UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

(Mark One)

| x | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended September 30, 2010

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number: 0-32259

ALIGN TECHNOLOGY, INC.

(Exact name of registrant as specified in its charter)

| | |

| Delaware | | 94-3267295 |

(State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification Number) |

2560 Orchard Parkway

San Jose, California 95131

(Address of principal executive offices)

(408) 470-1000

(Registrant’s telephone number, including area code)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| | | | | | |

| Large accelerated filer | | x | | Accelerated filer | | ¨ |

| | | |

| Non-accelerated filer | | ¨ (Do not check if a smaller reporting company) | | Smaller reporting company | | ¨ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

The number of shares outstanding of the registrant’s Common Stock, $0.0001 par value, as of October 29, 2010 was 76,311,295.

ALIGN TECHNOLOGY, INC.

INDEX

Invisalign, Align, ClinCheck, Invisalign Assist, Invisalign Teen and Vivera, amongst others, are trademarks belonging to Align Technology, Inc. and are pending or registered in the United States and other countries.

2

PART I—FINANCIAL INFORMATION

ITEM 1 FINANCIAL STATEMENTS

ALIGN TECHNOLOGY, INC.

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS

(in thousands, except per share data)

(unaudited)

| | | | | | | | | | | | | | | | |

| | | Three Months Ended

September 30, | | | Nine Months Ended

September 30, | |

| | | 2010 | | | 2009 | | | 2010 | | | 2009 | |

Net revenues: | | | | | | | | | | | | | | | | |

Invisalign (1) | | $ | 91,170 | | | $ | 75,092 | | | $ | 279,413 | | | $ | 212,748 | |

Non-case | | | 4,777 | | | | 4,177 | | | | 14,820 | | | | 12,969 | |

| | | | | | | | | | | | | | | | |

Total net revenues | | | 95,947 | | | | 79,269 | | | | 294,233 | | | | 225,717 | |

| | | | | | | | | | | | | | | | |

Cost of revenues | | | | | | | | | | | | | | | | |

Invisalign | | | 19,090 | | | | 18,491 | | | | 55,978 | | | | 50,278 | |

Non-case | | | 1,924 | | | | 1,777 | | | | 6,594 | | | | 5,753 | |

| | | | | | | | | | | | | | | | |

Total cost of revenues | | | 21,014 | | | | 20,268 | | | | 62,572 | | | | 56,031 | |

| | | | | | | | | | | | | | | | |

Gross profit | | | 74,933 | | | | 59,001 | | | | 231,661 | | | | 169,686 | |

| | | | | | | | | | | | | | | | |

Operating expenses: | | | | | | | | | | | | | | | | |

Sales and marketing | | | 26,905 | | | | 27,687 | | | | 83,790 | | | | 84,649 | |

General and administrative | | | 16,203 | | | | 16,224 | | | | 46,159 | | | | 46,231 | |

Research and development | | | 6,592 | | | | 5,611 | | | | 19,104 | | | | 16,471 | |

Restructurings | | | — | | | | — | | | | — | | | | 1,319 | |

Litigation settlement | | | 3,310 | | | | 69,673 | | | | 3,310 | | | | 69,673 | |

Insurance settlement | | | — | | | | — | | | | (8,666 | ) | | | — | |

| | | | | | | | | | | | | | | | |

Total operating expenses | | | 53,010 | | | | 119,195 | | | | 143,697 | | | | 218,343 | |

Profit (loss) from operations | | | 21,923 | | | | (60,194 | ) | | | 87,964 | | | | (48,657 | ) |

Interest and other income (expense), net | | | (83 | ) | | | (271 | ) | | | (480 | ) | | | 434 | |

| | | | | | | | | | | | | | | | |

Net profit (loss) before provision for income taxes | | | 21,840 | | | | (60,465 | ) | | | 87,484 | | | | (48,223 | ) |

Provision for (benefit from) income taxes | | | 5,025 | | | | (10,523 | ) | | | 23,136 | | | | (5,462 | ) |

| | | | | | | | | | | | | | | | |

Net profit (loss) | | $ | 16,815 | | | $ | (49,942 | ) | | $ | 64,348 | | | $ | (42,761 | ) |

| | | | | | | | | | | | | | | | |

Net profit (loss) per share: | | | | | | | | | | | | | | | | |

Basic | | $ | 0.22 | | | $ | (0.72 | ) | | $ | 0.85 | | | $ | (0.64 | ) |

| | | | | | | | | | | | | | | | |

Diluted | | $ | 0.22 | | | $ | (0.72 | ) | | $ | 0.83 | | | $ | (0.64 | ) |

| | | | | | | | | | | | | | | | |

Shares used in computing net profit (loss) per share: | | | | | | | | | | | | | | | | |

Basic | | | 76,081 | | | | 69,528 | | | | 75,653 | | | | 67,278 | |

| | | | | | | | | | | | | | | | |

Diluted | | | 78,109 | | | | 69,528 | | | | 77,852 | | | | 67,278 | |

| | | | | | | | | | | | | | | | |

| (1) | The nine months ended September 30, 2010 includes a $14.3 million release of previously deferred revenue for Invisalign Teen replacement aligners. |

The accompanying notes are an integral part of these unaudited condensed consolidated financial statements.

3

ALIGN TECHNOLOGY, INC.

CONDENSED CONSOLIDATED BALANCE SHEETS

(in thousands, except per share data)

(unaudited)

| | | | | | | | |

| | | September 30,

2010 | | | December 31,

2009 | |

ASSETS | | | | | | | | |

Current assets: | | | | | | | | |

Cash and cash equivalents | | $ | 264,924 | | | $ | 166,487 | |

Marketable securities, short-term | | | 7,396 | | | | 19,978 | |

Accounts receivable, net of allowance for doubtful accounts of $655 and $1,033, respectively | | | 63,811 | | | | 54,537 | |

Inventories | | | 2,382 | | | | 2,046 | |

Prepaid expenses and other current assets | | | 19,429 | | | | 18,251 | |

| | | | | | | | |

Total current assets | | | 357,942 | | | | 261,299 | |

| | | | | | | | |

Marketable securities, long term | | | 7,829 | | | | — | |

Property and equipment, net | | | 28,102 | | | | 24,971 | |

Goodwill | | | 478 | | | | 478 | |

Intangible assets, net | | | 2,888 | | | | 4,988 | |

Deferred tax asset, net | | | 43,778 | | | | 61,535 | |

Other assets | | | 4,218 | | | | 1,969 | |

| | | | | | | | |

Total assets | | $ | 445,235 | | | $ | 355,240 | |

| | | | | | | | |

| | |

LIABILITIES AND STOCKHOLDERS’ EQUITY | | | | | | | | |

Current liabilities: | | | | | | | | |

Accounts payable | | $ | 5,826 | | | $ | 6,122 | |

Accrued liabilities | | | 44,074 | | | | 42,822 | |

Deferred revenues | | | 30,136 | | | | 32,299 | |

| | | | | | | | |

Total current liabilities | | | 80,036 | | | | 81,243 | |

| | | | | | | | |

Other long-term liabilities | | | 5,797 | | | | 961 | |

| | | | | | | | |

Total liabilities | | | 85,833 | | | | 82,204 | |

| | | | | | | | |

Commitments and contingencies (Notes 5 and 8) | | | | | | | | |

Stockholders’ equity: | | | | | | | | |

Preferred stock, $0.0001 par value (5,000 shares authorized; none issued) | | | — | | | | — | |

Common stock, $0.0001 par value (200,000 shares authorized; 76,255 and 74,568 shares issued and outstanding, respectively) | | | 8 | | | | 7 | |

Additional paid-in capital | | | 547,228 | | | | 525,073 | |

Accumulated other comprehensive income, net | | | 317 | | | | 455 | |

Accumulated deficit | | | (188,151 | ) | | | (252,499 | ) |

| | | | | | | | |

Total stockholders’ equity | | | 359,402 | | | | 273,036 | |

| | | | | | | | |

Total liabilities and stockholders’ equity | | $ | 445,235 | | | $ | 355,240 | |

| | | | | | | | |

The accompanying notes are an integral part of these unaudited condensed consolidated financial statements.

4

ALIGN TECHNOLOGY, INC.

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(in thousands)

(unaudited)

| | | | | | | | |

| | | Nine Months Ended,

September 30, | |

| | | 2010 | | | 2009 | |

Cash Flows from Operating Activities: | | | | | | | | |

Net profit (loss) | | $ | 64,348 | | | $ | (42,761 | ) |

Adjustments to reconcile net profit (loss) to net cash provided by operating activities: | | | | | | | | |

Deferred income taxes | | | 17,631 | | | | 740 | |

Depreciation and amortization | | | 8,694 | | | | 7,582 | |

Amortization of intangibles | | | 2,100 | | | | 2,100 | |

Stock-based compensation | | | 12,138 | | | | 12,011 | |

Litigation settlement costs paid in stock | | | — | | | | 56,524 | |

Amortization of prepaid royalties | | | 827 | | | | 1,906 | |

(Benefit from) provision for doubtful accounts | | | (10 | ) | | | 958 | |

Loss on retirement and disposal of fixed assets | | | 60 | | | | 20 | |

Changes in assets and liabilities: | | | | | | | | |

Accounts receivable | | | (9,962 | ) | | | (3,167 | ) |

Inventories | | | (343 | ) | | | 74 | |

Prepaid expenses and other assets | | | (3,086 | ) | | | (7,036 | ) |

Accounts payable | | | 13 | | | | 816 | |

Accrued and other long-term liabilities | | | 6,260 | | | | (912 | ) |

Deferred revenues | | | (1,666 | ) | | | 11,051 | |

| | | | | | | | |

Net cash provided by operating activities | | | 97,004 | | | | 39,906 | |

| | | | | | | | |

Cash Flows from Investing Activities: | | | | | | | | |

Purchase of property and equipment | | | (11,932 | ) | | | (4,084 | ) |

Purchases of marketable securities | | | (12,742 | ) | | | (33,940 | ) |

Maturities of marketable securities | | | 17,474 | | | | 40,910 | |

Other assets | | | (1,356 | ) | | | 35 | |

| | | | | | | | |

Net cash (used in) provided by investing activities | | | (8,556 | ) | | | 2,921 | |

| | | | | | | | |

Cash Flows from Financing Activities: | | | | | | | | |

Proceeds from issuance of common stock | | | 10,907 | | | | 6,376 | |

Payments on short-term obligations | | | — | | | | (136 | ) |

Employees’ taxes paid upon the vesting of restricted stock units | | | (889 | ) | | | (264 | ) |

| | | | | | | | |

Net cash provided by financing activities | | | 10,018 | | | | 5,976 | |

| | | | | | | | |

Effect of foreign exchange rate changes on cash and cash equivalents | | | (29 | ) | | | 58 | |

Net increase in cash and cash equivalents | | | 98,437 | | | | 48,861 | |

Cash and cash equivalents at beginning of period | | | 166,487 | | | | 87,100 | |

| | | | | | | | |

Cash and cash equivalents at end of period | | $ | 264,924 | | | $ | 135,961 | |

| | | | | | | | |

The accompanying notes are an integral part of these unaudited condensed consolidated financial statements.

5

ALIGN TECHNOLOGY, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(unaudited)

Note 1. Summary of Significant Accounting Policies

Basis of presentation

The accompanying unaudited Condensed Consolidated Financial Statements have been prepared by Align Technology, Inc. (“we”, “our”, or “Align”) in accordance with the rules and regulations of the Securities and Exchange Commission (SEC) and contain all adjustments, including normal recurring adjustments, necessary to present fairly our financial position as of September 30, 2010, our results of operations for the three and nine months ended September 30, 2010 and 2009, and our cash flows for the nine months ended September 30, 2010 and 2009. The Condensed Consolidated Balance Sheet as of December 31, 2009 was derived from the December 31, 2009 audited financial statements. Revenues and cost of revenues in prior period amounts have been reclassified to conform with the current period presentation. These reclassifications had no impact on previously reported gross profit or financial position.

The results of operations for the three and nine months ended September 30, 2010 are not necessarily indicative of the results that may be expected for the year ending December 31, 2010 or any other future period, and we make no representations related thereto. The information included in this Quarterly Report on Form 10-Q should be read in conjunction with “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” “Quantitative and Qualitative Disclosures About Market Risk” and the Consolidated Financial Statements and notes thereto included in Items 7, 7A and 8, respectively, of the our Annual Report on Form 10-K for the year ended December 31, 2009.

The preparation of financial statements in accordance with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the amounts reported in our Condensed Consolidated Financial Statements and accompanying notes. Actual results could differ materially from those estimates.

Revenue recognition

Invisalign Teen is delivered in a single shipment except for six replacement aligners that are included in the price of the product and may be ordered at any time throughout treatment. We use vendor specific objective evidence of fair value to allocate revenue to the replacement aligners and recognize the residual revenue upon initial shipment. Through the second quarter of 2010, we deferred 100 percent of the fair value for the six replacement aligners. This deferred revenue was subsequently recognized as the replacement aligners were shipped or when the case was completed. Management evaluated the actual usage of replacement aligners since the launch of Invisalign Teen nearly two years ago, and believes that there is sufficient historical evidence to establish an estimated usage rate. As a result, in June 2010, we reduced deferred revenue for Invisalign Teen replacement aligners by $14.3 million to reflect the estimated usage for in-process cases and starting in July 2010, we began recognizing the fair value of the replacement aligners when they are shipped. We believe that this estimated usage is reasonable and appropriate because of the relative stability of the Invisalign Teen replacement utilization since it was first offered. Although we are not expecting any material changes, we will continue to analyze the usage of replacement aligners and may adjust the estimated usage rate as necessary.

Recent Accounting Pronouncements

In September 2009, the Financial Accounting Standards Board (FASB) amended the Accounting Standards Codification (ASC) as summarized in Accounting Standards Update (ASU) 2009-13, “Revenue Recognition (ASC 605): Multiple-Deliverable Revenue Arrangements.” Guidance in ASC 605-25 on revenue arrangements with multiple deliverables has been amended to require an entity to allocate revenue to deliverables in an arrangement using its best estimate of selling prices if the vendor does not have vendor-specific objective evidence or third-party evidence of selling prices, and to eliminate the use of the residual method and require the entity to allocate revenue using the relative selling price method. The new guidance also requires expanded quantitative and qualitative disclosures about revenue from arrangements with multiple deliverables. The update is effective for fiscal years beginning on or after June 15, 2010, with early adoption permitted. Adoption may either be on a prospective basis for new revenue arrangements entered into after adoption of the update, or by retrospective application. We are planning to adopt the update effective January 1, 2011 and are assessing the potential impact to our consolidated financial statements.

6

ALIGN TECHNOLOGY, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

(unaudited)

In January 2010, the FASB issued ASU 2010-06, “Fair Value Measurements and Disclosures (ASC 820): Improving Disclosures about Fair Value Measurements.” This update will require (1) an entity to disclose separately the amounts of significant transfers in and out of Levels 1 and 2 fair value measurements and to describe the reasons for the transfers; and (2) information about purchases, sales, issuances and settlements to be presented separately (i.e. present the activity on a gross basis rather than net) in the reconciliation for fair value measurements using significant unobservable inputs (Level 3 inputs). This guidance clarifies existing disclosure requirements for the level of disaggregation used for classes of assets and liabilities measured at fair value and require disclosures about the valuation techniques and inputs used to measure fair value for both recurring and nonrecurring fair value measurements using Level 2 and Level 3 inputs. The new disclosures and clarifications of existing disclosure are effective for fiscal years beginning after December 15, 2009, except for the disclosure requirements related to the purchases, sales, issuances and settlements in the rollforward activity of Level 3 fair value measurements. Those disclosure requirements are effective for fiscal years ending after December 31, 2010. We are still assessing the impact of this guidance and do not believe the adoption of this guidance will have a material impact to our consolidated financial statements.

On February 24, 2010, FASB issued ASU 2010-09, “Subsequent Events (ASC 855): Amendments to Certain Recognition and Disclosure Requirements.” The amendments in the ASU remove the requirement for a Securities and Exchange Commission (SEC) filer to disclose a date through which subsequent events have been evaluated in both issued and revised financial statements. Revised financial statements include financial statements revised as a result of either correction of an error or retrospective application of U.S. GAAP. We adopted this guidance in the first quarter of 2010.

Note 2. Marketable Securities and Fair Value Measurements

Our short-term and long-term marketable securities as of September 30, 2010 and December 31, 2009 are as follows (in thousands):

Short-term

| | | | | | | | | | | | | | | | |

September 30, 2010 | | Amortized

Costs | | | Gross

Unrealized

Gains | | | Gross

Unrealized

Losses | | | Fair Value | |

| | | | |

| | | | |

U.S. government notes and bonds | | $ | 2,999 | | | $ | 1 | | | $ | — | | | $ | 3,000 | |

Corporate bonds and certificate of deposit | | | 2,294 | | | | — | | | | (1 | ) | | | 2,293 | |

Foreign bonds | | | 706 | | | | — | | | | — | | | | 706 | |

Commercial paper | | | 1,398 | | | | — | | | | (1 | ) | | | 1,397 | |

| | | | | | | | | | | | | | | | |

Total | | $ | 7,397 | | | $ | 1 | | | $ | (2 | ) | | $ | 7,396 | |

| | | | | | | | | | | | | | | | |

Long-term

| | | | | | | | | | | | | | | | |

September 30, 2010 | | Amortized

Costs | | | Gross

Unrealized

Gains | | | Gross

Unrealized

Losses | | | Fair Value | |

| | | | |

| | | | |

Corporate bonds | | $ | 4,464 | | | $ | — | | | $ | (11 | ) | | $ | 4,453 | |

Foreign bonds | | | 1,321 | | | | 1 | | | | (2 | ) | | | 1,320 | |

Agency bonds | | | 2,055 | | | | 1 | | | | — | | | | 2,056 | |

| | | | | | | | | | | | | | | | |

Total | | $ | 7,840 | | | $ | 2 | | | $ | (13 | ) | | $ | 7,829 | |

| | | | | | | | | | | | | | | | |

Short-term

| | | | | | | | | | | | |

December 31, 2009 | | Amortized

Cost | | | Gross

Unrealized

Gains | | | Fair Value | |

| | | |

| | | |

U.S. government notes and bonds | | $ | 18,972 | | | $ | 6 | | | $ | 18,978 | |

Corporate bonds | | | 1,000 | | | | — | | | | 1,000 | |

| | | | | | | | | | | | |

Total | | $ | 19,972 | | | $ | 6 | | | $ | 19,978 | |

| | | | | | | | | | | | |

For the nine months ended September 30, 2010 and 2009, no significant gains or losses were realized on the sale of marketable securities.

7

ALIGN TECHNOLOGY, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

(unaudited)

Fair Value Measurements

We measure the fair value of our cash equivalents and marketable securities as the price that would be received from selling an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. We use the GAAP fair value hierarchy that prioritizes the inputs to valuation techniques used to measure fair value. This hierarchy requires an entity to maximize the use of observable inputs and minimize the use of unobservable inputs when measuring fair value. The three levels of inputs that may be used to measure fair value:

Level 1—Quoted (unadjusted) prices in active markets for identical assets or liabilities.

Our Level 1 assets consist of U.S. government debt securities and money market funds. We did not hold any Level 1 liabilities as of September 30, 2010.

Level 2—Observable inputs other than quoted prices included in Level 1, such as quoted prices for similar assets or liabilities in active markets; quoted prices for identical or similar assets or liabilities in markets that are not active; or other inputs that are observable or can be corroborated by observable market data for substantially the full term of the asset or liability.

Our Level 2 assets consist of corporate bonds, certificates of deposits, foreign bonds, agency bonds, and commercial paper. We did not hold any Level 2 liabilities as of September 30, 2010.

Level 3—Unobservable inputs to the valuation methodology that are supported by little or no market activity and that are significant to the measurement of the fair value of the assets or liabilities. Level 3 assets and liabilities include those whose fair value measurements are determined using pricing models, discounted cash flow methodologies or similar valuation techniques, as well as significant management judgment or estimation.

We did not hold any Level 3 assets or liabilities as of September 30, 2010.

The following table summarizes our financial assets measured at fair value on a recurring basis as of September 30, 2010 (in thousands):

| | | | | | | | | | | | |

Description | | Balance as of

September 30, 2010 | | | Quoted Prices in

Active Markets for

Identical Assets

(Level 1) | | | Significant Other

Observable Inputs

(Level 2) | |

Cash equivalents: | | | | | | | | | | | | |

Money market funds | | $ | 183,633 | | | $ | 183,633 | | | $ | — | |

| | | |

Short-term investments: | | | | | | | | | | | | |

U.S. government debt securities | | | 3,000 | | | | 3,000 | | | | — | |

Corporate bonds and certificate of deposit | | | 2,293 | | | | — | | | | 2,293 | |

Foreign bonds | | | 706 | | | | — | | | | 706 | |

Commercial paper | | | 1,397 | | | | — | | | | 1,397 | |

| | | |

Long-term investments: | | | | | | | | | | | | |

Corporate bonds | | | 4,453 | | | | — | | | | 4,453 | |

Foreign bonds | | | 1,320 | | | | — | | | | 1,320 | |

Agency bonds | | | 2,057 | | | | — | | | | 2,057 | |

| | | | | | | | | | | | |

| | $ | 198,859 | | | $ | 186,633 | | | $ | 12,226 | |

| | | | | | | | | | | | |

Note 3. Balance Sheet Components

Inventories are comprised of (in thousands):

| | | | | | | | |

| | | September 30,

2010 | | | December 31,

2009 | |

Raw materials | | $ | 1,557 | | | $ | 1,079 | |

Work in process | | | 667 | | | | 746 | |

Finished goods | | | 158 | | | | 221 | |

| | | | | | | | |

| | $ | 2,382 | | | $ | 2,046 | |

| | | | | | | | |

Work in process includes costs to produce the Invisalign product. Finished goods primarily represent ancillary products that support the Invisalign system.

8

ALIGN TECHNOLOGY, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

(unaudited)

Accrued liabilities consist of the following (in thousands):

| | | | | | | | |

| | | September 30,

2010 | | | December 31,

2009 | |

Accrued payroll and benefits | | $ | 20,519 | | | $ | 25,847 | |

Accrued litigation settlement | | | 3,310 | | | | — | |

Accrued income taxes | | | 2,714 | | | | 2,920 | |

Accrued sales rebate | | | 2,984 | | | | 2,610 | |

Accrued sales tax and value added tax | | | 2,788 | | | | 2,392 | |

Accrued warranty | | | 2,658 | | | | 2,376 | |

Accrued sales and marketing expenses | | | 2,794 | | | | 1,954 | |

Other | | | 6,307 | | | | 4,723 | |

| | | | | | | | |

| | $ | 44,074 | | | $ | 42,822 | |

| | | | | | | | |

Note 4. Intangible Assets

The intangible assets represent non-compete agreements received in conjunction with the October 2006 OrthoClear Agreement at gross value of $14.0 million. These assets are amortized on a straight-line basis over the expected useful life of five years. As of September 30, 2010 and December 31, 2009, the net carrying value of these non-compete agreements was $2.9 million (net of $11.1 million of accumulated amortization) and $5.0 million (net of $9.0 million of accumulated amortization), respectively.

We perform an impairment test whenever events or changes in circumstances indicate that the carrying value of such assets may not be recoverable. Examples of such events or circumstances include significant underperformance relative to historical or projected future operating results, significant changes in the manner of use of acquired assets or the strategy for its business, significant negative industry or economic trends, and/or a significant decline in our stock price for a sustained period. Impairments are recognized based on the difference between the fair value of the asset and its carrying value, and fair value is generally measured based on discounted cash flow analyses. There were no impairments of intangible assets during the periods presented.

The total estimated annual future amortization expense for these intangible assets as of September 30, 2010 is as follows (in thousands):

| | | | |

Fiscal Year | | | |

2010 (for the remaining 3 months) | | $ | 700 | |

2011 | | | 2,188 | |

| | | | |

Total | | $ | 2,888 | |

| | | | |

Note 5. Legal Proceedings

Weber

On May 18, 2007, Debra A. Weber filed a consumer class action lawsuit against us, OrthoClear, Inc. and OrthoClear Holdings, Inc. (d/b/a OrthoClear, Inc.) in Syracuse, New York, U.S. District Court. The complaint alleges two causes of action against the OrthoClear defendants and one cause of action against us for breach of contract. The cause of action against us titled “Breach of Third Party Benefit Contract” references our agreement to make Invisalign treatment available to OrthoClear patients, alleging that we failed “to provide the promised treatment to Plaintiff or any of the class members.” On June 2, 2010, the Court granted our motion for summary judgment and dismissed us from the action.

On June 29, 2010, Weber requested that the Court enter final judgment as to Align pursuant to Federal Rule of Civil Procedure 54(b) in order to certify Align’s dismissal for immediate appeal. We filed an opposition to Weber’s request on July 19, 2010, on the grounds that Weber failed to show that exceptional circumstances warranted the entry of a final judgment where fewer than all claims or parties had been dismissed. On August 20, 2010, the Court denied Weber’s motion. On October 29, 2010, the Court dismissed the action against OrthoClear and OrthoClear Holdings Inc. with prejudice at the request of the remaining parties pursuant to a settlement. The Stipulation and Order of Dismissal with Prejudice entered by the Court provides that the settlement and dismissal does not affect any rights Weber may have to appeal dismissal of the action as against us. We believe there is no evidence to indicate that a reasonable possibility exists that a loss had been incurred as of September 30, 2010.

Securities Litigation

In August 2009, Plaintiff Charles Wozniak filed a lawsuit against us and our Chief Executive Officer and President, Thomas M. Prescott (“Mr. Prescott”), in District Court for the Northern District of California on behalf of a claimed class consisting of all persons

9

ALIGN TECHNOLOGY, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

(unaudited)

or entities who purchased our common stock between January 30, 2007 and October 24, 2007. The complaint alleges that Align and Mr. Prescott violated Section 10(b) of the Securities Exchange Act of 1934 and that Mr. Prescott violated Section 20(a) of the Securities Exchange Act of 1934. Specifically, the complaint alleges that during the class period, we failed to disclose that we had shifted the focus of our sales force to clearing backlog, causing a significant decrease in the number of new case starts. On November 13, 2009, the Court appointed Plumbers and Pipefitters National Pension Fund as lead plaintiff. The lead plaintiff filed an amended complaint on January 29, 2010. The amended complaint alleges that we and Mr. Prescott issued a number of purportedly false and misleading statements throughout the class period concerning the Patients First program, our production capacity, a purported backlog, and the focus of our sales force. On March 26, 2010, we and Mr. Prescott filed a motion to dismiss the amended complaint. The motion was heard by the Court on July 9, 2010, and the Court has not yet released a ruling on the motion. We believe the lawsuit to be without merit and intend to vigorously defend ourselves. We believe there is not sufficient evidence to conclude that a reasonable possibility exists that a loss had been incurred as of September 30, 2010.

Note 6. Legal Settlements

Ormco

On August 16, 2009, we entered into three agreements with Ormco Corporation (“Ormco”), an affiliate of Danaher Corporation (“Danaher”): a Settlement Agreement, a Stock Purchase Agreement, and a Joint Development, Marketing and Sales agreement (“Collaboration Agreement”). The Settlement Agreement ended all pending litigations between the parties, and we agreed to (1) make a cash payment of $13.2 million upon the execution of the agreement and (2) issue a total of 7.6 million non-assessable shares of common stock pursuant to the Stock Purchase Agreement. The settlement value was allocated between past infringement and future use of the patent based on total case shipments during the period of infringement. We attributed $69.7 million to past infringement claims, based on case shipments from September 9, 2003 through August 16, 2009. This was recorded as litigation settlement costs and included in operating expenses during the period ended September 30, 2009. Additional royalty costs based on case shipments between August 17, 2009 through January 19, 2010 totaling $7.0 million were recorded as prepaid royalties as of the settlement date. We amortized $6.2 million of the prepaid royalties to cost of sales for the year ended December 31, 2009 and the remaining $0.8 million was amortized during first quarter of 2010.

OrthoClear

In June 2010, we received an $8.7 million insurance settlement over a disputed coverage under our general liability umbrella that was not previously reimbursed by our insurer related to the OrthoClear litigation.

Leiszler

On May 10, 2010, Christopher J. Leiszler filed a complaint against us in the United States District Court for the Northern District of California. The complaint alleges that we implemented unfair and fraudulent requirements for the prescription of Invisalign through the Invisalign Proficiency Requirements. In January 2010 Dr. Leiszler’s Invisalign provider status was suspended for failing to meet the Proficiency Requirements. Dr. Leiszler sued on behalf of himself and all others similarly situated. The complaint seeks a refund of the price paid to us for Invisalign training. On October 19, 2010, we entered into a memorandum of understanding to resolve this litigation. Under terms of the proposed settlement, class members can obtain reinstatement to prescribe Invisalign treatment under certain circumstances (the “Reinstatement Benefit”). Certain class members will have the option to elect a cash remedy instead of the Reinstatement Benefit. The proposed settlement remains subject to the execution of a formal settlement agreement and approval by the Court. We anticipate that a formal settlement agreement will be presented to the Court in December 2010. Under the proposed settlement, we will deposit approximately $7.5 million into an escrow account which will be used to pay eligible class members who elect the cash remedy, as well as legal fees and other costs. We recorded a litigation settlement charge of $3.3 million in the third quarter of 2010 for our estimated liability related to this settlement. We will continue to assess and evaluate the matter with our legal counsel and update the estimated settlement charge as appropriate as new information becomes available.

Note 7. Credit Facilities

On December 5, 2008, we renegotiated and amended our existing credit facility with Comerica Bank. Under this revolving line of credit, we have $25.0 million of available borrowings with a maturity date of December 31, 2010. This credit facility requires a quick ratio covenant and also requires us to maintain a minimum unrestricted cash balance of $10.0 million. The interest rate on borrowings will range from Libor plus 1.5% to 2.0% depending upon the amount of unrestricted cash we maintain at Comerica Bank above the $10.0 million minimum.

As of September 30, 2010, we had no outstanding borrowings under this credit facility and are in compliance with the financial covenants.

10

ALIGN TECHNOLOGY, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

(unaudited)

Note 8. Commitments and Contingencies

Leases

As of September 30, 2010, minimum future lease payments for non-cancelable leases are as follow (in thousands):

| | | | |

Fiscal Year | | | |

2010 (for the remaining 3 months) | | $ | 1,535 | |

2011 | | | 5,074 | |

2012 | | | 4,010 | |

2013 | | | 3,339 | |

2014 and thereafter | | | 9,900 | |

| | | | |

Total | | $ | 23,858 | |

| | | | |

On January 26, 2010, we entered into an agreement to lease new corporate headquarters of approximately 129,024 square feet in San Jose, California. The lease agreement commenced on June 28, 2010 and will continue for an initial term of seven years and two months. The agreement for our previous corporate headquarters in Santa Clara, California, expired on June 30, 2010.

Warranty

We warrant our products against material defects until the Invisalign case is complete. We accrue for warranty costs in cost of revenues upon shipment of products. The amount of accrued estimated warranty costs is primarily based on historical experience as to product failures as well as current information on replacement costs. We regularly review the accrued balances and update these balances based on historical warranty trends. Actual warranty costs incurred have not materially differed from those accrued. However, future actual warranty costs could differ from the estimated amounts.

The following table reflects the change in our warranty accrual during the nine months ended September 30, 2010 and 2009, respectively (in thousands):

| | | | | | | | |

| | | Nine Months Ended

September 30, | |

| | | 2010 | | | 2009 | |

Balance at beginning of period | | $ | 2,376 | | | $ | 2,031 | |

Charged to cost of revenues | | | 2,212 | | | | 2,046 | |

Actual warranty expenses | | | (1,930 | ) | | | (1,962 | ) |

| | | | | | | | |

Balance at end of period | | $ | 2,658 | | | $ | 2,115 | |

| | | | | | | | |

11

ALIGN TECHNOLOGY, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

(unaudited)

Note 9. Stock-based Compensation

Summary of stock-based compensation expense

On May 20, 2010 our stockholders voted to approve an amendment to the 2005 Incentive Plan. The amendment increased the plan by 3,300,000 shares for a total reserved for issuance of 13,283,379 shares, plus up to an aggregate of 5,000,000 shares that would have been returned to our 2001 Stock Incentive Plan as a result of termination of options or repurchase of shares on or after March 28, 2005.

The following table summarizes stock-based compensation expense related to all of our stock-based options and employee stock purchases for the three and nine months ended September 30, 2010 and 2009 (in thousands):

| | | | | | | | | | | | | | | | |

| | | Three Months Ended

September 30, | | | Nine Months Ended

September 30, | |

| | | 2010 | | | 2009 | | | 2010 | | | 2009 | |

Cost of revenues | | $ | 399 | | | $ | 359 | | | $ | 1,237 | | | $ | 1,150 | |

Sales and marketing | | | 1,280 | | | | 1,243 | | | | 3,387 | | | | 3,559 | |

General and administrative | | | 2,141 | | | | 1,885 | | | | 5,960 | | | | 5,839 | |

Research and development | | | 594 | | | | 500 | | | | 1,554 | | | | 1,463 | |

| | | | | | | | | | | | | | | | |

Total stock-based compensation expense | | $ | 4,414 | | | $ | 3,987 | | | $ | 12,138 | | | $ | 12,011 | |

| | | | | | | | | | | | | | | | |

Options

The fair value of stock options granted was estimated at the grant date using the Black-Scholes option pricing model with the following weighted average assumptions:

| | | | | | | | | | | | | | | | |

| | | Three Months Ended

September 30, | | | Nine Months Ended

September 30, | |

| | | 2010 | | | 2009 | | | 2010 | | | 2009 | |

Stock Options: | | | | | | | | | | | | | | | | |

Expected term (in years) | | | 4.4 | | | | 4.4 | | | | 4.4 | | | | 4.4 | |

Expected volatility | | | 63.4 | % | | | 64.0 | % | | | 63.3 | % | | | 61.6 | % |

Risk-free interest rate | | | 1.5 | % | | | 2.1 | % | | | 1.9 | % | | | 1.6 | % |

Expected dividend | | | — | | | | — | | | | — | | | | — | |

Weighted average fair value per share at grant date | | $ | 7.28 | | | $ | 5.42 | | | $ | 9.06 | | | $ | 4.15 | |

Stock option activity for the nine months ended September 30, 2010 under the stock incentive plans is set forth below:

| | | | | | | | | | | | | | | | |

| | | Total Shares Underlying Stock Options | |

| | Number of Shares

Underlying

Stock Options

(in thousands) | | | Weighted

Average

Exercise Price | | | Weighted Average

Remaining

Contractual Term

(in years) | | | Aggregate

Intrinsic Value

(in thousands) | |

Outstanding as of December 31, 2009 | | | 7,488 | | | $ | 11.49 | | | | | | | | | |

Granted | | | 1,458 | | | | 17.61 | | | | | | | | | |

Cancelled or expired | | | (243 | ) | | | 14.61 | | | | | | | | | |

Exercised | | | (806 | ) | | | 7.77 | | | | | | | | | |

| | | | | | | | | | | | | | | | |

Outstanding as of September 30, 2010 | | | 7,897 | | | $ | 12.90 | | | | 5.98 | | | $ | 53,180 | |

| | | | | | | | | | | | | | | | |

Vested and expected to vest at September 30, 2010 | | | 7,638 | | | $ | 12.83 | | | | 5.94 | | | $ | 51,983 | |

| | | | | | | | | | | | | | | | |

Exercisable at September 30, 2010 | | | 5,080 | | | $ | 11.97 | | | | 5.33 | | | $ | 39,086 | |

| | | | | | | | | | | | | | | | |

12

ALIGN TECHNOLOGY, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

(unaudited)

As of September 30, 2010, we expect to recognize $16.1 million of total unamortized compensation cost, net of estimated forfeitures, related to stock options over a weighted average period of 2.4 years.

Restricted Stock Units

In the amended 2005 Incentive Plan any shares subject to an award of restricted stock, restricted stock units, performance shares or performance units will be counted against the authorized share reserve as one and one-half (1 1/2) shares for every one share subject to the award, and any shares cancelled will be returned to the Plan at the same ratio.

A summary of the nonvested shares for the nine months ended September 30, 2010 is as follows:

| | | | | | | | | | | | |

| | | Number of Shares

Underlying RSUs

(in thousands) | | | Weighted Average

Remaining

Contractual Term | | | Aggregate

Intrinsic Value

(in thousands) | |

Nonvested as of December 31, 2009 | | | 876 | | | | | | | | | |

Granted | | | 420 | | | | | | | | | |

Vested and released | | | (288 | ) | | | | | | | | |

Forfeited | | | (64 | ) | | | | | | | | |

| | | | | | | | | | | | |

Nonvested as of September 30, 2010 | | | 944 | | | | 1.35 | | | $ | 18,486 | |

| | | | | | | | | | | | |

As of September 30, 2010 the total unamortized compensation cost related to restricted stock units, net of estimated forfeitures, was $9.0 million, which we expect to recognize over a weighted average period of 2.3 years.

Employee Stock Purchase Plan

Our 2005 Employee Stock Purchase Plan consists of overlapping twenty-four month offering periods with four six-month purchase periods in each offering period and will expire on January 31, 2011. In May 2010, our shareholders approved the 2010 Employee Stock Purchase Plan (the “2010 Purchase Plan”). The 2010 Purchase Plan consists of overlapping twenty-four month offering periods with four six-month purchase periods in each offering period. The 2010 Purchase Plan will continue until terminated by either the Board or its administrator. Employees purchase shares at 85% of the fair market value of the common stock at either the beginning of the offering period or the end of the purchase period, whichever is lower. The maximum number of shares available under the 2010 Purchase Plan is 2,400,000 shares.

The fair value of the option component of the Purchase Plan shares was estimated at the grant date using the Black-Scholes option pricing model with the following weighted average assumptions:

| | | | | | | | | | | | | | | | |

| | | Three Months Ended

September 30, | | | Nine Months Ended

September 30, | |

| | | 2010 | | | 2009 | | | 2010 | | | 2009 | |

Employee Stock Purchase Plan: | | | | | | | | | | | | | | | | |

Expected term (in years) | | | 1.3 | | | | 1.2 | | | | 1.3 | | | | 1.3 | |

Expected volatility | | | 53.4 | % | | | 72.8 | % | | | 55.9 | % | | | 74.6 | % |

Risk-free interest rate | | | 0.4 | % | | | 0.7 | % | | | 0.4 | % | | | 0.6 | % |

Expected dividend | | | — | | | | — | | | | — | | | | — | |

Weighted average fair value at grant date | | $ | 6.87 | | | $ | 5.10 | | | $ | 7.22 | | | $ | 3.78 | |

As of September 30, 2010, we expect to recognize $0.6 million of the total unamortized compensation cost related to employee purchases over a weighted average period of 0.1 years.

Note 10. Accounting for Income Taxes

The financial statement recognition of the benefit for an uncertain tax position is dependent upon the benefit being more-likely-than-not to be sustainable upon audit by the applicable taxing authority. If this threshold is met, the tax benefit is then measured and recognized at the largest amount that is greater than fifty percent likely of being realized upon ultimate settlement.

During the third quarter of fiscal 2010, the amount of unrecognized tax benefits was increased by approximately $2.7

million. The total amount of unrecognized tax benefits was $10.4 million as of September 30, 2010, which would impact our effective tax rate if recognized. We recognize interest and penalties related to unrecognized tax benefits as a component of income

13

ALIGN TECHNOLOGY, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

(unaudited)

taxes. Interest and penalties are not significant and are included in the unrecognized tax benefits. We are subject to taxation in the U.S. and various states and foreign jurisdictions. All of our tax years will be open to examination by the U.S. federal and most state tax authorities due to our net operating loss and overall credit carryforward position. With few exceptions, we are no longer subject to examination by foreign tax authorities for years before 2005.

Note 11. Net Profit (Loss) Per Share

Basic net profit (loss) per share is computed using the weighted average number of shares of common stock outstanding during the period. Diluted net profit (loss) per share is computed using the weighted average number of shares of common stock, adjusted for the dilutive effect of potential common stock. Potential common stock, computed using the treasury stock method, include options, restricted stock units, and the dilutive component of Purchase Plan shares.

The following table sets forth the computation of basic and diluted net profit (loss) per share attributable to common stock (in thousands, except per share amounts):

| | | | | | | | | | | | | | | | |

| | | Three Months Ended

September 30, | | | Nine Months Ended

September 30, | |

| | | 2010 | | | 2009 | | | 2010 | | | 2009 | |

Net profit (loss) | | $ | 16,815 | | | $ | (49,942 | ) | | $ | 64,348 | | | $ | (42,761 | ) |

| | | | | | | | | | | | | | | | |

| | | | |

Weighted-average common shares outstanding, basic | | | 76,081 | | | | 69,528 | | | | 75,653 | | | | 67,278 | |

| | | | |

Effect of potential dilutive common shares | | | 2,028 | | | | — | | | | 2,199 | | | | — | |

| | | | | | | | | | | | | | | | |

Total shares, diluted | | | 78,109 | | | | 69,528 | | | | 77,852 | | | | 67,278 | |

| | | | | | | | | | | | | | | | |

| | | | |

Basic net profit (loss) per share | | $ | 0.22 | | | $ | (0.72 | ) | | $ | 0.85 | | | $ | (0.64 | ) |

| | | | | | | | | | | | | | | | |

Diluted net profit (loss) per share | | $ | 0.22 | | | $ | (0.72 | ) | | $ | 0.83 | | | $ | (0.64 | ) |

| | | | | | | | | | | | | | | | |

For the three and nine months ended September 30, 2010, stock options and restricted stock units totaling 3.3 million and 3.0 million, respectively, were excluded from diluted net profit per share because of their anti-dilutive effect. For the three and nine months ended September 30, 2009, stock options and restricted stock units totaling 4.0 million and 5.1 million, respectively, were excluded from diluted net loss per share because of their anti-dilutive effect.

Note 12. Comprehensive Income (Loss)

Comprehensive income includes net profit (loss), foreign currency translation adjustments and unrealized gains (losses) on available-for-sale securities. The components of comprehensive income (loss) are as follows (in thousands):

| | | | | | | | | | | | | | | | |

| | | Three Months Ended

September 30, | | | Nine Months Ended

September 30, | |

| | | 2010 | | | 2009 | | | 2010 | | | 2009 | |

Net profit (loss) | | $ | 16,815 | | | $ | (49,942 | ) | | $ | 64,348 | | | $ | (42,761 | ) |

Foreign currency translation adjustments | | | 585 | | | | 214 | | | | (120 | ) | | | 242 | |

Change in unrealized gains (losses) on available-for-sale securities | | | (18 | ) | | | — | | | | (18 | ) | | | 20 | |

| | | | | | | | | | | | | | | | |

Comprehensive income (loss) | | $ | 17,382 | | | $ | (49,728 | ) | | $ | 64,210 | | | $ | (42,499 | ) |

| | | | | | | | | | | | | | | | |

Note 13. Segments and Geographical Information

Segment

We report segment data based on the internal reporting that is used by management for making operating decisions and assessing performance. During all periods presented, we operated as a single business segment.

14

ALIGN TECHNOLOGY, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

(unaudited)

Geographical Information

Net revenues and long-lived assets are presented below by geographic area (in thousands):

| | | | | | | | | | | | | | | | |

| | | Three Months Ended

September 30, | | | Nine Months Ended

September 30, | |

| | | 2010 | | | 2009 | | | 2010 | | | 2009 | |

Net revenues: | | | | | | | | | | | | | | | | |

North America | | $ | 72,555 | | | $ | 60,054 | | | $ | 223,141 | | | $ | 172,577 | |

Europe | | | 22,280 | | | | 18,206 | | | | 68,085 | | | | 50,986 | |

Other international | | | 1,112 | | | | 1,009 | | | | 3,007 | | | | 2,154 | |

| | | | | | | | | | | | | | | | |

Total net revenues | | $ | 95,947 | | | $ | 79,269 | | | $ | 294,233 | | | $ | 225,717 | |

| | | | | | | | | | | | | | | | |

| | | | | | | | |

| | |

| | | As of September 30,

2010 | | | As of December 31,

2009 | |

Long-lived assets: | | | | | | | | |

North America | | $ | 84,573 | | | $ | 91,548 | |

Europe | | | 872 | | | | 1,018 | |

Other international | | | 1,848 | | | | 1,375 | |

| | | | | | | | |

Total long-lived assets | | $ | 87,293 | | | $ | 93,941 | |

| | | | | | | | |

Note 14. Restructuring

In July and October 2008, we announced restructuring plans to increase efficiencies across the organization and lower the overall cost structure. The July 2008 plan reduced full time headcount primarily through a phased-consolidation of order acquisition operations from our corporate headquarters in Santa Clara, California to Juarez, Mexico, which was completed by the end of 2008. In addition to headcount reductions, the October restructuring plan included the phased relocation of our shared services organizations from Santa Clara, California to our facility in Costa Rica, which was completed during the second quarter of 2009.

In 2009, we incurred approximately $1.3 million of costs related to severance and termination benefits. There were no costs incurred relating to the restructuring plans during 2010.

15

| ITEM 2. | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS. |

In addition to historical information, this quarterly report on Form 10-Q contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. These statements include, among other things, our expectations regarding the elimination of the annual minimum case volume requirement, the anticipated impact of our new products and product enhancements, including Invisalign G3, will have on doctor utilization and our market share, our expectations regarding product mix and product adoption, our expectations regarding the existence and impact of seasonality, our expectations regarding the continued growth of our international markets, including the expected commercial launch of Invisalign in China in the second half of 2011, the anticipated level of our gross margins, and other factors beyond our control, as well as other statements regarding our future operations, financial condition and prospects and business strategies. These statements may contain words such as “expects,” “anticipates,” “intends,” “plans,” “believes,” “estimates,” or other words indicating future results. These forward-looking statements are subject to certain risks and uncertainties that could cause actual results to differ materially from those reflected in the forward-looking statements. Factors that could cause or contribute to such differences include, but are not limited to, those discussed in Item 2 “Management’s Discussion and Analysis of Financial Condition and Results of Operations”, and in particular, the risks discussed below in Part II, Item 1A “Risk Factors”. We undertake no obligation to revise or update these forward-looking statements. Given these risks and uncertainties, readers are cautioned not to place undue reliance on such forward-looking statements.

The following discussion and analysis of our financial condition and results of operations should be read together with our Condensed Consolidated Financial Statements and related notes included elsewhere in this Quarterly Report on Form 10-Q.

We design, manufacture and market the Invisalign system, a proprietary method for treating malocclusion, or the misalignment of teeth. Invisalign corrects malocclusion using a series of clear, nearly invisible, removable appliances that gently move teeth to a desired final position. Because it does not rely on the use of metal or ceramic brackets and wires, Invisalign significantly reduces the aesthetic and other limitations associated with metal arch wires and brackets, commonly referred to as braces. We received the United States Food and Drug Administration (“FDA”) clearance to market Invisalign in 1998. The Invisalign system is regulated by the FDA as a Class II medical device.

We distribute the vast majority of our products directly to our customers: the orthodontist and the general practitioner dentist, or GP. Orthodontists and GPs must complete an initial Invisalign training course in order to begin providing the Invisalign treatment solution to their patients. The Invisalign system is sold in North America, Europe, Asia Pacific, Latin America and Japan. We use a distributor model for the sale of our products in parts of the Asia Pacific, Latin American and EMEA (Europe, Middle East and Africa) regions.

Each Invisalign treatment plan is unique to the individual patient. Our Invisalign Full treatment consists of as many aligners as indicated by ClinCheck in order to achieve the doctors’ treatment goals. Our Invisalign Express is a dual arch orthodontic treatment for cases that meet certain predetermined clinical criteria and consist of up to ten sets of aligners. Invisalign Express treatment is intended to assist dental professionals to treat a broader range of patients by providing a lower-cost option for adult relapse cases, for minor crowding and spacing, or as a pre-cursor to restorative or cosmetic treatments such as veneers. In April 2010, we replaced Invisalign Express in international markets with the launch of Invisalign Lite. Invisalign Lite offers doctors a new option for less complex orthodontic cases, such as short-term aesthetic cases, relapsed cases and pre-restorative treatments, using up to 14 stages. Invisalign Teen is designed to meet the specific needs of the non-adult comprehensive or teen treatment market particularly younger teenagers aged 11 to 15 years. Invisalign Assist is intended to help newly-trained and lower volume Invisalign GPs accelerate the adoption and frequency of use of Invisalign into their practice. Upon completion of an Invisalign or non-Invisalign treatment, the patient may be prescribed our traditional retainer product, or our Vivera retainers, a clear aligner set designed for ongoing retention. Our goal is to establish Invisalign as the standard method for treating malocclusion ultimately driving increased product adoption by dental professionals by focusing on the four key objectives: driving product innovation and clinical effectiveness, enhancing the customer experience, generating consumer demand and expanding into international markets. Each of these four key objectives is described more fully inItem I—Business—Business Strategy of our 2009 Annual Report on Form 10-K. As we execute on our business strategy, we will continue to deliver significant evolutions in product features and functionality, as well as customer facing systems.

In addition to the successful execution of our business strategy, a number of other factors may affect our results in 2010 and beyond, the most important of which are set forth in our Annual Report in Form 10-K as updated below.

| | • | | Accelerate product and clinical innovation. In October 2010, we launched Invisalign G3, a collection of new features and innovations that touch every product and virtually every system at Align. Invisalign G3 is engineered to deliver even better clinical results, with new aligner and software features that make it easier to use Invisalign with more complex and challenging cases, including Precision Cuts designed for use with Class II and Class III patients, new SmartForce™ features designed for increased predictability of certain tooth movements, and simpler, more intuitive software to streamline treatment planning and review. We believe Invisalign G3 will have a positive impact on utilization and continue to support more widespread adoption into our customers’ practices. |

16

| | • | | Proficiency Program. Our success depends upon increasing acceptance and frequency of use of the Invisalign system by dental professionals (what we refer to as utilization). To achieve this, in June 2009 we introduced the Invisalign Product Proficiency Requirements (“Proficiency Program”) which mandated that every Invisalign provider in North America must submit a minimum number of case starts and complete a minimum number of continuing education (“CE”) credits. As the Proficiency Program progressed, many customers became frustrated with minimum case and education requirements. In response to this feedback, in April 2010 we eliminated the case start requirements and in October 2010 we eliminated the annual CE requirements, effectively terminating the Proficiency Program. |

With the elimination of the minimum case and annual CE requirements, it is uncertain how case volumes, particularly for lower volume doctors, will be impacted. We expect to experience variability in customer activity over the next several quarters as doctors adjust to the changes to the Proficiency Program requirements. We will continue to emphasize the importance of Invisalign professional education in treatment success and to promote the benefits of Invisalign Preferred Provider status for doctors who start ten or more cases each year.

| | • | | Number of new doctors trained. In 2009, we trained approximately 2,825 new doctors in North America. In the first three quarters of 2010, we trained approximately 2,100 doctors in North America (including 600 doctors who had their account suspended as a result of the Proficiency Requirements at the end of 2009). Our new doctor training in North America is evolving to identify and focus on practices that are interested in gaining the skills and experience necessary to be successful with Invisalign. As a result, we expect that the number of new and reactivated doctors trained in North America will be slightly lower in 2010 compared to 2009. Internationally, we continue expect that the number of new doctors trained to be comparable to 2009. |

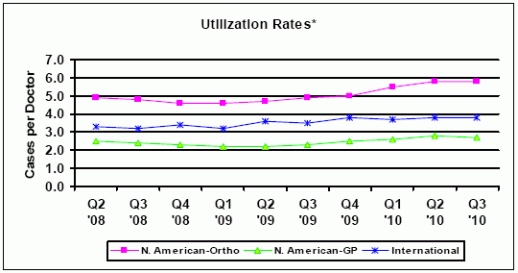

| | • | | Utilization rates. Our goal is to establish Invisalign as the treatment of choice for treating malocclusion ultimately driving increased product adoption and frequency of use by dental professionals, or utilization. Our quarterly utilization rates for the previous ten quarters are as follows: |

| * | Utilization rates = # of cases shipped divided by # of doctors cases were shipped to |

Utilization rates in the third quarter of 2010 for the North American Ortho and International channels remained unchanged compared to the second quarter of 2010. Since summer is typically the busiest season for orthodontists with practices that have a high percentage of adolescent and teenage patients, historically, adult appointments, including adult Invisalign patient starts, are often pushed further into late summer or early fall. We believe that the availability of Invisalign Teen helped moderate this historical downward trend from the second quarter compared to the third quarter since we are now able to actively compete for a share of teen patient starts. North American GP dentist utilization decreased from 2.8 to 2.7 cases per GP dentist compared to the second quarter of 2010, reflecting a decline in the number of cases shipped across all levels of GP submitters (high to low). In addition, there were fewer low volume GP submitters than the prior quarter. This is consistent with historical trends during our third quarter when more doctors are out of the office for summer vacation and holidays. We expect to continue to see fluctuation in our utilization rates as practices adjust to the Proficiency Program and our customer base evolves throughout the year. As a result of eliminating the annual case requirements, we expect that the number of doctors we ship to over the next several quarters will fluctuate. We therefore believe that quarter-to-quarter comparisons of utilization rates may not be as meaningful in 2010.

17

| | • | | Release of previously deferred revenue. In the second quarter of 2010, we released $14.3 million of previously deferred revenue for Invisalign Teen replacement aligners. Invisalign Teen, which was launched in July 2008, includes up to six replacement aligners which may be ordered at any time throughout treatment. Revenue for these replacement aligners was previously deferred based on 100 percent of the fair value of the aligners until the replacement aligners were used or the case completed. Over the past two years, we have evaluated the usage experience of the Invisalign Teen replacement aligners and determined that we have sufficient historical evidence to support an estimated usage rate. Since the deferral rate for estimated usage is significantly lower than our previous rate, we experienced a favorable impact to revenue from the second quarter to the third quarter of 2010. |

| | • | | Seasonal fluctuations. Seasonal fluctuations in the number of doctors in their offices and available to take appointments have affected, and are likely to continue to affect our business. Specifically, our customers often take vacation during the summer months and therefore tend to start fewer cases, especially North American GPs and European doctors. |

In 2010, sequential case growth from second quarter to the third quarter in the North American Ortho channel was essentially flat. With the availability of Invisalign Teen, we can actively compete for a share of teen patient starts. Summer is typically the busiest season for orthodontists with practices that have a high percentage of adolescent and teenage patients. Many parents want to get their teens started in treatment before the start of the school year. We believe that Invisalign Teen helped moderate the historical downward trend we have typically seen for our North American orthodontic customers during the summer months.

In the third quarter of 2010, we saw a decline in the number of cases submitted as well as a decline in the number of submitters in our North American GP channel which is consistent with our historical trend during this quarter. In addition, we believe that the elimination of the minimum case requirements announced in the second quarter at 2010 has reduced the number of case submissions across all levels of our GP customers.

| | • | | Foreign exchange rates. Although the U.S. dollar is our reporting currency, a portion of our revenues and profits are generated in foreign currencies. Revenues and profits generated by subsidiaries operating outside of the United States are translated into U.S. dollars using exchange rates effective during the respective period and as a result are affected by changes in exchange rates. We have generally accepted the exposure to exchange rate movements without using derivative financial instruments to manage this risk. Therefore, both positive and negative movements in currency exchanges rates against the U.S. dollar will continue to affect the reported amount of revenues and profits in our consolidated financial statements. |

| | • | | Impact on consumer spending due to uncertainty in the U.S. economy. Consumer spending habits are affected by, among other things, prevailing economic conditions, levels of employment, salaries and wage rates, gas prices, consumer confidence and consumer perception of economic conditions. During the third quarter of 2010, our North American GP customers reported lower dental visits and reduced demand for premium procedures. As a result, this is one factor that we believe will result in lower case shipments in the fourth quarter of 2010 compared to the third quarter, predominantly among our GP customers. |

| | • | | Growth of international markets. In October 2010, we announced regulatory approval to market and sell Invisalign in China and expect to begin commercial launch in the second half of 2011. |

| | • | | Operating Expenses. In the fourth quarter of 2010, we expect operating expenses to increase reflecting additional spending in international sales and marketing, commercialization activities for Invisalign G3 and pre-commercialization activities in China. |

18

Results of Operations

Net revenues and case volume by channel and product:

Invisalign product revenues by channel and other non-case revenues, which represents training, retainer and ancillary products, for the three and nine months ended September 30, 2010 and 2009 are as follows (in millions):

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Three Months Ended September 30, | | | Nine Months Ended September 30, | |

Net revenues | | 2010 | | | 2009 | | | Net

Change | | | % Change | | | 2010 | | | 2009 | | | Net

Change | | | % Change | |

North America: | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Ortho | | $ | 31.1 | | | $ | 22.7 | | | $ | 8.4 | | | | 37.0 | % | | $ | 88.4 | | | $ | 65.4 | | | $ | 23.0 | | | | 35.2 | % |

GP | | | 36.8 | | | | 33.9 | | | | 2.9 | | | | 8.6 | % | | | 111.4 | | | | 96.6 | | | | 14.8 | | | | 15.3 | % |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Total North American Invisalign | | | 67.9 | | | | 56.6 | | | | 11.3 | | | | 20.0 | % | | | 199.8 | | | | 162.0 | | | | 37.8 | | | | 23.3 | % |

International Invisalign | | | 23.2 | | | | 18.5 | | | | 4.7 | | | | 25.4 | % | | | 65.2 | | | | 50.8 | | | | 14.4 | | | | 28.3 | % |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Total Invisalign revenues | | | 91.1 | | | | 75.1 | | | | 16.0 | | | | 21.3 | % | | | 265.0 | | | | 212.8 | | | | 52.2 | | | | 24.5 | % |

Teen deferred revenue release | | | — | | | | — | | | | — | | | | N/A | | | | 14.3 | | | | — | | | | 14.3 | | | | N/A | |

Non-case revenues | | | 4.8 | | | | 4.2 | | | | 0.6 | | | | 14.3 | % | | | 14.9 | | | | 12.9 | | | | 2.0 | | | | 15.5 | % |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Total net revenues | | $ | 95.9 | | | $ | 79.3 | | | $ | 16.6 | | | | 20.9 | % | | $ | 294.2 | | | $ | 225.7 | | | $ | 68.5 | | | | 30.4 | % |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Case volume data which represents Invisalign case shipments by channel, for the three and nine months ended September 30, 2010 and 2009 are as follows (in thousands):

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Three Months Ended September 30, | | | Nine Months Ended September 30, | |

Invisalign case volume | | 2010 | | | 2009 | | | Net

Change | | | %

Change | | | 2010 | | | 2009 | | | Net

Change | | | %

Change | |

North America: | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Ortho | | | 23.2 | | | | 18.8 | | | | 4.4 | | | | 23.4 | % | | | 68.4 | | | | 53.2 | | | | 15.2 | | | | 28.6 | % |

GP | | | 26.8 | | | | 25.6 | | | | 1.2 | | | | 4.7 | % | | | 83.8 | | | | 72.4 | | | | 11.4 | | | | 15.7 | % |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Total North American Invisalign | | | 50.0 | | | | 44.4 | | | | 5.6 | | | | 12.6 | % | | | 152.2 | | | | 125.6 | | | | 26.6 | | | | 21.2 | % |

International Invisalign | | | 16.2 | | | | 12.1 | | | | 4.1 | | | | 33.9 | % | | | 45.1 | | | | 33.9 | | | | 11.2 | | | | 33.0 | % |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Total Invisalign case volume | | | 66.2 | | | | 56.5 | | | | 9.7 | | | | 17.2 | % | | | 197.3 | | | | 159.5 | | | | 37.8 | | | | 23.7 | % |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Invisalign revenues by product and other non-case revenues, which represents training, retainer and ancillary products, for the three and nine months ended September 30, 2010 and 2009 are as follows (in millions):

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Three Months Ended September 30, | | | Nine Months Ended September 30, | |

Net revenues | | 2010 | | | 2009 | | | Net

Change | | | %

Change | | | 2010 | | | 2009 | | | Net

Change | | | %

Change | |

Invisalign Full | | $ | 66.6 | | | $ | 58.5 | | | $ | 8.1 | | | | 13.8 | % | | $ | 199.8 | | | $ | 171.4 | | �� | $ | 28.4 | | | | 16.6 | % |

Invisalign Express/Lite | | | 8.9 | | | | 7.5 | | | | 1.4 | | | | 18.7 | % | | | 26.3 | | | | 21.4 | | | | 4.9 | | | | 22.9 | % |

Invisalign Teen (1) | | | 11.3 | | | | 7.7 | | | | 3.6 | | | | 46.8 | % | | | 42.2 | | | | 16.7 | | | | 25.5 | | | | 152.7 | % |

Invisalign Assist | | | 4.3 | | | | 1.4 | | | | 2.9 | | | | 207.1 | % | | | 11.0 | | | | 3.3 | | | | 7.7 | | | | 233.3 | % |

Non-case revenues | | | 4.8 | | | | 4.2 | | | | 0.6 | | | | 14.3 | % | | | 14.9 | | | | 12.9 | | | | 2.0 | | | | 15.5 | % |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Total net revenues | | $ | 95.9 | | | $ | 79.3 | | | $ | 16.6 | | | | 20.9 | % | | $ | 294.2 | | | $ | 225.7 | | | $ | 68.5 | | | | 30.4 | % |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| (1) | The nine months ended September 30, 2010 includes a $14.3 million release of previously deferred revenue for Invisalign Teen replacement aligners. |

19

Case volume data which represents Invisalign case shipments by product, for the three and nine months ended September 30, 2010 and 2009 are as follows (in thousands):

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Three Months Ended September 30, | | | Nine Months Ended September 30, | |

Invisalign case volume | | 2010 | | | 2009 | | | Net

Change | | | %

Change | | | 2010 | | | 2009 | | | Net

Change | | | %

Change | |

Invisalign Full | | | 44.9 | | | | 38.7 | | | | 6.2 | | | | 16.0 | % | | | 135.7 | | | | 113.9 | | | | 21.8 | | | | 19.1 | % |

Invisalign Express/Lite | | | 9.8 | | | | 8.4 | | | | 1.4 | | | | 16.7 | % | | | 28.6 | | | | 24.4 | | | | 4.2 | | | | 17.2 | % |

Invisalign Teen | | | 7.6 | | | | 7.9 | | | | (0.3 | ) | | | (3.8 | )% | | | 21.8 | | | | 17.7 | | | | 4.1 | | | | 23.2 | % |

Invisalign Assist | | | 3.9 | | | | 1.5 | | | | 2.4 | | | | 160.0 | % | | | 11.2 | | | | 3.5 | | | | 7.7 | | | | 220.0 | % |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Total Invisalign case volume | | | 66.2 | | | | 56.5 | | | | 9.7 | | | | 17.2 | % | | | 197.3 | | | | 159.5 | | | | 37.8 | | | | 23.7 | % |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Total net revenues increased for the three and nine months ended September 30, 2010 as compared to the same periods in 2009 primarily as a result of worldwide volume growth across all customer channels. The release of revenue previously deferred for Invisalign Teen replacement aligners in the second quarter of 2010 contributed an additional $14.3 million to total net revenues for the nine months ended September 30, 2010. We believe the United States economic downturn adversely impacted consumer spending habits in 2009, and doctors tended to focus on more traditional dental procedures. As a result, we experienced a lower sales growth rate between 2008 and 2009.

In the three months ended September 30, 2010, North America revenue increased 20.0% compared to the same period in 2009 due to case volume growth of 12.6% as well as an increase in our average selling price due to a significant reduction in our revenue deferral rate for Teen replacement aligners and lower discounts and rebates. Our International Invisalign revenue also increased 25.4% for the three months ended September 30, 2010 mainly due to growth in case volumes of 33.9% from all products partially offset by unfavorable foreign exchange rates.

In the nine months ended September 30, 2010, North America revenue increased 23.3% as compared to the same period in 2009 due to case volume growth of 21.2% as well as an increase in our average selling price due to a significant reduction in our revenue deferral rate for Teen replacement aligners and lower discounts and rebates. Our International Invisalign revenue also increased 28.3% for the nine months ended September 30, 2010, as compared to the same periods in 2009, mainly due to growth in case volumes of 33.0% from all products partially offset by unfavorable foreign exchange rates.

Invisalign Teen includes up to six replacement aligners which may be ordered at any time throughout treatment. Through the second quarter of 2010, revenue for these replacement aligners was deferred based on 100 percent of the fair value of the aligners until the replacement aligners were used or the case completed. Since the launch of Invisalign Teen nearly two years ago, we evaluated the usage experience of the replacement aligners and determined that there is sufficient historical experience to establish an estimated usage rate. As a result, in June 2010, we reduced deferred revenue for Invisalign Teen replacement aligners by $14.3 million to reflect the lower estimated usage for in-process cases.

Other non-case revenues, consisting of training fees and sales of ancillary products, were higher for the three and nine month periods ended September 30, 2010 compared to the same periods in 2009 primarily due to increased sales of our Vivera and retainer products.

Cost of revenues and gross profit (in millions):

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | Three Months Ended September 30, | | | Nine Months Ended September 30, | |

| | | 2010 | | | 2009 | | | Change | | | 2010 | | | 2009 | | | Change | |

Cost of revenues | | $ | 21.0 | | | $ | 20.3 | | | $ | 0.7 | | | $ | 62.6 | | | $ | 56.0 | | | $ | 6.6 | |

% of net revenues | | | 21.9 | % | | | 25.6 | % | | | | | | | 21.3 | % | | | 24.8 | % | | | | |

| | | | | | |

Gross profit | | $ | 74.9 | | | $ | 59.0 | | | $ | 15.9 | | | $ | 231.7 | | | $ | 169.7 | | | $ | 62.0 | |

Gross margin | | | 78.1 | % | | | 74.4 | % | | | | | | | 78.7 | % | | | 75.2 | % | | | | |

Cost of revenues includes salaries for staff involved in the production process, the cost of materials, packaging, shipping costs, depreciation on capital equipment used in the production process, training costs and stock-based compensation expense. Through April 2009, cost of revenues also included the cost of our third party shelter service provider in Juarez, Mexico. Royalties related to the Ormco litigation that were fully amortized in the first quarter of 2010 of $0.8 million are also included in cost of revenues for the nine months ended September 30, 2010.

20

Gross margin improved for the three and nine months ended September 30, 2010 compared to the same periods in 2009 primarily due to increased cost absorption because of higher production volumes. Additionally, the gross margin for the nine months ended September 30, 2010 was favorably impacted by the release of teen deferred revenue of $14.3 million during the second quarter of 2010.

Sales and marketing (in millions):

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | Three Months Ended September 30, | | | Nine Months Ended September 30, | |

| | | 2010 | | | 2009 | | | Change | | | 2010 | | | 2009 | | | Change | |

Sales and marketing | | $ | 26.9 | | | $ | 27.7 | | | $ | (0.8 | ) | | $ | 83.8 | | | $ | 84.6 | | | $ | (0.8 | ) |

% of net revenues | | | 28.0 | % | | | 34.9 | % | | | | | | | 28.5 | % | | | 37.5 | % | | | | |

Sales and marketing expense includes sales force compensation (including travel-related costs), marketing personnel-related costs, media and advertising, clinical education, product marketing and stock-based compensation expense.

Our sales and marketing expense for the three months ended September 30, 2010 decreased compared to the same period in 2009 primarily resulting from lower sales compensation expenses of approximately $0.8 million during the third quarter of 2010.

Our sales and marketing expense for the nine months ended September 30, 2010 decreased compared to the same period in 2009 primarily due to $3.0 million of lower clinical education expenses. Of these lower expenses, $1.6 million was included in gross margin during the first three quarters of 2010 and approximately $1.2 million was related to North America and European sales summits that took place in the first nine months 2009, whereas a North American summit will occur in fourth quarter of 2010. These reduced costs were partially offset by approximately $1.2 million associated with the preparation and transition into our new building and by higher marketing, media, advertising, and marketing personnel related costs totaling approximately $1.0 million.

General and administrative (in millions):

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | Three Months Ended September 30, | | | Nine Months Ended September 30, | |

| | | 2010 | | | 2009 | | | Change | | | 2010 | | | 2009 | | | Change | |