April 29, 2022

Division of Corporation Finance

Office of Energy & Transportation

Securities and Exchange Commission

100 F Street, NE

Washington, DC 20549-7010

| Re: | PetroChina Company Limited |

Form 20-F for Fiscal Year Ended December 31, 2020

Filed April 29, 2021

File No. 001-15006

Dear Sir/Madame,

I refer to the further comments set forth in the letter from the staff of the Commission (the “Staff”) dated March 28, 2022 (the “Letter”) relating to the annual report of PetroChina Company Limited (“PetroChina” or the “Company”) on Form 20-F for the fiscal year ended December 31, 2020 which was filed with the U.S. Securities and Exchange Commission (the “Commission”) on April 29, 2021. Set forth below are the Company’s responses to the comments contained in the Letter. The numbered paragraphs below correspond to the comments in the Letter, which have been retyped below in bold for your ease of reference. Our references to “PRC”, “China”, “Chinese” or “domestic” herein below are to “mainland China”, unless otherwise required by the context.

Risk Factors

1. Please present the revised disclosures you intend to provide regarding the legal and operational risks relating to being based in and having the majority of your operations in China among the first items in the Risk Factors section of your annual report.

Response: The Company respectfully advises the Staff that the Company has rearranged the disclosures on risks factors and presented the disclosures regarding the risks relating to being based in and having the majority of its operations in China among the first items in the Risk Factor section of its Form 20-F for 2021. Please see the “Risk Factors” section starting from page 7 in the Form 20-F for 2021 for details.

2. Please revise to provide risk factor disclosure specifically addressing the designation of the energy sector as a national security interest of The People’s Republic of China. This disclosure should explain how any change in this type of designation would impact your operations, including your ability to transfer money or other assets out of China or enter into business transactions with non-Chinese parties. Also address the impact this would have on the value of your ADSs. Provide us with your proposed revisions in response to this and our other comments.

1

4. We note your response to prior comment 1. It appears you should provide disclosure that addresses the risks to you of new rules and regulations promulgated by the Chinese government (whether enacted or proposed). For example, as you occupy a leading position in the oil and gas industry in China, address risks associated with energy security, including as it relates to the risks of new rules and regulations and potential limits on foreign ownership in the energy sector. Include disclosure addressing the scenario where foreign investment in the sectors in which your business activities are conducted is prohibited or restricted and the consequences to the value of your ADSs. Also, specifically explain that rules and regulations in China can change quickly with little advance notice.

5. Your response to prior comment 1 states that you do not have any plan for a follow- on offering or new overseas listing. However, it appears that disclosure should be provided regarding the potential for limits on foreign investment if you were to pursue a new offering. Please revise your disclosure accordingly.

6. We note from your response to prior comment 1 that there is no requirement for you to obtain any additional approval in order to maintain the listing of your H Shares and ADSs. We also note from your response that the Chinese government has drafted proposed regulation which would (i) regulate and supervise overseas listings of Chinese companies by filing clearance, and (ii) disallow overseas listings that may pose any threat to or harm China’s national security. Please revise to provide disclosure explaining how Chinese regulatory authorities could regulate, oversee, control or disallow your listing, resulting in the value of such securities significantly declining or becoming worthless.

7. In your response to prior comment 1, you state that the Chinese government has drafted proposed regulation which would subject overseas offerings to a security review if they cause cybersecurity, data security or national security concerns. Disclose how these proposed regulations and recent statements by China’s government may impact your ability to conduct your business, accept foreign investments, or maintain your listing on a U.S. or other foreign exchange. Also, provide similar type disclosure regarding recent statements and regulatory actions by China’s government regarding anti-monopoly concerns.

8. In light of recent events indicating greater oversight by the Cyberspace Administration of China (CAC) over data security, including regulations issued in 2022, please revise your disclosure to explain how this oversight impacts your business and your offering and to what extent you believe that you are compliant with the regulations or policies that have been issued by the CAC to date.

10. Please expand the risk factor disclosure provided in response to prior comment 2 regarding the introduction of new rules by the Chinese government to more clearly describe the possible impact on the liquidity and value of your securities. Acknowledging your belief that even if the value of your ADSs were to decline it would be unlikely to be worthless, more specifically explain that any actions by the Chinese government to exert more oversight and control over offerings that are conducted overseas and/or foreign investment in China-based issuers could significantly limit or completely hinder your ability to offer or continue to offer securities to investors and cause the value of your ADSs to significantly decline or be worthless.

2

Response: The Company respectfully advises the Staff that as comments 2, 4, 5, 6, 7, 8 and 10 in the Letter generally revolve around the same topic, so for the ease of your review, the Company has combined its responses to these comments into one consolidated response as follows.

We understand that the concerns expressed in the comments 2, 4, 5, 6, 7, 8 and 10 very likely arose from the new draft rules in relation to the Provisions on the Administration of Overseas Securities Offering and Listing by Domestic Companies (Draft for Comments) (the “Draft Overseas Listing Provisions”) published by the Chinese government in December 2021. As provided in the Draft Overseas Listing Provisions, if any domestic company proposes to conduct an overseas securities offering and listing, and (i) where it involves any regulations in connection with China’s foreign investment(1), cybersecurity(2), or data security(3) rules, the company is obligated to take action to protect national security; (ii) where it involves China’s national security review rules, the company must go through the review process in accordance with applicable laws; and (iii) the competent department under the State Council may require the company to divest relevant businesses and/or assets to eliminate the impact(4) on national security; if the filing for an overseas offering and listing has been cleared, it may be rescinded. According to the statement made by the China Securities Regulatory Commission, or the CSRC, at the release of the Draft Overseas Listing Provisions, the rules, once they become effective, will initially apply to initial overseas offerings and listings, follow-on offerings and refinancing transactions (“new listing transactions”). With respect to other companies which have been listed on overseas securities exchanges (“existing overseas listed companies”), the application of the rules will be arranged at a later stage, providing a sufficient transitional period(5) to such companies.

At this stage, the Draft Overseas Listing Provisions is only a draft for comment and has yet to be enacted. It remains unclear as to whether it will be enacted in the end, and if enacted, what the final rules will be like, and to what extent and degree the rules will be applied and enforced, and how long the transitional period will be for existing overseas listed companies. As a result, any discussion of the future impact of the proposed rules under the Draft Overseas Listing Provisions on the Company at this stage would not necessarily have an adequate and accurate basis and so the Company respectfully submits that the following discussion is highly hypothetical.

Firstly, we set forth below the possible impact of the foregoing provisions on the Company:

(1) Relating to the “foreign investment” regulatory concern, according to current PRC laws and regulations, if any business of a PRC domestic company falls into the list of businesses where foreign investment is prohibited, and that company seeks to offer its shares and list overseas, it shall obtain requisite approvals from the competent Chinese governmental authorities. As none of the business activities conducted by the Company falls into any sector where foreign investment is prohibited, the Company is currently not impacted from the perspective of “foreign investment”.

(2) Relating to the “cybersecurity security” regulatory concern, the Chinese government issued the amended Measures for Cybersecurity Review in early 2022, pursuant to which, any online platform operator holding personal information of more than one million users in China seeking to list overseas, must undergo a cybersecurity review with the Cybersecurity Review Office. We understand that as the Company is not an “online platform operator”, it is not impacted directly by this rule.

3

(3) Relating to the “data security” regulatory concern, we understand that the Company may be determined to be a critical information infrastructure operator in the energy sector in China and accordingly any outbound transfer of any energy data possessed by the Company, including making available any such data to any foreign regulatory authority, may require certain approvals from the Chinese government pursuant to the applicable PRC laws and regulations. Although currently there are no regulations, including but not limited to data security, restricting the Company from maintaining its listing in the U.S., we cannot fully rule out the possibility that the “data security” concern may affect the ability of relevant companies to maintain their listings on foreign securities exchanges. We believe that this may be the risk faced by such overseas listed companies. As a result, we have included disclosure of this risk in the discussions under the heading “Risks Related to Liquidity and Value of ADSs” in our prior response.

(4) Relating to the redressive measures to “eliminate the impact”, if the Draft Overseas Listing Provisions is enacted in the end and pursuant to any relevant regulations that may be enacted in the future the Company is determined by the Chinese government to be likely to cause security concerns in relation to any outbound data transfer, we cannot rule out the possibility that the Company could be delisted in the U.S., whether voluntarily or by mandatory requirement, after or even within the transitional period. As a result, we have included disclosure of this risk in the discussions under the heading “Risks Related to Liquidity and Value of ADSs” in the 20-F for 2021.

(5) Relating to the ‘transitional period”, as stated by the CSRC, the Chinese government will allow the existing overseas listed companies a sufficient transitional period. We therefore believe that the preceding risk factor (4) may not constitute an imminent risk for the Company.

Secondly, as for the Commission’s concern mentioned in comment 2 that the designation of the energy sector as a national security interest of the PRC “would impact your operations, including your ability to transfer money or other assets out of China or enter into business transactions with non-Chinese parties”, if the energy sector were to be designated as a national security interest of the PRC, we understand that such regulatory measure (if enacted) will most likely be designed to protect the security of China’s energy data, for example, lessening the risks that may arise from the outbound transfer of energy data by restricting the overseas listing of relevant companies instead of restricting oil and gas companies from engaging in international business activities. We therefore understand that the rules (if enacted) designating the energy sector as a national security interest of the PRC will not impose restrictions or limitations on the Company’s ability to carry out overseas exploration, development, production, transportation or trading activities or the related transfers of money or assets or settlement of funds.

As for the Commission’s concern mentioned in comment 4 that “rules and regulations in China can change quickly with little advance notice”, we have included disclosure worded to that effect in the discussions under the heading “Risks Related to Government Regulation” in the Company’s Form 20-F for 2021. In that disclosure, we explained that relevant PRC laws, regulations and legal requirements are evolving rapidly and that some laws having a material effect on our company may be put into force or implementation without any transitional period or only after a very short transitional period, which would require us to adjust our operation and compliance quickly in order to comply with such new rules.

In response to your comments, the Company has expanded the risk factor disclosure regarding the introduction of new rules (including the Draft Overseas Listing Provisions and other related regulations and rules) by the Chinese government in the Company’s Form 20-F for 2021. In particular, we have expanded the disclosure under the heading “Risks Related to Liquidity and Value of ADSs” in the Company’s Form 20-F for 2021 by revising the disclosure as follows:

4

Risks Related to Liquidity and Value of ADSs

In addition to the factors that have been included in this “Risk Factor” section and elsewhere of this annual report that have a potential impact on the liquidity and value of our ADSs, we foresee certain risks relating to the liquidity and value of our ADSs arising from potential changes in the legal environment and regulatory requirements in the countries we operate and where our securities are listed, including but not limited to, in the following respects:

Firstly, if in the future any restrictions are imposed, or any negative comments or warnings are made, by any government or governmental authorities on the flow of capital into China or China-based companies, or any escalation of geopolitical tensions or any news or rumors thereof, or if investment restrictions are imposed on us or we are threatened with investment restrictions, it may make potential investors shun away from our securities (including our ADSs) and/or certain of our existing investors (including ADS investors) may divest from us. As a result, the liquidity and value of our securities (including our ADSs) may be materially and adversely affected.

Secondly, if in the future, the Chinese government introduces new rules relating to “information security”, “data security” and/or “national security” with respect to overseas offerings and listings by China-based issuers and/or with respect to China-based issuers that are already listed, which results in our company being covered to any extent by any such new rules, we cannot rule out the risk that it may have an impact on the liquidity and value of our securities (including our ADSs). For example, in December 2021, the Chinese government published the Provisions on the Administration of Overseas Securities Offering and Listing of Domestic Companies (Draft for Comments) (the “Draft Overseas Listing Provisions”). The Draft Overseas Listing Provisions provides that if any domestic company proposes to conduct an overseas securities offering and listing, and (i) where it involves China’s foreign investment, cybersecurity, or data security rules, the company is obligated to take action to protect national security; (ii) where it involves security review rules, the company must go through the review process in accordance with applicable laws; and (iii) the competent department under the State Council may require the company to divest relevant businesses and/or assets to eliminate the impacts on national security, and if the filing of a proposed overseas offering and listing has been cleared, the filing may be rescinded. CSRC stated at the release of the Draft Overseas Listing Provisions that the rules after becoming effective will apply to initial offerings and listings, follow-on offerings and refinancing, while the application of these rules to other overseas listed companies will be arranged at a later stage, thus providing a sufficient transitional period to those other overseas listed companies. We understand that these draft rules will implicate the applicable laws and regulations in relation to national security review, and (i) if the rules are enacted in the end, (ii) if our company is determined to be an operator of critical information infrastructure in the energy sector, (iii) if the companies in the energy sector are required to undertake the national security review in relation to their overseas listing, and (iv) if after its review according to the relevant laws and regulations, the competent PRC regulator determines that for the sake of protecting relevant data from disclosure, companies operating in the sector in which we operate are no longer suitable for being listed overseas, then the PRC government may prohibit or restrict overseas listing of domestic companies operating in our sector (such as our company). In that case,

| • | we may be delisted from the U.S., whether voluntarily or by mandatory requirements, and investors of our ADSs will then have to sell their ADSs or convert the ADSs into our H Shares; |

| • | the market price of our ADSs may be materially and adversely affected by the risk aversion and other negative market sentiment, regardless of our actual operating conditions; |

| • | if any investor of our ADSs does not convert the ADSs held by him/her into our H Shares for any reason, those ADSs may eventually lose all market value due to the loss of liquidity on the NYSE; |

| • | affected by the decline in the market value of ADSs, the prices of our H Shares, the underlying securities of ADSs, may drop significantly; |

| • | the conversion of ADSs into H Shares will incur some costs and cause some inconvenience; and |

| • | if in the future we propose to conduct a follow-on offering overseas, the proposed offering may be hindered by the occurrence of any one or more of the foregoing events. |

See also other risks disclosed in this “Risk Factors” section, such as “Risks Related to Audit Reports Prepared by an Auditor Who Is Not Inspected by the Public Company Accounting Oversight Board”, “Risks Related to Government Regulation”, “Risks Related to Outbound Investments and Trading”, “Risks Related to Sanctions and Trade Controls”, “Risks Related to Macro Economic Conditions” and “Risks Related to Pricing and Exchange Rate.”

5

Thirdly, in response to the Staff’s request for disclosure regarding recent statements and regulatory actions by the Chinese government regarding anti-monopoly concerns, the Company respectively advises the Staff that it has noticed that in 2021 the Chinese government comprehensively enhanced its anti-monopoly rule-making and enforcement, including, inter alia, having introduced the anti-monopoly guidelines targeting the internet platform economy, having investigated and closed multiple monopoly cases, and imposed substantial penalties on anti-monopoly violators operating in the internet platform sector. We expect that the Chinese government would focus its enforcement efforts on anti-monopoly concerns for a certain period of time in the near future. We have included the following disclosure in the “Risk Factors” section in the Company’s Form 20-F for 2021:

Risks Related to Anti-Monopoly Initiatives

The Anti-Monopoly Law of the PRC (the “Anti-Monopoly Law”) prohibits the entry into or implementation of any horizontal or vertical monopoly agreements, the taking of any action by abusing dominant market position, and any concentration of business operators that has or may have the effect of excluding or limiting competition. Penalties for violations of the Anti-Monopoly Law include, inter alia, confiscation of illegal gains and imposition of penalties as high as 10% of the sales revenue of the violator in the preceding year. We have directed our headquarter office and subsidiaries not to take any action in violation of the Anti-Monopoly Law or any of its supporting laws and regulation in their conduct of business, and have monitored company-wide anti-monopoly compliance through our internal compliance system. Despite that, we cannot assure you that our company can prevent all anti-monopoly compliance risks due to the fact that our company occupies a leading market position, the large scale of our business operations and our company has a large number of subsidiaries and branches. If in the future our company is determined to have deficiencies in the anti-monopoly compliance, or any business model adopted or particular transaction conducted by our company is determined, for example, to have abused our market position, entered into monopoly agreements, or implemented a concentration of business operators in violation of anti-monopoly requirements, we may be subject to investigations or enforcement actions by the government. In the case of such determination, in addition to being subject to a substantial fine, we may need to adjust our business model accordingly or make corresponding changes to a particular transaction structure. All of these would have a material adverse effect on our business operations, financial condition, operating results and corporate reputation, and may reduce the value of our securities and the profits distributable to our shareholders (including investors of our ADSs).

3. As a company based in and with the majority of its operations in China, please revise to include a stand-alone risk factor regarding the enforceability of securities law liabilities against your officers and directors.

Response: The Company respectfully advises the Staff that the Company has presented the following stand-alone risk factor on the risks relating to the difficulty in enforcing securities law liabilities against its officers and directors in its Form 20-F for 2021.

Risks Related to the Enforceability of Securities Law Liabilities against Our Officers and Directors

PRC laws and regulations have their foundation in written laws, and PRC laws, regulations and legal requirements dealing with economic matters continue to evolve. PRC laws and regulations are different in certain material areas such as legislation, judicial system, and enforcement from those in the United States and other common law jurisdictions. Because of the non-binding nature of prior court decisions in China, the enforcement of laws, regulations and legal requirements involve some degree of uncertainty. The PRC laws and regulations with respect to companies, securities and litigation are different in certain important aspects from those in the United States and other common law jurisdictions, and most of our assets are located in the PRC and most of our directors and substantially all of our executive officers reside in the PRC. As a result, it may be difficult for our shareholders (including investors of our ADSs) to enforce any judgments against our assets or the assets of our directors and officers in an event that they believe their rights have been infringed and even if they successfully bring an action against us or our directors and officers and they are successful in an action of this kind.

6

Furthermore, due to jurisdictional limitations, the ability of U.S. government agencies, such as the U.S. Securities and Exchange Commission, or the SEC, and the U.S. Department of Justice, or the DOJ, to investigate and bring enforcement actions against us may be limited. PRC laws may constrain the ability of our company and our directors and officers to cooperate with such an investigation or action. For example, according to Article 177 of the PRC Securities Law, no overseas securities regulator is allowed to directly conduct investigations or evidence collection activities within the territory of the PRC. Without the consent of the securities regulatory department of the State Council and other competent authorities under the State Council, no organization or individual may provide documents or materials relating to securities business activities to overseas parties. As a result of the foregoing, our shareholders (including investors of our ADSs) may have difficulty in protecting their interests through actions against our company, directors, officers or our majority shareholder. Shareholder protection through actions initiated by the SEC, DOJ and other U.S. government agencies may also be limited. All these may have an adverse effect on the exercise of rights by the investors of our ADSs.”

9. Your response to prior comment 2 addresses the risks in relation to the liquidity and value of your ADSs. However, it appears that disclosure should be provided regarding the broader liquidity risks that operating in China poses to investors. Revise to provide a clear description of how cash is transferred through your organization. Quantify any cash flows and transfers of other assets by type that have occurred between you and your subsidiaries, including the direction of transfer. Quantify any dividends or distributions that a subsidiary has made to you and which entity made such transfer, and their tax consequences. Similarly quantify dividends or distributions made to U.S. investors, the source, and their tax consequences. Your risk factor disclosure should make clear whether transfers, dividends, or distributions have been made to date. Describe any restrictions on foreign exchange and your ability to transfer cash between entities, across borders, and to U.S. investors. Include information addressing cash flows related to subsidiaries or other entities located outside of China (i.e., explain how restrictions could impact your ability to fund your foreign operations). Describe any restrictions and limitations on your ability to distribute earnings, including with regard to your subsidiaries and U.S. investors.

Response: The Company respectfully advise the Staff that it did not adopt a VIE structure for the listing of its ADSs on the NYSE. Any transfer of funds between the Company and its subsidiaries, associate companies and joint ventures mainly involves (1) the contribution of capital or receipt of dividends based on shareholding and (2) funds transfer in the normal course of business. Since its listing in Hong Kong and the U.S. in 2000, the Company has distributed dividends to all its shareholders (including its ADS holders) twice a year. The Articles of Association of the Company stipulates that the total dividends for a given year shall not be less than 30% of the net profit attributable to the Company in that year. The Company’s actual distribution in the past has always been higher than this minimum ratio. As long as certain compliance requirements are satisfied, inter-company fund flows are not subject to additional restrictions. Details of such requirements have been disclosed in the various relevant items in the Form 20-F. The following is a brief summary of the inter-company fund flows and related compliance requirements.

| (1) | Capital contribution / dividend distribution on shareholding relationship |

The Company does not adopt a VIE structure. The fund flows between the Company and its domestic and foreign subsidiaries, associate companies and joint ventures directly held by the Company based on shareholding mainly involve: (1) the contribution of capital and (2) the receipt of dividends. Similarly, the fund flows between the Company’s subsidiaries and their subsidiaries, associate companies and joint ventures also mainly involve capital contributions and the receipt of dividends. As long as certain compliance requirements are satisfied, there are no additional restrictions on the inter-company fund flows. The profit of the Company is mainly generated from the profits earned by its branch companies and subsidiaries. In 2021, the dividends received by the Company from its subsidiaries, associate companies and joint ventures directly held domestically and abroad accounted for 13% of the Company’s pre-tax profits.

7

As far as domestic enterprises are concerned, the Company makes direct contributions in RMB to its subsidiaries, associate companies, and joint ventures in accordance with the relevant Chinese laws and regulations, the articles of association and the relevant shareholders’ agreements. According to Chinese company law and tax law, as well as pursuant to the articles of association and other provisions of such entities, domestic enterprises, after deducting income tax, statutory provident funds, public welfare funds and discretionary provident funds, may pay dividends to the Company in RMB as resolved by each of such entities’ board of directors and/or shareholders.

As far as overseas enterprises are concerned, due to foreign exchange controls implemented by the Chinese government over the capital account items, in order to convert the funds from RMB into foreign currencies to complete the contribution, capital contributions in foreign currencies to be paid from China by the Company to the Company’s overseas directly invested enterprises need to fulfill the relevant government filing and/or approval in advance in accordance with the laws and rules of the Chinese government on overseas investment and foreign exchange regulation. The after-tax profits of overseas enterprises invested in by the Company may be distributed to the Company in accordance with local laws, the overseas enterprises’ articles of association and the relevant shareholders agreements. In general, foreign exchange regulation implemented by the Chinese government over the capital account items will restrict the Company’s ability to carry out overseas investment and financing. However, there will be no additional restrictions on fund flows to and from a given overseas enterprise once the Company has completed the relevant foreign exchange regulatory reporting and/or review of the specific project, as applicable.

In terms of tax costs, the standard tax rate for China’s domestic enterprise income tax is 25% of the taxable income after deducting costs and expenses. The tax applicable to overseas enterprises shall be paid in accordance with the local policies, laws and tax treaties of the country where they operate.

| (2) | Cash flow in the normal course of business |

The Company is an enterprise with integrated upstream and downstream businesses, and the branch companies, subsidiaries, associate companies and joint ventures of the Company work closely together in their ordinary operations. The Company’s exploration and production enterprises, refining and chemical enterprises, sales enterprises and trading enterprises supply products and services to each other. CNPC Finance Co., Ltd., an associate company of the Company, provide financial services such as deposit, lending and settlement to the branch companies, subsidiaries, associate companies and joint ventures of Company. These businesses are carried out on normal commercial terms and are in compliance with the relevant regulatory requirements in all material aspects, and therefore the corresponding fund flows are not subject to any additional restrictions.

8

| (3) | Distribution of dividends to the shareholders |

The Company pays dividends to its shareholders (including overseas shareholders) in accordance with the PRC Company Law, the Articles of Association of the Company, and PRC laws and regulations on tax and foreign exchange, etc. The Articles of Association of the Company provides that if the net profit attributable to owners of the Company and the accumulated undistributed profit for a year are positive, and the cash flow of the Company can satisfy its normal operation and sustainable development, the amount of cash dividend to be distributed in a given year shall not be less than 30% of the net profit attributable to owners of the Company realized in that year and the dividend shall be distributed twice a year. In fact, since the Company listed its shares in Hong Kong and the U.S., the actual dividend payout ratio has always been higher than this ratio. The Company declares dividends in RMB and pays Hong Kong dollars and US dollars to the H shareholders and ADS holders, respectively, which are converted from RMB at the applicable exchange rates. Distribution to the ADS holders is handled by our depositary bank, the Bank of New York Mellon. Distribution to non-resident enterprise shareholders and individual shareholders shall be subject to withholding tax which will be withheld by the Company according to China’s tax law and the relevant tax treaties. Since the Company’s shares were listed in Hong Kong and the U.S. in 2000, the Company has distributed dividends to its shareholders for over 40 times, and has never experienced any restrictions. Every year the cash outflow for paying dividends has never exceeded the cash flow from operating activities of the Company.

| (4) | Income in Foreign Exchange and Overseas Settlement |

In 2021, the revenue from the Company’s international business accounted for 37.8% of the Company’s total revenue, and the profit from the Company’s international business accounted for 5.6% of the Company’s pre-tax profit. Due to its international business operations and financing activities, the Company maintains cash and cash equivalents in different currencies. As of December 31, 2021, the Company’s cash and cash equivalents denominated in RMB and US dollars accounted for 58.5% and 36.7%, respectively, of the total cash and cash equivalent of the Company. The Company and its subsidiaries, associate companies, joint ventures maintain domestic and foreign currency accounts with qualified financial institutions both domestically and abroad for fund settlement in accordance with laws and regulation, to enable the Company to conduct fund transfers conveniently.

For more information, please refer to “Item 3—Risks Related to Pricing and Exchange Rate”, “Item 5—Liquidity and Capital Sources”, “Item 10—Supplementary Information—Articles of Association of the Company – Dividends”, “Item 10—Supplementary Information—Foreign Exchange Control”, “Item 10—Supplementary Information—PRC Taxation”, “Item 7—Major Shareholders and Related Party Transaction”, the financial statements and the notes.

11. Your response to prior comment 3 states that the Chinese government generally does not directly intervene in or influence your business decisions or operations. However, we note from the disclosure in your Form 20-F that China National Petroleum Corporation (“CNPC”), which is controlled by the State-owned Assets Supervision and Administration Commission of the State Council of the People’s Republic of China, controls your policies and management affairs. You also state that CNPC’s interests may conflict with those of some or all of your minority shareholders. Revise to provide expanded disclosure addressing the Chinese government’s significant oversight and discretion over the conduct of your business and highlighting separately the risk that the Chinese government may intervene or influence your operations at any time. Your revised disclosure should address the nature of your relationship with the Chinese government, including as it relates to the interests of CNPC and the impact this could have on your corporate actions and their outcomes. This disclosure should be specific and cover the various ways the Chinese government could influence or control your operations and activities along with the different potential effects this could have on you, including as it relates to the value of your securities.

9

Response: The Company respectfully advises the Staff that the Company has revised the disclosures under the heading “Risks Related to Government Regulation” as follows to fully incorporate the Staff’s comments:

Risks Related to Government Regulation

Our operations in China currently contribute the large majority of our revenue. Accordingly, we are extensively affected and regulated by the economic and industrial policies, laws and regulations adopted in China. This may in turn adversely affect our financial condition, operation results, liquidity, and the value of our ADSs. These effects are reflected mainly in the following respects:

(1) In terms of general economic policies: The Chinese government regulates China’s economic development by setting general economic policies such as monetary and financial policy, fiscal and tax policy and foreign exchange policy. The application of any policy to us may affect our business decisions, production plans and strategy executions, which in turn may have an impact on our financial condition, operating results and value of our ADSs.

(2) In terms of industrial policies, laws and regulations: The sector in which we operate is subject to extensive regulation and regulatory control by the Chinese government. The regulation and regulatory control relate to many material aspects of our operations. As a result, we may face constraints and restrictions on our ability to implement our business strategies, to develop or expand our business operations or to maximize our profitability. For example:

| • | Energy transition policy: In order to address climate change concerns, the Chinese government has set the goal to hit carbon peak by 2030 and achieve carbon neutrality by 2060. To achieve that goal, China has introduced and is expected to introduce a series of economic policies and supporting laws and regulations. These regulations would pose severe challenges to traditional oil extraction and refining operations, and drive us to adjust our operational strategies and initiate steps to expand into new energy business while continuing to develop our traditional business with high quality. If our efforts to address climate change fail to produce satisfactory results, the overall operations, liquidity, profitability and the value of the ADSs of our company may suffer an adverse effect. |

| • | Product pricing mechanism: In China, the pricing of gasoline, diesel and natural gas products is subject to government regulation and we cannot freely set prices for these products. We are required to price these products in compliance with the Chinese government’s pricing mechanism. As a major supplier of essential energy sources in China, we are not permitted to cease supply to the market even if market prices are not favorable and we cannot exceed the pricing limit set by the government. |

| • | Crude oil special gain levy: China collects a crude oil special gain levy on all oil production companies that sell crude oil produced from China. At present, we are required to pay the crude oil special gain levy for the excessive revenue received by us from the sale of domestically produced crude oil above US$65 per barrel. |

| • | Mineral rights granting system: We are subject to various requirements under the Mineral Resources Law of the PRC and supporting laws and regulations, including those requirements relating to exploration licenses, production licenses, mineral rights fees, and minimum investment into mining blocks. |

| • | Ecological and environmental protection and safety production: We are subject to a series of ecological and environmental protection and safety production laws and standards, which have become increasingly stringent over recent years in China with respect to the oil and gas industries. |

| • | Project approvals: In China, the construction of significant refining and petrochemical facilities is subject to governmental approval. We presently have several significant projects pending approval from the relevant government authorities and will need approvals from the relevant government authorities in connection with several other significant projects. We do not have control over the timing and outcome of the final project approvals. |

10

| • | Oil and gas production targets: The National Energy Administration of the PRC publishes certain guiding targets for annual production of domestic energy companies. For example, for 2022, the National Energy Administration announced that its target is to procure China’s annual production of domestic crude oil to increase to about 200 million tons, annual production of domestic natural gas to increase to about 214 billion cubic meters, and the share of non-fossil energy in China’s domestic energy consumption to increase to about 17.3%. Although failure to achieve these targets will not subject us or other relevant companies to fines, these targets themselves would have an effect on our business decisions, hence, driving our management to make plans to work towards achievement of the pre-set targets. |

(3) In terms of generally applicable business laws and regulations: We are subject to generally applicable business laws and regulations, including, without limitation, corporate governance, securities regulation, employee benefits, information protection, anti-monopoly and anti-money-laundering laws and regulations. We are required to continue to invest substantial management resources to ensure compliance with all these laws and regulations. Any noncompliance with any of these laws or regulations will subject our company to penalties and reputational risks, and in turn harm the interests of our investors (including investors of our ADSs). For example:

| • | Anti-monopoly: We are subject to anti-monopoly laws and regulations. We are prohibited from entering into or implementing anti-competitive agreements or abusing our market position, or conducting any concentration of business operators which has or may have the effect of excluding or limiting competition. Occupying a leading position in the oil and gas industry, we are more susceptible to anti-monopoly compliance risks. See the “Risks Related to Anti-Monopoly Initiatives” for a more detailed discussion of this risk. |

| • | Corporate governance and securities regulatory compliance: Our securities are currently traded on the Shanghai Stock Exchange, Hong Kong Stock Exchange and New York Stock Exchange, or the NYSE. Accordingly, we are subject to all the applicable requirements under the listing rules, disclosure rules, securities laws as well as corporate governance and compliance rules adopted by all three markets. As a result, we are required to continue to invest substantial management resources to ensure compliance with all these requirements. |

(4) In terms of regulation and supervision of state-owned assets: We are a company with controlling shares ultimately owned by the state. Our controlling shareholder CNPC is a state-owned enterprise. Although the State-owned Assets Supervision and Administration Commission of the State Council does not exert influence directly on us, it is positioned to make decisions on significant matters of CNPC in its capacity as shareholder and CNPC can in turn resolve on significant matters of our company in its capacity as shareholder (see the provisions regarding shareholders’ rights and obligations in our Articles of Association). As a consolidated subsidiary of CNPC, we are subject to certain regulations in relation to state-owned assets. For example, we are subject to the audits by the National Audit Office of the PRC relating to our business, finance and staff. For material merger and acquisition transactions, we are required to retain external asset appraisal firms to evaluate the target assets. All these would increase our compliance burden. Please see “Item 7 — Major Shareholders and Related Party Transactions — Related Party Transactions” and “Item 3—Key Information—Risk Factors— Risks Related to Controlling Shareholder” for a detailed description of our transactions and relationships with our controlling shareholder.

(5) Impact of rapid evolution of PRC laws and regulations: PRC laws, regulations and legal requirements dealing with economic matters have experienced rapid development during the decades after China’s adoption of the reform and opening-up policy, especially during the most recent two decades. Some laws having a material effect on our company may be put into force or implementation without any transitional period or only after a very short transitional period, which have required us to quickly adjust our operation and compliance strategies in order to comply with the new rules.

See also “Item 4 — Information on the Company — Regulatory Matters” and the other relevant risk factors disclosed in this section, including without limitation, “Risks Related to Marco Economic Conditions”, “Risks Related to Competition”, “Risks Related to Financial Reporting Differences”, “Risks Related to Pricing and Exchange Rate”, “Risks Related to Environmental Protection and Safety Production”, and “Risks Related to Climate Change”, “Risks Related to Audit Reports Prepared by an Auditor Who Is Not Inspected by the Public Company Accounting Oversight Board”, “Risks Related to China’s Anti-Monopoly Initiatives”, and “Risks Related to Liquidity and Value of ADSs.”

11

Risks Related to Controlling Shareholder

12. In your response to prior comment 4, you provide proposed risk factor disclosure which explains that you are subject to the Chinese government’s industrial regulations “like those of other PRC oil and gas companies.” Please revise to remove this type of mitigating language as your disclosure should use descriptive wording relevant to your facts and circumstances that explains the extent to which you are subject to oversight and control by the Chinese government. This disclosure should be precise and should not suggest there are mitigating factors regarding the nature of your relationship with the Chinese government, the manner in which you are regulated, or the degree to which your operations could be affected by economic, industrial, or other policies in China. Note that this comment also applies to any other mitigating language provided in disclosure elsewhere in your risk factors.

Response: The Company respectfully advises the Staff that all the mitigating statements have been deleted from its Form 20-F for 2021, including the language “like those of other PRC oil and gas companies” particularly pointed out by the Staff in comment 12.

Risks Related to Audit Reports Prepared by an Auditor who is not Inspected by the Public Company Accounting Oversight Board

13. Your response to prior comment 7 states that both your current and previous external auditor are included in the list of accounting firms headquartered in mainland China that the PCAOB is unable to inspect completely. Provide expanded disclosure explaining that being identified as a company whose audit report was issued by a firm that cannot be inspected or investigated completely could have a negative effect on the value of your securities or cause investors to lose confidence in your financial statements and reporting. Also, explain that if your securities were prohibited from being traded on or were delisted from the U.S. securities exchanges, investors could lose all of the value of their investment and your securities could become worthless.

Response: The Company respectfully advises the Staff that the Company has expanded the disclosure under this risk factor to include a discussion explaining that being identified as a company whose audit report was issued by a firm that cannot be inspected or investigated completely could have a negative effect on the value of the Company’s securities or cause investors to lose confidence in the Company’s financial statements and reporting to a certain extent. The expanded disclosure also explains that if the Company’s securities were prohibited from being traded on or were delisted from the U.S. securities exchanges, the market value of the Company’s ADSs would be materially and adversely impacted. As of December 31, 2021, the Company’s ADSs accounted for 4.3% of the Company’s H Shares and 0.5% of the total share capital of the Company. Considering the fact that the Company’s ADSs are convertible to H Shares, it is unlikely that the Company’s ADSs could become worthless. Despite that, if any investor of the Company’s ADSs does not convert the ADSs held by him/her into H Shares for any reason, those ADSs may eventually lose all market value due to the loss of liquidity. The disclosure under this risk factor has been revised to reads as follows:

Risks Related to Audit Reports Prepared by an Auditor who is not Inspected by the Public Company Accounting Oversight Board

As a company with shares registered with the SEC, and traded publicly in the United States, our independent registered public accounting firm is required under the laws of the United States to be registered with the Public Company Accounting Oversight Board, or the PCAOB, and undergo regular inspections by the PCAOB to assess its compliance with the laws of the United States and professional standards. Under PRC laws, however, the

12

PCAOB is currently unable to inspect a registered public accounting firm’s audit work relating to a company’s operations in China without the approval of relevant Chinese authorities. The CSRC also stated that cross-border audit supervision should be realized through regulatory cooperation between China and the United States. Our independent registered public accounting firm’s audit of our operations in China is not subject to PCAOB inspections for the time being. In 2020, the Holding Foreign Companies Accountable Act, or the HFCAA, was signed into law. According to the HFCAA, where a covered foreign company listed in the U.S. retains an auditor who has a branch or office located in a foreign jurisdiction, and the PCAOB is unable to completely inspect or investigate the auditor for three consecutive years because of a position taken by an authority in the foreign jurisdiction, the SEC may prohibit securities of such covered foreign company from being traded on any national securities exchange or over-the-counter market in the U.S. and such covered foreign company is required to satisfy certain additional disclosure requirements. In December 2021, the SEC issued the rules to implement the requirements of the HFCAA. According to the rules, starting from the first half of 2022, the SEC will identify, determine and publish a list of the issuers identified by the SEC as subject to the HFCAA (a “covered issuer”); starting from 2024, SEC will impose a trading prohibition on issuers that remain covered issuers for three consecutive years. In December 2021, PCAOB issued the list of accounting firms that it is unable to inspect or investigate completely as determined by it. Both our current external auditor and our former external auditor were included in that list. It is possible that our company could be identified as a covered issuer shortly after the filing of this Form 20-F. Further, the United States may enact other laws that may include similar rules seeking to address the PCAOB inspection issue. For example, the Senate has passed the Accelerating Holding Foreign Companies Accountable Act, which, if enacted, would shorten the number of “non-inspection years” from three years to two years. Although the Chinese and U.S. regulators are currently having dialogues in order to reach a regulatory agreement, we cannot predict whether the dialogues will produce the desired results, and if any, whether they will arrive timely. Implementation of the HFCAA or other efforts to increase U.S. regulatory access to audit information could expose us and the investors of our ADSs to a series of risks. For example,

| • | the trading of our ADSs on the NYSE may be prohibited or our ADSs may be mandatorily delisted from the NYSE. If that happens, the investors of our ADSs will be forced to sell their ADSs or convert the ADSs into our H Shares; |

| • | the market price of our ADSs may be materially and adversely affected by the risk aversion and other negative market sentiment, regardless of our actual operating conditions; |

| • | if any investor of our ADSs does not convert the ADSs held by him/her into our H Shares for any reason, those ADSs may eventually lose all market value due to the loss of liquidity on the NYSE; |

| • | affected by the decline in the market value of ADSs, the prices of our H Shares, the underlying securities of ADSs, may drop down significantly; and |

| • | the conversion of ADSs into H Shares will incur some costs and cause some inconvenience. |

The PCAOB has conducted inspections of independent registered public accounting firms outside of China and has at times identified deficiencies in the audit procedures and quality control procedures of those accounting firms. Such deficiencies may be addressed in those accounting firms’ future inspection process to improve their audit quality. Due to the inability of PCAOB to conduct regular inspections of audit work undertaken in China for the time being, PCAOB is unable to assess the compliance of our independent registered public accounting firm according to applicable U.S. laws and professional standards. This may cause the investors to lose confidence in our financial statements and reports to a certain extent.

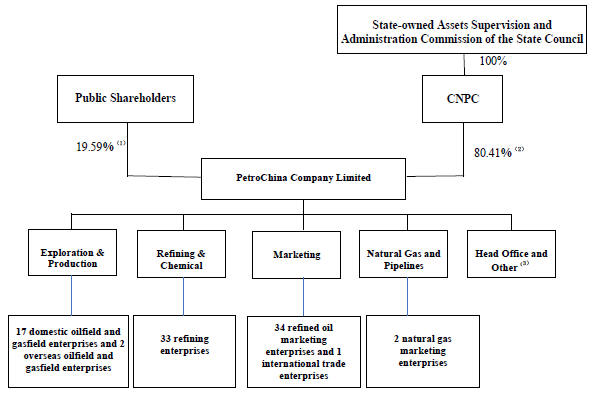

Item 4 — Information on the Company — Introduction History and Development of Our Company — Our Corporate Organization Structure

14. We note the chart illustrating your corporate organization structure on page 20 of your Form 20-F. Please expand this presentation to provide additional detail, including information depicting your principal subsidiaries and any entities in which your operations are conducted.

Response: The Company respectfully advises the Staff that the Company has revised the organization structure diagram to incorporate the Staff’s inputs and the diagram after being so revised included in the Form 20-F for 2021 is as set forth below:

13

Our Corporate Organization Structure

The following chart illustrates our corporate organization structure as of December 31, 2021.

| (1) | Indicates approximate shareholding. |

| (2) | Indicates approximate shareholding, including the 291,518,000 H Shares indirectly held by CNPC as of December 31, 2021 through Fairy King Investments Limited, a wholly owned overseas subsidiary of CNPC. |

| (3) | Includes PetroChina Exploration & Development Research Institute, PetroChina Planning & Engineering Institute, PetroChina Petrochemical Research Institute and several other companies. |

| * | Our major subsidiaries, all included in the chart above, are classified into different business segments based on the nature of their principal business activities. See Note 18 to our financial statements for a detailed discussion on this. Other than the major subsidiaries, companies in which we have equity interest mainly include China Oil & Gas Pipeline Network Corporation, CNPC Finance Co., Ltd., CNPC Captive Insurance Company Limited and other associate companies and joint ventures as well as other equity investments measured at fair value through other comprehensive income. See Note 16 and Note 17 to our financial statements for a detailed discussion. |

14

**********

Please do not hesitate to contact me or Mr. WEI Fang (hko@petrochina.com.hk; phone: +852.2899.2010; fax: +852.2899.2390) if you have additional questions or require additional information.

| Very truly yours, | ||

/s/ CHAI Shouping | ||

| Name: | CHAI Shouping | |

| Title: | CFO and Secretary to Board of Directors | |

Cc: By email

WEI Fang

Authorized Representative

PetroChina Co., Ltd.

Kyungwon (Won) Lee

Partner

Shearman & Sterling LLP

15