QuickLinks -- Click here to rapidly navigate through this document

First Community Bancorp

Rancho Santa Fe, CA

December 4, 2002

This presentation with respect to First Community Bancorp ("First Community") contains forward-looking statements that involve risks, uncertainties and assumptions. All statements other than statements of historical fact are forward-looking statements. Risks and uncertainties include, but are not limited to: the possibility that the acquisition of the Bank of Coronado may not close or that First Community may be required to modify aspects of the transaction prior to receiving regulatory approval; expected cost savings cannot be fully realized or realized within the expected time frame; revenues are lower than expected; competitive pressure among depository institutions increases significantly; the cost of integration of acquired businesses costs more, takes longer or is less successful than expected; the cost of additional capital is more than expected; changes in the interest rate environment reduces interest margins; general economic conditions, either nationally or in the market area in which First Community does business, are less favorable than expected; legislation or regulatory requirements or changes adversely affect First Community's business; changes that may occur in the securities markets; and other risks that are described in First Community's Securities and Exchange Commission filings (including but not limited to First Community's annual report on Form 10-K for the year ended December 31, 2001, and subsequently filed documents). If any of these uncertainties materializes or any of these assumptions proves incorrect, First Community's results could differ materially from First Community's expectations as set forth in these statements. First Community assumes no obligation and does not intend to update such forward-looking statements.

2

| NASDAQ Symbol | FCBP | |

| Fully Diluted Shares | 15.7 Million | |

| Market Capitalization | $460.7 Million* | |

| Average Volume | 42,100 shares per day* | |

| Dividends Per Share | $0.60 per year (2.00% yield*) | |

| Analyst Coverage | Friedman Billings Ramsey Keefe, Bruyette & Woods, Inc. Stifel, Nicolaus & Company, Inc. |

- *

- As of 11/20/02

3

- •

- A growing economy drives organic growth.

- •

- Small/medium-sized businesses represent a large, fragmented market.

- •

- Aggressive expense management is critical in consolidating businesses like banking.

- •

- Great execution beats great strategy.

- •

- Keep the business model simple.

4

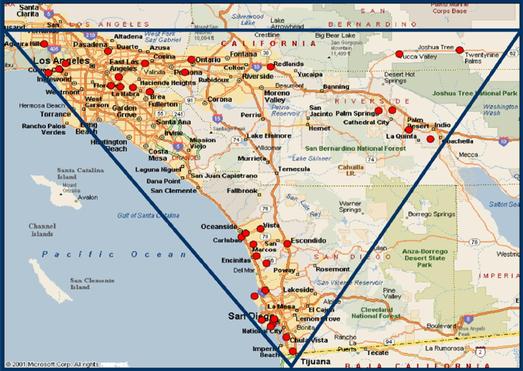

First Community Bancorp believes that a strong area of regional commerce and recreation exists in the geographic triangle that extends from Los Angeles to Palm Springs to San Diego.

5

A Growing Economy is Essential to Strong Organic Growth

- •

- Southern California is the 10th largest economy in the world.*

- •

- Economic growth is projected to be 4.5% in 2003, or 1.5 times the U.S. as a whole.**

- •

- Los Angeles, San Diego, Riverside and San Bernardino are among the ten fastest growing counties in the U.S.**

| Source: | * | Forbes http://www.forbes.com/newswire/2002/09/16/rtr722323.html | ||

** | Los Angeles Economic Development Corporation, http://www.laedc.org/data/press/PR65.shtml |

6

| Numbers in (000s) | Combined Initially * | 9/30/2002 | % Change | |||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Cash | $ | 115,831 | $ | 109,756 | -5 | % | ||||

| Investments / Fed Funds | 443,233 | 306,588 | -31 | % | ||||||

| Loans | 1,196,914 | 1,505,049 | 26 | % | ||||||

| Tangible Assets | 1,885,917 | 1,978,232 | 5 | % | ||||||

| Deposits | ||||||||||

| Non-interest bearing | 497,883 | 624,264 | 25 | % | ||||||

| Interest bearing | 742,468 | 813,663 | 10 | % | ||||||

| Certificates of deposit | 378,297 | 332,064 | -12 | % | ||||||

| Total Deposits | $ | 1,618,648 | $ | 1,769,991 | 9 | % | ||||

- *

- The combined numbers represent the aggregate balance sheet totals for banks acquired by First Community, from May 2000 through September 2002, as reported on the last call report prior to such bank's acquisition. The combined numbers are not in accordance with GAAP and are presented only to demonstrate the changes listed herein, and not to reflect numbers historically reported as combined.

7

Small/medium-sized Businesses Represent a Fragmented Market for Banks

- •

- The large banks are focused on selling standardized products and services.

- •

- A large market exists for personalized service with unique solutions to the problems faced by small/medium-sized businesses.

- •

- Most customers seeking highly personalized services are somewhat insensitive to price.

8

Expense Management is Critical in Consolidating Businesses Like Banking

- •

- Revenue can fluctuate, but expenses can be managed.

- •

- Effective expense management must focus on each component of operating cost:

- •

- Interest

- •

- Operating

- •

- Credit

9

Interest Expense is First Managed through the Deposit Mix

| | California Community Banks* | First Community 9/30/02 | ||||

|---|---|---|---|---|---|---|

| Deposit Mix | ||||||

| Non-Interest | 15 | % | 35 | % | ||

| Other Transactions | 37 | % | 45 | % | ||

| CDs | 38 | % | 17 | % | ||

| Borrowings | 10 | % | 3 | % | ||

- *

- Source: SNL Datasource

10

Pricing Discipline is the Other Critical Factor in Managing Deposit Costs

- •

- First Community seeks to price each of its deposit types in the third quartile among its peers.

- •

- Deposit changes are monitored continuously to understand sensitivity to pricing decisions.

- •

- Borrowings are only used to balance short-term funding needs.

11

Operating Expense can be Controlled by the Elimination of Redundancy

| | 3 Months Ended 9/30/2002 | 9 Months Ended 9/30/2002 | Combined Initially * | ||||

|---|---|---|---|---|---|---|---|

| Operating Expense/Avg. Tangible Assets | 3.99 | % | 4.21 | % | 4.58 | % | |

Efficiency Ratio | 63.6 | % | 65.0 | % | 78.8 | % |

- *

- The combined numbers represent the aggregate balance sheet totals for banks acquired by First Community, from May 2000 through September 2002, as reported on the last call report prior to such bank's acquisition. The combined numbers are not in accordance with GAAP and are presented only to demonstrate the changes listed herein, and not to reflect numbers historically reported as combined.

12

The First Community Model Emphasizes High Customer Service with Centralized Administrative Support

- •

- Loan decisions are made by local managers.

- •

- Area Presidents

- •

- Regional Chief Credit Officer

- •

- Administrative functions are centralized.

13

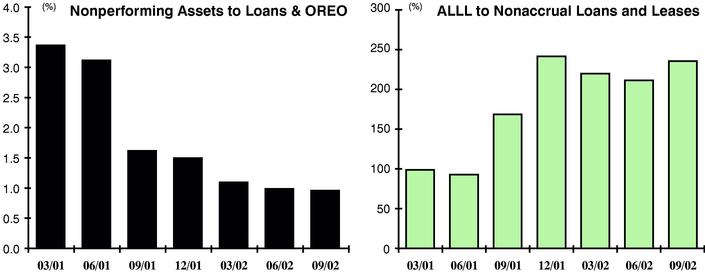

Credit Expense can be Controlled by Sound Underwriting and the Discipline of not Chasing Yield

Nonperforming Assets continue to trend downward despite the acquisition of banks with troubled portfolios while reserves remain strong

14

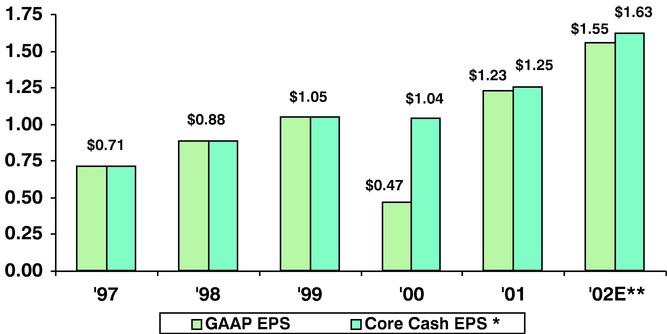

Great Execution Beats Great Strategy

- *

- Excludes one-time acquisition-related charges, goodwill amortization expense and core deposit intangible amortization expense.

- **

- Friedman Billings Ramsey estimates.

15

First Community is Well-Positioned for the Future because of its:

- •

- Experienced management team.

- •

- Excellent market characteristics.

- •

- Disciplined management process.

- •

- Simple business model.

16

First Community Bancorp

Rancho Santa Fe, CA

17

Forward-Looking Statements

Stock Summary

Investment Hypothesis

Market Area

A Growing Economy is Essential to Strong Organic Growth

Change in Loans & Deposits

Small/medium-sized Businesses Represent a Fragmented Market for Banks

Expense Management is Critical in Consolidating Businesses Like Banking

Interest Expense is First Managed through the Deposit Mix

Pricing Discipline is the Other Critical Factor in Managing Deposit Costs

Operating Expense can be Controlled by the Elimination of Redundancy

The First Community Model Emphasizes High Customer Service with Centralized Administrative Support

Credit Expense can be Controlled by Sound Underwriting and the Discipline of not Chasing Yield

Great Execution Beats Great Strategy

First Community is Well-Positioned for the Future because of its