Exhibit 99.1

November 2016 Berkshire Hills Bancorp Investor Presentation

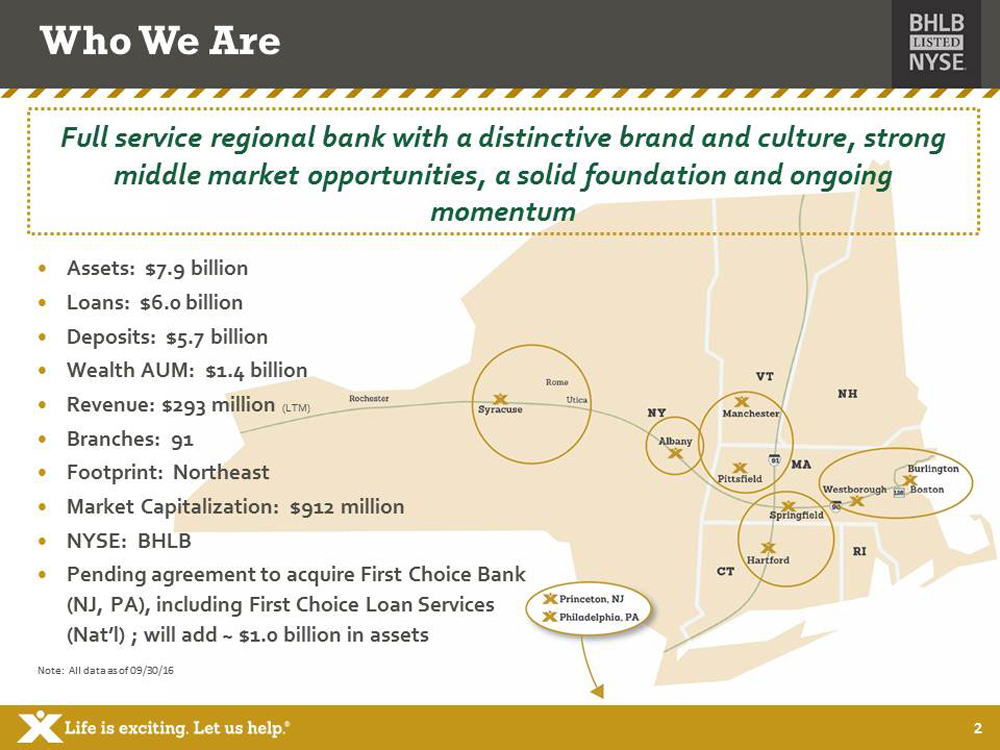

Assets: $7.9 billion Loans: $ 6.0 billion Deposits: $ 5.7 billion Wealth AUM: $1.4 billion Revenue : $293 million (LTM) Branches: 91 Footprint: Northeast Market Capitalization: $ 912 million NYSE: BHLB Pending agreement to acquire First Choice Bank (NJ, PA ), including First Choice Loan Services (Nat’l) ; will add ~ $1.0 billion in assets 2 Note: All data as of 09/30/16 Who We Are Full service regional bank with a distinctive brand and culture, strong middle market opportunities, a solid foundation and ongoing momentum

Why Berkshire? Strong momentum and improving profitability Diversified revenue drivers and controlled expenses Footprint positioned in attractive markets AMEB culture – results driven Acquisition disciplines a strength in a consolidating market 3

4 3Q16 Strategic Highlights • CORE EPS: $0.57 ; GAAP EPS: $0.53 • Net revenue increase: 7% Q/Q • Commercial loan growth: 6 % annualized Q/Q • Deposit growth: 7% annualized Q/Q • 17% increase in fee income Q/Q • Core ROTE: 13.0% ; ROE: 7.3% • Efficiency Ratio: 57.9% • Notable ROA improvement • Demonstrating positive operating leverage • #1 SBA Lender in Connecticut, Western Massachusetts, Vermont, and Capital and Central District’s of New York • Announced Congress St branch in Boston to open early 2017 Note: Non - GAAP measures of core EPS, Core ROTE, and efficiency reconciled in 3Q16 earnings release

5 Strong Earnings Momentum $236 $266 $296 $ 1.80 $2.09 $2.19 $1.36 $1.73 $2.09 $1.25 $1.45 $1.65 $1.85 $2.05 $2.25 $2.45 $100 $120 $140 $160 $180 $200 $220 $240 $260 $280 $300 2014 2015 9M16 Revenue Core EPS EPS $ Millions (annualized) 24 % EPS CAGR 10% Core EPS CAGR 12% Revenue CAGR Note: All CAGR comparisons are 9M16 annualized/ FY14

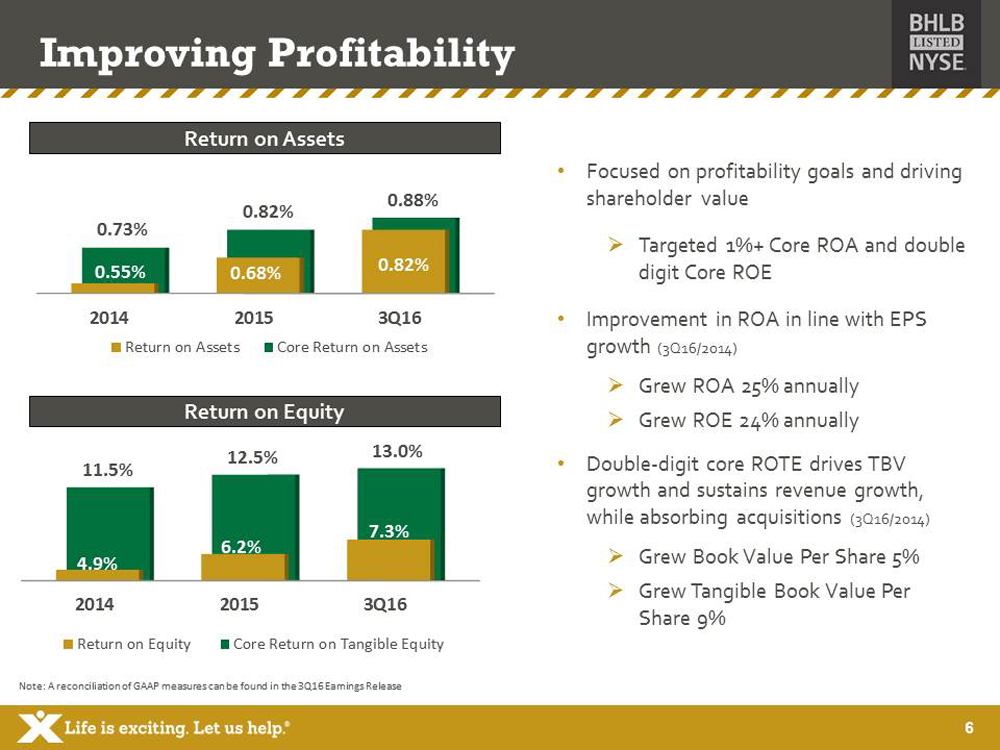

6 Improving Profitability 2014 2015 3Q16 0.55% 0.68% 0.82% 0.73% 0.82% 0.88% Return on Assets Core Return on Assets Note: A reconciliation of GAAP measures can be found in the 3Q16 Earnings Release 2014 2015 3Q16 4.9% 6.2% 7.3% 11.5% 12.5% 13.0% Return on Equity Core Return on Tangible Equity • Focused on profitability goals and driving shareholder value » Targeted 1%+ Core ROA and double digit Core ROE • Improvement in ROA in line with EPS growth (3Q16/2014) » Grew ROA 25% annually » Grew ROE 24% annually • Double - digit core ROTE drives TBV growth and sustains revenue growth, while absorbing acquisitions (3Q16/2014) » Grew Book Value Per Share 5% » Grew Tangible Book Value Per Share 9% Return on Assets Return on Equity

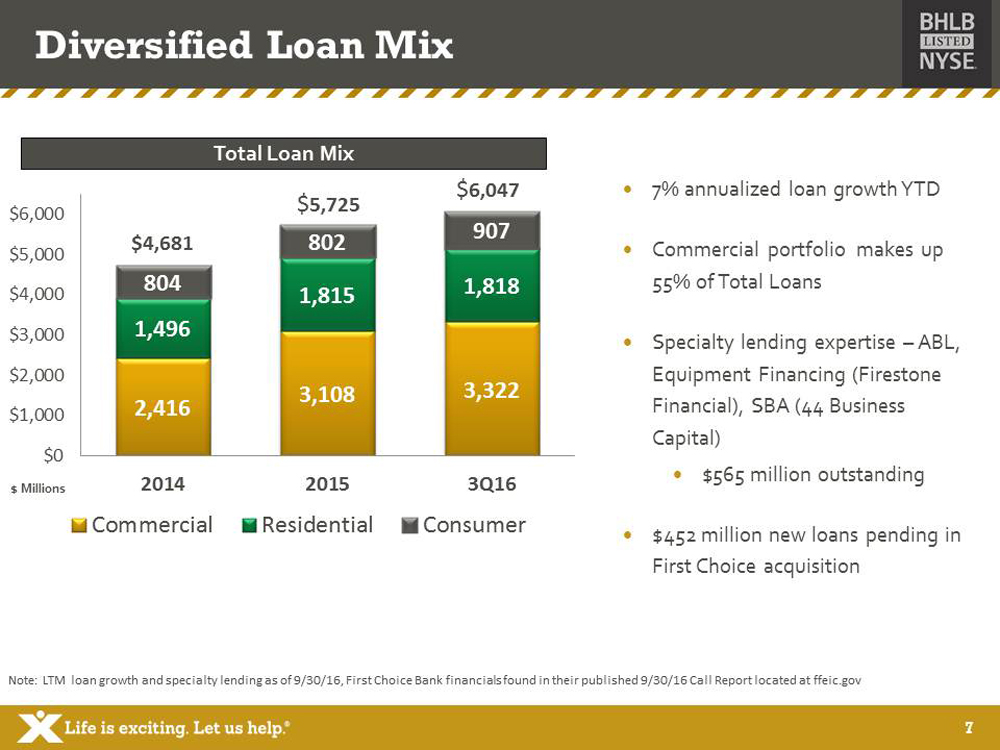

7 Diversified Loan Mix Note: LTM loan growth and specialty lending as of 9/30/16, First Choice Bank financials found in their published 9/30/16 Call Report located at ffeic.gov 2,416 3,108 3,322 1,496 1,815 1,818 804 802 907 $0 $1,000 $2,000 $3,000 $4,000 $5,000 $6,000 2014 2015 3Q16 Commercial Residential Consumer $ Millions 7% annualized loan growth YTD Commercial portfolio makes up 55% of Total Loans Specialty lending expertise – ABL, Equipment Financing (Firestone Financial), SBA (44 Business Capital) $565 million outstanding $452 million new loans pending in First Choice acquisition Total Loan Mix $4,681 $ 5,725 $ 6,047

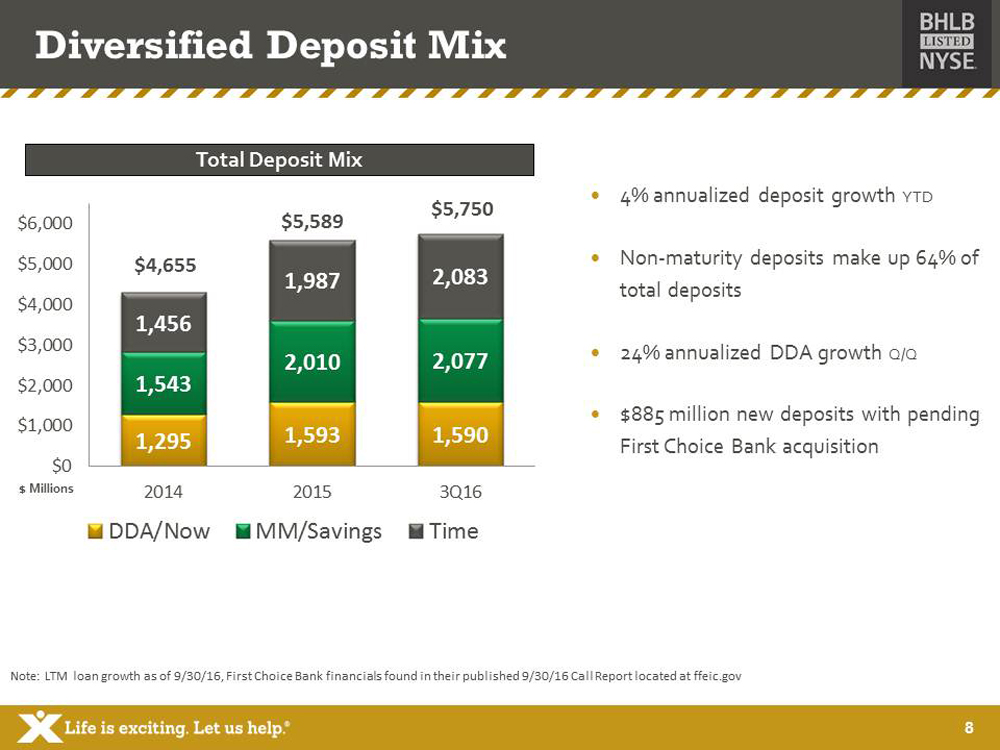

8 Diversified Deposit Mix 1,295 1,593 1,590 1,543 2,010 2,077 1,456 1,987 2,083 $0 $1,000 $2,000 $3,000 $4,000 $5,000 $6,000 2014 2015 3Q16 DDA/Now MM/Savings Time $ Millions 4% annualized deposit growth YTD Non - maturity deposits make up 64% of total deposits 24% annualized DDA growth Q/Q $ 885 million new deposits with pending First Choice Bank acquisition Note: LTM loan growth as of 9/30/16, First Choice Bank financials found in their published 9/30/16 Call Report located at ffeic.gov Total Deposit Mix $4,655 $5,589 $5,750

9 Loan 23% Mortgage Banking 8% Deposit 38% Insurance 17% Wealth Management 14% Focused on Diversifying Fee Revenue Fee Revenue Mix • Total fee income up 17% Q/Q • Focused on revenue diversification • Well positioned for expanded opportunities across lines of business • 44 Business Capital SBA team contributing $1MM+ in quarterly fee revenue • First Choice Bank acquisition expected to drive fee income to total revenue ratio north of 30% Note: All data as of 09/30/2016

10 Driving Fee Income Growth 6,328 8,310 14,728 2,561 4,133 5,357 24,635 25,084 24,904 10,364 10,251 10,872 9,546 9,702 9,341 $0 $10,000 $20,000 $30,000 $40,000 $50,000 $60,000 $70,000 2014 2015 9M16 Loan Related Mortgage Banking Deposit Related Insurance Wealth Management $ Thousands (Annualized) Fee Revenue Mix • Fee revenue as a percentage of total net revenue grew from 20% at 4Q15 to 24% in 3Q16 • Loan related fee income includes SBA sales, swap fee income, ABL fees, seasoned loan sales, and syndication fees • Total Wealth Assets Under Management: $1.4 billion (3Q16) ; an 8% improvement from $1.3 billion at 4Q13 $53,434 $57,480 $65,203

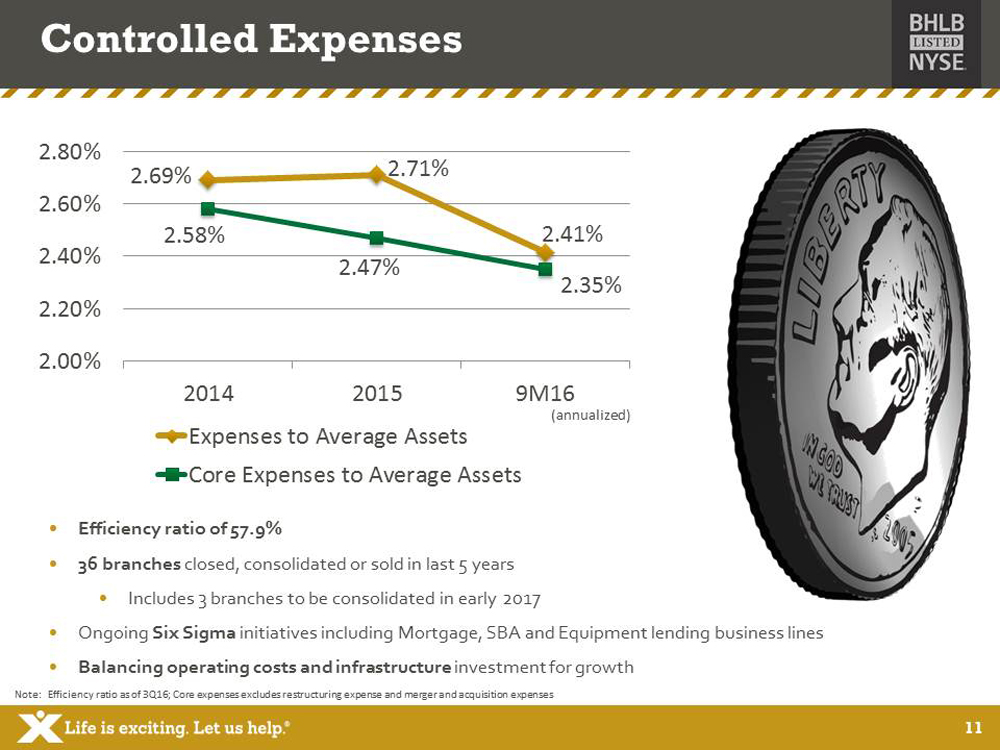

11 Controlled Expenses Efficiency ratio of 57.9% 36 branches closed, consolidated or sold in last 5 years Includes 3 branches to be consolidated in early 2017 Ongoing Six Sigma initiatives including Mortgage, SBA and Equipment lending business lines Balancing operating costs and infrastructure i nvestment for growth 2.69% 2.71% 2.41% 2.58% 2.47% 2.35% 2.00% 2.20% 2.40% 2.60% 2.80% 2014 2015 9M16 Expenses to Average Assets Core Expenses to Average Assets Note: Efficiency ratio as of 3Q16; Core expenses excludes restructuring expense and merger and acquisition expenses (annualized)

12 Strong Credit Quality 0.29% 0.25% 0.20% 0.37% 0.29% 0.26% 0.00% 0.10% 0.20% 0.30% 0.40% 0.50% 0.60% 0.70% 2014 2015 3Q16 NCO/Avg Loans NPA/Assets • Disciplined credit standards • Continued improvement in overall credit quality • 209% ALLL to Non - accrual loans (3Q16) Asset Quality Metrics

13 AMEB Culture – Results Driven RIGHT core values – Respect, Integrity, Guts, Having Fun and Teamwork Talent recruitment drives growth Engaging and innovative customer experience Driven to make a difference Community focused People, Attitude and Energy

14 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 Acquired Woronoco Bancorp, Inc. 6/1/2005 Assets: $898MM MA Acquired 6 independent insurance agencies 2006 MA Acquired Factory Point Bancorp, Inc. 9/21/2007 Assets: $339MM VT Acquired Rome Bancorp, Inc. 4/1/2011 Assets: $330MM NY Acquired Legacy Bancorp, Inc. 7/21/2011 Assets: $972MM MA Acquired Greenpark Mortgage Corporation 4/30/2012 Assets: $48MM MA/Northeast Acquired Connecticut Bank and Trust Company 4/20/2012 Assets: $283MM CT Acquired 20 branches from Bank of America 1/17/2014 Deposits: $440MM NY Acquired Beacon Federal Bancorp, Inc. 10/19/2012 Assets: $1,024MM NY Acquired Firestone Financial Corporation 8/7/2015 Assets: $192MM MA/Nat’l Acquired 44 Business Capital, LLC 4/29/2016 Assets: $40MM PA/Mid - Atlantic Announced agreement to acquire First Choice Bank 6/27/2016 Assets: $1,100MM NJ Acquired Hampden Bancorp, Inc 4/17/2015 Assets: $706MM MA • Successful acquisition integration a core competency for Berkshire ◦ 7 whole banks, 3 specialty finance companies, 6 insurance agencies and 1 branch deal closed since 2005 Proven Acquirer and Integrator

15 Financially attractive acquisition that immediately improves earnings, profitability, capital and liquidity ratios and further diversifies sources of revenue Upgrades and enhances Berkshire’s existing residential mortgage business with a nationally recognized “best in class” platform Provides entry into the demographically attractive Princeton, New Jersey and Greater Philadelphia banking markets Contributes an established banking franchise to complement Berkshire’s existing 44 Business Capital SBA lending team in Philadelphia First Choice Bank Acquisition

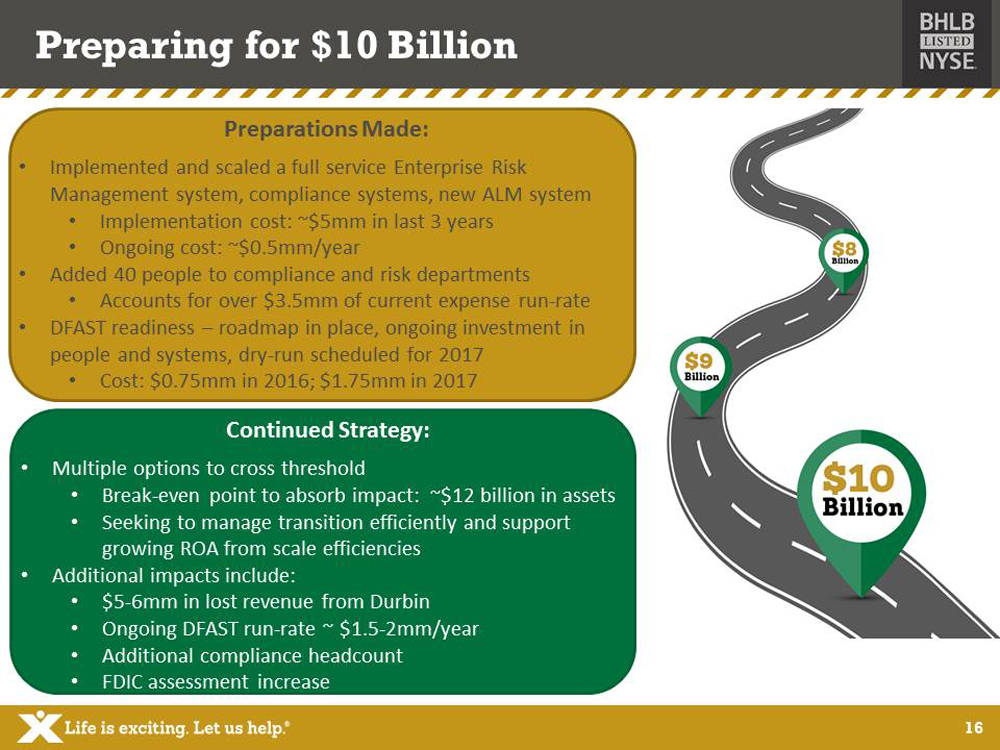

16 Preparations Made: • Implemented and scaled a full service Enterprise Risk Management system, compliance systems, new ALM system • Implementation cost: ~$5mm in last 3 years • Ongoing cost: ~$0.5mm/year • Added 40 people to compliance and risk departments • Accounts for over $3.5mm of current expense run - rate • DFAST readiness – roadmap in place, ongoing investment in people and systems, dry - run scheduled for 2017 • Cost: $0.75mm in 2016; $1.75mm in 2017 Preparing for $10 Billion Continued Strategy: • Multiple options to cross threshold • Break - even point to absorb impact: ~$12 billion in assets • Seeking to manage transition efficiently and support growing ROA from scale efficiencies • Additional impacts include: • $5 - 6mm in lost revenue from Durbin • Ongoing DFAST run - rate ~ $1.5 - 2mm/year • Additional compliance headcount • FDIC assessment increase

17 FY17 Guidance 2017 – Driving Profitability and Fee Revenue » Continued progress towards 1% ROA » Deepening and diversifying revenue sources 5 - 7% Core EPS growth Revenue growth driven by balance sheet expansion and fee sources » Minimal margin compression expected, assuming a flat rate environment Loan and deposit growth low - to - mid single digits Tax rate between 25 - 30% for next two years Disciplined M&A integration in expanding markets Note: Guidance issued on October 25, 2016. GAAP guidance is not provided for FY17 due to the uncertainty of the exact timing fo r the First Choice Bank noncore merger charges.

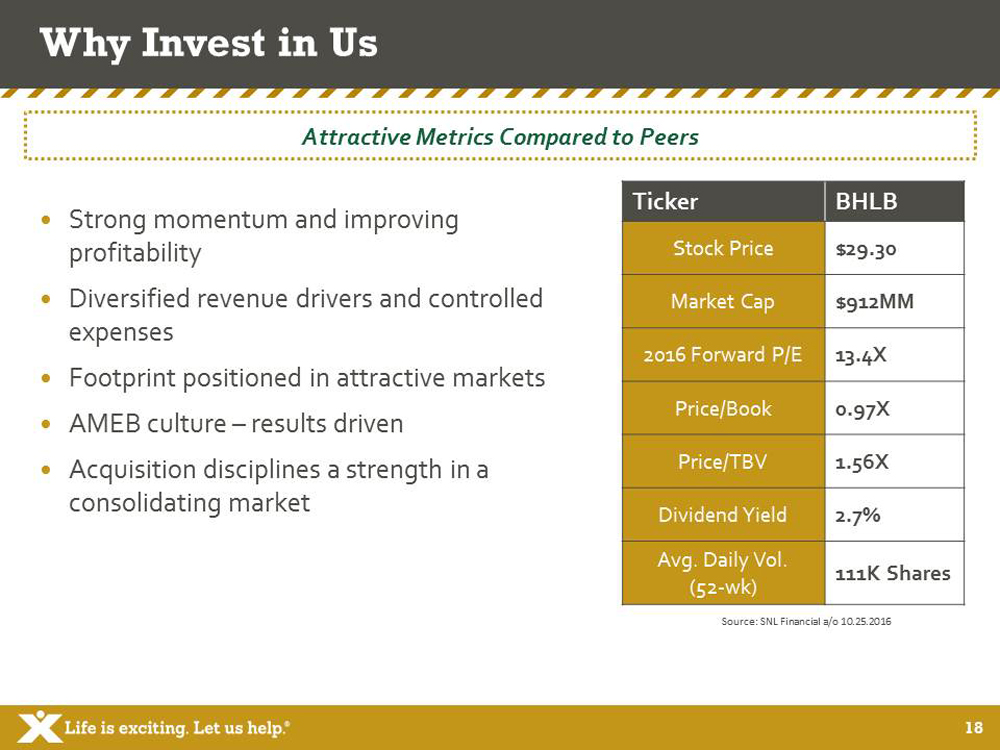

18 Why Invest in Us Strong momentum and improving profitability Diversified revenue drivers and controlled expenses Footprint positioned in attractive markets AMEB culture – results driven Acquisition disciplines a strength in a consolidating market Source: SNL Financial a/o 10.25.2016 Ticker BHLB Stock Price $29.30 Market Cap $912MM 2016 Forward P/E 13.4X Price/Book 0.97X Price/TBV 1.56X Dividend Yield 2.7% Avg. Daily Vol. (52 - wk) 111K Shares Attractive Metrics Compared to Peers

19 Loan and Deposit Mix Redefining Customer Experience Tax Credit Program Acquisition Discipline and Integration Experience Berkshire Franchise Overview Disclosures Appendix

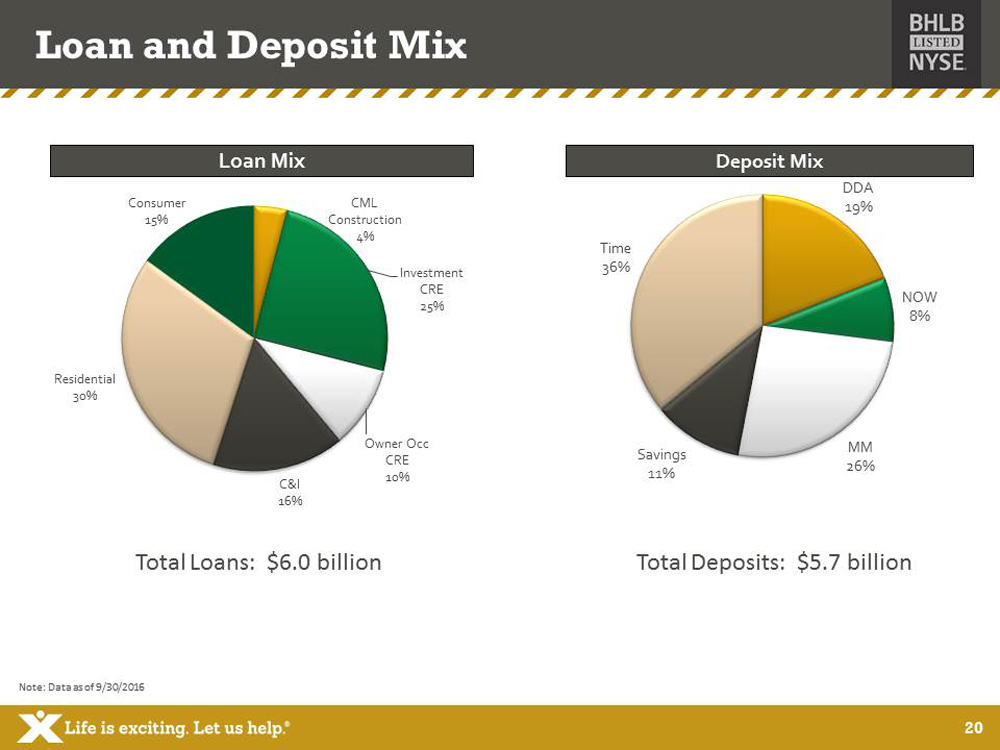

20 Loan and Deposit Mix Deposit Mix DDA 19% NOW 8% MM 26% Savings 11% Time 36% CML Construction 4% Investment CRE 25% Owner Occ CRE 10% C&I 16% Residential 30% Consumer 15% Loan Mix Total Loans: $6.0 billion Total Deposits: $5.7 billion Note: Data as of 9/30/2016

21 Redefining Customer Engagement Engaging Branches o Friendlier pods replace teller lines o Automated cash handling – lowers cost and improves customer engagement o Community rooms bring in traffic o Universal bankers create one stop shop for personal banking and insurance needs o Real time interactive customer feedback tool located in branches o Instant issue debit cards available in branches for account holders o Virtual Teller available beginning late 2016 in select branches » All transactions video teller assisted » Available 7 days a week with extended hours Virtual / Alternative o Sophisticated o nline and mobile platforms complement storefronts o MyBanke r travels to customer o State of the art call center o Enhanced online security o Apple Pay® capabilities for deposit customers o Customer support via Text AMEB1

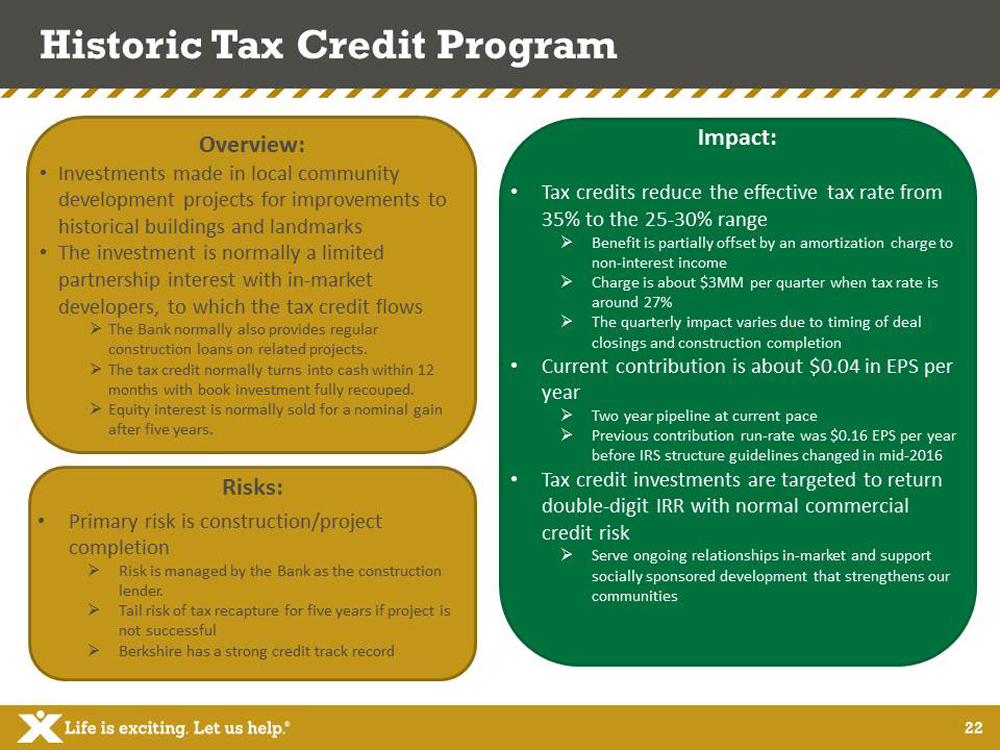

22 Risks: • Primary risk is construction/project completion » Risk is managed by the Bank as the construction lender. » Tail risk of tax recapture for five years if project is not successful » Berkshire has a strong credit track record Overview: • Investments made in local community development projects for improvements to historical buildings and landmarks • The investment is normally a limited partnership interest with in - market developers, to which the tax credit flows » The Bank normally also provides regular construction loans on related projects. » The tax credit normally turns into cash within 12 months with book investment fully recouped. » Equity interest is normally sold for a nominal gain after five years. Historic Tax Credit Program Impact: • Tax credits reduce the effective tax rate from 35% to the 25 - 30% range » Benefit is partially offset by an amortization charge to non - interest income » Charge is about $3MM per quarter when tax rate is around 27% » The quarterly impact varies due to timing of deal closings and construction completion • Current contribution is about $0.04 in EPS per year » Two year pipeline at current pace » Previous contribution run - rate was $0.16 EPS per year before IRS structure guidelines changed in mid - 2016 • Tax credit investments are targeted to return double - digit IRR with normal commercial credit risk » Serve ongoing relationships in - market and support socially sponsored development that strengthens our communities

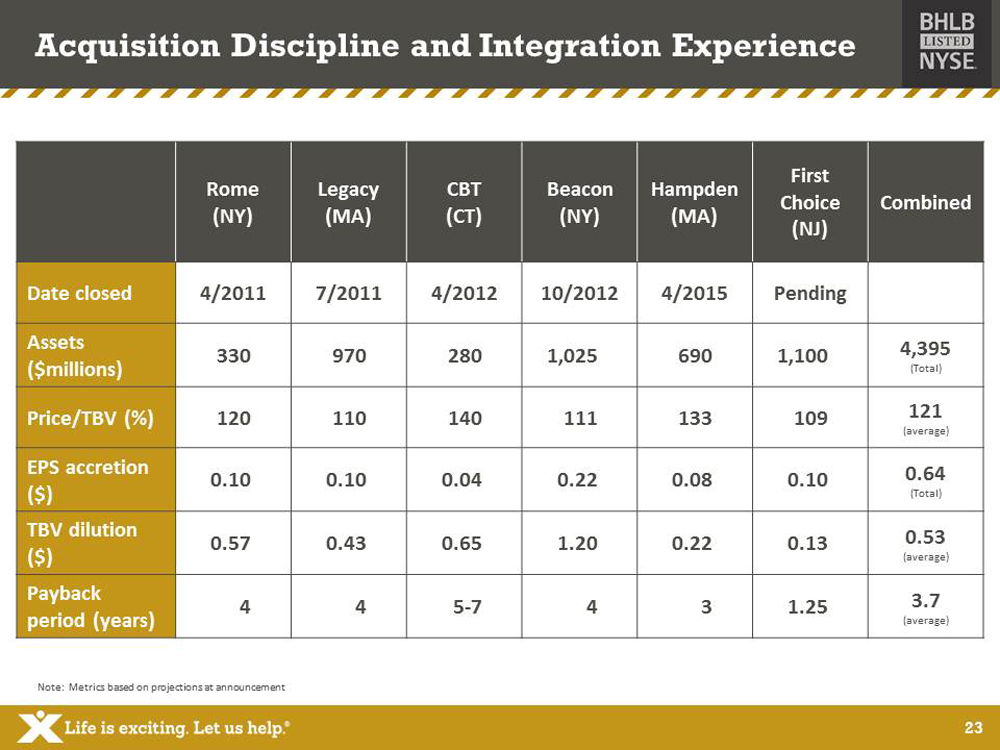

23 Rome (NY) Legacy (MA) CBT (CT) Beacon (NY) Hampden (MA) First Choice (NJ) Combined Date closed 4/2011 7/2011 4/2012 10/2012 4/2015 Pending Assets ($millions) 330 970 280 1,025 690 1,100 4,395 (Total) Price/TBV (%) 120 110 140 111 133 109 121 (average) EPS accretion ($ ) 0.10 0.10 0.04 0.22 0.08 0.10 0.64 (Total) TBV dilution ($) 0.57 0.43 0.65 1.20 0.22 0.13 0.53 (average) Payback period (years) 4 4 5 - 7 4 3 1.25 3.7 (average) Acquisition Discipline and Integration Experience Note: Metrics based on projections at announcement

24 Eastern MA – Greater Boston • Two branches and three lending offices located in Eastern MA • Commercial Lending headquarters in Burlington MA • Congress St, Boston branch to open early 2017 • Boston is the Capital of MA and a port city • Boston accounts for 45% of New England GDP • Total deposits in Region $55MM as of 06/30/2016 • Eastern MA is the home of Berkshire’s Firestone Financial, ABL and Berkshire Home Lending operations • Primary industries operating within footprint include education, biotechnology, healthcare and financial services • Official sponsor of Boston Bruin’s coverage on NESN since 2014 Worcester MA Boston MA Population 940M 4,832M GDP (2015) $39MM $397MM % Change Y/Y 3.6% 4.6% Avg Household Income $112M $90M Unemployment Rate (09/2016) 3.7% 2.9% Total Deposits $17B $215B % Change Y/Y 7.1% 2.5% BHLB Deposit Market Share 0.28% 0.02% Note: All data by MSA and as of 06/30/2016 unless otherwise stated

25 Hartford/Springfield • Twenty - five branches located in Hartford/Springfield footprint • Commercial Lending headquarters located in Hartford and Springfield • Hartford is the Capital of CT • Total deposits in Region increased 6% from YE15 to $ 1.4 billion as of 06/30/2016 • Primary industries operating within footprint include insurance, education, assembly/distribution and defense • MGM Resorts constructing a casino in Springfield MA with an expected opening in 2018; will create 3,000 jobs and bring in roughly $18 million in revenue to the city of Springfield • CRRC Railcar Manufacturing Facility project will create 150 jobs in Springfield Note: All data by MSA and as of 06/30/2016 unless otherwise stated Hartford CT Springfield MA Population 1,209M 635M GDP (2015) $86MM $25MM % Change Y/Y 3.1% 2.7% Avg Household Income $99M $75M Unemployment Rate 5.1% 4.2% Total Deposits $43B $14B % Change Y/Y 1.1% 4.2% BHLB Deposit Market Share 0.69% 8.22%

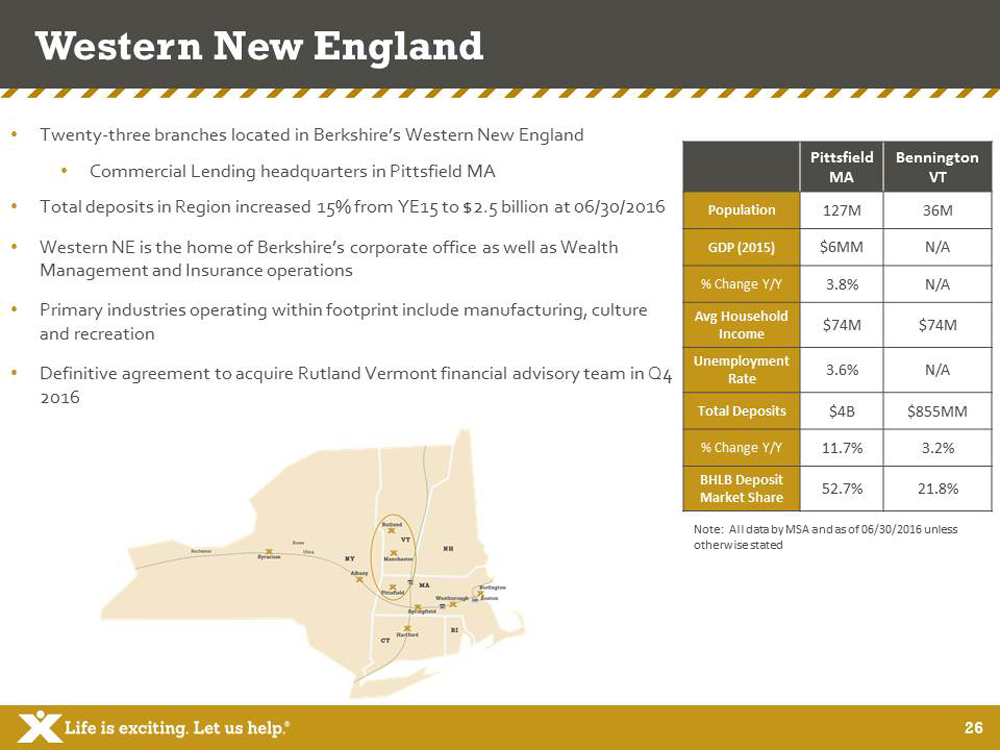

26 Western New England • Twenty - three branches located in Berkshire’s Western New England • Commercial Lending headquarters in Pittsfield MA • Total deposits in Region increased 15% from YE15 to $ 2.5 billion at 06/30/2016 • Western NE is the home of Berkshire’s corporate office as well as Wealth Management and Insurance operations • Primary industries operating within footprint include manufacturing, culture and recreation • Definitive agreement to acquire Rutland Vermont financial advisory team in Q4 2016 Note: All data by MSA and as of 06/30/2016 unless otherwise stated Pittsfield MA Bennington VT Population 127M 36M GDP (2015) $6MM N/A % Change Y/Y 3.8% N/A Avg Household Income $74M $74M Unemployment Rate 3.6% N/A Total Deposits $4B $855MM % Change Y/Y 11.7% 3.2% BHLB Deposit Market Share 52.7% 21.8%

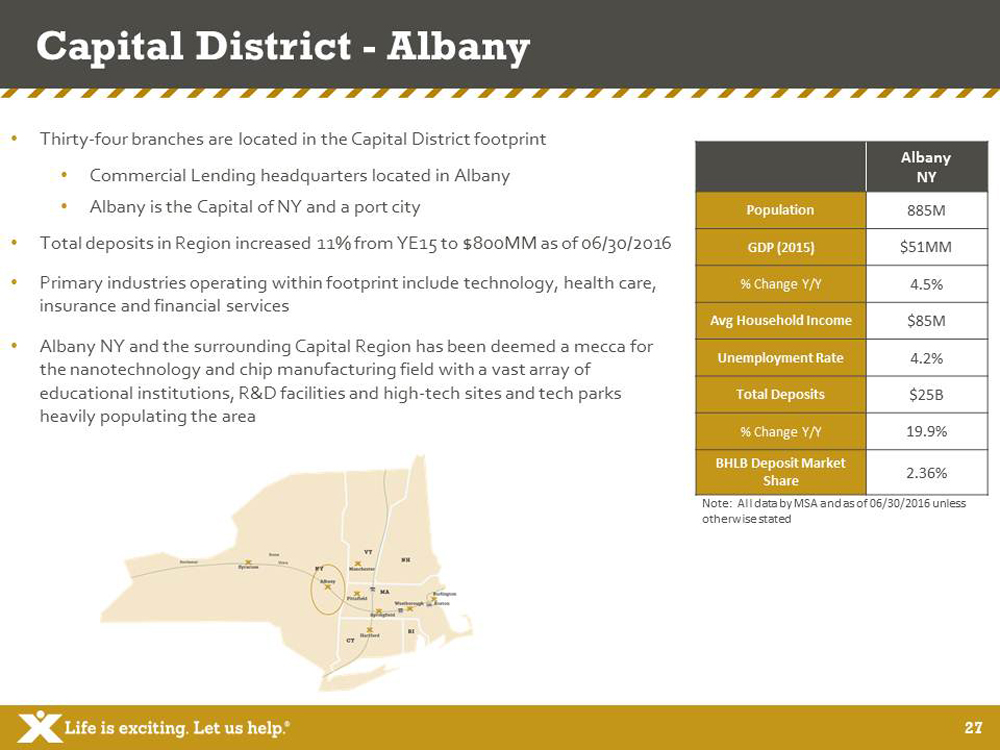

27 Capital District - Albany • Thirty - four branches are located in the Capital District footprint • Commercial Lending headquarters located in Albany • Albany is the Capital of NY and a port city • Total deposits in Region increased 11% from YE15 to $ 800MM as of 06/30/2016 • Primary industries operating within footprint include technology, health care, insurance and financial services • Albany NY and the surrounding Capital Region has been deemed a mecca for the nanotechnology and chip manufacturing field with a vast array of educational institutions, R&D facilities and high - tech sites and tech parks heavily populating the area Note: All data by MSA and as of 06/30/2016 unless otherwise stated Albany NY Population 885M GDP (2015) $51MM % Change Y/Y 4.5% Avg Household Income $85M Unemployment Rate 4.2% Total Deposits $25B % Change Y/Y 19.9% BHLB Deposit Market Share 2.36%

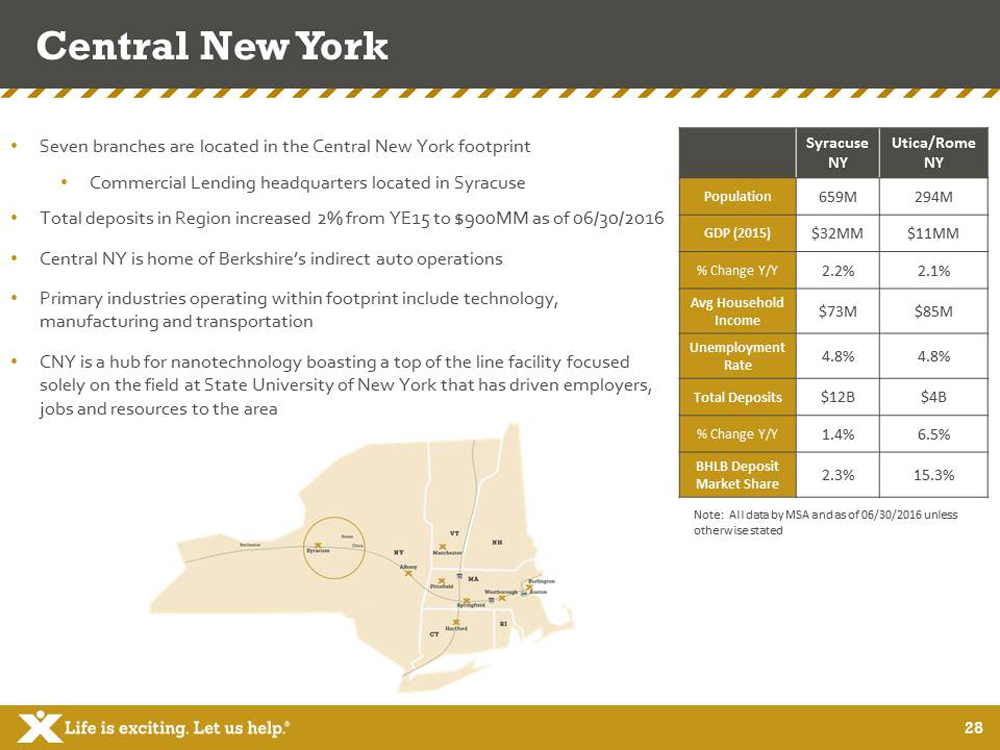

28 Central New York • Seven branches are located in the Central New York footprint • Commercial Lending headquarters located in Syracuse • Total deposits in Region increased 2% from YE15 to $900MM as of 06/30/2016 • Central NY is home of Berkshire’s indirect auto operations • Primary industries operating within footprint include technology, manufacturing and transportation • CNY is a hub for nanotechnology boasting a top of the line facility focused solely on the field at State University of New York that has driven employers, jobs and resources to the area Note: All data by MSA and as of 06/30/2016 unless otherwise stated Syracuse NY Utica/Rome NY Population 659M 294M GDP (2015) $32MM $11MM % Change Y/Y 2.2% 2.1% Avg Household Income $73M $85M Unemployment Rate 4.8% 4.8% Total Deposits $12B $4B % Change Y/Y 1.4% 6.5% BHLB Deposit Market Share 2.3% 15.3%

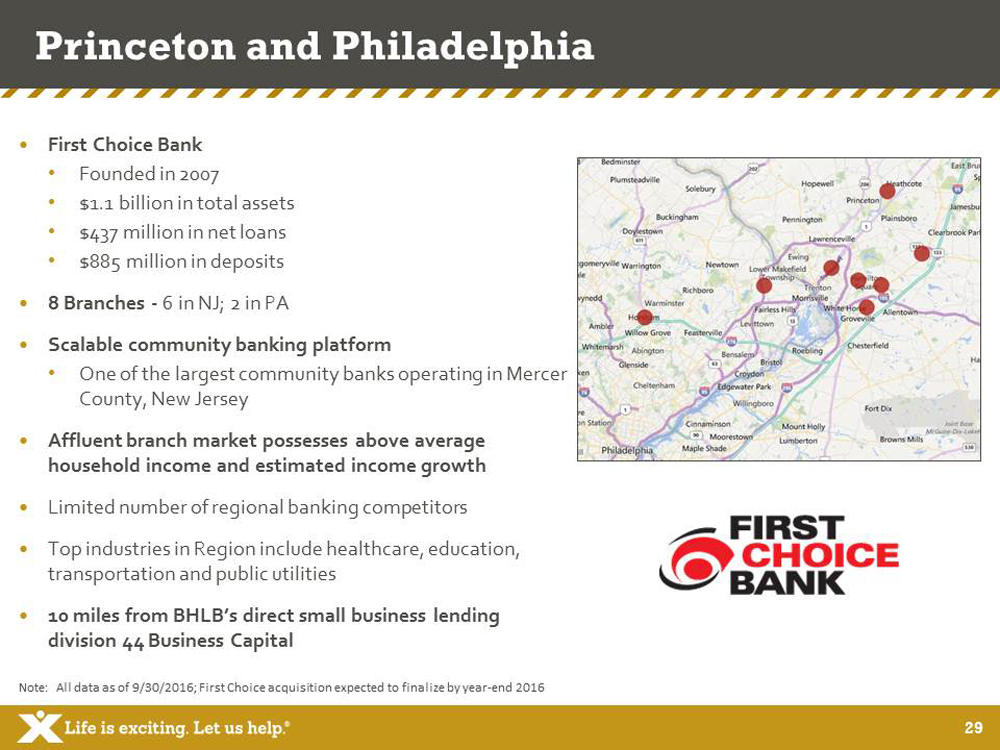

29 Princeton and Philadelphia First Choice Bank • Founded in 2007 • $1.1 billion in total assets • $437 million in net loans • $885 million in deposits 8 Branches - 6 in NJ; 2 in PA Scalable community banking platform • One of the largest community banks operating in Mercer County, New Jersey Affluent branch market possesses above average household income and estimated income growth Limited number of regional banking competitors Top industries in Region include healthcare, education, transportation and public utilities 10 miles from BHLB’s direct small business lending division 44 Business Capital Note: All data as of 9/30/2016; First Choice acquisition expected to finalize by year - end 2016

30 FORWARD LOOKING STATEMENTS This document contains forward - looking statements as defined in the Private Securities Litigation Reform Act of 1995 . There are several factors that could cause actual results to differ significantly from expectations described in the forward - looking statements . For a discussion of such factors, please see Berkshire’s most recent reports on Forms 10 - K and 10 - Q filed with the Securities and Exchange Commission and available on the SEC’s website at www . sec . gov . Berkshire does not undertake any obligation to update forward - looking statements .

31 NON - GAAP FINANCIAL MEASURES This document contains certain non - GAAP financial measures in addition to results presented in accordance with Generally Accepte d Accounting Principles (“GAAP”). These non - GAAP measures provide supplemental perspectives on operating results, performance tren ds, and financial condition. They are not a substitute for GAAP measures; they should be read and used in conjunction with the Co mpa ny’s GAAP financial information. A reconciliation of non - GAAP financial measures to GAAP measures is included on pages F - 9 and F - 10 i n the accompanying financial tables. In all cases, it should be understood that non - GAAP per share measures do not depict amounts that accrue directly to the benefit of shareholders. The Company utilizes the non - GAAP measure of core earnings in evaluating operating trends, including components for core revenue and expense. These measures exclude items which the Company does not view as related to its normalized operations. These items in clu de securities gains/losses, merger costs, restructuring costs, and systems conversion costs. Non - core adjustments are presented net of an adjustment for income tax expense. This adjustment is determined as the difference between the GAAP tax rate and the effectiv e t ax rate applicable to core income. The efficiency ratio is adjusted for non - core revenue and expense items and for tax preference items. The Company also calculates measures related to tangible equity, which adjust equity (and assets where applicable) to exclude int ang ible assets due to the importance of these measures to the investment community. Charges related to merger and acquisition activity consist primarily of severance/benefit related expenses, contract terminat ion costs, systems conversion costs, variable compensation expenses, and professional fees. These charges are related to the following b usi ness combinations: First Choice (pending), 44 Business Capital, Hampden Bancorp, and Firestone Financial. Restructuring costs gene ral ly consist of costs and losses associated with the disposition of assets and liabilities and lease terminations, including costs related to branch sales. The Company’s disclosures of organic growth of loans in 2016 are adjusted for the acquisition of the business operations rela ted to 44 Business Capital.

32 ADDITIONAL INFORMATION AND WHERE TO FIND IT In connection with the proposed merger, Berkshire has filed with the Securities and Exchange Commission (“SEC”) a Registratio n Statement on FormS - 4 that includes a Proxy Statement of First Choice and a Prospectus of Berkshire, as well as other relevant do cuments concerning the proposed merger. Investors and stockholders are urged to read the Registration Statement and the Proxy Statement/Prospectus regarding the proposed merger and any other relevant documents filed with the SEC, as well as any amendm ent s or supplements to those documents, because they will contain important information. A free copy of the Registration Statement an d Proxy Statement/Prospectus, as well as other filings containing information about Berkshire and First Choice, may be obtained at the SEC’s Internet site (www.sec.gov). Copies of the Registration Statement and Proxy Statement/Prospectus and the filings that w ill be incorporated by reference therein may also be obtained, free of charge, from Berkshire’s website at ir.berkshirebank.com or b y c ontacting Berkshire Investor Relations at 413 - 236 - 3149 or by contacting Lisa Tuccillo at First Choice at 609 - 503 - 4828. PARTICIPANTS IN SOLICITATION Berkshire and First Choice and certain of their respective directors and executive officers may be deemed to be participants in the solicitation of proxies from the stockholders of First Choice in connection with the proposed merger. Information about the d ire ctors and executive officers of Berkshire is set forth in the proxy statement for Berkshire’s 2016 annual meeting of stockholders, as f ile d with the SEC on a Schedule 14A on March 24, 2016. Information about the directors and executive officers of First Choice will be set f ort h in the Proxy Statement/Prospectus. Additional information regarding the interests of those participants and other persons who may be de emed participants in the transaction and a description of their direct and indirect interests, by security holdings or otherwise, may be obtained by reading the Proxy Statement/Prospectus and other relevant documents regarding the proposed merger to be filed with the SEC (w hen they become available). Free copies of these documents may be obtained as described in the preceding paragraph.

33 Notes

34 Notes

35 Notes

If you have any questions, please contact : Allison O’Rourke 99 North Street Pittsfield, MA 01202 Investor Relations Officer (413) 236 - 3149 aorourke@berkshirebank.com