1

NAPTP MLP Conference

May 22, 2008

Steve Blank

Senior VP, CFO & Treasurer

2

This presentation contains certain estimates, predictions, projections, assumptions

and other forward-looking statements that involve various risks and uncertainties.

While these forward-looking statements, and any assumptions upon which they are

based, are made in good faith and reflect our current judgment regarding the direction

of our business, actual results will almost always vary, sometimes materially, from any

estimates, predictions, projections, assumptions or other future performance

suggested in this report. These forward-looking statements can generally be identified

by the words "anticipates," "believes," "expects," "plans," "intends," "estimates,"

"forecasts," "budgets," "projects," "will," "could," "should," "may" and similar

expressions. These statements reflect our current views with regard to future events

and are subject to various risks, uncertainties and assumptions. For a discussion of

certain of those risks, please read "Risk Factors" in Item 1A of NuStar Energy L.P's and

NuStar GP Holdings, LLC's Form 10-K for the year ended December 31, 2007 and

subsequent quarterly reports as filed with the Securities and Exchange Commission.

Forward Looking Statements

3

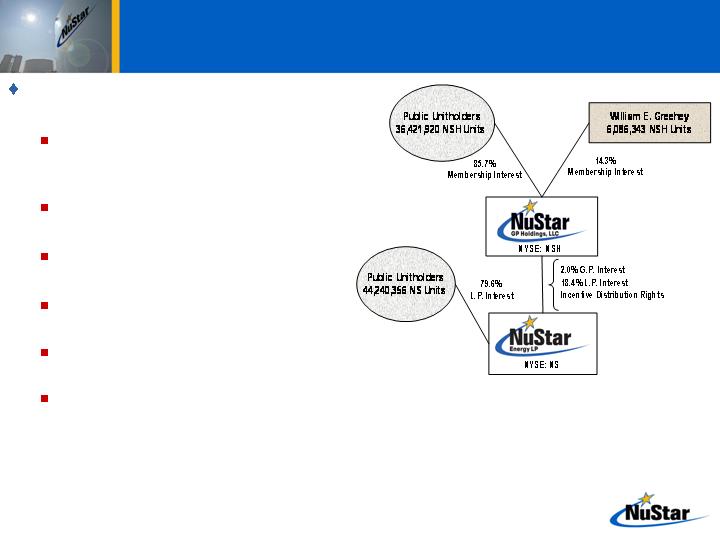

A leading publicly traded growth-

oriented partnership (NYSE: NS)

One of the largest independent

petroleum pipeline and terminal

operators in the U.S.

One of the largest asphalt refiners and

marketers in the U.S.

Total unitholder return of approximately

230% since IPO in April 2001

Recently reported record 1Q08

earnings

Public owns approximately 80% of

NuStar Energy L.P.’s common units

NuStar GP Holdings, LLC (NYSE: NSH)

holds remaining ownership of NuStar

Energy L.P. including 2% general

partner interest, around 18% of NuStar

Energy L.P.’s common units and all of

the incentive distribution rights

NuStar Overview

4

4

Well-Diversified Asset Base

Assets Stats:

9,063 miles of crude oil and refined

product pipelines

85 terminal facilities and four crude

oil storage tank facilities

Over 86 million barrels of storage

capacity

2 asphalt refineries capable of

processing 104,000 bpd of crude oil

5

5

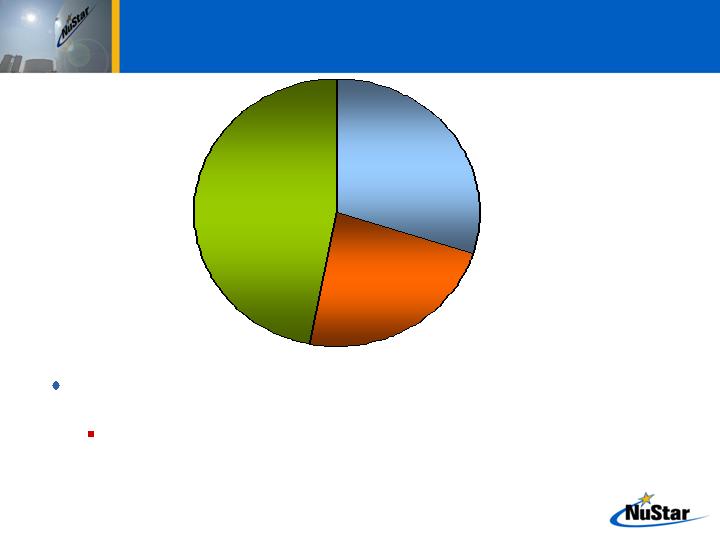

Primarily Fee-Based Assets

Nearly 80% of segment assets at NuStar Energy generate stable, fee-based

income

Includes refined product terminals, refined product and crude oil pipelines and crude

oil storage tanks

Storage

(Terminals & Tanks)

Transportation

(Refined Product & Crude

Oil Pipelines)

Refining & Marketing

47%

30%

23%

Note: Percentages are based on March 31, 2008 asset values, including a preliminary purchase price allocation for the CITGO

Asphalt Refining acquisition. Recently combined business segments into three primary segments instead of five

segments.

6

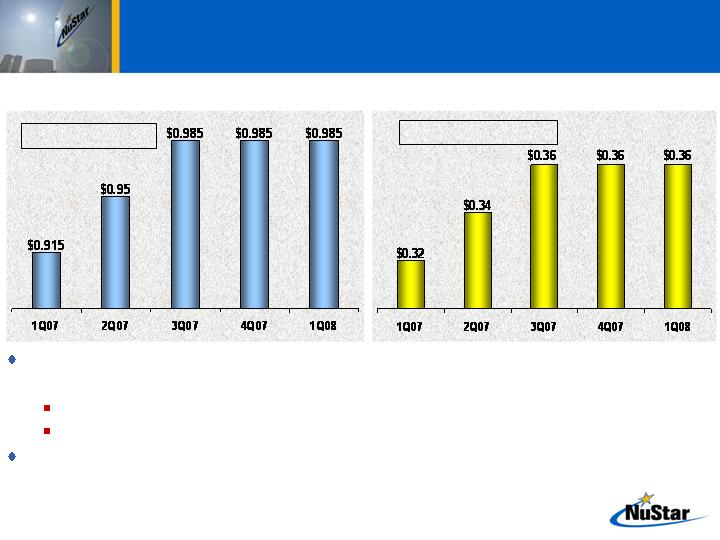

Good Distribution Growth

NuStar Energy L.P.

Quarterly Distribution Increases

NuStar Energy L.P. declared a 1st quarter 2008 distribution of $0.985 per unit, or $3.94 per unit,

on an annual basis

Healthy coverage ratio of 1.36 times applicable to the limited partners for 1st quarter of 2008

Cost of capital lower as incentive distribution rights are capped at 25%

NuStar GP Holdings, LLC declared a 1st quarter 2008 distribution to $0.36 per unit, or $1.44

per unit, on an annual basis

~8% Y-o-Y growth

NuStar GP Holdings, LLC

Quarterly Distribution Increases

~12.5% Y-o-Y growth

7

7

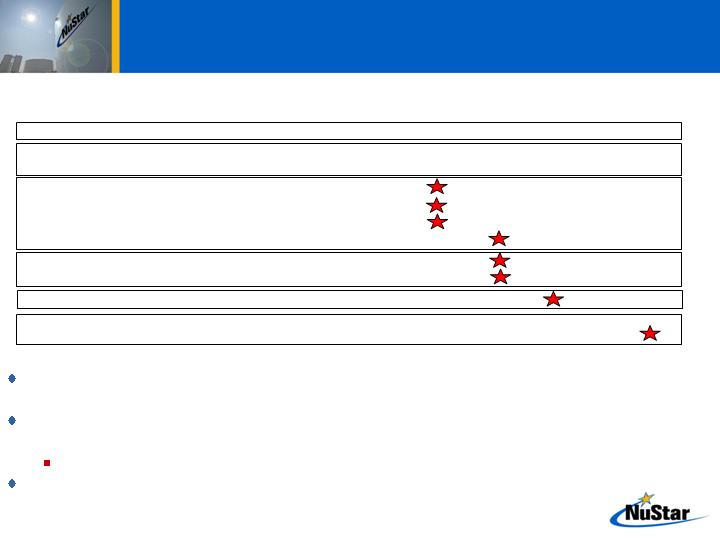

(Dollars in Millions)

P = Phase

Strategic Project Update

* Projects still under evaluation

Majority of projects under $400 million construction program expected to be complete by

the end of 2008

Recently announced $500 million of new pipeline and terminal projects to help fuel

partnership’s growth beyond 2008

Does not include other potential projects from acquisition of CITGO Asphalt Refining Company

Expect IRRs to be in the range of 15% to 20% for all projects

Completed

Completed

Total Capital

In-Service Dates

Major Projects Investment 1Q08 2Q08 3Q08 4Q08 2009-2011

Major Projects Completed in Late 2006 & 2007

~$90.0

Amsterdam Expansion – Partial P1

50.0

St. Eustatius Expansion – P3

19.5

Amsterdam Expansion – Partial P1 & P2

30.0

Linden, NJ Optimization

7.9

Texas City, TX Expansion

33.1

St. James, LA Expansion

52.1

Amsterdam Expansion – P3

28.5

Jacksonville Expansion

21.0

Texas City, TX Expansion

12.8

New Pipeline and Terminal Construction

Program*

500

Total

~$845

8

8

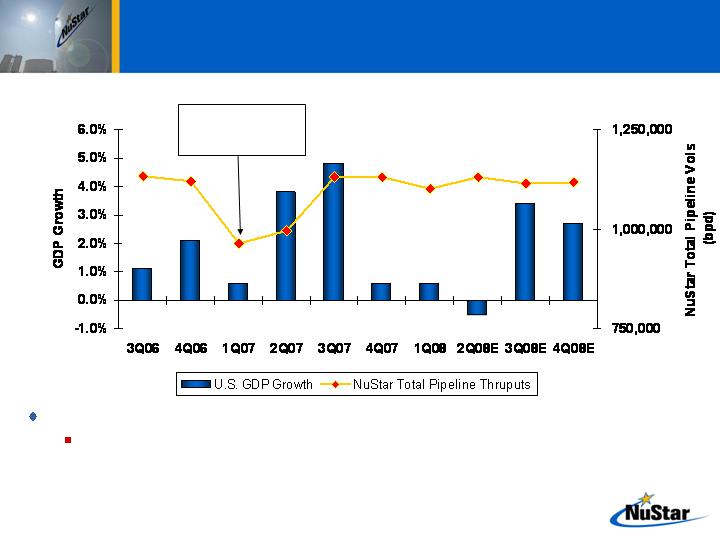

Slower Economic Growth Not Expected to

Materially Impact NuStar’s Throughputs

GDP Growth vs. NuStar Total Pipeline Throughputs

Majority of NuStar’s terminalling business supported by customer contracts

Approximately 90% of new terminal expansions supported by contracts ranging from 5 to 10 years

1.1%

2.1%

0.6%

3.8%

4.8%

0.6%

0.6%

(0.5)%

3.4%

2.7%

Impact of Fire at

Valero Energy’s

McKee Refinery

Source: U.S. Department of Commerce – Bureau of Economic Analysis: Historical GDP figures

Global Insight – Estimated 2008 Quarterly GDP Figures

Notes: Graph starts from 3Q06 to reflect last pipeline deal done at NuStar Energy L.P.

9

9

New Asphalt Business

10

Business comprised of two refineries, three owned

terminals, and leases on 14 third-party terminals

Paulsboro, NJ Refinery: 74 mbpd

Asphalt production is shipped to the Northeast

Total storage capacity of 3.4 million barrels

Savannah, GA Refinery: 30 mbpd

Asphalt production shipped to the Southeast

Sole refinery and asphalt producer on the Southeast

seaboard

Total storage capacity of 1.2 million barrels

Wilmington, North Carolina Terminal

Total storage capacity of 240,000 barrels

14 third-party leased terminals with total asphalt storage

capacity of 1.7 million barrels

Commitment by PDVSA to supply NuStar an annual

average of 75,000 bpd of crude oil

Right of first offer to purchase nearly 11,000 bpd of paving

grade asphalt and over 13,000 bpd of roofing flux asphalt

each year to the extent exported by PDVSA

Asphalt Asset Overview

11

Strategic Rationale

Compelling opportunity to buy assets at 50% of

replacement value

Over the long-term expect to benefit from higher

asphalt margins due to a tightening market

Provides exposure to one of the best asphalt

markets in the U.S.

Continues to diversify NuStar’s customer base and

expands geographic presence

Complements our existing asphalt marketing and

terminals business

Additional strategic projects expected to benefit

results from asphalt business

12

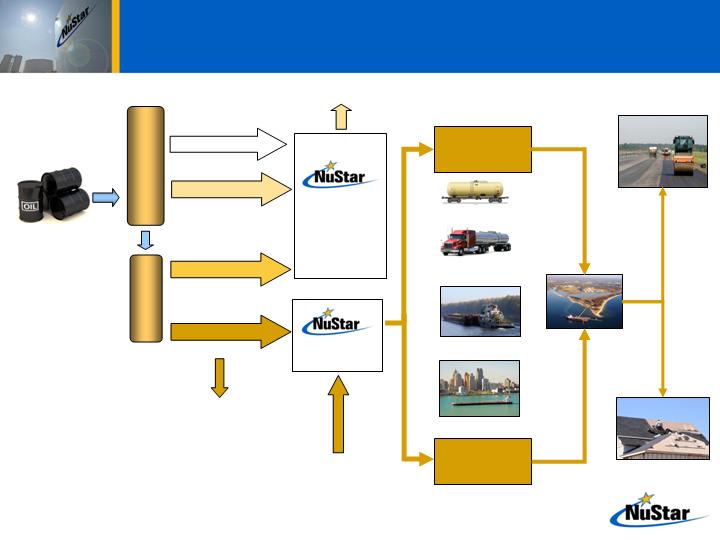

Asphalt Refining -

A Simple Process

Atmospheric

Distillation Tower

Vacuum

Unit

Naphtha

Vacuum Gas Oil

Marine Diesel Oil

Asphalt

~70% Yield

~3% Yield

~9% Yield

~18% Yield

Intermediate

Products

Marketing

Asphalt

Marketing

Paving Contractors

& Hot Mix Producers

80-90%

Asphalt Cement

10-20%

Roofing Flux

Rail

Truck

Barge

Ship

Roofing & Shingle

Manufacturers

Sold to 3rd Party

Refineries

NuStar Owned

& Network of

3rdParty

Terminals

Retail

Sales

(~85%)

Asphalt Imports

Wholesale

Asphalt Sales

(~15%)

13

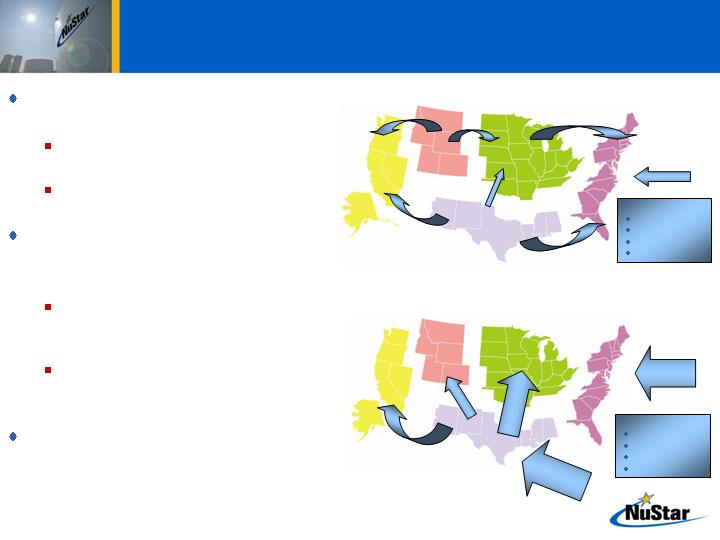

Imports from:

Latin America

Canada

Europe

Africa

East Coast and West Coast are currently

net short asphalt

Excess production in Mid-Continent and

Gulf Coast used to meet current demand

East Coast is also supplemented by

imports

New coker projects in Gulf Coast and

Mid-Continent expected to reduce asphalt

supply

Resulting imbalance expected to result in

higher call on imports and/or cutting back

on coker capacity

Level of coker projects has remained

constant despite recent weak gasoline

margins

Shifting trade flows expected to drive

asphalt margins higher

Imports from:

Latin America

Canada

Europe

Africa

2006 U.S. Inter-PADD Asphalt Flows

(thousands of barrels per day)

Projected 2012 U.S. Inter-PADD Asphalt Flows

(thousands of barrels per day)

15

5

13

19

3

8

3

63

82

53

18

25

Sources: Poten & Partners; PIRA Refinery

Database, Energy Information Agency

Note: Assumes no reduction in coker utilization rates

and fuel oil production

Asphalt Supply Drivers

14

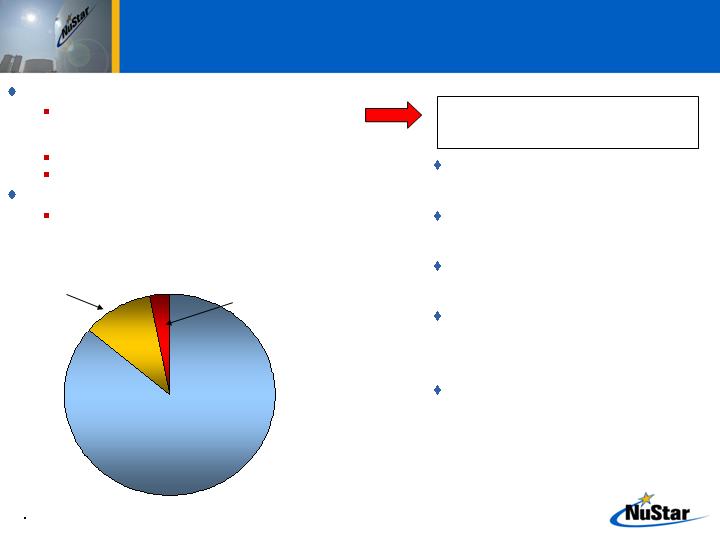

Asphalt Demand Drivers

U.S. Asphalt Demand

Asphalt Paving

~86%

Roofing

~11%

Other*

~3%

Paving

Aging highway system, increased focus on preventative

road maintenance and increases in total highway miles

driven

Residential and commercial construction

Federal, state and local funding for highway projects

Roofing

Re-roofing projects account for majority of asphalt

demand versus new builds

Consists of coating and sealer markets and asphalt consumed in

industrial applications such as paint, paper and steel manufacturing

Only spending a fraction of what we

should to maintain roads

Approximately 33% of roads are in fair

to poor condition**

Currently spending around $70 billion

annually on highways***

Estimated $185 billion required each

year to maintain roads in current

condition***

Estimated $200 billion required to

upgrade roads to good condition***

Significant Infrastructure

Needs in the U.S.

** Source: TRIP

*** Source: National Surface Transportation

Policy & Revenue Commission

15

15

Expect PADD I (i.e. East Coast) asphalt margins to recover from the first part of 2008 and

fourth quarter 2007 levels due to:

Seasonal asphalt demand ramping up during the second quarter

Low inventory levels on the U.S. East Coast compared to last year

Level of asphalt imports to PADD I has declined over the past six months

Expect a decrease in asphalt demand due to higher asphalt prices in PADD I

Continue to be bullish on long-term fundamentals given the coker projects coming on-stream

over the next few years

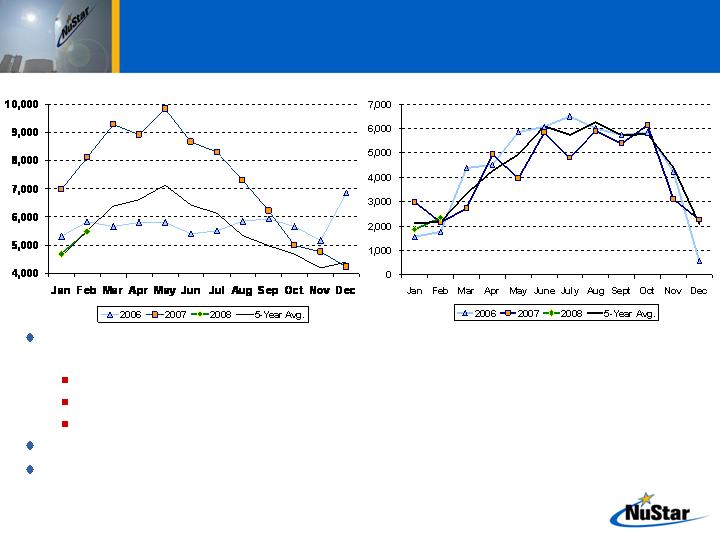

PADD I Asphalt

Current Supply & Demand Fundamentals

PADD I Asphalt Inventories (000 barrels)

PADD I Asphalt Demand (000 barrels)

Source of data for graphs: Energy Information Administration

16

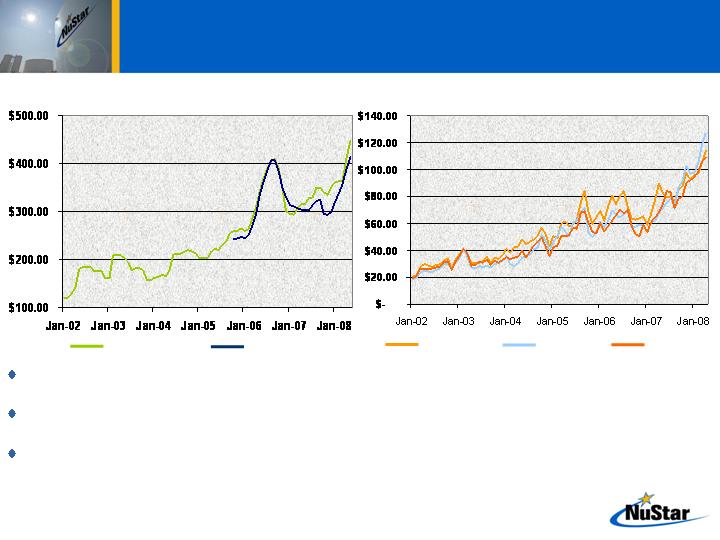

Increasing Product Prices

Asphalt and intermediate product prices have been generally increasing although have lagged the

rapid run-up in crude oil prices

Expect asphalt prices of $430 to $475 per short ton for the second and third quarters of 2008

reflective of seasonal demand

Prices for intermediate products continue to strengthen providing valuable contribution to NuStar’s

results

Asphalt Cement Price Index ($ per short ton)*

State of New Jersey State of Georgia

* Source: State of New Jersey Dept. of Transportation and State of Georgia Dept. of Transportation

** Source: OPIS

Note: Prices for intermediate products above are shown as proxies only for NuStar’s intermediate products

Intermediate Products - Proxy Prices

($ per barrel)**

USGC Naphtha

USGC LCO

USGC HSVGO

17

Buying Crude Oil Feedstocks

at Deep Discounts

Despite recent run-up in crude oil prices, NuStar is paying significant discounts for the

crude oil it is buying from Venezuela (i.e. BCF-13 and Boscan crude oils)

BCF-13 and Boscan crude oils are very low-quality crudes purchased at a deep-discount to

sweet crudes (i.e. WTI) and to other heavy-sour crudes (i.e. Mexican Maya)

Crude feedstocks are ideal to run at NuStar’s refineries since they produce a high yield

of asphalt

Comparative Crude Oil Prices ($ per barrel)

WTI *

Mexican Maya *

BCF-13 **

Boscan **

Discount b/w WTI and

Maya currently around

$22/bbl.

Venezuelan crudes

further discounted to

Maya crude by

approx. $15/bbl.

* Source: Platts

** Source: Company

18

18

Business Strategies

Complete existing $400 million construction program on time and on budget

Quickly integrate recently acquired asphalt business

Prioritize and execute projects on recently acquired asphalt business

Continue to focus on pipeline, transportation, storage and terminalling operations

Continue to expand terminals and storage in key hub locations and pipelines through internal growth

projects and acquisitions

Recently announced $500 million construction program beyond 2008 (excluding CITGO Asphalt

Refining Company)

Continue to expand opportunities for marketing business

Maintain financial strength, flexibility and investment grade debt rating

We believe this strategy will allow NuStar to continue to provide further

distribution growth