Friedman, Billings, Ramsey & Co.

New England in November

“Un-conference”

Michael P. Daly,

President & Chief Executive Officer

Wayne F. Patenaude, CFA

Senior Vice President & Chief Financial Officer

L. Alexandra Dest – Investor Relations

Vice President & Senior Investment Officer

Boston, Massachusetts

November 8-9, 2005

Cautionary Statement

Statements contained in this presentation contain forward-looking statements within the meaning of the

Private Securities Litigation Reform Act of 1995. These statements are based on the beliefs and

expectations of management as well as the assumptions made using information currently available to

management. Since these statements reflect the views of management concerning future events, these

statements involve risks, uncertainties and assumptions. These risks and uncertainties include among

others, changes in market interest rates and general and regional economic conditions, changes in

government regulations, changes in accounting principles and the quality or composition of the loan and

investment portfolios and other factors that may be described in Berkshire Hills Bancorp, Inc.’s quarterly

reports on Form 10-Q for the quarters ended March 31, June 30 and September 30 and in its annual

report on Form 10-K, each filed with the Securities and Exchange Commission, which are available at

the Securities and Exchange Commission’s internet website (www.sec.gov) and to which reference is

hereby made. Therefore, actual future results may differ significantly from results discussed in the

forward-looking statements.

You are cautioned not to place undue reliance on any forward-looking statements, which speak

only as of November 8 and November 9, 2005. Except as required by applicable law

or regulation, Berkshire Hills Bancorp, Inc. undertakes no obligation to update

any forward-looking statements, to reflect events or circumstances that occur

after November 8 and November 9, 2005.

Profile

Strategic Actions

Financial Report

Interest Rate Risk

Asset Quality

Creating Value

Berkshire Hills Bancorp

State chartered savings bank with commercial

bank balance sheet

Market capitalization - approximately $291

million at September 30, 2005

Ownership structure as of September 30, 2005

Insiders (not including options) 26%

Berkshire Bank Foundation 7%

Institutional holders 39%

Profile

Profile

At September 30, 2005

Assets

$2 billion

Loans

$1.4 billion

Deposits

$1.35 billion

Operations

24 full-service branches;

10 free standing ATMs

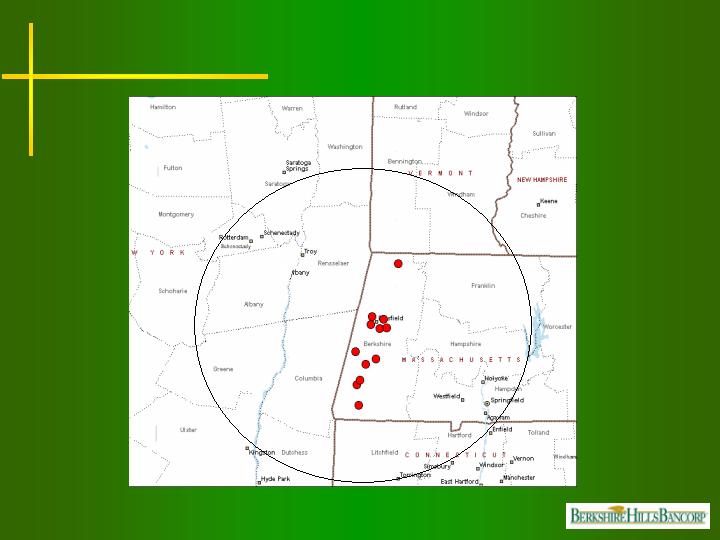

Original BHL Franchise

Current Franchise

Clifton Park

Strategic Actions

Proven ability to execute

October 2002

Management changes

December 2002

Sold $69.7 mm in sub-prime auto loans

March 2003

Performance benchmarks announced

December 2003

Sold $9.9 mm in sub-prime auto loans

January 2004

Six Sigma initiative implemented

June 2004

Sold 60% ownership of EastPoint

Technologies, LLC

July 2004

Opened representative (LPO) office in

Albany, NY

Strategic Actions

Proven ability to execute

October 2004

Purchased branch in Oriskany Falls, NY –

Allowing de novo branching in NY

December 2004

Purchased Berkshire Financial Planning

June 2005

Opened Albany and Clifton Park, NY branches

June 2005

Acquired Woronoco Bancorp creating a $2 billion

institution

October 2005

Acquired 2 insurance agencies; anticipate $500k

annual fee income

November 2005

Received approval for NY municipal bank

November 2005

Switched to NASDAQ national market; symbol

“BHLB”

No silos – keep it simple

Strong board of directors

Culture of enthusiasm, teamwork,

energy and cross-selling

Ability to attract and maintain the best

Six Sigma culture

Differentiating Factors

Efficiency Ratio and Non-Interest Expense

to Average Assets

(1)Exclusive of merger & conversion expenses and other non-recurring items

(2)In addition to note 1, also excludes amortization of intangible assets

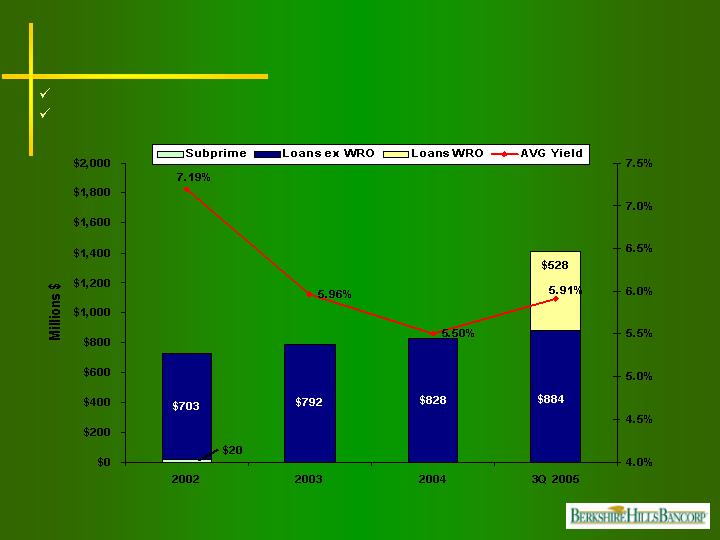

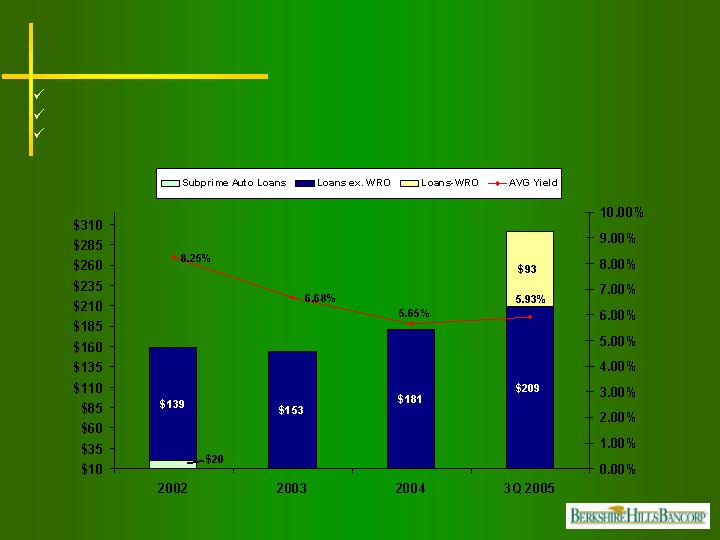

Quality Loan Growth

Compound growth rate since 2002 ex Woronoco and sub-prime = 9%

Compound growth rate since 2002 = 28%

$1,412

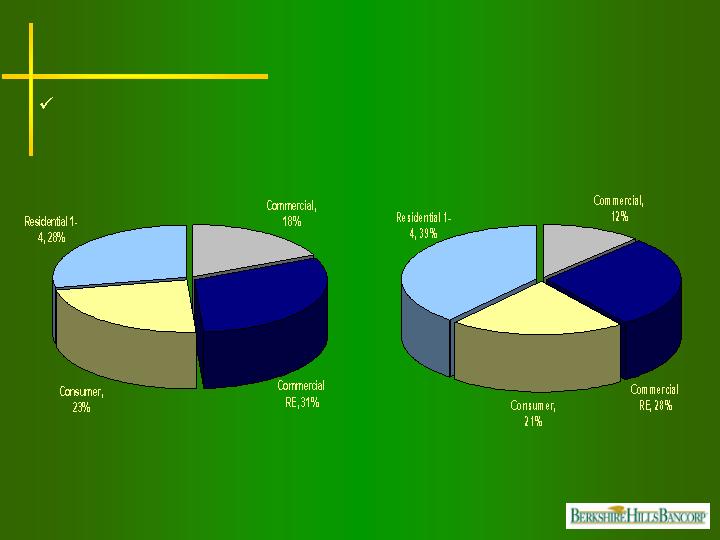

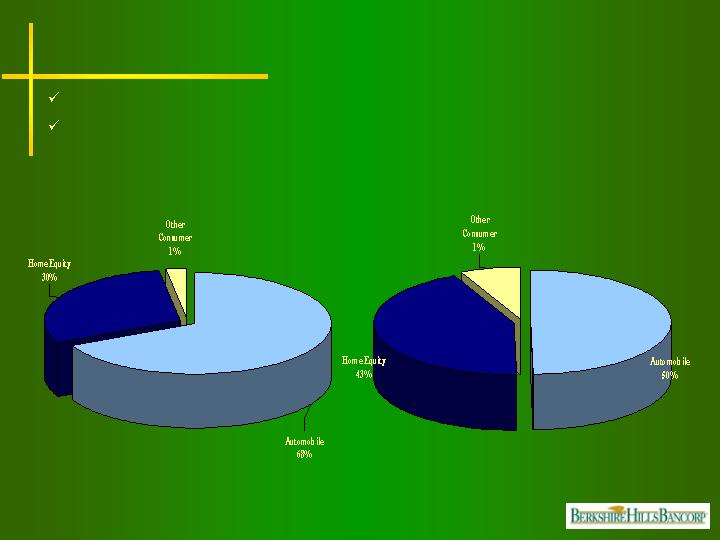

Loan Portfolio Composition

Commercial bank focus

At September 30, 2005

At December 31, 2004

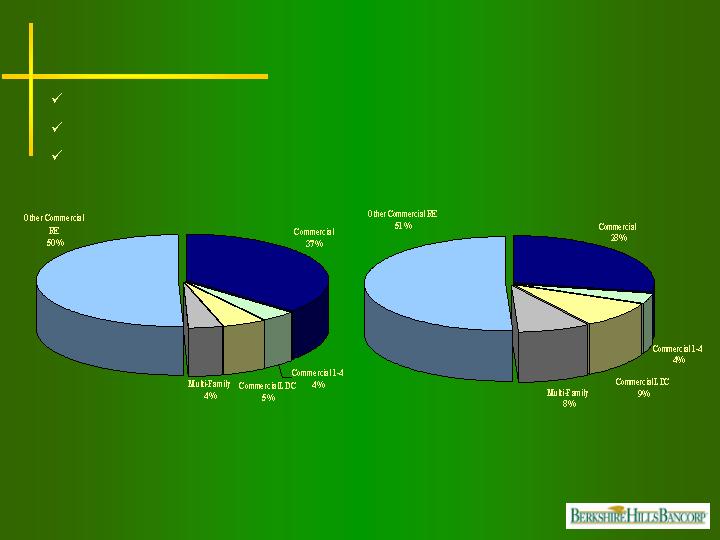

Commercial Loans

Compound growth rate since 2002 exclusive of Woronoco = 11%

Compound growth rate since 2002 = 22%

$559

Commercial Loans

At September 30, 2005

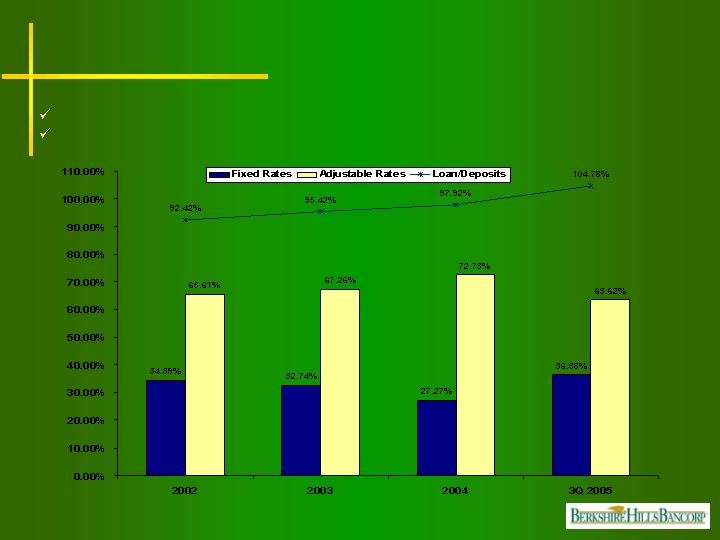

67% of portfolio re-prices within 1 year

Only 14% re-prices beyond 3 years

24% floating with prime or other short-term indexes

At December 31, 2004

Credit Profile - Commercial Loans

Lending criteria with few exceptions:

Personal guarantees required

Maximum loan to value 80%

Minimum debt service coverage 1.25X

Delinquency ratio

Net-charge-offs (recoveries)

0.43%

0.84%

0.96%

9/30/05

12/04

12/03

0.02%

0.05%

0.08%

9/30/05

12/04

12/03

Consumer Loans

Compound growth rate since 2002 exclusive of Woronoco and sub-prime auto loans = 16%

Compound growth rate since 2002 = 26%

Portfolio’s average FICO at 715 at 9/30/05

$159

$302

Consumer Loans

At September 30, 2005

Duration of auto loans = 2.25 years

Nearly all home equity loans float with prime

At December 31, 2004

Credit Profile - Residential/Consumer Loans

Prime auto loans – At September 30, 2005

0.42%

Net charge-offs (annualized)

0.47%

Delinquency

none

Sub-prime loans

732

FICO Score – Originations 2005

715

FICO Score – Portfolio Avg.

Credit Profile-Home Equity Lines of Credit

None

Losses (2002 – 2005)

0.25%

Delinquency

None

LTV > 80%

55%

Average LTV

756

FICO Score – Originations (2 yrs)

Home Equity Line of Credit – At September 30, 2005

Residential Mortgage Portfolio Mix

Prior to acquisition, sold $90mm in fixed rate WRO loans

Credit Profile – Residential Loans

Residential 1-4 family mortgages – At September 30, 2005

None

Losses (2002 – 2005)

0.12%

Delinquency

None

Uninsured loans w/LTV > 80%

None

Interest only product

61%

Average LTV

728

FICO Score – Originations (2 yrs)

Asset Quality

0.11%

0.06%

0.01%

Net loan charge-offs/average loans

691

705

715

Average FICO Score

0.67%

0.37%

0.24%

Loan delinquency/total loans

250%

811%

841%

Allowance/NPL’s

1.13%

1.13%

0.93%

Allowance/total loans

0.40%

0.14%

0.11%

NPA/total loans and REO

4Q03

4Q04

3Q05

Percent except NPA and NPL totals

Solid credit quality trends

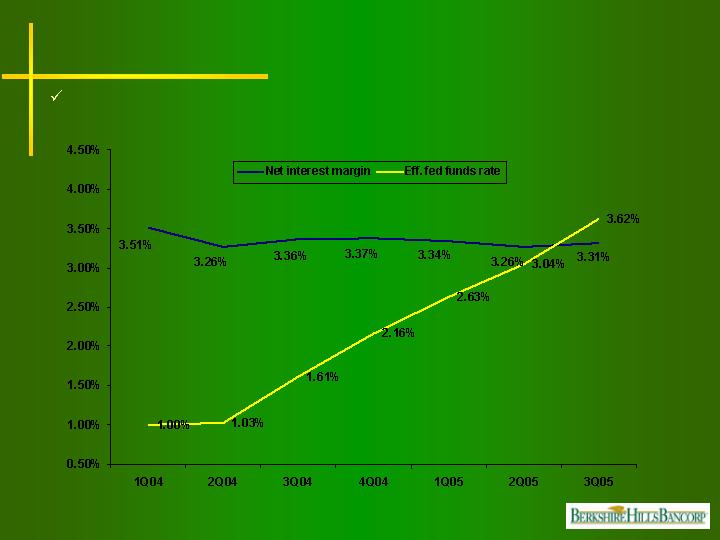

Interest Rate Risk Management

Stable margins against rising rates and flattening yield curve

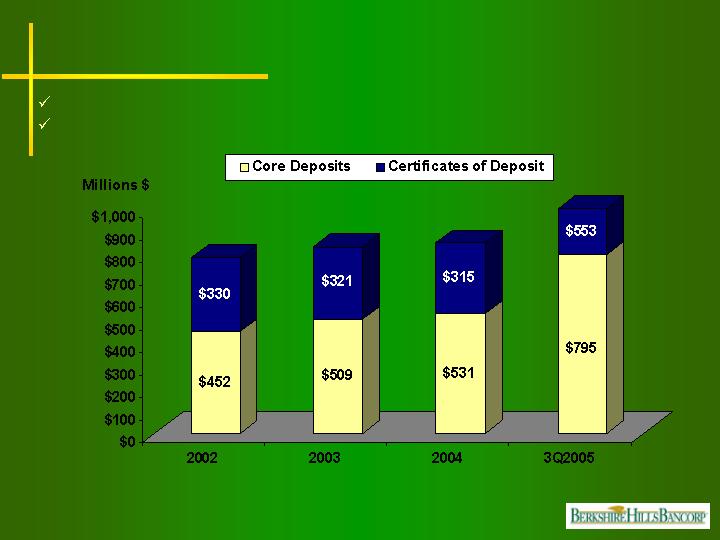

Total Deposits

Core deposit compound growth rate = 23%

Core deposit compound growth rate excluding Woronoco = 6%

Core deposits consist of demand, NOW, savings and money market accounts

$782

$830

$845

$1,348

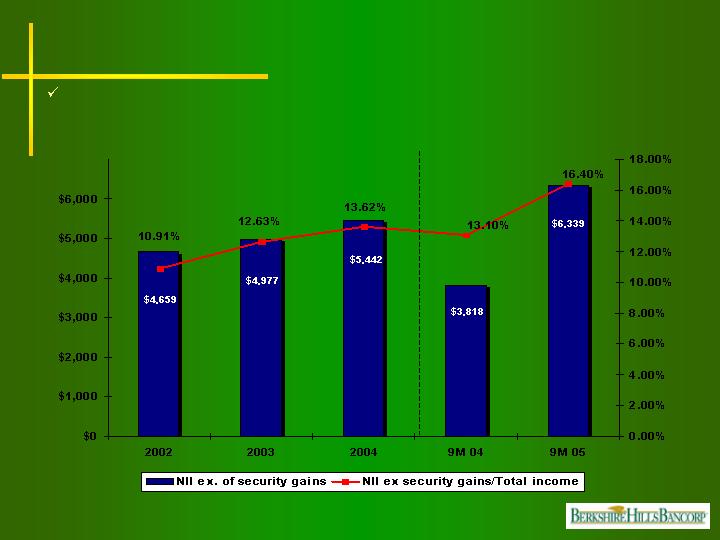

Non-Interest Income (NII) Ex. Security Gains

Main drivers of non-interest income: wealth management, insurance, loan service

and customer service fees

Wealth Management

11.1% asset growth

$398 mm under management

92% new money to Berkshire Bank

98% retention ratio

11.2% revenue growth

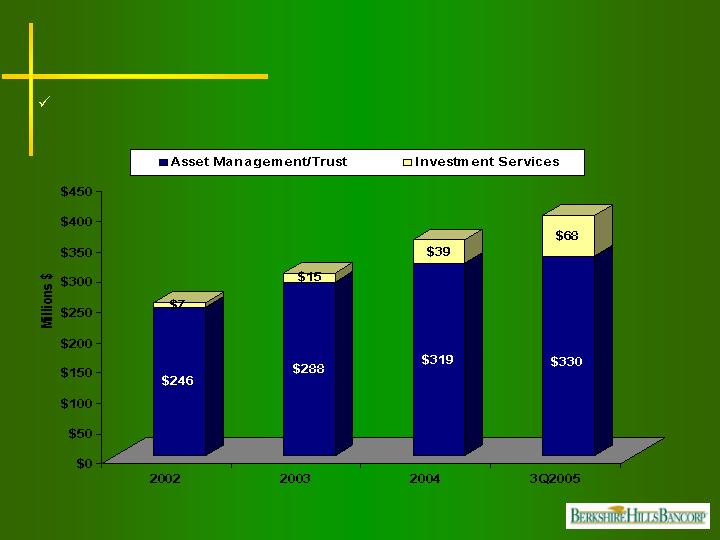

Wealth Management Asset Growth

Assets under management compounded growth rate = 18%

$253.3

$302.3

$357.9

$397.8

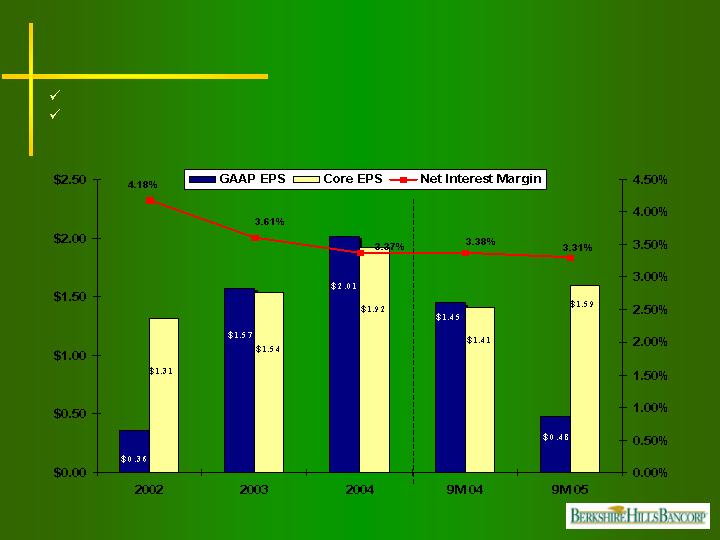

EPS/Net Interest Margin

Lower margins more than offset by strong credit quality and expense control

Well positioned for rising rate environment

Performance Benchmarks

0.80%

0.89%

0.92%

ROA

62.73%

60.66%

55.32%

Efficiency Ratio

7.94%

9.68%

13.45%

ROE-Tangible

2003

2004

3Q05

Annualized

Actual Results

Benchmarks announced in March 2003

Within 3 years:

Double digit ROE

1.0% ROA

Efficiency ratio below 60%

Creating Value

Successful WRO integration

Achieved 36% cost saves vs. 30% target

On target to provide accretion to earnings

Integrated 2 cultures seamlessly

Improved non-interest income

Double digit organic growth in all business lines

Diligent expense management

Strong asset quality

Effective capital management through de-novo branching, accretive

acquisitions and share repurchases

Proven execution

Creating Value

Attractive commercial & community bank franchise

Motivate & retain the best quality people

Drive organic loan & deposit growth; relationship building

Continue to expand fee based income

Consumer & commercial fee based business

Wealth management

Private banking

Insurance

Cross-selling initiatives

Develop Six Sigma culture

Expansion through de novo branching and acquisition

Management focused on delivering results & creating shareholder value

Creating Value

Join us December 1st in

New York City

for more details…

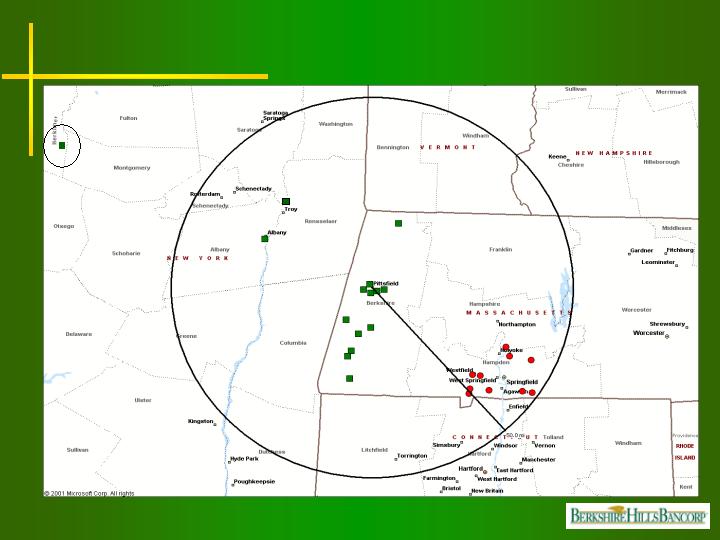

On the move

Appendix: Reconciliation of GAAP and Core Income

-

243

Add: Disallowance of the dividend

received deduction on the Bank’s REIT

9,211

1,107

Add: Net losses and expenses on sale of

sub-prime auto loans, net of tax

5,258

307

Add: Net other non-recurring, net of tax

$0.36

$1.57

$2.01

$1.45

$0.48

$0.54

Diluted earnings per share-GAAP

5,867

5,703

5,731

5,735

7,061

8,856

Average diluted share outstanding

9,550

2,022

953

689

1,722

541

Less: Gain on the sale of securities, net

of tax

$1.31

$1.54

$1.92

$1.41

$1.59

$0.54

Diluted earnings per share-Core

686

185

431

431

-

Add: Loss from discontinued operations

-Sale of EastPoint Technologies, net of

tax

-

-

-

-

8,379

-

Add: ESOP termination expense, net of

tax benefit of $288,000

$7,702

$8,785

$10,987

$8,075

$11,210

$4,743

Net core earnings

-

$2,097

2002

-

$8,965

2003

-

-

1,164

538

Add: Merger and conversion-related

expenses, net of tax

$11,509

$8,333

$3,389

$4,746

Net Income

2004

Nine

months

ended 2004

Nine

months

Ended 2005

3rd

Quarter

2005

Net Income and Earnings per share

($’s in millions)

Investor Presentation

November 8 & 9, 2005

If you have any questions, please contact:

Wayne F. Patenaude, CFA

Senior Vice President and CFO

(413) 236-3195

wpatenaude@berkshirebank.com

OR

L. Alexandra Dest, Investor Relations

Vice President and Senior Investment Officer

(413) 236-3163

adest@berkshirebank.com

Company website: www.berkshirebank.com

Loan Portfolio Characteristics

At September 30, 2005

Positioned for rising rates

Less reliant on earnings from the securities portfolio