Exhibit 4.7

Your Kraft Canada Inc.

Retirement andSavings Program

For legacy Kraft Salaried employees and non-union hourly employees, hired on or before December 31, 2010

TABLE OF CONTENTS

About Your Retirement and Savings Program | 1 | |||

The Basic Pension Plan | 2 | |||

The Optional Pension Plan | 2 | |||

The Employee Savings Plan | 2 | |||

Group Registered Retirement Savings Plan (GRRSP) | 2 | |||

The OPP, ESP and GRRSP at a Glance | 3 | |||

Why it’s Important to Think About Retirement Now | 4 | |||

Why Save Now? | 4 | |||

Start Early | 4 | |||

Contribute Regularly | 5 | |||

How Much Do I Need to Save? | 6 | |||

Where Will My Retirement Income Come From? | 7 | |||

About the OPP, ESP and GRRSP | 7 | |||

Eligibility | 7 | |||

Enrolment | 7 | |||

Enrolment Form | 8 | |||

Online Enrolment | 8 | |||

Contributions | 9 | |||

Your Contributions | 9 | |||

Lump-sum transfers | 10 | |||

Company Contributions | 10 | |||

Owning Contributions | 10 | |||

Investment Accounts | 11 | |||

Withdrawing Funds | 11 | |||

In the Event of... | 12 | |||

Marital Breakdown (applicable to OPP only) | 13 | |||

Your Investments | 14 | |||

Target Date Funds | 14 | |||

Build Your Own Funds | 14 | |||

Choosing What’s Right for You | 14 | |||

Managing Your Investments | 15 | |||

Transaction Processing | 16 | |||

Voting Rights Under the Kraft Foods Stock Fund, Altria Stock Fund and PMI Stock Fund | 16 | |||

The Retirement Modelling Tool | 17 | |||

Your Resources for More Information | 18 | |||

Your Responsibilities | 19 | |||

Privacy and Your Plan | 19 | |||

Even if you haven’t given it much thought, you probably have a good idea of how you’d like to enjoy your retirement. Perhaps you think of travel, or spending more time with your family or on a hobby. Whatever your dreams, it’s important for you to consider whether you have the financial means to enjoy your retirement years.

Becoming a member of the Kraft Canada Basic Pension Plan helps take you one step closer to reaching your retirement goals. However, it’s probably not the only step you’ll need to take to meet your financial goals. That’s where savings plans such as your group Registered Retirement Savings Plan (GRRSP) and Kraft’s Optional Pension Plan (OPP) and Employee Savings Plan (ESP) can help.

This booklet provides summaries of the OPP, ESP and GRRSP, as well as general retirement planning and investment information.

You are responsible for making investment decisions about your account balance in the Retirement and Savings Program. You are welcome to use the information and decision-making tools offered by Sun Life Financial. Please consider obtaining investment advice from other sources, since your personal financial situation is unique.

About Your Retirement and Savings Program

As a legacy Kraft full-time salaried or eligible non-union hourly employee, you are eligible to participate in the Kraft Canada Retirement and Savings Program, which has been designed to help you reach your future financial goals. If you are a part-time employee, you may also be eligible – contact the Kraft Canada Pension and Benefits Centre at 1-800-395-1270 for further details.

Your goals might be long-term (for retirement) or short-term (for other personal needs). Since everyone’s financial needs and goals are different, the program is designed to give you the flexibility to customize your savings so they can meet your needs.

The Retirement and Savings Program includes the following components:

Registered Pension Plan | ||||||

Basic Pension Plan | Optional Pension Plan (OPP) | Employee Savings Plan (ESP) | Group Registered Retirement Savings | |||

| Registered defined benefit component (tax-sheltered) | Registered defined contribution component (tax-sheltered) | Non-registered plan (after-tax account) | Registered retirement savings plan (tax-sheltered) | |||

Optional plans provide you with increased retirement savings opportunities | ||||||

1

A registered pension plan is a plan that has been submitted to and formally approved by the appropriate government agencies. Contributions are tax deductible, and investment earnings are tax-sheltered until they are withdrawn.

The Basic Pension Plan

TheBasic Pension Plan is the defined benefit component of the Registered Pension Plan. As a member, you are required to make regular payroll contributions. When you retire from Kraft Canada, you receive a pension benefit based on a set formula that takes into account your years of credited service and highest average earnings. The Basic Pension Plan is described in a separate brochure. If you have questions about it, please contact the Kraft Canada Pension and Benefits Centre at1-800-395-1270.

The Optional Pension Plan

TheOptional Pension Plan (OPP) is the defined contribution component of the Registered Pension Plan. If you choose to participate in the OPP, you make tax-deductible contributions to a personal account within the plan, up to certain legislated maximums. Kraft Canada matches a portion of your contributions, up to certain maximums. Investment income is not taxable until you retire and begin receiving income. Your entire account balance (including your contributions and investment earnings) is locked-in, i.e., it can only be used to provide retirement income. Your entire account balance is immediately vested, meaning you are entitled to Kraft’s matching contributions (including investment earnings) when you leave Kraft, in addition to your own contributions (including investment earnings).

The Employee Savings Plan

TheEmployee Savings Plan (ESP) is a non-registered savings plan that can be used to finance retirement or other personal goals. If you choose to participate, you make contributions and Kraft Canada matches a portion of your contributions, up to certain maximums. Your contributions are not tax-deductible and company contributions and all investment earnings are taxable. However, you can withdraw the money at any time for any purpose. Though your contributions (including investment earnings) always belong to you, Kraft’s matching contributions (including investment earnings) are subject to vesting rules. For more information, seeOwning Contributions on page 10.

You can contribute through payroll deductions as much as 16% of your pay to theOPP and ESP combined. Kraft will make a matching contribution to your account (currently 55 cents) for every dollar you contribute, on the first 6% of earnings you save through payroll deductions.That’s like getting an automatic 55% return on your initial contributions.

With both plans, you choose how much to contribute and you decide how to invest these contributions from a variety of investment options.

Group Registered Retirement Savings Plan (GRRSP)

TheGroup Registered Retirement Savings Plan (GRRSP) is a registered savings plan (tax sheltered). If you choose to participate, you make contributions up to your personal RRSP limit

2

set by the Canada Revenue Agency (CRA). You are responsible for monitoring your RRSP contributions to ensure that you do not exceed your annual limit. You will be issued an RRSP tax receipt for your RRSP contributions for the first 60 days and last 305 days of each calendar year. Investment income is not taxable until you begin receiving an income or assets are withdrawn in cash (deregistered). Your contributions are not locked-in and always belong to you.

The OPP, ESP and GRRSP at a Glance

Optional Pension Plan (OPP) | Employee Savings Plan (ESP) | Group Registered Retirement Savings Plan (GRRSP) | ||||

Status as a registered plan | • Defined contribution component of the Registered Pension Plan | • A non-registered savings plan separate from the Registered Pension Plan | • A registered savings plan separate from the Registered Pension Plan | |||

Company match | • Currently, $0.55 for every dollar you contribute, on the first 6% of earnings you save through payroll deductions | • Same as OPP | N/A | |||

Tax status | • Your contributions are tax-sheltered; i.e., they are deducted from your earnings, and capped at certain maximums

• Kraft’s contributions and all investment earnings are tax-sheltered and not added to your taxable income for the year

• All income is taxable as you receive it during retirement | • Your contributions arenot tax-deductible

• Kraft’s contributions are taxed in the year they are made

•�� You may incur a capital gain or loss from a withdrawal or transfer of funds in the ESP

• Kraft Canada may trigger a capital gain or loss by removing investment options at any time | • Your contributions are tax-sheltered; i.e., they are deducted from your earnings, and capped at certain maximums

• All income is taxable as you receive it during retirement | |||

Access to your money (i.e., locked-in status) | • Your entire account balance (including your contributions and investment earnings) is locked-in, i.e., it can only be used to provide retirement income (seeIn the Event of…on page 12 for payment options at retirement) | • You can withdraw the money at any time. However, you may forfeit a portion of the company’s contributions plus investment earnings – only contributions that have been in the account for three or more calendar years can be withdrawn with no penalty | • You can transfer or withdraw the money at any time. Taxes are withheld from any amount withdrawn in cash | |||

3

Optional Pension Plan (OPP) | Employee Savings Plan (ESP) | Group Registered Retirement Savings Plan (GRRSP) | ||||

Vesting rules | • You are immediately vested in your entire account balance | • Kraft’s matching contributions are subject to vesting rules (seeOwning Contributions on page 10) | • You are immediately vested | |||

Investments | • You decide how to invest all contributions from a variety of investment options (seeYour Investments on page 14) | • Same as OPP | • Same as OPP | |||

Lump-sum contributions | • Not allowed | • Allowed, but you do not receive a company match

• Subject to verification | • Allowed

• Bonus payments also can be directed to the GRRSP | |||

Why it’s Important to Think About Retirement Now

While your retirement may be many years away, the steps you take today can make a big difference in the lifestyle you’ll be able to enjoy once your work life ends. Even if you are close to retirement, it’s not too late to take advantage of the program and reap the rewards in your retirement years.

Here are answers to the questions many people ask about saving for retirement.

Why Save Now?

When it comes to saving and investing for retirement, the benefits of starting early and contributing regularly are significant. (Though if you haven’t started saving, it’s never too late.)

Start Early

The earlier you begin saving, the more you’ll accumulate, and the more your savings will have the opportunity to grow as a result of compound interest.

Compounding occurs when the interest or income from your savings and investments is reinvested to earn additional income. The more you set aside each year, the more income you can earn on it.

4

Example

Let’s say you want to save $500,000 for your retirement. Here’s how much you would need to save each year to reach your goal, depending on how many years you have until retirement and assuming money is invested in monthly installments, earns a 3% return before fees and is tax-sheltered.

As you can see from the example above, the earlier you start, the less you have to put aside each year towards your end goal. Even modest savings, set aside early, can have a dramatic effect on your ultimate retirement savings. Remember that income from tax-sheltered savings will be taxable as you receive it during retirement.

Contribute Regularly

One of the keys to saving successfully for retirement is deciding how much you can afford to put aside each month, then disciplining yourself to save at least this amount on a regular basis.

An advantage of making regular contributions is that you don’t have to be as concerned about the highs and lows of the stock market. If you’re putting a fixed amount into an investment fund every month, the same dollar amount will buy more units of the funds when stock prices are low.

When stock prices rise, your regular contribution will buy fewer units and/or shares. However, with a long-term approach to your investments, you can help weather the up-and-down swings in the stock market over an extended period of time.

The Kraft Canada Retirement and Savings Program makes it easy to save for retirement by enabling you to invest gradually over time, using the convenience of the regular payroll deductions. You also benefit from company contributions to your savings.

For example, this table shows how your savings can accumulate through regular contributions (in this case, $300 per month) as opposed to a year-end, lump-sum contribution of $3,600.

5

| Lump Sum | Monthly | |||

| (One deposit of $3,600 at year end) | (12 regular deposits of $300 each month) | |||

10 years | $41,300 | $41,900 | ||

20 years | $97,100 | $98,500 | ||

30 years | $172,400 | $174,800 | ||

40 years | $274,000 | $277,800 |

Note: This table assumes a 3% return (before fees) compounded monthly and tax-sheltered. This assumed rate of return may not be appropriate for your savings. It does not reflect the impact of fees.

How Much Do I Need to Save?

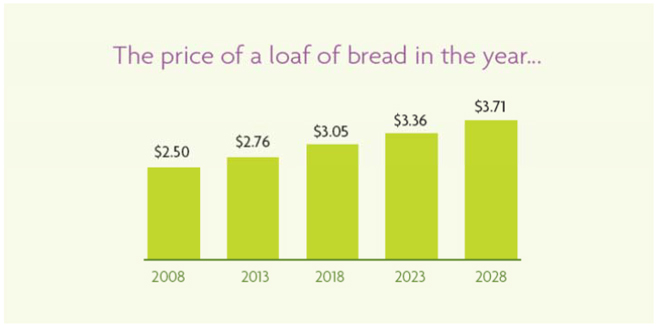

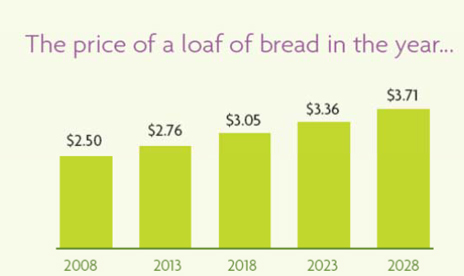

Only you can estimate your financial needs. Some experts say you’ll need the purchasing power of 60% to 80% of the income you earned in your final year of work to maintain a similar lifestyle during retirement. So, if you earned $60,000 the year before your retirement, you may need $36,000 to $48,000 of annual retirement income from all sources combined. It’s less money than you needed before retirement because you’ll likely have fewer living expenses – for example, you may no longer have a mortgage or child-rearing expenses to pay. However, let’s not forget about inflation. If the cost of goods and services increases, the buying power of your retirement dollar goes down. You need to make sure you have a big enough financial cushion to carry you through the ups and downs of the economy in future years. Kraft Canada cannot advise you on how much money you will need.

To illustrate, this chart shows what would happen to the cost of a simple loaf of bread over the next 20 years if the inflation rate were 2% per year.

At Kraft Canada, we believe that planning for retirement is very important. The online Retirement Modelling Tool can help you achieve your future financial wellness. See page 17 for details.

6

Where Will My Retirement Income Come From?

If you’re like most Canadians, you’ll probably draw on at least three sources of income when you retire:

| Your Company Pension and Savings Plans |

| Plans like the Kraft Basic Pension Plan, the OPP, ESP and GRRSP can provide a solid foundation depending on your earnings and years of service, as well as your savings plan contribution levels and investment performance. |

| + |

| Government Benefits |

| Old Age Security and the Canada/Quebec Pension Plan may give you some additional retirement dollars, but the amounts likely won’t be sufficient on their own. |

| + |

| Personal Savings |

| Personal savings such as Registered Retirement Savings Plans (RRSPs) can boost your retirement income even further. |

| = |

| RETIREMENT INCOME |

About the OPP, ESP and GRRSP

Eligibility

All legacy Kraft full-time salaried and eligible non-union hourly employees hired on or prior to December 31, 2010 automatically join the Basic Pension Plan on the first day of the month after one year of employment with Kraft.* Once you are a member of the Basic Pension Plan, you may voluntarily participate in the OPP and/or the ESP, as well as the GRRSP.

Your decision to participate will likely depend on your personal financial goals. If you wish to save additional money for retirement, consider participating in the registered OPP, which is subject to provincial pension legislation. The ESP can help you meet short- or long-term goals.

The GRRSP is available January 1, 2012. All employees are eligible to participate immediately.

| * | Different rules apply to part-time employees and employees in Quebec. For more information, please call the Kraft Canada Pension and Benefits Centre at1-800-395-1270. |

Enrolment

Enrol today! Joining the OPP, ESP and/or GRRSP is easy and only takes 5 to 10 minutes.

7

Enrolment Form

Enrol in the plan by simply completing the enrolment form found in the my money Investment and Savings Guide. If you need help, please call Sun Life Financial’s Customer Care Centre at1-866-896-6976 any business day from 8 a.m. to 8 p.m. ET.

Online Enrolment

You must first register for your access ID and password. Simply go towww.sunlife.ca/kraft and selectRegister now. You’ll need your account number and your date of birth. You can find your 14-digit account number in the welcome letter you received from Sun Life Financial. Your 14-digit account number starts with 02209 and is followed by your nine-digit Kraft employee number.

Once you have your personal access ID and password, sign intowww.sunlife.ca/kraft with your personal access ID and password and select theLet’s get started link.

8

Contributions

Eligible pay is your annual base salary, including regular incentive payments, overtime and premium pay, but excluding long-term incentive awards, prizes or additional awards in cash or otherwise.

About Tax-Sheltered Limits

The Canada Revenue Agency (CRA) limits the amount of money you can save on a tax-sheltered basis every year. Your tax-sheltered limit is equal to 18% of your income, up to a dollar maximum and is reduced by your pension adjustment (PA) for the current year. (For an example of your PA, see the T4 slip you received from Kraft Canada Inc. this year, which shows your PA from the previous year).

Therefore, depending on the OPP contribution level you select, you may not be able to contribute or receive Kraft Canada’s matching contributions on a fully tax-sheltered basis. Instead, OPP contributions that are above your tax-sheltered limit will be deposited in the ESP.

The payroll system will keep track of your OPP contributions and automatically direct contributions that are above the limit to the ESP. However, you are ultimately responsible for ensuring that you do not exceed your contribution limits set by CRA each year and are responsible for any penalties assessed on you.

Your contributions to the GRRSP are tax deductable up to the limits set by the CRA. You are responsible for ensuring you do not exceed your personal limit.

Your Contributions

You can choose to direct up to 6% of your eligible pay to the OPP. The only limit on ESP contributions is that you cannot contribute through payroll deductions more than 16% of earnings to the OPP and the ESP combined. Contributions to the GRRSP are allowed by payroll deductions and bonus deferral up to your personal limit set by the CRA.

| • | Your contributions to the OPP are tax-deductible up to the limits set by the Canada Revenue Agency (CRA). These limits apply because the OPP is part of a registered pension plan. Contributions above the CRA limit are automatically re-directed to the ESP. |

| • | Your contributions to the ESP are not tax-deductible. |

| • | Your contributions to the GRRSP are tax deductable up to the limits set by the CRA. You are responsible for ensuring you do not exceed your personal limit. |

You can change the percentage of your payroll contributions, discontinue contributions or re-direct future contributions from one plan to the other at any time. SeeManaging Your Investments on page 15 for more information.

9

Lump-sum transfers

You can also transfer cash invested in your other personal savings accounts into the ESP (subject to verification process) or GRRSP. These lump-sum contributionsare not eligible for a company matching contribution.

Company Contributions

As an incentive for saving, you receive a 55% matching contribution from Kraft Canada on the first 1% to 6% of earnings you save through payroll deductions. This means that Kraft Canada adds 55 cents to each dollar you contribute.

Company contributions are directed to the OPP and/or ESP in the same way as your own contributions. If you reach the maximum OPP contribution level permitted by the CRA, contributions will be re-directed to the ESP. Company contributions to the ESP are considered a taxable benefit.

With company contributions, your savings can really add up – and that’s without even considering investment earnings. Suppose you earn $60,000. The chart below shows the total annual amount directed to your savings at various contribution rates.

Your Contribution Rate (% of Earnings) | Your Contribution Amount | Company Contribution | Total Annual Contribution to Your Savings | |||

1% | $600 | $330 | $930 | |||

2% | $1,200 | $660 | $1,860 | |||

3% | $1,800 | $990 | $2,790 | |||

4% | $2,400 | $1,320 | $3,720 | |||

5% | $3,000 | $1,650 | $4,650 | |||

6% | $3,600 | $1,980 | $5,580 |

Owning Contributions

You always own your contributions and the investment earnings on those contributions. Ownership of company contributions differs depending on whether they are deposited in the OPP or the ESP.

OPP – You own company contributions and the related investment earnings in the OPP immediately after they are deposited into your investment account. (However, because they are part of the Registered Pension Plan, you are not permitted to withdraw funds from this account until you retire. Also seeIn the Event of… on page 12 for details on what happens in case of termination or death.)

10

ESP – Kraft contributions and related investment earnings in the ESP are owned gradually as shown in the following table.

Number of calendar years that Kraft contributions are in the ESP | Percentage of Kraft contributions you own | |

Less than two | 25% | |

Two | 50% | |

Three or more | 100% |

Once you become eligible for retirement, you own all company contributions to the ESP no matter how long they have been in your account.

GRRSP – Company contributions are not made to the GRRSP.

Investment Accounts

All contributions to the OPP, ESP and/or GRRSP are directed to investment accounts held in your name by Sun Life Financial. You control how contributions to your accounts are invested, choosing from a range of professionally managed investment options. SeeYour Investments on page 14 of this booklet for more information about your investment options.

Investment earnings in your OPP and GRRSP accounts are not taxed until you begin receiving retirement income. Investment earnings in your ESP account are taxable and must be reported on your income tax return each year. Sun Life Financial will send you a tax slip showing the amount of investment income earned in the ESP and company contributions to the ESP in the previous year.

Withdrawing Funds

Locked-in

Locked-in money must be used only to provide retirement income. It cannot be withdrawn as a lump sum and can be transferred, for example, to an insurance company to buy an annuity, or to a locked-in retirement vehicle.

From Your OPP Account

Because the OPP is part of the Registered Pension Plan, you are not permitted to withdraw funds from this account until retirement.

From Your ESP Account

Cash withdrawals from the ESP are permitted at any time subject to vesting, or ownership, rules that apply to company contributions. SeeOwning Contributions on page 10 for details.

Note that if you withdraw company contributions from the ESP deposited in the last two years, you will forfeit a portion of the company’s contributions plus investment earnings.

11

From your GRRSP Account

Cash withdrawals or transfers to other financial institutions are permitted at any time. Tax will be withheld on cash withdrawals and a tax slip will be issued to report the amount as withdrawn income.

In the Event of…

OPP | ESP | GRRSP | ||||

Retirement | You may transfer the value of your OPP account to any of the following:

• A Locked-in Retirement Account (LIRA) offered by Sun Life Financial or any other financial institution

• A Registered Retirement Income Fund (RRIF) or Life Income Fund (LIF) offered by Sun Life Financial or any other financial institution

• Sun Life Financial or any other Canadian insurer for the purchase of a life annuity

• Another registered pension plan, if that plan permits it

In addition, if you wish, your money may be left in the plan for up to three years from your retirement date. If Sun Life Financial does not receive your instructions within three years, you will become responsible for an additional monthly administration fee.* | You become automatically vested, and the full value of your ESP account is payable to you.

You may withdraw your account in cash, or transfer your account to Sun Life Financial or any other financial institution.

In addition, if you wish, your money may be left in the plan for up to three years from your retirement date.

If Sun Life Financial does not receive your instructions within three years, the funds in your non-registered plan will automatically be transferred to a non-registered account in Sun Life Financial’s Group Choices Plan.

If any of your current investment options are not available in the Group Choices Plan, the funds in these investments will be transferred to a money market fund. | You may transfer the value of your GRRSP account to any of the following:

• A Registered Retirement Income Fund (RRIF) or Life Income Fund (LIF) offered by Sun Life Financial or any other financial institution

• Sun Life Financial or any other Canadian insurer for the purchase of a life annuity

• Another registered savings plan, if that plan permits it

In addition, if you wish, your money may be left in the plan for up to three years from your retirement date. If Sun Life Financial does not receive your instructions within three years, the funds in your registered plan will automatically be transferred to a group registered retirement savings plan in Sun Life Financial’s Group Choices Plan.

If any of your current investment options are not available in the Group Choices Plan, the funds in these investments will be transferred to a money market fund.

| |||

Termination | You may transfer the value of your OPP account to any of the vehicles shown above.

You must make an election within 90 days of the date you receive your termination options package from Sun Life Financial.

If Sun Life Financial does not | Your ESP cash withdrawals are subject to vesting rules. You must make an election within 90 days of the date you receive your termination options package from Sun Life Financial.

If Sun Life Financial does not receive your instructions within | You may transfer the value of your OPP account to any of the vehicles shown above. You must make an election within 90 days of the date you receive your termination options package from Sun Life Financial.

If Sun Life Financial does not | |||

12

OPP | ESP | GRRSP | ||||

| receive your instructions within 90 days, you will become responsible for an additional monthly administration fee.* | 90 days, the funds in your non-registered plan will automatically be transferred to a non-registered account in Sun Life Financial’s Group Choices Plan.

If any of your current investment options are not available in the Group Choices Plan, the funds in these investments will be transferred to a money market fund. | receive your instructions within 90 days, the funds in your registered plan will automatically be transferred to a group registered retirement savings plan in Sun Life Financial’s Group Choices Plan.

If any of your current investment options are not available in the Group Choices Plan, the funds in these investments will be transferred to a money market fund.

| ||||

| Death | If you die before retirement, the total value of your OPP account will be paid as a lump sum, less taxes, to your spouse or beneficiary. If your spouse is your beneficiary, he or she may transfer this amount before taxes to another retirement vehicle, locked-in where required. | If you die before retirement, vesting is automatic. The total value of your ESP account will be paid to your beneficiary. | If you die before retirement, the total value of your GRRSP will be paid to your beneficiary. | |||

| * | Contact Sun Life Financial at 1-866-896-6976. |

Marital Breakdown (applicable to OPP only)

Locked-in Retirement Vehicle

A locked-in retirement vehicle is another plan or contract in which the funds must ultimately be used to provide a regular income during retirement, and cannot be withdrawn as a lump sum. The availability and exact rules pertaining to retirement vehicles such as a locked-in retirement account (LIRA), life income fund (LIF) or locked-in retirement income fund (LRIF) depend on applicable legislation in your province of employment.

According to family law, your Registered Pension Plan, of which the OPP is a component, may be considered a family asset. This means that your pension may be taken into account in the overall division of your family assets if you have a marital breakdown.

However, it is important to note that the law does not automatically require pensions to be divided at source where a marital breakdown occurs. Rather, the treatment of any pension benefits will typically be set out in the separation agreement or divorce order.

Therefore, if you have a marital breakdown, we require receipt of certain documentation in order to ensure the plan is administered appropriately. Specifically, you must forward to the Kraft Canada Pension and Benefits Centre documentation including, but not necessarily limited to, the separation agreement, the divorce certificate and the divorce order. The documentation you

13

provide must be complete and meet all administrative requirements. Strict confidentiality rules are in place at the Kraft Canada Pension and Benefits Centre and this documentation is used only for the necessary administration of the pension plan.

Please note that the actual division of a pension at source in the context of a marital breakdown is governed by applicable pension law and the terms of the pension plan itself.

“Marital breakdown” may include the breakdown of a marriage and the breakdown of a common-law relationship.

Your Investments

You are responsible for making all investment decisions within your OPP, ESP and GRRSP. You control the investment of contributions to your OPP, ESP and GRRSP accounts, choosing from a broad range of investment options. You can take a more hands-off approach by investing in Target Date funds, or you can build your own portfolio by investing in a mix of investment funds with different objectives, risk factors and return expectations.

Target Date Funds

Target Date funds are structured to coincide with an event or time in your life toward which you are saving, such as retirement or a major purchase. You determine when you will need your money and then pick the fund that matches that date. The fund’s asset mix will automatically shift towards more conservative investments as the target maturity date approaches.

Because Target Date funds are slightly more complex and require more active management by the fund manager, they typically have higher management fees than other investment options.

Build Your Own Funds

With build your own funds, you choose from a mix of investment funds to create your own personal asset mix. First, you complete the investment risk profiler found onwww.sunlife.ca/kraft or in themy money investment guide. Once your score has been determined, you build a portfolio based on the recommended profile. Profiles range from conservative to aggressive. It is up to you to monitor your portfolio over time. You may decide to rebalance your investments periodically to ensure that you maintain an investment mix that fits your needs and risk profile.

A description of each fund is found in the Sun Life Financial enrolment kit and throughwww.sunlife.ca/kraft. You should review the fund information thoroughly to make informed investment decisions and put your strategy into action.

Choosing What’s Right for You

How you invest your contributions to the OPP, ESP and GRRSP can be just as important as how much you save.

14

Diversification

It is important to keep in mind that diversification among funds with different objectives, risk factors and expected returns helps diminish investment volatility (i.e., sudden ups and downs). For example, although stocks offer potentially higher returns than bonds or cash, their value can fluctuate significantly over the short term. As such, you should consider mixing up your contributions by taking a closer look at the other choices available to you.

Managing Your Investments

Personal Statements

Over time, the value of your accounts will change, depending on the amount you and Kraft contribute, how your investments perform and any withdrawals you make. You can track investment performance through annual statements sent to your home or by checking the quarterly statements posted to the Sun Life Financial plan member website. These easy-to-read statements include a summary of your plans, your transaction history, personal rates of return, all fees associated with your accounts, as well as any new plan information. You can also check your account balance at any time on the Sun Life Financial Plan Member Services website.

To Access Your Online Statement

Sign intowww.sunlife.ca/kraft using your personal access ID and password.

You can track investment performance and manage your accounts online atwww.sunlife.ca/kraft. After you’ve signed in using your access ID and password, you’ll be able to:

| • | Monitor your account balances, transaction history and personal rates of return |

| • | View your quarterly online statement |

| • | Change your contribution rate, transfer money between investment funds and update future investment instructions |

| • | Get detailed fund information and analysis, including access to Morningstar where you can generate investment performance reports and conduct comparative analyses between the plan’s funds and Morningstar’s pooled fund universe |

| • | Access educational tools such as the investment risk profiler and other retirement and financial planning tools |

You can transfer money between investment funds and change your investment instructions for future contributions at any time. However, in order to discourage short-term trading which causes instability in the funds and affects all unit holders, Sun Life Financial charges a 2% penalty for multiple transfers in and out of the same investment fund within 30 days. The penalty does not apply to Kraft Foods, Altria and PMI stock, money market and guaranteed fund transactions.

15

If you prefer, you can also call the Sun Life Financial Customer Care Centre at1-866-896-6976 to access and manage your accounts over the telephone.

Kraft Foods, Altria and PMI Stock

Funds invested in Kraft Foods, Altria or PMI stock are invested directly in shares of these three companies. This means that you will see a direct correlation between the Kraft Foods, Altria and PMI stock traded on the New York Stock Exchange and your account value. The daily value of your stocks will represent the closing bid price, converted to Canadian dollars.

Any dividends received (excluding Altria and PMI dividends) will be allocated to your account the next day.

Transaction Processing

Your investment fund values are determined on a daily basis (except for Kraft Foods, Altria and PMI stock transactions). All transactions (contributions, transfers or withdrawals) requested over the phone by 3:00 p.m. ET and online by 4:00 p.m. ET (Monday to Friday) will be processed by Sun Life Financial that same day. The fund unit values will be determined at the 4:00 p.m. market close. For example, if you make a $100 contribution to a particular fund on Day 1, and the closing value of the fund on that day is $10 per unit, you would purchase 10 units of that fund and be able to see that transaction in your account on Day 2.

Kraft Foods, Altria and PMI stock transactions take longer to complete than other transactions. If you initiate a transaction on Day 1, stock will be bought or sold on Day 2. (Note that Altria and PMI stock may only be sold.) You will be able to see that transaction in your account on Day 3. The amount will be based on the average price of the Kraft Foods, Altria and PMI stock traded under the Kraft Canada plans on the day of the trade. The timing of stock transactions may also be affected by U.S. and Canadian statutory holidays.

Investment Fees

All fees associated with OPP, ESP and GRRSP investments, including recordkeeping, trustee, investment, stock and fund management charges are paid by plan members. Fees are outlined on the Sun Life Financial Plan Member Services website and on your personal statements. The fees you pay through group plans are typically much lower than what you’d pay if you were investing on your own.

Voting Rights Under the Kraft Foods Stock Fund, Altria Stock Fund and PMI Stock Fund

Ownership rights relating to shares of Kraft Foods Common Stock, Altria Common Stock and PMI Common Stock held in your OPP, ESP and/or GRRSP accounts, including voting rights, are passed through to you. The shares are voted through Sun Life Financial and they will work through the transfer agent and deliver a listing of the shareholders as of the record date. The transfer agent would then send out proxy material and shareholders would submit their voting instructions back to the transfer agent, who then feeds the information to Sun Life Financial to vote accordingly, since Sun Life Financial actually holds the shares.

16

Kraft Canada is responsible for ensuring that your purchase, holding and sale of Kraft Foods Common Stock, Altria Common Stock and PMI Common Stock and the exercise of voting rights are done in accordance with procedures that have been designed to safeguard the confidentiality of such information.

Your exercise of ownership rights with respect to shares of Kraft Foods Common Stock, Altria Common Stock and PMI Common Stock credited to your OPP, ESP and/or GRRSP accounts, including your voting directions, will be held in confidence by the trustee and will not be divulged to Kraft Foods, any affiliated company, or any officer or other employee, except as permitted by law.

To Review Account Fees Online

Sign intowww.sunlife.ca/kraft using your personal access ID and password.

The Retirement Modelling Tool

Easy Access!

You can access the RMT from work or home directly from theMy Benefits Online home page.

Please call the Kraft Canada Pension and Benefits Centre at1-800-395-1270 with any questions.

The Retirement Modelling Tool (RMT) is a valuable online tool that can help you estimate your potential retirement income. The planner is confidential and available virtually any time of the day.

Once you’ve logged into the secure website, you can:

| • | Review basic information about the Kraft Canada Basic Pension Plan. |

| • | Estimate your defined benefit retirement income under realistic assumptions you set yourself, such as retirement age and future earnings. |

| • | Complete your retirement picture by including savings from your various accounts, such as the Kraft Canada OPP, ESP and GRRSP, and other personal sources of retirement funds. |

| • | Review the impact of your projected government benefits. |

| • | Use financial calculators to estimate annuities and income from life income funds. |

17

Your Resources for More Information

Resource | Contact information | Contact for: | ||

| Kraft Canada Pension and Benefits Centre | My Benefits Online

(SelectBenefits underQuick Links onMy HR Online)

1-800-395-1270 from Monday to Friday, 8:30 a.m. to 5:00 p.m. ET | Basic Pension Plan questions | ||

| Sun Life Financial’s Customer Care Centre and Plan Member Services website | www.sunlife.ca/kraft

1-866-896-6976 from Monday to Friday, 8:00 a.m. to 8:00 p.m. ET (or anytime for self-serve options) or Sign in atwww.sunlife.ca/kraft and send a secure message | Optional Pension Plan (OPP), Employee Savings Plan (ESP) and Group Registered Retirement Savings Plan (GRRSP) questions | ||

| The Retirement Modelling Tool | My Benefits Online

(SelectBenefits under Quick Links onMy HR Online) | Potential retirement income estimates from all sources based on assumptions you enter | ||

This booklet is a summary intended to present the general provisions of the Kraft Canada Inc. Optional Pension Plan and Employee Savings Plan and Group Registered Retirement Savings Plan.

The Optional Pension Plan is a component of the following Registered Pension Plans:

| • | Kraft Canada Inc. Retirement Plan for Canadian Salaried Employees |

| • | Kraft Canada Inc. Retirement Plan for Non-Unionized Salaried Employees – Former Employees of Kraft Limited |

| • | Kraft Canada Inc. Retirement Plan for Non-Unionized Hourly Paid Employees – Bulk Cheese Plants and Mount Royal Plant |

| • | Kraft Canada Inc. Retirement Plan for Niagara Falls Salaried Cereal Division Employees |

| • | Kraft Canada Inc. Retirement Plan for Former Non-Unionized Employees of Nabob Foods Limited |

| • | Kraft Canada Inc. Retirement Plan for Former Salaried Employees of Nabisco Ltd. |

| • | Kraft Canada Inc. Trusteed Retirement Plan K |

The Optional Pension Plan is subject to applicable federal and provincial laws, and different rules may apply to employees in certain provinces.

The Employee Savings Plan is a nonregistered arrangement and is not subject to pension legislation.

The Group Registered Retirement Savings Plan is subject to applicable federal laws.

18

In the event of any discrepancy between the official documents and this summary brochure, the official documents will always govern. Kraft Canada reserves the right, from time to time and without advance notice, to change its benefits and retirement and savings programs for active, non-active and retired employees and their beneficiaries. Such changes may include, but are not limited to adding, altering or reducing benefits being received by individuals, changing carriers, amending plan provisions and merging plans. However, such changes will not impact benefits to the extent that the benefits are already paid for by individuals or to the extent expressly prohibited by statute.

Your Responsibilities

As a member of a capital accumulation plan with more than one investment option, you’re responsible for making investment decisions that are right for you. We’ve provided tools and information to assist you in making these decisions but not investment advice. You should also decide if seeking investment advice from a qualified individual makes sense for you.

Privacy and Your Plan

Protecting your privacy is a priority at Sun Life Financial. Sun Life Financial maintains a confidential file in their offices containing personal information about you and your contract(s) with Sun Life Financial. Their files are kept for the purpose of providing you with insurance and investment products or services that will help you meet your lifetime financial objectives. Access to your personal information is restricted to those employees and representatives who are responsible for the administration and servicing of your contract(s) with Sun Life Financial, or any other person whom you authorize. You are entitled to review the information contained in Sun Life Financial’s file and, if applicable, to have it corrected by sending a written request to Sun Life Financial.

To find out about Sun Life Financial’s Privacy Policy, visit their website atwww.sunlife.ca/kraft or call1-866-896-6976 and request that a copy of the Privacy Brochure be sent to you.

Your Kraft Canada Inc.

Retirement andSavings Program

For legacy Kraft Salaried employees and non-union hourly employees,

hired on or before December 31, 2010

For plan 04-15 Updated January 1, 2012

19

Your Kraft Canada Inc.

Retirement andSavings Program

For:

| • | All Salaried and Non-Unionized Hourly Employees hired on or after January 1, 2012 |

| • | All legacy Kraft Salaried and Non-Unionized Hourly Employees, other than non-union hourly employees employed at Dad’s, Peek Freans, Reid Milling and DSD locations, hired on or after January 1, 2011 |

| • | Legacy Cadbury Employees not eligible for a Defined Benefit Pension Plan |

20

TABLE OF CONTENTS

Introduction | 1 | |||

The Retirement Savings Plan (RSP), Non Registered Savings Plan (NREG) and Group Registered Retirement Savings Plan (GRRSP) at a Glance | 1 | |||

Why it’s Important to Think About Retirement Now | 3 | |||

Why Save Now? | 3 | |||

Start Early | 3 | |||

Contribute Regularly | 4 | |||

How Much Do I Need to Save? | 5 | |||

Where Will My Retirement Income Come From? | 5 | |||

About Your Retirement and Savings Program | 6 | |||

The Retirement Savings Plan (RSP) | 6 | |||

The Non-Registered Savings Plan (NREG) | 7 | |||

The Group Registered Retirement Savings Plan (GRRSP) | 7 | |||

Eligibility | 7 | |||

Contributions under the Retirement and Savings Program | 8 | |||

How are contributions allocated? | 9 | |||

Owning Contributions | 10 | |||

Investment Accounts | 10 | |||

Withdrawing Funds | 11 | |||

In the Event of... | 11 | |||

Your Investments | 13 | |||

Choosing What’s Right for You | 14 | |||

Marital Breakdown | 15 | |||

Build your own funds | 15 | |||

Diversification | 16 | |||

Transaction Processing | 17 | |||

Voting Rights under the Kraft Foods Stock Fund | 17 | |||

Account Fees | 18 | |||

Your Resources for more information | 18 | |||

About this booklet | 19 | |||

Your Responsibilities | 20 | |||

Privacy and your Plan | 20 | |||

Introduction

Even if you haven’t given it much thought, you probably have a good idea of how you’d like to enjoy your retirement. Perhaps you think of travel, or spending more time with your family or on a hobby. Whatever your dreams, it’s important for you to consider whether you have the financial means to enjoy your retirement years.

There are three common sources of retirement income: private pension plans, government pension programs and personal savings. Kraft Canada Inc. (“Kraft Canada”) offers the Retirement and Savings Program, which can help you achieve financial security for your future. By joining the Retirement and Savings Program and contributing regularly, you will play an active part in saving and investing for your retirement.

This booklet contains important information about the Retirement and Savings Program, including how it works, your eligibility, as well as general retirement planning and investment information.

You are responsible for making investment decisions about your account balance in the Retirement and Savings Program. You are welcome to use the information and decision-making tools offered by Sun Life Financial. Please consider obtaining investment advice from other sources, since your personal financial situation is unique.

The Retirement Savings Plan (RSP), Non Registered Savings Plan (NREG) and Group Registered Retirement Savings Plan (GRRSP) at a Glance

Retirement Savings Plan (RSP) | ||

| Type of Plan | • Defined Contribution component of a registered pension plan (tax-sheltered) | |

| Eligibility | • Full-time Salaried employees employed in any Kraft Canada Inc. location, and Non-union hourly employees employed at Mt. Royal, Ingleside, Vaudreuil, Oakville, Ewen and Bertrand locations, are automatically enrolled 30 days from hire date | |

| Basic Required contributions | • Kraft Canada’s Basic Contribution is 4% of your eligible pay

• You are required to contribute 2% of your eligible pay | |

| Voluntary contributions | • In addition to your required contributions, you can contribute from 1% to 4% of your eligible pay, and Kraft Canada will match dollar-for-dollar (100%) up to a maximum of 4%. This match is in addition to the 4% basic required contribution that Kraft Canada pays | |

| Tax status | • Your contributions are tax-sheltered (i.e., they are deducted from your earnings) and capped at certain maximums | |

1

Retirement Savings Plan (RSP) | ||

• Kraft Canada’s contributions and all investment earnings are tax-sheltered and not added to your taxable income for the year

• All income becomes taxable when you start receiving it during retirement | ||

| Access to your money (i.e. locked-in status) | • Your entire account balance (including your contributions and investment earnings) is locked-in, (i.e., it can only be used to provide retirement income ) (see In the Event of… on page 10 for payment options at retirement) | |

| Vesting rules | • You are immediately vested in your entire account balance | |

| Investments | • You are responsible for making the investment decisions within the Retirement and Savings Program

• You decide how to invest all contributions (Kraft Canada’s and your own) from a variety of investment options (see Your Investments on page 12) | |

| Lump-sum contributions | • Not allowed | |

Non Registered Savings Plan (NREG) | Group Registered Retirement Savings Plan (GRRSP) | |

• Non-Registered Savings Plan (after-tax account) | • Registered savings plan (tax-sheltered) | |

• Same as RSP | • Same as RSP | |

• Once you reach the CRA limit on contributions to a RSP, your contributions are automatically re-directed to the NREG | • N/A | |

• Once you reach the CRA limit on contributions to a RSP, your contributions are automatically re-directed to the NREG

• You may direct your contributions to the NREG, however, these contributions will not receive a company match

| • You may direct your contributions to the GRRSP, however, these contributions will not receive a company match | |

• Your contributions are not tax-deductible

• Kraft Canada’s contributions are taxed in the year they are made

• You may incur a capital gain or loss from a withdrawal or transfer of funds in the NREG

• Kraft Canada may trigger a capital gain or loss by removing investment options at any time | • Your contributions are tax-sheltered; i.e., they are deducted from your earnings, and capped at certain maximums

• All income is taxable as you receive it during retirement | |

• You are permitted to withdraw your contributions (and investment earnings on your contributions) while you are employed by Kraft Canada. Kraft contributions cannot be withdrawn while you are employed by Kraft Canada (see In the Event of... on page 10 for payment options at retirement) | • You can transfer or withdraw the money at any time. Taxes are withheld from any amount withdrawn in cash | |

2

Non Registered Savings Plan (NREG) | Group Registered Retirement Savings Plan (GRRSP) | |

• Same as RSP | • Same as RSP | |

• Same as RSP | • Same as RSP | |

• Not allowed | • Allowed

• Bonus payments also can be directed to the GRRSP | |

Why it’s Important to Think About Retirement Now

While your retirement may be many years away, the steps you take today can make a big difference in the lifestyle you’ll be able to enjoy once your work life ends. Even if you are close to retirement, it’s not too late to take advantage of the Retirement and Savings Program and reap the rewards in your retirement years. Here are answers to the questions many people ask about saving for retirement.

Why Save Now?

When it comes to saving and investing for retirement, the benefits of starting early and contributing regularly are significant. Though if you haven’t started saving, it’s never too late.

Start Early

The earlier you begin saving, the more you’ll accumulate, and the more your savings will have the opportunity to grow as a result of compound interest. Compounding occurs when the interest or income from your savings and investments is reinvested to earn additional income. The more you set aside each year, the more income you can earn on it.

Example

Let’s say you want to save $500,000 for your retirement. Here’s how much you would need to save each year to reach your goal, depending on how many years you have until retirement and assuming money is invested in monthly installments, earns a 3% return before fees and is tax-sheltered.

3

As you can see from the example above, the earlier you start, the less you have to put aside each year towards your end goal. Even modest savings, set aside early, can have a dramatic effect on your ultimate retirement savings. Remember that income from tax-sheltered savings will be taxable as you receive it during retirement.

Contribute Regularly

One of the keys to saving successfully for retirement is deciding how much you can afford to put aside each month, then disciplining yourself to save at least this amount on a regular basis.

An advantage of making regular contributions is that you don’t have to be as concerned about the highs and lows of the stock market. If you’re putting a fixed amount into an investment fund every month, the same dollar amount will buy more units of the funds when stock prices are low.

When stock prices rise, your regular contribution will buy fewer units and/or shares. However, with a long-term approach to your investments, you can help weather the up-and-down swings in the stock market over an extended period of time.

The Kraft Canada Retirement and Savings Program makes it easy to save for retirement by enabling you to invest gradually over time, using the convenience of the regular payroll deductions. You also benefit from company contributions to your savings.

For example, this table shows how your savings can accumulate through regular contributions (in this case, $300 per month) as opposed to a year-end, lump-sum contribution of $3,600.

| Lump Sum | Monthly | |||

(One deposit of $3,600 at year end) | (12 regular deposits of $300 each month) | |||

10 years | $41,300 | $41,900 | ||

20 years | $97,100 | $98,500 | ||

30 years | $172,400 | $174,800 | ||

40 years | $274,000 | $277,800 |

Note: This table assumes a 3% return (before fees) compounded monthly and tax-sheltered. This assumed rate of return may not be appropriate for your savings. It does not reflect the impact of fees.

4

How Much Do I Need to Save?

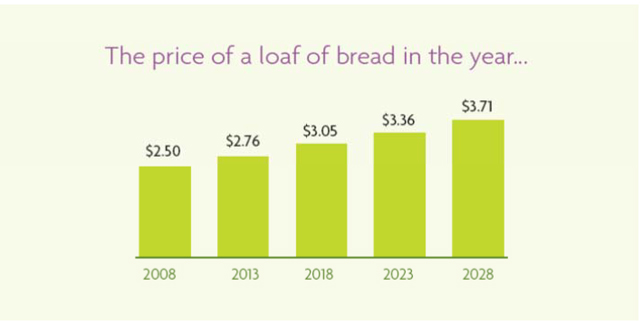

Only you can estimate your financial needs. Some experts say you’ll need the purchasing power of 60% to 80% of the income you earned in your final year of work to maintain a similar lifestyle during retirement. So, if you earned $60,000 the year before your retirement, you may need $36,000 to $48,000 of annual retirement income from all sources combined. It’s less money than you needed before retirement because you’ll likely have fewer living expenses – for example, you may no longer have a mortgage or child-rearing expenses to pay. However, let’s not forget about inflation. If the cost of goods and services increases, the buying power of your retirement dollar goes down. You need to make sure you have a big enough financial cushion to carry you through the ups and downs of the economy in future years. Kraft Canada cannot advise you on how much money you will need.

To illustrate, this chart shows what would happen to the cost of a simple loaf of bread over the next 20 years if the inflation rate were 2% per year.

Where Will My Retirement Income Come From?

If you’re like most Canadians, you’ll probably draw on at least three sources of income when you retire:

| Your Retirement and Savings Program |

Your Retirement Savings Plan (RSP), Your Non-Registered Savings Plan (NREG) Your Group Registered Retirement Savings Plan (GRRSP) and all investment earnings |

+

|

| Government Benefits |

Old Age Security and the Canada/Quebec Pension Plan may give you some additional retirement dollars, but the amounts likely won’t be sufficient on their own. |

+

|

| Personal Savings |

| Personal savings such as Registered Retirement Savings Plans (RRSPs) can boost your retirement income even further. |

=

|

| RETIREMENT INCOME |

5

About Your Retirement and Savings Program

Kraft Canada offers the Retirement and Savings Program to help you achieve financial security for your future. By joining the Retirement and Savings Program and contributing regularly, you will play an active part in saving and investing for your retirement.

There are three plans in the Retirement and Savings Program:

Retirement Savings Plan (RSP)

Non-Registered Savings Plan (NREG)

Group Registered Retirement Savings Plan (GRRSP)

The Retirement Savings Plan (RSP)

A registered pension plan is a plan that has been submitted to and formally approved by the appropriate government agencies. Contributions are tax deductible, and investment earnings are tax-sheltered until they are withdrawn.

A capital gain is the profit that is realized from the sale of an investment, while a capital loss is the loss that is realized from the sale of an investment. While capital gains and losses occur for both registered and non-registered plans, there is no tax consequence for registered plans.

The RSP is part of a registered defined contribution pension plan and it is tax-sheltered.

As a participant in the RSP, you make tax-deductible contributions to a personal account within the RSP, up to certain legislated maximums. Kraft Canada matches your contributions, up to certain maximums.

All contributions and investment income are not taxable until you retire and begin receiving income. Your entire account balance is locked-in and can only be used to provide retirement income (subject to certain exceptions).

Your entire account balance is immediately vested, meaning you are entitled to your contributions and Kraft Canada’s contributions (including investment earnings) when you terminate employment with Kraft Canada.

6

The Non-Registered Savings Plan (NREG)

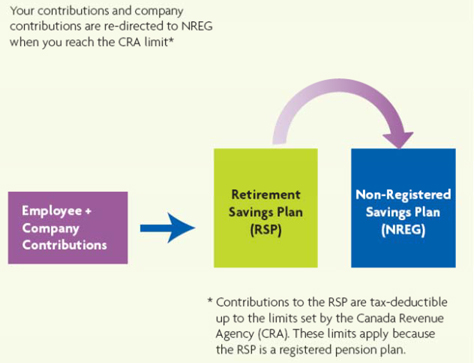

The NREG is an after tax, non-registered savings plan where your contributions and Kraft Canada’s contributions are deposited, once you reach the legislated maximum contributions to the RSP.

Effective January 1, 2012, you will be able to direct voluntary contributions to the NREG. Your contributions to the NREG will not be matched by Kraft Canada unless you have reached the legislated contributions limit in the RSP.

The NREG contributions are not tax-deductible, therefore your contributions, Kraft Canada’s contributions and all investment earnings are taxable.

Your entire account balance is immediately vested, meaning you are entitled to your contributions and Kraft Canada’s matching contributions (including investment earnings).

Effective January 1, 2012, you are permitted to withdraw your contributions (and investment earnings on your contributions) while you are employed by Kraft Canada. Kraft contributions cannot be withdrawn while you are employed by Kraft Canada.

The Group Registered Retirement Savings Plan (GRRSP)

TheGRRSP is a registered savings plan (tax sheltered). If you choose to participate, you make contributions up to your personal RRSP limit set by the Canada Revenue Agency (CRA). You are responsible for monitoring your RRSP contributions to ensure that you do not exceed your annual limit. You will be issued an RRSP tax receipt for your RRSP contributions for the first 60 days and last 305 days of each calendar year. Investment income is not taxable until you begin receiving an income or assets are withdrawn in cash (deregistered). Your contributions are not locked-in and always belong to you.

Eligibility

Eligibility in the Retirement and Savings Program is determined by youremployment category andwork location:

Enrolment after 30 days from hire date:

| • | Full-time Salaried employees (at any location) |

| • | Non-Union Hourly employees employed at Mt. Royal, Ingleside, Vaudreuil, Oakville, Ewen and Bertrand locations |

Please see front cover for your eligibility. Different rules apply to part-time employees and employees in the province of Quebec. For more information, please call the Sun Life Financial’s Customer Care Centre at1-866-896-6976.

7

Contributions under the Retirement and Savings Program

Eligible Pay

Your eligible pay is your annual base salary, including regular incentive payments, overtime and premium pay, but excluding long-term incentive awards, prizes or additional awards in cash or otherwise.

Required Contributions

You will automatically receive Kraft Canada’s Basic Contribution equal to 4% of your eligible pay, and your required contribution will be 2% of your eligible pay, each payroll period. So, right away, you can start saving 6% of your eligible pay towards your retirement.

Voluntary Contributions

You may contribute an additional 1% to 4% of your eligible pay, and Kraft Canada will give you a 100% company match on your voluntary contributions, up to a maximum of 4%.This represents an additional savings of up to 8% of your eligible pay.

You may also choose to direct your voluntary contributions to the GRRSP or NREG, however these contributions will not be matched by Kraft Canada.

Below is an example of the percentage of your eligible pay that will be contributed to your Retirement and Savings Program if you choose to make voluntary contributions at the maximum 4%.

| Your Contribution | Percentage of Match You Receive from Kraft Canada | |||

Required | 2% | 4% | ||

Voluntary | 1% to 4% | 100% match (dollar for dollar) | ||

Total | 6% | 8% |

By making regular contributions, your savings can really add up, and that’s without even considering investment earnings. For example, suppose you earn$60,000 and you have chosen to contribute the maximum allowed (6% of your eligible pay).

Contribution rate | Your Contribution | Company Contribution | Total Annual Contribution | |||||||||

Required | $ | 1,200 (2 | %) | $ | 2,400 (4 | %) | $ | 3,600 (6 | %) | |||

Voluntary | $ | 2,400 (4 | %) | $ | 2,400 (4 | %) | $ | 4,800 (8 | %) | |||

Total Savings | $ | 3,600 (6 | %) | $ | 4,800 (8 | %) | $ | 8,400 (14 | %) | |||

8

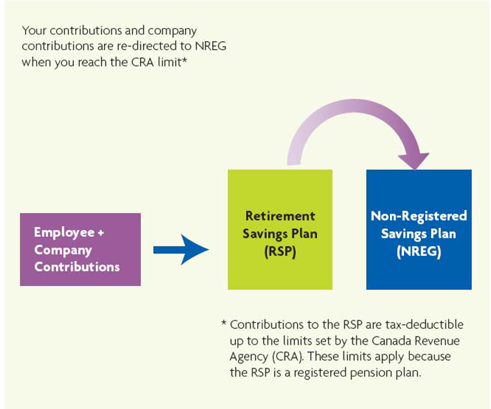

How are contributions allocated?

Both Employee Contributions and Kraft Canada’s Contributions arefirst directed to the Retirement Savings Plan (RSP).

Once you reach the RSP tax deductible limits set by the Canada Revenue Agency (CRA), your contributions are automatically re-directed to the Non-Registered Savings Plan (NREG).

About Tax-Sheltered Limits

The Canada Revenue Agency (CRA) limits the amount of money you can save on a tax-sheltered basis every year. Your tax-sheltered limit is equal to 18% of your income, up to a dollar maximum and is reduced by your pension adjustment (PA) for the current year. (For an example of your PA, see the T4 slip you received from Kraft Canada Inc. this year, which shows your PA from the previous year).

Therefore, depending on the RSP contribution level you select, you may not be able to contribute or receive Kraft Canada’s matching contributions on a fully tax-sheltered basis. Instead, RSP contributions that are above your tax-sheltered limit will be deposited in the NREG.

The payroll system will keep track of your RSP contributions and automatically direct contributions that are above the limit to the NREG. However, you are ultimately responsible for ensuring that you do not exceed your contribution limits set by CRA each year and are responsible for any penalties assessed on you.

Your contributions to the GRRSP are tax deductible up to the limits set by the CRA. You are responsible for ensuring you do not exceed your personal limit.

9

Owning Contributions

Your contributions and the contributions that the company has made on your behalf to the RSP, NREG and/or GRRSP, are yours immediately after they are deposited into your investment account. However, you are not permitted to withdraw funds from the RSP account until you terminate your employment or retire. Also see In the Event of… on page 10 for details on that happens in case of termination of employment or death.) You are permitted to withdraw your contributions from the NREG and the GRRSP. You are not permitted to withdraw contributions made by Kraft Canada to the NREG until you terminate or retire.

Investment Accounts

Locked-in

Locked-in money must be used only to provide retirement income. It cannot be withdrawn as a lump sum and can be transferred, for example, to an insurance company to buy an annuity, or a locked-in retirement vehicle.

All contributions to the RSP, NREG and/or GRRSP are directed to investment accounts held in your name by Sun Life Financial. You control how contributions to your accounts are invested, choosing from a range of investment options. See Your Investments on page 12 of this booklet for more information about your investment options.

Investment earnings in your RSP account are not taxed until you begin receiving them. Investment earnings in your NREG account are taxable and must be reported on your income tax return each year. Sun Life Financial will send you a tax slip each year showing the amount of investment income earned in the NREG in the previous year.

10

Withdrawing Funds

Locked-in Retirement Vehicle

A locked-in retirement vehicle is another plan or contract in which the funds must ultimately be used to provide a regular income during retirement, and cannot be withdrawn as a lump sum. The availability and exact rules pertaining to retirement vehicles such as a locked-in retirement account (LIRA), life income fund (LIF), or locked-in retirement income fund (LRIF) depend on applicable legislation in your province of employment.

From Your RSP Account

Because the RSP is part of a Registered Pension Plan, the funds in your RSP are locked-in, and cash withdrawals are not permitted (subject to certain exceptions).

From Your NREG Account

You are permitted to withdraw your contributions (and investment earnings on your contributions) while you are employed by Kraft Canada. Kraft contributions cannot be withdrawn while you are employed by Kraft Canada.

From your GRRSP Account

Cash withdrawals or transfers to other financial institutions are permitted at any time. Tax will be withheld on cash withdrawals and a tax slip will be issued to report the amount as withdrawn income.

In the Event of…

Retirement Savings Plan (RSP) | ||

| Retirement | You may transfer the value of your RSP account to any of the following:

• A Locked-in Retirement Account (LIRA) offered by Sun Life Financial or any other financial institution

• A Registered Retirement Income Fund (RRIF) or Life Income Fund (LIF) offered by Sun Life Financial or any other financial institution

• Sun Life Financial or any other Canadian insurer for the purchase of a life annuity

• Another registered pension plan, if that plan permits it

• In addition, if you wish, your money may be left in the plan for up to three years from your retirement date. If Sun Life Financial does not receive your instructions within three years, you will become responsible for an additional monthly administration fee* |

11

Retirement Savings Plan (RSP) | ||

| Termination | • You may transfer the value of your RSP account to any of the vehicles shown above

• You must make an election within 90 days of the date you receive your termination options package from Sun Life Financial

• If Sun Life Financial does not receive your instructions within 90 days, you will become responsible for an additional monthly administration fee* | |

| Death | • If you die before retirement, the total value of your RSP account will be paid as a lump sum, less taxes, to your spouse or beneficiary

• If your spouse is your beneficiary, he or she may transfer this amount before taxes to another retirement vehicle, locked-in where required | |

| * | Contact Sun Life Financial at 1-866-896-6976. |

In certain circumstances, your account balances may be paid to you in a lump sum payment if the account balance is considered small.

Non Registered Savings Plan (NREG) | Group Registered Retirement Savings Plan (GRRSP) | |

• You become automatically vested, and the full value of your NREG account is payable to you

• You may withdraw your account in cash, or transfer the balance of your account to any financial institution

• In addition, if you wish, your money may be left in the plan for up to three years from your retirement date

• If Sun Life Financial does not receive your instructions within three years, the funds in your non-registered plan will automatically be transferred to a non-registered account in Sun Life Financial’s Group Choices Plan

• If any of your current investment options are not available in the Group Choices Plan, the funds in these investments will be transferred to a money market fund

• Kraft Canada will have no responsibility for or knowledge of your funds, once the transfer occurs. Sun Life Financial will charge you higher fees. It is your responsibility to contact Sun Life Financial to find out what is happening with your funds | • You may transfer the value of your GRRSP account to any of the following:

• A Registered Retirement Income Fund (RRIF) or Life Income Fund (LIF) offered by Sun Life Financial or any other financial institution

• Sun Life Financial or any other Canadian insurer for the purchase of a life annuity

• Another registered savings plan, if that plan permits it

• In addition, if you wish, your money may be left in the plan for up to three years from your retirement date.

• If Sun Life Financial does not receive your instructions within three years, the funds in your GRRSP will automatically be transferred to a group registered retirement savings plan in Sun Life Financial’s Group Choices Plan

• If any of your current investment options are not available in the Group Choices Plan, the funds in these investments will be transferred to a money market fund

| |

12

Non Registered Savings Plan (NREG) | Group Registered Retirement Savings Plan (GRRSP) | |

• Kraft Canada will have no responsibility for or knowledge of your funds, once the transfer occurs. Sun Life Financial will charge you higher fees. It is your responsibility to contact Sun Life Financial to find out what is happening with your funds | ||

• You become automatically vested, and the full value of your NREG account is payable to you

• You must make an election within 90 days of the date you receive your termination options package from Sun Life Financial

• If Sun Life Financial does not receive your instructions within 90 days, the funds in your non-registered plan will automatically be transferred to a non-registered account in Sun Life Financial’s Group Choices Plan

• If any of your current investment options are not available in the Group Choices Plan, the funds in these investments will be transferred to a money market fund

• Kraft Canada will have no responsibility for or knowledge of your funds, once the transfer occurs. Sun Life Financial will charge you higher fees. It is your responsibility to contact Sun Life Financial to find out what is happening with your funds | • You may transfer the value of your GRRSP account to any of the vehicles shown above

• You must make an election within 90 days of the date you receive your termination options package from Sun Life Financial

• If Sun Life Financial does not receive your instructions within 90 days, the funds in your GRRSP will automatically be transferred to a group registered retirement savings plan in Sun Life Financial’s Group Choices Plan

• If any of your current investment options are not available in the Group Choices Plan, the funds in these investments will be transferred to a money market fund

• Kraft Canada will have no responsibility for or knowledge of your funds, once the transfer occurs. Sun Life Financial will charge you higher fees. It is your responsibility to contact Sun Life Financial to find out what is happening with your funds | |

• You become automatically vested, and the full value of your NREG account is payable to you

• If you die before retirement, the total value of your NREG account will be paid to your beneficiary | • If you die before retirement, the total value of your GRRSP will be paid to your beneficiary | |

Your Investments

You are responsible for making all investment decisions within the Retirement and Savings Program. You control the investment of contributions to your RSP, NREG and GRRSP

13

accounts, choosing from a broad range of investment options. You can take a more hands-off approach by investing in Target Date funds, or you can build your own portfolio by investing in a mix of investment funds with different objectives, risk factors and return expectations.

Choosing What’s Right for You

How you invest your contributions to the RSP, NREG and GRRSP can be just as important as how much you save. To assist you in making your investment decisions, read Sun Life Financial’s my money Savings and Investment Guide, included in your enrolment kit and available through the Plan Member Services website,www.sunlife.ca/kraft.

It can help you:

| • | Identify your retirement goals and how much you need to save |

| • | Consider the investment approach that best suits you – think about your comfort with risk and when you expect to need your money |

| • | Understand the investment options available to you, including fund performance and the fund manager strategy and style |

| • | Choose the funds that are right for you |

Kraft Canada provides you with tools to assist you in making your investment decisions but does not provide you with investment advice. If necessary, you should consider obtaining investment advice from an appropriately qualified individual in addition to using any tools provided by Kraft Canada.

Default Investment Funds

The default investment fund option for the RSP, NREG and GRRSP is a Target Date fund. Your RSP, NREG and GRRSP account balances will be invested in a Target Date fund that corresponds with your age if you do not make your own investment selection. Target Date funds are structured to coincide with an event or time in your life toward which you are saving, such as retirement or a major purchase. You determine when you will need your money and then pick the fund that matches that date. The fund’s asset mix will automatically shift towards more conservative investments as the target maturity date approaches.

Because Target Date funds are slightly more complex and require more active management by the fund manager, they typically have higher management fees than other investment options. For more information on Target Date funds, visit Sun Life Financial’s Plan Member Services website atwww.sunlife.ca/kraft.

14

Marital Breakdown

(applicable only to your Retirement Savings Plan)

Locked-in – Locked-in money must be used only to provide retirement income. It cannot be withdrawn as a lump sum and can be transferred, for example, to an insurance company to buy an annuity, or to a locked-in retirement vehicle.

Locked-in retirement vehicle – A locked-in retirement vehicle is another plan or contract in which the funds must ultimately be used to provide a regular income during retirement, and cannot be withdrawn as a lump sum. The availability and exact rules pertaining to retirement vehicles such as a locked-in retirement account (LIRA), life income fund (LIF) or locked-in retirement income fund (LRIF) depend on applicable legislation in your province of employment.

According to law, your Retirement Savings Plan (RSP) may be considered a family asset. This means that your pension may be taken into account in the overall division of your family assets if you have a marital breakdown.

However, it is important to note that the law does not automatically require pensions to be divided at source where a marital breakdown occurs. Rather, the treatment of any pension benefits will typically be set out in the separation agreement or divorce order.

Therefore, if you have a marital breakdown, we require receipt of certain documentation in order to ensure the plan is administered appropriately. Specifically, you must forward documentation including, but not necessarily limited to, the separation agreement, the divorce certificate and the divorce order to Sun Life Financial. The documentation you provide must be complete and meet all administrative requirements. Strict confidentiality rules are in place at Sun Life Financial and this documentation is used only for the necessary administration of the pension plan. Please note that the actual division of a pension at source in the context of a marital breakdown is governed by applicable pension law and the terms of the pension plan itself.

“Marital breakdown” may include the breakdown of a marriage and the breakdown of a common-law relationship.

Build your own funds