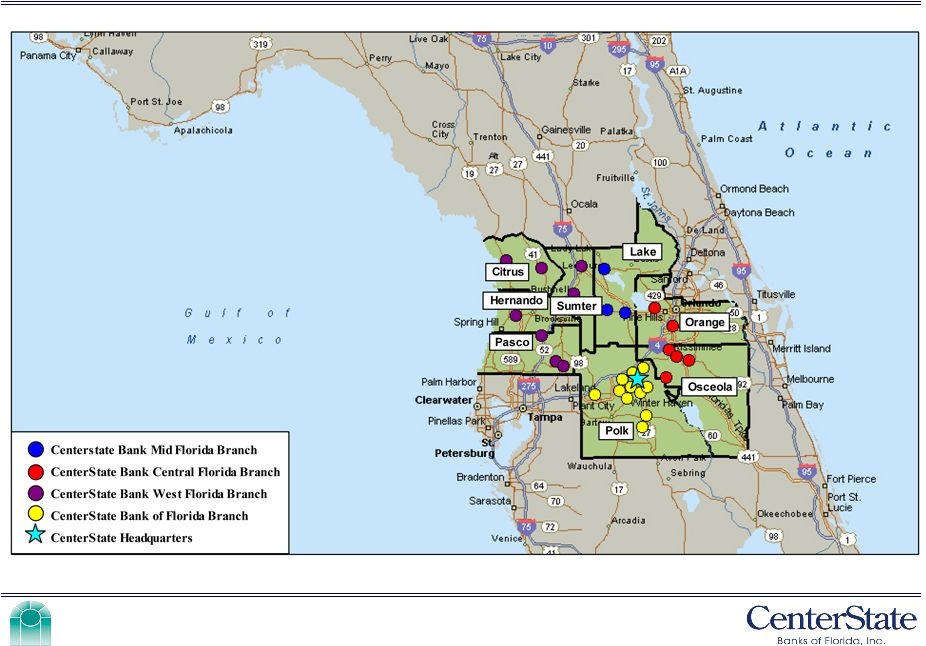

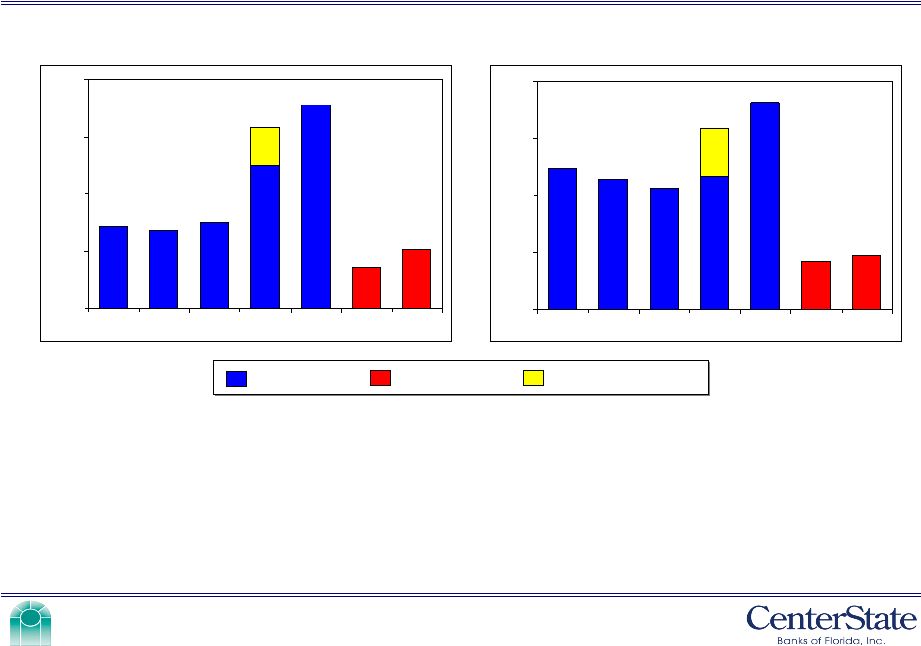

9 Strong Market Share Counties of Operation Osceola County - (Orlando MSA) # 4 in market share (7.4%) 2nd fastest growing county in Florida 2005 - 2010 population growth of 38.8% 4 branches Polk County - (Lakeland MSA) # 5 in market share (5.6%) 2005 - 2010 population growth of 11.5% 12 branches Sumter County - (The Villages MSA) # 5 in market share (7.3%) 5th fastest growing county in Florida 2005 - 2010 population growth of 26.2% 2 branches Pasco County - (Tampa MSA) #8 in market share (2.1%) 12th fastest growing county in Florida 2005 - 2010 population growth of 18.9% 3 branches Source: SNL Financial. Deposit data as of 6/30/05. Market share data for Citrus, Hernando, Lake, Osceola, Pasco, Polk and Sumter Counties, Florida. Excludes Orange County in which CSFL has $30 million in deposits. Deposits Market Rank Institution ($000s) Share Branches 1 SunTrust Banks Inc. (GA) 4,500,499 21.06 % 82 2 Bank of America Corp. (NC) 4,458,878 20.87 63 3 Wachovia Corp. (NC) 3,913,315 18.32 79 4 Colonial BancGroup Inc. (AL) 1,340,539 6.27 30 5 Centerstate Banks of Florida (FL) 720,839 3.37 27 6 AmSouth Bancorp. (AL) 700,908 3.28 27 7 Citrus & Chemical Bancorp. (FL) 656,025 3.07 10 8 BB&T Corp. (NC) 594,930 2.78 13 9 Villages Bancorp Inc. (FL) 570,836 2.67 7 10 Alabama National BanCorp. (AL) 457,946 2.14 10 |