David T. Taber, President & CEO

Forward-Looking Statements

Raymond James Bank Conference

August 10, 2011

Certain statements contained herein are forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934 and subject to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995, that involve risks and uncertainties. Actual results may differ materially from the results in these forward-looking statements. Factors that might cause such a difference include, among other matters, changes in interest rates, economic conditions, governmental regulation and legislation, credit quality, and competition affecting the Company’s businesses generally; the risk of natural disasters and future catastrophic events including terrorist related incidents; and other factors discussed in the Company’s Annual Report on Form 10-K for the year ended December 31, 2010, and in subsequent reports filed on Form 10-Q and Form 8-K. The Company does not undertake any obligation to publicly update or revise any of these forward-looking statements, whether to reflect new information, future events or otherwise, except as required by law.

Company Profile

Headquarters

Rancho Cordova, CA

a Suburb of Sacramento

| Founded | Total Assets |

| 1983 | $570 million |

| | |

| Shareholders’ Equity | 3-Month Average Volume |

| $91 million | 7,927 shares per day |

| | |

| Insider Ownership | Institutional Ownership |

| 8% | 43% |

As of June 30, 2011

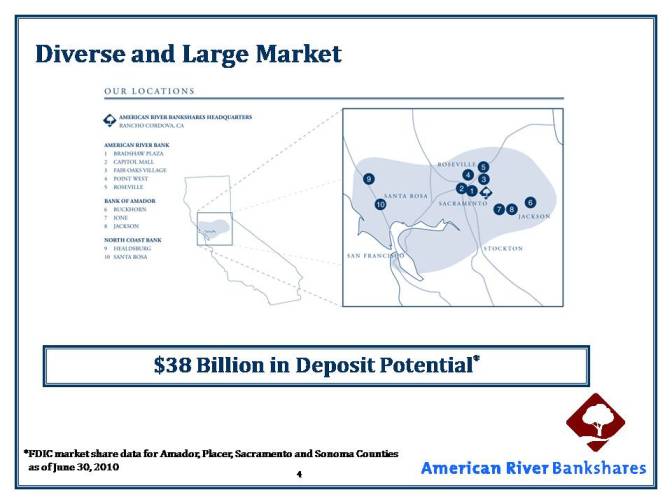

Diverse and Large Market

$38 Billion in Deposit Potential*

*FDIC market share data for Amador, Placer, Sacramento and Sonoma Counties as of June 30, 2010

Strategic Direction

| | •Organic Growth in Current Markets |

| | •Small business $1 – $30M |

| | •High Net Worth individuals |

| | •Building Trades, Wholesalers, Fiduciaries, Manufacturers, Professionals & Property Managers |

| | •Focus on the business, its owners, their families and their employees |

| | •Provide 360 degree banking needs for each relationship |

Experience Matters…Leadership Counts

Name | Position | Industry Experience |

| David Taber | President Chief Executive Officer | 28 years |

| Mitchell Derenzo | Executive Vice President Chief Financial Officer | 23 years |

| Doug Tow | Executive Vice President Chief Credit Officer | 35 years |

| Kevin Bender | Executive Vice President Chief Operating Officer | 28 years |

Our Executive Team has been Together for 17 Years

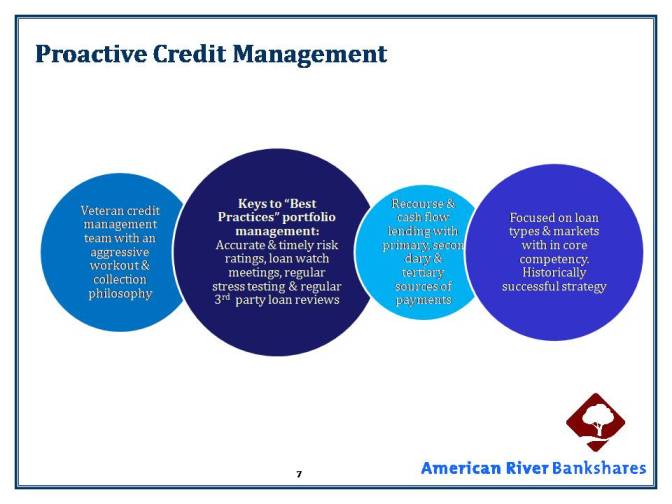

Proactive Credit Management

| | •Veteran credit management team with an aggressive workout & collection philosophy |

•Keys to “Best Practices” portfolio management: Accurate & timely risk ratings, loan watch meetings, regular stress testing & regular 3rd party loan reviews

| | •Recourse & cash flow lending with primary, secondary & tertiary sources of payments |

| | •Focused on loan types & markets with in core competency. Historically successful strategy |

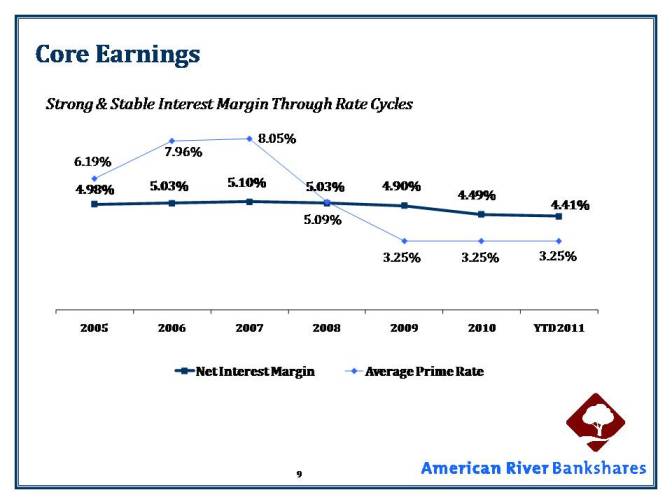

Core Earnings

Net Income vs. Income Before Credit Costs

Core Earnings

Strong & Stable Interest Margin Through Rate Cycles

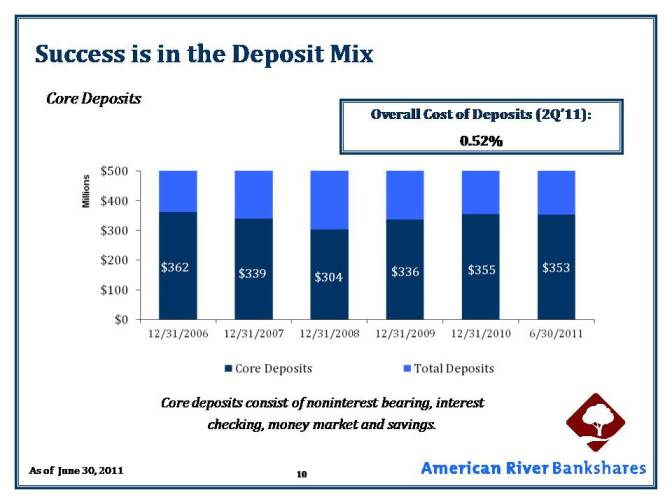

Success is in the Deposit Mix

Core Deposits

Overall Cost of Deposits (2Q’11):

0.52%

Core deposits consist of noninterest bearing, interest checking, money market and savings.

As of June 30, 2011

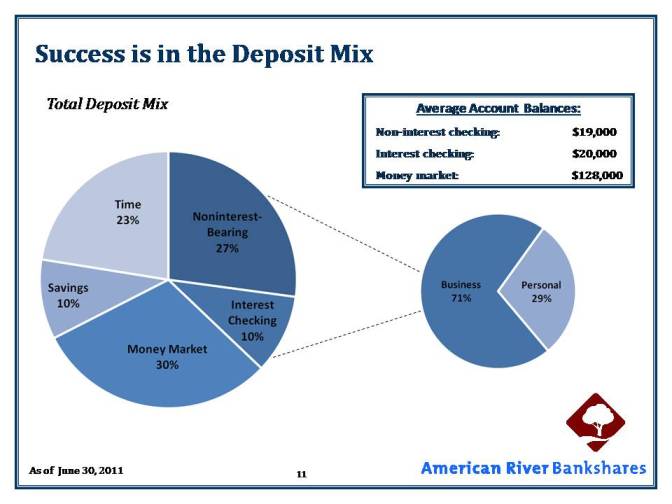

Success is in the Deposit Mix

Total Deposit Mix

Average Account Balances:

Non-interest checking: $19,000

Interest checking: $20,000

Money market: $128,000

As of June 30, 2011

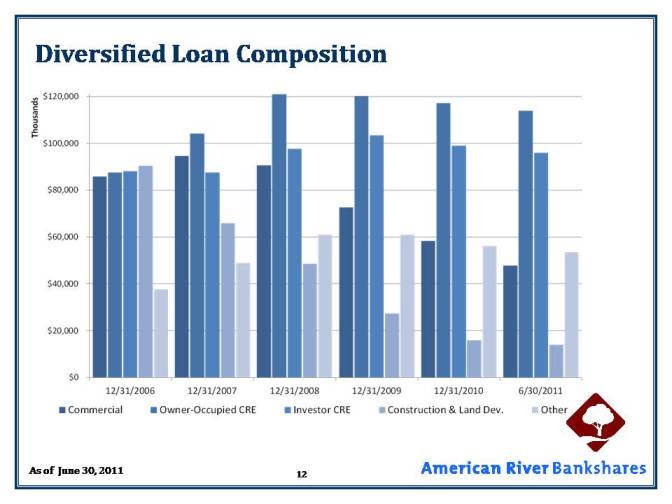

Diversified Loan Composition

As of June 30, 2011

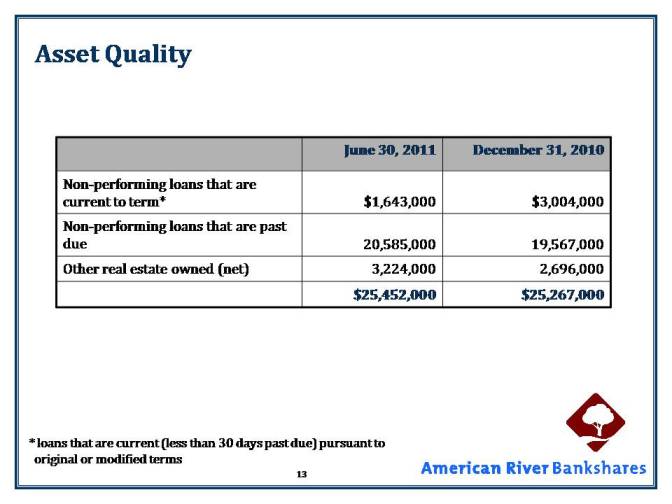

Asset Quality

| | June 30, 2011 | December 31, 2010 |

| Non-performing loans that are current to term* | $1,643,000 | $3,004,000 |

| Non-performing loans that are past due | 20,585,000 | 19,567,000 |

| Other real estate owned (net) | 3,224,000 | 2,696,000 |

| | $25,452,000 | $25,267,000 |

* loans that are current (less than 30 days past due) pursuant to original or modified terms

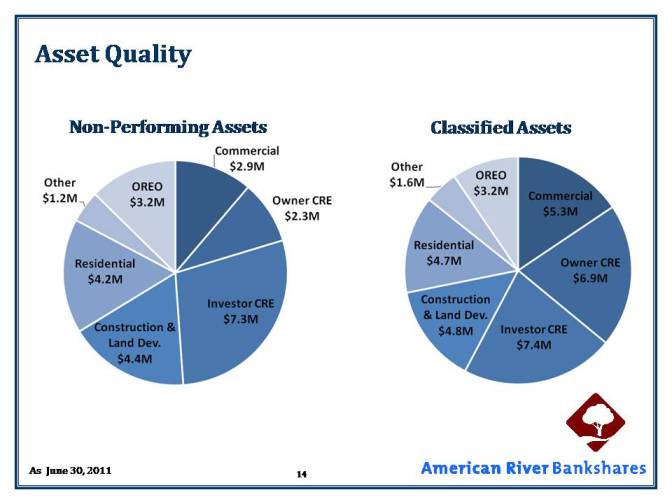

Asset Quality

Non-Performing Assets Classified Assets

As June 30, 2011

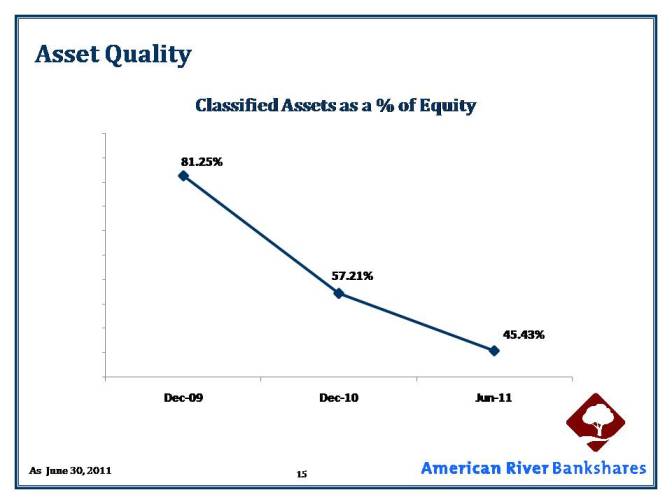

Asset Quality

Classified Assets as a % of Equity

As June 30, 2011

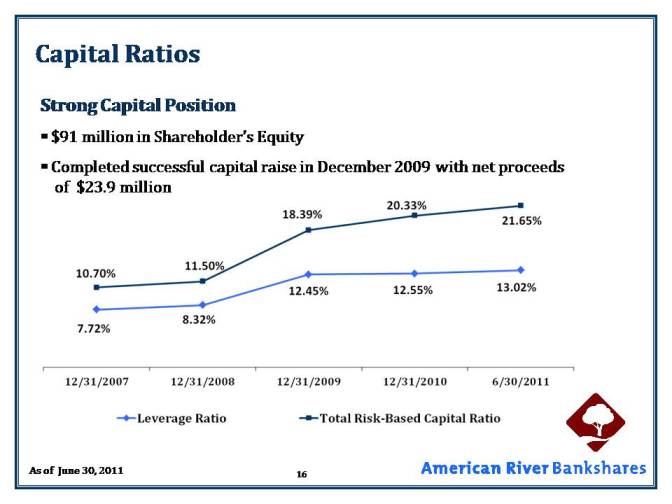

Capital Ratios

Strong Capital Position

§ $91 million in Shareholder’s Equity

§ Completed successful capital raise in December 2009 with net proceeds of $23.9 million

As of June 30, 2011

The Right Mix of Service and Sales

Sales

üFeet-on-the-Street Prospecting

üFinancial Reviews

üServices per Household

üBank Local

üResult-driven Marketing

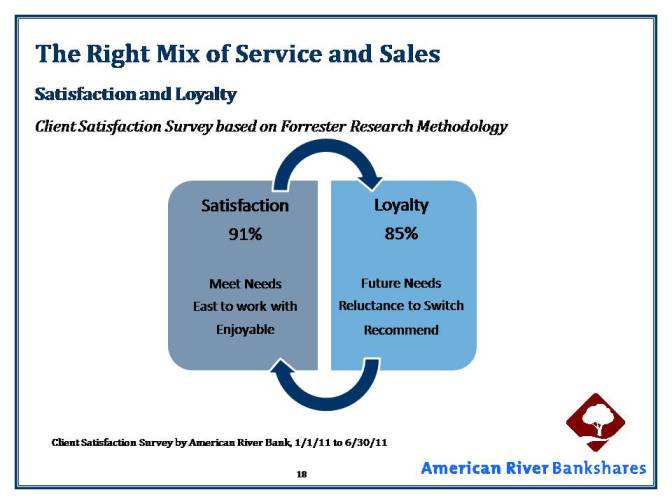

The Right Mix of Service and Sales

Satisfaction and Loyalty

Client Satisfaction Survey based on Forrester Research Methodology

Client Satisfaction Survey by American River Bank, 1/1/11 to 6/30/11

The AMRB Difference