Use these links to rapidly review the document

TABLE OF CONTENTS

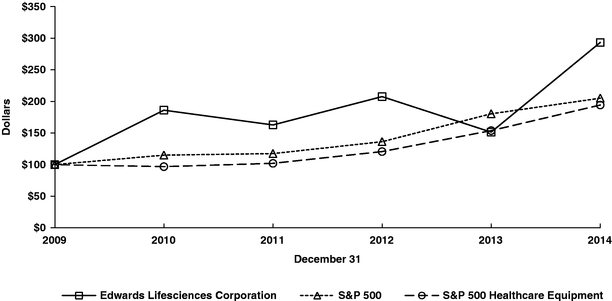

Item 8. Financial Statements and Supplementary Data

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| | |

| (Mark One) | | |

ý |

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Fiscal Year Ended December 31, 2014 |

OR |

o |

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Transition Period From to |

Commission File Number 1-15525 |

EDWARDS LIFESCIENCES CORPORATION

(Exact name of registrant as specified in its charter)

| | |

| Delaware | | 36-4316614 |

(State or other jurisdiction of

incorporation or organization) | | (I.R.S. Employer

Identification No.) |

One Edwards Way, Irvine, California 92614

(Address of principal executive offices) (ZIP Code) |

(949) 250-2500

Registrant's telephone number, including area code |

Securities registered pursuant to Section 12(b) of the Act: |

|

Name of each exchange on which registered: |

| Common Stock, par value $1.00 per share | | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act:None |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined by Rule 405 of the Securities Act. Yes ý No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Exchange Act. Yes o No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ý No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ý

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer," and "smaller reporting company" in Rule 12b-2 of the Exchange Act. (Check one):

| | | | | | |

| Large accelerated filerý | | Accelerated filero | | Non-accelerated filero

(Do not check if a smaller reporting company) | | Smaller Reporting Companyo |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No ý

The aggregate market value of the registrant's common stock held by non-affiliates as of June 30, 2014 (the last trading day of the registrant's most recently completed second quarter): $9,013,877,277 based on a closing price of $85.84 of the registrant's common stock on the New York Stock Exchange. This calculation does not reflect a determination that persons are affiliates for any other purpose.

The number of shares outstanding of the registrant's common stock, $1.00 par value, as of January 31, 2015, was 107,839,918.

Documents Incorporated by Reference

Portions of the registrant's proxy statement for the 2015 Annual Meeting of Stockholders (to be filed within 120 days of December 31, 2014) are incorporated by reference into Part III, as indicated herein.

Table of Contents

EDWARDS LIFESCIENCES CORPORATION

Form 10-K Annual Report—2014

Table of Contents

| | | | |

PART I | | | | |

Item 1. | | Business | | 1 |

Item 1A. | | Risk Factors | | 10 |

Item 1B. | | Unresolved Staff Comments | | 20 |

Item 2. | | Properties | | 21 |

Item 3. | | Legal Proceedings | | 21 |

Item 4. | | Mine Safety Disclosures | | 21 |

PART II | | | |

|

Item 5. | | Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | | 22 |

Item 6. | | Selected Financial Data | | 24 |

Item 7. | | Management's Discussion and Analysis of Financial Condition and Results of Operations | | 24 |

Item 7A. | | Quantitative and Qualitative Disclosures About Market Risk | | 38 |

Item 8. | | Financial Statements and Supplementary Data | | 41 |

Item 9. | | Changes in and Disagreements With Accountants on Accounting and Financial Disclosure | | 93 |

Item 9A. | | Controls and Procedures | | 93 |

Item 9B. | | Other Information | | 93 |

PART III | | | |

|

Item 10. | | Directors, Executive Officers and Corporate Governance | | 94 |

Item 11. | | Executive Compensation | | 94 |

Item 12. | | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | | 94 |

Item 13. | | Certain Relationships and Related Transactions, and Director Independence | | 94 |

Item 14. | | Principal Accounting Fees and Services | | 94 |

PART IV | | | |

|

Item 15. | | Exhibits, Financial Statement Schedules | | 95 |

| | Signatures | | 99 |

Table of Contents

PART I

Item 1. Business

This report contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. We intend the forward-looking statements contained in this report to be covered by the safe harbor provisions of such Acts. All statements other than statements of historical fact in this report or referred to or incorporated by reference into this report are "forward-looking statements" for purposes of these sections. These statements include, among other things, any predictions of earnings, revenues, expenses or other financial items, plans or expectations with respect to development activities, clinical trials or regulatory approvals, any statements of plans, strategies and objectives of management for future operations, any statements concerning our future operations, financial conditions and prospects, and any statements of assumptions underlying any of the foregoing. These statements can sometimes be identified by the use of the forward-looking words such as "may," "believe," "will," "expect," "project," "estimate," "should," "anticipate," "plan," "goal," "continue," "seek," "pro forma," "forecast," "intend," "guidance," "optimistic," "aspire," "confident," other forms of these words or similar words or expressions or the negative thereof. Investors are cautioned not to unduly rely on such forward-looking statements. These forward-looking statements are subject to substantial risks and uncertainties that could cause our results or future business, financial condition, results of operations or performance to differ materially from the our historical results or experiences or those expressed or implied in any forward-looking statements contained in this report. See "Risk Factors" below for a further discussion of these risks, as well as our subsequent reports on Forms 10-Q and 8-K. These forward-looking statements speak only as of the date on which they are made and we do not undertake any obligation to update any forward-looking statement to reflect events or circumstances after the date of the statement. If we do update or correct one or more of these statements, investors and others should not conclude that we will make additional updates or corrections.

Overview

Edwards Lifesciences Corporation is focused on technologies that treat structural heart disease and critically ill patients. A pioneer in the development and commercialization of heart valve therapies, we are the world's leading manufacturer of heart valve systems and repair products used to replace or repair a patient's diseased or defective heart valve. We are also a global leader in hemodynamic monitoring systems used to measure a patient's cardiovascular function in the hospital setting.

Cardiovascular disease is the number-one cause of death in the world, and is the top disease in terms of health care spending in nearly every country. Cardiovascular disease is progressive in that it tends to worsen over time and often affects an individual's entire circulatory system.

Patients undergoing treatment for cardiovascular disease may be treated using a variety of our products and technologies. For example, an individual with a heart valve disorder may have a faulty valve. A clinician may elect to remove the valve and replace it with one of our bioprosthetic surgical tissue heart valves, surgically re-shape and repair the faulty valve with an Edwards Lifesciences annuloplasty ring, or deploy an Edwards Lifesciences transcatheter valve via a minimally invasive catheter-based system. Patients in the hospital setting, including high-risk patients in the operating room or intensive care unit, are candidates for having their cardiac function or fluid levels monitored by our Critical Care products.

Segment and Geographical Information

We conduct operations worldwide and are managed in the following geographical regions: United States, Europe, Japan, and Rest of World. All regions sell products that are used to treat advanced cardiovascular disease. Additional segment and geographical information is incorporated herein by reference to Note 18 to the "Consolidated Financial Statements." See also the risk factor "Our business is subject to economic, political, and other risks associated with international sales and operations, including risks arising from currency exchange rate fluctuations" in Part I, Item 1A, "Risk Factors," for information regarding risks involving our international operations.

1

Table of Contents

Corporate Background

Edwards Lifesciences Corporation was incorporated in Delaware on September 10, 1999. Unless otherwise indicated or otherwise required by the context, the terms "we," "our," "it," "its," "Company," "Edwards," and "Edwards Lifesciences" refer to Edwards Lifesciences Corporation and its subsidiaries.

Our principal executive offices are located at One Edwards Way, Irvine, California 92614. The telephone number at that address is (949) 250-2500. We make available, free of charge on our website located at www.edwards.com, our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and any amendments to those reports, as soon as reasonably practicable after filing such reports with the Securities and Exchange Commission ("SEC"). The contents of our website are not incorporated by reference into this report.

Edwards Lifesciences' Product and Technology Offerings

The following discussion summarizes the main areas of products and technologies we offer to treat advanced cardiovascular disease. These are categorized into three main areas: Transcatheter Heart Valve Therapy, Surgical Heart Valve Therapy, and Critical Care. For more information on net sales from these three main areas, see"Net Sales by Product Group" under "Management's Discussion and Analysis of Financial Condition and Results of Operations."

We are the global leader in heart valve therapy and the world's leading manufacturer of heart valves and repair products, which are used to replace or repair a patient's diseased or defective heart valve. We produce pericardial valves from biologically inert animal tissue sewn onto proprietary wireform stents.

Transcatheter Heart Valve Therapy

We have leveraged the knowledge and experience from our Surgical Heart Valve Therapy portfolio to optimize transcatheter heart valve replacement technology, designed for the nonsurgical replacement of heart valves. TheEdwards SAPIEN, Edwards SAPIEN XT, andEdwards SAPIEN 3 transcatheter aortic heart valves, and their respective delivery systems, are used to treat heart valve disease using catheter-based approaches for certain patients deemed at high risk for traditional open-heart surgery. Delivered while the heart is beating, these valves can enable patients to experience a better quality of life sooner than patients receiving traditional surgical therapies. We began offering our transcatheter heart valves to patients commercially in Europe in 2007, in the United States in 2011, and in Japan in 2013. As of December 31, 2014, our transcatheter aortic heart valves were available for sale in more than 65 countries. Supported by extensive customer training and service, and a growing body of compelling clinical evidence, ourSAPIEN family of transcatheter aortic heart valves are the most widely prescribed transcatheter heart valves in the world.

Sales of our transcatheter heart valves represented approximately 41%, 35%, and 29% of our net sales in 2014, 2013, and 2012, respectively.

Surgical Heart Valve Therapy

The core of our surgical tissue heart valve product line is theCarpentier-Edwards PERIMOUNT pericardial valve, including the line ofPERIMOUNT Magna Ease valves, the newest generation pericardial valves for aortic and mitral surgical replacement. With significant clinical data on durability and performance,PERIMOUNT valves are the most widely prescribed tissue heart valves in the world. In addition to its replacement valves, we pioneered and are the worldwide leader in heart valve repair therapies, including annuloplasty rings and systems. We have also developed theEDWARDS INTUITY Valve System, a minimally invasive aortic heart valve system designed to enable a faster procedure, shorter patient time on cardiopulmonary bypass and a smaller incision.

2

Table of Contents

Sales of our surgical tissue heart valve products represented approximately 31%, 34%, and 36% of our net sales in 2014, 2013, and 2012, respectively.

Cardiac surgeons and their patients increasingly are seeking less invasive approaches to aortic or mitral valve surgery, which can offer a number of potential benefits, including smaller incisions, less blood loss, quicker recoveries, and less scarring. Edwards Lifesciences offers a variety of systems used to enable minimal incision valve surgery where surgeons perform intricate procedures through small incisions. We are also a global leader in protection cannulae, which are used during cardiac surgery.

Critical Care

We are a world leader in hemodynamic monitoring systems used to measure a patient's heart function in surgical and intensive care settings. Hemodynamic monitoring enables a clinician to balance the oxygen supply and demand of a critically ill patient and plays an important role in enhancing surgical recovery by enabling appropriate tissue and organ perfusion, and ultimately patient outcomes and survival. Our hemodynamic monitoring technologies are used before, during, and after surgeries, such as open-heart, major vascular, major abdominal, neurological, and orthopedic surgical procedures, as well as for acutely ill patients with conditions such as sepsis, acute respiratory distress syndrome, and multi-organ failure.

We manufacture products to help clinicians make more informed fluid management decisions for their patients, including the minimally invasiveFloTrac continuous cardiac output monitoring system, and the non-invasiveClearSight hemodynamic monitor that provides real-time, beat-to-beat information. Our hemodynamic monitoring product line also includes theSwan-Ganz line of pulmonary artery catheters, thePreSep continuous venous oximetry catheter for measuring central venous oxygen saturation, and theVolumeView sensor-catheter set that measures a critically ill patient's volumetric hemodynamic parameters. OurEV1000 clinical monitoring platform displays a patient's physiologic status and integrates many of our sensors and catheters into one intuitive platform.

We are also the global leader in disposable pressure monitoring devices and innovative closed blood sampling systems to help protect both patients and clinicians from the risk of infection.

Sales of our core hemodynamic products represented approximately 15%, 17%, and 19% of our net sales in 2014, 2013, and 2012, respectively.

We manufacture and sell a variety of peripheral vascular products used to treat endolumenal occlusive disease, including theFogarty line of embolectomy catheters, which has been an industry standard for removing blood clots from peripheral blood vessels for more than 40 years.

Competition

The medical device industry is highly competitive. We compete with many companies, including divisions of companies much larger than us and smaller companies that compete in specific product lines or certain geographies. Furthermore, new product development and technological change characterize the areas in which we compete. Our present or future products could be rendered obsolete or uneconomical as a result of technological advances by one or more of our present or future competitors or by other therapies, including drug therapies. We must continue to develop and commercialize new products and technologies to remain competitive in the cardiovascular medical device industry. We believe that we compete primarily on the basis of clinical superiority supported by extensive data, and innovative features that enhance patient benefit, product performance, and reliability. Customer and sales support, and cost-effectiveness are additional aspects of competition.

The cardiovascular segment of the medical device industry is dynamic and subject to significant change due to cost-of-care considerations, regulatory reform, industry and customer consolidation, and evolving patient needs. The ability to provide products and technologies that demonstrate value and improve clinical outcomes is becoming increasingly important for medical device manufacturers.

3

Table of Contents

We believe that we are a leading global competitor in each of our product lines. In Surgical and Transcatheter Heart Valve therapies, our primary competitors include Medtronic, Inc., St. Jude Medical, Inc., and Sorin Group. In Critical Care, we compete primarily with a variety of companies in specific product lines including ICU Medical, Inc., PULSION Medical Systems SE, a subsidiary of Getinge AB, and LiDCO Group PLC.

Sales and Marketing

We have a number of broad product lines that require a sales and marketing strategy tailored to our customers in order to deliver high-quality, cost-effective products and technologies to all of our customers worldwide. Our portfolio includes some of the most recognizable product brands in cardiovascular devices today. To help broaden awareness of our products and technologies, we conduct educational symposia and provide training to our customers.

Because of the diverse global needs of the population that we serve, our distribution system consists of a direct sales force as well as independent distributors. We are not dependent on any single customer and no single customer accounted for 10% or more of our net sales in 2014.

Where we choose to market our products is also influenced by the existence of, or potential for, adequate reimbursement to hospitals by national healthcare systems. Sales personnel work closely with the customers who purchase our products, which primarily include physicians, nurses, and other clinical personnel, but can also include decision makers such as material managers, biomedical staff, hospital administrators, purchasing managers, and ministries of health. Also, for certain of our products and where appropriate, our sales force actively pursues approval of Edwards Lifesciences as a qualified supplier for hospital group purchasing organizations ("GPOs") that negotiate contracts with suppliers of medical products. Additionally, we have contracts with a number of United States national and regional buying groups.

United States. In the United States, we sell substantially all of our products through our direct sales force. In 2014, 45% of our reported sales were derived from sales to customers in the United States.

International. In 2014, 55% of our reported sales were derived internationally through our direct sales force and independent distributors. Of the total international sales, 58% were in Europe, 20% were in Japan, and 22% were in Rest of World. We sell our products in approximately 100 countries, and our major international markets include Australia, Brazil, Canada, France, Germany, Italy, Japan, the Netherlands, Spain, and the United Kingdom. A majority of the sales and marketing approach outside the United States is direct sales, although it varies depending on each country's size and state of development.

Raw Materials and Manufacturing

We operate manufacturing facilities in various geographies around the world. Our Transcatheter Heart Valve Therapy and Surgical Heart Valve Therapy products are manufactured primarily in the United States (California and Utah), Switzerland, and Singapore. Critical Care products are manufactured primarily in our facilities located in Puerto Rico and the Dominican Republic.

We use a diverse and broad range of raw and organic materials in the design, development, and manufacture of our products. Our non-implantable products are manufactured from man-made raw materials including resins, chemicals, electronics, and metals. Most of our Transcatheter Heart Valve Therapy and Surgical Heart Valve Therapy products are manufactured from natural tissues harvested from animal tissue, as well as man-made materials. We purchase certain materials and components used in manufacturing our products from external suppliers. In addition, we purchase certain supplies from single sources for reasons of quality assurance, sole source availability, cost effectiveness, or constraints resulting from regulatory requirements.

We work closely with our suppliers to mitigate risk and assure continuity of supply while maintaining uncompromised quality and reliability. Alternative supplier options are generally considered and identified,

4

Table of Contents

although we do not typically pursue regulatory qualification of alternative sources due to the strength of our existing supplier relationships and the time and expense associated with the regulatory validation process.

We follow rigorous sourcing and manufacturing procedures intended to safeguard humans from potential risks associated with diseases such as bovine spongiform encephalopathy ("BSE"). International health and regulatory authorities have given guidance identifying three factors contributing to the control of BSE: source of animals, nature of tissue used, and manufacturing process controls. In the countries in which we sell our products, we comply with all current global guidelines regarding risks for products intended to be implanted in humans. We obtain bovine tissue used in our pericardial tissue valve products only from sources within the United States and Australia, where strong control measures and surveillance programs exist. In addition, bovine tissue used in our pericardial tissue valve products is from tissue types considered by global health and regulatory organizations to have shown no risk of infectibility. Our manufacturing and sterilization processes are designed to render tissue biologically safe from all known infectious agents and viruses, and exceed the worldwide standard for sterile medical products.

Quality Assurance

We are committed to providing quality products that comply with United States Food and Drug Administration ("FDA") and other applicable regulations to our customers. To meet this commitment, we have implemented modern quality systems and concepts throughout the organization. The quality system starts with the initial product specification and continues through the design of the product, component specification processes, and the manufacturing, sales, and servicing of the product. The quality system is intended to design quality into products and utilizes continuous improvement concepts, including Lean/Six Sigma principles, throughout the product lifecycle.

Our operations are inspected by the FDA and comply with all applicable international quality systems standards, including the International Organization for Standardization ("ISO") 13485. These standards require, among other items, quality system controls that are applied to product design, component material, suppliers, and manufacturing operations. These regulatory approvals and ISO certifications can be obtained only after a complete audit of a company's quality system has been conducted by regulatory or independent outside auditors. Periodic reexamination by an independent outside auditor is required to maintain these certifications.

Environmental, Health, and Safety

We are committed to providing a safe and healthy workplace, promoting environmental excellence in our communities, and complying with all relevant regulations and medical device industry standards. Through our corporate and site level Environmental, Health, and Safety functions, we establish and monitor programs to reduce pollution, prevent injuries, and maintain compliance. In order to measure performance, we monitor and report on a number of metrics, including regulated and non-regulated waste disposal, energy usage, water consumption, air toxic emissions, and injuries from our production activities. Each of our manufacturing sites is evaluated regularly with respect to a broad range of Environmental, Health, and Safety criteria.

Research and Development

We are engaged in ongoing research and development to deliver clinically advanced new products, to enhance the effectiveness, ease of use, safety and reliability of our current leading products, and to expand the applications of our products as appropriate. We focus on opportunities within specific areas of structural heart disease and critical care monitoring, and we are dedicated to developing novel technologies to better enable clinicians to treat patients.

5

Table of Contents

We invested $346.5 million in research and development in 2014, $323.0 million in 2013, and $291.3 million in 2012 (14.9%, 15.8%, and 15.3% of net sales, respectively). The majority of our research and development investment has been applied to strengthen our leadership position in transcatheter heart valve replacement technologies, surgical tissue heart valves, heart valve repair therapies, and hemodynamic monitoring products. We have also dedicated a sizable portion of our research and development investment to developing advanced technologies designed to address unmet clinical needs within the area of structural heart disease. A considerable portion of our research and development investment includes clinical trials and the collection of evidence that provide data for use in regulatory submissions, and post-market approval studies involving applications of our products.

We are investing substantially in the development of transcatheter heart valve technologies designed to treat heart valve disease using catheter-based approaches. In the area of transcatheter aortic valve replacement ("TAVR"), we are developing a repositionable, self-expanding transcatheter heart valve system, theEdwards CENTERA transcatheter valve system, in addition to next-generation balloon-expandable valves. We are also making significant investments in the development of transcatheter heart valve technologies designed to treat mitral valve disease.

Surgical Heart Valve Therapy development programs include theEDWARDS INTUITY Elite Valve System, a next-generation minimally invasive aortic heart valve system, andRESILIA, an advanced tissue platform designed to improve tissue valve durability and ease of use.

In our Critical Care product line, we are pursuing the development of non-invasive and minimally invasive hemodynamic monitoring systems, including continuous hemodynamic monitoring, and other technologies that collect critical patient information to help clinicians make more informed treatment decisions for larger patient populations.

Our research and development activities are conducted primarily in facilities located in the United States, Israel, and the Netherlands. Our experienced research and development staff is focused on product design and development, quality, clinical research, and regulatory compliance. To pursue primary research efforts, we have developed alliances with several leading research institutions and universities, and also work with leading clinicians around the world in conducting scientific studies on our existing and developing products.

Proprietary Technology

Patents and other proprietary rights are important to the success of our business. We also rely upon trade secrets, know-how, continuing innovations, and licensing opportunities to develop and maintain our competitive position.

We own more than 2,500 issued United States patents, pending United States patent applications, issued foreign patents, and pending foreign patent applications. We also have licensed various United States and foreign patents and patent applications that relate to aspects of the technology incorporated in certain of our products, including our heart valves and annuloplasty rings. We also own or have rights in United States and foreign patents and patent applications in the field of transcatheter heart valve repair and replacement. In addition, we own or have rights in United States and foreign patents and patent applications that cover catheters, systems and methods for hemodynamic monitoring, and vascular access products.

We are a party to several license agreements with unrelated third parties pursuant to which we have obtained, for varying terms, the exclusive or non-exclusive rights to certain patents held by such third parties in consideration for cross-licensing rights and/or royalty payments. We have also licensed certain patent rights to others.

We monitor the products of our competitors for possible infringement of our owned and licensed patents. Litigation has been necessary to enforce certain patent rights held by us, and we plan to continue to defend and prosecute our rights with respect to such patents.

6

Table of Contents

We own certain United States registered trademarks used in our business. Many of our trademarks have also been registered for use in certain foreign countries where registration is available and where we have determined it is commercially advantageous to do so.

Government Regulation and Other Matters

Our products and facilities are subject to regulation by numerous government agencies, including the U.S. FDA, European Community Notified Bodies, and the Japanese Pharmaceuticals and Medical Devices Agency, to confirm compliance to the various laws and regulations governing the development, testing, manufacturing, labeling, marketing, and distribution of our products. We are also governed by federal, state, local, and international laws of general applicability, such as those regulating employee health and safety and the protection of the environment. Overall, the amount and scope of domestic and foreign laws and regulations applicable to our business is increasing.

United States Regulation. In the United States, the FDA has responsibility for regulating medical devices. The FDA regulates design, development, testing, clinical studies, manufacturing, labeling, promotion, and record keeping for medical devices, and reporting of adverse events, recalls, or other field actions by manufacturers and users to identify potential problems with marketed medical devices. Many of the devices that we develop and market are in a category for which the FDA has implemented stringent clinical investigation and pre-market clearance or approval requirements. The process of obtaining FDA clearance or approval to market a product is resource intensive, lengthy, and costly. FDA review may involve substantial delays that adversely affect the marketing and sale of our products. A number of our products are pending regulatory clearance or approval to begin commercial sales in various markets. Ultimately, the FDA may not authorize the commercial release of a medical device if it determines the device is not safe and effective or does not meet other standards for clearance. Additionally, even if a product is cleared or approved, the FDA may require testing and surveillance programs to monitor the effects of these products once commercialized.

The FDA has the authority to halt the distribution of certain medical devices, detain or seize adulterated or misbranded medical devices, order the repair, replacement, or refund of the costs of such devices, or preclude the importation of devices that are or appear violative. The FDA also conducts inspections to determine compliance with the quality system regulations concerning the manufacturing and design of devices and current medical device reporting regulations, recall regulations, clinical testing regulations, and other requirements. The FDA may withdraw product clearances or approvals due to failure to comply with regulatory standards, or the occurrence of unforeseen problems following initial approval, and require notification of health professionals and others with regard to medical devices that present unreasonable risks of substantial harm to the public health. Additionally, the failure to comply with FDA or comparable regulatory standards or the discovery of previously unknown product problems could result in fines, delays, or suspensions of regulatory clearances or approvals, seizures, injunctions, recalls, refunds, civil money penalties, or criminal prosecution. Our compliance with applicable regulatory requirements is subject to continual review. Moreover, the FDA and several other United States agencies administer controls over the export of medical devices from the United States and the import of devices into the United States, which could also subject us to sanctions for noncompliance.

In May 2013, we received a warning letter from the Denver District Office of the FDA resulting from an inspection of our facility in Draper, Utah. The warning letter relates specifically to the execution of our quality systems at the Utah facility, including design and process validation, corrective and preventive actions, finished device acceptance, and packaging, and indicated that we would not receive pre-market approvals for devices reasonably related to those issues until the issues are resolved. Our Utah facility manufactures devices such as cannulae and cardioplegia catheters, heart valve repair rings, and transcatheter heart valve delivery system components and accessories. We are actively implementing the necessary actions to resolve these issues identified in the letter. In June 2014, we were granted a variance from the FDA through June 15, 2015 for theSAPIEN XT delivery systems and components that are manufactured at the Draper facility. Under the

7

Table of Contents

variance, we are complying with an agreed upon action plan for theSAPIEN XT delivery system that verifies the safety and effectiveness of its intended use.

We are also subject to additional laws and regulations that govern our business operations, products, and technologies, including:

- •

- federal, state, and foreign anti-kickback laws and regulations, which generally prohibit payments to physicians or other purchasers of medical products as an inducement to purchase a product;

- •

- the Stark law, which prohibits physicians from referring Medicare or Medicaid patients to a provider that bills these programs for the provision of certain designated health services if the physician (or a member of the physician's immediate family) has a financial relationship with that provider;

- •

- federal and state laws and regulations that protect the confidentiality of certain patient health information, including patient records, and restrict the use and disclosure of such information, in particular, the Health Insurance Portability and Accountability Act of 1996;

- •

- the Physician Payments Sunshine Act, which requires public disclosure of the financial relationships of United States physicians and teaching hospitals with applicable manufacturers, including medical device, pharmaceutical, and biologics companies;

- •

- the False Claims Act, which prohibits the submission of false or otherwise improper claims for payment to a federally funded health care program, and health care fraud statutes that prohibit false statements and improper claims to any third-party payor; and

- •

- the United States Foreign Corrupt Practices Act, which can be used to prosecute companies in the United States for arrangements with foreign government officials or other parties outside the United States.

Failure to comply with these laws and regulations could result in criminal liability, significant fines or penalties, negative publicity, and substantial costs and expenses associated with investigation and enforcement activities. To assist in our compliance efforts, we adhere to many codes of ethics and conduct regarding our sales and marketing activities in the United States and other countries in which we operate. In addition, we have in place a dedicated team to improve our internal business compliance programs and policies.

International Regulation. Internationally, the regulation of medical devices is complex. In Europe, our products are subject to extensive regulatory requirements. The regulatory regime in the European Union for medical devices became mandatory in June 1998. It requires that medical devices may only be placed on the market if they do not compromise safety and health when properly installed, maintained, and used in accordance with their intended purpose. National laws conforming to the European Union's legislation regulate our products under the medical devices regulatory system. Although the more variable national requirements under which medical devices were formerly regulated have been substantially replaced by the European Union Medical Devices Directive, individual nations can still impose unique requirements that may require supplemental submissions. The European Union medical device laws require manufacturers to declare that their products conform to the essential regulatory requirements after which the products may be placed on the market bearing the CE Mark. Manufacturers' quality systems for products in all but the lowest risk classification are also subject to certification and audit by an independent notified body. In Europe, particular emphasis is being placed on more sophisticated and faster procedures for the reporting of adverse events to the competent authorities.

In Japan, pre-market approval and clinical studies are required as is governmental pricing approval for medical devices. Clinical studies are subject to a stringent "Good Clinical Practices" standard. Approval time frames from the Japanese Ministry of Health, Labour and Welfare vary from simple notifications to review periods of one or more years, depending on the complexity and risk level of the device. In addition, importation of medical devices into Japan is subject to the "Good Import Practices" regulations. As with any highly regulated market, significant changes in the regulatory environment could adversely affect future sales.

8

Table of Contents

In many of the other foreign countries in which we market our products, we may be subject to regulations affecting, among other things:

- •

- product standards and specifications;

- •

- packaging requirements;

- •

- labeling requirements;

- •

- product collection and disposal requirements;

- •

- quality system requirements;

- •

- import restrictions;

- •

- tariffs;

- •

- duties; and

- •

- tax requirements.

Many of the regulations applicable to our devices and products in these countries are similar to those of the FDA. In some regions, the level of government regulation of medical devices is increasing, which can lengthen time to market and increase registration and approval costs. In many countries, the national health or social security organizations require our products to be qualified before they can be marketed and considered eligible for reimbursement.

Health Care Initiatives. Government and private sector initiatives to limit the growth of health care costs, including price regulation and competitive pricing, coverage and payment policies, comparative effectiveness reviews, technology assessments, and managed-care arrangements, are continuing in many countries where we do business, including the United States, Europe, and Japan. As a result of these changes, the marketplace has placed increased emphasis on the delivery of more cost-effective medical therapies. For example, government programs, private health care insurance, and managed-care plans have attempted to control costs by restricting coverage and limiting the level of reimbursement for procedures or treatments, and some third-party payors require their pre-approval before new or innovative devices or therapies are utilized by patients. These various initiatives have created increased price sensitivity over medical products generally and may impact demand for our products and technologies.

The delivery of our products is subject to regulation by the Department of Health and Human Services ("HHS") in the United States and comparable state and foreign agencies responsible for reimbursement and regulation of health care items and services. Foreign governments also impose regulations in connection with their health care reimbursement programs and the delivery of health care items and services. Reimbursement schedules regulate the amount the United States government will reimburse hospitals and doctors for the inpatient care of persons covered by Medicare. HHS' Centers for Medicare & Medicaid Services ("CMS") may also review whether and/or under what circumstances a procedure or technology is reimbursable for Medicare beneficiaries. Several legislative proposals in the United States have been advanced that would restrict future funding increases for government-funded programs, including Medicare and Medicaid. Changes in current reimbursement levels could have an adverse effect on market demand and our pricing flexibility.

Health care cost containment efforts have also prompted domestic hospitals and other customers of medical device manufacturers to consolidate into larger purchasing groups to enhance purchasing power, and this trend is expected to continue. The medical device industry has also experienced some consolidation, partly in order to offer a broader range of products to large purchasers. As a result, transactions with customers are larger, more complex and tend to involve more long-term contracts than in the past. These larger customers, due to their enhanced purchasing power, may attempt to increase the pressure on product pricing.

9

Table of Contents

Health Care Reform. In 2010, significant reforms to the health care system were adopted as law in the United States. The law includes provisions that, among other things, reduce or limit Medicare reimbursement, require all individuals to have health insurance (with limited exceptions), and impose increased taxes. Specifically, the law requires the medical device industry to subsidize health care reform in the form of a 2.3% excise tax on United States sales of most medical devices. The excise tax increased our operating expenses. Because other parts of the 2010 health care law remain subject to continued implementation, the long-term impact on us is uncertain. This law or any future legislation could reduce medical procedure volumes, lower reimbursement for our products, and impact the demand for our products or the prices at which we sell our products.

Seasonality

Our quarterly net sales are influenced by many factors, including new product introductions, acquisitions, regulatory approvals, patient and physician holiday schedules, and other factors. Net sales in the third quarter are typically lower than other quarters of the year due to the seasonality of the United States and European markets, where summer vacation schedules normally result in fewer medical procedures.

Employees

As of December 31, 2014, we had approximately 9,100 employees worldwide, the majority of whom were located in the United States, the Dominican Republic, Singapore, and Puerto Rico. Other major concentrations of employees are located in Europe and Japan. We emphasize competitive compensation, benefits, equity participation, and a positive and attractive work environment in our efforts to attract and retain qualified personnel, and employ a rigorous talent management system. None of our North American employees are represented by a labor union. In various countries outside of North America, we interact with trade unions and work councils that represent a limited number of employees.

Item 1A. Risk Factors

Our business and assets are subject to varying degrees of risk and uncertainty. An investor should carefully consider the risks described below, as well as other information contained in this Annual Report on Form 10-K and in our other filings with the Securities and Exchange Commission. Additional risks not presently known to us or that we currently deem immaterial may also adversely affect our business. If any of these events or circumstances occurs, our business, financial condition, results of operations, or prospects could be materially harmed. In that case, the value of our securities could decline and an investor could lose part or all of his or her investment. In addition, forward-looking statements within the meaning of the federal securities laws that are contained in this Annual Report on Form 10-K or in our other filings or statements may be subject to the risks described below as well as other risks and uncertainties. Please read the cautionary notice regarding forward-looking statements in Item 7, "Management's Discussion and Analysis of Financial Condition and Results of Operations," below.

If we do not introduce new products in a timely manner, our products may become obsolete and our operating results may suffer.

The cardiovascular products industry is characterized by technological changes, frequent new product introductions, and evolving industry standards. Without the timely introduction of new and improved products, our products could become technologically obsolete or more susceptible to competition and our revenue and operating results would suffer. Even if we are able to develop new or improved products, our ability to market them could be limited by the need for regulatory clearance, restrictions imposed on approved indications, entrenched patterns of clinical practice, uncertainty over third-party reimbursement, or other factors. We devote significant financial and other resources to our research and development activities; however, the research and development process is prolonged and entails considerable uncertainty. Accordingly, products we are currently developing may not complete the development process or obtain the regulatory or other approvals required to market such products in a timely manner or at all.

10

Table of Contents

Technical innovations often require substantial time and investment before we can determine their commercial viability. We may not have the financial resources necessary to fund all of these projects. In addition, even if we are able to successfully develop new or improved products, they may not produce revenue in excess of the costs of development, and they may be rendered obsolete or less competitive by changing customer preferences or the introduction by our competitors of products with newer technologies or features or other factors.

We may incur product liability losses that could adversely affect our operating results.

Our business exposes us to potential product liability risks that are inherent in the design, manufacture, and marketing of medical devices. Our products are often used in surgical and intensive care settings with seriously ill patients. In addition, many of the medical devices we manufacture and sell are designed to be implanted in the human body for long periods of time. Component failures, manufacturing flaws, design defects, or inadequate disclosure of product-related risks or product-related information could result in an unsafe condition or injury to, or death of, patients. Such a problem could result in product liability lawsuits and claims, safety alerts, or product recalls in the future, which, regardless of their ultimate outcome, could have a material adverse effect on our business, reputation, and ability to attract and retain customers. Product liability claims may be brought from time to time either by individuals or by groups seeking to represent a class. We may incur charges related to such matters in excess of any established reserves and such charges, including the establishment of any such reserves, could have a material adverse impact on our net income and net cash flows.

We may experience supply interruptions that could harm our ability to manufacture products.

We use a broad range of raw and organic materials and other items in the design and manufacture of our products. Our Surgical and Transcatheter Heart Valve Therapy products are manufactured from treated natural animal tissue and man-made materials. Our non-implantable products are manufactured from man-made raw materials including resins, chemicals, electronics, and metals. We purchase certain of the materials and components used in the manufacture of our products from external suppliers, and we purchase certain supplies from single sources for reasons of quality assurance, cost-effectiveness, availability, or constraints resulting from regulatory requirements. General economic conditions could adversely affect the financial viability of our suppliers, resulting in their inability to provide materials and components used in the manufacture of our products. While we work closely with suppliers to monitor their financial viability, assure continuity of supply, and maintain high quality and reliability, these efforts may not be successful. In addition, due to the rigorous regulations and requirements of the FDA and foreign regulatory authorities regarding the manufacture of our products (including the need for approval of any change in supply arrangements), we may have difficulty establishing additional or replacement sources on a timely basis or at all if the need arises. Although alternative supplier options are considered and identified, we typically do not pursue regulatory qualification of alternative sources due to the strength of our existing supplier relationships and the time and expense associated with the regulatory validation process. A change in suppliers could require significant effort or investment in circumstances where the items supplied are integral to product performance or incorporate unique technology, and the loss of any existing supply contract could have a material adverse effect on us.

Regulatory agencies in the United States or other international geographies from time to time have limited or banned the use of certain materials used in the manufacture of our products. In these circumstances, transition periods typically provide time to arrange for alternative materials. In addition, the SEC enacted disclosure rules regarding products that may contain certain minerals that originate from conflict areas in and around the Democratic Republic of Congo. If our suppliers cannot verify that their components do not originate from these conflict areas, we may need to source components from alternative suppliers. If we are unable to identify alternative materials or suppliers and secure approval for their use in a timely manner, our business could be harmed.

11

Table of Contents

Some of our suppliers are located outside the United States. As a result, trade or regulatory embargoes imposed by foreign countries or the United States could result in delays or shortages that could harm our business.

The manufacture of many of our products is highly complex and subject to strict quality controls. If we or one of our suppliers encounters manufacturing or quality problems, including as a result of natural disasters, our business could suffer.

The manufacture of many of our products is highly complex and subject to strict quality controls, due in part to rigorous regulatory requirements. In addition, quality is extremely important due to the serious and costly consequences of a product failure. Problems can arise during the manufacturing process for a number of reasons, including equipment malfunction, failure to follow protocols and procedures, raw material problems, or human error. If these problems arise or if we otherwise fail to meet our internal quality standards or those of the FDA or other applicable regulatory body, which include detailed record-keeping requirements, our reputation could be damaged, we could become subject to a safety alert or a recall, we could incur product liability and other costs, product approvals could be delayed, and our business could otherwise be adversely affected.

In addition, our manufacturing facilities in California, Utah, the Dominican Republic, and Puerto Rico could be materially damaged by earthquakes, hurricanes, and other natural disasters or catastrophic circumstances. While we believe that our exposure to significant losses from a catastrophic disaster could be partially mitigated by our ability to manufacture some of our products at our other manufacturing facilities, the losses could have a material adverse effect on our business for an indeterminate period of time before this manufacturing transition is complete and operates without significant disruption.

We may be required, from time to time, to recognize charges in connection with the write-down of our asset or business dispositions, or for other reasons.

From time to time, we identify businesses and products that are not performing at a level commensurate with the rest of our business. We may seek to dispose of these underperforming businesses or products. We may also seek to dispose of other businesses or products for strategic or other business reasons. If we cannot dispose of a business or product on acceptable terms, we may voluntarily cease operations related to that business or product. Any of these events could result in charges, which could be substantial and which could adversely affect our results of operations.

We may not successfully identify and complete acquisitions or strategic alliances on favorable terms or achieve anticipated synergies relating to any acquisitions or alliances, and such acquisitions could result in unforeseen operating difficulties and expenditures, require significant management resources, and require significant charges or write-downs.

We regularly explore potential acquisitions of complementary businesses, technologies, services, or products, as well as potential strategic alliances. We may be unable to find suitable acquisition candidates or appropriate partners with which to form alliances. Even if we identify appropriate acquisition or alliance candidates, we may be unable to complete the acquisitions or alliances on favorable terms, if at all. In addition, the process of integrating an acquired business, technology, service, or product into our existing operations could result in unforeseen difficulties and expenditures. Integration of an acquired company often requires significant expenditures as well as significant management resources that otherwise would be available for ongoing development of our other businesses. Moreover, we may not realize the anticipated financial or other benefits of an acquisition or alliance.

We may be required to take charges or write-downs in connection with acquisitions. In particular, acquisitions of businesses engaged in the development of new products may give rise to in-process research and development ("IPR&D") assets. To the extent that the value of these assets declines, we may be required

12

Table of Contents

to write down the value of the assets. Also, in connection with certain asset acquisitions, we may be required to take an immediate charge related to acquired IPR&D. Either of these situations could result in substantial charges, which could adversely affect our results of operations.

Future acquisitions could also involve the issuance of equity securities, the incurrence of debt, contingent liabilities, or amortization of expenses related to other intangible assets, any of which could adversely impact our financial condition or results of operations. In addition, equity or debt financing required for such acquisitions may not be available.

General economic and political conditions could have a material adverse effect on our business.

External factors can affect our profitability and financial condition. Such external factors include general domestic and global economic conditions, such as interest rates, tax rates, and factors affecting global economic stability, and the political environment regarding health care in general. The strength and timing of the current economic recovery remains uncertain, and we cannot predict to what extent the global economic conditions may negatively impact our business. For example, negative conditions in the credit and capital markets could impair our ability to access the financial markets for working capital or other funds, and could negatively impact our ability to borrow. An increase in interest rates could result in an increase in our borrowing costs and could otherwise restrict our ability to access the capital markets. Such conditions could result in decreased liquidity and impairments in the carrying value of our investments, and could adversely affect our results of operations and financial condition. These and other conditions could also adversely affect our customers, and may impact their ability or decision to purchase our products or make payments on a timely basis.

In 2010, significant reforms to the health care system were adopted as law in the United States. The law includes provisions that, among other things, reduce or limit Medicare reimbursement, require all individuals to have health insurance (with limited exceptions) and impose increased taxes. Specifically, the law requires the medical device industry to subsidize health care reform in the form of a 2.3% excise tax on United States sales of most medical devices. The excise tax increased our operating expenses. Because other parts of the 2010 health care law remain subject to continued implementation, the long-term impact on us is uncertain. This law or any future legislation, including deficit reduction legislation, could adversely affect our results of operations, financial condition, and prospects if they were to impact the demand for our products or pricing, or result in cuts to, or a restructuring of, entitlement programs such as Medicare and Medicaid.

Our business is subject to economic, political, and other risks associated with international sales and operations, including risks arising from currency exchange rate fluctuations.

Because we sell our products in a number of countries, our business is subject to the risks of doing business internationally, including risks associated with anti-corruption and anti-bribery laws. Our net sales originating outside the United States, as a percentage of total net sales, were 55% in 2014. We anticipate that sales from international operations will continue to represent a substantial portion of our total sales. In addition, many of our manufacturing facilities and suppliers are located outside of the United States. Accordingly, our future results could be harmed by a variety of factors, including:

- •

- changes in local medical reimbursement policies and programs;

- •

- changes in foreign regulatory requirements;

- •

- changes in a specific country's or region's political or economic conditions, such as the current financial uncertainties in Europe and changing circumstances in emerging regions, that may reduce the number of procedures that use our products;

- •

- trade protection measures, quotas, embargoes, import or export licensing requirements, and duties, tariffs, or surcharges;

13

Table of Contents

- •

- potentially negative impact of tax laws, including transfer pricing liabilities and tax costs associated with the repatriation of cash;

- •

- difficulty in staffing and managing global operations;

- •

- cultural, exchange rate, or other local factors affecting financial terms with customers;

- •

- local economic and financial conditions, including sovereign defaults and decline in sovereign credit ratings, affecting the collectability of receivables, including receivables from sovereign entities;

- •

- an outbreak of any life-threatening communicable disease;

- •

- economic and political instability and local economic and political conditions;

- •

- differing labor regulations; and

- •

- differing protection of intellectual property.

Substantially all of our sales outside of the United States are denominated in local currencies. Measured in local currency, a substantial portion of our international sales was generated in Europe (and primarily denominated in the Euro) and in Japan. The United States dollar value of our international sales varies with currency exchange rate fluctuations. Decreases in the value of the United States dollar to the Euro or the Japanese yen have the effect of increasing our reported revenues even when the volume of international sales has remained constant. Increases in the value of the United States dollar relative to the Euro or the Japanese yen, as well as other currencies, have the opposite effect and, if significant, could have a material adverse effect on our reported revenues and results of operations. We have a hedging program for certain currencies that attempts to manage currency exchange rate risks to an acceptable level based on management's judgment of the appropriate trade-off between risk, opportunity, and cost; however, this hedging program does not completely eliminate the effects of currency exchange rate fluctuations.

The United States Foreign Corrupt Practices Act, the United Kingdom Bribery Act, and similar laws in other jurisdictions contain prohibitions against bribery and other illegal payments, and make it an offense to fail to have procedures in place that prevent such payments. Recent years have seen an increasing number of investigations and other enforcement activities under these laws. Although we have compliance programs in place with respect to these laws, which may be used as a defense to prove we had adequate procedures, no assurance can be given that a violation will not be found, and if found, the resulting penalties could adversely affect us and our business.

The stock market can be volatile and fluctuations in our quarterly sales and operating results as well as other factors could cause our financial guidance to vary from actual results and our stock price to decline.

From time to time, the stock market experiences extreme price and volume fluctuations. This volatility can have a significant effect on the market prices of securities for reasons unrelated to underlying performance. These broad market fluctuations may materially adversely affect our stock price, regardless of our operating results. In addition, the market price of our common stock could fluctuate substantially in response to any of the other risk factors set out above and below, as well as a number of other factors, including the performance of comparable companies or the medical device industry, or changes in financial estimates and recommendations of securities analysts.

Our sales and operating results may vary significantly from quarter to quarter. A high proportion of our costs are fixed, due in part to significant selling, research and development, and manufacturing costs. Thus, small declines in revenue could disproportionately affect our operating results in a quarter, and the price of our common stock could fall. Other factors that could affect our quarterly sales and operating results include:

- •

- announcements of innovations, new products, strategic developments, or business combinations by us or our competitors;

14

Table of Contents

- •

- demand for and clinical acceptance of products;

- •

- the timing and execution of customer contracts, particularly large contracts that would materially affect our operating results in a given quarter;

- •

- the timing of sales of products and of the introduction of new products;

- •

- the timing of marketing, training, and other expenses related to the introduction of new products;

- •

- the timing of regulatory approvals;

- •

- changes in foreign currency exchange rates;

- •

- delays or problems in introducing new products, such as slower than anticipated adoption of transcatheter heart valves;

- •

- changes in our pricing policies or the pricing policies of our competitors;

- •

- the timing of approvals of governmental reimbursement rates or changes in reimbursement rates for our products;

- •

- increased expenses, whether related to sales and marketing, raw materials or supplies, product development, or administration;

- •

- changes in the level of economic activity in the United States or other regions in which we do business;

- •

- costs related to acquisitions of technologies or businesses; and

- •

- our ability to expand our operations and the amount and timing of expansion-related expenditures.

The quarterly and full-year financial guidance we provide to investors and analysts with insight to our view of our future performance is based on assumptions about our sales and operating results. Due to the nature of our business and the numerous factors that can impact our sales and operating performance, including those described above, our financial guidance may vary from actual results. If we fail to meet any financial guidance that we provide, or if we find it necessary to revise such guidance during the year, the price of our common stock could decline.

We face intense competition, and if we do not compete effectively, our business will be harmed.

The cardiovascular medical device industry is highly competitive. We compete with many companies, some of which have longer operating histories, better brand or name recognition, and broader product offerings. Our customers consider many factors when selecting a product, including product reliability, breadth of product line, clinical outcomes, product availability, price, availability and rate of reimbursement, and services provided by the manufacturer. In addition, our ability to compete will depend in large part on our ability to develop and acquire new products and technologies, anticipate technology advances, and keep pace with other developers of cardiovascular therapies and technologies. Our sales, technical, and other key personnel play an integral role in the development, marketing, and selling of new and existing products. If we are unable to recruit, hire, develop, and retain a talented, competitive workforce, our ability to compete may be adversely affected. Our competitive position can also be adversely affected by product problems, physician advisories and safety alerts, reflecting the importance of quality in the medical device industry. Our position can shift as a result of any of these factors. See "Competition" under "Business" included herein.

Consolidation in the health care industry could have an adverse effect on our sales and results of operations.

The health care industry has been consolidating, and organizations such as GPOs, independent delivery networks, and large single accounts, such as the United States Veterans Administration, continue to consolidate purchasing decisions for many of our health care provider customers. As a result, transactions with

15

Table of Contents

customers are larger, more complex, and tend to involve more long-term contracts. The purchasing power of these larger customers has increased, and may continue to increase, causing downward pressure on product pricing. If we are not one of the providers selected by one of these organizations, we may be precluded from making sales to its members or participants. Even if we are one of the selected providers, we may be at a disadvantage relative to other selected providers that are able to offer volume discounts based on purchases of a broader range of medical equipment and supplies. Further, we may be required to commit to pricing that has a material adverse effect on our revenues, profit margins, business, financial condition, and results of operations. We expect that market demand, governmental regulation, third-party reimbursement policies, and societal pressures will continue to change the worldwide health care industry, resulting in further business consolidations and alliances, which may exert further downward pressure on the prices of our products and could adversely impact our business, financial condition, and results of operations.

Our inability to protect our intellectual property or other sensitive company information could have a material adverse effect on our business.

Our success and competitive position are dependent in part upon our proprietary intellectual property. We rely on a combination of patents and trade secrets to protect our proprietary intellectual property, and we expect to continue to do so. Although we seek to protect our proprietary rights through a variety of means, we cannot guarantee that the protective steps we have taken are adequate to protect these rights. Patents issued to or licensed by us in the past or in the future may be challenged and held invalid. In addition, as our patents expire, we may be unsuccessful in extending their protection through patent term extensions. The expiration of, or the failure to maintain or extend our patents, could have a material adverse effect on us.

We also rely on confidentiality agreements with certain employees, consultants, and other third parties to protect, in part, trade secrets and other proprietary information. These agreements could be breached, and we may not have adequate remedies for such a breach. In addition, others could independently develop substantially equivalent proprietary information or gain access to our trade secrets or proprietary information.

Our intellectual property, other proprietary technology, and other sensitive company information is potentially vulnerable to loss, damage, or misappropriation from system malfunction, computer viruses, unauthorized access to our data, or misappropriation or misuse of it by those with permitted access, and other events. While we have invested to protect our intellectual property and other information, and continue to work diligently in this area, there can be no assurance that our precautionary measures will prevent breakdowns, breaches, cyber-attacks, or other events. Such events could have a material adverse effect on our reputation, financial condition, or results of operations.

We spend significant resources to enforce our intellectual property rights, sometimes resulting in litigation. Intellectual property litigation is complex and can be expensive and time-consuming. However, our efforts in this regard may not be successful. We may not be able to detect infringement. In addition, competitors may design around our technology or develop competing technologies. Patent litigation can result in substantial cost and diversion of effort. Intellectual property protection may also be unavailable or limited in some foreign countries, enabling our competitors to capture increased market position. The invalidation of key intellectual property rights or an unsuccessful outcome in lawsuits filed to protect our intellectual property could have a material adverse effect on our financial condition, results of operations, or prospects.

Third parties may claim we are infringing their intellectual property, and we could suffer significant litigation or licensing expenses or be prevented from selling products.

During recent years, we and our competitors have been involved in substantial litigation regarding patent and other intellectual property rights in the medical device industry. From time to time, we have been and may in the future be forced to defend against claims and legal actions alleging infringement of the intellectual property rights of others, and such intellectual property litigation is typically costly and time-consuming. Adverse determinations in any such litigation could result in significant liabilities to third parties or

16

Table of Contents

injunctions, or could require us to seek licenses from third parties and, if such licenses are not available on commercially reasonable terms, prevent us from manufacturing, selling, or using certain products, any one of which could have a material adverse effect on us. In addition, some licenses may be non-exclusive, which could provide our competitors access to the same technologies.

Third parties could also obtain patents that may require us to either redesign products or, if possible, negotiate licenses from such third parties. Such licenses may materially increase our expenses. If we are unable to redesign products or obtain a license, we might have to exit a particular product offering.

We and our customers are subject to rigorous governmental regulations and we may incur significant expenses to comply with these regulations and develop products that are compatible with these regulations. In addition, failure to comply with these regulations could subject us to substantial sanctions which could adversely affect our business, results of operations, and financial condition.

The medical devices we manufacture and market are subject to rigorous regulation by the FDA and numerous other federal, state, and foreign governmental authorities, including regulations that cover the composition, labeling, testing, clinical study, design, sourcing, manufacturing, packaging, marketing, advertising, promotion, and distribution of our products.

We are required to register with the FDA as a device manufacturer. As a result, we are subject to periodic inspection by the FDA for compliance with the FDA's Quality System Regulation ("QSR") requirements, which require manufacturers of medical devices to adhere to certain regulations, including testing, design, quality control, and documentation procedures. The FDA may also inspect our compliance with requirements related to adverse event reporting, recalls or corrections (field actions), the conduct of clinical studies, and other requirements. In the European Union, we are required to maintain certain CE Mark and ISO certifications in order to sell our products, and are subject to periodic inspections by notified bodies to obtain and maintain these certifications. If we or our suppliers fail to adhere to QSR, CE Mark, ISO, or similar requirements, this could delay or interrupt product production or sales and/or lead to fines, difficulties in obtaining regulatory clearances, recalls, or other consequences, which in turn could have a material adverse effect on our financial condition and results of operations or prospects.

Medical devices must receive FDA clearance or approval before they can be commercially marketed in the United States. In addition, the FDA may require testing and surveillance programs to monitor the effects of approved products that have been commercialized, and can prevent or limit further marketing of a product based upon the results of post-marketing programs. In addition, the federal Medical Device Reporting regulations require us to provide information to the FDA whenever there is evidence that reasonably suggests that a device may have caused or contributed to a death or serious injury or, if a malfunction were to occur, would be likely to cause or contribute to a death or serious injury. Federal regulations also require us to report certain recalls or corrective actions to the FDA. Furthermore, most major markets for medical devices outside the United States require clearance, approval, or compliance with certain standards before a product can be commercially marketed. The process of obtaining regulatory clearances or approvals to market a medical device, particularly from the FDA and certain foreign governmental authorities, can be costly and time-consuming, and clearances or approvals may not be granted for products or product improvements on a timely basis, if at all. Delays in receipt of, or failure to obtain, clearances or approvals for products or product improvements could result in delayed realization of product revenues or in substantial additional costs, which could have a material adverse effect on our business or results of operations or prospects. At any time after approval of a product for commercial sale, the FDA may conduct periodic inspections to determine compliance with QSR requirements, and/or current Medical Device Reporting regulations, or other regulatory requirements. Noncompliance with applicable requirements may subject us or responsible individuals to sanctions including civil money penalties, product seizure, injunction, or criminal prosecution. In addition, the FDA may withhold or delay pre-market approval of our products until the noncompliance is resolved. Product approvals by the FDA can also be withdrawn due to failure to comply with regulatory standards or the occurrence of unforeseen problems following initial approval.

17

Table of Contents