UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number: 811-09721

PIMCO Managed Accounts Trust

(Exact name of registrant as specified in charter)

1633 Broadway, New York, NY 10019

(Address of principal executive offices)

Bijal Y. Parikh

Treasurer (Principal Financial & Accounting Officer)

650 Newport Center Drive

Newport Beach, CA 92660

(Name and address of agent for service)

Copies to:

David C. Sullivan

Ropes & Gray LLP

Prudential Tower

800 Boylston Street

Boston, MA 02199

Registrant’s telephone number, including area code: (800) 927-4648

Date of fiscal year end: December 31

Date of reporting period: June 30, 2024

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 100 F Street, NE, Washington, DC 20549-1090. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

| Item 1. | Reports to Stockholders. |

| | (a) | The following is a copy of the reports transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940, as amended (the “1940 Act”) (17 CFR 270.30e-1). |

| | • | | Fixed Income SHares: Series C |

| | • | | Fixed Income SHares: Series LD |

| | • | | Fixed Income SHares: Series M |

| | • | | Fixed Income SHares: Series R |

| | • | | Fixed Income SHares: Series TE |

| | (b) | Not applicable to the Registrant. |

Fixed Income SHares: Series C

Semi-Annual Shareholder Report | June 30, 2024

This semi-annual shareholder report contains important information about the Fixed Income SHares: Series C (the "Portfolio") for the period of January 1, 2024 to June 30, 2024 (the "reporting period"). You can find additional information about the Portfolio at www.pimco.com/FISH. You can also request this information by contacting us at 888.87.PIMCO (888.877.4626).

What were the Portfolio costs for the last six months?

(based on a hypothetical $10,000 investment)

| Portfolio Name | Cost of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

|---|

| Fixed Income SHares: Series C | $7 | 0.14% |

How did the Portfolio perform during the reporting period and what affected its performance?

The following affected performance (on a gross basis) during the reporting period:

• Long exposure to securitized credit contributed to relative performance, as spreads tightened.

• Curve positioning in the U.S., primarily underweight exposure to the front-end of the yield curve, contributed to relative performance, as

yields rose.

• Security selection of subordinated financials within investment grade corporate credit contributed to relative performance, as spreads

tightened.

• Long exposure to duration in Canada detracted from relative performance, as yields rose.

• Underweight exposure to non-financial investment grade corporate credit detracted from relative performance, as spreads tightened.

• Underweight exposure to the U.S. dollar detracted from relative performance, as the currency appreciated against a basket of major

developed market currencies.

In addition to the Portfolio's performance, the tables in this section include performance of: (i) a broad-based securities market index (i.e., a regulatory index) and (ii) one or more supplemental index(es). Effective July 24, 2024, the Bloomberg U.S. Aggregate Index replaced the Bloomberg U.S. Intermediate Credit Index as the Portfolio's regulatory index. The Portfolio's regulatory index is shown in connection with certain regulatory requirements to provide a broad measure of market performance.

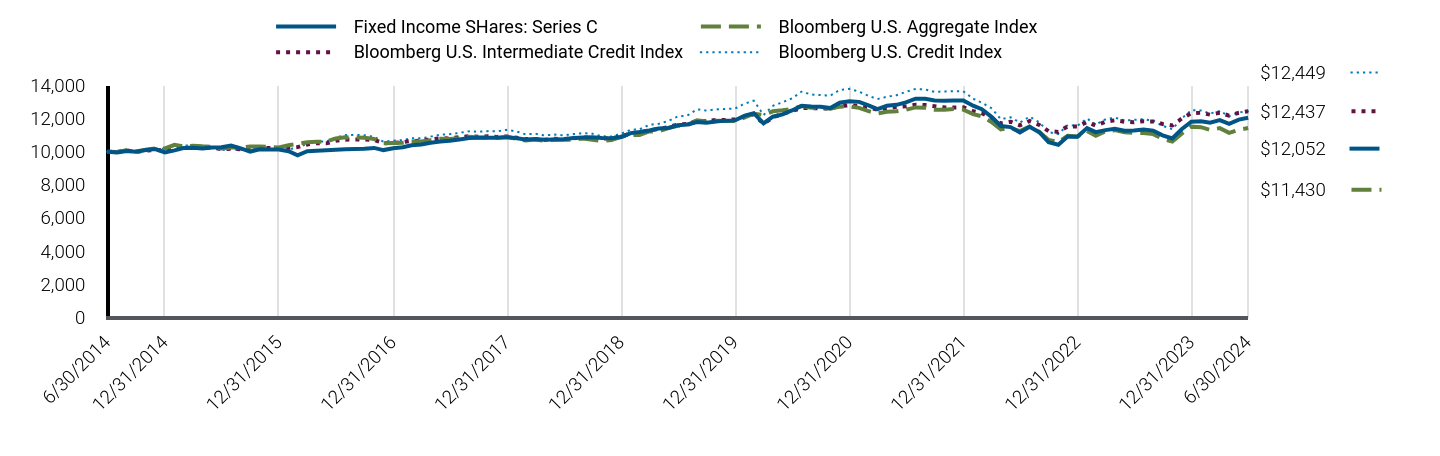

The table below illustrates cumulative returns for the 10-year period ended June 30, 2024 or the life of the Portfolio, if shorter. Cumulative returns are based on a hypothetical initial investment equal to the greater of either $10,000 or the investment minimum applicable to the share class.

Cumulative Returns Based on $10,000 Investment

| Fixed Income SHares: Series C | Bloomberg U.S. Aggregate Index | Bloomberg U.S. Intermediate Credit Index | Bloomberg U.S. Credit Index |

|---|

| 6/30/2014 | $10,000 | $10,000 | $10,000 | $10,000 |

| 7/31/2014 | $9,955 | $9,975 | $9,984 | $9,996 |

| 8/31/2014 | $10,043 | $10,085 | $10,068 | $10,140 |

| 9/30/2014 | $9,998 | $10,017 | $9,989 | $9,997 |

| 10/31/2014 | $10,098 | $10,115 | $10,060 | $10,104 |

| 11/30/2014 | $10,155 | $10,187 | $10,110 | $10,172 |

| 12/31/2014 | $9,952 | $10,196 | $10,069 | $10,173 |

| 1/31/2015 | $10,075 | $10,410 | $10,248 | $10,461 |

| 2/28/2015 | $10,219 | $10,312 | $10,204 | $10,357 |

| 3/31/2015 | $10,230 | $10,360 | $10,247 | $10,393 |

| 4/30/2015 | $10,190 | $10,323 | $10,253 | $10,332 |

| 5/31/2015 | $10,256 | $10,298 | $10,247 | $10,273 |

| 6/30/2015 | $10,271 | $10,186 | $10,151 | $10,093 |

| 7/31/2015 | $10,374 | $10,257 | $10,180 | $10,157 |

| 8/31/2015 | $10,195 | $10,242 | $10,149 | $10,096 |

| 9/30/2015 | $10,006 | $10,311 | $10,206 | $10,147 |

| 10/31/2015 | $10,142 | $10,313 | $10,231 | $10,195 |

| 11/30/2015 | $10,133 | $10,286 | $10,217 | $10,173 |

| 12/31/2015 | $10,125 | $10,252 | $10,160 | $10,095 |

| 1/31/2016 | $10,030 | $10,393 | $10,224 | $10,147 |

| 2/29/2016 | $9,780 | $10,467 | $10,273 | $10,232 |

| 3/31/2016 | $10,031 | $10,563 | $10,434 | $10,490 |

| 4/30/2016 | $10,061 | $10,604 | $10,510 | $10,618 |

| 5/31/2016 | $10,082 | $10,607 | $10,502 | $10,614 |

| 6/30/2016 | $10,112 | $10,797 | $10,655 | $10,856 |

| 7/31/2016 | $10,138 | $10,865 | $10,726 | $10,998 |

| 8/31/2016 | $10,154 | $10,853 | $10,729 | $11,020 |

| 9/30/2016 | $10,171 | $10,847 | $10,737 | $10,989 |

| 10/31/2016 | $10,227 | $10,764 | $10,704 | $10,895 |

| 11/30/2016 | $10,095 | $10,509 | $10,510 | $10,598 |

| 12/31/2016 | $10,210 | $10,524 | $10,533 | $10,663 |

| 1/31/2017 | $10,267 | $10,544 | $10,573 | $10,699 |

| 2/28/2017 | $10,384 | $10,615 | $10,649 | $10,817 |

| 3/31/2017 | $10,432 | $10,610 | $10,653 | $10,801 |

| 4/30/2017 | $10,532 | $10,692 | $10,736 | $10,909 |

| 5/31/2017 | $10,608 | $10,774 | $10,806 | $11,026 |

| 6/30/2017 | $10,653 | $10,763 | $10,800 | $11,055 |

| 7/31/2017 | $10,735 | $10,809 | $10,874 | $11,136 |

| 8/31/2017 | $10,830 | $10,906 | $10,935 | $11,229 |

| 9/30/2017 | $10,842 | $10,854 | $10,908 | $11,204 |

| 10/31/2017 | $10,843 | $10,861 | $10,926 | $11,242 |

| 11/30/2017 | $10,833 | $10,847 | $10,892 | $11,232 |

| 12/31/2017 | $10,867 | $10,897 | $10,919 | $11,322 |

| 1/31/2018 | $10,805 | $10,771 | $10,835 | $11,216 |

| 2/28/2018 | $10,730 | $10,669 | $10,758 | $11,047 |

| 3/31/2018 | $10,764 | $10,737 | $10,770 | $11,081 |

| 4/30/2018 | $10,721 | $10,658 | $10,722 | $10,980 |

| 5/31/2018 | $10,735 | $10,734 | $10,778 | $11,035 |

| 6/30/2018 | $10,748 | $10,720 | $10,761 | $10,983 |

| 7/31/2018 | $10,824 | $10,723 | $10,802 | $11,062 |

| 8/31/2018 | $10,862 | $10,792 | $10,865 | $11,119 |

| 9/30/2018 | $10,871 | $10,722 | $10,840 | $11,081 |

| 10/31/2018 | $10,819 | $10,638 | $10,794 | $10,926 |

| 11/30/2018 | $10,812 | $10,701 | $10,803 | $10,919 |

| 12/31/2018 | $10,890 | $10,898 | $10,921 | $11,083 |

| 1/31/2019 | $11,121 | $11,014 | $11,095 | $11,322 |

| 2/28/2019 | $11,187 | $11,007 | $11,133 | $11,347 |

| 3/31/2019 | $11,283 | $11,219 | $11,309 | $11,623 |

| 4/30/2019 | $11,403 | $11,221 | $11,358 | $11,680 |

| 5/31/2019 | $11,428 | $11,421 | $11,477 | $11,852 |

| 6/30/2019 | $11,590 | $11,564 | $11,647 | $12,119 |

| 7/31/2019 | $11,640 | $11,589 | $11,671 | $12,182 |

| 8/31/2019 | $11,793 | $11,890 | $11,872 | $12,563 |

| 9/30/2019 | $11,748 | $11,826 | $11,845 | $12,481 |

| 10/31/2019 | $11,828 | $11,862 | $11,913 | $12,552 |

| 11/30/2019 | $11,875 | $11,856 | $11,915 | $12,575 |

| 12/31/2019 | $11,890 | $11,848 | $11,961 | $12,612 |

| 1/31/2020 | $12,177 | $12,076 | $12,133 | $12,907 |

| 2/29/2020 | $12,322 | $12,293 | $12,256 | $13,082 |

| 3/31/2020 | $11,706 | $12,221 | $11,679 | $12,215 |

| 4/30/2020 | $12,112 | $12,438 | $12,081 | $12,774 |

| 5/31/2020 | $12,248 | $12,496 | $12,284 | $12,982 |

| 6/30/2020 | $12,490 | $12,575 | $12,459 | $13,219 |

| 7/31/2020 | $12,769 | $12,762 | $12,631 | $13,627 |

| 8/31/2020 | $12,731 | $12,659 | $12,631 | $13,454 |

| 9/30/2020 | $12,717 | $12,652 | $12,613 | $13,417 |

| 10/31/2020 | $12,633 | $12,596 | $12,614 | $13,387 |

| 11/30/2020 | $12,957 | $12,720 | $12,748 | $13,728 |

| 12/31/2020 | $13,051 | $12,737 | $12,808 | $13,791 |

| 1/31/2021 | $13,010 | $12,646 | $12,764 | $13,627 |

| 2/28/2021 | $12,807 | $12,463 | $12,661 | $13,390 |

| 3/31/2021 | $12,569 | $12,308 | $12,542 | $13,177 |

| 4/30/2021 | $12,771 | $12,405 | $12,629 | $13,317 |

| 5/31/2021 | $12,828 | $12,445 | $12,697 | $13,413 |

| 6/30/2021 | $12,982 | $12,533 | $12,739 | $13,615 |

| 7/31/2021 | $13,198 | $12,673 | $12,836 | $13,792 |

| 8/31/2021 | $13,195 | $12,649 | $12,815 | $13,759 |

| 9/30/2021 | $13,097 | $12,539 | $12,747 | $13,611 |

| 10/31/2021 | $13,071 | $12,536 | $12,678 | $13,641 |

| 11/30/2021 | $13,093 | $12,573 | $12,664 | $13,653 |

| 12/31/2021 | $13,095 | $12,541 | $12,677 | $13,642 |

| 1/31/2022 | $12,777 | $12,271 | $12,449 | $13,204 |

| 2/28/2022 | $12,568 | $12,134 | $12,322 | $12,955 |

| 3/31/2022 | $12,102 | $11,797 | $12,034 | $12,630 |

| 4/30/2022 | $11,549 | $11,349 | $11,707 | $11,968 |

| 5/31/2022 | $11,483 | $11,422 | $11,808 | $12,074 |

| 6/30/2022 | $11,158 | $11,243 | $11,597 | $11,758 |

| 7/31/2022 | $11,500 | $11,518 | $11,852 | $12,116 |

| 8/31/2022 | $11,175 | $11,192 | $11,614 | $11,773 |

| 9/30/2022 | $10,574 | $10,709 | $11,240 | $11,177 |

| 10/31/2022 | $10,418 | $10,570 | $11,194 | $11,061 |

| 11/30/2022 | $10,914 | $10,959 | $11,533 | $11,611 |

| 12/31/2022 | $10,904 | $10,909 | $11,523 | $11,561 |

| 1/31/2023 | $11,422 | $11,245 | $11,796 | $12,002 |

| 2/28/2023 | $11,180 | $10,954 | $11,571 | $11,640 |

| 3/31/2023 | $11,301 | $11,232 | $11,808 | $11,960 |

| 4/30/2023 | $11,377 | $11,300 | $11,896 | $12,054 |

| 5/31/2023 | $11,266 | $11,177 | $11,808 | $11,886 |

| 6/30/2023 | $11,278 | $11,137 | $11,778 | $11,922 |

| 7/31/2023 | $11,332 | $11,130 | $11,840 | $11,959 |

| 8/31/2023 | $11,273 | $11,059 | $11,824 | $11,873 |

| 9/30/2023 | $10,988 | $10,778 | $11,669 | $11,564 |

| 10/31/2023 | $10,794 | $10,607 | $11,588 | $11,358 |

| 11/30/2023 | $11,356 | $11,088 | $11,995 | $12,003 |

| 12/31/2023 | $11,813 | $11,512 | $12,322 | $12,506 |

| 1/31/2024 | $11,843 | $11,481 | $12,346 | $12,484 |

| 2/29/2024 | $11,752 | $11,318 | $12,236 | $12,304 |

| 3/31/2024 | $11,909 | $11,423 | $12,347 | $12,455 |

| 4/30/2024 | $11,676 | $11,134 | $12,181 | $12,145 |

| 5/31/2024 | $11,937 | $11,323 | $12,349 | $12,367 |

| 6/30/2024 | $12,052 | $11,430 | $12,437 | $12,449 |

The table below shows the average annual total returns of the Portfolio, a regulatory index, and one or more supplemental index(es) for certain periods ended June 30, 2024.

Average Annual Total Returns (%)

| Portfolio/Index Name | 1 Year | 5 Years | 10 Years |

|---|

| Fixed Income SHares: Series C | 6.86% | 0.78% | 1.88% |

| Bloomberg U.S. Aggregate Index | 2.63% | (0.23%) | 1.35% |

| Bloomberg U.S. Intermediate Credit Index | 5.60% | 1.32% | 2.20% |

| Bloomberg U.S. Credit Index | 4.42% | 0.54% | 2.21% |

All Portfolio returns are net of fees and expenses and include applicable fee waivers and/or expense limitations. Absent any applicable fee waivers and/or expense limitations, performance would have been lower and there can be no assurance that any such waivers or limitations will continue in the future.

Performance quoted represents past performance. Past performance is not a guarantee or a reliable indicator of future results.Current performance may be lower or higher than performance shown. Investment return and the principal value of an investment will fluctuate. Shares may be worth more or less than original cost when redeemed. Returns shown do not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or the redemption of Portfolio shares.Differences in the Portfolio’s performance versus an index and related attribution information with respect to particular categories of securities or individual positions may be attributable, in part, to differences in the pricing methodologies used by the Portfolio and the index.

Key Portfolio StatisticsFootnote Reference* (as of the end of the reporting period)

| Total Net Assets | $1,361,781 |

| # of Portfolio Holdings | 497 |

| Portfolio Turnover Rate | 251% |

Total Net Advisory Fees Paid During the Reporting PeriodFootnote Reference† | $0 |

| Footnote | Description |

Footnote† | No investment management fees or expenses are incurred by the Portfolio. The PIMCO Fixed Income SHares Portfolios are an integral part of “wrap-fee” programs sponsored by investment advisers and/or broker-dealers unaffiliated with the Portfolios and PIMCO. Participants in these programs pay a “wrap” fee to the sponsor of the program. |

Footnote* | Dollar amounts displayed in 000's |

What did the Portfolio invest in?

Allocation Breakdown (% of Net Assets)Footnote Reference*

| U.S. Government Agencies | 53.8% |

| Corporate Bonds & Notes | 45.1% |

| Asset-Backed Securities | 20.7% |

| U.S. Treasury Obligations | 17.4% |

| Non-Agency Mortgage-Backed Securities | 8.6% |

| Preferred Securities | 1.8% |

| Municipal Bonds & Notes | 1.7% |

| Affiliated Investments | 0.8% |

| Loan Participations and Assignments | 0.3% |

| Other Investments | 0.1% |

| Other Assets and Liabilities, Net | (50.3%) |

| Total | 100.0% |

| Footnote | Description |

Footnote* | % of Net Assets includes derivatives instruments, if any, valued at the value used for determining the Portfolio's net asset value. The notional exposure of such derivatives investments therefore may be greater than what is depicted. |

For additional information about the Portfolio, including the Portfolio's prospectus, financial information, holdings and proxy voting information, please visit www.pimco.com/FISH or contact 888.87.PIMCO (888.877.4626). For tax information about the Portfolio, please visit: https://www.pimco.com/tax.

Fixed Income SHares: Series C

Semi-Annual Shareholder Report | June 30, 2024

Fixed Income SHares: Series LD

Semi-Annual Shareholder Report | June 30, 2024

This semi-annual shareholder report contains important information about the Fixed Income SHares: Series LD (the "Portfolio") for the period of January 1, 2024 to June 30, 2024 (the "reporting period"). You can find additional information about the Portfolio at www.pimco.com/FISH. You can also request this information by contacting us at 888.87.PIMCO (888.877.4626).

What were the Portfolio costs for the last six months?

(based on a hypothetical $10,000 investment)

| Portfolio Name | Cost of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

|---|

| Fixed Income SHares: Series LD | $76 | 1.51% |

How did the Portfolio perform during the reporting period and what affected its performance?

The following affected performance (on a gross basis) during the reporting period:

• Underweight exposure to U.S. duration, specifically at the 7 year and 10 year part of the curve, contributed to relative performance, as

interest rates rose.

• Overweight exposure to commercial mortgage-backed securities ("CMBS") contributed to relative performance, as CMBS posted

positive returns.

• Overweight exposure to collateralized loan obligations contributed to relative performance, as spreads tightened.

• A long bias to the Japanese yen versus the U.S. dollar detracted from relative performance, as the Japanese yen depreciated.

• Long exposure to Australia duration, specifically at the 10 year part of the curve, detracted from relative performance, as interest rates

rose.

• Long exposure to United Kingdom duration, specifically at the 5 year part of the curve, detracted from relative performance, as interest

rates rose.

In addition to the Portfolio's performance, the tables in this section include performance of: (i) a broad-based securities market index (i.e., a regulatory index) and (ii) one or more supplemental index(es). Effective July 24, 2024, the Portfolio's regulatory index is the Bloomberg U.S. Aggregate Index. The Portfolio's regulatory index is shown in connection with certain regulatory requirements to provide a broad measure of market performance.

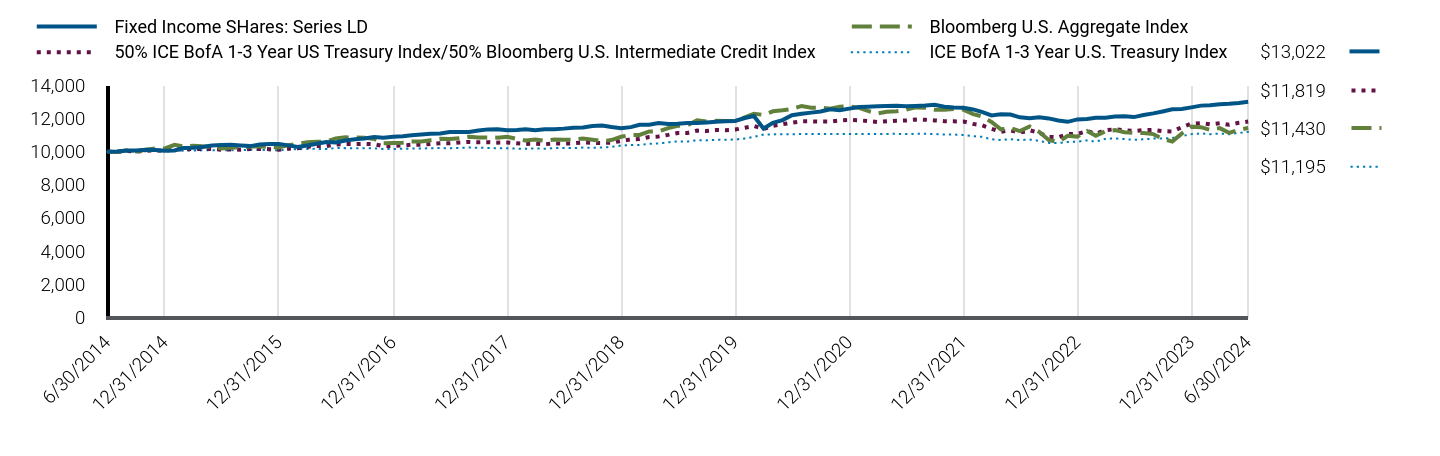

The table below illustrates cumulative returns for the 10-year period ended June 30, 2024 or the life of the Portfolio, if shorter. Cumulative returns are based on a hypothetical initial investment equal to the greater of either $10,000 or the investment minimum applicable to the share class.

Cumulative Returns Based on $10,000 Investment

| Fixed Income SHares: Series LD | Bloomberg U.S. Aggregate Index | 50% ICE BofA 1-3 Year US Treasury Index/50% Bloomberg U.S. Intermediate Credit Index | ICE BofA 1-3 Year U.S. Treasury Index |

|---|

| 6/30/2014 | $10,000 | $10,000 | $10,000 | $10,000 |

| 7/31/2014 | $10,016 | $9,975 | $9,988 | $9,992 |

| 8/31/2014 | $10,075 | $10,085 | $10,038 | $10,009 |

| 9/30/2014 | $10,076 | $10,017 | $9,996 | $10,003 |

| 10/31/2014 | $10,118 | $10,115 | $10,045 | $10,031 |

| 11/30/2014 | $10,095 | $10,187 | $10,078 | $10,045 |

| 12/31/2014 | $10,056 | $10,196 | $10,045 | $10,021 |

| 1/31/2015 | $10,076 | $10,410 | $10,159 | $10,071 |

| 2/28/2015 | $10,217 | $10,312 | $10,127 | $10,050 |

| 3/31/2015 | $10,233 | $10,360 | $10,160 | $10,073 |

| 4/30/2015 | $10,286 | $10,323 | $10,165 | $10,078 |

| 5/31/2015 | $10,365 | $10,298 | $10,166 | $10,085 |

| 6/30/2015 | $10,396 | $10,186 | $10,120 | $10,088 |

| 7/31/2015 | $10,423 | $10,257 | $10,137 | $10,093 |

| 8/31/2015 | $10,373 | $10,242 | $10,119 | $10,089 |

| 9/30/2015 | $10,335 | $10,311 | $10,163 | $10,119 |

| 10/31/2015 | $10,433 | $10,313 | $10,170 | $10,109 |

| 11/30/2015 | $10,469 | $10,286 | $10,151 | $10,084 |

| 12/31/2015 | $10,463 | $10,252 | $10,118 | $10,075 |

| 1/31/2016 | $10,380 | $10,393 | $10,181 | $10,136 |

| 2/29/2016 | $10,278 | $10,467 | $10,211 | $10,148 |

| 3/31/2016 | $10,377 | $10,563 | $10,300 | $10,166 |

| 4/30/2016 | $10,478 | $10,604 | $10,339 | $10,169 |

| 5/31/2016 | $10,579 | $10,607 | $10,330 | $10,158 |

| 6/30/2016 | $10,556 | $10,797 | $10,436 | $10,219 |

| 7/31/2016 | $10,675 | $10,865 | $10,467 | $10,213 |

| 8/31/2016 | $10,749 | $10,853 | $10,460 | $10,197 |

| 9/30/2016 | $10,799 | $10,847 | $10,471 | $10,208 |

| 10/31/2016 | $10,887 | $10,764 | $10,451 | $10,202 |

| 11/30/2016 | $10,841 | $10,509 | $10,336 | $10,161 |

| 12/31/2016 | $10,900 | $10,524 | $10,348 | $10,164 |

| 1/31/2017 | $10,934 | $10,544 | $10,374 | $10,177 |

| 2/28/2017 | $10,985 | $10,615 | $10,417 | $10,187 |

| 3/31/2017 | $11,040 | $10,610 | $10,421 | $10,191 |

| 4/30/2017 | $11,077 | $10,692 | $10,468 | $10,205 |

| 5/31/2017 | $11,094 | $10,774 | $10,509 | $10,217 |

| 6/30/2017 | $11,182 | $10,763 | $10,502 | $10,208 |

| 7/31/2017 | $11,195 | $10,809 | $10,549 | $10,230 |

| 8/31/2017 | $11,187 | $10,906 | $10,588 | $10,249 |

| 9/30/2017 | $11,277 | $10,854 | $10,566 | $10,233 |

| 10/31/2017 | $11,346 | $10,861 | $10,572 | $10,226 |

| 11/30/2017 | $11,360 | $10,847 | $10,545 | $10,206 |

| 12/31/2017 | $11,297 | $10,897 | $10,559 | $10,207 |

| 1/31/2018 | $11,309 | $10,771 | $10,503 | $10,178 |

| 2/28/2018 | $11,350 | $10,669 | $10,464 | $10,174 |

| 3/31/2018 | $11,290 | $10,737 | $10,480 | $10,194 |

| 4/30/2018 | $11,357 | $10,658 | $10,448 | $10,178 |

| 5/31/2018 | $11,358 | $10,734 | $10,494 | $10,215 |

| 6/30/2018 | $11,392 | $10,720 | $10,487 | $10,216 |

| 7/31/2018 | $11,446 | $10,723 | $10,506 | $10,216 |

| 8/31/2018 | $11,457 | $10,792 | $10,554 | $10,248 |

| 9/30/2018 | $11,546 | $10,722 | $10,535 | $10,236 |

| 10/31/2018 | $11,576 | $10,638 | $10,521 | $10,252 |

| 11/30/2018 | $11,489 | $10,701 | $10,544 | $10,287 |

| 12/31/2018 | $11,418 | $10,898 | $10,643 | $10,369 |

| 1/31/2019 | $11,482 | $11,014 | $10,742 | $10,396 |

| 2/28/2019 | $11,625 | $11,007 | $10,766 | $10,407 |

| 3/31/2019 | $11,621 | $11,219 | $10,884 | $10,471 |

| 4/30/2019 | $11,729 | $11,221 | $10,918 | $10,492 |

| 5/31/2019 | $11,667 | $11,421 | $11,014 | $10,566 |

| 6/30/2019 | $11,685 | $11,564 | $11,125 | $10,621 |

| 7/31/2019 | $11,735 | $11,589 | $11,129 | $10,609 |

| 8/31/2019 | $11,732 | $11,890 | $11,271 | $10,694 |

| 9/30/2019 | $11,767 | $11,826 | $11,251 | $10,682 |

| 10/31/2019 | $11,812 | $11,862 | $11,302 | $10,717 |

| 11/30/2019 | $11,835 | $11,856 | $11,301 | $10,714 |

| 12/31/2019 | $11,857 | $11,848 | $11,335 | $10,737 |

| 1/31/2020 | $12,032 | $12,076 | $11,447 | $10,795 |

| 2/29/2020 | $12,152 | $12,293 | $11,555 | $10,889 |

| 3/31/2020 | $11,399 | $12,221 | $11,362 | $11,038 |

| 4/30/2020 | $11,748 | $12,438 | $11,560 | $11,043 |

| 5/31/2020 | $11,906 | $12,496 | $11,661 | $11,050 |

| 6/30/2020 | $12,206 | $12,575 | $11,746 | $11,053 |

| 7/31/2020 | $12,291 | $12,762 | $11,833 | $11,064 |

| 8/31/2020 | $12,359 | $12,659 | $11,831 | $11,061 |

| 9/30/2020 | $12,429 | $12,652 | $11,824 | $11,064 |

| 10/31/2020 | $12,560 | $12,596 | $11,822 | $11,060 |

| 11/30/2020 | $12,506 | $12,720 | $11,888 | $11,065 |

| 12/31/2020 | $12,602 | $12,737 | $11,919 | $11,070 |

| 1/31/2021 | $12,702 | $12,646 | $11,899 | $11,072 |

| 2/28/2021 | $12,720 | $12,463 | $11,846 | $11,063 |

| 3/31/2021 | $12,739 | $12,308 | $11,792 | $11,065 |

| 4/30/2021 | $12,759 | $12,405 | $11,835 | $11,070 |

| 5/31/2021 | $12,773 | $12,445 | $11,871 | $11,078 |

| 6/30/2021 | $12,747 | $12,533 | $11,882 | $11,061 |

| 7/31/2021 | $12,761 | $12,673 | $11,937 | $11,079 |

| 8/31/2021 | $12,783 | $12,649 | $11,927 | $11,079 |

| 9/30/2021 | $12,835 | $12,539 | $11,890 | $11,068 |

| 10/31/2021 | $12,715 | $12,536 | $11,840 | $11,034 |

| 11/30/2021 | $12,675 | $12,573 | $11,831 | $11,036 |

| 12/31/2021 | $12,650 | $12,541 | $11,825 | $11,009 |

| 1/31/2022 | $12,552 | $12,271 | $11,679 | $10,936 |

| 2/28/2022 | $12,406 | $12,134 | $11,597 | $10,896 |

| 3/31/2022 | $12,189 | $11,797 | $11,383 | $10,751 |

| 4/30/2022 | $12,253 | $11,349 | $11,203 | $10,700 |

| 5/31/2022 | $12,242 | $11,422 | $11,284 | $10,759 |

| 6/30/2022 | $12,073 | $11,243 | $11,147 | $10,696 |

| 7/31/2022 | $12,018 | $11,518 | $11,293 | $10,732 |

| 8/31/2022 | $12,072 | $11,192 | $11,136 | $10,655 |

| 9/30/2022 | $12,010 | $10,709 | $10,894 | $10,530 |

| 10/31/2022 | $11,881 | $10,570 | $10,866 | $10,519 |

| 11/30/2022 | $11,802 | $10,959 | $11,064 | $10,585 |

| 12/31/2022 | $11,950 | $10,909 | $11,071 | $10,607 |

| 1/31/2023 | $11,978 | $11,245 | $11,240 | $10,680 |

| 2/28/2023 | $12,047 | $10,954 | $11,092 | $10,603 |

| 3/31/2023 | $12,050 | $11,232 | $11,295 | $10,772 |

| 4/30/2023 | $12,118 | $11,300 | $11,351 | $10,800 |

| 5/31/2023 | $12,135 | $11,177 | $11,290 | $10,762 |

| 6/30/2023 | $12,088 | $11,137 | $11,248 | $10,710 |

| 7/31/2023 | $12,211 | $11,130 | $11,298 | $10,748 |

| 8/31/2023 | $12,312 | $11,059 | $11,312 | $10,790 |

| 9/30/2023 | $12,430 | $10,778 | $11,237 | $10,789 |

| 10/31/2023 | $12,560 | $10,607 | $11,218 | $10,826 |

| 11/30/2023 | $12,581 | $11,088 | $11,472 | $10,936 |

| 12/31/2023 | $12,676 | $11,512 | $11,692 | $11,058 |

| 1/31/2024 | $12,782 | $11,481 | $11,726 | $11,101 |

| 2/29/2024 | $12,800 | $11,318 | $11,650 | $11,055 |

| 3/31/2024 | $12,866 | $11,423 | $11,721 | $11,091 |

| 4/30/2024 | $12,891 | $11,134 | $11,624 | $11,055 |

| 5/31/2024 | $12,944 | $11,323 | $11,744 | $11,131 |

| 6/30/2024 | $13,022 | $11,430 | $11,819 | $11,195 |

The table below shows the average annual total returns of the Portfolio, a regulatory index, and one or more supplemental index(es) for certain periods ended June 30, 2024.

Average Annual Total Returns (%)

| Portfolio/Index Name | 1 Year | 5 Years | 10 Years |

|---|

| Fixed Income SHares: Series LD | 7.72% | 2.19% | 2.68% |

| Bloomberg U.S. Aggregate Index | 2.63% | (0.23%) | 1.35% |

| 50% ICE BofA 1-3 Year US Treasury Index/50% Bloomberg U.S. Intermediate Credit Index | 5.08% | 1.22% | 1.69% |

| ICE BofA 1-3 Year U.S. Treasury Index | 4.53% | 1.06% | 1.14% |

All Portfolio returns are net of fees and expenses and include applicable fee waivers and/or expense limitations. Absent any applicable fee waivers and/or expense limitations, performance would have been lower and there can be no assurance that any such waivers or limitations will continue in the future.

Performance quoted represents past performance. Past performance is not a guarantee or a reliable indicator of future results.Current performance may be lower or higher than performance shown. Investment return and the principal value of an investment will fluctuate. Shares may be worth more or less than original cost when redeemed. Returns shown do not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or the redemption of Portfolio shares.Differences in the Portfolio’s performance versus an index and related attribution information with respect to particular categories of securities or individual positions may be attributable, in part, to differences in the pricing methodologies used by the Portfolio and the index.

Key Portfolio StatisticsFootnote Reference* (as of the end of the reporting period)

| Total Net Assets | $51,294 |

| # of Portfolio Holdings | 227 |

| Portfolio Turnover Rate | 177% |

Total Net Advisory Fees Paid During the Reporting PeriodFootnote Reference† | $0 |

| Footnote | Description |

Footnote† | No investment management fees or expenses are incurred by the Portfolio. The PIMCO Fixed Income SHares Portfolios are an integral part of “wrap-fee” programs sponsored by investment advisers and/or broker-dealers unaffiliated with the Portfolios and PIMCO. Participants in these programs pay a “wrap” fee to the sponsor of the program. |

Footnote* | Dollar amounts displayed in 000's |

What did the Portfolio invest in?

Allocation Breakdown (% of Net Assets)Footnote Reference*

| Corporate Bonds & Notes | 47.1% |

| Asset-Backed Securities | 37.3% |

| Non-Agency Mortgage-Backed Securities | 28.9% |

| U.S. Treasury Obligations | 6.9% |

| Sovereign Issues | 2.8% |

| U.S. Government Agencies | 2.2% |

| Affiliated Investments | 1.6% |

| Short-Term Instruments | 0.5% |

| Other Investments | 0.8% |

| Other Assets and Liabilities, Net | (28.1%) |

| Total | 100.0% |

| Footnote | Description |

Footnote* | % of Net Assets includes derivatives instruments, if any, valued at the value used for determining the Portfolio's net asset value. The notional exposure of such derivatives investments therefore may be greater than what is depicted. |

For additional information about the Portfolio, including the Portfolio's prospectus, financial information, holdings and proxy voting information, please visit www.pimco.com/FISH or contact 888.87.PIMCO (888.877.4626). For tax information about the Portfolio, please visit: https://www.pimco.com/tax.

Fixed Income SHares: Series LD

Semi-Annual Shareholder Report | June 30, 2024

Fixed Income SHares: Series M

Semi-Annual Shareholder Report | June 30, 2024

This semi-annual shareholder report contains important information about the Fixed Income SHares: Series M (the "Portfolio") for the period of January 1, 2024 to June 30, 2024 (the "reporting period"). You can find additional information about the Portfolio at www.pimco.com/FISH. You can also request this information by contacting us at 888.87.PIMCO (888.877.4626).

What were the Portfolio costs for the last six months?

(based on a hypothetical $10,000 investment)

| Portfolio Name | Cost of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

|---|

| Fixed Income SHares: Series M | $4 | 0.08% |

How did the Portfolio perform during the reporting period and what affected its performance?

The following affected performance (on a gross basis) during the reporting period:

• Tactical curve positioning within U.S. interest rate strategies, particularly underweight exposure to the intermediate section of the

curve in February and the first half of April 2024, as yields rose.

• Long exposure to securitized credit contributed to relative performance, as spreads tightened.

• Long exposure to investment grade corporate credit contributed to relative performance, as spreads tightened.

• Long exposure to duration in the dollar bloc, primarily Australia, detracted from relative performance, as yields rose.

• Selection across the coupon stack within agency mortgage-backed securities detracted from relative performance, as higher coupons

outperformed lower coupons.

• There were no other material detractors for this Portfolio.

In addition to the Portfolio's performance, the tables in this section include performance of: (i) a broad-based securities market index (i.e., a regulatory index) and (ii) one or more supplemental index(es). Effective July 24, 2024, the Bloomberg U.S. Aggregate Index replaced the Bloomberg U.S. MBS Fixed Rate Index as the Portfolio's regulatory index. The Portfolio's regulatory index is shown in connection with certain regulatory requirements to provide a broad measure of market performance.

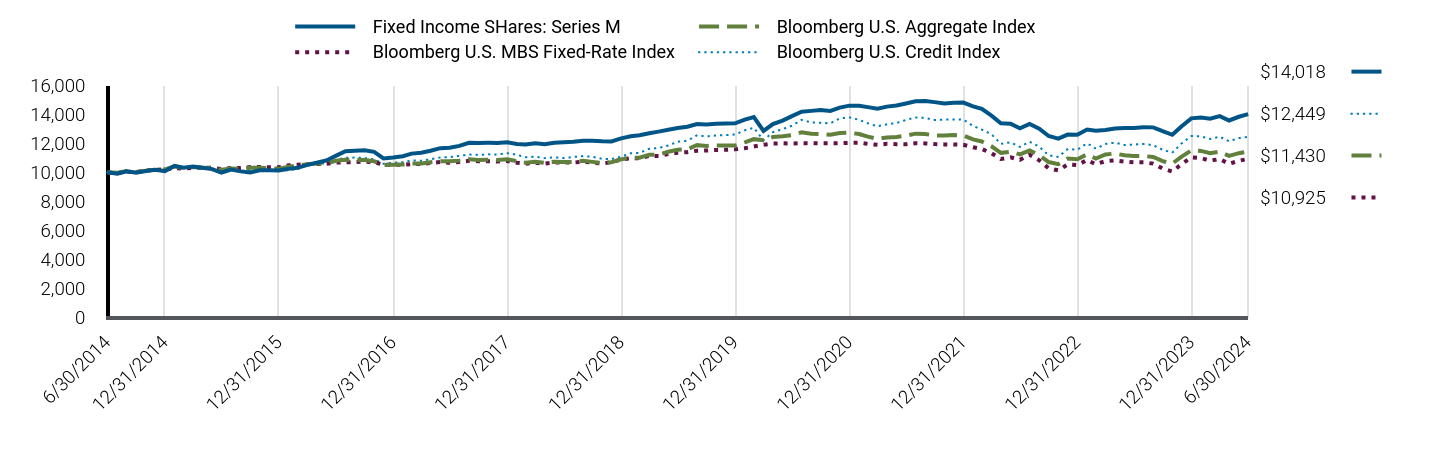

The table below illustrates cumulative returns for the 10-year period ended June 30, 2024 or the life of the Portfolio, if shorter. Cumulative returns are based on a hypothetical initial investment equal to the greater of either $10,000 or the investment minimum applicable to the share class.

Cumulative Returns Based on $10,000 Investment

| Fixed Income SHares: Series M | Bloomberg U.S. Aggregate Index | Bloomberg U.S. MBS Fixed-Rate Index | Bloomberg U.S. Credit Index |

|---|

| 6/30/2014 | $10,000 | $10,000 | $10,000 | $10,000 |

| 7/31/2014 | $9,912 | $9,975 | $9,940 | $9,996 |

| 8/31/2014 | $10,078 | $10,085 | $10,034 | $10,140 |

| 9/30/2014 | $9,975 | $10,017 | $10,018 | $9,997 |

| 10/31/2014 | $10,089 | $10,115 | $10,116 | $10,104 |

| 11/30/2014 | $10,171 | $10,187 | $10,183 | $10,172 |

| 12/31/2014 | $10,077 | $10,196 | $10,199 | $10,173 |

| 1/31/2015 | $10,454 | $10,410 | $10,285 | $10,461 |

| 2/28/2015 | $10,313 | $10,312 | $10,269 | $10,357 |

| 3/31/2015 | $10,406 | $10,360 | $10,307 | $10,393 |

| 4/30/2015 | $10,314 | $10,323 | $10,311 | $10,332 |

| 5/31/2015 | $10,222 | $10,298 | $10,309 | $10,273 |

| 6/30/2015 | $9,978 | $10,186 | $10,229 | $10,093 |

| 7/31/2015 | $10,189 | $10,257 | $10,294 | $10,157 |

| 8/31/2015 | $10,067 | $10,242 | $10,303 | $10,096 |

| 9/30/2015 | $9,996 | $10,311 | $10,363 | $10,147 |

| 10/31/2015 | $10,140 | $10,313 | $10,371 | $10,195 |

| 11/30/2015 | $10,152 | $10,286 | $10,356 | $10,173 |

| 12/31/2015 | $10,133 | $10,252 | $10,353 | $10,095 |

| 1/31/2016 | $10,239 | $10,393 | $10,488 | $10,147 |

| 2/29/2016 | $10,310 | $10,467 | $10,527 | $10,232 |

| 3/31/2016 | $10,519 | $10,563 | $10,558 | $10,490 |

| 4/30/2016 | $10,666 | $10,604 | $10,575 | $10,618 |

| 5/31/2016 | $10,822 | $10,607 | $10,589 | $10,614 |

| 6/30/2016 | $11,136 | $10,797 | $10,675 | $10,856 |

| 7/31/2016 | $11,464 | $10,865 | $10,697 | $10,998 |

| 8/31/2016 | $11,495 | $10,853 | $10,710 | $11,020 |

| 9/30/2016 | $11,526 | $10,847 | $10,739 | $10,989 |

| 10/31/2016 | $11,415 | $10,764 | $10,711 | $10,895 |

| 11/30/2016 | $10,957 | $10,509 | $10,527 | $10,598 |

| 12/31/2016 | $11,022 | $10,524 | $10,526 | $10,663 |

| 1/31/2017 | $11,113 | $10,544 | $10,523 | $10,699 |

| 2/28/2017 | $11,292 | $10,615 | $10,573 | $10,817 |

| 3/31/2017 | $11,351 | $10,610 | $10,576 | $10,801 |

| 4/30/2017 | $11,494 | $10,692 | $10,645 | $10,909 |

| 5/31/2017 | $11,672 | $10,774 | $10,712 | $11,026 |

| 6/30/2017 | $11,695 | $10,763 | $10,669 | $11,055 |

| 7/31/2017 | $11,828 | $10,809 | $10,717 | $11,136 |

| 8/31/2017 | $12,043 | $10,906 | $10,795 | $11,229 |

| 9/30/2017 | $12,034 | $10,854 | $10,771 | $11,204 |

| 10/31/2017 | $12,036 | $10,861 | $10,768 | $11,242 |

| 11/30/2017 | $12,027 | $10,847 | $10,752 | $11,232 |

| 12/31/2017 | $12,080 | $10,897 | $10,787 | $11,322 |

| 1/31/2018 | $11,964 | $10,771 | $10,661 | $11,216 |

| 2/28/2018 | $11,916 | $10,669 | $10,591 | $11,047 |

| 3/31/2018 | $12,015 | $10,737 | $10,658 | $11,081 |

| 4/30/2018 | $11,944 | $10,658 | $10,605 | $10,980 |

| 5/31/2018 | $12,041 | $10,734 | $10,679 | $11,035 |

| 6/30/2018 | $12,070 | $10,720 | $10,684 | $10,983 |

| 7/31/2018 | $12,108 | $10,723 | $10,673 | $11,062 |

| 8/31/2018 | $12,187 | $10,792 | $10,738 | $11,119 |

| 9/30/2018 | $12,186 | $10,722 | $10,672 | $11,081 |

| 10/31/2018 | $12,143 | $10,638 | $10,604 | $10,926 |

| 11/30/2018 | $12,138 | $10,701 | $10,700 | $10,919 |

| 12/31/2018 | $12,349 | $10,898 | $10,894 | $11,083 |

| 1/31/2019 | $12,497 | $11,014 | $10,980 | $11,322 |

| 2/28/2019 | $12,559 | $11,007 | $10,970 | $11,347 |

| 3/31/2019 | $12,704 | $11,219 | $11,130 | $11,623 |

| 4/30/2019 | $12,814 | $11,221 | $11,123 | $11,680 |

| 5/31/2019 | $12,942 | $11,421 | $11,267 | $11,852 |

| 6/30/2019 | $13,065 | $11,564 | $11,348 | $12,119 |

| 7/31/2019 | $13,148 | $11,589 | $11,394 | $12,182 |

| 8/31/2019 | $13,331 | $11,890 | $11,496 | $12,563 |

| 9/30/2019 | $13,308 | $11,826 | $11,504 | $12,481 |

| 10/31/2019 | $13,363 | $11,862 | $11,545 | $12,552 |

| 11/30/2019 | $13,381 | $11,856 | $11,554 | $12,575 |

| 12/31/2019 | $13,387 | $11,848 | $11,586 | $12,612 |

| 1/31/2020 | $13,646 | $12,076 | $11,667 | $12,907 |

| 2/29/2020 | $13,822 | $12,293 | $11,788 | $13,082 |

| 3/31/2020 | $12,865 | $12,221 | $11,912 | $12,215 |

| 4/30/2020 | $13,335 | $12,438 | $11,988 | $12,774 |

| 5/31/2020 | $13,577 | $12,496 | $12,003 | $12,982 |

| 6/30/2020 | $13,886 | $12,575 | $11,992 | $13,219 |

| 7/31/2020 | $14,184 | $12,762 | $12,013 | $13,627 |

| 8/31/2020 | $14,245 | $12,659 | $12,018 | $13,454 |

| 9/30/2020 | $14,308 | $12,652 | $12,005 | $13,417 |

| 10/31/2020 | $14,241 | $12,596 | $12,000 | $13,387 |

| 11/30/2020 | $14,471 | $12,720 | $12,009 | $13,728 |

| 12/31/2020 | $14,607 | $12,737 | $12,035 | $13,791 |

| 1/31/2021 | $14,596 | $12,646 | $12,044 | $13,627 |

| 2/28/2021 | $14,506 | $12,463 | $11,963 | $13,390 |

| 3/31/2021 | $14,391 | $12,308 | $11,902 | $13,177 |

| 4/30/2021 | $14,540 | $12,405 | $11,968 | $13,317 |

| 5/31/2021 | $14,618 | $12,445 | $11,947 | $13,413 |

| 6/30/2021 | $14,756 | $12,533 | $11,942 | $13,615 |

| 7/31/2021 | $14,910 | $12,673 | $12,016 | $13,792 |

| 8/31/2021 | $14,921 | $12,649 | $11,997 | $13,759 |

| 9/30/2021 | $14,850 | $12,539 | $11,954 | $13,611 |

| 10/31/2021 | $14,751 | $12,536 | $11,931 | $13,641 |

| 11/30/2021 | $14,807 | $12,573 | $11,920 | $13,653 |

| 12/31/2021 | $14,819 | $12,541 | $11,909 | $13,642 |

| 1/31/2022 | $14,556 | $12,271 | $11,732 | $13,204 |

| 2/28/2022 | $14,379 | $12,134 | $11,619 | $12,955 |

| 3/31/2022 | $13,914 | $11,797 | $11,317 | $12,630 |

| 4/30/2022 | $13,388 | $11,349 | $10,920 | $11,968 |

| 5/31/2022 | $13,353 | $11,422 | $11,040 | $12,074 |

| 6/30/2022 | $13,042 | $11,243 | $10,864 | $11,758 |

| 7/31/2022 | $13,346 | $11,518 | $11,213 | $12,116 |

| 8/31/2022 | $13,022 | $11,192 | $10,829 | $11,773 |

| 9/30/2022 | $12,508 | $10,709 | $10,282 | $11,177 |

| 10/31/2022 | $12,328 | $10,570 | $10,136 | $11,061 |

| 11/30/2022 | $12,608 | $10,959 | $10,549 | $11,611 |

| 12/31/2022 | $12,597 | $10,909 | $10,502 | $11,561 |

| 1/31/2023 | $12,960 | $11,245 | $10,848 | $12,002 |

| 2/28/2023 | $12,876 | $10,954 | $10,562 | $11,640 |

| 3/31/2023 | $12,924 | $11,232 | $10,768 | $11,960 |

| 4/30/2023 | $13,025 | $11,300 | $10,824 | $12,054 |

| 5/31/2023 | $13,055 | $11,177 | $10,744 | $11,886 |

| 6/30/2023 | $13,058 | $11,137 | $10,698 | $11,922 |

| 7/31/2023 | $13,117 | $11,130 | $10,690 | $11,959 |

| 8/31/2023 | $13,106 | $11,059 | $10,602 | $11,873 |

| 9/30/2023 | $12,845 | $10,778 | $10,265 | $11,564 |

| 10/31/2023 | $12,596 | $10,607 | $10,053 | $11,358 |

| 11/30/2023 | $13,184 | $11,088 | $10,577 | $12,003 |

| 12/31/2023 | $13,730 | $11,512 | $11,032 | $12,506 |

| 1/31/2024 | $13,779 | $11,481 | $10,981 | $12,484 |

| 2/29/2024 | $13,701 | $11,318 | $10,803 | $12,304 |

| 3/31/2024 | $13,884 | $11,423 | $10,917 | $12,455 |

| 4/30/2024 | $13,582 | $11,134 | $10,587 | $12,145 |

| 5/31/2024 | $13,838 | $11,323 | $10,798 | $12,367 |

| 6/30/2024 | $14,018 | $11,430 | $10,925 | $12,449 |

The table below shows the average annual total returns of the Portfolio, a regulatory index, and one or more supplemental index(es) for certain periods ended June 30, 2024.

Average Annual Total Returns (%)

| Portfolio/Index Name | 1 Year | 5 Years | 10 Years |

|---|

| Fixed Income SHares: Series M | 7.35% | 1.42% | 3.44% |

| Bloomberg U.S. Aggregate Index | 2.63% | (0.23%) | 1.35% |

| Bloomberg U.S. MBS Fixed-Rate Index | 2.12% | (0.76%) | 0.89% |

| Bloomberg U.S. Credit Index | 4.42% | 0.54% | 2.21% |

All Portfolio returns are net of fees and expenses and include applicable fee waivers and/or expense limitations. Absent any applicable fee waivers and/or expense limitations, performance would have been lower and there can be no assurance that any such waivers or limitations will continue in the future.

Performance quoted represents past performance. Past performance is not a guarantee or a reliable indicator of future results.Current performance may be lower or higher than performance shown. Investment return and the principal value of an investment will fluctuate. Shares may be worth more or less than original cost when redeemed. Returns shown do not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or the redemption of Portfolio shares.Differences in the Portfolio’s performance versus an index and related attribution information with respect to particular categories of securities or individual positions may be attributable, in part, to differences in the pricing methodologies used by the Portfolio and the index.

Key Portfolio StatisticsFootnote Reference* (as of the end of the reporting period)

| Total Net Assets | $1,359,318 |

| # of Portfolio Holdings | 1,011 |

| Portfolio Turnover Rate | 306% |

Total Net Advisory Fees Paid During the Reporting PeriodFootnote Reference† | $0 |

| Footnote | Description |

Footnote† | No investment management fees or expenses are incurred by the Portfolio. The PIMCO Fixed Income SHares Portfolios are an integral part of “wrap-fee” programs sponsored by investment advisers and/or broker-dealers unaffiliated with the Portfolios and PIMCO. Participants in these programs pay a “wrap” fee to the sponsor of the program. |

Footnote* | Dollar amounts displayed in 000's |

What did the Portfolio invest in?

Allocation Breakdown (% of Net Assets)Footnote Reference*

| U.S. Government Agencies | 54.3% |

| Asset-Backed Securities | 35.8% |

| Corporate Bonds & Notes | 27.5% |

| Non-Agency Mortgage-Backed Securities | 18.4% |

| U.S. Treasury Obligations | 6.0% |

| Municipal Bonds & Notes | 1.1% |

| Preferred Securities | 1.0% |

| Sovereign Issues | 0.8% |

| Loan Participations and Assignments | 0.6% |

| Affiliated Investments | 0.1% |

| Other Investments | 0.0% |

| Other Assets and Liabilities, Net | (45.6%) |

| Total | 100.0% |

| Footnote | Description |

Footnote* | % of Net Assets includes derivatives instruments, if any, valued at the value used for determining the Portfolio's net asset value. The notional exposure of such derivatives investments therefore may be greater than what is depicted. |

For additional information about the Portfolio, including the Portfolio's prospectus, financial information, holdings and proxy voting information, please visit www.pimco.com/FISH or contact 888.87.PIMCO (888.877.4626). For tax information about the Portfolio, please visit: https://www.pimco.com/tax.

Fixed Income SHares: Series M

Semi-Annual Shareholder Report | June 30, 2024

Fixed Income SHares: Series R

Semi-Annual Shareholder Report | June 30, 2024

This semi-annual shareholder report contains important information about the Fixed Income SHares: Series R (the "Portfolio") for the period of January 1, 2024 to June 30, 2024 (the "reporting period"). You can find additional information about the Portfolio at www.pimco.com/FISH. You can also request this information by contacting us at 888.87.PIMCO (888.877.4626).

What were the Portfolio costs for the last six months?

(based on a hypothetical $10,000 investment)

| Portfolio Name | Cost of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

|---|

| Fixed Income SHares: Series R | $221 | 4.42% |

How did the Portfolio perform during the reporting period and what affected its performance?

The following affected performance (on a gross basis) during the reporting period:

• Overweight exposure to U.S. breakeven inflation ("BEI") contributed to relative performance, as U.S. BEI moved higher.

• Short exposure to eurozone interest rates contributed to relative performance, as eurozone interest rates broadly rose.

• Exposure to agency mortgage-backed securities, including the associated carry, contributed to relative performance, as the sector

posted positive returns.

• Long exposure to Japanese BEI, contributed to relative performance, as Japanese BEI moved higher.

• Overweight exposure to U.S. interest rates detracted from relative performance, as U.S. interest rates broadly rose.

• Duration strategies in Japan, including short exposure to Japanese interest rate swap spreads, detracted from relative performance,

as Japanese interest rate swap spreads tightened.

• Long exposure to Australian interest rates, specifically in the last four months of the period, detracted from relative performance, as

Australian interest rates broadly moved higher.

In addition to the Portfolio's performance, the tables in this section include performance of: (i) a broad-based securities market index (i.e., a regulatory index) and (ii) one or more supplemental index(es). Effective July 24, 2024, the Portfolio's regulatory index is the Bloomberg U.S. Aggregate Index. The Portfolio's regulatory index is shown in connection with certain regulatory requirements to provide a broad measure of market performance.

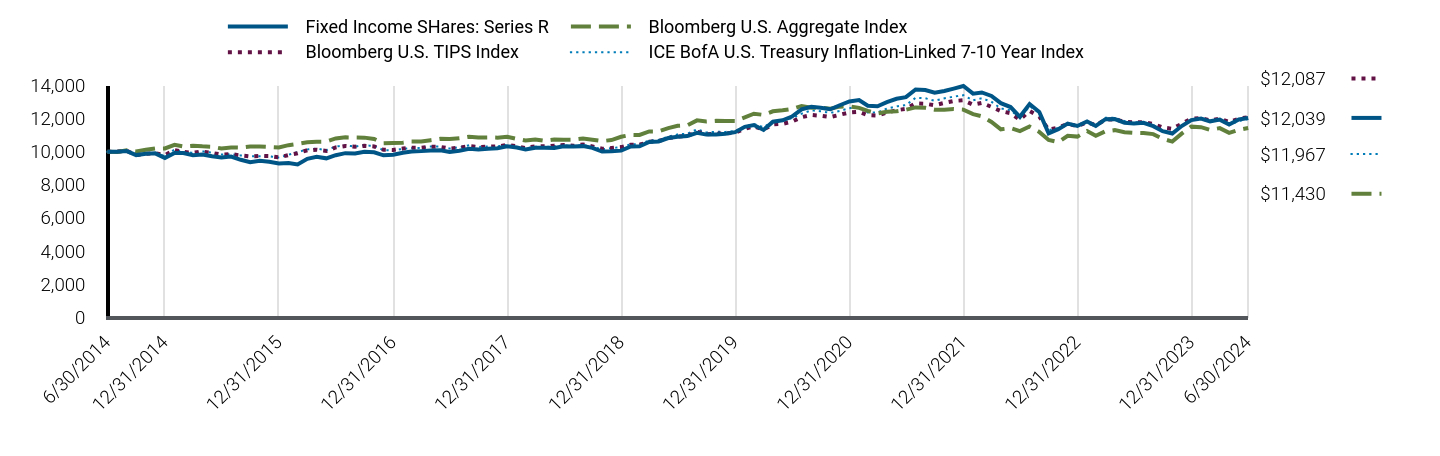

The table below illustrates cumulative returns for the 10-year period ended June 30, 2024 or the life of the Portfolio, if shorter. Cumulative returns are based on a hypothetical initial investment equal to the greater of either $10,000 or the investment minimum applicable to the share class.

Cumulative Returns Based on $10,000 Investment

| Fixed Income SHares: Series R | Bloomberg U.S. Aggregate Index | Bloomberg U.S. TIPS Index | ICE BofA U.S. Treasury Inflation-Linked 7-10 Year Index |

|---|

| 6/30/2014 | $10,000 | $10,000 | $10,000 | $10,000 |

| 7/31/2014 | $9,997 | $9,975 | $10,003 | $9,992 |

| 8/31/2014 | $10,035 | $10,085 | $10,047 | $10,029 |

| 9/30/2014 | $9,792 | $10,017 | $9,796 | $9,758 |

| 10/31/2014 | $9,871 | $10,115 | $9,879 | $9,849 |

| 11/30/2014 | $9,898 | $10,187 | $9,905 | $9,885 |

| 12/31/2014 | $9,622 | $10,196 | $9,793 | $9,735 |

| 1/31/2015 | $9,918 | $10,410 | $10,101 | $10,128 |

| 2/28/2015 | $9,918 | $10,312 | $9,980 | $9,975 |

| 3/31/2015 | $9,790 | $10,360 | $9,933 | $9,930 |

| 4/30/2015 | $9,829 | $10,323 | $10,006 | $10,020 |

| 5/31/2015 | $9,727 | $10,298 | $9,923 | $9,938 |

| 6/30/2015 | $9,647 | $10,186 | $9,827 | $9,831 |

| 7/31/2015 | $9,702 | $10,257 | $9,847 | $9,841 |

| 8/31/2015 | $9,508 | $10,242 | $9,772 | $9,770 |

| 9/30/2015 | $9,357 | $10,311 | $9,714 | $9,715 |

| 10/31/2015 | $9,455 | $10,313 | $9,739 | $9,726 |

| 11/30/2015 | $9,390 | $10,286 | $9,729 | $9,724 |

| 12/31/2015 | $9,288 | $10,252 | $9,652 | $9,638 |

| 1/31/2016 | $9,309 | $10,393 | $9,796 | $9,813 |

| 2/29/2016 | $9,226 | $10,467 | $9,905 | $9,973 |

| 3/31/2016 | $9,569 | $10,563 | $10,083 | $10,133 |

| 4/30/2016 | $9,685 | $10,604 | $10,117 | $10,183 |

| 5/31/2016 | $9,596 | $10,607 | $10,046 | $10,090 |

| 6/30/2016 | $9,787 | $10,797 | $10,255 | $10,308 |

| 7/31/2016 | $9,910 | $10,865 | $10,344 | $10,379 |

| 8/31/2016 | $9,887 | $10,853 | $10,297 | $10,308 |

| 9/30/2016 | $9,997 | $10,847 | $10,354 | $10,387 |

| 10/31/2016 | $9,960 | $10,764 | $10,312 | $10,339 |

| 11/30/2016 | $9,780 | $10,509 | $10,114 | $10,096 |

| 12/31/2016 | $9,816 | $10,524 | $10,104 | $10,077 |

| 1/31/2017 | $9,935 | $10,544 | $10,189 | $10,169 |

| 2/28/2017 | $10,006 | $10,615 | $10,237 | $10,224 |

| 3/31/2017 | $10,032 | $10,610 | $10,232 | $10,215 |

| 4/30/2017 | $10,066 | $10,692 | $10,292 | $10,308 |

| 5/31/2017 | $10,080 | $10,774 | $10,288 | $10,310 |

| 6/30/2017 | $9,986 | $10,763 | $10,190 | $10,192 |

| 7/31/2017 | $10,060 | $10,809 | $10,236 | $10,265 |

| 8/31/2017 | $10,179 | $10,906 | $10,345 | $10,386 |

| 9/30/2017 | $10,138 | $10,854 | $10,278 | $10,287 |

| 10/31/2017 | $10,182 | $10,861 | $10,300 | $10,308 |

| 11/30/2017 | $10,209 | $10,847 | $10,314 | $10,319 |

| 12/31/2017 | $10,323 | $10,897 | $10,408 | $10,412 |

| 1/31/2018 | $10,254 | $10,771 | $10,319 | $10,288 |

| 2/28/2018 | $10,137 | $10,669 | $10,219 | $10,182 |

| 3/31/2018 | $10,241 | $10,737 | $10,326 | $10,301 |

| 4/30/2018 | $10,235 | $10,658 | $10,320 | $10,283 |

| 5/31/2018 | $10,227 | $10,734 | $10,364 | $10,336 |

| 6/30/2018 | $10,320 | $10,720 | $10,406 | $10,382 |

| 7/31/2018 | $10,305 | $10,723 | $10,356 | $10,317 |

| 8/31/2018 | $10,334 | $10,792 | $10,430 | $10,407 |

| 9/30/2018 | $10,229 | $10,722 | $10,320 | $10,277 |

| 10/31/2018 | $10,003 | $10,638 | $10,172 | $10,147 |

| 11/30/2018 | $10,025 | $10,701 | $10,221 | $10,214 |

| 12/31/2018 | $10,062 | $10,898 | $10,277 | $10,274 |

| 1/31/2019 | $10,317 | $11,014 | $10,415 | $10,452 |

| 2/28/2019 | $10,323 | $11,007 | $10,414 | $10,450 |

| 3/31/2019 | $10,583 | $11,219 | $10,605 | $10,674 |

| 4/30/2019 | $10,614 | $11,221 | $10,640 | $10,711 |

| 5/31/2019 | $10,821 | $11,421 | $10,816 | $10,909 |

| 6/30/2019 | $10,897 | $11,564 | $10,909 | $11,042 |

| 7/31/2019 | $10,942 | $11,589 | $10,948 | $11,083 |

| 8/31/2019 | $11,140 | $11,890 | $11,208 | $11,350 |

| 9/30/2019 | $11,030 | $11,826 | $11,056 | $11,163 |

| 10/31/2019 | $11,038 | $11,862 | $11,084 | $11,203 |

| 11/30/2019 | $11,086 | $11,856 | $11,101 | $11,190 |

| 12/31/2019 | $11,180 | $11,848 | $11,143 | $11,247 |

| 1/31/2020 | $11,502 | $12,076 | $11,377 | $11,517 |

| 2/29/2020 | $11,609 | $12,293 | $11,534 | $11,671 |

| 3/31/2020 | $11,311 | $12,221 | $11,332 | $11,480 |

| 4/30/2020 | $11,809 | $12,438 | $11,647 | $11,820 |

| 5/31/2020 | $11,893 | $12,496 | $11,682 | $11,866 |

| 6/30/2020 | $12,121 | $12,575 | $11,812 | $12,022 |

| 7/31/2020 | $12,553 | $12,762 | $12,084 | $12,294 |

| 8/31/2020 | $12,709 | $12,659 | $12,216 | $12,496 |

| 9/30/2020 | $12,647 | $12,652 | $12,171 | $12,439 |

| 10/31/2020 | $12,563 | $12,596 | $12,092 | $12,348 |

| 11/30/2020 | $12,804 | $12,720 | $12,228 | $12,460 |

| 12/31/2020 | $13,034 | $12,737 | $12,368 | $12,627 |

| 1/31/2021 | $13,119 | $12,646 | $12,409 | $12,691 |

| 2/28/2021 | $12,778 | $12,463 | $12,209 | $12,363 |

| 3/31/2021 | $12,745 | $12,308 | $12,186 | $12,374 |

| 4/30/2021 | $12,996 | $12,405 | $12,356 | $12,602 |

| 5/31/2021 | $13,195 | $12,445 | $12,506 | $12,737 |

| 6/30/2021 | $13,294 | $12,533 | $12,582 | $12,816 |

| 7/31/2021 | $13,761 | $12,673 | $12,917 | $13,256 |

| 8/31/2021 | $13,722 | $12,649 | $12,894 | $13,228 |

| 9/30/2021 | $13,558 | $12,539 | $12,802 | $13,073 |

| 10/31/2021 | $13,666 | $12,536 | $12,947 | $13,220 |

| 11/30/2021 | $13,811 | $12,573 | $13,063 | $13,326 |

| 12/31/2021 | $13,970 | $12,541 | $13,105 | $13,411 |

| 1/31/2022 | $13,506 | $12,271 | $12,839 | $13,103 |

| 2/28/2022 | $13,577 | $12,134 | $12,949 | $13,226 |

| 3/31/2022 | $13,368 | $11,797 | $12,708 | $13,016 |

| 4/30/2022 | $12,930 | $11,349 | $12,449 | $12,608 |

| 5/31/2022 | $12,697 | $11,422 | $12,325 | $12,504 |

| 6/30/2022 | $12,106 | $11,243 | $11,935 | $12,049 |

| 7/31/2022 | $12,878 | $11,518 | $12,455 | $12,752 |

| 8/31/2022 | $12,393 | $11,192 | $12,123 | $12,348 |

| 9/30/2022 | $11,109 | $10,709 | $11,321 | $11,294 |

| 10/31/2022 | $11,362 | $10,570 | $11,462 | $11,420 |

| 11/30/2022 | $11,699 | $10,959 | $11,671 | $11,718 |

| 12/31/2022 | $11,554 | $10,909 | $11,552 | $11,537 |

| 1/31/2023 | $11,830 | $11,245 | $11,764 | $11,845 |

| 2/28/2023 | $11,554 | $10,954 | $11,603 | $11,569 |

| 3/31/2023 | $11,961 | $11,232 | $11,938 | $12,043 |

| 4/30/2023 | $11,972 | $11,300 | $11,951 | $12,046 |

| 5/31/2023 | $11,740 | $11,177 | $11,808 | $11,854 |

| 6/30/2023 | $11,703 | $11,137 | $11,768 | $11,765 |

| 7/31/2023 | $11,747 | $11,130 | $11,783 | $11,791 |

| 8/31/2023 | $11,538 | $11,059 | $11,678 | $11,598 |

| 9/30/2023 | $11,234 | $10,778 | $11,462 | $11,299 |

| 10/31/2023 | $11,095 | $10,607 | $11,379 | $11,165 |

| 11/30/2023 | $11,549 | $11,088 | $11,688 | $11,544 |

| 12/31/2023 | $11,907 | $11,512 | $12,002 | $11,924 |

| 1/31/2024 | $11,996 | $11,481 | $12,023 | $11,990 |

| 2/29/2024 | $11,832 | $11,318 | $11,894 | $11,784 |

| 3/31/2024 | $11,937 | $11,423 | $11,992 | $11,890 |

| 4/30/2024 | $11,642 | $11,134 | $11,790 | $11,625 |

| 5/31/2024 | $11,943 | $11,323 | $11,993 | $11,853 |

| 6/30/2024 | $12,039 | $11,430 | $12,087 | $11,967 |

The table below shows the average annual total returns of the Portfolio, a regulatory index, and one or more supplemental index(es) for certain periods ended June 30, 2024.

Average Annual Total Returns (%)

| Portfolio/Index Name | 1 Year | 5 Years | 10 Years |

|---|

| Fixed Income SHares: Series R | 2.87% | 2.01% | 1.87% |

| Bloomberg U.S. Aggregate Index | 2.63% | (0.23%) | 1.35% |

| Bloomberg U.S. TIPS Index | 2.71% | 2.07% | 1.91% |

| ICE BofA U.S. Treasury Inflation-Linked 7-10 Year Index | 1.72% | 1.62% | 1.81% |

All Portfolio returns are net of fees and expenses and include applicable fee waivers and/or expense limitations. Absent any applicable fee waivers and/or expense limitations, performance would have been lower and there can be no assurance that any such waivers or limitations will continue in the future.

Performance quoted represents past performance. Past performance is not a guarantee or a reliable indicator of future results.Current performance may be lower or higher than performance shown. Investment return and the principal value of an investment will fluctuate. Shares may be worth more or less than original cost when redeemed. Returns shown do not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or the redemption of Portfolio shares.Differences in the Portfolio’s performance versus an index and related attribution information with respect to particular categories of securities or individual positions may be attributable, in part, to differences in the pricing methodologies used by the Portfolio and the index.

Key Portfolio StatisticsFootnote Reference* (as of the end of the reporting period)

| Total Net Assets | $155,760 |

| # of Portfolio Holdings | 254 |

| Portfolio Turnover Rate | 157% |

Total Net Advisory Fees Paid During the Reporting PeriodFootnote Reference† | $0 |

| Footnote | Description |

Footnote† | No investment management fees or expenses are incurred by the Portfolio. The PIMCO Fixed Income SHares Portfolios are an integral part of “wrap-fee” programs sponsored by investment advisers and/or broker-dealers unaffiliated with the Portfolios and PIMCO. Participants in these programs pay a “wrap” fee to the sponsor of the program. |

Footnote* | Dollar amounts displayed in 000's |

What did the Portfolio invest in?

Allocation Breakdown (% of Net Assets)Footnote Reference*

| U.S. Treasury Obligations | 129.5% |

| U.S. Government Agencies | 37.6% |

| Sovereign Issues | 17.1% |

| Asset-Backed Securities | 8.6% |

| Non-Agency Mortgage-Backed Securities | 3.9% |

| Corporate Bonds & Notes | 1.8% |

| Short-Term Instruments | 1.7% |

| Other Investments | 0.7% |

| Other Assets and Liabilities, Net | (100.9%) |

| Total | 100.0% |

| Footnote | Description |

Footnote* | % of Net Assets includes derivatives instruments, if any, valued at the value used for determining the Portfolio's net asset value. The notional exposure of such derivatives investments therefore may be greater than what is depicted. |

For additional information about the Portfolio, including the Portfolio's prospectus, financial information, holdings and proxy voting information, please visit www.pimco.com/FISH or contact 888.87.PIMCO (888.877.4626). For tax information about the Portfolio, please visit: https://www.pimco.com/tax.

Fixed Income SHares: Series R

Semi-Annual Shareholder Report | June 30, 2024

Fixed Income SHares: Series TE

Semi-Annual Shareholder Report | June 30, 2024

This semi-annual shareholder report contains important information about the Fixed Income SHares: Series TE (the "Portfolio") for the period of January 1, 2024 to June 30, 2024 (the "reporting period"). You can find additional information about the Portfolio at www.pimco.com/FISH. You can also request this information by contacting us at 888.87.PIMCO (888.877.4626).

What were the Portfolio costs for the last six months?

(based on a hypothetical $10,000 investment)

| Portfolio Name | Cost of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

|---|

| Fixed Income SHares: Series TE | $0 | 0.00% |

How did the Portfolio perform during the reporting period and what affected its performance?

The following affected performance (on a gross basis) during the reporting period:

• A tactical allocation to taxable municipals contributed to performance, as taxable municipals outperformed the broader municipal

market.

• Security selection within the special tax sector contributed to performance, as holdings outperformed the broader municipal market.

• Overweight exposure to the housing sector contributed to performance, as the sector outperformed the broader municipal market.

• Overweight exposure to a duration position detracted from performance, as yields broadly rose.

• Security selection within the lease-backed sector detracted from performance, as the sector underperformed the broader municipal

market.

• Underweight exposure to the pre-refunded segment detracted from performance, as the segment outperformed the broader municipal

market.

In addition to the Portfolio's performance, the tables in this section include performance of: (i) a broad-based securities market index (i.e., a regulatory index) and (ii) one or more supplemental index(es). Effective July 24, 2024, the Bloomberg Municipal Bond Index replaced the Bloomberg 1-Year Municipal Bond Index as the Portfolio's regulatory index. The Portfolio's regulatory index is shown in connection with certain regulatory requirements to provide a broad measure of market performance.

The table below illustrates cumulative returns for the 10-year period ended June 30, 2024 or the life of the Portfolio, if shorter. Cumulative returns are based on a hypothetical initial investment equal to the greater of either $10,000 or the investment minimum applicable to the share class.

Cumulative Returns Based on $10,000 Investment

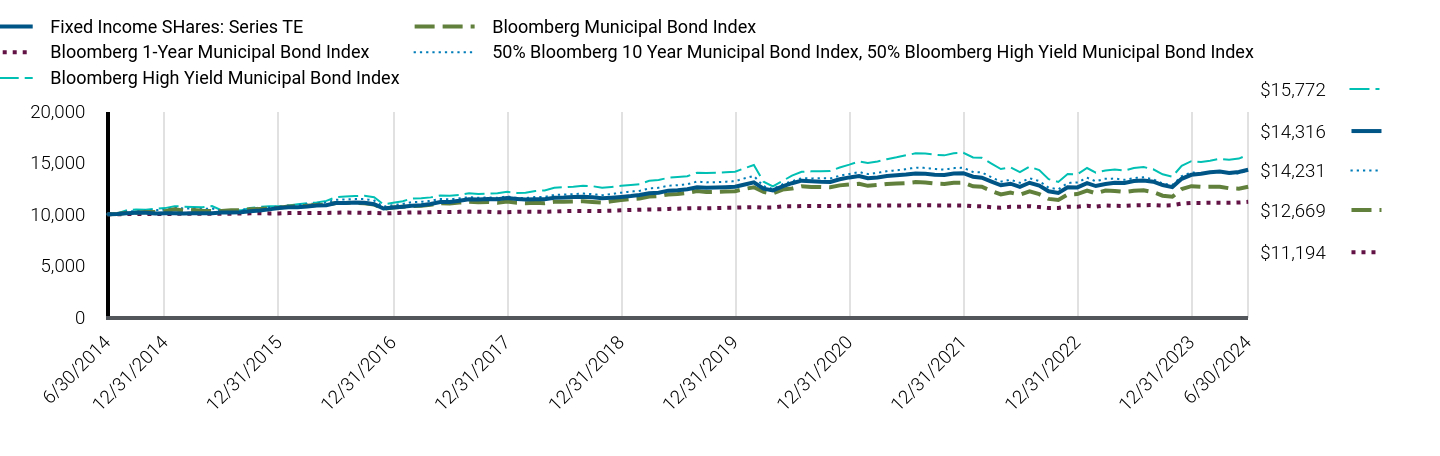

| Fixed Income SHares: Series TE | Bloomberg Municipal Bond Index | Bloomberg 1-Year Municipal Bond Index | 50% Bloomberg 10 Year Municipal Bond Index, 50% Bloomberg High Yield Municipal Bond Index | Bloomberg High Yield Municipal Bond Index |

|---|

| 6/30/2014 | $10,000 | $10,000 | $10,000 | $10,000 | $10,000 |

| 7/31/2014 | $10,020 | $10,018 | $10,000 | $10,045 | $10,063 |

| 8/31/2014 | $10,082 | $10,139 | $10,007 | $10,266 | $10,378 |

| 9/30/2014 | $10,144 | $10,149 | $10,007 | $10,303 | $10,461 |

| 10/31/2014 | $10,135 | $10,219 | $10,011 | $10,322 | $10,422 |

| 11/30/2014 | $10,073 | $10,236 | $10,017 | $10,384 | $10,531 |

| 12/31/2014 | $10,083 | $10,288 | $10,012 | $10,436 | $10,587 |

| 1/31/2015 | $10,084 | $10,470 | $10,031 | $10,635 | $10,777 |

| 2/28/2015 | $10,074 | $10,362 | $10,034 | $10,553 | $10,733 |

| 3/31/2015 | $10,084 | $10,392 | $10,034 | $10,560 | $10,705 |

| 4/30/2015 | $10,085 | $10,338 | $10,035 | $10,507 | $10,661 |

| 5/31/2015 | $10,085 | $10,309 | $10,034 | $10,550 | $10,781 |

| 6/30/2015 | $10,160 | $10,300 | $10,034 | $10,343 | $10,384 |

| 7/31/2015 | $10,165 | $10,375 | $10,048 | $10,354 | $10,328 |

| 8/31/2015 | $10,191 | $10,395 | $10,064 | $10,391 | $10,370 |

| 9/30/2015 | $10,283 | $10,470 | $10,077 | $10,551 | $10,591 |

| 10/31/2015 | $10,363 | $10,512 | $10,087 | $10,636 | $10,719 |

| 11/30/2015 | $10,466 | $10,554 | $10,074 | $10,678 | $10,762 |

| 12/31/2015 | $10,605 | $10,628 | $10,073 | $10,729 | $10,779 |

| 1/31/2016 | $10,674 | $10,755 | $10,104 | $10,840 | $10,840 |

| 2/29/2016 | $10,670 | $10,771 | $10,120 | $10,905 | $10,959 |

| 3/31/2016 | $10,739 | $10,806 | $10,105 | $10,978 | $11,074 |

| 4/30/2016 | $10,841 | $10,885 | $10,116 | $11,056 | $11,142 |

| 5/31/2016 | $10,868 | $10,915 | $10,122 | $11,130 | $11,289 |

| 6/30/2016 | $11,079 | $11,088 | $10,139 | $11,397 | $11,640 |

| 7/31/2016 | $11,076 | $11,095 | $10,157 | $11,438 | $11,716 |

| 8/31/2016 | $11,137 | $11,110 | $10,142 | $11,465 | $11,758 |

| 9/30/2016 | $11,114 | $11,054 | $10,120 | $11,463 | $11,789 |

| 10/31/2016 | $10,967 | $10,938 | $10,127 | $11,323 | $11,643 |

| 11/30/2016 | $10,551 | $10,531 | $10,083 | $10,732 | $10,950 |

| 12/31/2016 | $10,647 | $10,654 | $10,103 | $10,883 | $11,101 |

| 1/31/2017 | $10,729 | $10,724 | $10,140 | $11,000 | $11,257 |

| 2/28/2017 | $10,806 | $10,799 | $10,173 | $11,170 | $11,525 |

| 3/31/2017 | $10,862 | $10,822 | $10,173 | $11,200 | $11,552 |

| 4/30/2017 | $10,982 | $10,901 | $10,189 | $11,292 | $11,630 |

| 5/31/2017 | $11,170 | $11,074 | $10,208 | $11,479 | $11,808 |

| 6/30/2017 | $11,185 | $11,034 | $10,200 | $11,444 | $11,782 |

| 7/31/2017 | $11,305 | $11,123 | $10,224 | $11,535 | $11,859 |

| 8/31/2017 | $11,450 | $11,208 | $10,247 | $11,655 | $12,023 |

| 9/30/2017 | $11,429 | $11,151 | $10,235 | $11,590 | $11,958 |

| 10/31/2017 | $11,472 | $11,178 | $10,236 | $11,619 | $11,991 |

| 11/30/2017 | $11,439 | $11,118 | $10,190 | $11,582 | $12,021 |

| 12/31/2017 | $11,564 | $11,235 | $10,196 | $11,727 | $12,177 |

| 1/31/2018 | $11,484 | $11,102 | $10,225 | $11,582 | $12,063 |

| 2/28/2018 | $11,427 | $11,069 | $10,242 | $11,561 | $12,072 |

| 3/31/2018 | $11,441 | $11,110 | $10,235 | $11,666 | $12,249 |

| 4/30/2018 | $11,441 | $11,070 | $10,225 | $11,679 | $12,303 |

| 5/31/2018 | $11,590 | $11,197 | $10,259 | $11,863 | $12,561 |

| 6/30/2018 | $11,615 | $11,207 | $10,295 | $11,897 | $12,623 |

| 7/31/2018 | $11,673 | $11,234 | $10,317 | $11,940 | $12,668 |

| 8/31/2018 | $11,691 | $11,263 | $10,313 | $12,007 | $12,769 |

| 9/30/2018 | $11,642 | $11,190 | $10,293 | $11,945 | $12,719 |

| 10/31/2018 | $11,552 | $11,121 | $10,302 | $11,836 | $12,560 |

| 11/30/2018 | $11,604 | $11,244 | $10,335 | $11,955 | $12,648 |

| 12/31/2018 | $11,676 | $11,379 | $10,373 | $12,088 | $12,757 |

| 1/31/2019 | $11,761 | $11,465 | $10,406 | $12,194 | $12,842 |

| 2/28/2019 | $11,858 | $11,526 | $10,429 | $12,260 | $12,912 |

| 3/31/2019 | $12,038 | $11,708 | $10,458 | $12,509 | $13,245 |

| 4/30/2019 | $12,088 | $11,752 | $10,466 | $12,561 | $13,320 |

| 5/31/2019 | $12,284 | $11,914 | $10,505 | $12,758 | $13,536 |

| 6/30/2019 | $12,330 | $11,958 | $10,537 | $12,814 | $13,606 |

| 7/31/2019 | $12,414 | $12,055 | $10,572 | $12,910 | $13,692 |

| 8/31/2019 | $12,621 | $12,245 | $10,587 | $13,165 | $14,021 |

| 9/30/2019 | $12,560 | $12,147 | $10,564 | $13,087 | $13,993 |

| 10/31/2019 | $12,585 | $12,168 | $10,595 | $13,111 | $14,023 |

| 11/30/2019 | $12,623 | $12,199 | $10,613 | $13,152 | $14,077 |

| 12/31/2019 | $12,660 | $12,236 | $10,629 | $13,198 | $14,119 |

| 1/31/2020 | $12,881 | $12,456 | $10,666 | $13,488 | $14,467 |

| 2/29/2020 | $13,088 | $12,617 | $10,688 | $13,710 | $14,771 |

| 3/31/2020 | $12,472 | $12,159 | $10,635 | $12,721 | $13,147 |

| 4/30/2020 | $12,312 | $12,006 | $10,659 | $12,442 | $12,703 |

| 5/31/2020 | $12,707 | $12,388 | $10,765 | $12,899 | $13,222 |

| 6/30/2020 | $13,005 | $12,490 | $10,764 | $13,196 | $13,746 |

| 7/31/2020 | $13,255 | $12,701 | $10,791 | $13,493 | $14,119 |

| 8/31/2020 | $13,204 | $12,641 | $10,793 | $13,474 | $14,156 |

| 9/30/2020 | $13,154 | $12,644 | $10,801 | $13,483 | $14,170 |

| 10/31/2020 | $13,129 | $12,606 | $10,793 | $13,474 | $14,195 |

| 11/30/2020 | $13,391 | $12,796 | $10,806 | $13,736 | $14,536 |

| 12/31/2020 | $13,570 | $12,874 | $10,816 | $13,907 | $14,809 |

| 1/31/2021 | $13,705 | $12,956 | $10,834 | $14,092 | $15,118 |

| 2/28/2021 | $13,492 | $12,750 | $10,830 | $13,899 | $14,959 |

| 3/31/2021 | $13,569 | $12,829 | $10,838 | $14,013 | $15,121 |

| 4/30/2021 | $13,700 | $12,936 | $10,845 | $14,171 | $15,343 |

| 5/31/2021 | $13,775 | $12,975 | $10,850 | $14,264 | $15,519 |

| 6/30/2021 | $13,852 | $13,010 | $10,849 | $14,368 | $15,716 |

| 7/31/2021 | $13,956 | $13,118 | $10,863 | $14,522 | $15,905 |

| 8/31/2021 | $13,916 | $13,070 | $10,861 | $14,491 | $15,880 |

| 9/30/2021 | $13,839 | $12,976 | $10,849 | $14,384 | $15,776 |

| 10/31/2021 | $13,813 | $12,938 | $10,847 | $14,327 | $15,712 |

| 11/30/2021 | $13,944 | $13,048 | $10,850 | $14,472 | $15,918 |

| 12/31/2021 | $13,982 | $13,069 | $10,849 | $14,507 | $15,959 |

| 1/31/2022 | $13,640 | $12,711 | $10,777 | $14,094 | $15,513 |

| 2/28/2022 | $13,535 | $12,666 | $10,763 | $14,056 | $15,477 |

| 3/31/2022 | $13,156 | $12,255 | $10,674 | $13,582 | $14,917 |

| 4/30/2022 | $12,807 | $11,916 | $10,631 | $13,160 | $14,387 |

| 5/31/2022 | $12,958 | $12,093 | $10,712 | $13,338 | $14,546 |

| 6/30/2022 | $12,644 | $11,895 | $10,715 | $13,053 | $14,081 |

| 7/31/2022 | $13,049 | $12,210 | $10,773 | $13,488 | $14,607 |

| 8/31/2022 | $12,775 | $11,942 | $10,687 | $13,214 | $14,282 |

| 9/30/2022 | $12,221 | $11,484 | $10,595 | $12,572 | $13,402 |

| 10/31/2022 | $12,064 | $11,388 | $10,609 | $12,410 | $13,127 |

| 11/30/2022 | $12,612 | $11,921 | $10,731 | $13,030 | $13,891 |

| 12/31/2022 | $12,597 | $11,955 | $10,726 | $13,074 | $13,868 |

| 1/31/2023 | $13,011 | $12,298 | $10,816 | $13,541 | $14,484 |

| 2/28/2023 | $12,731 | $12,020 | $10,725 | $13,193 | $14,029 |

| 3/31/2023 | $12,923 | $12,287 | $10,840 | $13,434 | $14,247 |

| 4/30/2023 | $13,053 | $12,259 | $10,808 | $13,458 | $14,329 |

| 5/31/2023 | $13,022 | $12,153 | $10,797 | $13,337 | $14,230 |

| 6/30/2023 | $13,216 | $12,274 | $10,848 | $13,505 | $14,483 |

| 7/31/2023 | $13,266 | $12,323 | $10,871 | $13,580 | $14,577 |

| 8/31/2023 | $13,152 | $12,146 | $10,883 | $13,384 | $14,356 |

| 9/30/2023 | $12,828 | $11,790 | $10,838 | $12,972 | $13,868 |

| 10/31/2023 | $12,627 | $11,689 | $10,868 | $12,829 | $13,646 |

| 11/30/2023 | $13,434 | $12,431 | $11,026 | $13,690 | $14,704 |

| 12/31/2023 | $13,824 | $12,720 | $11,090 | $14,055 | $15,145 |

| 1/31/2024 | $13,923 | $12,655 | $11,086 | $13,987 | $15,075 |

| 2/29/2024 | $14,078 | $12,671 | $11,103 | $14,045 | $15,194 |

| 3/31/2024 | $14,138 | $12,671 | $11,103 | $14,122 | $15,374 |

| 4/30/2024 | $13,996 | $12,514 | $11,104 | $13,984 | $15,280 |

| 5/31/2024 | $14,102 | $12,477 | $11,131 | $13,955 | $15,396 |

| 6/30/2024 | $14,316 | $12,669 | $11,194 | $14,231 | $15,772 |

The table below shows the average annual total returns of the Portfolio, a regulatory index, and one or more supplemental index(es) for certain periods ended June 30, 2024.

Average Annual Total Returns (%)

| Portfolio/Index Name | 1 Year | 5 Years | 10 Years |

|---|

| Fixed Income SHares: Series TE | 8.32% | 3.03% | 3.65% |

| Bloomberg Municipal Bond Index | 3.21% | 1.16% | 2.39% |

| Bloomberg 1-Year Municipal Bond Index | 3.19% | 1.22% | 1.13% |

| 50% Bloomberg 10 Year Municipal Bond Index, 50% Bloomberg High Yield Municipal Bond Index | 5.37% | 2.12% | 3.59% |

| Bloomberg High Yield Municipal Bond Index | 8.90% | 3.00% | 4.66% |

All Portfolio returns are net of fees and expenses and include applicable fee waivers and/or expense limitations. Absent any applicable fee waivers and/or expense limitations, performance would have been lower and there can be no assurance that any such waivers or limitations will continue in the future.

Performance quoted represents past performance. Past performance is not a guarantee or a reliable indicator of future results.Current performance may be lower or higher than performance shown. Investment return and the principal value of an investment will fluctuate. Shares may be worth more or less than original cost when redeemed. Returns shown do not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or the redemption of Portfolio shares.Differences in the Portfolio’s performance versus an index and related attribution information with respect to particular categories of securities or individual positions may be attributable, in part, to differences in the pricing methodologies used by the Portfolio and the index.

Key Portfolio StatisticsFootnote Reference* (as of the end of the reporting period)

| Total Net Assets | $126,977 |

| # of Portfolio Holdings | 162 |

| Portfolio Turnover Rate | 8% |

Total Net Advisory Fees Paid During the Reporting PeriodFootnote Reference† | $0 |

| Footnote | Description |

Footnote† | No investment management fees or expenses are incurred by the Portfolio. The PIMCO Fixed Income SHares Portfolios are an integral part of “wrap-fee” programs sponsored by investment advisers and/or broker-dealers unaffiliated with the Portfolios and PIMCO. Participants in these programs pay a “wrap” fee to the sponsor of the program. |

Footnote* | Dollar amounts displayed in 000's |

What did the Portfolio invest in?

Allocation Breakdown (% of Net Assets)Footnote Reference*

| Municipal Bonds & Notes | 86.7% |

| Affiliated Investments | 8.2% |

| U.S. Government Agencies | 4.8% |

| Corporate Bonds & Notes | 0.8% |

| Short-Term Instruments | 2.4% |

| Other Assets and Liabilities, Net | (2.9%) |

| Total | 100.0% |

| Footnote | Description |

Footnote* | % of Net Assets includes derivatives instruments, if any, valued at the value used for determining the Portfolio's net asset value. The notional exposure of such derivatives investments therefore may be greater than what is depicted. |

For additional information about the Portfolio, including the Portfolio's prospectus, financial information, holdings and proxy voting information, please visit www.pimco.com/FISH or contact 888.87.PIMCO (888.877.4626). For tax information about the Portfolio, please visit: https://www.pimco.com/tax.

Fixed Income SHares: Series TE

Semi-Annual Shareholder Report | June 30, 2024

The information required by this Item 2 is only required in an annual report on this Form N-CSR.

| Item 3. | Audit Committee Financial Expert. |

The information required by this Item 3 is only required in an annual report on this Form N-CSR.

| Item 4. | Principal Accountant Fees and Services. |

The information required by this Item 4 is only required in an annual report on this Form N-CSR.

| Item 5. | Audit Committee of Listed Registrants. |

The information required by this Item 5 is only required in an annual report on this Form N-CSR.

The information required by this Item 6 is included as part of the Financial Statements and Financial Highlights filed under Item 7(a) of this Form N-CSR.

| Item 7. | Financial Statements and Financial Highlights for Open-End Management Investment Companies. |

| | (a) | The following is a copy of the report(s) of the Portfolios’ Financial Statements and Financial Highlights. |

PIMCO MANAGED ACCOUNTS TRUST

Semiannual Financial and Other Information

June 30, 2024

Fixed Income SHares (FISH)

Fixed Income SHares: Series C (“FISH: Series C”)

Fixed Income SHares: Series LD (“FISH: Series LD”)

Fixed Income SHares: Series M (“FISH: Series M”)

Fixed Income SHares: Series R (“FISH: Series R”)

Fixed Income SHares: Series TE (“FISH: Series TE”)

Table of Contents

| | | | |

| Important Information About the Portfolios | | | | |

We believe that bond funds have an important role to play in a well-diversified investment portfolio. It is important to note, however, that in an environment where interest rates may trend upward, rising rates would negatively impact the performance of most bond funds, and fixed income securities and other instruments held by a Portfolio are likely to decrease in value. A wide variety of factors can cause interest rates or yields of U.S. Treasury securities (or yields of other types of bonds) to rise (e.g., central bank monetary policies, inflation rates, general economic conditions, etc.). In addition, changes in interest rates can be sudden and unpredictable, and there is no guarantee that Portfolio management will anticipate such movement accurately. A Portfolio may lose money as a result of movements in interest rates.

As of the date of this report, interest rates in the United States and many parts of the world, including certain European countries, remain high. In efforts to combat inflation, the U.S. Federal Reserve (the “Fed”) raised interest rates multiple times in 2022 and 2023. In the second half of 2023 and the beginning of 2024, however, the Fed paused the rate hikes, keeping interest rates steady. It is uncertain whether rates will remain steady, increase or decrease in the future. As such, the Portfolios may face a heightened level of risk associated with rising interest rates and/or bond yields. This could be driven by a variety of factors, including but not limited to central bank monetary policies, changing inflation or real growth rates, general economic conditions, increasing bond issuances or reduced market demand for low yielding investments. Further, while bond markets have steadily grown over the past three decades, dealer inventories of corporate bonds are near historic lows in relation to market size. As a result, there has been a significant reduction in the ability of dealers to “make markets”.

Bond funds and individual bonds with a longer duration (a measure used to determine the sensitivity of a security’s price to changes in interest rates) tend to be more sensitive to changes in interest rates, usually making them more volatile than securities or funds with shorter durations. All of the factors mentioned above, individually or collectively, could lead to increased volatility and/or lower liquidity in the fixed income markets, or negatively impact a Portfolio’s performance or cause a Portfolio to incur losses. As a result, a Portfolio may experience increased shareholder redemptions, which, among other things, could further reduce the net assets of the Portfolio.

The Portfolios may be subject to various risks as described in each Portfolio’s prospectus and in the Principal and Other Risks in the Notes to Financial Statements.

Classifications of the Portfolios’ portfolio holdings in this report are made according to financial reporting standards. The classification of a particular portfolio holding as shown in the Schedule of Investments sections of this report may differ from the classification used for the

Portfolios’ compliance calculations, including those used in the Portfolios’ prospectus, investment objectives, regulatory and other investment limitations and policies, which may be based on different asset class, sector or geographical classifications. The Portfolios are separately monitored for compliance with respect to prospectus and regulatory requirements.

The geographical classification of foreign (non-U.S.) securities in this report, if any, are classified by the country of incorporation of a holding. In certain instances, a security’s country of incorporation may be different from its country of economic exposure.

In February 2022, Russia launched an invasion of Ukraine. As a result, Russia and other countries, persons and entities that provided material aid to Russia’s aggression against Ukraine, have been the subject of economic sanctions and import and export controls imposed by countries throughout the world, including the United States. Such measures have had and may continue to have an adverse effect on the Russian, Belarusian and other securities and economies, which may, in turn, negatively impact a Portfolio. The extent, duration and impact of Russia’s military action in Ukraine, related sanctions and retaliatory actions are difficult to ascertain, but could be significant and have severe adverse effects on the region, including significant adverse effects on the regional, European and global economies and the markets for certain securities and commodities, such as oil and natural gas, as well as other sectors. Further, a Portfolio may have investments in securities and instruments that are economically tied to the region and may have been negatively impacted by the sanctions and counter-sanctions by Russia, including declines in value and reductions in liquidity. The sanctions may cause a Portfolio to sell portfolio holdings at a disadvantageous time or price or to continue to hold investments that a Portfolio may no longer seek to hold. PIMCO will continue to actively manage these positions in the best interests of a Portfolio and its shareholders.

The United States’ enforcement of restrictions on U.S. investments in certain issuers and tariffs on goods from certain other countries has contributed to and may continue to contribute to international trade tensions and may impact portfolio securities. The United States’ enforcement of sanctions or other similar measures on various Russian entities and persons, and the Russian government’s response, may also negatively impact securities and instruments that are economically tied to Russia.