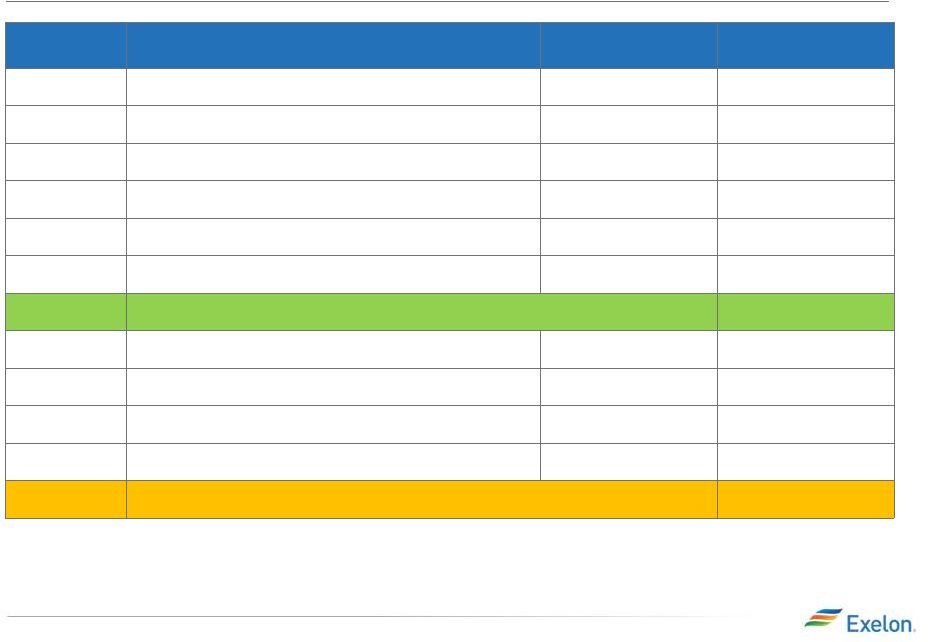

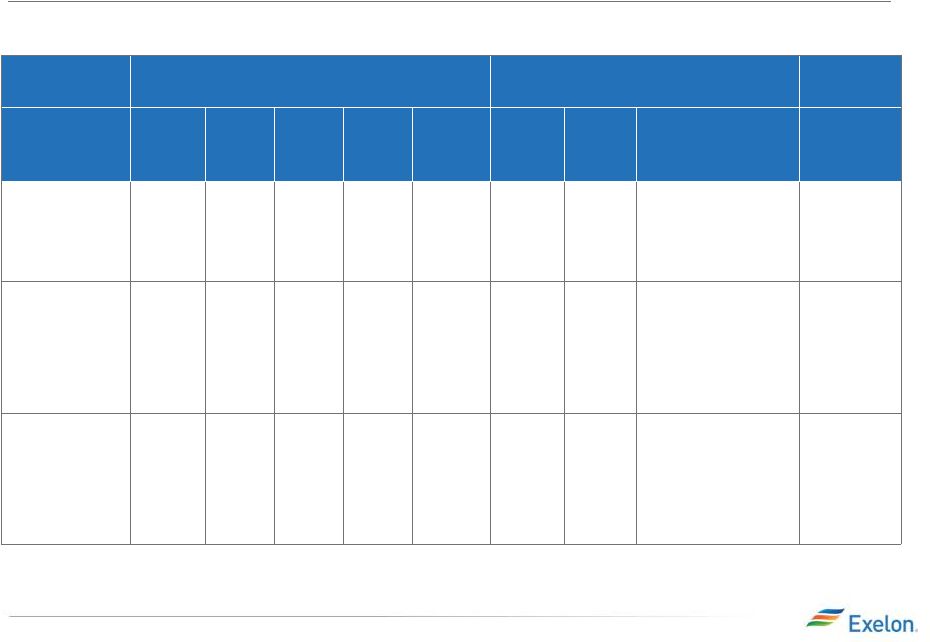

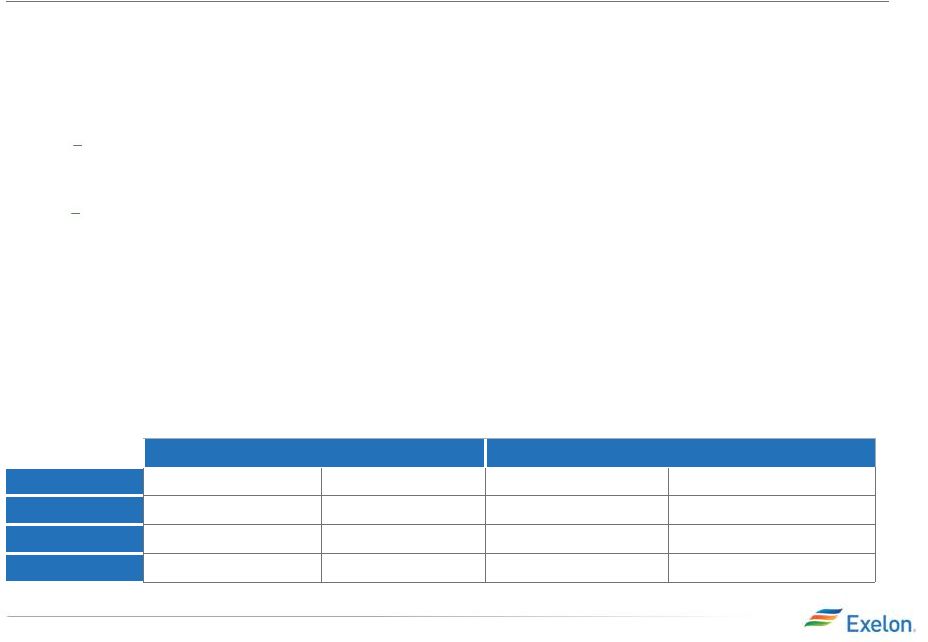

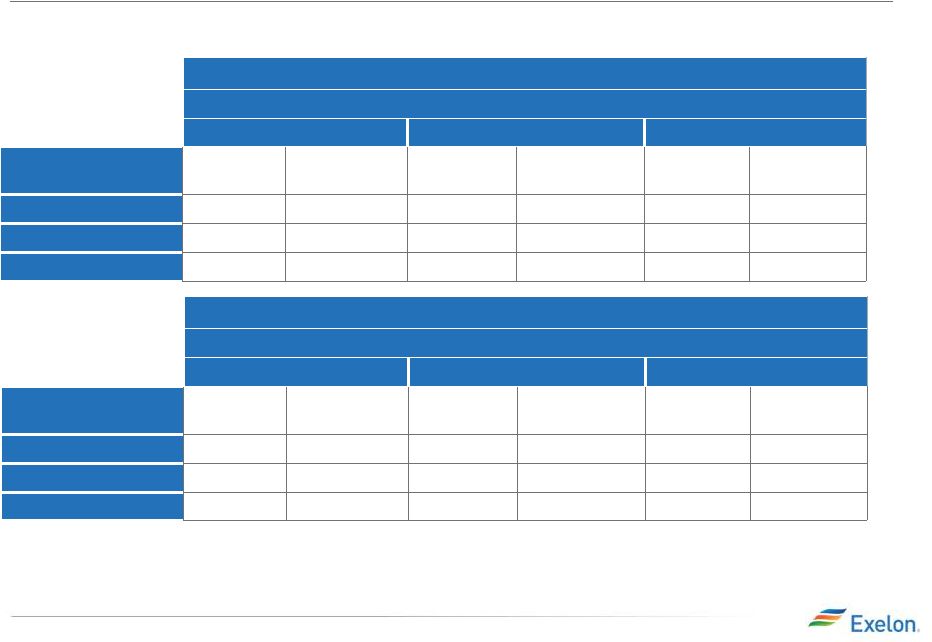

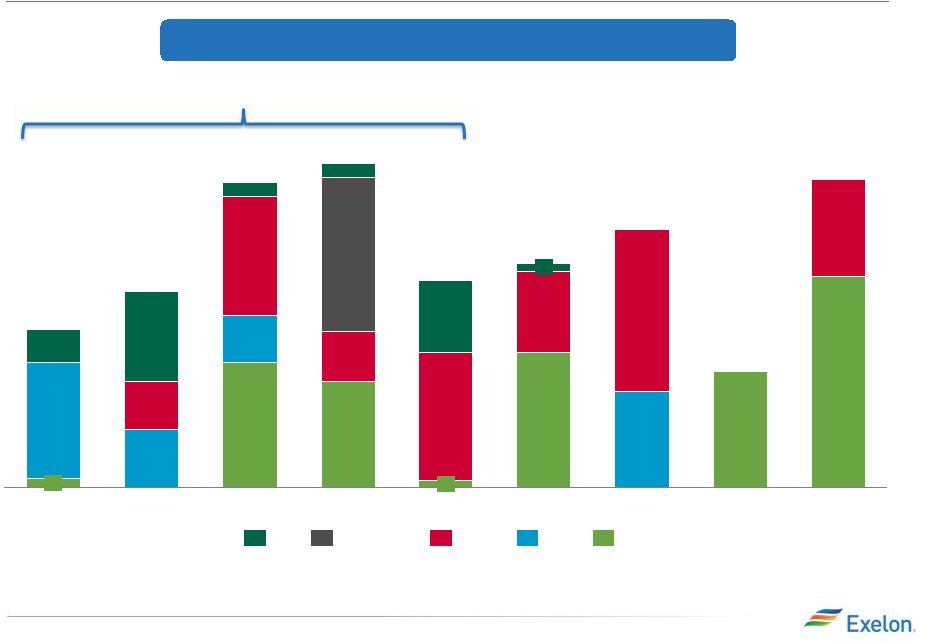

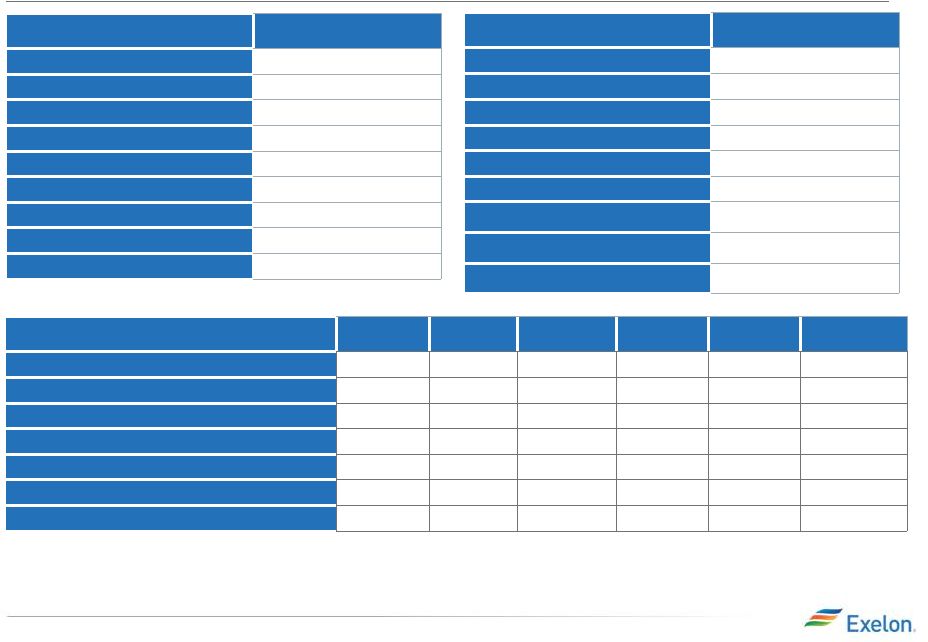

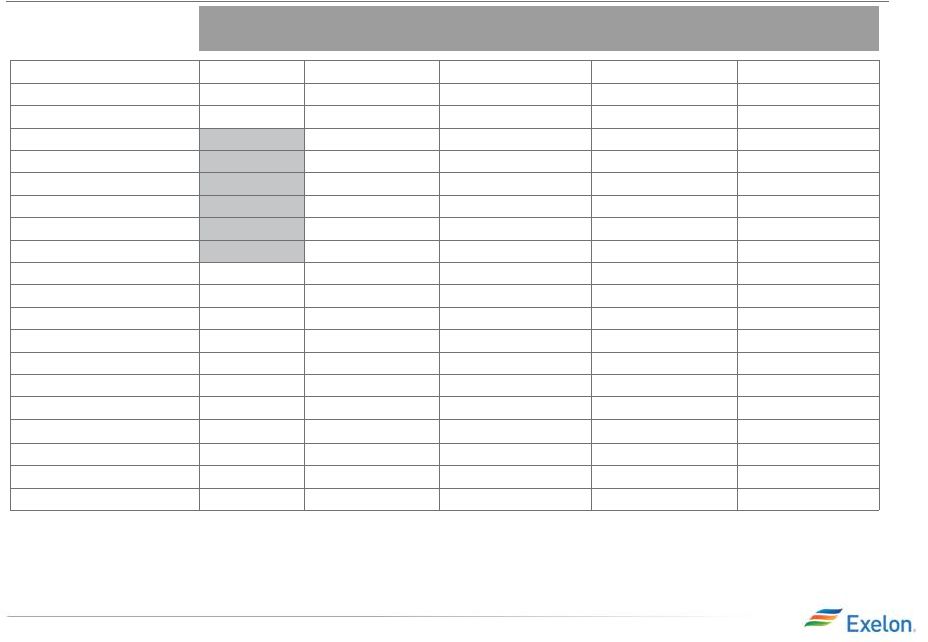

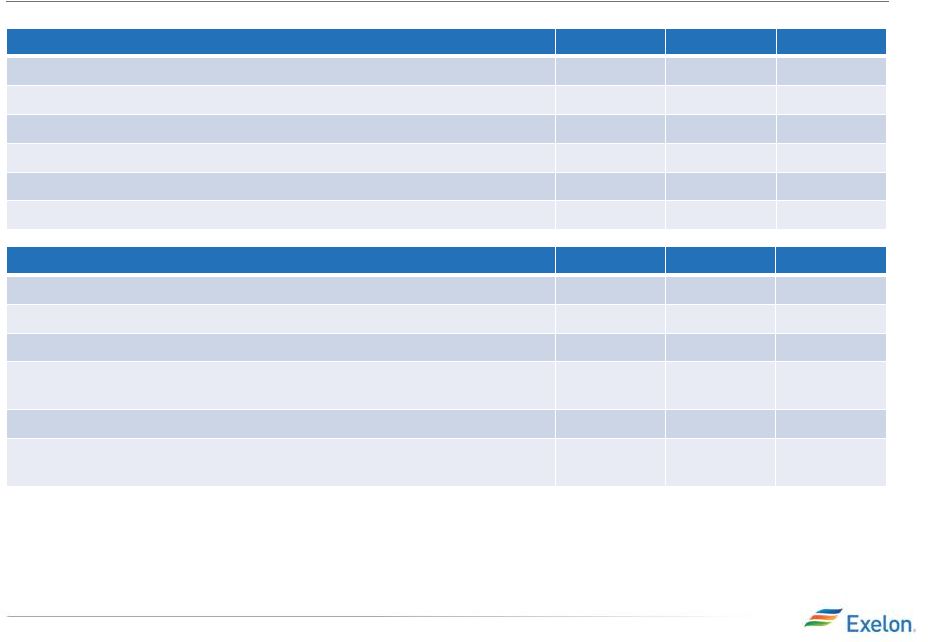

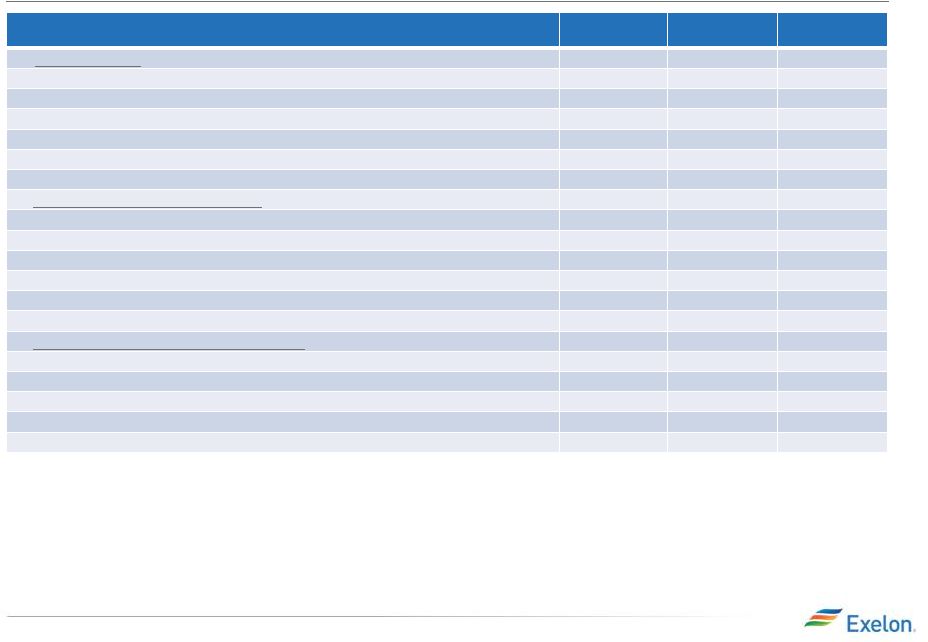

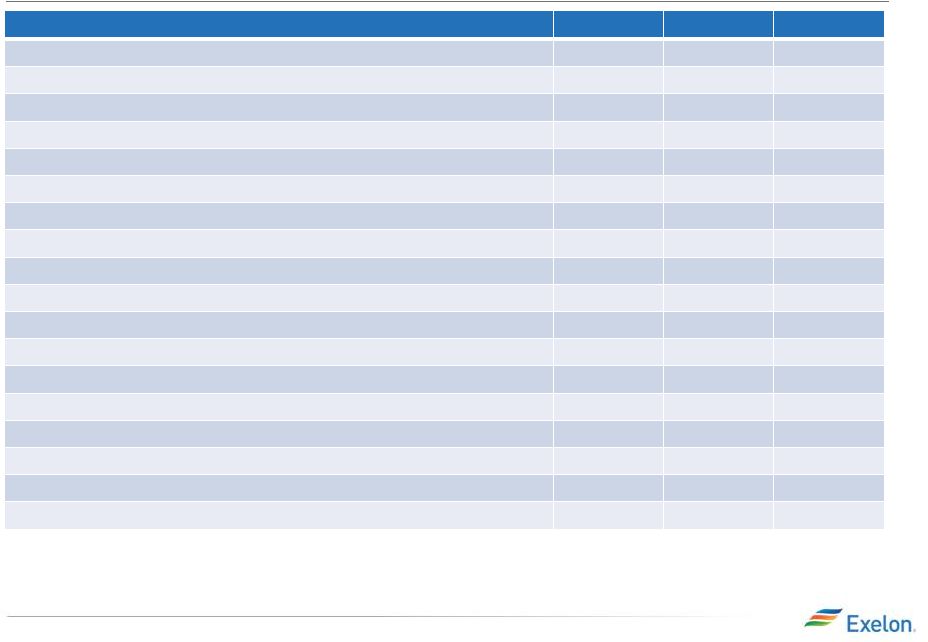

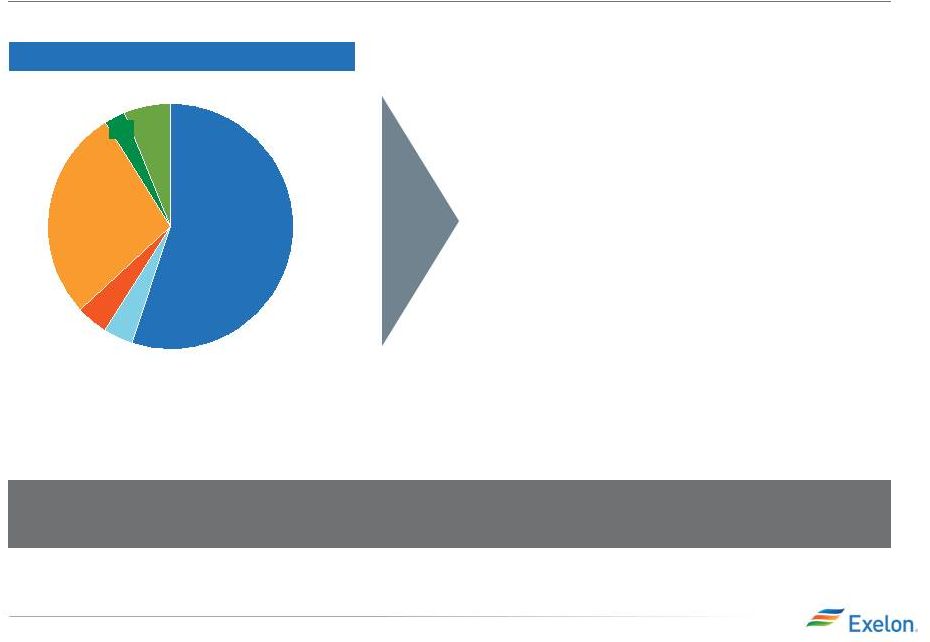

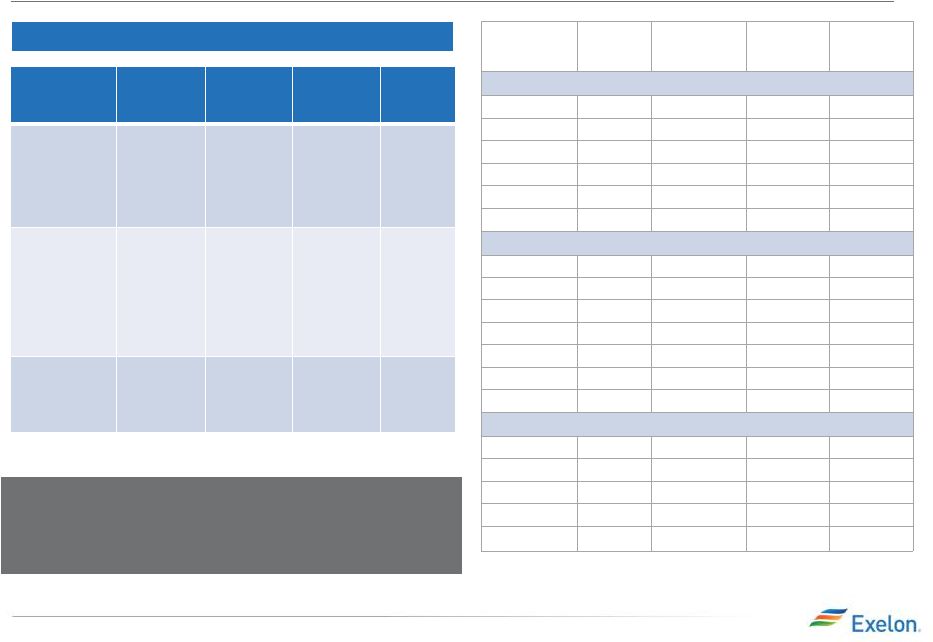

100 Exelon Generation Fleet Overview (1) Plant Location Owned Capacity (MW) LDA Hub/Zone Region for Disclosure Mapping Nuclear Braidwood Braidwood, IL 2,348 Rest of RTO NiHub Midwest Byron Byron, IL 2,323 Rest of RTO NiHub Midwest Calvert Cliffs I and II Calvert Co, MD 853 SWMAAC BGE Mid-Atlantic Clinton Clinton, IL 1,067 n/a Indiana Hub Midwest Dresden Morris, IL 1,753 Rest of RTO NiHub Midwest LaSalle Seneca, IL 2,316 Rest of RTO NiHub Midwest Limerick Limerick Twp.,PA 2,312 EMAAC PECO Zone Mid-Atlantic Nine Mile Point I and II Scriba, NY 782 NYPP Zone C New York Oyster Creek Forked River, NJ 625 EMAAC PECO Zone Mid-Atlantic Peach Bottom Peach Bottom Twp., PA 1,150 EMAAC PECO Zone Mid-Atlantic Quad Cities Cordova, IL 1,380 Rest of RTO NiHub Midwest R.E. Ginna Ontario, NY 291 NYPP Zone B New York Salem Hancock's Bridge, NJ 1,004 EMAAC PECO Zone Mid-Atlantic Three Mile Island Londonderry Twp, PA 837 MAAC Whub/MetEd Zone Mid-Atlantic Coal (2) ACE Trona, CA 32 n/a Other Conemaugh New Florence, PA 533 MAAC Whub/Penelec Zone Mid-Atlantic Jasmin Kern Co, CA 18 n/a Other Keystone Shelocta, PA 716 MAAC Whub/Penelec Zone Mid-Atlantic POSO Kern Co, CA 18 n/a Other Gas Colorado Bend Wharton, TX 550 Houston ERCOT Eddystone 3, 4 Eddystone, PA 760 EMAAC PECO Zone Mid-Atlantic Fore River North Weymouth, MA 688 ROP-NE Hub New England Gould Street Baltimore City, MD 97 SWMAAC BGE Mid-Atlantic Grande Prairie Alberta, Canada 93 n/a Other Handley 3, 4, 5 Fort Worth, TX 1,265 ERCOT N ERCOT Handsome Lake Rockland Twp, PA 268 MAAC Whub/Penelec Zone Mid-Atlantic Hillabee Energy Alexander City, Alabama 740 GTC Other LaPorte Laporte, TX 152 ERCOT ERCOT Medway West Medway, MA 105 ISO-NE Mass Hub New England Mountain Creek 6, 7, 8 Dallas, TX 805 ERCOT N ERCOT Mystic 7 Charlestown, MA 560 ROP-NE Hub New England Mystic 8,9 Charlestown, MA 1,398 NEMA Hub New England Notch Cliff Baltimore Co, MD 101 SWMAAC BGE Mid-Atlantic Perryman -Gas Harford Co, MD 147 SWMAAC BGE Mid-Atlantic Quail Run Energy Odessa, TX 550 West ERCOT Riverside -Gas Baltimore Co, MD 189 SWMAAC BGE Mid-Atlantic Southeast Chicago Chicago, IL 296 Rest of RTO NiHub Midwest West Valley Salt Lake City, UT 200 n/a Other Westport Baltimore Co, MD 116 SWMAAC BGE Mid-Atlantic Wolf Hollow 1, 2, 3 Granbury, TX 705 ERCOT N ERCOT Plant Location Owned Capacity (MW) LDA Hub/Zone Region for Disclosure Mapping Oil Chester Chester, PA 39 EMAAC PECO Zone Mid-Atlantic Conemaugh New Florence, PA 2 MAAC Whub/Penelec Zone Mid-Atlantic Croydon Bristol Twp., PA 391 EMAAC PECO Zone Mid-Atlantic Delaware Philadelphia, PA 56 EMAAC PECO Zone Mid-Atlantic Eddystone Eddystone, PA 60 EMAAC PECO Zone Mid-Atlantic Falls Falls Twp., PA 51 EMAAC PECO Zone Mid-Atlantic Framingham Framingham, MA 28 ISO-NE Mass Hub New England Keystone Shelocta, PA 2 MAAC Whub/Penelec Zone Mid-Atlantic Moser LowerPottsgrove Twp., PA 51 EMAAC PECO Zone Mid-Atlantic Mystic Jet Charlestown, MA 9 ROP-NE Hub New England New Boston South Boston, MA 12 ISO-NE Mass Hub New England Perryman - Oil Harford Co, MD 200 SWMAAC BGE Mid-Atlantic Philadelphia Road Baltimore Co, MD 61 SWMAAC BGE Mid-Atlantic Richmond Philadelphia, PA 98 EMAAC PECO Zone Mid-Atlantic Riverside - Oil Baltimore Co, MD 39 SWMAAC BGE Mid-Atlantic Salem Hancock's Bridge, NJ 16 EMAAC PECO Zone Mid-Atlantic Schuylkill Philadelphia, PA 199 EMAAC PECO Zone Mid-Atlantic Southwark Philadelphia, PA 52 EMAAC PECO Zone Mid-Atlantic Wyman Yarmouth, ME 36 ISO-NE Maine Zone New England Hydro Conowingo Harford Co., MD 572 EMAAC PECO Zone Mid-Atlantic Malacha Muck Valley, CA 16 n/a Other Muddy Run Lancaster, PA 1,070 EMAAC PECO Zone Mid-Atlantic Safe Harbor Safe Harbor, PA 278 MAAC Whub Mid-Atlantic Wind AgriWind Bureau Co., IL 8 IL Hub/Indiana Hub Midwest Blue Breezes Faribault Co., MN 3 MinnHub Midwest Bluegrass Ridge Gentry Co., MO 56 SERC Other Brewster Jackson Co., MN 6 MinnHub Midwest Cassia Twin Falls Co., ID 29 WECC/Mid-C Other Cisco Jackson Co., MN 8 MinnHub Midwest Conception Nodaway Co.,MO 50 SERC Other Cow Branch Atchinson Co.,MO 50 SERC Other Cowell Pipestone Co., MN 2 MinnHub Midwest CP Windfarm Faribault Co., MN 4 MinnHub Midwest Criterion Oakland, MD 70 Whub Mid-Atlantic Echo 1 Umatilla Co., OR 34 WECC/Mid-C Other Echo 2,3 Morrow Co., OR 30 WECC/Mid-C Other Ewington Jackson Co., MN 20 MinnHub Midwest Exelon Wind 1-11 Various Counties, TX 180 SPP Other Greensburg Kiowa Co., KS 13 SPP Other Harvest Huron Co., MI 53 MichHub Midwest (1) Total owned generation capacity as of 4/30/2012 for legacy Exelon and legacy Constellation combined, net of physical market mitigation assumed to be 2,648 MW. (2) Coal capacity shown does not include Eddystone 2 (309 MW) retired on 6/1/2012. 2012 Analyst Meeting – Performance that Drives Progress |