UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| X | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||||||

| For the fiscal year ended | December 31, 2008 | |||||||||

| TRANSITION REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||||||||||

| For the transition period from | to | |||||||||

| Commission file number | 000-30375 | |||||||||

| Las Vegas Gaming, Inc. | ||||||||||

| (Exact name of Registrant as specified in its charter) | ||||||||||

| Nevada | 88-0392994 | |||||||||

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||||||||

| 4000 West Ali Baba Lane, Suite D, Las Vegas, Nevada | 89118 | |||||||||

| (Address of principal executive offices) | (Zip Code) | |||||||||

| Registrant’s telephone number, including area code: | (702) 871-7111 | |||||||||

| Securities registered under Section 12(b) of the Act: | ||||||||||

| Title of each class | Name of each exchange on which registered | |||||||||

| Securities registered under Section 12(g) of the Act: | ||||||||||

| Common Stock Series A, $.001 par value | ||||||||||

| (Title of each class) | ||||||||||

| (Title of each class) | ||||||||||

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No x | ||||||||||

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No x | ||||||||||

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o | ||||||||||

Indicate by check mark if the disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained in herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o | ||||||||||

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. Large accelerated filer o Accelerated filer o Non-accelerated filer (do not check if smaller reporting company) o Smaller reporting company x | ||||||||||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No x | ||||||||||

State the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter. $24,458,146. | ||

Indicate the number of shares outstanding of each of the registrant’s classes of common stock, as of the latest practicable date. | ||

| Common Stock Series A, $.001 par value | 14,849,690 shares as of December 31, 2008 | |

Documents Incorporated By Reference: Portions of our Proxy Statement relating to the 2009 annual stockholders meeting are incorporated herein by reference in Part III. Such Proxy Statement will be filed with the Securities and Exchange Commission not later than 120 days after the conclusion of the registrant’s fiscal year ended December 31, 2008. | ||

| ITEM 1. | 1 | |

| ITEM 1A. | 17 | |

ITEM 1B. | 17 | |

| ITEM 2. | 17 | |

| ITEM 3. | 17 | |

| ITEM 4. | 18 | |

| ITEM 5. | 19 | |

| ITEM 6. | 24 | |

| ITEM 7. | 24 | |

ITEM 7A. | 31 | |

| ITEM 8. | 32 | |

| ITEM 9. | 56 | |

ITEM 9A(T). | 56 | |

ITEM 9B. | 56 | |

| ITEM 10. | 57 | |

| ITEM 11. | 57 | |

| ITEM 12. | 57 | |

| ITEM 13. | 57 | |

| ITEM 14. | 57 | |

| ITEM 15. | 57 |

__________________________

PlayerVision, RoutePromo, NumberVision, WagerVision, AdVision, Nevada Numbers, The Million Dollar Ticket, and Nevada Keno are some of our trademarks. This Annual Report on Form 10-K contains trademarks and trade names of other parties, corporations and organizations.

PART I

ITEM 1. BUSINESS.

Overview

During 2008 we continued to focus our development efforts on our proprietary application delivery system, known as PlayerVision. Through our PlayerVision system, we offer gaming operators the ability to increase the productivity of their existing gaming machines by delivering additional wagering opportunities, customer service enhancements, entertainment applications, games, and other content to their existing gaming machines, such as slot machines, poker machines, and video lottery terminals. Our PlayerVision system is flexible and compatible with virtually all gaming machines currently produced by all major manufacturers. As a result, we view every gaming machine as a revenue opportunity for our PlayerVision system. Since we plan to offer an option to acquire PlayerVision at little or no up front capital cost to casino operators in exchange for a recurring licensing fee, we expect to provide operators with an ability to increase significantly the earning power and functionality of their gaming machines with little or no financial risk. In addition, we are currently a leading supplier of keno and bingo games, systems, and supplies.

The PlayerVision system consists of proprietary software that runs on our own hardware as well as other vendors’ server based application delivery systems such as IGT’s sbX. Our ability to deliver applications through our own delivery system as well as that of other server based gaming systems provides our customers with the ability to achieve 100% gaming floor coverage without the need to replace their existing machines. Our system gives our customers a transition path from legacy machines to server based gaming.

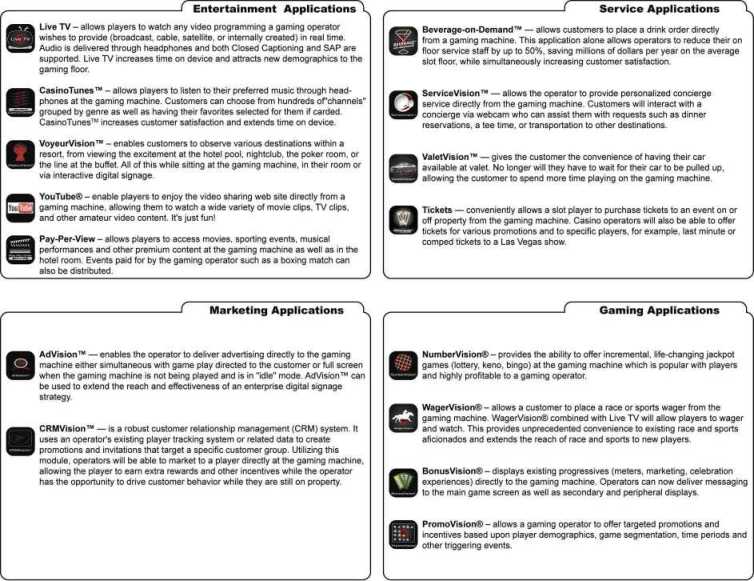

There are four delivery channels related to PlayerVision functionality: service, marketing, entertainment and gaming. Each application group addresses a specific cost reduction, revenue enhancing application set, player experience or operator control feature, including “Beverage-on-Demand”, NumberVision and WagerVision - turning each gaming machine into a multi-tasking touch-point for the customer who will see more, do more and - as a result - play more.

In addition to the PlayerVision applications identified above, it is our mission to develop new applications that will position PlayerVision as a platform for a variety of new multimedia and gaming functions.

We have received final regulatory approval from Nevada and Gaming Laboratories International (GLI), an independent accredited testing laboratory, for two applications on our PlayerVision 2 platform; AdVision and Live TV, on several different gaming machine platforms. We have also received GLI approval for NumberVision on our PlayerVision 2 platform. PlayerVision 3 is the next generation of our PlayerVision system. It is more robust and scalable than our PlayerVision 2 platform and has become our go-to-market product. The following applications will be submitted for regulatory review and approval to Nevada and GLI in April 2009 in regards to our PlayerVision 3 platform: Beverage on Demand, ServiceVision, ValetVision, AdVision, Live TV, Casino Tunes, You Tube, and VoyeurVision. Because these eight software applications do not interface with the slot accounting system and the regulators are

familiar with the earlier PlayerVision 2 platform, we expect a shorter approval time period from the regulators. We expect to submit WagerVision and NumberVision for regulatory approval from Nevada and GLI on the PlayerVision 3 platform sometime between June and August 2009. Because the regulatory approval of new gaming applications is a complex process, we may experience delays in developing and introducing the PlayerVision 3 applications. Because of the substantial ongoing costs of the PlayerVision system, we will continue to require substantial third-party financing, in addition to any funds from operations, to pursue our business plan. During 2008 we raised over $14 million in private placements, and we estimate that we will need to raise at least another $10 million in 2009 in order to accomplish our 2009 plan. We expect to raise the additional funds through one or more private placements and master lease equipment financings (see “Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations—Liquidity and Capital Resources”). No assurance can be given that we will be able to raise such additional funds or complete such private placements or equipment financings on terms acceptable to us, or at all.

Industry Overview

The domestic and global gaming markets have grown rapidly and consistently over most of the last decade despite some slowdown in the past year due to the macroeconomic recession. This growth has generally brought increased social and political acceptance of legalized gaming throughout many diverse societies. As a result, there is a rising public sector / municipal dependency on gaming revenues for funding of programs and projects that would not otherwise exist. In the United States, the gaming industry is a $60.3 billion business consisting of 860 casinos spread throughout 48 states. In addition, many jurisdictions are currently pushing for liberalization of existing gaming legislation and introduction of new regulations designed to augment sources of gaming tax revenue. Twelve states now allow commercial (non-tribal) gaming, compared to only two in 1980.

The conventional wisdom that the gaming industry is recession-proof has been challenged over the last 12 months. However, recent economic pressures have prompted new efforts to legalize casino gaming and to liberalize gaming laws to fill fiscal gaps. Furthermore, in the current environment, operators are pressured to extract the most out of existing operations by enhancing the competitiveness of their slot machine floor at minimal investment rather than deploying cash into new or expanded equipment or facilities. While historical U.S. trends suggest a resilient recovery will eventually be at hand, through our PlayerVision product we expect to offer the casino operator a product that will enhance the gaming machine’s productivity while simultaneously enhancing the customer’s playing experience – all with little or no money up front.

PlayerVision can also be deployed outside the United States. Casinos in jurisdictions such as Macau, Western and Central Europe, South Korea, Singapore, Australia, Japan, Vietnam, Taiwan, and the Philippines should be attracted to our product. However, we will need to get approval from the relevant regulatory bodies prior to a roll out of PlayerVision in these jurisdictions.

1.7 million EGMs (Electronic Gaming Machines or slot machines as they are commonly referred to) were installed worldwide as of the end of 2007, with approximately 50% in North America. These machines represent the gaming industry's most resilient and predictable revenue stream and usually comprise well over 50% of total gaming revenue for the typical casino operator. The historical EGM average unit replacement cycle of 5-6 years will likely be stretched out over the next few years as the recession works its way out of the world economy. However, new technology may disrupt the normal replacement cycle. The last such technology was the "Ticket-In-Ticket-Out" revolution in 2000. We believe the next such revolution will be Server-Based Gaming, which allows operators to manage casino floors more effectively and efficiently. It will also usher into the gaming industry the art of multi-tasking as the EGM will now be able to provide the player several experiences concurrently with gambling on the next pull of the handle (or more typically, the next push of the button).

Increased popularity and social acceptance of gaming as a leisure activity is also fueling the growth of server-based gaming. According to the 2008 American Gaming Association Survey of Casino Entertainment, 84% of Americans believe that casino gaming is an acceptable activity for themselves or

others, an increase of 5% since 2006. The simplicity and instant appeal of EGMs versus other gambling opportunities create familiarity and adoption across the board, characterized by ease-of-use and informality. EGMs have demonstrated greater appeal than any other gaming activity. Additionally, technology has become a significant part of the gaming experience, allowing for more innovative content and customer convenience. A new younger player demographic translates into a multi-tasking "user interface" that creates new revenue opportunities.

We believe that the global casino and gaming industry, over time, will grow due to the increasing acceptance of gaming as a form of entertainment and the increasing need of various jurisdictions for increased revenue from taxes. EGM growth is expected to grow even faster than casino growth as a result of the following:

| · | Simplicity and instant appeal of gaming machines versus other games. Characterized by simplicity and informality, gaming machines have greater appeal to all eligible demographic segments of the population than any other gaming activity. |

| · | Continuing evolution of gaming machines. The launch of cashless technology (ticket-in/ticket-out versus coins or tokens) in 2000, the introduction of new and more sophisticated and interactive theme-based games and the increasing non-gaming functionality currently becoming available on the EGM platform. |

As the gaming machine base continues to grow we believe that our target market will continue to expand. We believe that a consistent need for improvement in gaming activities and demand for greater entertainment value for players will give us the ability to market PlayerVision aggressively and to provide gaming operators with a single solution to introduce additional functionality without a wholesale replacement of their existing gaming machines.

Our Strategy

Our strategy is to provide the premier enhancement system for the installed base of gaming machines by delivering additional wagering opportunities, cost saving opportunities, promotions, games, and other content on existing gaming machines and delivering those same applications over the newer server based deliver systems and gaming machines. No assurance can be given, however, that we will be successful. In order to achieve this objective, we are pursuing the following strategies:

| · | Increased Revenue Potential for Operators. Our sales effort stresses the ability of our PlayerVision system to provide gaming operators with the opportunity to increase significantly the earning power and functionality of their gaming machines. Since our PlayerVision system directly interfaces with the existing video, audio, and printing functions of the machine, we are able to use the machine’s existing video screen (or attached alternatives) to deliver additional games, promotions, additional wagering opportunities, and other forms of entertainment. If desired by our customers, we have a kiosk driven ticket redemption system featuring its own accounting system separate and apart from the main slot accounting system. We can also provide alternative viewing options if the casino operator would prefer not to use the main screen. |

| · | Compelling Patron Experience. We expect to offer PlayerVision as a single multimedia delivery system for a wide range of content directly on the existing screens of gaming machines. By adding PlayerVision, a gaming machine is transformed from a single use, single wager option into a multimedia experience that can deliver to the player extra wagering opportunities and targeted, promotional content in addition to traditional slot play. Through PlayerVision, the operator will be able to enhance the functionality of its existing EGMs and deliver targeted gaming opportunities and promotional content to players. In exchange, the player will receive an enhanced playing experience, information about promotions, entertainment, and dining opportunities, and the opportunity to win jackpots and other prizes. |

| · | Reduce operating costs. Through our Beverage on Demand feature, an operator may be able to cut its drink delivery costs approximately in half. |

| · | Low Operator Risk. As an alternative, we expect to offer the gaming operators the ability to substantially reduce operating cost, extend the replacement cycle and increase significantly the earning power and functionality of their existing gaming machines at little or no up front capital cost. This strategy involves installing PlayerVision at little or no up front capital cost to gaming operators in exchange for recurring software license fees. |

| · | New Applications. We plan to continue the development of innovative applications to be delivered through our PlayerVision system. To date, we have designed our PlayerVision system to deliver advertisements, multimedia content, casino services, promotional materials, and wagering opportunities. Since PlayerVision engages the existing video, audio and printing functions of the gaming machine, and since our kiosk driven ticket redemption system features its own path to the slot accounting system, we believe that our PlayerVision system can be used as a platform to deliver a wide array of casino services, multimedia or gaming content directly to patrons. |

PlayerVision is a single, flexible, and dynamic platform that can be used to deliver casino services, multimedia or gaming content developed either by us or third parties. Because of the integration of PlayerVision with all of the functions of the gaming machine, we expect that PlayerVision can be used by gaming operators to control all aspects of their gaming machines. By establishing our PlayerVision system as the premier enhancement system for the installed base of gaming machines, we believe that we will be able to establish a significant barrier to entry for any potential competitors.

PlayerVision System

With deployment of PlayerVision, players will at once enjoy a multi-wagering/multi-tasking immersive experience that results in a substantial increase in percentage of wallet for the operator. A powerful retrofit solution, we expect that PlayerVision will enable operators to reduce operating costs and increase efficiencies for both new and legacy gaming floors, featuring;

| · | On-the-fly machine "customization" by casino and customer at minimal cost, using existing slot screens for a variety of innovative applications; |

| · | Increased time on device with added wagering and targeted marketing; |

| · | Beverage-on-demand, allowing reduced head count with improved player experience; |

| · | On-demand multimedia offering private access to shows, products and services. |

We expect to offer PlayerVision at a little to no up front capital cost to the operator in exchange for recurring license fees, thereby increasing earning power and functionality of gaming machines without financial risk.

Slot operations serve as the primary source of revenue in almost any gaming operation. In need of sources of incremental revenue and cost savings, the industry is primed for a technology that utilizes the processing power now available through server-based environments. By installing off-the-shelf CPUs into any EGM (a 30-minute process), PlayerVision converts a single-use slot machine into a multi-dimensional revenue generator and cost container. We believe we are the developer/owner of some of the most significant IP and technology in the industry related to deployment of server-based gaming applications. No assurances can be given that the deployment of server-based gaming applications will be successful or that our IP and technology will play a significant role in server-based gaming applications.

Casino Games

We operate two keno games, Nevada Numbers and The Million Dollar Ticket, and collect royalties on several bingo style games. The revenue generated from our casino games is primarily based on collecting per ticket or per game fees from our various customers. On March 31, 2009, our contract with Treasure Island to maintain the $3.9 million base jackpot bankroll for Nevada Numbers and The Million Dollar Ticket expired, and we shut down the games as a result. We expect to restart the games as soon as we find funding for the $3.9 million base jackpot.

Nevada Numbers

Nevada Numbers is a variation of classic keno which is currently played in many casinos in Nevada. Keno is a game in which bets are made and recorded on a keno ticket. This ticket contains 80 numbered squares that correspond exactly to 80 numbered balls in a selection hopper. A player marks a ticket to play between two and 20 different numbers. The keno operator then draws 20 out of the 80 numbers and displays the results throughout the casino. The more numbers that match, the more money the player wins. Payout awards vary from casino to casino and depend on the amounts wagered.

Nevada Numbers differs from classic keno in that fewer numbers (five rather than 20) are drawn and a “linked’’ or “progressive’’ component has been added. We have linked together the play of Nevada Numbers at multiple casinos so that players at several different locations all choose numbers that are matched to the same five-number draw. In addition, Nevada Numbers features a starting jackpot of $5.0 million that is progressive, in that it grows with the purchase of each Nevada Numbers ticket and can be won at each draw. Any winner of the Nevada Numbers progressive jackpot will be paid the amount of the progressive meter in equal installments over a period of 20 years. At our sole discretion, we may offer the winner an option to receive a discounted value immediately. The process of linking games and creating a progressive jackpot provides an enticement to players because of the potential for a life-changing event.

Although Nevada Numbers has traditionally been limited to the keno lounges of casinos, we are taking measures to expand its visibility. First, we have incorporated Nevada Numbers as part of NumberVision. Through NumberVision, we propose to position Nevada Numbers as a dynamic game that will give players the opportunity to win a progressive jackpot of at least $5.0 million. Second, subject to regulatory approval of NumberVision, we will market the game to third-party race and sports books for use on their existing wagering terminals.

The Million Dollar Ticket

Based on the classic keno game, The Million Dollar Ticket offers the chance to win $1.0 million and a progressive jackpot. In order to win the $1.0 million and the progressive jackpot, the player must pick 10 numbers correctly out of 20 drawn from a pool of 80. Although the distribution of The Million Dollar Ticket is limited, we are anticipating growth in 2009 by making the game available in third-party race and sports book locations.

Super Bingo Games

Super Bingo Games are odds-based bingo games with life-changing prizes that are offered as side bets to existing bingo games. We offer these games at various jackpot levels-as high as $500,000 in some cases. We purchase insurance for the larger jackpots. Our Super Games are structured so that the bingo operator is guaranteed a profit for each wager made. We have placed Super Bingo Games in seven Nevada casinos and eighteen non-Nevada locations. We expect to grow the Super Bingo Games segment in both Nevada and non-Nevada locations throughout 2009.

Keno and Bingo Systems and Supplies

The worldwide keno system market is limited and has been declining for several years. We are attempting to invigorate the market and gain an additional share of the market by enhancing our keno system through the addition of several new games and features to the platform.

Keno and bingo supplies sales contribute significantly to our revenue, but consist of low margin items, including crayons, various paper products, and ink.

Other Businesses

We also generate revenue through various keno participation agreements and the maintenance of our equipment under service contracts.

| · | Nevada Keno and Related Participation Agreements. Through agreements with participating casinos, we offer Nevada Keno, a “satellite-linked’’ traditional keno game played in multiple casinos. Nevada Keno was temporarily discontinued on February 29, 2008, and then restarted in the fall of 2008. We are currently operating Nevada Keno in two casinos. However, we believe we will soon be operating in 2-3 more. However, no assurances can be given that we will operate Nevada Keno in additional casinos. Additionally, principally in Nebraska, we provide equipment in return for a share in the revenue generated in various keno salons. |

| · | Service Contracts. Most of our customers that purchase keno and bingo equipment also purchase a service contract from us to provide routine maintenance for the equipment. |

RoutePromo

RoutePromo is designed to deliver promotional tickets or vouchers to players upon the occurrence of an event specified by the operator, such as hitting a four-of-a-kind or better on a video poker machine. The key feature of RoutePromo is its ability to recognize a specified event generated by the game and deliver the programmed response to the specified event.

RoutePromo is designed to work as follows:

| · | first, the operator specifies the events that will trigger RoutePromo, such as a four-of-a- kind or better on a video poker machine; |

| · | second, upon the occurrence of the specified event, RoutePromo is activated and a message is sent to the gaming machine to issue a promotional ticket or voucher; |

| · | third, the gaming machine alerts the player and prints the free promotional ticket or voucher; and |

| · | fourth, the gaming machine returns to its original state. |

We currently charge a fixed monthly fee for the ability to offer RoutePromo.

Through our agreement with United Coin Machine Company, the largest slot route operator in Nevada, we developed a variation of our keno game called The Million Dollar Ticket, known as the Gamblers Bonus Million Dollar Ticket, to be used in conjunction with RoutePromo. Gamblers Bonus Million Dollar Ticket is a free promotional game that gives players the chance to win various prizes,

including a $1.0 million grand prize, by matching numbers on their promotional tickets with numbers picked in a random weekly drawing. Under our agreement, we are obligated to provide software, hardware, and support to United Coin for the game. In addition, we are financially responsible for the payouts associated with the game. In return, United Coin is obligated to pay us $1.25 for each ticket distributed. During the second quarter of 2008, we rolled out Gamblers Bonus Million Dollar Ticket at approximately 100 United Coin route locations. On January 31, 2009, we closed down the game because there was little interest among bar owners and convenience store owners to offer an expensive promotion in difficult economic times.

Manufacturing

We outsource the manufacturing of the various components of our PlayerVision 3 system to Apple, Hitachi, and various other key suppliers. Lead times for certain key components can be as long as eight weeks.

Marketing and Distribution

PlayerVision

As part of our objective to provide the leading single multimedia and game delivery system, we have started to implement a plan that will market our PlayerVision system to customers through direct and indirect channels. Our plan involves the following steps:

| · | Direct Sales Efforts. Through the hiring of additional personnel to our sales and marketing staff, we will market PlayerVision to operators located primarily in North America and to Native American tribes. As part of our direct sales efforts, we attend trade shows, such as G2E in Las Vegas, Nevada. |

| · | Strategic Partnerships. We supplement our direct sales efforts by targeting third-party distributors and regional operators. IGT and Ebet are key examples of entities that we expect will be distributing our product. By forming strategic relationships with these parties, we hope to gain access to smaller and more fragmented markets around the globe and secure the broadest placement for PlayerVision. |

We plan to conduct all of our sales and marketing efforts from our headquarters in Las Vegas, Nevada. Although we do not have any current plans to open any sales offices, we will review the need for such additional offices in response to the needs of our customers and our strategic partners.

Casino Games

We license our games directly to casinos. We make initial contacts through the mailing of marketing materials, referrals, or direct solicitation by our employees and marketing agents. We promote licensed games to the general public using various types of media, including billboards, newspapers, magazines, radio, and television. Advertising within a particular casino may include advertisement on strategically placed LCDs, table tents, flyers, signs on the tops of gaming machines, and show cards to stimulate curiosity and game play.

Keno and Bingo Systems and Supplies.

We are one of the world’s few keno equipment suppliers. Most sales in this area result from unsolicited inquiries or direct solicitation of customers by our sales staff. The marketplace for bingo equipment, electronic playing devices, and supplies in Nevada is relatively small, consisting of approximately 40 potential customers. However, we believe that the recent introduction of wireless gaming devices into the marketplace in Nevada and other jurisdictions may increase the potential market

for bingo-related products. No assurance can be given that the market for bingo-related products will increase. Direct sales to the casino are the primary means of sale for these products. The marketplace for gaming supplies is large and geographically dispersed. Our primary marketing tool is a catalog that we periodically distribute to our customers and potential customers.

Competition

PlayerVision System

We encounter significant competition in the market for innovative gaming technologies that deliver interactive gaming, animated content, and cross-promotional opportunities to gaming operators. The key competitive factors are functionality, accuracy, reliability, and pricing. We believe that PlayerVision is a single, integrated solution because of the following:

| · | PlayerVision uses the existing primary screen of the gaming machine or a smaller secondary video screen or a mounted side screen; |

| · | PlayerVision engages the existing video, audio and printing functions of the gaming machine regardless of the manufacturer; |

| · | PlayerVision involves little or no up front capital cost to gaming operators; and |

| · | PlayerVision delivers a broad range of functionalities. |

We are unaware of any other product that delivers casino services, multimedia and gaming content through the existing various screens of gaming machines. Although we face competition from products that use smaller secondary video screens and cost thousands of dollars, such as iView developed by Bally Systems and NexGen developed by International Game Technology, we expect to be able to deliver content for little or no up front capital cost and deliver the content directly to the patron through all existing screens rather than just an auxiliary 2x6-inch screen. In terms of deployment, we believe that there is no one else offering a content delivery system for existing gaming machines on the main screen.

Since we are able to use all existing screens of a gaming machine, as well as its existing video, audio and printing functions, we expect to offer to gaming operators a solution that requires little or no up front capital cost, involves minimal installation time, and interfaces with virtually all gaming machines. In addition, although there are products that deliver advertising or promotional content through secondary video screens installed onto gaming machines, we do not believe that there are currently any products that can deliver the additional wagering opportunities that PlayerVision can or any products that can provide an expandable platform for additional content on the existing screens of gaming machines.

Nevertheless, there is no guarantee that PlayerVision will be accepted in the marketplace. Many of our potential competitors possess substantially greater financial, technical, marketing, and other resources than we do, which affords them competitive advantages over us. As a result, our competitors may introduce products that have advantages over PlayerVision in terms of features, functionality, ease of use, and revenue producing potential. If we are unable to compete effectively, or incur any delays, either regulatory or otherwise, in our ability to fully introduce PlayerVision, our operations and financial condition may be adversely affected.

Keno and Bingo Systems and Supplies.

The keno and bingo systems and supplies industry is characterized by limited competition. We compete primarily with other companies that provide keno and bingo systems, including electronic systems, keno, bingo supplies, and related services. In addition, we compete with other similar forms of entertainment, including casino gaming, other forms of Class II gaming, and lotteries. Our key competitor is XpertX in the keno market. We compete by providing superior service, lower prices, innovative games, and a quality fully functional keno system.

Research and Development

Our research and development efforts focus on developing new applications for our PlayerVision system and reducing its cost. During 2008 we considerably expanded our internal R&D effort by employing 5 new software engineers, one of which became our Chief Technical Officer in March 2008. In addition to our own research and development staff, we plan to engage, from time to time, independent consultants and advisors to assist us.

Intellectual Property and Other Proprietary Rights

We hold several patents, including a patent related to Nevada Numbers. We have been recently issued a patent for “closed loop,” a key application in our PlayerVision technology. In addition, we have several more patents pending with respect to the PlayerVision system and certain of its various applications. We also hold several trademarks filed with the state of Nevada and the U.S. Patent and Trademark Office, including trademark rights to PlayerVision, Nevada Numbers and The Million Dollar Ticket, and other intellectual property that is protected by federal copyright and trade secret laws.

We rely on the proprietary nature of our intellectual property, primarily in the form of patent protection, for development of our products. We believe that our success depends in part on protecting our intellectual property. If we cannot protect our intellectual property against the unauthorized use by others, our competitive position could be harmed.

The risks associated with our intellectual property, include the following:

| · | The inability of intellectual property laws to protect our intellectual property rights; |

| · | Attempts by third parties to challenge, invalidate, or circumvent our intellectual property rights; |

| · | The unauthorized use by third parties of information that we regard as proprietary despite our efforts to protect our proprietary rights; |

| · | The independent development of similar technology; and |

| · | The inability to protect our intellectual property rights in foreign jurisdictions. |

We may not be able to obtain effective patent, trademark, service mark, copyright, and trade secret protection in every country in which our products are used. We may find it necessary to take legal action to enforce or protect our intellectual property rights or to defend against claims of infringement, and such actions may be unsuccessful. In addition, we may not be able to obtain a favorable outcome in any intellectual property litigation. Significant amounts could be expended to defend and protect our intellectual property. Moreover, our competitors may develop products or technologies similar to ours without infringing on our intellectual property rights.

Government Regulation

We are subject to regulation by governmental authorities in most jurisdictions in which we operate. Gaming regulatory requirements vary from jurisdiction to jurisdiction, and obtaining licenses and findings of suitability for our officers, directors, and principal stockholders, registrations, and other required approvals with respect to us, our personnel, and our products are time consuming and expensive. Generally, gaming regulatory authorities have broad discretionary powers and may deny applications for or revoke approvals on any basis they deem reasonable. We have approvals that enable us to conduct our business in numerous jurisdictions, subject in each case to the conditions of the particular approvals. These conditions may include limitations as to the type of game or product we may sell or lease, as well as limitations on the type of facility, such as riverboats, and the territory within which we may operate, such as tribal nations.

Jurisdictions in which we, and specific personnel, where required, have authorizations with respect to some or all of our products and activities include New Jersey, Nevada, Mississippi, Arizona, Nebraska, Oregon, Washington, Iowa, Minnesota and Montana. In addition to these jurisdictions, we have authorizations with respect to certain Native American tribes throughout the United States that have compacts with the states in which their tribal dominions are located or operate or propose to operate casinos. These tribes may require suppliers of gaming and gaming-related equipment to obtain authorizations.

Overview

Gaming Devices and Equipment. We sell or lease products that are considered to be “gaming devices’’ or “gaming equipment’’ in jurisdictions in which gaming has been legalized. Although regulations vary among jurisdictions, each jurisdiction requires various licenses, findings of suitability, registrations, approvals, or permits for companies and their key personnel in connection with the manufacture and distribution of gaming devices and equipment.

Associated Equipment. Some of our products fall within the general classification of “associated equipment.’’ “Associated equipment’’ is equipment that is not classified as a “gaming device,’’ but which has an integral relationship to the conduct of licensed gaming. Regulatory authorities in some jurisdictions have the discretion to require manufacturers and distributors to meet licensing or suitability requirements prior to or concurrently with the use of associated equipment. In other jurisdictions, the regulatory authorities must approve associated equipment in advance of its use at licensed locations. We have obtained approval of our associated equipment in each jurisdiction that requires such approval and in which our products that are classified as associated equipment are sold or used.

Regulation of Officers, Directors, and Stockholders. In many jurisdictions, any officer or director is required to file an application for a license, finding of suitability, or other approval and, in the process, subject himself or herself to an investigation by those authorities. As for stockholders, any beneficial owner of our voting securities or other securities may, at the discretion of the gaming regulatory authorities, be required to file an application for a license, finding of suitability, or other approval and, in the process, subject himself or herself to an investigation by those authorities. The gaming laws and regulations of most jurisdictions require beneficial owners of more than 5% of our outstanding voting securities to file certain reports and may require our key employees or other affiliated persons to undergo investigation for licensing or findings of suitability.

In the event a gaming jurisdiction determines that an officer, director, key employee, stockholder, or other personnel of our company is unsuitable to act in such a capacity, we will be required to terminate our relationship with such person or lose our rights and privileges in that jurisdiction. This may have a materially adverse effect on us. We may be unable to obtain all the necessary licenses and approvals or ensure that our officers, directors, key employees, affiliates, and certain other stockholders will satisfy the suitability requirements in each jurisdiction in which our products are sold or used. The failure to obtain such licenses and approvals in one jurisdiction may affect our licensure and approvals in other jurisdictions. In addition, a significant delay in obtaining such licenses and approvals could have a material adverse effect on our business prospects.

Regulation and Licensing – Nevada

The manufacture, sale, and distribution of gaming devices for use or play in Nevada or for distribution outside of Nevada, the manufacturing and distribution of associated equipment for use in Nevada, and the operation of gaming machine routes and inter-casino linked systems in Nevada are subject to the Nevada Gaming Control Act and the regulations promulgated thereunder and various local ordinances and regulations. These activities are subject to the licensing and regulatory control of various Nevada gaming authorities, including the Nevada Gaming Commission, the Nevada State Gaming Control Board, and various local, city, and county regulatory agencies, collectively referred to as the Nevada Gaming Authorities.

The laws, regulations, and supervisory practices of the Nevada Gaming Authorities are based upon declarations of public policy with the following objectives:

| · | preventing any direct or indirect involvement of any unsavory or unsuitable persons in gaming or the manufacture or distribution of gaming devices at any time or in any capacity; |

| · | strictly regulating all persons, locations, practices, and activities related to the operation of licensed gaming establishments and the manufacturing or distribution of gaming devices and equipment; |

| · | establishing and maintaining responsible accounting practices and procedures; |

| · | maintaining effective controls over the financial practices of licensees, including requirements covering minimum procedures for internal fiscal controls and safeguarding assets and revenue, reliable recordkeeping, and periodic reports to be filed with the Nevada Gaming Authorities; |

| · | preventing cheating and fraudulent practices; and |

| · | providing and monitoring sources of state and local revenue based on taxation and licensing fees. |

Change in such laws, regulations, and procedures could have an adverse effect on our operations.

We are registered with the Nevada Gaming Commission as a publicly traded corporation, or a Registered Corporation. We are also licensed in Nevada as a manufacturer and distributor of gaming devices and as an operator of an inter-casino linked system. We have obtained from the Nevada Gaming Authorities the various authorizations they require to engage in manufacturing, distribution, and inter-casino linked system activities in Nevada. The regulatory requirements set forth below apply to us as a Registered Corporation and as a manufacturer, distributor, and operator of an inter-casino linked system. Our gaming approvals and licenses are also conditioned to allow the Chairman of the Nevada State Gaming Control Board or his designee to order us to cease any gaming activities if the Chairman determines that the minimum bankroll requirements set forth in the Nevada Gaming Control Act are not being met.

All gaming devices that are manufactured, sold, or distributed for use or play in Nevada, or for distribution outside of Nevada, must be manufactured by licensed manufacturers and distributed and sold by licensed distributors. The Nevada Gaming Commission must approve all gaming devices manufactured for use or play in Nevada before distribution or exposure for play. The Chairman of the Nevada State Gaming Control Board must administratively approve associated equipment before it is distributed for use in Nevada. Inter-casino linked systems must also be approved by the Nevada Gaming Commission. The approval process for an inter-casino linked system includes rigorous testing by the Nevada State Gaming Control Board, a field trial, and a determination as to whether the inter-casino linked system meets standards that are set forth in the regulations of the Nevada Gaming Commission. On November 19, 2001, we received the final approval of the Nevada Gaming Commission for our inter-casino linked system known as Nevada Numbers. In November 2007, we received final approval from Nevada for our AdVision and Live TV software applications on the PlayerVision 2 platform on IGT Game

King Machines only. In addition, the Nevada Gaming Control Act requires any person, such as our company as an operator of an inter-casino linked system, that receives a share of gaming revenue from a gaming device operated on the premises of a licensee, to remit and be liable to the licensee for that person’s proportionate share of the license fees and tax paid by the licensee. The gross revenue fees for non-restricted locations are 6.75% of gross revenue, which is equal to the difference between amounts wagered by casino players and payments made to casino players. Significant increases in the fixed fees or taxes currently levied per machine or the fees currently levied on gross revenue could have a material adverse effect on our operations.

As a gaming licensee (a “Registered Corporation”), we are periodically required to submit detailed financial and operating reports to the Nevada Gaming Commission and furnish any other information the Nevada Gaming Commission may require. No person may receive any percentage of gaming revenue from us without first obtaining authorizations from the Nevada Gaming Authorities.

The Nevada Gaming Authorities may investigate any individual who has a material relationship to, or material involvement with, us in order to determine whether such individual is suitable or should be licensed as a business associate of a gaming licensee. Our officers, directors, and certain key employees are required to file applications with the Nevada Gaming Authorities and may be required to be licensed or found suitable by the Nevada Gaming Authorities. The Nevada Gaming Authorities may deny an application for licensing for any cause that they deem reasonable. A finding of suitability is comparable to licensing. Both require submission of detailed personal and financial information, which is followed by a thorough investigation. The applicant for licensing or a finding of suitability must pay all the costs of the investigation. Changes in licensed positions must be reported to the Nevada Gaming Authorities. In addition to their authority to deny an application for a finding of suitability or licensure, the Nevada Gaming Authorities have the power to disapprove a change in corporate position.

If the Nevada Gaming Authorities were to find an officer, director, or key employee unsuitable for licensing or unsuitable to continue having a relationship with us, we would have to sever all relationships with that person. In addition, the Nevada Gaming Commission may require us to terminate the employment of any person who refuses to file appropriate applications. Determinations of suitability or of questions pertaining to licensing are not subject to judicial review in Nevada.

We are required to submit detailed financial and operating reports to the Nevada Gaming Commission. In addition, we are required to report to or have approved by the Nevada Gaming Commission substantially all material loans, leases, sales of securities, and similar financing transactions.

Should we be found to have violated the Nevada Gaming Control Act, the licenses we hold could be limited, conditioned, suspended, or revoked. In addition, we and the persons involved could be required to pay substantial fines, at the discretion of the Nevada Gaming Commission, for each separate violation of the Nevada Gaming Control Act. The limitation, conditioning, or suspension of any of our licenses could, and revocation of any license would, materially adversely affect our manufacturing, distribution, and inter-casino linked system operations.

Regulation of Security Holders. Any beneficial holder of our voting securities, regardless of the number of shares owned, may be required to file an application, be investigated, and have his or her suitability as a beneficial holder of our voting securities determined if the Nevada Gaming Commission finds reason to believe that such ownership would otherwise be inconsistent with the declared policies of the state of Nevada. The applicant must pay all costs of investigation incurred by the Nevada Gaming Authorities in conducting any such investigation.

The Nevada Gaming Control Act requires any person that acquires beneficial ownership of more than 5% of a Registered Corporation’s voting securities to report the acquisition to the Nevada Gaming Commission. It also requires beneficial owners of more than 10% of a Registered Corporation’s voting securities to apply to the Nevada Gaming Commission for a finding of suitability within 30 days after the

Chairman of the Nevada State Gaming Control Board mails a written notice requiring such filing. Under certain circumstances, an “institutional investor,’’ as defined in the Nevada Gaming Control Act, which acquires more than 10%, but not more than 15%, of the Registered Corporation’s voting securities may apply to the Nevada Gaming Commission for a waiver of such finding of suitability if such institutional investor holds the voting securities for investment purposes only. An institutional investor that has obtained a waiver may, in certain circumstances, hold up to 19% of a Registered Corporation’s voting securities for a limited period of time and maintain the waiver.

An institutional investor is deemed to hold voting securities for investment purposes if the voting securities were acquired and are held in the ordinary course of its business as an institutional investor and were not acquired and are not held for the purpose of causing, directly or indirectly (1) the election of a majority of the members of the board of directors of the Registered Corporation; (2) any change in the Registered Corporation’s corporate charter, bylaws, management, policies, or operations or those of any of its gaming affiliates; or (3) any other action that the Nevada Gaming Commission finds to be inconsistent with holding the Registered Corporation’s voting securities for investment purposes only. Activities which are not deemed to be inconsistent with holding voting securities for investment purposes only include (a) voting on all matters voted on by stockholders; (b) making financial and other inquiries of management of the type normally made by securities analysts for informational purposes and not to cause a change in management, policies or operations; and (c) other activities the Nevada Gaming Commission may determine to be consistent with investment intent. If the beneficial holder of voting securities that must be found suitable is a corporation, partnership, or trust, it must submit detailed business and financial information, including a list of beneficial owners. The applicant is required to pay all costs of investigation.

Any person who fails or refuses to apply for a finding of suitability or a license within 30 days after being ordered to do so by the Nevada Gaming Commission or the Chairman of the Nevada State Gaming Control Board may be found unsuitable. The same restrictions apply to a record owner if the record owner, after request, fails to identify the beneficial owner. Any stockholder of a Registered Corporation found unsuitable and that holds, directly or indirectly, any beneficial ownership in the voting securities beyond such period of time as the Nevada Gaming Commission may specify for filing any required application may be guilty of a criminal offense. Moreover, the Registered Corporation will be subject to disciplinary action if, after it receives notice that a person is unsuitable to be a stockholder or to have any other relationship with the Registered Corporation, it (i) pays that person any dividend on its voting securities; (ii) allows that person to exercise, directly or indirectly, any voting right conferred through securities ownership; (iii) pays remuneration in any form to that person for services rendered or otherwise; or (iv) fails to pursue all lawful efforts (including, if necessary, the immediate purchase of said voting securities for cash at fair value) to require such unsuitable person to completely divest all voting securities held.

The Nevada Gaming Commission, in its discretion, may require the holder of any debt security of a Registered Corporation to file applications, be investigated, and be found suitable to own the debt security of a Registered Corporation if the Nevada Gaming Commission finds reason to believe that such ownership would otherwise be inconsistent with the declared policies of the state of Nevada. If the Nevada Gaming Commission determines that a person is unsuitable to own such security, it may sanction the Registered Corporation, which sanctions may include the loss of its approvals if, without the prior approval of the Nevada Gaming Commission, it: (i) pays to the unsuitable person any dividend, interest, or other distribution; (ii) recognizes any voting right of such unsuitable person in connection with such securities; (iii) pays the unsuitable person remuneration in any form; or (iv) makes any payment to the unsuitable person by way of principal, redemption, conversion, exchange, liquidation, or similar transaction.

Regulation of Capital Stock. We are required to maintain current stock ledgers in Nevada that may be examined by the Nevada Gaming Authorities at any time. If any securities are held in trust by an agent or by a nominee, the record owner may be required to disclose the identity of the beneficial owner to the Nevada Gaming Authorities. A failure to make such disclosure may be grounds for finding the record owner unsuitable. We are also required to render maximum assistance in determining the identity of the beneficial owners of our securities. The Nevada Gaming Commission has the power to require us to imprint our stock certificates with a legend stating that the securities are subject to the Nevada Gaming Control Act. To date, the Nevada Gaming Commission has not imposed such a requirement on us.

We may not make a public offering of our securities without the prior approval of the Nevada Gaming Commission if the securities or proceeds are to be used to construct, acquire, or finance gaming facilities in Nevada or to retire or extend obligations incurred for such purposes. Such approval, if given, does not constitute a finding, recommendation, or approval by the Nevada Gaming Commission or the Nevada State Gaming Control Board as to the accuracy or adequacy of the prospectus or the investment merit of the offered securities, and any representation to the contrary is unlawful. Any offer by us to sell common stock will require the review of, and prior approval by, the Nevada Gaming Commission.

Changes in Control. Changes in control of a Registered Corporation through merger, consolidation, stock or asset acquisitions, management or consulting agreements, or any act or conduct, by which anyone obtains control, may not lawfully occur without the prior approval of the Nevada Gaming Commission. Entities seeking to acquire control of a Registered Corporation must meet the strict standards established by the Nevada State Gaming Control Board and the Nevada Gaming Commission prior to assuming control of a Registered Corporation. The Nevada Gaming Commission also may require persons that intend to become controlling stockholders, officers, or directors, and other persons who expect to have a material relationship or involvement with the acquired company, to be investigated and licensed as part of the approval process.

The Nevada legislature has declared that some corporate acquisitions opposed by management, repurchases of voting securities, and corporate defense tactics affecting Nevada corporate gaming licensees, and Registered Corporations that are affiliated with those operations, may be injurious to stable and productive corporate gaming. The Nevada Gaming Commission has established a regulatory scheme to minimize the potentially adverse effects of these business practices upon Nevada’s gaming industry and to further Nevada’s policy to:

| · | assure the financial stability of corporate gaming licensees and their affiliates, |

| · | preserve the beneficial aspects of conducting business in the corporate form, and |

| · | promote a neutral environment for the orderly governance of corporate affairs. |

In certain circumstances, approvals are required from the Nevada Gaming Commission before the Registered Corporation can make exceptional repurchases of voting securities above market price and before a corporate acquisition opposed by management can be consummated. The Nevada Gaming Control Act also requires prior approval of a plan of recapitalization proposed by the Registered Corporation’s board of directors in response to a tender offer made directly to the Registered Corporation’s stockholders for the purpose of acquiring control of the Registered Corporation.

License Fees and Taxes. License fees and taxes, computed in various ways depending on the type of gaming or activity involved, must be paid to the state of Nevada and to the counties and cities in which gaming operations are conducted. These fees and taxes, depending upon their nature, are payable monthly, quarterly, or annually and are based upon either a percentage of the gross revenue received or the number of gaming devices operated. Annual fees are also payable to the state of Nevada for renewal of licenses as an operator of a gaming machine route, manufacturer, and/or distributor.

Any person who is licensed, required to be licensed, registered, required to be registered, or who is under common control with any such persons, collectively, “Licensees,’’ and who proposes to become involved in a gaming venture outside of Nevada, is required to deposit with the Nevada State Gaming Control Board, and thereafter maintain, a revolving fund in the amount of $10,000 to pay the expenses of investigation by the Nevada State Gaming Control Board of his or her participation outside of Nevada. The revolving fund is subject to increase or decrease at the discretion of the Nevada Gaming Commission. Thereafter, Licensees are required to comply with certain reporting requirements imposed by the Nevada Gaming Control Act. Licensees also are subject to disciplinary action by the Nevada Gaming Commission if they knowingly violate any laws of the foreign jurisdiction pertaining to the non-Nevada gaming operations, fail to conduct the foreign gaming operations in accordance with the standards of honesty and integrity required of Nevada gaming operations, engage in activities or enter into associations that are harmful to the state of Nevada or its ability to collect gaming taxes and fees, or employ, contract with, or associate with, a person in the non-Nevada operations who has been denied a license or finding of suitability in Nevada on the ground of unsuitability.

Other Jurisdictions

All other jurisdictions that have legalized gaming require various licenses, registrations, findings of suitability, permits, and approvals of manufacturers and distributors of gaming devices and equipment as well as licensure provisions related to changes in control. In general, such requirements involve restrictions similar to those of Nevada.

For gaming device and system approvals, most jurisdictions in the United States, including most Native American tribes and state regulatory agencies, accept testing results from GLI, a leading private gaming device and systems testing laboratory. GLI also provides testing services for over 400 gaming regulatory bodies worldwide. GLI has already approved NumberVision, AdVision and Live TV on our PlayerVision2 platform. We expect to submit for approval all of our software applications on the PlayerVision 3 platform sometime between June and August 2009. If necessary, we also plan to apply directly for approvals from those jurisdictions that do not accept GLI testing results for certain devices and systems, such as New Jersey, Pennsylvania, and Montana.

Federal Regulation

The Federal Gambling Devices Act of 1962, or the Federal Act, makes it unlawful, in general, for any person to manufacture, transport, or receive gaming machines, gaming machine type devices, and components across state lines or to operate gaming machines unless that person has first registered with the Attorney General of the United States. We have registered and must renew our registration annually. In addition, the Federal Act imposes various record keeping and equipment identification requirements. Violation of the Federal Act may result in seizure and forfeiture of the equipment, as well as other penalties.

Application of Future or Additional Regulatory Requirements

In the future, we intend to seek the necessary registrations, licenses, approvals, and findings of suitability for us, our products, and our personnel in other jurisdictions throughout the world where significant sales of our products are expected to be made. However, we may be unable to obtain these registrations, licenses, approvals, or findings of suitability, which if obtained may be revoked, suspended, or conditioned. In addition, we may be unable to obtain on a timely basis, or to obtain at all, the necessary approvals of our future products as they are developed, even in those jurisdictions in which we already have existing products licensed or approved. If a registration, license, approval or finding of suitability is required by a regulatory authority and we fail to seek or do not receive the necessary registration, license, approval or finding of suitability, we may be prohibited from selling our products for use in that jurisdiction or may be required to sell our products through other licensed entities at a reduced profit.

Employees

As of December 31, 2008, we had 48 full-time employees, 22 of whom were involved in keno and bingo operations, 8 of whom were involved in engineering and research and development, 5 of whom were involved in sales, and 13 of whom were involved in finance and administration. With the implementation of our new business focus on our PlayerVision system, we anticipate an increase in employees dedicated to developing and growing this business in the third quarter of 2009. Our employees are not subject to any collective bargaining agreement with us. We have never experienced a work stoppage, and we believe our employee relations to be good.

Corporate History

We were incorporated in the State of Nevada on April 28, 1998.

ITEM 1A. RISK FACTORS.

Not required.

ITEM 1B. UNRESOLVED STAFF COMMENTS.

Not required.

ITEM 2. PROPERTIES.

Our headquarters are located at 4000 West Ali Baba Lane, Suite D, Las Vegas, Nevada, 89118, which is comprised of approximately 8,200 square feet of office space and 10,000 square feet of warehouse space under a lease agreement recently extended to May 31, 2009. This space adequately meets our facility and capacity requirements; however, we are currently evaluating our alternatives as we plan to move to another location. We also have a Reno, Nevada office consisting of approximately 7,500 square feet of space under a recently executed lease that expires in 2012, and an Omaha, Nebraska service office consisting of approximately 880 square feet of space under a lease expiring on November 30, 2010.

ITEM 3. LEGAL PROCEEDINGS

On September 12, 2007, IGT filed a lawsuit against us in the United States District Court of Nevada captioned IGT v. Las Vegas Gaming, Inc., case no. 3:07-cv-00415-BES-VPC alleging copyright infringement, trademark infringement, trade dress infringement and false designation of origin relating to the operation of our PlayerVision system on IGT’s Game King® gaming machines. IGT was seeking injunctive and monetary relief in the case, including treble damages and profits, claiming that IGT would be irreparably harmed by LVGI if LVGI’s PlayerVision were deployed in the marketplace. On June 12, 2008, IGT and LVGI jointly filed a “stay” of the lawsuit and began settlement negotiations. On October 14, 2008, pursuant to the settlement effective September 30, 2008, the case was dismissed with prejudice.

On September 15, 2008, Steven Brandstetter and J & S Gaming filed a lawsuit against us, among other defendants, in Department 11 of the Nevada Eighth Judicial District Court captioned Brandstetter, et al. v. Bally Gaming, Inc., et al., case no. 08-A-571641-C alleging against us claims of breach of contract, misrepresentation, breach of fiduciary duty and unjust enrichment regarding a non-disclosure agreement executed in May 2002 pertaining to the plaintiffs’ gaming concepts. The plaintiffs are seeking monetary damages, including attorney’s fees and costs. We filed an answer to the complaint on December 8, 2008 citing eighteen affirmative defenses. Depositions have been scheduled for some of the executives of the larger company defendants. No depositions have been requested of any of our executives.

ITEM 4. SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS.

No matters were submitted to a vote of our security holders during the fourth quarter of the fiscal year ended December 31, 2008.

PART II

ITEM 5. MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES.

Our authorized capital stock consists of 90,000,000 shares of common stock, par value $0.001 per share, and 10,000,000 shares of preferred stock, par value $0.001 per share, that may be issued in one or more series.

Common Stock

Our Board of Directors has designated two series of common stock, one referred to as “Common Stock’’ and the other referred to as “Common Stock Series A.’’ As of December 31, 2008, there were no shares of our Common Stock outstanding and 14,849,690 shares of our Common Stock Series A outstanding held of record by 575 stockholders. There is no active market for our Common Stock or our Common Stock Series A.

Each share of Common Stock and Common Stock Series A has identical rights and privileges in every respect. Each holder of either Common Stock or Common Stock Series A has the right to cast one vote for each share held of record on all matters submitted to a vote of our holders of common stock. The holders of either series of common stock vote together as a single class except to the extent that voting as a separate class or series is required by law. The holders of both series of common stock are entitled to receive dividends on a pro rata basis, payable in cash, stock, or otherwise, as may be declared by our Board of Directors out of any funds legally available for the payment of dividends, subject to the rights of holders of any outstanding preferred stock. We did not declare any cash dividend on our Common Stock or Common Stock Series A in fiscal 2008 or 2007. Upon our liquidation, dissolution or winding-up, the holders of both series of common stock will be entitled to receive after distribution in full of any preferential amounts owed to debt holders or holders of our preferred stock, all of the remaining assets available for distribution ratably in proportion to the number of shares of common stock held by them. Neither series of our common stock provides holders with preferences or any preemptive, conversion or exchange rights. There are no redemption or sinking fund provisions applicable to either series of common stock.

Preferred Stock

Our articles of incorporation authorize our Board of Directors, without further stockholder action, to issue up to 10,000,000 shares of preferred stock in one or more series and to fix the designations, powers, preferences, and privileges of the preferred stock, including dividend rights, conversion rights, voting rights, terms of redemption, liquidation preference, sinking fund terms, and number of shares constituting any series or the designation of any series. Our Board of Directors, without stockholder approval, has the authority to issue preferred stock with voting, conversion, or other rights that could adversely affect the voting power and other rights of the holders of common stock. Depending upon the terms of preferred stock established by our Board of Directors, any or all series of preferred stock could have preference over common stock with respect to dividends and other distributions and upon our liquidation, and could have the effect of delaying or preventing a change in control or making removal of management more difficult. If any shares of preferred stock are issued with voting powers, the voting power of the outstanding common stock would be diluted. Additionally, the issuance of preferred stock may have the effect of decreasing the market price of our common stock.

Our Board of Directors has designated the following six series of preferred stock, where the conversion ratio, the authorized number of shares and the outstanding number of shares for each series are provided:

| · | “Series B Convertible Preferred Stock’’ – convertible into Common Stock Series A on a one-to-five basis, 76,750 shares authorized and 50,000 shares outstanding as of December 31, 2008; |

| · | “Series E Convertible Preferred Stock” – convertible into Common Stock Series A on a one-to-one basis, 810,800 shares authorized and 810,800 shares outstanding as of December 31, 2008. |

| · | “Series F Convertible Preferred Stock” – convertible into Common Stock Series A at the lower of $3.50 or 30% off the IPO price, where “IPO price” means the per share price to the public of any common shares offered by us that in the aggregate results in capital in excess of $10.0 million being raised and the shares of a class of our common stock being listed and traded on a national stock exchange. There are 200,000 shares authorized and 200,000 shares outstanding as of December 31, 2008. |

| · | “Series G Convertible Preferred Stock” – convertible into Common Stock Series A at the lower of $3.50 or 30% off the IPO price, where “IPO price” means the per share price to the public of any common shares offered by us that in the aggregate results in capital in excess of $10.0 million being raised and the shares of a class of our common stock being listed and traded on a national stock exchange. There are 150,000 shares authorized and 150,000 shares outstanding as of December 31, 2008. |

| · | “Series H Convertible Preferred Stock” – convertible into Common Stock Series A at the lower of $2.50 or 30% off the IPO price, where “IPO price” means the per share price to the public of any common shares offered by us that in the aggregate results in capital in excess of $10.0 million being raised and the shares of a class of our common stock being listed and traded on a national stock exchange. There are 98,500 shares authorized and 98,500 shares outstanding as of December 31, 2008. |

| · | “Series I Preferred Stock” – convertible into Common Stock Series A on a one-for-one basis. There are 4,693,878 shares authorized and 4,693,878 shares outstanding as of December 31, 2008. |

In October 2008, we filed Certificates of Withdrawal with the Nevada Secretary of State whereby we withdrew the designations of our Series A, Series C and Series D Convertible Preferred Stock, as no shares of these series were then outstanding. Except for Series F, G and I, none of our series of preferred stock have dividend rights. In 2008, we paid $97,233 in dividends to the holders of our Series F and G Convertible Preferred Stock. Except for Series I, none of our series of preferred stock have voting rights. With respect to the rights upon liquidation, dissolution, or winding up, our preferred stock ranks senior to both series of common stock, but junior to any existing or future indebtedness. Among the holders of our outstanding preferred stock, the following preferences upon liquidation, dissolution or winding up are applicable:

| · | first, holders of Series F Convertible Preferred Stock are entitled to receive $5.00 per share before Series I, Series B, Series E, Series G and Series H Convertible Preferred Stock as to the $1,000,000 jackpot bankroll reserve for our Gamblers Bonus Million Dollar Ticket game; |

| · | second, holders of Series I Preferred Stock are entitled to receive $2.45 per share; |

| · | third, holders of Series B Convertible Preferred Stock are entitled to receive $5.00 per share; |

| · | fourth, holders of Series E and G Convertible Preferred Stock are entitled to receive $5.00 per share; and |

| · | fifth, holders of Series H convertible Preferred Stock are entitled to receive $5.00 per share. |

The liquidation preference for each series of preferred stock is equal to the original purchase price of the preferred stock.

On February 12, 2007, we issued notices to holders of our Series A Convertible Preferred Stock and holders of our Series B Convertible Preferred Stock as a result of an agreement with Treasure Island Las Vegas, a wholly-owned subsidiary of MGM Mirage, whereby Treasure Island agreed to maintain the required base jackpot bankroll of $2.9 million for our linked, progressive keno game, Nevada Numbers. Since the cash attributable to the Series A and Series B Convertible Preferred Stock was no longer required to bankroll Nevada Numbers, we provided notices to holders of our Series A Convertible Preferred Stock of our right to convert all of the outstanding shares of Series A Convertible Preferred Stock into shares of Common Stock Series A on a one-for-one basis and to holders of our Series B Convertible Preferred Stock of the opportunity to exchange one-half of their respective shares for either the return of their original investment or shares of Common Stock Series A.

The conversion date for the Series A Convertible Preferred Stock was March 15, 2007. Accordingly all 536,400 shares of Series A Convertible Preferred Stock were converted into 536,400 shares of Common Stock Series A. To holders of Series B Convertible Preferred Stock, we advised said holders of their right to exchange one-half of their respective shares of Series B Convertible Preferred Stock for either the return of their original investment (i.e., $5.00 per share) or five shares of Common Stock Series A for each share of Series B Convertible Preferred Stock. We have also notified holders of our Series B Convertible Preferred Stock that they may convert all of their shares into shares of Common Stock Series A on the same basis. The holders of our Series B Convertible Preferred Stock had until May 13, 2007 to make their decision. At December 31, 2007, holders of 179,890 shares of Series B Convertible Preferred Stock had converted their shares on a one-to-five basis for 899,450 shares of Common Stock Series A. We also redeemed 35,900 shares of Series B Convertible Preferred Stock at $5.00 per share for a total redemption of $179,500 during the year ended December 31, 2007. Late in 2007, pursuant to an agreement with Treasure Island Las Vegas, Treasure Island began maintaining the required base jackpot bankroll of $1 million for our Million Dollar Ticket game. We sent a letter dated January 28, 2008 to holders of our Series B Convertible Preferred Stock informing them that they had 90 days to exchange their shares on a one-to-five basis for Common Stock Series A or receive $5.00 in cash per share for their shares of Series B Convertible Preferred Stock. At December 31, 2008 only 50,000 Series B preferred shares remained outstanding.

During 2008, all shares of Series C and D Convertible Preferred Stock were converted to Common Stock Series A.

During the year ended December 31, 2008, holders of 52,850 shares of Series B Convertible Preferred Stock converted their shares on a one-to-five basis for 264,250 shares of Common Stock Series A. We also redeemed 27,500 shares of Series B Convertible Preferred Stock at $5 per share for a total redemption of $137,500 during the year ended December 31, 2008.

Options

As of December 31, 2008 we had outstanding options to purchase an aggregate of 2,645,900 of our Common Stock Series A at exercise prices ranging from $1.00 to $5.00 per share, with a weighted average exercise price of $3.36 per share.

Warrants

As of December 31, 2008, we had outstanding warrants to purchase an aggregate of 6,010,309 shares of our Common Stock Series A at exercise prices ranging from $1.00 to $5.00 per share with a weighted average exercise price of $2.08 per share.

Unregistered Sales of Equity Securities

During the year ended December 31, 2008, holders of 52,850 shares of Series B Convertible Preferred Stock converted their shares on a one-to-five basis for 264,250 shares of Common Stock Series A. This issuance was deemed to be exempt from registration under the Securities Act in reliance on Section 4(2) of the Securities Act in that the issuance did not involve a public offering. We also redeemed 27,500 shares of Series B Convertible Preferred Stock at $5 per share for a total redemption of $137,500 during the year ended December 31, 2008.

During the year ended December 31, 2008, holders of 35,000 shares of Series C Convertible Preferred Stock converted their shares on a one-to-five basis for 175,000 shares of Common Stock Series A. This issuance was deemed to be exempt from registration under the Securities Act in reliance on Section 4(2) of the Securities Act in that the issuance did not involve a public offering.