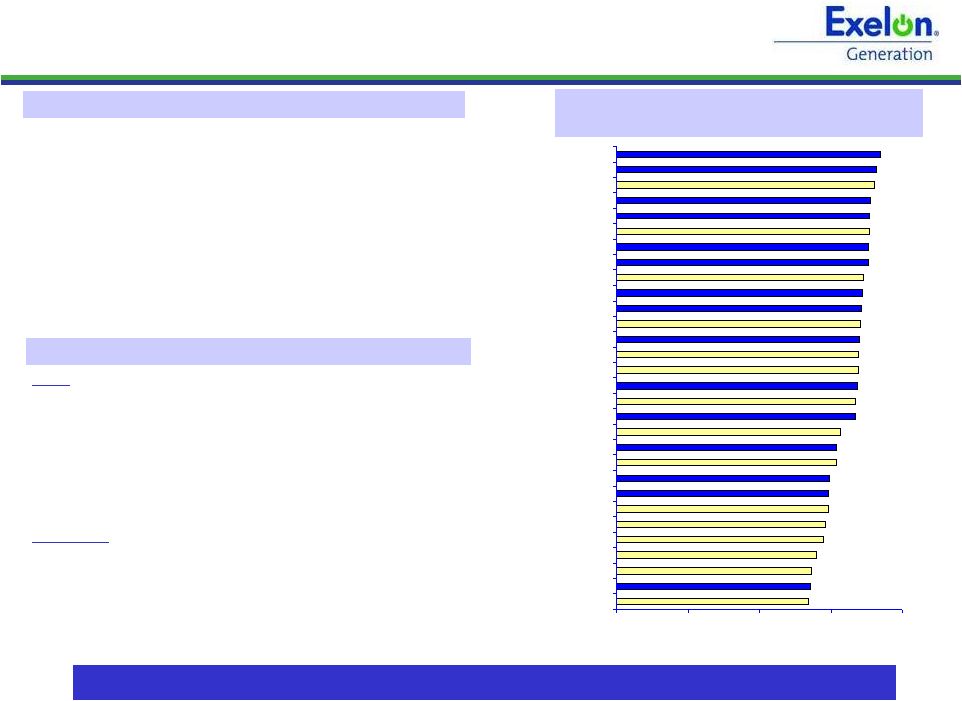

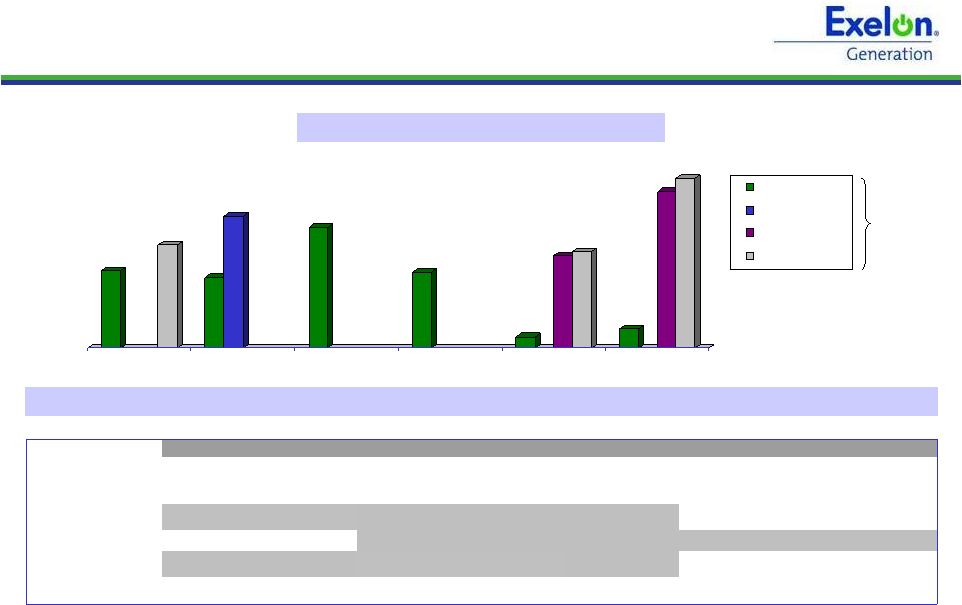

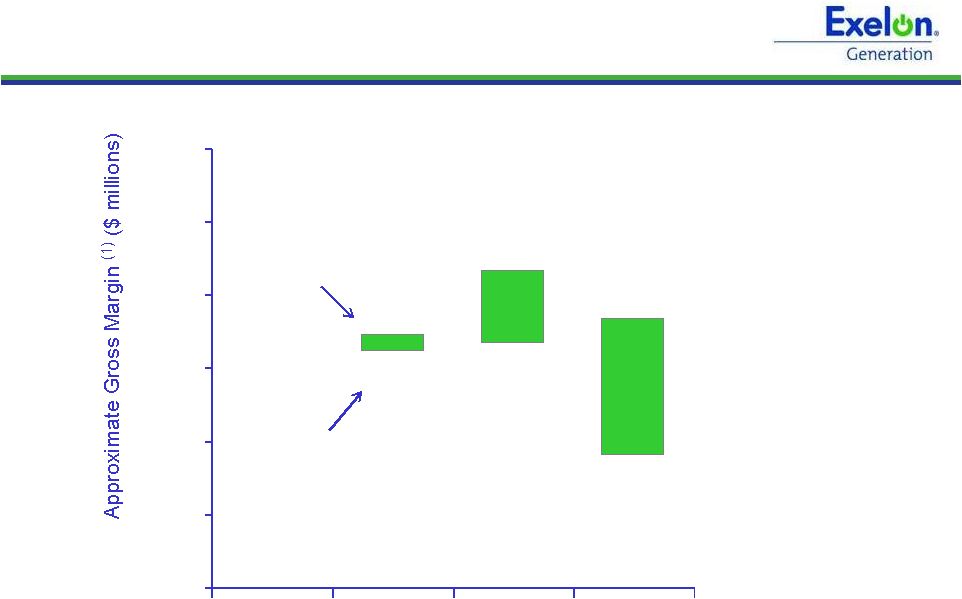

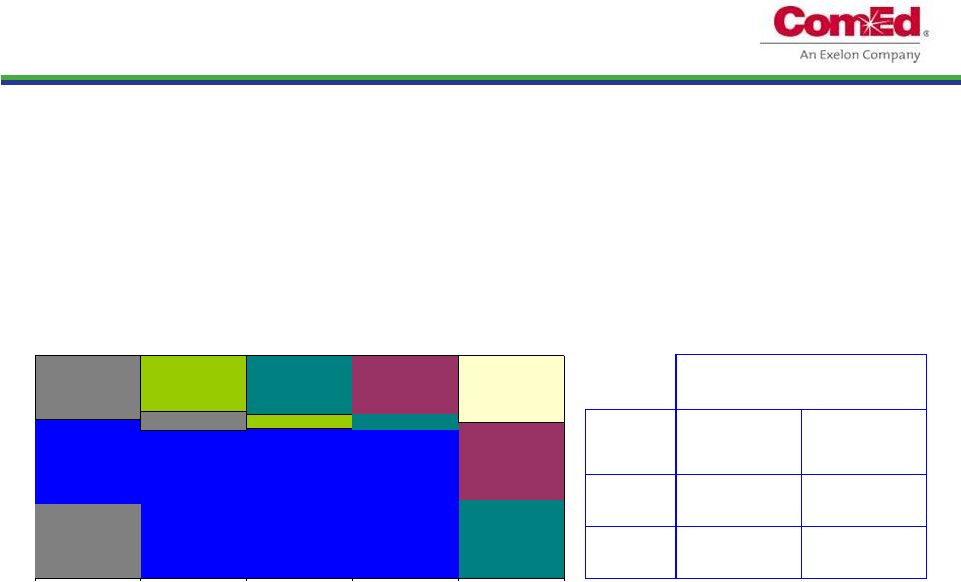

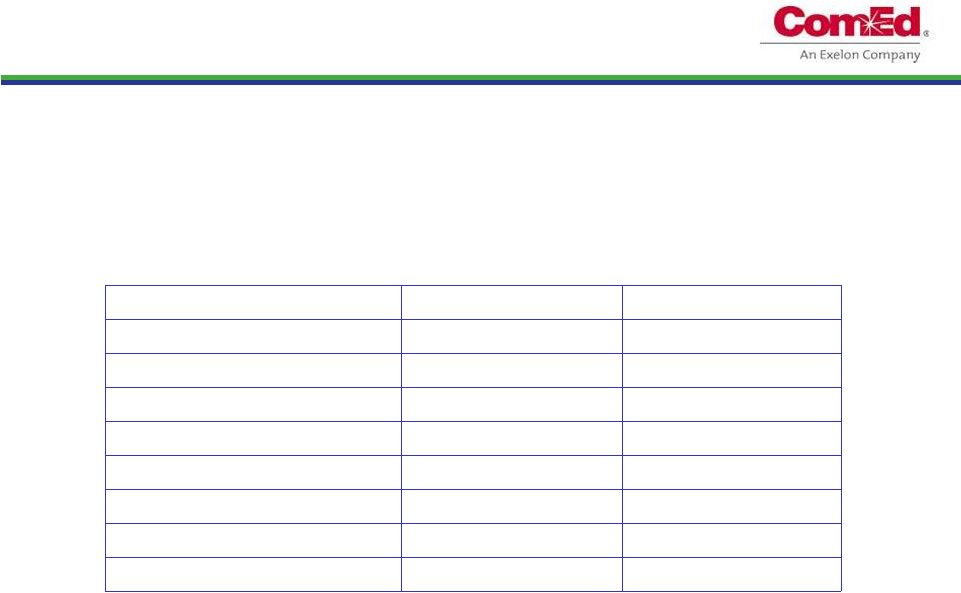

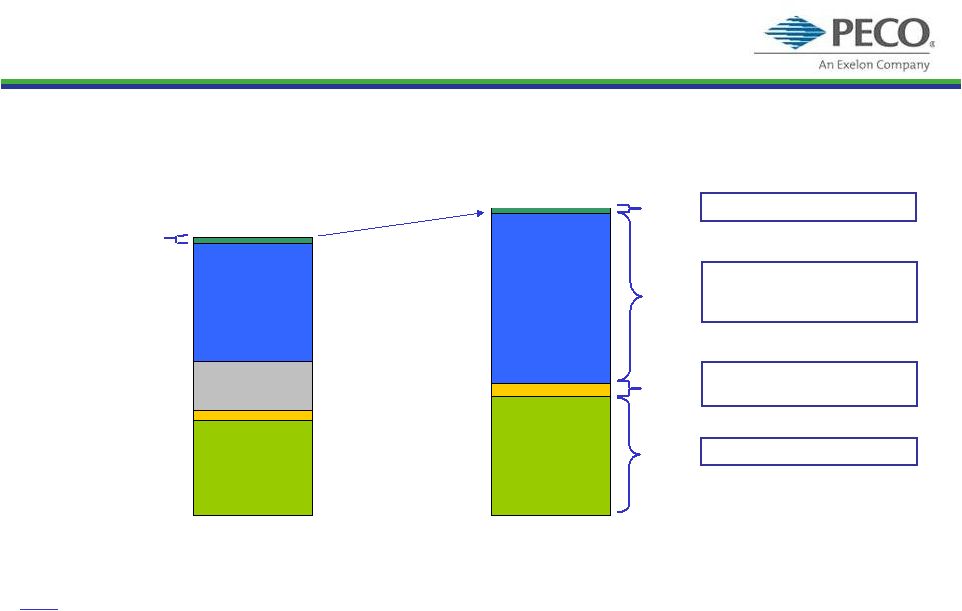

40 PECO Procurement RFP being held on May 24, 2010, results will be public 30 days thereafter; next RFP to be held on September 20, 2010 (1) See PECO Procurement website (http://www.pecoprocurement.com) for additional details regarding PECO’s procurement plan and RFP results. (2) Wholesale prices; no Small/Medium Commercial products were procured in the June 2009 RFP. (3) For Large C&I customers who have opted to participate in the fixed-priced full requirements product. Residential Sept ’09 RFP average price of $79.96/MWh (2) June ’09 RFP average price of $88.61/MWh (2) 49% of full requirements product procured 80 MW of block energy procured Small and Medium Commercial Sept ’09 RFP average blended price of $85.85/MWh (2) 24% of Small Commercial full requirements product procured 16% of Medium Commercial full requirements product procured 85% full requirements 15% full requirements spot Medium Commercial (peak demand >100 kW but <= 500 kW) fixed-priced full requirements (3) Hourly full requirements Large Commercial & Industrial (peak demand >500 kW) 90% full requirements 10% full requirements spot 75% full requirements 20% block energy 5% energy only spot Products Small Commercial (peak demand <100 kW) Residential Customer Class PECO Procurement Plan (1) 2011 Supply procured to date (including June and September 2009 RFPs) Large Commercial and Industrial 100% of planned fixed - price full requirements contracts (12-mo. term) Residential 23% of planned full requirements contracts (17 and 29-mo. terms) 140 MW of baseload (24x7) block energy products (12, 24 and 60-mo. duration) 40 MW of Jan-Feb 2011 on-peak block energy Small Commercial 36% of planned full requirements contracts (17 and 29-mo. term) Medium Commercial 42% of planned full requirements contracts (17-mo. term) May 24, 2010 RFP |