Michael P. Daly

President and Chief Executive Officer

NASDAQ : BHLB

www.berkshirebank.com

Cautionary Statement

Statements contained in this presentation contain forward-looking statements within the meaning of the

Private Securities Litigation Reform Act of 1995. These statements are based on the beliefs and

expectations of management as well as the assumptions made using information currently available to

management. Since these statements reflect the views of management concerning future events, these

statements involve risks, uncertainties and assumptions. These risks and uncertainties include among

others, changes in market interest rates and general and regional economic conditions, changes in

government regulations, changes in accounting principles and the quality or composition of the loan and

investment portfolios and other factors that may be described in Berkshire Hills Bancorp, Inc.’s quarterly

reports on Form 10-Q for the quarters ended March 31, June 30 and September 30 and in its 2005 annual

report on Form 10-K, each filed with the Securities and Exchange Commission, which are available at

the Securities and Exchange Commission’s internet website ( www.sec.gov) and to which reference is

hereby made. Therefore, actual future results may differ significantly from results discussed in the

forward-looking statements.

You are cautioned not to place undue reliance on any forward-looking statements, which speak

only as of January 9, 2007. Except as required by applicable law or regulation,

Berkshire Hills Bancorp, Inc. undertakes no obligation to update any forward-

looking statements, to reflect events or circumstances that occur

after January 9, 2007.

Please see appendix for GAAP and non-GAAP financial measures. Non-GAAP

financial measures are used by management to provide supplemental

analytical perspectives.

$2.2 billion in total assets (9/30/06)

$70 million in annual insurance premium volume (including recent agency

acquisitions)

$500 million in assets under management

$309 million market capitalization (9/30/06)

31 branches in Western MA and Eastern NY (including 4 announced)

Only locally headquartered regional bank in primary market

Largest bank in Western MA

Four state targeted footprint (MA, NY, CT, VT)

Strong growth based on organic, de novo and acquisition strategies

Diversified revenue sources with strong commercial components

Strengthening board and management team

Profile

Berkshire Hills Bancorp, Inc.

3

Deposit Growth – Total Deposits

($ Millions)

CAGR = 18%

$1,488

Core = 79%

of total

deposits

4

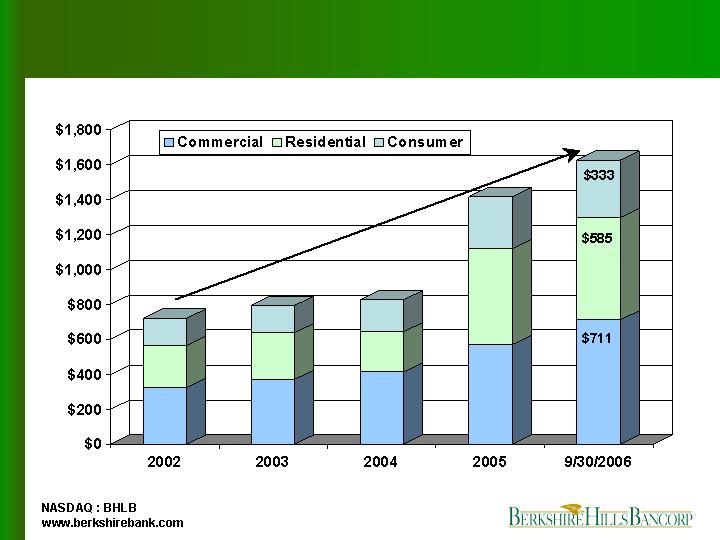

Loan Growth – Total Loans

($ Millions)

CAGR = 22%

$1,629

5

High Quality Loan Portfolio

(Period end ratios)

0.29%

0.31%

0.23%

0.28%

0.88%

Delinquents/

Total Loans

1.18%

0.92%

1.13%

1.13%

1.43%

Allowance/

Total Loans

0.08%

0.06%

2005

0.04%

0.15%

0.35%

0.87%

Net Charge-offs/

Average Loans

0.24%

0.09%

0.26%

0.36%

Non-performers/

Total Assets

9/30/2006

2004

2003

2002

Note: Delinquents are all accruing loans past due 30 days or more.

6

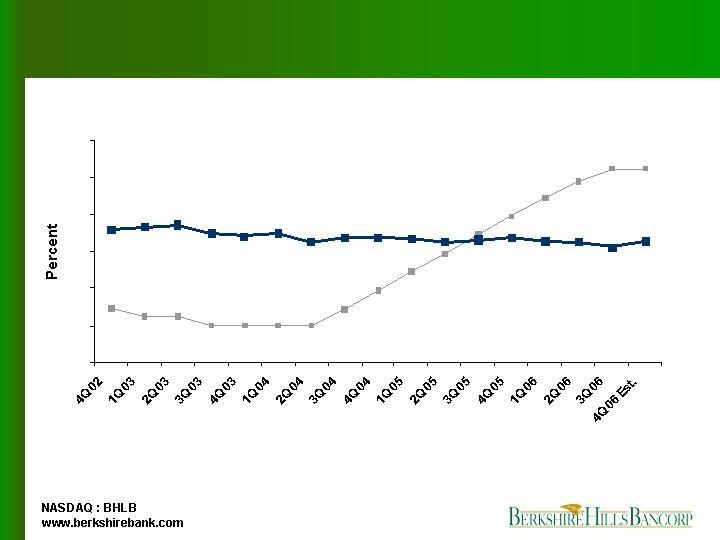

Net Interest Margin

3.27

0

1

2

3

4

5

6

Net Interest Margin

Fed Funds

*Note: Margin in 2Q06 and 3Q06 adjusted for delayed FHLBB dividend. Net

interest margin for 4Q06 based on guidance provided in October 2006.

7

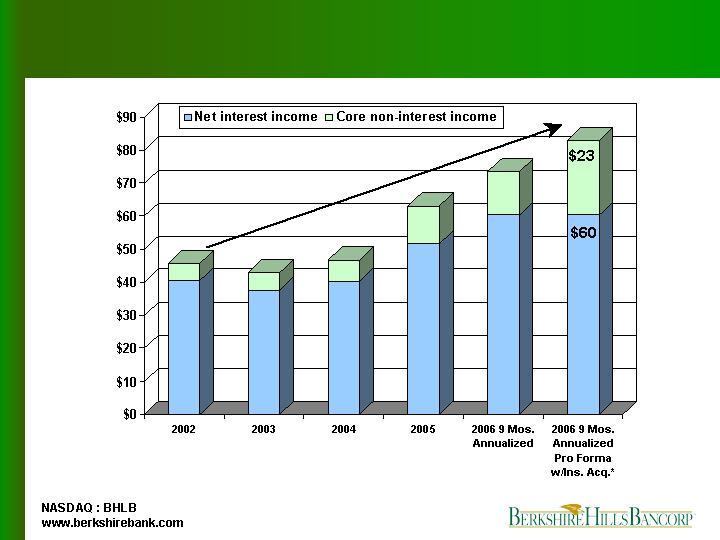

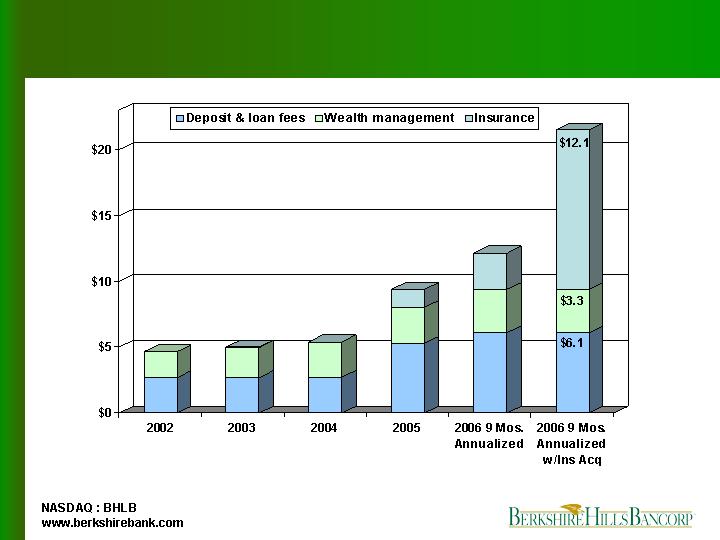

Core Operating Revenue

($ Millions)

CAGR = 16%

*Note: Pro forma is 9 months 2006 annualized plus pro forma

annualized revenues from insurance agencies acquired in 10/06

$83

8

9

Where We’re Headed

How we differentiate ourselves

Geographic expansion

Expansion of income streams

Broaden banking products

Improve profit metrics

10

How We Differentiate Ourselves

Enthusiastic and

focused teamwork

Culture

Six Sigma service

excellence, business

sense, productivity,

profitability

Process

Grow the “pool” of

customers and cross

sales

Relationships

Create exciting brand

experience

Brand

11

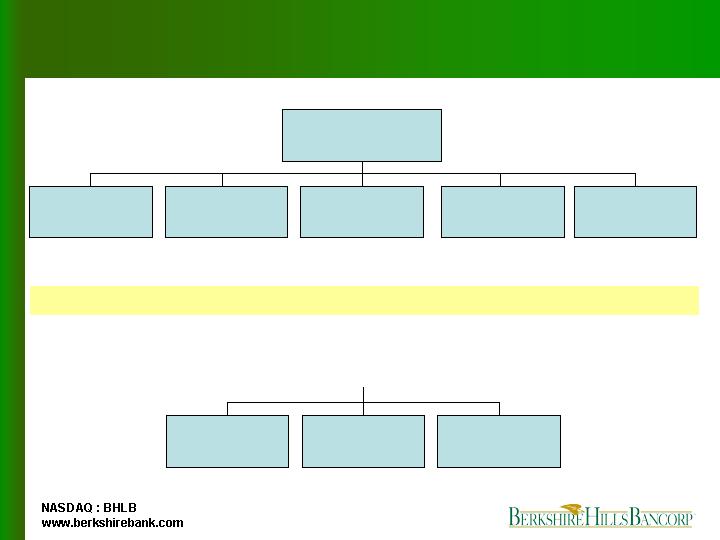

Organization Chart – CEO Reporting

Michael P. Daly

President and CEO

John Howard

EVP, Retail Banking

& Operations

Michael Oleksak

EVP, Commercial

Banking

Ross Gorman

CEO, Berkshire

Insurance Group

Shepard Rainie

SVP, Risk

Management

John Millet

SVP, Interim CFO

Thomas Barney

SVP, Wealth

Management

Linda Johnston

SVP, Human

Resources

Gerald Denmark

SVP, General

Counsel

New Hire CEO Reports

Existing CEO Reports

Hire date:

9/2006

Background:

Bank of America

Consumer Market Exec

Hire date:

2/2006

Background:

TD Banknorth

Co-Regional Exec

Hire date:

10/2006

Background:

Alliance Berkshire

President, MassOne

Hire date:

8/2006

Background:

Bank of America

Managing Director

Promo date:

12/2006

Background:

CPA,

President - Health

12

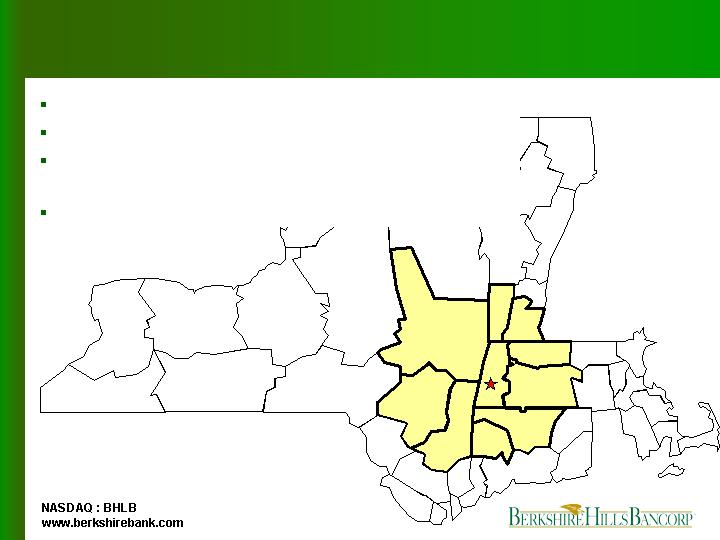

Regional Growth

Only regional bank headquartered in this market

Market area includes multi-state region

Building market share in attractive, under-served

markets

Regional population of 2.7 million

13

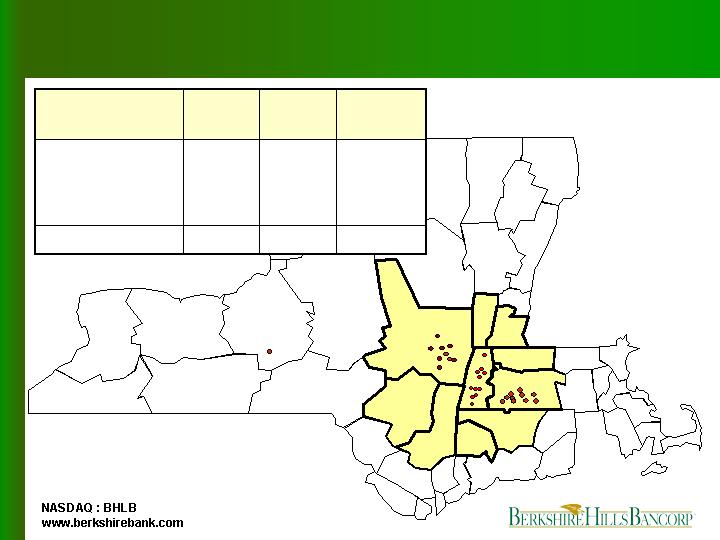

Branches

27

11

10

6

12/31/06

31

11

10

10

12/31/07

Proforma

24

Total

11

Berkshire County

10

3

12/31/05

Pioneer Valley

New York

Market

14

Fee Income

($ Millions)

*Note: Pro forma is 9 months 2006 annualized plus pro forma

annualized revenues from insurance agencies acquired in 10/06

$21.5

15

Insurance Acquisition

Berkshire Insurance Group, Inc.

$70 million annual premium volume

$12 million annual revenues

10 locations

100 employees

15% projected return on equity within

2 years

16

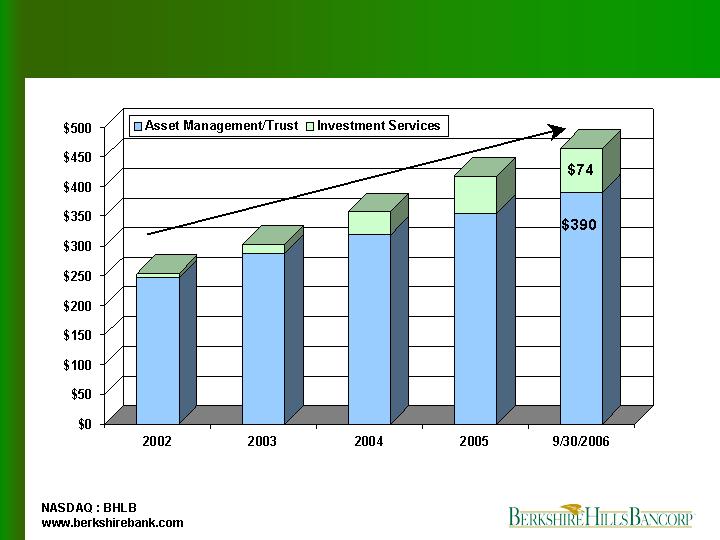

Wealth Management – Assets Under Management

($ Millions)

CAGR = 19%

$464

17

Product Expansion – Current Initiatives

Retail

Private banking

Home equity and mortgage enhancements

Health savings accounts

Remote capture

Commercial

Cash management

SBA lending program

Full follow asset based lending

Commercial real estate conduit

18

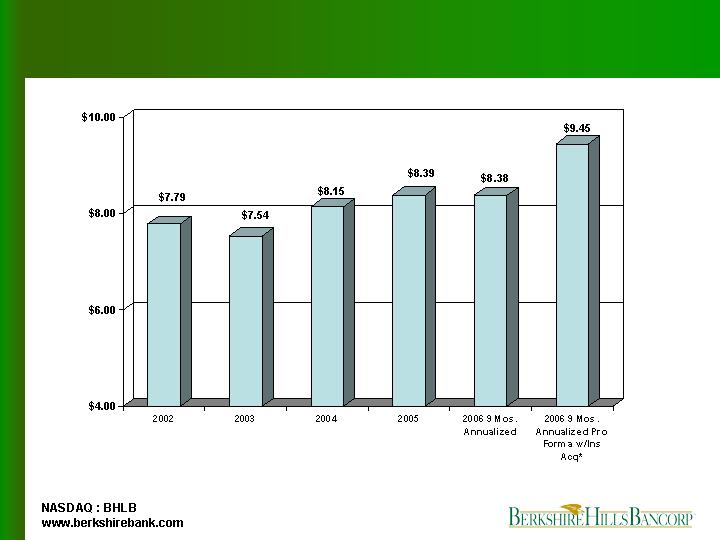

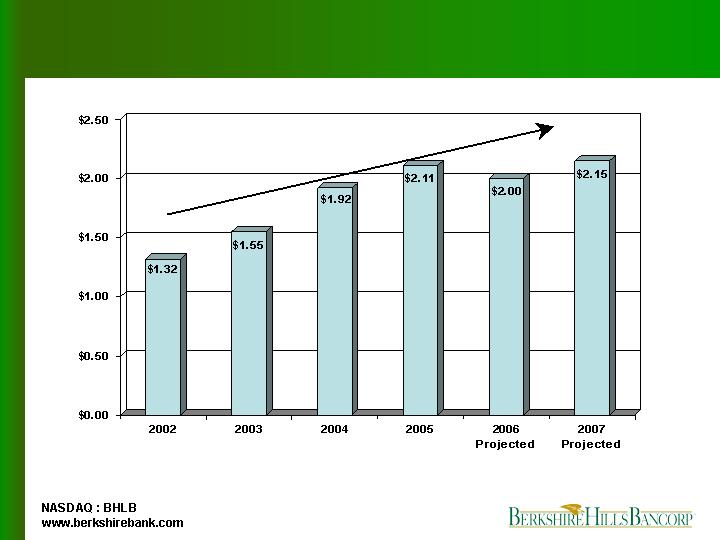

Core Operating Revenue per Share

*Note: Pro forma is 9 months 2006 annualized plus pro forma

annualized revenues from insurance agencies acquired in 10/06

19

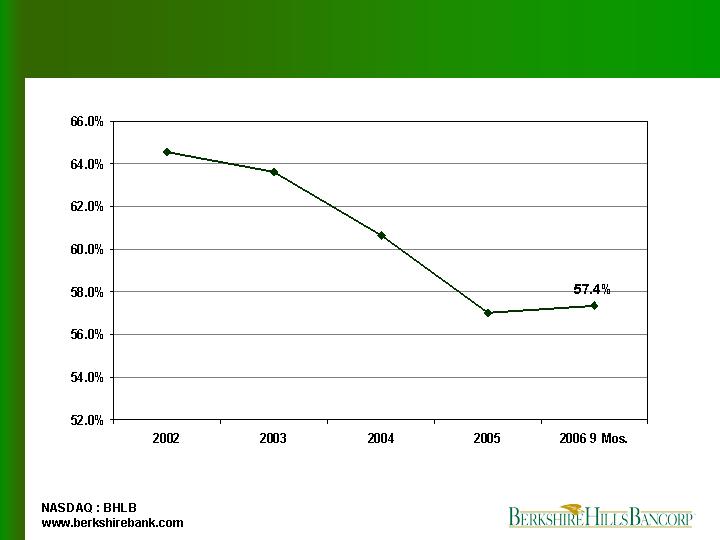

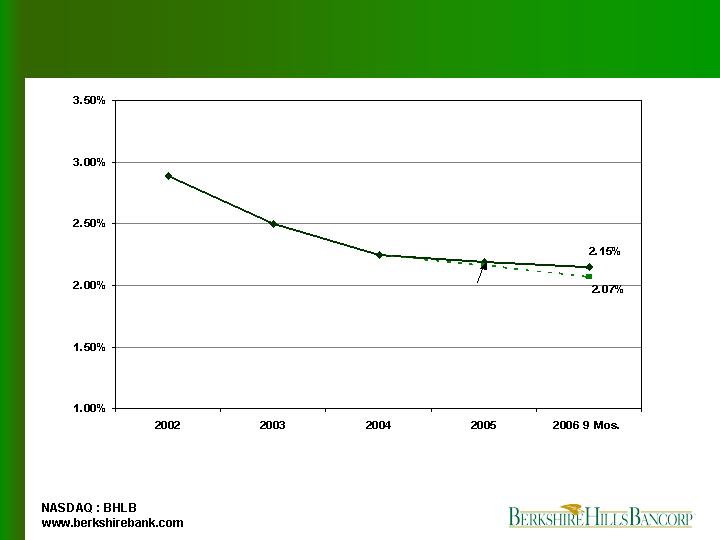

Efficiency Ratio

20

Core Non-interest Expense/Average Assets

Excluding de novo branch costs

*Note: Exclusive of merger and conversion expenses, other non-recurring items and amortization of intangible

assets. Costs of new branches were $1.28 million in the first nine months of 2006.

21

Core Earnings per Share

CAGR = 10%

*Note: Projections based on midpoint of December 2006 guidance.

22

Our Goals

Create nationally recognized brand and business style

Expand strong, high quality franchise through motivated

teamwork and relationship building

Take market share as a regional bank from national and

community competitors

Continue to generate strong top line growth from organic, de

novo, acquisition and product expansion

Achieve high performance profitability metrics

Produce attractive earnings growth and shareholder return

23

For questions, please contact:

David Gonci, Corporate Finance Officer

(413) 281-1973

dgonci@berkshirebank.com

NASDAQ : BHLB

www.berkshirebank.com

24

Appendix

25

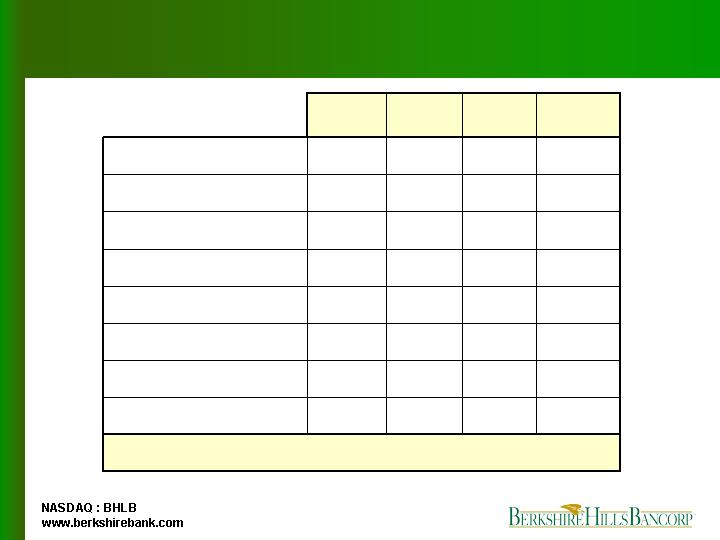

Key Measures

11.55

12.09

10.06

10.11

Equity/Assets %

Please see next slide for reconciliation of non-GAAP financial measures

7.41

7.56

9.55

9.35

Tangible equity/Assets %

57.35

57.03

60.66

63.64

Efficiency ratio %

3.22

3.33

3.37

3.61

Net interest margin (FTE) %

3.83

4.19

9.06

7.28

ROE %

12.26

12.30

9.36

7.97

Core tangible ROE %

0.47

0.95

2006

9 Mos.

0.47

0.89

0.80

ROA %

0.98

0.87

0.81

Core tangible ROA %

2005

2004

2003

26

Nine

(Dollars in thousands, except share data)

At and for the years ended December 31,

Months

2002

2003

2004

2005

2006

Net income

(A)

2,097

$

8,965

$

11,509

$

8,226

$

7,161

$

Less: Gain on sale of securities, net

(15,143)

(3,077)

(1,402)

(3,532)

4,054

Plus: Termination of ESOP

10,702

-

-

8,836

(576)

Plus: Merger and conversion expense

-

-

-

2,142

-

Plus: Sale of sub-prime auto loans

-

1,854

-

-

5,512

Plus: Other, net

9,155

754

653

385

Adj: Income taxes

962

360

261

133

(3,195)

Core income

(A1)

7,773

8,856

11,021

15,805

13,341

Plus: Amortization of intangible assets (net of taxes)

132

132

64

741

961

Tangible core income

(B)

7,905

$

8,988

$

11,085

$

16,546

$

14,302

$

Total non-interest income

6,427

$

6,448

$

7,764

$

14,923

$

6,217

$

Less: Gain on sale of securities, net

(15,143)

(3,077)

(1,402)

(3,532)

4,054

Plus: Other

13,704

2,060

-

-

Core non-interest income

(C)

4,988

5,431

6,362

11,391

10,271

Net interest income

40,700

37,566

40,357

51,617

44,669

Total core operating income

(C1)

45,688

$

42,997

$

46,719

$

63,008

$

54,940

$

Total non-interest expense

37,279

$

28,243

$

28,977

$

48,998

$

34,216

$

Less: Termination of ESOP

-

-

-

(8,836)

-

Less: Merger and conversion expense

-

-

-

(2,142)

Less: Other

(6,900)

(408)

-

-

(385)

Core non-interest expense

(D1)

30,379

27,835

28,977

38,020

33,831

Less: Amortization of intangible assets

(203)

(203)

(98)

(1,140)

(1,434)

Total core tangible non-interest expense

(D2)

30,176

$

27,632

$

28,879

$

36,880

$

32,397

$

Total average assets

(E)

1,051,800

$

1,115,800

$

1,289,500

$

1,745,200

$

2,105,000

$

Less: Average intangible assets

(10,300)

(10,300)

(8,700)

(62,000)

(99,000)

Total average tangible assets

(F)

1,041,500

$

1,105,500

$

1,280,800

$

1,683,200

$

2,006,000

$

Total average stockholders' equity

(G)

136,200

$

123,100

$

127,100

$

196,500

$

254,000

$

Less: Average intangible assets

(10,300)

(10,300)

(8,700)

(62,000)

(99,000)

Total average tangible stockholders' equity

(H)

125,900

$

112,800

$

118,400

$

134,500

$

155,000

$

Core return on tangible assets

(B/F)

0.76

%

0.81

%

0.87

%

0.98

%

0.95

%

Core return on tangible equity

(B/H)

6.28

7.97

9.36

12.30

12.26

Efficiency ratio

64.55

63.64

60.66

57.03

57.35

Total average diluted shares (in thousands)

(I)

5,867

5,703

5,731

7,503

8,776

Net income per diluted share

(A/I)

$0.36

$1.57

$2.01

$1.10

$0.82

Core income per diluted share

(A1/I)

$1.32

$1.55

$1.92

$2.11

$1.52

Efficiency Ratio is computed by dividing total tangible core non-interest expense by the sum of total net interest income on a fully taxable equivalent basis and

total core non-interest income. The Company uses this common non-GAAP measure to provide important information regarding its operational efficiency.

BERKSHIRE HILLS BANCORP, INC. AND SUBSIDIARIES

RECONCILIATION OF NON-GAAP FINANCIAL MEASURES

27