Exhibit 99.2

|

Exhibit 99.2

Creating Two Premier Energy Infrastructure Companies

NiSource Inc. Investor Day

Millennium Broadway

New York, NY | 09.29.14

|

Forward Looking Statements

This presentation contains forward-looking statements within the meaning of federal securities laws. These forward-looking statements are subject to various risks and uncertainties. Examples of forward-looking statements in this presentation include statements and expectations regarding future dividends, operating earnings growth, EBITDA growth, earnings per share growth, capital investments, net investment/rate base growth, financing needs and plans, and investment opportunities. Factors that could cause actual results to differ materially from the projections, forecasts, estimates and expectations discussed in these presentations include, among other things, the timing to consummate the transactions described herein; the risk that a condition to consummation is not satisfied; disruption to operations as a result of the proposed transactions; the inability of one or more of the businesses to operate independently following the completion of the proposed transactions; weather; fluctuations in supply and demand for energy commodities; growth opportunities for NiSource’s businesses; increased competition in deregulated energy markets; the success of regulatory and commercial initiatives; dealings with third parties over whom NiSource has no control; actual operating experience of NiSource’s assets; the regulatory process; regulatory and legislative changes; changes in general economic, capital and commodity market conditions; and counter-party credit risk, and the matters described in the “Risk Factors” section of the Form S-1 filed by Columbia Pipeline Partners LP and the matters described in the “Risk Factors” section in NiSource’s 2013 Form 10-K, and subsequent NiSource filings on Form 10-Q, many of which are beyond the control of NiSource. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of this presentation. Future earnings and other financial projections are illustrative only and do not constitute guidance by the Company. NiSource expressly disclaims a duty to update any of the forward-looking statements contained in these presentations.

The potential distribution of CPG shares is subject to the satisfaction of a number of conditions, including the final approval of NiSource’s Board of Directors. There is no assurance that such distribution will in fact occur.

2

|

Speaker Bios

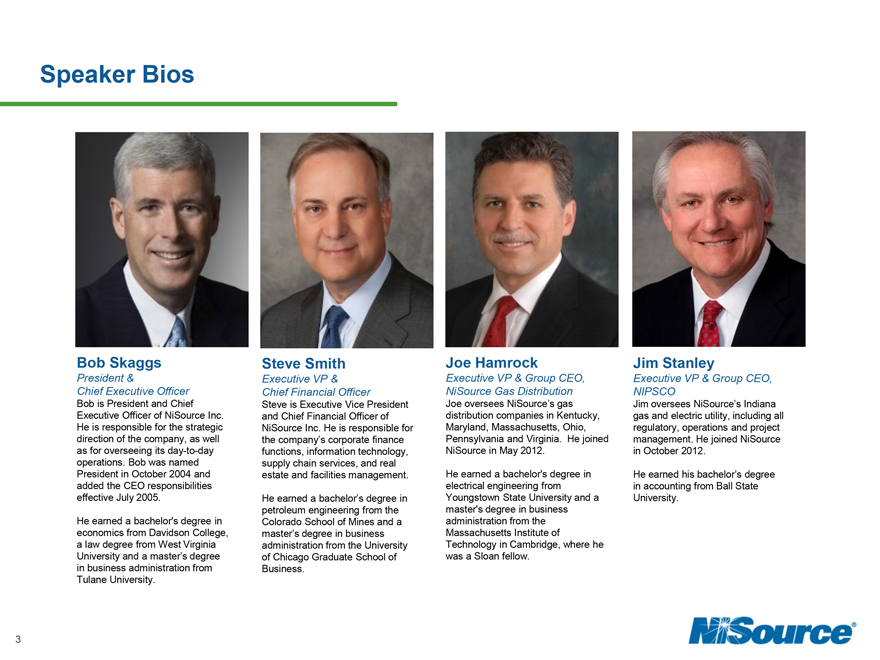

Bob Skaggs

President &

Chief Executive Officer

Bob is President and Chief Executive Officer of NiSource Inc. He is responsible for the strategic direction of the company, as well as for overseeing its day-to-day operations. Bob was named President in October 2004 and added the CEO responsibilities effective July 2005.

He earned a bachelor’s degree in economics from Davidson College, a law degree from West Virginia University and a master’s degree in business administration from Tulane University.

Steve Smith

Executive VP & Chief Financial Officer

Steve is Executive Vice President and Chief Financial Officer of NiSource Inc. He is responsible for the company’s corporate finance functions, information technology, supply chain services, and real estate and facilities management.

He earned a bachelor’s degree in petroleum engineering from the Colorado School of Mines and a master’s degree in business administration from the University of Chicago Graduate School of Business.

Joe Hamrock

Executive VP & Group CEO, NiSource Gas Distribution

Joe oversees NiSource’s gas distribution companies in Kentucky, Maryland, Massachusetts, Ohio, Pennsylvania and Virginia. He joined NiSource in May 2012.

He earned a bachelor’s degree in electrical engineering from Youngstown State University and a master’s degree in business administration from the Massachusetts Institute of Technology in Cambridge, where he was a Sloan fellow.

Jim Stanley

Executive VP & Group CEO, NIPSCO

Jim oversees NiSource’s Indiana gas and electric utility, including all regulatory, operations and project management. He joined NiSource in October 2012.

He earned his bachelor’s degree in accounting from Ball State University.

3

|

Speaker Bios

Glen Kettering

Executive VP & Group CEO, Columbia Pipeline Group

Glen oversees all regulatory, commercial, operations and capital investment programs at Columbia Pipeline Group.

He earned a bachelor’s degree in business administration from West Virginia University and a law degree from the West Virginia University College of Law

Stan Chapman III

Chief Commercial Officer, Columbia Pipeline Group

Stan is responsible for all of Columbia Pipeline Group’s regulated commercial operations, which includes marketing, business development, gas control, customer service, rates and regulatory affairs.

He earned a bachelor’s degree in economics from Texas A&M University and a master’s degree in business administration from the University of St. Thomas.

Brett Stovern

Chief Operating Officer, Midstream Services

Brett is responsible for all Columbia Pipeline Group’s midstream and minerals activities. Prior to his role, he served as Chief Financial Officer for Columbia Pipeline Group.

He earned his bachelor’s degree in accounting from California State Polytechnic University and is a Certified Public Accountant.

Shawn Patterson

President, Operations & Project Delivery, Columbia Pipeline Group

Shawn is responsible for operations, engineering and project management across Columbia Pipeline Group. He also oversees the execution of CPG’s modernization and growth programs.

He earned a bachelor’s degree in civil engineering from Rose-Hulman Institute of Technology and a master’s degree in business administration from University of Notre Dame.

4

|

Today’s Agenda

NiSource Investor Day 2014

8:00 – 8:30 AM 8:30 – 9:30 AM 9:30 – 9:45 AM 9:45 – 10:30 AM 10:30 – 11:30 AM

11:30 AM – 12:00 PM

12:00 – 12:30 PM

12:30 – 12:35 PM

Registration and Welcome Separation Overview Break NiSource Utility Company Columbia Pipeline Group Financial Profile Q&A

Closing Remarks

Bob Skaggs, Steve Smith

Jim Stanley, Joe Hamrock Glen Kettering, CPG Leadership Steve Smith Team Bob Skaggs

5

|

Separation Overview

Bob Skaggs

President & Chief Executive Officer

|

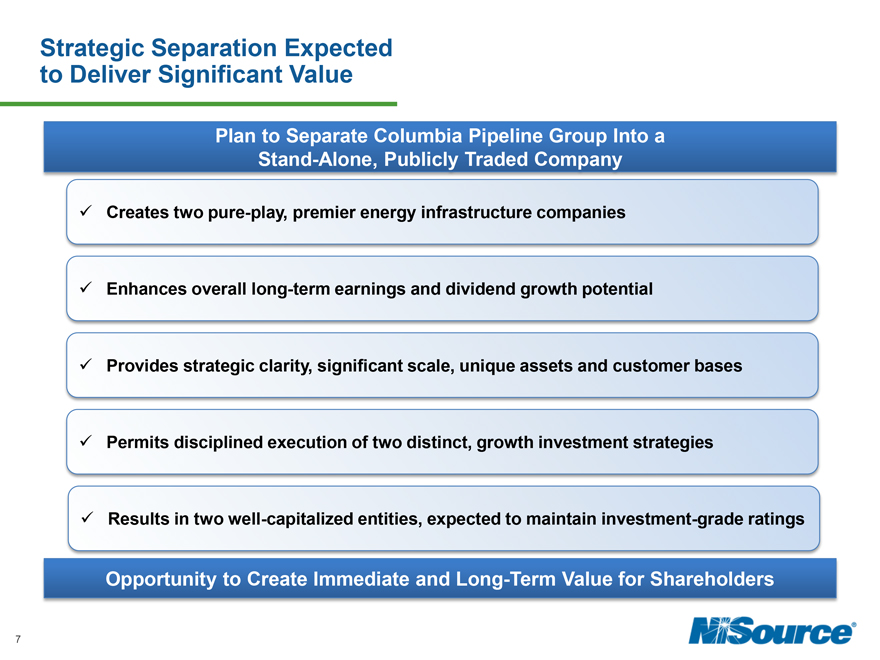

Strategic Separation Expected to Deliver Significant Value

Plan to Separate Columbia Pipeline Group Into a Stand-Alone, Publicly Traded Company

Creates two pure-play, premier energy infrastructure companies

Enhances overall long-term earnings and dividend growth potential

Provides strategic clarity, significant scale, unique assets and customer bases

Permits disciplined execution of two distinct, growth investment strategies

Results in two well-capitalized entities, expected to maintain investment-grade ratings

Opportunity to Create Immediate and Long-Term Value for Shareholders

7 |

|

|

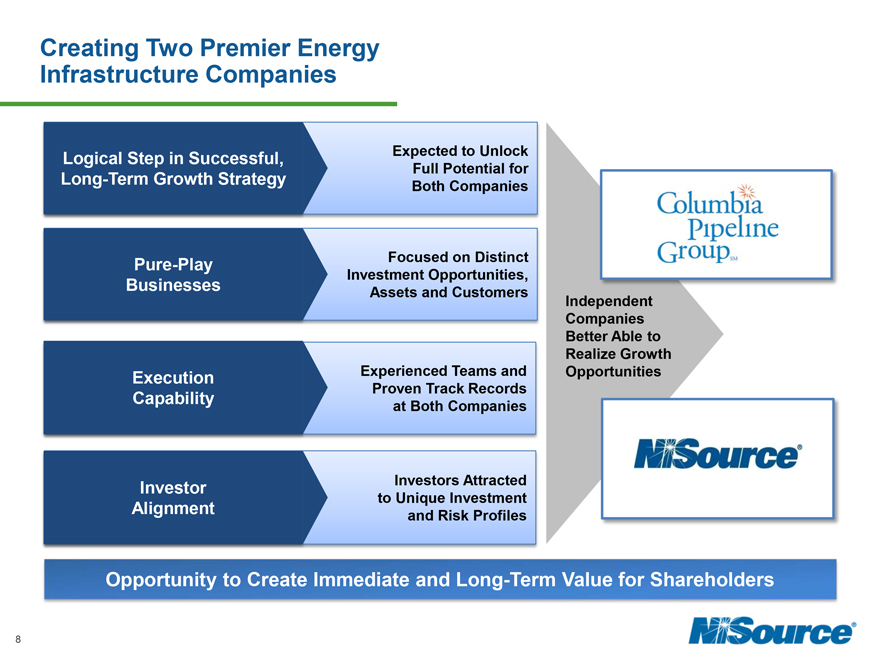

Creating Two Premier Energy Infrastructure Companies

Logical Step in Successful, Long-Term Growth Strategy

Expected to Unlock Full Potential for Both Companies

Pure-Play Businesses

Focused on Distinct

Investment Opportunities,

Assets and Customers

Execution Capability

Experienced Teams and Proven Track Records at Both Companies

Investor Alignment

Investors Attracted to Unique Investment and Risk Profiles

Independent Companies Better Able to Realize Growth Opportunities

Opportunity to Create Immediate and Long-Term Value for Shareholders

8 |

|

|

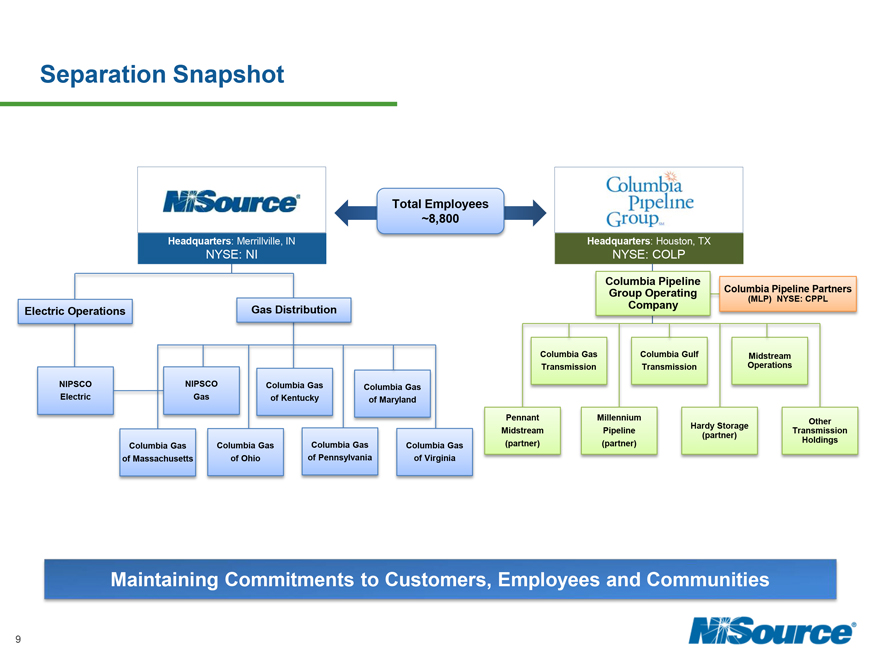

Separation Snapshot

Total Employees ~8,800

Headquarters: Merrillville, IN Headquarters: Houston, TX

NYSE: NI NYSE: COLP

Columbia Pipeline

Group Operating Columbia Pipeline Partners

Gas Distribution Company (MLP) NYSE: CPPL Electric Operations

Columbia Gas Columbia Gulf Midstream Transmission Transmission Operations NIPSCO NIPSCO Columbia Gas Columbia Gas Electric Gas of Kentucky of Maryland

Pennant Millennium Hardy Storage Other Midstream Pipeline Transmission (partner) (partner) (partner) Holdings Columbia Gas Columbia Gas Columbia Gas Columbia Gas of Massachusetts of Ohio of Pennsylvania of Virginia

Maintaining Commitments to Customers, Employees and Communities

9

|

Creating Two Premier Energy Infrastructure Companies

Pure-Play Natural Gas & Electric Utilities

Proven operators, focused on safety, reliability and customer service

Significant long-term infrastructure investment opportunity expected to sustain strong earnings and dividend growth

Constructive regulatory policies and stakeholder support across jurisdictions

Expected to maintain investment-grade credit rating

Pure-Play Pipeline, Midstream & Storage Company

Significant scale and footprint in Marcellus/Utica, Midwest, Mid-Atlantic and Gulf Coast markets

Significant modernization and organic growth opportunities expected to support robust EBITDA and dividend growth

Expected to maintain investment-grade credit rating

MLP expected to provide access to capital to fund CapEx needs

Two Well-Capitalized Energy Infrastructure Companies With Compelling Investment Propositions

10

|

Two Premier Pure-Play Companies With Significant Scale

LDCs, Producers, Marketers, Electric ~4M Gas/Electric Distribution Customers Generators and Other Large End Users

~15K Miles of Transmission ~58K Miles Distribution Pipe ~1.3 Tcf of Throughput Per Year 3,300 MW Generation Operations

35 Storage Fields, ~300 Bcf Working ~2,800 Circuit Miles Transmission Capacity

~$7.4B; Expected to Grow on Rate Base*/Net ~$4B; Expected to Grow Average by ~8% per year Investment Growth to ~$12.5B+ by 2020

~$30B Over Investment $12-15B Over 20+ Years Opportunity Next 10 Years Marcellus, Utica;

7 States Footprint Midwest, Mid-Atlantic and Gulf Coast Markets

Significant Growth Potential With Stable Financial Profiles

*As of 12/31/2013

11

|

Financial Overview of Separation

Steve Smith

Chief Financial Officer

|

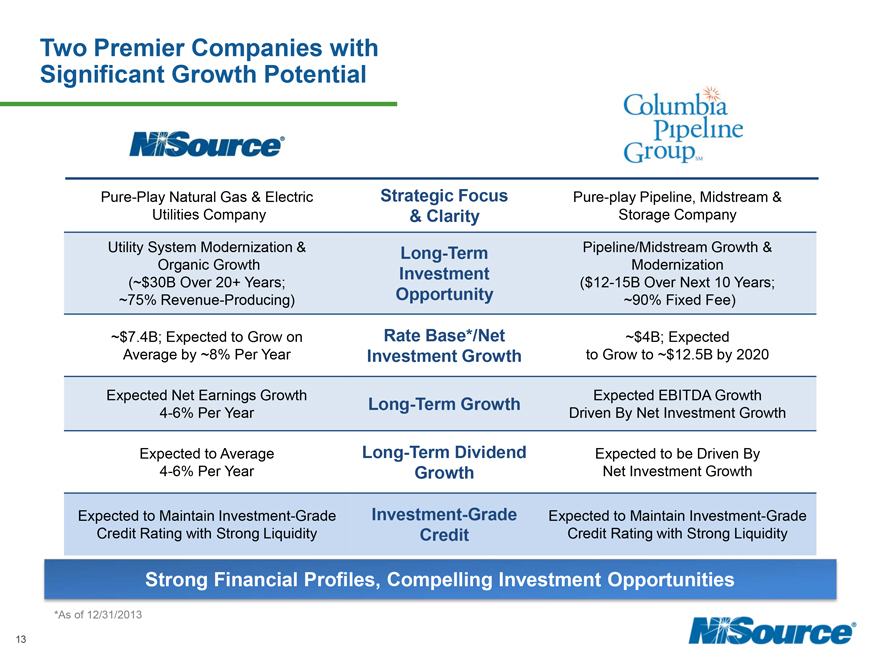

Two Premier Companies with Significant Growth Potential

Pure-Play Natural Gas & Electric Strategic Focus Pure-play Pipeline, Midstream & Utilities Company & Clarity Storage Company

Utility System Modernization & Long-Term Pipeline/Midstream Growth & Organic Growth Investment Modernization

(~$30B Over 20+ Years; ($12-15B Over Next 10 Years; ~75% Revenue-Producing) Opportunity ~90% Fixed Fee)

~$7.4B; Expected to Grow on Rate Base*/Net ~$4B; Expected Average by ~8% Per Year Investment Growth to Grow to ~$12.5B by 2020

Expected Net Earnings Growth Long-Term Growth Expected EBITDA Growth 4-6% Per Year Driven By Net Investment Growth

Expected to Average Long-Term Dividend Expected to be Driven By 4-6% Per Year Growth Net Investment Growth

Expected to Maintain Investment-Grade Investment-Grade Expected to Maintain Investment-Grade Credit Rating with Strong Liquidity Credit Credit Rating with Strong Liquidity

Strong Financial Profiles, Compelling Investment Opportunities

*As of 12/31/2013

13

|

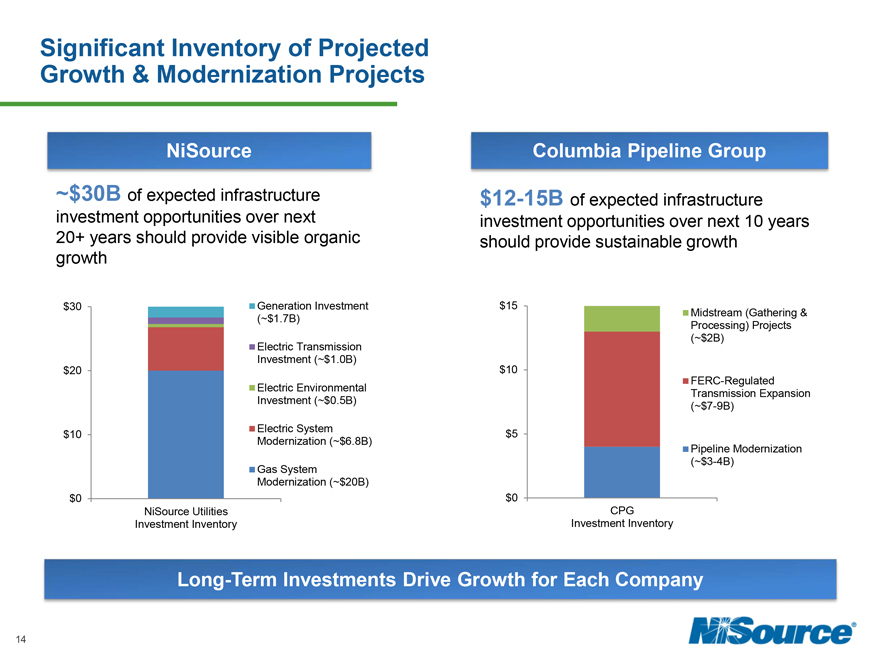

Significant Inventory of Projected Growth & Modernization Projects

NiSource

Columbia Pipeline Group

~$30B of expected infrastructure investment opportunities over next 20+ years should provide visible organic growth

$12-15B of expected infrastructure investment opportunities over next 10 years should provide sustainable growth

$30 Generation Investment

(~$1.7B)

Electric Transmission

Investment (~$1.0B)

$20

Electric Environmental

Investment (~$0.5B)

$10 Electric System

Modernization (~$6.8B)

Gas System

Modernization (~$20B)

$0

NiSource Utilities

Investment Inventory

$12-15B of expected infrastructure investment opportunities over next 10 years should provide sustainable growth

$15 Midstream (Gathering &

Processing) Projects

(~$2B)

$10 FERC-Regulated

Transmission Expansion

(~$7-9B)

$5 Pipeline Modernization

(~$3-4B)

$0 CPG

Investment Inventory

Long-Term Investments Drive Growth for Each Company

14

|

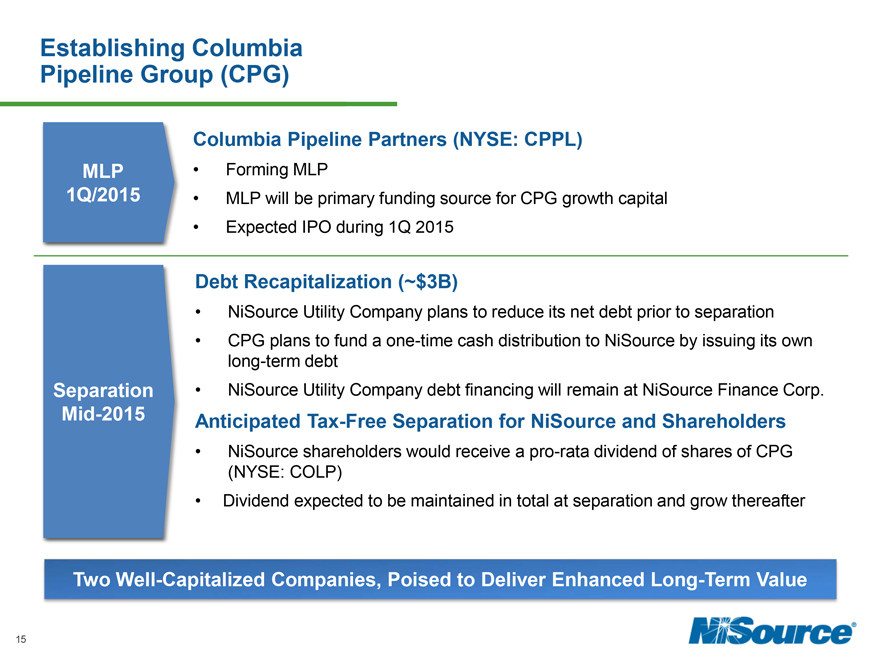

Establishing Columbia Pipeline Group (CPG)

MLP 1Q/2015

Columbia Pipeline Partners (NYSE: CPPL)

Forming MLP

MLP will be primary funding source for CPG growth capital

Expected IPO during 1Q 2015

Separation Mid-2015

Debt Recapitalization (~$3B)

NiSource Utility Company plans to reduce its net debt prior to separation

CPG plans to fund a one-time cash distribution to NiSource by issuing its own long-term debt

NiSource Utility Company debt financing will remain at NiSource Finance Corp.

Anticipated Tax-Free Separation for NiSource and Shareholders

NiSource shareholders would receive a pro-rata dividend of shares of CPG (NYSE: COLP)

Dividend expected to be maintained in total at separation and grow thereafter

Two Well-Capitalized Companies, Poised to Deliver Enhanced Long-Term Value

15

|

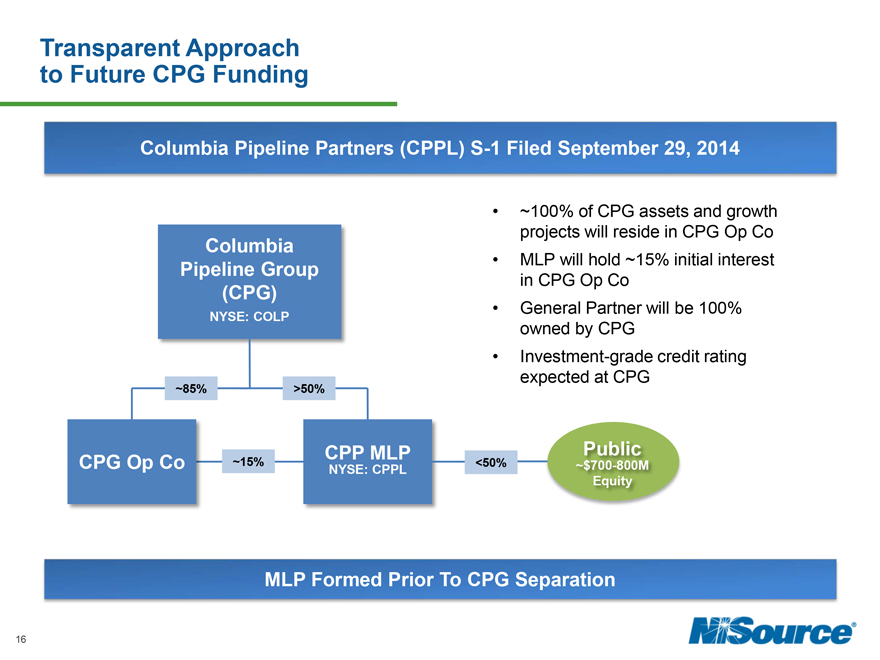

Transparent Approach to Future CPG Funding

Columbia Pipeline Partners (CPPL) S-1 Filed September 29, 2014

Columbia Pipeline Group (CPG)

NYSE: COLP

~100% of CPG assets and growth projects will reside in CPG Op Co

MLP will hold ~15% initial interest in CPG Op Co

General Partner will be 100% owned by CPG

Investment-grade credit rating expected at CPG

~85%

>50%

CPG Op Co

~15%

CPP MLP

NYSE: CPPL

<50%

Public

~$700-800M Equity

MLP Formed Prior To CPG Separation

16

|

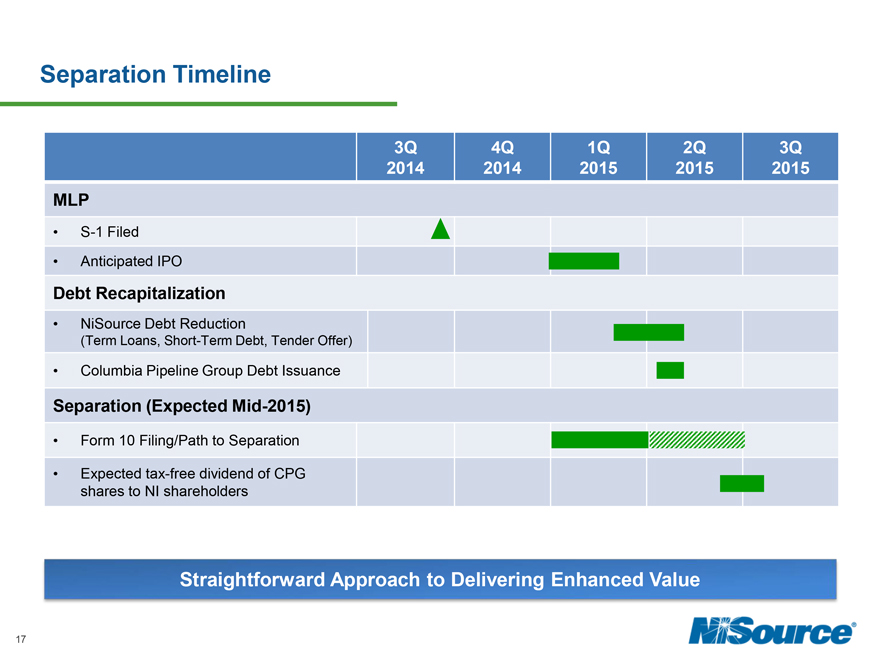

Separation Timeline

3Q 4Q 1Q 2Q 3Q

2014 2014 2015 2015 2015

MLP

S-1 Filed

Anticipated IPO

Debt Recapitalization

NiSource Debt Reduction

(Term Loans, Short-Term Debt, Tender Offer)

Columbia Pipeline Group Debt Issuance

Separation (Expected Mid-2015)

Form 10 Filing/Path to Separation

Expected tax-free dividend of CPG

shares to NI shareholders

Straightforward Approach to Delivering Enhanced Value

17

|

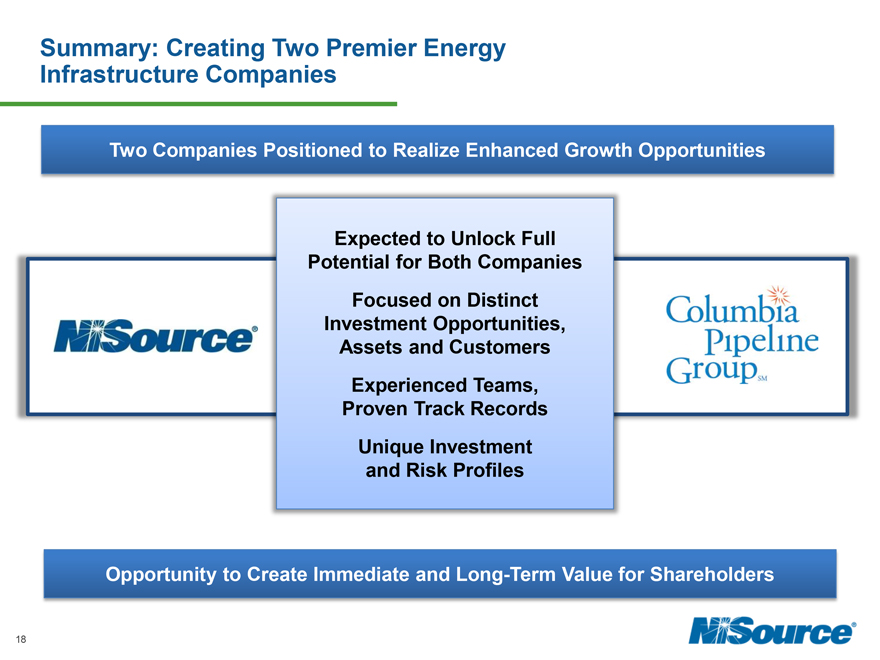

Summary: Creating Two Premier Energy Infrastructure Companies

Two Companies Positioned to Realize Enhanced Growth Opportunities

Expected to Unlock Full Potential for Both Companies Focused on Distinct Investment Opportunities, Assets and Customers Experienced Teams, Proven Track Records Unique Investment and Risk Profiles

Opportunity to Create Immediate and Long-Term Value for Shareholders

18

|

NiSource:

Premier, Pure-Play Natural Gas

& Electric Utilities

Joe Hamrock

EVP and Group CEO, NiSource Gas Distribution

Jim Stanley

EVP and Group CEO, NIPSCO

|

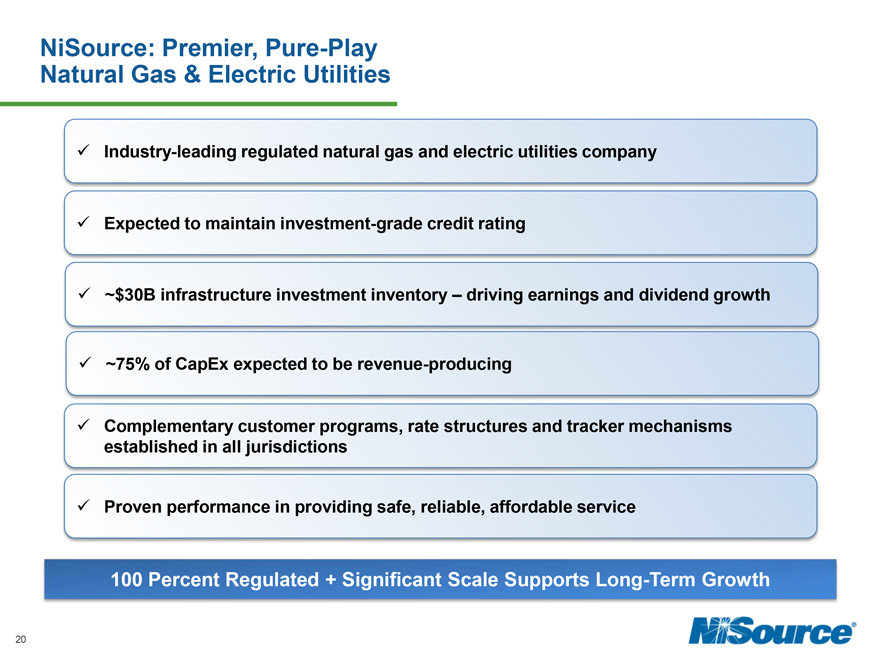

NiSource: Premier, Pure-Play Natural Gas & Electric Utilities

Industry-leading regulated natural gas and electric utilities company

Expected to maintain investment-grade credit rating

~$30B infrastructure investment inventory – driving earnings and dividend growth

~75% of CapEx expected to be revenue-producing

Complementary customer programs, rate structures and tracker mechanisms established in all jurisdictions

Proven performance in providing safe, reliable, affordable service

100 Percent Regulated + Significant Scale Supports Long-Term Growth

20

NiSource: 100% Regulated Natural Gas & Electric Utilities

Indiana Natural Gas Distribution

Indiana Electric Generation, Transmission & Distribution

Gas Distribution Companies

Kentucky

Maryland

Massachusetts

Ohio

Pennsylvania

Virginia

Large Scale Footprint Across 7 States

~3.5M Gas LDC Customers

~500K Electric Customers

Strong Performance and Execution Track Record

Extensive System Modernization and Organic Growth Inventory

Constructive Regulatory Environments

Strong Customer Service

A Strong, Well Established Platform for Growth

21

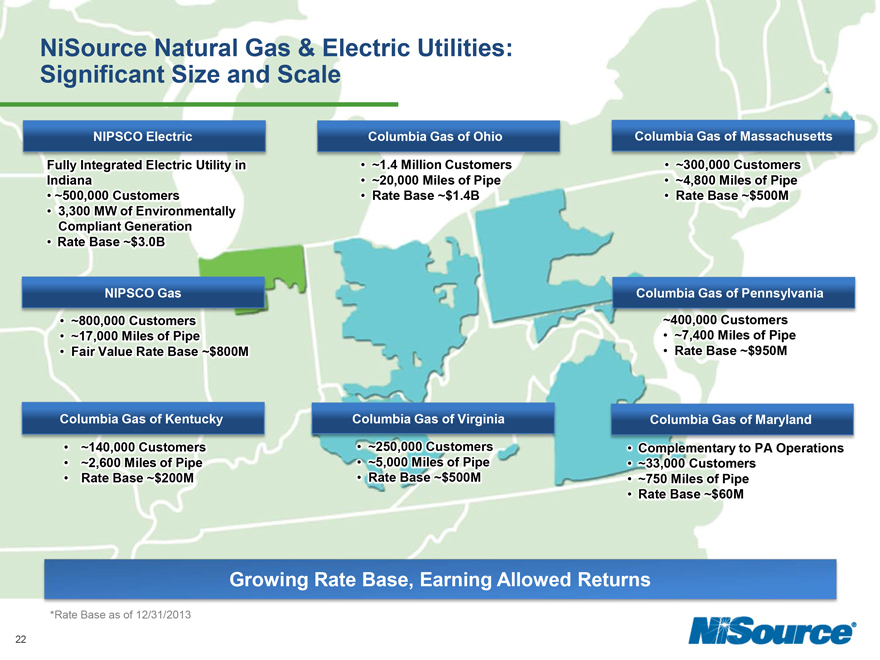

NiSource Natural Gas & Electric Utilities: Significant Size and Scale

NIPSCO Electric

Fully Integrated Electric Utility in Indiana

~500,000 Customers

3,300 MW of Environmentally Compliant Generation

Rate Base ~$3.0B

NIPSCO Gas • ~800,000 Customers • ~17,000 Miles of Pipe • Fair Value Rate Base ~$800M

Columbia Gas of Kentucky

~140,000 Customers

~2,600 Miles of Pipe

Rate Base ~$200M

Columbia Gas of Ohio • ~1.4 Million Customers • ~20,000 Miles of Pipe • Rate Base ~$1.4B

Columbia Gas of Virginia • ~250,000 Customers • ~5,000 Miles of Pipe • Rate Base ~$500M

Columbia Gas of Massachusetts • ~300,000 Customers • ~4,800 Miles of Pipe • Rate Base ~$500M

Columbia Gas of Pennsylvania ~400,000 Customers • ~7,400 Miles of Pipe • Rate Base ~$950M

Columbia Gas of Maryland

Complementary to PA Operations

~33,000 Customers

~750 Miles of Pipe

Rate Base ~$60M

Growing Rate Base, Earning Allowed Returns

*Rate Base as of 12/31/2013

22

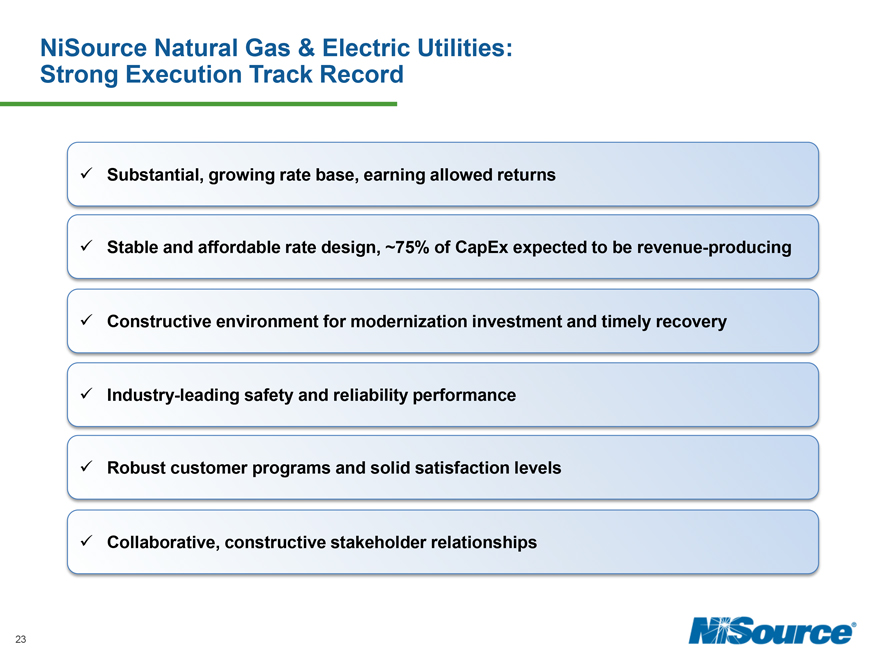

NiSource Natural Gas & Electric Utilities: Strong Execution Track Record

Substantial, growing rate base, earning allowed returns

Stable and affordable rate design, ~75% of CapEx expected to be revenue-producing Constructive environment for modernization investment and timely recovery Industry-leading safety and reliability performance Robust customer programs and solid satisfaction levels Collaborative, constructive stakeholder relationships

23

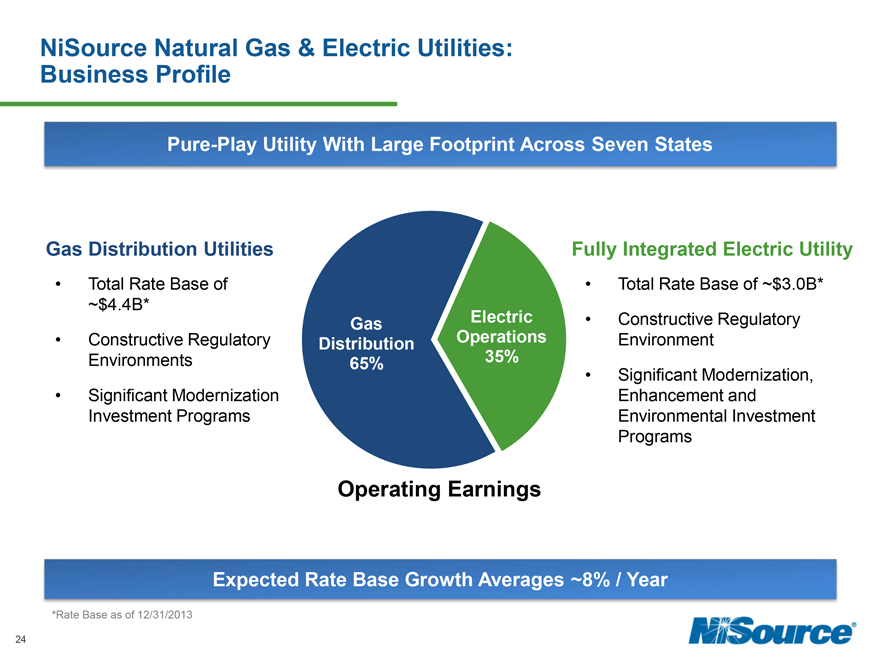

NiSource Natural Gas & Electric Utilities: Business Profile

Pure-Play Utility With Large Footprint Across Seven States

Gas Distribution Utilities

Total Rate Base of

~$4.4B*

Constructive Regulatory Environments

Significant Modernization Investment Programs

Operating Earnings

Fully Integrated Electric Utility

Total Rate Base of ~$3.0B*

Constructive Regulatory Environment

Significant Modernization, Enhancement and Environmental Investment Programs

Gas Distribution 65%

Electric Operations 35%

Expected Rate Base Growth Averages ~8% / Year

*Rate Base as of 12/31/2013

24

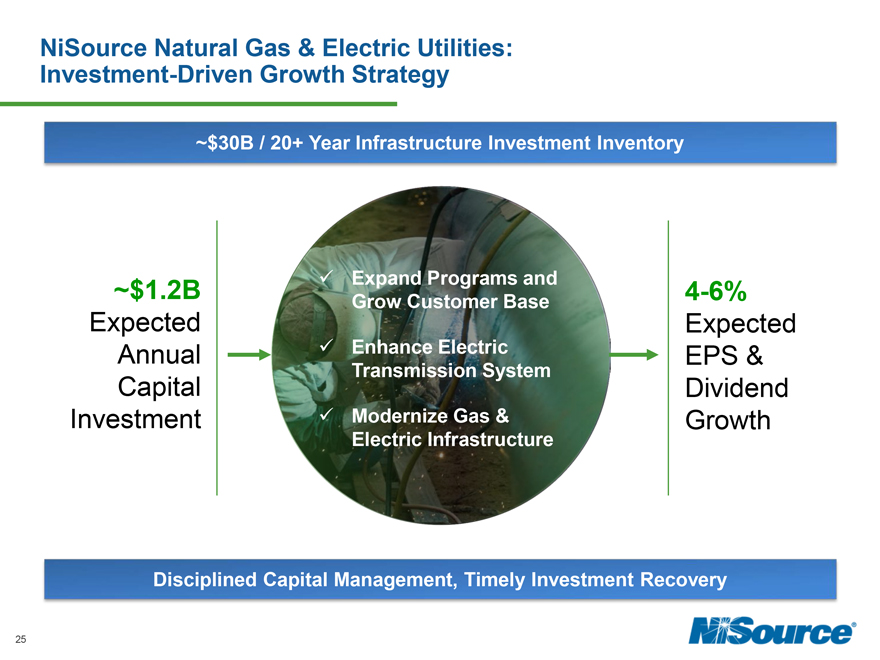

NiSource Natural Gas & Electric Utilities: Investment-Driven Growth Strategy

~$30B / 20+ Year Infrastructure Investment Inventory

~$1.2B

Expected

Annual

Capital

Investment

Expand Programs and Grow Customer Base

Enhance Electric Transmission System

Modernize Gas & Electric Infrastructure

4-6%

Expected EPS & Dividend Growth

Disciplined Capital Management, Timely Investment Recovery

25

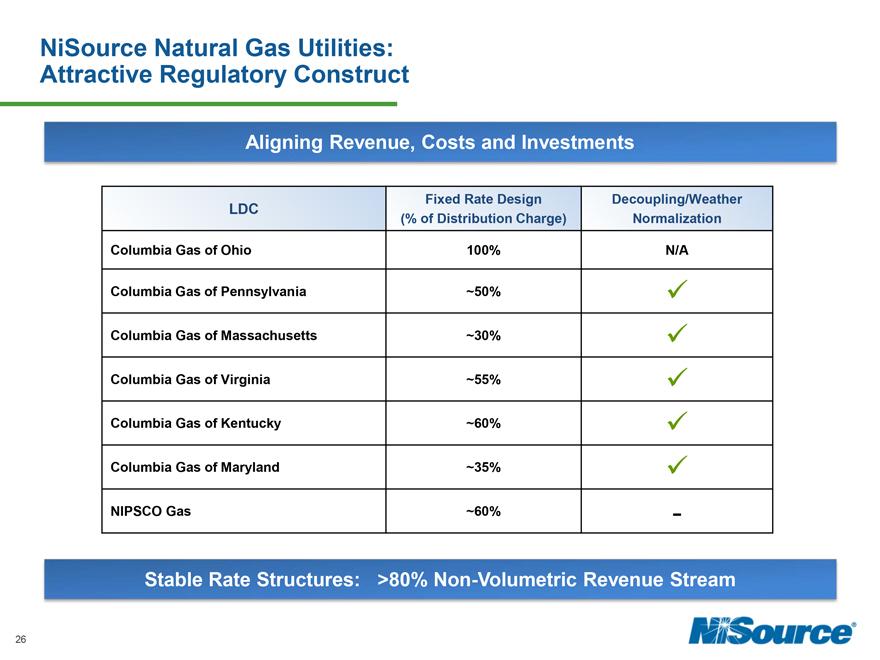

NiSource Natural Gas Utilities: Attractive Regulatory Construct

Aligning Revenue, Costs and Investments

LDC Fixed Rate Design Decoupling/Weather

(% of Distribution Charge) Normalization

Columbia Gas of Ohio 100% N/A

Columbia Gas of Pennsylvania ~50%

Columbia Gas of Massachusetts ~30%

Columbia Gas of Virginia ~55%

Columbia Gas of Kentucky ~60%

Columbia Gas of Maryland ~35%

NIPSCO Gas ~60% -

Stable Rate Structures: >80% Non-Volumetric Revenue Stream

26

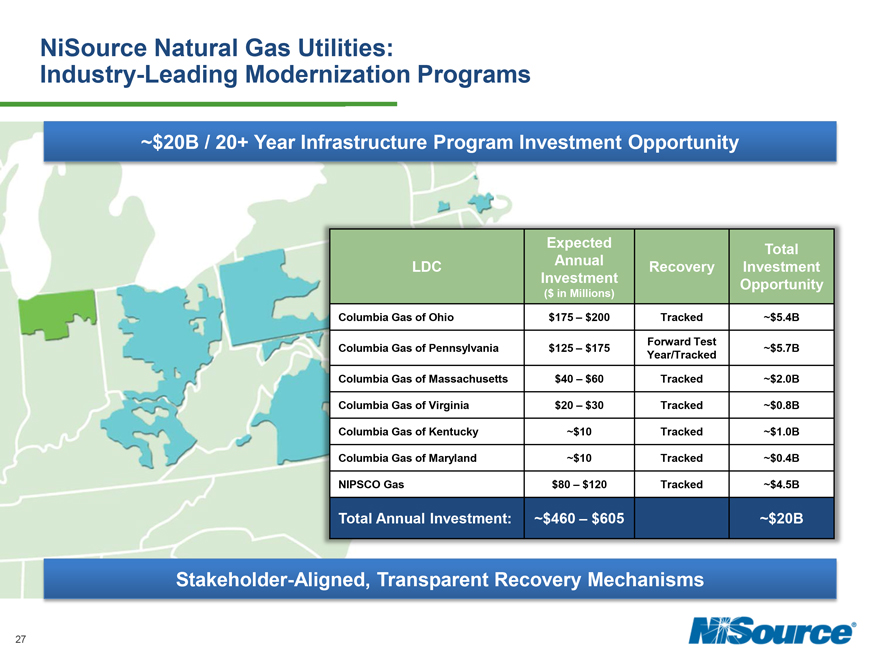

NiSource Natural Gas Utilities:

Industry-Leading Modernization Programs

~$20B / 20+ Year Infrastructure Program Investment Opportunity

Expected Total

LDC Annual Recovery Investment

Investment Opportunity

($ in Millions)

Columbia Gas of Ohio $175 – $200 Tracked ~$5.4B

Forward Test

Columbia Gas of Pennsylvania $125 – $175 ~$5.7B

Year/Tracked

Columbia Gas of Massachusetts $40 – $60 Tracked ~$2.0B

Columbia Gas of Virginia $20 – $30 Tracked ~$0.8B

Columbia Gas of Kentucky ~$10 Tracked ~$1.0B

Columbia Gas of Maryland ~$10 Tracked ~$0.4B

NIPSCO Gas $80 – $120 Tracked ~$4.5B

Total Annual Investment: ~$460 – $605 ~$20B

Stakeholder-Aligned, Transparent Recovery Mechanisms

27

NiSource Electric Utility:

NIPSCO Infrastructure Investment

~$10B / 20+ Year Electric Infrastructure Investment Opportunity

Expected Total

NIPSCO Electric Tracked Annual Investment

Investments Recovery Investment Opportunity

($ in millions)

Electric System $70 – $250 ~$ 6.8B

Modernization Program

Environmental Compliance $25 – $100 ~$ 0.5B

Transmission

Enhancements/Growth N/A $80 – $150 ~$ 1.0B

Generation Upgrades N/A TBD ~$ 1.7B

Total Annual ~$175 – $500 ~$10B

Investment:

Current Transmission Projects

Stakeholder-Aligned, Transparent Recovery Mechanisms

28

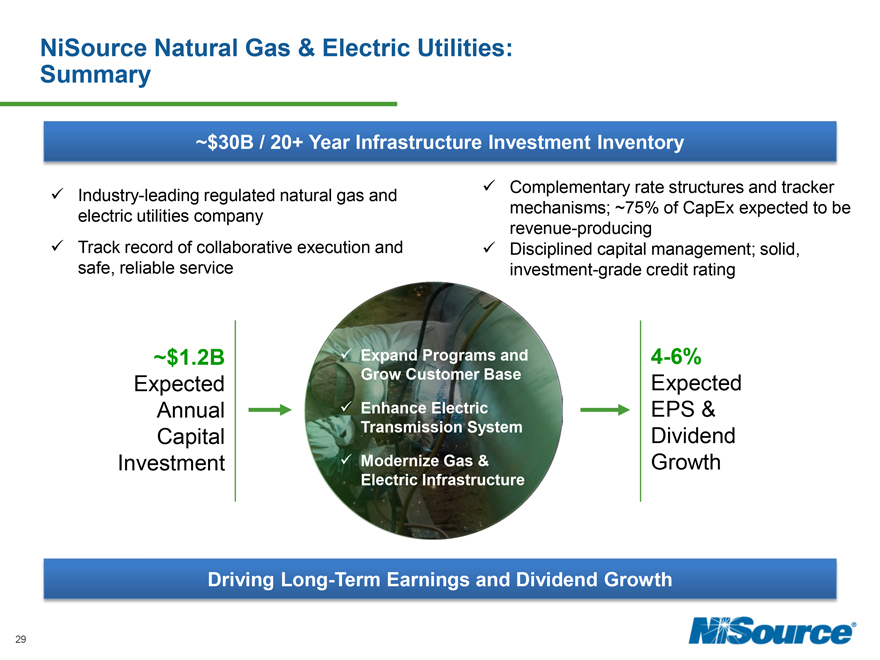

NiSource Natural Gas & Electric Utilities: Summary

~$30B / 20+ Year Infrastructure Investment Inventory

Industry-leading regulated natural gas and electric utilities company

Track record of collaborative execution and safe, reliable service

Complementary rate structures and tracker mechanisms; ~75% of CapEx expected to be revenue-producing

Disciplined capital management; solid, investment-grade credit rating

~$1.2B

Expected

Annual

Capital

Investment

Expand Programs and Grow Customer Base

Enhance Electric Transmission System

Modernize Gas & Electric Infrastructure

4-6%

Expected EPS & Dividend Growth

Driving Long-Term Earnings and Dividend Growth

29

Columbia Pipeline Group (CPG):

A Premier Pipeline, Midstream

& Storage Company

Glen Kettering

EVP and Group CEO, Columbia Pipeline Group

Stan Chapman

EVP and Chief Commercial Officer

Brett Stovern

Chief Operating Officer, Midstream

Shawn Patterson

President, Operations and Project Delivery

30

|

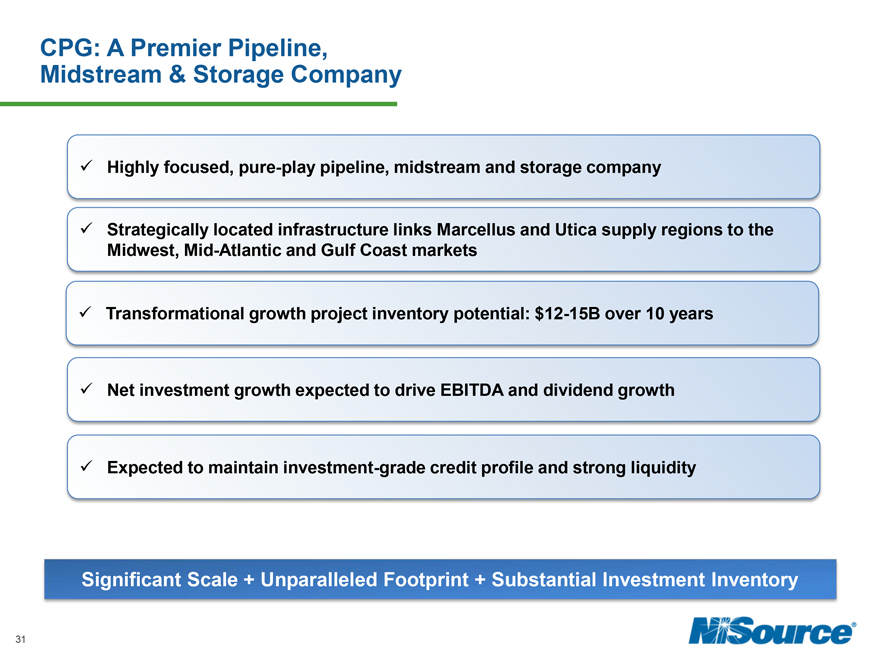

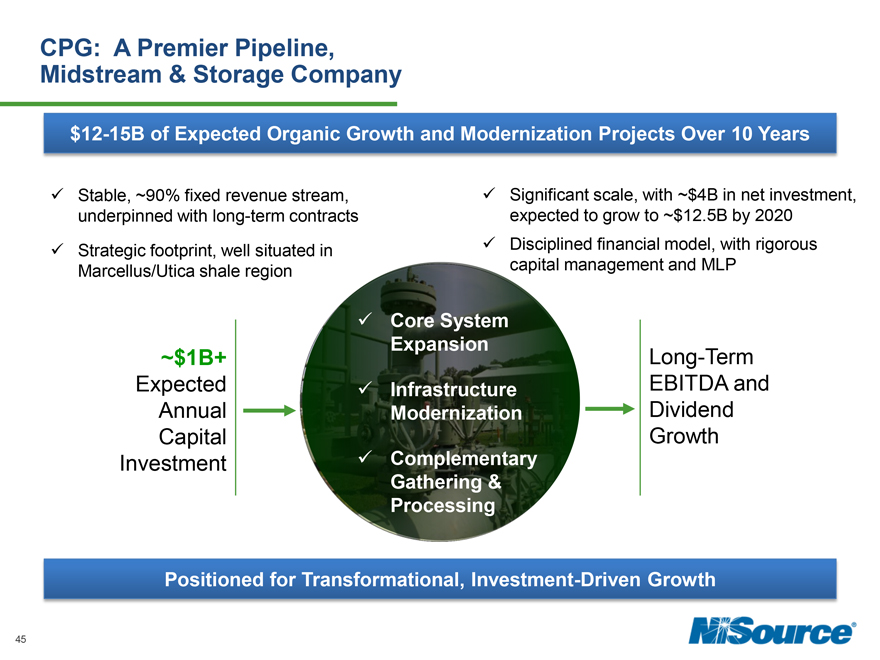

CPG: A Premier Pipeline, Midstream & Storage Company

Highly focused, pure-play pipeline, midstream and storage company

Strategically located infrastructure links Marcellus and Utica supply regions to the Midwest, Mid-Atlantic and Gulf Coast markets

Transformational growth project inventory potential: $12-15B over 10 years

Net investment growth expected to drive EBITDA and dividend growth

Expected to maintain investment-grade credit profile and strong liquidity

Significant Scale + Unparalleled Footprint + Substantial Investment Inventory

31

|

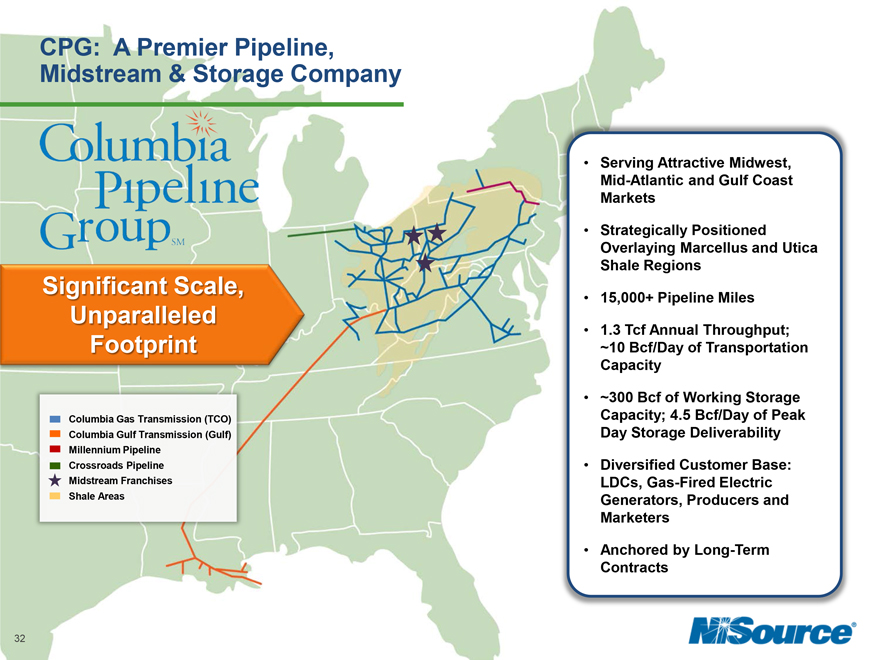

CPG: A Premier Pipeline, Midstream & Storage Company

Significant Scale,

Unparalleled

Footprint

Columbia Gas Transmission (TCO) Columbia Gulf Transmission (Gulf) Millennium Pipeline Crossroads Pipeline Midstream Franchises Shale Areas

Serving Attractive Midwest, Mid-Atlantic and Gulf Coast Markets Strategically Positioned Overlaying Marcellus and Utica Shale Regions 15,000+ Pipeline Miles 1.3 Tcf Annual Throughput; ~10 Bcf/Day of Transportation Capacity ~300 Bcf of Working Storage Capacity; 4.5 Bcf/Day of Peak Day Storage Deliverability Diversified Customer Base: LDCs, Gas-Fired Electric Generators, Producers and Marketers Anchored by Long-Term Contracts

32

|

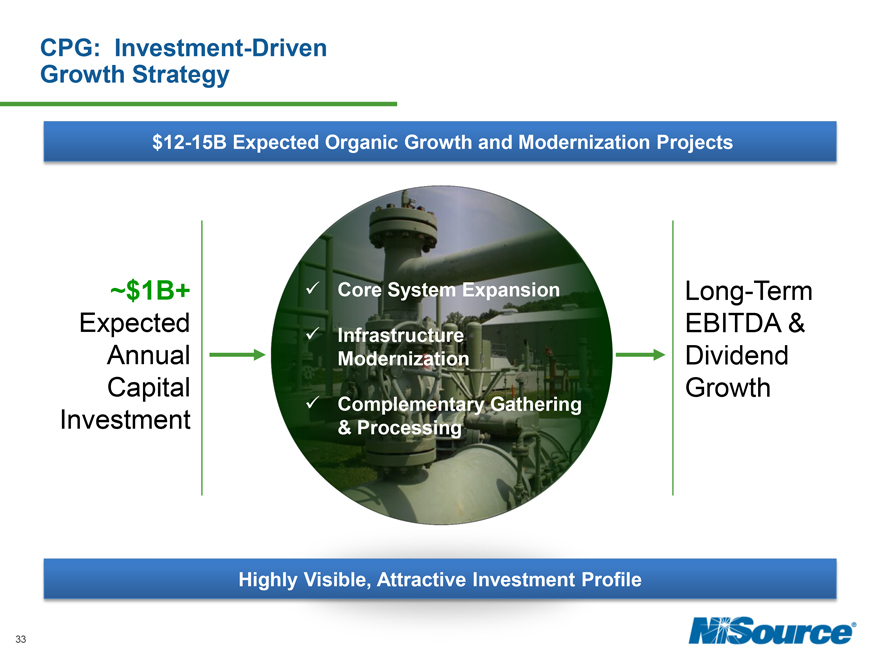

CPG: Investment-Driven Growth Strategy

$12-15B Expected Organic Growth and Modernization Projects

~$1B+

Expected

Annual

Capital

Investment

Core System Expansion

Infrastructure Modernization

Complementary Gathering

& Processing

Long-Term EBITDA & Dividend Growth

Highly Visible, Attractive Investment Profile

33

|

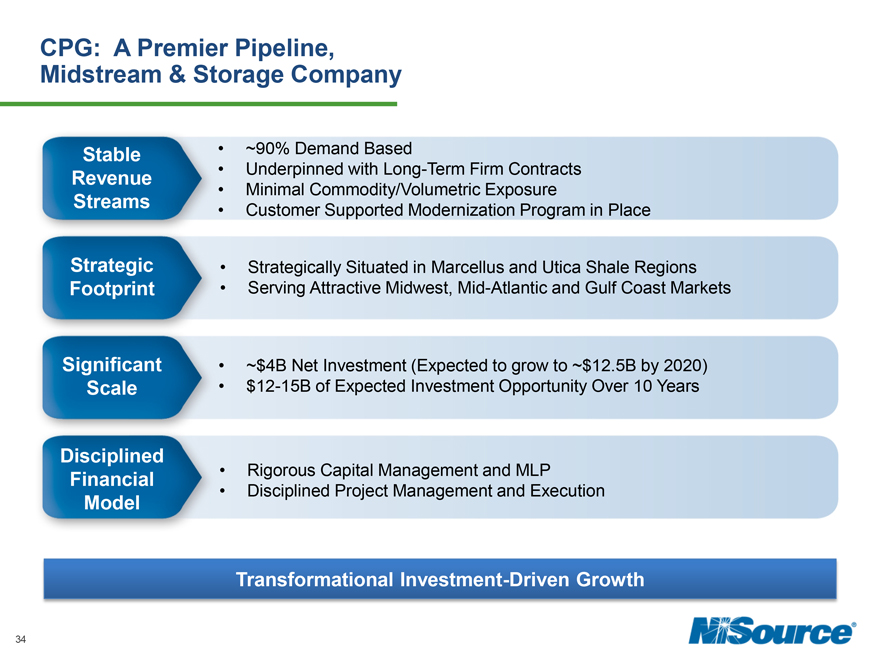

CPG: A Premier Pipeline, Midstream & Storage Company

Stable Revenue Streams

Strategic Footprint

Significant Scale

Disciplined Financial Model

~90% Demand Based

Underpinned with Long-Term Firm Contracts Minimal Commodity/Volumetric Exposure

Customer Supported Modernization Program in Place

Strategically Situated in Marcellus and Utica Shale Regions Serving Attractive Midwest, Mid-Atlantic and Gulf Coast Markets

~$4B Net Investment (Expected to grow to ~$12.5B by 2020) $12-15B of Expected Investment Opportunity Over 10 Years

Rigorous Capital Management and MLP Disciplined Project Management and Execution

Transformational Investment-Driven Growth

34

|

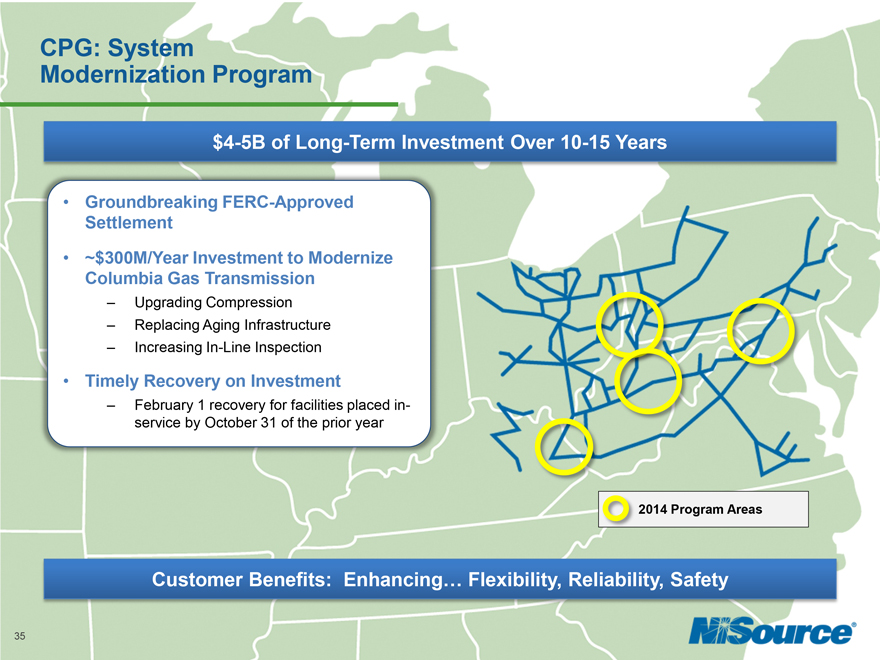

CPG: System

Modernization Program

$4-5B of Long-Term Investment Over 10-15 Years

Groundbreaking FERC-Approved Settlement

~$300M/Year Investment to Modernize Columbia Gas Transmission

Upgrading Compression

Replacing Aging Infrastructure

Increasing In-Line Inspection

Timely Recovery on Investment

February 1 recovery for facilities placed in-service by October 31 of the prior year

2014 Program Areas

Customer Benefits: Enhancing… Flexibility, Reliability, Safety

35

|

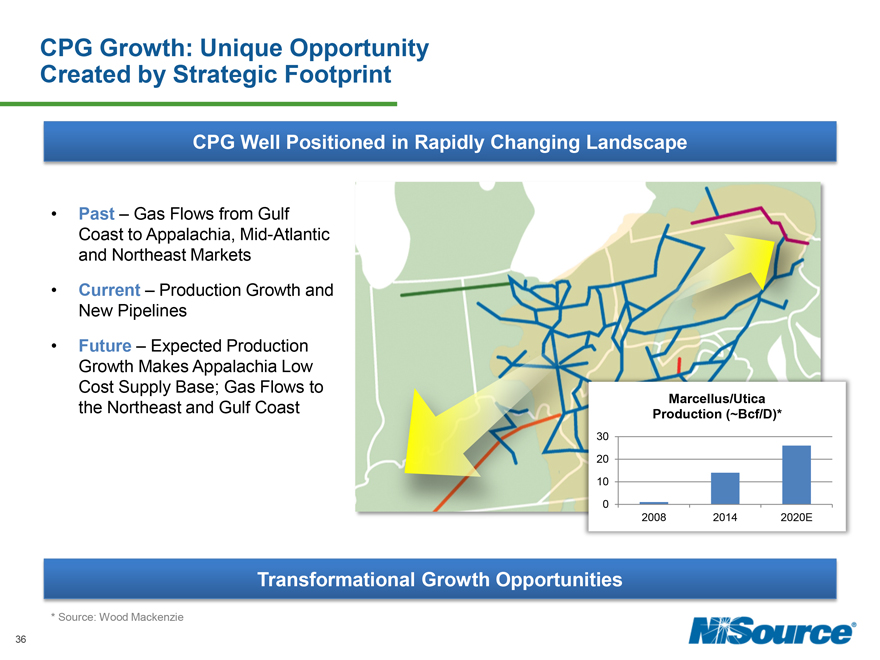

CPG Growth: Unique Opportunity Created by Strategic Footprint

CPG Well Positioned in Rapidly Changing Landscape

Past – Gas Flows from Gulf Coast to Appalachia, Mid-Atlantic and Northeast Markets

Current – Production Growth and New Pipelines

Future – Expected Production Growth Makes Appalachia Low Cost Supply Base; Gas Flows to the Northeast and Gulf Coast

Marcellus/Utica Production (~Bcf/D)*

30

20

10

0

2008 2014 2020E

Transformational Growth Opportunities

* Source: Wood Mackenzie

36

|

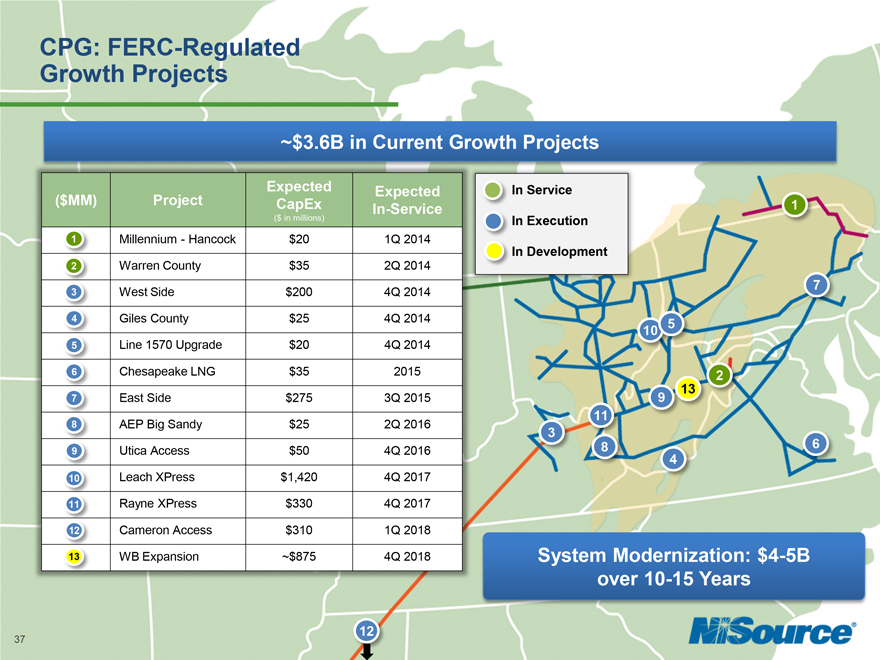

CPG: FERC-Regulated Growth Projects

~$3.6B in Current Growth Projects

Expected Expected

($MM) Project CapEx In-Service

($ in millions)

1 Millennium—Hancock $20 1Q 2014

2 Warren County $35 2Q 2014

3 West Side $200 4Q 2014

4 Giles County $25 4Q 2014

5 Line 1570 Upgrade $20 4Q 2014

6 Chesapeake LNG $35 2015

7 East Side $275 3Q 2015

8 AEP Big Sandy $25 2Q 2016

9 Utica Access $50 4Q 2016

10 Leach XPress $1,420 4Q 2017

11 Rayne XPress $330 4Q 2017

12 Cameron Access $310 1Q 2018

13 WB Expansion ~$875 4Q 2018

In Service In Execution In Development

1 2 3 4 5 6 7 8 9 10 11 12 13

System Modernization: $4-5B over 10-15 Years

37

|

CPG Growth: East Side Expansion

~$275M Investment, Supported by East Coast LDCs and Marcellus Producers

Expands facilities to transport Northeast Marcellus supplies to Mid-Atlantic markets

~315 MMcf/D of additional capacity

Key Customers: South Jersey Gas, South Jersey Resources, New Jersey Natural Gas, Cabot, Southwest Energy

Planned In-Service: 3Q 2015

Columbia Transmission Expansion

Linking New Supplies to Growing Markets

38

|

CPG Growth:

Leach and Rayne XPress Projects

Combined ~$1.75B Investment, Supported by Long-Term Firm Contracts

Adding capacity to transport 1.5 Bcf/D of Marcellus and Utica supplies from constrained production areas to liquid transaction locations/markets

~160 miles of new gas transmission pipeline

~165,000 HP of additional compression across multiple sites

Key Customers: Range Resources, Kaiser Francis, Noble and American Energy Partners

Planned In-Service: 4Q 2017

Utica Receipts

- Clarington, Seneca, Berne, Cadiz

Marcellus Receipts

- Majorsville, Mobley, Sherwood

Leach/ TCO Pool Greenfield Corridor Existing Corridor

Transformational Growth Opportunities

39

|

CPG Growth:

Cameron Access Project

~$310M Investment, Linking Shale Supplies to LNG Export Market

Transports supplies from numerous basins to Cameron LNG facility

New pipeline to the Cameron LNG Facility providing 800 MMcf/D of capacity from Rayne, Louisiana compressor station

Key Customers: GDF Suez SA and MMGS, Inc.

Planned In-Service: 1Q 2018

Leach, KY (TCO)

(Hackberry, LA Cameron LNG)

Delhi, LA

Rayne, LA

Transformational Growth Opportunities

40

CPG Growth: WB XPress Project*

~$875M Investment, Linking Marcellus Supplies to Gulf and East Coast Markets

Additional capacity providing market access for Marcellus supplies

– 500 MMcf/D east toward Loudon

– 800 MMcf/D west toward Broad Run

Looping and compression

Key Customers: Antero and Noble Energy

Planned In-Service: 4Q 2018

Cleveland Station Loudoun (DTI Cove Point) Dranesville (Transco Z5) Broad Run (TGP) Looping and HP

Transformational Growth Opportunities

* In Advanced Development

41

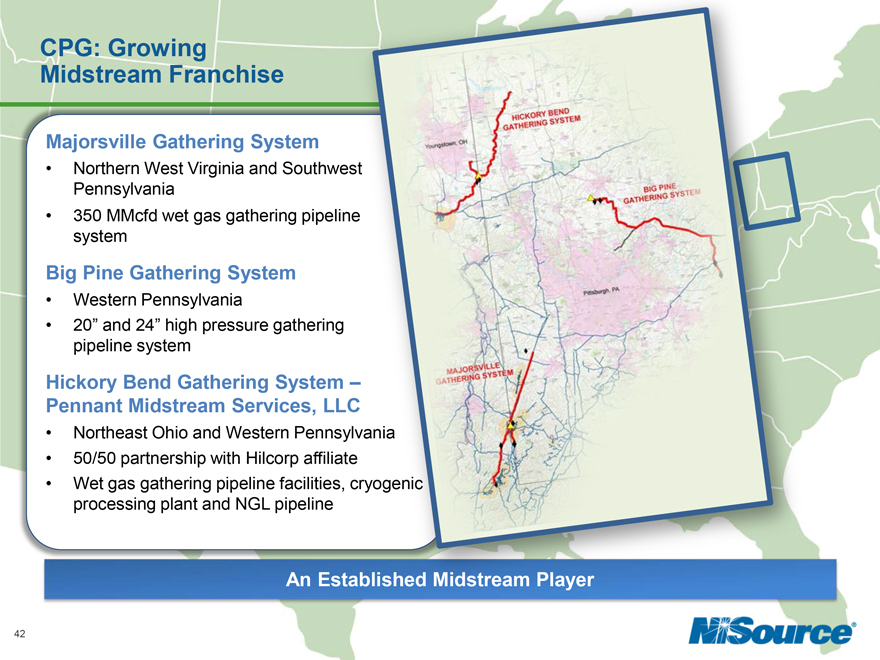

CPG: Growing Midstream Franchise

Majorsville Gathering System

Northern West Virginia and Southwest Pennsylvania

350 MMcfd wet gas gathering pipeline system

Big Pine Gathering System

Western Pennsylvania

20” and 24” high pressure gathering pipeline system

Hickory Bend Gathering System Pennant Midstream Services, LLC

Northeast Ohio and Western Pennsylvania

50/50 partnership with Hilcorp affiliate

Wet gas gathering pipeline facilities, cryogenic processing plant and NGL pipeline

An Established Midstream Player

42

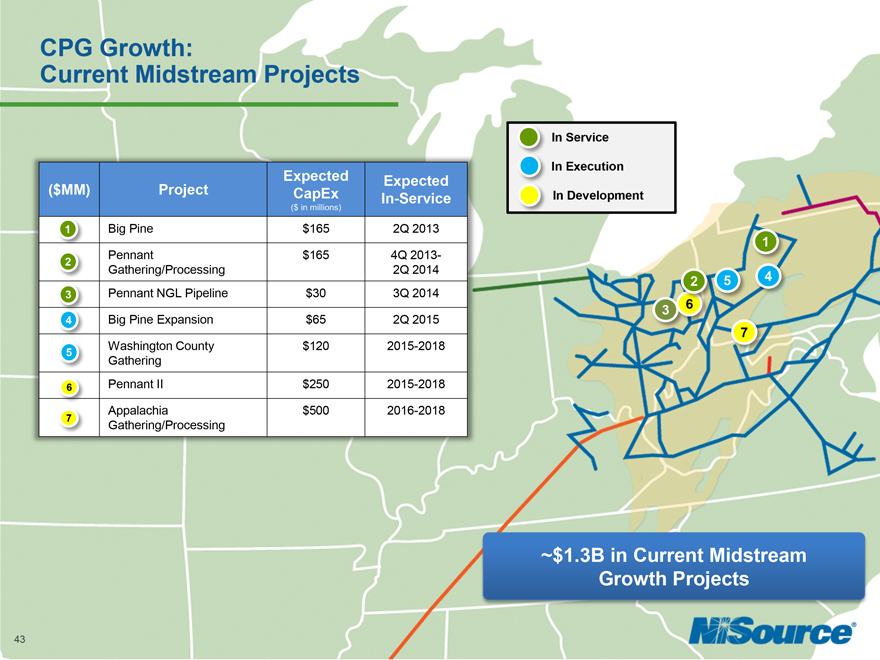

CPG Growth:

Current Midstream Projects

In Service In Execution In Development

Expected Expected

($MM) Project CapEx In-Service

($ in millions)

1 Big Pine $165 2Q 2013

2 Pennant $165 4Q 2013-

Gathering/Processing 2Q 2014

3 Pennant NGL Pipeline $30 3Q 2014

4 Big Pine Expansion $65 2Q 2015

5 Washington County $120 2015-2018

Gathering

6 Pennant II $250 2015-2018

Appalachia $500 2016-2018

7 Gathering/Processing

~$1.3B in Current Midstream Growth Projects

43

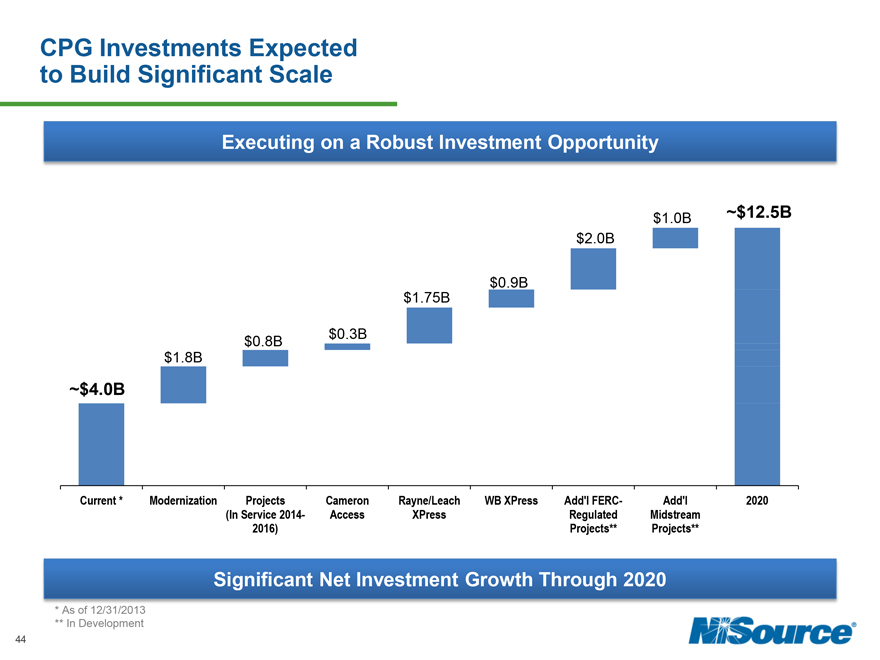

CPG Investments Expected to Build Significant Scale

Executing on a Robust Investment Opportunity

$1.0B ~$12.5B

$2.0B

$0.9B

$1.75B

$0.8B $0.3B

$1.8B

~$4.0B

Current *

Modernization

(In Service Projects 2014-2016)

Cameron Access

Rayne/Leach XPress

WB XPress

Add’l Regulated FERC-Projects**

Midstream Add’l Projects**

2020

Significant Net Investment Growth Through 2020

As of 12/31/2013

In Development

44

CPG: A Premier Pipeline, Midstream & Storage Company

$12-15B of Expected Organic Growth and Modernization Projects Over 10 Years

Stable, ~90% fixed revenue stream, underpinned with long-term contracts Strategic footprint, well situated in Marcellus/Utica shale region

Significant scale, with ~$4B in net investment, expected to grow to ~$12.5B by 2020 Disciplined financial model, with rigorous capital management and MLP

~$1B+

Expected

Annual

Capital

Investment

Core System Expansion

Infrastructure Modernization

Complementary Gathering & Processing

Long-Term EBITDA and Dividend Growth

Positioned for Transformational, Investment-Driven Growth

45

Investment Proposition

Steve Smith

Chief Financial Officer

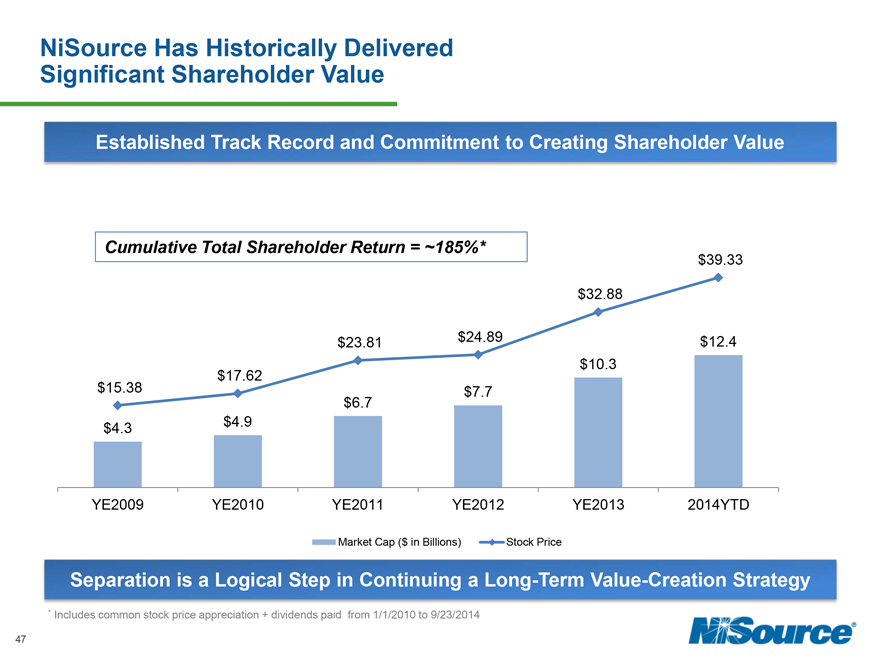

NiSource Has Historically Delivered Significant Shareholder Value

Established Track Record and Commitment to Creating Shareholder Value

Cumulative Total Shareholder Return = ~185%*

$39.33

$32.88

$23.81 $24.89 $12.4

$10.3

$17.62

$15.38 $7.7

$6.7

$4.3 $4.9

YE2009 YE2010 YE2011 YE2012 YE2013 2014YTD

Market Cap ($ in Billions) Stock Price

Separation is a Logical Step in Continuing a Long-Term Value-Creation Strategy

* Includes common stock price appreciation + dividends paid from 1/1/2010 to 9/23/2014

47

Potential to Deliver

Enhanced Shareholder Value

Separation would create two well-positioned energy companies, each with high quality assets, focused investment plans and opportunities

Unique strengths should lead to enhanced valuations

Other expected key shareholder/stakeholder benefits:

Highlights and unlocks the value of two unique businesses Both businesses positioned to deliver enhanced earnings growth driven by clear, identified investment-based growth plans Track record of sustained execution for both businesses

Increased transparency for each business Improved investor alignment Robust capital investment portfolios for both companies

Strong credit profile Manageable cost to achieve

Efficient capital funding for each business Dividend expected to be maintained in total at separation and grow thereafter

48

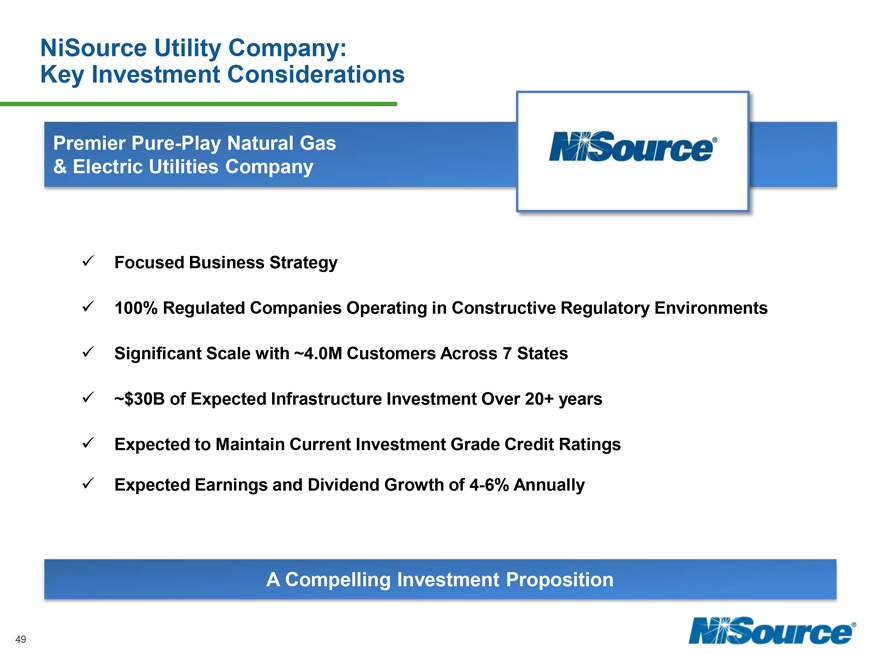

NiSource Utility Company: Key Investment Considerations

Premier Pure-Play Natural Gas

& Electric Utilities Company

Focused Business Strategy

100% Regulated Companies Operating in Constructive Regulatory Environments

Significant Scale with ~4.0M Customers Across 7 States

~$30B of Expected Infrastructure Investment Over 20+ years Expected to Maintain Current Investment Grade Credit Ratings Expected Earnings and Dividend Growth of 4-6% Annually

A Compelling Investment Proposition

49

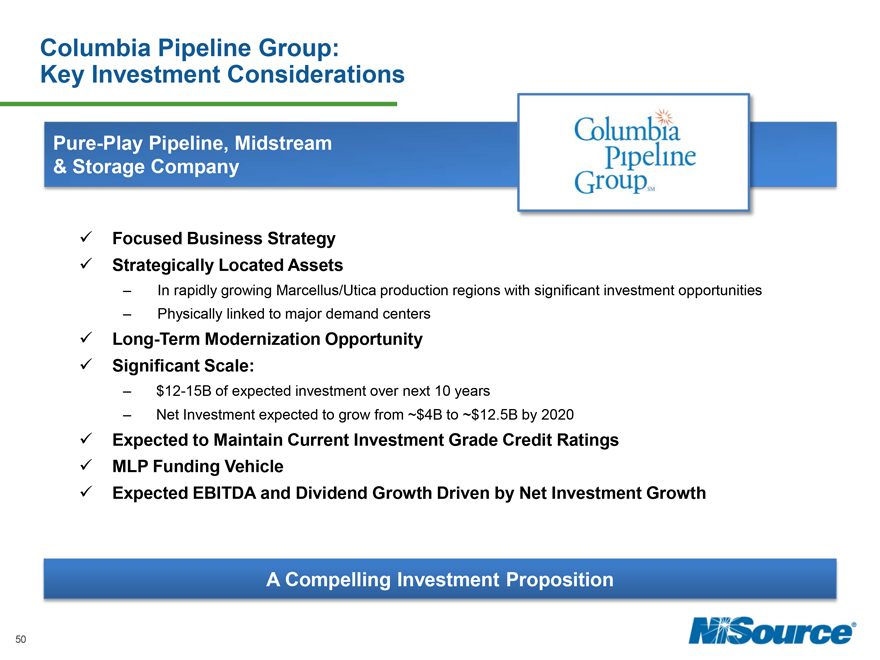

Columbia Pipeline Group: Key Investment Considerations

Pure-Play Pipeline, Midstream

& Storage Company

Focused Business Strategy Strategically Located Assets

In rapidly growing Marcellus/Utica production regions with significant investment opportunities

Physically linked to major demand centers

Long-Term Modernization Opportunity Significant Scale:

$12-15B of expected investment over next 10 years

Net Investment expected to grow from ~$4B to ~$12.5B by 2020

Expected to Maintain Current Investment Grade Credit Ratings MLP Funding Vehicle

Expected EBITDA and Dividend Growth Driven by Net Investment Growth

A Compelling Investment Proposition

50

Closing Remarks

Bob Skaggs

President & Chief Executive Officer

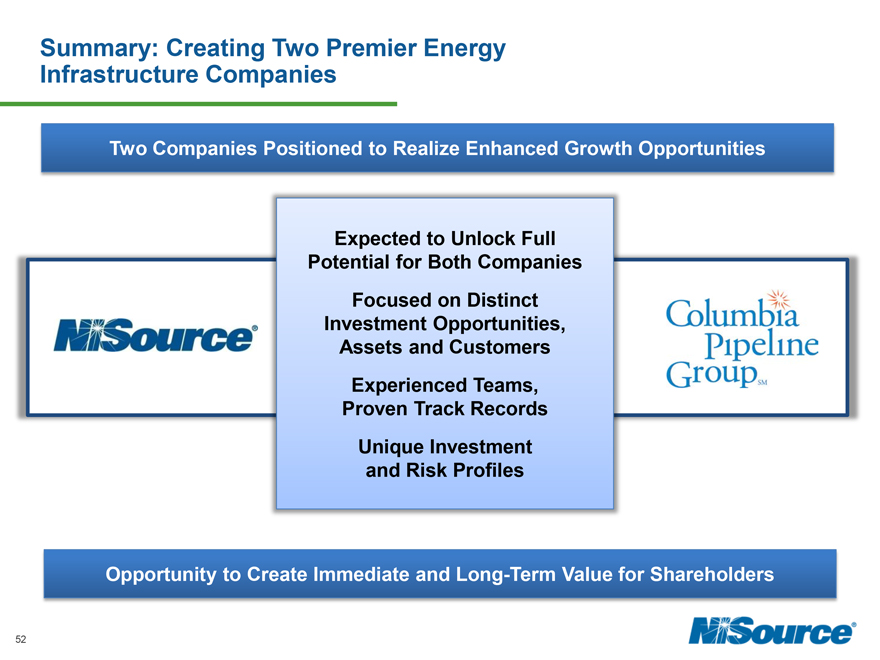

Summary: Creating Two Premier Energy Infrastructure Companies

Two Companies Positioned to Realize Enhanced Growth Opportunities

Expected to Unlock Full Potential for Both Companies Focused on Distinct Investment Opportunities, Assets and Customers Experienced Teams, Proven Track Records Unique Investment and Risk Profiles

Opportunity to Create Immediate and Long-Term Value for Shareholders

52