FY 2005 2nd Quarter

Earnings Conference Call

Chip McClure, President, Chairman and CEO

Jim Donlon, Senior Vice President and CFO

Rakesh Sachdev, Senior Vice President Corporate Strategy

May 3, 2005

1

Forward-Looking Statements

This presentation contains “forward-looking statements” as defined in the Private Securities Litigation

Reform Act of 1995. These forward-looking statements are based on currently available competitive,

financial and economic data and management’s views and assumptions regarding future events. Such

forward-looking statements are inherently uncertain, and actual results may differ materially from those

projected as a result of certain risks and uncertainties, including but not limited to global economic and

market conditions; the demand for commercial, specialty and light vehicles for which the company

supplies products; risks inherent in operating abroad, including foreign currency exchange rates and

potential disruption production and supply due to terrorist attacks or acts of aggression; availability and

cost of raw materials, including steel; OEM program delays; demand for and market acceptance of

new and existing products; reliance on major OEM customers; labor relations of the company, its

customers and suppliers; the financial condition of the company’s suppliers and customers, including

potential bankruptcies; successful integration of acquired or merged businesses; achievement of the

expected annual savings and synergies from past and future business combinations; success and

timing of potential divestitures; potential impairment of long-lived assets, including goodwill;

competitive product and pricing pressures; the amount of the company’s debt; the ability of the

company to access capital markets; the credit ratings of the company’s debt; the outcome of existing

and any future legal proceedings, including any litigation with respect to environmental or asbestos-

related matters; as well as other risks and uncertainties, including but not limited to those detailed

herein and from time to time in ArvinMeritor’s Securities and Exchange Commission filings.

2

2nd Quarter Income Statement

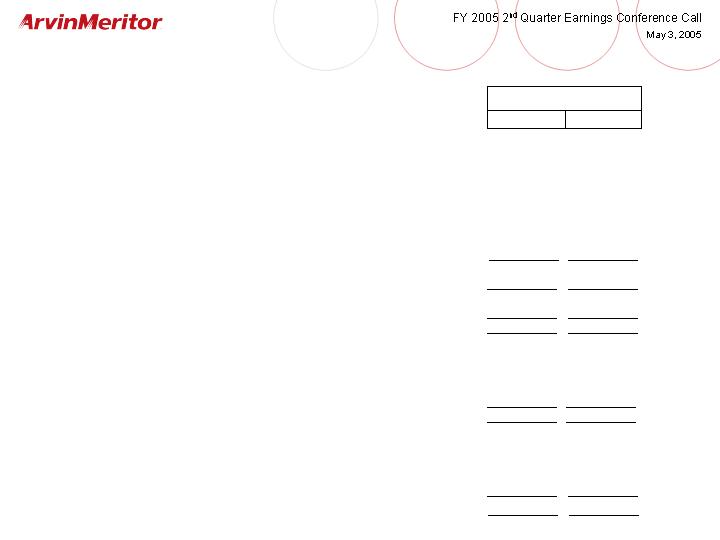

(in millions, except per share amounts)

2005

2004

$

%

Sales

2,276

$

1,996

$

280

$

14%

Cost of Sales

(2,124)

(1,825)

(299)

-16%

GROSS MARGIN

152

171

(19)

-11%

SG&A

(100)

(99)

(1)

-1%

Gain on Divestitures

-

20

(20)

Customer Bankruptcy

(5)

-

(5)

Environmental Remediation Costs

(6)

(8)

2

Restructuring Costs

(64)

(6)

(58)

OPERATING INCOME (LOSS)

(23)

78

(101)

-129%

Equity in Earnings of Affiliates

7

5

2

40%

Interest Expense, Net and Other

(30)

(25)

(5)

-20%

INCOME (LOSS) BEFORE INCOME TAXES

(46)

58

(104)

-179%

Benefits (Provisions) for Income Taxes

13

(15)

28

187%

Minority Interests

(2)

(3)

1

33%

Income (Loss) From Continuing Operations

(35)

40

(75)

-188%

Income from Discontinued Operations

2

1

1

100%

NET INCOME (LOSS)

(33)

$

41

$

(74)

$

-180%

DILUTED EARNINGS (LOSS) PER SHARE

Continuing Operations

(0.51)

$

0.58

$

(1.09)

$

-188%

Discontinued Operations

0.03

0.01

0.02

200%

Diluted EPS

(0.48)

$

0.59

$

(1.07)

$

-181%

Three Months Ended March 31,

Better/(Worse)

3

Restructuring Actions

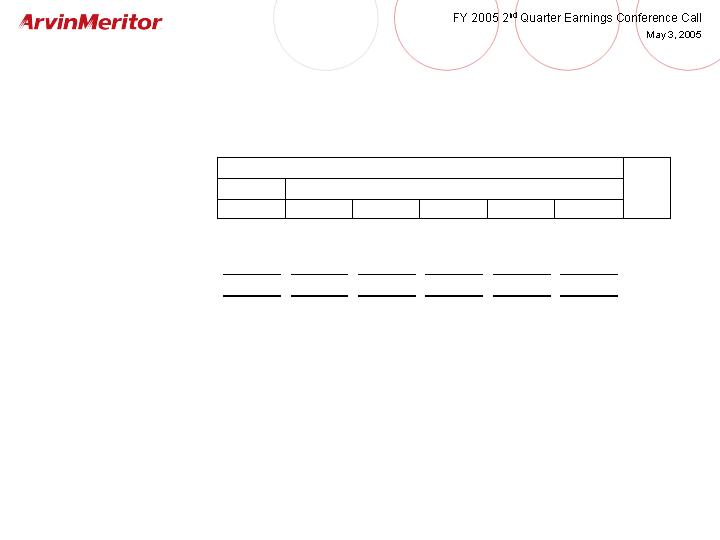

Annual savings estimated at $50 – $60 million.

($ in millions)

LVS

CVS

Total

1Q

2Q

YTD

New Actions

Salaried reduction in force

10

$

13

$

23

$

-

$

23

$

23

$

Facility rationalization

Employee severance

47

6

53

-

16

16

Shutdown costs and other

27

9

36

-

-

-

Total facility rationalization

74

15

89

-

16

16

Asset impairments

23

-

23

-

23

23

Total New Actions

107

28

135

-

62

62

Total Previous Actions

16

-

16

10

2

12

Total Estimated Restructuring Costs

123

$

28

$

151

$

10

$

64

$

74

$

Total Estimated Costs

Total Recorded Fiscal 2005

4

Segment Sales

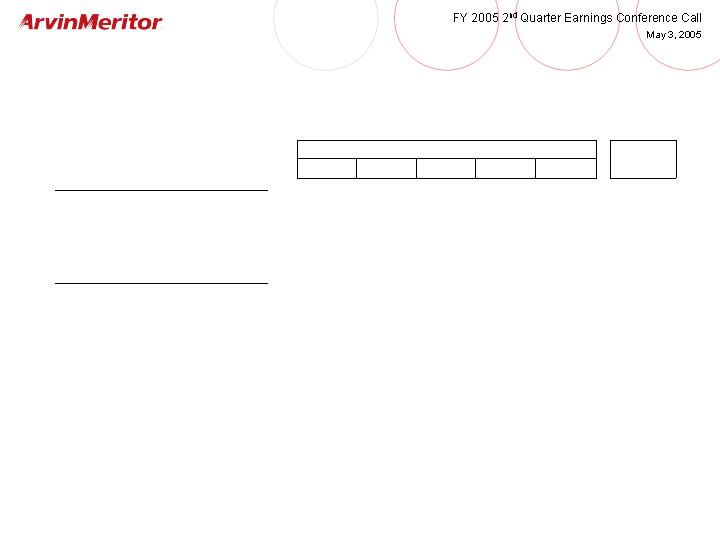

(in millions)

2005

2004

$

%

Light Vehicle Systems

North America

537

$

511

$

26

$

5%

Europe

576

606

(30)

-5%

South America

60

44

16

36%

Asia-Pacific and Other

71

66

5

8%

Total Sales

1,244

1,227

17

1%

Commercial Vehicle Systems

North America

618

471

147

31%

Europe

298

210

88

42%

South America

52

29

23

79%

Asia-Pacific and Other

64

59

5

8%

Total Sales

1,032

769

263

34%

Reported Sales

2,276

$

1,996

$

280

$

14%

Better/(Worse)

Quarter Ended March 31,

5

Segment Operating Income

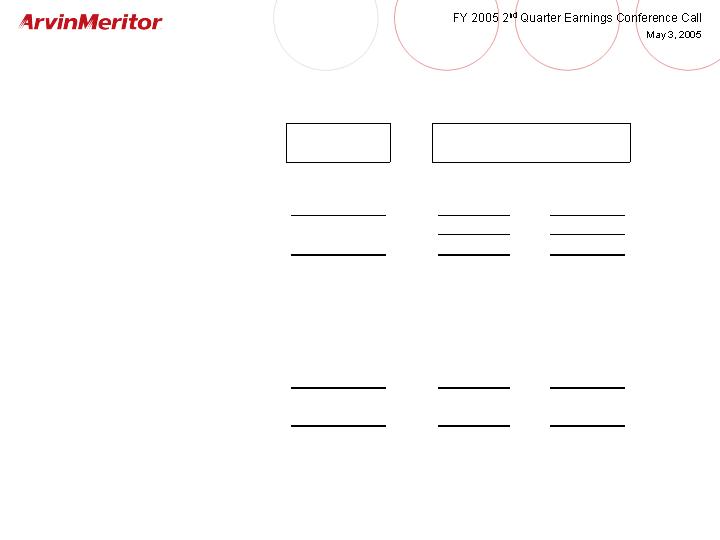

Total Operating Margins

2.4%

3.3%

(0.9)

(in millions)

2005

2004

$

%

Operating Income

Light Vehicle Systems

(54)

$

50

$

(104)

$

-208%

Commercial Vehicle Systems

37

36

1

3%

Segment Operating Income

(17)

86

(103)

-120%

Environmental Remediation Costs

(6)

(8)

2

25%

Operating Income

(23)

$

78

$

(101)

$

-129%

Operating Margins

Light Vehicle Systems

-4.3%

4.1%

(8.4)

Commercial Vehicle Systems

3.6%

4.7%

(1.1)

Segment Operating Margins

-0.7%

4.3%

(5.0)

Total Operating Margins

-1.0%

3.9%

(4.9)

Operating Margins Before Special Items

Light Vehicle Systems

0.3%

2.4%

(2.1)

Commercial Vehicle Systems

4.8%

4.7%

0.1

Better/(Worse)

Quarter Ended March 31,

6

Balance Sheet Highlights

(1)

Net debt is calculated as total debt less fair value of interest rate swaps plus factored and securitized receivables less cash.

(2)

Includes accounts receivable securitization and factored receivables and excludes cash, short-term debt, and assets and liabilities

of discontinued operations.

(3)

Calculated using quarterly average working capital and current quarter annualized sales.

(in millions)

03/31/05

12/31/04

09/30/04

06/30/04

03/31/04

Cash

99

$

91

$

132

$

122

$

119

$

Short-term Debt

7

$

7

$

3

$

3

$

2

$

Long-term Debt

1,537

1,516

1,487

1,585

1,527

Total Debt

1,544

$

1,523

$

1,490

$

1,588

$

1,529

$

Minority Interests

59

62

61

60

64

Equity

1,062

1,170

988

1,123

1,076

Total Debt to Capital

58%

55%

59%

57%

57%

Factored Receivables

15

-

10

9

16

Securitized Receivables

65

1

32

142

225

Net Debt (1)

1,504

1,396

1,364

1,588

1,600

Working Capital (2)

465

469

293

553

570

Working Capital % of Sales (3)

5.1%

4.6%

5.3%

6.7%

7.2%

7

$

Six Months Ended

(in millions)

2005

2004

OPERATING ACTIVITIES

Income (loss) from continuing operations

Adjustments to income (loss) from continuing operations:

Depreciation and amortization

93

95

Other non-cash adjustments

54

(30)

Pension and retiree medical expense

55

66

Pension and retiree medical contributions

(46)

(44)

Changes in assets and liabilities

(244)

(84)

Net cash flows provided by (used for) continuing operations

(111)

58

Net cash flows provided by (used for) discontinued operations

(130)

3

Cash provided by (used for) operations (excluding securitization and factoring)

(241)

61

Changes in receivables securitization and factoring

38

(27)

CASH PROVIDED BY (USED FOR) OPERATING ACTIVITIES

INVESTING ACTIVITIES

Capital expenditures

Other investing cash flows provided by continuing operations

Net investing cash flows provided by (used for) discontinued operations

159

(7)

CASH PROVIDED BY INVESTING ACTIVITIES

107

18

$

FINANCING ACTIVITIES

Net change in debt

Proceeds from exercise of stock options

5

5

Cash dividends

(14)

(14)

CASH PROVIDED BY FINANCING ACTIVITIES

$

March 31,

Cash Flow Highlights

$

(23)

55

$

$

(203)

34

$

$

(63)

(63)

$

11

88

$

68

(32)

$

$

59

(41)

8

Light Vehicle Systems Net New Business

Implied

Actual

Annual

2004

2005

2006

2007

2008

Cumulative

Growth

January 2005 Guidance

4,818

$

260

$

(20)

$

-

$

130

$

370

$

1.9%

Pass Through Sales

-

30

(3)

27

23

77

Other Changes, Net (1)

-

1

23

23

6

53

Revised Guidance

4,818

$

291

$

-

$

50

$

159

$

500

$

2.5%

(1) Primarily Emissions Technologies

Sales (in millions)

Incremental

9

FY 2005 Commercial Vehicle Production Outlook

(in thousands)

Calendar

Q1

Q2

Q3

Q4

Full Year

Year

North America - Class 8 Trucks (1)

2005 Outlook

74

79

80

74

307

304

2004 Actual

47

54

63

71

235

262

Change

57%

46%

27%

4%

31%

16%

Western Europe - Heavy & Medium Trucks

2005 Outlook

96

108

117

100

421

425

2004 Actual

95

93

98

90

376

377

Change

1%

16%

19%

11%

12%

13%

(1) - Includes U.S., Canada and Mexico

Source: Western Europe - Global Insight

Fiscal Year Ended September 30

10

FY 2005 Light Vehicle Production Outlook

(in millions)

Calendar

Q1

Q2

Q3

Q4

Full Year

Year

North America

2005 Outlook

3.8

4.0

4.2

3.6

15.6

15.7

2004 Actual

3.9

4.2

4.2

3.6

15.9

15.8

Change

-3%

-5%

0%

0%

-2%

-1%

Western Europe (1)

2005 Outlook

4.2

4.3

4.6

3.8

16.9

17.1

2004 Actual

4.3

4.3

4.6

3.7

16.9

16.8

Change

-2%

0%

0%

3%

0%

2%

(1) - Includes Czech Republic

Source: CSM Worldwide, Inc.

Fiscal Year Ended September 30

11

FY 2004 Results and FY 2005 Outlook – Continuing Operations

(in millions, except EPS)

FY 2004

Full Year

Sales

8,033

$

-

8,033

$

Light Vehicle Systems

4,818

$

(30)

-

(5)

Commercial Vehicle Systems

3,215

800

-

825

770

820

Sales

8,033

$

8,803

$

-

8,853

$

Operating Margin

3.2%

2.6%

-

2.8%

Interest Expense

(107)

(120)

-

(119)

Effective Tax Rate

25%

27%

-

27%

Income from Continuing Operations

127

$

97

$

-

110

$

Diluted Earnings Per Share

1.85

$

1.40

$

-

1.60

$

Full Year Outlook (1)

FY 2005

(1) Outlook does not include the impact of any future acquisitions or divestitures, or the impact of additional

restructuring actions. Outlook also excludes $0.10 per diluted share of customer bankruptcy write offs, $0.06 per diluted

share of environmental remediation costs and $0.65 of restructuring charges, each of which were recorded in the second

quarter of fiscal 2005.

12

FY 2004 3rd Quarter Results and FY 2005 3rd Quarter Outlook –

Continuing Operations

(in millions, except EPS)

FY 2004

3rd Quarter

Sales

2,099

$

-

2,099

$

Light Vehicle Systems

1,237

$

40

-

50

Commercial Vehicle Systems

862

225

-

230

265

-

280

Sales

2,099

$

2,364

$

-

2,379

$

Operating Margin

4.0%

3.7%

-

4.0%

Interest Expense

(26)

(30)

-

(31)

Effective Tax Rate

27%

27%

-

27%

Income from Continuing Operations

42

$

42

$

-

49

$

Diluted Earnings Per Share

0.61

$

0.60

$

-

0.70

$

(1) Outlook does not include the impact of any future acquisitions or divestitures, or the impact of additional restructuring actions.

FY 2005

3rd Quarter Outlook (1)

13

FY 2005 Cash Flow Outlook – Continuing Operations

(in millions)

Income From Continuing Operations

97

$

-

110

$

Adjustments to Income

Depreciation and Other Amortization

190

-

195

Pension and Retiree Medical Expense

110

-

110

Pension and Retiree Medical Contributions

(160)

-

(170)

Changes in Assets and Liabilities

(157)

-

(180)

Cash Provided by Operations

80

-

65

Capital Expenditures

(155)

-

(165)

Free Cash Flow

(75)

$

-

(100)

$

Net Proceeds from Acquisitions and Divestitures (1)

195

$

-

195

$

Cash Dividends ($0.40 per share)

(28)

$

-

(28)

$

(1) Includes sale of Roll Coater and the Automotive Stamping and Components businesses.

Note: Does not include the effects of any changes in A/R securitization and factoring or any future

acquisitions or divestitures.

Full Year

FY 2005

14

Non-GAAP Financial Information

15

Use of Non-GAAP Financial Information

In addition to the results reported in accordance with accounting principles generally accepted in the United States (“GAAP”)

included throughout this presentation, the Company has provided information regarding income from continuing operations,

diluted earnings per share and segment operating income and margins before special items which are non-GAAP financial

measures. These non-GAAP measures are defined as reported income or loss from continuing operations, reported diluted

earnings or loss per share and segment operating income plus or minus special items. Other non-GAAP financial measures

include “net debt” and “free cash flow”. Net debt is defined as total debt less the fair value adjustment of debt due to interest

rate swaps, plus securitized and factored receivables, less cash. Free cash flow represents net cash provided by operating

activities before the net change in accounts receivable securitized or factored, less capital expenditures. The Company

believes it is appropriate to exclude the net change in securitized and factored accounts receivable in the calculation of free

cash flow since the sale of receivables may be viewed as a substitute for borrowing activity.

Management believes that the non-GAAP financial measures used in this presentation are useful to both management and

investors in their analysis of the Company’s financial position and results of operations. In particular, management believes

that net debt is an important indicator of the Company’s overall leverage and free cash flow is useful in analyzing the

Company’s ability to service and repay its debt. Further, management uses these non-GAAP measures for planning and

forecasting in future periods.

These non-GAAP measures should not be considered a substitute for the reported results prepared in accordance with GAAP.

Neither, net debt nor free cash flow should be considered substitutes for debt, cash provided by operating activities or other

balance sheet or cash flow statement data prepared in accordance with GAAP or as a measure of financial position or liquidity.

In addition, the calculation of free cash flow does not reflect cash used to service debt and thus, does not reflect funds

available for investment or other discretionary uses. These non-GAAP financial measures, as determined and presented by

the Company, may not be comparable to related or similarly titled measures reported by other companies.

Set forth on the following slides are reconciliations of these non-GAAP financial measures, if applicable, to the most directly

comparable financial measures calculated and presented in accordance with GAAP.

16

Non-GAAP Financial Information – Net Debt

(in millions)

03/31/05

12/31/04

09/30/04

06/30/04

03/31/04

Short-term debt

7

$

7

$

3

$

3

$

2

$

Long-term debt

1,537

1,516

1,487

1,585

1,527

Total Debt

1,544

1,523

1,490

1,588

1,529

Less:

Fair value of interest rate swaps

(21)

(37)

(36)

(29)

(51)

Plus:

Receivable securitization

65

1

32

142

225

Plus:

Receivable factorization

15

-

10

9

16

Subtotal

1,603

1,487

1,496

1,710

1,719

Less:

Cash

(99)

(91)

(132)

(122)

(119)

Net Debt

1,504

$

1,396

$

1,364

$

1,588

$

1,600

$

Net debt is calculated as total debt less fair value of interest rate swaps plus factored and securitized receivables less cash.

17

$

Non-GAAP Financial Information –

2nd Qtr FY 05 Results before Special Items

Q2 FY 05

Reported

Customer

Bankruptcy

Environmental

New

Restructuring

Actions

Q2 FY05

Adjusted

Sales

2,276

$

-

-

$

-

$

2,276

$

Gross Margin

152

4

-

-

156

Operating Income (Loss)

(23)

9

6

62

54

Income (Loss) from Continuing Operations

(35)

7

4

45

21

Diluted Earnings (Loss) Per Share -

Continuing Operations

(0.51)

$

0.10

$

0.06

$

0.65

$

0.30

$

Guidance

$0.30 - $0.35

Segment Operating Income (Loss)

LVS Operating Income (Loss)

(54)

$

9

$

49

$

4

$

CVS Operating Income (Loss)

37

-

-

13

50

Segment Operating Income (Loss)

(17)

9

-

62

54

Environmental remediation costs

(6)

-

6

-

-

Total Operating Income (Loss)

(23)

$

9

$

6

$

62

$

54

$

Operating Margins

LVS

-4.3%

0.3%

CVS

3.6%

4.8%

Segment Operating Margins

-0.7%

Total Operating Margins

-1.0%

2.4%

18

Non-GAAP Financial Information –

2nd Qtr FY 04 Results before Special Items

Q2 FY 04

Reported

Gain on Sale

of Business

Environmental

Q2 FY04

Adjusted

Sales

1,996

$

-

$

-

$

1,996

$

Gross Margin

171

-

-

171

Operating Income (Loss)

78

(20)

8

66

Income (Loss) from Continuing

Operations

40

(15)

6

31

Diluted Earnings (Loss) Per Share -

Continuing Operations

0.58

$

(0.22)

$

0.09

$

0.45

$

Segment Operating Income (Loss)

LVS Operating Income (Loss)

50

$

(20)

$

-

$

30

$

CVS Operating Income (Loss)

36

-

-

36

Segment Operating Income (Loss)

86

(20)

-

66

Environmental remediation costs

(8)

-

8

-

Total Operating Income (Loss)

78

$

(20)

$

8

$

66

$

Operating Margins

LVS

4.1%

2.4%

CVS

4.7%

4.7%

Segment Operating Margins

4.3%

Total Operating Margins

3.9%

3.3%

19

20