UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-Q

(Mark One)

| þ | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended September 30, 2013

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission File Number 001-33038

ZIOPHARM Oncology, Inc.

(Exact name of registrant as specified in its charter)

| | |

| Delaware | | 84-1475642 |

(State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification No.) |

One First Avenue, Parris Building 34, Navy Yard Plaza

Boston, Massachusetts 02129

(617) 259-1970

(Address, including zip code, and telephone number, including

area code, of registrant’s principal executive offices)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period than the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes: þ No: ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes: þ No: ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| | | | | | |

| Large accelerated filer | | ¨ | | Accelerated filer | | þ |

| | | |

| Non-accelerated filer | | ¨ (Do not check if a smaller reporting company) | | Smaller reporting company | | ¨ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes: ¨ No: þ

The number of shares of the registrant’s common stock, $.001 par value, outstanding as of October 14, 2013, was 83,696,029 shares.

ZIOPHARM Oncology, Inc. (a development stage company)

NOTE REGARDING FORWARD-LOOKING STATEMENTS

This report contains forward-looking statements that are based on our current beliefs and expectations. These forward-looking statements may be accompanied by such words as “anticipate,” “believe,” “estimate,” “expect,” “forecast,” “intend,” “may,” “plan,” “project,” “target,” “will” and other words and terms of similar meaning. Reference is made in particular to forward-looking statements regarding:

| | • | | the anticipated amount, timing and accounting of deferred revenues, milestone and other payments under licensing, collaboration or acquisition agreements, research and development costs and other expenses; |

| | • | | the protection afforded by our patent rights; |

| | • | | our assessment of the potential impact on our future revenues of healthcare reform legislation in the United States; |

| | • | | the timing and impact of measures worldwide designed to reduce healthcare costs; |

| | • | | the impact of the deterioration of the credit and economic conditions in certain countries in Europe; |

| | • | | our ability to finance our operations and business initiatives and obtain funding for such activities; |

| | • | | the sufficiency of our cash, investments and cash flows from operations and our expected uses of cash; |

| | • | | the costs and timing of the development and commercialization of our pipeline products and services; |

| | • | | additional planned regulatory filings for and commercialization of our synthetic biology product candidates and Palifosfamide; and |

| | • | | contract manufacturing activity. |

These forward-looking statements involve risks and uncertainties, including those that are described in the “Risk Factors” section of this report and elsewhere within this report that could cause actual results to differ materially from those reflected in such statements. You should not place undue reliance on these statements. Forward-looking statements speak only as of the date of this report. We do not undertake any obligation to publicly update any forward-looking statements.

NOTE REGARDING COMPANY REFERENCES

Throughout this report, “ZIOPHARM,” the “Company,” “we,” “us” and “our” refer to ZIOPHARM Oncology, Inc.

NOTE REGARDING TRADEMARKS

Our registered trademarks include Zymafos and Zinapar. Our trademarks include Zybulin. All other trademarks, trade names and service marks appearing in this Quarterly Report on Form 10-Q are the property of their respective owners.

2

ZIOPHARM Oncology, Inc. (a development stage company)

Table of Contents

3

Part I—Financial Information

Item 1. Consolidated Financial Statements

ZIOPHARM Oncology, Inc. (a development stage company)

BALANCE SHEETS

(unaudited)

(in thousands, except share and per share data)

| | | | | | | | |

| | | September 30,

2013 | | | December 31,

2012 | |

ASSETS | | | | | | | | |

Current assets: | | | | | | | | |

Cash and cash equivalents | | $ | 23,631 | | | $ | 73,306 | |

Receivables | | | 449 | | | | 58 | |

Prepaid expenses and other current assets | | | 3,195 | | | | 6,912 | |

| | | | | | | | |

Total current assets | | | 27,275 | | | | 80,276 | |

Property and equipment, net | | | 1,336 | | | | 1,994 | |

Deposits | | | 128 | | | | 133 | |

Other non-current assets | | | 739 | | | | 1,001 | |

| | | | | | | | |

Total assets | | $ | 29,478 | | | $ | 83,404 | |

| | | | | | | | |

LIABILITIES AND STOCKHOLDERS’ EQUITY | | | | | | | | |

Current liabilities: | | | | | | | | |

Accounts payable | | $ | 891 | | | $ | 1,509 | |

Accrued expenses | | | 11,573 | | | | 16,516 | |

Deferred revenue—current portion | | | 800 | | | | 800 | |

Deferred rent—current portion | | | 98 | | | | 39 | |

| | | | | | | | |

Total current liabilities | | | 13,362 | | | | 18,864 | |

Deferred revenue | | | 2,133 | | | | 2,733 | |

Deferred rent | | | 349 | | | | 400 | |

Warrant liabilities | | | 9,983 | | | | 12,962 | |

Other long-term liabilities | | | 20 | | | | — | |

| | | | | | | | |

Total liabilities | | | 25,847 | | | | 34,959 | |

| | | | | | | | |

Commitments and contingencies (note 7) | | | | | | | | |

Stockholders’ equity: | | | | | | | | |

Preferred stock, $0.001 par value; 30,000,000 shares authorized and no shares issued and outstanding | | | — | | | | — | |

Common stock, $0.001 par value; 250,000,000 shares authorized; 83,681,579 and 83,236,840 shares issued and outstanding at September 30, 2013 and December 31, 2012, respectively | | | 84 | | | | 83 | |

Additional paid-in capital—common stock | | | 331,817 | | | | 325,177 | |

Additional paid-in capital—warrants issued | | | 3,657 | | | | 6,909 | |

Deficit accumulated during the development stage | | | (331,927 | ) | | | (283,724 | ) |

| | | | | | | | |

Total stockholders’ equity | | | 3,631 | | | | 48,445 | |

| | | | | | | | |

Total liabilities and stockholders’ equity | | $ | 29,478 | | | $ | 83,404 | |

| | | | | | | | |

The accompanying notes are an integral part of the unaudited interim financial statements.

4

ZIOPHARM Oncology, Inc. (a development stage company)

STATEMENTS OF OPERATIONS

(unaudited)

(in thousands, except share and per share data)

| | | | | | | | | | | | | | | | | | | | |

| | | For the Three Months Ended

September 30, | | | For the Nine Months Ended

September 30, | | | Period from

September 9, 2003

(date of inception)

through | |

| | | 2013 | | | 2012 | | | 2013 | | | 2012 | | | September 30, 2013 | |

Research contract revenue | | $ | 200 | | | $ | 200 | | | $ | 600 | | | $ | 600 | | | $ | 2,067 | |

| | | | | | | | | | | | | | | | | | | | |

Operating expenses: | | | | | | | | | | | | | | | | | | | | |

Research and development, including costs of research contracts | | | 6,247 | | | | 16,215 | | | | 40,133 | | | | 48,464 | | | | 252,478 | |

General and administrative | | | 3,068 | | | | 5,712 | | | | 11,459 | | | | 15,462 | | | | 99,777 | |

| | | | | | | | | | | | | | | | | | | | |

Total operating expenses | | | 9,315 | | | | 21,927 | | | | 51,592 | | | | 63,926 | | | | 352,255 | |

| | | | | | | | | | | | | | | | | | | | |

Loss from operations | | | (9,115 | ) | | | (21,727 | ) | | | (50,992 | ) | | | (63,326 | ) | | | (350,188 | ) |

Other income (expense), net | | | (191 | ) | | | (42 | ) | | | (190 | ) | | | (65 | ) | | | 4,511 | |

Change in fair value of warrants | | | (7,407 | ) | | | 3,945 | | | | 2,979 | | | | (2,516 | ) | | | 13,750 | |

| | | | | | | | | | | | | | | | | | | | |

Net loss | | $ | (16,713 | ) | | $ | (17,824 | ) | | $ | (48,203 | ) | | $ | (65,907 | ) | | $ | (331,927 | ) |

| | | | | | | | | | | | | | | | | | | | |

Net loss per share—basic and diluted | | $ | (0.20 | ) | | $ | (0.23 | ) | | $ | (0.58 | ) | | $ | (0.85 | ) | | | | |

| | | | | | | | | | | | | | | | | | | | |

Weighted average common shares outstanding to compute net loss per share—basic and diluted | | | 83,161,927 | | | | 78,670,222 | | | | 83,051,151 | | | | 77,605,590 | | | | | |

| | | | | | | | | | | | | | | | | | | | |

The accompanying notes are an integral part of the unaudited interim financial statements.

5

ZIOPHARM Oncology, Inc. (a development stage company)

STATEMENT OF STOCKHOLDERS’ EQUITY

For the nine Months Ended September 30, 2013

(unaudited)

(in thousands, except share and per share data)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Stockholders’ Equity | |

| | Preferred Stock | | | Common Stock | | | Additional

Paid-in

Capital

Common

Stock | | | Additional

Paid-in

Capital

Warrants | | | Deficit

Accumulated

During the

Development

Stage | | | Total

Stockholders’

Equity | |

| | Shares | | | Amount | | | Shares | | | Amount | | | | | |

Balance at December 31, 2012 | | | — | | | $ | — | | | | 83,236,840 | | | $ | 83 | | | $ | 325,177 | | | $ | 6,909 | | | $ | (283,724 | ) | | $ | 48,445 | |

Stock-based compensation | | | — | | | | — | | | | — | | | | — | | | | 2,482 | | | | — | | | | — | | | | 2,482 | |

Exercise of employee stock options | | | — | | | | — | | | | 570,168 | | | | 1 | | | | 955 | | | | — | | | | — | | | | 956 | |

Exercise of warrants to purchase common stock | | | — | | | | — | | | | 98,359 | | | | — | | | | 343 | | | | (142 | ) | | | — | | | | 201 | |

Expired warrants | | | — | | | | — | | | | — | | | | — | | | | 3,110 | | | | (3,110 | ) | | | — | | | | — | |

Cancelled restricted stock | | | — | | | | — | | | | (163,747 | ) | | | — | | | | — | | | | — | | | | — | | | | — | |

Repurchase of shares of restricted common stock | | | — | | | | — | | | | (60,041 | ) | | | | | | | (250 | ) | | | — | | | | — | | | | (250 | ) |

Net loss | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | | | | (48,203 | ) | | | (48,203 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Balance at September 30, 2013 | | | — | | | $ | — | | | | 83,681,579 | | | $ | 84 | | | $ | 331,817 | | | $ | 3,657 | | | $ | (331,927 | ) | | $ | 3,631 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

The accompanying notes are an integral part of the unaudited interim financial statements.

6

ZIOPHARM Oncology, Inc. (a development stage company)

STATEMENTS OF CASH FLOWS

(unaudited)

(in thousands)

| | | | | | | | | | | | |

| | | For the Nine Months

Ended September 30, | | | Period from

September 9, 2003

(date of inception)

through | |

| | | 2013 | | | 2012 | | | September 30, 2013 | |

Cash flows from operating activities: | | | | | | | | | | | | |

Net loss | | $ | (48,203 | ) | | $ | (65,907 | ) | | $ | (331,927 | ) |

Adjustments to reconcile net loss to net cash used in operating activities: | | | | | | | | | | | | |

Depreciation and amortization | | | 582 | | | | 466 | | | | 3,156 | |

Stock-based compensation | | | 2,482 | | | | 3,482 | | | | 22,663 | |

Change in fair value of warrants | | | (2,979 | ) | | | 2,516 | | | | (13,750 | ) |

Loss on disposal of fixed assets | | | 194 | | | | 48 | | | | 251 | |

Common stock issued in exchange for in-process research and development | | | — | | | | — | | | | 36,151 | |

Change in operating assets and liabilities: | | | | | | | | | | | | |

(Increase) decrease in: | | | | | | | | | | | | |

Receivables | | | (391 | ) | | | 66 | | | | (449 | ) |

Prepaid expenses and other current assets | | | 3,717 | | | | (5,922 | ) | | | (3,195 | ) |

Other noncurrent assets | | | 262 | | | | (47 | ) | | | (739 | ) |

Deposits | | | 5 | | | | (42 | ) | | | (129 | ) |

Increase (decrease) in: | | | | | | | | | | | | |

Accounts payable | | | (618 | ) | | | 2,521 | | | | 891 | |

Accrued expenses | | | (4,943 | ) | | | 5,861 | | | | 11,573 | |

Deferred revenue | | | (600 | ) | | | (600 | ) | | | 2,933 | |

Deferred rent | | | 8 | | | | 226 | | | | 447 | |

Other liabilities | | | 20 | | | | — | | | | 20 | |

| | | | | | | | | | | | |

Net cash used in operating activities | | | (50,464 | ) | | | (57,332 | ) | | | (272,104 | ) |

| | | | | | | | | | | | |

Cash flows from investing activities: | | | | | | | | | | | | |

Purchases of property and equipment | | | (119 | ) | | | (1,482 | ) | | | (4,745 | ) |

Proceeds from sale of property and equipment | | | 1 | | | | — | | | | 2 | |

| | | | | | | | | | | | |

Net cash used in investing activities | | | (118 | ) | | | (1,482 | ) | | | (4,743 | ) |

| | | | | | | | | | | | |

Cash flows from financing activities: | | | | | | | | | | | | |

Stockholders’ capital contribution | | | — | | | | — | | | | 500 | |

Proceeds from exercise of stock options | | | 956 | | | | 30 | | | | 2,329 | |

Payments to employees for repurchase of common stock | | | (250 | ) | | | (96 | ) | | | (3,117 | ) |

Proceeds from exercise of warrants | | | 201 | | | | 330 | | | | 13,280 | |

Proceeds from issuance of common stock and warrants, net | | | — | | | | 49,170 | | | | 270,726 | |

Proceeds from issuance of preferred stock, net | | | — | | | | — | | | | 16,760 | |

| | | | | | | | | | | | |

Net cash provided by financing activities | | | 907 | | | | 49,434 | | | | 300,478 | |

| | | | | | | | | | | | |

Net increase (decrease) in cash and cash equivalents | | | (49,675 | ) | | | (9,380 | ) | | | 23,631 | |

Cash and cash equivalents, beginning of period | | | 73,306 | | | | 104,713 | | | | — | |

| | | | | | | | | | | | |

Cash and cash equivalents, end of period | | $ | 23,631 | | | $ | 95,333 | | | $ | 23,631 | |

| | | | | | | | | | | | |

Supplementary disclosure of cash flow information: | | | | | | | | | | | | |

Cash paid for interest | | $ | — | | | $ | — | | | $ | — | |

| | | | | | | | | | | | |

Cash paid for income taxes | | $ | — | | | $ | — | | | $ | — | |

| | | | | | | | | | | | |

Supplementary disclosure of noncash investing and financing activities: | | | | | | | | | | | | |

Warrants issued to placement agents and investors | | $ | — | | | $ | — | | | $ | 47,276 | |

| | | | | | | | | | | | |

Preferred stock conversion to common stock | | $ | — | | | $ | — | | | $ | 16,760 | |

| | | | | | | | | | | | |

Exercise of equity-classified warrants to common shares | | $ | 142 | | | $ | 269 | | | $ | 9,466 | |

| | | | | | | | | | | | |

Exercise of liability-classified warrants to common shares | | $ | — | | | $ | 412 | | | $ | 352 | |

| | | | | | | | | | | | |

The accompanying notes are an integral part of the unaudited interim financial statements.

7

ZIOPHARM Oncology, Inc. (a development stage company)

NOTES TO FINANCIAL STATEMENTS

(unaudited)

1. Business

Overview

ZIOPHARM Oncology, Inc. (“ZIOPHARM” or the “Company”) is a biopharmaceutical company that seeks to acquire, develop and commercialize, on its own or with commercial partners, a diverse portfolio of cancer drugs that can address unmet medical needs through the development of a proprietary synthetic biology platform and small molecule drug candidates.

The Company’s operations to date have consisted primarily of raising capital and conducting research and development. Accordingly, the Company is considered to be in the development stage at September 30, 2013. The Company’s fiscal year ends on December 31.

The Company has operated at a loss since its inception in 2003 and has minimal revenues. The Company anticipates that losses will continue for the foreseeable future. At September 30, 2013, the Company’s accumulated deficit was approximately $331.9 million. Following the restructuring described in Note 3, the Company currently believes that it has sufficient capital to fund development and commercialization activities into the first quarter of 2014. The Company’s ability to continue operations after its current cash resources are exhausted depends on its ability to obtain additional financing or to achieve profitable operations, as to which no assurances can be given. Cash requirements may vary materially from those now planned because of changes in the Company’s focus and direction of its research and development programs, competitive and technical advances, patent developments, regulatory changes or other developments. Additional financing will be required to continue operations after the Company exhausts its current cash resources and to continue its long-term plans for clinical trials and new product development. There can be no assurance that any such financing can be obtained by the Company, or if obtained, what the terms thereof may be, or that any amount that the Company is able to raise will be adequate to support the Company’s working capital requirements until it achieves profitable operations.

Basis of Presentation

The accompanying unaudited interim financial statements have been prepared in accordance with the instructions to Form 10-Q pursuant to the rules and regulations of the Securities and Exchange Commission. Certain information and note disclosures required by generally accepted accounting principles in the United States have been condensed or omitted pursuant to such rules and regulations.

It is management’s opinion that the accompanying unaudited interim financial statements reflect all adjustments (which are normal and recurring) that are necessary for a fair statement of the results for the interim periods. The unaudited interim financial statements should be read in conjunction with the audited financial statements and the notes thereto for the year ended December 31, 2012, included in the Company’s Form 10-K, as amended, for such fiscal year.

The year-end balance sheet data was derived from the audited financial statements but does not include all disclosures required by generally accepted accounting principles in the United States.

The results disclosed in the Statements of Operations for the three and nine months ended September 30, 2013 are not necessarily indicative of the results to be expected for the full fiscal year.

Use of Estimates

The preparation of financial statements in conformity with accounting principles generally accepted in the United States requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and the disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Although the Company regularly assesses these estimates, actual results could differ from those estimates. Changes in estimates are recorded in the period in which they become known.

8

ZIOPHARM Oncology, Inc. (a development stage company)

NOTES TO FINANCIAL STATEMENTS (unaudited)

1. Business – (continued)

The Company’s most significant estimates and judgments used in the preparation of its financial statements are:

| | • | | Clinical trial expenses; |

| | • | | Fair value measurements for stock based compensation and warrants; and |

Subsequent Events

The Company evaluated all events and transactions that occurred after the balance sheet date through the date of this filing. During this period, the Company did not have any material recognizable or disclosable subsequent events.

2. Summary of Significant Accounting Policies

The Company’s significant accounting policies were identified in the Company’s Form 10-K, as amended, for the fiscal year ended December 31, 2012. There have been no material changes in those policies since the filing of our Form 10-K, as amended.

3. Restructuring

On April 3, 2013, the Company completed a workforce reduction plan to reduce costs as part of the Company’s decision to terminate development of palifosfamide in first-line metastatic soft tissue sarcoma and place exclusive strategic focus on its synthetic biology programs, which are being developed in partnership with Intrexon Corporation (“Intrexon”) (see Notes 6, 7 and 9). Pursuant to the workforce reduction plan, the Company eliminated a total of 65 positions, comprised of 40 filled positions and 25 unfilled positions across various functions and locations. Employees whose positions were eliminated as part of the plan were notified beginning on April 2, 2013. Affected employees were offered separation benefits, including severance payments, and temporary healthcare coverage assistance. In connection with the elimination of filled positions as part of the workforce reduction plan, the Company incurred charges of $1.7 million during the second quarter of 2013, primarily for one-time contractual severance benefits.

On July 16, 2012, the Company announced that it restructured its management team and closed its Germantown, MD office. As a result of this action, the Company recorded a restructuring charge, consisting primarily of severance, stock based compensation associated with stock option modifications (see Note 9) and health benefit continuation costs of approximately $1.3 million. These costs are included in general and administrative expense for the nine month period ending September 30, 2012 and the period from inception (September 9, 2003) through September 30, 2013.

On August 30, 2013, the Company entered into a sublease agreement to lease 5,249 square feet in its Boston office to a subtenant. The Company remains primarily liable to pay rent on the original lease. We recorded a loss on the sublease in the amount of $42 thousand during the three and nine months ended September 30, 2013, representing the remaining contractual obligation of $367 thousand, less $325 thousand in expected sublease revenue from our subtenant. We retired assets in this subleased area as a result of this sublease with a net book value of $194 thousand, and recorded a loss on disposal of fixed assets for the same amount in the three and nine months ended September 30, 2013.

9

ZIOPHARM Oncology, Inc. (a development stage company)

NOTES TO FINANCIAL STATEMENTS (unaudited)

4. Fair Value Measurements

The Company accounts for its financial assets and liabilities using fair value measurements. The accounting standard defines fair value, establishes a framework for measuring fair value under generally accepted accounting principles and enhances disclosures about fair value measurements. Fair value is defined as the exchange price that would be received for an asset or paid to transfer a liability (an exit price) in the principal or most advantageous market for the asset or liability in an orderly transaction between market participants on the measurement date. Valuation techniques used to measure fair value must maximize the use of observable inputs and minimize the use of unobservable inputs. The standard describes a fair value hierarchy based on three levels of inputs, of which the first two are considered observable and the last unobservable, that may be used to measure fair value which are the following:

| | • | | Level 1—Quoted prices in active markets for identical assets or liabilities. |

| | • | | Level 2—Inputs other than Level 1 that are observable, either directly or indirectly, such as quoted prices for similar assets or liabilities; quoted prices in markets that are not active; or other inputs that are observable or can be corroborated by observable market data for substantially the full term of the assets or liabilities. |

| | • | | Level 3—Unobservable inputs that are supported by little or no market activity and that are significant to the fair value of the assets or liabilities. |

Assets and liabilities measured at fair value on a recurring basis as of September 30, 2013 and December 31, 2012 are as follows:

| | | | | | | | | | | | | | | | |

| ($ in thousands) | | | | | Fair Value Measurements at Reporting Date Using | |

Description | | Balance as of

September 30, 2013 | | | Quoted Prices in

Active Markets for

Identical

Assets/Liabilities

(Level 1) | | | Significant Other

Observable Inputs

(Level 2) | | | Significant

Unobservable Inputs

(Level 3) | |

Cash equivalents | | $ | 22,680 | | | $ | 22,680 | | | $ | — | | | $ | — | |

| | | | | | | | | | | | | | | | |

Warrant liability | | $ | 9,983 | | | $ | — | | | $ | 9,983 | | | $ | — | |

| | | | | | | | | | | | | | | | |

10

ZIOPHARM Oncology, Inc. (a development stage company)

NOTES TO FINANCIAL STATEMENTS (unaudited)

4. Fair Value Measurements – (continued)

| | | | | | | | | | | | | | | | |

| ($ in thousands) | | | | | Fair Value Measurements at Reporting Date Using | |

Description | | Balance as of

December 31, 2012 | | | Quoted Prices in

Active Markets for

Identical

Assets/Liabilities

(Level 1) | | | Significant Other

Observable Inputs

(Level 2) | | | Significant

Unobservable Inputs

(Level 3) | |

Cash equivalents | | $ | 72,002 | | | $ | 72,002 | | | $ | — | | | $ | — | |

| | | | | | | | | | | | | | | | |

Warrant liability | | $ | 12,962 | | | $ | — | | | $ | 12,962 | | | $ | — | |

| | | | | | | | | | | | | | | | |

The cash equivalents represent deposits in a short term United States treasury money market mutual fund quoted in an active market and classified as a Level 1 asset. The Company’s Level 2 financial liabilities consist of long-term investor and placement agent warrants issued in connection with its December 2009 public offering. The warrants were valued using Binomial/Monte Carlo valuation models. See Note 8 for additional disclosures on the valuation methodology and significant assumptions.

5. Net Loss per Share

Basic net loss per share is computed by dividing net loss by the weighted average number of shares of common stock outstanding for the period. The Company’s potential dilutive shares, which include outstanding common stock options, unvested restricted stock and warrants, have not been included in the computation of diluted net loss per share for any of the periods presented as the result would be anti-dilutive. Such potential shares of common stock at September 30, 2013 and 2012 consist of the following:

| | | | | | | | |

| | | September 30, | |

| | | 2013 | | | 2012 | |

Stock options | | | 5,730,169 | | | | 5,361,487 | |

Unvested restricted common stock | | | 431,178 | | | | 922,838 | |

Warrants | | | 10,392,387 | | | | 11,197,454 | |

| | | | | | | | |

| | | 16,553,734 | | | | 17,481,779 | |

| | | | | | | | |

6. Related Party Transactions

On January 6, 2011, the Company entered into an Exclusive Channel Partner Agreement (the “Channel Agreement”) with Intrexon (see Note 7 for additional disclosure relating to the Channel Agreement). Our director, Randall J. Kirk, is the CEO, a director, and the largest stockholder of Intrexon. During the nine months ended September 30, 2012, the Company paid Intrexon approximately $11.4 million, of which $4.8 million was for services already incurred and the remaining $6.6 million expected to be incurred within a year. This amount was included as part of prepaid expenses and other current assets on the balance sheet as of September 30, 2012. During the nine months ended September 30, 2013, the Company was billed $5.9 million for services performed by Intrexon, of which $4.9 million was applied to the prepaid expenses balance and the rest was accrued. As of September 30, 2013, the prepaid balance in other current assets on the accompanying balance sheet had been reduced to $0.

On January 25, 2012, Intrexon purchased 1,923,075 shares of common stock in the Company’s public offering (see Note 9).

On November 7, 2012, the Company issued 3,636,926 shares of common stock to Intrexon under the terms of its Stock Purchase Agreement with Intrexon dated January 6, 2011 (see Note 9).

11

ZIOPHARM Oncology, Inc. (a development stage company)

NOTES TO FINANCIAL STATEMENTS (unaudited)

7. Commitments and Contingencies

Patent and Technology License Agreement—The University of Texas M. D. Anderson Cancer Center and the Texas A&M University System.

On August 24, 2004, the Company entered into a patent and technology license agreement with The Board of Regents of the University of Texas System, acting on behalf of The University of Texas M. D. Anderson Cancer Center and the Texas A&M University System (collectively, the “Licensors”). Under this agreement, the Company was granted an exclusive, worldwide license to rights (including rights to United States and foreign patent and patent applications and related improvements and know-how) for the manufacture and commercialization of two classes of organic arsenicals (water- and lipid-based) for human and animal use. The class of water-based organic arsenicals includes darinaparsin.

As partial consideration for the license rights obtained, the Company made an upfront payment in 2004 of $125 thousand and granted the Licensors 250,487 shares of the Company’s common stock. In addition, the Company issued options to purchase an additional 50,222 shares outside the 2003 Stock Option Plan for $0.002 per share following the successful completion of certain clinical milestones, which vested with respect to 12,555 shares upon the filing of an Investigation New Drug application (“IND”) for darinaparsin in 2005 and vested with respect to another 25,111 shares upon the completion of dosing of the last patient for both Phase 1 clinical trials in 2007. The Company recorded $120 thousand of stock based compensation expense related to the vesting in 2007. The remaining 12,556 shares will vest upon enrollment of the first patient in a multi-center pivotal clinical trial, i.e. a human clinical trial intended to provide the substantial evidence of efficacy necessary to support the filing of an approvable New Drug Application (“NDA”). In addition, the Licensors are entitled to receive certain milestone payments, including $100 thousand that was paid in 2005 upon the commencement of Phase 1 clinical trial and $250 thousand that was paid in 2006 upon the dosing of the first patient in the Company-sponsored Phase 2 clinical trial for darinaparsin. The Company may be required to make additional payments upon achievement of certain other milestones in varying amounts which on a cumulative basis could total up to an additional $4.5 million. In addition, the Licensors are entitled to receive single-digit percentage royalty payments on sales from a licensed product and will also be entitled to receive a portion of any fees that the Company may receive from a possible sublicense under certain circumstances.

The license agreement also contains other provisions customary and common in similar agreements within the industry, such as the right to sublicense the Company rights under the agreement. However, if the Company sublicenses its rights prior to the commencement of a pivotal study, i.e. a human clinical trial intended to provide the substantial evidence of efficacy necessary to support the filing of an approvable NDA, the Licensors will be entitled to receive a share of the payments received by the Company in exchange for the sublicense (subject to certain exceptions). The term of the license agreement extends until the expiration of all claims under patents and patent applications associated with the licensed technology, subject to earlier termination in the event of defaults by the Company or the Licensors under the license agreement, or if the Company becomes bankrupt or insolvent. No milestones under the license agreement were reached or expensed since 2006.

12

ZIOPHARM Oncology, Inc. (a development stage company)

NOTES TO FINANCIAL STATEMENTS (unaudited)

7. Commitments and Contingencies – (continued)

License Agreement with DEKK-Tec, Inc.

On October 15, 2004, the Company entered into a license agreement with DEKK-Tec, Inc., pursuant to which it was granted an exclusive, worldwide license for palifosfamide. As part of the signing of license agreement with DEKK-Tec, the Company expensed an upfront $50 thousand payment to DEKK-Tec in 2004.

In consideration for the license rights, DEKK-Tec is entitled to receive payments upon achieving certain milestones in varying amounts, which on a cumulative basis may total $4.0 million. Of the aggregate milestone payments, most will be creditable against future royalty payments as referenced below. The Company expensed a $100 thousand milestone payment upon achieving Phase 2 milestones during the year ended December 31, 2006. Additionally, in 2004 the Company issued DEKK-Tec an option to purchase 27,616 shares of the Company’s common stock for $0.02 per share. Upon the execution of the license agreement, 6,904 shares vested and were subsequently exercised in 2005 and the remaining options will vest upon certain milestone events, culminating with final United States Food and Drug Administration (“FDA”) approval of the first NDA submitted by the Company (or by its sublicensee) for palifosfamide. DEKK-Tec is entitled to receive single-digit percentage royalty payments on the sales of palifosfamide should it be approved for commercial sale. On March 16, 2010, the Company expensed a $100 thousand milestone payment upon receiving a United States Patent for palifosfamide. In December 2010, the Company expensed a $300 thousand milestone payment and vested 6,904 stock options upon achieving Phase 3 milestones. These options were subsequently exercised in 2011. The Company’s obligation to pay royalties will terminate on a country-by-country basis upon the expiration of all valid claims of patents in such country covering licensed product, subject to earlier termination in the event of defaults by the parties under the license agreement. No milestones under the license agreement were reached or expensed since 2010.

Option Agreement with Southern Research Institute (“SRI”)

On December 22, 2004, the Company entered into an Option Agreement with Southern Research Institute (“SRI”) (the “Option Agreement”), pursuant to which the Company was granted an exclusive option to obtain an exclusive license to SRI’s interest in certain intellectual property, including exclusive rights related to certain isophosphoramide mustard analogs.

Also on December 22, 2004, the Company entered into a Research Agreement with SRI pursuant to which the Company agreed to spend a sum not to exceed $200 thousand between the execution of the agreement and December 21, 2006, including a $25 thousand payment that was made simultaneously with the execution of the agreement, to fund research and development work by SRI in the field of isophosphoramide mustard analogs. The Option Agreement was exercised on February 13, 2007. Under the license agreement entered into upon exercise of the option, the Company is required to remit minimum annual royalty payments of $25 thousand until the first commercial sale of a licensed product. These payments were made for the years ended December 31, 2008, 2009, 2010, 2011 and 2012. The Company may be required to make payments upon achievement of certain milestones in varying amounts which on a cumulative basis could total up to $775 thousand. In addition, SRI will be entitled to receive single digit percentage royalty payments on the sales of a licensed product in any country until all licensed patents rights in that country which are utilized in the product have expired. No milestones under the license agreement were reached or expensed since the agreement’s inception.

13

ZIOPHARM Oncology, Inc. (a development stage company)

NOTES TO FINANCIAL STATEMENTS (unaudited)

7. Commitments and Contingencies – (continued)

License Agreement with Baxter Healthcare Corporation

On November 3, 2006, the Company entered into a definitive Asset Purchase Agreement for indibulin and a License Agreement to proprietary nanosuspension technology with affiliates of Baxter Healthcare S.A. The purchase included the entire indibulin intellectual property portfolio as well as existing drug substance and capsule inventories. The terms of the Asset Purchase Agreement included an upfront cash payment of approximately $1.1 million and an additional $100 thousand payment for existing inventory, both of which were expensed in 2006. In addition to the upfront costs, the Asset Purchase Agreement includes additional diligence and milestone payments that could amount to approximately $8 million in the aggregate and royalties on net sales of products covered by a valid claim of a patent for the life of the patent on a country-by-country basis. The Company expensed a $625 thousand milestone payment upon the successful United States IND application for indibulin in 2007. The License Agreement requires payment of a $15 thousand annual patent and license prosecution/maintenance fee through the expiration of the last of the licensed patents, which is expected to expire in 2025, and single-digit royalties on net sales of licensed products covered by a valid claim of a patent for the life of the patent on a country-by-country basis. The term of the license agreement extends until the expiration of the last to expire of the patents covering the licensed products, subject to earlier termination in the event of defaults by the parties under the license agreement.

In October 2009, the Baxter License Agreement was amended to allow the Company to manufacture indibulin. During the year ended December 31, 2012, a milestone of $250 thousand was reached and expensed. No milestones under the license agreement were reached or expensed during the nine months ended September 30, 2013.

Exclusive Channel Partner Agreement with Intrexon Corporation

On January 6, 2011, we entered into the Channel Agreement, with Intrexon that governs a “channel partnering” arrangement in which we use Intrexon’s technology directed towardsin vivo expression of effectors in connection with the development of DC-RTS-IL-12 and Ad-RTS-IL-12 and generally to research, develop and commercialize products, in each case in which DNA is administered to humans for expression of anti-cancer effectors for the purpose of treatment or prophylaxis of cancer, which we collectively refer to as the Cancer Program. The Channel Agreement establishes committees comprised of representatives of us and Intrexon that govern activities related to the Cancer Program in the areas of project establishment, chemistry, manufacturing and controls, clinical and regulatory matters, commercialization efforts and intellectual property.

The Channel Agreement grants us a worldwide license to use patents and other intellectual property of Intrexon in connection with the research, development, use, importing, manufacture, sale, and offer for sale of products involving DNA administered to humans for expression of anti-cancer effectors for the purpose of treatment or prophylaxis of cancer (collectively the “ZIOPHARM Products”). Such license is exclusive with respect to any clinical development, selling, offering for sale or other commercialization of ZIOPHARM Products, and otherwise is non-exclusive. Subject to limited exceptions, we may not sublicense the rights described without Intrexon’s written consent.

Under the Channel Agreement, and subject to certain exceptions, we are responsible for, among other things, the performance of the Cancer Program, including development, commercialization and certain aspects of manufacturing of ZIOPHARM Products. Intrexon is responsible for the costs of establishing manufacturing capabilities and facilities for the bulk manufacture of products developed under the Cancer Program, certain other aspects of manufacturing and costs of discovery-stage research with respect to platform improvements and costs of filing, prosecution and maintenance of Intrexon’s patents.

Subject to certain expense allocations and other offsets provided in the Channel Agreement, we will pay Intrexon on a quarterly basis 50% of net profits derived in that quarter from the sale of ZIOPHARM Products, calculated on a ZIOPHARM Product-by- ZIOPHARM Product basis. We have likewise agreed to pay Intrexon on a quarterly basis 50% of revenue obtained in that quarter from a sublicensor in the event of a sublicensing arrangement. In addition, in partial consideration for each party’s execution and delivery of the Channel Agreement, we entered into a Stock Purchase Agreement with Intrexon.

14

ZIOPHARM Oncology, Inc. (a development stage company)

NOTES TO FINANCIAL STATEMENTS (unaudited)

7. Commitments and Contingencies – (continued)

Intrexon may terminate the Channel Agreement if we fail to use diligent efforts to develop and commercialize ZIOPHARM Products or if we elect not to pursue the development of a Cancer Program identified by Intrexon that is a “Superior Therapy” as defined in the Channel Agreement. We may voluntarily terminate the Channel Agreement upon 90 days written notice to Intrexon.

Upon termination of the Channel Agreement, we may continue to develop and commercialize any ZIOPHARM Product that, at the time of termination:

| | • | | is being commercialized by us; |

| | • | | has received regulatory approval; |

| | • | | is a subject of an application for regulatory approval that is pending before the applicable regulatory authority; or |

| | • | | is the subject of at least an ongoing Phase 2 clinical trial (in the case of a termination by Intrexon due to an uncured breach or a voluntary termination by us), or an ongoing Phase 1 clinical trial in the field (in the case of a termination by us due to an uncured breach or a termination by Intrexon following an unconsented assignment by us or our election not to pursue development of a Superior Therapy). |

Our obligation to pay 50% of net profits or revenue described above with respect to these “retained” products will survive termination of the Channel Agreement.

Also see Notes 6 and 9.

Collaboration Agreement with Harmon Hill, LLC

On April 8, 2008, the Company signed a collaboration agreement for Harmon Hill, LLC (“Harmon Hill”) to provide consulting and other services for the development and commercialization of oncology therapeutics by ZIOPHARM. Under the agreement the Company has agreed to pay Harmon Hill $20 thousand per month for the consulting services and has further agreed to pay Harmon Hill (a) $500 thousand upon the first patient dosing of the Specified Drug in a pivotal trial, which trial uses a dosing Regimen introduced by Harmon Hill; and (b) provided that the Specified Drug receives regulatory approval from the FDA, the European Medicines Agency (“EMA”) or another regulatory agency for the marketing of the Specified Drug, a 1% royalty of the Company’s net sales will be awarded to Harmon Hill. If the Specified Drug is sublicensed to a third party, the agreement entitles Harmon Hill to 1% award of royalties or other payments received from a sublicense. Subject to renewal or extension by the parties, the term of the agreement was for a one year period that expired April 8, 2009. Following such expiration, the parties continued to operate under the terms of the agreement and, in 2010, the agreement was formally extended through April 8, 2011 and again through April 8, 2012. The agreement was extended through November 8, 2012 upon which date it expired. The Company expensed $240 thousand during the years ended December 31, 2010 and 2011 and expensed $200 thousand during the year ended December 31, 2012 for consulting services per the aforementioned agreement. No milestones under the collaboration agreement were reached or expensed since the agreement’s inception.

On June 27, 2013, the Company signed a new collaboration agreement with Harmon Hill to provide consulting and other services for the development and commercialization of oncology therapeutics by ZIOPHARM, effective April 1, 2013. Under the agreement the Company has agreed to pay Harmon Hill $15 thousand per month for the consulting services. Subject to renewal or extension by the parties, the term of the agreement is for a one year period. The Company expensed $90 thousand for the nine months ended September 30, 2013.

Collaboration Agreement with Solasia Pharma K.K.

On March 7, 2011, we entered into a License and Collaboration Agreement with Solasia Pharma K.K., (“Solasia”).

Pursuant to the License and Collaboration Agreement, we granted Solasia an exclusive license to develop and commercialize darinaparsin in both intravenous (“IV”) and oral forms and related organic arsenic molecules, in all indications for human use in a pan- Asian/Pacific territory comprised of Japan, China, Hong Kong, Macau, Republic of Korea, Taiwan, Singapore, Australia, New Zealand, Malaysia, Indonesia, Philippines and Thailand.

15

ZIOPHARM Oncology, Inc. (a development stage company)

NOTES TO FINANCIAL STATEMENTS (unaudited)

7. Commitments and Contingencies – (continued)

As consideration for the license, we received an upfront payment of $5.0 million to be used exclusively for further clinical development of darinaparsin outside of the pan-Asian/Pacific territory, and will be entitled to receive additional payments of up to $32.5 million in development-based milestones and up to $53.5 million in sales-based milestones. We will also be entitled to receive double-digit royalty payments from Solasia based upon net sales of licensed products in the applicable territories, once commercialized, and a percentage of sublicense revenues generated by Solasia.

The upfront payment for research and development funding is earned over the period of effort. We currently estimate this period to be 75 months, which could be adjusted in the future.

Under the License and Collaboration Agreement, we provide Solasia with drug product to conduct clinical trials. These transfers are accounted for as a reduction of research and development costs and an increase in collaboration receivables.

The agreement provides that Solasia will be responsible for the development and commercialization of darinaparsin in the pan-Asian/Pacific territory.

CRO Services Agreement with PPD Development, L.P.

We are party to a Master Clinical Research Organization Services Agreement with PPD Development, L.P., or PPD, dated January 29, 2010, a related work order dated June 25, 2010 and a related work order dated April 8, 2011 under which PPD provides clinical research organization, or CRO, services in support of our clinical trials. PPD is entitled to cumulative payments of up to $20.0 million under these arrangements, which is payable by us in varying amounts upon PPD achieving specified milestones. During the year ended December 31, 2010, we expensed $1.8 million upon contract execution and $1.1 million upon a clinical study commencement of enrollment in North America. During the year ended December 31, 2011, additional milestones related to commencing enrollment in Europe, Latin America and Asia along with enrollment based milestones were met and we recorded an aggregate $4.0 million expense. During the year ended December 31, 2012, additional enrollment-based and contract modification milestones were met and expensed totaling $3.8 million. During the nine months ended September 30, 2013, patient progression and data based milestones totaling $9.2 million were met and expensed.

CRO Services Agreement with Pharmaceutical Research Associates, Inc.

On December 13, 2011, we entered into a Master Clinical Research Organization Services Agreement with Pharmaceutical Research Associates, Inc., or PRA, under which PRA provides CRO services in support of our clinical trials. PRA is entitled to cumulative payments of up to $9.5 million under these arrangements, which is payable by us in varying amounts upon PRA achieving specified milestones. During the year ended December 31, 2012, we expensed $7.3 million upon the achievement of various letter of intent and enrollment-based milestones. During the nine months ended September 30, 2013, contract modification and patient enrollment based milestones totaling $2.2 million were met and expensed.

16

ZIOPHARM Oncology, Inc. (a development stage company)

NOTES TO FINANCIAL STATEMENTS (unaudited)

7. Commitments and Contingencies – (continued)

CRO Services Agreement with Novella Clinical, Inc.

On December 4, 2008, we entered into a Master Clinical Research Organization Services Agreement with Novella Clinical, Inc., or Novella, under which PRA provides CRO services in support of our clinical trials. The work order for the current trial being conducted by Novella was signed on November 2, 2012. Novella is entitled to cumulative payments of up to $790 thousand under these arrangements, which is payable by us in varying amounts upon Novella achieving specified milestones. During the year ended December 31, 2012, we expensed $256 thousand upon the achievement of various milestones. During the nine months ended September 30, 2013, two database related milestones and one site activation related milestone were met and expensed totaling $136 thousand.

8. Warrants

The Company has issued both warrants that are accounted for as liabilities and warrants that are accounted for as equity instruments. The number of warrants outstanding at September 30, 2013 and December 31, 2012 were as follows:

| | | | | | | | |

| | | September 30,

2013 | | | December 31,

2012 | |

Liability-classified warrants | | | 8,050,709 | | | | 8,050,709 | |

Equity-classified warrants | | | 2,341,678 | | | | 3,146,745 | |

| | | | | | | | |

Total warrants | | | 10,392,387 | | | | 11,197,454 | |

| | | | | | | | |

17

ZIOPHARM Oncology, Inc. (a development stage company)

NOTES TO FINANCIAL STATEMENTS (unaudited)

8. Warrants – (continued)

Liability-Classified Warrants

In May 2005, the Company issued 419,786 warrants to placement agents for services performed in connection with a 2005 private placement (the “2005 Warrants”), 11,083 of which were subsequently exercised. The remaining 408,703 warrants were originally valued at $1.6 million. Subject to certain exceptions, the 2005 Warrants provide for anti-dilution protection should common stock or common stock equivalents be subsequently issued at a price less than the exercise price of the 2005 Warrants then in effect, which was initially $4.75 per share. This provision was triggered when the Company sold stock in a 2006 private placement at $4.63 per share. Accordingly, the 2005 Warrants were re-priced at $4.69. The provision was triggered a second time upon completion of a 2009 private placement in which the Company sold stock at $1.825 per share and issued common stock purchase warrants with an exercise price of $2.04, and the 2005 Warrants were re-priced at $4.25. The provision was triggered again when the Company sold stock in a December 2009 public offering at $3.10 per share and the 2005 Warrants were re-priced at $3.93 per share. Of the total warrant tranche, 419,207 were exercised and the remaining 579 expired on May 31, 2012.

Also, in connection with its December 2009 public securities offering, the Company issued warrants to purchase an aggregate of 8,206,520 shares of common stock (including the investor warrants and 464,520 warrants issued to the underwriters for the offering) (the “2009 Warrants”). The 2009 Warrants issued to investors were exercisable immediately and the warrants issued to underwriters became exercisable six months after the date of issuance. The 2009 Warrants have an exercise price of $4.02 per share and have a five-year term. The fair value of the 2009 Warrants was estimated at $22.9 million using a Black-Scholes model with the following assumptions: expected volatility of 105%, risk free interest rate of 2.14%, expected life of five years and no dividends.

The Company assessed whether the 2005 Warrants and the 2009 Warrants require accounting as derivatives. The Company determined that these warrants were not indexed to the Company’s own stock in accordance with accounting standards codification Topic 815,Derivatives and Hedging. As such, the Company has concluded these warrants did not meet the scope exception for determining whether the instruments require accounting as derivatives and were classified as liabilities.

The Company uses the Binomial/Monte Carlo pricing model to estimate the value of the liability-classified warrants. The following assumptions were used in the Binomial/Monte Carlo valuation model at September 30, 2013 and 2012:

| | | | |

| | | September 30, 2013 | | September 30, 2012 |

Risk-free interest rate | | 0.10% | | 0.23% |

Expected life in years | | 1.19 | | 2.19 |

Expected volatility | | 75% | | 70% |

Expected dividend yield | | 0 | | 0 |

Steps per year | | 13 | | 12 |

The change in the fair value of the warrant liability resulted in a loss of $7.4 million and a gain of $3.0 million for the three and nine months ended September 30, 2013, respectively. The change in the fair value of the warrant liability resulted in a gain of $3.9 million for the three months ended September 30, 2012 and a loss of $2.5 million for the nine months ended September 30, 2012, respectively. The change in the fair value of the warrant liability was charged to other income (expense) in the Statements of Operations.

18

ZIOPHARM Oncology, Inc. (a development stage company)

NOTES TO FINANCIAL STATEMENTS (unaudited)

8. Warrants – (continued)

During the nine months ended September 30, 2013, warrant exercises were as follows:

| | | | | | | | | | | | | | | | | | | | |

| (in thousands, except share data) | | Equity

Warrants | | | Liability

Warrants | | | Common

Stock

Issued | | | Liability

Reclassed

to Equity | | | Cash

Received | |

Cash exercises | | | 98,359 | | | | — | | | | 98,359 | | | $ | — | | | $ | 201 | |

Cashless exercises | | | — | | | | — | | | | — | | | | — | | | | — | |

| | | | | | | | | | | | | | | | | | | | |

| | | 98,359 | | | | — | | | | 98,359 | | | $ | — | | | $ | 201 | |

| | | | | | | | | | | | | | | | | | | | |

During the nine months ended September 30, 2012, warrant exercises were as follows:

| | | | | | | | | | | | | | | | | | | | |

| (in thousands, except share data) | | Equity

Warrants | | | Liability

Warrants | | | Common

Stock

Issued | | | Liability

Reclassed

to Equity | | | Cash

Received | |

Cash exercises | | | 161,639 | | | | — | | | | 161,639 | | | $ | — | | | $ | 330 | |

Cashless exercises | | | 24,658 | | | | 373,617 | | | | 98,021 | | | | 412 | | | | — | |

| | | | | | | | | | | | | | | | | | | | |

| | | 186,297 | | | | 373,617 | | | | 259,660 | | | $ | 412 | | | $ | 330 | |

| | | | | | | | | | | | | | | | | | | | |

During the nine months ended September 30, 2013, 706,708 warrants issued on May 3, 2006, exercisable at $5.09 per share, expired unexercised on May 3, 2013.

During the nine months ended September 30, 2012, 1,359,317 warrants issued on February 23, 2007, exercisable at $5.75 per share, expired unexercised on February 23, 2012 and 579 warrants issued on May 31, 2005, exercisable at $3.93 per share, expired unexercised on May 31, 2012.

9. Common Stock

On January 20, 2012, pursuant to an underwriting agreement between the Company and J. P. Morgan Securities LLC, as representative of the several underwriters named therein, the Company completed the sale of an aggregate 10,114,401 shares of the Company’s common stock at a price of $5.20 per share in a public offering. The total gross proceeds resulting from the 2012 public offering were approximately $52.6 million, before deducting selling commissions and expenses.

On November 7, 2012, the Company issued 3,636,926 shares of our common stock, which we refer to as the Milestone Shares, to Intrexon under the terms of its Stock Purchase Agreement with Intrexon dated January 6, 2011. Under the terms of the Stock Purchase Agreement with Intrexon, the Company agreed to issue the Milestone Shares under certain conditions upon dosing of the first patient in a ZIOPHARM-conducted Phase 2 clinical trial in the Unites States, or similar study as the parties may agree in a country other than the United States, of a product candidate that is created, produced, developed or identified directly or indirectly by us during the term of the Channel Agreement and that, subject to certain exceptions, involves DNA administered to humans for expression of anti-cancer effectors for the purpose of treatment or prophylaxis of cancer. On October 24, 2012, the Company initiated dosing in a Phase 2 study of Ad-RTS-IL-12 for unresectable Stage III or IV melanoma, triggering the issuance of the Milestone Shares.

19

ZIOPHARM Oncology, Inc. (a development stage company)

NOTES TO FINANCIAL STATEMENTS (unaudited)

10. Stock-Based Compensation

The Company recognized stock-based compensation expense on all employee and non-employee awards as follows:

| | | | | | | | | | | | | | | | |

| | | For the three months

ended September 30, | | | For the nine months

ended September 30, | |

| (in thousands) | | 2013 | | | 2012 | | | 2013 | | | 2012 | |

Research and development | | $ | 119 | | | $ | 363 | | | $ | 511 | | | $ | 1,305 | |

General and administrative | | | 690 | | | | 828 | | | | 1,971 | | | | 2,177 | |

| | | | | | | | | | | | | | | | |

Stock-based employee compensation expense | | $ | 809 | | | $ | 1,191 | | | $ | 2,482 | | | $ | 3,482 | |

| | | | | | | | | | | | | | | | |

The Company granted 125,000 and 1,551,400 stock options during the three and nine months ended September 30, 2013 that had a weighted-average grant date fair value of $2.47 and $1.94 per share, respectively. The Company granted 76,300 and 508,700 stock options during the three and nine months ended September 30, 2012 that had a weighted-average grant date fair value of $3.95 and $3.56 per share, respectively.

At September 30, 2013, total unrecognized compensation costs related to unvested stock options outstanding amounted to $8.8 million. The cost is expected to be recognized over a weighted-average period of 1.68 years.

On July 16, 2012, the Company extended the contractual life of 829,488 fully vested stock options held by 3 employees from 12 to 18 months, and extended the vesting period for 200,000 unvested stock options and 147,427 unvested shares of restricted stock held by 2 employees from 6 to 12 months (also see Note 3 Restructuring).

On May 31, 2013, the Company extended the contractual life of 66,667 fully vested stock options held by one employee from 3 to 12 months (see Note 3 Restructuring).

On June 14, 2013, the Company extended the contractual life of 71,167 fully vested stock options held by one employee from 3 to 12 months (see Note 3 Restructuring).

20

ZIOPHARM Oncology, Inc. (a development stage company)

NOTES TO FINANCIAL STATEMENTS (unaudited)

10. Stock-Based Compensation – (continued)

For the three months ended September 30, 2013 and 2012, the fair value of stock options was estimated on the date of grant using a Black-Scholes option valuation model with the following assumptions:

| | | | |

| | | For the three months ended September 30, |

| | | 2013 | | 2012 |

Risk-free interest rate | | 1.61 - 1.74% | | 0.79 - 1.04% |

Expected life in years | | 6 | | 6 |

Expected volatility | | 94.96 - 95.64% | | 83.37 - 83.51% |

Expected dividend yield | | 0 | | 0 |

Stock option activity under the Company’s stock option plan for the nine months ended September 30, 2013 is as follows:

| | | | | | | | | | | | | | | | |

| (in thousands, except share and per share data) | | Number of

Shares | | | Weighted-

Average Exercise

Price | | | Weighted-

Average

Contractual

Term (Years) | | | Aggregate

Intrinsic Value | |

Outstanding, December 31, 2012 | | | 7,147,303 | | | $ | 4.11 | | | | | | | | | |

Granted | | | 1,551,400 | | | | 2.55 | | | | | | | | | |

Exercised | | | (570,168 | ) | | | 1.68 | | | | | | | | | |

Cancelled | | | (2,398,366 | ) | | | 4.57 | | | | | | | | | |

| | | | | | | | | | | | | | | | |

Outstanding, September 30, 2013 | | | 5,730,169 | | | $ | 3.73 | | | | 6.89 | | | $ | 4,255 | |

| | | | | | | | | | | | | | | | |

Vested and unvested expected to vest at September 30, 2013 | | | 5,675,997 | | | $ | 3.95 | | | | 4.75 | | | $ | 4,215 | |

| | | | | | | | | | | | | | | | |

Options exercisable, September 30, 2013 | | | 2,996,068 | | | $ | 3.95 | | | | 4.75 | | | $ | 2,203 | |

| | | | | | | | | | | | | | | | |

Options exercisable, December 31, 2012 | | | 3,683,786 | | | $ | 3.56 | | | | 5.28 | | | $ | 3,972 | |

| | | | | | | | | | | | | | | | |

Options available for future grant | | | 1,565,070 | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

A summary of the status of unvested restricted stock for the nine months ended September 30, 2013 is as follows:

| | | | | | | | |

| | | Number of Shares | | | Weighted-Average

Grant Date Fair Value | |

Non-vested, December 31, 2012 | | | 733,739 | | | $ | 4.37 | |

Granted | | | — | | | | — | |

Vested | | | (138,814 | ) | | | 4.26 | |

Cancelled | | | (163,747 | ) | | | 4.42 | |

| | | | | | | | |

Non-vested, September 30, 2013 | | | 431,178 | | | $ | 4.38 | |

| | | | | | | | |

At September 30, 2013, total unrecognized compensation costs related to unvested restricted stock outstanding amounted to $1.5 million. The cost is expected to be recognized over a weighted-average period of 1.32 years.

21

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations

Forward Looking Statements

This quarterly report on Form 10-Q contains “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. In particular, statements contained in this Form 10-Q, including but not limited to, statements regarding the costs and timing our clinical trials and of the development and commercialization of our pipeline products and services; the sufficiency of our cash, investments and cash flows from operations and our expected uses of cash; our ability to finance our operations and business initiatives and obtain funding for such activities; our future results of operations and financial position, business strategy and plan prospects, projected revenue or costs and objectives of management for future research, development or operations, are forward-looking statements. These statements relate to our future plans, objectives, expectations and intentions and may be identified by words such as “may,” “will,” “should,” “expects,” “plans,” “anticipates,” “intends,” “targets,” “projects,” “contemplates,” “believes,” “seeks,” “goals,” “estimates,” “predicts,” “potential” and “continue” or similar words. Readers are cautioned that these forward-looking statements are only predictions and are subject to risks, uncertainties, and assumptions that are difficult to predict, including those identified below, under Part II, Item 1A. “Risk Factors” and elsewhere herein. Therefore, actual results may differ materially and adversely from those expressed in any forward-looking statements. We undertake no obligation to revise or update any forward-looking statements for any reason.

Company Overview

ZIOPHARM Oncology, Inc. is a biopharmaceutical company that seeks to acquire, develop and commercialize, on its own or with commercial partners, a diverse portfolio of cancer therapies that can address unmet medical needs through synthetic biology. Pursuant to an exclusive channel agreement with Intrexon Corporation, or Intrexon, we obtained rights to Intrexon’s synthetic biology platform for use in the field of oncology, which included two existing clinical stage product candidates, Ad-RTS-IL-12 + Activator Ligand and DC-RTS-IL-12 + Activator Ligand. The synthetic biology platform employs an inducible gene-delivery system that enables controlled delivery of genes that produce therapeutic proteins to treat cancer. Ad-RTS IL-12 is our lead drug candidate, which uses this gene delivery system to produce Interleukin-12, or IL-12, a potent, naturally occurring anti-cancer protein. We are currently studying Ad-RTS-IL-12 in two Phase 2 studies, the first for the treatment of metastatic melanoma, and the second for the treatment of metastatic breast cancer, and expect to announce early, preliminary data from these Phase 2 studies in the fourth quarter of 2013 and final data in 2014. We plan to continue to combine Intrexon’s synthetic biology platform with our capabilities to translate science to the patient setting to develop additional products to stimulate key pathways, including those used by the body’s immune system to inhibit the growth and metastasis of cancers. We have multiple programs under development and expect to file at least eight investigational new drug, or IND, applications through 2015. We also have a portfolio of small molecule drug candidates in early stages of development, which we are not actively developing ourselves but are seeking partners to pursue further development and potential commercialization.

Enabling Technology

Synthetic biology entails the application of engineering principles to biological systems for the purpose of designing and constructing new biological systems or redesigning/modifying existing biological systems. Biological systems are governed by DNA, the building blocks of gene programs, which control cellular processes by coding for the production of proteins and other molecules that have a functional purpose and by regulating the activities of these molecules. This regulation occurs via complex biochemical and cellular reactions working through intricate cell signaling pathways, and control over these molecules modifies the output of biological systems. Synthetic biology has been enabled by the application of information technology and advanced statistical analysis, also known as bioinformatics, to genetic engineering, as well as by improvements in DNA synthesis. Synthetic biology aims to engineer gene-based programs or codes to modify cellular function to achieve a desired biological outcome. Its application is intended to allow more precise control of drug concentration and dose, thereby improving the therapeutic index associated with the resulting drug.

On January 6, 2011, we entered into an Exclusive Channel Partner Agreement with Intrexon, which we refer to as the Channel Agreement, to develop and commercialize novel DNA-based therapeutics in the field of cancer treatment by combining Intrexon’s synthetic biology platform with our capabilities to translate science to the patient setting. As a result, our DNA synthetic biology platform employs an inducible gene-delivery system that enables controlled delivery of genes that produce therapeutic proteins to treat cancer. The first example of this regulated controlled delivery is achieved by producing IL-12, a potent, naturally occurring anti-cancer protein, under the control of Intrexon’s proprietary biological “switch” to turn on/off the therapeutic protein expression at the tumor site. We and Intrexon refer to this “switch” as the RheoSwitch Therapeutic System® or RTS® platform. Our initial drug candidates being developed using the synthetic biology platform are Ad-RTS-IL-12 and DC-RTS-IL-12, with a current focus on Ad-RTS-IL-12.

We have demonstrated that we are able to simultaneously express multiple effectors under control of the RTS® platform from the same construct. In the mouse, we have also shown that we are able to express multigenic DNA constructs in an embedded, controlled bioreactor, by injecting into skeletal muscle and measuring the DNA-coded proteins in the blood. Furthermore, we have also demonstrated the ability to express these same three genes under RTS® platform control in mesenchymal stem cells, or MSCs.

22

Recent Developments

On October 21 and 22, 2013, we presented preclinical data from four studies at the 2013 joint meeting of the American Association for Cancer Research, the National Cancer Institute and the European Organization for Research and Treatment of Cancer, which we refer to as the 2013 AARC-NCI-EORTC. The reported data further supports the breadth of the Intrexon synthetic biology platform technology and the ability to express immunotherapies, and other therapies, in bothin vitro andin vivo models. The following summarizes the reported results:

The Controlled Local Expression of IL-12 as an Immunotherapeutic Treatment of Glioma study was designed to evaluate the viability of IL-12 expression-based therapeutic candidates in the treatment of glioma, or brain cancer. Two different RTS® controlled IL-12 expression-based therapeutic candidates were explored for the study, Ad-RTS-IL-12 (AD) and DC-RTS-IL-12 (DC), along with the orally-available small molecule activator ligand veledimex. Results demonstrated that the activator ligand achieved brain penetration in normal mouse and monkey models. Further, treatment with both AD and DC demonstrated dose-related increase in survival in a mouse model with no adverse clinical signs. Animals treated with DC > 5000 MOI (multiplicity of infection) or AD 5 x 109 viral particles survived throughout the duration of the study (100% survival at 75 days) with no adverse clinical signs observed. In contrast, the mean survival in the control groups was 22 (±3) days. We believe these findings support the utility of localized regulated IL-12 production as an approach for the treatment of malignant glioma.

The three additional abstracts presented at the 2013 AARC-NCI-EORTC meeting demonstrated (i) systemic expression of three distinct immune effectors from a single RTS® regulated multigenic construct in mice; (ii) in vitro data supporting the potential use of MSCs for tumor-targeted delivery of single or multiple RTS® regulated cancer immunotherapies; and (iii) data supporting functional single chain variable fragment-Fc fusion proteins as an alternate approach to monoclonal antibodies which are more amenable for multi-genic therapies. These results highlight the potential use of skeletal muscle as an embedded controllable bioreactor to generate therapeutics for tumor-targeted delivery of single or multiple RTS® regulated cancer immunotherapies which could potentially be translated into an effective clinical regimen in the treatment of cancer. Furthermore, the potential use of MSCs for tumor-targeted delivery of single or multiple RTS® regulated cancer immunotherapies could potentially be translated into an effective clinical regimen for a variety of cancers. Furthermore, RTS® driven expression of trastuzumab- and cetuximab-based scFv-Fc constructs from an embedded controllable bioreactor have potential utility as DNA-based anticancer therapeutics.

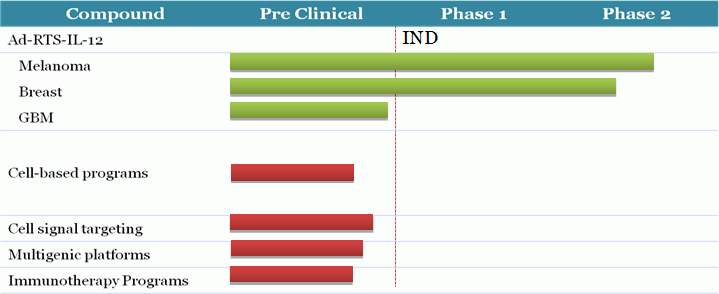

Product candidates

The following chart identifies our current synthetic biology product candidates and their stage of development, each of which are described in more detail below.

Synthetic Biology Programs:

Ad-RTS-IL-12 + Activator Ligand.Ad-RTS-IL-12 is currently being tested in two Phase 2 studies, the first for the treatment of metastatic melanoma, and the second for the treatment of non-resectable recurrent or metastatic breast cancer. Ad-RTS IL-12 is our lead drug candidate, which uses our gene delivery system to produce Interleukin-12, or IL-12, a potent, naturally occurring anti-cancer protein.

In March 2013, we announced the initiation of a randomized, open label Phase 2 clinical study of Ad-RTS-IL-12 to treat metastatic breast cancer. The two-part, multi-center U.S. study is enrolling patients with non-resectable, recurrent or metastatic breast cancer who have visible lesions or lesions accessible by injection. The primary endpoint of the study is rate of progression-free survival at 16 weeks. Secondary endpoints include objective response rate and duration of response. Initiation of the clinical study was followed by

23

the presentation of results, from a study in a breast cancer murine preclinical model, demonstrating the anti-tumor effects and tolerability of Ad-RTS-IL-12. The data were presented at the American Association for Cancer Research 2013 Annual Meeting in April.

In May 2013, we announced promising results from nonclinical studies and a Phase 1/2 study in metastatic melanoma using Ad-RTS-IL-12. In these studies, the controlled expression of IL-12, through a regulatable gene therapy strategy, was found to limit systemic toxicity while inducing biological and clinical activity in a dose-dependent fashion. The findings were presented in an oral session at the 16th Annual Meeting of the American Society of Gene and Cell Therapy, or ASGCT. In June, updated results were presented at the 2013 American Society for Clinical Oncology, or ASCO. Ad-RTS-IL-12 + Activator Ligand induce production of IL-12 mRNA in the tumor microenvironment (switch on). Upon removal of the oral activator ligand, IL-12 mRNA levels return to baseline (switch off). Following treatment with Ad-RTS-IL-12 + Activator Ligand, increases in TILs (CD8+, CD45RO+) were observed in the tumor microenvironment. Clinical activity was observed in injected and non-injected lesions primarily at the higher doses of the activator ligand. Inflammation, shrinkage, flattening, and depigmentation of lesions correlated with the highest serum levels of IFN-g. Ad-RTS-IL-12 + Activator Ligand therapy was generally well-tolerated and its safety profile is consistent with other immunotherapies.

The Phase 1 portion of the Phase 1/2 is study is complete, and the Phase 2 portion is on-going. This Phase 2 study, a multi-center, single-arm, open-label study, is enrolling patients with unresectable Stage III or IV melanoma and further evaluating the safety and efficacy of intratumoral injections of Ad-RTS-IL-12 in combination with an oral activator ligand. Data from this Phase 2 study is expected in the fourth quarter of 2013.

We are in the process of finalizing clinical protocol designs that will lead to the initiation of Phase 2 studies in the combination with standard of care, or SOC, in first quarter 2014 for the treatment of metastatic melanoma and metastatic breast cancer. Specifically, we expect to commence enrollment in a glioblastoma mulitforme Phase 1 dose-escalation study in the first quarter of 2014, with preliminary data expected near the end of 2014; in a melanoma Phase 2 combination study with SOC study in the first quarter of 2014, with preliminary data expected near the end of 2014; and in a breast cancer Phase 2 combination study with SOC in the first quarter of 2014, with preliminary data expected in the first quarter of 2015. Melanoma, breast cancer, and glioma (detailed below) represent significant market potentials with high unmet medical needs. The incidence of melanoma is 76,690, breast cancer is 234,580, and glioblastoma is 18,000 with the majority of patients representing a high unmet medical need.

DC-RTS-IL-12 + Activator Ligand. We completed enrollment in a Phase 1 dose escalation study of DC-RTS-IL-12 in the second quarter of 2012 in the United States. DC-RTS-IL-12 employs intratumoral injection of modified dendritic cells from each patient and oral dosing of an activator ligand to turn on in vivo expression of IL-12. DC-RTS-IL-12, through the RTS® platform, controls the timing and level of transgene expression. The RTS® technology functions as a “gene switch” for the regulated expression of human IL-12 in the patients’ dendritic cells which are transduced with a replication incompetent adenoviral vector carrying the IL-12 gene under the control of the RTS® platform. Currently, there are no actively enrolling studies using DC-RTS-IL-12, as we have prioritized our clinical development efforts on Ad-RTS-IL-12.