Exhibit 99.1

|

NiSource Investor Day

Millennium Broadway Hotel New York, New York September 12, 2012

|

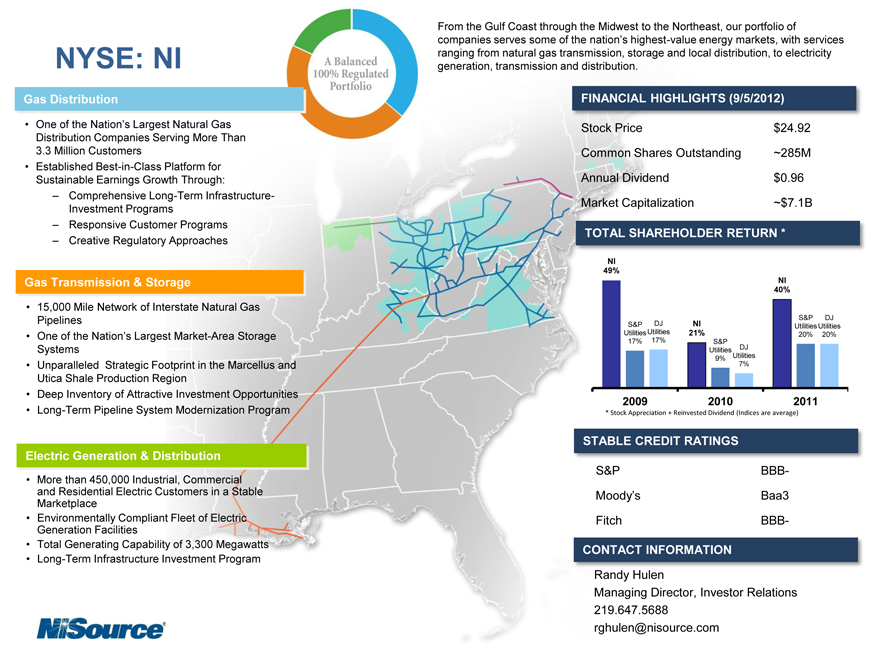

From the Gulf Coast through the Midwest to the Northeast, our portfolio of companies serves some of the nation’s highest-value energy markets, with services ranging from natural gas transmission, storage and local distribution, to electricity generation, transmission and distribution.

NYSE: NI

Gas Distribution

• One of the Nation’s Largest Natural Gas

Distribution Companies Serving More Than

3.3 Million Customers

• Established Best-in-Class Platform for Sustainable Earnings Growth Through:

– Comprehensive Long-Term Infrastructure-Investment Programs

– Responsive Customer Programs

– Creative Regulatory Approaches

Gas Transmission & Storage

• 15,000 Mile Network of Interstate Natural Gas Pipelines

• One of the Nation’s Largest Market-Area Storage

Systems

• Unparalleled Strategic Footprint in the Marcellus and Utica Shale Production Region

• Deep Inventory of Attractive Investment Opportunities

• Long-Term Pipeline System Modernization Program

Electric Generation & Distribution

• More than 450,000 Industrial, Commercial and Residential Electric Customers in a Stable Marketplace

• Environmentally Compliant Fleet of Electric Generation Facilities

• Total Generating Capability of 3,300 Megawatts

• Long-Term Infrastructure Investment Program

FINANCIAL HIGHLIGHTS (9/5/2012)

Stock Price $24.92

Common Shares Outstanding ~285M

Annual Dividend $0.96

Market Capitalization ~$7.1B

TOTAL SHAREHOLDER RETURN *

NI 49%

S&P DJ Utilities Utilities 17% 17%

NI 21%

S&P Utilities DJ

9% Utilities 7%

NI 40%

S&P DJ Utilities Utilities 20% 20%

2009 2010 2011

* |

| Stock Appreciation + Reinvested Dividend (Indices are average) |

STABLE CREDIT RATINGS

S&P BBB-

Moody’s Baa3

Fitch BBB-

CONTACT INFORMATION

Randy Hulen

Managing Director, Investor Relations 219.647.5688 rghulen@nisource.com

|

Forward Looking Statements

Today’s presentations contain forward-looking statements within the meaning of federal securities laws. These forward-looking statements are subject to various risks and uncertainties. Examples of forward-looking statements in these presentations include statements and expectations regarding future dividends, operating earnings growth, earnings per share growth, capital investments, financing needs and plans, and investment opportunities. Factors that could cause actual results to differ materially from the projections, forecasts, estimates and expectations discussed in these presentations include, among other things, weather; fluctuations in supply and demand for energy commodities; growth opportunities for NiSource’s businesses; increased competition in deregulated energy markets; the success of regulatory and commercial initiatives; dealings with third parties over whom NiSource has no control; actual operating experience of NiSource’s assets; the regulatory process; regulatory and legislative changes; changes in general economic, capital and commodity market conditions; and counter-party credit risk, and the matters set forth in the “Risk Factors” section in NiSource’s 2011 Form 10-K (which section is incorporated herein by reference) and in conjunction with other SEC reports filed by NiSource, many of which are beyond the control of NiSource. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of this presentation. Future earnings are illustrative only and do not constitute guidance by the Company. NiSource expressly disclaims a duty to update any of the forward-looking statements contained in these presentations.

With regard to Net Operating Earnings Guidance for 2012 – it should be noted that there will likely be differences between net operating earnings and GAAP earnings for matters including, but not limited to, weather, restructuring costs and accounting changes. NiSource is not able to estimate the impact of such items on GAAP earnings and, as such, is not providing earnings guidance on a GAAP basis.

Regulation G Disclosure Statement

Today’s presentations include certain non-GAAP financial measures as defined by the SEC’s Regulation G. A reconciliation of those measures to the most directly comparable GAAP measures is contained in [Schedules 1 and 2 of the NiSource quarterly earnings release and pages 8 and 15 through 18 in the 2011 Statistical Summary Book, both of which are available on the NiSource Investor Relations website at http://ir.nisource.com/results.cfm and http://ir.nisource.com/annuals.cfm.

|

Today’s Agenda

Building Investment-Driven Growth

Strategic Framework

Bob Skaggs and Key Takeaways

Business Unit NiSource Gas Distribution, Joe Hamrock NIPSCO Electric, Jimmy Staton

Discussions NiSource Gas Transmission & Storage, Jimmy Staton

Financial Profile Steve Smith

Closing Remarks Bob Skaggs

|

Speaker Bios

Bob Skaggs

President & Chief Executive Officer

Robert (Bob) Skaggs, Jr., is president and chief executive officer of NiSource Inc. He is responsible for the strategic direction of the company as well as for overseeing its day-to-day operations. Bob was named president in Oct. 2004 and added the CEO responsibilities effective July 2005. Bob earned a bachelor’s degree in economics from Davidson College, a law degree from West Virginia University and a master’s degree in business administration from Tulane University. .

Steve Smith

Executive Vice President & Chief Financial Officer

Stephen (Steve) Smith is executive vice president and chief financial officer of NiSource Inc. He is responsible for the company’s corporate finance functions, information technology, supply chain services, and real estate and facilities management.

Steve earned a bachelor’s degree in petroleum engineering from the Colorado School of Mines and a master’s degree in business administration from the University of Chicago Graduate School of Business.

Glen Kettering

Senior Vice President, Corporate Affairs

Glen Kettering is senior vice president, Corporate Affairs at

NiSource Inc. He is responsible for leading the company’s investor relations, communications and federal government affairs functions. Glen earned a bachelor’s degree in business administration from West Virginia University and a doctor of jurisprudence degree from the West Virginia University College of Law.

Joe Hamrock

Executive Vice President & Group CEO NiSource Gas Distribution

Joseph (Joe) Hamrock serves as executive vice president and group CEO for NiSource Gas Distribution, which includes local gas distribution companies in Kentucky, Maryland, Massachusetts, Ohio, Pennsylvania and Virginia. In this role, he has profit-and-loss responsibility for all operations, regulatory and commercial functions. Joe received a bachelor’s degree in electrical engineering from Youngstown State University and a master’s degree in business administration from the Massachusetts Institute of Technology.

Jimmy Staton

Executive Vice President & Group CEO

NiSource Gas Transmission & Storage & NIPSCO

Jimmy Staton serves as executive vice president and group CEO for NiSource Gas Transmission & Storage (NGT&S) and also is responsible for Northern Indiana Public Service Company (NIPSCO) through Oct. 1, 2012. In these roles, he oversees all commercial, regulatory, operations and project development, and is responsible for execution of the business growth strategies. Jimmy earned a bachelor’s degree in petroleum engineering from Louisiana State

University.

|

Strategic Framework and Key Takeaways

Bob Skaggs

President & CEO September 12, 2012

|

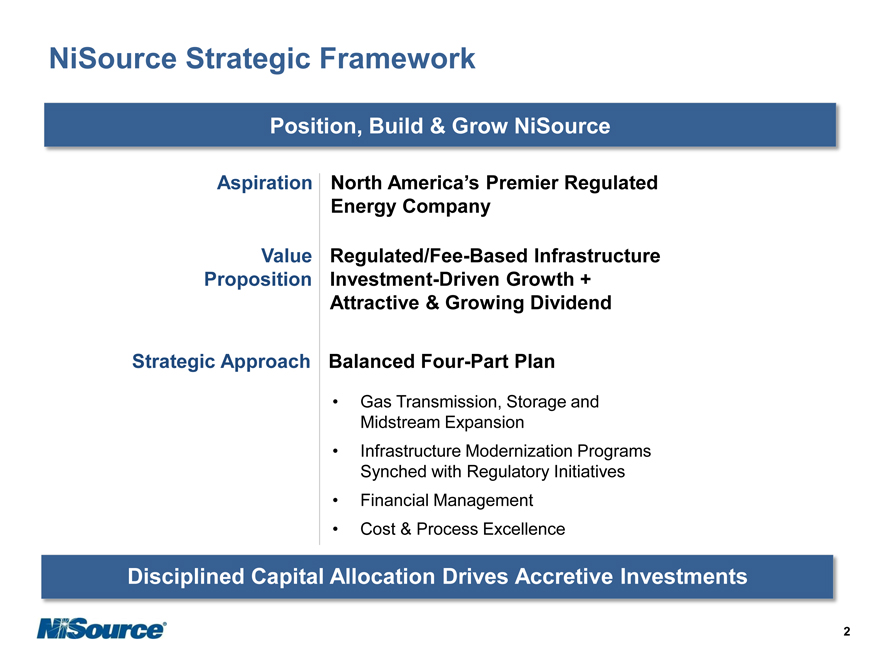

NiSource Strategic Framework

Position, Build & Grow NiSource

Aspiration

Value

Proposition

Strategic Approach

North America’s Premier Regulated

Energy Company

Regulated/Fee-Based Infrastructure Investment-Driven Growth + Attractive & Growing Dividend

Balanced Four-Part Plan

• Gas Transmission, Storage and Midstream Expansion

• Infrastructure Modernization Programs Synched with Regulatory Initiatives

• Financial Management

• Cost & Process Excellence

Disciplined Capital Allocation Drives Accretive Investments

2 |

|

|

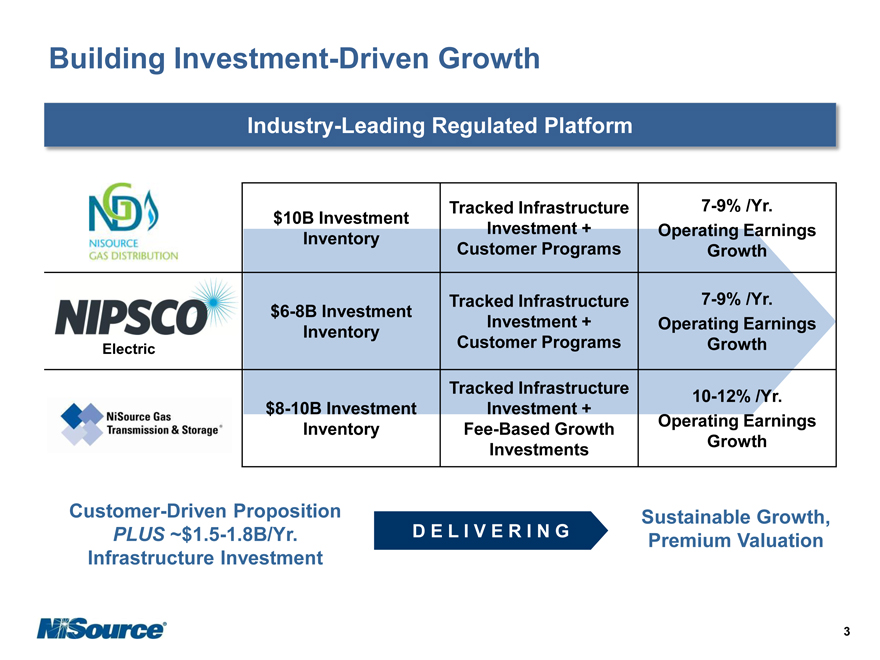

Building Industry-Leading Investment Regulated -Driven Platform Growth

Industry-Leading Regulated Platform

Electric

$10B Investment Tracked Infrastructure 7-9% /Yr.

Inventory Investment + Operating Earnings

Customer Programs Growth

$6-8B Investment Tracked Infrastructure 7-9% /Yr.

Inventory Investment + Operating Earnings

Customer Programs Growth

Tracked Infrastructure 10-12% /Yr.

$8-10B Investment Investment +

Inventory Fee-Based Growth Operating Earnings

Investments Growth

Customer-Driven Proposition PLUS ~$1.5-1.8B/Yr.

Infrastructure Investment

D E L I V E R I N G

Sustainable Growth, Premium Valuation

3 |

|

|

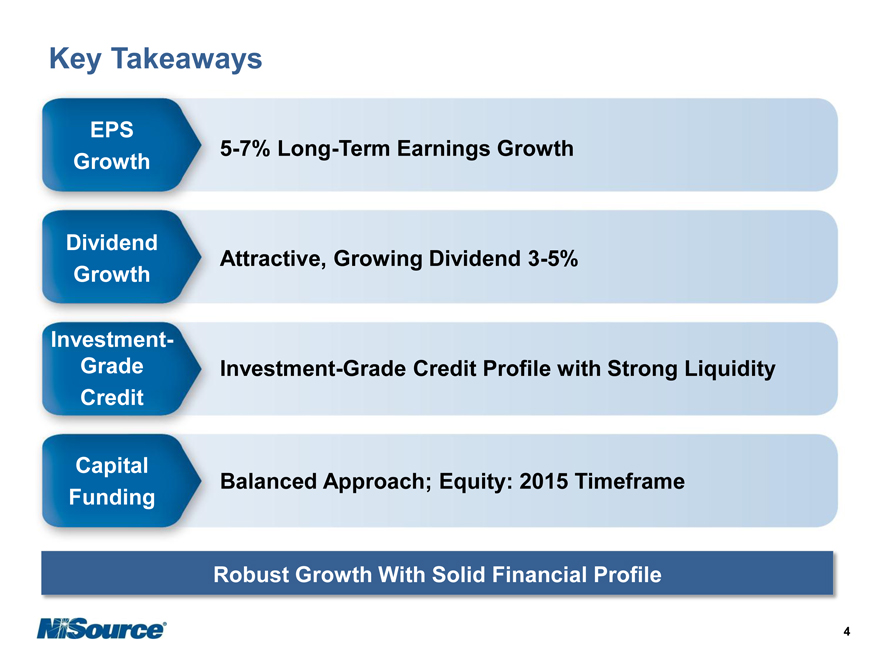

Key Takeaways

EPS Growth

Dividend Growth

Investment-

Grade Credit

Capital Funding

5-7% Long-Term Earnings Growth Attractive, Growing Dividend 3-5%

Investment-Grade Credit Profile with Strong Liquidity

Balanced Approach; Equity: 2015 Timeframe

Robust Growth With Solid Financial Profile

4 |

|

|

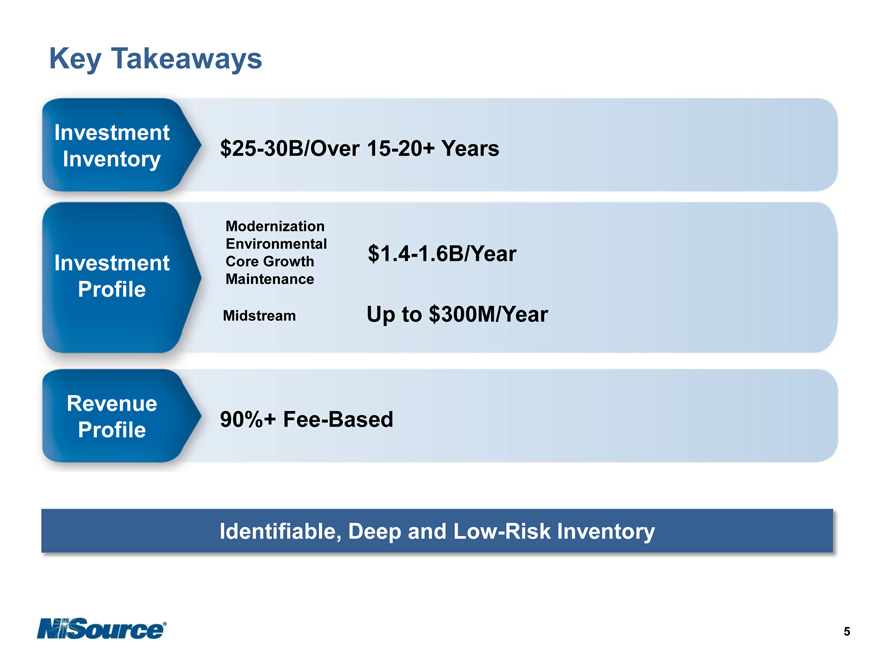

Key Takeaways

Investment

Inventory

Investment

Profile

Revenue

Profile

$25-30B/Over 15-20+ Years

Modernization

Environmental $1.4-1.6B/Year

Core Growth Maintenance

Midstream Up to $300M/Year

90%+ Fee-Based

Identifiable, Deep and Low-Risk Inventory

5 |

|

|

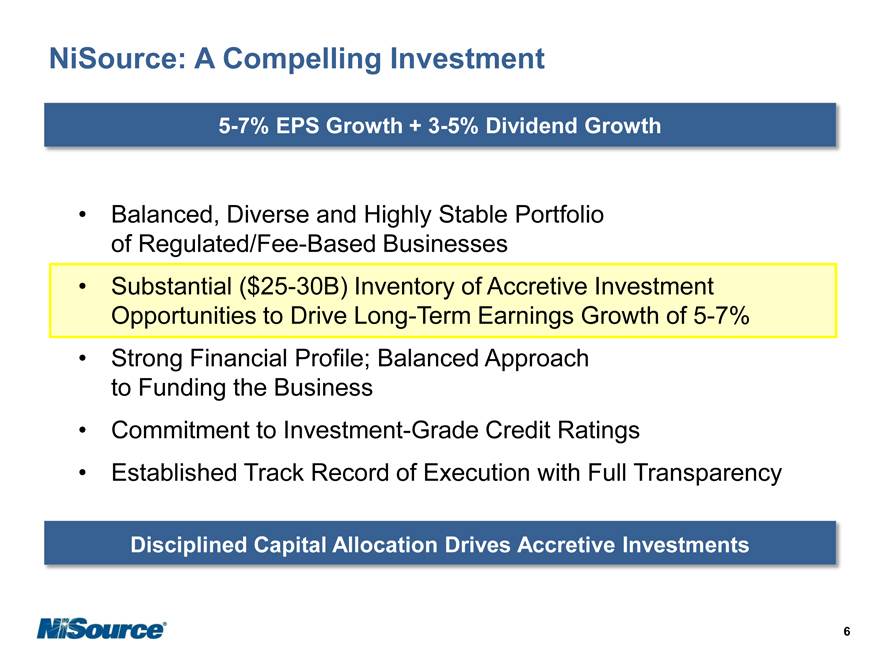

NiSource: A Compelling Investment

5-7% EPS Growth + 3-5% Dividend Growth

Balanced, Diverse and Highly Stable Portfolio of Regulated/Fee-Based Businesses

Substantial ($25-30B) Inventory of Accretive Investment Opportunities to Drive Long-Term Earnings Growth of 5-7% Strong Financial Profile; Balanced Approach to Funding the Business Commitment to Investment-Grade Credit Ratings Established Track Record of Execution with Full Transparency

Disciplined Capital Allocation Drives Accretive Investments

6 |

|

|

Gas Distribution

Joe Hamrock

EVP & Group CEO September 12, 2012

|

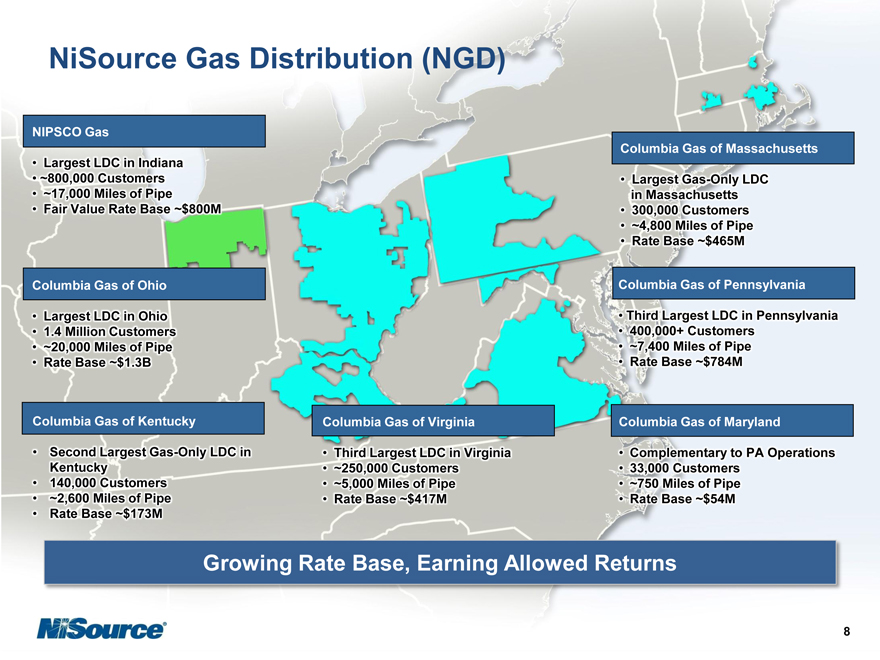

NiSource Gas Distribution (NGD)

NIPSCO Gas

• Largest LDC in Indiana

• ~800,000 Customers • ~17,000 Miles of Pipe

• Fair Value Rate Base ~$800M

Columbia Gas of Ohio

• Largest LDC in Ohio • 1.4 Million Customers • ~20,000 Miles of Pipe • Rate Base ~$1.3B

Columbia Gas of Kentucky

• Second Largest Gas-Only LDC in Kentucky

• 140,000 Customers

• ~2,600 Miles of Pipe

• Rate Base ~$173M

Columbia Gas of Virginia

• Third Largest LDC in Virginia • ~250,000 Customers • ~5,000 Miles of Pipe • Rate Base ~$417M

Columbia Gas of Massachusetts

• Largest Gas-Only LDC in Massachusetts • 300,000 Customers • ~4,800 Miles of Pipe • Rate Base ~$465M

Columbia Gas of Pennsylvania

• Third Largest LDC in Pennsylvania • 400,000+ Customers • ~7,400 Miles of Pipe • Rate Base ~$784M

Columbia Gas of Maryland

• Complementary to PA Operations

• 33,000 Customers

• ~750 Miles of Pipe

• Rate Base ~$54M

Growing Rate Base, Earning Allowed Returns

8 |

|

|

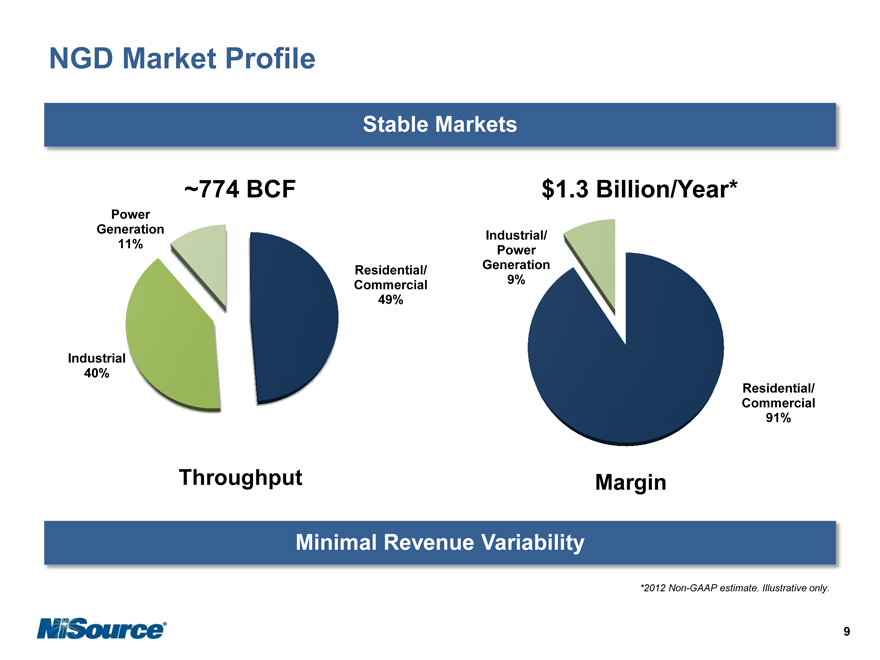

NGD Market Profile

Stable Markets

~774 BCF

Power Generation 11%

Industrial 40%

Residential/ Commercial 49%

Throughput

$1.3 Billion/Year*

Industrial/ Power Generation 9%

Margin

Residential/ Commercial 91%

Minimal Revenue Variability

*2012 Non-GAAP estimate. Illustrative only.

9

|

NGD Performance

Delivering for Our Customers, Communities and Other Key Stakeholders

Safety/ Reliability

Customer Experience

Stakeholder Relations

Customer Rates

Financial Performance

Top Decile/Quartile Performance Robust Programs and Satisfaction Scores Collaborative, Constructive Approach Competitive, Affordable, Innovative Designs

Growing Rate Base, Earning Allowed Returns

10

|

NGD Business Strategy

Executing a Strategy for Sustainable Long-Term Growth

Long-Term Growth Through Investment in

Infrastructure Modernization and Innovative Rate Structures

• Expanded Infrastructure Programs Under Similar Policy Frameworks

• Total Asset Base Modernization

• Reliable, Safe and Economic Services for Customers

• Local Economic Development

~$10B Investment Opportunity Over 20+ Years

11

|

NGD Business Strategy

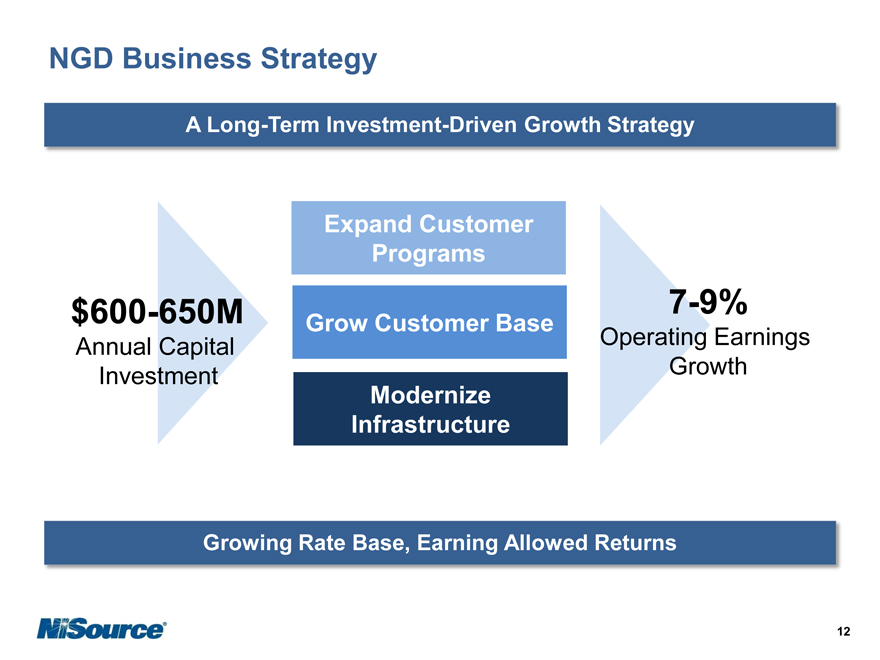

A Long-Term Investment-Driven Growth Strategy

$600-650M

Annual Capital Investment

Expand Customer Programs

Grow Customer Base

Modernize Infrastructure

7-9%

Operating Earnings Growth

Growing Rate Base, Earning Allowed Returns

12

|

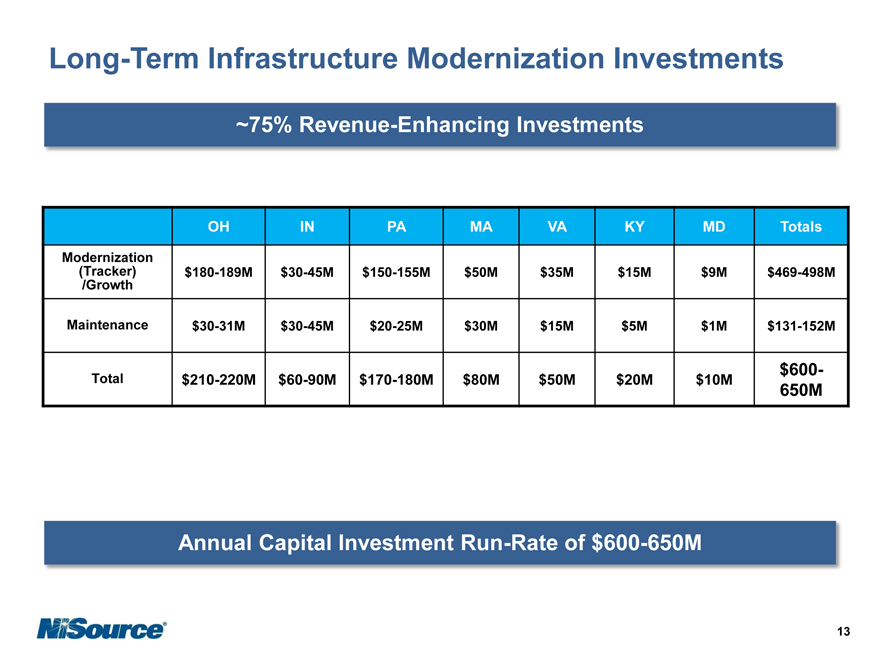

Long-Term Infrastructure Modernization Investments

~75% Revenue-Enhancing Investments

OH IN PA MA VA KY MD Totals

Modernization

(Tracker) $180-189M $30-45M $150-155M $50M $35M $15M $9M $469-498M

/Growth

Maintenance $30-31M $30-45M $20-25M $30M $15M $5M $1M $131-152M

Total $210-220M $60-90M $170-180M $ 80M $ 50M $20M $10M $600-

650M

Annual Capital Investment Run-Rate of $600-650M

13

|

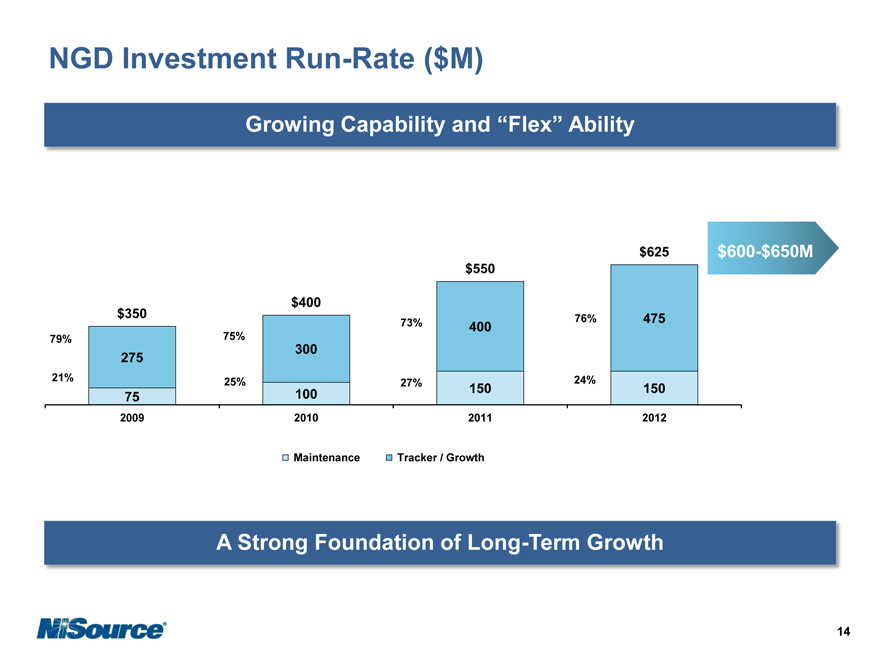

NGD Investment Run-Rate ($M)

Growing Capability and “Flex” Ability

$600-$650M

$625 $550

$350 $400

73% 76% 475

400

79% 75%

300 275

21% 25% 24%

100 27% 150 150 75

2009 2010 2011 2012

Maintenance Tracker / Growth

A Strong Foundation of Long-Term Growth

14

|

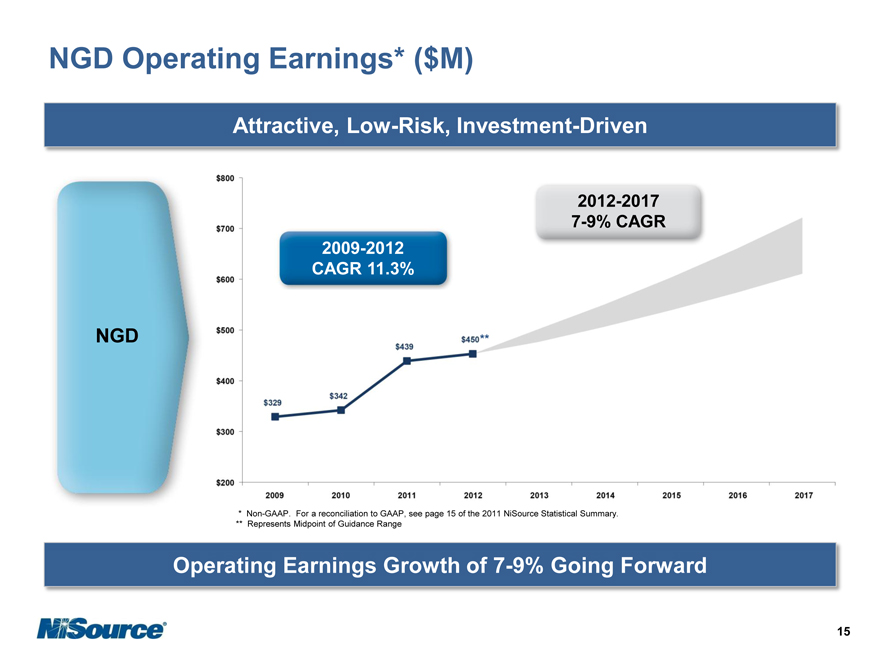

NGD Operating Earnings* ($M)

Attractive, Low-Risk, Investment-Driven

NGD

2009-2012

CAGR 11.3%

2012-2017

7-9% CAGR

* |

| Non-GAAP. For a reconciliation to GAAP, see page 15 of the 2011 NiSource Statistical Summary. |

** Represents Midpoint of Guidance Range

Operating Earnings Growth of 7-9% Going Forward

15

|

NGD Business Strategy

NiSource’s Foundation

Expand Customer Programs

Grow Customer Base

Modernize Infrastructure

Ongoing Disciplined Execution

Sustain Growth Through Long-Term Investment in Infrastructure

Modernization

Maintain Innovative Rate Structures

Deliver Exceptional Customer Satisfaction and Experience

~$10B Investment Opportunity Over 20+ Years

16

|

Appendix

17

|

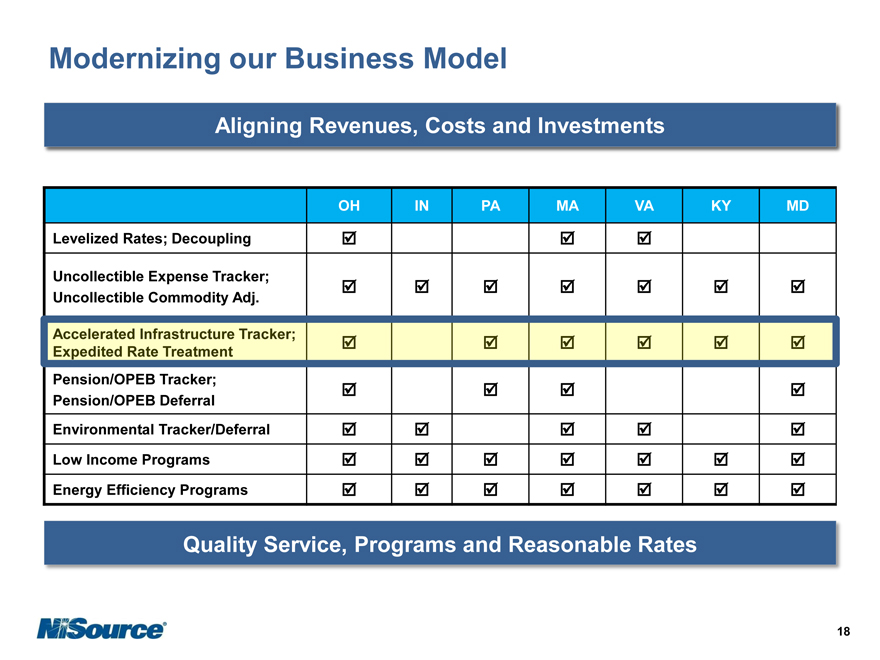

Modernizing our Business Model

Aligning Revenues, Costs and Investments

OH IN PA MA VA KY MD

Levelized Rates; Decoupling

Uncollectible Expense Tracker; Uncollectible Commodity Adj.

Pension/OPEB Tracker; Pension/OPEB Deferral

Environmental Tracker/Deferral Low Income Programs Energy Efficiency Programs

Quality Service, Programs and Reasonable Rates

18

|

NIPSCO Electric

Jimmy Staton

EVP & Group CEO September 12, 2012

|

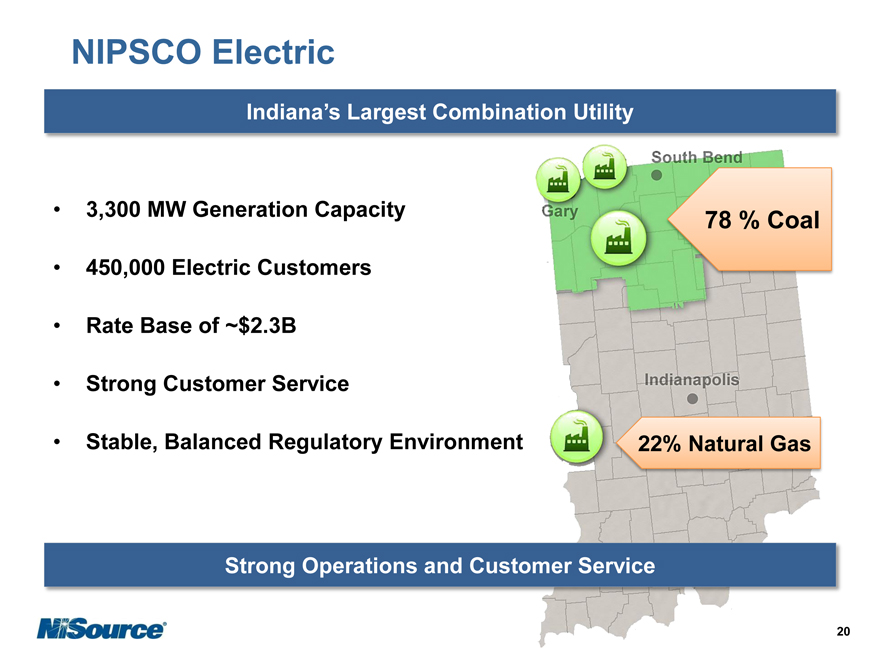

Indiana’s Largest Combination Utility

450,000 Electric Customers Rate Base of ~$2.3B Strong Customer Service

Stable, Balanced Regulatory Environment

78 % Coal

22% Natural Gas

Strong Operations and Customer Service

20

|

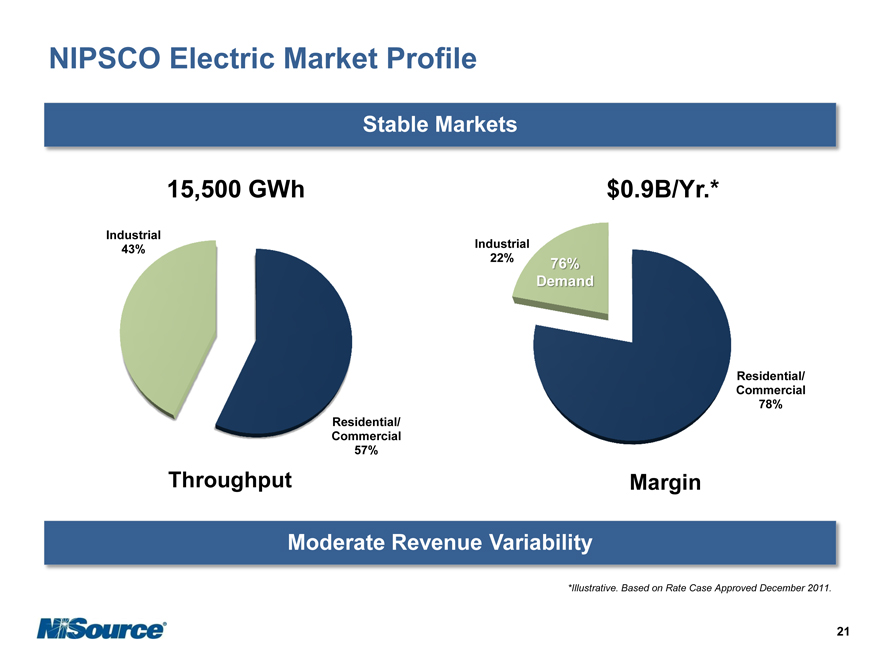

NIPSCO Electric Market Profile

Stable Markets

15,500 GWh

$0.9B/Yr.*

Industrial 43%

Residential/ Commercial 57%

Throughput

Industrial 22%

76% Demand

Residential/ Commercial 78%

Margin

Moderate Revenue Variability

*Illustrative. Based on Rate Case Approved December 2011.

21

|

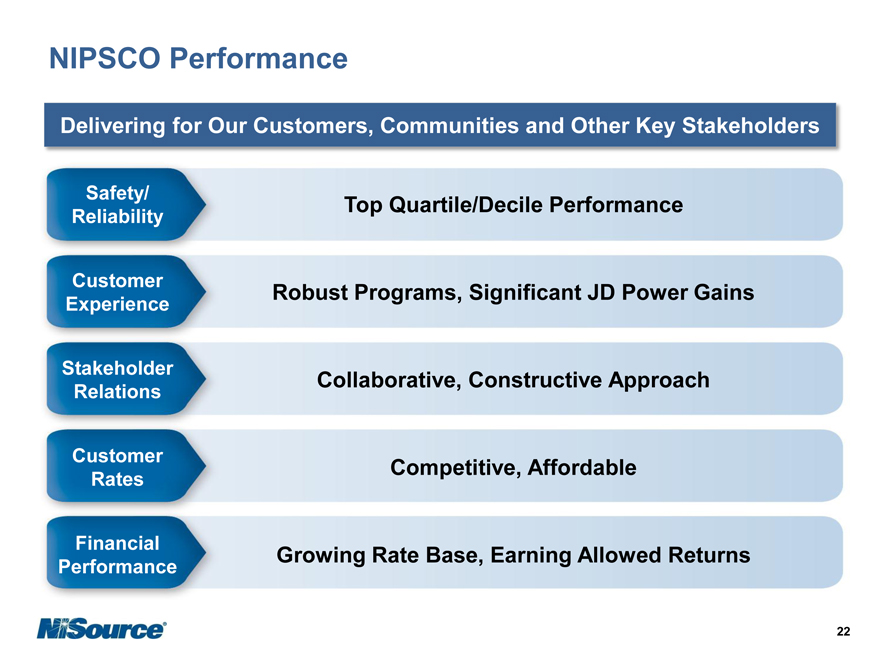

NIPSCO Performance

Delivering for Our Customers, Communities and Other Key Stakeholders

Safety/ Reliability

Customer Experience

Stakeholder Relations

Customer Rates

Financial Performance

Top Quartile/Decile Performance Robust Programs, Significant JD Power Gains Collaborative, Constructive Approach Competitive, Affordable

Growing Rate Base, Earning Allowed Returns

22

|

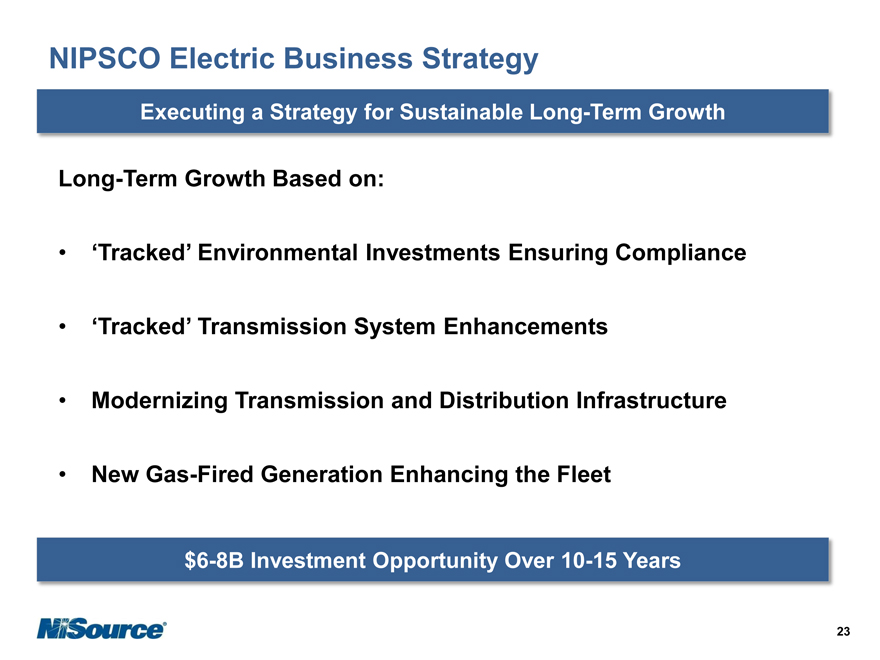

NIPSCO Electric Business Strategy

Executing a Strategy for Sustainable Long-Term Growth

Long-Term Growth Based on:

• ‘Tracked’ Environmental Investments Ensuring Compliance

• ‘Tracked’ Transmission System Enhancements

• Modernizing Transmission and Distribution Infrastructure

• New Gas-Fired Generation Enhancing the Fleet

$6-8B Investment Opportunity Over 10-15 Years

23

|

NIPSCO Electric Business Strategy

Investment-Driven Growth

$400-450M

Annual Capital Investment

Upgrade Generation Fleet

Enhance Transmission System

Modernize

Infrastructure

7-9%

Operating Earnings Growth

Growing Rate Base, Earning Allowed Returns

24

|

NIPSCO Electric Business Strategy

Upgrade Generation Fleet

Plants Investment Compliance Recovery

Technology

Schahfer $525-775M FGDs Tracker

FGD Michigan City (SO2)

All Plants $80M—$ 200M Enhanced Mercury and Tracker

MATS Particulate Controls

All Plants $25M—$ 100M Enhanced Wastewater In S.B. 251

Treatment & Intake Tracker

Water Modification

All Plants $100M—$300M Upgraded Ash In S.B. 251

Ash Handling and Disposal Tracker

$700M-$1.4B Investment Opportunity

25

|

NIPSCO Electric Business Strategy

Enhance Transmission System

Strategically Located at MISO/PJM SEAM

Two MISO Multi-Value Projects

Ongoing Work with MISO to Reduce Congestion

FERC Allowed Returns

Capital Investment

Reynolds to Hiple $250-300M

Reynolds to Greentown $150-200M

(Pioneer Partnership)

$500M-$1B Investment Opportunity

26

|

NIPSCO Electric Business Strategy

Modernize Infrastructure

Systematic Replacement of Aging Infrastructure

Spurs Redevelopment Opportunities, Economic Growth & Jobs

Improved Reliability and System Integrity; Meets Increasing Customer Expectations

Developing DSIC-Type Legislation

$3-4B Investment Opportunity

27

|

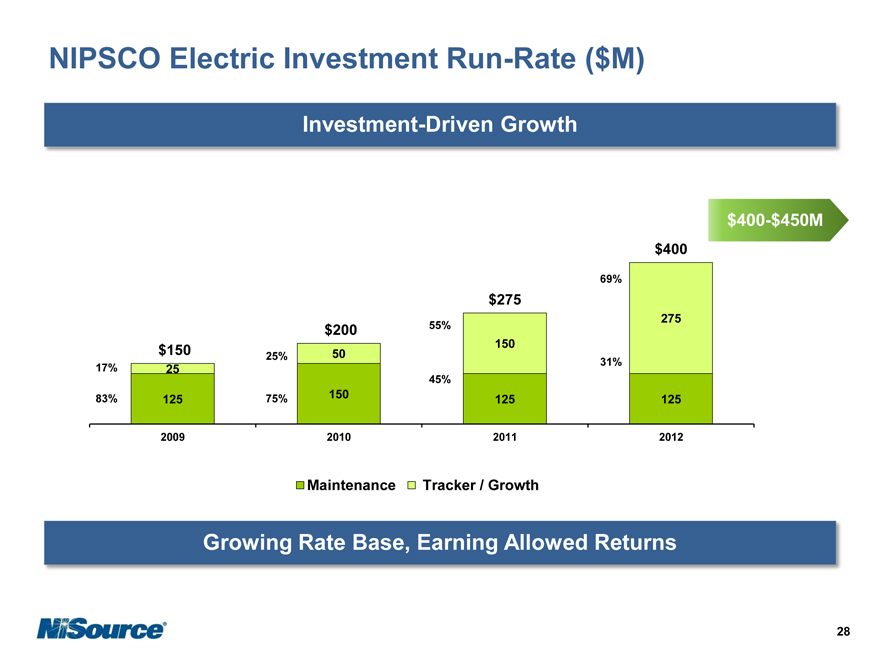

NIPSCO Electric Investment Run-Rate ($M)

Investment-Driven Growth

$400

69%

$275

275

$200 55% $150 50 150

25%

31% 17% 25 45%

83% 125 75% 150 125 125

2009 2010 2011 2012

$400-$450M

Maintenance Tracker / Growth

Growing Rate Base, Earning Allowed Returns

28

|

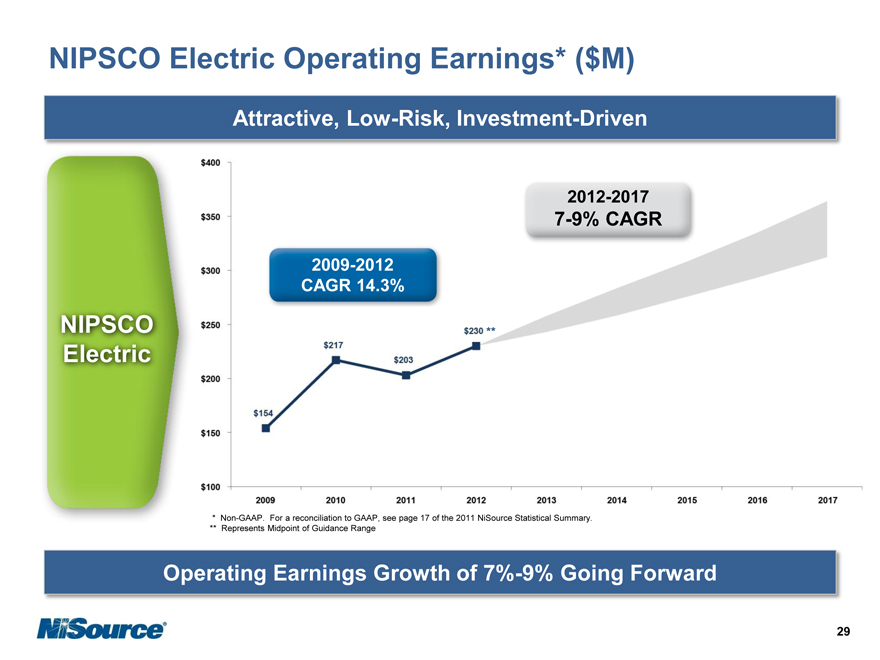

NIPSCO Electric Operating Earnings* ($M)

Attractive, Low-Risk, Investment-Driven

2009-2012

CAGR 14.3%

2012-2017

7-9% CAGR

NIPSCO Electric

* |

| Non-GAAP. For a reconciliation to GAAP, see page 17 of the 2011 NiSource Statistical Summary. |

** Represents Midpoint of Guidance Range

Operating Earnings Growth of 7%-9% Going Forward

29

|

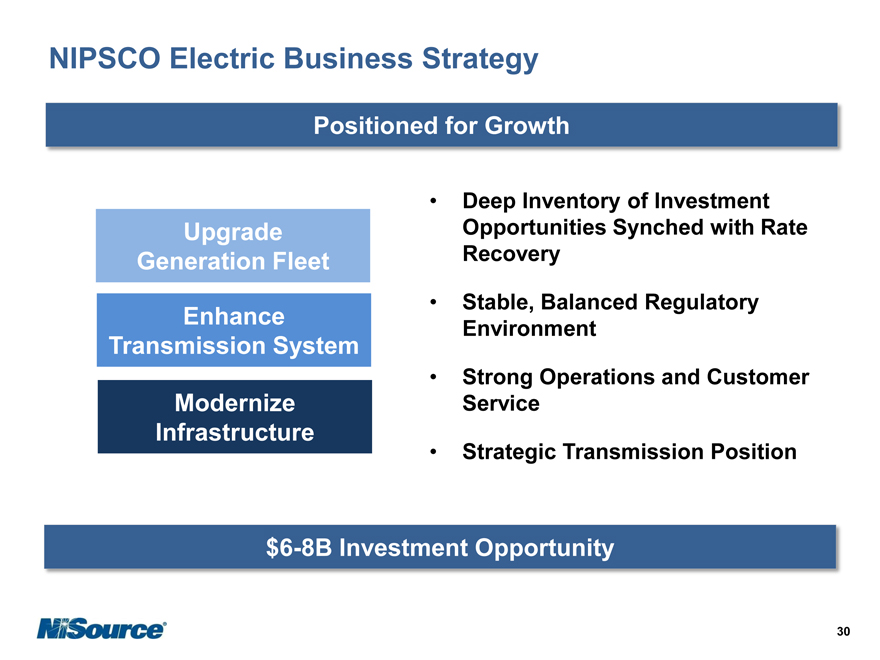

NIPSCO Electric Business Strategy

Positioned for Growth

Upgrade Generation Fleet

Enhance Transmission System

Modernize Infrastructure

Deep Inventory of Investment Opportunities Synched with Rate Recovery

Stable, Balanced Regulatory Environment

Strong Operations and Customer Service

Strategic Transmission Position

$6-8B Investment Opportunity

30

|

Gas Transmission & Storage

Jimmy Staton

EVP & Group CEO September 12, 2012

|

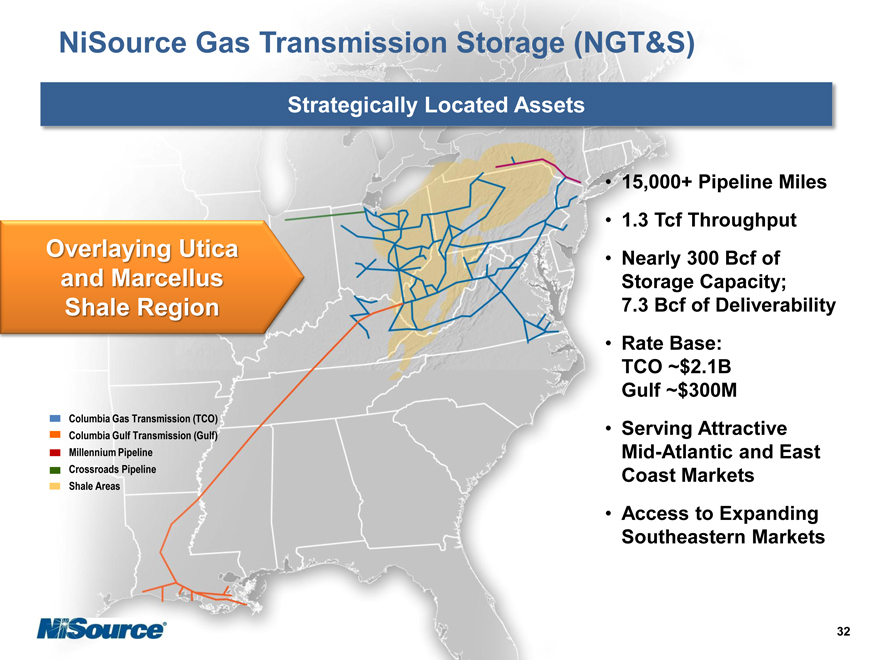

NiSource Gas Transmission Storage (NGT&S)

Strategically Located Assets

Columbia Gas Transmission (TCO) Columbia Gulf Transmission (Gulf) Millennium Pipeline Crossroads Pipeline Shale Areas

15,000+ Pipeline Miles

1.3 Tcf Throughput Nearly 300 Bcf of Storage Capacity;

7.3 Bcf of Deliverability Rate Base: TCO ~$2.1B

Gulf ~$300M Serving Attractive Mid-Atlantic and East Coast Markets Access to Expanding Southeastern Markets

32

|

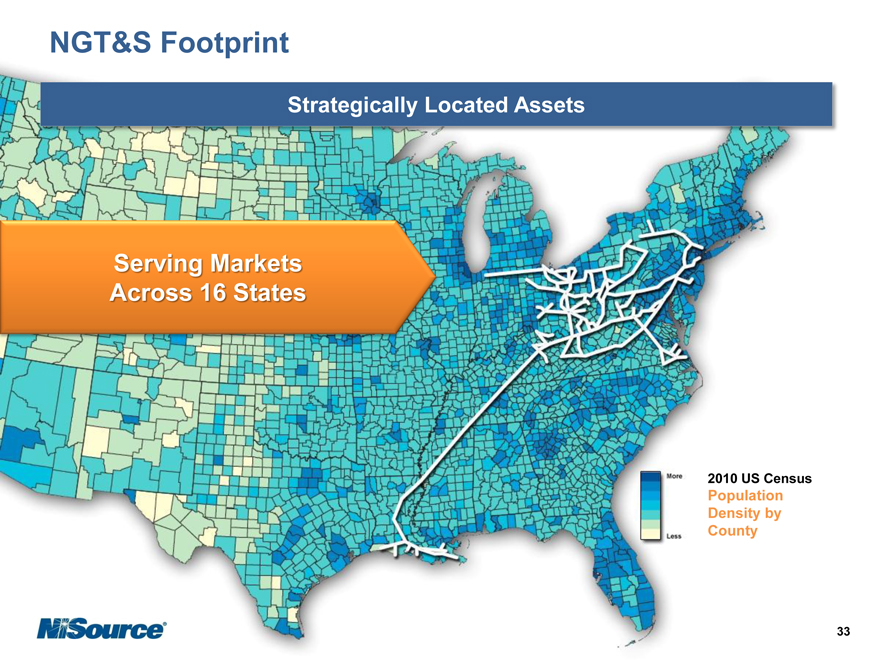

NGT&S Footprint

Strategically Located Assets

Serving Market Across 16 State

2010 US Census

Population Density by County

33

|

NGT&S

Positioned for Growth

Safety/ Reliability

Customer Experience

Stakeholder Relations

Customer Rates

Financial Performance

Solid Safety Results; Proactive Reliability Efforts Ongoing Engagement Focus, Satisfaction Gains Collaborative, Constructive Approach Highly Competitive, Fee-Based

Positioned for Ongoing, Robust Growth

34

|

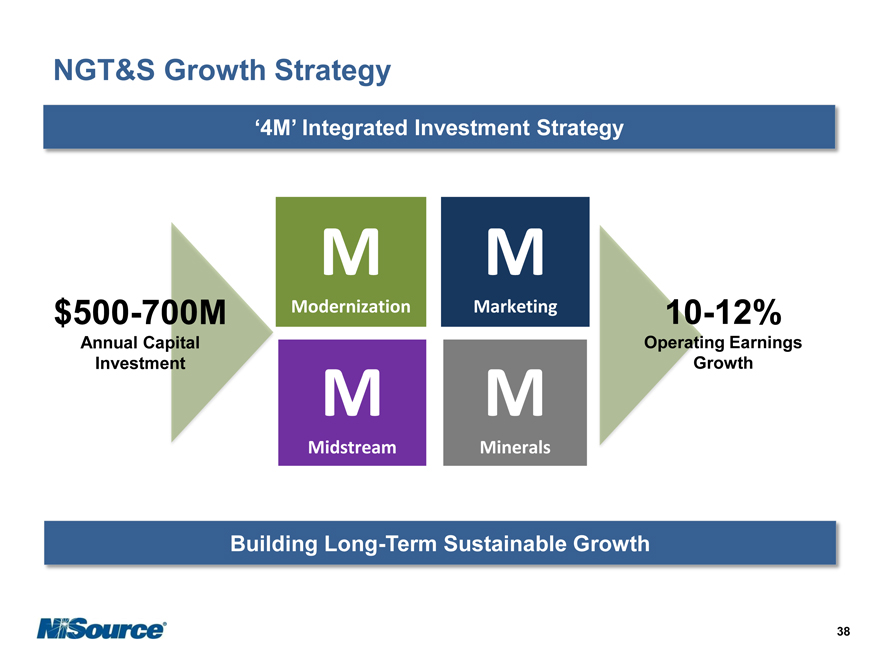

NGT&S Growth Strategy

‘4M’ Integrated Investment Strategy

Modernize Our Infrastructure

Reconfigure Our System for an Evolving Market Capture Emerging Midstream

Opportunities

Leverage Our Minerals Positions

Modernization

Marketing

Midstream

Minerals

Comprehensive, Balanced Portfolio

35

|

NGT&S Growth Strategy

Regulated Pipeline & Storage

Rebuilding Our System in

Partnership with our

Customers

Linking New Supplies to Markets

$7-9B Investment Over 10-15 Years

Modernization

Marketing

Midstream & Minerals

Leveraging Strategic Assets and Footprint Developing Fee-Based Gathering and Processing Opportunities

$1-1.5B Investment Over 5-10 Years

Midstream

Minerals

36

|

NGT&S Growth Strategy

Strengthening Our System Foundation

Linking New Supplies to Growing Markets

Providing Market Access for Shale Supplies

Leveraging Our Minerals Assets

$1-1.5B

Self-Funded

Investment

$3-4B

$4-5B

$ 10B Investment Inventory

37

|

NGT&S Growth Strategy

‘4M’ Integrated Investment Strategy

$500-700M

Annual Capital Investment

Modernization

Marketing

Midstream

Minerals

10-12%

Operating Earnings Growth

Building Long-Term Sustainable Growth

38

|

NGT&S Growth Strategy

Strengthening Our System Foundation

Modernization

Building Long-Term Sustainable Growth

39

|

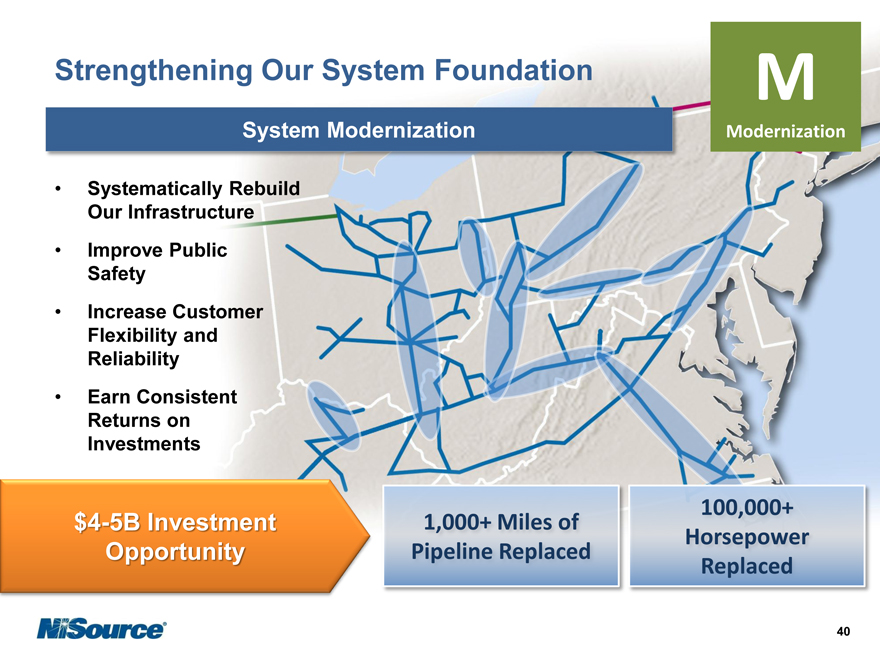

Strengthening Our System Foundation

System Modernization

Modernization

Systematically Rebuild Our Infrastructure Improve Public Safety Increase Customer Flexibility and Reliability Earn Consistent Returns on Investments

$ 5B Investment Opportunity

1,000+ Miles of Pipeline Replaced

100,000+ Horsepower Replaced

40

|

Strengthening Our System Foundation

Unprecedented Settlement

Collaboration: Near-Unanimous Settlement Annual Investment: $300M

Minimal Regulatory Lag: Annual ‘Tracker’

Recovery of Return, Taxes & Depreciation Initial Term: 5 Years, With Extension Provisions Cost to Achieve: Within Expectations Timeline: FERC Filing September 4; Anticipate Approval Late 2012

Partnering With Our Customers

41

|

NGT&S Growth Strategy

Linking New Supplies to Growing Markets

Marketing

Opportunistic, Disciplined Approach

42

|

Linking New Supplies to Growing Markets

Marketing Strategy

Enhance Market Liquidity Increase Supply Optionality Provide Market Access for Emerging Appalachian Supplies Access East Coast and Gulf LNG Export Markets

4B Investment Opportuni

Underpinned by Fee-Based Contracts

43

|

Linking New Supplies to Growing Markets

West Side Expansion

GOAL

Move Marcellus Supply to Growing Southeast Markets

INVESTMENT

CapEx: $200-250M 440 Mdt/d TCO Expansion 540 Mdt/d Gulf Expansion Line Looping at TCO

Re-Piping for Bi-Directional Flow on Gulf

CUSTOMERS

Antero Rice Petro Edge

Other Marcellus Producers

STATUS

FERC Filing: Spring 2013 In-Service: November 2014

Marketing

Shale Gas to the Southeast

44

|

Linking New Supplies to Growing Markets

East Side Expansion

GOAL

Provide Northern Marcellus Supplies to Northeast and Mid-Atlantic Markets

INVESTMENT

CapEx: $200-300M

220-300 Mdt/d TCO Expansion Pipeline Looping; Interconnects

CUSTOMERS

East Coast LDCs Gas-fired Generation Producers

Negotiating Precedent Agreements In-Service: September 2015

Competing in the Northeast and Mi Atlanti

45

|

Linking New Supplies to Growing Markets

Quick Link Expansion

GOAL

INVESTMENT

CUSTOMERS

STATUS

Deliver Utica Shale Supplies to Multiple Markets

CapEx: ~$300M

500 Mdt/d TCO Expansion Pipeline Looping, Extension

Various Utica Producers

In Development

In-Service Date: Q4 2015

Majorsville

Moving Utica Gas to market

46

|

Linking New Supplies to Growing Markets

LNG Export Opportunities

GOAL

Deliver Shale Gas to LNG Export Hubs

INVESTMENT

CapEx: $0.5-1.3B

1-2 MMdt/d TCO/Gulf Expansion TCO Pipeline Looping/Expansion; Additional Compression and Reconfiguration of Gulf System

CUSTOMERS

LNG Exporters

STATUS

Negotiating Agreements In-Service: 2016+

Cameron

Accessing Multiple LNG

Market

47

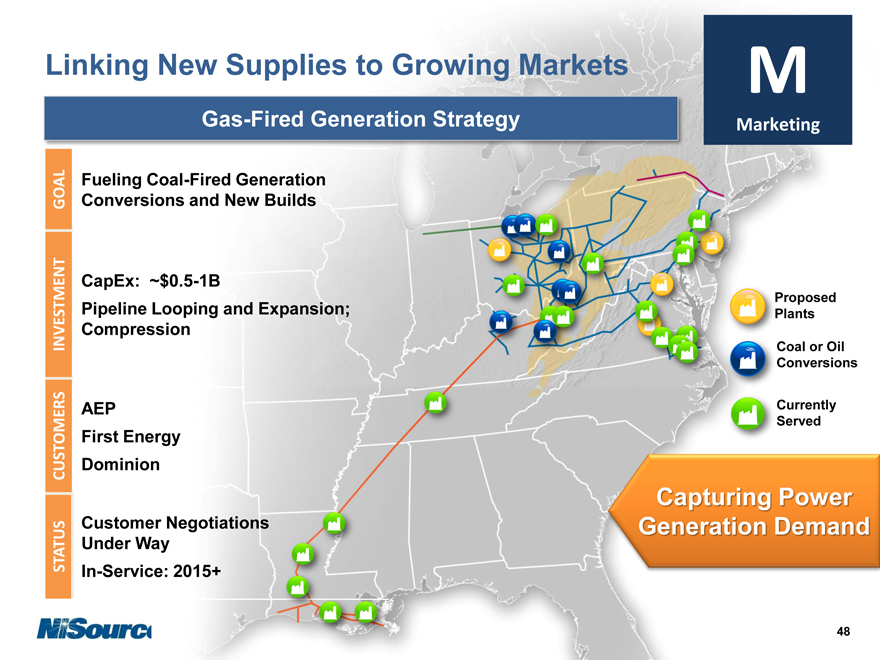

|

Cove Point

Linking New Supplies to Growing Markets

Gas-Fired Generation Strategy

GOAL

Fueling Coal-Fired Generation Conversions and New Builds

INVESTMENT

CapEx: ~$0.5-1B

Pipeline Looping and Expansion; Compression

CUSTOMERS

AEP

First Energy Dominion

STATUS

Customer Negotiations Under Way In-Service: 2015+

roposed lants

Coal or Oil Conversions

Currently Served

Capturing Power Generation Demand

48

|

Linking New Supplies to Growing Markets

Warren County Expansion

GOAL

Additional Capacity to Serve New 1,300MW Generating Facility

INVESTMENT

CapEx: ~$35M

~250 Mdt/d TCO Expansion

2.5 Mile Pipeline Extension; Interconnect Facilities

CUSTOMERS

Dominion

STATUS

FERC Certificate: February 2012 In-Service: April 2014

Fueling Virginia’s

Electric Needs

49

|

Linking New Supplies to Growing Markets

Millennium Pipeline

GOAL

Deliver Marcellus Shale Supplies to Multiple Markets

INVESTMENT

~$40M (NiSource’s Share)

Minisink Compressor: Expand Capacity by 120 MDt/d Hancock Compressor: Expand Capacity by 150 MDt/d

CUSTOMERS

Northeast PA Producers

STATUS

Minisink In-Service: Q1 2013 Hancock In-Service: Q4 2013

Hancock

Minisink

Moving North Marcellu Gas to Market

50

|

NGT&S Growth Strategy

Providing Market Access for Shale Supplies

Midstream

Attractive Investment; Fee-Based Structures

51

|

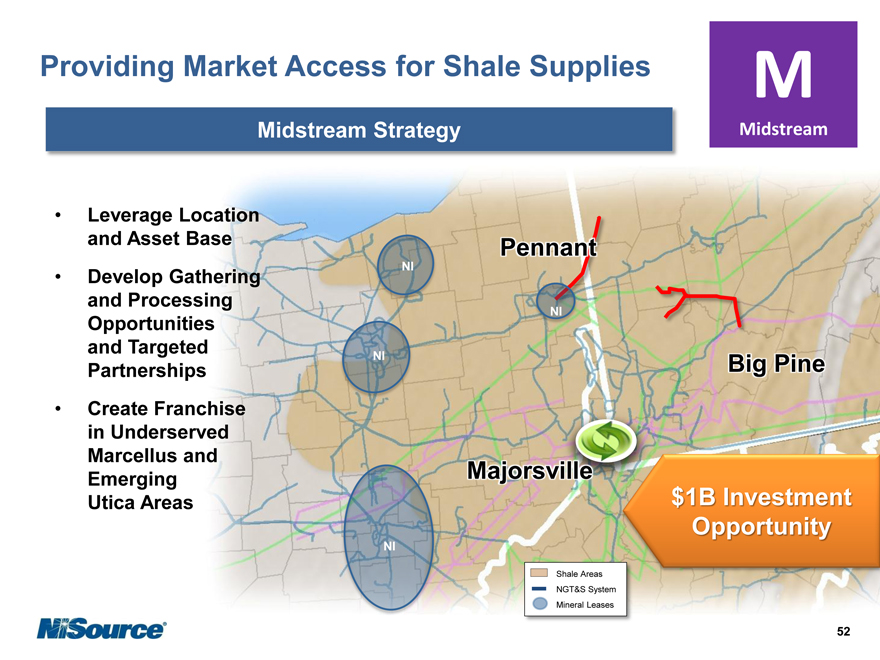

Providing Market Access for Shale Supplies

Midstream Strategy

Midstream

Leverage Location and Asset Base Develop Gathering and Processing Opportunities and Targeted Partnerships Create Franchise in Underserved Marcellus and Emerging Utica Areas

Pennant

Majorsville

Big Pine

$1B Investment Opportunity

Shale Areas NGT&S System Mineral Leases

52

|

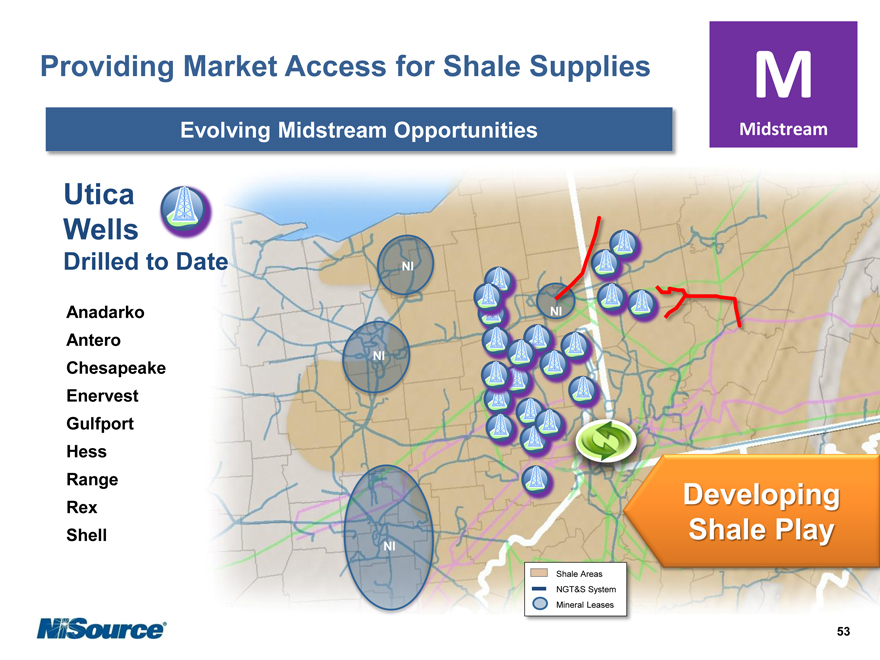

Providing Market Access for Shale Supplies

Evolving Midstream Opportunities

Utica Wells

Drilled to Date

Anadarko Antero Chesapeake Enervest Gulfport Hess Range Rex Shell

Shale Areas NGT&S System Mineral Leases

Developing Shale Play

53

|

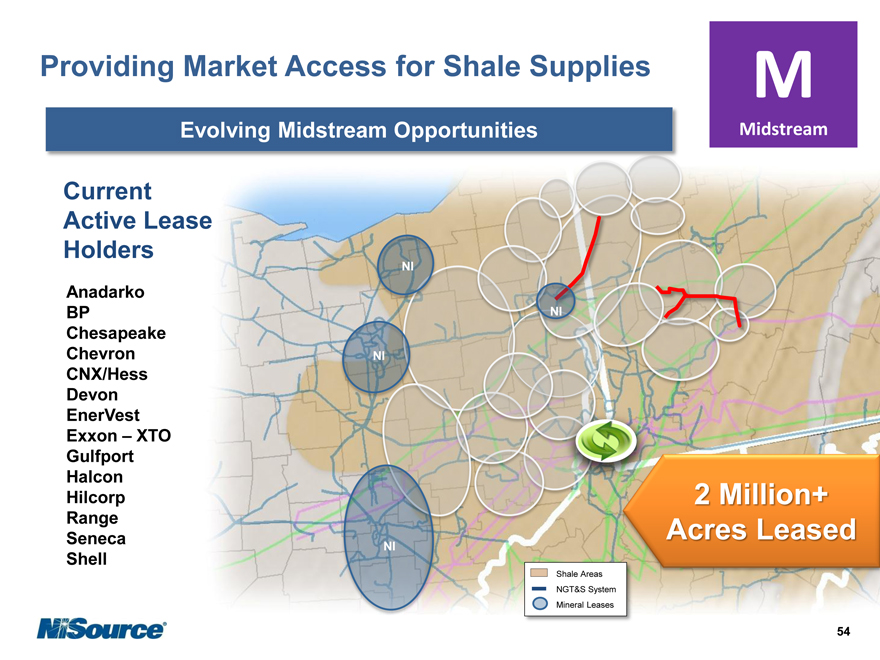

Providing Market Access for Shale Supplies

Evolving Midstream Opportunities

Current Active Lease Holders

Anadarko BP Chesapeake Chevron CNX/Hess Devon EnerVest Exxon – XTO Gulfport Halcon Hilcorp Range Seneca Shell

2 |

| Million+ Acres Leased |

Shale Areas NGT&S System Mineral Leases

54

|

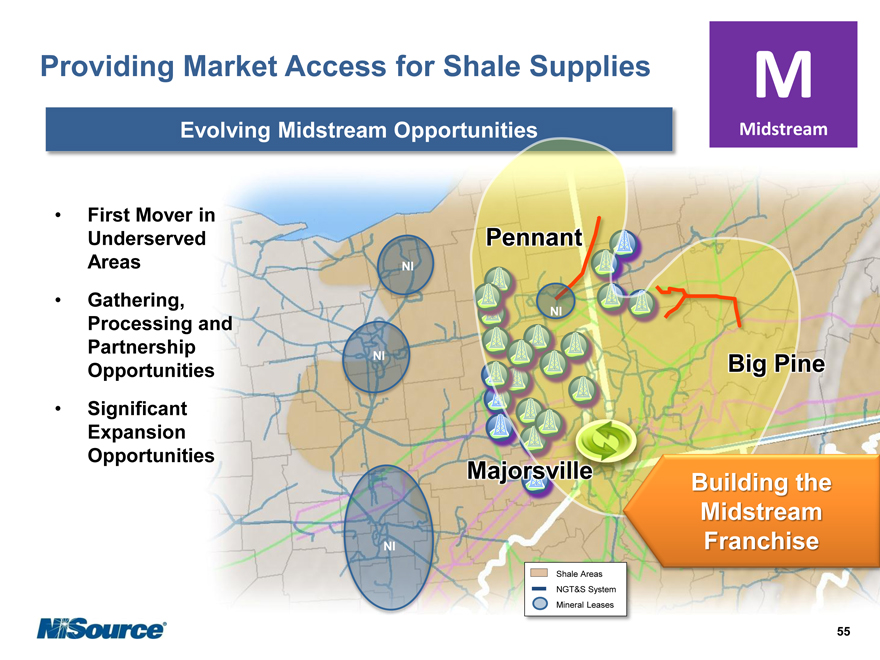

Providing Market Access for Shale Supplies

Evolving Midstream Opportunities

First Mover in Underserved Areas Gathering, Processing and Partnership Opportunities Significant Expansion Opportunities

Pennant

Big Pine

Majorsville

Building the Midstream Franchise

Shale Areas NGT&S System Mineral Leases

55

|

Providing Market Access for Shale Supplies

Majorsville Processing Complex Inlet/Outlet Pipelines

GOAL

Gather Wet Marcellus Gas to Processing Facility and Provide Downstream Pipeline Market Access

INVESTMENT

Repurposing Existing Pipeline; Adding New Interconnect $85M Gathering Extension

CUSTOMERS

Range CNX Chesapeake Chevron

STATUS

In Service: September 2010

ille

Repurposing Existing Asset

Shale Area NGT&S System

56

|

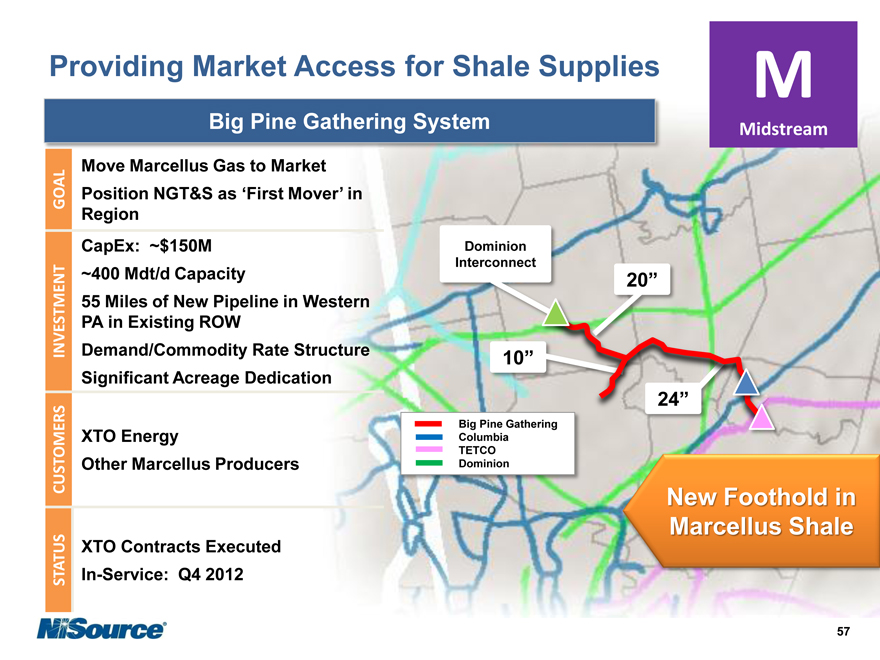

Providing Market Access for Shale Supplies

Big Pine Gathering System

GOAL

Move Marcellus Gas to Market

Position NGT&S as ‘First Mover’ in

Region

INVESTMENT

CapEx: ~$150M ~400 Mdt/d Capacity

55 Miles of New Pipeline in Western PA in Existing ROW

Demand/Commodity Rate Structure Significant Acreage Dedication

Dominion Interconnect

CUSTOMERS

XTO Energy

Other Marcellus Producers

STATUS

XTO Contracts Executed In-Service: Q4 2012

20”

10”

Big Pine Gathe Columbia TETCO

Dominion

New Foothold in Marcellus Shal

57

|

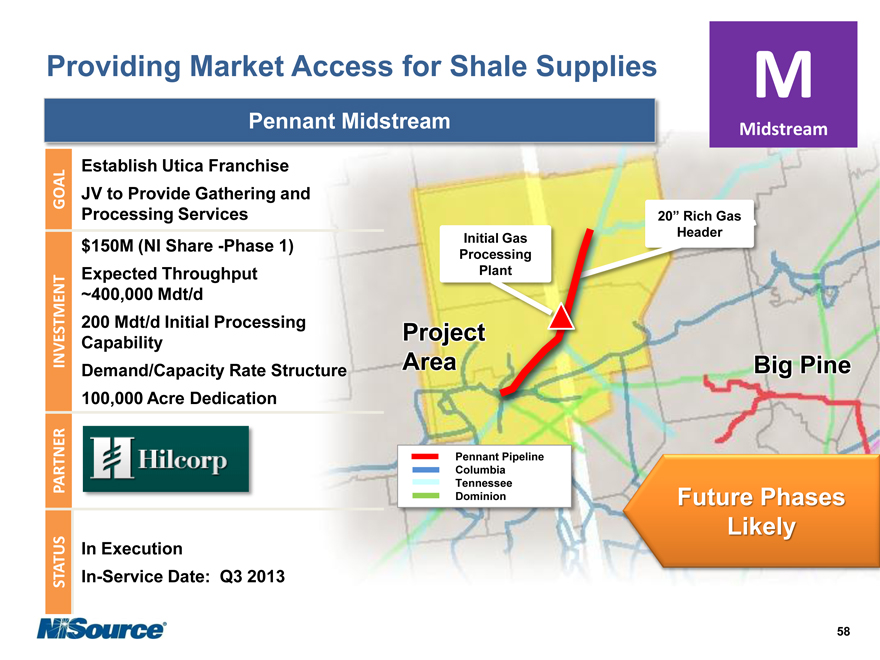

Providing Market Access for Shale Supplies

Pennant Midstream

GOAL

Establish Utica Franchise JV to Provide Gathering and Processing Services

INVESTMENT

$150M (NI Share -Phase 1) Expected Throughput ~400,000 Mdt/d 200 Mdt/d Initial Processing Capability Demand/Capacity Rate Structure 100,000 Acre Dedication

PARTNER

STATUS

In Execution

In-Service Date: Q3 2013

Initial Process

Project Area

20” Rich Gas

Header

Big Pine

Pennant Pipeline Columbia Tennessee Dominion

Future Phases Likel

58

|

NGT&S Growth Strategy

Leveraging Our Mineral Assets

Minerals

Supports, Complements Midstream Strategy

59

|

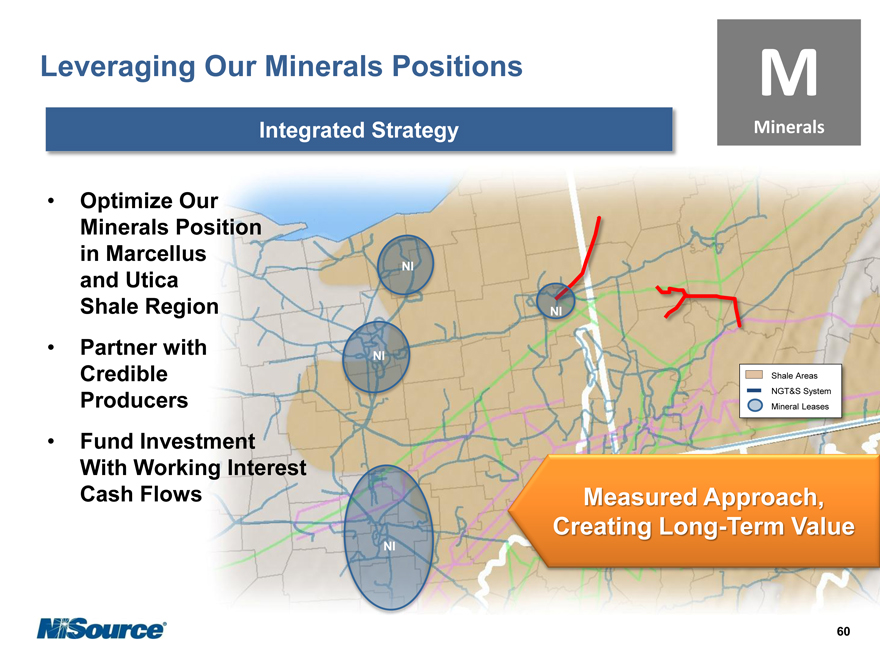

Leveraging Our Minerals Positions

Integrated Strategy

Optimize Our Minerals Position in Marcellus and Utica Shale Region Partner with Credible Producers Fund Investment With Working Interest Cash Flows

Shale Areas NGT&S System Mineral Leases

Measured Approach, Creating Long Term Value

60

|

Leveraging Our Minerals Positions

Hilcorp Upstream Agreement

GOAL

Jointly Develop and Extract Value of ~100k Acres of Mineral Rights

INVESTMENT

Market-Based Cash Payment

• Consistent with market values

(e.g. Recent Halcon/NCL transaction)

• 50% ‘cash’; 50% ‘carry’

Working Interest of 5% Across AMI Overriding Royalty Interest of 0.7% Acreage Dedicated to Pennant

PARTNER

STATUS

Under Development

Strong Partnership, Creating Long Term Value

61

|

Leveraging Our Minerals Positions

Significant Potential Minerals Opportunities

Expect Utica to Develop East to West Small Number of Wells Drilled to Date Area Continues to Evolve Continue to Monitor Devon and Anadarko Increased Drilling Expected Over Next Several Years

Majorsville

Shale Areas NGT&S System Mineral Leases

Measured Approach, Long Term Value Focus

62

|

NGT&S Growth Strategy

Strengthening Our System Foundation

Linking New Supplies to Growing Markets

Providing Market Access for Shale Supplies

Leveraging Our Minerals Assets

$1-1.5B

Self-Funded

Investment

$4-5B

$3-4B

$ 10B Investment Inventory

63

|

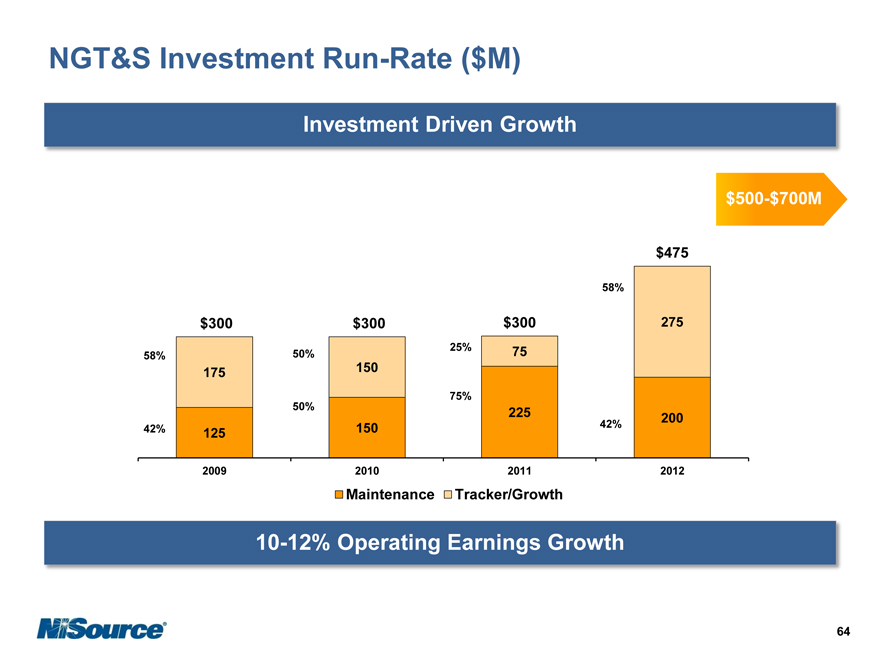

NGT&S Investment Run-Rate ($M)

Investment Driven Growth

$500-$700M

$475

58%

$300 $300 $300 275

25% 75 58% 50%

175 150

75%

50% 225 200

42% 150 42%

125

2009 2010 2011 2012

Maintenance Tracker/Growth

10-12% Operating Earnings Growth

64

|

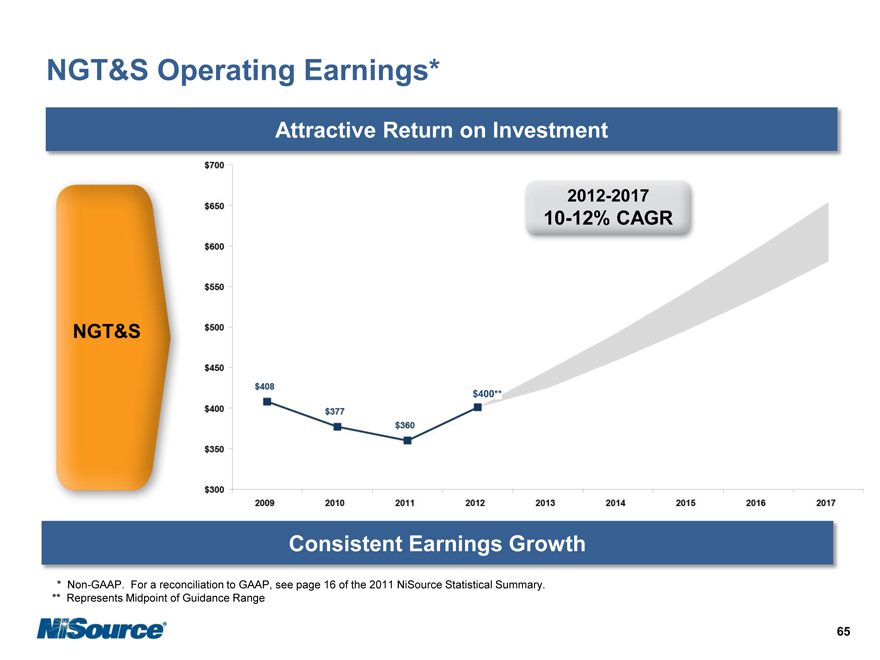

NGT&S Operating Earnings*

Attractive Return on Investment

2012-2017

10-12% CAGR

NGT&S

Consistent Earnings Growth

* |

| Non-GAAP. For a reconciliation to GAAP, see page 16 of the 2011 NiSource Statistical Summary. |

** Represents Midpoint of Guidance Range

65

|

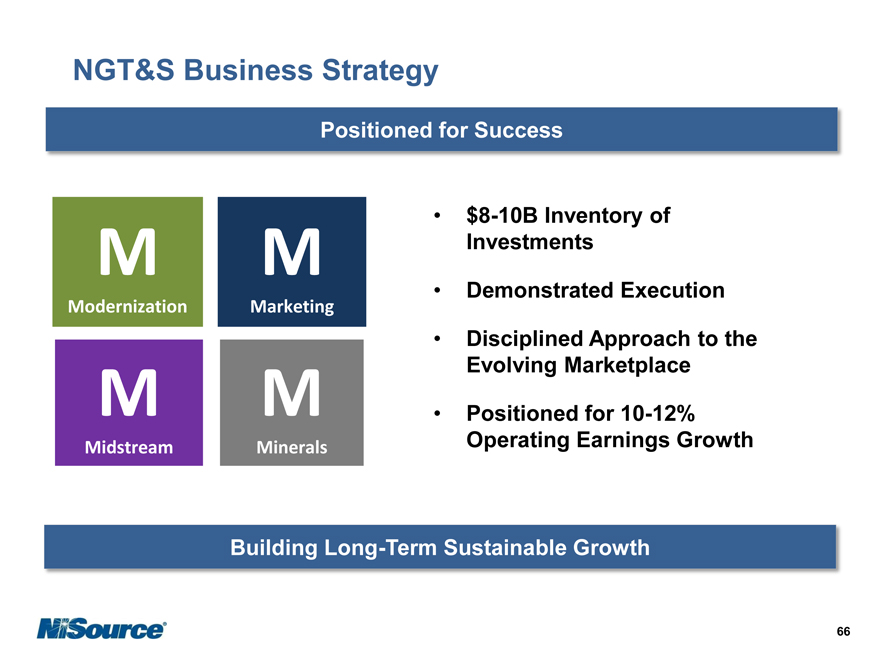

NGT&S Business Strategy

Positioned for Success

Modernization

Marketing

Midstream

Minerals

$8-10B Inventory of Investments

Demonstrated Execution

Disciplined Approach to the Evolving Marketplace

Positioned for 10-12% Operating Earnings Growth

Building Long-Term Sustainable Growth

66

|

Appendix

67

|

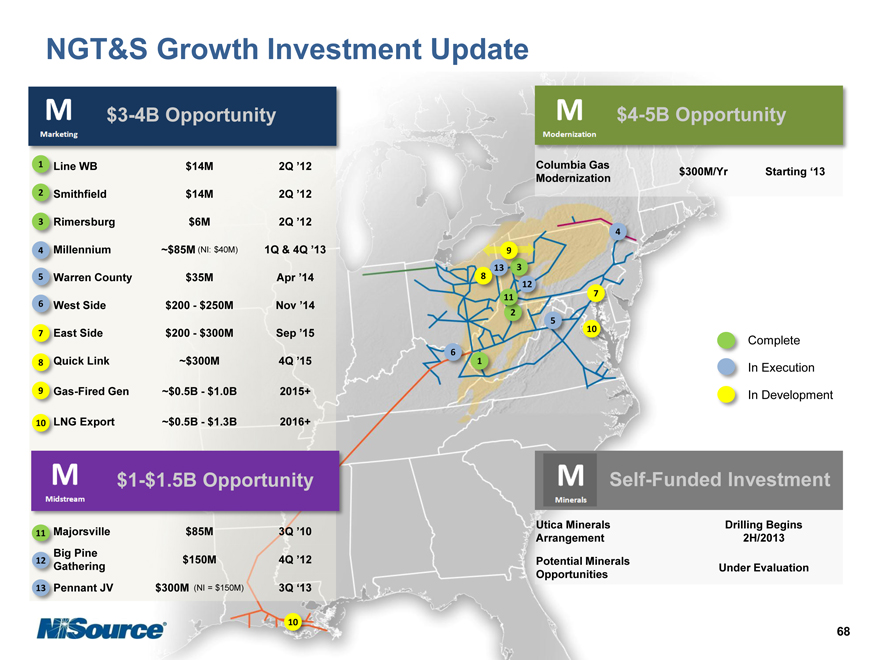

NGT&S Growth Investment Update

$3-4B Opportunity

1 |

| line WB $14M 2Q ‘12 |

2 |

| Smithfield $14M 2Q ‘12 |

3 |

| Rimersburg $6M 2Q ‘12 |

4 |

| millennium ~$85M (NI: $40M) 1Q & 4Q ‘13 |

5 |

| Warren County $35M Apr ‘14 |

6 |

| West Side $200—$250M Nov ‘14 |

7 |

| East Side $200—$300M Sep ‘15 |

8 |

| quick Link ~$300M 4Q ‘15 |

9 as-Fired Gen ~$0.5B—$1.0B 2015+

10 LNG Export ~$0.5B—$1.3B 2016+

$1-$1.5B Opportunity

$4-5B Opportunity

Columbia Gas

Modernization $300M/Yr Starting ‘13

Complete In Execution In Development

Utica Minerals Arrangement

Potential Minerals Opportunities

Drilling Begins 2H/2013

Under Evaluation

Self-Funded Investment

68

|

Financial Profile

Steve Smith

Executive Vice President & CFO September 12, 2012

|

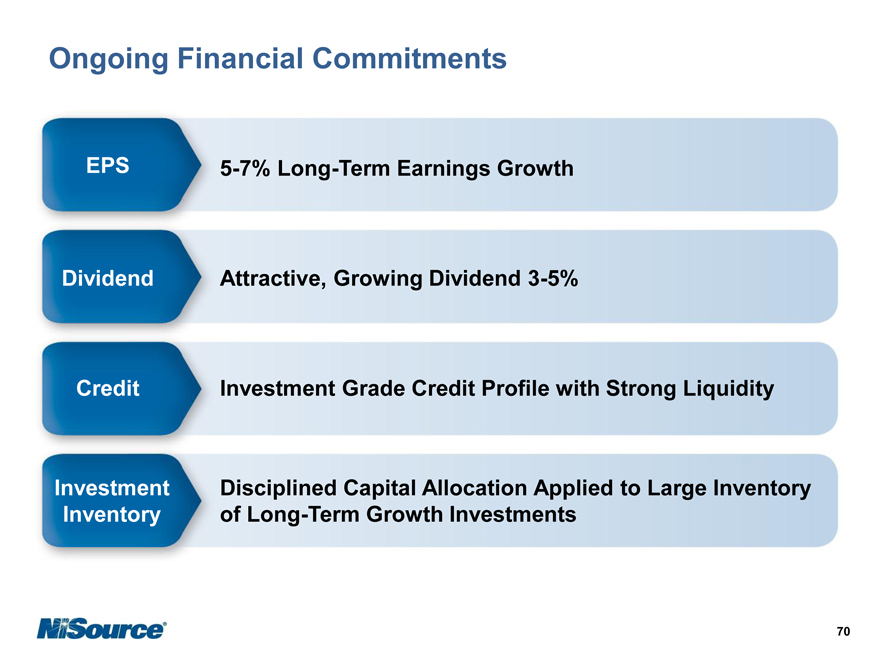

Ongoing Financial Commitments

EPS

Dividend

Credit

Investment

Inventory

5-7% Long-Term Earnings Growth

Attractive, Growing Dividend 3-5%

Investment Grade Credit Profile with Strong Liquidity

Disciplined Capital Allocation Applied to Large Inventory of Long-Term Growth Investments

70

|

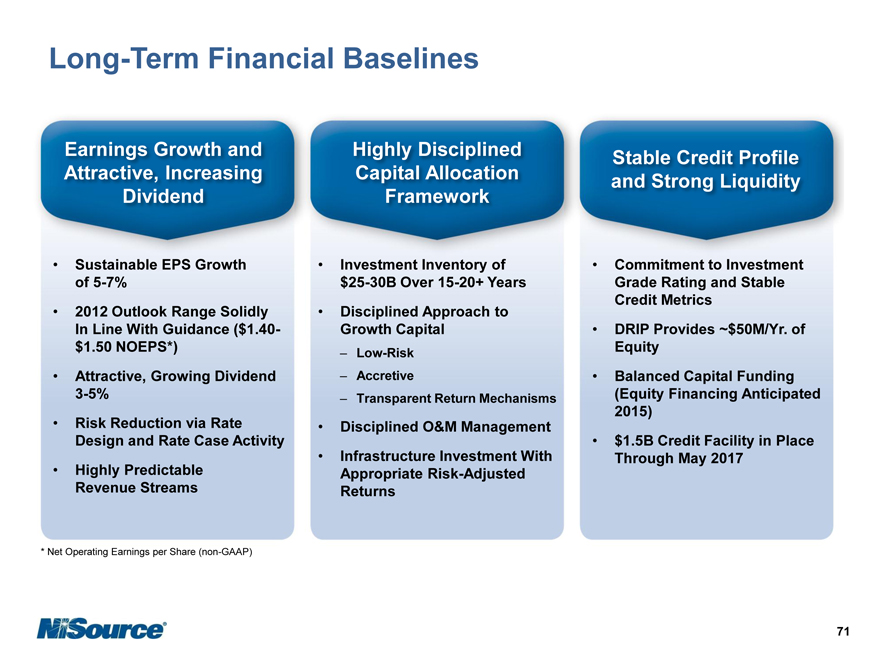

Long-Term Financial Baselines

Earnings Growth and Attractive, Increasing Dividend

Highly Disciplined Capital Allocation Framework

Stable Credit Profile and Strong Liquidity

Sustainable EPS Growth of 5-7%

2012 Outlook Range Solidly In Line With Guidance ($1.40-

$1.50 NOEPS*)

Attractive, Growing Dividend

3-5%

Risk Reduction via Rate Design and Rate Case Activity

Highly Predictable Revenue Streams

Investment Inventory of

$25-30B Over 15-20+ Years

Disciplined Approach to Growth Capital

– Low-Risk

– Accretive

– Transparent Return Mechanisms

Disciplined O&M Management

Infrastructure Investment With Appropriate Risk-Adjusted Returns

Commitment to Investment Grade Rating and Stable Credit Metrics

DRIP Provides ~$50M/Yr. of Equity

Balanced Capital Funding (Equity Financing Anticipated 2015)

$1.5B Credit Facility in Place Through May 2017

* |

| Net Operating Earnings per Share (non-GAAP) |

71

|

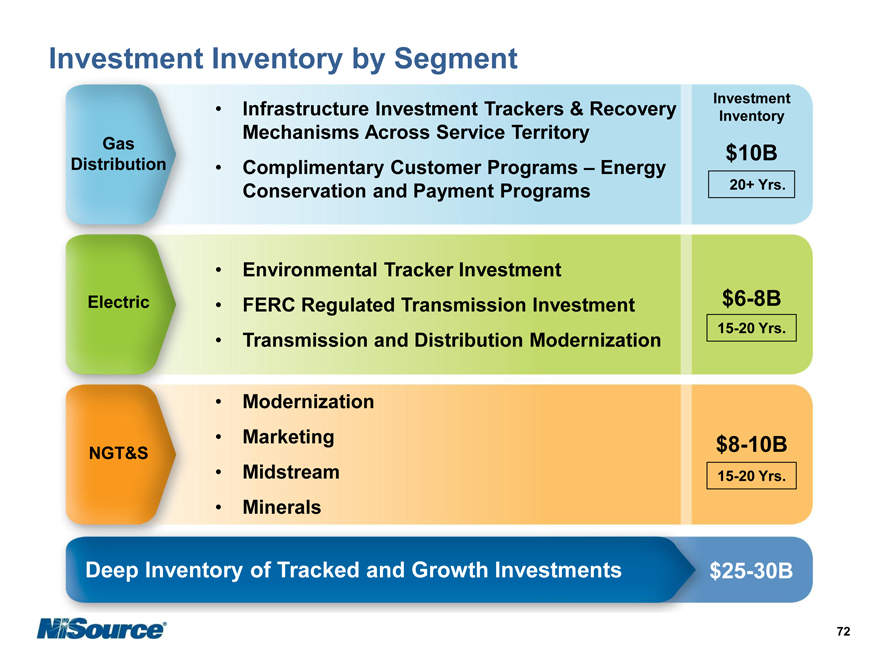

Investment Inventory by Segment

Gas Distribution

Infrastructure Investment Trackers & Recovery Mechanisms Across Service Territory Complimentary Customer Programs – Energy Conservation and Payment Programs

Investment Inventory

$10B

20+ Yrs.

Electric

Environmental Tracker Investment

FERC Regulated Transmission Investment Transmission and Distribution Modernization

$6-8B

15-20 Yrs.

NGT&S

Modernization Marketing Midstream Minerals

$8-10B

15-20 Yrs.

Deep Inventory of Tracked and Growth Investments

$25-30B

72

|

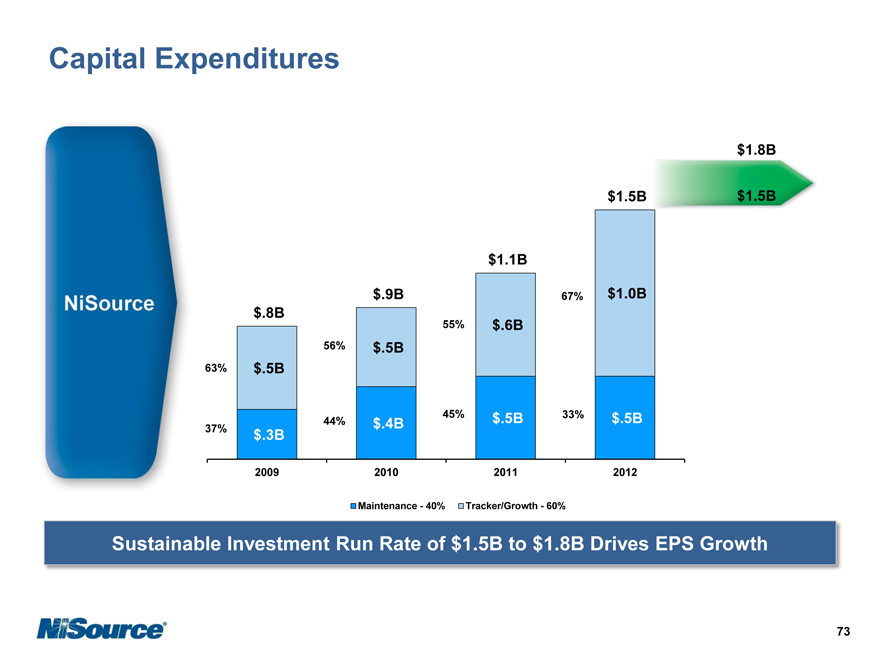

Capital Expenditures

$1.8B

$1.5B

$1.5B

$1.1B

$.9B 67% $1.0B $.8B

55% $.6B 56% $.5B

63% $.5B

45% $.5B 33% $.5B 44% $.4B

37% $.3B

2009 2010 2011 2012

Maintenance—40% Tracker/Growth—60%

Sustainable Investment Run Rate of $1.5B to $1.8B Drives EPS Growth

73

|

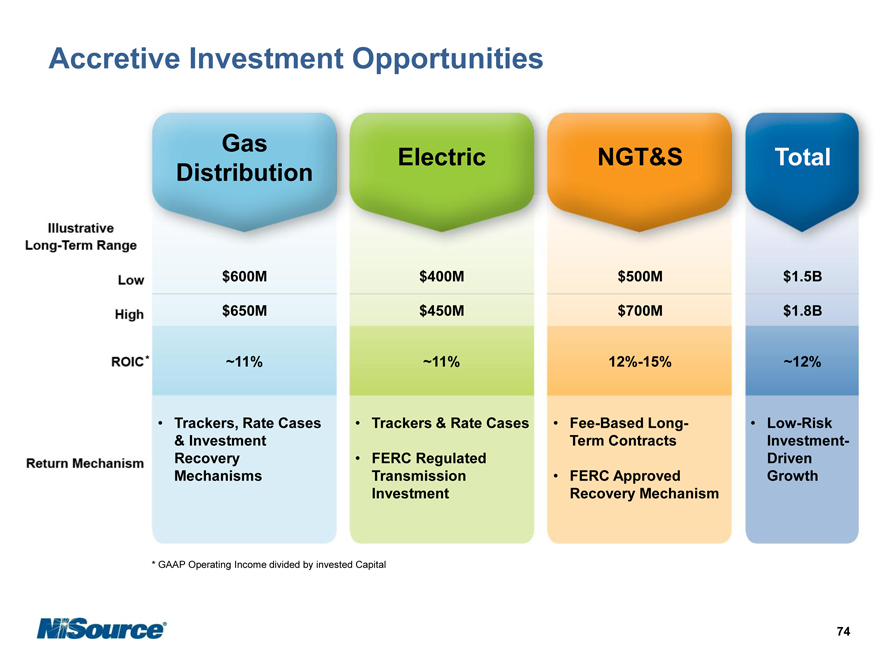

Accretive Investment Opportunities

Gas Distribution

Electric

NGT&S

Total

$600M

$650M

~11%

Trackers, Rate Cases

& Investment Recovery Mechanisms

$400M

$450M

~11%

Trackers & Rate Cases

FERC Regulated Transmission Investment

$500M

$700M

12%-15%

Fee-Based Long-Term Contracts

FERC Approved Recovery Mechanism

$1.5B

$1.8B

~12%

Low-Risk Investment-Driven Growth

* |

| GAAP Operating Income divided by invested Capital |

74

|

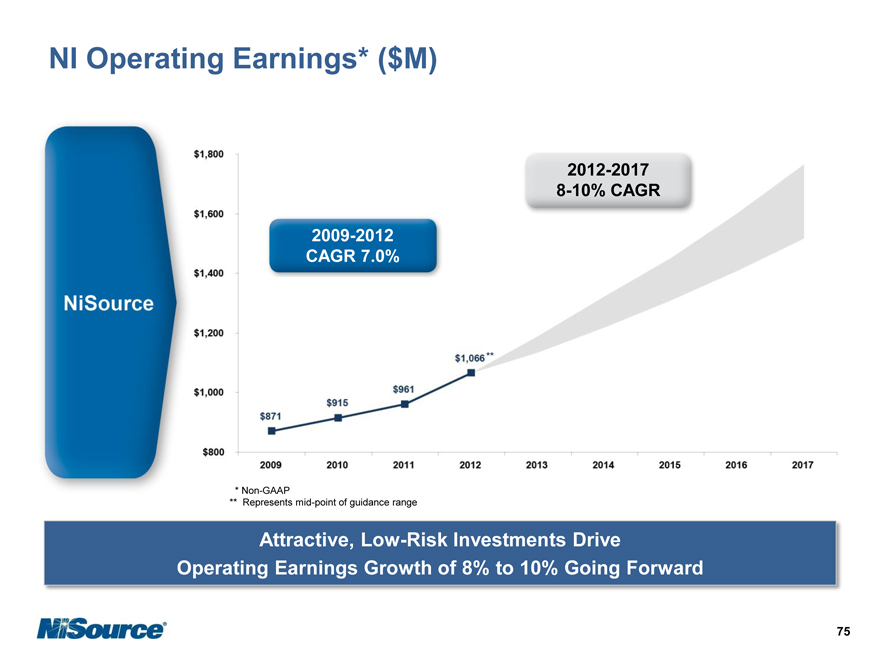

NI Operating Earnings* ($M)

2012-2017

8-10% CAGR

2009-2012 CAGR 7.0%

* |

| Non-GAAP |

** Represents mid-point of guidance range

Attractive, Low-Risk Investments Drive

Operating Earnings Growth of 8% to 10% Going Forward

75

|

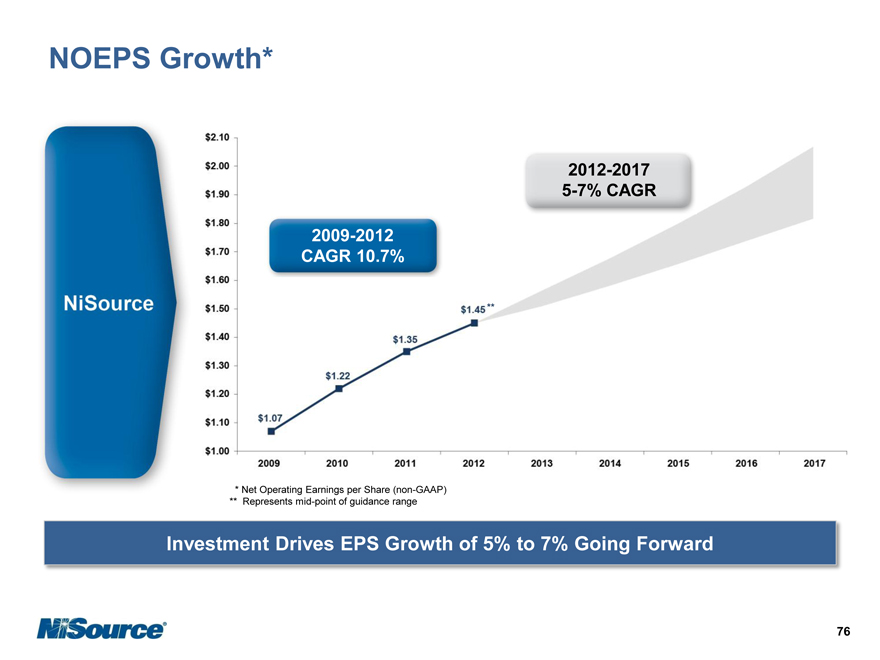

NOEPS Growth*

2009-2012

CAGR 10.7%

2012-2017

5-7% CAGR

* |

| Net Operating Earnings per Share (non-GAAP) |

** Represents mid-point of guidance range

Investment Drives EPS Growth of 5% to 7% Going Forward

76

|

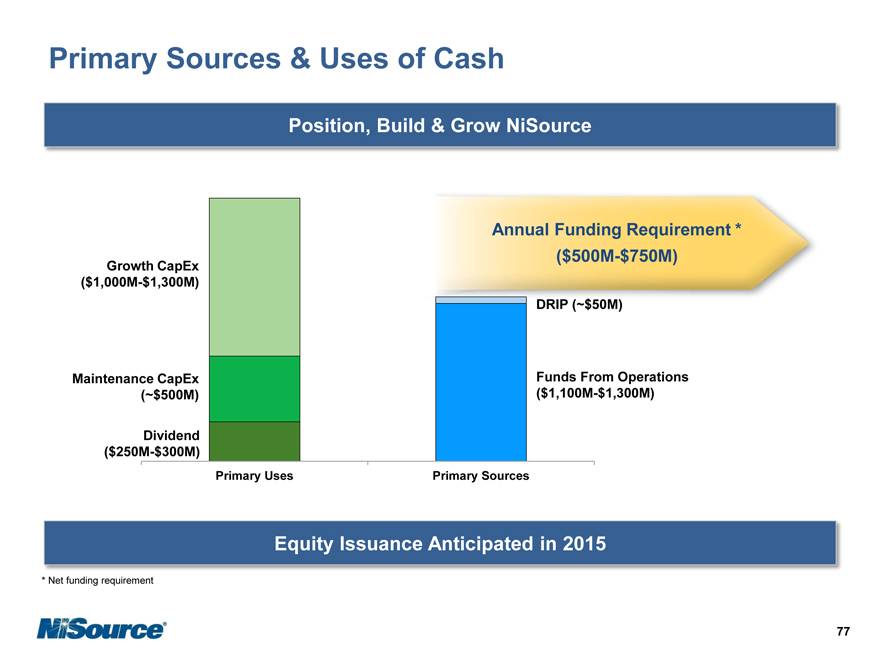

Primary Sources & Uses of Cash

Position, Build & Grow NiSource

Growth CapEx

($1,000M-$1,300M)

Maintenance CapEx

(~$500M)

Dividend

($250M-$300M)

Primary Uses

Primary Sources

Annual Funding Requirement *

($500M-$750M)

DRIP (~$50M)

Funds From Operations

($1,100M-$1,300M)

Equity Issuance Anticipated in 2015

* |

| Net funding requirement |

77

|

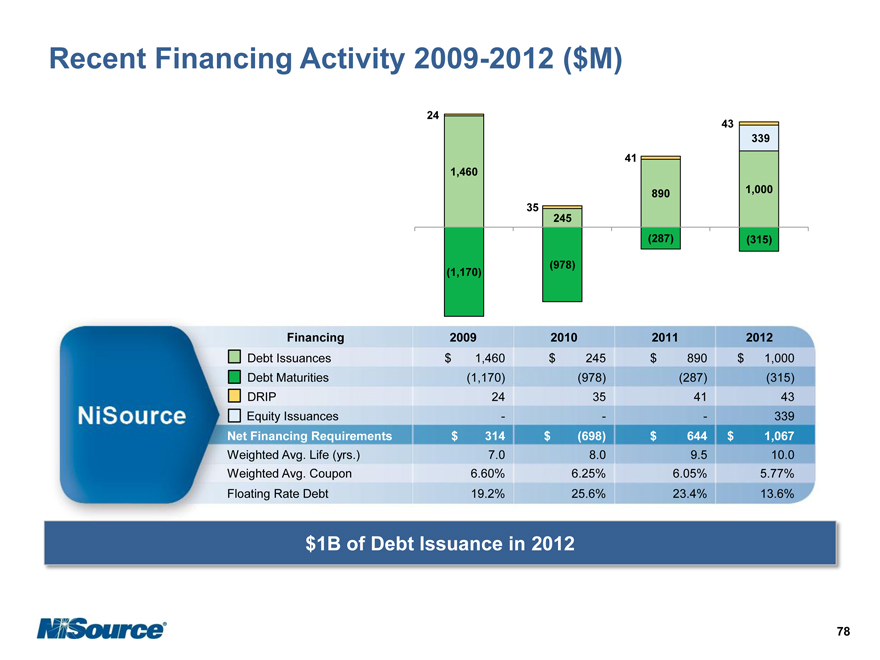

Recent Financing Activity 2009-2012 ($M)

24

43 339 41 1,460 890 1,000 35 245 (287) (315)

(978) (1,170)

Financing 2009 2010 2011 2012

Debt Issuances $ 1,460 $ 245 $ 890 $ 1,000

Debt Maturities (1,170) (978) (287) (315)

DRIP 24 35 41 43

Equity Issuances ——— 339

Net Financing Requirements $ 314 $ (698) $ 644 $ 1,067

Weighted Avg. Life (yrs.) 7.0 8.0 9.5 10.0

Weighted Avg. Coupon 6.60% 6.25% 6.05% 5.77%

Floating Rate Debt 19.2% 25.6% 23.4% 13.6%

$1B of Debt Issuance in 2012

78

|

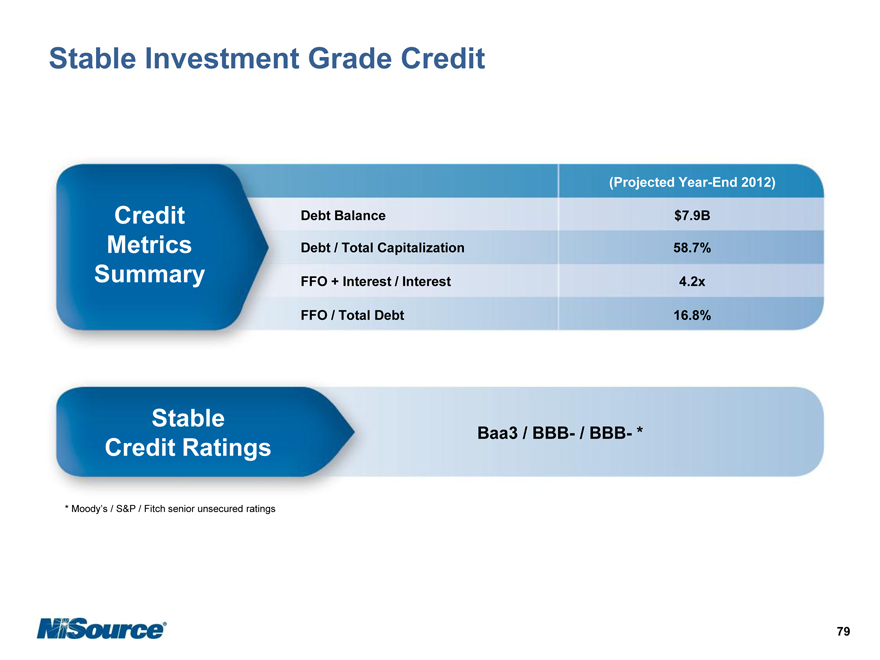

Stable Investment Grade Credit

Credit Metrics Summary

(Projected Year-End 2012)

Debt Balance $7.9B

Debt / Total Capitalization 58.7%

FFO + Interest / Interest 4.2x

FFO / Total Debt 16.8%

Stable Credit Ratings

Baa3 / BBB- / BBB- *

* |

| Moody’s / S&P / Fitch senior unsecured ratings |

79

|

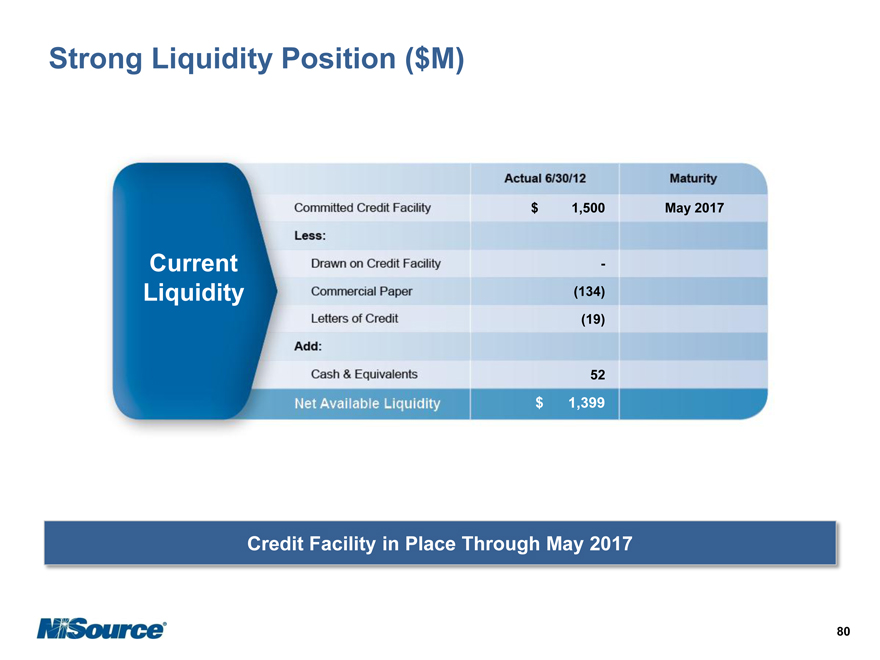

Strong Liquidity Position ($M)

Current Liquidity

$ 1,500 May 2017

-

(134)

(19) |

|

52

$ 1,399

Credit Facility in Place Through May 2017

80

|

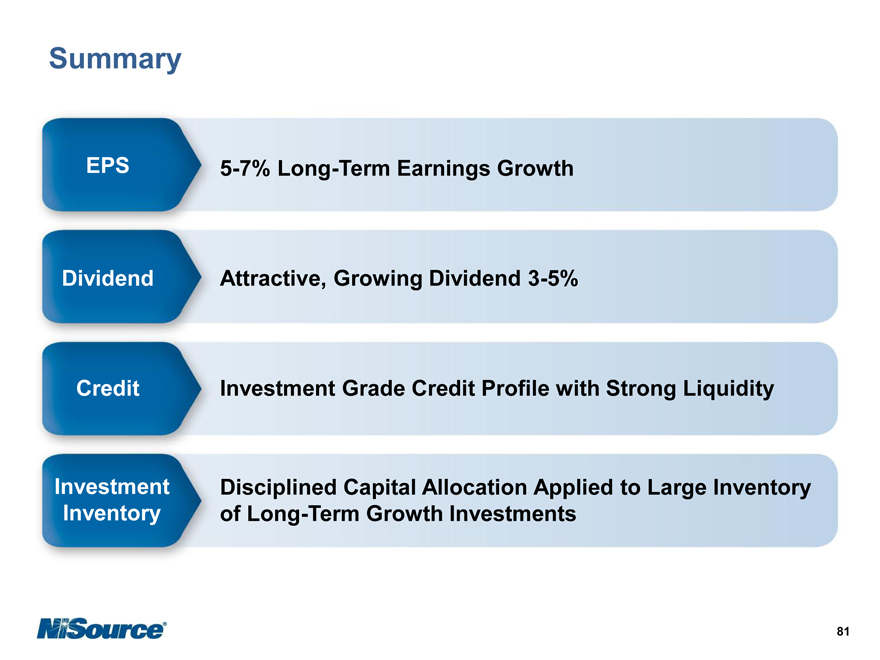

Summary

EPS

Dividend

Credit

Investment Inventory

5-7% Long-Term Earnings Growth Attractive, Growing Dividend 3-5%

Investment Grade Credit Profile with Strong Liquidity

Disciplined Capital Allocation Applied to Large Inventory of Long-Term Growth Investments

81

|

Appendix

82

|

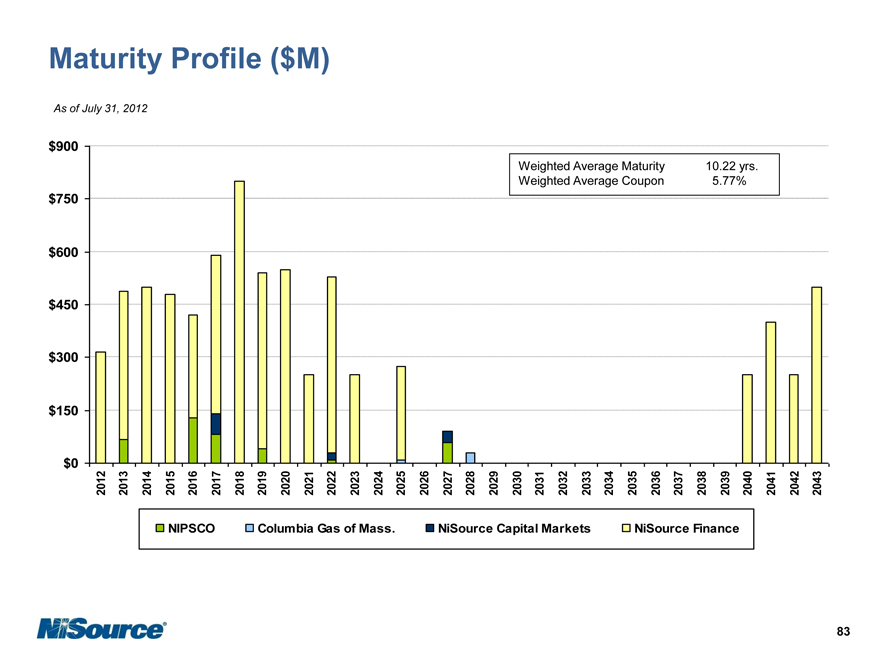

Maturity Profile ($M)

As of July 31, 2012

$900

$750

$600 $450 $300

$150

$0

Weighted Average Maturity 10.22 yrs.

Weighted Average Coupon 5.77%

2012 2013

2014

2015 2016

2017

2018 2019

2020

2021 2022

2023

2024 2025

2026

2027 2028

2029

2030 2031

2032

2033 2034

2035

2036 2037

2038

2039 2040

2041

2042 2043

NIPSCO Columbia Gas of Mass. NiSource Capital Markets NiSource Finance

83