SCHEDULE 14A

INFORMATION REQUIRED IN PROXY STATEMENT

SCHEDULE 14A INFORMATION

Proxy Statement Pursuant to Section 14(a) of the Securities

Exchange Act of 1934

(Amendment No. )

Filed by the registrant þ

Filed by a party other than the registrant o

Check the appropriate box:

o Preliminary proxy statement.

o Confidential, for use of the Commission only (as permitted by Rule 14a-6(e)(2).

þ Definitive proxy statement.

o Definitive additional materials.

o Soliciting material pursuant to Rule 14a-12.

FRONTIER OIL CORPORATION |

(Name of Registrant as Specified in Its Charter) |

(Name of Person(s) Filing Proxy Statement, if other Than the Registrant) |

Payment of filing fee (Check the appropriate box):

þ No fee required.

o Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11.

(1) Title of each class of securities to which transaction applies:

(2) Aggregate number of securities to which transaction applies:

(3) Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined.)

(4) Proposed maximum aggregate value of transaction:

(5) Total fee paid:

o Fee paid previously with preliminary materials.

o Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the form or schedule and the date of its filing.

(1) Amount Previously Paid:

(2) Form, Schedule or Registration Statement No.:

(3) Filing Party:

(4) Date Filed:

March 22, 2010

To Our Shareholders:

On behalf of the Board of Directors, I cordially invite all shareholders to attend the Annual Meeting of Frontier Oil Corporation to be held on Wednesday, April 28, 2010 at 9:00 a.m. (Houston time) in the offices of Andrews Kurth LLP located at 600 Travis, Suite 4200, Houston, Texas. Proxy materials, which include a Notice of the Meeting, Proxy Statement and proxy card, are enclosed with this letter. The Company’s 2009 Annual Report to shareholders, which is not a part of the proxy materials, is also enclosed and provides additional information regarding the financial results of the Company in 2009.

Even if you plan to attend the meeting, you are requested to sign, date and return the proxy card in the enclosed envelope. If you attend the meeting after having returned the enclosed proxy card, you may revoke your proxy, if you wish, and vote in person. If you would like to attend and your shares are not registered in your own name, please ask the broker, trust, bank or other nominee that holds the shares to provide you with evidence of your share ownership.

Thank you for your support.

| Sincerely, | |

| |

| James R. Gibbs | |

| Chairman of the Board |

10000 Memorial Drive, Suite 600 Houston, Texas 77024-3411 (713) 688-9600 fax (713) 688-0616

10000 Memorial Drive, Suite 600

Houston, Texas 77024-3411

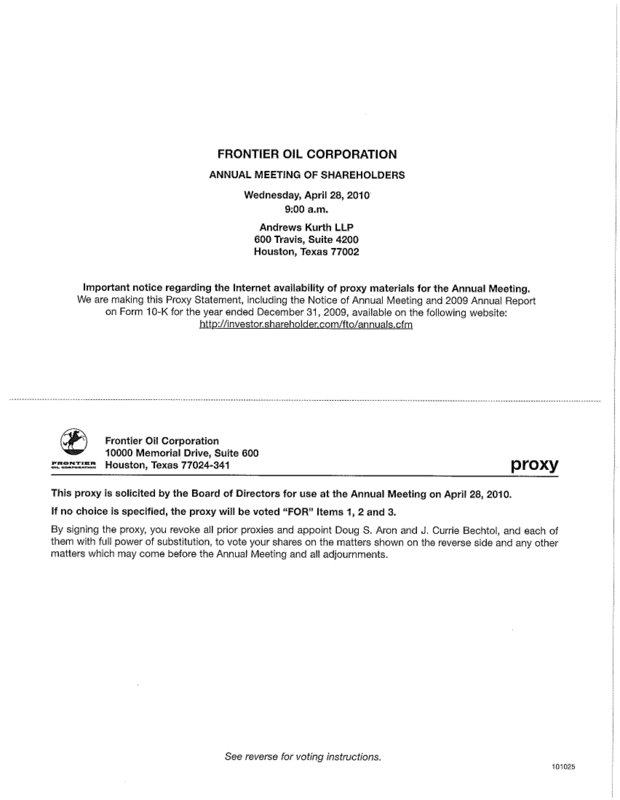

NOTICE OF ANNUAL MEETING OF SHAREHOLDERS

April 28, 2010

To Our Shareholders:

The 2010 Annual Meeting of Shareholders of Frontier Oil Corporation (the “Company”) will be held in the offices of Andrews Kurth LLP located at 600 Travis, Suite 4200, Houston, Texas at 9:00 a.m. (Houston time) on Wednesday, April 28, 2010, for the following purposes:

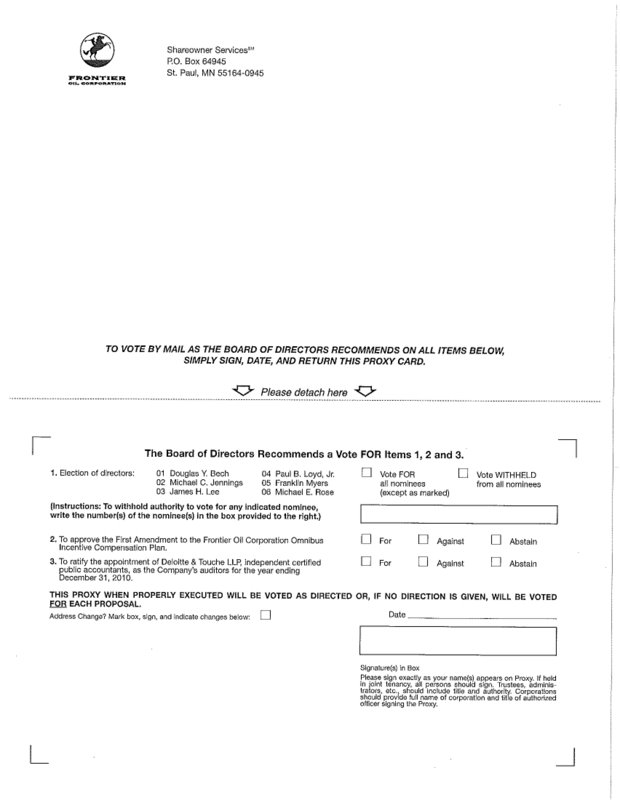

| 1. | To elect six directors (constituting the entire Board of Directors) to serve until the next Annual Meeting of Shareholders or until their respective successors have been elected or appointed. |

| 2. | To approve First Amendment to the Frontier Oil Corporation Omnibus Incentive Compensation Plan. |

| 3. | To ratify the appointment of Deloitte & Touche LLP, independent certified public accountants, as the Company’s auditors for the year ending December 31, 2010. |

| 4. | To act upon any and all matters incident to the foregoing and to transact such other business as may properly be brought before the meeting or any postponement or adjournment thereof. |

The Board of Directors recommends that you vote FOR each of the first three proposals set forth above. The accompanying Proxy Statement contains information relating to each of such proposals. The holders of record of the Company’s common stock at the close of business on March 8, 2010 are entitled to notice of and to vote at the meeting with respect to all proposals. We urge you to sign and date the enclosed proxy and return it promptly by mail in the enclosed envelope, whether or not you plan to attend the meeting in person. No postage is required if mailed in the United States. If you do attend the meeting in person, you may withdraw your proxy and vote personally on all matters brought before the meeting.

| By Order of the Board of Directors, | |

| |

| J. Currie Bechtol | |

| Vice President-General Counsel & Secretary |

Houston, Texas

March 22, 2010

Electronic Availability of Proxy Materials:

We are making this Proxy Statement, including the Notice of Annual Meeting and 2009 Annual Report on Form 10-K for the year ended December 31, 2009, available on the following website: http://investor.shareholder.com/fto/annuals.cfm.

FRONTIER OIL CORPORATION

10000 Memorial Drive, Suite 600

Houston, Texas 77024-3411

PROXY STATEMENT

SOLICITATION AND REVOCABILITY OF PROXIES

This Proxy Statement is furnished by the Board of Directors of Frontier Oil Corporation (the “Company”) in connection with the solicitation of proxies for use at the Annual Meeting of Shareholders to be held April 28, 2010, and at any postponement or adjournment thereof. The shares represented by the form of proxy enclosed herewith will be voted in accordance with the specifications noted thereon. If no choice is specified, said shares will be voted in favor of the proposals set forth in the notice attached hereto. The form of proxy also confers discretionary authority with respect to amendments or variations to matters identified in the notice of meeting and any other matters, which may properly come before the meeting. This Proxy Statement and the enclo sed proxy form are first being sent to shareholders on or about March 22, 2010.

A shareholder who has given a proxy may revoke it as to any motion on which a vote has not already been taken by signing a proxy bearing a later date or by a written notice delivered to the Secretary of the Company in care of Wells Fargo Bank, N.A., Shareowners Services, 161 N. Concord Exchange, S. St. Paul, MN 55075 (“Wells Fargo”) or at the executive offices of the Company, 10000 Memorial Drive, Suite 600, Houston, Texas 77024-3411, at any time up to the meeting or any postponement or adjournment thereof, or by delivering it to the Chairman of the meeting on such date.

The cost of solicitation of these proxies will be paid by the Company, including reimbursement paid to brokerage firms and other custodians, nominees and fiduciaries for reasonable costs incurred in forwarding the proxy material to and soliciting of proxies from the shareholders of record. In addition to such solicitation and the solicitation made hereby, certain directors, officers and employees of the Company may solicit proxies by fax, telephone and personal interview.

VOTING SECURITIES

All shareholders of record as of the close of business on March 8, 2010 are entitled to notice of and to vote at the meeting. On March 8, 2010, the Company had 105,229,685 shares of common stock, without par value (“Common Stock”), outstanding, excluding Common Stock held by the Company. The Common Stock is the only class of voting securities of the Company. Shareholders are entitled to one vote, exercisable in person or by proxy, for each share of Common Stock held on the record date.

The presence in person or by proxy of the holders of a majority of the issued and outstanding Common Stock, excluding Common Stock held by the Company, is necessary to constitute a quorum at this meeting. In the absence of a quorum at the meeting, the meeting may be postponed or adjourned from time to time without notice, other than announcement at the meeting, until a quorum shall be formed. Abstentions and broker non-votes represented by submitted proxies will be included in the calculation of the number of the shares present at the meeting for the purposes of determining a quorum. “Broker non-votes” means shares held of record by a broker that are not voted on a matter because the broker has not received voting instructions from the beneficial owner of the shares and either lacks or declines to exercise the authority to vote the shares in its discretion.

Proposal 1 – Directors are elected by a plurality of the votes cast at the meeting and the six nominees who receive the most votes will be elected. Please note that the New York Stock Exchange (“NYSE”) rules that guide how brokers vote your stock have changed. Your brokerage firm or other nominee may no longer vote your shares with respect to Proposal One without specific instructions from you as to how to vote with respect to the election of each of the six nominees for director, because the election of directors is no longer considered a “routine” matter under the NYSE rules. Abstentions and broker non-votes represented by submitted proxies will not be taken into account in determining the outcome of the election of directors.

Proposal 2 – To be approved, this proposal regarding approval of an amendment to our equity incentive plan must receive an affirmative majority of the total votes cast with respect to this proposal at the meeting. Proposal 2 is considered a “non-routine” matter under the NYSE rules and, therefore, brokerage firms and nominees that are members of the NYSE do not have the authority under those rules to vote their customers’ unvoted shares on Proposal 2 if their customers have not furnished voting instructions within a specified period of time prior to the meeting. Accordingly, broker non-votes represented by submitted proxies will not be taken into account in determining the outcome of this proposal; abstentions will be counted as a vote against this proposal.

Proposal 3 – To be approved, this proposal regarding ratification of the appointment of our accountants must receive an affirmative majority of the total votes cast with respect to this proposal at the meeting. Proposal 3 is considered a “routine” matter under the NYSE rules and, therefore, brokerage firms and nominees that are members of the NYSE have the authority under those rules to vote their customers’ unvoted shares on Proposal 3 if their customers have not furnished voting instructions within a specified period of time prior to the meeting. Accordingly, broker non-votes represented by submitted proxies will be taken into account in determining the outcome of this proposal; abstentions will be counted as a vote against this proposal.

ANNUAL REPORT

The Company’s 2009 Annual Report on Form 10-K to shareholders, including consolidated financial statements, accompanies this Proxy Statement. Such annual report does not form any part of the proxy solicitation materials.

PRINCIPAL SHAREHOLDERS

The following table sets forth, as of March 8, 2010, the beneficial ownership of the Company’s Common Stock, with respect to each person known by the Company to be the beneficial owner of more than five percent of the Company’s outstanding voting securities, excluding Common Stock held by the Company:

Name and Address of Beneficial Owner | Amount and Nature of Beneficial Ownership | Percentage of Shares of Common Stock (1) |

FMR LLC 82 Devonshire Street Boston, MA 02109 | 14,852,387(2) | 14.1% |

Blackrock, Inc. 40 East 52nd Street New York, NY 10022 | 5,767,071(3) | 5.5% |

Allianz Global Investors Management Partners LLC(4) Nicholas-Applegate Capital Management LLC Oppenheimer Capital LLC NFJ Investment Group LLC | 5,559,600(5) | 5.3% |

| (1) | Represents percentage of 105,229,685 outstanding shares of the Company as of March 8, 2010. |

| (2) | FMR LLC has filed with the U.S. Securities and Exchange Commission (the “Commission”) a Schedule 13G/A on January 11, 2010. Based on the filing, Fidelity Management & Research Company (“Fidelity”), 82 Devonshire Street, Boston, MA 02109, a wholly owned subsidiary of FMR LLC and an investment adviser registered under Section 203 of the Investment Advisers Act of 1940, is the beneficial owner of 12,410,040 shares of the outstanding Common Stock as a result of acting as investment adviser to various investment companies (such investment companies collectively, the “Funds”) registered under Section 8 of the Investment Company Act of 1940 (“ICA”). Edward C. Johnson 3d, as Chairman of FMR LLC, and FMR LLC, through its control of Fidelity, and the Funds each has sole power to dispose of 12,410,040 shares owned by the Funds. Neither FMR LLC nor Edward C. Johnson 3d has the sole power to vote or direct the voting of the shares owned directly by the Funds, which power resides with the Funds’ boards of trustees. Fidelity carries out the voting of the shares under written guidelines established by the Funds’ boards of trustees. Members of the family of Edward C. Johnson 3d are the predominant owners, directly or through trusts, of Series B shares of FMR LLC, representing 49% of the voting power of FMR LLC. The Johnson family group and all other Series B shareholders have entered into a shareholders’ voting agreement under which all Series B shares will be voted in accordance with the majority vote of the Series B shares. Accordingly, through their ownership of voting common shares and the execution of the shareholders’ voting agreement, members of the Johnson family may be deemed under ICA to form a controlling group with respect to FMR LLC. Strategic Advisers, Inc., 82 Devonshire Street, Boston, MA 02109, a wholly-owned subsidiary of FMR LLC and an investment adviser registered under Section 203 of the Investment Advisers Act of 1940, provides investment advisory services to individuals. As such, FMR LLC’s beneficial ownership includes 4,669 shares of the outstanding Common Stock beneficially owned through Strategic Advisers, Inc. Pyramis Global Advisors, LLC (“PGALLC”), 900 Salem Street, Smithfield, RI 02917, an indirect wholly-owned subsidiary of FMR LLC and an investment advisor registered under Section 203 of the Investment Advisors Act of 1940 is the beneficial owner of 250,000 shares of the Common Stock as a result of its serving as investment adviser to institutional accounts, non-U.S. mutual funds or investment companies registered under Section 8 of ICA owning such shares. Edward C. Johnson 3d and FMR LLC, through its control of PGALLC, each has sole dispositive and sole voting power with respect to 250,000 shares of Common Stock owned by the institutional accounts or funds advised by PGALLC. FIL Limited (“FIL”), Pembroke Hall, 42 Crow Lane, Hamilton, Bermuda, is the beneficial owner of 2,187,678 shares of the outstanding Common Stock. Partnerships controlled predominantly by members of the family of Edward C. Johnson 3d, or trusts for their benefit, own shares of FIL voting stock with the right to cast approximately 47% of the total votes which may be cast by all holders of FIL voting stock. FMR LLC and FIL are of the view that they are not acting as a “group” for purposes of Section 13(d) under the Exchange Act of 1934 (the “Exchange Act”) and that they are not otherwise required to attribute to each other the “beneficial ownership” of securities “beneficially owned” by the other corporation within the meaning of Rule 13d-3 promulgated under the Exch ange Act. Therefore, they are of the view that the shares held by the other corporation need not be aggregated for purposes of Section 13(d). |

| (3) | Blackrock, Inc. has filed with the Commission a Schedule 13G/A on January 29, 2010. Based on the filing, Blackrock, Inc. has sole dispositive and voting power over all of the shares of Common Stock reported. |

| (4) | The address for Allianz Global Investors Management Partners LLC (“AGIMP”) is 680 Newport Center Drive, Suite 250, Newport Beach, CA 92660. The address for Nicholas-Applegate Capital Management LLC (“NACM”) is 600 West Broadway, Suite 2900, San Diego, CA 92101. The address for Oppenheimer Capital LLC (“OpCap”) is 1345 Avenue of the Americas, New York, NY 10105. The address for NFJ Investment Group LLC (“NFJ”) is 2100 Ross Avenue, Suite 700, Dallas, TX 75201. |

| (5) | AGIMP, NACM, OpCap and NFJ filed with the Commission a Schedule 13G on February 12, 2010. Based on the filing, NFJ has the sole power to vote and dispose of 5,334,600 shares of Common Stock, and OpCap has the sole power to vote and dispose of 225,000 shares of Common Stock. Each of NACM, OpCap and NFJ is an investment adviser registered under Section 203 of the Investment Advisers Act of 1940 and are wholly-owned subsidiaries of AGIMP. The shares of Common Stock are held by investment advisory clients or discretionary accounts of which NACM, OpCap or NFJ is the investment adviser. As a result, each may be deemed to be the beneficial owner of the securities owned by such clients or accounts within the meaning of Rule 13d-3 of the Securities Act of 1933, as amended. |

COMMON STOCK OWNED BY DIRECTORS AND EXECUTIVE OFFICERS

The following table sets forth, as of March 8, 2010, the amount of Common Stock beneficially owned by: (i) each director of the Company, (ii) each named executive officer listed on the Summary Compensation Table on page 30 and (iii) all directors and executive officers as a group:

| Name | Amount and Nature of Beneficial Ownership | Percentage of Shares of Common Stock (1) | |

| James R. Gibbs | 584,009 | (2) | * |

| Douglas Y. Bech | 145,789 | (3) | * |

| G. Clyde Buck | 183,702 | (4) | * |

| T. Michael Dossey | 51,995 | (5) | * |

| James H. Lee | 80,209 | (6) | * |

| Paul B. Loyd, Jr. | 35,510 | (7) | * |

| Franklin Myers | – | (8) | – |

| Michael E. Rose | 20,478 | (9) | * |

| Michael C. Jennings | 273,989 | (10) | * |

| Doug S. Aron | 95,421 | (11) | * |

| J. Currie Bechtol | 148,754 | (12) | * |

| Paul Eisman | 14,688 | (13) | * |

| Jon D. Galvin | 256,528 | (14) | * |

| Nancy J. Zupan | 194,242 | (15) | * |

| Directors and executive officers as a group (16 persons) | 2,214,178 | 2.1% | |

____________________

* Less than 1%

| (1) | Represents percentage of outstanding shares plus shares issuable upon exercise of all stock options owned by the individual listed that are currently exercisable or that will become exercisable within 60 days of the date for which beneficial ownership is provided in the table, assuming stock options owned by all other shareholders are not exercised. As of March 8, 2010, 105,229,685 shares of Common Stock were outstanding and an additional 434,793 option shares were exercisable within 60 days. |

| (2) | Includes 147,976 shares which Mr. Gibbs has the right to acquire under the Company’s Omnibus Incentive Compensation Plan within 60 days of the date for which beneficial ownership is provided in the table. Mr. Gibbs has sole voting power and sole dispositive power with respect to 463,033 shares. |

| (3) | Mr. Bech has sole voting and sole dispositive power with respect to 145,789 shares. |

| (4) | Mr. Buck has sole voting and sole dispositive power with respect to 183,702 shares. |

| (5) | Mr. Dossey has sole voting and sole dispositive power with respect to 51,995 shares. |

| (6) | Mr. Lee has sole voting and sole dispositive power with respect to 80,209 shares. |

| (7) | Mr. Loyd has sole voting and sole dispositive power with respect to 35,510 shares. |

| (8) | Mr. Myers was appointed to the Board in November, 2009. |

| (9) | Mr. Rose has sole voting power and sole dispositive power with respect to 20,478 shares. |

(10) | Includes 33,294 shares which Mr. Jennings has the right to acquire under the Company’s Omnibus Incentive Compensation Plan within 60 days of the date for which beneficial ownership is provided in the table. Mr. Jennings has sole voting and sole dispositive power with respect to 103,050 shares and sole voting power for an additional 137,645 shares of restricted stock. |

(11) | Includes 9,866 shares which Mr. Aron has the right to acquire under the Company’s Omnibus Incentive Compensation Plan within 60 days of the date for which beneficial ownership is provided in the table. Mr. Aron has sole voting and sole dispositive power with respect to 30,182 shares and sole voting power for an additional 55,373 shares of restricted stock. |

(12) | Includes 19,730 shares which Mr. Bechtol has the right to acquire under the Company’s Omnibus Incentive Compensation Plan within 60 days of the date for which beneficial ownership is provided in the table. Mr. Bechtol has sole voting and sole dispositive power with respect to 70,838 shares and sole voting power for an additional 58,186 shares of restricted stock. |

(13) | Mr. Eisman has sole voting and sole dispositive power with respect to 14,688 shares. Mr. Eisman retired effective November 1, 2009. |

| (14) | Includes 14,798 shares which Mr. Galvin has the right to acquire under the Company’s Omnibus Incentive Compensation Plan within 60 days of the date for which beneficial ownership is provided in the table. Mr. Galvin has sole voting and sole dispositive power with respect to 190,093 shares and sole voting power for an additional 51,637 shares of restricted stock. Mr. Galvin has pledged 179,195 shares as security for a line of credit. |

(15) | Includes 14,798 shares which Ms. Zupan has the right to acquire under the Company’s Omnibus Incentive Compensation Plan within 60 days of the date for which beneficial ownership is provided in the table. Ms. Zupan has sole voting and sole dispositive power with respect to 112,037 shares and sole voting power for an additional 67,407 shares of restricted stock. |

PROPOSAL 1:

ELECTION OF DIRECTORS

The Board of Directors recommends that you vote FOR each of the nominees named below. A Board of Directors is to be elected, with each director to hold office until the next Annual Meeting of Shareholders or until his successor shall be elected or appointed. The persons whose names are set forth as proxies in the enclosed form of proxy will vote all shares over which they have control “FOR” the election of the Board of Directors’ nominees, unless otherwise directed. Although the Board of Directors of the Company does not contemplate that any of the nominees will be unable to serve, if such a situation should arise prior to the meeting, the appointed proxies will use their discretionary authority pursuant to the proxy and vote in accordance with their best judgment.

Nominees

All of the persons listed below are members of the present Board of Directors and have consented in writing to be named in this Proxy Statement and to serve as a director, if elected.

Mr. Douglas Y. Bech (64) has been since August 1997 Chairman and Chief Executive Officer of Raintree Resorts International (“Raintree”), a company engaged in resort development, vacation ownership sales and resort management. In November 2003, Teton Club LLC, a private resident club in Jackson, Wyoming owned by an affiliate of Raintree and a non-affiliated third party filed for protection under Chapter 11 and Teton Club LLC was successfully reorganized in August 2004. From 1994 to 1997, Mr. Bech was a partner in the law firm of Akin, Gump, Strauss, Hauer & Feld, L.L.P. of Houston, Texas. From 1993 to 1994, Mr. Bech was a partner in Gardere & Wynne, L.L.P. of Houston, Texas. From 1970 until 1993, Mr. Bech was associated with and a senior partner of Andrews Kurth LLP of Houston, Tex as. Mr. Bech has been since 2000 and is a member of the Board of Directors of j2 Global Communications Inc. (NASDAQ: JCOM), an internet document communications and messaging company. He was appointed a director of the Company in 1993.

Mr. Michael C. Jennings (44) joined the Company in June 2005 as Executive Vice President and Chief Financial Officer and became President and Chief Executive Officer on January 1, 2009. Prior to joining the Company, Mr. Jennings was employed by Cooper Cameron Corporation beginning in May 2000 as Vice President & Treasurer, with responsibilities including managing merger and acquisition activities, the tax and corporate finance areas, Cooper Cameron’s liquidity and capitalization and overseeing bank and rating agency relationships. From November 1998 until May 2000, he was Vice President Finance & Corporate Development of Unimin Corporation, a producer of industrial minerals. Prior to November 1998, Mr. Jennings was employed by Cooper Cameron Corporation as Director, Acquisitions and Cor porate Finance from July 1995 until November 1998. He was appointed a director of the Company in 2008.

Mr. James H. Lee (61) is Managing General Partner and principal owner of Lee, Hite & Wisda Ltd., an oil and gas consulting and exploration firm, which he founded in 1984. From 1981 to 1984, Mr. Lee was a Principal with the oil and gas advisory firm of Schroder Energy Associates. He had prior experience in investment management, corporate finance and mergers and acquisitions at Cooper Industries Inc., a manufacturer of consumer and industrial products, and at White, Weld & Co. Incorporated, an investment bank and brokerage firm. Mr. Lee has been since 1991 and is a member of the Board of Directors of Forest Oil Corporation (NYSE:FST), an oil and gas exploration and production company. He was appointed a director of the Company in 2000.

Mr. Paul B. Loyd, Jr. (63) has been an independent private investor since 2002. His investment activities have included being a manager or co-manager of several Texas limited liability companies, all of which are private companies engaged in oil and gas exploration and production or ranching, and Chairman, Vice President & Secretary of Penloyd LLC, an Oklahoma limited liability company in the business of manufacturing and selling commercial fixtures, that in February 2010 filed for protection under Chapter 7 of the Federal Bankruptcy laws. Prior to 2002, he served as Chairman of the Board and Chief Executive Officer of R&B Falcon Corporation, the world’s largest offshore drilling company, from December 1997 until its merger in January 2001 with Transocean Sedco Forex. From April 1991 un til December 1997, Mr. Loyd was Chairman of the Board and Chief Executive Officer of Reading & Bates Corporation, and prior to that time he had served as Assistant to the president of Atwood Oceanics International, President of Griffin-Alexander Company, and Chief Executive Officer of Chiles-Alexander International, Inc., all of which are companies in the offshore drilling industry. He has served as consultant to the Government of Saudi Arabia, and was a founder and principal of Loyd & Associates, Inc., an investment company focusing on the energy industry. Mr. Loyd is a member of the Board of Directors of Carrizo Oil & Gas, Inc. (NASDAQ: CRZO), a public company engaged in oil and gas exploration and production, and he serves on the Board of Trustees of Southern Methodist University and the Executive Board of the Cox School of Business. He was appointed a director of the Company in 1994.

Mr. Franklin Myers (57) served as Senior Advisor to Cameron International Corporation, a publicly traded provider of flow equipment products, from April 2008 through March 2009, prior to which, from 2003 through March 2008, he served as the Senior Vice President and Chief Financial Officer. From 1995 to 2003, he served at various times as Senior Vice President and President of a division within Cooper Cameron Corporation as well as General Counsel and Secretary. Prior to joining Cooper Cameron Corporation in 1995, Mr. Myers served as Senior Vice President and General Counsel of Baker Hughes Incorporated, and as attorney and partner at the law firm of Fulbright & Jaworski. Mr. Myers serves on the Board of Directors of ION Geophysical Corporation (NYSE: IO), a technology-focused seismic solutions p ublic company, Comfort Systems USA, Inc. (NYSE: FIX), a national heating, ventilation and cooling public company and Seahawk Drilling, Inc. (NASDQ: HAWK), a public offshore drilling company. He was appointed a director of the Company in 2009.

Mr. Michael E. Rose (63) has been involved in private investments since retiring from Anadarko Petroleum Corporation, one of the nation’s largest independent oil and gas companies, in January 2004. Mr. Rose had been with Anadarko for 24 years prior to his retirement, and from August 2000 until January 2004 he served as Executive Vice President Finance & Chief Financial Officer of Anadarko. He also served as Senior Vice President Finance & Chief Financial Officer from January 1993 until August 2000 and prior to that time was Vice President Finance & Chief Financial Officer from January 1987 until January 1993. From May 1981 until January 1987, he was Vice President & Controller of Anadarko. From 1971 until joining Anadarko as their Chief Accountant in 1978, he held a variety of p ositions with Atlantic Richfield Company, an integrated oil company now owned by British Petroleum. He was appointed a director of the Company in 2005.

Other Directors

The following persons are also members of the present Board of Directors but are not standing for re-election.

Mr. James R. Gibbs (65) joined the Company in February 1982, became President and Chief Operating Officer in January 1987, assumed the additional position of Chief Executive Officer in April 1992 and became Chairman of the Board in April 1999. Effective January 1, 2009, Mr. Gibbs resigned his positions as President and Chief Executive Officer and is the Chairman of the Board. Mr. Gibbs is a member of the Board of Directors of Smith International, Inc. (NYSE: SII), a public oilfield service company; an advisory director of Frost National Bank, Houston; and serves on the Board of Trustees of Southern Methodist University. Mr. Gibbs was elected a director of the Company in 1985. Mr. Gibbs’ leadership of the Company for many years has provided historical insight about our operations and industry.

Mr. G. Clyde Buck (72) has been a financial consultant located in Houston, Texas since January 2008. From 1998 through 2007, Mr. Buck was a Senior Vice President and Managing Director of the investment banking firm Sanders Morris Harris, Inc. (including predecessor firms). From 1983 to 1998, he was a Managing Director of Dain Rauscher Corporation, also an investment banking firm. Mr. Buck is also an advisor to and former member of the Board of Directors of Smith International, Inc. (NYSE: SII), a public oilfield service company. He was appointed a director of the Company in 1999. Mr. Buck has provided experience with capital markets and financial expertise.

Mr. T. Michael Dossey (67) has been a management consultant located in Houston, Texas since April 2000. From April 2000 through September 2002, Mr. Dossey was a management consultant affiliated with the Adizes Institute of Santa Barbara, California. Prior to April 2000, Mr. Dossey spent 35 years with Shell Oil Company and its affiliates. Prior to his retirement from Shell, his last assignment with Shell was General Manager-Mergers and Acquisitions for Equilon Enterprises LLC, an alliance between the domestic downstream operations of Shell and Texaco. He also had been Vice President and Business Manager for Shell Deer Park Refining Company, which was a joint venture operation with Pemex. Previously, he spent several years in Saudi Arabia where he was General Operations Manager fo r Saudi Petrochemical Company, a joint venture between Shell and the Saudi Arabian government. Earlier in his career, Mr. Dossey’s positions included various business and operational positions in Shell’s refining and petrochemical operations domestically and in Europe. He was appointed a director of the Company in 2000. Mr. Dossey’s experience as an officer of a major oil and gas company enabled him to provide relevant insight into our industry.

Structure of the Board of Directors and Its Committees

Director Independence

The Board has determined that no relationship, other than as a director, exists between the Company and its non-employee directors, that each of the nominees standing for election at the 2010 Annual Shareholders Meeting, other than Michael C. Jennings, our President and Chief Executive Officer, is independent within the meaning of New York Stock Exchange director independence standards, including those attached to this proxy as Annex A (“NYSE standards”), and that each of the nominees otherwise has no material relationship with the Company, either directly or as a partner, shareholder or affiliate of an organization that has a relationship with the Company. The Board based its independence determinations upon a review of all the relevant facts and circumstances, including the responses of the directors to ques tions regarding their employment history, compensation, affiliations and family and other relationships the Board, (iv) recommending for Board approval the members and chairman for each standing committee, (v) overseeing the annual evaluations of the performance of the Board and its standing committees and the effectiveness of the Board, the standing committees and management, (vi) considering questions of independence and possible conflicts of interest of members of the Board and executive officers and (vii) reviewing the Company’s Code of Business Conduct and Ethics and the Code of Ethics for the Chief Executive Officer, Chief Financial Officer and Chief Accounting Officer.

Board Leadership

Our Board is headed by its Chairman, Mr. Gibbs, who has been Chairman since 1999 and served as CEO through December 31, 2008. On January 1, 2009 when Mr. Jennings became our President and CEO, the positions of CEO and Chairman were separated as part of our succession planning process. Mr. Gibbs retained the Chairman position for purposes of continuity during this process. When his service on the Board ends following the 2010 Annual Meeting of Shareholders, Mr. Gibbs will no longer be the Chairman. We have a lead independent director, Mr. Bech, who presides at executive sessions of the independent directors and functions as a liaison between management and the independent directors. This Board leadership structure has worked well for the Company in our succession plan ning and the Board will determine the future leadership structure following the election of the Company’s directors.

The primary risks facing the Company are overseen by the Board and committees thereof and consist of financial risks, operating risks, liquidity risks and environmental/health/safety risks. The Board generally oversees management of the Company’s operating risks and strategic direction. The Board regularly reviews the Company’s liquidity and operations and associated risks. Our financial risks are monitored by the Audit Committee at regular meetings. This includes reviewing with management the significant financial and accounting risks and how they are reported in the financial statements. The Audit Committee monitors the work performed by internal audits in such areas as hedging our inventory positions and risk policies that are followed in purchasing cr ude oil and other feed stocks. The compensation structure established by the Compensation Committee includes a compensation structure that not only rewards performance and is competitive with the Company’s peer group, but also provides incentives for reducing environmental, health and safety incidents. The Safety & Environmental Committee regularly reviews reports and information from management about our compliance with environmental laws, worker safety, process safety and health matters and makes reports to the Board to assist in its oversight function.

Committees

The Board of Directors has five standing committees comprised of directors of the Company: audit, compensation, executive, safety & environmental and nominating & corporate governance.

Audit Committee: The Audit Committee is comprised of three non-employee directors, currently Messrs. Rose, Buck and Lee. Each of the members of the Audit Committee is independent as defined by New York Stock Exchange listing requirements and as required by Rule 10A-3 under the Securities and Exchange Act, and the Board of Directors of the Company has determined that Mr. Rose is an “audit committee financial expert” within the meaning of Item 407 of Regulation S-K under the federal securities laws. The Audit Committee’s responsibilities include: (i) retaining, compensating and overseeing the independent public accountants performing the audit services on behalf of the Company, (ii) reviewing the Company’s annual a nd quarterly financial statements with management and with the independent public accountants, (iii) reviewing the report submitted in connection with the performance of the audit services by the independent public accountants on behalf of the Company, (iv) approving professional services provided by the independent public accountants, (v) reviewing the independence of the independent public accountants, (vi) considering the range of audit and non-audit fees and (vii) reviewing with management the integrity of the Company’s financial reporting process, both internal and external, and the adequacy of the Company’s internal accounting controls. The Audit Committee met seven times during 2009.

Compensation Committee: The Compensation Committee is comprised of three non-employee directors, currently Messrs. Bech, Loyd and Rose. The Compensation Committee’s responsibilities include: (i) establishing the Company’s philosophy for executive compensation to ensure it rewards performance, promotes the interests of the Company’s shareholders and is competitive with the Company’s peer group, (ii) reviewing the performance of corporate officers against goals and objectives approved by the Compensation Committee and approving their salaries, salary increases, and bonuses, (iii) approving compensation and benefit plans, including incentive compensation and equity based compensation plans and awards for officers and key employees, (iv) monitoring the benefits under all of the Company employee savings, thrift and retirement plans and (v) adopting a plan for the orderly succession of the officers of the Company. Each of the members of the Compensation Committee is independent as defined by the New York Stock Exchange listing requirements. The Compensation Committee met five times during 2009.

Executive Committee: The Executive Committee is comprised of five members of the Board of Directors, currently consisting of the Chairman of the Board, the Chief Executive Officer and three non-employee directors, currently Messrs. Gibbs, Jennings, Bech, Dossey and Loyd. The Executive Committee’s responsibilities include: (i) being able to act on and exercise all of the powers and authority of the Board, subject to the limitations imposed by Wyoming law and the Company’s bylaws, in connection with those matters which the Board may delegate to the Committee that require expeditious consideration and resolution at times between regular meetings or when the Board cannot be convened in a timely manner for a special meeting and (ii) approvi ng capital expenditures not to exceed $20 million and disposition of Company assets not to exceed $10 million. The Executive Committee met six times during 2009.

Safety & Environmental Committee: The Safety & Environmental Committee is comprised of three non-employee directors, currently Messrs. Buck, Dossey and Loyd. The Safety & Environmental Committee’s functions include: (i) reviewing reports and information provided by Company management or consultants regarding material regulatory compliance matters arising out of worker safety, process safety and health issues, (ii) reviewing reports and information provided by Company management or consultants regarding material regulatory compliance matters or legislative developments related to environmental protection concerns and (iii) reporting material issues or compliance concerns included in the reports by management to the Board. 60;The Safety & Environmental Committee met four times during 2009.

Nominating & Corporate Governance Committee: The Nominating & Corporate Governance Committee is comprised of three non-employee directors, currently Messrs. Lee, Bech and Dossey. The responsibilities of the committee include: (i) reviewing possible candidates for the Board of Directors and recommending nomination of appropriate candidates to the Board, including those that contribute to the Board’s diversity, (ii) developing and periodically reviewing the Company’s corporate governance guidelines, (iii) evaluating the structure, operation, size and membership of each standing committee of the Board, (iv) recommending for Board approval the members and chairman for each standing committee, (v) overseeing the annual evaluations o f the performance of the Board and its standing committees and the effectiveness of the Board, the standing committees and management, (vi) considering questions of independence and possible conflicts of interest of members of the Board and executive officers and (vii) reviewing the Company’s Code of Business Conduct and Ethics and the Code of Ethics for the Chief Executive Officer, Chief Financial Officer and Chief Accounting Officer. Each of the members of the Nominating & Corporate Governance Committee is independent as defined by the New York Stock Exchange listing requirements. The Nominating & Corporate Governance Committee met four times during 2009.

Meeting Attendance

The Board of Directors met five times in 2009, and each incumbent director of the Company attended 100 percent of the meetings of the Board of Directors held in 2009 while he was a director and committees of the Board while he served on such committee. The non-employee directors of the Board met five times in 2009 without management present. Beginning in 2007, the directors elected Mr. Bech to serve as presiding director for meetings when the non-employee directors meet without management present.

The Company does not maintain a formal policy regarding the Board’s attendance at annual shareholder meetings. None of the directors attended the 2009 annual meeting of shareholders.

Director Qualifications and Nominations

The Board has concluded that, in light of our business and structure, each of our directors standing for re-election possesses relevant experience, qualifications, attributes and skills and should continue to serve on our Board. The primary qualifications of these directors are further discussed below. Mr. Bech’s previous experience as a securities and corporate finance attorney and current experience as the chief executive officer of a company provides him with insight into corporate finance and governance, including matters regarding compensation and retention of management and key employees. As our CEO, Mr. Jennings is most familiar with our day-to-day operations, and he provides a significant resource for the Board and facilitates communications between management and the Board. Mr. Lee has extensive experience as a consultant and investor in the oil and gas industry and provides significant insights into industry issues. Mr. Loyd’s experience as chief executive officer of several energy companies provides the board with executive level expertise in corporate finance, the capital markets and governance. As the most recently elected member to the Board with experience in senior finance and legal positions at publicly traded energy companies, Mr. Myers provides fresh perspectives to the Board regarding our operations, management and finances. Mr. Rose has significant financial and investment experience with oil and gas companies, and also qualifies as an audit committee financial expert.

The Nominating & Corporate Governance Committee has established procedures for identifying and evaluating nominees. First, the Committee considers the Board’s needs. For instance, the Committee may determine that, due to vacancies or current developments, the election of a director with a particular specialty (e.g., in a specific industry or other diversity qualification) would benefit the Board. The Committee then solicits recommendations from the Chief Executive Officer and other Board members and considers recommendations, if any, made by shareholders, advisors and third-party search firms. The Committee then evaluates these recommendations and identifies prospective nominees to interview. Results from the interview process are considered by the Committee, and the C ommittee then recommends nominees to the full Board, which, upon approval by the Board, recommends the nominees for election by the shareholders. In connection with the 2010 election of directors, we have not paid any fee to a third party to identify, evaluate or assist in identifying or evaluating such nominees.

We seek a diverse group of candidates for nomination as directors for shareholders to consider and vote upon at the annual meeting. Qualifications for consideration as a Board nominee may vary according to the particular areas of expertise being sought to complement the existing Board composition. As reflected in the charter of our Nominating & Corporate Governance Committee, diversity is considered by the committee and the Board of Directors, with diversity consisting of a variety of factors such as background, skills, experience, expertise, gender, race and culture. Minimum qualifications for directors include: (i) business and/or professional knowledge and experience applicable to the Company, its business and the goals and perspe ctives of its shareholders; (ii) being well-regarded in the community, with a long-term, good reputation for the highest ethical standards; (iii) having good common sense and judgment; (iv) having a positive record of accomplishment in present and prior positions; (v) having an excellent reputation for preparation, attendance, participation, interest and initiative on other boards on which he or she may serve; and (vi) having the time, energy, interest and willingness to become involved in the Company and its future.

The Nominating & Corporate Governance Committee will consider nominees recommended by shareholders in the same manner as all other candidates. Pursuant to our bylaws, nominations for candidates for election to the Board of Directors may be made by any shareholder entitled to vote at a meeting of shareholders called for the election of directors. Nominations made by a shareholder must be made by giving notice in writing to the Secretary of the Company before the later to occur of (i) 60 days prior to the date of the meeting of shareholders called for the election of directors or (ii) ten days after the Board first publishes the date of such meeting. The notice shall include all information concerning each nominee as would be required to be included in a proxy statement soliciting proxies for the election of such nominee under the Exchange Act and such other information required by our bylaws. The notice shall also include a signed consent of each nominee to hold office until the next Annual Meeting of Shareholders or until his successor shall be elected or appointed.

Director Compensation

The Company uses a combination of cash and stock-based incentive compensation to attract and retain qualified candidates to serve on its Board of Directors. In setting non-employee director compensation, the Company considers the significant amount of time that directors spend fulfilling their duties to the Company, as well as the skill level required of members of the Company’s Board. The non-employee directors have stock ownership guidelines similar to the executive officers. Within three years after joining the Board, each non-employee director is expected to own shares of the Company’s common stock with an aggregate value of at least five times the annual cash retainer.

The following table provides compensation information for the one-year period ending December 31, 2009 for each of the Company’s non-employee directors:

Name | Fees Earned or Paid in Cash ($)(1) | Stock Awards ($)(2) | Change in Pension Value and Nonqualified Deferred Compensation Earnings ($)(4) | All Other Compensation ($)(5) | Total ($) |

| Mr. Bech | $93,500 | $125,093 | $100,455 | $0 | $319,048 |

| Mr. Buck | $72,500 | $125,093 | $0 | $0 | $197,593 |

| Mr. Dossey | $87,000 | $125,093 | $0 | $684 | $212,777 |

| Mr. Lee | $84,000 | $125,093 | $0 | $0 | $209,093 |

| Mr. Loyd | $78,500 | $125,093 | $0 | $0 | $203,593 |

| Mr. Rose | $89,000 | $125,093 | $0 | $680 | $214,773 |

| Mr. Myers (3) | $7,750 | $0 | $0 | $0 | $7,750 |

| (1) | During 2009, the directors each received an annual cash retainer of $50,000, plus a cash payment of $1,500 per meeting attended. The Chair of the Nominating & Corporate Governance Committee (Mr. Lee) and the Chair of the Safety & Environmental Committee (Mr. Dossey) each received a stipend of $10,000. The Chair of the Audit Committee (Mr. Rose) and the Chair of the Compensation Committee (Mr. Bech) each received a stipend of $15,000. |

(2) | The grant date fair value is computed in accordance with Financial Accounting Standards Codification Topic 718, Compensation, Stock Compensation (FASB ASC 718). As part of the 2009 compensation package, each director received a restricted stock unit award equivalent to 8,760 shares of common stock. These restricted stock units vested in aggregate on December 31, 2009. Mr. Loyd exercised 15,000 options on February 6, 2009 at a $4.6625 grant price. There are no outstanding stock options as of December 31, 2009. Please see Note 10 to Notes to Consolidate Financial Statements included in the Company’s 2009 Annual Report filed on Form 10K for the valuation assumptions used in accordance with ASC 718. |

| (3) | Mr. Franklin Myers was elected to the Board of Directors on November 18, 2009. |

| (4) | The Company does not provide a defined benefit pension plan for its directors. Mr. Bech participates in the Company’s Deferred Compensation Plan. The earnings on his deferred compensation balances exceeded 120% of the applicable long-term federal rate (4.30%) and therefore are reflected as compensation. As with all participants in the Company’s Deferred Compensation Plan, there is no subsidy provided by the Company nor is there any guarantee of investment earnings on Mr. Bech’s deferred compensation balances. |

| (5) | Tax gross-up for aircraft use deemed taxable by the IRS but considered business-related by the Company. |

The Company’s directors were compensated in 2009 pursuant only to the standard compensation arrangements described above. No director received compensation from the Company under any special compensation arrangement.

PROPOSAL 2:

APPROVAL OF FIRST AMENDMENT TO THE FRONTIER OIL CORPORATION OMNIBUS INCENTIVE COMPENSATION PLAN

The Board of Directors unanimously adopted the Frontier Oil Corporation Omnibus Incentive Compensation Plan (“OICP”) in February 2006, and the shareholders approved the OICP in April 2006.

Proposed Amendments

On February 24, 2010, the Board of Directors adopted the First Amendment to the OICP (“First Amendment”). The First Amendment revises the OICP as follows:

| • | increases by 7,100,000 the maximum number of shares of Common Stock that may be awarded under the OICP; |

| • | decreases that ratio by which stock-denominated awards, other than options and Stock Appreciation Rights (“SARs”) will be credited or debited against the number of shares available under the OICP to 1.6; |

| • | expands the list of permissible business criteria pursuant to which Performance Awards may be granted under the OICP to include the following: cash flow from operating activities, cash flow before financing activities, targeted cash balances, and compliance with debt covenants; |

| • | eliminates the right to receive Dividend Equivalent Rights (“DERs”) with respect to stock options and SARs; and |

| • | certain other technical amendments to the provisions of the OICP. |

No additional substantive amendments to the OICP were adopted by the Board of Directors pursuant to Amendment No 1. Certain of the amendments effected by the First Amendment require approval of our shareholders pursuant to Section 162(m) of the Code. These amendments will not become effective unless shareholder approval of the First Amendment is obtained at the meeting.

If the shareholders approve Proposal 2, the First Amendment will be effective as of the date of the adoption by the shareholders. Attached hereto as Annex B is the First Amendment to the OICP, as approved by the Board of Directors and as submitted to our shareholders for their approval.

Reasons for the Proposed Amendment

As of March 15, 2010, we estimate that only 217,709 shares of common stock of the Company remained available for issuance under the OICP from the initial stock pool. The First Amendment continues the purpose of the OICP to enable the Company and its affiliates to provide those individuals upon whom the responsibilities of the successful management of the Company and its affiliates rest with stock-based incentive opportunities that align their interests with those of the stockholders of the Company, thereby enhancing the growth and success of the Company. A further purpose of the First Amendment is to enable the OICP to provide a means for the Company to attract and retain those individuals in the service of the Company and its affiliates.

Summary of the OICP

Below is a summary of the terms of the OICP, as amended by the First Amendment, which is qualified in its entirety by reference to the full text of the OICP, which may be obtained, at no cost, from the Company.

Number of Shares Subject to the OICP

The maximum number of shares of the Company’s Common Stock that may be issued under the OICP with respect to awards was initially 6,000,000 shares, subject to certain adjustments as provided by the OICP. A subsequent 2-for-1 stock split increased the initial share pool to 11,683,077 shares. The First Amendment would authorize an additional 7,100,000 shares for delivery with respect to awards, and also be subject to certain adjustments as provided by the OICP. Except as provided below with respect to options and SARs, stock-denominated awards from the additional 7,100,000 share pool (the “new share pool”) will be credited or debited on their grant, payment in shares, forfeiture or termination without payment in shares, as the case may be, to the new share pool on the basis of 1.6 sha res for each share subject to such share-denominated awards. In addition, any shares used to satisfy a dollar-denominated performance award will reduce the new share pool on the basis of 1.6 shares for each share so paid. (The factor applicable to shares from the initial share pool (as adjusted for the stock split) will remain 1.7.) The number of shares subject to an option and SAR award will be debited or credited to the initial and new share pools on a 1.0 for 1.0 basis. Substitute awards that are granted to new participants as replacement awards for a prior employer’s equity awards forfeited or converted in connection with an acquisition or purchase made by the Company (“Substitute Awards”) will not be debited or credited against a share pool. In addition, upon certain corporate events, such as a stock split, recapitalization, reorganization, spinoff and other similar events, the number of shares available under the OICP will be adjusted to app ropriately reflect that event. Thus, depending on the type of award granted, whether it is forfeited or paid in shares, and whether or not a corporate event has occurred, it is possible that a greater or lesser number than 18,783,077 shares (which includes the 7,100,000 shares to be provided by the First Amendment) may actually be delivered with respect to awards under the OICP.

No participant may receive stock-denominated awards with respect to more than 1,500,000 shares in any calendar year. The maximum amount of cash-denominated awards that may be granted to any participant during any calendar year may not exceed $5,000,000.

The shares of Common Stock to be delivered under the OICP may be treasury shares or authorized but unissued shares. To the extent that an award (other than a Substitute Award) terminates, expires, lapses or is settled in cash, the shares subject to the award may be used again with respect to new grants under the OICP (subject to the applicable adjustment factor). However, shares tendered or withheld to satisfy an exercise price or tax withholding obligations may not be used again for grants under the OICP.

Administration

In general, the OICP is administered by the Compensation Committee of the Board of Directors of the Company (the “Committee”). The Committee has the full authority, subject to the terms of the OICP, to establish rules and regulations for the proper administration of the OICP, to select the employees, consultants and directors to whom awards are granted, and to determine the amount and type of awards made and the terms of the awards.

Eligibility

All employees, consultants and directors of the Company and its affiliates are eligible to participate in the OICP. The selection of which eligible individuals will receive awards is within the sole discretion of the Committee.

Term of OICP

The OICP became effective on April 24, 2006, and no further awards may be granted under the OICP after February 22, 2016. The Board or the Committee may terminate the OICP earlier at any time with respect to any shares of Common Stock for which awards have not theretofore been granted.

Stock Options and SARs

The term of each option and SAR will be as specified by the Committee at the date of grant (but not more than ten years), and the exercise price for each option and SAR may not be less than the fair market value of the shares on the date that the option or SAR is granted (unless it is a Substitute Award). The Committee also determines the method by which the option price may be paid upon exercise. No more than 2,000,000 shares may be delivered with respect to incentive stock options.

Restricted Stock

Pursuant to a Restricted Stock award, shares of the Company’s Common Stock are issued in the name of the employee, consultant or director at the time the award is made, but remain subject to certain vesting and transfer restrictions, which may be linked to performance criteria or other specified criteria, including the passage of time, as determined in the discretion of the Committee.

Performance Awards

The Committee may grant dollar-denominated Performance Awards that may be paid in cash, Company Common Stock or any combination thereof, as determined by the Committee in its discretion. The Committee will establish the performance criteria that must be achieved and the performance period over which the performance or vesting goals will be measured. Following the end of the performance period, the Committee will determine the amount payable to the holder of the Performance Award based on the achievement of the vesting goals. Payment of vested awards may be made in cash and/or in shares of Common Stock, as determined by the Committee.

Stock Units

Stock Units (sometimes called phantom shares) are awards of rights with respect to a specified number of notional shares of Common Stock. Such awards are subject to the fulfillment of such vesting criteria as the Committee may specify. Payment of Stock Units may be made in cash, shares of Common Stock or any combination thereof, as determined by the Committee in its discretion. Any payment to be made in cash will be based on the fair market value of a share of Common Stock on the payment date.

Bonus Shares

Bonus Shares are unrestricted shares of Common Stock and may be paid as part of, or in lieu of all or any portion of, any cash bonus, deferred compensation or other compensation of an eligible individual.

Dividend Equivalent Rights (DERs)

Dividend equivalent rights (“DERs”) are rights, generally granted in tandem with another award under the OICP, to receive an amount of cash equal to the value of any cash dividends made on shares of Common Stock during the period the tandem award is outstanding. Payment of DERs may be made subject to the same vesting terms as the tandem award (if any) or may have different vesting and payment terms, in the discretion of the Committee. If the First Amendment is approved, DERs may be granted only in tandem with Stock Units.

Other Stock-Based Awards

An Other Stock-Based Award is an award the value of which is based in whole or in part on a share of Common Stock. The Committee may set such vesting and/or performance criteria as it chooses with respect to such award. Upon vesting, the award may be paid in shares of Common Stock, cash or any combination thereof, as decided by the Committee.

Substitute Awards

The Committee may grant to individuals who become employees, consultants or directors of the Company or its subsidiaries in connection with a merger or other corporate transaction awards under the OICP that are intended to replace an equity award such person may have received from his or her prior employer and forfeited as a result of the transaction. In general, a Substitute Award will be similar in terms and type to the award it replaces.

Performance-Based Compensation

With respect to awards that are intended to qualify as “performance-based compensation” under Section 162(m) of the Internal Revenue Code, the Committee establishes performance goals based upon the attainment of such target levels of one or more of the Performance Criteria (as described below) over one or more periods of time, which may be of varying and overlapping durations, as the Committee may select. A performance goal need not be based upon an increase or positive result under a Performance Criteria and could, for example, be based upon limiting economic losses or maintaining the status quo. Which Performance Criteria to be used with respect to any grant, and the weight to be accorded thereto if more than one criteria is used, will be determined by the Committee at the time of grant. 0;Following the completion of each specified performance period, the Committee will certify in writing whether the applicable performance goals have been achieved for such performance period. In determining the amount earned by a participant, the Committee will have the right to reduce or eliminate (but not to increase) the amount payable at a given level of performance to take into account additional factors that the Committee may deem relevant to the assessment of individual or corporate performance for the performance period.

For purposes of the OICP, the term “Performance Criteria” means the following business criteria with respect to the Company, any subsidiary or any division or operating unit: net income per share, net income per share from operations, cash flow, cash flow per share, pre-tax income, return on capital employed, return on equity, return on assets, stock price, shareholder return, net income, operating income, earnings before interest, taxes, depreciation and amortization expenses, cost controls, reductions or savings, safety, refinery reliability, and economic value added. If the First Amendment is approved, cash flow from operating activities, cash flow before financing activities, targeted cash balances, and compliance with debt covenants will be additional business criteria that may be used for Perf ormance Criteria. Such targets may be expressed in terms of the Company, a subsidiary, division or business unit, as determined by the Committee. The performance measures shall be subject to adjustment for changes in accounting standards required by the Financial Accounting Standards Board after the goal is established, and, to the extent provided for in the award agreement and permitted by Section 162(m), shall be subject to adjustment for specified significant extraordinary items or events. In this regard, performance goals based on stock price shall be proportionately adjusted for any changes in the price due to a stock split. Performance measures may be absolute, relative to one or more other companies, or relative to one or more indexes, and may be contingent upon future performance of the Company or any subsidiary, division, or department thereof. A performance goal need not be based upon an increase or positive result under a business criterion an d may be based upon limiting economic losses or maintaining the status quo.

Miscellaneous

The Committee may amend or modify the OICP at any time; provided, however, that shareholder approval will be obtained for any amendment (i) to the extent necessary and desirable to comply with any applicable law, regulation or stock exchange rule, (ii) to increase the number of shares available or (iii) to permit the exercise price of any outstanding option or SAR that is “underwater” to be reduced or for an “underwater” option or SAR to be cancelled and replaced with a new award.

Upon a change of control of the Company (as defined in the OICP), awards automatically become fully vested and payable unless the individual’s award agreement provides to the contrary.

Federal Income Tax Aspects of the OICP

The following is a brief summary of certain of the U.S. federal income tax consequences under the OICP as normally operated and is not intended to be exhaustive.

As a general rule, no federal income tax is imposed on a participant upon the grant of a an award under the OICP, other than Bonus Shares, and the Company is not entitled to a tax deduction by reason of such grant, other than Bonus Shares. When an award is paid or becomes vested, the holder will realize ordinary income in an amount equal to the cash and/or the fair market value of the shares of Common Stock received at that time, and, subject to Section 162(m) of the Internal Revenue Code, the Company will be entitled to a corresponding deduction. Upon the exercise of a non-statutory stock option or SAR, the participant will be treated as receiving compensation taxable as ordinary income in the year of exercise in an amount equal to the excess of the fair market value of the shares of stock at the time of exerc ise over the exercise price paid for such shares, and the Company may claim a deduction for compensation paid at the same time and in the same amount as compensation is recognized by the holder, assuming applicable federal income tax reporting requirements are satisfied. Stock options that are incentive stock options (“ISOs”) under Section 422 of the Internal Revenue Code are subject to special federal income tax treatment. In general, no federal income tax is imposed on exercise of an ISO although the exercise may trigger alternative minimum tax liability to the optionee, and the Company is not entitled to any deduction for federal income tax purposes in connection with the grant or exercise of an ISO. However, if the optionee disposes of the shares acquired upon exercise of an ISO before satisfying certain holding period requirements, the optionee will be treated, in general, as having received, at the time of disposition, compensation taxable as ordinary income , and in such event, the Company may claim a deduction for compensation paid at the same time and in the same amount as the compensation treated as being received by the optionee.

In general, Section 162(m) of the Internal Revenue Code precludes a public corporation from taking a deduction for annual compensation in excess of $1 million paid to its chief executive officer or any of its four other highest-paid officers unless the compensation qualifies under Section 162(m) of the Internal Revenue Code as “performance-based”. The OICP has been designed to provide flexibility with respect to whether awards granted by the Committee will qualify as performance-based compensation under Section 162(m) of the Internal Revenue Code and, therefore, be exempt from the deduction limit.

Upon a change of control of the Company, awards granted to certain individuals may be “excess parachute” payments for purposes of Section 280G of the Internal Revenue Code and, in such event, the individual would be subject to an additional 20% excise tax with respect to the “parachute value” of the awards and the Company would not be entitled to a tax deduction for such parachute amount.

The OICP and awards granted under it are intended to be either exempt from or comply with Section 409A of the Internal Revenue Code, concerning deferred compensation. For those awards intended to be subject to Section 409A, their terms will be construed as necessary to comply with Section 409A. Failure to comply with Section 409A, if applicable, could subject a participant to an additional 20% tax.

Application of Section 16 of the Securities Exchange Act of 1934

Special rules may apply in the case of individuals subject to Section 16 of the Securities Exchange Act. In particular, unless a special election is made by the participant pursuant to Section 83 of the Internal Revenue Code, shares received pursuant to certain awards may be treated as restricted as to transferability and subject to a substantial risk of forfeiture for a period of up to six months after the date of exercise or vesting of the award. In such event, the amount of any ordinary income recognized, and the amount of the Company’s tax deduction, are determined as of the end of such period.

Inapplicability of ERISA

Based upon current law and published interpretations, the Company does not believe that the OICP is subject to any of the provisions of the Employee Retirement Income Security Act of 1974, as amended.

Recommendation of the Company’s Board

The Board of Directors approved the First Amendment to the OICP and believes the First Amendment is in the best interests of the Company and our shareholders. The Board of Directors recommends that the shareholders approve the First Amendment to the OICP and, accordingly, recommends a vote FOR Proposal 2.

Equity Compensation Plan Information

The following table sets forth securities authorized for issuance under the Company’s equity compensation plan as of December 31, 2009:

Plan category | Number of securities to be issued upon exercise of outstanding options, warrants and rights (#)(a) | Weighted-average exercise price of outstanding options, warrants and rights ($)(b) | Number of securities remaining available for future issuance under equity compensation plans (excluding securities reflected in column (a)) (#)(c) |

| Equity compensation plan approved by security holders – OICP | 434,793 | $29.385 | 2,283,313 |

| Equity compensation plans not approved by security holders | --- | --- | --- |

| Total | 434,793 | $29.385 | 2,283,313 |

Equity Compensation Plan Information as of March 15, 2010

The 2010 annual grants in the form of Restricted Stock Awards (RSAs) and Performance Stock Units (PSUs) were made to employees on February 23, 2010. The 2010 annual grants in the form of Restricted Stock Units (RSUs) were made to non-employee directors on January 26, 2010. As a result of these annual grants of RSAs and RSUs in 2010, 217,709 shares remained available to be granted as part of the OICP as of March 15, 2010.

On February 23, 2010, 206,348 PSUs issued in 2007 were converted into stock based upon achievement of certain share price criteria being met over a three-year period that ended December 31, 2009. In addition, on March 9, 2010, the 625,582 PSUs issued in 2009 were converted to RSAs, based on Frontier’s financial performance compared to its peer group as of December 31, 2009. Based on the conversion of these PSUs to stock and the 2010 PSU grants, there were a total of 1,291,776 PSUs outstanding as of March 15, 2010. On December 31, 2009, we reported a total of 842,067 RSAs and RSUs outstanding. As of March 15, 2010, we had a total of 1,677,892 RSAs and RSUs outstanding due to the 2010 annual grants of RSAs to employees, 2010 annual grants of RSUs to non-employee directors (net of forfeitures), conversion of PSUs to RSAs and the vesting of 251,801 RSAs, all of which have occurred since December 31, 2009. As of March 15, 2010, there remain 434,793 options outstanding with a weighted average exercise price of $29.385 and a weighted average remaining contractual life of 1.12 years.

PROPOSAL 3:

The Board of Directors recommends that you vote FOR the ratification of the appointment of Deloitte & Touche LLP as independent auditors for the Company for the year ending December 31, 2010. This firm has served in such capacity since March 2002 and is familiar with the Company’s affairs and procedures.

Deloitte & Touche LLP has advised the Company that its representatives will be present at the 2010 Annual Shareholders Meeting to discuss results for the year ended December 31, 2009 and to make a statement if they desire to do so and to respond to appropriate questions.

REPORT OF THE AUDIT COMMITTEE

The following Report of the Audit Committee does not constitute soliciting material and should not be deemed filed or incorporated by reference into any other Company filing under the Securities Act of 1933, as amended, or the Exchange Act of 1934, as amended, except to the extent the Company specifically incorporates this Report by reference therein.

February 23, 2010

| To the Board of Directors of Frontier Oil Corporation: |

We have reviewed and discussed with management the Company’s audited financial statements as of and for the year ended December 31, 2009.

We have discussed with the independent auditors the matters required to be discussed by Public Company Accounting Oversight Board Auditing Standard AU Section 380 (Communication with Audit Committees) and Rule 2-07 of SEC Regulation S-X.

We have received and reviewed the written disclosures and the letter from the independent auditors required by applicable requirements of the Public Company Accounting Oversight Board regarding the independent accountant’s communications with the audit committee concerning independence, and have discussed with the auditors the auditors’ independence.

Based on the reviews and discussions referred to above, we recommend to the Board of Directors that the financial statements referred to above be included in the Company’s Annual Report on Form 10-K for the year ended December 31, 2009.

Members of the Audit Committee

Michael E. Rose, Chairman

G. Clyde Buck

James H. Lee

Audit Fees

The following table sets forth the fees billed to the Company from its principal independent auditor, Deloitte & Touche LLP, for professional services rendered for the fiscal years ended December 31, 2009 and 2008:

| Fee Category | Fiscal 2009 | Fiscal 2008 | ||||||

Audit Fees | $ | 984,200 | $ | 1,084,698 | ||||

Audit-Related Fees | 61,828 | 68,500 | ||||||

Tax Fees | 305,577 | 228,908 | ||||||

All Other Fees | – | – | ||||||

Total | $ | 1,351,605 | $ | 1,382,106 | ||||

Audit Fees for the fiscal years ended December 31, 2009 and 2008 were for professional services rendered for the audits of the consolidated financial statements of the Company, quarterly reviews of the financial statements included in the Company’s Quarterly Reports on Form 10-Q, attestation of management’s assessment of internal control, as required by Sarbanes-Oxley Act, Section 404, consents, comfort letters and other services related to SEC matters.

Audit-Related Fees for the fiscal years ended December 31, 2009 and 2008 were for assurance and related services associated with employee benefit plan audits.

Tax Fees for the fiscal years ended December 31, 2009 and 2008 were for services related to tax compliance and tax consultation.

All Other Fees for the fiscal years ended December 31, 2009 and 2008 were zero.

Pre-Approval Policy

All of the services performed by the independent auditor in 2009 were pre-approved in accordance with the pre-approval policy and procedures adopted by the Audit Committee. This policy describes the permitted audit, audit-related, tax, and other services (collectively, the “Disclosure Categories”) that the independent auditor may perform. The policy requires that prior to the beginning of each fiscal year, a description of the services (the “Service List”) expected to be performed by the independent auditor in each of the Disclosure Categories in the following fiscal year be presented to the Audit Committee for approval.

Services provided by the independent auditor during 2009 that were included in the Service List were pre-approved following the policies and procedures of the Audit Committee.

Any requests for audit, audit-related, tax, and other services not contemplated on the Service List must be submitted to the Audit Committee for specific pre-approval and cannot commence until such approval has been granted. Normally, pre-approval is provided at regularly scheduled meetings, but the Chairman of the Audit Committee has authority to grant pre-approval as necessary. The Chairman must update the Audit Committee at the next regularly scheduled meeting of any services that were granted specific pre-approval.

In addition, although not required by the rules and regulations of the SEC, the Audit Committee generally requests a range of fees associated with each proposed service on the Service List and any services that were not originally included on the Service List. Providing a range of fees for a service incorporates appropriate oversight and control of the independent auditor relationship, while permitting the Company to receive immediate assistance from the independent auditor when time is of the essence.

On a quarterly basis, the Audit Committee reviews the status of services and fees incurred year-to-date against the original Service List and the forecast of remaining services and fees for the fiscal year.

OTHER BUSINESS