Table of Contents

As filed with the Securities and Exchange Commission on August 3, 2006

Registration No. 333-136019

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 1

to

Form S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Basic Energy Services, Inc.

(Exact name of registrant as specified in its charter)

| Delaware | 1389 | 54-2091194 | ||

| (State or other jurisdiction of incorporation or organization) | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification No.) |

400 W. Illinois, Suite 800

Midland, Texas 79701

(432) 620-5500

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Kenneth V. Huseman

President

400 W. Illinois, Suite 800

Midland, Texas 79701

(432) 620-5500

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copy to:

Andrews Kurth LLP

600 Travis, Suite 4200

Houston, Texas 77002

(713) 220-4200

Attn: David C. Buck

Approximate date of commencement of proposed sale to the public: As soon as practicable after this Registration Statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, please check the following box. o

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

The Registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

| The information in this prospectus is not complete and may be changed. These securities may not be sold until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell nor does it seek an offer to buy these securities in any jurisdiction where the offer or sale is not permitted. |

Subject to Completion dated August 3, 2006

2,101,641 Shares

Basic Energy Services, Inc.

Common Stock

Basic Energy Services, Inc. is registering 2,101,641 shares of common stock which will be distributed by Fortress Holdings, LLC to its members and by Southwest Partners II, L.P. and Southwest Partners III, L.P. to their partners. We will not receive any of the proceeds from the shares of common stock distributed by the distributing stockholders.

Our common stock is listed on The New York Stock Exchange under the symbol “BAS.” The last reported sales price of our common stock on August 2, 2006 was $27.62 per share.

See “Risk Factors” beginning on page 11 to read about factors you should consider before buying our common stock.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed on the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

Prospectus dated , 2006

Table of Contents

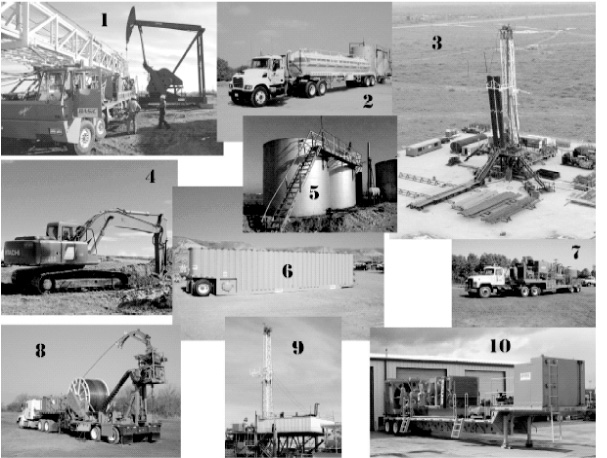

1. Well Servicing Rig Preparing to Begin Work

2. Fluid Services Transport Truck

3. 24 Hour Workover Rig

4. Well Site Construction Equipment

5. Saltwater Disposal Facility

6. Frac Tank Utilized for Storage of Fluids

7. Trailer-Mounted Pressure Pumping Equipment

8. Coiled Tubing Unit Used in Pressure Pumping

9. Inland Barge Workover Rig

10. Trailer-Mounted Foam Circulating Unit Used in Underbalanced Workover Operations

TABLE OF CONTENTS

| Page | ||||||||

| 1 | ||||||||

| 11 | ||||||||

| 20 | ||||||||

| 21 | ||||||||

| 23 | ||||||||

| 23 | ||||||||

| 24 | ||||||||

| 25 | ||||||||

| 28 | ||||||||

| 54 | ||||||||

| 72 | ||||||||

| 85 | ||||||||

| 87 | ||||||||

| 91 | ||||||||

| 92 | ||||||||

| 96 | ||||||||

| 97 | ||||||||

| 97 | ||||||||

| 97 | ||||||||

| F-1 | ||||||||

Appendix A —Glossary of Terms | A-1 | |||||||

| Consent of KPMG LLP | ||||||||

You should rely only on the information contained in this prospectus or to which we have referred you. We have not authorized anyone to provide you with information that is different from what we have provided to you. This document may only be used where it is legal to sell these securities. The information in this document may only be accurate on the date of this document.

In this prospectus, we use the terms “Basic Energy Services,” “we,” “us” and “our” to refer to Basic Energy Services, Inc. together with its subsidiaries unless the context otherwise requires. The term “distributing stockholders” refers collectively to Fortress Holdings, LLC, Southwest Partners II, L.P. and Southwest Partners III, L.P.

-i-

Table of Contents

PROSPECTUS SUMMARY

This summary highlights information contained elsewhere in this prospectus. You should read the entire prospectus carefully, including the risks discussed in the “Risk Factors” section, the historical consolidated financial statements and notes to those financial statements. This summary may not contain all of the information that investors should consider before investing in our common stock. If you are not familiar with some of the oil and gas industry terms used in this prospectus, please read our Glossary of Terms included as Appendix A to this prospectus.

Our Company

We provide a wide range of well site services to oil and gas drilling and producing companies, including well servicing, fluid services, drilling and completion services and well site construction services. These services are fundamental to establishing and maintaining the flow of oil and gas throughout the productive life of a well. Our broad range of services enables us to meet multiple needs of our customers at the well site. Our operations are managed regionally and are concentrated in the major United States onshore oil and gas producing regions in Texas, New Mexico, Oklahoma and Louisiana and the Rocky Mountain states. We provide our services to a diverse group of over 1,000 oil and gas companies. We operate the third-largest fleet of well servicing rigs (also commonly referred to as workover rigs) in the United States, representing approximately 13% of the overall available U.S. fleet. Our two larger competitors control approximately 31% and 18%, respectively, as of May 2006, according to the Association of Energy Services Companies and other publicly available data. We have expanded our asset base from $53.0 million of total assets as of December 31, 2000 to $497.0 million of total assets as of December 31, 2005 and increased our revenues from $56.5 million in 2000 to $459.8 million in 2005.

We derive a majority of our revenues from services supporting production from existing oil and gas operations. Demand for these production-related services, including well servicing and fluid services, tends to remain relatively stable in moderate oil and gas price environments, as ongoing maintenance spending is required to sustain production. As oil and gas prices reach higher levels, demand for all of our services generally increases as our customers increase spending for drilling new wells and well servicing activities related to maintaining or increasing production from existing wells. The utilization rate for our fleet of well servicing rigs increased from approximately 71% in 2003 to 78% in 2004, 87% in 2005, and 89% in the first quarter of 2006. Because our services are required to support drilling and workover activities, we are also subject to changes in capital spending by our customers as oil and gas prices increase or decrease.

We currently conduct our operations through the following four business segments:

| • | Well Servicing. Our well servicing segment (48% of our revenues in 2005 and 47% of our revenues in the first quarter of 2006) currently operates our fleet of over 330 well servicing rigs and related equipment. This business segment encompasses a full range of services performed with a mobile well servicing rig, including the installation and removal of downhole equipment and elimination of obstructions in the well bore to facilitate the flow of oil and gas. These services are performed to establish, maintain and improve production throughout the productive life of an oil and gas well and to plug and abandon a well at the end of its productive life. Our well servicing equipment and capabilities are essential to facilitate most other services performed on a well. | |

| • | Fluid Services. Our fluid services segment (29% of our revenues in 2005 and 28% of our revenues in the first quarter of 2006) currently utilizes our fleet of over 550 fluid services trucks and related assets, including specialized tank trucks, storage tanks, water wells, disposal facilities and related equipment. These assets provide, transport, store and |

1

Table of Contents

| dispose of a variety of fluids. These services are required in most workover, drilling and completion projects and are routinely used in daily producing well operations. | ||

| • | Drilling and Completion Services. Our drilling and completion services segment (13% of our revenues in 2005 and 18% of our revenues in the first quarter of 2006) currently operates our fleet of 70 pressure pumping units, 29 air compressor packages specially configured for underbalanced drilling operations and 10 cased-hole wireline units. These services are designed to initiate or stimulate oil and gas production. The largest portion of this business consists of pressure pumping services focused on cementing, acidizing and fracturing services in niche markets. We also entered the fishing and rental tool business through an acquisition in the first quarter of 2006. | |

| • | Well Site Construction Services. Our well site construction services segment (10% of our revenues in 2005 and 7% of our revenues in the first quarter of 2006) currently utilizes our fleet of over 200 operated power units, which include dozers, trenchers, motor graders, backhoes and other heavy equipment. We utilize these assets primarily to provide services for the construction and maintenance of oil and gas production infrastructure, such as preparing and maintaining access roads and well locations, installation of small diameter gathering lines and pipelines and construction of temporary foundations to support drilling rigs. |

Our industry historically has consisted of a large number of small companies, several regional contractors and a few large national companies. Over the last decade, our industry has consolidated, including the consolidation of the well servicing segment of our industry, from nine large competitors (with 50 or more well servicing rigs) to four. However, the industry still remains fragmented with an estimated 120 companies owning approximately 900 remaining well servicing rigs, or approximately 26% of the industry’s total fleet. We have led recent consolidation of this industry by acquiring regional businesses and assets in 40 separate acquisitions from the beginning of 2001 through March 31, 2006. We plan to continue participating in the consolidation of our industry by selectively acquiring additional businesses and assets that complement and expand our existing service offerings and geographic footprint and offer attractive projected rates of return on capital employed. However, we cannot assure you that we can complete such acquisitions.

General Industry Overview

Demand for services offered by our industry is a function of our customers’ willingness to make operating and capital expenditures to explore for, develop and produce hydrocarbons in the U.S., which in turn is affected by current and expected levels of oil and gas prices. The following industry statistics illustrate the growing spending dynamic in the U.S. oil and gas sector (including the offshore sector that we do not serve):

| • | With the rebound in oil and gas prices in early 1999, oil and gas companies have increased their drilling and workover activities. The increased activity resulted in increased exploration and production spending compared to the prior year of 16% and 30% in 2004 and 2005, respectively, and is expected to increase 16% in 2006, according to www.WorldOil.com. | |

| • | A survey of 18 U.S. major integrated and 130 independent oil and gas companies by World Oil Magazine projected the U.S. drilling activity in 2006 to be skewed more towards independent players. Specifically, independent oil and gas companies, which represent over 90% of our revenues, are expected to drill 27% more wells in 2006 than in 2005, while the major integrated producers are expected to drill only 16% more wells over the same period. This trend is primarily driven by the increased acquisitions of proved oil and gas properties by independent producers. When these types of properties are acquired, |

2

Table of Contents

| purchasers typically intensify drilling, workover and well maintenance activities to accelerate production from the newly acquired reserves. |

Increased expenditures for exploration and production activities generally involve the deployment of more drilling and well servicing rigs, which often serves as an indicator of demand for our services. Rising oil and gas prices since early 1999 and the corresponding increase in onshore oil exploration and production spending have led to expanded drilling and well service activity, as the U.S. land-based drilling rig count increased approximately 36% fromyear-end 2002 toyear-end 2003, 11% fromyear-end 2003 toyear-end 2004, 22% fromyear-end 2004 toyear-end 2005 and 7% during the first quarter of 2006, according to Baker Hughes. In addition, the U.S. land-based workover rig count increased approximately 13% fromyear-end 2002 toyear-end 2003, 10% fromyear-end 2003 toyear-end 2004, 17% fromyear-end 2004 toyear-end 2005 and 3% during the first quarter of 2006, according to Baker Hughes.

Our business is influenced substantially by both operating and capital expenditures by oil and gas companies. Because existing oil and gas wells require ongoing spending to maintain production, expenditures by oil and gas companies for the maintenance of existing wells are relatively stable and predictable. In contrast, capital expenditures by oil and gas companies for exploration and drilling are more directly influenced by current and expected oil and gas prices and generally reflect the volatility of commodity prices.

Competitive Strengths

We believe that the following competitive strengths currently position us well within our industry:

| • | Significant Market Position. We maintain a significant market share for our well servicing operations in our core operating areas throughout Texas and a growing market share in the other markets that we serve. Our fleet of over 330 well servicing rigs represents the third-largest fleet in the United States, and our goal is to be one of the top two providers of well site services in each of our core operating areas. Our market position allows us to expand the range of services performed on a well throughout its life, such as completion, maintenance, workover and plugging and abandonment services. | |

| • | Modern and Active Fleet. We operate a modern and active fleet of well servicing rigs. We believe over 95% of the active US well servicing rig fleet was built prior to 1985. Approximately 98, or 30%, of our rigs at March 31, 2006 were either 2000 model year or newer, or have undergone major refurbishments during the last four years. Since October 2004, we have taken delivery of 45 newbuild well servicing rigs through March 31, 2006 as part of a102-rig newbuild commitment, driven by our desire to maintain one of the most efficient, reliable and safest fleets in the industry. The remainder of these newbuilds is scheduled to be delivered to us prior to the end of December 2007. Approximately 98% of our fleet was active or available for work and the remainder was awaiting refurbishment at March 31, 2006. Since 2003, we have obtained annual independent reviews and evaluations of substantially all of our assets, which confirmed the location and condition of these assets. | |

| • | Extensive Domestic Footprint in the Most Prolific Basins. Our operations are concentrated in the major United States onshore oil and gas producing regions in Texas, New Mexico, Oklahoma and Louisiana and the Rocky Mountain states. We operate in states that accounted for approximately 57% of the approximately 900,000 existing onshore oil and gas wells in the 48 contiguous states and approximately 77% of onshore oil production and 72% of onshore gas production in 2005. We believe that our operations are located in the most active U.S. well services markets, as we currently focus our operations on onshore domestic oil and gas production areas that include both the highest concentration of existing oil and gas production activities and the largest |

3

Table of Contents

| prospective acreage for new drilling activity. This extensive footprint allows us to offer our suite of services to more than 1,000 customers who are active in those areas and allows us to redeploy equipment between markets as activity shifts. | ||

| • | Diversified Service Offering for Further Revenue Growth. Our experience, equipment and network of over 90 service locations position us to market our full range of well site services to our existing customers. We believe our range of well site services provides us a competitive advantage over smaller companies that typically offer fewer services. By utilizing a wider range of our services, our customers can use fewer service providers, which enables them to reduce their administrative costs and simplify their logistics. Furthermore, offering a broader range of services allows us to capitalize on our existing customer base and management structure to grow within existing markets, generate more business from existing customers, and increase our operating profits as we spread our overhead costs over a larger revenue base. | |

| • | Decentralized Management with Strong Corporate Infrastructure. Our corporate group is responsible for maintaining a unified infrastructure to support our diversified operations through standardized financial and accounting, safety, environmental and maintenance processes and controls. Below our corporate level, we operate a decentralized operational organization in which our seven regional managers are responsible for their regional operations, including asset management, cost control, policy compliance and training and other aspects of quality control. With an average of over 28 years of industry experience, each regional manager has extensive knowledge of the customer base, job requirements and working conditions in each local market. This management structure allows us to monitor operating performance on a daily basis, maintain financial, accounting and asset management controls, integrate acquisitions, prepare timely financial reports and manage contractual risk. |

Our Business Strategy

We intend to increase our shareholder value by pursuing the following strategies:

| • | Establish and Maintain Leadership Position in Core Operating Areas. We strive to establish and maintain market leadership positions within our core operating areas. To achieve this goal, we maintain close customer relationships, seek to expand the breadth of our services and offer high quality services and equipment that meet the scope of customer specifications and requirements. In addition, our significant presence in our core operating areas facilitates employee retention and attraction, a key factor for success in our business. Our significant presence in our core operating areas also provides us with brand recognition that we intend to utilize in creating leading positions in new operating areas. | |

| • | Expand Within Our Regional Markets. We intend to continue strengthening our presence within our existing geographic footprint through internal growth and acquisitions of businesses with strong customer relationships, well-maintained equipment and experienced and skilled personnel. Our larger competitors have not actively pursued acquisitions of small to mid-size regional businesses or assets in recent years due to the small relative scale and financial impact of these potential acquisitions. In contrast, we have successfully pursued these types of acquisitions, which remain attractive to us and make a meaningful impact on our overall operations. | |

| • | Develop Additional Service Offerings Within the Well Servicing Market. We intend to continue broadening the portfolio of services we provide to our clients by leveraging our well servicing infrastructure. Our rigs are often the first equipment to arrive at the well site and typically the last to leave, providing us the opportunity to offer our customers other complementary services. We believe the fragmented nature of the well servicing market |

4

Table of Contents

| creates an opportunity to sell more services to our core customers and to expand our total service offering within each of our markets. We have expanded our suite of services available to our customers and increased our opportunities to cross-sell new services to our core well servicing customers through recent acquisitions and internal growth. We expect to continue to develop or selectively acquire capabilities to provide additional services to expand and further strengthen our customer relationships. | ||

| • | Pursue Growth Through Selective Capital Deployment. We intend to continue growing our business through selective acquisitions, continuing a newbuild program and/or upgrading our existing assets. Our capital investment decisions are determined by an analysis of the projected return on capital employed of each of those alternatives, which is substantially driven by the cost to acquire existing assets from a third party, the capital required to build new equipment and the point in the oil and gas commodity price cycle. Based on these factors, we make capital investment decisions that we believe will support our long-term growth strategy. |

Our strategies could be affected by any of the risk factors described in “Risk Factors” beginning on page 11.

How You Can Contact Us

Our principal executive offices are located at 400 W. Illinois, Suite 800, Midland, Texas 79701, and our telephone number is (432) 620-5500.

Recent Developments

On January 31, 2006, we acquired all of the outstanding capital stock of LeBus Oil Field Service Co. for a total acquisition price of approximately $26 million in cash, subject to adjustment. LeBus, which generated approximately $21 million in revenues in 2005, has 57 fluid services trucks, 225 frac tanks, and six disposal facilities. LeBus provides transportation, storage and disposal of oilfield fluids in the East Texas and North Louisiana regions from its New London and Tenaha, Texas operating locations. This acquisition is indicative of our acquisition strategy to expand within our regional markets.

On February 28, 2006, we purchased substantially all of the operating assets of G&L Tool, Ltd., an oilfield services fishing and rental tool business headquartered in Abilene, Texas, for total consideration of $58 million in cash. The assets acquired from G&L generated approximately $39 million in revenues during 2005. This acquisition provides us entry into the fishing and rental tool business and allows us to pursue complementary and cross-selling opportunities throughout our West and North Texas locations. This acquisition is indicative of our strategy to develop additional service offerings within the well servicing market.

In April 2006, we completed a private offering for $225 million aggregate principal amount of 7.125% Senior Notes due April 15, 2016. The Senior Notes are jointly and severally guaranteed by each of our subsidiaries. The net proceeds from the offering were used to retire the outstanding Term B Loan balance and to pay down the revolving balance under our 2005 Credit Facility. Remaining proceeds will be used for general corporate purposes, including acquisitions. For a description of our 2005 Credit Facility, please read “Management’s Discussion and Analysis of Financial Condition and Results of Operations — Liquidity and Capital Resources — Credit Facilities.”

5

Table of Contents

The Distribution

The 2,101,641 shares of our common stock are being registered to permit a one-time distribution of controlled securities to the partners of Southwest Partners II, L.P. and Southwest Partners III, L.P. and to the members of Fortress Holdings, LLC. Neither we, nor the distributing stockholders will receive any proceeds from this transaction.

The partners and members of the distributing stockholders who will receive shares of our common stock in this registered offering may sell the shares of common stock directly to purchasers or through underwriters, broker-dealers or agents under Section 4(1) of the Securities Act, except to the extent any such partner or member is deemed to be our “affiliate” under Rule 144 of the Securities Act. After receiving shares of our common stock in this offering, the partners and members of the distributing stockholders, to the extent not deemed to be our “affiliate” under Rule 144 of the Securities Act, will act independently of us, and the distributing stockholders, in making decisions regarding the timing, manner and size of each sale of our common stock.

We are not aware of any plans, arrangements or understandings between the partners or members of the distributing stockholders and any underwriter, broker-dealer or agent regarding the sale of the shares of common stock and we do not assure you that the partners or members of the distributing stockholders will sell any or all of the registered shares of common stock following distribution. In addition, we do not assure you that the partners or members will not transfer, devise or gift the shares of common stock by other means not described in this prospectus. Moreover, any securities covered by this prospectus that qualify for sale pursuant to Rule 144 of the Securities Act may be sold under Rule 144 rather than pursuant to this prospectus.

H.H. Wommack, III, one of our directors and an affiliate of the distributing stockholders, will receive shares of common stock in connection with the distributions.

We will not receive any of the net proceeds from the distribution of shares of our common stock by the distributing stockholders. See “Use of Proceeds” and “Plan of Distribution.”

See “Risk Factors” beginning on page 11 of this prospectus for a discussion of factors that you should carefully consider before deciding to invest in shares of our common stock.

6

Table of Contents

Summary Historical Financial Information

The following table sets forth our summary historical financial and operating data for the periods shown. The following information should be read in conjunction with “Capitalization,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our financial statements included elsewhere in this prospectus. The amounts for each historical annual period presented below were derived from our audited financial statements.

| Three Months | ||||||||||||||||||||||

| Ended | ||||||||||||||||||||||

| Year Ended December 31, | March 31, | |||||||||||||||||||||

| 2003 | 2004 | 2005 | 2005 | 2006 | ||||||||||||||||||

| (unaudited) | ||||||||||||||||||||||

| (dollars in thousands, except per share data) | ||||||||||||||||||||||

Statement of Operations Data: | ||||||||||||||||||||||

| Revenues: | ||||||||||||||||||||||

| Well servicing | $ | 104,097 | $ | 142,551 | $ | 221,993 | $ | 44,798 | $ | 73,465 | ||||||||||||

| Fluid services | 52,810 | 98,683 | 132,280 | 29,303 | 43,121 | |||||||||||||||||

| Drilling and completion services | 14,808 | 29,341 | 59,832 | 10,764 | 27,455 | |||||||||||||||||

| Well site construction services | 9,184 | 40,927 | 45,647 | 8,948 | 10,265 | |||||||||||||||||

| Total revenues | 180,899 | 311,502 | 459,752 | 93,813 | 154,306 | |||||||||||||||||

| Expenses: | ||||||||||||||||||||||

| Well servicing | 73,244 | 98,058 | 137,392 | 28,191 | 41,610 | |||||||||||||||||

| Fluid services | 34,420 | 65,167 | 82,551 | 19,238 | 26,305 | |||||||||||||||||

| Drilling and completion services | 9,363 | 17,481 | 30,900 | 5,860 | 13,854 | |||||||||||||||||

| Well site construction services | 6,586 | 31,454 | 32,000 | 7,108 | 7,643 | |||||||||||||||||

| General and administrative(1) | 22,722 | 37,186 | 55,411 | 13,091 | 18,005 | |||||||||||||||||

| Depreciation and amortization | 18,213 | 28,676 | 37,072 | 8,047 | 12,837 | |||||||||||||||||

| Loss (gain) on disposal of assets | 391 | 2,616 | (222 | ) | 102 | (200 | ) | |||||||||||||||

| Total expenses | 164,939 | 280,638 | 375,104 | 81,637 | 120,054 | |||||||||||||||||

| Operating income | 15,960 | 30,864 | 84,648 | 12,176 | 34,252 | |||||||||||||||||

| Other income (expense): | ||||||||||||||||||||||

| Net interest expense | (5,174 | ) | (9,550 | ) | (12,660 | ) | (2,960 | ) | (2,779 | ) | ||||||||||||

| Loss on early extinguishment of debt | (5,197 | ) | — | (627 | ) | — | — | |||||||||||||||

| Other income (expense) | 146 | (398 | ) | 220 | 75 | 27 | ||||||||||||||||

| Income from continuing operations before income taxes | 5,735 | 20,916 | 71,581 | 9,291 | 31,500 | |||||||||||||||||

| Income tax expense | (2,772 | ) | (7,984 | ) | (26,800 | ) | (3,490 | ) | (11,819 | ) | ||||||||||||

| Income from continuing operations | 2,963 | 12,932 | 44,781 | 5,801 | 19,681 | |||||||||||||||||

| Discontinued operations, net of tax | 22 | (71 | ) | — | — | — | ||||||||||||||||

| Cumulative effect of accounting change, net of tax | (151 | ) | — | — | — | — | ||||||||||||||||

| Net income | 2,834 | 12,861 | 44,781 | 5,801 | 19,681 | |||||||||||||||||

| Preferred stock dividend | (1,525 | ) | — | — | — | — | ||||||||||||||||

| Accretion of preferred stock discount | (3,424 | ) | — | — | — | — | ||||||||||||||||

| Net income (loss) available to common stockholders | $ | (2,115 | ) | $ | 12,861 | $ | 44,781 | $ | 5,801 | $ | 19,681 | |||||||||||

| Net income (loss) per share of common stock:(2) | ||||||||||||||||||||||

| Basic | $ | (0.09 | ) | $ | 0.46 | $ | 1.57 | $ | 0.21 | $ | 0.59 | |||||||||||

| Diluted | $ | (0.09 | ) | $ | 0.42 | $ | 1.35 | $ | 0.18 | $ | 0.53 | |||||||||||

7

Table of Contents

| Three Months | |||||||||||||||||||||

| Ended | |||||||||||||||||||||

| Year Ended December 31, | March 31, | ||||||||||||||||||||

| 2003 | 2004 | 2005 | 2005 | 2006 | |||||||||||||||||

| (unaudited) | |||||||||||||||||||||

| (dollars in thousands, except per share data) | |||||||||||||||||||||

Statement of Cash Flow Data: | |||||||||||||||||||||

| Cash flows from operating activities | $ | 29,815 | $ | 46,539 | $ | 99,189 | $ | 16,734 | $ | 25,915 | |||||||||||

| Cash flows from investing activities | (84,903 | ) | (73,587 | ) | (107,679 | ) | (19,946 | ) | (111,584 | ) | |||||||||||

| Cash flows from financing activities | 79,859 | 21,498 | 21,188 | (2,817 | ) | 72,777 | |||||||||||||||

| Capital expenditures: | |||||||||||||||||||||

| Acquisitions, net of cash acquired | 61,885 | 19,284 | 25,378 | 3,909 | 87,520 | ||||||||||||||||

| Property and equipment | 23,501 | 55,674 | 83,095 | 16,083 | 24,812 | ||||||||||||||||

Other Financial Data: | |||||||||||||||||||||

| EBITDA(3) | $ | 28,993 | $ | 59,071 | $ | 121,313 | $ | 20,298 | $ | 47,116 | |||||||||||

| As of December 31, | As of | |||||||||||||||

| March 31, | ||||||||||||||||

| 2003 | 2004 | 2005 | 2006 | |||||||||||||

| (unaudited) | ||||||||||||||||

| (dollars in thousands) | ||||||||||||||||

Balance Sheet Data: | ||||||||||||||||

| Cash and cash equivalents | $ | 25,697 | $ | 20,147 | $ | 32,845 | $ | 19,953 | ||||||||

| Property and equipment, net | 188,243 | 233,451 | 309,075 | 399,865 | ||||||||||||

| Total assets | 302,653 | 367,601 | 496,957 | 616,787 | ||||||||||||

| Total long-term debt, including current portion | 148,509 | 182,476 | 126,887 | 210,047 | ||||||||||||

| Total stockholders’ equity | 107,295 | 121,786 | 258,575 | 278,241 | ||||||||||||

| (1) | Includes approximately $994,000, $1,587,000 and $2,890,000 of non-cash stock-based compensation expense for the years ended December 31, 2003, 2004 and 2005, respectively, and $591,000 and $758,000 for the three months ended March 31, 2005 and 2006, respectively. |

| (2) | Reflects a 5-for-1 stock split effected as a stock dividend in September 2005. |

| (3) | EBITDA means earnings before interest, taxes, depreciation and amortization. EBITDA is used as a supplemental financial measure by our management and directors and by external users of our financial statements, such as investors, to assess: |

| • | the financial performance of our assets without regard to financing methods, capital structure or historical cost basis; | |

| • | the ability of our assets to generate cash sufficient to pay interest on our indebtedness; and | |

| • | our operating performance and return on invested capital as compared to those of other companies in the well services industry, without regard to financing methods and capital structure. |

8

Table of Contents

EBITDA has limitations as an analytical tool and should not be considered an alternative to net income, operating income, cash flow from operating activities or any other measure of financial performance or liquidity presented in accordance with generally accepted accounting principles (GAAP). EBITDA excludes some, but not all, items that affect net income and operating income, and these measures may vary among other companies. Limitations to using EBITDA as an analytical tool include:

| • | EBITDA does not reflect our current or future requirements for capital expenditures or capital commitments; | |

| • | EBITDA does not reflect changes in, or cash requirements necessary to service interest or principal payments on, our debt; | |

| • | EBITDA does not reflect income taxes; | |

| • | although depreciation and amortization are non-cash charges, the assets being depreciated and amortized will often have to be replaced in the future, and EBITDA does not reflect any cash requirements for such replacements; and | |

| • | other companies in our industry may calculate EBITDA differently than we do, limiting its usefulness as a comparative measure. |

The following table presents a reconciliation of EBITDA to net income, which is the most directly comparable GAAP financial performance measure, for each of the periods indicated:

| Three Months | |||||||||||||||||||||

| Ended | |||||||||||||||||||||

| Year Ended December 31, | March 31, | ||||||||||||||||||||

| 2003 | 2004 | 2005 | 2005 | 2006 | |||||||||||||||||

| (unaudited) | |||||||||||||||||||||

| (dollars in thousands) | |||||||||||||||||||||

Reconciliation of EBITDA to Net Income: | |||||||||||||||||||||

| Net income | $ | 2,834 | $ | 12,861 | $ | 44,781 | $ | 5,801 | $ | 19,681 | |||||||||||

| Income taxes | 2,772 | 7,984 | 26,800 | 3,490 | 11,819 | ||||||||||||||||

| Net interest expense | 5,174 | 9,550 | 12,660 | 2,960 | 2,779 | ||||||||||||||||

| Depreciation and amortization | 18,213 | 28,676 | 37,072 | 8,047 | 12,837 | ||||||||||||||||

| EBITDA | $ | 28,993 | $ | 59,071 | $ | 121,313 | $ | 20,298 | $ | 47,116 | |||||||||||

9

Table of Contents

Operating Data

The following table sets forth operating data for our well servicing, fluid services, drilling and completion services and well site construction services segments for the periods shown. The data presented below reflects the following:

| • | we charge our well servicing customers on an hourly basis — rig hours reflect actual billed hours; | |

| • | our rig utilization rate is calculated using a55-hour work week per rig; | |

| • | our fluid services segment includes an array of services billed on an hourly, daily and per barrel basis; accordingly, we believe revenue per truck is the more meaningful information for this measure; and | |

| • | in our drilling and completion services segment, we charge different rates for our pressure pumping trucks based on the type of services performed and varying horsepower requirements, and in our well site construction services segment, we similarly charge different rates for different equipment, in each case making segment profits the most meaningful measure of performance. |

| Three Months | ||||||||||||||||||||

| Year Ended | Ended | |||||||||||||||||||

| December 31, | March 31, | |||||||||||||||||||

| 2003 | 2004 | 2005 | 2005 | 2006 | ||||||||||||||||

Well Servicing | ||||||||||||||||||||

| Weighted average number of rigs | 257 | 279 | 305 | 291 | 327 | |||||||||||||||

| Rig hours (000’s) | 523.9 | 618.8 | 760.7 | 175.3 | 209.0 | |||||||||||||||

| Rig utilization rate | 71.4 | % | 77.8 | % | 87.1 | % | 84.3 | % | 89.4 | % | ||||||||||

| Revenue per rig hour | $ | 199 | $ | 230 | $ | 292 | $ | 255 | $ | 352 | ||||||||||

| Segment profits per rig hour | $ | 59 | $ | 72 | $ | 111 | $ | 94 | $ | 152 | ||||||||||

| Segment profits as a percent of revenue | 29.6 | % | 31.2 | % | 38.1 | % | 37.1 | % | 43.4 | % | ||||||||||

Fluid Services | ||||||||||||||||||||

| Weighted average number of fluid service trucks | 249 | 386 | 455 | 435 | 529 | |||||||||||||||

| Revenue per fluid service truck (000’s) | $ | 212 | $ | 256 | $ | 291 | $ | 67 | $ | 82 | ||||||||||

| Segment profits per fluid service truck (000’s) | $ | 74 | $ | 87 | $ | 109 | $ | 24 | $ | 32 | ||||||||||

| Segment profits as a percent of revenue | 34.8 | % | 34.0 | % | 37.6 | % | 34.3 | % | 39.0 | % | ||||||||||

Drilling and Completion Services | ||||||||||||||||||||

| Segment profits as a percent of revenue | 36.8 | % | 40.4 | % | 48.4 | % | 45.6 | % | 49.5 | % | ||||||||||

Well Site Construction Services | ||||||||||||||||||||

| Segment profits as a percent of revenue | 28.3 | % | 23.1 | % | 29.9 | % | 20.6 | % | 25.5 | % | ||||||||||

Please read “Management’s Discussion and Analysis of Financial Condition and Results of Operations — Well Servicing,” “— Fluid Services,” “— Drilling and Completion Services” and “— Well Site Construction Services” for an analysis of our well servicing, fluid services, drilling and completion and well site construction services.

10

Table of Contents

RISK FACTORS

You should carefully consider the risks described below, as well as the other information included in this prospectus, before making an investment decision to invest in our common stock. If any of these risks were to occur, our business, results of operations or financial condition could be materially and adversely affected. In that case, the trading price of our common stock could decline, and you could lose all or part of your investment.

Risks Related to Our Business

A decline in or substantial volatility of oil and gas prices could adversely affect the demand for our services.

The demand for our services is primarily determined by current and anticipated oil and gas prices and the related general production spending and level of drilling activity in the areas in which we have operations. Volatility or weakness in oil and gas prices (or the perception that oil and gas prices will decrease) affects the spending patterns of our customers and may result in the drilling of fewer new wells or lower production spending on existing wells. This, in turn, could result in lower demand for our services and may cause lower rates and lower utilization of our well service equipment. A decline in oil and gas prices or a reduction in drilling activities could materially and adversely affect the demand for our services and our results of operations.

Prices for oil and gas historically have been extremely volatile and are expected to continue to be volatile. For example, although oil and natural gas prices have recently hit record prices exceeding $70 per barrel and $14.00 per mcf, respectively, oil and natural gas prices fell below $11 per barrel and $2 per mcf, respectively, in early 1999. The Cushing WTI Spot Oil Price averaged $31.08, $41.51, $56.64 and $63.27 per barrel in 2003, 2004, 2005, and the first three months of 2006, respectively, and the average wellhead price for natural gas, as recorded by the Energy Information Agency, was $4.98, $5.49, $7.51 and $7.49 per mcf for 2003, 2004, 2005, and the first three months of 2006, respectively. Commodity prices have increased significantly in recent years, and these prices may not remain at current levels.

Our business depends on domestic spending by the oil and gas industry, and this spending and our business may be adversely affected by industry conditions that are beyond our control.

We depend on our customers’ willingness to make operating and capital expenditures to explore, develop and produce oil and gas in the United States. Customers’ expectations for lower market prices for oil and gas may curtail spending thereby reducing demand for our services and equipment.

Industry conditions are influenced by numerous factors over which we have no control, such as the supply of and demand for oil and gas, domestic and worldwide economic conditions, political instability in oil and gas producing countries and merger and divestiture activity among oil and gas producers. The volatility of the oil and gas industry and the consequent impact on exploration and production activity could adversely impact the level of drilling and workover activity by some of our customers. This reduction may cause a decline in the demand for our services or adversely affect the price of our services. In addition, reduced discovery rates of new oil and gas reserves in our market areas also may have a negative long-term impact on our business, even in an environment of stronger oil and gas prices, to the extent existing production is not replaced and the number of producing wells for us to service declines.

We may not be able to grow successfully through future acquisitions or successfully manage future growth, and we may not be able to effectively integrate the businesses we do acquire.

Our business strategy includes growth through the acquisitions of other businesses. We may not be able to continue to identify attractive acquisition opportunities or successfully acquire

11

Table of Contents

identified targets. In addition, we may not be successful in integrating our current or future acquisitions into our existing operations, which may result in unforeseen operational difficulties or diminished financial performance or require a disproportionate amount of our management’s attention. Even if we are successful in integrating our current or future acquisitions into our existing operations, we may not derive the benefits, such as operational or administrative synergies, that we expected from such acquisitions, which may result in the commitment of our capital resources without the expected returns on such capital. Furthermore, competition for acquisition opportunities may escalate, increasing our cost of making further acquisitions or causing us to refrain from making additional acquisitions. We also must meet certain financial covenants in order to borrow money under our existing credit agreement to fund future acquisitions.

Our auditors have previously identified material weaknesses in our internal controls, and if we fail to develop or maintain an effective system of internal controls, we may not be able to accurately report our financial results or prevent fraud. As a result, investors could lose confidence in our financial reporting, which would harm our business and the trading price of our common stock.

Effective internal controls, including internal control over financial reporting and disclosure controls and procedures, are necessary for us to provide reliable financial reports and effectively prevent fraud and to operate successfully as a public company. If we cannot provide reliable financial reports or prevent fraud, our reputation and operating results could be materially harmed. We have in the past discovered, and may in the future discover, areas of our internal controls that need improvement.

In July 2004, our independent auditors advised our board of directors that they had identified material weaknesses in our internal controls in connection with the audit of our 2003 consolidated financial statements. The material weaknesses noted consisted of an inadequacy of our procedures or errors regarding account reconciliations not being performed timely or properly; formal procedures for establishing certain accounting assumptions, estimates and/or conclusions; and recording of certain expenses in the incorrect period. Our auditors also noted certain other items specific to our operations that they did not consider to be material weaknesses.

To improve our financial accounting organization and processes, we have established an internal audit department and have added new personnel and positions in our accounting and finance organization. We also implemented a new accounting software system throughout our operations during the third quarter of 2004 and adopted additional policies and procedures to address the items noted by our auditors and generally to strengthen our financial reporting system. We believe that as of December 31, 2005, we have remediated the material weaknesses previously identified. However, the process of designing and implementing an effective financial reporting system is a continuous effort that requires us to anticipate and react to changes in our business and the economic and regulatory environments and to expend significant resources to maintain a financial reporting system that is adequate to satisfy our reporting obligations.

We have had only limited operating experience with the improvements we have made to date. We may not be able to implement and maintain adequate controls over our financial processes and reporting in the future, which may require us to restate our financial statements in the future. In addition, we may discover additional past, ongoing or future weaknesses or significant deficiencies in our financial reporting system in the future. Any failure to implement required new or improved controls, or difficulties encountered in their implementation, could cause us to fail to meet our reporting obligations or result in material misstatements in our financial statements. Any such failure also could adversely affect the results of the periodic management evaluations and annual auditor attestation reports regarding the effectiveness of our “internal control over financial reporting” that will be required when the SEC’s rules under

12

Table of Contents

Section 404 of the Sarbanes-Oxley Act of 2002 become applicable to us beginning with our Annual Report on Form 10-K for the year ending December 31, 2006 to be filed in the first quarter of 2007. Inferior internal controls could also cause investors to lose confidence in our reported financial information, which could result in a lower trading price of our common stock.

We may require additional capital in the future. We cannot assure you that we will be able to generate sufficient cash internally or obtain alternative sources of capital on favorable terms, if at all. If we are unable to fund capital expenditures our business may be adversely affected.

We anticipate that we will continue to make substantial capital investments to purchase additional equipment to expand our services, refurbish our well servicing rigs and replace existing equipment. For the year ended December 31, 2005, we invested approximately $83.1 million in cash for capital investments, excluding acquisitions. During the first quarter of 2006, we made capital expenditures of approximately $30.0 million, and we expect to spend a total of approximately $93 million in cash capital expenditures during fiscal year 2006, excluding acquisitions. Historically, we have financed these investments through internally generated funds, debt and equity offerings, our capital lease program and our secured credit facilities. These significant capital investments require cash that we could otherwise apply to other business needs. However, if we do not incur these expenditures while our competitors make substantial fleet investments, our market share may decline and our business may be adversely affected. In addition, if we are unable to generate sufficient cash internally or obtain alternative sources of capital to fund our proposed capital expenditures, acquisitions, take advantage of business opportunities or respond to competitive pressures, it could materially adversely affect our results of operations, financial condition and growth. If we raise additional funds by issuing equity securities, dilution to existing stockholders may result.

Competition within the well services industry may adversely affect our ability to market our services.

The well services industry is highly competitive and fragmented and includes numerous small companies capable of competing effectively in our markets on a local basis as well as several large companies that possess substantially greater financial and other resources than we do. Our larger competitors’ greater resources could allow those competitors to compete more effectively than we can. The amount of equipment available may exceed demand, which could result in active price competition. Many contracts are awarded on a bid basis, which may further increase competition based primarily on price. In addition, recent market conditions have stimulated the reactivation of well servicing rigs and construction of new equipment, which could result in excess equipment and lower utilization rates in future periods.

We depend on several significant customers, and a loss of one or more significant customers could adversely affect our results of operations.

Our customers consist primarily of major and independent oil and gas companies. During 2005 and the first three months of 2006, our top five customers accounted for 16% and 14%, respectively, of our revenues. The loss of any one of our largest customers or a sustained decrease in demand by any of such customers could result in a substantial loss of revenues and could have a material adverse effect on our results of operations.

We are dependent on particular suppliers for our newbuild rig program and are vulnerable to delayed deliveries and future price increases.

We currently purchase our well servicing rigs from a single supplier as part of a 102-rig commitment for rigs to be delivered through the end of December 2007, of which 45 rigs have been delivered as of March 31, 2006. There is also a limited number of suppliers that manufacture this type of equipment. Although pricing is generally fixed for this newbuild contract

13

Table of Contents

and program, future price increases could affect our ability to continue to increase the number of newbuild rigs in our fleet at economic levels. In addition, the failure of our current supplier to timely deliver the newbuild rigs could adversely affect our budgeted or projected financial and operational data.

Our industry has experienced a high rate of employee turnover. Any difficulty we experience replacing or adding personnel could adversely affect our business.

We may not be able to find enough skilled labor to meet our needs, which could limit our growth. Our business activity historically decreases or increases with the price of oil and gas. We may have problems finding enough skilled and unskilled laborers in the future if the demand for our services increases. We have raised wage rates to attract workers from other fields and to retain or expand our current work force during the past year. If we are not able to increase our service rates sufficiently to compensate for wage rate increases, our operating results may be adversely affected.

Other factors may also inhibit our ability to find enough workers to meet our employment needs. Our services require skilled workers who can perform physically demanding work. As a result of our industry volatility and the demanding nature of the work, workers may choose to pursue employment in fields that offer a more desirable work environment at wage rates that are competitive with ours. We believe that our success is dependent upon our ability to continue to employ and retain skilled technical personnel. Our inability to employ or retain skilled technical personnel generally could have a material adverse effect on our operations.

Our success depends on key members of our management, the loss of any of whom could disrupt our business operations.

We depend to a large extent on the services of some of our executive officers. The loss of the services of Kenneth V. Huseman, our President and Chief Executive Officer, or other key personnel could disrupt our operations. Although we have entered into employment agreements with Mr. Huseman and our other executive officers that contain, among other provisions, non-compete agreements, we may not be able to enforce the non-compete provisions in the employment agreements.

Our operations are subject to inherent risks, some of which are beyond our control. These risks may not be fully covered under our insurance policies.

Our operations are subject to hazards inherent in the oil and gas industry, such as, but not limited to, accidents, blowouts, explosions, craterings, fires and oil spills. These conditions can cause:

| • | personal injury or loss of life; | |

| • | damage to or destruction of property, equipment and the environment; and | |

| • | suspension of operations. |

The occurrence of a significant event or adverse claim in excess of the insurance coverage that we maintain or that is not covered by insurance could have a material adverse effect on our financial condition and results of operations. In addition, claims for loss of oil and gas production and damage to formations can occur in the well services industry. Litigation arising from a catastrophic occurrence at a location where our equipment and services are being used may result in us being named as a defendant in lawsuits asserting large claims.

We maintain insurance coverage that we believe to be customary in the industry against these hazards. However, we do not have insurance against all foreseeable risks, either because insurance is not available or because of the high premium costs. We are also self-insured up to

14

Table of Contents

retention limits with regard to workers’ compensation and medical and dental coverage of our employees and, with certain exceptions, we generally maintain no physical property damage coverage on our workover rig fleet. We maintain accruals in our consolidated balance sheets related to self-insurance retentions by using third-party data and historical claims history. The occurrence of an event not fully insured against, or the failure of an insurer to meet its insurance obligations, could result in substantial losses. In addition, we may not be able to maintain adequate insurance in the future at rates we consider reasonable. Insurance may not be available to cover any or all of these risks, or, even if available, it may be inadequate, or insurance premiums or other costs could rise significantly in the future so as to make such insurance prohibitive. It is likely that, in our insurance renewals, our premiums and deductibles will be higher, and certain insurance coverage either will be unavailable or considerably more expensive than it has been in the recent past. In addition, our insurance is subject to coverage limits and some policies exclude coverage for damages resulting from environmental contamination.

We are subject to federal, state and local regulation regarding issues of health, safety and protection of the environment. Under these regulations, we may become liable for penalties, damages or costs of remediation. Any changes in laws and government regulations could increase our costs of doing business.

Our operations are subject to federal, state and local laws and regulations relating to protection of natural resources and the environment, health and safety, waste management, and transportation of waste and other materials. Our fluid services segment includes disposal operations into injection wells that pose some risks of environmental liability, including leakage from the wells to surface or subsurface soils, surface water or groundwater. Liability under these laws and regulations could result in cancellation of well operations, fines and penalties, expenditures for remediation, and liability for property damage and personal injuries. Sanctions for noncompliance with applicable environmental laws and regulations also may include assessment of administrative, civil and criminal penalties, revocation of permits and issuance of corrective action orders.

Laws protecting the environment generally have become more stringent over time and are expected to continue to do so, which could lead to material increases in costs for future environmental compliance and remediation. The modification or interpretation of existing laws or regulations, or the adoption of new laws or regulations, could curtail exploratory or developmental drilling for oil and gas and could limit well servicing opportunities. Some environmental laws and regulations may impose strict liability, which means that in some situations we could be exposed to liability as a result of our conduct that was lawful at the time it occurred or conduct of, or conditions caused by, prior operators or other third parties.Clean-up costs and other damages arising as a result of environmental laws, and costs associated with changes in environmental laws and regulations could be substantial and could have a material adverse effect on our financial condition. Please read “Business — Environmental Regulation” for more information on the environmental laws and government regulations that are applicable to us.

Our indebtedness could restrict our operations and make us more vulnerable to adverse economic conditions.

As of May 31, 2006, our total debt was $249.6 million, including $225.0 million of Senior Notes due 2016 and capital lease obligations in the aggregate amount of $24.6 million. Our Senior Notes due 2016 bear interest at 7.125%, payable semi-annually in arrears on April 15 and October 15 of each year, starting October 15, 2006. In addition, as of May 31, 2006, we had $9.6 million of letters of credit outstanding and availability for up to $140.4 million of additional borrowings under our 2005 Credit Facility and the potential to expand term or revolving borrowings under our 2005 Credit Facility by up to an additional $75 million.

15

Table of Contents

Our current and future indebtedness could have important consequences to you. For example, it could:

| • | impair our ability to make investments and obtain additional financing for working capital, capital expenditures, acquisitions or other general corporate purposes; | |

| • | limit our ability to use operating cash flow in other areas of our business because we must dedicate a substantial portion of these funds to make principal and interest payments on our indebtedness; | |

| • | make us more vulnerable to a downturn in our business, our industry or the economy in general as a substantial portion of our operating cash flow will be required to make principal and interest payments on our indebtedness, making it more difficult to react to changes in our business and in industry and market conditions; | |

| • | limit our ability to obtain additional financing that may be necessary to operate or expand our business; | |

| • | put us at a competitive disadvantage to competitors that have less debt; and | |

| • | increase our vulnerability to interest rate increases to the extent that we incur variable rate indebtedness. |

If we are unable to generate sufficient cash flow or are otherwise unable to obtain the funds required to make principal and interest payments on our indebtedness, or if we otherwise fail to comply with the various covenants in our 2005 Credit Facility, the indenture governing our Senior Notes or other instruments governing any future indebtedness, we could be in default under the terms of our 2005 Credit Facility, the indenture governing our Senior Notes or such instruments. In the event of a default, the holders of our indebtedness could elect to declare all the funds borrowed under those instruments to be due and payable together with accrued and unpaid interest, the lenders under our 2005 Credit Facility could elect to terminate their commitments thereunder and we or one or more of our subsidiaries could be forced into bankruptcy or liquidation. Any of the foregoing consequences could restrict our ability to grow our business and cause the value of our common stock to decline.

| Our 2005 Credit Facility and the indenture governing our Senior Notes impose restrictions on us that may affect our ability to successfully operate our business. |

Our 2005 Credit Facility and the indenture governing our Senior Notes limit our ability to take various actions, such as:

| • | limitations on the incurrence of additional indebtedness; | |

| • | restrictions on mergers, sales or transfer of assets without the lenders’ consent; and | |

| • | limitation on dividends and distributions. |

In addition, our 2005 Credit Facility requires us to maintain certain financial ratios and to satisfy certain financial conditions and covenants, several of which become more restrictive over time and may require us to reduce our debt or take some other action in order to comply with them. The failure to comply with any of these financial conditions, financial ratios or covenants would cause a default under our 2005 Credit Facility. A default, if not waived, could result in acceleration of the outstanding indebtedness under our 2005 Credit Facility, in which case the debt would become immediately due and payable. In addition, a default or acceleration of indebtedness under our 2005 Credit Facility could result in a default or acceleration of our Senior Notes or other indebtedness with cross-default or cross-acceleration provisions. If this occurs, we may not be able to pay our debt or borrow sufficient funds to refinance it. Even if new financing is available, it may not be available on terms that are acceptable to us. These restrictions could also limit our ability to obtain future financings, make needed capital

16

Table of Contents

expenditures, withstand a downturn in our business or the economy in general, or otherwise conduct necessary corporate activities. We also may be prevented from taking advantage of business opportunities that arise because of the limitations imposed on us by the restrictive covenants under our 2005 Credit Facility. Please read “Management’s Discussion and Analysis of Financial Condition and Results of Operations — Liquidity and Capital Resources — Credit Facilities — 2005 Credit Facility” for a discussion of our 2005 Credit Facility.

| One of our directors may have a conflict of interest because he is also currently an affiliate, director or officer of a private equity firm that makes investments in the energy sector. The resolution of this conflict of interest may not be in our or our stockholders’ best interests. |

Steven A. Webster, the Chairman of our Board of Directors, is the Co-Managing Partner of Avista Capital Holdings, L.P., a private equity firm that makes investments in the energy sector. This relationship may create a conflict of interest because of his responsibilities to Avista and its owners. His duties as a partner in, or director or officer of, Avista or its affiliates may conflict with his duties as a director of our company regarding corporate opportunities and other matters. The resolution of this conflict may not always be in our or our stockholders’ best interest.

Risks Related to our Relationship with DLJ Merchant Banking

| Affiliates of DLJ Merchant Banking will have a substantial influence on the outcome of stockholder voting and may exercise this voting power in a manner that may not be in the best interest of our other stockholders. |

As of May 18, 2006, DLJ Merchant Banking Partners III, L.P. and affiliated funds (“DLJ Merchant Banking”), which are managed by affiliates of Credit Suisse, a Swiss Bank, and Credit Suisse Securities (USA) LLC, beneficially owned approximately 47.4% of our outstanding common stock. After giving effect to the shares to be sold in this offering, DLJ Merchant Banking will beneficially own approximately 26.9% of our outstanding common stock (or approximately 23.8% if the underwriters’ over-allotment option is exercised in full), although DLJ Merchant Banking will own only approximately 17.5% of our outstanding shares of common stock (or approximately 14.0% if the underwriters’ over-allotment option is exercised in full) due to their ownership of warrants that would not entitle DLJ Merchant Banking to vote unless the warrants were exercised for shares. Nonetheless, DLJ Merchant Banking is in a position to have a substantial influence on the outcome of matters requiring a stockholder vote, including the election of directors, adoption of amendments to our certificate of incorporation or bylaws or approval of transactions involving a change of control. The interests of DLJ Merchant Banking may differ from those of our other stockholders, and DLJ Merchant Banking may vote its common stock in a manner that may not be in the best interest of the other stockholders.

Risks Related to this Distribution

| Certain stockholders’ shares are restricted from immediate resale but may be sold into the market in the near future. This could cause the market price of our common stock to drop significantly. |

As of July 24, 2006, we had outstanding 33,827,105 shares of common stock. In addition to shares issuable upon the exercise of options issued under our 2003 Incentive Plan, there are 4,350,000 shares that may be issued upon the exercise of warrants held by DLJ Merchant Banking. Of these outstanding shares, after this distribution, 17,708,335 shares will be freely tradable without restriction under the Securities Act except for any shares purchased by one of our “affiliates” as defined in Rule 144 under the Securities Act.

After this distribution, the holders of 13,709,424 shares (not including shares issuable upon the exercise of warrants held by DLJ Merchant Banking) will have rights, subject to some limited conditions, to demand that we include their shares in registration statements that we file on their

17

Table of Contents

behalf, on our behalf or on behalf of other stockholders. By exercising their registration rights and selling a large number of shares, these holders could cause the price of our common stock to decline. Furthermore, if we file a registration statement to offer additional shares of our common stock and have to include shares held by those holders, it could impair our ability to raise needed capital by depressing the price at which we could sell our common stock.

| Our certificate of incorporation and bylaws, as well as Delaware law, contain provisions that could discourage acquisition bids or merger proposals, which may adversely affect the market price of our common stock. |

Our certificate of incorporation authorizes our board of directors to issue preferred stock without stockholder approval. If our board of directors elects to issue preferred stock, it could be more difficult for a third party to acquire us. In addition, some provisions of our certificate of incorporation and bylaws could make it more difficult for a third party to acquire control of us, even if the change of control would be beneficial to our stockholders, including:

| • | a classified board of directors, so that only approximately one-third of our directors are elected each year; | |

| • | limitations on the removal of directors; | |

| • | the prohibition of stockholder action by written consent; and | |

| • | limitations on the ability of our stockholders to call special meetings and establish advance notice provisions for stockholder proposals and nominations for elections to the board of directors to be acted upon at meetings of stockholders. |

Delaware law prohibits us from engaging in any business combination with any “interested stockholder,” meaning generally that a stockholder who beneficially owns more than 15% of our stock cannot acquire us for a period of three years from the date this person became an interested stockholder, unless various conditions are met, such as approval of the transaction by our board of directors.

| Because we have no plans to pay dividends on our common stock, investors must look solely to stock appreciation for a return on their investment in us. |

We do not anticipate paying any cash dividends on our common stock in the foreseeable future. We currently intend to retain all future earnings to fund the development and growth of our business. Any payment of future dividends will be at the discretion of our board of directors and will depend on, among other things, our earnings, financial condition, capital requirements, level of indebtedness, statutory and contractual restrictions applying to the payment of dividends and other considerations that the board of directors deems relevant. The terms of our 2005 Credit Facility and the indenture governing our Senior Notes may restrict the payment of dividends without the prior written consent of the lenders. Investors must rely on sales of their common stock after price appreciation, which may never occur, as the only way to realize a return on their investment. Investors seeking cash dividends should not purchase our common stock.

| If our stock price declines after this distribution, you could lose a significant part of your investment. |

The market price of our common stock could be subject to wide fluctuations in response to a number of factors, most of which we cannot control, including:

| • | changes in securities analysts’ recommendations and their estimates of our financial performance; |

18

Table of Contents

| • | the public’s reaction to our press releases, announcements and our filings with the Securities and Exchange Commission; | |

| • | fluctuations in broader stock market prices and volumes, particularly among securities of oil and gas service companies; | |

| • | changes in market valuations of similar companies; | |

| • | additions or departures of key personnel; | |

| • | commencement of or involvement in litigation; | |

| • | announcements by us or our competitors of strategic alliances, significant contracts, new technologies, acquisitions, commercial relationships, joint ventures or capital commitments; | |

| • | variations in our quarterly results of operations or cash flows or those of other oil and gas service companies; | |

| • | changes in our pricing policies or pricing policies of our competitors; | |

| • | future issuances and sales of our common stock; and | |

| • | changes in general conditions in the U.S. economy, financial markets or the oil and gas industry. |

In recent years, the stock market has experienced extreme price and volume fluctuations. This volatility has had a significant effect on the market price of securities issued by many companies for reasons unrelated to the operating performance of these companies. These market fluctuations may also result in a lower price of our common stock.

19

Table of Contents

FORWARD-LOOKING STATEMENTS AND INDUSTRY DATA

This prospectus contains certain statements that are, or may be deemed to be, “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended. We have based these forward-looking statements largely on our current expectations and projections about future events and financial trends affecting the financial condition of our business. These forward-looking statements are subject to a number of risks, uncertainties and assumptions, including, among other things, the risk factors discussed in this prospectus and other factors, most of which are beyond our control.

The words “believe,” “may,” “estimate,” “continue,” “anticipate,” “intend,” “plan,” “expect” and similar expressions are intended to identify forward-looking statements. All statements other than statements of current or historical fact contained in this prospectus are forward-looking statements.

Although we believe that the forward-looking statements contained in this prospectus are based upon reasonable assumptions, the forward-looking events and circumstances discussed in this prospectus may not occur and actual results could differ materially from those anticipated or implied in the forward-looking statements.

Important factors that may affect our expectations, estimates or projections include:

| • | a decline in or substantial volatility of oil and gas prices, and any related changes in expenditures by our customers; | |

| • | the effects of future acquisitions on our business; | |

| • | changes in customer requirements in markets or industries we serve; | |

| • | competition within our industry; | |

| • | general economic and market conditions; | |

| • | our access to current or future financing arrangements; | |

| • | our ability to replace or add workers at economic rates; and | |

| • | environmental and other governmental regulations. |

Our forward-looking statements speak only as of the date of this prospectus. Unless otherwise required by law, we undertake no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise.

This prospectus includes market share, industry data and forecasts that we obtained from internal company surveys (including estimates based on our knowledge and experience in the industry in which we operate), market research, consultant surveys, publicly available information, industry publications and surveys. These sources include Oil & Gas Journal magazine, World Oil magazine, Baker Hughes Incorporated, the Association of Energy Service Companies, and the Energy Information Administration of the U.S. Department of Energy. Industry surveys, publications, consultant surveys and forecasts generally state that the information contained therein has been obtained from sources believed to be reliable. Although we believe such information is accurate and reliable, we have not independently verified any of the data from third-party sources cited or used for our management’s industry estimates, nor have we ascertained the underlying economic assumptions relied upon therein. For example, the number of onshore well servicing rigs in the U.S. could be lower than our estimate to the extent our two larger competitors have continued to report as stacked rigs equipment that is not actually complete or subject to refurbishment. Statements as to our position relative to our competitors or as to market share refer to the most recent available data.

20

Table of Contents

PLAN OF DISTRIBUTION

The shares of our common stock are being registered to permit a one time distribution of controlled securities to the partners of Southwest Partners II, L.P. and Southwest Partners III, L.P. and to the members of Fortress Holdings, LLC. Neither we, nor the distributing stockholders will receive any proceeds from this transaction.

The partners and members of the distributing stockholders who will receive shares of our common stock in this registered offering may sell the shares of common stock directly to purchasers or through underwriters, broker-dealers or agents under Section 4(1) of the Securities Act, except to the extent any such partner or member is deemed to be our “affiliate” under Rule 144 of the Securities Act. After receiving shares of our common stock in this offering, the partners and members of the distributing stockholders, to the extent not deemed to be our “affiliate” under Rule 144 of the Securities Act, will act independently of us, and the distributing stockholders, in making decisions regarding the timing, manner and size of each sale of our common stock.