Investor Presentation Second Quarter 2011 Exhibit 99.1 |

This presentation contains forward-looking statements, as defined by Federal Securities Laws, relating to present or future trends or factors affecting the operations, markets and products of CenterState Banks, Inc. (CSFL). These statements are provided to assist in the understanding of future financial performance. Any such statements are based on current expectations and involve a number of risks and uncertainties. For a discussion of factors that may cause such forward-looking statements to differ materially from actual results, please refer to CSFL’s most recent Form 10-Q and Form 10-K filed with the Securities Exchange Commission. CSFL undertakes no obligation to release revisions to these forward-looking statements or reflect events or circumstances after the date of this presentation. Forward Looking Statement 2 |

Birmingham Atlanta Winston-Salem Tamp a Winter Haven Corporate Overview 3 Correspondent Banking market Headquartered in Davenport, FL $2.2 billion in assets $1.2 billion in loans $1.8 billion in deposits Company formed: June 2000 2 Subsidiary Banks 53 locations |

Conservative Balance Sheet • Total Risk-Based Capital Ratio - 18% • Loans / Assets - 55% • Loans with credit protection – 24% • 15% of loans are covered by loss sharing agreements with the FDIC • 9% are subject to a 2 year “Put Back” agreement with TD Bank • Assets backed by the US Government* – 40% • Low Concentration Levels • CRE at 139% of capital vs. 300% guidance • CD&L at 34% of capital vs. 100% guidance • Operating leverage that is yet untapped 4 *Includes cash and cash equivalents, AFS securities issued by U.S. Government Sponsored Entities, FDIC covered assets, and FHLB and FRB stock. |

Opportunistic through the Crisis 5 1) FDIC Acquisitions • Ocala National Bank • Olde Cypress Community Bank • Independent National Bank of Ocala • Community National Bank of Bartow 3) New Fee-Based Business Lines • Correspondent Banking Division • Prepaid Card Division • Wealth Management Division 2) Non – FDIC Acquisitions • TD Bank divesture in Putnam • Federal Trust Acquisition from The Hartford Insurance Company 4) Strategic Expansion & Management Lift-Outs • Vero Beach • Okeechobee • Jacksonville |

Reserves / Loans (%) Credit Cycle Burn Down Since 12-31-07, 9.3% of the loan portfolio balance has been expensed as a write down or elevated reserves. Credit Quality Trends NPAs / Loans & OREO (%) Problem Loan Trends ($MM) 6 Source: SNL Financial Nonperforming assets include 90 days or more past due. Florida peers include publicly traded banks and thrifts headquartered in Florida. Southeastern peers include publicly traded financial institutions located in AL, AR, FL, GA, MS, NC, SC, TN VA, and WV with total assets between $2 and $5 billion. |

7 NPA Inflows - Slowing Down |

Building Franchise Value with Core Deposits Value of core deposits not fully realized in this low rate environment. Approximately 103,171 total accounts - $17,117 average balance per account Core deposits defined as non-time deposits. 22% 18% 25% 15% 20% Total Deposits ($MM) Number of Deposit Accounts 8 DDA and NOW 6/30/10 6/30/11 Change % Change Balance $497MM $707MM $210MM 42% No. of Accounts 45,365 66,930 21,565 48% 2006 2007 2008 2009 2010 6/30/11 Jumbo Time Retail Time MMDA & Savings NOW DDA 0 500 1,000 1,500 2,000 352 260 448 311 396 10,579 13,191 11,001 12,025 14,998 14,802 32,280 40,822 43,974 54,561 78,874 88,369 0 25,000 50,000 75,000 2006 2007 2008 2009 2010 6/30/2011 Time Deposits Core Deposits 100,000 |

9 Profitability Metrics Return on Assets % (PTPP excluding nonrecurring items and Correspondent Division) Net Interest Margin % (excluding Correspondent Division) Operating Expenses as a % of Avg Assets (excluding credit costs, nonrecurring items, and Corresp Div) |

10 Conversions Will Bring Efficiencies Scheduled for September and December Five Completed since December |

11 Talent Acquisition through the Crisis Name Position Age Years in Banking Prior Experience Dan Bockhorst Chief Risk Officer 48 28 Fifth Third, IRNB Chief Credit Officer - $800M Jennifer Idell CFO of Bank 36 15 Bank of Florida - CFO Darlene Bennett Director of Operations 55 38 SunTrust -Central FL Operations & Technology Cindy Robbins Director of Retail 50 33 Barnett & Riverside - Director of Retail - $3B Debbie Harsh Director of HR 56 35 First Sterling & Colonial Dave Kopec Director of Residential Lending 52 28 First Federal S&L and Highland Homes Brad Jones Director of Correspondent Banking 46 20 Silverton - $5B Joe Keating Director of Wealth Management 59 35 Federal Res., Old Kent & Alabama National - $8B Presidents Andy Beindorf Treasure Coast 55 33 Flagship, Indian River National Bank CEO - $800M Gil Pomar Northeast Florida 50 30 First Union & Jacksonville Bancorp CEO - $600M John Williams Okeechobee Region 56 32 Farm Credit & Riverside National Bank - President |

12 Results of Opportunities Since Crisis **Results include approximate deposits and number of deposit accounts from Federal Trust acquisition but does not include net income impact of $46M discount on performing loans. OFFENSE INITIATIVE Net Income since Inception Total Deposits / Assets $M # of Deposit Accounts FDIC Acquisitions $3,041 $327,981 33,862 Non-FDIC Acquisitions ** $7,696 $341,616 17,922 New Business Lines $15,679 $362,429 714 Strategic Expansion ($1,150) $69,233 2,812 Totals $25,266 $1,101,259 55,310 |

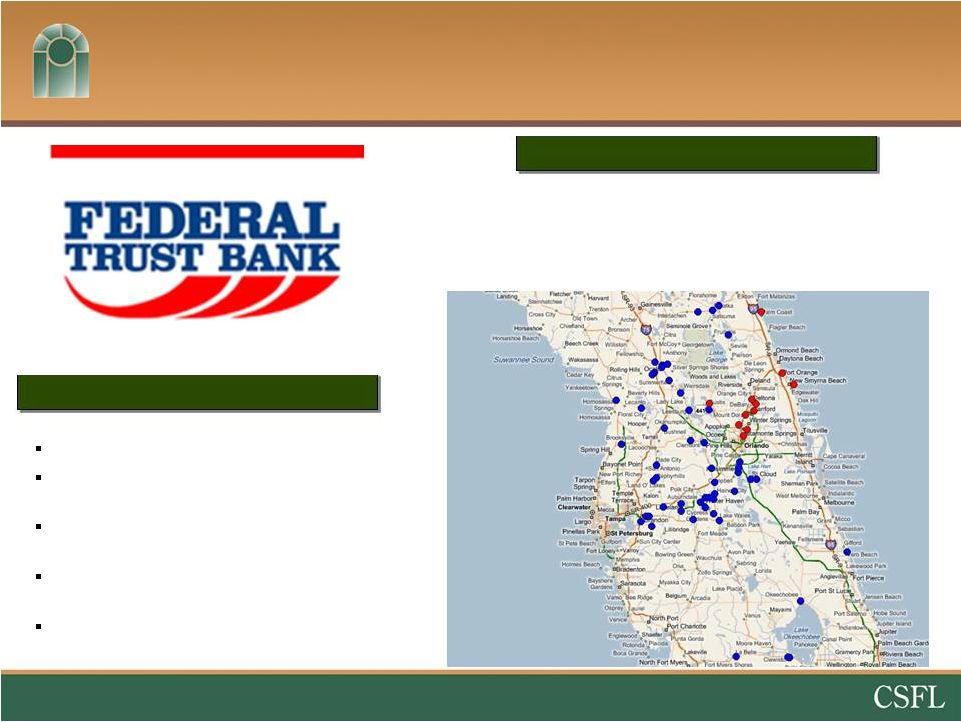

Federal Trust Acquisition 13 Headquarters Sanford, FL Year Established 1988 Deposits $230,000 Loans $170,000 Self-capitalizing transaction 27% loan discount on selected performing loans; 0% deposit premium 1 year put back on any past due or adversely classified loan Assumption of approximately $5 million of TruPs at LIBOR + 2.95% Efficiency achieved as 6 of 11 branches closed Dollars in thousands Selected Deal Terms Financial Highlights |

14 Federal Trust Loans Selected SF 1-4 Balances by Origination Year (Percent of Outstandings, excluding HELOCs) Selected Residential Loans by Florida County Selected Loan Criteria: Loan portfolio mix - 90% 1-4 Single Family, 6% HELOCs, 4% Commercial No problem loans - excludes all OREO, nonaccrual loans, adversely classified for regulatory purposes and Troubled Debt Restructures No past due loans – excludes all loans 60 days past due anytime during the last 12 months and all loans 30 days past due more than 2 times during last 12 months |

15 Greater Jacksonville Expansion Gil Pomar on board as Market President of Northeast Florida Previously served as President & CEO of The Jacksonville Bank Worked with CSFL management in the 90’s at First Union |

Summary Energetic & experienced local management team taking advantage of opportunities NPA inflow rate declining the last three quarters On the brink of realizing conversion related efficiencies & operating leverage Turmoil offers significant organic growth & FDIC acquisition opportunities 16 |

Investor Presentation Second Quarter 2011 |

Appendix |

Florida Economy Slowly Recovering 19 Source: The Florida Legislature Office of Economic and Demographic Research & US Bureau of Labor Statistics Unemployment at 10.6%, down from 12% - eight consecutive months of job growth after losing jobs for three years Florida Unemployment Rate Florida Median Home Price Median home prices for existing homes have been essentially flat since February 2009 (27 Months) with a slight downward drift |

Birmingham Atlanta Winston-Salem Tamp a Winter Haven Primary business lines – Bond Sales – Fed funds – Safekeeping, bond accounting, and asset/liability consulting services Customer base – 557 community banks Opportunity – Bank Clearing & Cash Management – Talent Recruiting / M&A Correspondent Banking Division Division Contribution 20 ($000s, except per share) 2Q10 3Q10 4Q10 1Q11 2Q11 Net Interest Income $1,319 $1,148 $974 $662 $1,113 Non-Interest Income 7,758 12,358 7,576 4,984 6,305 Non-Interest Expense (6,740) (9,249) (6,689) (4,978) (5,732) Income Tax Expense (900) (1,564) (700) (251) (634) Net Income Impact $1,437 $2,693 $1,161 $417 $1,052 EPS Impact $0.05 $0.09 $0.04 $0.01 $0.04 Management lift out from RBC (formerly ALAB) and Capital Markets Division of Silverton (73 employees) |

Loan Portfolio (excluding FDIC Covered Loans) 21 Loan Type No. of Loans 06/30/11 Balance Avg Loan Balance Residential Real Estate 2,918 $262MM $90,000 Commercial Real Estate 1,405 485MM 345,000 Construction, A&D, & Land 584 101MM 173,000 Commercial & Industrial 1,187 113MM 95,000 Consumer /Other 2,944 53MM 18,000 Total 9,038 $1,014MM $112,000 Includes $105MM of loans purchased from TD Bank which are subject to a 2 year “Put Back” option . Total Loans by Type (%) Total Loans Detail |

$65,959,000 (6.50% of Gross Loans) 25% of NPLs are current 74% of legal unpaid loan balance (net of specific reserves and partial charge-offs) $11,284,000 55% of legal unpaid loan balance at repossession date Residential Real Estate $18,951K (128 loans) Commercial Real Estate $29,437K (76 loans) Construction, A&D, & Land $15,344K (61 loans) Commercial $1,612K (27 loans) Consumer / Other $615K (39 loans) 22 Commercial Buildings (13) $4,615K Mobile Homes w/ Land (5) $262K Vacant Land (8 parcels of land) $1,783K Single Family Homes (17) $2,239K Residential Lots (69) $2,385K Data as of 6/30/11 Non Performing Assets (excluding FDIC Covered Assets) Other Real Estate Owned Non-Performing Loans |

23 Federal Trust Deposits Total Deposits by Type (%) Total Deposits Detail Deposit Type No. of Accts 12/31/10 Balance Avg Balance WA Rate Demand Deposits 3,289 $11MM $3,300 0.00% NOW 778 18MM 23,100 0.42% Savings & MMDA 2,307 118MM 51,100 0.98% Time Deposits 3,107 87MM 28,000 2.42% Total 9,481 $234MM $24,700 1.44% Data as of 12/31/10 |