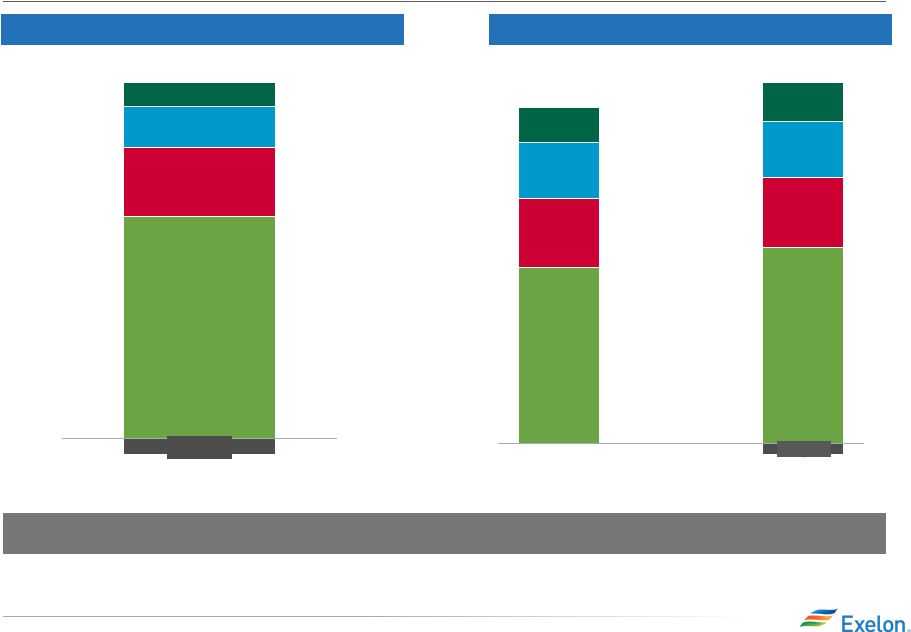

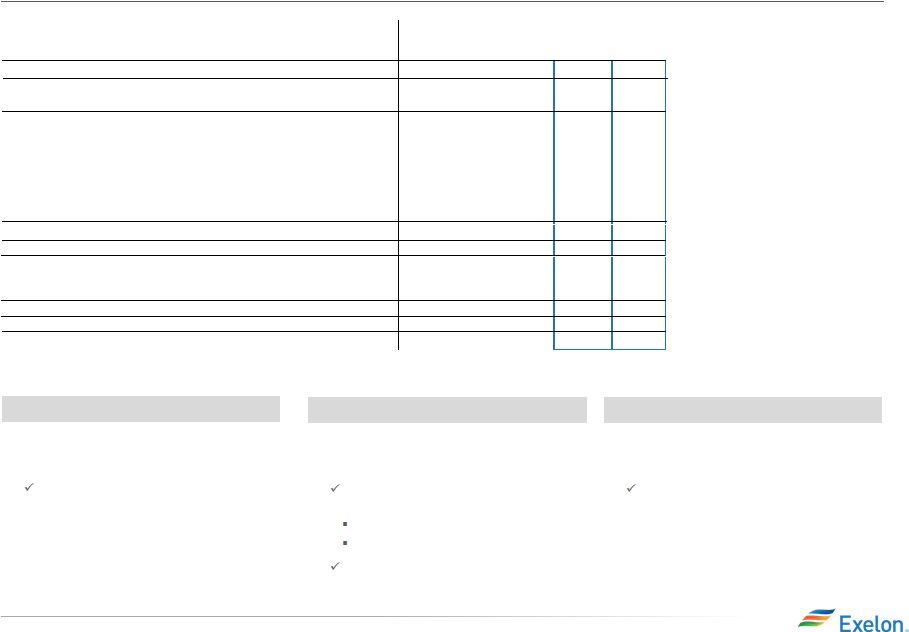

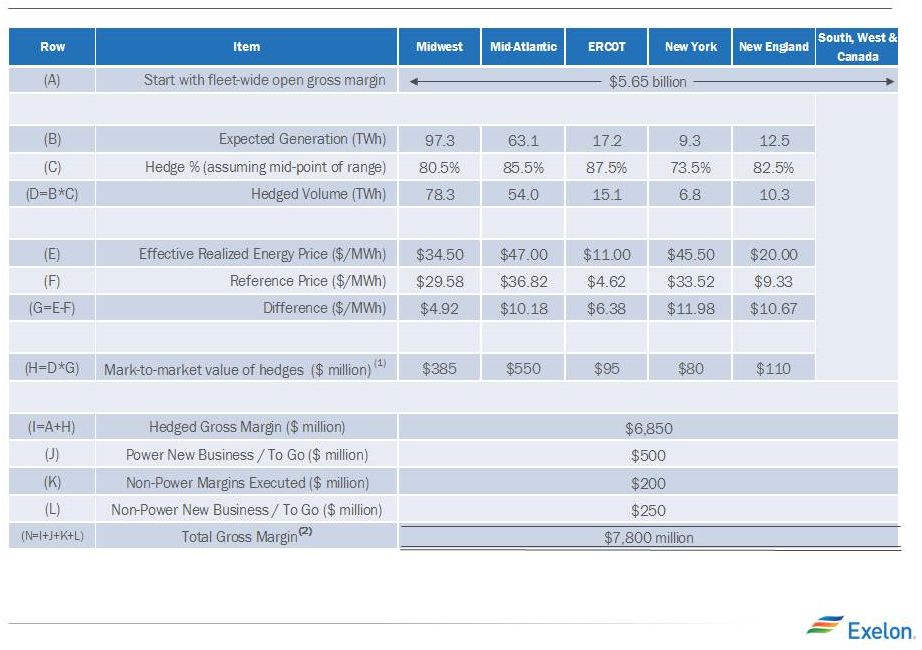

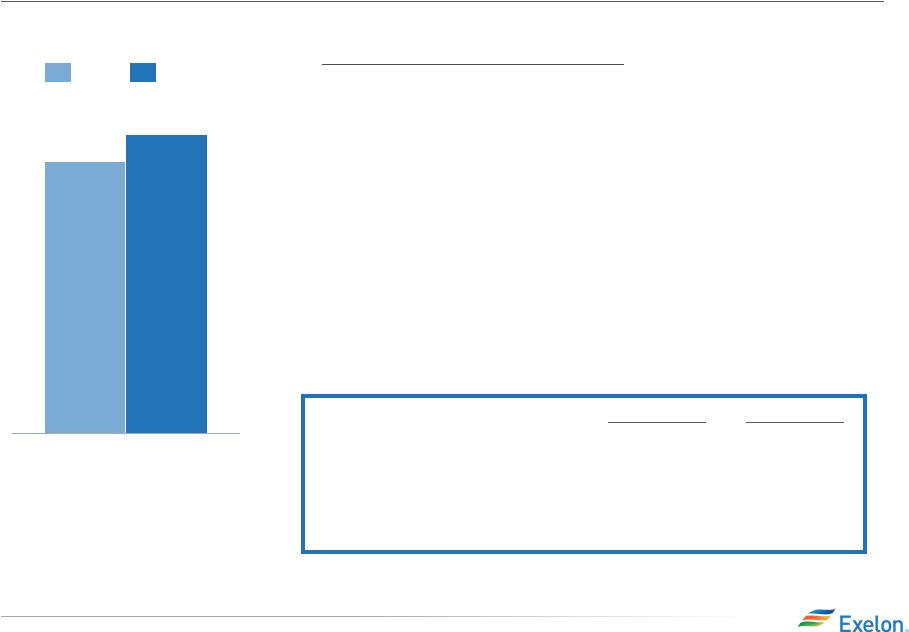

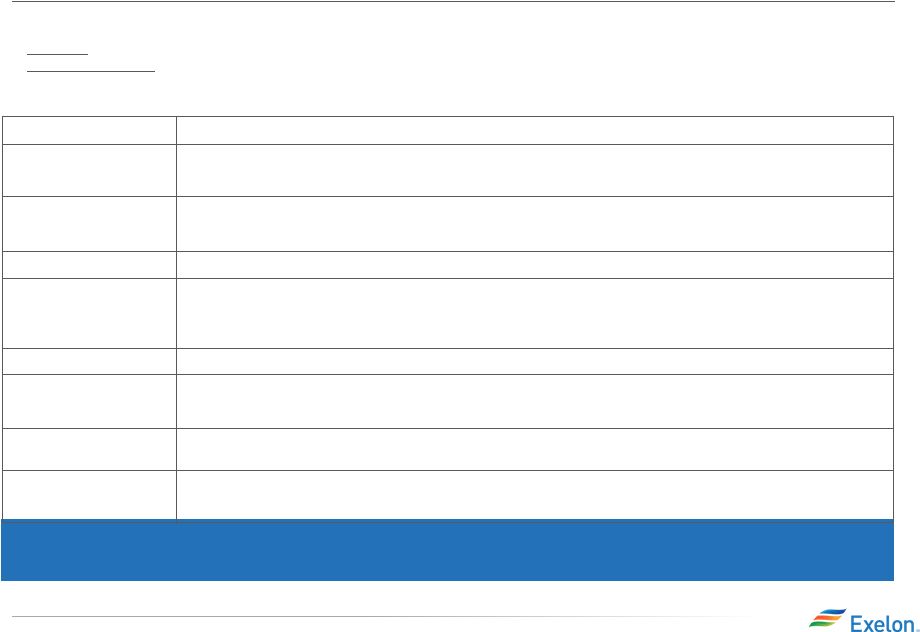

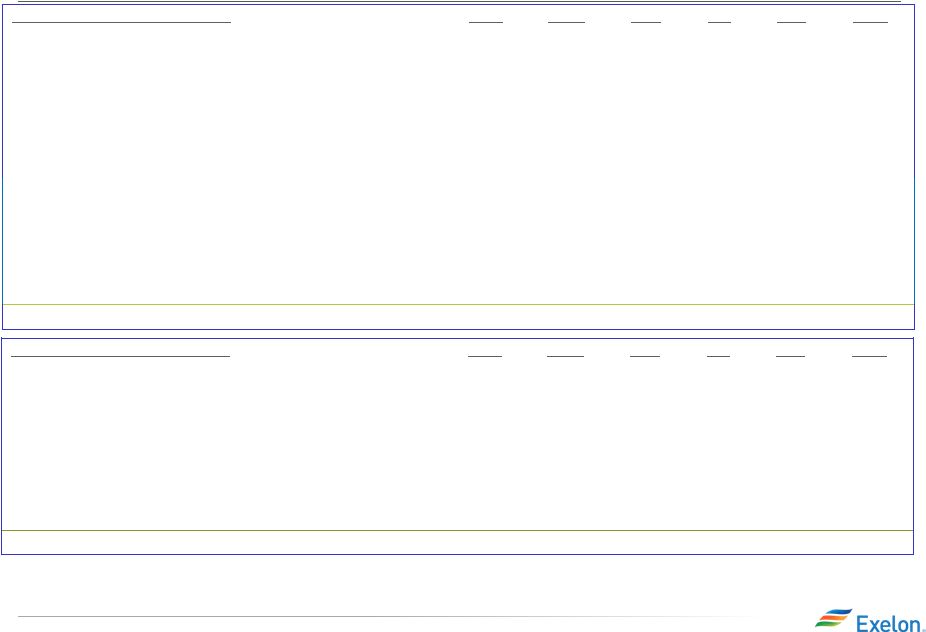

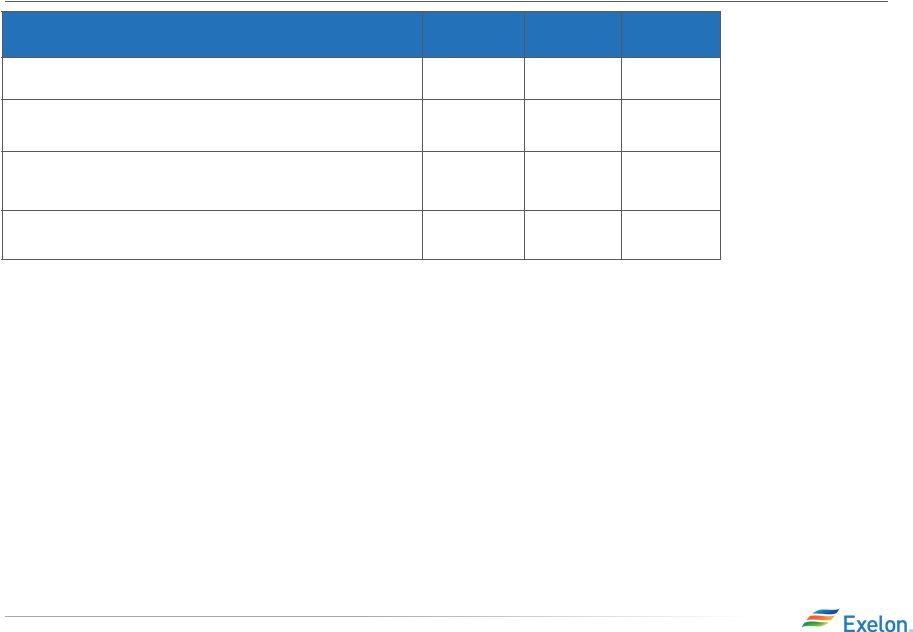

19 Q3 2015 Earnings Release Slides ComEd April 2015 Distribution Formula Rate The 2015 distribution formula rate filing establishes the net revenue requirement used to set the rates that will take effect in January 2016 after the Illinois Commerce Commission's (ICC’s) review. There are two components to the annual distribution formula rate filing: • Filing Year: Based on prior year costs (2014) and current year (2015) projected plant additions. • Annual Reconciliation: For the prior calendar year (2014), this amount reconciles the revenue requirement reflected in rates during the prior year (2014) in effect to the actual costs for that year. The annual reconciliation impacts cash flow in the following year (2016) but the earnings impact has been recorded in the prior year (2014) as a regulatory asset. Given the retroactive ratemaking provision in the Energy Infrastructure Modernization Act (EIMA) legislation, ComEd net income during the year will be based on actual costs with a regulatory asset/liability recorded to reflect any under/over recovery reflected in rates. Revenue Requirement in rate filings impacts cash flow. Revenue Requirement Decrease Rate Base (1) (1) Docket # 15-0287 Filing Year 2014 Calendar Year Actual Costs and 2015 Projected Net Plant Additions are used to set the rates for calendar year 2016. Rates currently in effect (docket 14-0312) for calendar year 2015 were based on 2013 actual costs and 2014 projected net plant additions Reconciliation Year Reconciles Revenue Requirement reflected in rates during 2014 to 2014 Actual Costs Incurred. Revenue requirement for 2014 is based on docket 13-0318 (2012 actual costs and 2013 projected net plant additions) approved in December 2013 and reflects the impacts of PA 98-0015 (SB9) Common Equity Ratio ~ 46% for both the filing and reconciliation year ROE 9.14% for the filing year (2014 30-yr Treasury Yield of 3.34% + 580 basis point risk premium) and 9.09% for the reconciliation year (2014 30-yr Treasury Yield of 3.34% + 580 basis point risk premium – 5 basis points performance metrics penalty). For 2015 and 2016, the actual allowed ROE reflected in net income will ultimately be based on the average of the 30-year Treasury Yield during the respective years plus 580 basis point spread, absent any metric penalties Requested Rate of Return ~ 7% for both the filing and reconciliation years $8,277 million– Filing year (represents projected year-end rate base using 2014 actual plus 2015 projected capital additions). 2015 and 2016 earnings will reflect 2015 and 2016 year-end rate base respectively. $7,082 million - Reconciliation year (represents year-end rate base for 2014) $55M decrease ($145M decrease due to the 2014 reconciliation offset by a $90M increase related to the filing year). The 2014 reconciliation impact on net income was recorded in 2014 as a regulatory asset. Timeline • 04/15/15 Filing Date • 240 Day Proceeding ��� ICC order expected to be issued by December 11, 2015 (1) Amounts represent ComEd’s position filed in surrebuttal testimony on August 20, 2015. Note: Disallowance of any items in the 2015 distribution formula rate filing could impact 2015 earnings in the form of a regulatory asset adjustment. |