SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended: December 31, 2012

OR

o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from __________ to __________

Commission File No. 000-30563

DELTA MUTUAL, INC.

(Exact name of Registrant as Specified in Its Charter)

| Delaware | | 14-1818394 |

| (State or other jurisdiction of | | (I.R.S. Employer |

| Incorporation or organization) | | Identification No.) |

| 16427 North Scottsdale Road, Suite 410, Scottsdale, AZ | | 85254 |

| (Address of principal executive offices) | | |

Registrant’s Telephone Number, Including Area Code: (480) 483-0420 |

Securities registered pursuant to Section 12(b) of the Act: None

Securities registered pursuant to Section 12(g) of the Act: Common Stock, $.0001 par value per share

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No x

Indicate by checkmark if the registrant is not required to file reports to Section 13 or 15(d)Of the Act. o Yes x No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. x Yes o No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes o No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a smaller reporting company. (Check One):

Large accelerated filer o Accelerated filer o

Non-accelerated filer o Smaller reporting company x

(Do not check if a smaller reporting company)

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).o Yesx No

The aggregate market value of the voting and non-voting common equity held by non-affiliates as of the last business day of the registrant’s most recently completed second fiscal quarter was $7,252,918.

Number of shares of Common Stock outstanding as of March 21,2013: 32,086,826.

TABLE OF CONTENTS

| PART I | 1 |

| Item 1. Business. | 13 |

| Item 1A. Risk Factors. | 18 |

| Item 1B. Unresolved Staff Comments. | 18 |

| Item 2. Properties. | 18 |

| Item 3. Legal Proceedings. | 18 |

| Item 4. Mine Safety Disclosures. | 18 |

| PART II | 19 |

| Item 5. Market for Registrant's Common Equity, Related Shareholder Matters and Issuer Purchases of Equity Securities. | 19 |

| Item 6. Selected Financial Data. | 19 |

| Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations. | 20 |

| Item 7A. Quantitative and Qualitative Disclosures About Market Risk. | 26 |

| Item 8. Financial Statements and Supplementary Data. | 28 |

| Item 9. Changes In and Disagreements With Accountants on Accounting and Financial Disclosure. | 29 |

| Item 9A. Controls and Procedures. | 30 |

| Item 9B. Other Information. | 30 |

| PART III | 31 |

| Item 10. Directors, Executive Officers, and Corporate Governance. | 31 |

| Item 11. Executive Compensation. | 32 |

| Item 12. Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters. | 35 |

| Item 13. Certain Relationships and Related Transactions, and Director Independence. | 36 |

| Item 14. Principal Accountant Fees and Services | 36 |

| PART IV | 37 |

| Item 15. Exhibits and Financial Statement Schedules. | 37 |

NOTE REGARDING FORWARD LOOKING STATEMENTS

CAUTIONARY STATEMENT FOR PURPOSES OF THE "SAFE HARBOR" PROVISIONS

OF THE PRIVATE SECURITIES LITIGATION REFORM ACT OF 1995

This Annual Report contains historical information as well as forward- looking statements. Statements looking forward in time are included in this Annual Report pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. Such statements involve known and unknown risks and uncertainties that may cause our actual results in future periods to be materially different from any future performance suggested herein. We wish to caution readers that in addition to the important factors described elsewhere in this Form 10-K, the following forward-looking statements, among others, sometimes have affected, and in the future could affect, our actual results and could cause our actual consolidated results during 2013, and beyond, to differ materially from those expressed in any forward-looking statements made by or on our behalf.

Item 1. Business.

Unless the context otherwise requires, the terms "the Company," "we," "our" and "us" refers to Delta Mutual, Inc., and, as the context requires, its consolidated subsidiaries.

Background

We were incorporated under the name Delta Mutual, Inc. on November 17, 1999, in the State of Delaware. In 2003, we established business operations focused on providing environmental and construction technologies and services. Our operations in the Far East (Indonesia) and our construction operations in Puerto Rico were discontinued in 2008.

Effective March 4, 2008, we acquired 100% of the issued and outstanding membership interests in the parent of South American Hedge Fund LLC, (sometimes herein referred to as “SAHF”). For accounting purposes, the transaction was treated as a recapitalization of the Company, as of March 4, 2008, with the parent of SAHF as the acquirer. SAHF maintains a branch office in Argentina, where it is engaged in oil and gas exploration and development activities.

Dr. Daniel R. Peralta, our President and Chief Executive Officer, director, and major stockholder, and his wife died in their home November 7, 2012. Dr. Peralta was responsible for initiating our efforts to acquire and develop oil and gas concessions in Argentina. Our board has appointed Malcolm Sherman, who was our Executive Vice President, as President and Chief Executive Officer and elected Santiago Peralta, the son of Dr. Peralta, as a member of our Board of Directors.

Our principal offices are located at 16427 North Scottsdale Road, Suite 410, Scottsdale, AZ 85254. Our telephone number is (480)483-0420. Our common stock is quoted on the Over-the-Counter Electronic Bulletin Board under the symbol "DLTZ.OB".

General

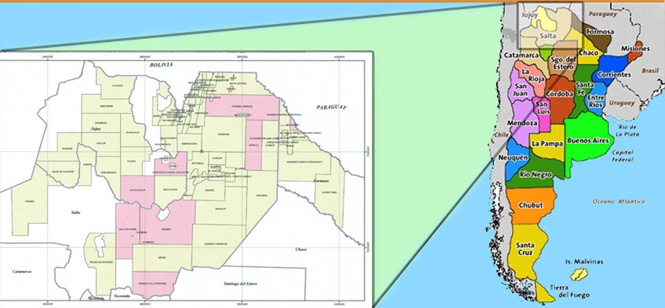

We are an independent oil and gas company engaged in oil and gas concession investments, exploitation, production and exploration activities primarily in Argentina. In addition, we have ownership interests in certain mineral rights that are located in Argentina.

We are currently involved in developing our existing oil and gas properties discussed below and securing additional concessions in Argentina which either are producing economical quantities of oil and gas or which demonstrate favorable characteristics for well “workovers” with a history of excellent production. Some of these concessions require workover procedures to bring them up to profitable production. Several of the projects now being visited and discussed have multiple producing wells, as well as a history of excellent production. It is the goal of the Company to target these concessions as compared to concessions which will be exploratory and would require drilling new wells.

Final contracts and documentation are expected to be completed in May 2013 on a concession area where one productive oil and gas well was drilled in the 1980’s, with positive pressure and no water. Upon conclusion of final contracts, together with our partners Grasta Petroleum and PPL, we plan to develop the block, commencing with two seismic interpretations and a hydrocarbon micro seepage survey prior to a workover of the previously drilled well utilizing a local rig company.

Business Strategy

The key elements of our business strategy are to:

| ● | Make accretive acquisitions of producing properties generally characterized by long-lived reserves with stable production and reserve development potential; |

| ● | Add proved reserves and maximize cash flow and production through development projects and operational efficiencies; and |

| ● | Engage in adjacent exploration drilling where evaluation of the property is positive. |

Our investments have focused on concessions where there are shut-in, plugged and abandoned wells that have, in our assessment, a high probability of additional recovery of reserves through revitalization processes that are commonly used in the oil and gas industry. The revitalization processes are directed toward bringing wells back into production or to enhance production with newer technology.

Specifically, we have focused, and plan to continue to focus, on the following investments in South America.

Our Oil and Gas Investments

Our main source of revenue will derive from the sale of the crude oil and natural gas produced from the oil and gas concessions in which we have made investments. In August 2007, SAHF signed agreements to purchase partial ownership interests in four oil and gas concessions in Northern Argentina. The joint venture owning these concessions then started the process to obtain the necessary government and environmental operating permits for the commercial exploitation of these concessions. While we are not the operators of certain of these concessions, we generally have representation on the operating committees that are responsible for managing the business affairs of these concessions.

At December 2012 the SAHF participations in the Argentina concessions are as follows:

| Block | Province | Status | Delta [SAHF] % | Partner(s) |

| Jollin | Salta | Testing | 10% CO | JHP (China), Maxipetrol |

| Tonono | Salta | Testing | 10% CO | JHP (China), Maxipetrol |

| Tartagal | Salta | 2 Work over wells drilled; 20 prospects | 9% CO | New Times Energy (HK), Maxipetrol |

| Morillo | Salta | 3D seismic interpretation; 2 exploratory wells to be drilled | 9% CO | New Times Energy (HK), Maxipetrol |

| Guemes | Salta | Drill Complete | 20% | Ketsal |

| Valle de Lerma | Salta | Workover well on adjacent property to be assigned by Salta Government | 60% | Remsa, PetroNexus, Grasta |

*CO means a carryover interest in the project.

** Of these five properties, SAHF and its joint venture partner have made initial investments in Guemes.

*** In the Jollin, Tonono and Tartagal, and Morillo concessions the carry over mode relieved SAHF from the payment of canon, landlord fees of any kind or any other expense until production is realized. In the exploratory area Guemes, proportional exploratory canons were paid as explained in the financials.

Agreements with Principle Petroleum Limited

Effective March 30, 2012, we entered into an Asset Purchase and Cooperation Agreement (the “Cooperation Agreement”) with Principle Petroleum Limited (“PPL”), headquartered in the British Virgin Islands. Under the Cooperation Agreement, PPL agreed to pay us $7,000,000 for certain exploration and exploitation rights to oil and gas deposits and certain bidding rights held by Delta on the following areas: Valle de Lerma in the province of Salta; San Salvador de Jujuy; Libertador General San Martin in the province of Jujuy; and Selva Maria in the province of Formosa. The San Salvador and Lebertador concessions have since been awarded by the government to another party. Pursuant to a separate Agreement dated March 31, 2012, we agreed with PPL to assign and transfer 50% of SAHF's ownership of the Tartagal and Morillo (i.e., a 9% interest in the concession) to PPL for a purchase price of $500,000. PPL has also agreed in an Undertaking to provide funds to the operating entities of Valle de Lerma and Selva Maria, in the aggregate amount of up to $10,000,000 (Selva Maria is pending for approval from the government, which is standard procedure in Argentina). In all of the concession interests mentioned in the Cooperation Agreement and the other agreements, except for Tartagal and Morillo, SAHF will be the operator.

Jollin and Tonono Concessions

SAHF has a 10% ownership interest in the Jollin and Tonono oil and gas concessions located in Salta Province, Argentina. SAHF originally purchased an 20% carry-over interest in the Jollin and Tonono concessions on May 15, 2007, and subsequently increased its ownership to 47%, 20% of which was carry-over and 27% which was working. Subsequently, in 2008, SAHF sold half of its stake, giving SAHF a 10% carry-over and 13.5% working interest in the concessions. SAHF in 2009 transferred 13.5% to Maxipetrol, under an arrangement where SAHF’s remaining 10% interest would be in a carry-over mode.

SAHF received its foreign registration in Argentina and was admitted as a member of the joint venture on July 2, 2010.

Tartagal and Morillo Concessions

Tartagal Oriental - The Tartagal Oriental (“Tartagal”) exploration license area, extended to February 2014, covers 7,065 square kilometers in Salta Province, located in the northern part of Argentina. Exploration dates back into the mid 20th century, and 22 wells, some oil producers, have been drilled in Tartagal Oriental since the 1960s. Of the 22 wells that have been drilled in Tartagal Oriental in the past decades, several were judged to be workover candidates by New Times Energy Corporation Limited, Hong Kong, who purchased 60% of the ownership in the Tartagal and Morillo oil and gas concessions, and has invested approximately $60 million to date on geological studies, 2D and 3D seismic surveys on both blocks and two work-over drills and an exploratory well drill in Tartagal. Production from the two Campo Alcoba test wells commenced in 2011 and has continued into the 2012 second quarter. A work over of one the two previously reopened wells is planned, and currently an analytic test to drill one more exploratory well is under way.

Morillo - The Morillo exploration license area covers 3,518 square kilometers in Salta Province, contiguous with and south of the Tartagal Oriental license. Granted at the same time as Tartagal Oriental, the Morillo license was also extended to February 2014. In 2011, High Luck ordered a 274 square kilometer 3D seismic to be shot in the southwestern corner of the property because of a recent discovery made by Petrobras in an adjacent block. Once the data is processed, a decision will be made as to further drilling.

SAHF had 9% ownership of the Tartagal and Morillo oil and gas concessions located in Salta Province, Argentina, at December 31, 2010. Subsequent to year end, our ownership interest was increased to 18% in March 2011, and we sold 50% of that interest to PPL in 2012.

On May 11, 2011, SAHF received the Argentinean Salta Government’s approval for its 18% ownership share for the Tartagal and Morillo concessions.

Exploration Rights

(Guemes Block)

On February 6, 2008, SAHF purchased 40% of the oil and gas exploration rights to five geographically defined areas in the Salta Province of Northern Argentina for $697,000. During 2008, SAHF sold 50% of its rights in these concessions to a third party. Provided certain development activities are undertaken by owners, these exploration rights will remain in effect through the year 2015. The initial development costs and fees were paid by the majority owner and SAHF incurred no additional expenses related to this investment in 2008.

Exploratory drilling activities commenced in April 2010 on the Guemes Block and the first well was spud in September 2010. In July 2010, SAHF found positive traces of the presence of natural gas and hydrocarbons of low-density quality through its analysis of core samples. Well logging while drilling also confirmed the potential existence of formations with sufficient hydrocarbons to make the well economically productive. Production testing to verify the commercial sustainability of the well still needs to be done.

The UTE for this concession is in litigation with the drilling company that drilled the test well and has sued for an alleged $3,000,000 of additional expenses over and above the contract amount under the fixed price drilling contract, where the contract amount was set at $1,000,000, and overage amounts were to be set prior to execution. The operator of the concession, Ketsal, is in the process of settlement negotiations. SAHF has no obligation or liability for any amounts paid in settlement of, or as a result of an adverse judgment in, this litigation. However, the resolution of this lawsuit may affect the schedule for the future development of this property.

Valle de Lerma Block

On August 10, 2011, the Company’s tender offer, made through our wholly-owned subsidiary, SAHF, for the ownership right to explore, and eventually, produce oil and natural gas in the block known as “Valle de Lerma” was declared the winning bid by the Salta provincial government. SAHF made the offer in a joint venture agreement with Remsa, PetroNexus and Grasta SA, a local mid-size gasoline refinery located in Buenos Aires, Argentina. The joint venture paid US$5,000 to enter the international bid and presented a business plan, a contingency plan and economic offer to the government of Salta. In this offer, the Company committed 401 work units in the form of 2D seismic reinterpretation, 3D seismic shooting, and geochemistry for the first exploration period, which is 4 years. Each work unit has the equivalent of US$5,000, so the joint venture committed US$2,005,000 across a four-year span in the form of "soft" work units, or work units used to discover potential oil fields. The offer was originally approved by Resolution from the Secretary of Energy of the Salta Government, and then approved by a governor's decree in Salta published on August 11, 2011 in the daily bulletin of the province. In addition, the joint venture took out an insurance policy through Fianzas y Credito for the 10% of the committed amount for US$1000 per quarter, as is mandatory.

The Valle de Lerma block is located in the province of Salta in the northwestern region of Argentina and has an area of 5259 km2. SAHF has done the measurement and survey study and filed an environmental impact study, which was approved. Upon completion of the study it was determined that the actual well site was within the boundaries of the City of Salta, where government restrictions do not allow oil to be produced from this site. We are currently negotiating with the government to add an additional site to the concession area from among three sites adjacent to the concession area with similar wells. When the extension of the concession area is accomplished, we will commence work on the new site, following receipt of all government approvals. SAHF holds a majority of the license interest and is the responsible operator. The license allows SAHF 20 years to explore and produce hydrocarbons with a renewal option of ten more years. The Company will commence the Valle de Lerma well work over with a local rig company. The exploration terms are four years for the first period, three years for the second and two years for the last period.

The Valle de Lerma block has been explored in the past by YPF and several seismic 2D lines were extensively performed to research the area. Two Exploratory Wells were drilled in December 1990 and November 1994 by a private company; both indicated hydrocarbon traces or presence. In the second well, named "La Troja" (total depth of 1433 mbbp), an oil production of 28 API density was tested at 1277 mbbp for a test time of 19 hs. For strategic reasons, the wells were capped.

SAHF currently owns 60% of the rights to explore Valle de Lerma; Grasta owns 5%; PetroNEXUX owns 30%; and Remsa owns 5%.

Caimancito Refinery

On January 13, 2012, we, through our wholly-owned subsidiary, SAHF, signed a purchase option agreement with Cruz Norte, SA to purchase 33.33% of the Caimancito Refinery, located in the Jujuy Province, Argentina. In March, 2012, the purchase option agreement was finalized and signed and Cruz Norte transferred 1/3 of its stake in the refinery to SAHF. The purchase price of the refinery was US$150,000 for the 33.33% of the outstanding shares of Caimancito Refinery. A contract with NOA, a service company, was entered into for NOA to advise us of the expected costs to rehabilitate the plant. Due to required rehabilitation work, currently this refinery is not being operated to produce gasoline or diesel fuel.

The Caimancito Refinery was built in the 1980's, in the Province of Jujuy, by Gas del Estado, a formerly State-owned natural gas company in order to produce propane, butane and natural gasoline. In 1997, management converted some of its equipment into equipment used for petroleum distillation and for solvent, gasoline, diesel oil and thinner production. During 2000, a biodiesel plant with the capacity of 10m3/day was built and operated until 2001 when the plant was revamped to 15m3/day. The Caimancito plant is the only refining plant in Jujuy.

Terms of Carryover Arrangements

We entered into a carryover arrangement for Jollin and Tonono on September 25, 2009. The Tartagal and Morillo interest was a carry-over interest from inception, May 15, 2007.

The carrying party for Jollin, Tonono, Tartagal and Morillo concessions is Oxipetrol-Petroleros de Occidente SA (Maxipetrol). Jollin and Tonono went into a carry-over mode after a buy-sell agreement with Maxipetrol on September 29, 2009.

Under the terms of the carry over, 50% of the production profits will be applied to the investment payment. The balance of the production profits (50%) will be distributed proportionally according to the percentage of each JV member. These terms apply for the Jollin, Tonono, Tartagal & Morillo concessions.

Admission of SAHF to Joint Ventures Operating Oil Concessions

SAHF received the approval for the Jollin Block and Tonono Block on July 2, 2010, 14 months after filing for such. The approval for the Tartagal and Morillo Blocks application was filed in August 2010 and approved May 11, 2011.

Prior to formal admittance into the joint ventures, SAHF’s 10% carry-over interest in the Jollin and Tonono concessions and 9% carry-over interest in the Tartagal and Morillo Concessions were assigned to and held in Trust for SAHF by Maxipetrol for the sole use and benefit of SAHF, including any proceeds from the sale of hydrocarbons or property interests. The Assignment Agreement did not affect the rights, privileges, obligations and liabilities of the parties to the agreement related to their respective interests in any way. This is a common practice in Argentina due to the lengthy period required for obtaining government approvals.

The 2010 concessions for the Salta Province Exploration Rights Concession total approximately $1.1 million of which SAHF’s share is $220,000. Prior to the drilling of the Guemes well, the managing partner began negotiating with the government of Argentina to have the concessions' penalties waived and it was agreed that the Government will not draw on the Performance Bond posted by Ketsal, in exchange for opening a well on Guemes and continued development activities in the province. SAHF opened up well in Guemes known as "Dos Morros" and the overdue charges have been waived. When the transactions with the government and partners are finalized, SAHF will register to become an official member of the new remaining joint venture.

Development Schedule for Our Oil and Gas Investments

The focus of operations for the Company's immediate development is Valle de Lerma. SAHF has done the measurement and survey study and filed an environmental impact study, which was approved. Upon completion of the study it was determined that the actual “La Troja” well site was within the boundaries of the City of Salta, where government restrictions do not allow oil to be produced from this site. We are currently negotiating with the government to add an additional site to the concession area from among three sites adjacent to the concession area with similar wells. When the extension of the concession area is accomplished, we will commence work on the new site, following receipt of all government approvals.

In addition the operators of Tartagal and Morillo have stated that they expect to be delivering crude to the local refineries as soon as their wells are approved for commercial production and the battery and required lines and infrastructure are installed. The main costs associated with our oil and gas investments are related to oil and gas property acquisition, drilling costs, initial well revitalization, gas pipeline construction and ongoing operating expenses. The revitalization of wells allows short-term cash increases while holding the lease for additional future development.

Commitment to Technology

In each of our core operating areas, we have accumulated detailed geologic and geophysical knowledge and have developed significant technical and operational expertise. This data is analyzed with advanced geophysical and geological computer resources dedicated to the accurate and efficient characterization of the subsurface oil and gas reservoirs that comprise our asset base. This commitment to technology has increased the productivity and efficiency of our field operations and development activities.

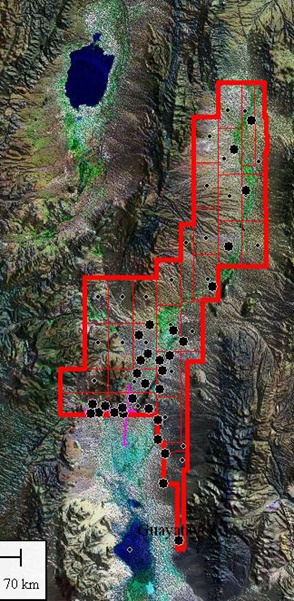

Lithium Project

On March 1, 2010, we purchased control of 51% of approximately 143,000 hectares with 29 mines located in the Northwest part of Argentina, south of the border with Bolivia, with high lithium and borates brines concentration. This property is held under a concession for a period of 20 years that provides for the following rights: to explore, evaluate, develop, produce and arrange mineral resources on the property. Subject to the terms and conditions of this agreement, SAHF has been appointed as Chief Operating Officer (COO) of the project. The project involves the exploration and eventual exploitation of 29 mines in one block of a salt plateau located in Jujuy Province, Argentina. None of the 29 mines is being actively mined. We have performed sampling and geological analyses with a local geological company to determine value to the property. The condition to retain the claims is payment of the annual fee renewal and the approval of the Operation Plan and Environmental Impact Report by government authorities before any major drilling. We are actively seeking a partner or buyer to take over the development of this property.

Each of the black dots represents a mine location.

Cachi

In the fourth quarter of 2010, SAHF exercised a purchase option agreement with Minera Ansotana, SA to explore and develop columbite-tantalite (coltan) from a set of mines in Cachi, Salta. Some of the key mines in Cachi are El Quemado, Penas Blancas and Tres Tetas, which were used for mining in the 1950's by German immigrants. After reviewing various reports detailing the potential of these mines, the Company purchased 51% of the mine and immediately began sampling the property. In the fourth quarter of 2011, the Company received very promising results from the Tres Tetas mines from samples that were taken throughout 2011 by a team of local geologists and engineers. The samples were originally analyzed in labs at a local Salta University, and then exported to Chile and Australia for further analysis.

Because of the location and height, the window for the government’s construction of a road, further work is currently on hold until next summer, when the government is expected to complete the road.

SAHF is still exploring several options to arrange partnership interests with other firms to exploit the Cachi and lithium properties or to sell the concessions.

Development Activities

Development projects on the concessions in which we have investments include accessing additional productive formations in existing well bores, formation stimulation, infill drilling on closer well spacing, and retrofitting or reworking existing wells.

Reserve Reports for the Properties

The Company is working with some of its partners in certain joint ventures and with NSAI to develop reserve reports and prospective resources reports for Tartagal, Morillo and Valle de Lerma.

Customers

Petroleum and natural gas in the Northwest Basin of Argentina are traded freely and on a transaction by transaction basis. There are no long term contracts due to the supply deficit in this area. The buyers are the local refineries, and deliveries are made by pipelines or by truck in remote sites. Refineries pay for the transportation cost. At present, SAHF does not have a contract with any customer and, if current circumstances continue to prevail, when we commence oil production SAHF will entertain the daily spot offers to maximize profit.

Title to Properties

We believe we have satisfactory title in all of our producing properties; and we investigate title and title opinions from counsel only when we acquire producing properties or before commencement of drilling operations. All of our current properties have been acquired directly from the government, except in the case of the Caimancito refinery. As all of our current property titles are issued by the Argentine government (Department of Energy), we believe that we are in full compliance with the title requirements for each of our properties.

Competition

Our ability to acquire additional prospects and to find and develop reserves in the future will depend on our ability to evaluate and select suitable properties and to consummate transactions in a highly competitive environment. Also, there is substantial competition for capital available for investment in the oil and gas industry.

Governmental Regulation

The key points of the statutory and regulatory regime in respect of oil and gas operations in Argentina are as follows:

The Company’s operations in Argentina are subject to various laws, taxes and regulations governing the oil and gas industry. Information concerning SAHF is registered in the Public Registry of Commerce, and the conduct and dealing of SAHF are governed by the commercial code and supplementary laws and regulations. Taxes generally include income taxes, value added taxes, export taxes, and other production taxes such as provincial production taxes and turnover taxes. Labor laws and provincial environmental regulations are also in place.

According to the Argentinean Hydrocarbons Law, number 6747 and Decrees 3560/95 and 2219/96, an Oil Operator License is needed to work in exploration and Exploitation of Hydrocarbons in the country. The Company has a Federal Operator License issued by the Federal Secretary of Energy and a Salta Province Producer License issued by the Salta Secretary of Energy. The company's partner, Grasta Petroleo has the refinery license to operate the Caimancito Plant.

Oil Concessions

Our right to conduct exploration and production activities in Argentina is derived from participation in concessions and exploration permits granted by the Argentine federal government and provincial governments that control sub-surface minerals. In general, provincial governments have had full jurisdiction over concession contracts since early 2007, when the Argentine federal government transferred to the provincial government’s full ownership and administration rights over all hydrocarbon deposits located within the respective territories of the provinces, including all exploration permits and exploitation concessions originally granted by the federal government.

A concession granted by the government gives the concession holders, or the joint venture partners, ownership of hydrocarbons at the moment they are produced through the wellhead. Under this arrangement, the concession holders have the right to freely sell produced hydrocarbons, and have authority over operations including exploration and development plans. The concessions have a term of 25 years which can be extended for 10 years with the consent of the government. Throughout the term of their concessions, the partners are subject to provincial production taxes, turnover taxes, and federal income taxes. These tax rates are fixed by law and are currently 12% to 18.5%, two percent, and 35 percent, respectively. Subsequent to the transfer of ownership and administrative rights over hydrocarbon deposits to the provinces, provincial governments have sometimes required higher provincial production tax rates in blocks awarded by the provinces or in concessions that have been granted the 10 year extension.

In Argentina, material mining regulations are promulgated by the Federal Congress and have been contained since 1884 as a part of the Mining Code. On the other hand, original domain of mining natural resources belongs to the provinces. Thus, provinces (i) appoint concession authorities and (ii) provide procedural mining regulations that individuals and legal entities must follow in order to be awarded mining rights and property. Exploration concessions granted are subject to specific terms, but resulting exploitation concessions––provided that certain requirements are met–– are perpetual.

Mining prospecting and exploration rights are easements which title can be granted to individuals or legal entities through administrative or judicial concessions ("exploration concessions"). Any mineral discovery made either by the concessionaire or third parties, provided they take place in the area and term of the concession, grants the concessionaire the right to turn such discovery into a mine.

The term of exploration concessions depends on the size of the granted concession area. The basic 500 hectares concession lasts for 150 days and each surface unit added to such basic concession increases the term in 50 additional days. Therefore, the largest possible concession will last for a 1,100 days term. In addition, there is an area limit of 200,000 hectares per area and a maximum of 20 areas that can be owned by a single entity.

Provincial governments in Argentina recently have established production floors and conditions for producing concessions, designed to force companies to increase production or else face a revocation in their concessions. We expect that our concession terms in the future will be affected by these changes in producing concession terms.

SAHF received on April 29, 2011 its producing license for oil and gas. Our partners in the joint ventures that SAHF is involved in have all the other required licenses and permits to commercially produce oil and gas.

In the lithium (North Guayatayoc) and Coltan (Cachi) properties, licenses have not yet been pursued because SAHF is still exploring several options to arrange partnership interests with other firms to exploit the properties or to sell the concessions. Once management has made a decision, the appropriate licenses will be acquired by either SAHF or its partners in the respective joint ventures.

The main effects of government regulations on the Company are that it will take a longer amount of time for properties to start producing commercially and that it will cost more money. The longer time frame from acquisition of the property to their commercial production stage can be attributed to the higher amount of time and focus that has to be put on paperwork and legal work. Because all of our contracts and corporate documents are written in English in the U.S, they need to be translated and notarized with an apostille to be valid in Argentina, which can cause delays in the applications for permits and licenses in Argentina. The higher expected cost can be attributed to the legal fees incurred to comply with the government regulations, along with the royalties, canons, and landowner fees that are particular to each concession.

Exchange Controls

As a result of the devaluation of the Argentine peso at the beginning of 2002, several foreign exchange regulations were issued to limit the transfer of money abroad. On October 13, 2011, the Argentine government launched a series of regulations in order to control the sale of foreign currency. The measures aim to slow the rise in value of the North American dollar, of which the Argentine Central Bank has had to reduce its reserves in order to avoid the continuing devaluation of the Argentine peso against the dollar.

There are no restrictions for the payment abroad of interest, dividends or profits, royalties and other commercial payments duly supported by the corresponding documentation. There are presently no restrictions on foreign investment in the capital of local corporations. However, pursuant to a 2005 rule issued by the central bank, any transfer of funds into Argentina as a result of a financial debt is subject to a compulsory one-year temporary and non-interest bearing deposit equivalent to 30% of the funds transferred into Argentina. Investments in mining projects or to increase the capital requirement of a company's branch(es) in Argentina are exempt from this deposit rule.

Research and Development

We do not anticipate performing any significant product research and development under our plan of operation.

Employees

Currently, we have three management employees: Malcolm W. Sherman, President and Chief Executive Officer, and two SAHF employees, a field operations manager and a general manager. In our operations in Argentina, we utilize temporary employees and consultants under contract. While in operations, the number of independent contractors hired temporarily by the Company for specific projects exceeds 70.

Available Information

We maintain a website at the address www.deltamutual.com. We are not including the information contained on our website as part of, or incorporating it by reference into, this report. We make available free of charge (other than an investor’s own Internet access charges) through our website our Annual Report on Form 10-K, quarterly reports on Form 10-Q and current reports on Form 8-K, and amendments to these reports, as soon as reasonably practicable after we electronically file such material with, or furnish such material to, the Securities and Exchange Commission.

Item 1A. Risk Factors.

Our oil and gas investments made by our subsidiary SAHF may not be profitable.

The success of our investments in Argentina will depend to a great extent on the operations, financial condition and management of the oil and gas concession and exploration rights in which we have investments. Their success may depend upon management of the operations in which the investments were made and numerous other factors beyond our control.

Drilling for and producing oil and natural gas are high risk activities with many uncertainties.

Our future success will depend on the success of our development, exploitation, production and exploration activities. Our oil and natural gas exploration and production activities are subject to numerous risks beyond our control, including the risk that drilling will not result in commercially viable oil or natural gas production. Our decisions to purchase, explore, develop or otherwise exploit prospects or properties will depend in part on the evaluation of data obtained through geophysical and geological analyses, production data and engineering studies, the results of which are often inconclusive or subject to varying interpretations. Our cost of drilling, completing and operating wells is often uncertain before drilling commences. Overruns in budgeted expenditures are common risks that can make a particular project uneconomical. Further, many factors may curtail, delay or cancel drilling, including the following:

| | ● | delays imposed by or resulting from compliance with regulatory requirements; |

| | ● | pressure or irregularities in geological formations; |

| | ● | shortages of or delays in obtaining qualified personnel or equipment, including drilling rigs and CO2; |

| | ● | equipment failures or accidents; and |

| | ● | adverse weather conditions, such as freezing temperatures, hurricanes and storms. |

The presence of one or a combination of these factors at our properties could adversely affect our business, financial condition or results of operations.

Prospects that we decide to drill may not yield oil or gas in commercially viable quantities.

A prospect is a property on which we have identified what our geoscientists believe, based on available seismic and geological information, to be indications of oil or gas. Our prospects are in various stages of evaluation, ranging from a prospect which is ready to drill to a prospect that will require substantial additional seismic data processing and interpretation. There is no way to predict in advance of drilling and testing whether any particular prospect will yield oil or gas in sufficient quantities to recover drilling or completion costs or to be economically viable. The use of seismic data and other technologies and the study of producing fields in the same area will not enable us to know conclusively prior to drilling whether oil or gas will be present or, if present, whether oil or gas will be present in commercial quantities. In addition, because of the wide variance that results from different equipment used to test the wells, initial flowrates may not be indicative of sufficient oil or gas quantities in a particular field. The analogies we draw from available data from other wells, from more fully explored prospects, or from producing fields may not be applicable to our drilling prospects. We may terminate our drilling program for a prospect if results do not merit further investment.

We are subject to complex laws that can affect the cost, manner or feasibility of doing business.

Exploration, development, production and sale of oil and natural gas are subject to extensive federal and state regulation in Argentina. We may be required to make large expenditures to comply with governmental regulations. Matters subject to regulation include:

| | ● | the exploitation of our oil and gas concessions as governed by the terms of the concession agreements; |

| | ● | royalties, canons and landlord fees; |

| | ● | production permits; |

| | ● | discharge permits for drilling operations; |

| | ● | drilling bonds; |

| | ● | reports concerning operations; |

| | ● | the spacing of wells; |

| | ● | unitization and pooling of properties; and |

| | ● | taxation. |

Under these laws, we could be liable for personal injuries, property damage and other damages. Failure to comply with these laws also may result in the suspension or termination of our operations and subject us to administrative, civil and criminal penalties. Moreover, these laws could change in ways that could substantially increase our costs. Any such liabilities, penalties, suspensions, terminations or regulatory changes could materially adversely affect our financial condition and results of operations.

Our operations may incur substantial liabilities to comply with environmental laws and regulations.

Our oil and gas operations are subject to stringent federal and state laws and regulations relating to the release or disposal of materials into the environment or otherwise relating to environmental protection. These laws and regulations require an environmental impact study before drilling commences; and impose substantial liabilities for pollution resulting from our operations. Failure to comply with these laws and regulations may result in the assessment of penalties or the incurrence of investigatory or remedial obligations.

Market conditions or operational impediments may hinder our access to oil and gas markets or delay our production.

In connection with our continued development of oil and gas properties, we may be disproportionately exposed to the impact of delays or interruptions of production from wells in these properties, caused by transportation capacity constraints, curtailment of production or the interruption of transporting oil and gas volumes produced. In addition, market conditions or a lack of satisfactory oil and gas transportation arrangements may hinder our access to oil and gas markets or delay our production. The availability of a ready market for our oil and natural gas production depends on a number of factors, including the demand for and supply of oil and natural gas and the proximity of reserves to pipelines and terminal facilities.

Crude oil and natural gas prices are volatile and a substantial reduction in these prices could adversely affect our results and the price of our common stock.

Our revenues, operating results and future rate of growth depend highly upon the prices we receive from crude oil and natural gas produced by the concession in which we have investments. Historically, the markets for crude oil and natural gas have been volatile and are likely to continue to be volatile in the future. The markets and prices for crude oil and natural gas depend on factors beyond our control. These factors include demand for crude oil and natural gas, which fluctuates with changes in market and economic conditions, and other factors, including:

| | ● | worldwide and domestic supplies of crude oil and natural gas; |

| | ● | actions taken by foreign oil and gas producing nations; |

| | ● | political conditions and events (including instability or armed conflict) in crude oil or natural gas producing regions; |

| | ● | the level of global crude oil and natural gas inventories; |

| | ● | the price and level of foreign imports; |

| | ● | the price and availability of alternative fuels; |

| | ● | the availability of pipeline capacity and infrastructure; |

| | ● | the availability of crude oil transportation and refining capacity; |

| | ● | weather conditions; |

| | ● | domestic and foreign governmental regulations and taxes; and |

| | ● | the overall economic environment. |

Significant declines in crude oil and natural gas prices for an extended period may have the following effects on our business:

| | ● | limiting our financial condition, liquidity, and ability to finance planned capital expenditures and results of operations; |

| | ● | reducing the amount of crude oil and natural gas that can be produced economically; |

| | ● | causing us to delay or postpone some of our capital projects; |

| | ● | reducing our revenues, operating income and cash flows; |

| | ● | reducing the carrying value of our investments in crude oil and natural gas properties; or |

| | ● | limiting our access to sources of capital, such as equity and long-term debt. |

Our business involves many operating risks that may result in substantial losses for which insurance may be unavailable or inadequate.

Our oil and gas investments are subject to hazards and risks inherent in operating and restoring oil and gas wells, such as fires, natural disasters, explosions, casing collapses, surface cratering, pipeline ruptures or cement failures, and environmental hazards such as natural gas leaks, oil spills and discharges of toxic gases. Any of these risks can cause substantial losses resulting from injury or loss of life, damage to or destruction of property, natural resources and equipment, pollution and other environmental damages, regulatory investigations and penalties, suspension of our operations and repair and remediation costs. In addition, our liability for environmental hazards may include conditions created by the previous owners of properties in which we have investments or purchase or lease.

We do not believe that insurance coverage for all environmental damages that could occur is available at a reasonable cost. Losses could occur for uninsurable or uninsured risks. The occurrence of an event that is not fully covered by insurance could harm our financial condition and results of operations.

Competition in our industry is intense and many of our competitors have greater financial and technological resources.

We have investments in the competitive area of oil and gas exploration and production. Many competitors are large, well-established companies that have larger operating staffs and significantly greater capital resources.

Competition for experienced personnel may negatively impact our operations.

Our future profitability will depend on our ability to attract and retain qualified personnel. The loss of any key executives or other key personnel could have a material adverse effect on investments results and revenues. In particular, the loss of the services of our President, Dr. Daniel Peralta, could adversely affect our South American oil and gas investment results.

International operations expose us to political, economic and currency risks.

With regard to our investments in oil and gas concessions located outside of the United States, we are subject to the risks of doing business abroad, including,

| ● | Changes in tariffs and taxes; and |

| ● | Political and economic instability. |

Changes in currency exchange rates may affect the relative costs of operations in Argentina, and may affect the cost of certain items required in oil and gas processing, thus possibly adversely affecting our profitability.

There are inherent risks for the foreseeable future of conducting business internationally. Language barriers, foreign laws and tariff and taxation issues all have a potential negative effect on our ability to transact business. Changes in tariffs or taxes applicable to our investments in foreign operations may adversely affect our profitability. Political instability may increase the difficulties and costs of doing business. We may be subject to the jurisdiction of the government and/or private litigants in foreign countries where we transact business, and may be forced to expend funds to contest legal matters in those countries in disputes with those governments or with customers or suppliers.

We are subject to changing governmental regulations concerning our oil and gas properties and with respect to investments.

Provincial governments in Argentina have established production floors and conditions for producing concessions that are required to be met by the companies holding the concessions. Our operations in Argentina may in the future be adversely impacted by these measures currently being taken by provincial governments.

Although, there are no restrictions for the payment abroad of interest, dividends or profits, royalties and other commercial payments duly supported by the corresponding documentation, exchange control regulations could be implemented to restrict transfers of funds from SAHF to the Company, which would limit our ability to pay dividends.

Historically we have not paid dividends.

We have never paid dividends on our common stock, and management does not anticipate payment of dividends until such time as our Board of Directors determines that our profitability warrants payment of dividends.

Item 1B. Unresolved Staff Comments.

Not applicable.

Item 2. Properties.

As of December 31, 2012, our principal assets included Partial Rights Ownership in five oil and gas properties.

| Block | Province | Status | Delta % | Partner(s) |

| Jollin | Salta | Testing | 10% CO | JHP (China), Maxipetrol |

| Tonono | Salta | testing | 10% CO | JHP (China), Maxipetrol |

| Tartagal | Salta | Seismic | 9% CO | New Times Energy (HK), Maxipetrol |

| Morillo | Salta | Seismic | 9% CO | New Times Energy (HK), Maxipetrol |

| Guemes | Salta | Drill Complete | 20% | Ketsal |

| Valle de Lerma | Salta | Well Workover | 60% | Remsa, PetroNexus, Grasta |

*CO means a carryover interest in the project.

** Of these five properties, SAHF and its joint venture partner have made initial investments in Guemes.

*** In the Jollin, Tonono, Tartagal, Morillo and Coltan concession the carry over mode relieved SAHF from the payment of canon, or landlord, fees of any kind. In the exploratory areas, Guemes proportional exploratory canons were paid as explained in the financials. Surface canon were not paid due to the lack of surface operations in those blocks, with the exception of Guemes where an old YPF road, built by the former National Company of Argentina and now owned by Repsol of Spain) was used in 2010 to access the drilling site.

Executive Offices

Effective March 1, 2013, we entered into a one-year lease for our new executive offices, at a net monthly rental of $3,100. The lease contains a renewal option for one year. We anticipate that this office space will accommodate our operations for the next several years.

Item 3. Legal Proceedings.

None.

Item 4. Mine Safety Disclosures.

Not applicable.

Item 5. Market for Registrant's Common Equity, Related Shareholder Matters and Issuer Purchases of Equity Securities.

Our common stock has been quoted on the Over-the-Counter Bulletin Board operated by the National Association of Securities Dealers, since approximately February 1, 2001.

Our shares are listed under the symbol "DLTZ”. The quotations in the table below reflect inter-dealer prices, without retail mark-up, mark-down, or commission and may not represent actual transactions.

| | | | High | | | Low | |

| 2010: | 1st Quarter | | | 0.49 | | | | 0.15 | |

| | 2nd Quarter | | | 0.49 | | | | 0.23 | |

| | 3rd Quarter | | | 0.43 | | | | 0.23 | |

| | 4th Quarter | | | 0.70 | | | | 0.43 | |

| | | | | | | | | | |

| 2011 | 1st Quarter | | | 0.58 | | | | 0.49 | |

| | 2nd Quarter | | | 0.50 | | | | 0.11 | |

| | 3rd Quarter | | | 0.44 | | | | 0.23 | |

| | 4th Quarter | | | 0.42 | | | | 0.20 | |

| | | | | | | | | | |

| 2012 | 1st Quarter | | | 0.51 | | | | 0.38 | |

| | 2nd Quarter | | | 0.50 | | | | 0.20 | |

| | 3rd Quarter | | | 0.40 | | | | 0.20 | |

| | 4th Quarter | | | 0.23 | | | | 0.20 | |

| | | | | | | | | | |

| 2013 | 1st Quarter | | | 0.25 | | | | 0.20 | |

During the last two fiscal years, no cash dividends have been declared on Delta's common stock and Company management does not anticipate that dividends will be paid in the foreseeable future. The payment of dividends is within the discretion of the board of directors and will depend on the Company's earnings, capital requirements, financial condition, and other relevant factors. There are no restrictions that currently limit the Company's ability to pay dividends on its common stock other than those generally imposed by applicable state law.

As of March 21, 2013, there were approximately 100 record holders of our common stock.

The Company has no equity compensation plans in effect, or any securities outstanding under equity compensation plans, as of the date of this report.

Item 6. Selected Financial Data.

Not applicable.

Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations.

The following discussion of our consolidated financial condition and results of operations should be read in conjunction with the consolidated financial statements and notes thereto and the other financial information included elsewhere in this report.

Certain statements contained in this report, including, without limitation, statements containing the words "believes," "anticipates," "expects" and words of similar import, constitute "forward looking statements" within the meaning of the Private Securities Litigation Reform Act of 1995. Such forward-looking statements involve known and unknown risks and uncertainties. Our actual results may differ materially from those anticipated in these forward-looking statements as a result of certain factors, including our ability to create, sustain, manage or forecast our growth; our ability to attract and retain key personnel; changes in our business strategy or development plans; competition; business disruptions; adverse publicity; and international, national and local general economic and market conditions.

GENERAL

The following discussion of our consolidated financial condition and results of operations should be read in conjunction with the consolidated financial statements and notes thereto and the other financial information included elsewhere in this report.

Certain statements contained in this report, including, without limitation, statements containing the words "believes," "anticipates," "expects" and words of similar import, constitute "forward looking statements" within the meaning of the Private Securities Litigation Reform Act of 1995. Such forward-looking statements involve known and unknown risks and uncertainties. Our actual results may differ materially from those anticipated in these forward-looking statements as a result of certain factors, including our ability to create, sustain, manage or forecast our growth; our ability to attract and retain key personnel; changes in our business strategy or development plans; competition; business disruptions; adverse publicity; and international, national and local general economic and market conditions.

GENERAL

Delta Mutual, Inc. (the “Company”)was incorporated in Delaware on November 17, 1999. In 2003, we established business operations focused on providing environmental and construction technologies and services. Our operations in the Far East (Indonesia) and our construction operations in Puerto Rico were discontinued in 2008.

Effective March 4, 2008, we acquired 100% of the issued and outstanding membership interests in the parent of South American Hedge Fund LLC, a Delaware limited liability company, sometimes herein referred to as “SAHF”). For accounting purposes, the transaction was treated as a recapitalization of the Company, as of March 4, 2008, with the parent of SAHF as the acquirer. SAHF maintains a branch office in Argentina, where it is engaged in oil and gas exploration and development activities.

Overview

We are an independent oil and gas company, with the SIC Code classification 1311 (oil and gas production)for SEC filing purposes, engaged in oil and gas acquisition, exploitation, production and exploration activities primarily in Argentina. In addition, we have ownership interests in certain mineral rights that are located in Argentina. In August 2007, SAHF signed agreements to purchase partial ownership interests in four oil and gas concessions in Northern Argentina. The joint venture owning these concessions then started the process to obtain the necessary government and environmental operating permits for the commercial exploitation of these concessions. These oil and gas investments were contributed to the Company as part of the reverse merger transaction in March 2008.

Our goal is to generate meaningful growth in shareholder value through the discovery and development of proved oil and gas reserves or other minerals, and we have focused on concessions where there are shut-in, plugged or abandoned wells that have, in our assessment, a high probability of additional recovery of reserves through the revitalization of the wells using standard oil and gas industry practices to bring back wells into production or to enhance production. In addition, our growth plan is centered upon the pursuit of energy related development projects that we believe will generate attractive rates of return while maintaining a balanced portfolio of lower risk, long-lived oil and gas properties that provide stable cash flows.

The Company's business is subject to the risks of its oil and gas investments in South America. The likelihood of success of the Company must be considered in light of the expenses, difficulties, delays and unanticipated challenges encountered in connection with the operations of oil and gas concessions in Argentina.

Recent Developments

Dr. Daniel R. Peralta, our President and Chief Executive Officer, director, and major stockholder, and his wife died in their home November 7, 2012. Our board appointed Malcolm Sherman, who was our Executive Vice President, as President and Chief Executive Officer and elected Santiago Peralta, the son of Dr. Peralta, as a member of our Board of Directors.

Principle Petroleum Ltd. Agreement

Effective March 30, 2012, we entered into the Cooperation Agreement with Principle Petroleum Ltd. (“PPL”). Under the Cooperation Agreement, PPL agreed to pay us $7,000,000 for certain exploration and exploitation rights to oil and gas deposits and certain bidding rights held by Delta on the following areas: Valle de Lerma in the province of Salta; San Salvador de Jujuy; Libertador General San Martin in the province of Jujuy; and Selva Maria in the province of Formosa. Pursuant to a separate Agreement dated March 31, 2012, we agreed with PPL to assign and transfer 50% of SAHF's ownership of the Tartagal and Morillo (i.e., a 9% interest in the concession) to PPL for a purchase price of $500,000, which was paid in 2012. PPL has also agreed in an Undertaking to provide funds to the operating entities of Valle de Lerma, Selva Maria, San Salvador and Libertador, in the aggregate amount of up to $10,000,000 (Selva Maria is pending for approval from the government, which is standard procedure in Argentina). The San Salvador and Libertador concessions were, upon the receipt by the government of a higher bid, awarded to another company.

As part of PPL’s obligations under the Cooperation Agreement, PPL made partial payments of $2,000,000 in our 2012 first fiscal quarter, $999,979 in the second quarter and $499,979 in the third quarter towards the full amount of $7,000,000 provided under the Cooperation Agreement. Both parties are working to execute the full amount of PPL’s payment obligations as agreed. A further payment of $500,000 was made by PPL in January 2013.

Development of Our Oil and Gas Properties

Specifically, we have focused, and plan to continue to focus, on the following investments in South America.

Valle de Lerma

On August 10, 2011, the Company’s tender offer, made through our wholly-owned subsidiary, SAHF, for the ownership right to explore, and eventually, produce oil and natural gas in the block known as “Valle de Lerma” was declared the winning bid by the Salta provincial government. SAHF made the offer in a joint venture agreement with Grasta SA, a local mid-size gasoline refinery located in Buenos Aires, Argentina. Other partners in the block include PetroNEXUS and REMSA. On October 25, 2011 SAHF was awarded an Exploration and Exploitation Oil & Gas Block License by the Government of Salta, Argentina.

The Valle de Lerma block is located in the province of Salta in the northwestern region of Argentina and has an area of 5259 km2. SAHF has done the measurement and survey study and filed an environmental impact study, which was approved. Upon completion of the study it was determined that the actual well site was within the boundaries of the City of Salta, where government restrictions do not allow oil to be produced from this site. We are currently negotiating with the government to add an additional site to the concession area from among three sites adjacent to the concession area with similar wells. When the extension of the concession area is accomplished, we will commence work on the new site, following receipt of all government approvals. SAHF holds a majority of the license interest and is the responsible operator. The license allows SAHF 20 years to explore and produce hydrocarbons with a renewal option of ten more years. The Company will commence the Valle de Lerma well work over with a local rig company. The exploration terms are four years for the first period, three years for the second and two years for the last period.

SAHF currently owns 60% of the rights to explore Valle de Lerma; GRASTA owns 5%; PetroNEXUS owns 30%; and REMSA owns 5%.

The total investment commitment originally approved is of 401 work units within a three year term. Each work unit has a value of $5,000 totaling a $2,005,000 of committed investment for the first quarter. In the second quarter of 2011, the Company executed 175 work units and the conclusions were submitted to the proper regulatory government agency, which approved the work performed with the Resolution 021/2012 dated May 11, 2012. Our insurance policy for the remnant amount of $1,155,000 was issued in the second quarter of 2012.

Tartagal and Morillo

As of December 31, 2012, the Company, through SAHF, retained 9% of the total concession in the carryover mode ("no cost obligations to SAHF") in the Tartagal and Morillo oil and gas concessions located in Northern Argentina. In March 2009, a Hong Kong public company purchased 60% of the ownership in the Tartagal and Morillo oil and gas concessions, and has invested approximately $60 million to date on geological studies, 2D and 3D seismic surveys on both blocks and two work-over drills and an exploratory well drill in Tartagal. The exploration period of the licenses for the Tartagal and Morillo blocks has been extended until February 2014. Production from the two Campo Alcoba test wells commenced in 2011 and has continued into the 2012 second quarter. A work over of one the two previously reopened wells is planned, and currently an analytic test to drill one more exploratory well is under way. On May 11, 2011, SAHF received the Salta Government’s approval for its 18% ownership share for the Tartagal and Morillo concessions. Effective March 30, 2012, we agreed to sell 50% of our interest in these concessions to PPL.

Jollin and Tonono Oil and Gas Concessions

As of December 31, 2012, the Company, through SAHF, has a 10% interest concession in the carryover mode ("no cost obligations to SAHF") in the Jollin and Tonono oil and gas concessions located in Northern Argentina.

SAHF received its foreign registration in Argentina and was admitted as a member of the joint venture on July 2, 2010. Accordingly, the Company has reclassified its concession costs in the amount of $688,475 associated with this property to proved oil and gas properties as of December 31, 2010 based upon the reserve report received from the third party working interest owner of the joint venture. The Company will begin receiving revenue from the Jollin and Tonono blocks when the first well is approved for commercial production. The joint venture is currently developing a future plan for continuing the exploration of the concessions.

Salta Province Exploration Rights

During 2008, SAHF purchased 40% of the oil and gas exploration rights to five geographically defined areas in the Salta Province of Northern Argentina from Ketsal, SA (“Ketsal”) for $697,000 cash. In 2009, SAHF assigned 50% of its rights to a third party. As of December 31, 2012, SAHF owns 20% of the rights to this oil and gas concession. SAHF is responsible for managing the drilling activities in the Salta Province and bears its pro-rata share of the costs. Exploratory drilling activities commenced in April 2010 on the Guemes Block and the first well was spud in September 2010. In July 2010, SAHF found positive traces of the presence of natural gas and hydrocarbons of low-density quality through its analysis of core samples. Well logging while drilling also confirmed the potential existence of formations with sufficient hydrocarbons to make the well economically productive.

The UTE for this concession is in litigation with the drilling company that drilled the test well and has sued for an alleged $3,000,000 of additional expenses over and above the contract amount under the fixed price drilling contract, where the contract amount was set at $1,000,000, and overage amounts were to be set prior to execution. The operator of the concession, Ketsal, is in the process of settlement negotiations. SAHF has no obligation or liability for any amounts paid in settlement of, or as a result of an adverse judgment in, this litigation. However, the resolution of this lawsuit may affect the schedule for the future development of this property.

Production testing to verify the commercial sustainability of the well is expected to commence in the third quarter of 2013, subject to favorable settlement of the litigation.

Caimancito Refinery

We, through our wholly-owned subsidiary, SAHF, have purchased 33.33% of the Caimancito Refinery, located in the Jujuy Province, Argentina, pursuant to a March, 2012 purchase option agreement. The purchase price for the 33.33% of the outstanding shares of Caimancito Refinery was $150,000, which has been paid in full. A contract with NOA, a service company, was entered into for NOA to advise us of the expected costs to rehabilitate the plant. Due to required rehabilitation work, currently this refinery is not being operated to produce gasoline or diesel fuel.

Lithium Production Properties

On March 1, 2010, we signed a purchase option agreement with Minera Jujuy from the Jujuy Province, Argentina related to the acquisition of approximate 143,000 hectares with 29 mines located in the Northwest part of Argentina, south of the border with Bolivia, with high lithium and borates brines concentration. Currently, we are performing sampling and geological conclusions with a local geological company in order to determine value to the property. SAHF purchased control of 51% of the Guayatayoc project via a partnership agreement with Oscar Chedrese and Servicios Mineros SA. The project holds the concession for a period of 20 years.

RESULTS OF OPERATIONS

YEAR ENDED DECEMBER 31, 2012 COMPARED TO THE YEAR ENDED DECEMBER 31, 2011

During the year ended December 31, 2012, we had net earnings of $5,043,149 compared to a net loss of $786,826 for the year ended December 31, 2011. The gain for the year ended December 31, 2012 over the prior year is primarily due to the gain on the sale of certain bidding rights to PPL.

During the year ended December 31, 2012 our loss from operations was approximately $1,361,718 compared to a net loss from operations of approximately $787,566 in 2011, due to a higher level of general and administrative expenses in 2012.

LIQUIDITY

At December 31, 2012, we had a working capital surplus of approximately $4.2 million, compared with a working capital deficit of approximately $1.3 million at December 31, 2011. The significant improvement is due to the sale of certain bidding rights and oil and gas properties to PPL as of March 30, 2012.

At December 31, 2012, we had total assets of approximately $8.3 million compared to total assets of approximately $2.6 million at December 31, 2011. Net cash used in operating activities in the year ended December 31, 2012 was approximately $1.4 million, as compared with approximately $0.7 million in 2011; and net cash generated from investing activities was approximately $3 million 2012, as compared with cash used of approximately $0.4 in 2011. Cash used in operations and investing activities in 2012 was offset by net cash provided from investing and financing activities of approximately $3 million. Net cash used by financing activities was $50,000 in the year ended December 31, 2012, compared to approximately $1.0 million in 2011.

Estimated 2012 Capital Requirements

In the case of the Jollin and Tonono and Tartagal and Morillo oil and gas properties, we have carried interests; therefore, no further capital expenditures are required on our part. For the exploration rights in Salta Province, we have completed the drilling and development of one well in Guemes that is expected to begin production testing in 2013. We have sufficient funds for our portion (20%) of the costs of installation of the battery storage facility to complete the Guemes production and storage facilities, although further development efforts on this concession are dependent on successful settlement of litigation with regards to amounts owed under the drilling contract. In the event our revenue expectations for 2012 are not met, we are not required to make any additional capital investment to protect our assets.

We estimate that our capital requirements in 2013 to develop the Valle de Lerma (where we have applied for extension of the concession to permit oil production from an existing site) and Selva Maria properties (the award of the Selva Maria concession is pending approval from the government) will approximate $1,350,000 for Selva Maria and $800,000 for Valle de Lerma. The funds for which investments would be provided by in part by PPL (and by the other partners in the respective UTE’s) pursuant to PPL’s commitment to provide up to $10,000,000 in developmental funds for these properties.

USE OF ESTIMATES

The preparation of the financial statements requires the Company to make estimates and judgments that affect the reported amount of assets, liabilities, and expenses, and related disclosures of contingent assets and liabilities. On an on-going basis, the Company evaluates its estimates, including those related to oil and gas properties, intangible assets, income taxes and contingencies and litigation. The Company bases its estimates on historical experience and on various assumptions that are believed to be reasonable under the circumstances, the results of which form the basis for making judgments about carrying values of assets and liabilities that are not readily apparent from other sources. Actual results may differ from these estimates under different assumptions or conditions. In the opinion of management, all normal recurring adjustments considered necessary for a fair presentation have been included in these financial statements. Certain amounts for prior periods have been reclassified to conform to the current presentation.

Management believes that it is reasonably possible that the following material estimates affecting the financial statements could happen in the coming year:

| | ● | Proved oil and gas reserves; |

| | ● | Expected future cash flow from proved oil and gas properties; |

| | ● | Future exploration and development costs; and |

| | ● | Future dismantlement and restoration costs. |

NEW FINANCIAL ACCOUNTING STANDARDS

For a summary of new financial accounting standards applicable to the Company, please refer to the accompanying notes to the financial statements.

Critical Accounting Policies

The Securities and Exchange Commission recently issued “Financial Reporting Release No. 60 Cautionary Advice About Critical Accounting Policies” (“FRR 60”), suggesting companies provide additional disclosures, discussion and commentary on their accounting policies considered most critical to its business and financial reporting requirements. FRR 60 considers an accounting policy to be critical if it is important to the Company’s financial condition and results of operations, and requires significant judgment and estimates on the part of management in the application of the policy.

The Company assesses potential impairment of its long-lived assets, which include its property and equipment, investments, and its identifiable intangibles such as deferred charges under the guidance of SFAS 144 “Accounting for the Impairment or Disposal of Long-Lived Assets.” The Company must continually determine if a permanent impairment of its long-lived assets has occurred and write down the assets to their fair values and charge current operations for the measured impairment.

Investments in non-consolidated affiliates – These investments consist of the Company’s ownership interests in oil and gas development and exploration rights in Argentina, net of impairment losses if any.

We evaluate these investments for impairment when indicators of potential impairment are present. Indicators of impairment include, but are not limited to, levels of oil and gas reserves, availability of pipeline (or other transportation) capacity and infrastructure and management of the operations in which the investments were made.

Item 7A. Quantitative and Qualitative Disclosures About Market Risk.

Interest Rate Risk - Interest rate risk refers to fluctuations in the value of a security resulting from changes in the general level of interest rates. Investments that are classified as cash and cash equivalents have original maturities of three months or less. Our interest income is sensitive to changes in the general level of U.S. interest rates.

We do not have significant short-term investments, and due to their short-term nature, we believe that there is not a material risk exposure.

Credit Risk - Our accounts receivable are subject, in the normal course of business, to collection risks. We regularly assess these risks and have established policies and business practices to protect against the adverse effects of collection risks. As a result we do not anticipate any material losses in this area.

Commodity Price Risk – We are exposed to market risks related to price volatility of crude oil and natural gas. The prices of crude oil and natural gas affect our revenues, since sales of crude oil and natural gas from our South American investments comprise nearly all of the components of our revenue. A decline in crude oil and natural gas prices will likely reduce our revenues, unless there are offsetting production increases. We do not use derivative commodity instruments for trading purposes.