EXHIBIT 3

Annual Information Form

Sun Life Financial Inc.

For the Year Ended December 31, 2011

February 15, 2012

ANNUAL INFORMATION FORM 2011

Table of Contents

| Annual Information Form | Management’s Discussion & Analysis | Consolidated Financial Statements and Notes | ||||

Corporate Structure | 4 | |||||

General Development of the Business | 5 | |||||

Business of Sun Life Financial | 7 | 3 | ||||

Business Performance | 6 | 1-6 | ||||

Investments | 32 | 30 | ||||

Risk Management | 40 | 41 | ||||

Capital Structure | 8 | 58 | 73 | |||

Dividends | 11 | 61 | 5 | |||

Security Ratings | 12 | |||||

Transfer Agent and Registrar | 15 | |||||

Directors and Executive Officers | 16 | |||||

Interests of Experts | 20 | |||||

Regulatory Matters | 20 | |||||

Risk Factors | 29 | |||||

Legal and Regulatory Proceedings | 41 | 76 | ||||

Additional Information | 42 | |||||

Appendices | ||||||

A – Charter of Audit Committee | 43 | |||||

B – Policy Restricting the Use of External Auditors

| 46

| |||||

Sun Life Financial Inc. | sunlife.com | 1 |

ANNUAL INFORMATION FORM 2011

The following table provides a list of abbreviations frequently used throughout this document.

Abbreviation

|

Description

|

Abbreviation

|

Description

| |||

AIF | Annual Information Form | OSFI | Office of the Superintendent of Financial Institutions, Canada | |||

GAAP | Generally Accepted Accounting Principles | OSC | Ontario Securities Commission | |||

IFRS | International Financial Reporting Standards | SEC | United States Securities and Exchange Commission | |||

ISDA | International Swaps and Derivatives Association, Inc. | Sun Life Assurance | Sun Life Assurance Company of Canada | |||

MCCSR | Minimum Continuing Capital and Surplus Requirements | SLF Inc. | Sun Life Financial Inc. | |||

MD&A | Management’s Discussion & Analysis | Sun Life (U.S.) | Sun Life Assurance Company of Canada (U.S.) | |||

NAIC | National Association of Insurance Commissioners, United States | Superintendent | The Superintendent under the Office of the Superintendent of Financial Institutions Act | |||

Presentation of Information

In this AIF, SLF Inc. and its consolidated subsidiaries, significant equity investments and joint ventures are collectively referred to as “Sun Life Financial”, the “Company”, “we”, “us” or “our”.

Unless otherwise indicated, all information in this AIF is presented as at and for the year ended December 31, 2011, and amounts are expressed in Canadian dollars. Financial information is presented in accordance with IFRS and the accounting requirements of OSFI.

Documents Incorporated by Reference

The following documents are incorporated by reference in and form part of this AIF:

| (i) | SLF Inc.’s MD&A for the year ended December 31, 2011 (our “2011 MD&A”), and |

| (ii) | SLF Inc.’s Consolidated Financial Statements and accompanying notes for the year ended December 31, 2011 (our “2011 Consolidated Financial Statements”). |

These documents have been filed with securities regulators in Canada and with the SEC and may be accessed at www.sedar.com and www.sec.gov, respectively.

Forward-looking Information

Certain statements in this AIF, including those relating to our strategies and statements (i) that are predictive in nature, (ii) that depend upon or refer to future events or conditions, or (iii) that include words such as “expects”, “anticipates”, “intends”, “plans”, “believes”, “estimates” or similar expressions, are forward-looking information within the meaning of securities laws. Forward-looking information includes the information concerning our possible or assumed future results of operations. These statements represent our current expectations, estimates and projections regarding future events and are not historical facts. Forward-looking information is not a guarantee of future performance and involves risks and uncertainties that are difficult to predict. Future results and shareholder value may differ materially from those expressed in these forward-looking statements due to, among other factors, the matters set out in this AIF under “Risk Factors” and in our annual and interim MD&A under Critical Accounting Policies and Estimates and Risk Management and the factors detailed and our annual and interim financial statements and other filings with Canadian and U.S. securities regulators, which are available for review at www.sedar.com and www.sec.gov.

Factors that could cause actual results to differ materially from expectations include, but are not limited to, economic uncertainty, market conditions that affect the Company’s capital position or its ability to raise capital; changes or volatility in interest rates or credit/swap spreads; the performance of equity markets; credit risks related to issuers of securities held in our investment portfolio, debtors, structured securities, reinsurers, derivative counterparties, other financial institutions and other entities; risks in implementing business strategies; risk management; changes in legislation and regulations including capital requirements and tax laws; legal and regulatory proceedings, including

Sun Life Financial Inc. | sunlife.com | 2 |

ANNUAL INFORMATION FORM 2011

inquiries and investigations; risks relating to product design and pricing; downgrades in financial strength or credit ratings; the ability to attract and retain employees; the performance of the Company’s investments and investment portfolios managed for clients such as segregated and mutual funds; the impact of higher-than-expected future expenses; risks relating to mortality and morbidity, including the occurrence of natural or man-made disasters, pandemic diseases and acts of terrorism; risks relating to the rate of mortality improvement; risks relating to policyholder behaviour; risks relating to liquidity; dependence on third-party relationships including outsourcing arrangements; the inability to maintain strong distribution channels and risks relating to market conduct by intermediaries and agents; breaches or failure of information system security and privacy, including cyber terrorism; business continuity risks; risks relating to financial modelling errors; risks relating to real estate investments; risks relating to estimates and judgements used in calculating taxes; the impact of mergers and acquisitions; risks relating to operations in Asia including the Company’s joint ventures; the impact of competition; fluctuations in foreign currency exchange rate; risks relating to the closed block of business; risks relating to the environment, environmental laws and regulations and third party policies; and the availability, cost and effectiveness of reinsurance.

The Company does not undertake any obligation to update or revise its forward-looking information to reflect events or circumstances after the date of this AIF or to reflect the occurrence of unanticipated events, except as required by law.

Sun Life Financial Inc. | sunlife.com | 3 |

ANNUAL INFORMATION FORM 2011

Corporate Structure

SLF Inc. was incorporated under the Insurance Companies Act, Canada (the “Insurance Act”) on August 5, 1999, to become the holding company of Sun Life Assurance in connection with the demutualization of Sun Life Assurance.

Sun Life Assurance was incorporated in 1865 as a stock insurance company and was converted into a mutual insurance company in 1962. On March 22, 2000, Sun Life Assurance implemented a plan of demutualization under which it converted back to a stock company pursuant to Letters Patent of Conversion issued under the Insurance Act. Under this plan of demutualization, Sun Life Assurance became a wholly-owned subsidiary of SLF Inc.

The head and registered office of SLF Inc. is located at 150 King Street West, Toronto, Ontario, M5H 1J9.

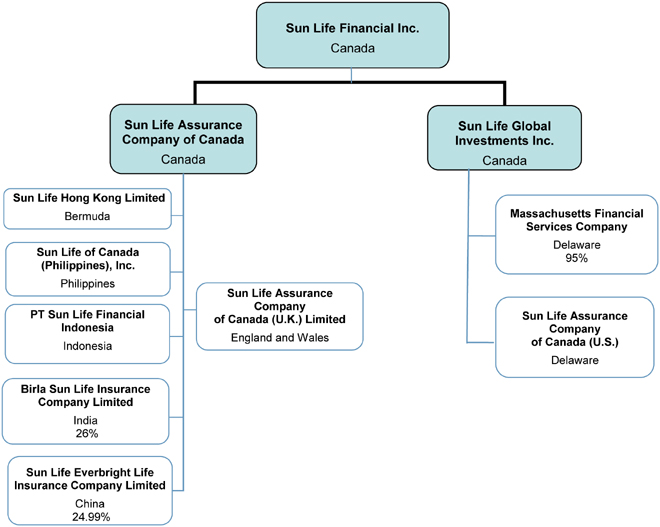

Principal Subsidiaries and Significant Equity Investments

Sun Life Financial’s corporate structure as at December 31, 2011, including its principal direct and indirect subsidiaries and joint ventures and their respective jurisdiction of incorporation, continuation, formation or organization, is shown below. Where a company is not a direct or indirect wholly owned subsidiary of SLF Inc. the following chart shows the percentage of voting securities that are beneficially owned or controlled by SLF Inc. Additional information on subsidiary and affiliate companies of SLF Inc. can be found in the Company’s 2011 Annual Report.

Sun Life Financial Inc. | sunlife.com | 4 |

ANNUAL INFORMATION FORM 2011

General Development of the Business

Sun Life Financial is a leading international financial services organization providing a diverse range of life and health insurance, savings, investment management, retirement, and pension products and services to individuals and corporate customers. Sun Life Financial and its partners today have operations in markets worldwide, including Canada, the United States, the United Kingdom, Ireland, Hong Kong, the Philippines, Japan, Indonesia, India, China and Bermuda. As of December 31, 2011, the Sun Life Financial group of companies had total assets under management of $466 billion.

We manage our operations and report our financial results in five business segments: Sun Life Financial Canada (“SLF Canada”), Sun Life Financial United States (“SLF U.S.”), MFS Investment Management (“MFS”), Sun Life Financial Asia (“SLF Asia”), and Corporate. The Corporate segment includes the operations of our United Kingdom business unit (“SLF U.K.”) and Corporate Support operations. Our Corporate Support operations includes our run-off reinsurance business and investment income, expenses, capital and other items not allocated to other business segments.

Mission

To help customers achieve lifetime financial security.

Vision

To be an international leader in protection and wealth management.

Strategy

We will leverage our strengths around the world to help our customers achieve lifetime financial security and create value for our shareholders.

Our strategy is based on growing our diverse set of businesses where we have important market positions and can leverage strengths across these businesses. We have chosen to be active in businesses that are supported by strong growth prospects, demographic trends and long-term drivers of demand for the insurance industry – the aging of baby boomers, the downloading of responsibility from governments and employers to employees and the growth of the middle class in the emerging markets of Asia. We will work to achieve our strategy by focusing our resources on four key pillars for future growth:

| • | Continuing to build on our leadership position in Canadian insurance, wealth management and employee benefits; |

| • | Becoming a leader in group insurance and voluntary benefits in the U.S.; |

| • | Supporting continued growth in MFS, and broadening our other asset management businesses around the world; and |

| • | Strengthening our competitive position in Asia. |

In targeting these four pillars of growth, we will shift our focus to products that have superior growth characteristics, better product economics and lower capital requirements in order to reduce net income volatility and improve our return on equity. As we focus our growth on key opportunities, the maintenance of a balanced and diversified portfolio of businesses remains fundamental to our strategy.

Values

These values guide us in achieving our strategy:

| • | Integrity – We are committed to the highest standards of business ethics and good governance. |

| • | Engagement – We value our diverse, talented workforce and encourage, support and reward them for contributing to the full extent of their potential. |

| • | Customer Focus – We provide sound financial solutions for our customers and always work with their interests in mind. |

| • | Excellence – We pursue operational excellence through our dedicated people, our quality products and services, and our value-based risk management. |

| • | Value – We deliver value to the customers and shareholders we serve and to the communities in which we operate. |

Sun Life Financial Inc. | sunlife.com | 5 |

ANNUAL INFORMATION FORM 2011

Three Year History: Acquisitions, Disposals, and Other Developments

We assess our businesses and corporate strategies on an ongoing basis to ensure that we make optimal use of our capital and provide maximum shareholder value. The following summary outlines our major acquisitions, dispositions and other developments in the past three years. Additional information is provided in Note [3] to SLF Inc.’s 2011 Consolidated Financial Statements.

Acquisition of U.K. Business

On October 1, 2009, we acquired the United Kingdom operations of Lincoln National Corporation for $387 million. At that time, the acquisition increased Sun Life U.K.’s assets under management nearly 60% to $20 billion and doubled the number of policies in force to 1.1 million. The complementary operations of SLF U.K. and Lincoln National U.K. each held books of business in life insurance, pensions and annuities.

Sale of Reinsurance Business

On December 31, 2010, we completed the sale our life reinsurance business. The transaction was part of our strategy to deploy capital to parts of our business that can best achieve strong sustainable growth. The sale increased Sun Life Assurance’s MCCSR by 14 points as at December 31, 2010.

Acquisition in the Philippines

On October 24, 2011, we acquired a 49% stake of Grepalife Financial, Inc. and formed a new joint venture, Sun Life Grepa Financial Inc. The new joint venture includes an exclusive bancassurance relationship with the Yuchengco-owned Rizal Commercial Banking Corporation, which serves two million customers in more than 350 branches nationwide.

Chairman and Chief Executive Officer Appointments

Dean A. Connor was appointed as President and Chief Executive Officer of Sun Life Financial Inc. effective December 1, 2011, upon the retirement of Donald A. Stewart. James H. Sutcliffe was appointed as Chairman of Sun Life Financial Inc. effective December 1, 2011. Mr. Sutcliffe replaced Ronald W. Osborne, who stepped down as Chairman effective November 30, 2011 and who will retire as a Director at the 2012 annual meeting.

Strengthening Asset Management Capabilities

On November 7, 2011, we acquired the minority shares of McLean Budden Limited (“McLean Budden”), our Canadian investment management subsidiary, and subsequently transferred all of the shares of McLean Budden to MFS Investment Management. McLean Budden is now a wholly owned subsidiary of MFS and continues to be based in Toronto.

Discontinuing Sales of Domestic Individual Life and Annuity Products in SLF U.S.

On December 12, 2011, we announced the completion of a strategic review of our businesses. As a result of this review, we closed our domestic U.S. variable annuity and individual life products to new sales effective December 30, 2011. This decision reflects our focus on reducing volatility and improving return on shareholders’ equity by shifting capital to businesses with superior growth, risk and return characteristics.

Restructuring in the United Kingdom

Effective December 30, 2011, we reorganized the business of our two main operating companies in the United Kingdom to create a more efficient operational and financial business structure. Under the reorganization, all the long-term policies of SLFC Assurance (UK) Limited were transferred to Sun Life Assurance Company of Canada (U.K.) Limited.

Other Developments

On July 15, 2009, we established a joint venture with CIMB Group to distribute life, accident and health insurance products through the 600-plus retail branches of P.T. Bank CIMB Niaga in Indonesia.

On July 20, 2010, Sun Life Everbright Life Insurance Company Limited (“Sun Life Everbright”) was restructured as a domestic insurance company. Under the restructuring of our joint venture with China Everbright Group Company, additional strategic investors were introduced, which reduced our ownership in Sun Life Everbright from 50% to 24.99%.

On December 31, 2010, Sun Life Assurance entered into an external reinsurance agreement for the insured business in SLF Canada’s Group Benefits operations. The implementation of this agreement resulted in an increase in Sun Life Assurance’s MCCSR ratio by 12 points.

Sun Life Financial Inc. | sunlife.com | 6 |

ANNUAL INFORMATION FORM 2011

Business of Sun Life Financial

Information about our business and operating segments, our products and methods of distribution, risk management policies and investment activities, is included in SLF Inc.’s 2011 MD&A which is incorporated by reference in this AIF.

Protection and Wealth Businesses

The global financial services industry continues to evolve rapidly in response to demographic and economic trends. The aging of the population in developed markets is placing a greater demand for wealth accumulation products for working age employees, income distribution products for employees closer to retirement and wealth transfer vehicles for retirees. The aging of the population is also straining existing health care systems, as a larger portion of the population is expected to require health care services over a longer timeframe. Demand for products such as long-term care, critical illness and voluntary group insurance is growing as consumers turn to products that help ensure direct access to a range of health care services and employers continue to download health costs to employees amid tough economic environment. Concern about the adequacy of public pension plans and employer funded retirement plans is continuing to provide growth in other financial vehicles that address baby boomers’ concerns about the need for adequate resources and safeguards against market volatility in retirement.

In the emerging markets of Asia, demand for a wide variety of financial products, including protection, savings and investment vehicles is growing strongly driven by the rising affluence of consumers, further urbanization and regional demographic changes such as the aging population in China. Furthermore, these markets are expected to grow much faster than the industrialized countries as penetration rates there are much lower.

Competition

The markets in which Sun Life Financial engages are highly competitive. We are not only competing against other insurance companies, but also investment managers, mutual fund companies, banks, financial planners and other financial service providers. Frequently, competition is based on pricing, the ability to provide value-added services and deliver excellence to both distributors and customers, and financial strength.

The insurance markets in which we compete are diverse and at different stages of development. In Canada, the industry is relatively mature and the three largest companies serve more than two-thirds of the Canadian insurance market. In the United States, the largest insurance market in the world, the market is more fragmented and characterized by a large number of competitors. The resilience of the economies in emerging markets, along with the growth potential in Asian markets such as India and China, has created strong competition from domestic and international insurers. Global economic weakness, which continues to persist, has placed substantive competitive pressure on insurers. Increased volatility, lower investment yields and higher capital requirements have forced insurers to review their businesses, re-focus their operations on strategically important businesses and in some cases discontinue or divest non-core lines of business.

Seasonality

Certain lines of our business are subject to seasonal factors. In Canada, sales of investment products spike during the first quarter of the year due to a contribution deadline for Registered Retirement Savings Plan. Timing of sales campaigns also influences sales of individual products in Canada. In the U.S., the sales pattern of our group life and health business largely reflects the renewal timing of employee benefit plans of our corporate clients, many of which begin on January 1 each year. This often results in higher sales in the fourth quarter. In India, the sales of individual products through our insurance joint venture usually peak in the first quarter of each year due to tax planning. Overall, the impact of seasonal trends is not material to Sun Life Financial.

Number of Employees

As at December 31, 2011, we had 15,000 full-time equivalent employees across our operations excluding joint ventures.

| Business Segment | Employees | |||

SLF Canada | 5,480 | |||

SLF U.S. | 2,960 | |||

MFS | 1,750 | |||

SLF Asia | 1,700 | |||

Corporate* | 3,110 | |||

*Corporate includes SLF U.K., reinsurance, investments, enterprise services and other supporting functions.

Sun Life Financial Inc. | sunlife.com | 7 |

ANNUAL INFORMATION FORM 2011

Sustainability Commitment

We are committed to the principle of sustainability in conducting our business, which means we meet present needs in a responsible manner without comprising the ability of future generations to meet their needs. It is our view that sustainability extends well beyond the environmental definition into every aspect of business. Our commitment is set out in our Code of Business Conduct which applies to all employees and directors. We have an International Sustainability Council composed of senior representatives from key functions across the organization with the mandate to review our current practices, examine benchmarks, establish targets, identify opportunities and recommend new policies and initiatives. The International Sustainability Council meets regularly and reports progress to our senior executive management. In 2011, we began seeking opportunities that exist through increasing our knowledge of the social and environmental practices of our suppliers so they may be considered in our purchasing decisions. We continued our efforts to manage our buildings efficiently and improve the environment in our offices; we built on our leadership as a major investor in projects of social and environmental value; and we introduced innovations that improve access to our products and services while at the same time reducing paper in our dealings with customers.

Capital Structure

General

SLF Inc.’s authorized capital consists of unlimited numbers of common shares (“Common Shares”), Class A Shares (the “Class A Preferred Shares”) and Class B Shares (the “Class B Preferred Shares”), each without nominal or par value.

The Class A Preferred Shares and Class B Preferred Shares may be issued in series as determined by SLF Inc.’s Board of Directors. The Board of Directors is authorized to fix the number, consideration per share, designation and rights and restrictions attached to each series of shares. The holders of Class A Preferred Shares and Class B Preferred Shares are not entitled to any voting rights except as described below or as otherwise provided by law. Additional information concerning our capital structure is included in SLF Inc.’s 2011 MD&A under the heading Capital and Liquidity Management and in Note 23 to SLF Inc.’s 2011 Consolidated Financial Statements.

Common Shares

Each Common Share is entitled to one vote at meetings of the shareholders of SLF Inc., except for meetings at which only holders of another specified class or series of shares are entitled to vote separately as a class or series.

Common Shares are entitled to receive dividends if and when declared by the Board of Directors. Dividends must be declared and paid in equal amounts per share on all Common Shares, subject to the rights of holders of the Class A Preferred Shares and Class B Preferred Shares. Holders of Common Shares will participate in any distribution of the net assets of SLF Inc. upon its liquidation, dissolution or winding-up on an equal basis per share, subject to the rights of the holders of the Class A Preferred Shares and Class B Preferred Shares. There are no pre-emptive, redemption, purchase or conversion rights attaching to the Common Shares.

As at February 10, 2012, SLF Inc. had 587,814,237 common shares issued and outstanding, which are listed on the Toronto, New York and Philippines stock exchanges, under the ticker symbol “SLF”.

Class A Preferred Shares

The Class A Preferred Shares of each series rank on parity with the Class A Preferred Shares of each other series with respect to the payment of dividends and the return of capital on the liquidation, dissolution or winding-up of SLF Inc. The Class A Preferred Shares are entitled to preference over the Class B Preferred Shares, the Common Shares and any other shares ranking junior to the Class A Preferred Shares with respect to the payment of dividends and the return of capital. The special rights and restrictions attaching to the Class A Preferred Shares as a class may not be amended without such approval as may then be required by law, subject to a minimum requirement of approval by the affirmative vote of at least two-thirds of the votes cast at a meeting of the holders of Class A Preferred Shares held for that purpose.

The following table provides information on SLF Inc.’s issued and outstanding Class A Preferred Shares. These Class A Preferred Shares are listed on the Toronto Stock Exchange (“TSX”).

Sun Life Financial Inc. | sunlife.com | 8 |

ANNUAL INFORMATION FORM 2011

Class A Preferred Shares

| Series | Number of Shares Issued | TSX Ticker | Quarterly Dividend ($) | Early Redemption Date | Prospectus Date | |||||||||||

Series 1 | 16,000,000 | SLF.PR.A | 0.296875 | March 31, 2011 | February 17, 2005 | |||||||||||

Series 2 | 13,000,000 | SLF.PR.B | 0.300000 | September 30, 2011 | July 8, 2005 | |||||||||||

Series 3 | 10,000,000 | SLF.PR.C | 0.278125 | March 31, 2011 | January 6, 2006 | |||||||||||

Series 4 | 12,000,000 | SLF.PR.D | 0.278125 | December 31, 2011 | October 2, 2006 | |||||||||||

Series 5 | 10,000,000 | SLF.PR.E | 0.281250 | March 31, 2012 | January 25, 2007 | |||||||||||

Series 6R | 10,000,000 | SLF.PR.F | 0.375000 | June 30, 2014 | May 8, 2009 | |||||||||||

Series 8R | 11,200,000 | SLF.PR.G | 0.271875 | June 30, 2015 | May 13, 2010 | |||||||||||

Series 10R | 8,000,000 | SLF.PR.H | 0.243750 | September 30, 2016 | August 5, 2011 | |||||||||||

Series 12R | 12,000,000 | SLF.PR.I | 0.265625 | December 31, 2016 | November 3, 2011 | |||||||||||

The shares in each series of Class A Preferred Shares were issued for $25 per share and holders are entitled to receive the non-cumulative quarterly dividends outlined in the preceding table. Subject to regulatory approval, SLF Inc. may redeem these shares on or after the early redemption dates noted above, in whole or in part at a declining premium. Additional information concerning these shares is contained in the prospectus under which the shares were issued, which may be accessed at www.sedar.com.

Class B Preferred Shares

The Class B Preferred Shares of each series rank on a parity with the Class B Preferred Shares of each other series with respect to the payment of dividends and the return of capital on the liquidation, dissolution or winding-up of SLF Inc. The Class B Preferred Shares are entitled to preference over the Common Shares and any other shares ranking junior to the Class B Preferred Shares with respect to the payment of dividends and the return of capital, but are subordinate to the Class A Preferred Shares and any other shares ranking senior to the Class B Preferred Shares with respect to the payment of dividends and return of capital. The special rights and restrictions attaching to the Class B Preferred Shares as a class may not be amended without such approval as may then be required by law, subject to a minimum requirement of approval by the affirmative vote of at least two-thirds of the votes cast at a meeting of the holders of Class B Preferred Shares held for that purpose. No Class B Preferred Shares have been issued.

Constraints on Shares

The Insurance Act contains restrictions on the purchase or other acquisition, issue, transfer and voting of the shares of SLF Inc. and Sun Life Assurance. Information on those restrictions can be found in this AIF under the heading Regulatory Matters – Canada – Restrictions on Ownership.

Market for Securities

The following tables set out the price range and trading volumes of SLF Inc.’s Common Shares and Class A Preferred Shares on the TSX during 2011:

Common Shares | ||||||||

| Price ($) | Trading volume | |||||||

| High | Low | Close | (thousands) | |||||

January | 31.91 | 30.15 | 31.51 | 19,960 | ||||

February | 34.39 | 31.65 | 32.27 | 34,689 | ||||

March | 32.25 | 29.21 | 30.47 | 36,180 | ||||

April | 31.03 | 29.14 | 30.97 | 25,994 | ||||

May | 31.50 | 29.41 | 30.45 | 26,404 | ||||

June | 30.48 | 27.93 | 29.05 | 24,390 | ||||

July | 29.58 | 26.41 | 26.41 | 19,625 | ||||

August | 26.79 | 24.04 | 26.54 | 41,483 | ||||

September | 26.69 | 23.43 | 25.03 | 33,859 | ||||

October | 26.58 | 23.21 | 25.16 | 36,325 | ||||

November | 24.80 | 17.92 | 18.46 | 52,929 | ||||

December | 20.04 | 18.06 | 18.90 | 54,892 | ||||

Sun Life Financial Inc. | sunlife.com | 9 |

ANNUAL INFORMATION FORM 2011

Class A Preferred Shares

| Series 1 | Series 2 | |||||||||||||||||

| Price ($) | Trading volume | Price ($) | Trading volume | |||||||||||||||

| High | Low | Close | (thousands) | High | Low | Close | (thousands) | |||||||||||

January | 23.10 | 21.57 | 22.85 | 473 | 23.36 | 21.90 | 23.10 | 518 | ||||||||||

February | 23.84 | 22.83 | 23.23 | 411 | 23.99 | 23.00 | 23.57 | 328 | ||||||||||

March | 23.34 | 22.50 | 22.80 | 404 | 23.60 | 22.81 | 23.00 | 554 | ||||||||||

April | 22.93 | 22.04 | 22.25 | 270 | 23.06 | 22.29 | 22.70 | 196 | ||||||||||

May | 23.79 | 22.30 | 23.75 | 319 | 24.16 | 22.65 | 23.97 | 358 | ||||||||||

June | 23.98 | 23.03 | 23.37 | 450 | 24.39 | 23.31 | 23.39 | 217 | ||||||||||

July | 23.55 | 22.75 | 23.55 | 198 | 23.65 | 23.01 | 23.65 | 233 | ||||||||||

August | 23.84 | 22.50 | 23.20 | 515 | 23.98 | 22.66 | 23.41 | 203 | ||||||||||

September | 23.33 | 22.28 | 22.50 | 290 | 23.46 | 22.59 | 22.68 | 234 | ||||||||||

October | 23.05 | 21.60 | 23.05 | 254 | 23.20 | 21.51 | 23.20 | 275 | ||||||||||

November | 23.10 | 21.88 | 22.04 | 251 | 23.26 | 22.03 | 22.03 | 202 | ||||||||||

December | 22.23 | 21.20 | 22.15 | 236 | 22.39 | 21.52 | 22.35 | 163 | ||||||||||

| Series 3 | Series 4 | |||||||||||||||||

| Price ($) | Trading volume | Price ($) | Trading volume | |||||||||||||||

| High | Low | Close | (thousands) | High | Low | Close | (thousands) | |||||||||||

January | 21.69 | 20.37 | 21.45 | 245 | 21.70 | 20.33 | 21.41 | 560 | ||||||||||

February | 22.57 | 21.33 | 22.00 | 353 | 22.58 | 21.40 | 22.00 | 317 | ||||||||||

March | 22.06 | 21.19 | 21.40 | 244 | 22.11 | 21.25 | 21.35 | 318 | ||||||||||

April | 21.59 | 20.73 | 21.05 | 320 | 21.62 | 20.73 | 21.15 | 138 | ||||||||||

May | 22.75 | 21.03 | 22.53 | 466 | 22.54 | 21.17 | 22.52 | 302 | ||||||||||

June | 23.48 | 22.00 | 22.06 | 497 | 22.93 | 21.94 | 22.05 | 251 | ||||||||||

July | 22.21 | 21.80 | 22.18 | 251 | 22.19 | 21.72 | 22.12 | 247 | ||||||||||

August | 22.34 | 21.30 | 21.90 | 247 | 22.27 | 21.25 | 21.94 | 287 | ||||||||||

September | 22.09 | 20.93 | 21.00 | 451 | 21.95 | 20.91 | 21.03 | 384 | ||||||||||

October | 21.77 | 19.89 | 21.67 | 321 | 21.75 | 19.90 | 21.60 | 389 | ||||||||||

November | 21.77 | 20.71 | 20.75 | 179 | 21.58 | 20.63 | 20.63 | 246 | ||||||||||

December | 21.08 | 20.23 | 20.80 | 247 | 21.19 | 20.25 | 20.85 | 241 | ||||||||||

| Series 5 | Series 6R | |||||||||||||||||

| Price ($) | Trading volume | Price ($) | Trading volume | |||||||||||||||

| High | Low | Close | (thousands) | High | Low | Close | (thousands) | |||||||||||

January | 21.88 | 20.51 | 21.52 | 346 | 27.79 | 26.97 | 27.00 | 148 | ||||||||||

February | 22.95 | 21.45 | 22.20 | 266 | 27.75 | 26.58 | 26.99 | 250 | ||||||||||

March | 22.18 | 21.26 | 21.51 | 265 | 27.35 | 26.60 | 27.10 | 545 | ||||||||||

April | 21.76 | 20.81 | 21.12 | 172 | 27.40 | 26.85 | 27.00 | 136 | ||||||||||

May | 22.80 | 20.93 | 22.60 | 267 | 27.77 | 26.80 | 27.10 | 163 | ||||||||||

June | 22.94 | 22.16 | 22.25 | 319 | 27.35 | 26.78 | 26.90 | 104 | ||||||||||

July | 22.29 | 21.90 | 22.17 | 392 | 27.46 | 26.90 | 27.37 | 121 | ||||||||||

August | 22.43 | 21.27 | 22.02 | 286 | 27.30 | 26.45 | 26.80 | 79 | ||||||||||

September | 22.10 | 21.15 | 21.25 | 315 | 27.12 | 26.36 | 26.64 | 132 | ||||||||||

October | 21.94 | 20.15 | 21.82 | 202 | 26.95 | 25.88 | 26.95 | 77 | ||||||||||

November | 21.88 | 20.82 | 21.11 | 144 | 27.20 | 25.75 | 25.88 | 519 | ||||||||||

December | 21.37 | 20.42 | 21.13 | 181 | 26.59 | 25.71 | 26.29 | 87 | ||||||||||

| Series 8R | Series 10R(1) | |||||||||||||||||

| Price ($) | Trading volume | Price ($) | Trading volume | |||||||||||||||

| High | Low | Close | (thousands) | High | Low | Close | (thousands) | |||||||||||

January | 26.00 | 25.28 | 25.50 | 165 | - | - | - | - | ||||||||||

February | 26.25 | 25.07 | 25.25 | 188 | - | - | - | - | ||||||||||

March | 26.05 | 24.96 | 25.64 | 225 | - | - | - | - | ||||||||||

April | 25.74 | 25.17 | 25.41 | 135 | - | - | - | - | ||||||||||

May | 25.96 | 25.14 | 25.25 | 230 | - | - | - | - | ||||||||||

June | 25.58 | 25.00 | 25.14 | 338 | - | - | - | - | ||||||||||

July | 25.98 | 25.01 | 25.69 | 73 | - | - | - | - | ||||||||||

August | 25.85 | 24.91 | 25.00 | 210 | 24.87 | 24.67 | 24.77 | 1,234 | ||||||||||

September | 25.32 | 24.69 | 25.10 | 120 | 24.93 | 24.25 | 24.80 | 357 | ||||||||||

October | 25.22 | 24.37 | 25.00 | 264 | 24.90 | 24.00 | 24.65 | 321 | ||||||||||

November | 25.45 | 23.00 | 23.21 | 284 | 24.70 | 23.16 | 23.18 | 322 | ||||||||||

December | 23.50 | 21.40 | 22.40 | 279 | 23.50 | 21.70 | 22.77 | 210 | ||||||||||

| (1) Series 10R shares were issued on August 12, 2011 | ||||||||||||||||||

Sun Life Financial Inc. | sunlife.com | 10 |

ANNUAL INFORMATION FORM 2011

| Series 12R(2) | ||||||||

| Price ($) | Trading volume | |||||||

| High | Low | Close | (thousands) | |||||

January | - | - | - | - | ||||

February | - | - | - | - | ||||

March | - | - | - | - | ||||

April | - | - | - | - | ||||

May | - | - | - | - | ||||

June | - | - | - | - | ||||

July | - | - | - | - | ||||

August | - | - | - | - | ||||

September | - | - | - | - | ||||

October | - | - | - | - | ||||

November | 24.90 | 24.30 | 24.35 | 1,047 | ||||

December | 24.49 | 23.00 | 24.15 | 335 | ||||

(2) Series 12R shares were issued on November 10, 2011 | ||||||||

Sales of Unlisted Securities

SLF Inc. has not issued any securities that are not listed or quoted on a marketplace since January 1, 2012.

Dividends

The declaration, amount and payment of dividends by SLF Inc. is subject to the approval of its Board of Directors and is dependent on our results of operations, financial condition, cash requirements, regulatory and contractual restrictions and other factors considered by the Board of Directors.

The dividends declared by SLF Inc. in the three years ended December 31, 2011 are shown below.

| 2011 | 2010 | 2009 | ||||||

Common Shares | $ 1.44 | $ 1.44 | $ 1.44 | |||||

Class A Preferred Shares | ||||||||

Series 1 | $1.187500 | $1.187500 | $1.187500 | |||||

Series 2 | $1.200000 | $1.200000 | $1.200000 | |||||

Series 3 | $1.112500 | $1.112500 | $1.112500 | |||||

Series 4 | $1.112500 | $1.112500 | $1.112500 | |||||

Series 5 | $1.125000 | $1.125000 | $1.125000 | |||||

Series 6R | $1.500000 | $1.500000 | $0.921580 | |||||

Series 8R | $1.087500 | $0.653245 | - | |||||

Series 10R | $0.376640 | - | - | |||||

Series 12R(1) | - | - | - | |||||

(1) The Series 12R shares were issued on November 10, 2011. The first dividend is scheduled to be paid on March 31, 2012 subject to the approval of the Board of Directors as described above.

The Insurance Act prohibits the declaration or payment of dividends on shares of an Insurance Holding Company or a Canadian life insurance company if there are reasonable grounds for believing the company does not have, or the payment of the dividend would cause the company not to have, adequate capital or liquidity, or upon any direction made by the Superintendent. The Insurance Act also requires that an insurance company notify the Superintendent of the declaration of a dividend at least fifteen days before the dividend payment date.

As a holding company, SLF Inc. depends primarily on the receipt of funds from its subsidiaries to pay shareholder dividends, interest payments and operating expenses. The source of these funds is primarily dividends and capital repayments that SLF Inc. receives from its subsidiaries. The inability of its subsidiaries to pay dividends or return capital in the future may materially impair SLF Inc.’s ability to pay dividends to shareholders or to meet its cash obligations. Additional information concerning legislation regulating the ability of SLF Inc.’s subsidiaries in Canada, the U.S. and the U.K. to pay dividends or return capital can be found in this AIF under the heading Regulatory Matters.

We have covenanted that, if a distribution is not paid when due on any outstanding Sun Life ExchangEable Capital Securities (“SLEECS”) issued by Sun Life Capital Trust and Sun Life Capital Trust II, Sun Life Assurance will not pay dividends on its Public Preferred Shares, if any are outstanding. If Sun Life Assurance does not have any Public Preferred Shares, then SLF Inc. will not pay dividends on its preferred shares or Common Shares, in each case, until the 12th month (in the case of the SLEECS issued by Sun Life Capital Trust) or 6th month (in the case of SLEECS issued by Sun Life Capital Trust II) following the failure to pay the required distribution in full, unless the required distribution is paid to the holders of the SLEECS. Public Preferred Shares means preferred shares issued by Sun Life Assurance which: (a) have

Sun Life Financial Inc. | sunlife.com | 11 |

ANNUAL INFORMATION FORM 2011

been issued to the public (excluding any preferred shares held beneficially by affiliates of Sun Life Assurance); (b) are listed on a recognized stock exchange; and (c) have an aggregate liquidation entitlement of at least $200 million. Sun Life Assurance has not issued any shares that qualify as Public Preferred Shares as at the date of this AIF.

The terms of SLF Inc.’s outstanding Class A Preferred Shares provide that for so long as Sun Life Assurance is a subsidiary, no dividends on such preferred shares may be declared or paid if the MCCSR ratio of Sun Life Assurance is less than 120%.

Security Ratings

SLF Inc.’s Class A Preferred Shares, senior unsecured debentures, and subordinated unsecured debentures are rated by independent rating agencies. Security ratings assigned to securities by the rating agencies may be subject to revision or withdrawal at any time by the applicable rating agency and are not a recommendation to purchase, hold or sell these securities as such ratings do not comment as to market price or suitability for a particular investor. Security ratings are intended to provide investors with an independent measure of the credit quality of an issue of securities.

The table below provides the security ratings for SLF Inc.’s securities as at February 10, 2012.

Security Ratings | ||||||||||||||||

| DBRS1 | S&P2 | Moody’s3 | Fitch4 | |||||||||||||

| Rating | Rank | Rating | Rank | Rating | Rank | Rating | Rank | |||||||||

Class A Preferred Shares | Pfd-1(low) | 3 of 16 | P-2(high) /BBB+5 | 4 of 18/ 8 of 225 | Baa3 | 10 of 21 | BBB | 9 of 19 | ||||||||

Series 1 to 12R | ||||||||||||||||

Senior Unsecured Debentures | AA (low) | 4 of 26 | A | 6 of 22 | NR6 | A- | 7 of 19 | |||||||||

Series A,B,D & E | ||||||||||||||||

Subordinated Unsecured Debentures | A(high) | 5 of 26 | A- | 7 of 22 | NR6 | BBB+ | 8 of 19 | |||||||||

Series 2007-1, Series 2008-1, Series 2008-2 and Series 2009-1 | ||||||||||||||||

| 1 | DBRS Limited |

| 2 | Standard & Poor’s, a division of McGraw-Hill Companies |

| 3 | Moody’s Investors Service has only provided a rating for SLF Inc.’s Class A Preferred Shares Series 2 |

| 4 | We do not participate in Fitch’s rating process, or provide additional information to Fitch Ratings, beyond our available public disclosures |

| 5 | The Canadian scale rating/global scale rating for preferred shares |

| 6 | Not Rated |

Since January 1, 2011, rating agencies have taken the following actions with respect to the securities issued by SLF Inc. which are listed above:

| • | On January 26, 2011, Fitch Ratings (“Fitch”) affirmed the long term counterparty credit (debt) and security ratings and revised outlook to Stable from Negative |

| • | On April 15, 2011, Standard & Poor’s (“S&P”) affirmed the counterparty and security credit ratings and revised its outlook to Stable from Negative |

| • | On June 13, 2011, DBRS Limited (“DBRS”) affirmed its long term counterparty credit (debt) ratings |

| • | On June 22, 2011, Fitch affirmed all its ratings with a Stable outlook |

| • | On October 18, 2011, Moody’s Investors Service (Moody’s) affirmed security ratings but revised its outlook to Negative from Stable |

| • | On December 13, 2011, S&P affirmed the counterparty and security credit ratings but placed them on CreditWatch with negative implications following the Company’s decision to discontinue sales of domestic individual life and annuity products in SLF U.S. |

| • | On January 19, 2012, Fitch affirmed the long term counterparty credit (debt) and security ratings and revised outlook to Negative from Stable |

| • | On January 26, 2012, Moody’s downgraded the preferred stock rating of SLF Inc. to Baa3 from Baa2 and left Negative outlook in place, concluding the review initiated in October 2011. |

We expect S&P to resolve its outlook during Q1 2012, and there can be no assurance, nor can we predict, that there will be no downgrades.

The descriptions of the ratings below are sourced from public information as disclosed by each rating agency.

DBRS

DBRS assigns ratings for preferred shares in a range from Pfd-1 to D. Reference to “high” and “low” designations indicate standing within the major rating categories. The DBRS preferred share rating scale is used in the Canadian securities market and is meant to give an indication of the risk that a borrower will not fulfill its full obligations in a timely manner, with respect to both dividend and principal commitments.

SLF Inc.’s Class A Preferred Shares have been assigned a Pfd-1 rating, the highest among rating categories used by DBRS. Preferred shares rated Pfd-1 are of superior credit quality and are supported by entities with strong earnings and balance sheet characteristics.

Sun Life Financial Inc. | sunlife.com | 12 |

ANNUAL INFORMATION FORM 2011

The DBRS long-term rating scale provides an opinion on the risk of default. That is, the risk that an issuer will fail to satisfy its financial obligations in accordance with the terms under which an obligation has been issued. Ratings are based on quantitative and qualitative considerations relevant to the issuer, and the relative ranking of claims. DBRS assigns long-term ratings in a range from AAA to D, and “high” and “low” designations indicate standing within the major rating categories.

SLF Inc.’s Senior Unsecured Debentures have been assigned an AA (low) rating. AA ratings, reflecting a superior credit quality, are assigned to issues when the capacity for the payment of financial obligations is considered high. Credit quality differs from AAA, the highest possible rating category, only to a small degree, and significant vulnerability to future events is unlikely.

SLF Inc.’s Subordinated Unsecured Debentures have been assigned an A (high) rating. A ratings, reflecting a good credit quality, are assigned to issues when the capacity for the payment of financial obligations is substantial, but of lesser credit quality than AA, and the issue may be vulnerable to future events, but qualifying negative factors are considered manageable.

Standard & Poor’s

S&P has Canadian and global rating scales for preferred shares. S&P assigns ratings for Canadian preferred shares in a range from P-1 to D on the Canadian scale and from AAA to D on the global rating scale. S&P uses “high” and “low” designations to indicate standing within the major rating categories on the Canadian rating scale and + or - designations to indicate the relative standing of securities within a particular rating category on the global rating scale.

S&P’s preferred share rating on the Canadian scale is a forward-looking opinion about the creditworthiness of an obligor with respect to a specific preferred share obligation issued in the Canadian market, relative to preferred shares issued by other issuers in the Canadian market. The Canadian scale rating is fully determined by the applicable global scale rating, and there are no additional analytical criteria associated with the determination of ratings on the Canadian scale. S&P presents an issuer’s preferred share ratings on both the global rating scale and on the Canadian national scale when listing the ratings for a particular issuer.

SLF Inc.’s Class A Preferred Shares have been assigned a P-2 rating on the Canadian scale, which corresponds to a BBB+ rating on the global scale. The P-2 rating denotes that the specific obligation exhibits adequate protection parameters. However, adverse economic conditions or changing circumstances are more likely to lead to a weakened capacity of the obligor to meet its financial commitment on the obligation.

The S&P rating scale for long-term debt is based on the likelihood of payment-capacity and willingness of the obligor to meet its financial commitment on an obligation in accordance with the terms of the obligation; and the protection afforded by, and the relative position of, the obligation in the event of bankruptcy, reorganization, or other arrangement under the laws of bankruptcy and other laws affecting creditor’s rights.

S&P assigns long-term ratings in a range from AAA to D and uses + or - designations to indicate the relative standing of securities within a particular rating category.

SLF Inc.’s Senior Unsecured Debentures and Subordinated Unsecured Debentures have been assigned A and A- ratings, respectively. An A rating category indicates that the obligor’s capacity to meet its financial commitment is strong.

Moody’s

Moody’s long-term obligation ratings are opinions of the relative credit risk of financial obligations with an original maturity of one year or more. They address the possibility that a financial obligation will not be honoured as promised. Such ratings use Moody’s Global Scale and reflect both the likelihood of default and any financial loss suffered in the event of default.

Moody’a assigns long-term ratings for debt and preferred shares in a range from Aaa to C. Moody’s appends numerical modifiers 1, 2, and 3 to each generic rating classification from Aa through Caa. The modifier 1 indicates that the obligation ranks in the higher end of its generic rating category; the modifier 2 indicates a mid-range ranking; and the modifier 3 indicates a ranking in the lower end of that generic rating category.

SLF Inc.’s Class A Preferred Shares Series 2 have been assigned a Baa3 rating. Obligations rated Baa are subject to moderate credit risk. They are considered medium grade and as such may possess certain speculative characteristics.

Fitch

Fitch’s credit ratings provide an opinion on the relative ability of an entity to meet financial commitments, such as interest, preferred dividends, repayment of principal, insurance claims or counterparty obligations. Fitch’s credit ratings do not directly address any risk other than credit risk. In particular, ratings do not deal with the risk of a market value loss on a rated security due to changes in interest rates, liquidity and other market considerations.

Sun Life Financial Inc. | sunlife.com | 13 |

ANNUAL INFORMATION FORM 2011

Fitch assigns long-term ratings for debt and preferred shares in a range from AAA to D. The modifiers + or - may be appended to a rating to denote relative status within major rating categories.

SLF Inc.’s Class A Preferred Shares and Subordinated Unsecured Debentures have been assigned BBB and BBB+ ratings, respectively. A BBB rating indicates that expectations of default risk are currently low and the capacity for payment of financial commitments is considered adequate but adverse business or economic conditions are more likely to impair this capacity.

SLF Inc.’s Senior Unsecured Debentures have been assigned an A- rating. An A rating denotes expectations of low default risk and the capacity for payment of financial commitments is considered strong. This capacity may, nevertheless, be more vulnerable to adverse business or economic conditions than is the case for higher ratings.

Asset-backed Securities

We have issued asset-backed securities in the past as part of our normal course of business. Information about our asset securitization program is provided in SLF Inc.’s 2011 MD&A under the Capital and Liquidity Management section under the heading Asset Securitizations.

Transfer Agents and Registrars

Common Shares

CIBC Mellon Trust Company is the principal Transfer Agent for SLF Inc.’s common shares. The central securities register is maintained in Toronto, Ontario, Canada.

Transfer Agent | ||

Canada | CIBC Mellon Trust Company P.O. Box 7010 Adelaide Street Postal Station Toronto, Ontario Canada M5C 2W9 | |

Co-Transfer Agents

| ||

United States | American Stock Transfer & Trust Company, LLC 6201 15th Avenue Brooklyn, NY 11219 United States | |

United Kingdom | Capita Registrars The Registry 34 Beckenham Road Beckenham Kent BR3 4TU United Kingdom | |

Philippines | The Hongkong and Shanghai Banking Corporation Limited HSBC Stock Transfer 7/F, HSBC Centre 3058 Fifth Avenue West Bonifacio Global City Taguig City, 1634, Philippines | |

Hong Kong | Computershare Hong Kong Investor Services Limited 17M Floor, Hopewell Centre 183 Queen’s Road East Wanchai, Hong Kong | |

Sun Life Financial Inc. | sunlife.com | 14 |

ANNUAL INFORMATION FORM 2011

Preferred Shares and Debentures

CIBC Mellon Trust Company is the transfer agent for SLF Inc.’s Class A Preferred Shares, and CIBC Mellon Trust Company c/o BNY Trust Company of Canada is the trustee and the registrar for SLF Inc.’s senior unsecured debentures, Series A, B, D and E and its subordinated debentures, Series 2007-1, Series 2008-1, Series 2008-2 and Series 2009-1. The registers for those securities are maintained in Toronto, Ontario, Canada.

Directors and Executive Officers

Board of Directors

At December 31, 2011, the Board of Directors of SLF Inc. had five standing committees: Audit Committee, Governance and Conduct Review Committee, Investment Oversight Committee, Management Resources Committee and Risk Review Committee.

The following table sets out the directors of SLF Inc. as of the date of this AIF and, for each director, the province or state and country of his or her residence, principal occupation, years as a director, and membership on board committees. The term of each director expires at the close of business of the Annual Meeting in 2012. Each director of SLF Inc. is an independent director as defined in the Company’s Director Independence Policy, except Mr. Connor, the President and Chief Executive Officer of SLF Inc. and Mr. Boscia, a former executive of SLF Inc.

Name and Province/State and | Principal Occupation | Director Since | Board Committee Membership | |||

William D. Anderson Ontario, Canada | Corporate Director | 2010 | Audit Risk Review | |||

Richard H. Booth Connecticut, USA | Vice Chairman, Guy Carpenter & Company, LLC (global risk management and reinsurance specialist) | 2011 | Audit Committee Governance and Conduct Review | |||

Jon A. Boscia Florida, USA | President and Chief Executive Officer, Boardroom Advisors, LLC (management consulting firm) | 2011 | Investment Oversight Risk Review | |||

John H. Clappison Ontario, Canada | Corporate Director | 2006 | Audit Risk Review | |||

Dean A. Connor Ontario, Canada | President and Chief Executive Officer, SLF Inc. and Sun Life Assurance | 2011 | None | |||

David A. Ganong, CM New Brunswick, Canada | Chairman, Ganong Bros. Limited (private confectionery manufacturer) | 2002 | Governance and Conduct Review Investment Oversight | |||

Martin J. G. Glynn British Columbia, Canada | Corporate Director | 2010 | Audit Investment Oversight | |||

Krystyna T. Hoeg Ontario, Canada | Corporate Director | 2002 | Management Resources Risk Review | |||

David W. Kerr Ontario, Canada | Managing Partner, Edper Financial Group (investment holding company) | 2004 | Governance and Conduct Review Management Resources | |||

Idalene F. Kesner Indiana, USA | Associate Dean of Faculty and Research and Frank P. Popoff Chair of Strategic Management, Kelley School of Business, Indiana University | 2002 | Investment Oversight Management Resources | |||

Mitchell M. Merin New Jersey, USA | Corporate Director | 2007 | Investment Oversight Management Resources | |||

Ronald W. Osborne Ontario, Canada | Corporate Director | 1999 | Governance and Conduct Review Investment Oversight | |||

Hugh D. Segal, CM Ontario, Canada | Senator, Parliament of Canada | 2009 | Investment Oversight Management Resources | |||

James H. Sutcliffe London, England | Chairman, SLF Inc. and Sun Life Assurance | 2009 | Governance and Conduct Review Risk Review |

Sun Life Financial Inc. | sunlife.com | 15 |

ANNUAL INFORMATION FORM 2011

Each director of SLF Inc. has been engaged for more than five years in his or her present principal occupation or in other capacities with the company or organization (or predecessor thereof) in which he or she currently holds his or her principal occupation, except:

| (i) | Mr. Sutcliffe, who prior to September 2008, was Group Chief Executive Officer of Old Mutual plc.; |

| (ii) | Mr. Booth, who from 2000 to 2009 was Chairman of HSB Group, Inc., from 2000 to 2007 was President and Chief Executive Officer of HSB Group, and in 2008 and 2009 was also Vice Chairman, Transition Planning and Chief Administrative Officer of American International Group; and |

| (iii) | Mr. Boscia, who from 2008 to 2010, was President, Sun Life Financial, and prior to 2008, was Chairman and Chief Executive Officer of Lincoln Financial Group. |

Audit Committee

The responsibilities and duties of the Audit Committee are set out in its charter, a copy of which is attached as Appendix A.

The Board of Directors has determined that each member of its Audit Committee is independent as defined in the Company’s Director Independence Policy and is financially literate. In the board’s judgment, a member of the Committee is financially literate if, after seeking and receiving any explanations or information from senior financial management of the Company or the auditors of the Company that the member requires, the member is able to read and understand the consolidated financial statements of the Company to the extent sufficient to be able to intelligently ask, and to evaluate the answers to, probing questions about the material aspects of those financial statements.

The members of the Audit Committee as of the date of this AIF and their qualifications and education are set out below.

John H. Clappison (Chairman) is a Chartered Accountant who joined the firm of Price Waterhouse in 1968. He became a Partner of the firm in 1980 and in 1990 became Managing Partner of the Greater Toronto Area office, a position he continued to hold after the merger of Price Waterhouse with Coopers & Lybrand to form PricewaterhouseCoopers in 1998, until he retired in December 2005. He was appointed a Fellow of the Institute of Chartered Accountants of Ontario in 1988. He has lectured on accounting practices at Ryerson University, the University of Toronto and the Institute of Chartered Accountants of Ontario School of Accountancy. Mr. Clappison joined the Board of Directors, the Audit Committee and the Risk Review Committee of SLF Inc. and Sun Life Assurance in 2006. In May 2010 he was appointed Chairman of the Audit Committee. Mr. Clappison is a director and chairman of the audit committee of Cameco Corporation and Inmet Mining Corporation and a director and member of the audit committee of Rogers Communications Inc. Until February 15, 2011, Mr. Clappison was a trustee and chairman of the audit committee of Canadian Real Estate Investment Trust. He is director of Summit Energy Holdings LLP, a private company, a board member of the Canadian Foundation for Facial Plastic and Reconstructive Surgery and a trustee of the Shaw Festival Theatre Endowment Foundation and Roy Thomson Hall and Massey Hall Endowment Foundation. Mr. Clappison is a member of the Canadian Audit Committee Network.

William D. Anderson is a Chartered Accountant who joined BCE Inc., the global telecommunications company, in 1991. He held progressively senior positions including Chief Financial Officer of BCE Inc. from 1998 to 2001, President of BCE Ventures, the strategic investment unit of BCE Inc. from 2001 to 2005, and Chairman and Chief Executive Officer of Bell Canada International Inc. from 2000 to 2007. Prior to joining BCE, Mr. Anderson spent 17 years with the public accounting firm KPMG, where he was a partner for 11 years. He was appointed a Fellow of the Institute of Chartered Accountants of Ontario in October 2011. Mr. Anderson joined the Board of Directors, the Audit Committee and the Risk Review Committee of SLF Inc. and Sun Life Assurance in May 2010. Mr. Anderson serves as chairman of Gildan Activewear Inc. and Nordion Inc. (formerly MDS Inc.), and a director and chairman of the audit and risk committee of TransAlta Corporation. He became a Fellow of the Institute of Corporate Directors in June 2010.

Richard H. Booth is a certified public accountant who is Vice Chairman of Guy Carpenter & Company, LLC, a global risk management and reinsurance specialist and a wholly-owned subsidiary of Marsh & McLennan Companies, Inc. Mr. Booth has held progressively senior positions in the insurance industry throughout his career. From 2000 to 2009 he was Chairman of HSB Group, Inc., a specialty insurer and reinsurer, and from 2000 to 2007 was President and Chief Executive Officer of HSB Group. In 2008 and 2009 Mr. Booth was also Vice Chairman, Transition Planning and Chief Administrative Officer of HSB’s parent company, American International Group, an insurance and financial services company. He joined the Board of Directors, the Audit Committee and the Governance and Conduct Review Committee of SLF Inc. and Sun Life Assurance in May 2011. Mr. Booth serves as a director of Northeast Utilities and WorldBusiness Capital, Inc., a private company, and an advisor to Century Capital LLC. Mr. Booth is a chartered life underwriter, a chartered financial consultant and a former member of the Financial Accounting Standards Advisory Council and its Steering Committee. He is also a director of the National Association of Corporate Directors – Connecticut Chapter.

Sun Life Financial Inc. | sunlife.com | 16 |

ANNUAL INFORMATION FORM 2011

Martin J. Glynn joined the HSBC group, an international banking and financial services organization, in 1982. He held progressively senior positions during his 24-year career at HSBC. Mr. Glynn became Chief Operating Officer of HSBC Bank Canada in 1997, following which he was President and Chief Executive Officer of HSBC Bank Canada from 1999 to 2003 and President and Chief Executive Officer, HSBC Bank USA from 2003 until his retirement in 2006. He joined the Board of Directors, the Audit Committee and the Investment Oversight Committee of SLF Inc. and Sun Life Assurance in December 2010. In addition to serving as a director of HSBC Bank Canada from 1999 to 2006, Mr. Glynn was Chairman from 2004 to 2006. He was also a director of HSBC Bank USA from 2000 to 2006. Mr. Glynn is a director of Husky Energy Inc., was a member of the audit committee from 2000 to 2010 and served as the chairman of the audit committee from 2002 to 2005. He is a director and member of the audit committee of VinaCapital Vietnam Opportunity Fund Limited and was chairman of the audit committee from 2008 to 2009. From 2007 until December 2011, Mr. Glynn was a director and member of the audit committee of Hathor Exploration Limited. He is on the board of the VGH and UBC Hospital Foundation and The American Patrons of the National Library and Galleries of Scotland. Mr. Glynn has a Masters of Business Administration degree and was the Jarislowsky Fellow in Business Management, Haskayne School of Business, University of Calgary, from September 2009 to April 2010.

SLF Inc.’s Board of Directors has determined that John H. Clappison is an audit committee financial expert as defined by the SEC. The SEC has indicated that the designation of a person as an audit committee financial expert does not make that person an “expert” for any purpose, or impose any duties, obligations or liabilities on that person that are greater than those imposed on members of the audit committee and board of directors who do not carry this designation or affect the duties, obligations or liabilities of any other member of the Audit Committee or Board of Directors.

Executive Officers

The following table sets out the Company’s executive officers as at February 15, 2012.

| Name | Province/State and Country of Residence | Position | ||

Dean A. Connor | Ontario, Canada | President and Chief Executive Officer | ||

Claude A. Accum | Massachusetts, USA | Executive Vice-President, Actuarial and Risk Management | ||

Thomas A. Bogart | Ontario, Canada | Executive Vice-President, Business Development & General Counsel | ||

Kevin P. Dougherty | Ontario, Canada | President, SLF Canada and President, Sun Life Global Investments | ||

Colm J. Freyne | Ontario, Canada | Executive Vice-President and Chief Financial Officer | ||

Stephen C. Peacher | Massachusetts, USA | Executive Vice-President and Chief Investment Officer | ||

Mark S. Saunders | Ontario, Canada | Executive Vice-President and Chief Information Officer | ||

Michael P. Stramaglia | Ontario, Canada | Executive Vice-President and Chief Risk Officer | ||

Westley V. Thompson | Connecticut, USA | President, SLF U.S. | ||

Each executive officer of SLF Inc. has held his current position or other senior positions with the Company during the past five years with the following exceptions. Prior to October 2009, Mr. Peacher was Managing Director, Head of Fixed Income and Liquidity Strategies at Columbia Management Group. Prior to March 2009, Mr. Saunders was Senior Technology Officer, Barclays Commercial Bank. Prior to October 2008, Mr. Thompson was President, Employer Markets, Lincoln National Corporation.

Cease Trade Orders, Bankruptcies, Penalties and Sanctions

Except as disclosed below, no director or executive officer of SLF Inc. is or has been, in the last 10 years, a director, chief executive officer or chief financial officer of a company that, while that person was acting in that capacity, (a) was the subject of a cease trade or similar order or an order that denied the company access to any exemption under Canadian securities legislation, for a period of more than 30 consecutive days, or (b) was subject to an event that resulted, after that person ceased to be a director, chief executive officer or chief financial officer, in the company being the subject of a

Sun Life Financial Inc. | sunlife.com | 17 |

ANNUAL INFORMATION FORM 2011

cease trade or similar order or an order that denied the company access to any exemption under Canadian securities legislation, for a period of more than 30 consecutive days. No director or executive officer of SLF Inc. is or has been, in the last 10 years, a director or executive officer of a company that, while that person was acting in that capacity or within a year of that person ceasing to act in that capacity, became bankrupt, made a proposal under any legislation relating to bankruptcy or insolvency or was subject to or instituted any proceedings, arrangement or compromise with creditors or had a receiver, receiver manager or trustee appointed to hold its assets except for the following:

| (i) | Mr. Ganong and Mr. Osborne were directors of Air Canada in April 2003, when it filed for protection under the CCAA. It successfully emerged from proceedings under the CCAA and was restructured according to a plan of arrangement in September 2004. Mr. Ganong and Mr. Osborne are no longer directors of Air Canada. |

| (ii) | Mr. Glynn was a director of MF Global Holdings Ltd. when it filed a voluntary petition under Chapter 11 of the Bankruptcy Code in the United States in October 2011. Mr. Glynn is no longer a director of MF Global Holdings Ltd. |

| (iii) | Mr. Kerr became a director of Canwest Global Communications Corp. in 2007. In October 2009, it filed for protection under the Companies’ Creditors Arrangement Act (“CCAA”) and filed for recognition and ancillary relief under Chapter 15 of the Bankruptcy Code in the United States. Mr. Kerr is no longer a director of Canwest Global Communications Corp. |

| (iv) | Professor Kesner was a director of Harriet & Henderson Yarns, Inc. until May 2003. In July 2003, it filed a voluntary petition under Chapter 11 of the Bankruptcy Code in the United States. |

| (v) | Mr. Osborne was a director of Nortel Networks Corporation and Nortel Networks Limited (collectively known as Nortel) when the OSC issued a management cease trade order on April 10, 2006, prohibiting all directors, officers and certain other current and former employees of Nortel from trading its securities until two business days after receipt by the OSC of all filings required under Ontario securities laws. The OSC issued the order because Nortel needed to restate certain financial results and was delayed in filing some of its 2005 financial results. The order was revoked as of June 8, 2006. Mr. Osborne is no longer a director of Nortel. |

Code of Business Conduct

Our approach to business conduct is based on ethical behaviour, adhering to high business standards, integrity and respect. The Board of Directors sets the “tone from the top” and satisfies itself that senior management sustains a culture of integrity throughout the organization. The Board has adopted the Sun Life Financial Code of Business Conduct that applies to all directors, officers and employees. The Sun Life Financial Code of Business Conduct may be accessed on the Sun Life Financial website at www.sunlife.com. It has been filed with securities regulators in Canada and with the SEC and may be accessed atwww.sedar.com andwww.sec.gov, respectively.

The Governance and Conduct Review Committee reviews the effectiveness of, and compliance with, the Code of Business Conduct, reports on its review to the Board of Directors on an annual basis, and makes recommendations on amendments as required. No waivers of the Code for directors or executive officers have been granted.

Shareholdings of Directors and Executive Officers

As at December 31, 2011, SLF Inc.’s directors and executive officers, as a group, owned, directly or indirectly, or had voting control or direction over 173,424 Common Shares of SLF Inc., or less than 1% of the total Common Shares outstanding.

Principal Accountant Fees and Services

The following table shows the fees related to services provided by the Company’s external auditors for the past two years.

| Year Ended December 31 ($ millions) | ||||

| 2011 | 2010* | |||

Audit Fees | 17.5 | 22.1 | ||

Audit-Related Fees | 1.6 | 2.3 | ||

Tax Fees | 0.1 | 0.4 | ||

All other Fees | 0.3 | 0.3 | ||

| * | The 2010 amounts have been adjusted to include $0.6 million in fees related to fiscal 2010 audits. These fees could not be estimated at the time of reporting in 2010. |

Sun Life Financial Inc. | sunlife.com | 18 |

ANNUAL INFORMATION FORM 2011

Audit fees relate to professional services rendered by the auditors for the audit of our annual consolidated financial statements, the statements for our segregated funds as well as services related to statutory and regulatory filings. Fees in 2010 included services provided in support of our transition to IFRS.

Audit-related fees include assurance and services related to performing the audit or reviewing the annual consolidated financial statements that were not part of audit services. These include internal control reviews, consulting on financial accounting and reporting standards not arising as part of the audit, CFA Institute verifications and employee benefit plan audits.

Tax fees relate to tax compliance, tax advice and tax planning.

All other fees relate to products and services other than audit, audit-related and tax as described above.

Policy for Approval of Auditor Services

SLF Inc. has established a policy requiring pre-approval of services provided by its external auditors, a copy of which is attached as Appendix B. All fees paid to SLF Inc.’s external auditors since the policy was established have been approved by the Audit Committee in accordance with the policy in effect at the relevant time.

None of the services provided by the Company’s external auditors described above were approved pursuant to the waiver of pre-approval provisions under SEC rules (paragraph (c)(7)(i)(C) of Rule 2-01 of Regulation S-X).

Interest of Experts

Deloitte & Touche LLP, Independent Registered Chartered Accountants and Licensed Public Accountants, are the external auditors of SLF Inc., and are independent within the meaning of the Rules of Professional Conduct of the Institute of Chartered Accountants of Ontario.

Lesley Thomson, the Appointed Actuary of SLF Inc., has provided an opinion on the value of policy liabilities for SLF Inc.’s consolidated balance sheet as at December 31, 2011 and 2010 and the change in the consolidated statements of operations for the years then ended. Ms. Thomson owned beneficially, directly or indirectly, less than 1% of all outstanding securities or other property of SLF Inc. or its affiliates when she prepared that opinion, or after that opinion was prepared, and she does not expect to receive any such securities or other property in excess of that amount in the future.

Sun Life Financial Inc. | sunlife.com | 19 |

ANNUAL INFORMATION FORM 2011

Regulatory Matters

Sun Life Financial is subject to regulation and supervision by government authorities in the jurisdictions in which it does business.

Canada

General

SLF Inc. is incorporated under and governed by the Insurance Act. OSFI administers the Insurance Act and supervises the activities of Sun Life Financial. SLF Inc. has all the powers and restrictions applicable to life insurance companies governed by the Insurance Act, which permits insurance companies to offer, directly or through subsidiaries or networking arrangements, a broad range of financial services, including:

| • | insurance and reinsurance, |

| • | investment counselling and portfolio management, |

| • | mutual funds, |

| • | trust services, |

| • | banking services, |

| • | real property brokerage and appraisal, and |

| • | merchant banking services. |

The Insurance Act requires the filing of annual and other reports on the financial condition of insurance companies, provides for periodic examinations of insurance companies’ affairs, imposes restrictions on transactions with related parties, and sets out requirements governing certain aspects of insurance companies’ businesses.

OSFI supervises SLF Inc. on a consolidated basis to ensure that it has an overview of activities of SLF Inc. and its consolidated subsidiaries. This consolidated supervision includes the ability to review insurance and non-insurance operations of SLF Inc. and subsidiaries and supervisory power to bring about corrective action. OSFI has extensive powers to intervene in the affairs of regulated insurance companies, including the power to request information or documents, to conduct investigations, to require that appropriate actions are taken to address issues identified by OSFI and to levy fines. OSFI may intervene and assume control of an Insurance Holding Company or a Canadian life insurance company if it deems the amount of available capital insufficient.

Investment Powers

Under the Insurance Act, a life insurance company must maintain a prudent portfolio of investments, subject to certain overall limitations on the amount it may invest in certain classes of investments, such as commercial loans, real estate and stocks. Additional restrictions (and, in some cases, the need for regulatory approvals) limit the type of investments which Sun Life Financial can make in excess of 10% of the voting rights or 25% of the equity of any entity.

Capital and Surplus Requirements

OSFI has established Guideline A-2 – Capital Regime for Regulated Insurance Holding Companies and Non-Operating Life Companies, which sets out the framework within which OSFI will assess whether regulated non-operating life companies and insurance holding companies (collectively, “Insurance Holding Companies”) are maintaining adequate capital. Under this guideline, Insurance Holding Companies, such as SLF Inc., are expected to manage their capital in a manner commensurate with their risk profile and control environments. The Company’s regulated subsidiaries are expected to comply with the capital adequacy requirements imposed in the jurisdictions in which they operate. The Company’s principal operating life insurance subsidiary in Canada, Sun Life Assurance, is subject to the MCCSR capital rules and the principal operating life insurance subsidiary in the United States, Sun Life (U.S.), is subject to the risk-based capital rules issued by the NAIC.

Sun Life Assurance is subject to the MCCSR rules on a consolidated basis. The MCCSR calculation involves using qualifying models or applying quantitative factors to specific assets and liabilities, as well as to certain off-balance sheet items, based on the following risk components: (i) asset default risk, (ii) mortality, morbidity and lapse risk, (iii) changes in interest rate environment risk, (iv) segregated fund guarantee risk, (v) off-balance sheet activity exposure and (vi) foreign exchange risk. The total capital required is the sum of the capital required calculated for each of these six risk components. OSFI uses this total, in conjunction with the amount calculated as available capital, together with other

Sun Life Financial Inc. | sunlife.com | 20 |

ANNUAL INFORMATION FORM 2011

considerations, in assessing the capital adequacy of Canadian life insurance companies. The minimum regulatory MCCSR ratio is 120%, with a supervisory target ratio of 150%. OSFI may require a higher amount of capital be available, taking into account factors such as operating experience and diversification of asset or insurance portfolios. OSFI expects life insurance companies to establish a target capital level plus a buffer to take into account such factors as market volatility and operational risk. Capital requirements may be adjusted by OSFI as experience develops, the risk profile of an insurance company, or the industry more broadly, changes or to reflect other risks.

The principal elements used to calculate available capital for Insurance Holding Companies and for Canadian life insurance companies include common shares, contributed surplus, retained earnings, the participating account, accumulated currency translation account, unrealized gains and losses on available-for-sales equities, qualifying preferred shares, innovative capital instruments and subordinated debt, and a portion of actuarial liabilities related to future policyholder terminal dividends. Funds raised by Insurance Holding Companies or Canadian life insurance companies through borrowing or issuing securities are treated as different categories of available capital, depending on the characteristics of the instrument issued.

Insurance Holding Companies and Canadian life insurance companies must then reduce the amount of their available capital by the aggregate of their goodwill and controlling interests in non-life financial corporations, non-controlling substantial investments in corporations, a portion of cash value deficiencies and credit taken on reserves on reinsurance ceded to unregistered reinsurers and the net decrease in policy liabilities arising from assumed mortality improvements. OSFI may require that a higher amount of capital be available, taking into account factors such as operating experience and diversification of asset or insurance portfolios.

Sun Life Financial adopted International Financial Reporting Standards as of January 1, 2011. Under OSFI’s IFRS transition guidance, companies can elect to phase in the impact of the conversion to IFRS on adjusted Tier 1 available capital over eight quarters ending in the fourth quarter of 2012. Sun Life Assurance has made this election and will be phasing in a reduction of approximately $300 million to its adjusted Tier 1 capital over this period, largely related to the recognition of deferred actuarial losses on defined benefit pension plans.