | Percentage of Total Receivables | Receivables | Percentage of Total Receivables | Receivables | Percentage of Total Receivables | Receivables | Percentage of Total Receivables | |||||||||||||

| Average Receivables Outstanding (1) (4) | 7,644,449,748 | 100.00% | 8,240,046,846 | 100.00% | 9,127,756,808 | 100.00% | 8,789,036,883 | 100.00% | 8,274,226,639 | 100.00% | 7,465,464,580 | 100.00% | ||||||||||||

| Total Gross Charge-Offs(2) (4) | 582,231,384 | 7.62% | 737,497,154 | 8.95% | 584,218,300 | 6.40% | 478,032,471 | 5.44% | 419,128,023 | 5.07% | 422,145,364 | 5.65% | ||||||||||||

| Recoveries(3) (4) | 84,142,232 | 1.10% | 122,970,703 | 1.49% | 121,728,191 | 1.33% | 119,717,964 | 1.36% | 85,647,951 | 1.04% | 67,430,553 | 0.90% | ||||||||||||

| Total Net Charge-Offs(4) | 498,089,152 | 6.52% | 614,526,451 | 7.46% | 462,490,108 | 5.07% | 358,314,507 | 4.08% | 333,480,072 | 4.03% | 354,714,811 | 4.75% | ||||||||||||

| Total Net Charge-Offs as a percentage of Average Receivables Outstanding(4) | 6.52% | 7.46% | 5.07% | 4.08% | 4.03% | 4.75% | ||||||||||||||||||

| Notes: |

| (1) | Average receivables outstanding is the average of the month end balances during the period indicated. |

| (2) | Total gross charge-offs are total principal and fee charge-offs before recoveries and do not include the amount of any reductions in average receivables outstanding due to fraud, returned goods, customer disputes or other miscellaneous credit adjustments. See “The Receivables” in the accompanying base prospectus. |

| (3) | Recoveries are payments received in respect of principal and fee amounts on accounts which have been previously written off. |

| (4) | All percentages shown above are annualised. |

[Discussion of information presented in table to follow]

S-19

The following table sets forth the highest and lowest cardholder monthly payment rates for the Securitised Portfolio during any month in the periods shown and the average cardholder monthly payment rates for all months during the periods shown, in each case calculated as a percentage of total opening monthly receivables outstanding during the periods shown. Payment rates shown in the table are based on amounts which would be deemed payments of Principal Receivables and Finance Charge Receivables with respect to the related credit card accounts.

Cardholder Monthly Payment Rates

Securitised Portfolio

3 Months Ended | Year Ended | |||||||||||

31 March 2008 | 31 December 2007 | 31 December 2006 | 31 December 2005 | 31 December 2004 | 31 December 2003 | |||||||

| Lowest Month | • | • | • | • | • | • | ||||||

| Highest Month | • | • | • | • | • | • | ||||||

| Monthly Average | • | • | • | • | • | • | ||||||

[Discussion of information presented in table to follow]

S-20

The following tables summarise the Securitised Portfolio by various criteria as of the billing dates of accounts in the month ending on 31 December 2007. Each table has been provided by Barclays Bank PLC and has not been audited. Because the future composition of the Securitised Portfolio may change over time, these tables are not necessarily indicative of the composition of the Securitised Portfolio at any time subsequent to 31 December 2007.

For an indication of the credit quality of the cardholders whose receivables are included in the Securitised Portfolio, investors may refer to the discussion under “Barclaycard and the Barclaycard Card Portfolio” in the accompanying base prospectus (page 60), and to the historical performance of the Securitised Portfolio included in this prospectus supplement/final terms and of the historical performance of the Securitised Portfolio available as set forth under “Portfolio Information – Static Pool Information”. In particular, significant indicatives of the credit quality are the accountholders’ payment behaviour summarized in the table “Composition by Payment Behaviour – Securitised Portfolio” (page S-23) and the delinquency profile of the Securitised Portfolio set forth in the tables “Composition by Period of Delinquency – Securitised Portfolio” (page S-22) and “Delinquency and Loss Experience – Securitised Portfolio” (page S-18).

Composition by Account Balance

Securitised Portfolio

Account Balance Range | Total Number of Accounts | Percentage of Total Number of Accounts | Receivables | Percentage of Total Receivables | |||||

| Credit Balance | 533,076 | 6.41 | % | - £20,176,560 | -0.26 | % | |||

| Nil Balance | 2,731,340 | 32.84 | % | £0 | 0.00 | % | |||

| £0.01 – £5,000.00 | 4,672,041 | 56.18 | % | £5,015,308,766 | 64.01 | % | |||

| £5000.01 – £10,000.00 | 336,051 | 4.04 | % | £2,302,059,780 | 29.38 | % | |||

| £10,000.01 – £15,000.00 | 38,967 | 0.47 | % | £444,950,166 | 5.68 | % | |||

| £15,000.01 – £20,000.00 | 3,312 | 0.04 | % | £55,923,517 | 0.71 | % | |||

| £20,000.01 – £25,000.00 | 931 | 0.01 | % | £20,716,424 | 0.26 | % | |||

| £25,000.01 and more | 465 | 0.01 | % | £16,717,714 | 0.21 | % | |||

| TOTAL | 8,316,183 | 100.00 | % | £7,835,499,807 | 100.00 | % |

S-21

Composition by Credit Limit

Securitised Portfolio

Credit Limit Range | Total Number of Accounts | Percentage of Total Number of Accounts | Receivables | Percentage of Total Receivables | |||||

| £0 – £500.00 | 828,148 | 9.96 | % | £127,670,747 | 1.63 | % | |||

| £500.01 – £1,000.00 | 746,893 | 8.98 | % | £217,595,898 | 2.78 | % | |||

| £1,000.01 – £1,500.00 | 555,694 | 6.68 | % | £212,983,239 | 2.72 | % | |||

| £1,500.01 – £2,000.00 | 526,943 | 6.34 | % | £279,506,838 | 3.57 | % | |||

| £2,000.01 – £2,500.00 | 515,562 | 6.20 | % | £279,807,326 | 3.57 | % | |||

| £2,500.01 – £3,000.00 | 603,123 | 7.25 | % | £322,181,870 | 4.11 | % | |||

| £3,000.01 – £3,500.00 | 754,384 | 9.07 | % | £446,693,557 | 5.70 | % | |||

| £3,500.01 – £4,000.00 | 506,077 | 6.09 | % | £343,442,739 | 4.38 | % | |||

| £4,000.01 – £4,500.00 | 406,595 | 4.89 | % | £343,501,039 | 4.38 | % | |||

| £4,500.01 – £5,000.00 | 437,978 | 5.27 | % | £427,672,526 | 5.46 | % | |||

| £5,000.01 – £10,000.00 | 2,018,865 | 24.28 | % | £3,364,107,284 | 42.93 | % | |||

| £10,000.01 – £15,000.00 | 355,101 | 4.27 | % | £1,230,586,860 | 15.71 | % | |||

| £15,000.01 – £20,000.00 | 45,798 | 0.55 | % | £161,071,035 | 2.06 | % | |||

| £20,000.01 – £25,000.00 | 10,971 | 0.13 | % | £51,076,908 | 0.65 | % | |||

| £25,000.01 and more | 4,051 | 0.05 | % | £27,601,940 | 0.35 | % | |||

| TOTAL | 8,316,183 | 100.00 | % | £7,835,499,807 | 100.00 | % |

Composition by Period of Delinquency

Securitised Portfolio

Period of Delinquency (Days Contractually Delinquent) | Total Number of Accounts | Percentage of Total Number of Accounts | Receivables | Percentage of Total Receivables | |||||

| Not Delinquent | • | • | % | £6,277,278,438 | 80.11 | % | |||

| Up to 29 days | • | • | % | £644,755,721 | 8.23 | % | |||

| 30-59 days | • | • | % | £128,202,385 | 1.64 | % | |||

| 60 – 89 days | • | • | % | £71,284,632 | 0.91 | % | |||

| 90-119 days | • | • | % | £44,562,875 | 0.57 | % | |||

| 120-149 days | • | • | % | £32,995,680 | 0.42 | % | |||

| 150-179 days | • | • | % | £30,170,615 | 0.39 | % | |||

| 180 or more days | • | • | % | £23,867,638 | 0.30 | % | |||

| Repayment Programme | • | • | % | £582,381,822 | 7.43 | % | |||

| TOTAL | • | 100.0 | % | £7,835,499,807 | 100.0 | % | |||

S-22

Composition by Account Age

Securitised Portfolio

Account Age | Total Number of Accounts | Percentage of Total Number of Accounts | Receivables | Percentage of Total Receivables | |||||

| 0 – 3 months | 171,643 | 2.06 | % | £148,654,924 | 1.90 | % | |||

| 3- 6 months | 192,657 | 2.32 | % | £221,022,106 | 2.82 | % | |||

| 6 – 9 months | 150,311 | 1.81 | % | £168,078,966 | 2.15 | % | |||

| 9 – 12 months | 119,855 | 1.44 | % | £102,542,848 | 1.31 | % | |||

| 12 – 15 months | 116,721 | 1.40 | % | £71,640,234 | 0.91 | % | |||

| 15 – 18 months | 116,874 | 1.41 | % | £66,803,663 | 0.85 | % | |||

| 18 – 21 months | 112,813 | 1.36 | % | £79,275,729 | 1.01 | % | |||

| 21 – 24 months | 107,974 | 1.30 | % | £71,380,121 | 0.91 | % | |||

| 2 – 3 years | 404,594 | 4.87 | % | £237,047,986 | 3.03 | % | |||

| 3 – 4 years | 646,763 | 7.78 | % | £463,626,584 | 5.92 | % | |||

| 4 – 5 years | 604,872 | 7.27 | % | £580,067,219 | 7.40 | % | |||

| 5 – 10 years | 1,790,560 | 21.53 | % | £1,828,325,595 | 23.33 | % | |||

| Over 10 years | 3,780,546 | 45.46 | % | £3,797,033,831 | 48.46 | % | |||

| TOTAL | 8,316,183 | 100.00 | % | £7,835,499,807 | 100.00 | % |

Composition by Payment Behaviour

Securitised Portfolio

Payment Behaviour | Total Number of Accounts | Percentage of Total Number of Accounts | Receivables | Percentage of Total Receivables | |||||

| Receivables Accounts with minimum payment made | • | • | % | £• | • | % | |||

| Accounts with full payment made | • | • | % | £• | • | % |

S-23

Geographic Distribution of Accounts

Securitised Portfolio

Region | Total Number of Accounts | Percentage of Total Number of Accounts | Receivables | Percentage of Total Receivables | Total Number of Accounts with Active Balances | Percentage of Total Number of Accounts with Active Balances | |||||||

| East | 932,611 | 11.36 | % | £887,383,247 | 11.50 | % | • | • | % | ||||

| East Midlands | 493,954 | 5.99 | % | £467,325,606 | 6.10 | % | • | • | % | ||||

| London | 1,444,641 | 17.81 | % | £1,394,345,570 | 19.33 | % | • | • | % | ||||

| North East | 436,787 | 5.35 | % | £400,274,893 | 5.15 | % | • | • | % | ||||

| North West | 731,654 | 9.00 | % | £683,610,501 | 8.96 | % | • | • | % | ||||

| Northern Ireland | 110,266 | 1.25 | % | £86,907,362 | 1.24 | % | • | • | % | ||||

| Rest of UK | 31,629 | 0.39 | % | £34,057,566 | 0.42 | % | • | • | % | ||||

| Scotland | 341,651 | 3.70 | % | £311,562,595 | 4.25 | % | • | • | % | ||||

| South East | 1,290,775 | 15.86 | % | £1,279,432,044 | 16.91 | % | • | • | % | ||||

| South West | 669,844 | 8.13 | % | £624,092,741 | 8.08 | % | • | • | % | ||||

| Wales | 351,519 | 4.50 | % | £316,233,960 | 4.07 | % | • | • | % | ||||

| West Midlands | 651,264 | 8.04 | % | 600,504,217 | 7.81 | % | • | • | % | ||||

| Yorks & Humb | 507,810 | 6.14 | % | £475,739,935 | 6.17 | % | • | • | % | ||||

| Unknown Postcode | 139,154 | 0.31 | % | £165,595,814 | 0.40 | % | • | • | % | ||||

| Non-UK | 182,624 | 2.18 | % | £108,433,757 | 1.33 | % | • | • | % | ||||

| TOTAL | 8,316,183 | 100.00 | % | £7,835,499,807 | 101.72 | % | • | 100.0 | % | ||||

S-24

| Names of underwriters: | [Barclays Capital] | |

| Stabilising Manager (if any): | [Give names] | |

| Additional Selling Restrictions: | [Give Details] |

Class A | Class B | Class C | Class D | ||||||

| ISIN: | • | • | • | • | |||||

| Common Code: | • | • | • | • | |||||

| CUSIP: | • | • | • | • |

Subject to the terms and conditions of the programme dealer agreement as supplemented by the relevant subscription agreement for these series 2008-1 notes, the issuing entity has agreed to sell to each of the underwriters named below, and each of those underwriters has severally agreed to purchase, the Principal Amount of these series 2008-1 notes set forth opposite its name:

| Underwriters | Class A | Class B | Class C | Class D | Aggregate Amount | ||||||

| • | • | • | • | • | • | ||||||

| • | • | • | • | • | • | ||||||

| Total | $ | ||||||||||

The several underwriters have agreed, subject to the terms and conditions of the programme dealer agreement and the subscription agreement, to purchase all $• aggregate principal amount of the series 2008-1 class A, class B, class C and class D notes if any of such notes are purchased.

After the public offering, the public offering price and other selling terms may be changed by the underwriters.

In connection with the sale of these series 2008-1 notes, the underwriters may engage in:

| • | over-allotments, in which members of the syndicate selling these series 2008-1 notes sell more notes than the issuing entity actually sold to the syndicate, creating a syndicate short position; |

| • | stabilising transactions, in which purchases and sales of these series 2008-1 notes may be made by the members of the selling syndicate at prices that do not exceed a specified maximum; |

| • | syndicate covering transactions, in which members of the selling syndicate purchase these series 2008-1 notes in the open market after the distribution has been completed in order to cover syndicate short positions; and |

| • | penalty bids, by which underwriters reclaim a selling concession from a syndicate member when any of these series 2008-1 notes originally sold by that syndicate member are purchased in a syndicate covering transaction to cover syndicate short positions. |

These stabilising transactions, syndicate covering transactions and penalty bids may cause the price of these series 2008-1 to be higher than it would otherwise be. These transactions, if commenced, may be discontinued at any time.

The issuing entity has agreed to indemnify the underwriters against certain liabilities, including liabilities under applicable securities laws.

S-25

The gross proceeds of the issue of the notes will be $•. The sum of the fees and commissions payable on the issue of the notes is estimated to be •. The fees and commissions payable on the issue of the notes will not be deducted from the gross proceeds of the issue. The issuing entity will use its reasonable endeavours to claim an amount equal to such fees and commissions under the Indemnity Agreement such that Barclays Bank PLC shall reimburse the issuing entity for its payment of such fees and commissions. The proceeds of the issue of the notes after exchanging such amounts into sterling pursuant to the relevant swap agreement will be applied by the issuing entity, to purchase the series 2008-1 medium term note issued by the MTN issuing entity on the closing date. The net proceeds of the issue of the class A notes will be •, the net proceeds of the class B notes will be •, the net proceeds of the class C notes will be • and the net proceeds of the class D notes will be •.

S-26

WHERE YOU CAN FIND MORE INFORMATION