Wolfe Trahan Power & Gas Deep Dive Conference Houston, TX Joe Nigro, SVP Portfolio Strategy Ed Quinn, SVP Wholesale Trading & Origination April 11, 2013 Exhibit 99.1 |

Cautionary Statements Regarding Forward Looking Information Wolfe Trahan Power & Gas Deep Dive Conference 1 This presentation contains certain forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995, that are subject to risks and uncertainties. The factors that could cause actual results to differ materially from the forward-looking statements made by Exelon Corporation, Commonwealth Edison Company, PECO Energy Company, Baltimore Gas and Electric Company and Exelon Generation Company, LLC (Registrants) include those factors discussed herein, as well as the items discussed in (1) Exelon’s 2012 Annual Report on Form 10-K in (a) ITEM 1A. Risk Factors, (b) ITEM 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations and (c) ITEM 8. Financial Statements and Supplementary Data: Note 19; and (2) other factors discussed in filings with the SEC by the Registrants. Readers are cautioned not to place undue reliance on these forward-looking statements, which apply only as of the date of this presentation. None of the Registrants undertakes any obligation to publicly release any revision to its forward-looking statements to reflect events or circumstances after the date of this presentation. |

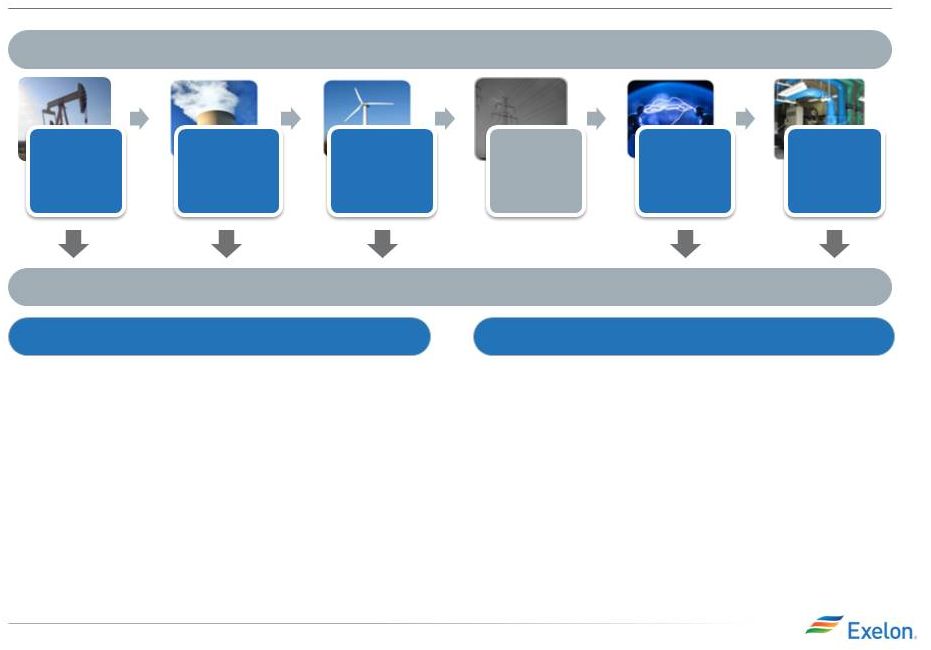

Conventional Generation Fuels Retail Renewable Generation Electric & Gas Utilities Beyond The Meter Presence across the entire energy value chain Unique Combination of Scale, Scope and Flexibility to Invest Across The Value Chain with Metrics Oriented Operational Model Wolfe Trahan Power & Gas Deep Dive Conference 2 Exelon Generation Components • Leading competitive energy provider in the U.S. • Constellation’s retail business serves more than 100,000 business and public sector customers and approximately 1 million residential customers o Wide range of products and services, including load response, energy efficiency and distributed solar • Top-notch portfolio and risk management capabilities • 35,000 megawatts (1) of diverse generation across 22 states and Canada • One of the largest and best-managed nuclear fleets in the world (approximately 19,000 megawatts) (1) • Ten consecutive years with nuclear capacity factor over 92% • One of the nation’s cleanest fleets as measured by CO2, SO2 and NOx intensity Constellation Power Generation (1) Includes ~2,000 megawatts from Exelon Generation’s investment in CENG, a joint venture with EDF. |

Wolfe Trahan Power & Gas Deep Dive Conference 3 Portfolio Management Strategy Protect Balance Sheet Ensure Earnings Stability Create Value Exercising Market Views Purely ratable Actual hedge % Market views on timing, product allocation and regional spreads reflected in actual hedge % High End of Profit Low End of Profit % Hedged Open Generation with LT Contracts Portfolio Management & Optimization Portfolio Management Over Time Align Hedging & Financials Establishing Minimum Hedge Targets Strategic Policy Alignment •Aligns hedging program with financial policies and financial outlook •Establish minimum hedge targets to meet financial objectives of the company (dividend, credit rating) •Hedge enough commodity risk to meet future cash requirements under a stress scenario Three-Year Ratable Hedging • Ensure stability in near-term cash flows and earnings • Disciplined approach to hedging • Tenor aligns with customer preferences and market liquidity • Multiple channels to market that allow us to maximize margins • Large open position in outer years to benefit from price upside Bull / Bear Program •Ability to exercise fundamental market views to create value within the ratable framework •Modified timing of hedges versus purely ratable •Cross-commodity hedging (heat rate positions, options, etc.) •Delivery locations, regional and zonal spread relationships Credit Rating Capital & Operating Expenditure Dividend Capital Structure |

Creating Value in a Low Commodity Price Environment Wolfe Trahan Power & Gas Deep Dive Conference 4 • The competitive advantage of our platform is the scale and scope of the business across the energy value chain • Exelon is well positioned for any power market recovery Market Forces Customer Focused • Deregulation of non-competitive states • Hyper competitive retail market Constellation’s platform provides opportunities to create value in this low commodity price environment RGGI = Regional Greenhouse Gas Initiative Constellation Actions • New product and service bundles • Cross-selling products • Disciplined pricing • Regulatory advocacy • Flexible hedging strategy • Selection of products (i.e. sell gas instead of power) • Regulatory advocacy • Portfolio optimization (short, medium and long term) – physical presence provides increased optimization opportunities • Effective channel management • EPA Regulation • Natural gas price • Power demand • Power market design (ERCOT and PJM) • PTC (Production Tax Credit) • Subsidized generation • RGGI Proposed Changes • Technological Innovation Generation Focused |

(1) Owned and contracted generation capacity converted from MW to MWh assuming 100% capacity factor for all technology types, except for renewable capacity which is shown at estimated capacity factor. Generation Fleet Overview Wolfe Trahan Power & Gas Deep Dive Conference 5 Owned Generation (Technology Type) Generation and Load Match (2013 TWh) (1,2) Multiple paths to market available to hedge the ~35,000 MW fleet that has both technological and regional diversification New York New England ERCOT MidAtlantic 116 MidWest 118 Renewables Baseload Intermediate Peaking Expected Load Expected Generation Generation capacity 43 30 26 14 15 6 12 17 14 17 18 48 75 25 97 11 South/West/ Canada (2) Expected generation and load shown in the chart above will not tie out with load volume and ExGen disclosures. Load shown above does not include indexed products and generation reflects a net owned and contracted position. Estimates as of 9/30/2012. Hydro 6% Wind/Solar/Other 4% Coal 4% Oil 3% Gas 28% Nuclear 55% |

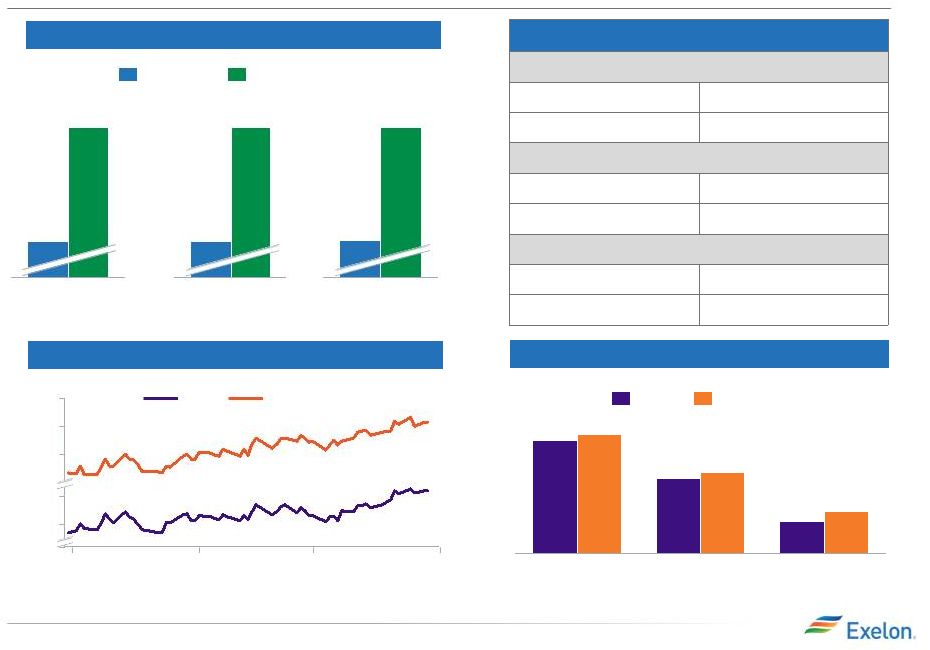

Market Update Wolfe Trahan Power & Gas Deep Dive Conference 6 2015 Henry Hub $4.30 $4.23 3/31/2013 12/31/2012 2015 PJM-W ATC $41.43 $39.17 2015 NiHub ATC $33.72 $31.87 2015 Gross Margin Sensitivities (1) ($M) Henry Hub + $1/Mmbtu $590 - $1/Mmbtu ($520) NiHub ATC + $5/MWh $410 - $5/MWh ($410) PJM-W ATC + $5/MWh $260 - $5/MWh ($250) 2015 Price Change ATC = Around the Clock. (1) Sensitivity data as of 12/31/12. (2) Uses midpoint of hedge percentage provided in 4Q12 earnings release (data as of 12/31/12). 9.8 9.6 9.4 7.8 7.6 0.0 3/31/13 3/1/13 2/1/13 1/1/13 9.6 7.8 9.3 7.5 PJM W NiHub 26.5% 62.5% 93.5% 34.5% 67.5% 98.5% 2015 2014 2013 Mid-Atlantic Midwest 2015 ATC Heat Rate – 1Q13 % of Expected Generation Hedged (2) |

Other Constellation Businesses 7 • Provides strong returns ( >12% IRR) • $140M (~50% utilized) Reserve Based Lending (RBL) facility in place • Receives off-balance sheet treatment from S&P • Provides valuable market intelligence in complex natural gas markets • 266 Bcfe of net proved reserves as of 12/31/12 Presence and experience across the value chain allows Constellation to offer customers multiple products to manage their energy risk • Retail Gas: • All States are competitive • ~430 Bcf projected to be served in 2013 • Month to month customers, with high retention rates • Wholesale Gas: • Expand presence to complement power assets • Portfolio Size: 5 Bcf wholesale storage, 200,000 MMBtus per day of term transport and over 1.5 Bcf/day of plant supply • 2013 market size of 5.5 GW estimated to grow 1-2 GW per year for the next 5 years • Focus on states with established markets in place and where there is potential for new incentives • Pursue opportunities in non-Solar REC markets where there is increased interest in solar • ~155 MW in operation or under construction (excludes Antelope Valley Solar Ranch facility) • Load Response: • ~2 GW of load response under contract • Roughly 100 GW total market • Energy Efficiency: • Over 4,000 projects implemented to date • Focus on government, education, healthcare and multi-family housing sectors Upstream E&P Assets Retail and Wholesale Gas Solar Energy Efficiency and Load Response E&P = Exploration and Production. REC = Renewable Energy Credit. Wolfe Trahan Power & Gas Deep Dive Conference |

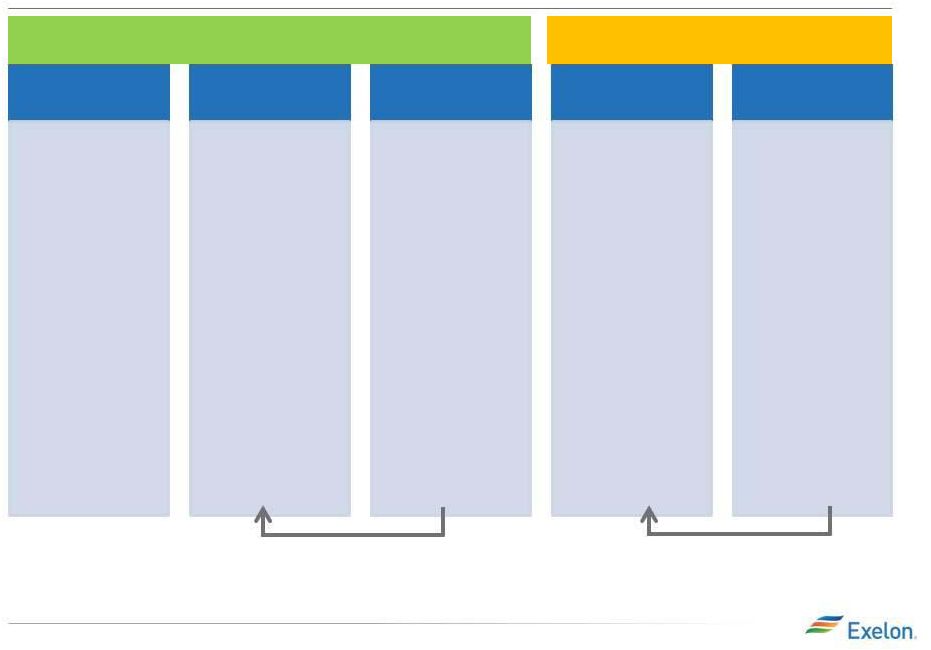

8 Components of Gross Margin Categories Margins move from new business to MtM of hedges over the course of the year as sales are executed Margins move from “Non power new business” to “Non power executed” over the course of the year Gross margin linked to power production and sales Gross margin from other business activities Open Gross Margin MtM of Hedges (2) “Power” New Business “Non Power” Executed “Non Power” New Business • Generation Gross Margin at current market prices, including capacity and ancillary revenues, nuclear fuel amortization and fossils fuels expense • Exploration and Production • Power Purchase Agreement (PPA) Costs and Revenues • Provided at a consolidated level for all regions (includes hedged gross margin for South, West and Canada (1) ) • Mark to Market (MtM) of power, capacity and ancillary hedges, including cross commodity, retail and wholesale load transactions • Provided directly at a consolidated level for five major regions. Provided indirectly for each of the five major regions via Effective Realized Energy Price (EREP), reference price, hedge %, expected generation • Retail, Wholesale planned electric sales • Portfolio Management new business • Mid marketing new business • Retail, Wholesale executed gas sales • Load Response • Energy Efficiency • BGE Home • Distributed Solar • Retail, Wholesale planned gas sales • Load Response • Energy Efficiency • BGE Home • Distributed Solar • Portfolio Management / origination fuels new business • Proprietary trading (3) Wolfe Trahan Power & Gas Deep Dive Conference (1) Hedged gross margins for South, West and Canada region will be included with Open Gross Margin, and no expected generation, hedge %, EREP or reference prices provided for this region. (2) MtM of hedges provided directly for the five larger regions. MtM of hedges is not provided directly at the regional level but can be easily estimated using EREP, reference price and hedged MWh. (3) Proprietary trading gross margins will remain within “Non Power” New Business category and not move to “Non Power” Executed category. |