Banking as a Business

Lawrence A. Bossidy

Chairman

Michael P. Daly

President & Chief Executive Officer

New York City

December 1, 2005

1

Cautionary Statement

Statements contained in this presentation contain forward-looking statements within the meaning of the

Private Securities Litigation Reform Act of 1995. These statements are based on the beliefs and

expectations of management as well as the assumptions made using information currently available to

management. Since these statements reflect the views of management concerning future events, these

statements involve risks, uncertainties and assumptions. These risks and uncertainties include among

others, changes in market interest rates and general and regional economic conditions, changes in

government regulations, changes in accounting principles and the quality or composition of the loan and

investment portfolios and other factors that may be described in Berkshire Hills Bancorp, Inc.’s quarterly

reports on Form 10-Q for the quarters ended March 31, June 30 and September 30 and in its annual

report on Form 10-K, each filed with the Securities and Exchange Commission, which are available at

the Securities and Exchange Commission’s internet website (www.sec.gov) and to which reference is

hereby made. Therefore, actual future results may differ significantly from results discussed in the

forward-looking statements.

You are cautioned not to place undue reliance on any forward-looking statements, which speak

only as of December 1, 2005. Except as required by applicable law

or regulation, Berkshire Hills Bancorp, Inc. undertakes no obligation to update

any forward-looking statements, to reflect events or circumstances that occur

after December 1, 2005.

2

Agenda

Overview

Part I: 1997-2002

Where We Started

Part II: 2002 - 2005

Where We Are Today

How We Got Here

Part III: 2005-2008

Where We Are Going

How We Will Get There

Wrap Up

3

Mission Statement

Berkshire Bank is committed to being the financial institution of

choice for individuals, businesses, and municipalities in the

markets we serve.

We will achieve this position of competitive leadership by

consistently meeting and exceeding the expectations of our

customers in the delivery of

Trusted Solutions.

We value and respect our customers and employees and will

strive to maintain an environment within which employees will

want to work and customers will want to bank.

Overview

4

Berkshire Bank is a bank

managed as a business, with

the ongoing support and

wisdom of Mr. Bossidy

Lawrence Bossidy

Former Vice-chair of General Electric Company

Former Chairman and CEO of AlliedSignal Inc.

Retired Chairman and CEO of Honeywell International

Named CEO of the Year – 1994 – by Financial World

Member of the Boards of Directors of JPMorgan Chase,

Merck & Company and Berkshire Hills Bancorp Inc.

Co-author - Execution: The Discipline of Getting Things

Done and Confronting Reality: Doing What Matters to Get

Things Right

Bio

5

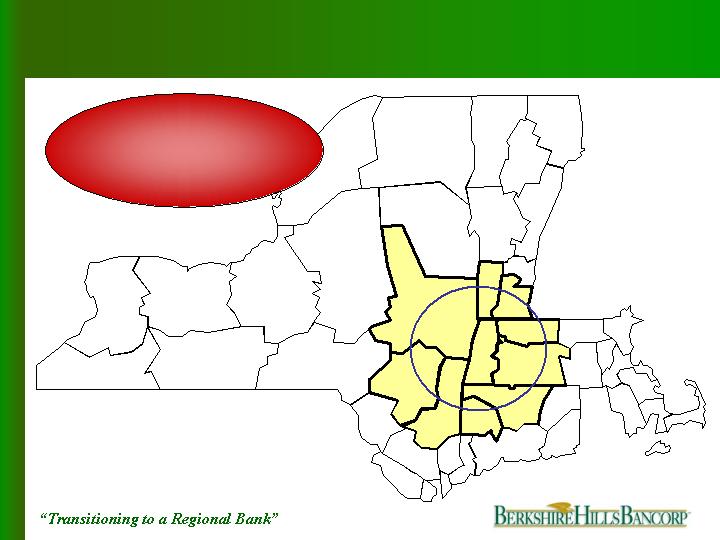

Overview - Today

Berkshire County

Pioneer Valley

Capital Region

6

State chartered savings bank with commercial bank balance sheet

Ownership Structure – September 30, 2005

Institutional holders

39%

Insiders*

12%

Individuals

42%

Foundation

7%

Corporate Profile – September 30, 2005

Market capitalization

$291 million

Assets

$2.0 billion

Loans

$1.4 billion

Deposits

$1.35 billion

Employees

374 FTEs

Operations

24 full-service branches

10 free standing ATMs

*Not including options

Where We Started

Part I: 1997 - 2002

7

Confined to

Berkshire County

1997 Merger

Berkshire County Savings Bank

Great Barrington Savings Bank

Where We Started 1997-2002

11

11

Branches

$723

$498

Loans ($M)

$782

$539

Deposits ($M)

2002

1997

8

Merger

Cultural integration

Initial IPO

Capital deployment

Data processing company

Sub-prime lending

Constant throughout

Commercial lending discipline

Where We Started 1997 - 2002

Lacked

management

strength & depth

9

“Management Changes and Gaining Credibility”

Where We Are Today

and

How We Got Here

Part II: 2002 - 2005

10

How We Got Here 2002 - 2005

20 years commercial banking experience

Bank of Boston

MBA from Columbia University

Co-chair with Massachusetts Lt. Governor;

Regional Competitiveness Council

Member Massachusetts Business

Roundtable

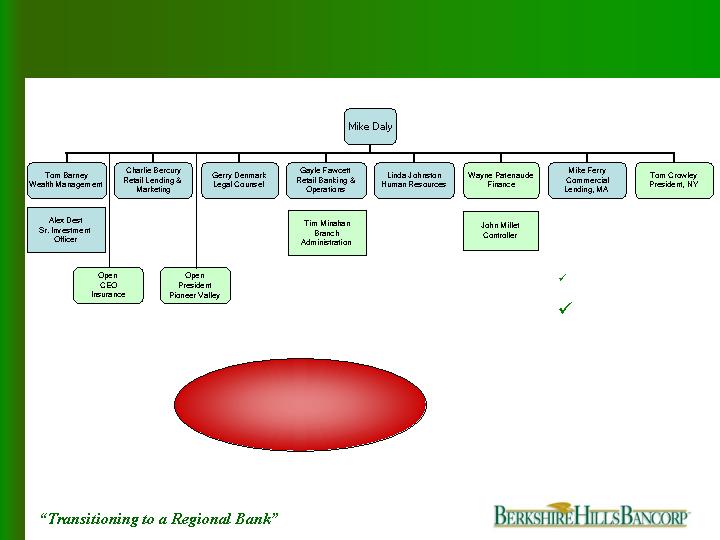

Mike Daly – President and CEO

11

Culture

People

Growth

Asset quality

Asset liability management

Operational efficiencies

Strategic capital allocation

How we got here

Mike’s Agenda

Turnaround keys

12

How we got here

Culture

Realign team, stay focused,

breakdown barriers

Strengthen board

Instill culture of enthusiasm,

teamwork, energy and cross-selling

Drive customer satisfaction

Team transformation

Culture

People

Growth

Asset Quality

Asset Liability

Efficiencies

Capital Allocation

13

Attract and retain very good people

Committed

Ambitious

Accountability

Pay for performance

Six Sigma training

Corporate governance

How we got here

People

Team committed to

accelerated growth

Culture

People

Growth

Asset Quality

Asset Liability

Efficiencies

Capital Allocation

14

How we got here

People

Culture

People

Growth

Asset Quality

Asset Liability

Efficiencies

Capital Allocation

Diversified and

experienced

management

15

3

$29

New York State

24

$1,348

Total

Branches

9/30/05

Deposits

($millions)

Market

$464

$855

10

11

Pioneer Valley

Berkshire County

How we got here

Growth by Region

Expansion has

exceeded our

expectations

Culture

People

Growth

Asset Quality

Asset Liability

Efficiencies

Capital Allocation

16

How we got here

Growth

Significant annual

growth in every

division

Culture

People

Growth

Asset Quality

Asset Liability

Efficiencies

Capital Allocation

17

Balance sheet composition

How we got here

Growth by Product Line

Less

“thrift-like”

Culture

People

Growth

Asset Quality

Asset Liability

Efficiencies

Capital Allocation

Loans

Deposits

18

Main drivers of non-interest income: wealth management, insurance, loan service

and customer service fees

How we got here

Non-Interest Income

Culture

People

Growth

Asset Quality

Asset Liability

Efficiencies

Capital Allocation

19

*Annualized

0.15

810.5

1.13

0.14

$1,152

2004

0.35

280.4

1.13

0.40

$3,199

2003

0.87

275.5

1.43

0.72

$5,241

2002

0.04

841.2

0.93

0.11

$1,560

3Q05*

NCOs/avg. loans (%)

Allowance/NPLs (%)

Allowance/loans (%)

NPAs/loans + REO (%)

NPAs (000s)

How we got here

Asset Quality

Reduce credit risk

Culture

People

Growth

Asset Quality

Asset Liability

Efficiencies

Capital Allocation

Portfolio well protected…

Positioned for growth

20

Stable margins against rising rates and flattening yield curve

How we got here

Asset Liability Management

1.95

1.00

1.46

3.31

3.37

3.42

3.59

3.46

1.74

4.36

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

5.00

Net Interest Margin

Effective Fed Funds

Sub-Prime Sale

Culture

People

Growth

Asset Quality

Asset Liability

Efficiencies

Capital Allocation

Effectively

matched our

assets &

liabilities

21

D M A I C

Six Sigma literally means 3.4 defects per million opportunities

It is also means continual process improvement that is:

Customer focused

A disciplined approach to problem solving

How we got here

Operating Efficiencies

Six Sigma – Improving business performance

Berkshire Six Sigma…is the new way to think about how we do business.

Growth is a function of achieving performance excellence in all that we do.

Define, Measure, Analyze, Improve, Control

22

How we got here

Operating Efficiencies

2004

11 employees certified as Green Belts

Hired certified Black Belt for training

2005

Created customized materials for in-house training

9 additional Green Belt candidates in progress

Projects range from sales to marketing to recruiting

Culture

People

Growth

Asset Quality

Asset Liability

Efficiencies

Capital Allocation

Six Sigma – Deployment

36% ROI in 2004

$250,000 gross

savings

23

Efficiency through acquisition

How we got here

Operating Efficiencies

41%

518

636

289

347

Data Processing

24%

1,655

1,816

676

1,140

Occupancy

(18%)

2,120

1,996

705

1,291

Other

50%

590

759

336

423

Prof. Services

12,379

$7,172

Total

1Q05

10,582

$5,699

Combined

3Q05*

*Excludes expenses from operating new branches of $190,000, and merger

and conversion charges of $828,000.

37%

4,843

7,536

Total

52%

$2,837

$4,335

Salaries & Benefits

Savings

(% of

Woronoco

1Q05)

Woronoco

1Q05

Berkshire

1Q05

($000s)

Exceeded our

target cost

savings

Culture

People

Growth

Asset Quality

Asset Liability

Efficiencies

Capital Allocation

24

How we got here

Operating Efficiencies

Grow into infrastructure

64.55%

62.73%

60.66%

55.32%

2.89%

2.49%

2.25%

2.09%

50.00%

52.00%

54.00%

56.00%

58.00%

60.00%

62.00%

64.00%

66.00%

2002

2003

2004

3Q 05

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

Efficiency Ratio (1)

Non-Interest Expense/ Average Assets (2)

(1)

Exclusive of merger and conversion expenses, other non-recurring items, and amortization of intangible assets

(2)

Exclusive of merger and conversion expenses and other non-recurring items

Culture

People

Growth

Asset Quality

Asset Liability

Efficiencies

Capital Allocation

Operating efficiencies

key to turnaround

25

Stock buybacks

Repurchased 16.1% of outstanding stock 2002-2005

Over 1 million shares; average price: $25.49

Expansion

Woronoco

Non-interest income

Berkshire Financial Planning, Inc.

Two insurance agencies

De novo branches

How we got here

Strategic Capital Allocation

Returned capital

to shareholders &

invested for future

growth

Culture

People

Growth

Asset Quality

Asset Liability

Efficiencies

Capital Allocation

26

How we got here

Strategic Capital Allocation

Technology subsidiary

Nearly $500 thousand per year

pretax loss between 2001-2004

Divested in 2004

Sub-prime auto

Nearly $3.5 million net charge-offs

per year between 2000-2003

Divested in 2003

Meet income

standards or

gone

Culture

People

Growth

Asset Quality

Asset Liability

Efficiencies

Capital Allocation

Divested non-core assets

27

How we got here

Strategic Capital Allocation

Effectively

employed

excess capital

Culture

People

Growth

Asset Quality

Asset Liability

Efficiencies

Capital Allocation

28

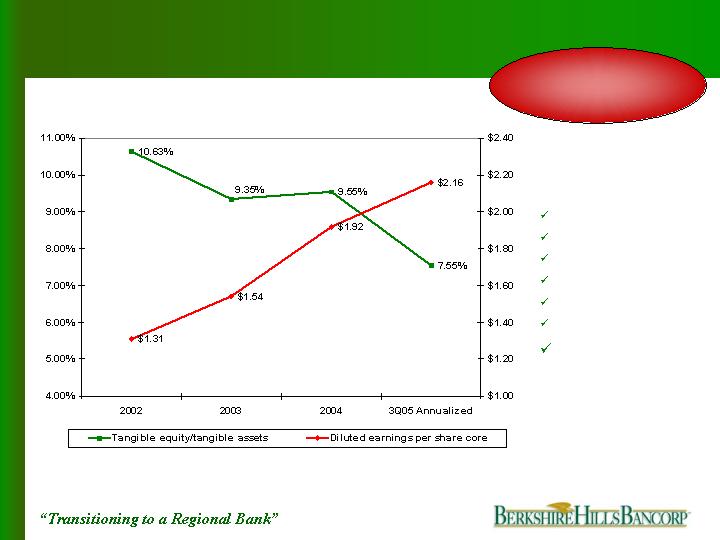

Where We Are Now

13.45

9.72

7.60

1.54

ROTE %

0.97

0.90

0.81

0.20

ROTA %

*Annualized

**All measures, except net interest margin, exclude non-recurring items, securities gains, and intangible

amortization. The non-interest expense to average assets includes intangible amortization.

8,988

2.49

62.73

3.61

7.61

0.81

2003

2.09

2.25

2.89

NI exp/average assets %

3Q05*

2004

2002

20,588

11,085

7,905

Core net income ($000s)

(excl. intangible amortization)

55.32

60.66

64.55

Efficiency ratio %

Key Measures**

3.31

3.37

4.18

Net interest margin (FTE)%

14.52

9.37

3.97

Core ROTE % (excl.

intangible amortization)

1.05

0.87

0.75

Core ROTA % (excl.

intangible amortization)

Successful

turnaround

Culture

People

Growth

Asset Quality

Asset Liability

Efficiencies

Capital Allocation

29

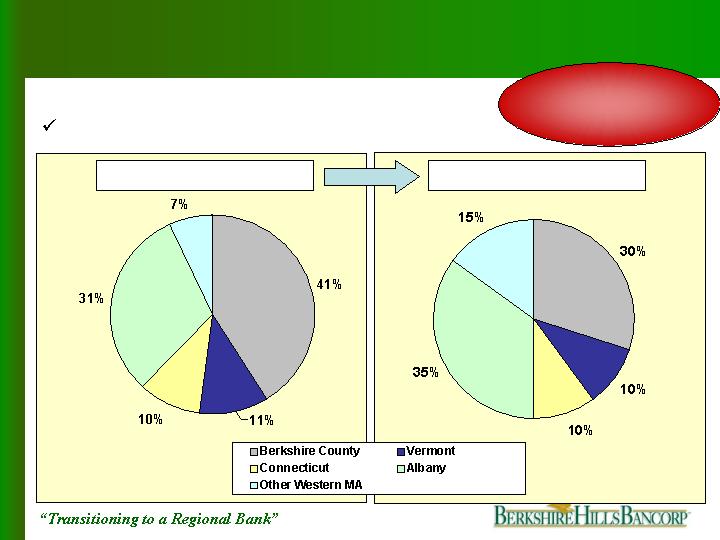

“Transitioning to a Regional Bank”

Where We Are Going

and

How We Will Get There

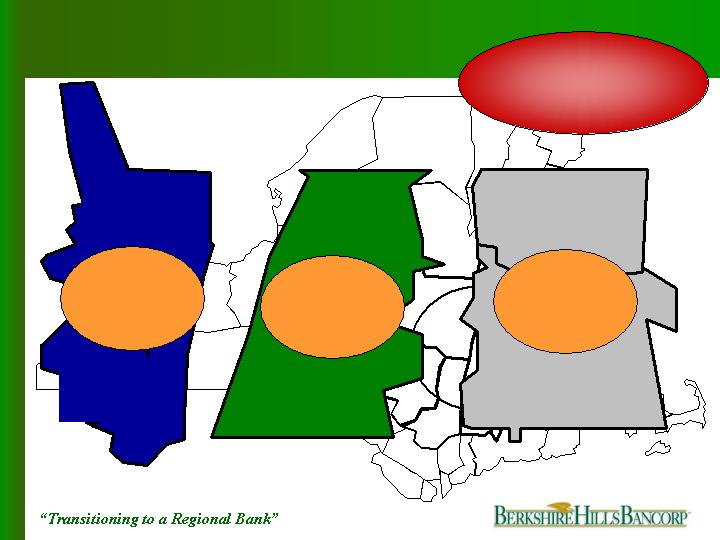

Regional Growth

Retail Banking

Deposit Gathering

Mortgage Lending

Consumer Lending

Commercial Banking

Wealth Management

Insurance

Financial Highlights

Corporate

Part III: 2005 - 2008

30

Where we are going

Regional Growth

Extend our

success beyond

Berkshire County

31

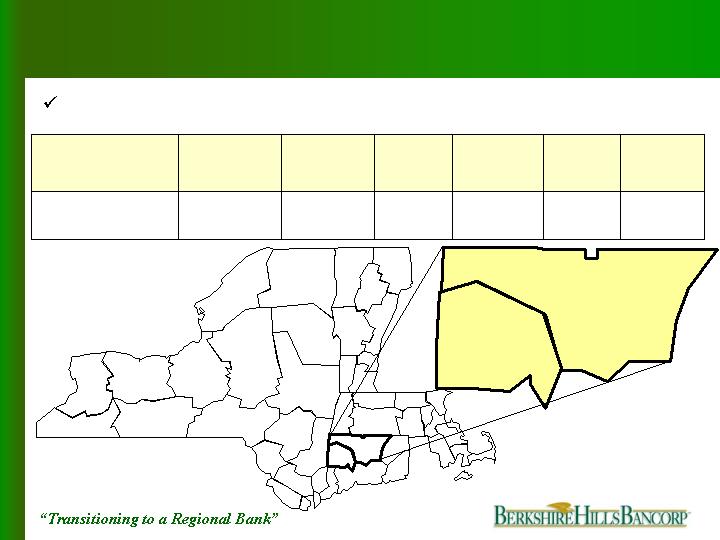

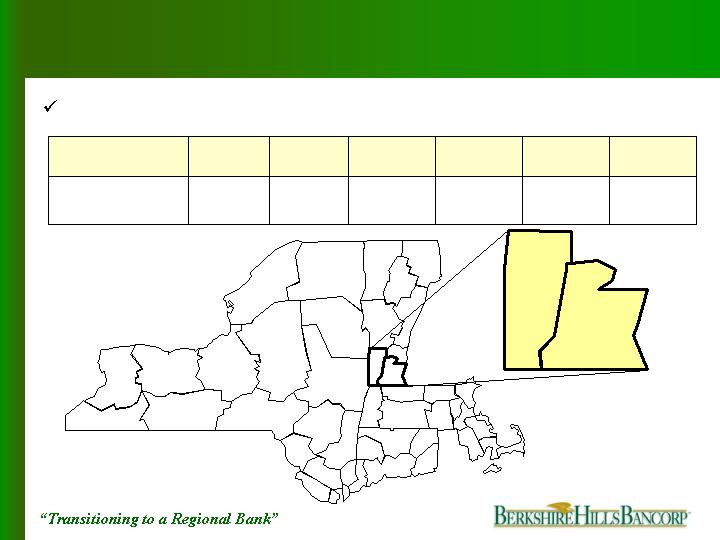

Where we are going

Competition

Regional bank

niche opportunity

Capital Region

Under $1.5 Billion

48 banks & CUs

$30 Billion +

6 - B of A, Citizens

HSBC, Key,

M&T, & Banknorth

$1.5 - $30 Billion

4 – First Niagara,

NBT, Trustco &

Berkshire Bank

Berkshire County

Under $1.5 Billion

19 banks & CUs

$30 Billion +

2- Citizens & Banknorth

$1.5 - $30 Billion

1 – Berkshire Bank

Pioneer Valley

Under $1.5 Billion

39 banks & CUs

$30 Billion +

4 – B of A, Citizens,

Sovereign & Banknorth

$1.5 - $30 Billion

2 – Chittenden &

Berkshire Bank

32

Retail Banking

Part III: 2005 - 2008

33

2,801

3,185

2,418

Population/ branch

$13.9

$9.1

$2.7

Deposits 6/05 (billions)

3.46%

2.23%

-1.65%

5 Year projected growth

$49,634

618

Pioneer

Valley

Capital

Region

Berkshire

County

$46,954

133

$51,351

818

Median HH income

Population (000s)

Regional growth opportunity

Where we are going

Retail Banking - Deposit Gathering

Opportunities in

contiguous markets

34

Where we are going

Retail Banking - Deposit Gathering

De novo branching

Double number of

branches by 2008

50

24

Total

11

11

Berkshire County

10

3

2005

18

Pioneer Valley

21

New York

2008

Projected Yr End

35

Where we are going

Retail Banking - Deposit Gathering

Strategy and goals

Maintain

Berkshire County

dominance

Branding

Centers of influence

Relentless calling effort

Municipal banking

Deposit insurance fund

Double Pioneer

Valley market

share

Gain 3% market

share in Capital

Region

36

Where we are going

Retail Banking - - Deposit Gathering

48%

$2,000

N/A

$1,348

Total

1066%

$338

<1%

$ 29

New York State

$748

$914

Projected

Deposits

2008

(millions)

4.6%

31.7%

Estimated

Market

Share

Projected

Growth

Through 2008

Deposits

9/05

(millions)

Market

$465

$854

61%

7%

Pioneer Valley

Berkshire County

Regional growth goals

90% of projected

growth from outside

Berkshire County

37

$4,000

$3,500

$800

Mortgage originations 2004

(millions)

3.46%

2.23%

-1.65%

5 Year projected growth

$49,634

618

Pioneer

Valley

Capital

Region

Berkshire

County

$46,954

133

$51,351

818

Median HH income

Population (000s)

Regional growth opportunity

Where we are going

Retail Banking – Mortgages

Opportunity in

contiguous markets

38

Where we are going

Retail Banking - Mortgages

42%

$781

N/A

$551

Total

327%

28%

23%

$141

$361

$291

.5%

2%

$33

12%

$282

Projected

Mortgages

2005-2008

(millions)

Estimated

Market Share

Projected

Growth

Through 2008

Mortgages

9/05

(millions)

Market

$236

Capital Region

Pioneer Valley

Berkshire County

Regional growth

42% three

year growth

39

Where we are going

Retail Banking - - Mortgages

Strategy and goals

Engage branch personnel

Triple outside origination staff

Capitalize on second home market and

metropolitan relocation

40

6%

Albany

8%

Pittsfield

17%

Springfield

21%

Boston

40%

Long Island

48%

Cape Cod

% Overvalued

Market

Overvalued Real Estate

* Source National City Bank 1st Qtr 2005

Credit risk partially protected from bubble

Where we are going

Retail Banking - Mortgages

41

Where we are going

Retail Banking - Mortgages

Portfolio protected

Interest only loans: None

Uninsured mortgages with LTV in excess

of 80%: None

Losses 2000 – 2005: None

Average LTV: 61%

Average FICO: 728

Delinquency 2005: .12%

Maintain credit

standards

42

Where we are going

Retail Banking – Consumer Lending

29%

$169

1.2%

$131

Total

360%

13%

20%

$23

$85

$61

.1%

5%

$5

12%

$75

Projected

Growth

2005-2008

(Millions)

Estimated

Market

Share

Projected

Growth

Through

2008

Equity

Loans 9/05

(Millions)

Market

$51

Capital Region

Pioneer Valley

Berkshire County

Equity Lines

Regional growth

29% three year

growth

43

Where we are going

Retail Banking - - Consumer Lending

Equity Lines

Maintain credit quality

HELOC

LTV in excess of 80%: None

Losses 2002 - 2005: None

Average FICO 2004-2005: 756

Average LTV: 55%

Delinquency 2005: .25%

44

Indirect Auto

Regional growth opportunity

Where we are going

Retail Banking - Consumer Lending

21%

15

73

Southern Vermont

34%

45

132

Capital Region

8%

94%

Penetration

10

34

Active BHLB

Dealers

# of Dealers

Market

122

36

Pioneer Valley

Berkshire County

Opportunity in

contiguous markets

45

Where are we going

Retail Banking – Consumer Lending

Indirect Auto

Regional growth goals

Absolutely no

subprime loans

3Q05 - $150 Million

2008 - $268 Million

79% growth

46

Where we are going

Retail Banking - - Consumer Lending

Strategy and goals

Advertise service

Benefit from Six Sigma principles

Answers in 30 minutes

Payments to dealers same day

Call program on high quality dealers

Utilization of branch network

Continue personal contact…people dealing with

people

Critical when accepting no subprime

47

Where we are going

Retail Banking - - Consumer Lending

Indirect Lending

Maintain credit quality

Sub-prime loans since 2001: None

Average FICO of portfolio: 715

Average 2005 FICO: 732

Delinquency 2005: .47%

Losses 2005: .42%

48

Where we are going

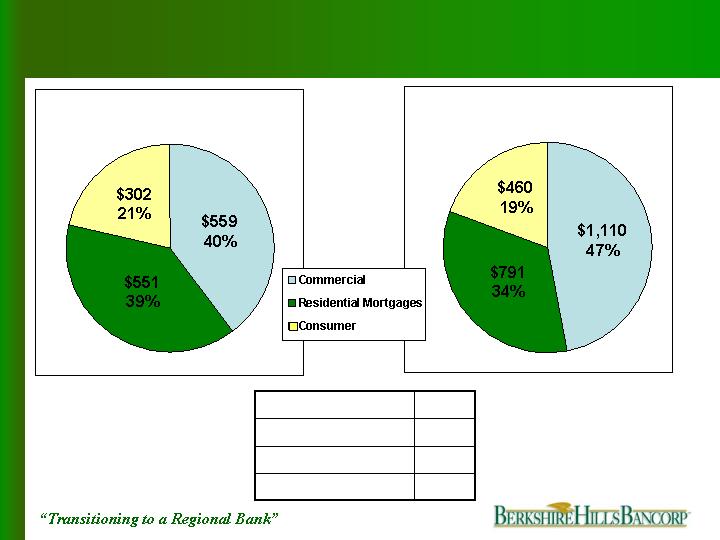

Retail Banking

$17,009

$3,213

$432

$781

$2,000

Projected

2008

25%

46%

43%

42%

48%

% Increase

$13,557

Pretax income

$2,201

Total

$302

$551

9/30/2005

Annualized

$1,348

Consumer loans

Mortgages

Deposits

Growth

Note: All numbers in millions except pretax income which is in thousands.

49

Commercial Banking

Part III: 2005 - 2008

50

Where we are going

Commercial Banking

Massachusetts

Why we have been successful

Not a priority for large banks

Smaller banks have been acquired

Mid-cap borrowers prefer local relationship

Community involvement leads to business

Corporate commitment to commercial banking

Growth plan

Maintain dominance in Berkshire County

Opportunity from Woronoco acquisition

Robust growth in Capital Region

Regional presence in adjacent markets with quality leadership

Consistent growth

51

Where we are going

Commercial Banking

Why the Capital Region

Lack of focus by larger banks

Tech Valley growth initiative

Demand for local bank presence

Capital Region

Ignored Market

52

What we have now

4 lenders with 125 years combined experience

$83 million loans, $44 million pipeline

Growth plan

Add 2 seasoned lenders by 3/31/2006

Add 2 lenders in 2007

Grow to $345 million by 2008

Where we are going

Commercial Banking

Capital Region

53

1%

3%

35%

BHLB estimated market share

83

121

355

BHLB commercial loans ($M)

47,926

32,216

7,781

Total business revenues ($M)

4,250

23,736

Pioneer

Valley

Capital

Region

Berkshire

County

1,025

6,984

6,300

31,434

Estimated commercial loans ($M)

Total businesses

How we will get there

Commercial Banking

Regional growth opportunity

Opportunity in

contiguous markets

54

Deposits

($billion)

Sales

($billion)

Businesses

Median

HH

Income

Projected

Growth

Population

(000s)

Market

$76.9

$7.7

$19.1

$2.7

50,207

6,984

2.74%

-1.65%

1,039

133

$60,534

$46,954

Northern Connecticut

Berkshire County

Potential growth in northern Connecticut

Where we are going

Commercial Banking

55

Deposits

($billion)

Sales

($billion)

Businesses

Median HH

Income

Projected

Growth

Population

(000s)

Market

$5.3

$7.7

$1.5

$2.7

5,241

6,984

1.07%

-1.65%

81

133

$43,769

$46,954

Southern Vermont

Berkshire County

Where we are going

Commercial Banking

Potential growth in southern Vermont

56

How we will get there

Commercial Banking

71%

$21,419

$12,492

Pretax income

98%

$1,109

$559

Totals

316%

127%

$345

$275

1%

3%

$489

Projected

Commercial

Loans 2008

(millions)

35%

Estimated

Current

Market Share

38%

Percentage

Increase

2005 - 2008

Commercial

Loans 9/05

(millions)

Market

$83

$121

$355

Capital Region

Pioneer Valley

Berkshire County

Regional growth goals

57

Wealth Management

Part III: 2005 - 2008

58

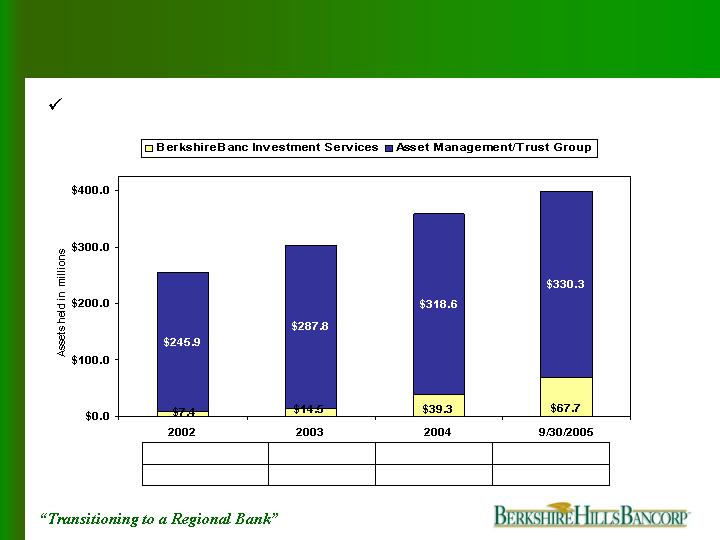

Where are we going

Wealth Management

11.2%

18.4%

19.3%

Annual growth rate

$397.9

$357.9

$302.3

$253.3

Assets under management

$253.3

$302.3

$357.9

$398.0

59

Where are we going

Wealth Management

Client centered/consultative wealth

management relationship

Financial planning platform with 5 CFPs

Investment management capabilities are not

outsourced

Credible investment results – 10 year history

Emphasis on personal investment management

Strategy and goals

Building momentum with

a proven process

60

Where are we going

Wealth Management

Peer comparison

Ranked 374th largest trust department out of 1,500

Ranked 12th largest in Massachusetts out of 35

departments

Ranked 9th (tied) nationally out of the largest 400

trust departments (fiduciary income as percent of

trust assets)

Favorable

peer comparison

2004

11%

21%

Growth in revenue

8%

11%

Growth in AUM

Peer Group

Berkshire Bank

61

How we will get there

Wealth Management

100%

$795

$398

Total

$186

$84

$525

Projected

AUM 2008

(millions)

<1%

<1%

19.7%

Estimated

Market

Share

Projected

Growth

Through 2008

AUM

9/30/05

(millions)

Market

$2

$23

$373

920%

265%

41%

Capital Region

Pioneer Valley

Berkshire County

Regional growth

62

How we will get there

Wealth Management

Regional growth

51.31

49.82

47.13

% of households $50K+

818

618

133

Population (000s)

$1.3

$23.3

$373.4

BHLB AUM (millions)

$14.8

$11.2

$2.4

Estimated market (billions)

23.95

Pioneer

Valley

Capital

Region

Berkshire

County

30.25

24.27

% of population 55+

63

Insurance

Part III: 2005 - 2008

64

Where are we going

Insurance – An Emerging Business

Referral source of over 400 people

Captive audience with existing customers

Qualified leads through lending activities

Additional lines of business

Life

Disability

Health

Expect 15-20% pretax profit margin within 3 years

Overview

65

Where are we going

Insurance

Strategy and goals

Key to our strategy

going forward

Percent of Revenues

25%

10%

5%

0%

Capital Region

Pioneer Valley

Berkshire County

Market

100%

0%

2005

85%

10%

2006

70%

20%

2007

45%

30%

2008

66

818

618

133

Population (000’s)

<0.1%

<1.0%

<0.1%

Market share

$774

$585

$172

Estimated insurance

revenue (millions)

23,736

Pioneer Valley

Capital Region

Berkshire

County

6,984

31,434

Businesses

Regional growth

How we will get there

Insurance

67

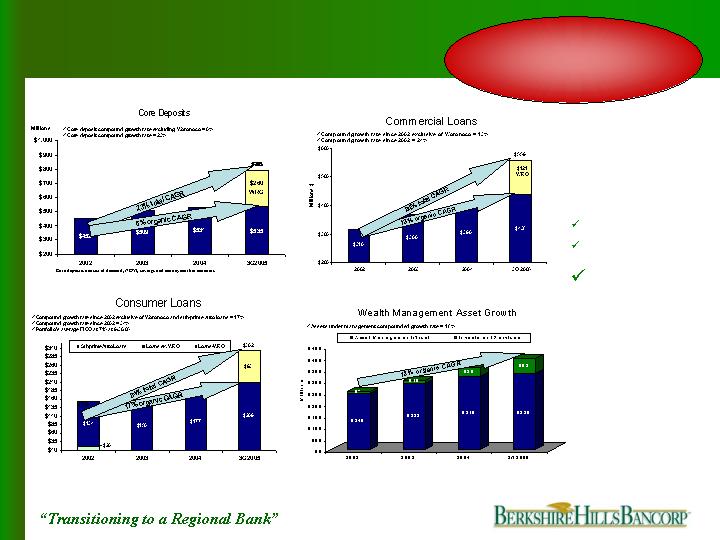

Financial Highlights

Part III: 2005 - 2008

68

17%

Total

14%

Consumer lending

12%

Residential mortgages

23%

Commercial

CAGR

Actual 9/30/05

(millions)

ProForma 12/31/08

(millions)

Financial Highlights

Loan Growth

69

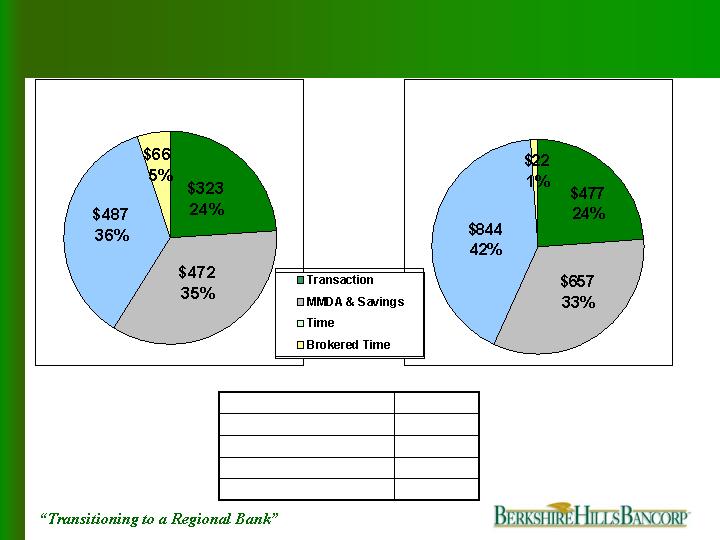

13%

Total

-29%

Brokered Time

18%

Time

11%

MMDA & Savings

13%

Transaction

CAGR

Financial Highlights

Deposit Growth

Actual 9/30/05

(millions)

ProForma 12/31/08

(millions)

70

Financial Highlights

Revenue Distribution

3rd Qtr 2005

ProForma 2008

13%

Total Revenues

16%

Sub total

20%

Wealth Mgmt & Ins

21%

Comm’l

13%

Retail

CAGR

71

Financial Highlights

Pretax Profit Distribution

3rd Qtr 2005

ProForma 2008

11%

Total Pretax Profit

14%

Sub-total

82%

Wealth Mgmt & Ins

18%

Comm’l

7%

Retail

CAGR

72

Financial Highlights

Service fee income

73

Remain well capitalized

Execute de novo branching and commercial banking strategy without

raising capital

Capital alternatives

Trust preferred

Subordinated debt

Financial Highlights

Capital Management

10.1%

10.9%

Total risk based capital (bank)

7.4%

7.3%

Tier 1 leverage capital (bank)

7.0%

7.6%

Tangible equity/assets

ProForma

12/31/08

9/30/2005

74

Wrap – Up

Strategic Highlights

Part III: 2005 - 2008

75

Wrap up

Strategic Highlights

Maintain focus on our strengths

Culture

People

Growth

Asset quality

Asset liability management

Operational efficiencies

Strategic capital allocation

76

Where we are going

Competition

Regional bank

niche opportunity

Capital Region

Under $1.5 Billion

48 banks & CUs

$30 Billion +

6 - B of A, Citizens

HSBC, Key,

M&T, & Banknorth

$1.5 - $30 Billion

4 – First Niagara,

NBT, Trustco &

Berkshire Bank

Berkshire County

Under $1.5 Billion

19 banks & CUs

$30 Billion +

2- Citizens & Banknorth

$1.5 - $30 Billion

1 – Berkshire Bank

Pioneer Valley

Under $1.5 Billion

39 banks & CUs

$30 Billion +

4 – B of A, Citizens,

Sovereign & Banknorth

$1.5 - $30 Billion

2 – Chittenden &

Berkshire Bank

77

Wrap up

Financial Highlights

1.02%

1.05%

Core ROTA

(excl. intangible amortization)

3.31%

55.32%

0.97%

14.52%

13.45%

Actual Q3 2005

Annualized

ProForma

FY 2008

3.49%

Net interest margin

57.62%

Efficiency ratio

1.00%

Return on tangible assets

14.54%

Core ROTE

(excl. intangible amortization)

14.15%

Return on tangible equity

78

Wrap up

Strategic Highlights

14.0%

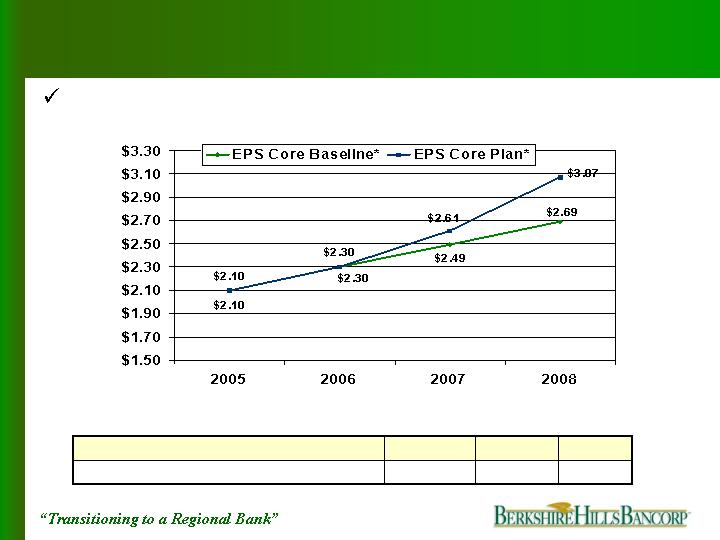

4.8%

0

Accretion/(Dilution) to core baseline

2008

2007

2006

Projected core EPS performance

*Exclusive of security gains and non-recurring expenses

79

Wrap up

Strategic Highlights

Summary

Significant

organic growth

Double branch

network size

Double

Commercial loans

Double size of

wealth management

Emerging

insurance

business

58% increase in

total fee income

48% increase in

deposits

43% increase in

consumer loans

42% increase in

mortgages

80

Banking as a Business

Lawrence A. Bossidy

Chairman

Michael P. Daly

President & Chief Executive Officer

New York City

December 1, 2005

81

Appendix

82

Appendix: Reconciliation of GAAP and Core Income

$1.31

$1.54

$1.92

$0.54

Diluted core earnings per share

$7,702

$8,785

$10,987

$4,743

Net core earnings

203

203

98

404

Add: Amortization of intangibles, net of tax

-

243

Add: Disallowance of the dividend received deduction on the Bank’s REIT

9,211

1,107

Add: Net losses and expenses on sale of sub-prime auto loans, net of tax

5,258

307

Add: Net other non-recurring, net of tax

$0.36

$1.57

$2.01

$0.54

Diluted earnings per share-GAAP

5,867

5,703

5,731

8,856

Average diluted shares outstanding (000s)

9,550

2,022

953

541

Less: Gain on the sale of securities, net of tax

$1.35

$1.58

$1.93

$0.58

Diluted core earnings per share, excluding intangible amortization

686

185

431

Add: Loss from discontinued operations -Sale of EastPoint Tech., net of tax

$7,905

$8,988

$11,085

$5,147

Net core earnings, excluding intangible amortization

-

$2,097

2002

-

$8,965

2003

-

538

Add: Merger and conversion-related expenses, net of tax

$11,509

$4,746

Net income

2004

3rd Qtr

2005

($000s) Except earnings per share

83