SCHEDULE 14A

(Rule 14a-101)

INFORMATION REQUIRED IN PROXY STATEMENT

SCHEDULE 14A INFORMATION

Proxy Statement Pursuant to Section 14(a) of the Securities Exchange Act of 1934

Filed by the registrant ![]()

Filed by a party other than the registrant

Check the appropriate box:

![]() Preliminary Proxy Statement

Preliminary Proxy Statement

![]() Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2))

Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2))

![]() Definitive Proxy Statement

Definitive Proxy Statement

![]() Definitive Additional Materials

Definitive Additional Materials

Soliciting Material Under Rule 14a-12

–––––––––––––––––––––––––––––––––––––––

THE PEP BOYS—MANNY, MOE & JACK

(Name of Registrant as Specified in Its Charter)

–––––––––––––––––––––––––––––––––––––––

BARINGTON COMPANIES EQUITY PARTNERS, L.P.

(Name of Person(s) Filing Proxy Statement if Other Than the Registrant)

_____________________________________________________________________________

Payment of Filing Fee (Check the appropriate box):

No fee required.

![]() Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11.

Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11.

| (1) Title of each class of securities to which transaction applies: |

| (2) Aggregate number of securities to which transaction applies: |

| (3) Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): |

| (4) Proposed maximum aggregate value of transaction: |

| (5) Total fee paid: |

![]() Fee paid previously with preliminary materials.

Fee paid previously with preliminary materials.

![]() Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the form or schedule and the date of its filing.

Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the form or schedule and the date of its filing.

| (1) Amount Previously Paid: |

| (2) Form, Schedule or Registration Statement No.: |

| (3) Filing Party: |

| (4) Date Filed: |

1

CERTAIN INFORMATION CONCERNING PARTICIPANTS

�� No meeting of shareholders of The Pep Boys—Manny, Moe & Jack (the “Company”) is currently pending or scheduled. Neither Barington Companies Equity Partners, L.P. (“Barington”) nor any other person named herein is currently soliciting, or has determined to solicit in the future, any proxies with respect to shares of common stock of the Company. Notwithstanding the foregoing, the attached presentation is being filed with the Securities and Exchange Commission under Rule 14a-12 out of an abundance of caution. Barington does not believe that the filing of such presentation is required under Rule 14a-12 and is making such filing for supplemental informational purposes only.

In the event that Barington were to determine to solicit proxies with respect to shares of the Company in the future, the following persons, which have joined with Barington in filing a Statement on Schedule 13D with respect to the Company’s common stock, are anticipated to be, or may be deemed to be, participants in any such proxy solicitation: Barington Companies Equity Partners, L.P., Barington Companies Investors, LLC, Barington Companies Offshore Fund, Ltd. (BVI), Barington Investments, L.P., Barington Companies Advisors, LLC, Barington Capital Group, L.P., LNA Capital Corp., James Mitarotonda, Parche, LLC, Starboard Value and Opportunity Master Fund Ltd., RCG Carpathia Master Fund, Ltd., Admiral Advisors, LLC, Ramius Capital Group, LLC, C4S & Co., LLC, Peter A. Cohen, Morgan B. Stark, Jeffrey M. Solomon, Thomas W. Strauss, RJG Capital Partners, L.P., RJG Capital Management, LLC, Ronald Gross, D.B. Zwirn Special Opportunities Fund, L.P., D.B. Zwirn Special Opportunities Fund (TE), L.P., D.B. Zwirn Special Opportunities Fund, Ltd., HCM/Z Special Opportunities LLC, D.B. Zwirn & Co., L.P., DBZ GP, LLC, Zwirn Holdings, LLC and Daniel B. Zwirn.

IF BARINGTON ENGAGES IN ANY SOLICITATION WITH RESPECT TO SHARES OF THE COMPANY, IT WILL PREPARE AND DISSEMINATE A PROXY STATEMENT WITH RESPECT TO SUCH SOLICITATION. BARINGTON STRONGLY ADVISES ALL SHAREHOLDERS OF THE COMPANY TO READ ANY SUCH PROXY STATEMENT IF AND WHEN IT BECOMES AVAILABLE BECAUSE IT WILL CONTAIN IMPORTANT INFORMATION, INCLUDING INFORMATION RELATING TO THE PARTICIPANTS IN ANY SUCH PROXY SOLICITATION. ANY SUCH PROXY STATEMENT, IF AND WHEN FILED, AND ANY OTHER RELEVANT DOCUMENTS WILL BE AVAILABLE AT NO CHARGE ON THE SEC'S WEBSITE AT HTTP://WWW.SEC.GOV. IN ADDITION, SHAREHOLDERS MAY ALSO OBTAIN A COPY OF ANY SUCH PROXY STATEMENT, IF AND WHEN FILED, WITHOUT CHARGE, BY CONTACTING BARINGTON BY ORAL OR WRITTEN REQUEST AT: BARINGTON COMPANIES EQUITY PARTNERS, L.P., C/O BARINGTON CAPITAL GROUP, L.P., 888 SEVENTH AVENUE, 17TH FLOOR, NEW YORK, NEW YORK 10019, ATTN: JAMES MITAROTONDA.

CERTAIN INFORMATION REGARDING THE DIRECT OR INDIRECT INTERESTS OF CERTAIN PERSONS ANTICIPATED TO BE, OR WHO MAY BE DEEMED TO BE, PARTICIPANTS IN ANY SUCH SOLICITATION, IF ANY, IS AVAILABLE IN THE SCHEDULE 13D FILED WITH THE SEC BY BARINGTON AND OTHERS ON NOVEMBER 21, 2005, AS THE SAME MAY BE AMENDED FROM TIME TO TIME, COPIES OF WHICH ARE AVAILABLE AT NO CHARGE ON THE SEC’S WEBSITE AT HTTP://WWW.SEC.GOV.

2

Forum of Shareholders of:

The Pep Boys – Manny, Moe & Jack

December 6, 2005

Presentation of Barington Capital Group, L.P.

Disclaimer

This presentation is for general informational purposes only. The views expressed

herein represent the opinions of Barington Capital Group, L.P., whose analysis is

based on publicly available information. No representation or warranty, express or

implied, is made as to the accuracy or completeness of any information contained in

this presentation. Barington Capital Group disclaims any obligation to update the

information contained herein and reserves the right to modify or change its conclusions

at any time in the future.

This presentation does not recommend the purchase or sale of any security nor is it an

offer to sell or a solicitation of an offer to buy any security. Furthermore, this

presentation is not and should not be considered a solicitation of proxies in connection

with any present or future proxy solicitation.

Barington Capital Group represents a group of investors (the “Barington Group”) that

as of the date hereof beneficially owns, in the aggregate, approximately 5.85% of the

outstanding shares of common stock of the Company as disclosed in the Barington

Group’s Schedule 13D filed with the Securities and Exchange Commission on November

21, 2005. Members of the Barington Group reserve the right to acquire additional

shares of common stock or sell or otherwise dispose of any or all of the shares of

common stock of the Company beneficially owned by them, in the open market, in

privately negotiated transactions or otherwise. The Barington Group may also take

any other action with respect to the Company or any of its debt or equity securities in

any manner permitted by law.

2

Agenda

I. Introduction

II. Overview of Pep Boys

III. Need for a Change Now at Pep Boys

IV. Strategies to Create Value at Pep Boys

V. Concluding Items

Endnotes

3

Agenda

I. Introduction

II. Overview of Pep Boys

III. Need for a Change Now at Pep Boys

IV. Strategies to Create Value at Pep Boys

V. Concluding Items

Endnotes

4

We are holding a

shareholder forum to

listen to the opinions

and insights of our

fellow Pep Boys

shareholders

Barington Capital Group, L.P. represents a group

of investors that beneficially owns, in the

aggregate, approximately 5.85% of the

outstanding common stock of Pep Boys

In our Schedule 13D filing, we have disclosed our

desire to engage in discussions with the

independent members of Pep Boys’ Board of

Directors concerning measures to improve

shareholder value

We have received unsolicited telephone calls from

a number of Pep Boys shareholders interested in

talking about the Company

We therefore decided to hold this Forum to listen

to the opinions and insights of our fellow

shareholders

5

Agenda

I.

I. Introduction

II. Overview of Pep Boys

III. Need for a Change Now at Pep Boys

IV. Strategies to Create Value at Pep Boys

V. Concluding Items

Endnotes

6

Review of Pep Boys

Pep Boys is the 3rd

largest publicly-

traded automotive

aftermarket chain

with approximately

$2.2 billion in sales

$1.3 billion enterprise value

Store format unique to market offering:

Retail to DIY market (60% of sales)

Service Center to DIFM market (40% of sales)

Significant real estate portfolio with 593 stores

and 6,000+ attached service bays

55% owned land and building

30% ground leased at attractive terms

National chain, but limited critical mass

History of operational challenges due to:

Larger store size vs. peers

Lower store-level productivity vs. peers

Increased competition

7

Review of Management’s Turnaround Plan

Main objective of

Management’s

turnaround plan is to

build “Pep Boys to

become the

dominant, one-stop

shop retailer for

automotive

maintenance and

accessories” 1

Under the leadership of the current CEO hired in

April 2003, Pep Boys implemented its “Go-

Forward Strategy” in September 2003. 1 Among

other things, this turnaround strategy is focused

on:

Improving retail productivity by introducing new product

categories and re-working larger store footprint

Improving service quality by streamlining offerings,

introducing branded tires and upgrading service managers

Investing in store base by upgrading systems and re-

designing store format

Follow-on organizational restructurings

implemented in 2005 to:

Reorganize field operations into separate Retail and Service

organizations 2

Reallocate management responsibilities “in response to

weak Service Center performance” 3

8

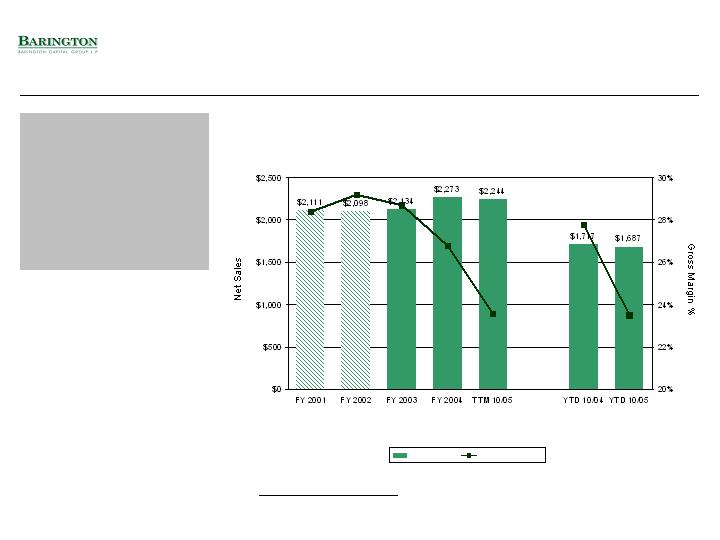

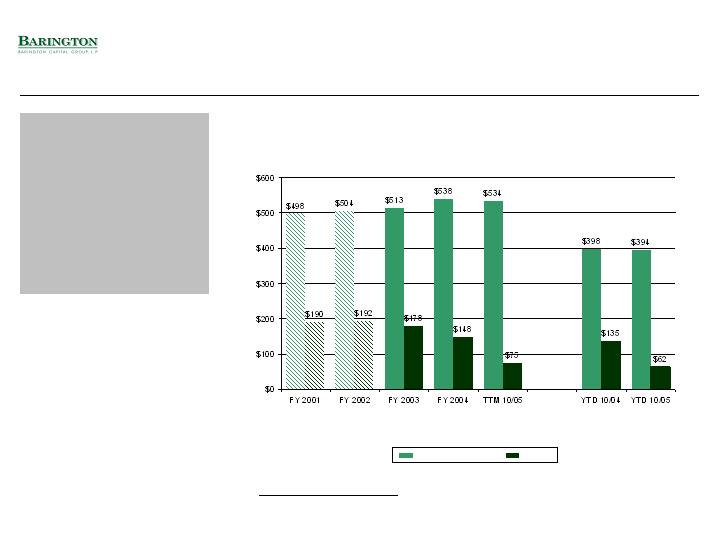

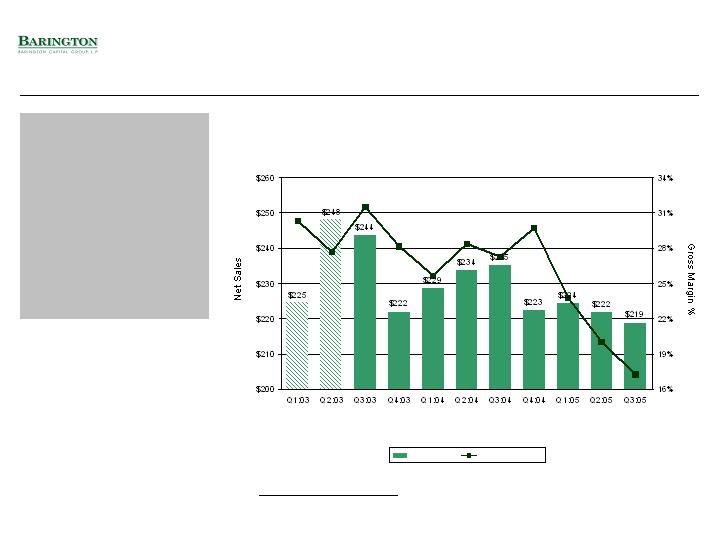

On a consolidated

basis, turnaround

plan has yielded

minimal sales growth

with no

corresponding

increase in profits

Consolidated Financial Performance

Pep Boys Sales and Gross Margin Performance

($ in mm)

See endnotes 4, 5, 6, 7, 8 and 9.

(6.0%)

(0.7%)

1.6%

6.6%

7.2%

(1.6%)

Net Sales

Gross Margin %

Comp Store

Sales

9

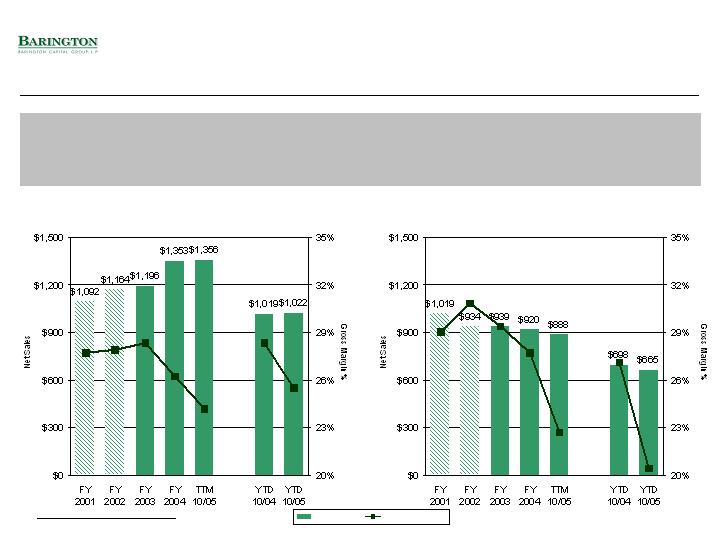

We believe turnaround plan has placed significant stress on both Retail and Service

Center segments. Retail has experienced modest revenue growth to the detriment

of margin. Service Center has lost sales and margin due to ineffective execution. 10

Net Sales

Gross Margin %

Segment Financial Performance

Retail and Service Center

Retail Sales and Gross Margin Performance

($ in mm)

Service Center Sales and Gross Margin Performance

($ in mm)

See endnotes 4, 5, 6, 7, 8, and 9.

10

Turnaround plan has

led to a nearly $40

million increase in

Pep Boys’ operating

expense base,

leading to further

reduction in EBITDA

performance

Pep Boys Operating Expense and EBITDA Performance

($ in mm)

9.0%

9.2%

8.3%

6.5%

7.9%

3.7%

EBITDA

Margin %

3.3%

Operating Expenses

EBITDA

Consolidated Financial Performance

(Cont’d)

See endnotes 4, 5, 6, 7, 8, and 9.

11

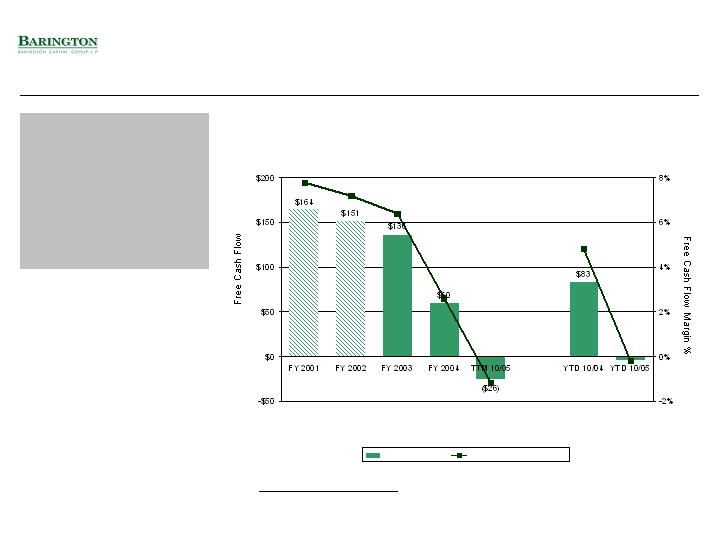

Store investment

initiatives have

eroded strong

historical base of free

cash flow and yielded

little return to

shareholders to date

Pep Boys Free Cash Flow and Margin Performance

($ in mm)

See endnotes 4, 5, 6, 7, 8 and 9.

Free Cash Flow = EBITDA – Capital Expenditures.

ROIC = EBIT (tax-effected at 40%) / Total Capitalization and Other Liabilities.

4.4%

5.0%

5.1%

3.5%

3.8%

1.1%

ROIC

(0.2%)

Free Cash Flow

Free Cash Flow Margin %

Consolidated Financial Performance

(Cont’d)

($3)

12

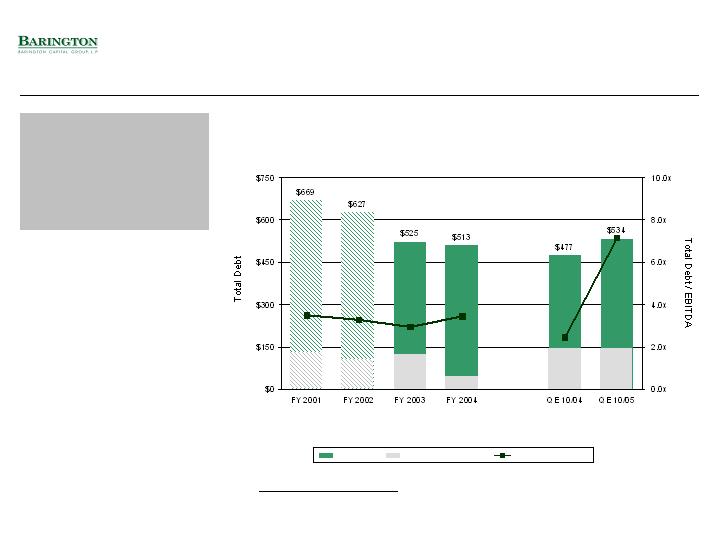

Credit quality has

deteriorated due to

weakening

fundamentals and

near-term maturities

Pep Boys Total Debt and Capitalization Statistics

($ in mm)

See endnotes 4, 5, 6, 7, 8 and 9.

Total Debt / EBITDA statistics for QE periods based on TTM EBITDA.

Total Cap = Total Debt + Total Equity.

52.0%

50.9%

48.0%

44.0%

41.5%

Total Debt /

Total Cap

46.2%

Consolidated Capitalization Statistics

Total Debt

Total Debt / EBITDA

Total Short Term Debt

$125

$102

$117

$41

$147

$144

13

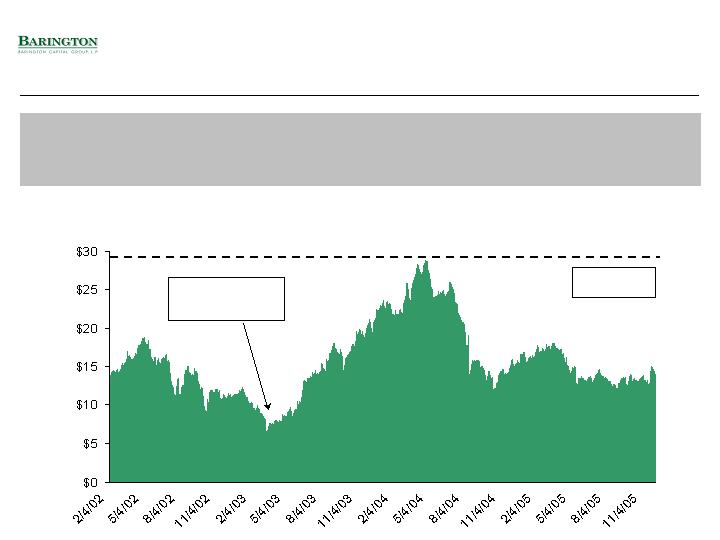

In our opinion, the approximately 50% decrease in stock price from recent high was

primarily due to management’s poor execution of turnaround plan. We are

convinced that the Company’s asset value is providing main support in market.

Stock Price Performance

FY 2001 to Current

Pep Boys Stock Price Performance

($ per share)

4/29/03: Pep Boys

announces hiring of

new CEO

4/22/04: High

of $29.26

14

Agenda

I.

I. Introduction

II. Overview of Pep Boys

III. Need for a Change Now at Pep Boys

IV. Strategies to Create Value at Pep Boys

V. Concluding Items

Endnotes

15

As shareholders, we

believe that change is

necessary now to

enhance value at Pep

Boys

Need For Change at Pep Boys

We lack confidence in turnaround plan

Ineffective execution by management

Poor financial results

Drop-off in Service Center performance

Steep decline in recent quarters has been alarming to us

Liquidity position

Expiration of CEO employment agreement on

April 28, 2006

Renewal / non-extension decision required by February 28,

2006

16

We believe that

ineffective execution

of turnaround plan

has led to a decrease

in shareholder value

Retail strategy has produced a nominal

improvement in sales to the detriment of margins

Flat comps suggest that merchandising strategy is not

“anniversary-ing” well

Seasonal inventory levels appear high (up 6%)

Service Center strategy has weakened segment

Replacing 300+ service managers (and subsequent

performance issues) highly disruptive and costly

Time guarantees to mechanics suggest low bay activity

Branded tire initiative not gaining traction

Store investment initiatives have proven costly

with little payback to shareholders to date

Two organizational restructurings in 2005 alone

We Lack Confidence in Turnaround Plan

17

We are alarmed by

the recent decline in

Service Center

performance and

believe that

management’s

actions have created

undue turmoil in the

segment

Pep Boys Quarterly Service Center Performance

($ in mm)

NA

Net Sales

Gross Margin %

Drop-Off in Service Center Performance

NA

1.7%

NA

NA

(5.3%)

(3.4%)

(0.3%)

(2.1%)

(6.4%)

(7.6%)

Comp Store

Sales

See endnotes 11, 12 and 13.

18

Pep Boys’ poor

operating

performance has

resulted in two recent

downgrades to its

credit outlook

Liquidity Position

S&P and Moody’s have both recently lowered

their outlook at Pep Boys to “Negative,”

citing 14 15:

Deteriorating operating performance and diminished cash

flow protection

Disruptions associated with aggressive store remodeling

program

Struggling service business

Approximately $260 million in debt maturities are

due at Pep Boys through 2007

March 2006: Medium Term Notes = $43 million

July 2006: ReMarketable Notes = $100 million

June 2007: Convertible Notes = $119 million

19

Upcoming expiration

of CEO’s employment

agreement provides

Board with an

opportunity to

consider replacing

CEO at limited

financial cost to

shareholders

Expiration of CEO Employment Agreement

Initial term of CEO’s employment agreement expires on

April 28, 2006 16

Signing bonus = $500,000

Annual compensation = $900,000 base salary + performance bonus

$8.0 million in stock options (906,000 stock options priced at $8.83

per share)

Glass Lewis & Co. gave Pep Boys an “F” grade in the

area of pay-for-performance earlier this year 17

Noted that the Company paid its CEO more than the median CEO

compensation paid by its peers (while the Company performed

worse than its peers)

Pep Boys must give notice at least two months prior to

employment agreement’s expiration date (by February

28, 2006) or agreement automatically extends 16

If notice of non-extension is not given employment agreement

automatically renews for successive one year periods

If employment agreement is not extended, Pep Boys would be

obligated to pay only CEO’s base salary through termination date

20

Agenda

I.

I. Introduction

II. Overview of Pep Boys

III. Need for a Change Now at Pep Boys

IV. Strategies to Create Value at Pep Boys

V. Concluding Items

Endnotes

21

We believe that

efforts must be made

at once to maximize

value for each of Pep

Boys’ core assets

Value Opportunities at Pep Boys

We believe that Pep Boys has three core assets:

Retail

Service Center

Real Estate

It appears that management’s strategy is focused

on “justifying” Pep Boys’ asset base

Barington believes that Pep Boys should be

focused on “rationalizing” its asset base,

reducing costs and re-evaluating its retail strategy

22

We believe that a

strategy grounded in

rationalizing Pep

Boys’ asset base,

reducing costs and

re-evaluating Retail

operations will best

maximize

shareholder value

Strategies to Improve Value

Hire a new CEO and appoint an independent

Chairman

Rationalize asset base

Explore strategic alternatives for Service Center

Evaluate Real Estate portfolio

Pursue cost reductions

Reduce operating costs

Reduce capital expenditures

Re-evaluate Retail strategy

23

We believe that a

new CEO and an

independent

Chairman are a

necessary part of any

strategy to improve

value at Pep Boys

Hire New CEO and Appoint Independent

Chairman

CEO has had 2½ years to generate sustainable

value from turnaround plan

To date, we believe that the turnaround plan has

led to a deterioration in Pep Boys’ core assets

Retail strategy has yielded minimal revenue growth, but

lower profits

Service Center strategy has weakened segment

Store investment initiatives have generated little return on

invested capital

We believe that the Board of Directors should

begin the search now for a new CEO

24

We believe that the

Pep Boys Board of

Directors should

consider a range of

alternatives to

maximize the value of

Service Center

Explore Strategic Alternatives for Service

Center

Despite poor recent performance, we believe that

Service Center has a number of positive

investment merits including:

Annual revenue base of $900 million

Sizable PP&E investment

High traffic locations

Positive long-term industry fundamentals

In our opinion, there are a number of alternatives

that could enhance value at Service Center

including:

Sale of segment to new owner

Outsource / franchise segment to new operator

We believe that most if not all of resulting cash

proceeds should be used to reduce indebtedness

25

Given recent real

estate appraisal, we

believe that Pep Boys

has the internal data

necessary to evaluate

a value creation

alternative from its

Real Estate assets

Evaluate Real Estate Portfolio

We believe that Pep Boys should conduct a

“highest and best use” analysis of owned stores

Develop “true” store-level P&L with operating expenses

and corporate costs properly allocated

Use recent real estate appraisal to assess store market value

relative to expected future operating results

Potential to unlock value in ground-leased stores

given favorable lease terms

Other value considerations include:

Utilizing $45 million NOL to reduce tax liability

Exploring field organization cost savings that might come

from exiting certain regions

26

We believe that

opportunities exist to

reduce operating

expenses and scale

back store investment

initiatives

Pursue Cost Reductions

Turnaround plan has led to a nearly $40 million

increase in operating expense base

We believe that the increase is attributable mostly to

turnaround plan initiatives

We believe cost cuts are available in corporate overhead,

marketing, field staffing and inventory management

Store investment plan has led to a doubling of

capital expenditures with little return to

stockholders to date

Based on management guidance, Pep Boys is likely to

spend approximately $55 million refurbishing 200 stores by

the end of FY 2005 18

We believe that management’s intention is to spend an

incremental $110 million through 2008 refurbishing

balance of store base 18

We believe that the payback time on capex is too long and

return on invested capital targets should be re-evaluated

27

If Pep Boys sells

Service Center and

selected Real Estate

assets, the remaining

$1.4 billion Retail

business still requires

improved execution

Re-evaluate Retail Strategy

In our view, retail excellence requires that Pep Boys:

Continually look to sublet or redeploy retail space to higher

margin use, as we believe that Pep Boys is competitively

challenged with too much retail footage per store

Manage a focused, retail business at best-in-class levels

To achieve rationalization of retail space, we believe

that Pep Boys high traffic locations with automotive

core could prove valuable to certain tenant types

To achieve best-in-class retail, we believe that Pep

Boys needs:

Highly experienced retail leader with merchandising expertise

and creativity

Cost excellence

Labor productivity focus

Improved assortment management

28

Agenda

I.

I. Introduction

II. Overview of Pep Boys

III. Need for a Change Now at Pep Boys

IV. Strategies to Create Value at Pep Boys

V. Concluding Items

Endnotes

29

We welcome the

opinions and insights

of our fellow Pep

Boys shareholders

Conclusion

Barington Group plans to continue to monitor the

performance of the Company closely

Barington Group welcomes the opinions and

insights of our fellow Pep Boys shareholders,

including with respect to alternatives to maximize

shareholder value

30

Agenda

I.

I. Introduction

II. Overview of Pep Boys

III. Need for a Change Now at Pep Boys

IV. Strategies to Create Value at Pep Boys

V. Concluding Items

Endnotes

31

Endnotes

(1) Pep Boys Press Release, dated September 23, 2003.

(2) Pep Boys Press Release, dated January 7, 2005.

(3) Pep Boys Press Release, dated October 5, 2005.

(4) For purposes of this analysis, we have assumed that pretax charges and one-time items

included in Pep Boys’ merchandising segment are allocated to retail segment and those

included in Pep Boys’ service segment are allocated to service center segment.

(5) FY 2001 excludes pretax charges of $5.2 million related to the Profit Enhancement Plan of

which $4.2 million was attributable to gross margin from retail sales, $0.8 million was

attributable to gross profit from service center sales and $0.2 million was attributable to selling,

general and administrative expenses per Pep Boys Form 10-K for the fiscal year ended

January 29, 2005.

(6) FY 2002 excludes pretax charges of $2.5 million related to the Profit Enhancement Plan of

which $2.0 million was attributable to gross profit from retail sales, $0.5 million was attributable

to gross profit from service center sales and $0.02 million was attributable to selling, general

and administrative expenses per Pep Boys Form 10-K for the fiscal year ended January 29,

2005.

(7) FY 2003 excludes pretax charges of $89.0 million related to corporate restructuring,

impairment charges and other one-time events of which $29.3 million was attributable to gross

profit from retail sales, $3.3 million was attributable to gross profit from service center sales and

$56.4 million was attributable to selling, general and administrative expenses per Pep Boys

Form 10-K for the fiscal year ended January 29, 2005.

(8) FY 2004 excludes one-time items of ($3.7) million of which ($12.7) million was related to a

pretax gain from the sale of a distribution center attributable to gross profit from retail sales per

Pep Boys Form 10-K for the fiscal year ended January 29, 2005 and $9.0 million was related to

a charge for reorganization of field operations attributable to selling, general and administrative

expenses per Pep Boys Press Release, dated January 7, 2005.

32

Endnotes

(9) YTD 10/05 excludes one-time items of ($1.8) million of which $1.9 million was related to a non-

cash charge for warranty reserves attributable to net sales from service center per Pep Boys

Press Release, dated November 10, 2005, ($4.7) million was related to a pretax gain from the

sale of two stores attributable to gross margin from retail sales per Pep Boys Form 10-Q for

the quarter ended July 30, 2005 and $1.0 million was related to self-insured costs for hurricane

damage claims attributable to selling, general and administrative expenses per Pep Boys Press

Release, dated November 10, 2005.

(10) See, e.g. Goldman Sachs Retailing Conference, September 9, 2005.

(11) Segment results may exhibit certain discrepancies from those reported in Pep Boys Forms

10-Q or Press Releases due to discrepancies with quarterly unaudited results and year-end

audited statements.

(12) Q2:03 excludes $3.3 million corporate restructuring charge per Pep Boys Form 10-K for fiscal

year ended January 31, 2004.

(13) Q3:05 excludes $1.9 million non-cash charge for warranty reserves per Pep Boys Press

Release, dated November 10, 2005.

(14) Standard & Poor’s Press Release, dated July 21, 2005.

(15) Moody’s Press Release, dated November 28, 2005.

(16) Employment Agreement between Pep Boys and Lawrence Napier Stevenson, dated April 28,

2003.

(17) Glass Lewis & Co. Proxy Paper, dated May 5, 2005.

(18) Pep Boys Press Release, dated November 10, 2005.

We did not seek or obtain the consent of any author or publication whose materials or quotations are

cited herein.

33

Certain Information Concerning Participants

No meeting of shareholders of The Pep Boys—Manny, Moe & Jack (the “Company”) is currently pending or scheduled. Neither Barington Companies Equity Partners, L.P. (“Barington”) nor any other member of the Barington Group is currently soliciting, or has determined to solicit in the future, any proxies with respect to shares of common stock of the Company.

In the event that Barington were to determine to solicit proxies with respect to shares of the Company in the future, the following persons, which have joined with Barington in filing a Statement on Schedule 13D with respect to the Company’s common stock, are anticipated to be, or may be deemed to be, participants in any such proxy solicitation: Barington Companies Equity Partners, L.P., Barington Companies Investors, LLC, Barington Companies Offshore Fund, Ltd. (BVI), Barington Investments, L.P., Barington Companies Advisors, LLC, Barington Capital Group, L.P., LNA Capital Corp., James Mitarotonda, Parche, LLC, Starboard Value and Opportunity Master Fund Ltd., RCG Carpathia Master Fund, Ltd., Admiral Advisors, LLC, Ramius Capital Group, LLC, C4S & Co., LLC, Peter A. Cohen, Morgan B. Stark, Jeffrey M. Solomon, Thomas W. Strauss, RJG Capital Partners, L.P., RJG Capital Management, LLC, Ronald Gross, D.B. Zwirn Special Opportunities Fund, L.P., D.B. Zwirn Special Opportunities Fund (TE), L.P., D.B. Zwirn Special Opportunities Fund, Ltd., HCM/Z Special Opportunities LLC, D.B. Zwirn & Co., L.P., DBZ GP, LLC, Zwirn Holdings, LLC and Daniel B. Zwirn.

IF BARINGTON ENGAGES IN ANY SOLICITATION WITH RESPECT TO SHARES OF THE COMPANY, IT WILL PREPARE AND DISSEMINATE A PROXY STATEMENT WITH RESPECT TO SUCH SOLICITATION. BARINGTON STRONGLY ADVISES ALL SHAREHOLDERS OF THE COMPANY TO READ ANY SUCH PROXY STATEMENT IF AND WHEN IT BECOMES AVAILABLE BECAUSE IT WILL CONTAIN IMPORTANT INFORMATION, INCLUDING INFORMATION RELATING TO THE PARTICIPANTS IN ANY SUCH PROXY SOLICITATION. ANY SUCH PROXY STATEMENT, IF AND WHEN FILED, AND ANY OTHER RELEVANT DOCUMENTS WILL BE AVAILABLE AT NO CHARGE ON THE SEC'S WEBSITE AT HTTP://WWW.SEC.GOV. IN ADDITION, SHAREHOLDERS MAY ALSO OBTAIN A COPY OF ANY SUCH PROXY STATEMENT, IF AND WHEN FILED, WITHOUT CHARGE, BY CONTACTING BARINGTON BY ORAL OR WRITTEN REQUEST AT: BARINGTON COMPANIES EQUITY PARTNERS, L.P., C/O BARINGTON CAPITAL GROUP, L.P., 888 SEVENTH AVENUE, 17TH FLOOR, NEW YORK, NEW YORK 10019, ATTN: JAMES MITAROTONDA.

CERTAIN INFORMATION REGARDING THE DIRECT OR INDIRECT INTERESTS OF CERTAIN PERSONS ANTICIPATED TO BE, OR WHO MAY BE DEEMED TO BE, PARTICIPANTS IN ANY SUCH SOLICITATION, IF ANY, IS AVAILABLE IN THE SCHEDULE 13D FILED WITH THE SEC BY BARINGTON AND OTHERS ON NOVEMBER 21, 2005, AS THE SAME MAY BE AMENDED FROM TIME TO TIME, COPIES OF WHICH ARE AVAILABLE AT NO CHARGE ON THE SEC’S WEBSITE AT HTTP://WWW.SEC.GOV.

34