Worldwide Energy & Manufacturing USA Inactive

Filed: 19 Aug 09, 12:00am

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K/A

(Amendment no. 1)

[X] ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2008

[ ] TRANSITION REPORT PURSUANT TO SECTION 13OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from to ______

WORLDWIDE ENERGY AND MANUFACTURING USA, INC.

(Exact name of registrant as specified in its charter)

Colorado |

| 77-0423745 |

(State or other jurisdiction of incorporation or organization) |

| (I.R.S. Employer Identification No.) |

|

|

|

408 N. Canal Street |

| |

South San Francisco, California | 94080 | |

(Address of principal executive offices) | (Zip Code) | |

Registrant’s telephone number, including area code: (650) 794-9888

Securities registered pursuant to Section 12(b) of the Act:

None

Securities registered pursuant to Section 12(g) of the Act:

Common Stock, no par value

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes _ NoX

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes _ NoX

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. YesX No _

- - 1 - -

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. Yes __ NoX

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer

___

Accelerated filer ____

Non-accelerated filer__ (Do not check if a smaller reporting company) Smaller reporting companyX

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ___ NoX

State the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter.

The aggregate market value of the voting stock held by non-affiliates of the registrant as of

March 31, 2009 is approximately $5,855,944.

(APPLICABLE ONLY TO CORPORATE REGISTRANTS)

Indicate the number of shares outstanding of each of the registrant’s classes of common stock, as of the latest practicable date:

As of March 31, 2009, the registrant has 3,493,512 shares of common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE: NONE

EXPLANATORY NOTE

On August 10, 2009, the management of Worldwide Energy and Manufacturing USA, Inc. concluded that its financial statements for the year ended December 31, 2008, which are included in its Form 10-K for the year ended December 31, 2008, did not properly account for certain items as of December 31, 2008 and for the year then ended in accordance with United States generally accepted accounting principles, and, as a result, the accompanying financial statements have been restated..

.

- - 2 - -

WORLDWIDE ENERGY AND MANUFACTURING USA, INC.

2008 ANNUAL REPORT ON FORM 10-K

INDEX

PART I

- 4 -

Item 1. Business

- 4 -

General

- 7 -

Item 1B. Unresolved Staff Comments

- 12 -

Item 2. Properties

- 12 -

Item 3. Legal Proceedings

- 13 -

Item 4. Submission of Matters to a Vote of Security Holders

- 13 -

PART II

- 14 -

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities & nbsp; - 14 - -

Item 6. Selected Financial Data

- 15 -

Summary Consolidated Financial Data

- 15 -

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations.

- 16 -

Tabular disclosure of contractual obligations

- 23 -

Item 7A. Quantitative and Qualitative Disclosure About Market Risk

- 25 -

Item 8. Financial Statements and Supplementary Data

- 25 -

Index to Consolidated Financial Statements

- 26 -

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

- 27 -

Item 9.

Changes in and Disagreements With Accountants on Accounting and Financial Disclosure

59

Item 9A. Controls and Procedures

60

Item 9B. Other Information

61

PART III

62

Item 10. Directors, Executive Officers and Corporate Governance.

62

Item 11. Executive Compensation

64

Item 12. Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters.

65

Item 13. Certain Relationships and Related Transactions, and Director Independence.

66

Item 14. Principal Accounting Fees and Services.

67

Item 15. Exhibits, Financial Statement Schedules.

68

SIGNATURES

70

- - 3 - -

PART I

Item 1. Business

When used in this Form 10-K, the words “expects,” “anticipates,” “estimates” and similar expressions are intended to identify forward-looking statements. Such statements are subject to risks and uncertainties, including those set forth below under “Risks and Uncertainties,” that could cause actual results to differ materially from those projected. These forward-looking statements speak only as of the date hereof. Worldwide expressly disclaims any obligation or undertaking to release publicly any updates or revisions to any forward-looking statements contained herein to reflect any change in the Company’s expectations with regard thereto or any change in events, conditions or circumstances on which any statement is based. This discussion should be read together with the financial statements and other financial information included in this Form 10-KSB.

Background

Worldwide was incorporated under the laws of the State of Colorado on March 17, 2000, under the name of Tabatha III, Inc. We changed our name to Worldwide Manufacturing USA, Inc. on November 4, 2003. On February 4, 2008 we changed our name to Worldwide Energy and Manufacturing USA, Inc. to better reflect our business plan to engage in the solar module market. We were formed as a “blind pool” or “blank check” company whose business plan was to seek to acquire a business opportunity through completion of a merger, exchange of stock, or other similar type of transaction. In furtherance of our business plan, we voluntarily elected to become subject to the periodic reporting obligations of the Securities Exchange Act of 1934 by filing a registration statement on Form 10-SB.

Prior to our identification of Worldwide Manufacturing USA, Inc., a privately held California corporation (“Worldwide USA”) as an acquisition target, our only business activities were the organizational activities described above, including the filing of a registration statement on Form SB-2 under the Securities Exchange Act of 1934, and our efforts to locate a suitable business opportunity for acquisition.

On September 30, 2003, we acquired all of the issued and outstanding common stock of Worldwide USA in a share exchange transaction. We issued 27,900,000 shares of common stock in the share exchange transaction for 100%, or 10,000, of the issued and outstanding shares of Worldwide USA’s common stock. As a result of the share exchange transaction, Worldwide USA became our wholly owned subsidiary.

The former stockholders of Worldwide USA acquired 93% of our issued and outstanding common stock as a result of the completion of the share exchange transaction. Therefore, although Worldwide USA became our wholly owned subsidiary, the transaction was accounted for as a recapitalization of Worldwide USA, whereby Worldwide USA is deemed to be the accounting acquirer and is deemed to have adopted our capital structure. No finder’s fee was paid to any person in connection with the transaction.

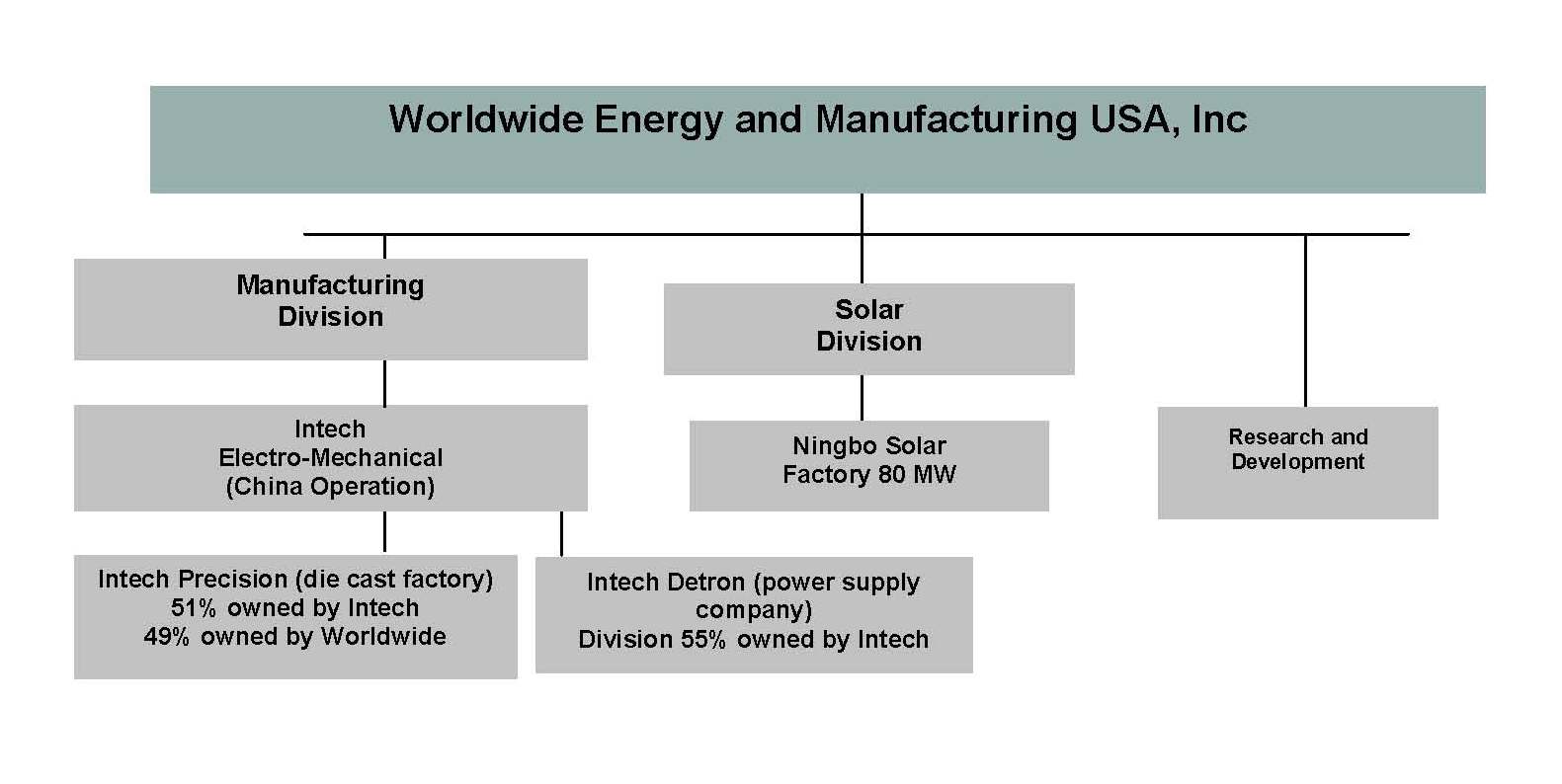

All operating activities are carried out through Worldwide USA and our subsidiaries located in Shanghai and Ningbo, China which include: (1) Worldwide USA’s wholly owned subsidiary, Shanghai Intech Electro-Mechanical Products Co., Ltd. (“Intech”). Intech was incorporated as a

- - 4 - -

United States subsidiary doing business in China, and registered in the city of Shanghai, China, in 1997. This unit is the quality assurance arm and engineering division and produces various types of electrical components and assemblies; (2) Shanghai Intech Precision Mechanical Products Ltd. (“Precision”) manufactures die-casting and machined parts for the automotive, telecommunications and home supply industries; (3) Shanghai Intech-Detron Electric and Electronic Company Limited, (“Detron”), which produces power supply units and has research and development capabilities and (4) Ningbo Solar Factory (“Ningbo”). This factory produces solar modules whose customers are primarily in Europe and South Korea. Besides producing the products listed above, Worldwide contracts with factories in China to produce a wide variety of components and assemblies.

Worldwide’s factories employ approximately 450 workers in China. Intech, Worldwide’s quality assurance arm located in Shanghai, China employs 33 engineers. As the engineering division and quality assurance arm of the Company, Intech provides technical advice, design, delivery, material procurement and manufacturing quality control services to companies in the United States seeking to manufacture or purchase components from manufacturers in China. Worldwide’s manufacturing operations are located in China and its sales and headquarters are located in the state of California.

In 2005, the Company began to make the transition from being an engineering and contract manufacturing firm which depended completely on subcontractors to becoming a direct manufacturer. In the beginning of 2005 we did not own any of our own factories and used as our suppliers of material and labor approximately 100 factories in China, mostly from Shanghai or the surrounding area.

On August 18, 2005, Worldwide established its own electronics manufacturing division located in Shanghai, PRC. Worldwide purchased approximately $250,000 worth of electronics production equipment from Opel Technology, a former Worldwide electronics supplier, as the initial manufacturing equipment. In establishing this electronics factory, Worldwide has been able to compete more effectively in the PC board and cable assembly industry, as well as gain complete control over its electronics components production. The Company established Shanghai Intech Precision Mechanical Products Manufacturing Ltd. (“Precision”) on November 1, 2005. Precision is 51% owned by Intech and 49% owned by Worldwide. This factory performs die-casting and machining services for the automotive, motorcycle, telecommunications and home supply industries. Precision is located in the suburbs of Shanghai, PRC, and occupies an area of approximately 71,043 square feet. The factory contains three workshops: a die-casting shop, a machining shop, and a printing shop.

In February 2008 Worldwide established a solar division that focuses on photovoltaic module technology under the brand name of “AmeriSolar.” Worldwide issued 300,000 restricted shares for the AmeriSolar brand name. This division generated $30,999,962 in sales for the period ending December 31, 2008.

On October 14, 2008, Worldwide, through Intech, completed the acquisition of 55% of Shanghai De Hong Electric and Electronic Company Limited (“De Hong”). The terms of the Agreement dated February 3, 2008 were that Intech paid cash consideration of approximately $1 million dollars for a 55% interest in DeHong in two installments, with the first installment of $714,286.00 being paid on October 10, 2008, and the second installment of $285,714 being paid no later than December 15, 2008. The Company funded the acquisition with some of the proceeds from its sale of 1,055,103 ($4,747,970) shares of unregistered common stock on June 23, 2008. Shanghai De

- - 5 - -

Hong Electric and Electronic Company is the holding company for the operating subsidiary Shanghai Intech -Detron Electronic Co. (“Detron”). Therefore, Worldwide received 55% control of the operating subsidiary Shanghai Intech-Detron Electric and Electronic Company Limited (“Detron”). Detron’s management remained in place.

Detron is a power supply factory in Shanghai, China with design and R & D capabilities. Detron���s revenues were about $6.1million for the twelve months ended December 31, 2008, and

$ 4.1for the twelve months ended December 31, 2007.

Through these acquisition and establishment of our solar division our corporate structure is depicted as follows:

- - 6 - -

General

Worldwide USA, together with its Chinese subsidiaries, is a contract manufacturer, engineering firm and direct manufacturer. A contract manufacturer supplies components and assemblies, either through direct manufacturing or through sub contracting to other manufacturers, according to the customers’ designs, drawings and quality criteria. When utilizing our subcontractors, they will provide the plant, equipment, manufacturing working capital and factory labor and Worldwide provides the sales, management, production control and technical support for the products. Worldwide’s goal is to provide timely delivery and high quality components at manufacturing costs less than what Worldwide’s customers would pay for similar parts in the United States. Worldwide’s website address iswww.wwmusa.com.

Worldwide provides its services to several companies in the United States, Europe and South Korea primarily in the solar module, aerospace, automotive, and electronics industries. Although Worldwide historically focused on manufacturing components for high tech industries, in 2008 the Company expanded into the solar module markets. Worldwide’s CEO, Jimmy Wang, realizes that the solar module industry provided Worldwide with a unique opportunity to use its core strength of providing high quality components and assemblies, with timely delivery, to develop a solar module team capable of successfully entering the solar module markets. The Company’s solar module brand “AmeriSolar” has already earned numerous quality certifications including IEC612215, TUV, CE and has recently applied for the UL certification. These solar modules meet or exceed all industry norms for performance, quality and functional life in the field.

With respect to its contract manufacturing business, Worldwide has the ability to arrange for the manufacture of products, parts, and components for a broad number of industries and customers. In order to ensure a consistently high quality product, it is imperative for a company in the contract manufacturing business to have a local quality assurance team. The team’s responsibility is to institute quality assurance procedures that ensure the quality of products from start to finish. This function is carried out through Worldwide’s wholly owned subsidiary, Intech.

Worldwide sells to its customers under purchase orders. We have only a few long-term contracts with customers. As a result, it is difficult to forecast revenues, and planning for future operations is also difficult. Because many of our costs and operating expenses are fixed, any unforeseen reduction in purchase orders can affect our gross margin and operating income.

Worldwide employs rigid quality assurance procedures, product enhancements and strict testing of its products to attract customers. Other than rigid quality controls and timely delivery, another important factor in attracting customers from the United States is our Kanban program. The Kanban program is an inventory system that stocks at least one month’s supply of inventory needed to meet the various customers’ demand. Thus, if Worldwide receives a contract with a scheduled six months or more of deliveries, we will stock at least one month’s inventory in the California warehouse, or a warehouse that is close to the customer’s facility so a twenty-four hour delivery turn-around may be accomplished. This process of stocking at least one month’s worth of inventory is maintained until the entire contract is completed. We have won many new customers as a result of the Kanban inventory program. Using Kanban inventory controls allows us to help customers meet challenges with working capital returns, and the need to have supply products necessary to complete manufacturing of those parts in a shorter period of time.

- - 7 - -

Worldwide manages the entire production of its customers’ products. Worldwide’s engineers maintain the highest levels of quality by supervising all aspects of the manufacturing process. Worldwide’s engineers write the production and inspection procedures, obtain the materials, audit and perform all of the in-progress and final inspections.

All of Worldwide’s active subcontractors have received ISO 9000 certifications. ISO-9000 certifications are issued by the International Organization for Standardization and represents the approval of the manufactures quality system and the application of said quality system to the production processes. These certifications are issued to each factory after its management receives the prerequisite training and is verified by periodic audits.

The unique business relationships between Worldwide and its subcontractors allow Worldwide to offer its customers lower manufacturing costs, and at the same time maintain high standards of quality and timely delivery schedules.

Worldwide’s success stems from the following factors for both direct manufacturing and outsourcing of its production service:

Worldwide has a wide range of manufacturing capability as a result of:

-

offering, through subcontractor and our own factories, many of manufacturing processes required for our customers components and assemblies,

-

providing engineering services to interact with the various factories, and

-

coordinating and planning for complete turn-key assemblies.

Worldwide’s quality control is highly effective as a result of:

-

setting inspection criterion for manufacturers based on the customers’ quality criteria,

-

conducting material auditing, in process inspection, and the final inspection, and

-

providing incentive-reward packages to Worldwide’s quality control employees.

Worldwide’s quick turn-around time compared with other offshore suppliers is ensured by:

-

committing 60-75 days for completing complicated tooling and two to six weeks for basic tooling;

-

committing 30-60 days for first delivery, and seven days for the deliveries afterwards, and

-

our team in China is continually monitoring production progress.

Worldwide offers:

-

competitive prices,

-

significant flexibility towards customers’ needs,

-

local team to perform quality assurance functions,

-

the Kanban inventory for 24-hour delivery for its contract parts, and

-

quick responses to customer questions and concerns.

Additionally, Worldwide has a customer reception office at its Shanghai subsidiary, which makes arrangements for its customers’ airline tickets and hotels at a discounted rate, along with providing

- - 8 - -

local transportation and language interpretation during customer visits.

Worldwide is able to provide its customers with considerable cost advantages while eliminating the disadvantages of quality and delivery issues frequently experienced by companies which have direct contracts with manufacturers in China.

Since Worldwide primarily employs engineers and engages a broad variety of subcontractors, Worldwide is able to manufacture parts for a broad range of industries. As demand for manufacturing slows for a particular product, industry or sector, Worldwide is able to remain flexible as a result of its being in a position to pursue opportunities to manufacture other products. There are no special governmental regulations or governmental approvals with respect to our business.

Suppliers and Customers

In 2008, our six largest customers were: Pramac Swiss SA, Enesystem Inc, Provent Solarpark, Pvline Gmbh and Schueco International KG; accounting for 72% of our consolidated business. In 2007 Joslyn Sunbank, Joslyn Manufacturing, Radio Waves Corp and Teleflex Electrical, GE Transportation and Pacific Scientific-CA accounted for approximately 48% of consolidated net sales. The shift in our top customers was the result of the Company’s 2008 entry into solar module markets, where we experienced the majority of our sales.

Our five largest suppliers in 2008 were Changzhou Trina Solar Energy, Zhejiang Shuqimeng Photo Voltaic, Jiangsu Aide Solar Energy Technology Co., Jiangyin Hareon Power Co., Ltd. and Baoding Tianwei Yingli New Energy Resource. These represented approximately $23 million of our purchases from external suppliers, or approximately 75% of materials purchased by the Company. In 2007, our two largest material suppliers were Shanghai Huanxinnuo Electro-Mechanical Products Company (formerly named Shanghai Xinli Trading Company Ltd.) and Shanghai Machine Tool Co. Ltd. They accounted for $573,328 or 6.8% and $724,891 or 8.6% respectively, of the total materials purchased by Worldwide. The shift in our top suppliers was also the result of the Company’s focus on the solar module industry.

Competition

Worldwide strives to ensure quality and provide low cost to customers so that it can remain competitive. The solar module industry and the contract manufacturing service industry remain strongly competitive. There are hundreds of companies, many larger than Worldwide, that have substantially greater manufacturing, financial, research and development, engineering and marketing resources. Worldwide is a small competitor in these multi-billion dollar industries for both solar modules and contract manufacturing. If overall demand for solar modules and contract manufacturing services should decrease, this could result in substantial pricing pressure, which would negatively affect revenue and net profit for Worldwide.

- - 9 - -

Employees

Worldwide currently employs approximately 450 employees, including 33 staff engineers and 12 administrative personnel at Worldwide’s wholly owned subsidiary Intech in Shanghai, China and 400 employees who work at our factories in China. The remaining 13 employees work at the California office in South San Francisco. Five of these employees are in sales with the remaining eight employees working in support and administrative roles. All employees are full time.

Item 1A. Risk Factors

THE SHARES OF WORLDWIDE ARE SPECULATIVE AND INVOLVE A HIGH DEGREE OF RISK INCLUDING THE COMPREHENSIVE DISCUSSION OF MATERIAL RISK FACTORS DESCRIBED BELOW. EACH PROSPECTIVE INVESTOR SHOULD CAREFULLY CONSIDER THE FOLLOWING RISK FACTORS INHERENT IN AND AFFECTING THE BUSINESS OF THE COMPANY BEFORE MAKING AN INVESTMENT DECISION.

1. Resale of our securities may be difficult because there may not be sufficient market activity to provide liquidity of the Company’s shares.

There is no assurance that the market for the Company’s shares will be maintained or that it will be sufficiently active or liquid to allow stockholders to easily dispose of their shares.

2. Because we work under short-term contracts, it is very difficult to forecast our operational and cash needs.

Contract manufacturing service providers must provide increasingly rapid product turnaround for their customers. We generally do not obtain firm long-term purchase commitments from our customers. Customers may cancel their orders, change production quantities, or delay production because of consumer demand or technological changes; however, we are often obligated to expend significant amounts for retooling or other start-up costs of manufacturing. Any costs due to cancellations, reductions, customer returns and/or delays by a significant customer or by a group of customers might not be recoverable. The loss could be greater than our projected profit on the contract, resulting in a net loss for the contract. The short-term nature of our customers’ commitments and the possibility of rapid changes in demand for their products reduce our ability to estimate accurately future customer requirements. On occasion, customers may require rapid increases in production, which can stress our resources and reduce margins. Although we have several manufacturing facilities in China that we do business with, there can be no assurances we will have sufficient capacity at any given time to meet our customers’ demands. We could lose orders or fail to complete orders in a timely manner. In addition, because many of our costs and operating expenses are relatively fixed, any reduction in customer demand can adversely affect our gross margins and operating income.

3. A few customers and contract manufacturers account for a large percentage of our business. Therefore, the loss of any one customer or contract manufacturers could reduce our sales significantly or impede our ability to comply with our manufacturing contracts, respectively.

- - 10 - -

In 2008 our six largest customers, Pramac Swiss SA, Enesystem Inc., Provent Solarpark, Pvline Gmbh, and Schueco International KG accounted for 72% of our consolidated business. In 2007, Joslyn Sunbank, Joslyn Manufacturing, Radiowaves Corporation, Teleflex Electrical, GE Transportation and Pacific Scientific accounted for approximately 48% of our consolidated net sales. Our five largest suppliers in 2008 were: Changzhou Trina Solar Energy, Zhejiang Shuqimeng Photo Voltaic, Jiangsu Aide Solar Energy Technology Co, Jiangyin Hareon Power Co., Ltd. and Baoding Tianwei Yingli New Energy Resource. These represented approximately $23 million of our purchases from external suppliers, or approximately 75% of materials purchased by the Company. In 2007, our two largest material suppliers were Shanghai Huanxinnuo Electro-Mechanical Products Company (formerly named Shanghai Xinli Trading Company Ltd.) and Shanghai Machine Tool Co. Ltd. Together they accounted for $573,328 or 6.8% and $724,891 or 8.6% respectively of the total materials purchased by Worldwide. The loss of any one customer could significantly reduce our sales. The loss of one contract manufacturer could cause delays in our performance of contracts or reduce our gross margin if a substitute manufacturer could not deliver on time or at the same contract price.

4. Taxing authorities could modify our tax exemptions or challenge our tax allocations and require us to pay more taxes.

Our operations are predominantly located in China, where tax incentives have been extended to encourage foreign investment. Our effective tax rate could increase if these tax incentives are not renewed upon expiration or tax rates applicable to us are increased. Tax authorities in jurisdictions in the United States could challenge the manner in which profits are allocated between US and Chinese subsidiaries and if we do not prevail in any such challenge we will be required to pay more taxes

5. Unforeseen changes in suppliers can result in losses of tooling deposits and other pre-production costs.

In most cases the tool, die, or mold from which a part is made is paid for and owned by the customer, and is designed for a specific customer. We require our customers to provide a non-refundable down payment to cover tooling costs, including pre-production machine set-up costs. In the event that a supplier is unable to fulfill its production agreements with us, management believes that other suppliers can be found. However, a change in suppliers would cause a delay in the production process and could result in loss of tooling deposits and other supplier advances, causing Worldwide to not comply with the timely delivery requirements of our contract with our customer, and loss of tooling deposits will reduce our gross margin on the contract.

6. Doing business in China is subject to legal risks and political and economic changes over which we have no control.

Under its current leadership, the Chinese government has been pursuing economic reform policies. Changes in these policies or political instability could affect our ability to operate, to repatriate funds from China, or increase our costs of doing business or our tax rate. Even though the United States has granted a most favored nation status to China, this could be revoked or retaliatory tariffs could make the import of our products prohibitively expensive. The Chinese government could change its policies toward private enterprise or even nationalize or expropriate private enterprises, which could result in the total loss of our investment in that country.

- - 11 - -

We periodically enter into agreements governed by Chinese law. Unlike the United States, China has a civil law system based on written statutes in which judicial decisions have little precedential value. The Chinese government has enacted some laws and regulations dealing with matters such as corporate organization and governance, foreign investment, commerce, taxation and trade. However, the government’s experience in implementing, interpreting and enforcing these recently enacted laws and regulations is limited, and our ability to enforce commercial claims or to resolve commercial disputes is uncertain. Furthermore, enforcement of the laws and regulations may be subject to the exercise of considerable discretion by agencies of the Chinese government, and forces unrelated to the legal merits of a particular matter or dispute may influence their determination. These uncertainties mean that we cannot rely on legal protections to ensure that suppliers honor their contracts with us. If we suffer a loss because of breach of contract by a Chinese supplier, we might not be able to recover the loss.

7. Currency fluctuations can cause us significant losses.

Some of our costs such as payroll, material and equipment costs are denominated in Chinese Renminbi. In addition, most of our solar module customers pay in Euros. Changes in the exchange rate between the Renminbi, Euros and the U.S. dollar will affect our costs of sales and operating margins.

Item 1B. Unresolved Staff Comments

Not applicable.

Item 2. Properties

On June 1, 2008, Worldwide entered into a 61-month lease for 9,680 square feet of office/ warehouse space located at 408 N canal Street, South San Francisco, California. The rent per month is $10,164 with rent increasing three percent each year. The rent for 2008 was $60,984, and the lease expires on May 31, 2013. On June 1, 2008, Shanghai Intech, the Company’s quality control division, entered into a one-year lease expiring June 1, 2009 for $3,998 per month. Additionally, the rent for our electronics factory is $1,496 per month and expires March 14, 2010. The total square feet for Intech's operations is 13,265. Shanghai Intech Precision (our die-cast factory) pays rent of $1,460 per month, which includes 71,043 square feet. The lease expires March 14, 2010. In addition, Worldwide has leased a 129,167 square foot facility in Ningbo, China. The lease term is from July 18, 2008 to July 17, 2013.This facility houses the production operations and R&D center for the Company’s solar division. The rent is approximately $17,600 per month; the first three months were free.

The following is a tabular description of our lease obligations:

Company | Lease Term | Square Feet | Monthly Rent | 2008 rent | Expected 2009 rent |

Worldwide (California headquarters warehouse) | June 1, 2008 to May 31, 2013 | 9,680 | $10,164 (increase of 3% per year) | $60,984 | $121,968 |

- - 12 - -

Shanghai Intech Electro-Mechanical Products Co., Ltd. | June 1, 2008 to June 1, 2009 | 13,165 | $3,998 | $23,988 | $23,988, per current lease terms |

Shanghai Intech-Detron Electric and Electronic Company Limited | Expires March 14, 2010 | 19,375 | $1,496 |

| $17,952 |

Shanghai Intech Precision Mechanical Products Ltd. | Expires March 14, 2010 | 71,043 | $1,460 |

| $17,520 |

Ningbo Solar Factory | July 18, 2008 to July 17, 2013 | 129,167 | $17,600 |

| $211,200 |

Item 3. Legal Proceedings

Not applicable.

Item 4. Submission of Matters to a Vote of Security Holders

No matters were submitted to a vote of security holders during the fourth quarter of the fiscal year ended December 31, 2008.

- - 13 - -

PART II

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

Market Information

Our stock is quoted on the OTC Bulletin Board under the symbol “WEMU.” Worldwide began trading on June 1, 2004. The stock symbol was changed on February 25, 2008 as a result of a name change from Worldwide Manufacturing USA, Inc. to Worldwide Energy and Manufacturing USA, Inc. There are 3,509,512 shares outstanding. The Company recently applied for listing on the NASDAQ Capital Market. The Company believes it meets all of the necessary requirements with the exception of a bid price of $4.00. The below table provides the average low and high bid and ask prices for the preceding quarters of 2008.

Year ended December 31, 2008 | ||

|

|

|

| BID | ASK |

1st QTR | $ 7.37 | $9.74 |

2nd QTR | $6.58 | $9.05 |

3rd QTR | $5.54 | $7.69 |

4th QTR | $3.36 | $5.58 |

|

|

|

| Year ended December 31, 2007 | |

|

|

|

| BID | ASK |

1st QTR | $ 2.50 | $8.00 |

2nd QTR | $4.90 | $5.80 |

3rd QTR | $4.00 | $5.70 |

4th QTR | $4.85 | $9.00 |

(b)

Stockholders of Record

As of December 31, 2008, there were approximately 317 stockholders of record.

(c)

Dividends

The Company paid no dividends in 2008. The Company may or may not pay dividends in the future depending on Company performance.

(d)

Equity Compensation Plans

Worldwide established a stock option plan for its employees on April 1, 2004 in order to attract and retain qualified employees on behalf of the Company, as well as provide employees with an opportunity to participate in the growth of the Company. Worldwide approved the authorization of 300,000 shares. As of December 31, 2008, no option shares have been exercised under this plan. The 2004 Stock Option Plan provides the opportunity for employees to purchase shares at $6.00.

- - 14 - -

As of March 31, 2009, 131,292 option shares have been granted at an option price of $6.00.

Item 6. Selected Financial Data

Summary Consolidated Financial Data

The following summary of consolidated statements of income data for the years ended December 31, 2008, 2007, 2006 and 2005 and the selected consolidated balance sheet data as of the years ended December 31, 2008, 2007, 2006 and 2005 are derived from, and are qualified by reference to, the audited consolidated financial statements of Worldwide that have been audited by Child, Van Wagoner & Bradshaw, PLLC, independent registered public accounting firms, and that are included elsewhere in this report.

The following summary of consolidated financial information should be read in conjunction with our consolidated financial statements and related notes and the information contained in “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” appearing elsewhere in this report. Our historical results are not necessarily indicative of our results for any future periods.

(In U.S. dollars, except per share data)

|

|

| December 31, 2008 (restated) |

| December 31, 2007 |

| December 31, 2006 |

| December 31, 2005 |

| December 31, 2004 |

| December 31, 2003 |

| ||||||||||||||

| Statement of Income Data |

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||

| Revenues | $ | 45,913,957 | $ | 12,132,710 | $ | 11,409,300 | $ | 8,713,431 | $ | 6,700,593 | $ | 5,999,630 |

| ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||

| Cost of Sales | $ | 39,746,286 | $ | 8,350,621 | $ | 8,022,875 | $ | 5,911,417 | $ | 4,153,368 | $ | 4,051,225 |

| ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||

| Operating Expenses | $ | 4,389,883 | $ | 3,086,327 | $ | 2,183,056 | $ | 2,285,085 | $ | 1,777,379 | $ | 1,948,405 |

| ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||

| Income From Operations | $ | 1,777,788 | $ | 695,762 | $ | 1,203,369 | $ | 516,929 | $ | 769,846 | $ | 520,777 |

| ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||

| Income Taxes | $ | (284,278) | $ | 65,726 | $ | 38,937 | $ | 1,700 | $ | 256,492 | $ | 38,500 |

| ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||

| Net Income | $ | 1,001,648 | $ | 575,674 | $ | 969,429 | $ | 581,166 | $ | 521,486 | $ | 540,872 |

| ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||

| Number of Shares Issued and Outstanding |

| 3,493,512 |

| 2,047,363 |

| 2,030,863 |

| 2,024,002 |

| 2,011,842 |

| 2,000,000 |

| ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||

| Income from Operations Per Share |

| .65 |

| .34 |

| .59 |

| .26 |

| .38 |

| .26 |

| ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||

| Weighted Average Number of Shares Outstanding |

| 2,731,995 |

| 2,035,495 |

| 2,030,863 |

| 2,024,002 |

| 2,011,842 |

| 2,000,000 |

| ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||

| Net Income Per Share |

| .37 |

| .28 |

| .48 |

| .29 |

| .26 |

| .27 |

| ||||||||||||||

- - 15 - -

|

| December 31, 2008 |

| December 31, 2007 |

| December 31, 2006 |

| December 31, 2005 |

| December 31, 2004 |

| December 31, 2003 |

| |||||||||||||||

Balance Sheet Data |

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||

Current Assets | $ | 14,660,221 |

| 8,210,711 | $ | 6,599,094 | $ | 4,916,119 | $ | 2,199,978 | $ | 1,760,468 |

| |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||

Total Assets | $ | 19,133,009 |

| 8,762,841 | $ | 7,127,847 | $ | 5,427,736 | $ | 2,621,760 | $ | 2,562,792 |

| |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||

Total Current Liabilities | $ | 7,125,493 |

| 4,447,946 | $ | 3,562,899 | $ | 2,773,935 | $ | 1,311,219 | $ | 1,751,211 |

| |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||

Total Long-Term Liabilities | $ | 997,099 |

| 498,812 | $ | 522,024 | $ | 1,268 | $ | 16,827 | $ | 174,353 |

| |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||

Total Shareholders’ Equity | $ | 10,397,778 |

| 3,816,083 | $ | 3,042,924 | $ | 1,942,573 | $ | 1,293,714 | $ | 637,228 |

| |||||||||||||||

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations.

Certain statements in this report, which are not statements of historical fact, are what are known as “forward-looking statements,” which are basically statements about the future. For that reason, these statements involve risk and uncertainty since no one can accurately predict the future. Words such as “plans,” “intends,” “hopes,” “seeks,” “anticipates,” “expects, “and the like, often identify such forward looking statements, but are not the only indication that a statement is a forward-looking statement. Such forward-looking statements include statements concerning our plans and objectives with respect to our present and future operations, and statements, which express or imply that such present and future operations will or may produce revenues, income or profits. In evaluating these forward-looking statements, you should consider various factors, including those described in this report under the heading “Risk Factors” in Part I, Item 1A. These and other factors may cause our actual results to differ materially from any forward- looking statement. We caution you not to place undue reliance on these forward-looking statements. Although we base these forward-looking statements on our expectations, assumptions, and projections about future events, actual events and results may differ materially, and our expectations, assumptions, and projections may prove to be inaccurate. The forward-looking statements speak only as of the date hereof, and we expressly disclaim any obligation to publicly release the results of any revisions to these forward-looking statements to reflect events or circumstances after the date of this filing.

- - 16 - -

Overview

We are an engineering, contract manufacturing and direct manufacturing Company, primarily servicing customers in Europe and South Korea for our solar modules and United States companies that outsource their smaller scale production orders for offshore production in China. From our inception in 1993 until 2005, we were strictly an intermediary or “middleman,” working with our customers and our subcontractors to assure that our customers received high quality components on a timely basis. While we still subcontract a significant portion of our business, since 2005 we have begun the transition to becoming a direct contract manufacturer, operating several of our own factories. Recently, we announced two additional factories, allowing us to become a direct manufacturer for solar modules and for power supply units as described below:

In February of 2008, Worldwide established a solar division that focuses on photovoltaic module technology under the brand name of “AmeriSolar.” On February 4, 2008, the Company changed its name from Worldwide Manufacturing USA, Inc. to Worldwide Energy and Manufacturing USA, Inc. in order to reflect its expansion into the solar energy industry. The Company issued 300,000 restricted shares for the AmeriSolar brand name.Worldwide then leased a 129,167 square foot facility in Ningbo, China. The lease term is from July 18, 2008 to July 17, 2013.This facility houses the production operations and R&D center for the Company’s solar division. This factory has the capability of producing 80MW in solar modules per year, which translates into approximately $224 million in revenues at full capacity, based on current prices. By opening this factory we hope to increase gross and net margins in our solar division. Furthermore, it will help us through the R&D department to continue to improve, develop and enhance our solar modules. We will continue to explore opportunities as well as expand our solar sales and distribution in the United States and Latin America. We currently sell our solar modules in Europe and South Korea. Our research shows that the United States has an abundance of solar rebate programs for both the commercial and residential markets at the local, state and federal level. We feel we are well positioned to sell our modules to large institutions in the U.S.This division generated $30,999,962 in sales for period ending December 31, 2008.

On October 14, 2008, Worldwide completed the acquisition of 55% of Shanghai De Hong Electric and Electronic Company Limited (“De Hong”) through acquiring 55% of the outstanding capital stock of De Hong, a Chinese corporation, through Worldwide’s wholly owned subsidiary Intech Electro-Mechanical Products Co., Ltd., a China corporation (“Intech”). The terms of the Agreement dated February 3, 2008 were that Intech paid cash consideration of approximately $1 million dollars for a 55% interest in DeHong in two installments with the first installment of $714,286 being paid within three months of receiving the business license which occurred on October 10, 2008 and the second installment of $285,714 being paid no later than December 15, 2008. The Company funded the acquisition with some of the proceeds from the sale of 1,055,103 shares of its common stock, or $4,747,970, on June 23, 2008. Shanghai De Hong Electric and Electronic Company is the holding company for the operating subsidiary Shanghai Intech - -Detron Electronic Co. (“Detron”).

Therefore, Worldwide received 55% control of the operating subsidiary Shanghai Intech-Detron Electric and Electronic Company Limited (“Detron”). Detron is a power supply factory in Shanghai, China with designing and R & D capabilities. Detron’s revenues were about $6.17 million for the twelve months ended December 31, 2008, and $ 4.1 million for the twelve months ended December 31, 2007.

- - 17 - -

We made the transition to become a direct manufacturer in several product areas because we felt that as a contract manufacturer we were constrained in our growth. Many Fortune 500 and other large companies either cannot or choose not to work with contract manufacturers, preferring to go directly to the source that can manufacture the product and thereby avoid the additional expense of a middleman. This is particularly true for very large orders where the added cost of a middleman can have a material impact on the customer’s bottom line. As a result, our revenues have for the most part been limited to smaller scale production orders placed by companies that are not among the largest companies in the United States or elsewhere. Additionally, as a middleman we must share any potential gross profit with the subcontracting factory. Therefore, our customers are generally smaller, the orders they place are smaller, and the income and profit we can generate from those orders is of necessity limited because we are not directly manufacturing the products. On the other hand, when we subcontract the actual manufacturing of our customers’ products and components, we do not need to hire factory employees, purchase materials, purchase and maintain manufacturing equipment or incur the costs of the manufacturing facilities. To some extent, these costs are built into the price charged by our subcontractors, but if we do not place orders, we do not incur those costs.

Our management has carefully considered these factors and during 2005 made the strategic decision to move our Company away from our historical complete reliance on subcontractors. At the beginning of 2005 we did not own any of our own factories and used as our suppliers of materials and labor approximately 100 factories in China, mostly in Shanghai or the surrounding area. During the first quarter of 2005, we acquired the assets of Chengde, a factory that manufactures automobile air conditioning units. We discontinued operations of this factory in May 2008. We wanted to divest ourselves of this factory in 2008 to focus on our new business plan of entering the solar module industry; as well, as this factory failed to perform to our expectations, generating little revenue and profit in 2007 and 2008. In the year ending December 31, 2007, Chengde provided revenues of approximately $267,000 and no net income.

In the fourth quarter of 2005 we established a die-casting and machining factory through leasing an existing facility from a former supplier and initially investing approximately $500,000 to upgrade the equipment and manufacturing buildings. In these transactions we acquired assets, the expertise of the employees, the managers of the factories, and a portion of the existing customer base of those factories. In the third quarter of 2005, we also established an electronics manufacturing factory. As a result of these two continued factory operations and the recently announced new factories described above, as of December 31, 2008 we own and operate four factories that we now use for the manufacture of certain product lines that we historically had to subcontract, and we are using the services of approximately 40 subcontractors to manufacture those product lines for which we do not have our own manufacturing capabilities. The establishment of these factories, including asset purchases and factory upgrades, was funded primarily with some of the proceeds from its unregistered sales on June 23 of 1,055,103 common stock or $4,747,970. In addition, the Company had more subscriptions for the sale of an aggregate of $252,027 or 56,007 shares of common stock, which was used to help fund these new acquisitions as well as to provide additional working capital for the Company.

In 2008 our credit line was increased by approximately $775,000 from a line of credit in the amount of $2.25 million with Golden Gate Bank to $3.025 million, as a result of securing two new credit lines with Bank of the West, one for $1,025,000 and the other for $2,000,000. The credit line with

- - 18 - -

Golden Gate Bank was subsequently cancelled.In the future, we expect to continue to acquire or establish factories in China which will give us the capability to manufacture those product lines our management believes are the most profitable.

The impact of our four factory operations is as follows:

(i)

In February of 2008, Worldwide established a solar division that focuses on photovoltaic module technology under the brand name of “AmeriSolar.” For the year ended December 31, 2008, this division generated $30,999,962 in sales with a net profit of $865,860. We expect profits and revenues to increase in 2009.

(ii)

Shanghai Intech Precision Machinery Co. Ltd. generated revenues of approximately $3,887,410 and a net income of $144,000 for the year ending December 31, 2008. Revenues increased by $1,042,410 or approximately 36.6% over period ending December 31, 2007 where revenues were $2,845,000. Revenue increase as a result of increased orders from Shanghai GM. Net profit decreased from $257,000 for the year ending December 31, 2007 to $144,000 for the period ending December 31, 2008. The decrease was $113,000 or approximately 44%. This decrease in net profit was the result of renovation costs for a high capacity machine that will be placed into operation in the second half of 2009. In addition, the profit margins on GM products are less than other die-cast customers, resulting in lower margins and causing the decline in net profits.

(iii)

Shanghai Intech, the Company’s quality assurance arm and electronics factory, had revenues of approximately $6,613,502 and net income of $382,088 for the year ending December 31, 2008 compared to revenues of $5,969,000 for the year ending December 31, 2007 and net income of $287,000. Revenues increased by $644,502 or 10.8%. Additionally, net profits increased by $95,088 or 33.1%. The increase in net profit and revenues was result of continued demand from our customers. Further, the recently announced Detron acquisition will be combined with Intech’s electronics factory. This will serve to reduce overhead and streamline some of the operations. In 2008, Detron had revenues of approximately $5,401,962 and a net profit of $518,670. The acquisition was not completed until October 14, 2008; therefore, Detron’s revenue numbers and profits have little impact on Intech’s financial results.

With the continuing transition into direct manufacturing, we expect to continue to increase sales outside the United States, and in particular, increase the number of customers in the PRC and European countries with our solar modules. Our costs to establish and improve these factories and enter new market with our solar modules will increase along with sales and profits.

Through the development of our product mix, which consists of solar modules, foundry, machining and stamping, electronics and fiber optics products lines, our business has become more diverse. In the past, foundry and machining and stamping accounted for more than 90% of our business. This percentage has decreased to approximately 45% since forming our solar division and factory. We expect that the solar module business will continue to become a larger part of the Company’s

- - 19 - -

revenues and profits. For 2009, we expect solar modules sales to represent an excess of 65% of our total revenues.

Generally, our operating results have been, and will continue to be, affected by a number of factors, including the following:

| • | our customers may cancel or delay orders or change production quantities; |

|

|

|

| • | overall market conditions in the solar industry; |

|

|

|

| • | integration of acquired businesses and facilities; and |

|

|

|

| • | managing growth and changes in our operations. |

|

|

|

We also are subject to other risks, including risks associated with operating in foreign countries, changes in our tax rates, and fluctuations in currency exchange rates.

Management’s Discussion for December 31, 2008

Financial Condition

As of December 31, 2008, the current assets of Worldwide were $14,660,221 compared to current assets as of December 31, 2007 of $8,210,711. This represents an increase of $6,449,510 or approximately 78.5%. The increase in current assets was primarily the result of an increase in cash, accounts receivable, and inventory. The Company’s cash increased by $2,980,651 largely as a result of the Company’s sales in June 2008 of 1,055,103 shares of its common stock. As well, the Company had additional subscriptions for the sale of an aggregate of $252,027, or 56,007 shares of common stock. In addition, accounts receivable increased by 1,515,482 or 31.6% as a result of the Company’s sales growth. Accounts receivable were $4,790,506 for the year ending December 31, 2008 compared to $3,275,024 for the year ending December 31, 2007. The last major factor contributing to the increase in current assets was the increase in inventory of $1,421,617. Inventory was $3,754,765 for the year ending December 31, 2008 compared to $2,333,148 for the year ending December 31, 2007. Inventory increased as a result of the establishment in December of 2008 of the Ningbo Solar factory and the acquisition of Detron in October of 2008.

Current liabilities at December 31, 2008 totaled $7,125,493 compared with $4,447,946 at December 31, 2007. This represents an increase of $2,677,547 or 60.20%. The increase in current liabilities was due to an increase in accounts payable of $946,936 or 38.6% as the result of the Company’s growth. Accounts payables were $3,400,253 in December of 2008 compared to accounts payable of $2,453,317 in December of 2007. The other major contributor to the increase in current liabilities was liabilities due to our recent acquisition of Detron in October of 2008, which amounted to $1,243,024.

Total assets were $ 19,133,009 for the year ended December 31, 2008 compared to $8,762,841 for the year ended December 31, 2007. The increase of $10,370,168 or approximately 118.3% was the result of the following factors: (1) sale of unregistered securities for $4,597,587; (2) the acquisition of Detron, and the establishment of the new solar factory in Ningbo, China. This resulted in increases in property plant and equipment of $808,045. (3) Property, Plant and equipment totaled

- - 20 - -

$1,353,539 in year ending December 31, 2008 compared to $545,494 in December of 2007; (4) increase in inventory and accounts receivable due to the Company’s growth in 2008, and (5) the purchase of the AmeriSolar brand name and technology.

Results of Operations

Net sales for the year ending December 31, 2008 were $45,913,957 compared to $12,132,710 for the year ending December 31, 2007, an increase of $33,781,247 or approximately 278.4%. The primary reason for the increase was due to our energy division which started in February 2008 and generating sales of $30,999,962. Additionally, the acquisition of Detron generated sales of $1,720,965 for the Company in the fourth quarter.

For the year ending December 31, 2008, gross profits were $6,167,671 (13.4%) compared to $3,782,089 in 2007 (31% of sales). The decline of gross profits as a percentage of sales (17.6 percentage points) occurred because the Company utilized more sub-contractors for the production of our solar modules, along with softness in the price of solar modules. It is expected that gross margins will improve as the Company continues its transition of becoming a direct manufacturer for its solar module products as the newly established factory becomes operational. As well, the outlook for solar modules margins will improve as the raw material necessary for the production of modules are expected to decline.

Cost of goods sold for the year ending December 31, 2008 was $39,746,286 compared to $8,350,621 for the year ending December 31, 2007. The increase of $31,395,665 or 376% was the result of greater sales and lower margins in the solar module industry.

Net profit for the year ending December 31, 2008 was $1,001,648 compared to $575,674 for the year ending December 31, 2007. The increase of $425,974 or 74.0% was the result of higher sales from our solar division. Net profit from this division was approximately 3%. It is expected that gross margins will improve as the Company continues its transition to becoming a direct manufacturer for its solar module products as the newly established factory becomes operational. Further, the outlook for solar modules margins looks to improve as raw material necessary for production of modules are expected to decline.

General and administrative expenses for the year ending December 31, 2008 were $3,832,363 (8.3% of sales) compared to $2,769,847 (22.8% of sales) for the year ending December 31, 2007. The increase of $ 1,004,900, or 35.5%, was the result of increased staff and expenses associated with providing an appropriate infrastructure to support our growth and future growth. Further, the costs associated with being public increased over the last year.

Liquidity

The following is a summary of Worldwide’s cash flows from operating, investing, and financing activities during the periods indicated:

- - 21 - -

Year ended December 31, | ||

| 2008 | 2007 |

|

|

|

Operating activities | $2,682,044 | $252,456 |

Investing activities | $(2,811,318) | $(791,302) |

Financing activities | $3,169,596 | $1,133,674 |

Net effect on cash | $2,980,651 | $672,024 |

|

|

|

The Company funded its growth largely from its proceeds of $4,747,970 from the sale on June 23, 2008 of 1,055,103 shares of its common stock. As well, the Company had additional subscriptions for the sale of an aggregate of $252,027 or 56,007 shares of common stock. This was used to help fund these new acquisitions and to provide additional working capital for the Company. The Company netted $4,608,036 from the sales of these securities.

In 2008 our credit line was increased by approximately $775,000 from a line of credit in the amount of $2.25 million with Golden Gate Bank to $3.025 million, as a result of securing two new credit lines with Bank of the West, one for $1,025,000 and the other for $2,000,000. The credit line with Golden Gate Bank was subsequently cancelled. These revolving lines of credit are secured by the assets of the Company and guaranteed by its officers. At December 31, 2008 and 2007, the balances on the lines of credit with Bank of the West were $921,619 and $1,758,584, respectively. The maturity date of these two credit lines is May 20, 2009 and June 1, 2011, respectively. The balance outstanding as of March 31, 2009 is $1,300,000, and $700,000 is still available for use on the line of credit. Additionally, the second line of credit has a balance of $877,869 as of March 31, 2009, with $147,131 still available for use of equipment and facility purchases.

Further, the increase in net profits of $884,201 or 153.6% over the last year provided the Company with greater liquidity and financial resources. The Company feels that it has sufficient capital to continue to fund its operations.

For 2008, net cash provided by operations was $2,682,044 compared to net cash provided by operations of $252,456 for the year ended December 31, 2007, an increase of $2,429,588. The major factors for this increase in net cash through operations were customer deposits for our solar modules which totaled $960,873, and our accounts receivables, which provided $521,719 due to growth in solar modules. Net cash used in investing was $2,811,318 in 2008, compared to net cash used of $791,302 in 2007. This increase was the result of our acquisition of Detron and the establishment of our new solar module factory. The Company anticipates further expansion in 2009 and will finance this growth through Company profitability as well as outside sources of funding if required. Net cash flows provided by financing activities in 2008 was $3,169,596 compared to $1,133,674 in December 31, 2007. The increase was due to proceeds from the Company’s sales of unregistered securities which provided the Company with net proceeds of $4,608,036, and which helped the Company to expand its operations.

New Markets and Expansion of Operations in 2009

We plan to continue our expansion efforts in the solar module industry through expansion of our

- - 22 - -

solar module factory in Ningbo, China. We will attempt to increase our customer base in this industry by achieving greater product enhancements and sales efforts. Further, we feel that our recent acquisition of Detron will bring more revenues and profits as we continue to streamline our present electronic factory into the new acquisition as well as improve the operation of Detron and our other factories in China. Additionally, we intend to begin expansion into the U.S. solar module market in the third quarter of 2009.

Off-Balance Sheet Arrangements

We do not have any off-balance sheet arrangements that are currently material or reasonably likely to be material to our financial position or results of operations.

Tabular disclosure of contractual obligations

Contractual obligations | Payments due by period | |||||||||||

|

| Total | Less than 1 year | 1-3 years | 3-5 years | More than 5 years | ||||||

Long-Term Debt Obligations | 921,619 |

|

| 921,619 |

| |||||||

Capital Lease Obligations | 911,111 | 267,831 | 340,984 | 302,296 |

| |||||||

Operating Lease Obligations |

|

|

|

|

| |||||||

Purchase Obligations |

|

|

|

|

| |||||||

Other Long-Term Liabilities Reflected on the Registrant’s Balance Sheet under GAAP | 75,480 |

| 75,480 |

|

| |||||||

Total | 1,908,210 | 267,831 | 416,464 | 1,223,915 |

| |||||||

Critical Accounting Policies, Estimates and Judgments

This discussion and analysis of financial condition and results of operations is based on our consolidated financial statements, which have been prepared in accordance with U.S. generally accepted accounting principles. The preparation of these financial statements requires us to make estimates and judgments that affect the reported amounts of assets, liabilities, revenues and expenses and related disclosures. On an on-going basis, we evaluate our estimates, including those related to property, plant and equipment, inventories, revenue recognition, inventories, accounts receivable and foreign currency transactions and translation. We base our estimates on historical experience and on various other market-specific assumptions that are believed to be reasonable under the circumstances, the results of which form the basis for making judgments about the carrying values of assets and liabilities that are not readily apparent from other sources. Actual results, however, may differ significantly from these estimates.

We believe the following critical accounting policies reflect the more significant judgments and estimates used in the preparation of our consolidated financial statements:

- - 23 - -

Property, plant and equipment

Property, plant and equipment are stated at historical cost and are depreciated over the useful lives of the assets. Leasehold improvements and capitalized leased equipment are amortized over the life of the lease. Repair and maintenance expenditures that do not significantly add to the value of the equipment or prolong its life are charged to expense as incurred. Gains and losses on dispositions of property, plant and equipment are included in the related period’s statement of operations. Depreciation is computed primarily using the straight-line method based on estimated useful lives, which range from 3 to 25 years.

Inventories

Inventories consist of finished goods of manufactured products. Our inventory is based on customer orders and the duration of those orders. Cost is stated at the lower of cost or market on a first-in, first-out (FIFO) basis. We have not recorded an allowance for slow-moving or obsolete inventory. Obsolete inventory at December 31, 2008 and 2007 was minimal.

Revenue Recognition

We recognize revenues in accordance with the guidelines of the Securities and Exchange Commission (“SEC”) Staff Accounting Bulletin (“SAB”) No. 104 “Revenue Recognition.” We recognize revenue from product sales when the orders are completed and shipped, provided that collection of the resulting receivable is reasonably assured. Amounts billed to customers are recorded as sales while the shipping costs are included in cost of sales. Returns on defective custom parts may only be exchanged for replacement parts within 30 days of the invoice date. Returns on defective parts, which can be resold, may be exchanged for replacement parts or for a refund. Revenue from non-refundable customer tooling deposits is recognized when the materials are shipped or when the deposit is forfeited, whichever is earlier.

Foreign Currency Transactions and Translation

Transaction gains and losses result from a change in exchange rates between the functional currencies in which a foreign currency transaction is denominated and the reporting currency. They represent an increase or decrease in (i) the actual functional current cash flows realized upon settlement of foreign currency transactions and (ii) the expected functional currency cash flows on unsettled foreign currency transactions. All transaction gains and losses are included in other income or expense. For all periods presented, sales to customers were primarily denominated in Euros and U.S. dollars.

Assets and liabilities of foreign subsidiaries are translated into U.S. dollars at the prevailing exchange rate in effect at each period end. Revenue and expenses are translated into U.S. dollars at the average exchange rate during the reporting period. Contributed capital is translated into U.S. dollars at the historical exchange rate when capital was injected. Any difference resulting from using the current rate, historical rate, and average rate in determination of retained earnings is accounted for as a translation adjustment and reported as part of comprehensive income or loss in the equity section. Exchange differences are recognized in the income statement in the period in which they occur.

- - 24 - -

Management has discussed the development and selection of these critical accounting policies with the Board of Directors and the Board has reviewed the disclosures presented above relating to them.

Item 7A. Quantitative and Qualitative Disclosure About Market Risk

Not applicable.

Item 8. Financial Statements and Supplementary Data

See the following pages.

- - 25 - -

WORLDWIDE ENERGY AND MANUFACTURING USA, INC. AND SUBSIDIARIES

Index to Consolidated Financial Statements

CONTENTS

| Page |

Report of Independent Registered Public Accounting Firm | 27 |

Consolidated Balance Sheets | 28 |

Consolidated Statements of Operations and Other Comprehensive Income | 30 |

Consolidated Statements of Stockholders’ Equity | 32 |

Consolidated Statements of Cash Flows | 33 |

Notes to Consolidated Financial Statements | 35 |

- - 26 - -

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To The Board of Directors

WORLDWIDE ENERGY AND MANUFACTURING USA, INC.

South San Francisco, CA USA

We have audited the accompanying consolidated balance sheets of WORLDWIDE ENERGY AND MANUFACTURING USA, INC. and subsidiaries as of December 31, 2008 and 2007, and the related consolidated statements of operations and other comprehensive income, stockholders’ equity, and cash flows for the years ended December 31, 2008 and 2007. These financial statements are the responsibility of the Company’s management. Our responsibility is to express an opinion on these financial statements based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States of America). Those standards require that we plan and perform the audits to obtain reasonable assurance about whether the financial statements are free of material misstatement. The Company is not required to have, nor were we engaged to perform, an audit of its internal controls over financial reporting. Our audits included consideration of internal control over financial reporting, as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Company’s internal control over financial reporting. Accordingly, we express no such opinion. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements referred to above present fairly, in all material respects, the consolidated financial position of WORLDWIDE ENERGY AND MANUFACTURING USA, INC. and subsidiaries as of December 31, 2008 and 2007 and the results of their operations and their cash flows for the years ended December 31, 2008 and 2007, in conformity with accounting principles generally accepted in the United States of America.

Child, Van Wagoner & Bradshaw, PLLC

Salt Lake City, Utah

April 05, 2009

- - 27 - -

WORLDWIDE ENERGY AND MANUFACTURING USA, INC. AND SUBSIDIARIES

CONSOLIDATED BALANCE SHEETS

|

| December 31 |

| December 31 |

|

| 2008 |

| 2007 |

ASSETS |

|

|

|

|

Current assets: |

|

|

|

|

Cash and cash equivalents | $ | 5,092,476 | $ | 2,111,825 |

Accounts receivables, net of allowances of $45,634 |

| 4,790,506 |

| 3,275,024 |

Notes receivables |

| 269,507 |

| - |

Inventories |

| 3,754,765 |

| 2,333,148 |

Income tax receivable |

| - |

| 82,131 |

Advances to suppliers |

| 99,824 |

| 260,540 |

Related parties receivables |

| 446,373 |

| 30,422 |

Prepaid and other current assets |

| 206,770 |

| 117,621 |

|

|

|

|

|

Total current assets |

| 14,660,221 |

| 8,210,711 |

|

|

|

|

|

Deposits paid for investment |

| 1,724,976 |

| - |

Property, plant and equipment, net |

| 1,353,539 |

| 545,494 |

Intangible assets |

| 1,386,714 |

| - |

Other assets |

| 7,559 |

| 6,636 |

|

|

|

|

|

Total assets | $ | 19,133,009 | $ | 8,762,841 |

|

|

|

|

|

LIABILITIES AND STOCKHOLDERS’ EQUITY |

|

|

|

|

|

|

|

|

|

Current liabilities: |

|

|

|

|

Accounts payable | $ | 3,400,253 | $ | 2,453,317 |

Lines of credit |

| - |

| 1,758,584 |

Accrued expenses |

| 867,291 |

| 156,524 |

Tax payable |

| 364,213 |

| 78,637 |

Acquisition Cost Payable |

| 285,714 |

|

|

Due to related parties |

| 1,243,024 |

| - |

Customer deposits |

| 964,998 |

| - |

Current portion of long-term debt (note 10) |

| - |

| 884 |

|

|

|

|

|

Total current liabilities |

| 7,125,493 |

| 4,447,946 |

|

|

|

|

|

Non-current liabilities |

|

|

|

|

Long term loan |

| 937,075 |

| - |

Loan payable to stockholders |

| 60,024 |

| 498,812 |

Total non-current liabilities |

| 997,099 |

| 498,812 |

|

|

|

|

|

Total liabilities |

| 8,122,592 |

| 4,946,758 |

|

|

|

|

|

Minority interest in subsidiary |

| 612,639 |

| - |

|

|

|

|

|

Stockholders’ equity |

|

|

|

|

Common stock (No Par Value: 100,000,000 shares authorized; |

|

|

|

|

3,493,512 shares issued and outstanding) |

| 6,108,379 |

| 270,746 |

- - 28 - -

Retained earnings |

| 3,801,921 |

| 3,250,112 |

Accumulated other comprehensive income |

| 487,478 |

| 295,225 |

|

|

|

|

|

Total stockholders’ equity |

| 10,397,778 |

| 3,816,083 |

|

|

|

|

|

Total liabilities and stockholders’ equity | $ | 19,133,009 | $ | 8,762,841 |

See accompanying notes to consolidated financial statements.

- - 29 - -

WORLDWIDE ENERGY AND MANUFACTURING USA, INC. AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF INCOME AND

COMPREHENSIVE INCOME

|

| For The Year Ended | ||

|

| December 31 | ||

|

| 2008 |

| 2007 |

Revenue |

|

|

|

|

Regular sales, net of returns of $0 in 2007 and $0 in 2006 | $ | 45,913,957 | $ | 12,132,710 |

|

|

|

|

|

Cost of goods sold |

| 39,746,286 |

| 8,350,621 |

Gross profit |

| 6,167,671 |

| 3,782,089 |

|

|

|

|

|

Operating Expenses |

|

|

|

|

Other selling, general and administrative expenses |

| 3,832,363 |

| 2,769,847 |

Management and professional fees paid to shareholders (Note 13) |

| 306,000 |

| 210,000 |

Stock based compensation |

| 128,597 |

| - |

Depreciation |

| 122,923 |

| 106,480 |

|

|

|

|

|

Total operating expenses |

| 4,389,883 |

| 3,086,327 |

|

|

|

|

|

Net operating income |

| 1,777,788 |

| 695,762 |

|

|

|

|

|

Other Income (expenses) |

|

|

|

|

Interest income |

| 21,995 |

| 12,548 |

Interest expenses |

| (120,038) |

| (79,544) |

Interest expense paid to shareholders (Note 13) |

| (27,284) |

| (17,371) |

Other income |

| 114,057 |

| 254,265 |

Other expenses |

| (243,765) |

| - |

Dividend income |

| 242,770 |

|

|

Exchange loss |

| (364,067) |

| (355,712) |

Loss on Disposal |

| (101,982) |

|

|

Gain on disposal |

| - |

| - |

|

|

|

|

|

Total other expenses |

| (478,314) |

| (185,814) |

|

|

|

|

|

Income from continuing operations before income taxes |

| 1,299,474 |

| 509,948 |

Income taxes (expense) /benefit |

| (284,278) |

| 65,726 |

|

|

|

|

|

Income from continuing operations before minority interest |

| 1,015,106 |

| 575,674 |

Loss share by minority interest |

| (15,843) |

| - |

|

|