May 23, 2012 May 23, 2012 2012 Analyst Day 2012 Analyst Day Exhibit 99.1 |

Analyst Day 2012 | 2 Safe Harbor Safe Harbor Certain information contained in this presentation may constitute forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements involve substantial risks and uncertainties that could cause actual results to differ materially from the results expressed in, or implied by, these forward-looking statements. Statements that include such words as “anticipate,” “believe,” “estimate,” “expect,” “forecast,” “may,” “will,” “should” or the negative thereof and similar expressions as they relate to Entegris or our management are intended to identify such forward-looking statements. These statements are not guarantees of future performance and involve risks, uncertainties and assumptions that are difficult to predict. These risks include, but are not limited to, fluctuations in the market price of Entegris’ stock, Entegris’ future operating results, other acquisition and investment opportunities available to Entegris, general business and market conditions and other factors. Additional information concerning these and other risk factors may be found in previous financial press releases issued by Entegris and Entegris’ periodic public filings with the Securities and Exchange Commission, including discussions appearing under the headings “Risks Relating to our Business and Industry,” “Risks Related to our Borrowings,” “Manufacturing Risks,” “International Risks,” and “Risks Related to Owning Our Securities” in Item 1A of our Annual Report on Form 10–K for the fiscal year ended December 31, 2011, as well as other matters and important factors disclosed previously and from time to time in the filings of Entegris with the U.S. Securities and Exchange Commission. Except as required under the federal securities laws and the rules and regulations of the Securities and Exchange Commission, we undertake no obligation to update publicly any forward-looking statements contained herein. |

Analyst Day 2012 | 3 Agenda Agenda The Path to $1B Gideon Argov President and CEO What Node Transitions Mean for Entegris Bertrand Loy Executive Vice President and COO Delivering Higher Value at Advanced Nodes Todd Edlund Vice President and General Manager, CCS Division Why We Are Winning in the Market Greg Morris Vice President and General Manager, Global Field Operations What This Means for Investors Greg Graves Executive Vice President and CFO Q&A All |

Gideon Argov President and CEO Gideon Argov President and CEO The Path to $1B The Path to $1B |

Analyst Day 2012 | 5 2011: Another Record Year 2011: Another Record Year We achieved record sales, earnings and cash flow in 2011 We out-performed our markets Strong contribution from new products New emerging markets did well, despite challenging environment We delivered on our operating model |

Analyst Day 2012 | 6 Proven Strategies in Place to Achieve Superior Growth and Profitability Proven Strategies in Place to Achieve Superior Growth and Profitability Growth Strategies Concentrating on the highest growth fab processes Increasing collaboration with technology leaders and largest customers Creating and leveraging technology hubs close to critical customers around the world Focusing on markets with high growth potential (LED, PV, etc.) Targeting our market approach to early technology adopters Adapting our core technologies to new markets Core Market Semiconductor 1. Macro Industry Growth 2. Semi Market Initiatives Diversification 3. Adjacent Market Expansion |

Analyst Day 2012 | 7 Our Strategy is Working: We’re Growing Faster than Our Markets Our Strategy is Working: We’re Growing Faster than Our Markets Source: Gartner, March 2012; Entegris Entegris vs. Industry (CAGR) 3-yr. CAGR = 14% 3-yr. CAGR = 4% (65% MSI + 35% WFE) *In millions of square inches of silicon Semiconductor Unit Production (MSI*) $36 $24 $13 $32 $36 2007 2008 2009 2010 2011 Industry Wafer Fab Equipment ($B) 8,900 8,400 7,000 9,700 9,400 2007 2008 2009 2010 2011 10.5% 9.0% 7.5% 2.0% 2008- 2011 2010-2011 Entegris Industry blend |

Analyst Day 2012 | 8 Growing middle class will continue to purchase electronics Why the Industry Will Continue to Grow Why the Industry Will Continue to Grow Source: Organization for Economic Cooperation and Development (OECD), 2010 Billions of 2005 PPP$ 100% 100% 26% 38% 7% 23% 4% 1% 1% 17% 29% 7% 42% 4% 12-yr. CAGR = 4.2% 21,278 35,000 2009 2020 (E) Global Middle Class Spending 2009 2020 (E) Global Middle Class Spending Composition North America Europe South America Asia Pacific MENA Sub Saharan Africa |

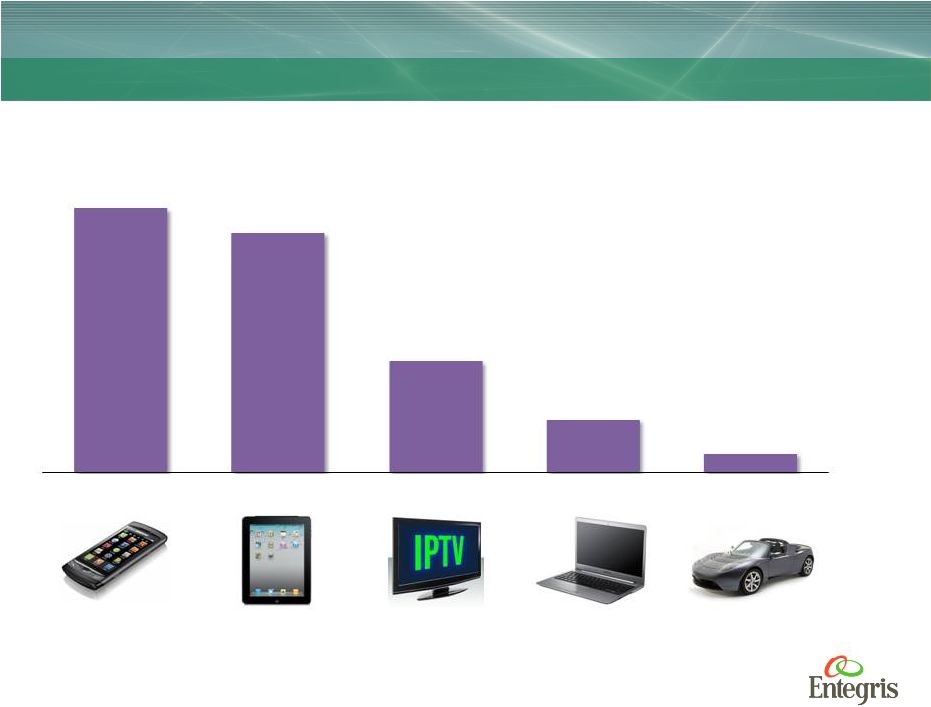

Analyst Day 2012 | 9 Why the Industry Will Continue to Grow Why the Industry Will Continue to Grow Semiconductor market drivers remain strong Source: Gartner, December 2011 and March 2012 Annual Unit Growth 2011 to 2015 79% 71% 33% 16% 6% Smartphones Tablets IPTV Set-Tops Mobile PCs Automotive |

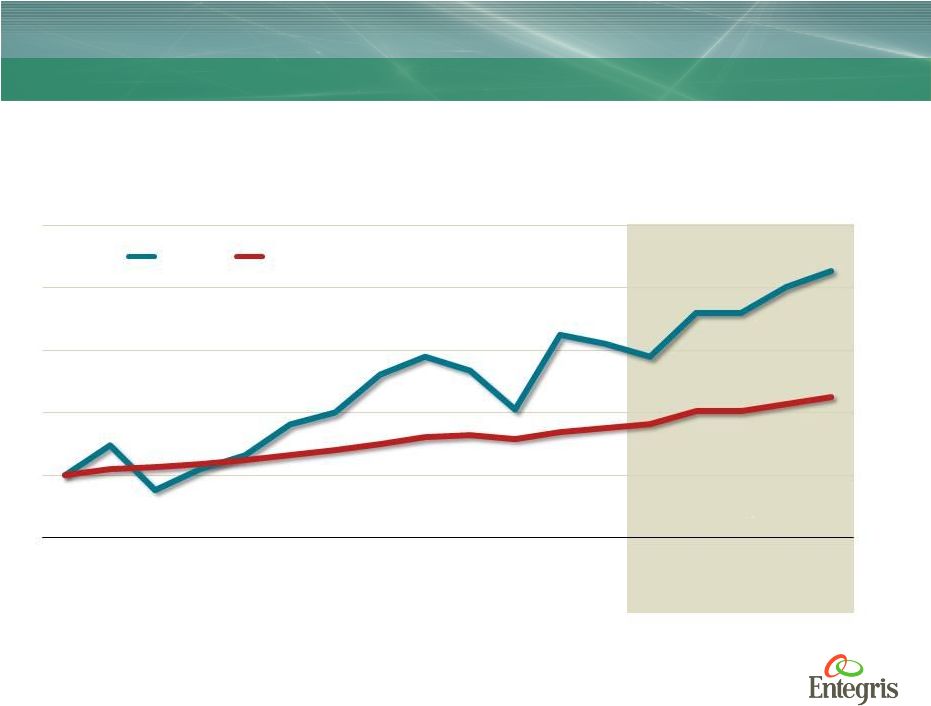

Analyst Day 2012 | 10 Why the Industry Will Continue to Grow Why the Industry Will Continue to Grow MSI = millions of square inches of silicon Source: Gartner, March 2012 Industry outperforms worldwide GDP Estimated 5-yr. CAGR = 5.1% 5-yr. CAGR = 3.3% 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 Worldwide Silicon Demand in MSI and Global GDP MSI GDP |

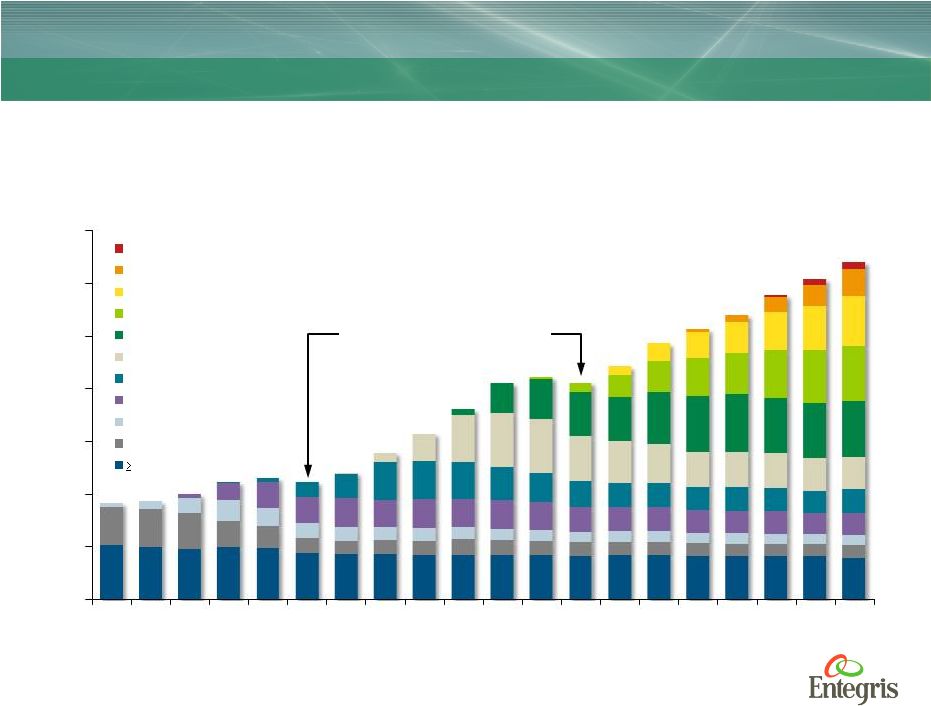

Analyst Day 2012 | 11 Why the Industry Will Continue to Grow Why the Industry Will Continue to Grow Source: Gartner, March 2012 Year-End Capacity by Linewidth (MSI/Quarter) Worldwide capacity increases through advanced technologies; maintains strong base at legacy nodes WW capacity has only contracted twice 0 500 1,000 1,500 2,000 2,500 3,000 3,500 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 MSI 15 nm 22 nm 32 nm 45 nm 65 nm 90 nm 130 nm 0.18 Micron 0.25 Micron 0.35 Micron 0.5 Micron |

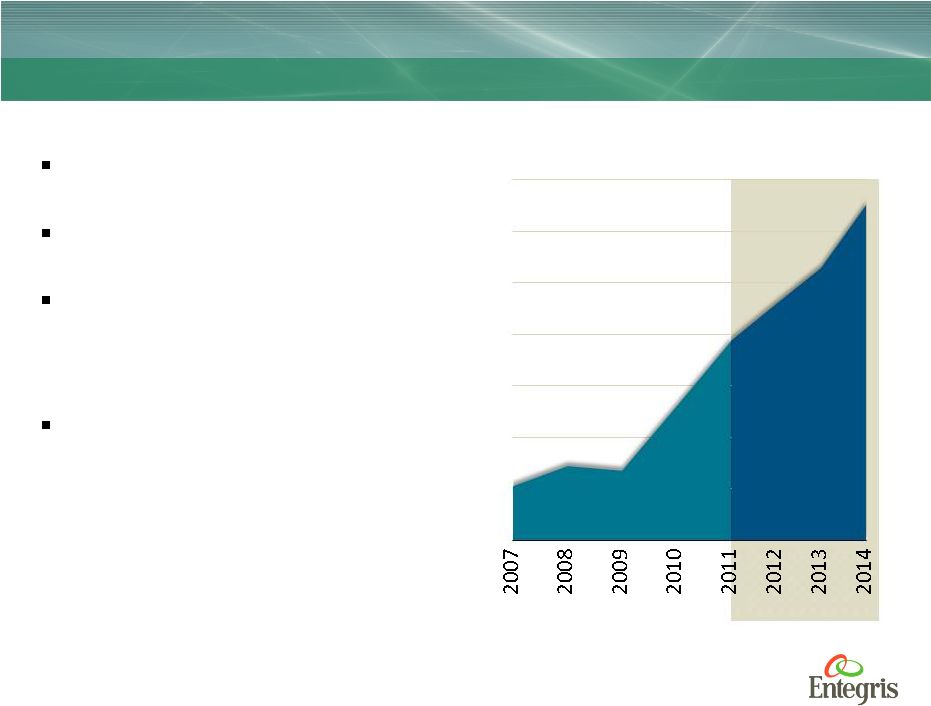

Analyst Day 2012 | 12 Revenue Drivers The Path to $1 Billion The Path to $1 Billion 1 Industry growth less ASP erosion. Based on $35B annual WFE Spend and 12.6B MSI market size in 2014 2 Semi Market initiatives in Wet Etch and Clean, Lithography, CMP and 450 mm 3 Incremental growth from market share gains in Solar, Life Sciences, LED, LiB, Aerospace, Alt Energy, Consumer Electronics and Optics Macro Industry Growth Semi Market Initiatives Non-Semi Market Expansion 1 2 3 $749 $90 $80 $80 ~$1B 2011 Revenue Macro Industry Growth Semi Market Initiatives Non-Semi Market Expansion 2014E |

Analyst Day 2012 | 13 When Will We Reach $1 Billion? When Will We Reach $1 Billion? Need strong industry environment Unit production of 12.6 billion in MSI (5-yr. CAGR = 5.1%) $35 billion in capital investment Continued strong execution New differentiated product solutions Expanding customer relationships Growing adjacent markets and acceptance of new solutions We believe we can achieve a $1 Billion run rate in 2014 organically |

Analyst Day 2012 | 14 What Makes Entegris Unique What Makes Entegris Unique Importance of what we do in the industry Increasing need for contamination control in advanced manufacturing Entegris is uniquely positioned in the industry Fully engaged with the industry market and technology leaders on key technologies including EUV, 3D and 450 mm Predominantly recurring, unit-driven business with a long tail of legacy products Ability to apply breadth of technology to adjacent areas Investing to extend our market and technology leadership and to increase future cash flows |

Bertrand Loy Executive Vice President and COO Bertrand Loy Executive Vice President and COO What Node Transitions Mean for Entegris What Node Transitions Mean for Entegris |

Analyst Day 2012 | 16 Key Points Key Points We are gaining share due to increased customer focus We are expanding the breadth and depth of our technology Our “seat at the table” is becoming bigger as our customers expect us to do more Increasing costs of next generations of technology are creating Darwinian pressure on the entire industry, particularly the supply chain We are confident about our long-term opportunities in Semi and in our adjacent markets |

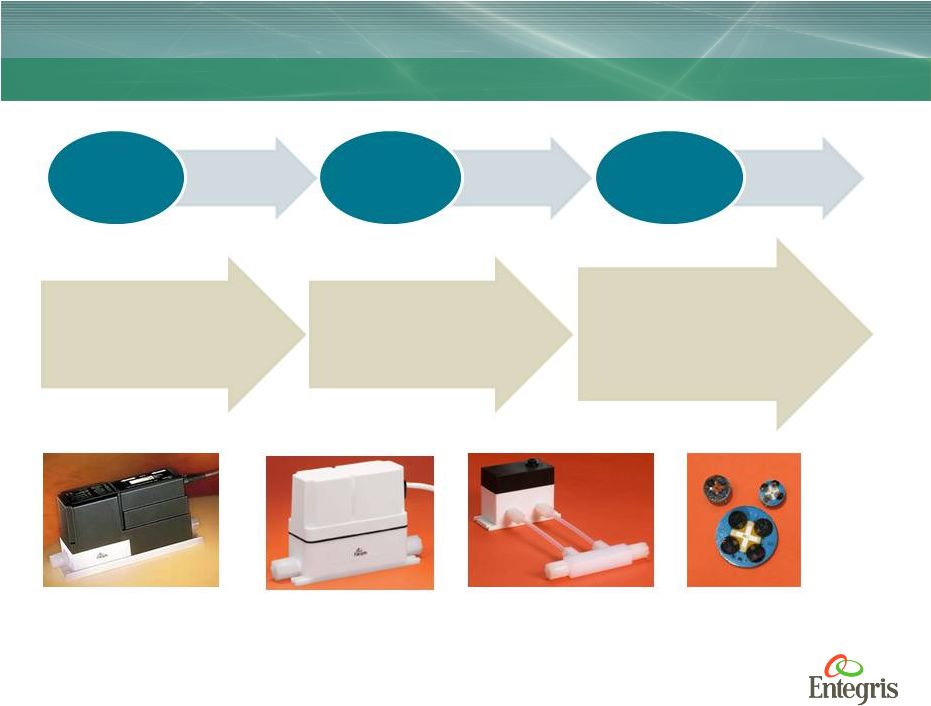

Analyst Day 2012 | 17 Breadth and Depth of Technology Breadth and Depth of Technology Microenvironments $182 M Wafer and Reticle Handling Specialty Materials $83 M Ion Implant, Dry Etch Contamination Control Solutions $484 M Lithography, WEC, CMP, Deposition 2011 Sales Process Application Product Platforms Graphite Components, Proprietary Coatings, E-Chucks FOUPs, Wafer Shippers, Wafer Carriers, Reticle Pods Valves, Fittings, Sensors, Dispense/Pumps Gas Purifiers, Purification Systems Liquid Filters, Gas Filters Wafer/Reticle Handling Advanced Materials Technology Filtration Purification Fluid Handling |

Analyst Day 2012 | 18 Contamination Control Solutions Contamination Control Solutions Focused on three rapidly growing process areas Wet etch and clean Lithography Chemical mechanical planarization $1.2B served available market Largest, rapidly growing, most profitable division Liquid Filtration Dispense/Pumps Gas Purification Fluid Handling Sensing and Control Containers Products Financial Highlights 28% 29% 12% $241 $436 $484 Revenue (in $M) Operating Margin (%) FY2009 FY2010 FY2011 |

Analyst Day 2012 | 19 Reticle Pods Carriers and shippers for handling wafers, reticles and other critical substrates Investing in advanced process carriers $400M served available market Solid cash generator Microenvironments Microenvironments 450 mm HVM MAC Products 300 mm+ Wafer Shipping 300 mm+ Wafer Handling Financial Highlights $111 $182 $182 FY2009 FY2010 FY2011 Revenue (in $M) Operating Margin (%) 21% 16% 2% |

Focused on high-temperature applications in semiconductor and adjacent markets $300M served available market Newest division with diversified opportunities for growth Specialty Materials Specialty Materials Premium Graphite and Silicon Carbide E-chucks Products/Technologies Coatings 16% 22% 9% Financial Highlights $46 $70 $83 0% 5% 10% 15% 20% 25% FY2009 FY2010 FY2011 Revenue (in $M) Operating Margin (%) Analyst Day 2012 | 20 |

Analyst Day 2012 | 21 Technology Advances Drive Demand Technology Advances Drive Demand Mobile apps, 3D TV 140 million active Twitter users Predictive safety systems OLED screens widespread HD video conferencing Cloud computing USB flash drives Broadband Streams to HDTVs China plans moon rover launch 3D technologies are widespread 200 megapixel camera Nano- hummingbird drone 185 billion mobile app downloads Terabyte SD cards 3G |

Analyst Day 2012 | 22 Technology Advances Drive Demand Technology Advances Drive Demand |

Analyst Day 2012 | 23 Cost per gate increases at 20 nm Technological Advancements are Now More Costly Technological Advancements are Now More Costly Source: International Business Strategies Inc 2012 2008 2006 2002 Wrong Trend Future Cost per Million Gates ($) 90 nm 65 nm 40 nm 28 nm 20 nm 14 nm .0636 .0521 .0362 .0267 .0275 .0278 |

Analyst Day 2012 | 24 A Massive Technology Shift Ahead A Massive Technology Shift Ahead Transistor Cost Scaling Factor Yield Optimization Wafer Cost EUV Litho Contamination Control 450 mm 90% 450 mm 300 mm |

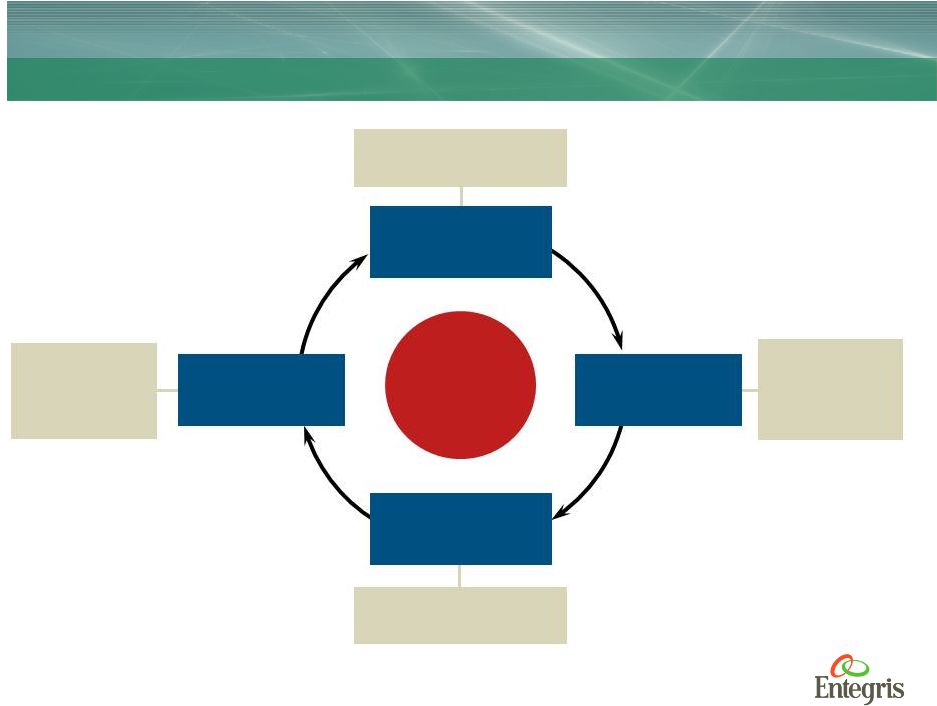

Analyst Day 2012 | 25 Direct Engagement by Engineering Teams Faster New Product Development Expand Applications Excellence Pilot Capability at Most Sites Customer shares sensitive product roadmap information Customer enters problem-solving relationship Customer provides feedback on prototype performance Customer views Entegris as solutions provider Our Business Model: Increasing Customer Intimacy – How It Works Our Business Model: Increasing Customer Intimacy – How It Works Relevant, Trusted, Technology Partner Application and Process Knowledge We Develop Relevant Final Solution We Listen We Respond Quickly with Prototypes |

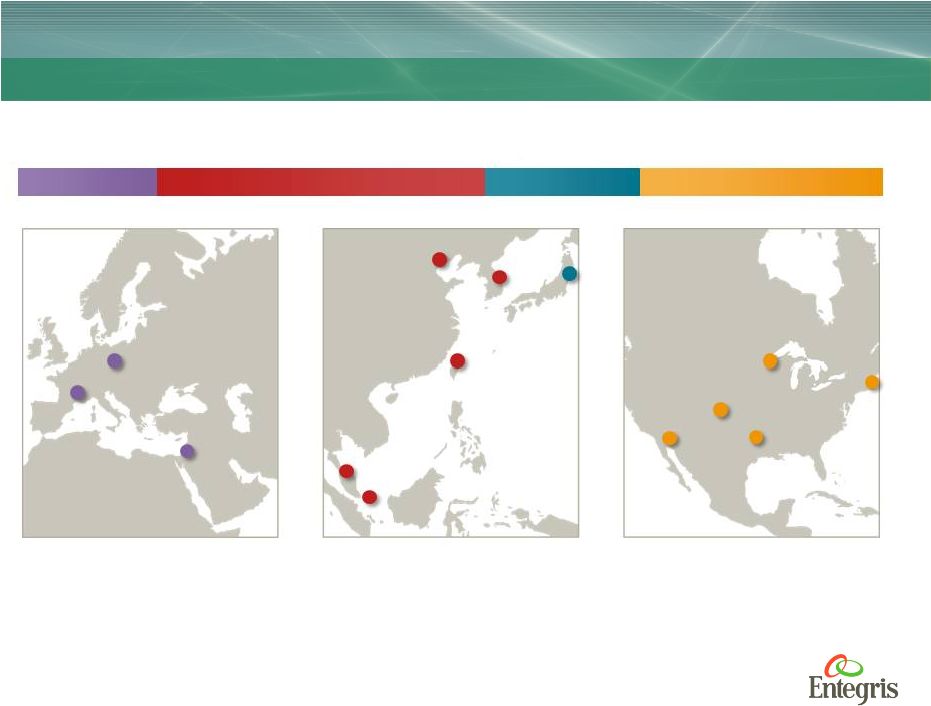

Analyst Day 2012 | 26 Strategically Augmenting Capabilities Close to Customers Strategically Augmenting Capabilities Close to Customers FY11 Sales by Region North America 29% Asia 38% Europe 14% Japan 19% R&D, manufacturing, sales and labs close to customers around the world Europe and Israel Asia and Japan North America Germany Israel France Singapore Malaysia China Korea Japan California Colorado Minnesota Texas Massachusetts Taiwan |

Analyst Day 2012 | 27 Europe and Israel Germany Israel France Strategically Augmenting Capabilities Close to Customers Strategically Augmenting Capabilities Close to Customers Europe COATINGS MANUFACTURING FACILITY Lyon, France |

Analyst Day 2012 | 28 Asia and Japan Singapore Malaysia China Korea Japan Taiwan TAIWAN SCIENCE PARK BRANCH Taiwan Strategically Augmenting Capabilities Close to Customers Strategically Augmenting Capabilities Close to Customers Asia PURELINE CO., LTD. An Entegris Company Korea |

Analyst Day 2012 | 29 Strategically Augmenting Capabilities Close to Customers Strategically Augmenting Capabilities Close to Customers North America North America California Colorado Minnesota Texas Massachusetts i2M CENTER FOR ADVANCED MATERIALS SCIENCE Massachusetts ADVANCED TECHNOLOGY CENTER Colorado |

Analyst Day 2012 | 30 R&D Leveraged to Key Technology Trends R&D Leveraged to Key Technology Trends EUV 3D New Materials 450 mm Filtration Purification Fluid Handling Wafer/Reticle Handling Advanced Materials/Coatings Entegris Technologies Key Technology Trends Increasing focus on JDAs and partnerships |

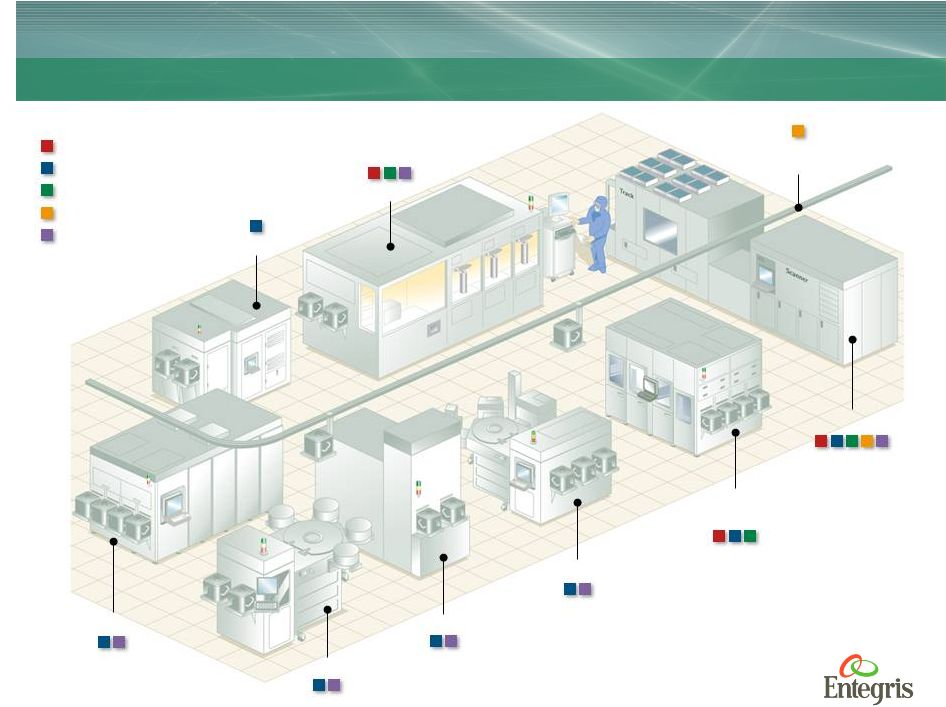

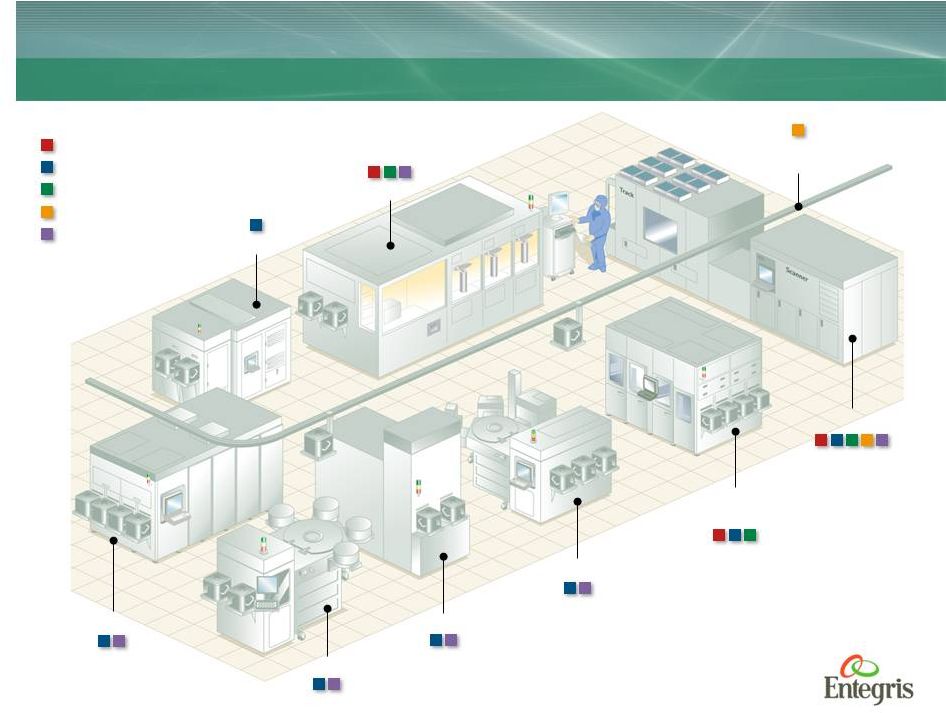

Entegris’ Technologies Touch All Fab Critical Processes Entegris’ Technologies Touch All Fab Critical Processes Filtration Fluid Handling Wafer Handling Purification Advanced Materials Diffusion CVD Ion Implant Metrology Overhead Transport System Wet Etch and Clean CMP Dry Etch Lithography Analyst Day 2012 | 31 |

Analyst Day 2012 | 32 Leveraging Entegris Technologies into Adjacent Markets Leveraging Entegris Technologies into Adjacent Markets Semi Flat Panel PV Solar Data Storage Compound Semi / LED Energy Storage Life Sciences Adjacent markets moving closer in process control and purity requirements Leveraging current Entegris technologies into adjacent markets Non-Semi Semi 70% 2011 Sales by Market 70% |

Analyst Day 2012 | 33 A Portfolio of Opportunities in Adjacent Markets A Portfolio of Opportunities in Adjacent Markets Comp Semi/LED PV Solar Aerospace |

Analyst Day 2012 | 34 A Portfolio of Opportunities in Adjacent Markets A Portfolio of Opportunities in Adjacent Markets Gas purification systems for the MOCVD process Entegris Solution Process gas purity has been shown to increase yields in HBLEDs Customer Issue Comp Semi/LED PV Solar Aerospace |

Analyst Day 2012 | 35 A Portfolio of Opportunities in Adjacent Markets A Portfolio of Opportunities in Adjacent Markets Gas and liquid filtration combined with ultra-high purity components Process gas purity has been shown to increase yields in HBLEDs Gas purification systems for the MOCVD process Entegris Solution Customer Issue Reducing contaminants in process fluids improves PV cell efficiencies Comp Semi/LED PV Solar Aerospace |

Analyst Day 2012 | 36 A Portfolio of Opportunities in Adjacent Markets A Portfolio of Opportunities in Adjacent Markets Entegris Solution Gas and liquid filtration combined with ultra-high purity components Specialized graphite bushings, rings and air seals replace existing materials Reducing contaminants in process fluids improves PV cell efficiencies Customer Issue Process gas purity has been shown to increase yields in HBLEDs High temperatures in jet engines require enhanced material performance Gas purification systems for the MOCVD process Comp Semi/LED PV Solar Aerospace |

Analyst Day 2012 | 37 Positioned for Growth Positioned for Growth The technology changes facing our industry over the next five years are massive Contamination control is becoming even more critical to the industry We are working more closely than ever with our customers We are investing to fully realize both our near-term and long-term opportunities Adjacent markets will recover and will continue to offer paths for growth |

Todd Edlund Vice President and General Manager, CCS Division Todd Edlund Vice President and General Manager, CCS Division Delivering Higher Value at Advanced Nodes Delivering Higher Value at Advanced Nodes |

Analyst Day 2012 | 39 Contamination Control Solutions Division – Focus on Growth Contamination Control Solutions Division – Focus on Growth Bring greater value and additional product solutions to growing semi processes Wet Etch and Clean Lithography CMP Apply solutions to other challenging markets Growth Drivers CCS is uniquely positioned to control contamination from production of raw chemicals to point of use |

Entegris’ Technologies Touch All Fab Critical Processes Entegris’ Technologies Touch All Fab Critical Processes Filtration Fluid Handling Wafer Handling Purification Advanced Materials Diffusion CVD Ion Implant Metrology Overhead Transport System Wet Etch and Clean CMP Dry Etch Lithography Analyst Day 2012 | 40 |

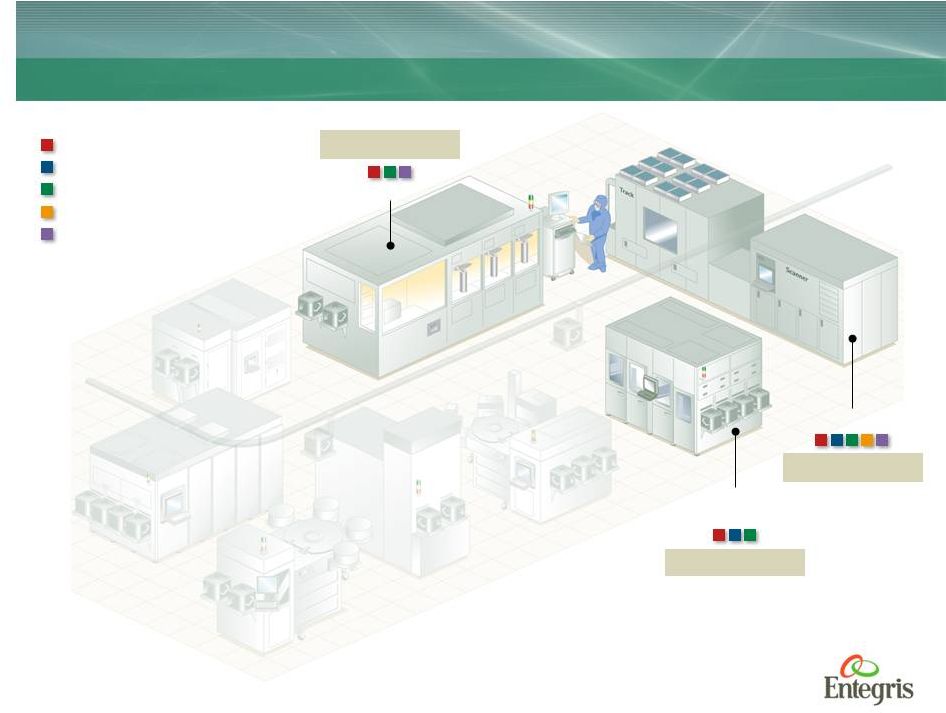

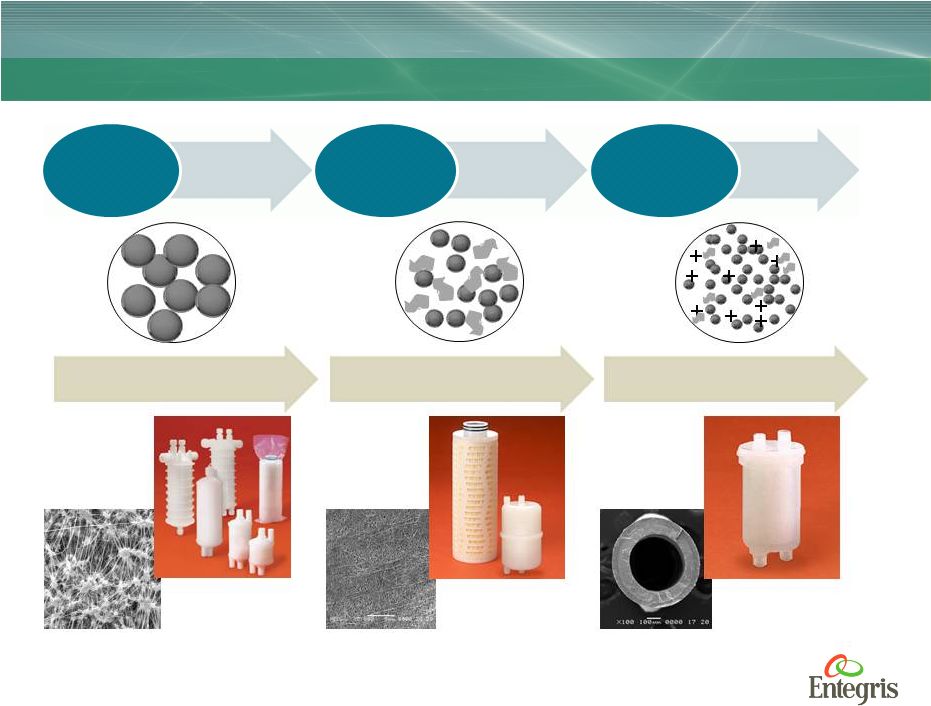

Three Key Process Areas for Entegris Three Key Process Areas for Entegris Lithography Wet Etch and Clean CMP 26% CCS Revenue 28% CCS Revenue 7% CCS Revenue Filtration Fluid Handling Wafer Handling Purification Advanced Materials Analyst Day 2012 | 41 |

Analyst Day 2012 | 42 Advancing Technology Nodes Drive Our Product Demands Advancing Technology Nodes Drive Our Product Demands Litho WEC CMP 193 nm 6X nm – 4X nm 193 nm Immersion Double Patterning 3X nm – 2X nm Multiple Patterning 193 nm/DSA EUV/DSA <2X nm High Concentration Recirculation / Batch 6X nm – 4X nm Weaker Concentration Mixed Batch / Single Wafer 3X nm – 2X nm Ultra Dilute Specialized Cleaning Single Wafer <2X nm Glass (oxide) Tungsten <90 nm Glass (oxide) Tungsten Cu, STI Polysilicon 90-6X nm Glass (oxide) Tungsten Cu, STI Polysilicon Cu LK Cap LK 6X-4X nm Glass (oxide) Tungsten Cu, STI Polysilicon Cu LK Cap LK Metal Gates 4X-2X nm Glass (oxide) Tungsten Cu, STI Polysilicon Cu LK Cap LK Metal Gates High K 3D packaging TSV ... 2X-1X nm Analyst Day 2012 | 42 |

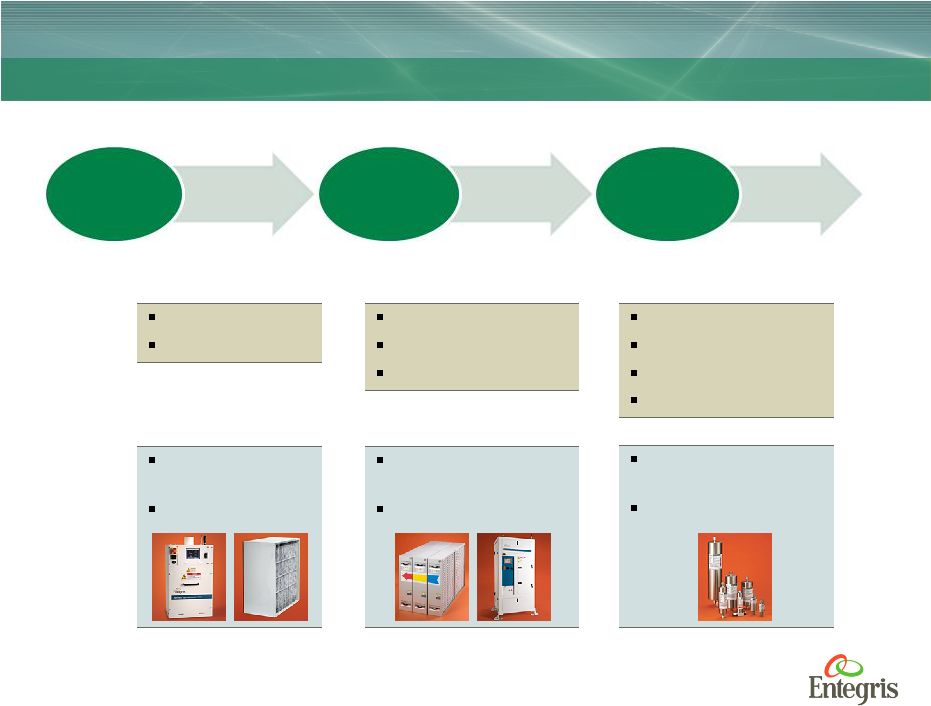

Analyst Day 2012 | 43 Photolithography Solutions: Blanketing the Process Photolithography Solutions: Blanketing the Process Valves Fittings Pumps POU filters Gas filters Chemical filters HUGs Reticle pods UPW purification systems Scanning mirrors |

Analyst Day 2012 | 44 ArF Immersion ppt detection CO 2 gas purification Many contaminants Multi-gas purification systems Asymmetric AMC filters Litho Technology Driving Gas Contamination Control Solutions Litho Technology Driving Gas Contamination Control Solutions Challenges Entegris Solutions EUV/others? Vacuum environment Component outgassing Numerous purge gases ppt validation ppt purifier media validation in vacuum ppt outgassing particle filters ArF, KrF Dry Sub ppb detection Few contaminants Gas purification systems AMC filters 6X nm – 4X nm 193 nm 3X nm – 2X nm 193 nm Immersion Double Patterning <2X nm Multiple Patterning 193 nm/DSA EUV/DSA |

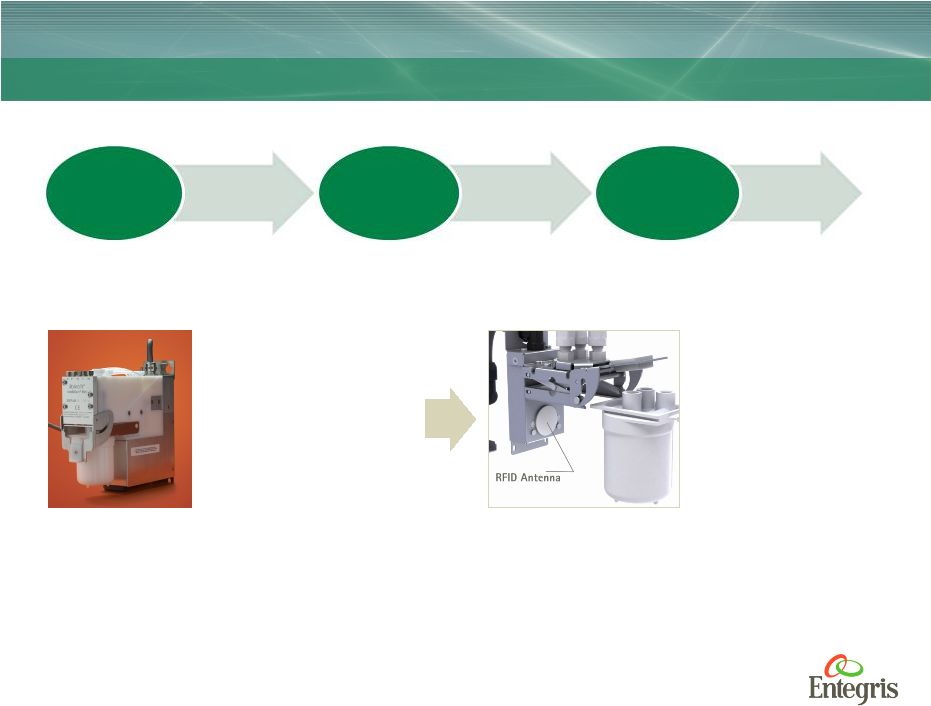

Analyst Day 2012 | 45 Dispense and Filtration Combination: Increasing Throughput and Yield and Decreasing Waste Dispense and Filtration Combination: Increasing Throughput and Yield and Decreasing Waste Combining two-stage filtration/dispense and asymmetric filters to reduce microbridging Leveraging RFID smart technology to rapidly eliminate defect-causing microbubbles 6X nm – 4X nm 193 nm 3X nm – 2X nm 193 nm Immersion Double Patterning <2X nm Multiple Patterning 193 nm/DSA EUV/DSA |

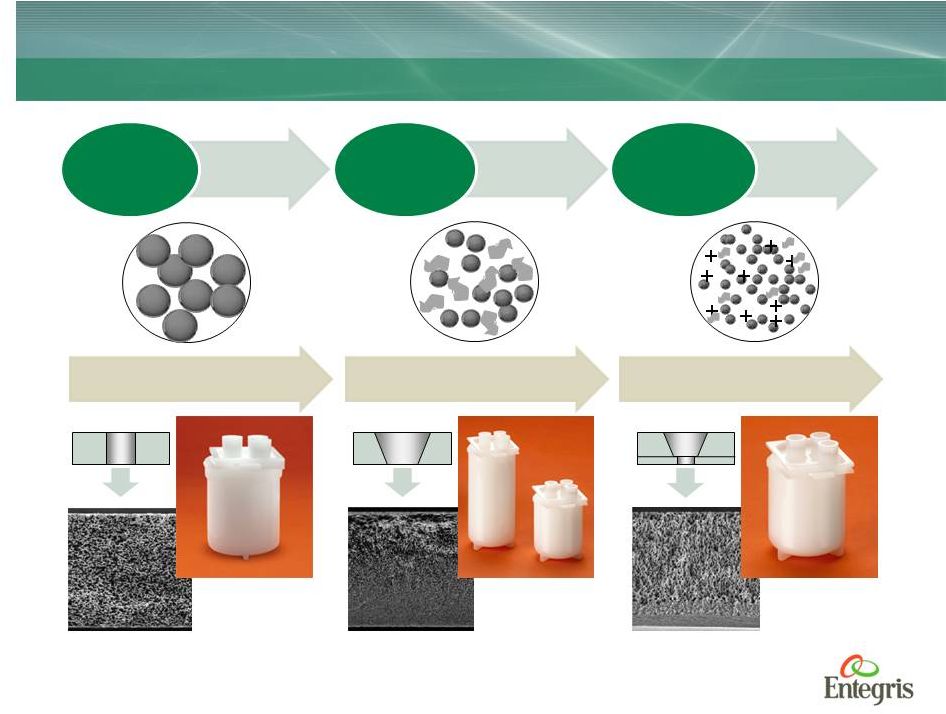

Photochemical Filtration Challenges and Solutions Photochemical Filtration Challenges and Solutions 3 and 5 nm UPE/Duo Filtration 50 nm UPE Symmetric Membrane Selective Nano Filtration/ Purification Impact 2 UPE Impact 8G UPE/DUO Impact SNFP 193 nm 193 nm Immersion Double Patterning Multiple Patterning 193 nm/DSA EUV/DSA 6X nm – 4X nm 3X nm – 2X nm <2X nm Analyst Day 2012 | 46 |

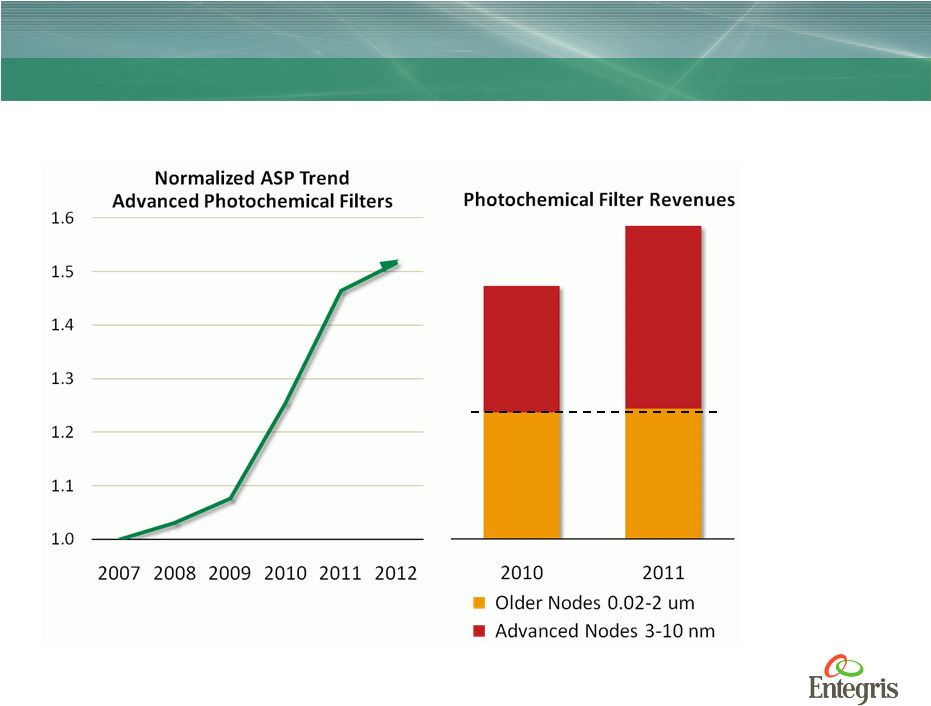

Analyst Day 2012 | 47 Photochemical Filtration Delivering Higher Value to Customers Photochemical Filtration Delivering Higher Value to Customers Advanced Nodes Grew >44% Older Nodes 1.5X ASP |

Wet Etch and Clean Solutions: Production to Consumption Wet Etch and Clean Solutions: Production to Consumption Valves Fittings Liquid filters Flow control Containers Manifolds Analyst Day 2012 | 48 |

Analyst Day 2012 | 49 Dilute Chemistries/ Etch Control Process Flexibility In-line Mixing Particle Generation Higher Temperatures Selective Etching / Precise Cleaning Tighter Control for Resource Reduction Evolving Challenges for Wet Etch and Clean Applications Evolving Challenges for Wet Etch and Clean Applications NT6500 NT6510 Sensor Technology NT6510 Phase II NT4401 Sensing and Control Solutions 6X nm – 4X nm High Concentration Recirculation / Batch 3X nm – 2X nm Weaker Concentration Mixed Batch / Single Wafer <2X nm Ultra Dilute Specialized Cleaning Single Wafer |

Analyst Day 2012 | 50 Wet Etch and Clean Revenue: Sensing and Control Wet Etch and Clean Revenue: Sensing and Control Entegris benefits from WEC move to sophisticated flow control 0.0 0.5 1.0 1.5 2.0 2.5 2006 2007 2008 2009 2010 2011 Normalized Sensing and Control Revenues |

Analyst Day 2012 | 51 Evolving Contamination Control Challenges for WEC Applications Evolving Contamination Control Challenges for WEC Applications QuickChange ATM/ATE Symmetric PTFE Media Asymmetric PTFE Media Asymmetric Hollow Fiber Torrento AT3 Protego Plus LTX POU Nozzle Filters Protego IPA Protego Chemical 20-15 nm Filtration Metal Ion Removal – DIW 50-30 nm Filtration <10 nm Filtration Metal Ion Removal – Chemicals 6X nm – 4X nm High Concentration Recirculation / Batch 3X nm – 2X nm Weaker Concentration Mixed Batch / Single Wafer <2X nm Ultra Dilute Specialized Cleaning Single Wafer |

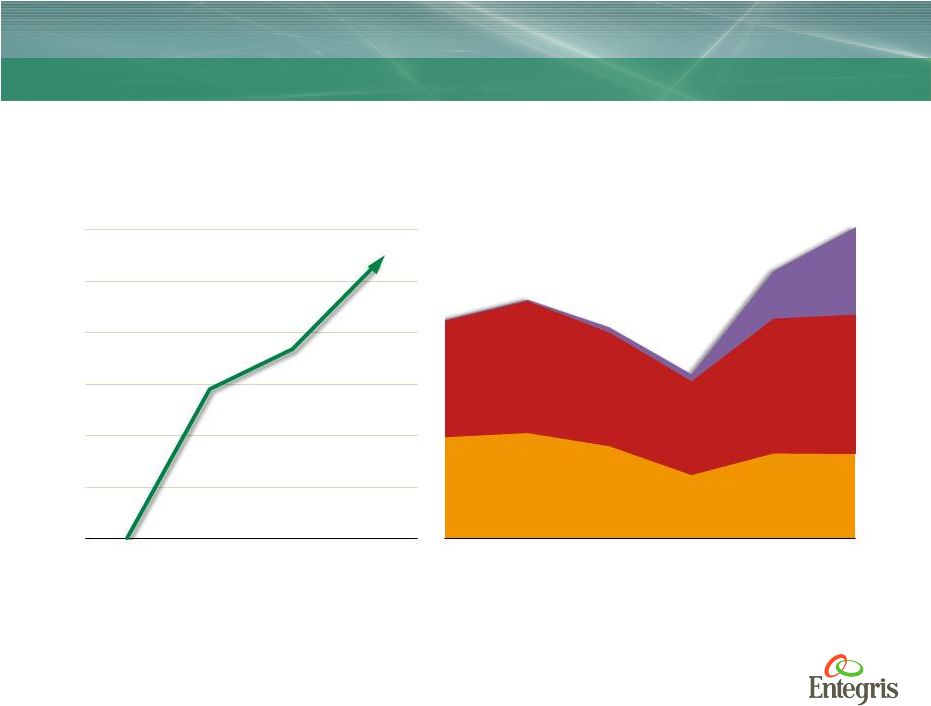

Analyst Day 2012 | 52 WEC Filtration Value Growing with Advanced Technology WEC Filtration Value Growing with Advanced Technology 2X ASP <0.1 um >20 nm 0.1 um and larger 20 nm and below 1.0 1.2 1.4 1.6 1.8 2.0 2.2 2006 2008 2010 2012 2006 2007 2008 2009 2010 2011 Normalized ASP Advanced Filters Advanced Solutions Impact on Filter Revenues Trend |

Analyst Day 2012 | 53 Total CMP Solutions: Room to Grow our SAM Total CMP Solutions: Room to Grow our SAM Filters Flow control PVA brushes Valves Fittings Containers Coatings |

Analyst Day 2012 | 54 Advanced production line Ultraclean materials High cleaning efficiency / low defects Particle cleaning Organic residue cleaning Minimize induced defect Consistent cleaning Longer life Post CMP Clean Brush: Establishing New SAM Post CMP Clean Brush: Establishing New SAM Glass (oxide) Tungsten Cu, STI Polysilicon Cu LK Cap LK 6X-4X nm Glass (oxide) Tungsten Cu, STI Polysilicon Cu LK Cap LK Metal Gates 4X-2X nm Glass (oxide) Tungsten Cu, STI Polysilicon Cu LK Cap LK Metal Gates High K 3D packaging TSV ... 2X-1X nm Analyst Day 2012 | 54 |

Analyst Day 2012 | 55 CMP Pad Conditioner: Combining Capabilities to Expand our SAM CMP Pad Conditioner: Combining Capabilities to Expand our SAM Diamond film grown on substrate Eliminates contamination and diamond loss issues 2-3x longer lifetime than diamond grit Easily tunable for each process, slurry and pad Yield: Metal contamination Scrap: Diamond loss COO: Short lifetime Inside 2000°C CVD Reactor New Technology: CVD Diamond Film Diamond Grit Conditioner Optimized Conditioners for Each Process Hitting the Wall 6X-4X nm Glass (oxide) Tungsten Cu, STI Polysilicon Cu LK Cap LK 4X-2X nm Glass (oxide) Tungsten Cu, STI Polyilicon Cu LK Cap LK Metal Gates 2X-1X nm Glass (oxide) Tungsten Cu, STI Polysilicon Cu LK Cap LK Metal Gates High K 3D packaging TSV ... |

Analyst Day 2012 | 56 Entegris R&D Infrastructure Serves Our Diverse Solution Set Entegris R&D Infrastructure Serves Our Diverse Solution Set IMEC, IBM, several universities and customer joint developments address emerging needs and work on yield and efficiency improvements Partnerships |

Analyst Day 2012 | 57 The New i2M Center for Advanced Materials Science The New i2M Center for Advanced Materials Science Bedford, MA $55M to $60M investment 100 employees Purpose-built for coming generation of nano level capabilities Advanced membrane/separation media manufacturing and R&D – liquid and gas applications Advanced specialty coating manufacturing and R&D New synergistic products Commitment to investing in critical capabilities around clean materials and leading-edge contamination control solutions |

Analyst Day 2012 | 58 Advancing Customer Demands Play to Our Strengths Advancing Customer Demands Play to Our Strengths Challenging contamination control demands at advanced nodes are driving up the value of what we do Entegris is already delivering solutions that are being quickly adopted for use in key semiconductor processes We’re uniquely positioned to deliver comprehensive solutions from material production to consumption Applicable to new market space We will make appropriate investments to support the customers that are setting the pace for the industry |

Greg Morris Vice President and General Manager, Global Field Operations Greg Morris Vice President and General Manager, Global Field Operations Why We Are Winning in the Market Why We Are Winning in the Market |

Analyst Day 2012 | 60 Across the Semiconductor Ecosystem Across the Semiconductor Ecosystem Device Makers OEMs Materials Suppliers Foundries Logic Memory OEM Tool Co’s Wafer Growers Chemical Co’s R&D Consortia Eng. Contractors Materials Suppliers 18% Device Makers 53% OEMs 26% Semiconductor-related sales by key customer type Other 3% Note: Data reflects sales for FY2011 |

Analyst Day 2012 | 61 Only a Handful of Companies Can Afford to Drive Industry Technology Roadmap Only a Handful of Companies Can Afford to Drive Industry Technology Roadmap Source: Gartner, March 2012 Fewer fabs can afford cost of next generation Top three IDMs (Samsung, Intel and TSMC) control half of total industry spending in 2012 Top ten control approximately 60% of global capacity More logic IDMs go fabless More tech partners and joint ventures Device makers are managing their technology roadmaps and supply chains more globally |

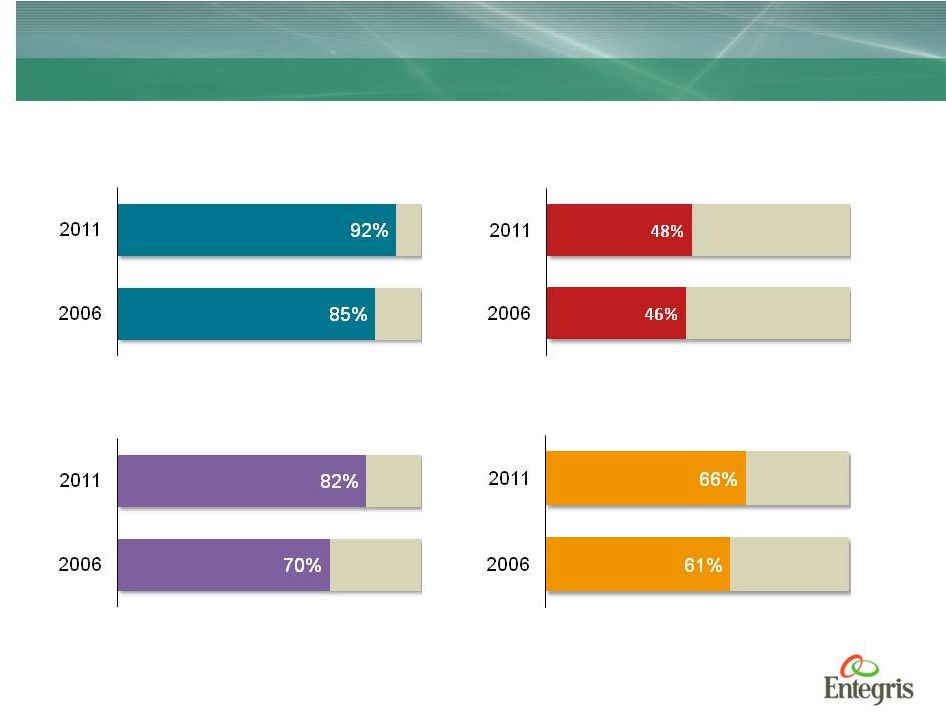

Our Changing Market Dynamics – Consolidation of OEMs Our Changing Market Dynamics – Consolidation of OEMs Source: Gartner, March 2012 and April 2007 Market Share of Top 2 Lithography Tool OEMs Market Share of Top 2 Etch/CMP Tool OEMs Market Share of Top 2 RTP/Diffusion Tool OEMs Market Share of Top 2 Ion Implant Tool OEMs Analyst Day 2012 | 62 |

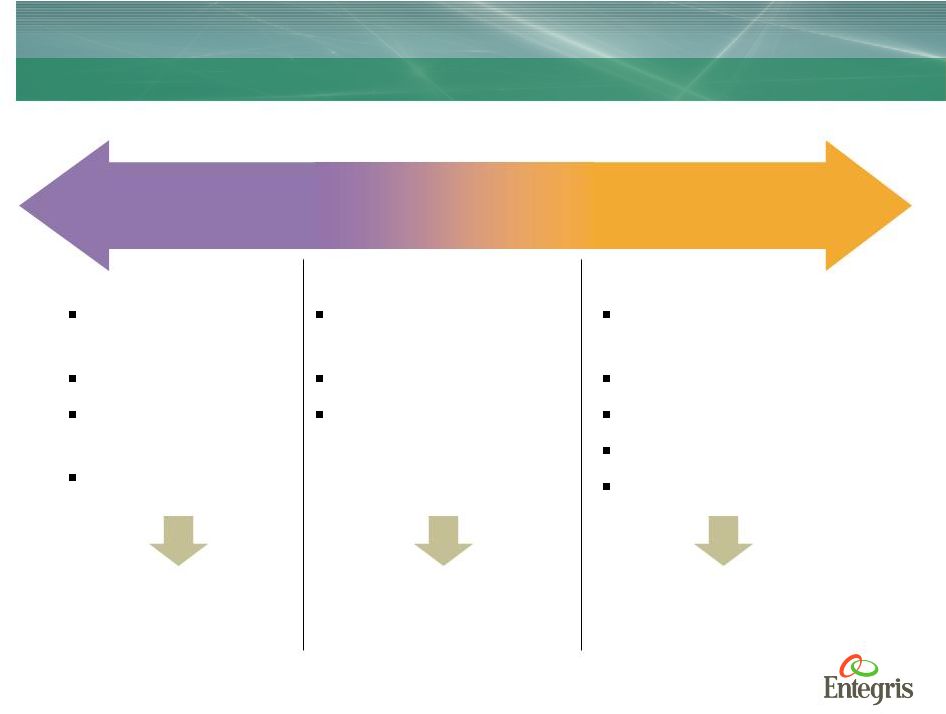

Analyst Day 2012 | 63 Focusing Our Resources On the Most Strategic and Critical Customers Focusing Our Resources On the Most Strategic and Critical Customers Unclear commitment to ITRS Regional powerhouses “Opportunity enablers” Tier 2 Tier 1 General Sales Force Companies committed to ITRS Financially strong Market leaders Global and complex Increasingly demanding Strategic and Critical Dedicated Sales Account Teams Technology follower Migrating to fabless Weaker financial position Local Tier 3 Sales Channel Partner |

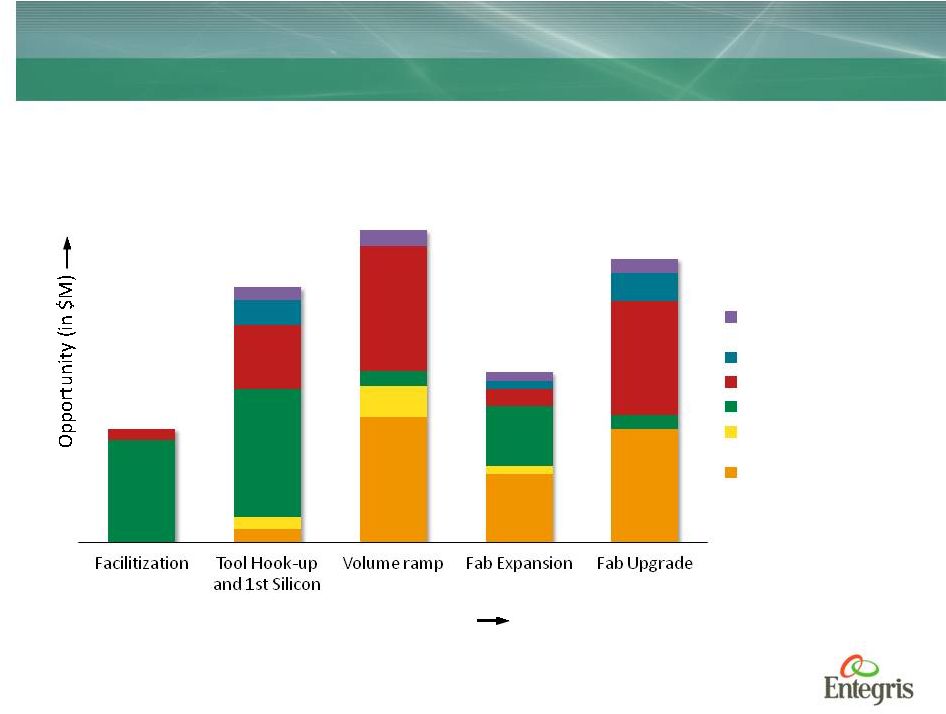

Entegris is Leveraged Throughout the Fab Life Cycle Entegris is Leveraged Throughout the Fab Life Cycle Our solutions have a critical role in volume ramp and fab upgrades Entegris Sales Opportunity by Product Advanced Materials and Coatings Purification Filtration Fluid Handling Wafer Handling: Shippers Wafer Handling: FOUP Fab Life Cycle (Time) Analyst Day 2012 | 64 |

Analyst Day 2012 | 65 Our Business Model: Increasing Customer Intimacy to Increase Share Our Business Model: Increasing Customer Intimacy to Increase Share Pilot Capability at Most Sites Customer provides feedback on prototype performance We Respond Quickly with Prototypes Customer enters problem-solving relationship Engagement by Engineering Direct Teams Relevant, Trusted, Technology Partner Expand Applications Excellence Product Faster New Development Relevant Final Solution We Develop We Listen Customer shares sensitive product roadmap information Process Knowledge Application and Customer views Entegris as solutions provider |

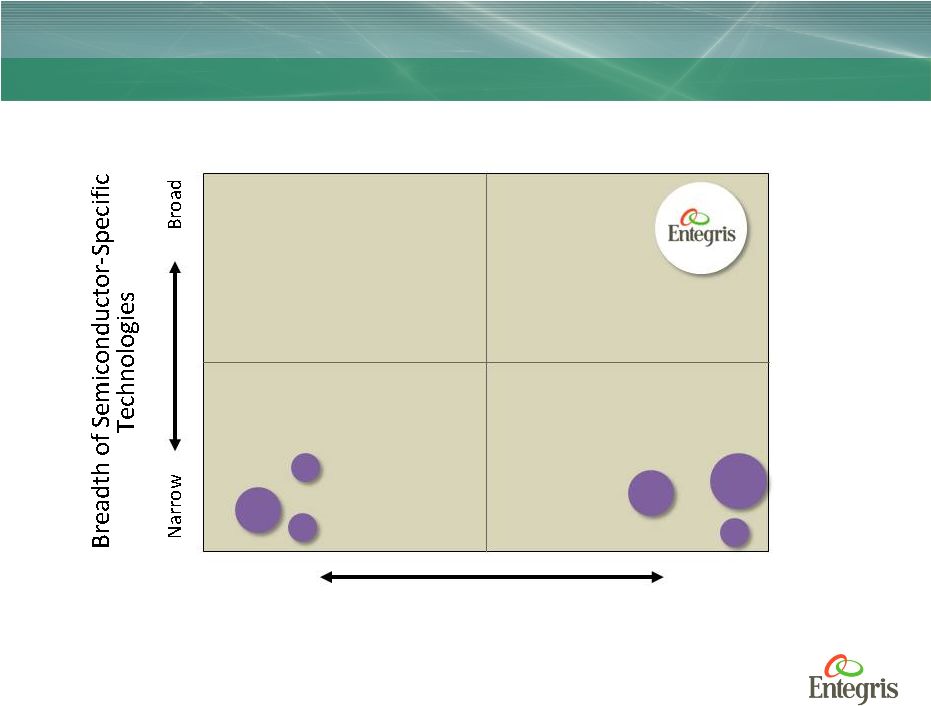

Analyst Day 2012 | 66 Global Footprint and Breadth of Technology Provide Unique Competitive Position Global Footprint and Breadth of Technology Provide Unique Competitive Position Infrastructure/Footprint Global Regional SAES GEMU Miraial Pall Parker SEP |

Cross contamination, moisture control and particle reduction at 32 nm created new technical requirements We demonstrated our understanding of problem with our ongoing work with OEMs, consortia and technology leaders Our investments through the last cycle yielded the right technology at the right time Advanced FOUPs at fab customer Market Share Wins: The Right Technology at the Right Time Market Share Wins: The Right Technology at the Right Time Device Makers Analyst Day 2012 | 67 |

Leading fabs consulted with Entegris regarding yield issues occurring during ramp of 32 nm and 28 nm processes We quickly delivered our Torrento® filter for wet etch and clean processes Torrento uses Entegris’ membrane and surface modification expertise to provide the most advanced product on the market for this application Advanced wet etch and clean filtration for fab customers Market Share Wins: Offering the Most Pure Solutions Market Share Wins: Offering the Most Pure Solutions Device Makers Analyst Day 2012 | 68 |

Analyst Day 2012 | 69 Advanced ion implant processes require chamber components and materials that can withstand high temperature and corrosion We used our proprietary coatings technology to develop the market-leading cleaning and coating solution for e-chucks Our deep understanding of the OEMs’ required technology enabled us to gain share in other advanced materials product areas Advanced coatings at OEM customer Market Share Wins: Understanding Customer Needs Enables Share Gains in Other Areas Market Share Wins: Understanding Customer Needs Enables Share Gains in Other Areas OEMs |

Analyst Day 2012 | 70 Higher levels of purity of all chemicals is required for 2X technology nodes Chemical suppliers require that new container solutions also seamlessly fit with existing fab connections Entegris offers the most pure container solutions By meeting all country-specific transportation standards prior to product launch, Entegris’ solutions speed user deployment New container solutions for materials customers Market Share Wins: Offering the Most Pure Solutions Market Share Wins: Offering the Most Pure Solutions Materials Suppliers |

Analyst Day 2012 | 71 In Summary In Summary Customer consolidation in our markets is providing opportunities to leverage technology and product breadth and global footprint We’ve aligned our field operations to focus on the most impactful customers We’re winning in the market by increasing our intimacy with key customers |

Greg Graves Executive Vice President and CFO Greg Graves Executive Vice President and CFO What This Means for Investors What This Means for Investors |

Analyst Day 2012 | 73 Record sales of $749M in 2011 Grew faster than our markets and our peers Record operating profit Achieved target model Record cash flow from operations The 2011 Scorecard: Building on Another Great Year The 2011 Scorecard: Building on Another Great Year Cash balance exceeding $265 million Zero debt Strengthened Financial Position Superior Profitability Superior Growth |

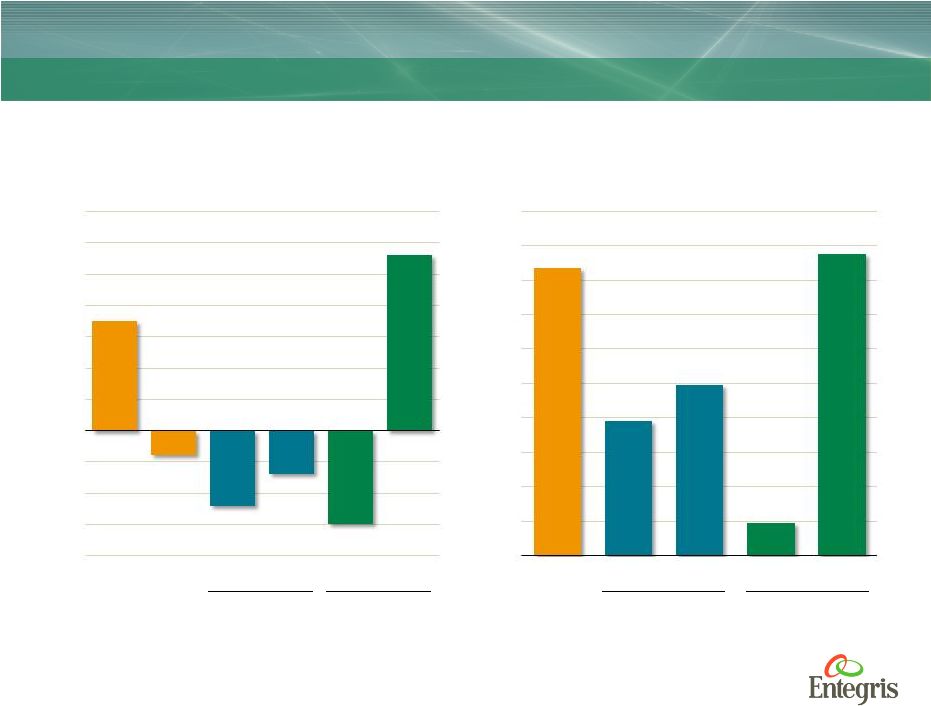

Analyst Day 2012 | 74 Strong Relative Revenue Growth Strong Relative Revenue Growth 2011 revenue growth vs. peers *Comparable weighted average growth rate based on 65% unit-driven and 35% capital-driven Capital-Driven Peers Unit-Driven Peers -6% -4% -2% 0% 2% 4% 6% 8% 10% 12% 14% Entegris Comp Avg* Company A Company B Company C Company D |

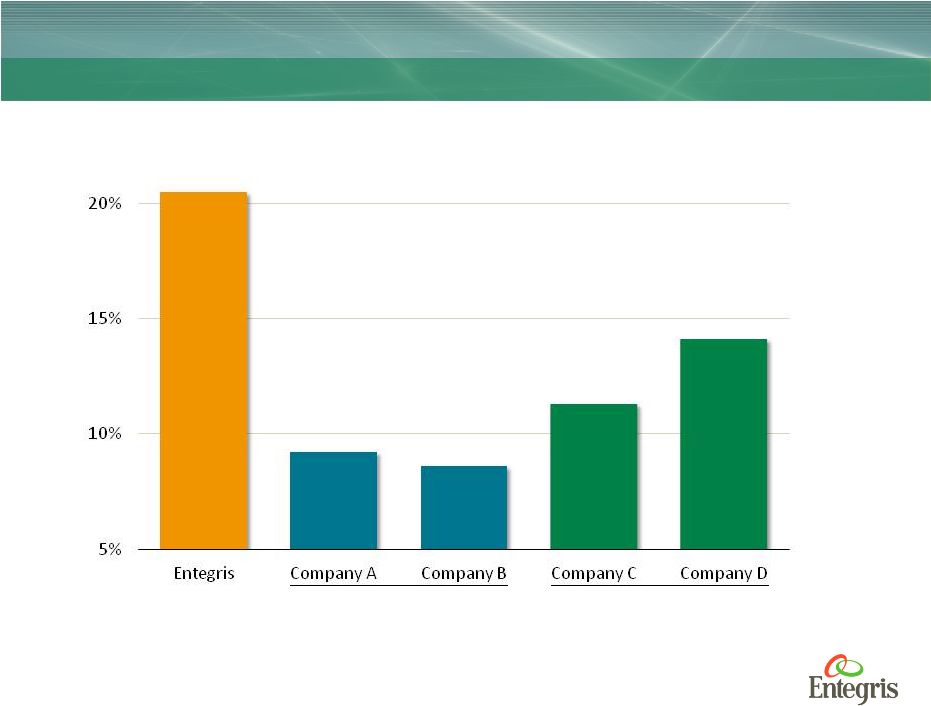

Analyst Day 2012 | 75 Strong Relative Profitability Strong Relative Profitability 2011 operating margin (EBITA) vs. peers Capital-Driven Peers Unit-Driven Peers 5% 10% 15% 20% Entegris Company A Company B Company C Company D |

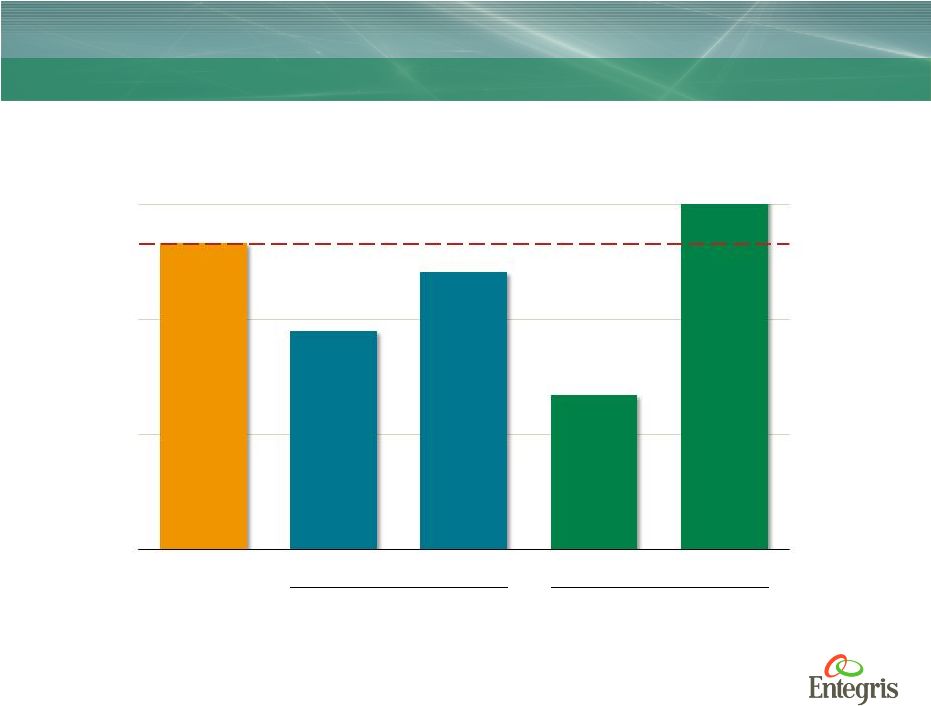

Analyst Day 2012 | 76 Best-in-Class Return on Invested Capital Best-in-Class Return on Invested Capital 2011 ROIC vs. peers Capital-Driven Peers Unit-Driven Peers |

Analyst Day 2012 | 77 Q1-12 Revenue Growth vs. Peers Strong Performance Continues in 2012 Strong Performance Continues in 2012 *Comparable weighted average growth rate based on 65% unit-driven and 35% capital-driven Capital-Driven Peers Unit-Driven Peers Q1-12 Operating Margin (EBITA) vs. Peers Capital-Driven Peers Unit-Driven Peers -8% -6% -4% -2% 0% 2% 4% 6% 8% 10% 12% 14% Entegris Comp Avg* Comp A Comp B Comp C Comp D 0% 2% 4% 6% 8% 10% 12% 14% 16% 18% 20% Entegris Comp A Comp B Comp C Comp D |

Analyst Day 2012 | 78 Achieved Target Model Every Quarter Since Introduction Achieved Target Model Every Quarter Since Introduction Percent Sales 0% 5% 10% 15% 20% 25% Q3-09 Q4-09 Q1-10 Q2-10 Q3-10 Q4-10 Q1-11 Q2-11 Q3-11 Q4-11 Q1-12 Target Operating Model % Actual Operating Margin (EBITA) |

Analyst Day 2012 | 79 Well Positioned to Continue to Perform: Division Portfolio Well Positioned to Continue to Perform: Division Portfolio CCS High growth driven by increasing contamination control requirements 23% - 28% High investment to sustain superior growth and margins High-Profit Growth Engine ME Mature market gains at larger diameters; offset by declines in 200 mm and below 14% - 19% Minimal investment beyond 450 mm and EUV Pods High Cash Flow SMD Growth in adjacent markets and geographic expansion 15% - 20% Modest investment to expand materials capabilities and reach beyond North America Diversified Growth Growth Profile Operating Margin at Mid-cycle Portfolio Position Investment 2008 2011 2008 2011 2008 2011 CAGR: 13.5% CAGR: -1.5% CAGR: 3.9% $484 $331 $74 $83 $182 $191 |

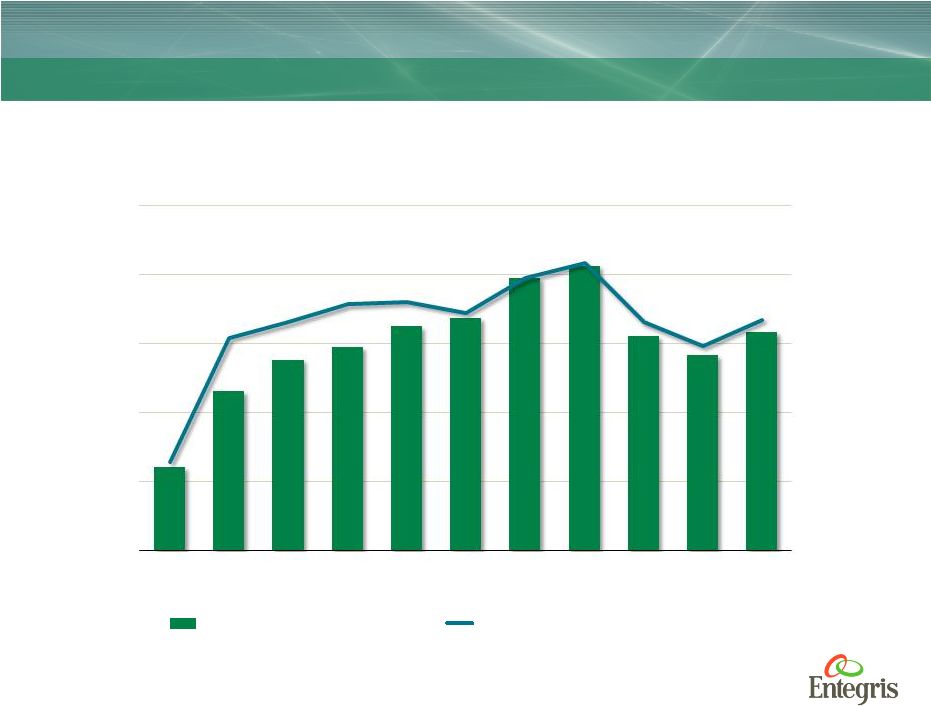

Analyst Day 2012 | 80 Well Positioned to Continue to Perform: Largely Unit-Driven Business Provides a Stable, Growing Base Well Positioned to Continue to Perform: Largely Unit-Driven Business Provides a Stable, Growing Base Source: Gartner March 2012 Entegris Quarterly Revenue Contribution ($M) Capex-Driven Sales Unit-Driven Sales 2007 2008 2009 2010 2011 2012 Revenue per MSI has increased over time Approximately two thirds of Entegris revenue is driven by wafer starts Entegris Unit-Driven Revenue per MSI 2007 2008 2009 2010 2011 2012 Average Range: $4-5 $0 $1 $2 $3 $4 $5 $6 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 0 50 100 150 $200 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 |

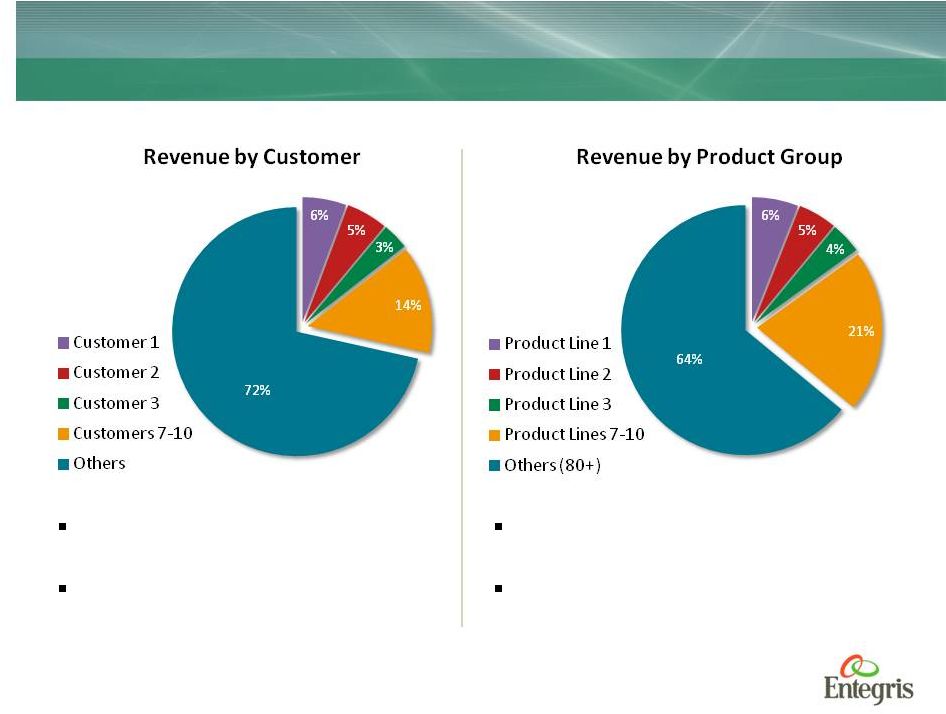

Well Positioned to Continue to Perform: Customer and Product Diversification Contribute to Stability Well Positioned to Continue to Perform: Customer and Product Diversification Contribute to Stability Our largest customers are typically only 5% to 7% of total revenue Our top ten customers are less than 30% of revenue Our largest product lines are typically only 5% to 7% of total revenue Our top ten product lines are less than 40% of revenue Analyst Day 2012 | 81 |

Analyst Day 2012 | 82 Investing to Insure Future Growth Investing to Insure Future Growth Enhancement of 300 mm wafer shipping and process products Market-leading 450 mm solutions Advanced filtration for Wet Etch and Clean i2M Center for Advanced Materials Science to support next-generation development of membranes and coatings Sales organization focused on critical customers Labs and specialized manufacturing sites close to key customers 450 300 Leveraged Infrastructure Enhanced Capabilities New Technologies Analyst Day 2012 | 82 |

Analyst Day 2012 | 83 Updated Target Earnings Model at Various Revenue Levels Updated Target Earnings Model at Various Revenue Levels 1 Q1-08, Q1-11 and Q1-12 results are on a non-GAAP basis. 2 Represents range of adjusted operating margin based on respective quarterly revenue levels. 3 Adjusted operating margin defined as GAAP operating income plus amortization, restructuring costs, impairment of goodwill, and fair value mark-up of inventory. 4 Q1-08 shares outstanding equal 116 million. Q1-11 shares outstanding equal 135 million. Q1-12 and all other scenarios shares outstanding equal 138 million. Q1-08 1 Q1-11 1 Q1-12 1 Quarterly Revenue Level Revenue ($M) $148 $203 $175 $170 $190 $220 Adjusted Operating Margin 3 9.4% 19.7% 16.7% 13% - 15% 16% - 18% 20%+ Earnings Per Share 4 $0.10 $0.23 $0.14 $0.11 - $0.13 $0.15 - $0.17 $0.22+ Goal of $1 EPS at $1 billion run rate remains intact Increased investment levels will be staged over the next several quarters Operating margins are attractive and remain above most comparable companies Increased spending at lower revenue levels allows for continued investment through the cycle 2 |

Analyst Day 2012 | 84 Strong Cash Flow Across the Cycle Strong Cash Flow Across the Cycle Generated $127 million of free cash flow in 2011 Cumulative free cash flow of $387 million since 2007 During the worst downturn in the industry’s history, free cash flow was only $9 million negative 2011 EBITDA of $163 million Cumulative Free Cash Flow (in $M) Free Cash Flow Capability¹ Actual Free Cash Flow 1 Free cash flow capability assumes no M&A activity or change in capital structure Estimated $0 $100 $200 $300 $400 $500 $600 $700 |

Analyst Day 2012 | 85 Balance Sheet Continues to Strengthen Balance Sheet Continues to Strengthen $ and share data in millions 1 Total debt equals long-term debt, current maturities of long-term debt, and short-term borrowings March 31, 2012 Dec. 31, 2011 Dec. 31, 2010 Dec. 31, 2009 Cash $267 $274 $134 $69 Total Assets $736 $725 $601 $505 Total Debt 1 $0 $0 $0 $72 Shareholders’ Equity $628 $608 $464 $350 Common Shares Outstanding 137 136 133 130 At December 2011, Entegris had debt-free balance sheet and $2 in cash per share |

Analyst Day 2012 | 86 In Summary In Summary Our results in the past two years demonstrate our ability to out-grow the market and deliver superior profitability and excellent cash flow Our core technologies are critical in solving the industry’s most difficult contamination issues We are expanding the breadth of our technology through sustained and focused investment The changes to our target model will provide the flexibility to strategically invest through the semiconductor cycle We are committed to continued growth and achieving superior profitability |

|