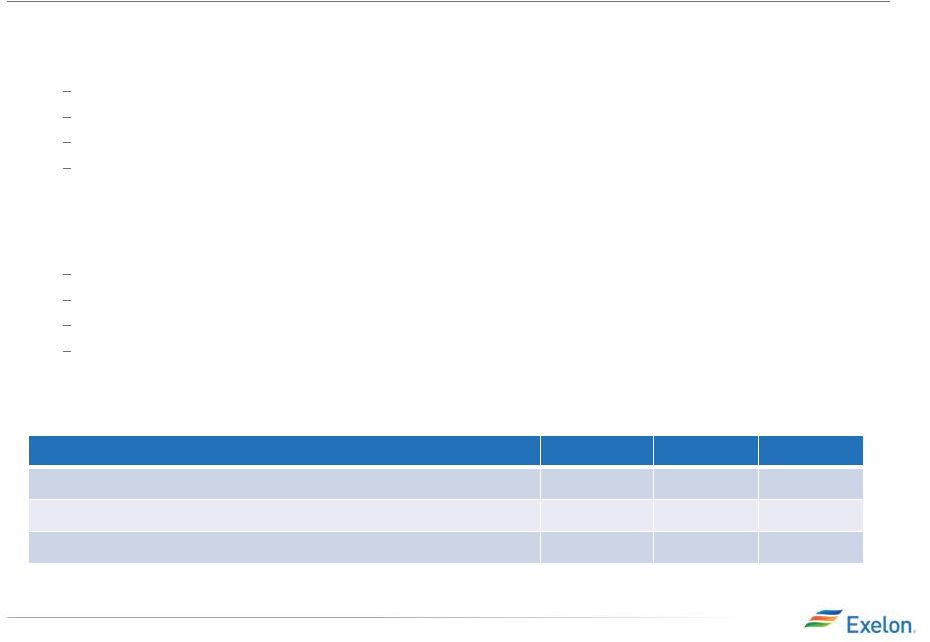

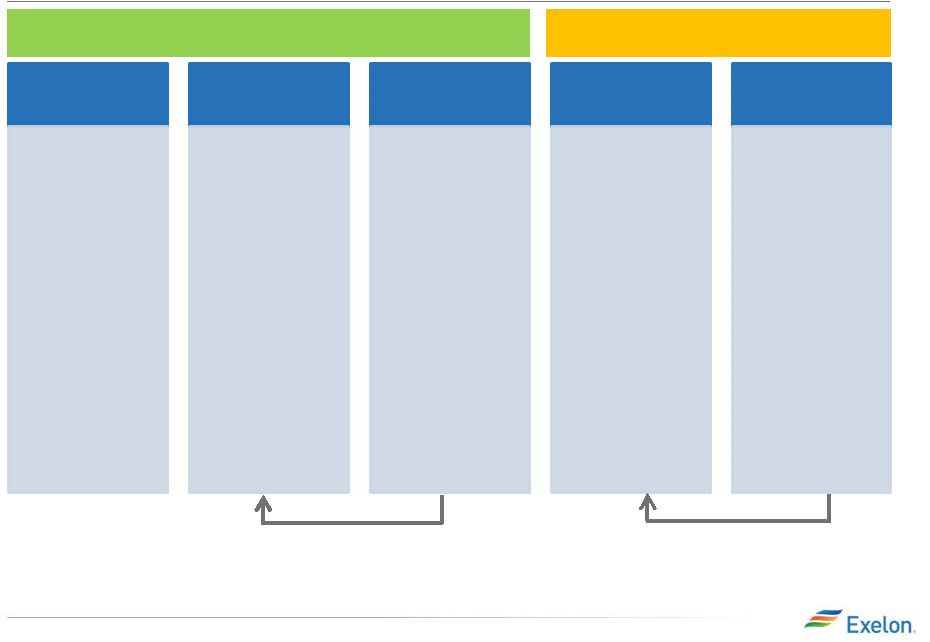

19 ComEd Distribution Rate Case Update 2011 Formula Rate Filing (Docket # 11-0721 filed 11/8/11; rates eff. June 2012): • Based on 2010 calendar year costs and 2011 net plant additions • Supported $59M distribution revenue requirement reduction • 10.05% ROE (2010 Treasury yield of 4.25% + 580 basis point risk premium) ICC Final Order (issued 5/30/12): • $168M revenue requirement reduction; incremental reduction includes: ~$50M related to costs ICC determined should be recovered through alternative rate recovery tariffs or reflected in reconciliation proceeding; primarily delays timing of cash flows ~$35M reflects disallowance of return on pension asset ~$10M reflects incentive compensation related adjustments ~$15M reflects various adjustments for cash working capital, operating reserves and other technical items • ComEd requested and the ICC granted expedited rehearing on the pension, interest rate, and average rate base issues; Commission Final Order expected by Sept. 19. 2012 Formula Rate Filing (Docket # 12-0321 filed 4/30/12, rates eff. Jan 2013) • 2012 plan year based on 2011 actual costs and 2012 net plant additions 9.71% ROE (2011 Treasury yield of 3.91% + 580 basis point risk premium) • Reconciled 2011 revenue requirements in effect to 2011 actual costs incurred 9.81% ROE (3.91% plus 590 basis point risk premium) (1) • Initial filing supported $106M distribution revenue requirement increase relative to Dec. 2012 rates as ComEd initially proposed. When factoring in 5/30/12 order for #11-0721, ComEd proposed a $34M reduction • Received staff and intervener testimony on 7/17/12 – Staff proposes an additional $35M reduction beyond ComEd’s filing • ICC order by year end; rates effective January 2013 Summary of Filings 2010 2011 2012 J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D Costs used for filing Plant additions used for filing Formula rate filing Rates in effect 2011 2012 2013 J F M A M J J A S O N D J F M A M J J A S O N D J F M A J J A S O N D Costs used for filing Plant additions used for filing Formula rate filing Rates in effect (1) 590 basis point premium applies only to 2011 revenue reconciliation. All subsequent revenue reconciliations will assume a 580 basis point premium. 2012 2Q Earnings Release Slides |