VIKING ENERGY GROUP, INC.

15915 Katy Freeway, Suite 450

Houston, TX 77094

Tel (281) – 404-4387

November 24, 2021

Mr. John Cannarella

Staff Accountant.

Division of Corporation Finance

Officer of Energy & Transportation

U.S. Securities and Exchange Commission

Washington, D.C 20549

Phone: (202) 551-3337

| Re: | Viking Energy Group, Inc. |

|

| Form 10-K for the Fiscal Year ended December 31, 2020 |

|

| File No. 000-29219 |

|

| Filed March 25, 2021 |

Dear Mr. Cannarella:

On behalf of Viking Energy Group, Inc., (the “Company” or “Viking”), we have the following responses to the November 5, 2021 letter from the staff of the Securities and Exchange Commission (the “SEC” or the “Staff”) relating to comments the Staff had on the Company’s Form 10-K for the Fiscal Year ended December 31, 2020 filed with the Commission on March 25, 2021.

Our responses to the Staff’s comments are indicated below, directly following a restatement of each comment in bold type.

Form 10-K for the Fiscal Year ended December 31, 2020

Financial Statements

Note 3 – Summary of Significant Accounting Policies, page F-10

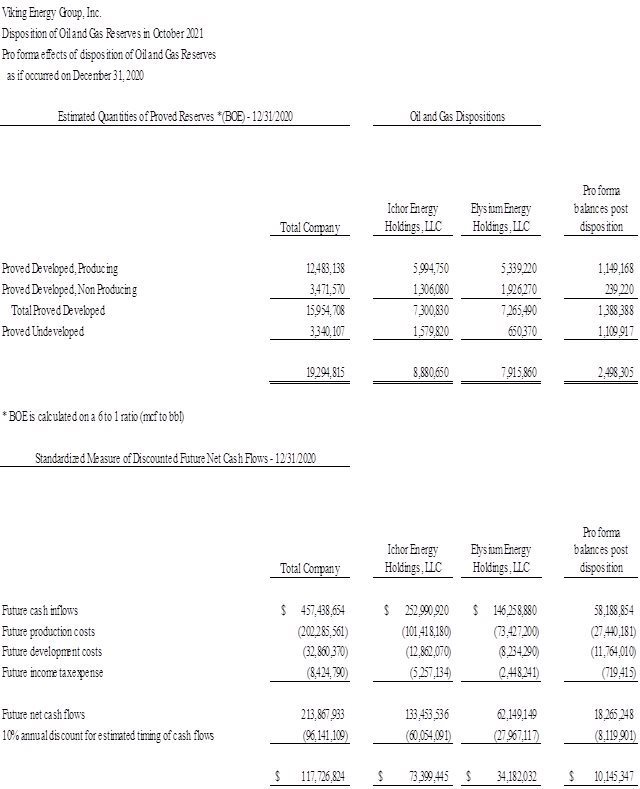

1. | We note that you filed a Form 8-K on October 12, 2021 and October 18, 2021 to report the disposals of your subsidiaries Ichor Energy Holdings, L.L.C. and Elysium Energy Holdings, LLC. You indicate these entities were assigned to TO Ichor 2021, L.L.C. and to TO Elysium 2021, L.L.C., affiliates of the entities from whom you originally acquired the assets, in exchange for the assumption of all related obligations, including the December 28, 2018 Term Loan Credit Agreement and the February 3, 2020 Term Loan Agreement. |

|

|

| We see that you included pro forma financial statements depicting both transactions in the second Form 8-K referenced above. Please revise both filings to include the pro forma effects of the disposition on your oil and gas reserves and the standardized measure of future net cash flows, based on the information that you disclosed in your annual report pursuant to FASB ASC 932-235-50-3 through 932-235-50-11B and FASB ASC 932-235- 50-29 through 932-235-50-36. You may refer to SAB Topic 2: D, Question 4, paragraph (5), if you require further clarification or guidance.

Please also quantify the obligations assumed by the counterparties in each instance, disclose the amount of gain or loss recognized on the dispositions, and identify the precipitating events, as may include default or the prospect of litigation, and which may otherwise clarify your rationale for each transaction. |

RESPONSE:

The Company will revise both Form 8-K filings to include the pro forma effects of the dispositions on our oil and gas reserves and the standardized measure of future net cash flows on each, based on the information disclosed in our annual report to include the following information as it applies to each of the filings:

Mr. John Cannarella

November 24, 2021

Page | 2

The Company provided line-item detail in the proforma June 30, 2021 balance sheets of the obligations assumed by the counterparties, specifically as it relates to (i) accounts payable and accrued expenses; (ii) derivative liability; (iii) undistributed revenue and royalties; (iv) long term debt; and (v) asset retirement obligations. In doing so, the combined change in stockholders’ equity (deficit) reflected a proforma gain on the disposals of approximately $11.4 million as of that date.

The Company will amend the Form 8-K’s, and at that time quantify an estimate at each of the transaction dates of the obligations assumed by the counterparties in each instance, and the amount of gain or loss recognized. Additionally, the Company will include in the amended Form 8-K’s, a summary of the precipitating events to assist the reader in understanding the rationale for each transaction.

Mr. John Cannarella

November 24, 2021

Page | 3

Note 6 – Equity, page F-19

2. | We note that your 28,092 Series C preferred shares were originally issued during 2012 with voting rights based on a ratio of 2,000:1 and conversion rights based on a ratio of 1:1. We understand that changes were made to the Certificate of Designation to increase the voting rights ratio to 10,000:1 in 2017, and to 32,500:1 in 2019, while the conversion ratio remained unchanged at 1:1, as reflected in the amended Certificate of Designation that you filed with the Form 8-K on September 5, 2019. |

|

|

| We note that you filed a Form 8-K on September 3, 2020 with another amendment to the Certificate of Designation in which the conversion ratio appears to have been changed for the first time since issuance, to 4,900:1, and we see there was a corresponding change to the voting rights ratio. However, you also filed a Form 8-K on December 28, 2020 with yet another amendment to the Certificate of Designation, in which both the voting and conversion ratios were changed to 37,500:1.

We see that you disclose the voting and conversion rights on pages 14 and F-19 of the annual report, and on pages 19 and 20 of your subsequent first and second quarter interim reports, respectively, although the ratios that you disclose do not appear to have been adjusted for the 1:9 reverse stock split that you conducted on January 5, 2021.

Please revise the disclosures in your annual report to clarify how the voting and conversion provisions have been affected by the reverse stock split, based on Sections 4(a), 6(c), 6(d), and 6(e) of the Certificate of Designation, and to explain the rationale or justification for each change to the voting and conversion provisions. |

RESPONSE:

Since James Doris’ involvement in Viking, the business intention has been such that any “super-voting” rights associated with the Series C Preferred Shares (“Series C Shares”) would be:

| · | extinguished upon Viking’s up-listing to a national stock exchange, whether via a direct up-listing or through a merger with an existing-listed entity; and |

|

|

|

| · | replaced (whether via amendment or exchange with another class of security) with a share structure with less votes and additional conversion entitlements. |

Mr. John Cannarella

November 24, 2021

Page | 4

In the meantime, while Viking remained listed on the OTCQB, the Company deemed it important for Mr. Doris to have a significant number of votes to avoid obstacles or delays vis-à-vis the Company executing on its business strategy. A summary of the changes to the voting and/or conversion rights regarding the Series C Shares, and the reasons therefor, is as follows:

Date |

Voting Right Change | Conversion Entitlement Change |

Rationale |

2017 | Change from 2,000:1 to 10,000:1 | N/A | In anticipation of potential increase(s) in the company’s authorized capital and/or issuances of shares of common stock. |

2019 | Change from 10,000:1 to 32,500:1 | N/A | In anticipation of potential increase(s) in the company’s authorized capital and/or issuances of shares of common stock. |

Sept. 2020 | Change from 32,500:1 to 4,900:1 | N/A | To facilitate the then planned merger with Camber Energy, Inc. (the “2020 Planned Merger”) pursuant to a merger agreement dated February 2020, as amended, which was ultimately terminated. The 2020 Planned Merger contemplated Mr. Doris exchanging his Series C Shares for a new class of Preferred Shares of Camber Energy. Again, this merger arrangement was terminated. |

Dec. 2020 | Change from 4,900: 1 to 37,500:1 | Change from 1:1 to 37,500:1 | To restore voting rights given the termination of the 2020 Planned Merger, and to address business matters related to an equity transaction involving the Company and Camber Energy, Inc. that closed on December 23, 2020 (the “Equity Transaction”). |

Pursuant to the Equity Transaction, Camber acquired 51% of Viking’s issued and outstanding common shares, with an antidilution provision protecting Camber’s 51% ownership interest through July 1, 2022.

As a result of the termination of the 2020 Planned Merger, it was necessary to return additional voting rights to the Series C Shares. It was also decided to increase the conversion entitlement associated with the Series C Shares at that time in case for any reason there could not be a full combination of Camber and Viking in the future (e.g., if shareholders decided to vote against a full combination). Additionally, if Mr. Doris were to convert any of the Series C Shares prior to July 1, 2022, causing Camber’s interest in Viking to fall below 51%, that Viking would have to issue additional common shares to Camber to maintain at least the 51% voting threshold.

Relative to the comments contained herein, the Company would like to correct its disclosures prospectively in its annual report for the year ended December 31, 2021 to reflect the voting and conversion rights associated with each Series C Share to reflect the 1:9 reverse split completed on January 5, 2021. The updated disclosure, pursuant to the relevant sections of the Certificate of Designation, will clarify that the voting and conversion rights were reduced from 37,500 per share to 4,167 per share as a result of the reverse split.

Mr. John Cannarella

November 24, 2021

Page | 5

3. | Given that the number of common shares issuable pursuant to the conversion provisions of your Series C preferred stock increased from 28,092 at the beginning of your 2020 fiscal year to 1,053,450,000 at the end of the year as a result of your modifications, based on the pre-reverse-stock-split figures, it appears that you would need to account for your changes to the voting and conversion provisions as an extinguishment and redemption consistent with the guidance in FASB ASC 260-10-S99-2. |

|

|

| This would generally involve recognizing the difference between the fair value of the modified instrument and the carrying amount of the preferred stock in the balance sheet as a deemed dividend. FASB ASC 260-10-45-11 provides guidance on the adjustment required in computing net income or loss attributable to common shareholders, which should be presented on the Statements of Operations, and utilized in computing earnings or loss per share. Please submit the revisions that you propose to address the aforementioned guidance or explain to us why you believe it would not apply or yield an appropriate characterization of the value conveyed, if this is your view. |

RESPONSE:

The Company is preparing an analysis using outside valuation consultants to determine if a change in the fair value of the preferred stock before and after the modifications are substantially different, to determine the appropriate accounting treatment. We will supplement this response with any proposed revisions that we propose to address upon completion of the valuations. If extinguishment accounting treatment is determined to be material, the Company will revise its disclosures to include the recognition of a deemed dividend in accordance with ASC 260-10-S99-2 in determining net income or loss attributable to common shareholders, which will be reported in the Statement of Operations, and utilized in computing earnings or loss per share.

Sincerely,

/s/ Frank Barker, Jr.

Frank Barker, Jr.

Chief Financial Officer

cc. James Doris, Chief Executive Officer