UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM 10-K

| þ | annual report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

| For the fiscal year ended | June 30, 2013 |

or

| o | Transition report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

| For the transition period from | _________________________________ to ___________________________________ |

| | |

| Commission File Number: | 001-15931 |

| SINOCOKING COAL AND COKE CHEMICAL INDUSTRIES, Inc. |

| (Exact name of issuer as specified in its charter) |

| Florida | | 98-0695811 |

(State or other jurisdiction of incorporation or organization) | | (I.R.S. employer identification number) |

| | | |

Kuanggong Road and Tiyu Road 10th Floor Chengshi Xin Yong She, Tiyu Road Xinhua District Pingdingshan, Henan Province People’s Republic of China | | 467000 |

| (Address of principal executive offices) | | (Zip Code) |

| Registrant’s telephone number, including area code | +86-3752882999 |

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | | Name of each exchange on which registered |

| Common stock, $0.001 par value | | NASDAQ Capital Market |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No þ

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every, Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (Sec.232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes þ No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act (Check one):

| | Large Accelerated Filer o | Accelerated Filer o |

| | Non-accelerated filer o | Smaller reporting company þ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No þ

As of December 31, 2012, the aggregate market value of the voting stock held by non-affiliates of the registrant was approximately $17 million, based on a closing price of $1.18 per share of common stock as reported on the NASDAQ Stock Market on such date.

As of September 19, 2013, the registrant had 21,121,372 shares of common stock outstanding.

TABLE OF CONTENTS

TO ANNUAL REPORT ON FORM 10-K

FOR YEAR ENDED JUNE 30, 2013

| | | | Page |

| PART I | | | |

| Item 1. | Business | | 4 |

| Item 1A. | Risk Factors | | 22 |

| Item 1B. | Unresolved Staff Comments | | 33 |

| Item 2. | Properties | | 34 |

| Item 3. | Legal Proceedings | | 34 |

| Item 4. | Mine Safety Disclosures | | 34 |

| | | | |

| PART II | | | |

| Item 5. | Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | | 35 |

| Item 6. | Selected Financial Data | | 35 |

| Item 7. | Management’s Discussion and Analysis of Financial Conditions and Results of Operations | | 35 |

| Item 7A. | Quantitative and Qualitative Disclosures About Market Risk | | 42 |

| Item 8. | Financial Statements | | 43 |

| Item 9. | Changes in and Disagreements With Accountants on Accounting and Financial Disclosure | | 43 |

| Item 9A. | Controls and Procedures | | 44 |

| Item 9B. | Other Information | | 45 |

| | | | |

| PART III | | | |

| Item 10. | Directors, Executive Officers and Corporate Governance | | 45 |

| Item 11. | Executive Compensation | | 48 |

| Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | | 49 |

| Item 13. | Certain Relationships and Related Transactions | | 51 |

| Item 14. | Principal Accounting Fees and Services | | 51 |

| | | | |

| PART IV | | | |

| Item 15. | Exhibits, and Financial Statement Schedules | | 51 |

| | | | |

| Signatures | | | 54 |

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This annual report on Form 10-K (the “Report”) and other reports (collectively the “Filings”) filed by the registrant from time to time with the Securities and Exchange Commission (the “SEC”) contain or may contain forward looking statements and information that are based upon beliefs of, and information currently available to, the registrant’s management as well as estimates and assumptions made by the registrant’s management. When used in the filings the words “anticipate,” “believe,” “estimate,” “expect,” “future,” “intend,” “plan” or the negative of these terms and similar expressions as they relate to the registrant or the registrant’s management identify forward looking statements. Such statements reflect the current view of the registrant with respect to future events and are subject to risks, uncertainties, assumptions and other factors (including the risks contained in the section of this Report entitled “Risk Factors”) relating to the registrant’s industry, the registrant’s operations and results of operations and any businesses that may be acquired by the registrant. Should one or more of these risks or uncertainties materialize, or should the underlying assumptions prove incorrect, actual results may differ significantly from those anticipated, believed, estimated, expected, intended or planned.

Although the registrant believes that the expectations reflected in the forward looking statements are reasonable, the registrant cannot guarantee future results, levels of activity, performance or achievements. Except as required by applicable law, including the securities laws of the United States, the registrant does not intend to update any of the forward-looking statements to conform these statements to actual results. The following discussion should be read in conjunction with the registrant’s financial statements and the related notes thereto included in this Report.

In this Report, “we,” “our,” “us,” “SinoCoking” or the “Company” sometimes refers collectively to SinoCoking Coal and Coke Chemical Industries, Inc. and its subsidiaries and affiliated companies.

PART I

General Overview

We are a vertically-integrated coal and coke producer based in Henan Province, People’s Republic of China (“PRC” or “China”). Our products include raw coal, washed coal, “medium” or mid-coal, coal slurries, coke, coal tar and crude benzol. We also generate electricity from gas emitted during the coking process, which we use primarily to power our operations.

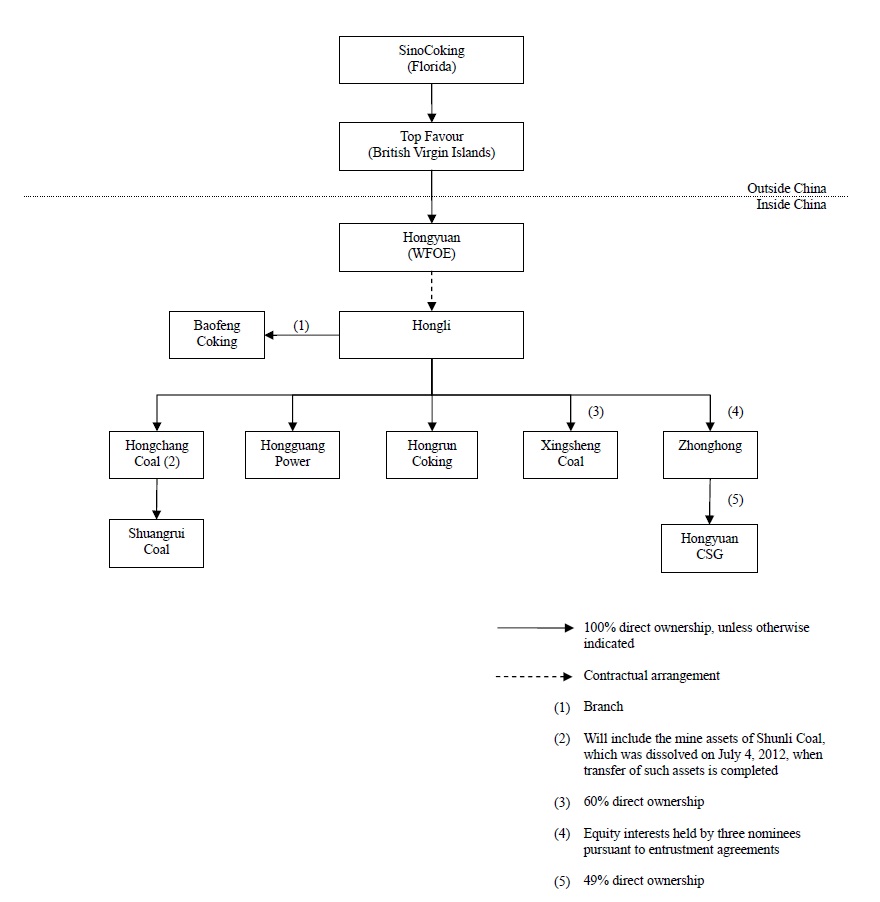

All of our business operations are conducted by Henan Province Pingdingshan Hongli Coal & Coke Co., Ltd. (“Hongli”), which we control through contractual arrangements that Hongli and its owners have entered into with Pingdingshan Hongyuan Energy Science and Technology Development Co., Ltd. (“Hongyuan”). These contractual arrangements provide for management and control rights, and in addition entitle us to receive the earnings and control the assets of Hongli. Hongyuan is wholly-owned by Top Favour Limited (“Top Favour”), of which we are the sole shareholder. Other than our interests in the contractual arrangements, we do not own any equity interests in Hongli.

Currently:

| · | Coking related operations are carried out by Hongli and its branch, Baofeng Coking Factory (“Baofeng Coking). |

| · | Coal related operations are under the following three subsidiaries of Hongli, although all mining activities are currently on hold pending the ongoing mining moratorium (see “Our Products and Operations – Coal – Coal Mining Moratorium” below): |

| (1) | Baofeng Hongchang Coal Co., Ltd. (“Hongchang Coal”); |

| (2) | Baofeng Shuangrui Coal Mining Co., Ltd. (“Shuangrui Coal”), which is wholly owned by Hongchang Coal; and |

| (3) | Baofeng Xingsheng Coal Mining Co., Ltd. (“Xingsheng Coal”). |

| · | Electricity generation is carried out by Baofeng Hongguang Environment Protection Electricity Generating Co., Ltd. (“Hongguang Power”), also a wholly owned subsidiary of Hongli. |

It is our intention to transfer all coal related operations from Hongli’s subsidiaries to a joint-venture established with Henan Province Coal Seam Gas Development and Utilization Co., Ltd. (“Henan Coal Seam Gas”), a state-owned enterprise and qualified provincial-level coal mine consolidator. The joint-venture, Henan Hongyuan Coal Seam Gas Engineering Technology Co., Ltd. (“Hongyuan CSG”), has been established, although our planned transfer of coal related activities to Hongyuan CSG has not been carried out as of the date of this Report. Our interests in Hongyuan CSG are held by Henan Zhonghong Energy Investment Co., Ltd. (“Zhonghong”), which equity interests are presently held on Hongli’s behalf and for its benefit by three nominees pursuant to share entrustment agreements.

In addition, once we complete construction of our new coking plant, we intend to operate the plant through Baofeng Hongrun Coal Chemical Co., Ltd. (“Hongrun Coking”), a wholly-owned subsidiary of Hongli. As of the date of this Report, however, construction has not been completed (see “Our Products and Operations – Coke – New Coking Facility” below), and Hongrun Coking has not commenced operations.

As of June 30, 2013, our current liabilities exceeded our current assets by $24,312,407. Our ability to continue as a going concern depends upon our expenditure requirements and repayments of our long-term loan facilities with Bairui Trust Co., Ltd. (“Bairui Trust”) as and when they fall due. See “Risk Factors – Risks Related to Our Business – If we cannot continue as a going concern, you will lose your entire investment” and“If we do not raise additional capital or refinance our debt, we will not be able to achieve our objectives and we may need to curtail or even discontinue operations”.

History and Corporate Structure

We were incorporated in Florida on September 30, 1996, originally under the name “J. B. Financial Services, Inc.” We changed our name to “Ableauctions.com, Inc.” on July 19, 1999.

On December 30, 2009, our shareholders approved a Plan and Agreement of Share Exchange, dated July 17, 2009, with Top Favour under which we agreed to acquire all of the outstanding capital stock of Top Favour in exchange for the issuance of 13,117,952 shares of our common stock to the shareholders of Top Favour (the “Share Exchange”). The Share Exchange was consummated on February 5, 2010.

On March 11, 2010, we completed two private placement financings, pursuant to exemptions under Regulation S and Regulation D, respectively, in which we sold and issued a total of 7,344,935 shares of common stock, and five-year warrants for the purchase of an additional 3,789,631 shares of common stock, resulting in aggregate proceeds of $44 million.

Top Favour

Top Favour is a holding company incorporated in the British Virgin Islands on July 2, 2008. Top Favour was formed by the owners of Hongli as a special vehicle for raising capital outside of the PRC. Other than holding 100% of the equity interests in Hongyuan and facilitating loan transactions for Hongli and its subsidiaries, Top Favour has no operations of its own.

Hongyuan

Hongyuan is a limited liability company organized in the PRC with registered capital of $3 million and is wholly-owned by Top Favour. Hongyuan was approved as a wholly foreign owned enterprise (“WFOE”) by the Henan government on February 26, 2009 and formally organized on March 18, 2009. Other than activities relating to its contractual arrangements with Hongli, Hongyuan has no separate operations of its own.

Hongli

Hongli is a limited liability company organized in the PRC on July 5, 1996, and held by four Chinese nationals (the “Owners”) initially as follows: 83.66% by Mr. Jianhua Lv, our Chairman and Chief Executive Officer, 6.44% by Ms. Xin Zheng, 4.95% by Mr. Wenqi Xu, and 4.95% by Mr. Guoxiang Song. In August 2010, the Pingdingshan government directed Hongli to increase its registered capital from 8,808,000 Renminbi (“RMB”) to RMB 28,080,000 in order to maintain its coal trading license. Accordingly, the Owners contributed the additional registered capital in full in August 2010, although not in proportion to their original ownership percentages: Mr. Lv and Ms. Zheng increased their holdings to 85.40% and 9.19%, respectively, while Mr. Xu and Mr. Song decreased their holdings to 3.99% and 1.42%, respectively. Registration of such additional contribution and change in ownership percentages with Pingdingshan’s Administration for Industry and Commerce (“AIC”) was completed in April 2011.

Currently, Hongli has a branch, six subsidiaries and a joint-venture as follows (each a “Hongli company,” and with Hongli collectively “Hongli Group”):

Branch:

| · | Baofeng Coking was established on May 31, 2002 as a branch of Hongli. |

Subsidiaries:

| · | Hongchang Coal is a limited liability company formed in the PRC on July 19, 2007 with registered capital of RMB 3 million. Hongchang Coal is wholly-owned by Hongli and holds the rights to mine. |

| · | Hongguang Power is a limited liability company formed in the PRC on August 1, 2006 with registered capital of RMB 22 million. Hongguang Power is wholly owned by Hongli. |

| · | Hongrun Cokingis a limited liability company formed in the PRC on May 17, 2011 with registered capital of RMB 30 million. Hongrun Coking is a wholly-owned subsidiary of Hongli. |

| · | Shuangrui Coal is a limited liability company formed in the PRC on March 17, 2009 with registered capital of RMB 4,029,960. Hongchang Coal currently holds 100% of the equity interests of Shuangrui Coal. Hongli initially acquired 60% of such interests on May 20, 2011, and subsequently acquired the remaining 40% on June 20, 2012. Hongli concurrently transferred all 100% of Shuangrui Coal to Hongchang Coal, which transfer has been registered with the Pingdingshan AIC. As of the date of this Report, Hongli has not yet paid any consideration for the 40% as negotiations with the seller remains ongoing, although we have accrued for such consideration based on its fair market value. Shuangrui Coal holds the rights to mine the Shuangrui coal mine. We intend to dissolve Shuangrui Coal in the future and consolidate its mine assets under Hongchang Coal. |

| · | Xingsheng Coal is a limited liability company formed in the PRC on December 6, 2007 with registered capital of RMB 3,634,600. Hongli currently holds 60% of the equity interests of Xingsheng Coal. Xingsheng Coal holds the rights to mine the Xingsheng coal mine. |

| · | Zhonghongis a limited liability company formed in the PRC on December 30, 2010 with registered capital of RMB 10,010,000, which was increased to RMB 20 million on April 14, 2011, and to RMB 51 million on July 12, 2011, of which RMB 30 million has been paid and the balance due by December 20, 2015. Zhonghong’s equity interests are presently held on Hongli’s behalf and for its benefit by three nominees pursuant to share entrustment agreements, namely, Messrs. Hui Zheng and Jiangong Fan, vice president of operations and a department manager at Hongli, respectively, and an unrelated party who also serves as Zhonghong’s general manager. Zhonghong holds our interests in Hongyuan CSG, our joint-venture with Henan Coal Seam Gas. |

Joint-Venture:

| · | Hongyuan CSG is a joint-venture established in the PRC on April 28, 2011 by Zhonghong (49%) and Henan Coal Seam Gas (51%). Hongli’s interests in the joint-venture are held by Zhonghong. |

We also acquired 100% of Baofeng Shunli Coal Ming Co., Ltd. (“Shunli Coal”) on May 20, 2011. On July 4, 2012, Shunli Coal was dissolved, and we are in the process of applying to transfer its mine assets to, and consolidating them under, Hongchang Coal, which we currently expect to complete by the end of fiscal 2014. Shunli Coal’s mine assets consist of the rights to mine Shunli coal mine.

Contractual Arrangements with Hongli Group and the Owners

Our relationship with Hongli Group and the Owners are governed by a series of contractual arrangements, under which our subsidiary Hongyuan holds and exercises ownership and management rights over Hongli Group. While we do not own any equity interest in Hongli Group, the contractual arrangements are designed to provide us with rights equivalent in all material respects to those we would possess as its sole equity holder, including absolute control rights and the rights to assets, property and income. According to a legal opinion issued by our PRC counsel, the contractual arrangements constitute valid and binding obligations of the parties to such agreements, and are enforceable and valid in accordance with the laws of the PRC.

The contractual arrangements, entered into on March 18, 2009, consist of the following:

| · | Consulting Services Agreement: Hongyuan provides each Hongli company with general consulting services relating to its business management and operations on an exclusive basis. Additionally, Hongyuan owns any intellectual property rights that are developed during the course of providing such services. Each Hongli company pays a quarterly consulting service fee in RMB equal to its net income for such quarter to Hongyuan. This agreement is in effect unless and until terminated by written notice of either party if: (a) the other party causes a material breach of the agreement, provided that if the breach does not relate to a financial obligation, the breaching party has 14 days to cure following the receipt of written notice; (b) the other party becomes bankrupt, insolvent, is the subject of proceedings or arrangements for liquidation or dissolution, ceases to carry on business, or becomes unable to pay its debts as they become due; (c) Hongyuan terminates its operations; (d) a Hongli Group business license or any other approval for its business operations is terminated, cancelled or revoked; or (e) circumstances arise which would materially and adversely affect the performance or the objectives of this agreement. Additionally, Hongyuan may terminate the agreement without cause. |

| · | Operating Agreement*: Hongyuan provides guidance and instructions for each Hongli company’s daily operations, financial management and employment issues. In addition, Hongyuan agrees to guarantee the performance of each Hongli company under any agreements or arrangements relating to its business arrangements with any third party. In return, the Owners must designate Hongyuan’s designees as their representatives on each Hongli company’s board of directors, and Hongyuan has the right to appoint senior executives of each Hongli company. Additionally, each Hongli company agrees to pledge its accounts receivable and all of its assets to Hongyuan. Moreover, each Hongli company agrees not to engage in any transactions that could materially affect its assets, liabilities, rights or operations without Hongyuan’s prior consent, including without limitation, incurrence or assumption of any indebtedness, sale or purchase of any assets or rights, incurrence of any encumbrance on any of its assets or intellectual property rights in favor of a third party or transfer of any agreements relating to its business operation to any third party. The term of this agreement is the maximum period of time permitted by law unless sooner terminated by any other agreements reached by all parties or upon a 30-day written notice from Hongyuan. The term may be extended only upon Hongyuan’s written confirmation prior to the expiration of the agreement, with the extended term to be mutually agreed upon by the parties. Under current applicable PRC law, there is no limitation on the maximum term permitted by law for this agreement. |

| · | Equity Pledge Agreement*: The Owners pledged all of their equity interests in Hongli Group to Hongyuan to guarantee each Hongli company’s performance of the consulting services agreement. If a Hongli company or the owners breach their respective contractual obligations, Hongyuan, as pledgee, will be entitled to certain rights, including, but not limited to, the right to vote with, control and sell the pledged equity interests. The Owners also agreed that upon occurrence of any event of default, Hongyuan shall be granted an exclusive, irrevocable power of attorney to take actions in the place and stead of the owners to carry out the security provisions of the equity pledge agreement, and take any action and execute any instrument as required by Hongyuan to accomplish the purposes of the agreement. The Owners agreed not to dispose of the pledged equity interests or take any actions that would prejudice Hongyuan’s interest. This agreement will expire two years from the fulfillment of Hongli Group’s obligations under the consulting services agreement. |

| · | Option Agreement*: The Owners irrevocably granted Hongyuan an exclusive option to purchase, to the extent permitted under PRC law, all or part of their equity interests in Hongli Group at a price equal to their initial registered capital contributions or the minimum amount of consideration permitted under PRC law. Hongyuan has sole discretion to decide when to exercise the option, and whether in part or in full. The term of this agreement is ten years from January 1, 2006 and may be extended prior to its expiration by written agreement of the parties. |

| · | Voting Rights Proxy Agreement*: The Owners irrevocably granted a Hongyuan designee the right to exercise all their voting rights in accordance with PRC laws and each Hongli company’s governing charters. This agreement may not be terminated without the unanimous consent of all parties, except that Hongyuan may terminate the proxy agreement with or without cause upon 30-day written notice to the owners. |

| * | Re-executed on September 9, 2011, to reflect RMB 20 million of additional registered capital contributed by the Owners in August 2010, and the resulting change in ownership percentages. We were made a party to the re-executed agreements to acknowledge them. |

As a result of the foregoing contractual arrangements, we have the ability to effectively control Hongli Group’s daily operations and financial affairs, appoint senior executives and decide on all matters requiring the Owners’ approval. While the Owners continue to own 100% of equity interests, they have given us their rights attendant to such ownership through the contractual arrangements. Accordingly, we are considered the primary beneficiary of Hongli Group and each Hongli company is deemed our variable interest entity (“VIE”).

However, control based on contractual arrangements may ultimately not be as effective as direct ownership, as we will need to enforce our rights through quasi-judicial proceeding in the event Hongli Group fails to perform its contractual obligations. In the event the outcome of such proceeding is unfavorable to us, we may effectively lose control over Hongli Group. See “Risk Factors – Risks Related to Our Corporate Structure – Our contractual arrangements with Hongli and its owners as well as our ability to enforce our rights thereunder may not be as effective in providing control over Hongli as direct ownership.” As of September 19, 2013, Mr. Lv held approximately 31.7% of our issued and outstanding common stock, and 85.40% of the equity interests of Hongli. As such, we believe that our interests remain aligned with the Owners. However, we cannot give assurance that such interests will always be aligned, or that we can effectively control Hongli Group if and when such interests are no longer aligned. See“Risk Factors - Risks Related to Our Corporate Structure – Management members of Hongli have potential conflicts of interest with us, which may adversely affect our business and your ability for recourse.”

Our Current Corporate Structure

The following diagram illustrates our current corporate structure:

Our Products and Operations

Overview

We are based in Henan Province in the central part of China, known as a coal-rich region. Our current operations are located in west Baofeng County, a part of Pingdingshan Prefecture south of Zhengzhou, the provincial capital. Our three principal products are coal, coke and electricity.

Coal

We sell coal, including raw (unprocessed) coal, washed coal, mid-coal and coal slurries (see “Coal Washing” below), and also use washed coal to make coke. We currently control four coal mines (see “Property, Plant and Equipment” below). Until June 2010, we largely extracted coal from Hongchang coal mine to meet our needs, although we also engaged in coal trading. As described under “Coal Mining Moratorium” below, however, we have been unable to extract coal since September 2011. We have instead been relying on coal purchased elsewhere, including from Shanxi, Qinghai and Inner Mongolia, to meet our requirements. Our coal purchases for the fiscal years ended June 30, 2012 and 2013 are as follows:

| Fiscal Year | | | Annual Purchases* (metric tons) | |

| 2012 | | | | 461,932 | |

| 2013 | | | | 384,515 | |

* Including coal for washing, coking and trading.

Generally, if the coal that we purchase meets coking requirements, we will reserve it for that purpose. Occasionally, however, we sell the coal (also known as coal trading) when market conditions are favorable.

Coal Mining Moratorium

In December 2009, the Henan government issued a directive to consolidate coal mines with annual production capacity below 300,000 metric tons (each a “targeted mine” and collectively the “targeted mines”), spurred by the central government’s decision to consolidate China’s coal industry in order to improve production efficiency and reduce coal mine accidents. In March 2010, the Henan government directed all lower-level governments within the province to begin shutting down all targeted mines, and further designated six state-owned enterprises (“SOEs”) to consolidate the targeted mines. Once shut down, the targeted mines cannot resume operations until they are consolidated and their facilities satisfy certain safety requirements.

In February and April 2010, the Baofeng government and the Pingdingshan government designated Hongli to consolidate targeted mines within the county and municipality, respectively. Because the Henan government’s directive requires that safety responsibility at each targeted mine be borne by a designated SOE, we reached an arrangement with one of them, Henan Coal Seam Gas, to form a joint-venture that would allow us to comply with the Henan government’s directive while maintaining operational control over any targeted mine that we consolidate. Such joint-venture, Hongyuan CSG, was formed in April 2011.

In late June 2010, pursuant to the Henan government’s directive, the Pingdingshan government imposed a mining moratorium on all targeted mines within Pingdingshan. Nevertheless, we continued to operate our only mine at that time, Hongchang coal mine, at approximately 50% capacity until September 2011, when we halted operation in order to complete certain engineering and safety upgrades. Operations at our other three mines (Shuangrui, Xingsheng and Shunli) were already halted when we acquired controlling interests in them in May 2011, and have not resumed since.

In August 2011, Henan Coal Seam Gas, as a designated SOE consolidator, determined that Hongchang and Xingsheng coal mines were safe to resume operations, and applied with the Henan government to confirm such determination and issue the necessary licenses and permits to resume operations at both mine sites. However, due to an accident in November 2011 at a mine owned by Yima Coal Group, another designated SOE consolidator, the Henan government ordered all targeted mines to undergo further safety inspections and upgrades. We have made approximately $3.2 million in prepayments for works to increase our mining capacity at Hongchang coal mine to 450,000 metric tons, as well as to upgrade the monitoring system (by installing additional detectors), automatic control system (including power controls and ventilation), and escape system (with additional refuge compartments) at Hongchang and Xingsheng coal mines. Although such works have not commenced, we have submitted the related engineering plans to Henan Coal Seam Gas for its approval and submission to the Henan government. Accordingly, the applications to resume operations at these two mines remain pending as of the date of this Report. As we are also in the process of consolidating Shunli coal mine under Hongchang Coal (see “History and Corporate Structure – Hongli” above), the application approval for Hongchang coal mine may be subject to additional delay.

Henan Coal Seam Gas has not yet made a determination as to the safety at Shuangrui and Shunli coal mines, and we do not know when such determination will be made, if at all. In addition, our objective in acquiring Shuangrui Coal, Xingsheng Coal and Shunli Coal is their mining rights, and their sellers were required to dispose of all other assets and liabilities before the transfer of equity interests to us is complete, and to assume all rights and obligations to such assets and liabilities until their disposal, which rights and obligations we would disclaim should any such asset or liability remains in the company after the transfer of equity interests to us is complete. Although equity interests have been transferred to us, the assets and liabilities that the sellers agreed to dispose of remain intact as of the date of this Report. In accordance with our agreements with them, the sellers are in the process of disposing all such assets and liabilities, and on September 2, 2011, we entered into a supplemental agreement with them to memorialize such agreements, which were not previously reduced to writing. Aside from the mining moratorium, we expect such disposals to be completed prior to any resumption of mining operations.

Assuming all four mines can resume operations, it is our present intention to transfer our interests in them to, and to operate them through, Hongyuan CSG. Such transfer, if carried out, would reduce any future revenue we may receive from these mines by 31%, or pro rata to the 49% of the joint-venture that we control. Nevertheless, we believe that such transfer would be in our best interests by reducing any risk of loss from potential future policy changes by the central and provincial governments through the presence and influence of Henan Coal Seam Gas, our joint-venture partner.

Coal Washing

At the Baofeng plant (see “Coke” below), we operate a coal-washing facility that is capable of processing up to 750,000 metric tons of coal per year. Under current Chinese coking industry standards, raw coal with no more than 1% sulfur content is deemed suitable for coking, although other factors are also considered. In addition to low sulfur content, the industry preference is for lower ash content and volatile matters. While much of the coal from our mines and that we purchase is generally suitable for coking based on these parameters, the coal must nevertheless be washed before it is ready for the coking ovens, in order to reduce ash and sulfur content, and to increase thermal value. We use a water-based jig washing process, which is prevalent in China, and use both underground and recycled water. Sorting machines that can process up to 600 metric tons per hour sort the washed coal according to size. Washed coal is also typically blended with other coal in order to achieve the proper chemical composition and thermal value for coking.

Approximately 1.33 - 1.38 metric tons of raw coal yield 1 metric ton of washed coal. The bulk of the washed coal we produce is intended for our coking needs, although we sell if the pricing is favorable. In addition to washed coal, the coal-washing process produces two byproducts:

| · | “Medium” coal (or “mid-coal”), a PRC coal industry classification, is coal that does not have sufficient thermal value for coking, and is mixed with raw coal and even coal slurries, then sold for electricity generation, and domestic and industrial heating applications. |

| · | Coal slurries (or coal slime) are the castoffs and debris from the washing process. Coal slurries can be used as a fuel with low thermal value, and are sold “as is” or mixed with mid-coal to produce a blended mixture. |

Our annual production volumes of washed coal, mid-coal and coal slurries for the fiscal years ended June 30, 2012 and 2013, are as follows:

| | | Annual Production

(metric tons) | |

Fiscal

Year | | Washed Coal | | | Mid-

Coal* | | | Coal

Slurries* | |

| 2012 | | | 104,545 | | | | 34,848 | | | | 17,424 | |

| 2013 | | | 90,461 | | | | 45,230 | | | | 15,077 | |

* Estimated based on amount of raw coal used.

Coke

Coke is a hardened, solid carbonaceous residue derived from low-ash, low-sulfur bituminous coal from which the volatile constituents are driven off by baking in an oven without oxygen at high temperatures so that the fixed carbon and residual ash are fused together. Volatile constituents of the coal include water, coal-gas, and coal-tar.

We currently produce metallurgical coke, which is primarily used for steel manufacturing. China has exacting national standards for coke, based upon a variety of metrics, including most importantly, ash content, volatilization, caking qualities, sulfur content, mechanical strength and abrasive resistance. Typically, metallurgical coke must have more than 80% fixed carbon, less than 15% ash content, less than 0.8% sulfur content and less than 1.9% volatile matter. Our metallurgical coke is typically 85% fixed carbon, less than 12% ash, less than 1.9% volatile matter and less than 0.7% sulfur.

According to national standards, metallurgical coke is classified into three grades – Grade I, Grade II and Grade III, with Grade I being the highest quality. Generally, our customers do not have specific content requirements, but we may make certain adjustments, such as to moisture content, upon request. The amount of each grade of coke that we produce is based on market demands, although historically our customers have mostly required Grade II coke which has higher profit margin than other types of coke. For the fiscal years ended June 30, 2012 and 2013, we only produced Grade II coke.

We currently operate two plants. At the plant that we own (the “Baofeng plant”), we produce coke from a series of three WG-86 Type coke ovens lined up in a row with an annual capacity of 250,000 metric tons. SinceApril 2013, we have also been leasing a plant from Pingdingshan Hongfeng Coal Processing and Coking, Ltd. (the “Hongfeng plant”). The Hongfeng plant has an annual capacity of 200,000 metric tons and is approximately 3 miles from the Baofeng plant. We conducted trial production near the end of April and commenced production in August. We believe that the skills we gain from operating its ZN-43 type coke ovens will be invaluable for operating our 900,000 metric ton facility still under construction (see “New Coking Facility” below).

After being processed at our coal-washing facility, coal is sent to a coal blending room (either at the Baofeng plant or the Hongfeng plant) where it is crushed and blended to achieve an optimal coking mixture. Samples are taken from the coal blend and tested for moisture, chemical composition and other properties. The crushed and blended coal is next tamped, or packed, prior to being transported by conveyor to a coal bin to be fed into the waiting oven below. This tamping process allows the use of lower quality washed coal without affecting the quality of the coke produced. After processing through temperature-controlled ovens at temperature of 1200° C (2,192° F), hot coke is pushed out of the oven chamber onto a waiting coke cart, transported to an adjacent quench tower where it is cooled with water spray, and hauled to a platform area adjacent to our private rail line to be air-dried. Coke samples are taken at several stages during the process and analyzed in our testing facility, and data is recorded daily and kept by technicians. After drying, the coke is sorted according to size to meet customer requirements.

For the fiscal years ended June 30, 2012 and 2013, we produced the following volumes of metallurgical coke:

| Fiscal Year | | | Annual Production

(metric tons) | |

| 2012 | | | | 163,202 | |

| 2013 | | | | 152,384 | |

Since the mining moratorium and the cessation of our mining operations, we have largely relied on purchased coal to make coke.

Coke Emissions Recycling

In the coke oven, coal’s volatile contents, including water and coal tar, are driven off in gaseous forms, which we capture and recycle. We pipe coal gas into a cooling tower to separate coal tar by condensation, which we sell as a fuel byproduct (see “Coal Byproducts” below). We burn the remaining purified coal gas to generate steam that drives steam-powered turbines to produce electricity (see “Electricity Generation” below).

Coking Byproducts

Coal tar is an ingredient of coal tar pitch used in the aluminum industry, and can be further refined to create chemicals and additives such as fine phenol, fine naphthalene and modified pitch that can be used as raw material in making concrete sealant, wood treatment compounds, agricultural pesticides and other chemical products.

Our annual production volumes of coal tar for the years ended June 30, 2012 and 2013 are as follows:

| Fiscal Year | | | Annual Production

(metric tons) | |

| 2012 | | | | 7,421 | |

| 2013 | | | | 6,379 | |

There are other byproducts which the Baofeng plant does not produce. In addition to coal tar, the Hongfeng plant also produces crude benzol and purified coal gas.

New Coking Facility

On March 3, 2010, we commenced construction of a new state-of-the-art coking plant on a 460,000 square meter site adjacent to the Baofeng plant. As of the date of this Report, we have completed construction of the shallow foundation, an underground workshop and the furnace and chimney rack, and are in the process of installing the coal preparation, cooling, recycling, and auxiliary systems, as well as framing the coal blending structure and coal yard. Originally anticipated to be completed at the end of December 2011, we have slowed down construction in light of ongoing weak demand for coke. We plan to complete the plant and commence operations once market improves and stabilizes, which we currently expect to be some time in fiscal 2014, although there is no guaranty that this will happen.

When completed as designed, this new plant is expected to have an estimated coke-producing capacity of up to 900,000 metric tons per year, as well as the ability to generate power and distill chemicals such as crude benzol, sulfur and ammonium sulfate from the coking process. The new plant is also expected to produce purified coal gas. Our plans to provide the coal gas as a fuel source to local residents through the state-owned gas grid have received approval from the authorities of Daying County, and we currently plan to offer the coal gas at a price per thermal equivalent unit that is estimated to be 20% less than the current price of liquid natural gas, a competing alternative. Hongrun Coking will operate the new plant.

Electricity Generation

After coal tar is separated at the Baofeng plant, the remaining coal gas is piped to two onsite 3,000-kilowatt power stations (the Daying power station and the Sunling power station) to generate electricity, each of which has an estimated maximum generating capacity of 26,280,000 kilowatt-hours per year. The generated electricity primarily powers operations at the Baofeng plant and at Hongchang coal mine. Local state-owned utilities supply electricity to the Hongfeng plant and Shunli coal mine, Xingsheng coal mine and Shuangrui coal mine.

Our annual amounts of electricity generated for the years ended June 30, 2012 and 2013 are as follows:

| Fiscal Year | | | Annual Generation

(kilowatt) | |

| 2012 | | | | 6,783,760 | |

| 2013 | | | | 5,790,938 | |

Sales and Marketing

We enter into non-binding annual letters of intent that set forth current year supply quantities, suggested pricing, and monthly delivery schedules with our customers for both coal and coke products at the beginning of each calendar year. The terms of the letters of intent are usually negotiated during the Annual National Coal Trading Convention organized by the China Coal Transport and Distribution Association. A significant portion of our sales are made through attendance at this convention. Changes in delivery quantity and pricing, which is based on open market pricing at the time of delivery, must be documented in a final written contract on a 30-day advance notice submitted by the party making the change and accepted by the other party. All of our current customers are generally required to make payment upon delivery of each shipment. In pricing our products, we consider factors such as the prices offered by competitors, the quality and grade of the product, the volume in national and regional coal inventory build-up and forecasted future trends for coal and coke prices. The remaining portion of our sales is derived from purchase orders placed by customers throughout the year when they require additional coal and coke products.

We have a flexible credit policy, and adjust credit terms for different types of customers. Depending on the customer, we may allow open accounts, or require acceptance bills or cash on delivery. We consider the creditworthiness and the requested credit amount of each customer when determining the appropriate payment arrangements and credit terms, which generally do not exceed a period over 90 days. We evaluate the creditworthiness of potential new customers before entering into sales contracts and reassesses customer creditworthiness on an annual basis. For customers without an established history, we require immediate settlement of accounts upon delivery.

Coke Sales

Coke sales for the last two fiscal years in volume, dollar amount and as a percentage of our total revenue, and the weighted average selling price per metric ton for each fiscal year, are as follows:

| | | Coke Sales | |

| Fiscal Year | | Annual Sales

(metric tons) | | | Annual Sales ($) | | | % of Revenue | | | Weighted

Average

Sale Price Per

Metric Ton ($) | |

| 2012 | | | 166,373 | | | $ | 38,656,636 | | | | 49 | % | | $ | 232 | |

| 2013 | | | 149,882 | | | $ | 31,171,635 | | | | 47 | % | | $ | 208 | |

China’s coke market was fairly soft for much of fiscal 2013, impacted by weak steel demands from tighter government control of real estate and land developments, as well as general economic slowdown which negatively affected heavy industries. The resulting excess in production capacity and inventory of crude steel pushed down the coke market accordingly.

Raw Coal Sales

Raw coal sales for the last two fiscal years in volume, dollar amount and as a percentage of our total revenue, and the weighted average selling price per metric ton for each fiscal year, are as follows:

| | | Raw Coal Sales | |

| Fiscal Year | | Annual Sales*

(metric tons) (1) | | | Annual Sales* ($) | | | % of Revenue | | | Weighted

Average

Sale Price Per

Metric Ton ($) | |

| 2012 | | | 73,990 | | | $ | 5,441,981 | | | | 7 | % | | $ | 74 | |

| 2013 | | | 55,012 | | | $ | 3,356,797 | | | | 5 | % | | $ | 61 | |

| * | Includes raw coal we purchased as well as some we managed to extract from Hongchang coal mine (approximately 7,000 metric tons), and raw coal/mid-coal/coal slurries mixtures. Excludes any raw coal we used internally as raw material to produce washed coal and coke. |

Generally, coal’s sale price is affected by its thermal value, together with its chemical composition and other properties such as moisture, ash and sulfur. Sale prices are also affected by general market conditions and supply and demand. Corresponding to the general slowdown of the Chinese economy, demand for raw coal dropped especially since the second half of fiscal 2013.

Washed Coal Sales

Washed coal sales for the last two fiscal years in volume, dollar amount and as a percentage of our total revenue, and the weighted average selling price per metric ton for each fiscal year, are as follows:

| | | Washed Coal Sales | |

Fiscal

Year | | Annual Sales

(metric tons) | | | Annual Sales ($) | | | % of Revenue | | | Weighted

Average

Sale Price Per

Metric Ton ($) | |

| 2012 | | | 183,903 | | | $ | 32,867,839 | | | | 42 | % | | $ | 179 | |

| 2013 | | | 132,930 | | | $ | 24,272,969 | | | | 36 | % | | $ | 183 | |

In addition to general market conditions and supply and demand, washed coal’s sale price is heavily dependent on its quality and composition. Like raw coal, demand for washed coal was weak in fiscal 2013, although demand for high quality washed coal remained fairly robust.

Coal Tar Sales

Coal tar sales for the last two fiscal years ended in volume, dollar amount and as a percentage of our total revenue, and the weighted average selling price per metric ton for each fiscal year, are as follows:

| | | Coal Tar Sales | |

| Fiscal Year | | Annual Sales

(metric tons) | | | Annual Sales ($) | | | % of Revenue | | | Weighted

Average

Price Per

Metric Ton ($) | |

| 2012 | | | 7,648 | | | $ | 1,946,314 | | | | 2 | % | | $ | 254 | |

| 2013 | | | 6,433 | | | $ | 1,719,416 | | | | 3 | % | | $ | 267 | |

Because we currently lack a separate process to refine and prepare coal tar as a homogenous product, the quality and characteristics of coal tar that we produce can vary, which in turn affect our sale price. General market conditions and supply and demand also affect sale price.

Customers

We sell our products only in China. The following customers each accounted for 10% or more of our fiscal 2013 revenue:

| Customer | | Sales to Customer

($) | | | Sales to Customer

as a % of Revenue | |

| Wuhan Railway Zhongli Group | | $ | 16.54 million | | | | 24.7 | % |

| Zhengzhou Baonuo Trading Ltd. | | $ | 13.85 million | | | | 20.7 | % |

| Hongxin Industrial Co., Ltd. | | $ | 10.49 million | | | | 15.7 | % |

| Daye Special Steel Ltd. | | $ | 9.85 million | | | | 14.7 | % |

The largest customer of each principal product for fiscal 2013 is as follows:

| Customer | | Product | | % of Product Bought by

Customer | |

| Wuhan Railway Zhongli Group | | Coke | | | 44.3 | % |

| Zhengzhou Baonuo Trading Ltd. | | Coal* | | | 50.0 | % |

| Wang Fashun | | Coal tar | | | 24.9 | % |

| * | Includes both raw and washed coal. |

None of these customers are related to or affiliated with us. Our sales personnel conduct routine visits to our customers. We have long-standing relationships with our customers, and management believes that our relationships with them are stable.

Transportation and Distribution

We own and operate a private rail track of 4.5 kilometers in length that connects the Baofeng plant to the national railway system at both the East Pingdingshan Railway Station and the Baofeng Railway Station. Industrial loaders load coal and coke from our platform onto railcars to be transported to customers primarily in central and southeastern China in the provinces of Henan, Hubei, Hunan and Fujian. We also truck coke from the Hongfeng plant to our platform for loading. Our private railway affords us some measures of control over transportation cost and delivery execution. See also “Property, Plant and Equipment – Railway Assets” below.

Customers can also arrange for trucks to take delivery from both plants.

Competitors

We compete primarily with coal and coke producers in the central, eastern and southern regions of China. Coke competitors range from Shanxi Coking Co., Ltd., a national coke producer, to local operations like Hongyue Coke Factory, Dongxin Coke Factory and Hongjiang Coke Factory. We also compete with China Pingmei Shenma Group (“China Pingmei”), a Pingdingshan-based state-owned coke and coal producer with similar product-mix as us. China Pingmei is also the largest regional coal producer and one of Henan’s six SOE consolidators, all of whom are our competitors in the coal market. Competitive factors include geographic location, quality (i.e. thermal value, ash and sulfur content, washing and processing, and other characteristics), and reliability of delivery. The mining moratorium has also given the six SOE consolidators a competitive advantage as their mines are the only ones currently operating in Henan.

Suppliers

We purchase from various suppliers within China. The following suppliers each accounted for 10% or more our total purchases for fiscal 2013:

| Supplier | | Materials

Supplied | | Amount of Purchase

($) | | | % of Total

Purchases | |

| Gansu Yiaojie Coal & Electricity Group Ltd. | | washed coal | | | 7,870,721 | | | | 14.1 | % |

| Henan Shenhuo International Trade Ltd. | | washed coal | | | 6,962,315 | | | | 12.5 | % |

| Ruzhou Shi Xiaotun Jialingnan mining Ltd. | | washed coal | | | 5,974,658 | | | | 10.7 | % |

None of these suppliers are related to or affiliated with us.

As with our coke and coal sales, we meet our washed coal needs by entering into non-binding annual letters of intent with suppliers that set forth supply quantities, proposed pricing and monthly delivery schedules at the beginning of the year. Subject to changes in delivery quantity and pricing, which is based on the open market price at the time of delivery and agreed to by the parties, we generally make payment upon each delivery throughout the year.

We believe that we have established stable cooperative relationships with our suppliers. In light of the mining moratorium, we have been sourcing coal from outside of Henan. During the 2013 fiscal year, about 47.6% of our coal purchases were from outside Henan, with the remaining from SOEs in Henan whose mining operations have not been affected by the ongoing mining moratorium and consolidation.

Our other principal raw materials include water and electricity. The Baofeng plant gets its water without charge in the form of treated underground water from the operator of the nearby Hangzhuang coal mines, and its electricity from our own power stations (see “Electricity Generation” above). The Hongfeng plant, on the other hand, buys water on the market and electricity from a local state-owned utility. We also require wood and steel for our operations, and source these materials from nearby suppliers on a per purchase order basis. These materials are readily available and there is no shortage of suppliers to choose from.

Employees

The following table sets forth the number of our employees for each of our areas of operations and as a percentage of our total workforce as of June 30, 2013:

| | | Number of

Employees | | | % of

Employees | |

| Coal-related operations | | 19 | | | 4 | % |

| Coke-related operations | | | 391 | | | | 79 | % |

| Sales and marketing | | | 4 | | | | 1 | % |

| Administrative (including management) | | | 86 | | | | 16 | % |

| TOTAL | | | 500 | | | | 100.0 | % |

Both the Baofeng plant and Hongfeng plant operates year round in three shifts of eight hours per day. Although mining operations are currently shut down, we have staff at the mine sites for necessary maintenance and repairs during the moratorium. Once our coal mines can resume full operations, we anticipate operating in three shifts of eight hours per day. In compliance with theEmployment Contract Law of PRC, we have written contracts with all of our employees. We consider our relationship with our employees to be good.

Research and Development

On June 18, 2013, Pingdingshan Municipal Science and Technology Bureau issued us a “Certificate of Achievement” in connection with advances that we made in coke sintering. Sintering is the process of bonding small particles with heat that does not reach the melting point of such particles. We developed and completed initial testing of a new sintering fuel in November 2012, and commenced trial production in December 2012. After preliminary testing followed by a full evaluation, experts at Henan Province Science and Technology Bureau determined that our sintering fuel, when compared to conventional sintering fuel, can reduce dust and sulfur dioxide emissions at various stages of steel production. In connection with our Certificate of Achievement, we are also approved to commercially produce our sintering fuel, although we have not done so as of the date of this Report.

In addition, we are currently working with the Chinese Academy of Agricultural Sciences to evaluate the economic feasibility of extracting humic acid from mid-coal and coal slurries.

Intellectual Property

We have no patents, trademarks, licenses, franchises, or royalty arrangements.

Relevant PRC Regulations

We operate in an industry that is highly regulated by local, provincial and central government authorities in the PRC. Applicable regulations include those relating to safety, production, environmental, energy use and labor. While it is not practicable to summarize all applicable laws, the following is a list of names of significant laws and regulations that apply to our business:

Laws and regulations concerning safety of coal mines:

| · | Law of the People’s Republic of China on the Coal Industry |

| · | Regulation on Work Safety Licenses |

| · | Regulations on Administration of Village’s and County’s Coal Mines |

| · | Production Safety Law, which applies to production activities in general |

| · | Law of the Coal Industry |

| · | Regulations on Coal Mine Safety Supervision and Inspection |

| · | Regulations on Coal Mine Explosives Control |

| · | Special Provisions for the Prevention of Coal Mine Incidents |

| · | Requirements for Basic Production Conditions for Coal Mines |

| · | Penalties for Coal Mine Safety Violations |

| · | Penalties for Production Safety Violations |

Laws and regulations concerning environmental protection and energy conservation:

| · | Law of the Prevention and Control of Solid Waste Environmental Pollution, which applies to entities whose production activities may generate pollutive solid waste |

| · | Law of the Prevention and Control of Atmospheric Pollution, which set restrictions in coal burning and emissions that cause air pollution |

| · | Mineral Resources Law, which regulates the extraction of mineral resources including coal |

| · | Law Regarding the Prevention and Control of Water Pollution, which regulates pollution of underground water caused by mining activities |

| · | Land Administration Law, which restricts mining activities on agricultural land |

| · | Law of Prevention and Control of Radioactive Pollution, which regulates and prohibits the release of radioactive pollution caused by certain mining activities |

| · | Laws of Water and Soil Conservation, which regulates mining activities with the aim of preventing soil erosion |

| · | Environmental Protection Law, which contains certain general provisions that apply to the operation of coal mines |

Laws and regulations concerning labor:

| · | Labor Law, which protects workers, and contains provisions that apply to a broad range of industries including the mining industry |

| · | Labor Contract Law of the People’s Republic of China and its implementation, which protect workers, and contains laws that apply to a broad range of industries including the mining industry |

Environmental Protection Measures

We incorporate measures to reduce the environmental impacts of our operations. Our large-sized furnace reduces the frequency of coal loading and trundling, thereby reducing the amount of dust and soot that is generated. We capture coal gas emitted during the coking process to generate electricity which we use in our operations. We also recycle water - water that is used for coal washing is treated to remove phenol and other contaminants, and then re-used in the coal washing operation. We also use recycled water, in the form of treated underground water, to quench coke and for our power stations, which is provided without cost by the nearby Hanzhuang coal mines, which mining rights are owned and operated by unrelated third parties. Additionally, we use sound insulation to reduce noise pollution, and we plant vegetation throughout our plant to help mitigate the environmental impact of our operations.

Safety

Under PRC law, companies with mining operations are required to report violations or mining incidents and casualties to the government authorities. Since inception, except for ordinary and minor injuries, we have suffered no major accidents and no casualties in connection with our mining operations, and have not suffered any reportable incident. In addition, mining companies are subject to random and periodic safety inspections by government mine regulators. Since inception, we have not been found to be in material violation of any mining regulations. As we have no record of violations or mining incidents, management considers our safety record to be excellent. See also “Our Products and Operations – Coal – Coal Mining Moratorium” above.

Property, Plant and Equipment

The location of Pingdingshan, where we are based, is illustrated below:

The locations of our executive office, current coking plant and coal mines, are all in and around Pingdingshan, and are illustrated below:

Coal Mines and Production Facilities

The description below is based on operations prior to the mining moratorium (see “Our Products and Operations – Coal – Coal Mining Moratorium” above):

All four coal mines that we currently control are located at Baofeng County in the central part of Henan Province and are in close proximity to one another as well as to roadways. All are underground mines, and the “room-and-pillar” method is used to extract coal. Under such method, a coal stratum is divided into horizontal planes and the coal is removed from each plane while leaving “pillars” of un-mined materials as supports, working from the uppermost plane down. Each plane is further divided into grids to determine the optimal pillar placements. Drilling and blasting techniques are used to extract the coal.

Raw coal would be loaded and transported by a chain conveyor into crates which are carried out to the surface by an electrical winch. Each crate carries approximately 2.5 metric tons, and approximately 400 crates would be carried to the surface during each 8-hour mining shift. Rock material is used for floor ballast with the excess sent to the surface for disposal. Air compressors would provide for underground air tool use. Electrical power comes from our own power stations as well as the state grid, and supplied down mineshafts through a double-circuit cable designed to mitigate and circumvent potential power disruptions.

Normal water inflow into the mines would be controlled by a system of ditches, sumps, pumps and drainpipes installed throughout the mine tunnels. Each mine’s ventilation system includes an exhaustive fan on the surface of the main incline. Auxiliary fans would be used as needed.

The principal pieces of equipment used in our mining operations, including safety system, underground transportation system and loading system, are manufactured in the PRC, and they generally have an estimated useful life of 15 years. Once the mining moratorium is lifted and we are able to resume operations, we currently estimate the total annual operating costs for the four coal mines to be approximately $45 million, or $50 per metric ton of coal produced, based on an average output of 900,000 metric tons per year in the aggregate.

The extracted coal would be trucked to the Baofeng plant (approximately 1.5 kilometers from Hongchang coal mine) for washing and sorting. Samples would be taken prior to and after washing to analyze and determine coking suitability based primarily on moisture, ash, sulfur and volatile contents.

We intend to transfer all of our coal mining operations to Hongyuan CSG. As of the date of this Report, however, such transfers have not been carried out.

Hongchang Coal Mine

Hongchang coal mine originally consisted of four underground mines: Yongshun mine, Liangshuiquan mine, Zhaoxi secondary mine and Zhaozhuang Tanglishu mine. These mines were positioned adjacent to one another, and although once owned and operated by different parties, these mines made use of common passageways and mine shafts. In June 2005 we acquired Yongshun mine (built in 1996) and Zhaoxi secondary mine (built in 1988) from Quinmin Chen. Also in June 2005, we acquired Liangshuiquan mine (built in 1984) from Minjie Li. In April 2005 we acquired Zhaozhuang Tanglishu mine (built in 1984) from Liuqing He and Jiti Li. We assumed the ongoing mining operations, and initiated the consolidation, of these mines, which consolidation process was completed in 2006. Since acquisition in 2005, we have extracted a total of 709,202 metric tons of coal from Hongchang coal mine, and prior to such time, its predecessor owners extracted a total of 345,000 metric tons. Coal extracted from Hongchang coal mine consists of bituminous coal, and based on historical mining activities, approximately 75% of the coal extracted typically possesses properties that meet the requirements for coking (metallurgical) coal.

Hongchang coal mine is currently not operational (see “Our Products and Operations – Coal – Coal Mining Moratorium” above).

Shuangrui Coal Mine

Shuangrui coal mine originally consisted of five underground mines: Zhaozhuang mine (built in 1970), Longsheng mine (built in 1995), New Zhaozhuang mine (built in 2000), Jinpo mine (built in 1999) and West Zhaozhuang mine (built in 1998). The first on-site geological survey for mining purpose of these mines was conducted in 1950s, with several subsequent surveys carried out from 1960s to 2001. Hongchang Coal currently holds 100% of the mine’s operator, Shuangrui Coal (see “History and Corporate Structure – Hongli” above). Coal extracted from Shuangrui coal mine consists of bituminous coal, and based on historical mining activities, approximately 75% of the coal extracted typically possesses properties that meet the requirements for coking (metallurgical) coal.

Shuangrui coal mine is currently not operational (see “Our Products and Operations – Coal – Coal Mining Moratorium” above). We also plan to dissolve Shuangrui Coal and consolidate its coal mine under Hongchang Coal (see “History and Corporate Structure – Hongli” above). Once such consolidation is completed, Shuangrui coal mine will become part of Hongchang coal mine.

Xingsheng Coal Mine

Xingsheng coal mine originally consisted of No. 2 Qingnian mine (operation started in 2000) and No. 3 Shuangyushan mine (operation started in 1998). The first on-site geological survey for mining purpose of these mines was conducted in 1958. The coal extracted from Xingsheng coal mine is bituminous coal which is suitable for coke production. In August 2010, we entered into an agreement to acquire 60% of the mine’s operator, Xingsheng Coal, and the registration for the transfer of such equity interests to Hongli was completed on May 20, 2011. Coal extracted from Xingsheng coal mine consists of bituminous coal, and based on historical mining activities, approximately 75% of the coal extracted typically possesses properties that meet the requirements for coking (metallurgical) coal.

Xingsheng coal mine is currently not operational (see “Our Products and Operations – Coal – Coal Mining Moratorium” above).

Shunli Coal Mine

Shunli coal mine originally consisted of Dongfanghong mine (built in 1995) and Zhenxing mine (built in 1998). The first on-site geological survey for mining purpose of these mines was conducted in 1950s. In May 2011, we entered into an agreement to acquire 100% of the mine’s operator, Shunli Coal, and the registration for the transfer of such equity interests to Hongchang was completed on May 20, 2011. Coal extracted from Shunli coal mine consists of bituminous coal, and based on historical mining activities, approximately 75% of the coal extracted typically possesses properties that meet the requirements for coking (metallurgical) coal.

Shunli coal mine is currently not operational (see “Our Products and Operations – Coal – Coal Mining Moratorium” above). We are also in the process of consolidating Shunli coal mine under Hongchang Coal (see “History and Corporate Structure – Hongli” above). Once consolidation is completed, Shunli coal mine will become part of Hongchang coal mine.

Additional information regarding these mines is listed below:

| | | Hongchang Mine

(6) | | | Shuangrui Mine (9) | | | Xingsheng Mine

(12) | | | Shunli Mine (15) | |

| Background data: | | | | | | | | | | | | | | | | |

| Commencement of construction | | | 1984 | | | | 1970 | | | | 1970 | | | | 1995 | |

| Commencement of commercial production | | | 1987 | | | | 1970 | | | | 1998 | | | | 1998 | |

| Coalfield area (square kilometers) | | | 0.65 | | | | 0.47 | | | | 0.19 | | | | 0.08 | |

| Reserve data:(1) | | | | | | | | | | | | | | | | |

| Total in-place proven and probable reserves (metric tons) (2) | | | 2,479,000 | (7) | | | 1,674,000 | (10) | | | 2,475,000 | (13) | | | 1,373,300 | (16) |

| Recoverable reserves (metric tons) (3) | | | 1,215,100 | | | | 1,539,000 | | | | 2,233,000 | | | | 1,122,000 | |

| Coal washing recovery rate (%) (4) | | | 75 | | | | 75 | | | | 75 | | | | 75 | |

| Depth of mining (meters underground) | | | 10 – 210 | | | | 40 – 270 | | | | 80 - 90 | | | | 100 - 130 | |

| Average thickness of main coal seams (meters) | | | Seam B1: 1.14 Seam A4: 5.50 (8) | | | | 6.78 | | | | Seam A4: 0.70 – 1.08 Seam B1: 4.50 – 14.40 (14) | | | | Seam A4: 2.0 Seam A6: 1.6 Seam B1: 6.5 – 10.2 (17) | |

| Type of coal | | | Thermal/Metallurgical | | | | Thermal/Metallurgical | | | | Thermal/Metallurgical | | | | Thermal/Metallurgical | |

| Assigned/unassigned (5) | | | Assigned | | | | Assigned | | | | Assigned | | | | Assigned | |

| Sulfur content (%) | | | Seam B1: 2.64 Seam A4: 0.55 | | | | Seam B1: 0.55 (11) | | | | Seam A4: 4.90 Seam B1: 0.55 | | | | Seam A4: 1.50 Seam A6: 0.87 Seam B1: 0.55 | |

| Water content (%) | | | Seam B1: 0.83 Seam A4: 1.5 | | | | Seam B1: 1.5 | | | | N/A | | | | Seam A4: 1.50 Seam A6: 1.08 Seam B1: 1.50 | |

| Ash content (%) | | | Seam B1: 15.3 Seam A4: 14.0 | | | | Seam B1: 14 | | | | Seam A4: 18.64 Seam B1: 14.00 | | | | Seam A4: 16 Seam A6: 33.44 Seam B1: 15 | |

| Volatility content (%) | | | Seam B1: 32.5 Seam A4: 29.0 | | | | Seam B1: 29 | | | | Seam A4: 38.45 Seam B1: 33.15 | | | | Seam A4: 32 Seam A6: 20.59 Seam B1: 29 | |

| Thermal Value (megajoules per kilogram) | | | 31.9 | | | | 28.5 | | | | 31.2 | | | | Seam A4: 30.10 Seam A6: 18.56 Seam B1: 31.30 | |

| Production data:(metric tons) | | | | | | | | | | | | | | | | |

| Designed raw coal production capacity (per year) | | | 150,000 | | | | 150,000 | | | | 150,000 | | | | 150,000 | |

| Raw coal production: | | | | | | | | | | | | | | | | |

| For the year ended June 30, 2012 | | | 19,160 | | | | 0 | | | | 0 | | | | 0 | |

| As of June 30, 2013 | | | 0 | | | | 0 | | | | 0 | | | | 0 | |

| Cumulative raw coal production as of June 30, 2013 | | | 709,202 | | | | 301,020 | | | | 367,981 | | | | 300,000 | |

| (1) | The reserve data including (i) total in-place proven and probable reserves, (ii) mining and coal preparation plant recovery rates; (iii) depth of mine; and (iv) average thickness of main coal seam are based on the relevant information from the mining report of each mine issued by our provincial mining authorities, the Regional Geological Survey Team of the Henan Bureau of Geology and Mineral Exploration and Development, and records of the Company. Non-accessible reserves are defined as the portion of identified resources estimated to be not accessible by application of one or more accessibility factors within an area. We note that the degree of assurance between what would meet the definition of “proven reserves” on the one hand, and “probable reserves” on the other hand, cannot be readily defined. Accordingly, pursuant to the SEC’s Industry Guide 7 – Description of Property by Issuers Engaged or to be Engaged in Significant Mining Operations, in the table above we report proven and probable reserves on a combined basis. |

| (2) | In-place reserves refer to coal in-situ prior to the deduction of pillars of support, barriers or constraints. |

| (3) | Recoverable reserves refer to identified coal reserves that are technologically and economically feasible to extract prior to the deduction of losses during extraction. We note that the estimated recoverable reserves is a government estimate created and used by local mining authorities to determine permissible extraction rates, the duration of our mining license, and to approve mine designs and that it is subject to revision. We also utilize this estimate for accounting purposes, to amortize our mining rights. Currently estimated recoverable coal may not necessarily be consistent with the results of future mining, engineering and feasibility studies or reports. |

| (4) | Coal washing recovery rate refers to the rate of recovery of coal in the production of our washed coal products. |

| (5) | “Assigned” reserves refer to coal which has been committed to a particular mining complex (mine shafts, mining equipment, and plant facilities), and all coal which has been leased by the company to others. “Unassigned” reserves refer to coal which has not been committed, and which would require new mineshafts, mining equipment, or plant facilities before operations could begin on the property. |

| (6) | The mining report of Hongchang coal mine is dated November 2005 (the “Hongchang Mining Report”). |

| (7) | According to the Hongchang Mining Report, Hongchang coal mine was initially found to have total estimated reserves and resources of 2.81 million metric tons. 334,000 metric tons were removed during exploration, leaving approximately 2.47 million metric tons of estimated reserves and resources. |

| (8) | Hongchang coal mine contains two major economically exploitable coal seams, referred to in this table as the “Seam B1” and the “Seam A4”. |

| (9) | The mining report of Shuangrui coal mine is dated February 17, 2006 (the “Shuangrui Mining Report”). |

| (10) | According to the Shuangrui Mining Report, Shuangrui coal mine was initially found to have total estimated reserves and resources of 4 million metric tons. 2.33 million metric tons were removed during exploration, leaving approximately 1.67 million metric tons of estimated reserves and resources. |

| (11) | Shuangrui Ming contains one major economically exploitable coal seam, referred to in this table as the “Seam B1.” |

| (12) | The mining report of Xingsheng coal mine is dated April 10, 2006 (the “Xingsheng Mining Report”). |

| (13) | According to the Xingsheng Mining Report, Xingsheng coal mine was initially found to have total estimated reserves and resources of 2.74 million metric tons. 260,000 metric tons were removed during exploration, leaving approximately 2.48 million metric tons of estimated reserves and resources. |

| (14) | Xingsheng coal mine contains two major economically exploitable coal seams, referred to in this table as the “Seam A4” and the “Seam B1.” |

| (15) | The mining report of Shunli coal mine is dated March 2, 2006 (the “Shunli Mining Report”). |

| (16) | According to the Shunli Mining Report, Shunli coal mine was initially found to have total estimated reserves and resources of 1.44 million metric tons. 647,000 metric tons were removed during exploration, leaving approximately 1.37 million metric tons of estimated reserves and resources. |

| (17) | Shunli coal mine contains three major economically exploitable coal seams, referred to in this table as the “Seam A4”, the “Seam A6”, and the “Seam B1.” |

Mining Rights

Like all coal mines in the PRC, the four mines that we control, including the mine sites and the underlying coal and other minerals, are state-owned. Accordingly, the amount of coal that we can extract from each of mine is based on the mining permit issued to the mine’s operator by the Henan Province Bureau of Land and Resources (the “Henan Land Resources Bureau”). For example, we extract coal from Hongchang coal mine based on the permit issued to Hongchang Coal. The permit is issued when the Henan Land Resources Bureau approves the reserves appraisal report submitted by authorized mining engineers. The amount of coal that can be extracted under the permit represents what we can economically and legally extract under applicable PRC law and as determined by the Henan Land Resources Bureau.

The table below lists our current mining permits:

| | | Hongchang coal

mine | | Shuangrui coal

mine | | Xingsheng coal

mine | | Shunli coal

mine | |

| Issuance date | | July 6, 2007 | | June 4, 2007 | | May 30, 2007 | | November 17, 2009 | |

| Expiration date (unless extended) | | September 6, 2013 (1) | | October 4, 2011 (1) | | July 30, 2012 (1) | | September 2011 (1) | |

| Permitted mining amount (metric tons per year) | | 150,000 | | 150,000 | | 150,000 | | 150,000 | |

| (1) | These permits have not been renewed in light of the ongoing mining moratorium (see “Our Products and Operations – Coal – Coal Mining Moratorium” above). In addition, we are in the process of consolidating Shunli coal mine under Hongchang Coal, and plans to do the same with Shuangrui coal mine (see “History and Corporate Structure – Hongli” above). Once consolidation is completed, we will have only one permit to mine all three mine sites. |

Under our current mining permits, we are theoretically allowed to extract up to 8,001,300 metric tons of coal from the four coal mines, representing their aggregate estimated in-place proven and probable reserves. Out of such proven and probable reserves, 6,109,100 metric tons are recoverable according to the reserves appraisal reports for these mines.

We are also required to pay for the amount of coal that we wish to extract under each mining permit, generally determined on a per metric ton basis based on proven and probable reserves (rather than actual recoverable coal), as well as prevailing market prices as determined by the Henan Land Resources Bureau. In the event that further exploration results in an increase of estimated proven and probable reserves (and we desire to extract such additional reserves), or if we desire to continue mining beyond a mining permit’s expiration date, we must obtain an additional permit from the Henan Land Resources Bureau and may be subject to additional fees to acquire such permit or to modify an existing permit. We expect that the cost of further exploration in and around the four coal mines would be borne by us. We have been conducting additional geological studies around Hongchang coal mine, and expect to report our findings to the local mining authority. We note that the estimated 6,109,100 metric tons of recoverable reserves for the four coal mines in the aggregate is a government estimate created and used by local mining authorities to determine permissible extraction rates and the duration of our mining permits, and to approve mine designs, and is subject to revision. Currently estimated recoverable coal may not necessarily be consistent with the results of future mining, engineering and feasibility studies or reports.

In August 2007, we made a partial payment of approximately $0.6 million (RMB 4.46 million) to extract from Hongchang coal mine its 2,479,000 metric tons of total reserves. A final payment of approximately $0.4 million (RMB 2.7 million) is anticipated to become due when charged by the Henan Land Resources Bureau. The exact amount of this final payment, however, will depend on market prices as determined by our negotiations with the Henan Land Resources Bureau, as well as any new regulations after the consolidation program ends.

Payments in connection with the mining permits for Shuangrui, Shunli and Xingsheng coal mines were made in full in 2005 by their then owners.

Railway Assets

Currently, we have rail assets consisting of approximately 4.5 kilometers of special purpose transportation railway tracks that serve to facilitate the transportation of coal and coke from our site to the national railway system, and ultimately to our customers. We do not own any railcars and locomotives, but instead pay access fees to the Zhengzhou Railway Bureau for the use of government-owned and operated railcars and locomotives. These railcars are loaded with coal and coke products at our yard for delivery through the national railway system.

ITEM 1A.RISK FACTORS