Exelon Announces Acquisition of Pepco Holdings, Inc. April 30, 2014 Exhibit 99.2 |

1 Cautionary Statements Regarding Forward-Looking Information Except for the historical information contained herein, certain of the matters discussed in this communication constitute “forward- looking statements” within the meaning of the Securities Act of 1933 and the Securities Exchange Act of 1934, both as amended by the Private Securities Litigation Reform Act of 1995. Words such as “may,” “might,” “will,” “should,” “could,” “anticipate,” “estimate,” “expect,” “predict,” “project,” “future”, “potential,” “intend,” “seek to,” “plan,” “assume,” “believe,” “target,” “forecast,” “goal,” “objective,” “continue” or the negative of such terms or other variations thereof and words and terms of similar substance used in connection with any discussion of future plans, actions, or events identify forward-looking statements. These forward-looking statements include, but are not limited to, statements regarding benefits of the proposed merger, integration plans and expected synergies, the expected timing of completion of the transaction, anticipated future financial and operating performance and results, including estimates for growth. These statements are based on the current expectations of management of Exelon Corporation (Exelon) and Pepco Holdings, Inc. (PHI), as applicable. There are a number of risks and uncertainties that could cause actual results to differ materially from the forward-looking statements included in this communication. For example, (1) PHI may be unable to obtain shareholder approval required for the merger; (2) the companies may be unable to obtain regulatory approvals required for the merger, or required regulatory approvals may delay the merger or cause the companies to abandon the merger; (3) conditions to the closing of the merger may not be satisfied; (4) an unsolicited offer of another company to acquire assets or capital stock of Exelon or PHI could interfere with the merger; (5) problems may arise in successfully integrating the businesses of the companies, which may result in the combined company not operating as effectively and efficiently as expected; (6) the combined company may be unable to achieve cost-cutting synergies or it may take longer than expected to achieve those synergies; (7) the merger may involve unexpected costs, unexpected liabilities or unexpected delays, or the effects of purchase accounting may be different from the companies’ expectations; (8) the credit ratings of the combined company or its subsidiaries may be different from what the companies expect; (9) the businesses of the companies may suffer as a result of uncertainty surrounding the merger; |

2 Cautionary Statements Regarding Forward-Looking Information (Continued) (10) the companies may not realize the values expected to be obtained for properties expected or required to be sold; (11) the industry may be subject to future regulatory or legislative actions that could adversely affect the companies; and (12) the companies may be adversely affected by other economic, business, and/or competitive factors. Other unknown or unpredictable factors could also have material adverse effects on future results, performance or achievements of the combined company. Therefore, forward-looking statements are not guarantees or assurances of future performance, and actual results could differ materially from those indicated by the forward-looking statements. Discussions of some of these other important factors and assumptions are contained in Exelon’s and PHI’s respective filings with the Securities and Exchange Commission (SEC), and available at the SEC’s website at www.sec.gov, including: (1) Exelon’s 2013 Annual Report on Form 10-K in (a) ITEM 1A. Risk Factors, (b) ITEM 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations and (c) ITEM 8. Financial Statements and Supplementary Data: Note 22; and (2) PHI’s 2013 Annual Report on Form 10-K in (a) ITEM 1A. Risk Factors, (b) ITEM 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations and (c) ITEM 8. Financial Statements and Supplementary Data: Note 15. In light of these risks, uncertainties, assumptions and factors, the forward-looking events discussed in this communication may not occur. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of this communication. Neither Exelon nor PHI undertakes any obligation to publicly release any revision to its forward- looking statements to reflect events or circumstances after the date of this communication. New factors emerge from time to time, and it is not possible for Exelon or PHI to predict all such factors. Furthermore, it may not be possible to assess the impact of any such factor on Exelon’s or PHI’s respective businesses or the extent to which any factor, or combination of factors, may cause results to differ materially from those contained in any forward-looking statement. Any specific factors that may be provided should not be construed as exhaustive. |

3 Agenda Transaction Overview and Exelon Strategic Rationale Chris Crane President and CEO, Exelon Benefits to PHI Shareholders and Customers Joe Rigby Chairman, President and CEO, Pepco Holdings Combined Company Profile and Financial Summary Jack Thayer Executive Vice President and CFO, Exelon Closing Comments Chris Crane President and CEO, Exelon Q&A Session |

4 Executive Summary • A strategic acquisition that creates the leading Mid-Atlantic electric and gas utility. The combined utility businesses will serve nearly 10 million customers, with a rate base of ~$26 billion. • Purchase price of $27.25 per share. • Earnings composition supports incremental leverage and is expected to be highly accretive to operating earnings starting in the first full year post-close with steady- state accretion of $0.15-$0.20 per share starting in 2017 • Increases Exelon’s utility derived earnings and cash flows, providing a solid base for the dividend and maintaining the upside from a recovery in power markets. • Balanced financing mix allows Exelon to maintain balance sheet strength and provides flexibility to continue to invest in opportunities aligned with our growth strategy. • The combination of Exelon and Pepco Holdings (PHI) will offer significant benefits to customers. |

5 Strategic Rationale Growing regulated cash flow and earnings while maintaining upside from power price recovery Strong financial fit Strong geographic fit and operations mix |

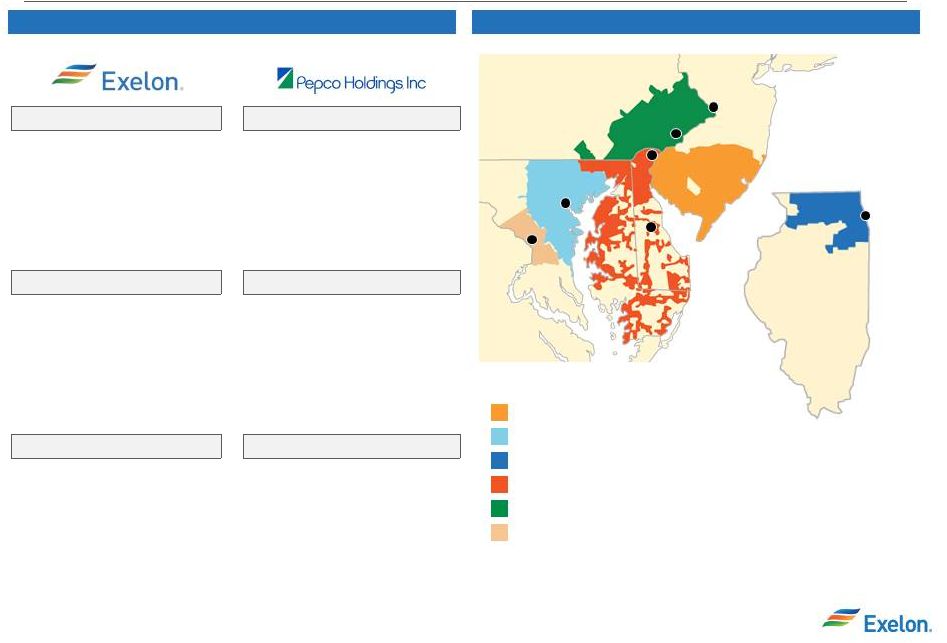

6 Expertise in Operating Regulated Utilities in Large Metropolitan Areas Commonwealth Edison Potomac Electric Power Customers: Service Territory: Peak Load: 2013 Rate Base: 3,800,000 11,400 sq. miles 23,753 MW $8.7 bn Customers: Service Territory: Peak Load: 2013 Rate Base: 801,000 640 sq. miles 6,674 MW $3.4 bn PECO Energy Atlantic City Electric Co. Customers: Service Territory: Peak Load: 2013 Rate Base: 2,100,000 2,100 sq. miles 8,983 MW $5.4 bn Customers: Service Territory: Peak Load: 2013 Rate Base: 545,000 2,700 sq. miles 2,797 MW $1.6 bn Baltimore Gas & Electric Delmarva Power & Light Customers: Service Territory: Peak Load: 2013 Rate Base: 1,900,000 2,300 sq. miles 7,236 MW $4.6 bn Customers: Service Territory: Peak Load: 2013 Rate Base: 632,000 5,000 sq. miles 4,121 MW $2.0 bn ___________________________ Source: Company filings. Note: Operational statistics as of 12/31/2013 DE MD PA NJ VA Philadelphia Baltimore Dover Wilmington Trenton Washington, DC IL Chicago Potomac Electric Power Service Territory Atlantic City Electric Co. Service Territory Delmarva Power & Light Service Territory Baltimore Gas and Electric Co. Service Territory PECO Energy Service Territory ComEd Service Territory Operating Statistics Combined Service Territory |

7 Transaction Overview Consideration Headquarters Governance All-cash transaction Upfront transaction premium of 24.7% (1) Corporate headquarters: Chicago No change to utilities’ headquarters Significant employee presence maintained in IL, PA, MD, DC, DE and NJ President and CEO: Chris Crane No change to Exelon senior management team No change to Exelon Board of Directors Expect to close 2 nd or 3 rd quarter 2015 PHI shareholder approval later in 2014 Regulatory approvals including FERC, DOJ, DC, DE, MD, NJ and VA (1) Based on PHI closing stock price as of April 25, 2014. (2) Subject to market conditions ~50% debt Remainder via issuance of equity (including mandatory convertibles) and up to $1B of cash from non-core asset sales (2) Approvals and Timing Financing |

8 Regulatory Approval Timeline • Applications for approval will be filed as promptly as possible and no later than 60 days from the time of the announcement. • FERC has 180 days to review the transaction and issue an order. We would expect approvals by FERC, Virginia and DOJ within 180 days. • Expect Maryland PSC to issue a merger order within 225 days of the application as required by law. • Anticipate other state commissions may take as long as Maryland or slightly longer to review merger applications. • Targeting a 2 or 3 quarter 2015 closing. rd nd |

9 • Attractive 24.7% premium (1) for PHI shares • Commitment to build upon significant improvements in system reliability, customer service and outage restoration • Direct benefits for Atlantic City Electric, Delmarva Power and Pepco’s customers $100 million Customer Investment Fund for rate credits, low income assistance, energy efficiency programs Commitment to further improve system reliability Enhanced storm restoration capabilities • Shared culture of continuous improvement, accountability, safety, and community support Leverage operational and customer service best practices Commitment to highest ever levels of charitable giving for 10 years Delivering Value to PHI’s Shareholders, Employees, Customers and Local Communities (1) Based on PHI closing stock price as of April 25, 2014. • Immediately takes PHI to the “next level” as part of larger, well capitalized company |

Financial Overview |

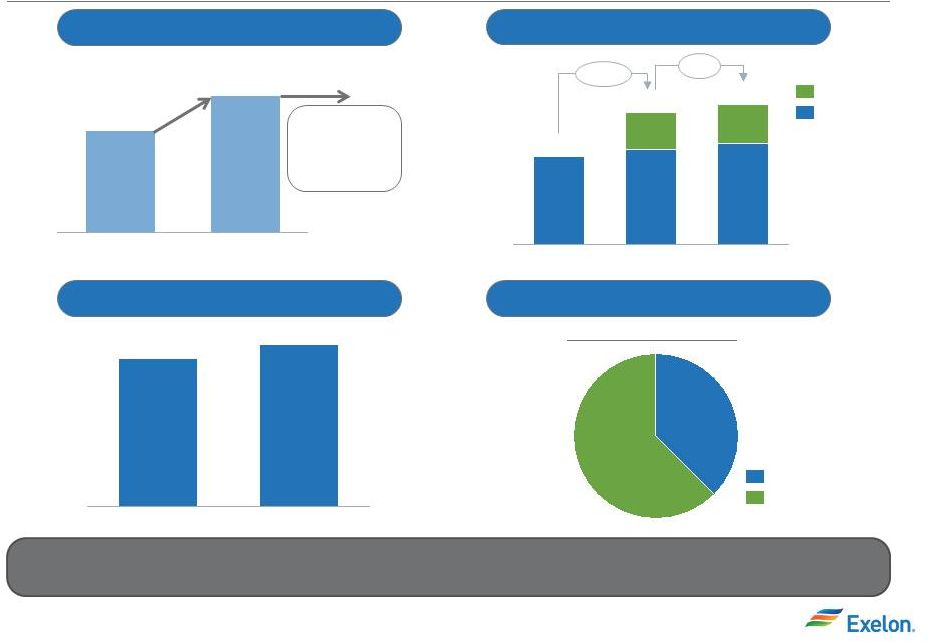

11 Transaction Economics Are Attractive (1) (3) (1) Reflects 2015 YE rate base • Significantly earnings accretive starting in first full year after closing. Anticipate run-rate accretion of $0.15-$0.20 per share starting in 2017. • Supports incremental leverage at Exelon and maintains investment grade ratings at Exelon and PHI entities. • An incremental ~$8.3 billion (1) in regulated rate base adds meaningful size to Exelon’s regulated business -- bolstering regulated earnings, stable cash flows and financial strength. • ~$3.1 billion of regulated CapEx during 2015-2017 adds attractive rate base growth opportunities to supplement Exelon’s current investment program. • Utility earnings can fully support Exelon dividend of $1.24 per share by 2015. • Net synergies of more than $250 million over the first five years, of which one-third is retained. • Preserves power market recovery upside. • Committed financing in place with balanced permanent financing mix. |

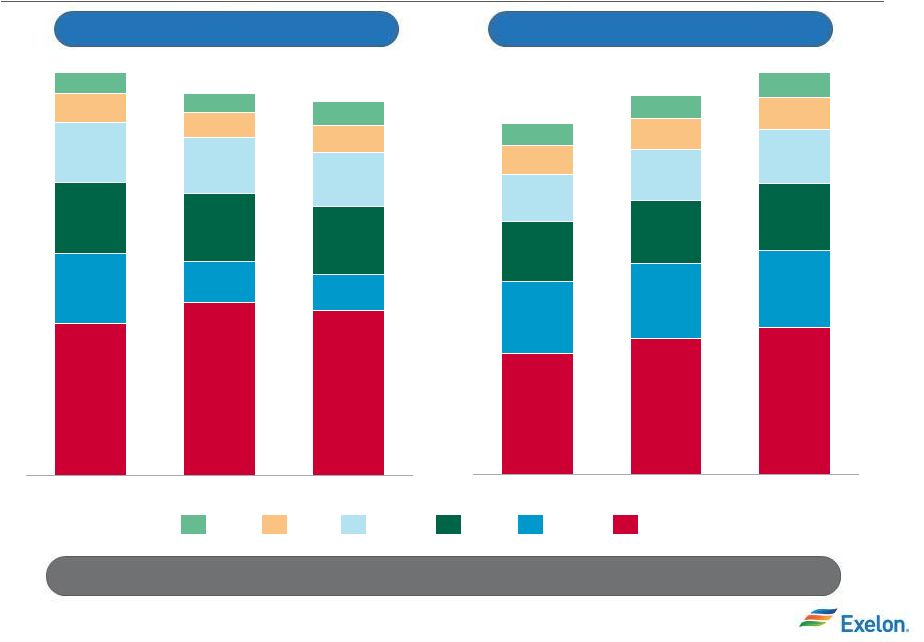

12 Earnings Accretive First Full Year (1) Transaction Economics Exelon Consolidated S&P FFO/Debt 2016 2015 (1) Assumes funding mix of assumed debt, new debt, asset sales and equity issuance with appropriate discount to market price (2) Reflects YE rate base The transaction is significantly EPS accretive, adds to rate base growth and further strengthens our financials 2015-2016 Operating Earnings 60%-65% 35%-40% Pro Forma Business Mix Regulated Unregulated Rate Base Growth ($B) (2) 2016 $31.8 $23.0 $8.8 2015 $30.0 $21.7 $8.3 2014 Exelon PHI 2017 2016 $0.10 - $0.15 $0.15 - $0.20 $20.0 24% 22% Achieve run-rate accretion of $0.15-$0.20 starting in 2017 +6% +50% |

13 Financing Overview Committed $7.2 billion bridge facility signed and in place to support the contemplated transaction and provide flexibility for timing of permanent financing. Interim Financing Permanent Financing Exelon will use a balanced mix of debt, equity and cash to finance the acquisition in order to maintain current investment grade ratings at all registrants Strong liquidity profile for combined company, supported by revolving credit facilities totaling $9.5 billion. Adequate liquidity will be maintained to support all utility operations. Opportunities to right size liquidity facilities will be explored. Liquidity No change of control provisions in public debt of PHI or subsidiaries. Future PHI maturities expected to be refinanced at Exelon Corp as needed – no further debt issuance at PHI expected post-closing. Exelon Corporation debt will be used for regulated investment in utilities; Exelon Generation debt will be used to fund competitive growth. Go Forward Financing Plan (1) Subject to market conditions Financing structure fully expected to maintain investment grade ratings at all Exelon and PHI registrants. Permanent financing will include Exelon Corp debt, equity (including mandatory convertibles) and cash proceeds from asset sales (1) . |

14 Closing Comments • Transaction is another example of our actions to grow our company, our earnings and our returns to our shareholders. • Opportunity to create significant customer savings and build upon existing reliability enhancements. • Tremendous value unlocked through the addition of incremental regulated operating earnings and cash flows. • Accelerates our ability to fully fund the external dividend from our regulated operations. • Balance sheet remains strong after this transaction and allows us flexibility to pursue additional regulated and merchant investments. |

Appendix |

16 Standalone Pro Forma Exelon PHI Regulated Jurisdictions IL, MD, PA DC, DE, MD, NJ DC, DE, IL, MD, NJ, PA Electric Customers (in M) 6.65 1.85 8.50 Gas Customers (in M) 1.15 0.13 1.28 Total Customers (in M) 7.80 1.98 9.78 Utility Service Area (Square Miles) 15,800 8,340 24,140 Electric Transmission (Miles) 7,404 4,600 12,004 Electric Distribution (Miles) 113,345 34,100 147,445 Gas Transmission (Miles) 194 105 299 Gas Distribution (Miles) 13,818 3,157 16,975 A Compelling Combination – Creates The Premier Mid-Atlantic Utility Franchise ___________________________ Source: Company filings. Note: Operational statistics as of 12/31/2013 Combined Statistics |

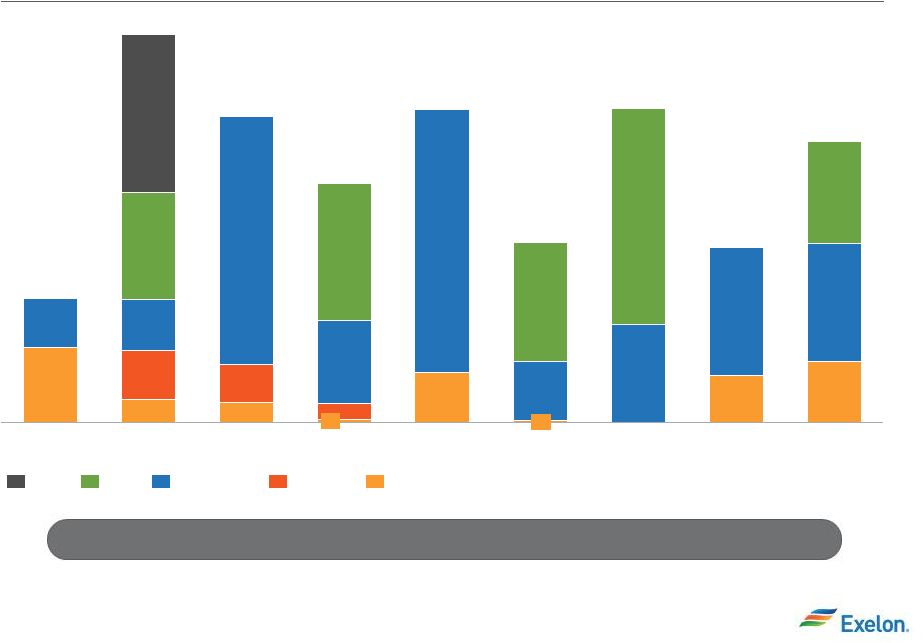

17 $700 $600 $550 $350 $300 $325 Exelon Utilities: Capital Expenditures and Rate Base (1) 2016E $4,300 $1,925 $425 $800 $275 2015E $4,425 $2,025 $475 $800 $225 2014E $4,725 $1,775 $825 $825 $250 ComEd PECO BGE Pepco DPL ACE Strong rate base growth will provide stable utility earnings growth Rate Base ($B) Capital Expenditures ($M) (2) $4.0 $4.3 $2.4 $2.5 $3.8 $2.3 2016E $6.1 $5.3 $11.6 $2.0 $30.0 $10.7 $5.9 $5.1 $1.8 2014E $27.7 $9.5 $5.7 $4.8 $1.7 2015E $31.8 (1) Illustrative view of combined company (2) Numbers rounded to nearest $25 million |

18 Pro Forma Debt Maturity Profile (1) 310 2022 1,433 700 2016 1,557 102 190 1,265 2015 1,975 115 250 260 800 2014 632 382 250 550 600 523 2021 889 239 650 2020 1,600 500 1,100 2019 912 12 300 600 2018 1,594 254 1,340 2017 1,220 14 81 425 ExCorp PHI Holdco PHI Regulated EXC Regulated ExGen Ample liquidity and manageable debt maturities (1) PHI Regulated debt includes $100 mm term loan which matures in 2014; ExGen debt includes former CEG debt assumed by ExGen; Excludes PHI unregulated debt which totals $25 mm; Includes Exelon’s regulated capital trust securities; Excludes tax-exempt, preferred and non-recourse debt; Acquisition debt will be held at corporate but is not included. Source Bloomberg, Company Filings. |

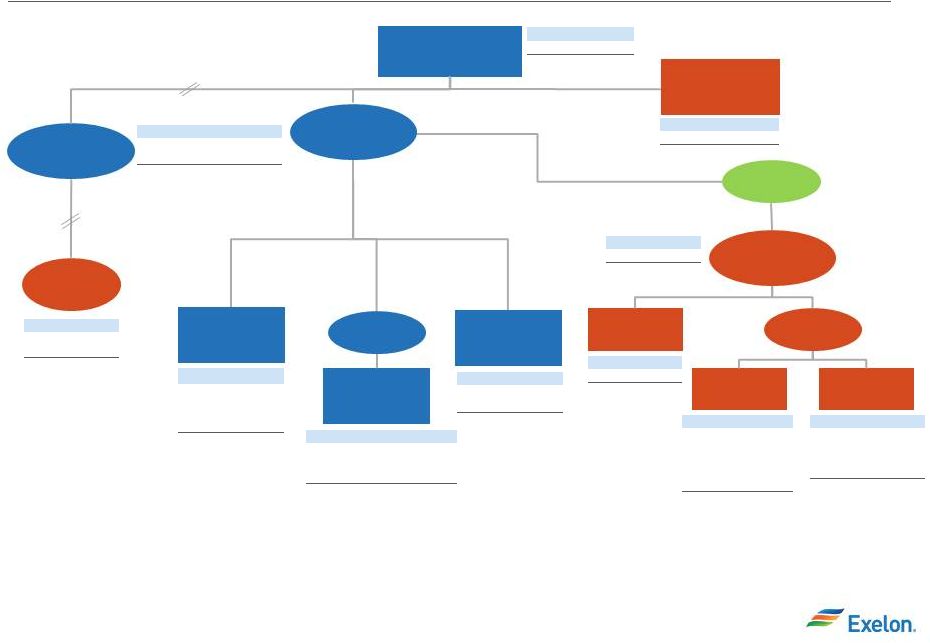

19 Corporate Structure Exelon Corporation Commonwealth Edison Baltimore Gas & Electric Potomac Electric Power Company Delmarva Power & Light Atlantic City Electric Company Exelon Energy Delivery Company Conectiv Pepco Holdings SPE RF Holdco Exelon Generation Pepco Energy Services Type Amt ($mm) FMB $650 Notes $200 Tax Exempt $78 Medium Term Notes $40 Total $968 Type Amt ($mm) FMB $761 Transition Bonds (2) $246 Term Loan $100 Total $1,107 Type Amt ($mm) Recourse (2) $11 Total $11 Type Amt ($mm) FMB (2) $2,310 Total $2,310 Type Amt ($mm) Secured Notes $14 Total $14 Type Amt ($mm) Notes $706 Total $706 Type Amt ($mm) Notes $1,750 Rate Stabilization (2) $265 Trusts $258 Total $2,273 Type Amt ($mm) FMB $5,579 Trusts $206 Other $140 Total $5,924 Type Amt ($mm) FMB $2,200 Trusts $184 Total $2,384 Type Amt ($mm) Notes (1) $5,771 Non-Recourse (2) $1,516 Total $7,287 Type Amt ($mm) Notes $1,300 Total $1,300 PECO Energy Potomac Capital Investment Corporation Note: Simplified organizational chart; additional subsidiaries are not shown. Former direct and indirect subsidiaries of PHI are in red; newly created ring fencing entity is in green Note: Debt outstanding is as of 3/31/14; does not include any projected acquisition financing (1) Includes intercompany loan agreements between Exelon and Generation that mirror the terms and amounts of the third-party obligations of Exelon (2) The following retirements occurred in April 2014 and are not reflected on the chart above: PCI Recourse Debt - $11M, PEPCO FMB $175M, ACE Transition Bonds - $10M, BGE Rate Stabilization Bonds - $35M, various ExGen Project Finance Debt - $3M |